Supply and Demand Micro Unit 2: chapters 4, 5, 6.

26

Supply and Demand Micro Unit 2: chapters 4, 5, 6

-

Upload

janice-thomas -

Category

Documents

-

view

225 -

download

3

Transcript of Supply and Demand Micro Unit 2: chapters 4, 5, 6.

Supply and Demand

Micro Unit 2: chapters 4, 5, 6

Chapter 4

The market forces of Supply and Demand

THE MARKET FORCES OF SUPPLY AND DEMAND

3

Markets and Competition• A market is a group of buyers and sellers of a

particular product. • A competitive market is one with many buyers

and sellers, each has a negligible effect on price. • In a perfectly competitive market:– All goods exactly the same– Buyers & sellers so numerous that no one can affect

market price – each is a “price taker”• In this chapter, we assume markets are perfectly

competitive.

THE MARKET FORCES OF SUPPLY AND DEMAND

4

Demand

• The quantity demanded of any good is the amount of the good that buyers are willing and able to purchase.

• Law of demand: the claim that the quantity demanded of a good falls when the price of the good rises, other things equal

THE MARKET FORCES OF SUPPLY AND DEMAND

5

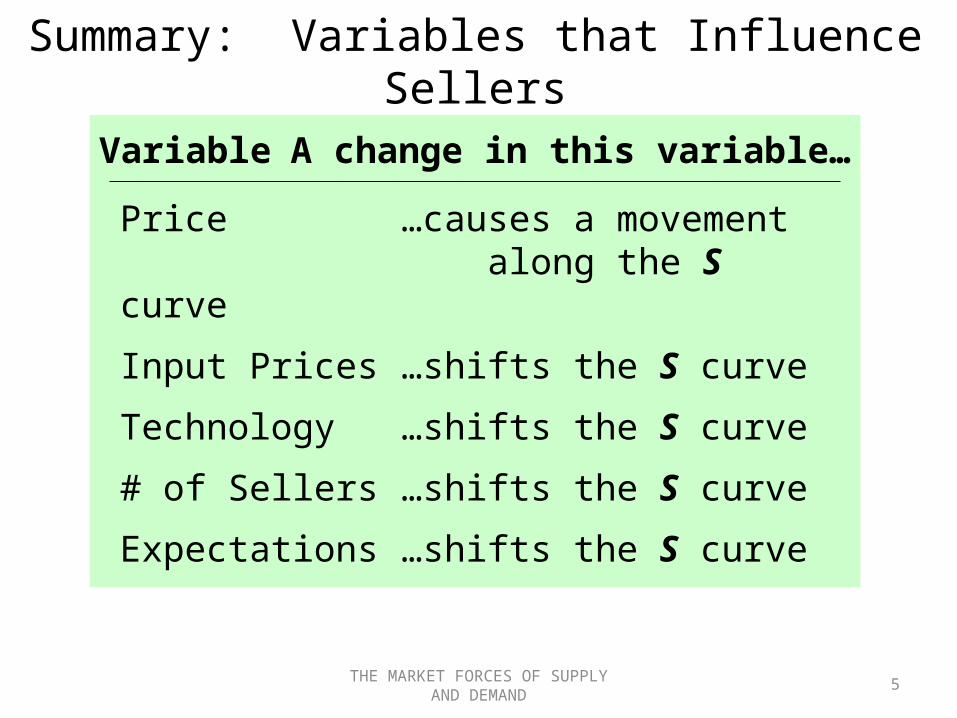

Summary: Variables that Influence Sellers

Variable A change in this variable…

Price …causes a movement along the S curve

Input Prices …shifts the S curve

Technology …shifts the S curve

# of Sellers …shifts the S curve

Expectations …shifts the S curve

THE MARKET FORCES OF SUPPLY AND DEMAND

6

Supply

• The quantity supplied of any good is the amount that sellers are willing and able to sell.

• Law of supply: the claim that the quantity supplied of a good rises when the price of the good rises, other things equal

THE MARKET FORCES OF SUPPLY AND DEMAND

7

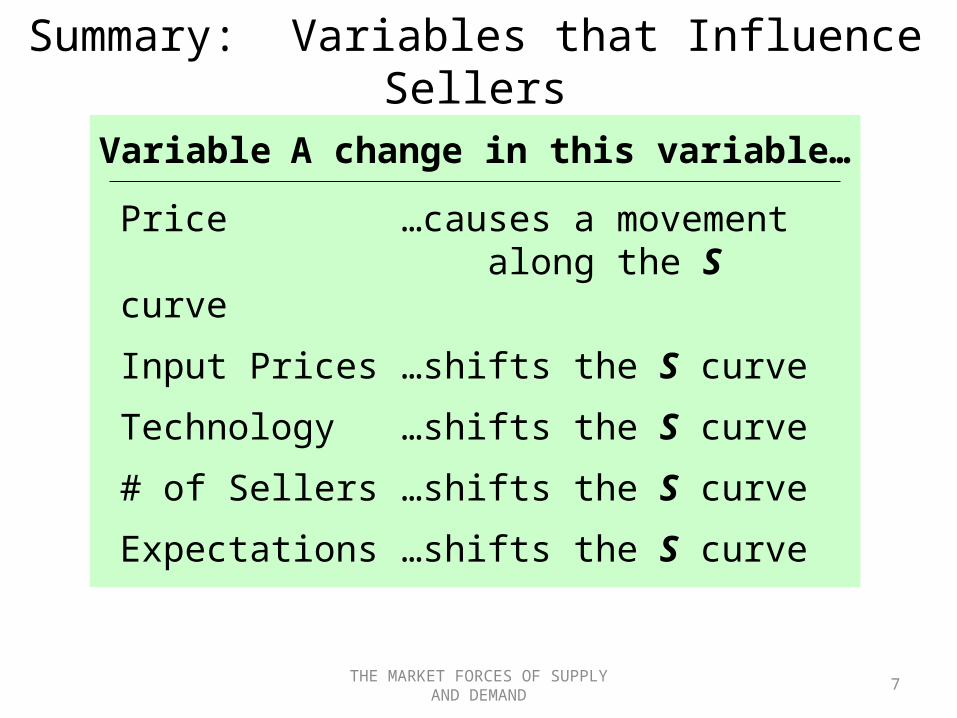

Summary: Variables that Influence Sellers

Variable A change in this variable…

Price …causes a movement along the S curve

Input Prices …shifts the S curve

Technology …shifts the S curve

# of Sellers …shifts the S curve

Expectations …shifts the S curve

THE MARKET FORCES OF SUPPLY AND DEMAND

8

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

0 5 10 15 20 25 30 35

P

Q

Supply and Demand Together

D S Equilibrium: P has reached the level where quantity supplied equals quantity demanded

Equilibrium

• Equilibrium price: the price that equates quantity supplied with quantity demanded

• Equilibrium Quantity: the quantity supplied and quantity demanded at the equilibrium price

• Surplus: when quantity supplied is greater than quantity demanded

• Shortage: when quantity demanded is greater than quantity supplied

THE MARKET FORCES OF SUPPLY AND DEMAND

10

Three Steps to Analyzing Changes in Eq’m

To determine the effects of any event,

1. Decide whether event shifts S curve, D curve, or both.

2. Decide in which direction curve shifts.

3. Use supply-demand diagram to see how the shift changes eq’m P and Q.

To determine the effects of any event,

1. Decide whether event shifts S curve, D curve, or both.

2. Decide in which direction curve shifts.

3. Use supply-demand diagram to see how the shift changes eq’m P and Q.

Chapter 5

Elasticity and application

Elasticity

• Elasticity is a numerical measure of the responsiveness of Qd or Qs to one of its determinants.

• Price elasticity of demand measures how much Qd responds to a change in P.

Price elasticity of demand =

Percentage change in Qd

Percentage change in P

How to calculate percentage change?• Standard method

of computing the percentage (%) change:End value – start value/ start value= x times 100Problem: The standard method gives different answers depending on where you start. So we use the midpoint method – End value- start value/ midpoint = x times 100Where midpoint is the value halfway between the start and end value

Lessons of elasticity

• Lesson: Price elasticity is higher when close substitutes are available.

• Lesson: Price elasticity is higher for narrowly defined goods than broadly defined ones.

• Lesson: Price elasticity is higher for luxuries than for necessities.

• Lesson: Price elasticity is higher in the long run than the short run.

Types of demand• Perfectly inelastic demand – Vertical Demand

curve with an elasticity of 0• Inelastic demand – relatively steep demand

curve with elasticity < 1• Unit elastic demand – Diagonal demand curve

with elasticity of 1• Elastic demand – relatively flat demand curve

with elasticity > 1• Perfectly elastic demand – Horizontal demand

curve with elasticity of infinity

Effects of elasticity on revenue

• If demand is elastic, then when Q decreases as P increases, revenue falls because the % change in Q is greater than the % change in P

• If demand is inelastic, then when Q decreases as P increases, revenue rises because the % change in P is greater than the % change in Q

ELASTICITY AND ITS APPLICATION

17

Price Elasticity of Supply

• Price elasticity of supply measures how much Qs responds to a change in P.

Price elasticity of supply =

Percentage change in Qs

Percentage change in P

Loosely speaking, it measures sellers’ price-sensitivity.

Again, use the midpoint method to compute the percentage changes.

Different classifications of supply

• Perfectly inelastic Supply – Vertical supply curve with a elasticity of 0

• Inelastic supply – relatively steep curve with elasticity < 1

• Unit elastic supply – diagonal curve with elasticity of 1

• Elastic Supply – relatively flat curve with elasticity > 1

• Perfectly Elastic Supply – Horizontal Supply with elasticity of infinity

Income Elasticity

• Income elasticity – measures the response of Qd to a change In consumer income

• Normal Good – As income increases, demand increases – income elasticity > 0

• Inferior Good – As income increases, demand decreases – income elasticity < 0

Income elasticity of demand =

Percent change in Qd

Percent change in income

Cross-price elasticity• Cross-price elasticity of demand:

measures the response of demand for one good to changes in the price of another good

• Substitutes – Cross-price elasticity> 0• Complements – Cross-price elasticity<0

Cross-price elast. of demand

=% change in Qd for good 1

% change in price of good 2

Chapter 6

Supply, Demand and Government Policies

Government policies that change market outcome

•Price controls– Price ceiling: a legal maximum on the price

of a good or service Example: rent control – Price floor: a legal minimum on the price of

a good or service Example: minimum wage

• Taxes– The govt can make buyers or sellers pay a specific

amount on each unit bought/sold.

Price ceilings and price floors

• Price ceilings above equilibrium are not binding, must be below equilibrium to be considered binding

• Price floors on the other hand must be above equilibrium in order to be binding.

Taxes

• The govt levies taxes on many goods & services to raise revenue to pay for national defense, public schools, etc.

• The govt can make buyers or sellers pay the tax.

• The tax can be a % of the good’s price, or a specific amount for each unit sold.

Taxes continued

• When a tax is placed on buyers, the demand curve shifts left by the amount of the tax. The same occurs for sellers with the supply curve

• Whether the tax is placed on sellers or buyers, the end result is the same, the tax creates a wedge between the price buyers pay and the price sellers receive.

Tax Incidence

• Is how the burden of the tax is shared among market participants.

• Whichever curve is more elastic, it hold less of the burden because it is easier to leave the market .