SUPPLEMENTARY HEALTH AND...

34

SUPPLEMENTARY HEALTH AND REGULATION Sector Development Department - DIDES/ANS

Transcript of SUPPLEMENTARY HEALTH AND...

SUPPLEMENTARY HEALTH AND REGULATION

Sector Development Department - DIDES/ANS

2

Why does the government participate in the sector?

• Basic assumptions

The best way to obtain better prices and qualityfor consumers is free competition.

Economic Regulation is justified by marketflaws.

2

3

Why does the government participate in the sector?

• Basic assumptions

The best way to obtain better prices and qualityfor consumers is free competition.

Economic Regulation is justified by marketflaws.

3

4

Why does the government participate in the sector?

• Arrow, 1963

Characteristics of the market for health services thatdiffer from the competitive market

Nature of demand (irregular and unpredictable)

Expected physician’s behavior (unselfish, based onreputation, problem of the agent/principal)

Product uncertainty (the result is stochastic)

Supply conditions (physician supply is regulated)

Price practice (fee for service)

4

5

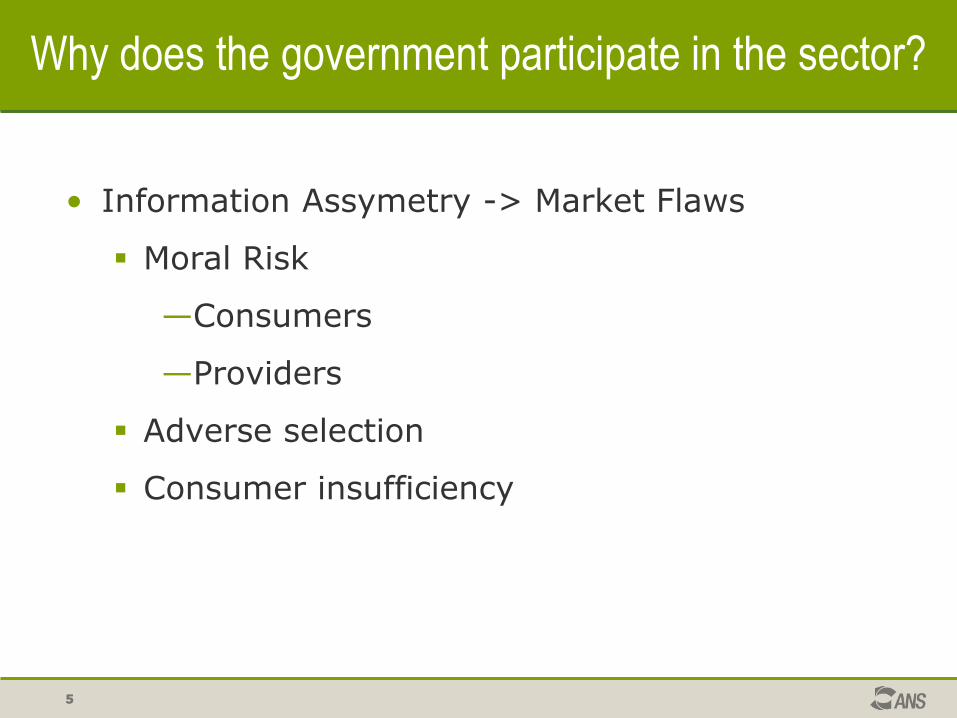

Why does the government participate in the sector?

• Information Assymetry -> Market Flaws

Moral Risk

—Consumers

—Providers

Adverse selection

Consumer insufficiency

5

6

Regulatory Actions

• Determination of maximum consultation waitingperiod

• Definition of criteria for the analysis of sufficiencyof

• Oversight of negative coverage – NIP

• Visit and Technical Direction

6

7

Regulatory Actions

Clearly define the parameters of the collectivenegotiation (jointly with the SBDC).

Seek the (technical) hierarchization of the procedures.

Facilitation of dialog by the ANS on an case by case basis.

Encourage an alternative compensation model.

Consolidating the relationship on an contractual basis.

Supplementary Health Information Exchange (TISS) and Supplementary Health Unified Terminology (TUSS).

7

8

Regulatory Actions

• Health plan products with mixed mutualism and capitalization alternatives

• Analyze the Actuarial Technical Product Invoice.

• Assess the consequences of the currentintergenerational pact (six times between thelower and the higher age group)

• Debate: ―compulsory nature‖ of the system.

8

9

Consumer InsufficiencyRegulatory Actions

9

• Supplementary Health Performance Index (IDSS) – comparison of health plan providers.

• Consumer satisfaction index.

• Supplementary Health Financial Map.

• Waiting period portability.

• Operator accreditation program.

• Service provider qualification program.

• Qualiss.

• Georeferencing of the service provider network (Google).

• Electronic Health Records.

• Promoting health, preventing diseases and active aging

• Pursuit: possibility of comparing plans.

10

Topic 1 Sector Finaning Model;

Topic 2 Quality Guarantee and Assistencial Access;

Topic 3 Model of Payment to Service Providers;

Topic 4 Pharmaceutical Assistance;

Topic 5 Incentive to Competition;

Topic 6 Guarantee of Access to Information;

Topic 7 Old Agreements;

Topic 8 Assistance to the Elderly;

Topic 9 Integration of Supplementary Health with SUS.

Regulatory Agenda

Agenda 2011/2012ANS’ Commitment to Society

Regulatory

11

Returning to the assumptions.

• Regulatory action

Transparent

Efficient – do more with less (taxpayer $$)

Preferably inducing.

Pro-competitive.

Focused on the solution/reduction of the MARKET FLAW.

The regulation cannot be self-centered and...

... it needs to be self-destructive.

11

SECTOR DATA

Sector Development Department - DIDES/ANS

13

Health plan coverage ratio according to income groups (Brazil

– 1998, 2003 and 2008)

Source: IBGE, Department of Research, Work Coordination and Income, National Household Sample Survey 1998, 2003 and 2008. Access to and Use of Health Services.

Note: Excluding the income of people under 10 years of age and people, lodgers, maids and maids’ relatives.(2) Including people who received only in benefits.

2,64,8

9,4

18,6

34,7

54,0

76,2

2,96,7

14,1

24,9

83,8

3,8

8,7

24,5 24,6

65,8

43,8

83,2

25,9

69,2

47,4

27,1

15,9

0,0

20,0

40,0

60,0

80,0

100,0

Total Até 1 salário

mínimo

Mais de 1 a 2

salários mínimos

Mais de 2 a 3

salários mínimos

Mais de 3 a 5

salários mínimos

Mais de 5 a 10

salários mínimos

Mais de 10 a 20

salários mínimos

Mais de 20

salários mínimos

1998 2003 2008

To 1 minimum

wage

More than 1 to

2 minimum

wages

More than 2 to

3 minimum

wages

More than 3 to

5 minimum

wages

More than 5 to

10 minimum

wages

More than 10

to 20 minimum

wages

More than 20

minimum

wages

Total

14

Beneficiaries of private health plans by coverage of the plan(Brazil - 2000-2011)

Source: Beneficiary Information System – ANS/MS – 05/2011

30,7 31,1 31,1 31,833,7

35,036,8

38,540,4

41,7

45,446,6

2,8 3,2 3,8 4,4 5,5 6,17,3

8,810,4

12,714,6

15,8

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

45,0

50,0

dez/00 dez/01 dez/02 dez/03 dez/04 dez/05 dez/06 dez/07 dez/08 dez/10 dez/10 mai/11

Milh

ões

Assistência médica com ou sem odontologia

Exclusivamente odontológico

Health Care whith or without Dental Care

Only Dental Care

Mil

lio

n

15

Beneficiaries of health care plans by type of plan (Brazil 2000-2011)

Source: Beneficiary Information System – ANS/MS – 05/2011

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

dez/00 dez/01 dez/02 dez/03 dez/04 dez/05 dez/06 dez/07 dez/08 dez/09 dez/10 mai/11

Milh

ões

Coletivo empresarial Coletivo por adesão Individual Não InformadoCollective Corporate Collective Group Individual Not Informed

Mil

lio

n

16

Beneficiaries of collective health care plans by selected state(Brazil 2000-2011)

Source: Beneficiary Information System – ANS/MS – 05/2011

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

mar/00 mar/01 mar/02 mar/03 mar/04 mar/05 mar/06 mar/07 mar/08 mar/09 mar/10 mar/11

Milh

ões

RJ SP

RS MG

PE CE

Mill

ion

17

Coverage ratio of private health care plans by state (Brazil –May/2011)

Sources: Beneficiary Information System – ANS/MS – 05/2011 and Population – IBGE/DATASUS/2010

Up to 5%

Between 5% and 10%

Between 10% and 20%

Between 20% and 30%

More than 30%

18

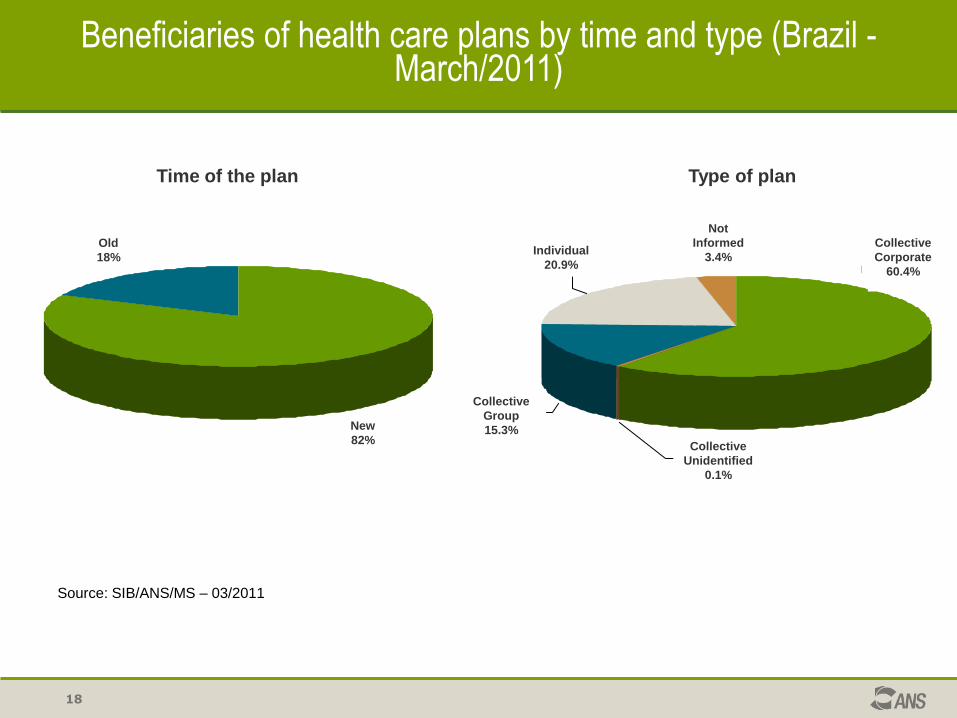

Beneficiaries of health care plans by time and type (Brazil -March/2011)

Source: SIB/ANS/MS – 03/2011

Time of the plan Type of plan

Novo

82%

Antigo

18%Coletivo

Empresarial

60,4%

Coletivo Não

identif icado

0,1%

Individual

20,9%

Não Informado

3,4%

Coletivo por

adesão

15,3%New

82%

Old

18%

Collective

Corporate

60.4%

Collective

Unidentified

0.1%

Collective

Group

15.3%

Individual

20.9%

Not

Informed

3.4%

19

Beneficiaries of health care plans

Age pyramid of health care plan beneficiaries, by type (Brazil - December/2010)

Source: SIB/ANS/MS – 12/2010

6,7

6,6

6,6

6,6

9,8

11,7

11,0

8,9

7,7

7,0

5,6

4,2

2,7

1,7

1,3

0,9

6,2

6,1

6,2

6,3

9,3

11,6

11,0

8,9

7,6

6,9

5,7

4,4

3,0

2,0

1,6

1,3

1,7

12,7

10,0

8,1

6,3

6,2

7,1

6,8

5,9

5,6

5,6

5,2

5,0

4,3

3,5

2,9

2,2

2,5

8,2

6,5

5,4

4,9

6,6

8,7

8,2

6,9

6,3

6,4

6,1

5,9

5,1

4,2

3,7

3,0

4,01,0

15,0 12,0 9,0 6,0 3,0 0,0 3,0 6,0 9,0 12,0 15,0

0 a 4 anos

5 a 9 anos

10 a 14 anos

15 a 19 anos

20 a 24 anos

25 a 29 anos

30 a 34 anos

35 a 39 anos

40 a 44 anos

45 a 49 anos

50 a 54 anos

55 a 59 anos

60 a 64 anos

65 a 69 anos

70 a 74 anos

75 a 79 anos

80 anos ou mais

Coletivo - Homens Coletivo - Mulheres

Individual - Homens Individual - Mulheres

(%)(%)0 to 4 years

5 to 9 years

10 to 14 years

15 to 19 years

20 to 24 years

25 to 29 years

30 to 34 years

35 to 39 years

40 to 44 years

45 to 49 years

50 to 54 years

55 to 59 years

60 to 64 years

65 to 69 years

70 to 74 years

75 to 79 years

80 years and over

Collective – Men

Individual - Men

Collective – Women

Individual - Women

1

2

3

7

10

19

37

91

491

0 50 100 150 200 250 300 350 400 450 500

30,1%

36,9%

41,1%

54,5%

60,3%

70,5%

80,3%

90,5%

100,0%

4.761.976

5.843.371

6.496.129

8.620.029

11.155.705

12.640.830

15.821.230

9.541.037

Número de operadoras

Pe

rce

ntu

al d

e b

en

efic

iário

s

14.323.375

20

Distribution of beneficiaries among the operators (Brazil – May/2011)

Health care beneficiaries Dental plan beneficiaries only

Sources: SIB/ANS/MS – 05/2011 and CADOP/ANS/MS – 05/2011

2

5

10

18

34

64

111

191

341

1.032

0 200 400 600 800 1.000 1.200

10,2%

20,0%

30,0%

40,0%

50,0%

60,2%

70,2%

80,1%

90,1%

100,0%

4.737.606

9.343.033

14.005.400

18.644.862

28.046.559

32.711.386

37.360.510

46.619.931

23.309.985

Número de operadoras

Pe

rce

ntu

al d

e b

en

eficiá

rio

s

41.991.473

Perc

enta

ge o

f B

eneficia

ries

Perc

en

tag

e o

f B

en

efi

cia

rie

s

Number of ProvidersNumber of Providers

21

Compensation revenue and assistencial expense of medical hospital operators (Brasil – 2003-2010)

Sources: DIOPS/ANS/MS – 08/19/2011 and FIP – 12/2006

Revenue (R$ billion)

Assistencial expense (R$ billion)

Loss Ratio (%)

22

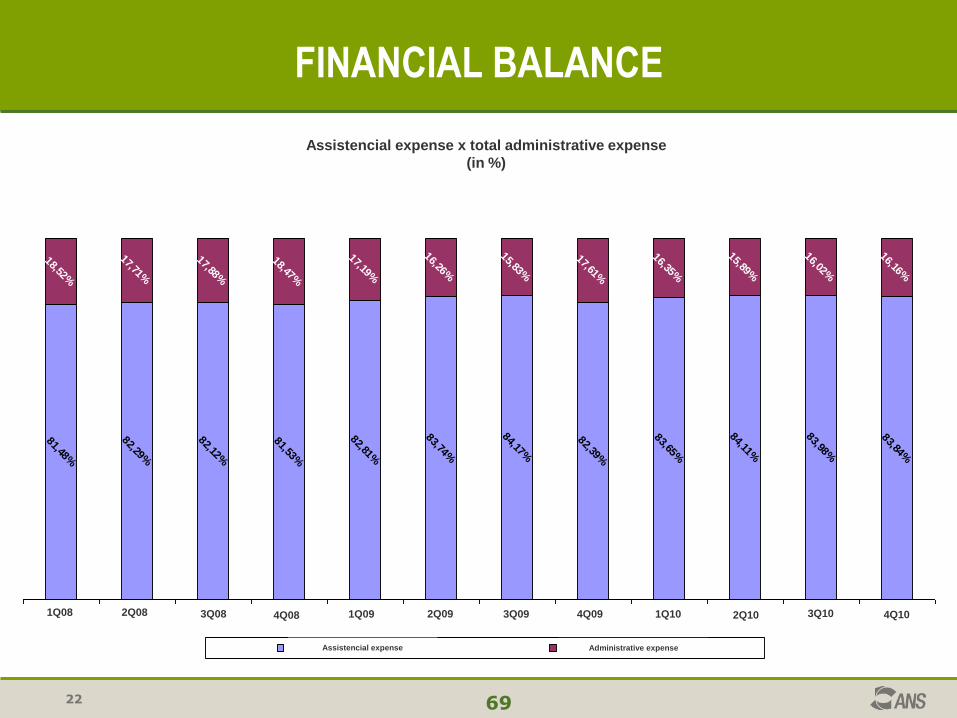

Efeitos Potenciais da Insolvência de OperadorasFINANCIAL BALANCE

69

Despesa Assistencial x Despesa Administrativa Total

(em %)

81,48%

82,29%

82,12%

81,53%

82,81%

83,74%

84,17%

82,39%

83,65%

84,11%

83,98%

83,84%

18,52%

17,71%

17,88%

18,47%

17,19%

16,26%

15,83%

17,61%

16,35%

15,89%

16,02%

16,16%

1ºtri08 2ºtri08 3ºtri08 4ºtri08 1ºtri09 2ºtri09 3ºtri09 4ºtri09 1ºtri10 2ºtri10 3ºtri10 4ºtri10

Despesa Assistencial Despesa Administrativa

Assistencial expense x total administrative expense

(in %)

Assistencial expense Administrative expense

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10

23

Efeitos Potenciais da Insolvência de OperadorasFINANCIAL BALANCE

73

MEDICINA DE GRUPO

Despesa Assistencial x Despesa Administrativa

83,05%

83,30%

82,25%

82,48%

82,85%

83,67%

83,62%

80,98%

83,93%

84,95%

83,46%

81,50%

16,95%

16,70%

17,75%

17,52%

17,15%

16,33%

16,38%

19,02%

16,07%

15,05%

16,54%

18,50%

1ºtri08 2ºtri08 3ºtri08 4ºtri08 1ºtri09 2ºtri09 3ºtri09 4ºtri09 1ºtri10 2ºtri10 3ºtri10 4ºtri10

Despesa Assistencial Despesa Administrativa

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10

GROUP MEDICINE

Assistencial Expense x Administrative Expense

Assistencial expense Administrative expense

24

Efeitos Potenciais da Insolvência de OperadorasFINANCIAL BALANCE

76

SEGURADORA

Despesa Assistencial x Despesa Administrativa

89,27%

89,52%

91,32%

90,35%

90,87%

91,83%

92,03%

91,54%

92,31%

91,89%

92,14%

91,18%

10,73%

10,48%

8,68%9,65%

9,13%

8,17%

7,97%

8,46%

7,69%

8,11%

7,86%8,82%

1ºtri08 2ºtri08 3ºtri08 4ºtri08 1ºtri09 2ºtri09 3ºtri09 4ºtri09 1ºtri10 2ºtri10 3ºtri10 4ºtri10

Despesa Assistencial Despesa Administrativa

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10

Assistencial expense Administrative expense

INSURANCE COMPANY

Assistencial Expense x Administrative Expense

25

Efeitos Potenciais da Insolvência de OperadorasFINANCIAL BALANCE

61

Liquidez Corrente

1,19

1,14

1,18

1,49 1,49 1,491,52

1,54

1,811,79

1,98

1,25 1,241,20

1,181,21

1,15

1,231,211,21

1,48

1,401,37

1,81

1ºtri08 2ºtri08 3ºtri08 4ºtri08 1ºtri09 2ºtri09 3ºtri09 4ºtri09 1ºtri10 2ºtri10 3ºtri10 4ºtri10

Médico Hospitalar (exclui Autogestão) Odontológicas

Fonte: Relatório PRISMA/ANS

Current Liquidity

Medical Hospital (excludes self-management) Dental

Source: PRISMA Report/ANS

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10

26

Efeitos Potenciais da Insolvência de OperadorasFINANCIAL BALANCE

60

Endividamento

0,62

0,68

0,53

0,62

0,67

0,640,68

0,69

0,65

0,66

0,660,640,67

0,600,57

0,58

0,58 0,58 0,59 0,59

0,62

0,56 0,56

0,54

1ºtri08 2ºtri08 3ºtri08 4ºtri08 1ºtri09 2ºtri09 3ºtri09 4ºtri09 1ºtri10 2ºtri10 3ºtri10 4ºtri10

Médico Hospitalar (exclui Autogestão) Odontológicas

Fonte: Relatório PRISMA/ANS

Debt

Medical Hospital (excludes self-management) Dental

Source: PRISMA Report/ANS

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10

27

Efeitos Potenciais da Insolvência de OperadorasPROFITABILITY

78

Retorno sobre o Ativo

0,010

0,005 0,005 0,005

0,0080,006

0,033

0,020

0,023

0,012

0,046

0,012

0,026

0,016

0,020

0,0040,005

0,010

0,021

0,015

0,027

0,0120,013

0,013

1ºtri08 2ºtri08 3ºtri08 4ºtri08 1ºtri09 2ºtri09 3ºtri09 4ºtri09 1ºtri10 2ºtri10 3ºtri10 4ºtri10

Médico Hospitalar (exclui Autogestão) Odontológicas

Fonte: Relatório PRISMA/ANS

Return on Assets

Medical Hospital (excludes self-management) Dental

Source: PRISMA Report/ANS

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10

28

Efeitos Potenciais da Insolvência de OperadorasPROFITABILITY

79

Retorno sobre o PL

0,014

0,025 0,0230,020

0,022

0,0280,033

0,075

0,057

0,069

0,051

0,114

0,046

0,0390,055

0,072

0,029

0,018

0,050

0,051

0,042

0,0380,034

0,066

1ºtri08 2ºtri08 3ºtri08 4ºtri08 1ºtri09 2ºtri09 3ºtri09 4ºtri09 1ºtri10 2ºtri10 3ºtri10 4ºtri10

Médico Hospitalar (exclui Autogestão) Odontológicas

Fonte: Relatório PRISMA/ANS

Return on Equity

Medical Hospital (excludes self-management) Dental

Source: PRISMA Report/ANS

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10

29

Efeitos Potenciais da Insolvência de OperadorasPROFITABILITY

80

Margem de Lucro Líquido

0,02

0,01

0,02

0,010,01

0,010,02

0,020,02

0,06

0,04

0,06

0,040,05

0,03

0,02

0,10

0,04

0,03

0,06

0,04

0,04 0,03

0,04

1ºtri08 2ºtri08 3ºtri08 4ºtri08 1ºtri09 2ºtri09 3ºtri09 4ºtri09 1ºtri10 2ºtri10 3ºtri10 4ºtri10

Médico Hospitalar (exclui Autogestão) Odontológicas

Fonte: Relatório PRISMA/ANS

Net Margin

Medical Hospital (excludes self-management) Dental

Source: PRISMA Report/ANS

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10

30

Efeitos Potenciais da Insolvência de OperadorasRISK

85

Prazo Médio

(em dias)

15,0614,70

23,79

25,8126,25

24,5025,09

22,3422,85

21,5120,91

21,56

19,4218,66

16,59

17,56

19,49

27,03

26,1025,74

26,89

25,3524,63

24,31

1ºtri08 2ºtri08 3ºtri08 4ºtri08 1ºtri09 2ºtri09 3ºtri09 4ºtri09 1ºtri10 2ºtri10 3ºtri10 4ºtri10

Contraprestrações a Receber Pagamento de Eventos

Fonte: Relatório PRISMA/ANS

Average Term

(in days)

Compensation receivable Payment of events

Source: PRISMA Report/ANS

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10

31

Efeitos Potenciais da Insolvência de OperadorasRISK

86

Ativos Garantidores

(em R$ milhões)

5.114,02 5.083,785.505,44 5.384,11 5.108,09 5.223,39

6.091,035.465,74

1.183,08 1.269,841.286,71 1.270,19

1.238,24 1.253,05

1.301,65

1.327,51

1.245,02 1.467,78

1.585,762.395,35 2.710,68

2.925,90

2.459,58

2.583,08480,88

515,12

527,10

624,07

-

-

-

-

1ºtri09 2ºtri09 3ºtri09 4ºtri09 1ºtri10 2ºtri10 3ºtri10 4ºtri10

Títulos e V. Mobiliários Privados (CETIP) Títulos Públicos (SELIC) Fundos Dedicados (CONVÊNIOS) Imóveis

Fonte: CETIP, SELIC, CBLC

Guaranteeing assets(in R$ million)

Private securities Government bonds (SELIC) Dedicated funds (PARTNERSHIPS)

Source: Cetip, Selic, CBLC

RealEstateProperty

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10

32

Efeitos Potenciais da Insolvência de OperadorasRISK

87

Ativos Garantidores

(em nº de operadoras)

419491

745

565648 666

761717

564492

238

418335 317

222266

1ºtri09 2ºtri09 3ºtri09 4ºtri09 1ºtri10 2ºtri10 3ºtri10 4ºtri10

Regulares Insuficientes

Fonte: ANS

Guaranteeing assets(in number of providers)

Regular Insufficient

Source: ANS

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10

33

Efeitos Potenciais da Insolvência de OperadorasRISK

89

Provisões Técnicas

(em nº de operadoras)

818 850 840907 889 884 888

938

165 133 14376 94 99 95

45

1ºtri09 2ºtri09 3ºtri09 4ºtri09 1ºtri10 2ºtri10 3ºtri10 4ºtri10

Regulares Insuficientes

Fontes: SAGA e controles internos/ANS

Technical Provisions(in number of providers)

Regular Insufficient

Source: SAGA and internal controls/ANS

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10

Thank you

Bruno Sobral Sector Development Officer

Diretoria de Desenvolvimento Setorial - DIDES/ANS