SUPPLEMENT DATED MARCH 2018 TO THE COLLEGE SAVE PLAN...

73

1 CSNDD-05666 Please file this Supplement to the College SAVE Plan Disclosure Statement and Participant Agreement with your records. SUPPLEMENT DATED JULY 2018 TO THE COLLEGE SAVE PLAN DISCLOSURE STATEMENT AND PARTICIPATION AGREEMENT DATED DECEMBER 2015 This Supplement describes important changes affecting College SAVE. Changes to the BND Match (formerly, the Matching Grant Program) Effective May 29, 2017, 2018, BND Match will no longer offer consecutive year matching. BND Match will only match a single year of contributions, up to $300. 1. The following replaces the first paragraph of the section entitled “BND Match” on page 26 of the Plan Disclosure Statement and page 2 of the January 2018 Supplement: BND Match The Bank has created BND Match, a program that will award a single year of matching grant(s) to North Dakota resident(s) and active duty military families that meet the eligibility requirements set forth below. Active duty Military families must be either (i) currently stationed on a military base located in North Dakota or (ii) former North Dakota residents stationed on a military base located outside of North Dakota. The matching grant amount is a dollar-for-dollar match and is based on Contributions up to $300.00 made by a Participant within 12 months of enrolling in BND Match. The BND Match award will be deposited into a separate matching grant account that is owned by the Bank and will be invested according to the allocation instructions on file for the Participant’s College SAVE Account. The BND Match account will be linked to the Participant’s College SAVE Account. Qualified withdrawals to Eligible Educational Institutions generally will be taken proportionately from the College SAVE Account and the related BND Match account. 2. The following replaces the fourth bulleted paragraph in the section entitled “BND Match” on page 26 of the Plan Disclosure Statement: A Participant’s adjusted gross income on the most recently filed North Dakota state income tax return must have been $0-$120,000, if married and filing jointly, or $0-$80,000, if single, to qualify for a one-time matching grant. If you are married, filing separately, a copy of your spouse’s North Dakota state income tax return must be included to determine your adjusted gross income. 3. The fifth bulleted paragraph in the section entitled “BND Match” on page 26 of the Plan Disclosure Statement is deleted. Changes to the Age-Based Options Beginning August 17, 2018, College SAVE will be making changes to the Age-Based Options. The glide path for the three Age-Based Options will be expanded to include six new Portfolios and will provide for a smoother transition as the Designated Beneficiary approaches college age and the asset allocation becomes more conservative. These six new Portfolios will only be available as part of the Age-Based Options and will not be available as Individual Portfolios. The new Portfolios are: Aggressive Portfolio, Blended Growth Portfolio, Blended Moderate Growth Portfolio, Conservative Portfolio, Balanced Income Portfolio, and Conservative Income Portfolio. If you are not invested in one of the Age-Based Options, the glide path changes will not affect your Account. If you have assets in one of the Age-Based Options, depending on the age of the Designated Beneficiary as of August 17, 2018, the addition of these new Portfolios may result in some or all of your assets moving from an existing Portfolio into one of the new Portfolios, or into a different existing Portfolio. You should consider the age of the Designated Beneficiary and review the glide path charts below to see if your investments will change. After August 17, 2018, participants who are invested in an Age-Based Option may end up with more, less, or the same amount of stock exposure. All changes to your Account resulting from these investment changes will be automatic and will not count towards your twice per year investment exchange limit. If you have not used your two allowable investment exchanges for 2018, you may choose to move some or all of your assets to other

Transcript of SUPPLEMENT DATED MARCH 2018 TO THE COLLEGE SAVE PLAN...

1 CSNDD-05666

Please file this Supplement to the College SAVE Plan Disclosure Statement and Participant Agreement with your records.

SUPPLEMENT DATED JULY 2018 TO THE COLLEGE SAVE

PLAN DISCLOSURE STATEMENT AND PARTICIPATION AGREEMENT DATED DECEMBER 2015

This Supplement describes important changes affecting College SAVE.

Changes to the BND Match (formerly, the Matching Grant Program)

Effective May 29, 2017, 2018, BND Match will no longer offer consecutive year matching. BND Match will only match a single year of contributions, up to $300.

1. The following replaces the first paragraph of the section entitled “BND Match” on page 26 of the Plan Disclosure Statement and page2 of the January 2018 Supplement:

BND Match

The Bank has created BND Match, a program that will award a single year of matching grant(s) to North Dakota resident(s) and activeduty military families that meet the eligibility requirements set forth below. Active duty Military families must be either (i) currentlystationed on a military base located in North Dakota or (ii) former North Dakota residents stationed on a military base located outsideof North Dakota. The matching grant amount is a dollar-for-dollar match and is based on Contributions up to $300.00 made by aParticipant within 12 months of enrolling in BND Match. The BND Match award will be deposited into a separate matching grantaccount that is owned by the Bank and will be invested according to the allocation instructions on file for the Participant’s CollegeSAVE Account. The BND Match account will be linked to the Participant’s College SAVE Account. Qualified withdrawals to EligibleEducational Institutions generally will be taken proportionately from the College SAVE Account and the related BND Match account.

2. The following replaces the fourth bulleted paragraph in the section entitled “BND Match” on page 26 of the Plan Disclosure Statement:

A Participant’s adjusted gross income on the most recently filed North Dakota state income tax return must have been $0-$120,000,if married and filing jointly, or $0-$80,000, if single, to qualify for a one-time matching grant. If you are married, filing separately, acopy of your spouse’s North Dakota state income tax return must be included to determine your adjusted gross income.

3. The fifth bulleted paragraph in the section entitled “BND Match” on page 26 of the Plan Disclosure Statement is deleted.

Changes to the Age-Based Options

Beginning August 17, 2018, College SAVE will be making changes to the Age-Based Options. The glide path for the three Age-Based Options will be expanded to include six new Portfolios and will provide for a smoother transition as the Designated Beneficiary approaches college age and the asset allocation becomes more conservative. These six new Portfolios will only be available as part of the Age-Based Options and will not be available as Individual Portfolios. The new Portfolios are: Aggressive Portfolio, Blended Growth Portfolio, Blended Moderate Growth Portfolio, Conservative Portfolio, Balanced Income Portfolio, and Conservative Income Portfolio.

If you are not invested in one of the Age-Based Options, the glide path changes will not affect your Account. If you have assets in one of the Age-Based Options, depending on the age of the Designated Beneficiary as of August 17, 2018, the addition of these new Portfolios may result in some or all of your assets moving from an existing Portfolio into one of the new Portfolios, or into a different existing Portfolio. You should consider the age of the Designated Beneficiary and review the glide path charts below to see if your investments will change. After August 17, 2018, participants who are invested in an Age-Based Option may end up with more, less, or the same amount of stock exposure.

All changes to your Account resulting from these investment changes will be automatic and will not count towards your twice per year investment exchange limit.

If you have not used your two allowable investment exchanges for 2018, you may choose to move some or all of your assets to other

2 CSNDD-05666

Portfolios at any time before and after the transition (except for the blackout period as specified below).

Transition Information

The transition will begin at 4 p.m. ET on Thursday, August 16, 2018, and is expected to be completed by Monday, August 20, 2018. On Friday, August 17, 2018 we will calculate your current Account balances, and College SAVE will reinvest those balances in your new Investment Options, as applicable.

To facilitate the transition, you will not be able to access your Account or request transactions (including contributions, withdrawals, rollovers, or investment exchanges) online or by phone starting at 4 p.m. ET on Thursday, August 16, 2018, through 8 a.m. ET on Monday, August 20, 2018, while the changes are being implemented. NSCC transactions will not be accepted beginning on Wednesday, August 15, 2018. Participants will bear the risk of any investment loss or gain during this blackout period. You will also be unable to initiate or request any other Account changes online or by phone during this blackout period. Recurring contributions scheduled for Friday, August 17, 2018, and Participant transaction or Account change requests received by mail in good order after the close of the New York Stock Exchange on Thursday, August 16, 2018, will be processed after completion of the transition, using Portfolio Unit prices as of Monday, August 20, 2018.

Additional information (including details about the transition and the new Portfolios underlying the Age Based Options) are provided below and through our website at www.collegesave4u.com as the time for the transition approaches.

The following table details some key dates and actions.*

Key Dates Action

Ongoing Contact a Client Service Representative at 866-SAVE-529 (1-866-728-3529) if you have any questions regarding your Account.

August 14, 2018 Tuesday, August 14, 2018 is the last day financial advisors can initiate transactions through the NSCC prior to the transition. We will not accept transactions through the NSCC beginning on Wednesday, August 15, 2018.

August 16, 2018 We will not accept contributions, transactions or maintenance requests, including withdrawals or Investment Option changes, after 4 p.m. ET, on Thursday, August 16, 2018.

August 16 -August 20, 2018

Account assets are transferred and allocations updated. You will not have access to your Account during this time period.

August 20, 2018 First day of transaction processing following the transition. Transaction requests received in good order after 4 p.m. ET on Thursday, August 16, 2018 and by 4 p.m. ET on Monday, August 20, 2018 will be processed using Unit Values as of 4 p.m. ET on Monday, August 20. We will begin accepting NSCC transactions.

*All dates are approximate.

1. Effective August 20, 2018, the following replaces the table on page 14 of the Plan Disclosure Statement, assupplemented in the April 2016 Supplement:

Age of Designated Beneficiary

Conservative Option Moderate Option Aggressive Option

Newborn through 4 years Blended Growth Portfolio* 62.5% Stocks 37.5% Bonds

Aggressive Portfolio* 87.5% Stocks 12.5% Bonds

Aggressive Growth Portfolio 100% Stocks

5 through 6 years Moderate Growth Portfolio 50% Stocks 50% Bonds

Growth Portfolio 75% Stocks 25% Bonds

Aggressive Portfolio* 87.5% Stocks 12.5% Bonds

7 through 8 years Blended Moderate Growth Portfolio* 37.5% Stocks 62.5% Bonds

Blended Growth Portfolio* 62.5% Stocks 37.5% Bonds

Aggressive Portfolio* 87.5% Stocks 12.5% Bonds

3 CSNDD-05666

9 through 10 years Conservative Growth Portfolio 25% Stocks 75% Bonds

Moderate Growth Portfolio 50% Stocks 50% Bonds

Growth Portfolio 75% Stocks 25% Bonds

11 through 12 years Conservative Portfolio* 12.5% Stocks 87.5% Bonds

Blended Moderate Growth Portfolio* 37.5% Stocks 62.5% Bonds

Blended Growth Portfolio* 62.5% Stocks 37.5% Bonds

13 through 14 years Income Portfolio 75% Bonds 25% Short-Term Reserves

Conservative Growth Portfolio 25% Stocks 75% Bonds

Moderate Growth Portfolio 50% Stocks 50% Bonds

15 through 16 Years Balanced Income Portfolio* 50% Bonds 50% Short-Term Reserves

Conservative Portfolio* 12.5% Stocks 87.5% Bonds

Blended Moderate Growth Portfolio* 37.5% Stocks 62.5% Bonds

17 through 18 years Conservative Income Portfolio* 25% Bonds 75% Short-Term Reserves

Income Portfolio 75% Bonds 25% Short-Term Reserves

Conservative Growth Portfolio 25% Stocks 75% Bonds

19 years or older Interest Accumulation Portfolio 100% Short-Term Reserves

Income Portfolio 75% Bonds 25% Short-Term Reserves

Conservative Portfolio* 12.5% Stocks 87.5% Bonds

*Not available for investment as an Individual Investment Option.

4 CSNDD-05666

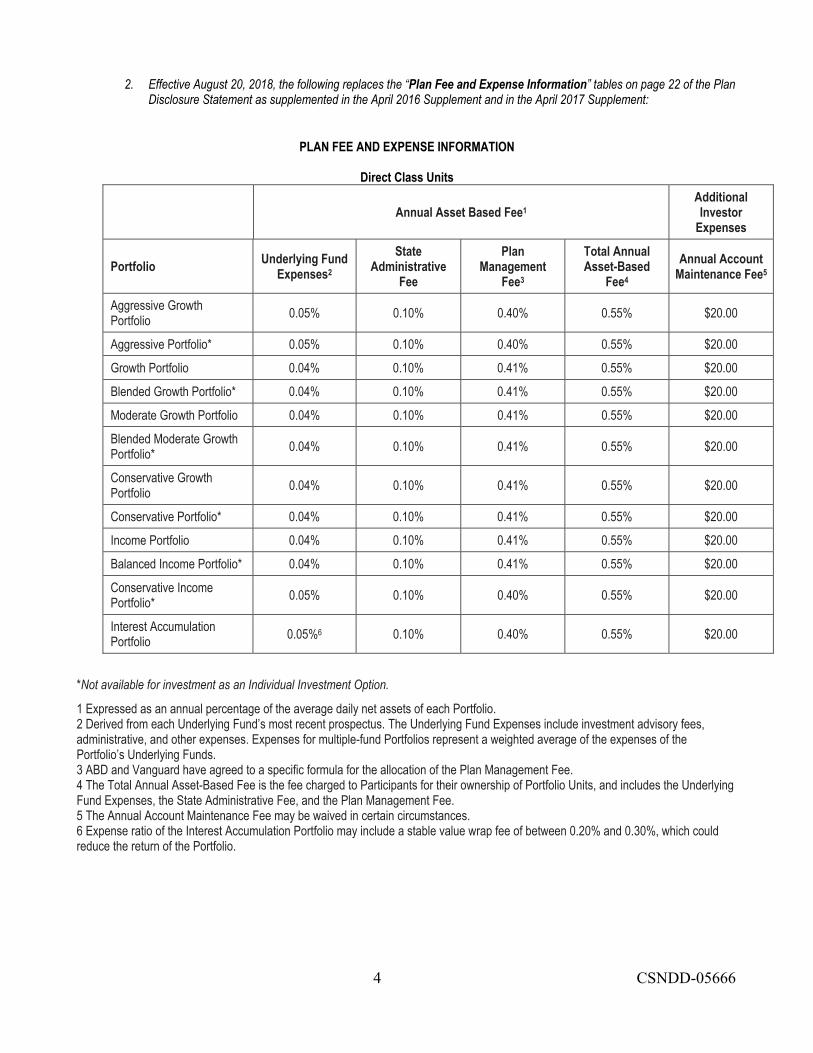

2. Effective August 20, 2018, the following replaces the “Plan Fee and Expense Information” tables on page 22 of the PlanDisclosure Statement as supplemented in the April 2016 Supplement and in the April 2017 Supplement:

PLAN FEE AND EXPENSE INFORMATION

Direct Class Units

Annual Asset Based Fee1 Additional Investor

Expenses

Portfolio Underlying Fund

Expenses2

State Administrative

Fee

Plan Management

Fee3

Total Annual Asset-Based

Fee4

Annual Account Maintenance Fee5

Aggressive Growth Portfolio

0.05% 0.10% 0.40% 0.55% $20.00

Aggressive Portfolio* 0.05% 0.10% 0.40% 0.55% $20.00

Growth Portfolio 0.04% 0.10% 0.41% 0.55% $20.00

Blended Growth Portfolio* 0.04% 0.10% 0.41% 0.55% $20.00

Moderate Growth Portfolio 0.04% 0.10% 0.41% 0.55% $20.00

Blended Moderate Growth Portfolio*

0.04% 0.10% 0.41% 0.55% $20.00

Conservative Growth Portfolio

0.04% 0.10% 0.41% 0.55% $20.00

Conservative Portfolio* 0.04% 0.10% 0.41% 0.55% $20.00

Income Portfolio 0.04% 0.10% 0.41% 0.55% $20.00

Balanced Income Portfolio* 0.04% 0.10% 0.41% 0.55% $20.00

Conservative Income Portfolio*

0.05% 0.10% 0.40% 0.55% $20.00

Interest Accumulation Portfolio 0.05%6 0.10% 0.40% 0.55% $20.00

*Not available for investment as an Individual Investment Option.

1 Expressed as an annual percentage of the average daily net assets of each Portfolio. 2 Derived from each Underlying Fund’s most recent prospectus. The Underlying Fund Expenses include investment advisory fees, administrative, and other expenses. Expenses for multiple-fund Portfolios represent a weighted average of the expenses of the Portfolio’s Underlying Funds. 3 ABD and Vanguard have agreed to a specific formula for the allocation of the Plan Management Fee. 4 The Total Annual Asset-Based Fee is the fee charged to Participants for their ownership of Portfolio Units, and includes the Underlying Fund Expenses, the State Administrative Fee, and the Plan Management Fee. 5 The Annual Account Maintenance Fee may be waived in certain circumstances. 6 Expense ratio of the Interest Accumulation Portfolio may include a stable value wrap fee of between 0.20% and 0.30%, which could reduce the return of the Portfolio.

5 CSNDD-05666

Advisor Class Units

Annual Asset Based Fee1 Additional Investor

Expenses

Portfolio Underlying

Fund Expenses2

State Administrative

Fee

Distribution and

Service Fee

Plan Management

Fee3

Total Annual Asset-

Based Fee4

Annual Account

Maintenance Fee5

Aggressive Growth Portfolio

0.05% 0.10% 0.30% 0.40% 0.85% $20.00

Aggressive Portfolio* 0.05% 0.10% 0.30% 0.40% 0.85% $20.00

Growth Portfolio 0.04% 0.10% 0.30% 0.41% 0.85% $20.00

Blended Growth Portfolio* 0.04% 0.10% 0.30% 0.41% 0.85% $20.00

Moderate Growth Portfolio 0.04% 0.10% 0.30% 0.41% 0.85% $20.00

Blended Moderate Growth Portfolio* 0.04% 0.10% 0.30% 0.41% 0.85% $20.00

Conservative Growth Portfolio

0.04% 0.10% 0.30% 0.41% 0.85% $20.00

Conservative Portfolio* 0.04% 0.10% 0.30% 0.41% 0.85% $20.00

Income Portfolio 0.05% 0.10% 0.30% 0.40% 0.85% $20.00

Balanced Income Portfolio* 0.04% 0.10% 0.30% 0.41% 0.85% $20.00

Conservative Income Portfolio*

0.05% 0.10% 0.30% 0.40% 0.85% $20.00

Interest Accumulation Portfolio 0.05%6 0.10% 0.00%7 0.40% 0.55% $20.00

*Not available for investment as an Individual Investment Option.

1 Expressed as an annual percentage of the average daily net assets of each Portfolio. 2 Derived from each Underlying Fund’s most recent prospectus. The Underlying Fund Expenses include investment advisory fees, administrative, and other expenses. Expenses for multiple-fund Portfolios represent a weighted average of the expenses of the Portfolio’s Underlying Funds. 3 ABD and Vanguard have agreed to a specific formula for the allocation of the Plan Management Fee. 4 The Total Annual Asset-Based Fee is the fee charged to Participants for their ownership of Portfolio Units, and includes the Underlying Fund Expenses, the State Administrative Fee, and the Plan Management Fee. 5 The Annual Account Maintenance Fee may be waived in certain circumstances. 6 Expense ratio of the Interest Accumulation Portfolio may include a stable value wrap fee of between 0.20% and 0.30%, which could reduce the return of the Portfolio. 7 The Distribution and Service Fee is currently being waived on assets on the Interest Accumulation Portfolio for the benefit of Participants.

6 CSNDD-05666

3. Effective August 20, 2018, the following new section is added beginning on page 19 of the Plan Disclosure Statement:

Additional Multi-Fund Portfolios

Certain Portfolios are only available within the Age-Based Option and not as a stand-alone Individual Portfolio. Information about their investment strategies and risks is presented below.

Aggressive Portfolio

Investment Objective The Portfolio seeks to provide capital appreciation.

Investment Strategy The Portfolio invests in two Vanguard stock index funds and two Vanguard bond index funds, resulting in an allocation of 87.5% of assets to stocks and 12.5% to bonds. The percentages of the Portfolio’s assets allocated to each Underlying Fund are:

Vanguard Total Stock Market Index Fund 52.50% Vanguard Total International Stock Index Fund 35.00% Vanguard Total Bond Market II Index Fund 8.75% Vanguard Total International Bond Index Fund 3.75%

Through its investment in Vanguard Total Stock Market Index Fund, the Portfolio indirectly invests in U.S. stocks. The Fund employs an indexing investment approach designed to track the performance of the CRSP US Total Market Index, which represents approximately 100% of the investable U.S. stock market and includes large-, mid-, small-, and micro-cap stocks regularly traded on the New York Stock Exchange (“NYSE”) and Nasdaq. The Fund invests by sampling the Index, meaning that it holds a broadly diversified collection of securities that, in the aggregate, approximates the full Index in terms of key characteristics. These key characteristics include industry weightings and market capitalization, as well as certain financial measures, such as price/earnings ratio and dividend yield.

Through its investment in Vanguard Total International Stock Index Fund, the Portfolio also indirectly invests in international stocks. The Fund employs an indexing investment approach designed to track the performance of the FTSE Global All Cap ex US Index, a float-adjusted, market-capitalization-weighted index designed to measure equity market performance of companies located in developed and emerging markets, excluding the United States. As of October 31, 2017, the Index includes approximately 5,902 stocks of companies located in 46 countries. The largest markets covered in the Index as of October 31, 2017, were Japan, the United Kingdom, Canada, France, Germany, and China (which made up approximately 17%, 13%, 7%, 7%, 7%, and 6%, respectively, of the Index’s market capitalization). The Fund invests all, or substantially all, of its assets in the common stocks included in its target index.

Through its investment in Vanguard Total Bond Market II Index Fund, the Portfolio also indirectly invests in U.S. bonds. The Fund employs an indexing investment approach designed to track the performance of the Bloomberg Barclays U.S. Aggregate Float Adjusted Index. This Index represents a wide spectrum of public, investment-grade, taxable, fixed income securities in the United States—including government, corporate, and international dollar-denominated bonds, as well as mortgage-backed and asset-backed securities—all with maturities of more than 1 year. The Fund invests by sampling the Index, meaning that it holds a broadly diversified collection of securities that, in the aggregate, approximates the full Index in terms of key risk factors and characteristics. All of the Fund’s investments will be selected through the sampling process, and at least 80% of the Fund’s assets will be invested in bonds held in the Index. The Fund maintains a dollar-weighted average maturity consistent with that of the Index, which generally ranges between 5 and 10 years.

Through its investment in Vanguard Total International Bond Index Fund, the Portfolio also indirectly invests in international bonds. The Fund employs an indexing investment approach designed to track the performance of the Bloomberg Barclays Global Aggregate ex-USD Float Adjusted RIC Capped Index (USD Hedged), which provides a broad-based measure of the global, investment-grade, fixed-rate debt markets. The Index includes government, government agency, corporate, and securitized non-U.S. investment-grade fixed income investments, all issued in currencies other than the U.S. dollar and with maturities of more than one year. The Index is capped to comply with investment company diversification standards of the Internal Revenue Code, which state that, at the close of each fiscal quarter, a fund’s (1) exposure to any particular bond issuer may not exceed 25% of the fund’s assets, and (2) aggregate exposure to issuers that individually constitute 5% or more of the fund may not exceed 50% of the fund’s assets. To help enforce these limits, if the Index, on the last business day of any month, were to have greater than 20% exposure to any particular bond issuer, or greater than 48% aggregate

7 CSNDD-05666

exposure to issuers that individually constitute 5% or more of the Index, then the excess would be reallocated to bonds of other issuers represented in the Index. The Index methodology is not designed to satisfy the diversification requirements of the Investment Company Act of 1940. The Fund will attempt to hedge its foreign currency exposure, primarily through the use of foreign currency exchange forward contracts, in order to correlate to the returns of the Index, which is U.S. dollar hedged. Such hedging is intended to minimize the currency risk associated with investment in bonds denominated in currencies other than the U.S. dollar. The Fund invests by sampling the Index, meaning that it holds a range of securities that, in the aggregate, approximates the full Index in terms of key risk factors and other characteristics. All of the Fund’s investments will be selected through the sampling process and, under normal circumstances, at least 80% of the Fund’s assets will be invested in bonds included in the Index. The Fund maintains a dollar-weighted average maturity consistent with that of the Index, which generally ranges between 5 and 10 years.

Investment Risks The Portfolio invests 87.5% of its assets in stock funds and the remaining 12.5% in bond funds. Through its U.S. and international stock fund holdings, the Portfolio is subject to stock market risk, country/regional risk, currency risk, and emerging markets risk. Through its U.S. and international bond fund holdings, the Portfolio is subject to interest rate risk, income risk, prepayment risk, extension risk, call risk, credit risk, country/regional risk, liquidity risk, currency hedging risk, and derivatives risk. The Portfolio is also subject to investment style risk and index sampling risk, and, through its investment in Vanguard Total International Bond Index Fund, nondiversification risk.

Blended Growth Portfolio

Investment Objective The Portfolio seeks to provide capital appreciation and low to moderate current income.

Investment Strategy The Portfolio invests in two Vanguard stock index funds and two Vanguard bond index funds, resulting in an allocation of 62.5% of assets to stocks and 37.5% to bonds. The percentages of the Portfolio’s assets allocated to each Underlying Fund are:

Vanguard Total Stock Market Index Fund 37.50% Vanguard Total International Stock Index Fund 25.00% Vanguard Total Bond Market II Index Fund 26.25% Vanguard Total International Bond Index Fund 11.25%

Through its investment in Vanguard Total Stock Market Index Fund, the Portfolio indirectly invests in U.S. stocks. The Fund employs an indexing investment approach designed to track the performance of the CRSP US Total Market Index, which represents approximately 100% of the investable U.S. stock market and includes large-, mid-, small-, and micro-cap stocks regularly traded on the New York Stock Exchange (“NYSE”) and Nasdaq. The Fund invests by sampling the Index, meaning that it holds a broadly diversified collection of securities that, in the aggregate, approximates the full Index in terms of key characteristics. These key characteristics include industry weightings and market capitalization, as well as certain financial measures, such as price/earnings ratio and dividend yield.

Through its investment in Vanguard Total International Stock Index Fund, the Portfolio also indirectly invests in international stocks. The Fund employs an indexing investment approach designed to track the performance of the FTSE Global All Cap ex US Index, a float-adjusted, market-capitalization-weighted index designed to measure equity market performance of companies located in developed and emerging markets, excluding the United States. As of October 31, 2017, the Index includes approximately 5,902 stocks of companies located in 46 countries. The largest markets covered in the Index as of October 31, 2017, were Japan, the United Kingdom, Canada, France, Germany, and China (which made up approximately 17%, 13%, 7%, 7%, 7%, and 6%, respectively, of the Index’s market capitalization). The Fund invests all, or substantially all, of its assets in the common stocks included in its target index.

Through its investment in Vanguard Total Bond Market II Index Fund, the Portfolio also indirectly invests in U.S. bonds. The Fund employs an indexing investment approach designed to track the performance of the Bloomberg Barclays U.S. Aggregate Float Adjusted Index. This Index represents a wide spectrum of public, investment-grade, taxable, fixed income securities in the United States—including government, corporate, and international dollar-denominated bonds, as well as mortgage-backed and asset-backed securities—all with maturities of more than 1 year. The Fund invests by sampling the Index, meaning that it holds a broadly diversified collection of securities that, in the aggregate, approximates the full Index in terms of key risk factors and other characteristics. All of the Fund’s investments will be selected through the sampling process, and at least 80% of the Fund’s assets will be invested in bonds held in the Index. The Fund maintains a dollar-weighted average maturity consistent with that of the Index, which generally ranges between 5 and 10 years.

8 CSNDD-05666

Through its investment in Vanguard Total International Bond Index Fund, the Portfolio also indirectly invests in international bonds. The Fund employs an indexing investment approach designed to track the performance of the Bloomberg Barclays Global Aggregate ex-USD Float Adjusted RIC Capped Index (USD Hedged), which provides a broad-based measure of the global, investment-grade, fixed-rate debt markets. The Index includes government, government agency, corporate, and securitized non-U.S. investment-grade fixed income investments, all issued in currencies other than the U.S. dollar and with maturities of more than one year. The Index is capped to comply with investment company diversification standards of the Internal Revenue Code, which state that, at the close of each fiscal quarter, a fund’s (1) exposure to any particular bond issuer may not exceed 25% of the fund’s assets, and (2) aggregate exposure to issuers that individually constitute 5% or more of the fund may not exceed 50% of the fund’s assets. To help enforce these limits, if the Index, on the last business day of any month, were to have greater than 20% exposure to any particular bond issuer, or greater than 48% aggregate exposure to issuers that individually constitute 5% or more of the Index, then the excess would be reallocated to bonds of other issuers represented in the Index. The Index methodology is not designed to satisfy the diversification requirements of the Investment Company Act of 1940. The Fund will attempt to hedge its foreign currency exposure, primarily through the use of foreign currency exchange forward contracts, in order to correlate to the returns of the Index, which is U.S. dollar hedged. Such hedging is intended to minimize the currency risk associated with investment in bonds denominated in currencies other than the U.S. dollar. The Fund invests by sampling the Index, meaning that it holds a range of securities that, in the aggregate, approximates the full Index in terms of key risk factors and other characteristics. All of the Fund’s investments will be selected through the sampling process and, under normal circumstances, at least 80% of the Fund’s assets will be invested in bonds included in the Index. The Fund maintains a dollar-weighted average maturity consistent with that of the Index, which generally ranges between 5 and 10 years.

Investment Risks The Portfolio invests 62.5% of its assets in stock funds and the remaining 37.5% in bond funds. Through its U.S. and international stock fund holdings, the Portfolio is subject to stock market risk, country/regional risk, currency risk, and emerging markets risk. Through its U.S. and international bond fund holdings, the Portfolio is subject to is subject to interest rate risk, income risk, prepayment risk, extension risk, call risk, credit risk, country/regional risk, liquidity risk, currency hedging risk, and derivatives risk. The Portfolio is also subject to investment style risk and index sampling risk, and, through its investment in Vanguard Total International Bond Index Fund, nondiversification risk.

Blended Moderate Growth Portfolio

Investment Objective The Portfolio seeks to provide income and some capital appreciation.

Investment Strategy The Portfolio invests in two Vanguard stock index funds and two Vanguard bond index funds, resulting in an allocation of 62.5% of assets to bonds and 37.5% to stocks. The percentages of the Portfolio’s assets allocated to each Underlying Fund are:

Vanguard Total Bond Market II Index Fund 43.75% Vanguard Total International Bond Index Fund 18.75% Vanguard Total Stock Market Index Fund 22.50% Vanguard Total International Stock Index Fund 15.00%

Through its investment in Vanguard Total Bond Market II Index Fund, the Portfolio indirectly invests in U.S. bonds. The Fund employs an indexing investment approach designed to track the performance of the Bloomberg Barclays U.S. Aggregate Float Adjusted Index. This Index represents a wide spectrum of public, investment-grade, taxable, fixed income securities in the United States—including government, corporate, and international dollar-denominated bonds, as well as mortgage-backed and asset-backed securities—all with maturities of more than 1 year. The Fund invests by sampling the Index, meaning that it holds a broadly diversified collection of securities that, in the aggregate, approximates the full Index in terms of key risk factors and other characteristics. All of the Fund’s investments will be selected through the sampling process, and at least 80% of the Fund’s assets will be invested in bonds held in the Index. The Fund maintains a dollar-weighted average maturity consistent with that of the Index, which generally ranges between 5 and 10 years.

Through its investment in Vanguard Total International Bond Index Fund, the Portfolio also indirectly invests in international bonds. The Fund employs an indexing investment approach designed to track the performance of the Bloomberg Barclays Global Aggregate ex-USD Float Adjusted RIC Capped Index (USD Hedged), which provides a broad-based measure of the global, investment-grade, fixed-rate debt markets. The Index includes government, government agency, corporate, and securitized non-U.S. investment-grade fixed income investments, all issued in currencies other than the U.S. dollar and with maturities of more than one year. The Index is capped to comply

9 CSNDD-05666

with investment company diversification standards of the Internal Revenue Code, which state that, at the close of each fiscal quarter, a fund’s (1) exposure to any particular bond issuer may not exceed 25% of the fund’s assets, and (2) aggregate exposure to issuers that individually constitute 5% or more of the fund may not exceed 50% of the fund’s assets. To help enforce these limits, if the Index, on the last business day of any month, were to have greater than 20% exposure to any particular bond issuer, or greater than 48% aggregate exposure to issuers that individually constitute 5% or more of the Index, then the excess would be reallocated to bonds of other issuers represented in the Index. The Index methodology is not designed to satisfy the diversification requirements of the Investment Company Act of 1940. The Fund will attempt to hedge its foreign currency exposure, primarily through the use of foreign currency exchange forward contracts, in order to correlate to the returns of the Index, which is U.S. dollar hedged. Such hedging is intended to minimize the currency risk associated with investment in bonds denominated in currencies other than the U.S. dollar. The Fund invests by sampling the Index, meaning that it holds a range of securities that, in the aggregate, approximates the full Index in terms of key risk factors and other characteristics. All of the Fund’s investments will be selected through the sampling process and, under normal circumstances, at least 80% of the Fund’s assets will be invested in bonds included in the Index. The Fund maintains a dollar-weighted average maturity consistent with that of the Index, which generally ranges between 5 and 10 years.

Through its investment in Vanguard Total Stock Market Index Fund, the Portfolio indirectly invests in U.S. stocks. The Fund employs an indexing investment approach designed to track the performance of the CRSP US Total Market Index, which represents approximately 100% of the investable U.S. stock market and includes large-, mid-, small-, and micro-cap stocks regularly traded on the New York Stock Exchange (“NYSE”) and Nasdaq. The Fund invests by sampling the Index, meaning that it holds a broadly diversified collection of securities that, in the aggregate, approximates the full Index in terms of key characteristics. These key characteristics include industry weightings and market capitalization, as well as certain financial measures, such as price/earnings ratio and dividend yield.

Through its investment in Vanguard Total International Stock Index Fund, the Portfolio indirectly invests in international stocks. The Fund employs an indexing investment approach designed to track the performance of the FTSE Global All Cap ex US Index, a float-adjusted, market-capitalization-weighted index designed to measure equity market performance of companies located in developed and emerging markets, excluding the United States. As of October 31, 2017, the Index includes approximately 5,902 stocks of companies located in 46 countries. The largest markets covered in the Index as of October 31, 2017, were Japan, the United Kingdom, Canada, France, Germany, and China (which made up approximately 17%, 13%, 7%, 7%, 7%, and 6%, respectively, of the Index’s market capitalization). The Fund invests all, or substantially all, of its assets in the common stocks included in its target index.

Investment Risks The Portfolio invests 62.5% of its assets in bond funds and the remaining 37.5% in stock funds. Through its U.S. and international bond holdings, the Portfolio is subject to interest rate risk, income risk, prepayment risk, extension risk, call risk, credit risk, country/regional risk, liquidity risk, currency hedging risk, and derivatives risk. Through its U.S. and international stock holdings, the Portfolio is subject to stock market risk, country/regional risk, currency risk, and emerging markets risk. The Portfolio is also subject to investment style risk and index sampling risk, and, through its investment in Vanguard Total International Bond Index Fund, nondiversification risk.

Conservative Portfolio

Investment Objective The Portfolio seeks to provide income and some capital appreciation.

Investment Strategy The Portfolio invests in two Vanguard bond index funds and two Vanguard stock index funds, resulting in an allocation of 87.5% of assets to bonds and 12.5% of assets to stocks. The percentages of the Portfolio’s assets allocated to each Underlying Fund are:

Vanguard Total Bond Market II Index Fund 61.25% Vanguard Total International Bond Index Fund 26.25% Vanguard Total Stock Market Index Fund 7.50% Vanguard Total International Stock Index Fund 5.00%

Through its investment in Vanguard Total Bond Market II Index Fund, the Portfolio indirectly invests in U.S. bonds. The Fund employs an indexing investment approach designed to track the performance of the Bloomberg Barclays U.S. Aggregate Float Adjusted Index. This Index represents a wide spectrum of public, investment-grade, taxable, fixed income securities in the United States—including government, corporate, and international dollar-denominated bonds, as well as mortgage-backed and asset-backed securities—all with maturities of more than 1 year. The Fund invests by sampling the Index, meaning that it holds a broadly diversified collection of securities

10 CSNDD-05666

that, in the aggregate, approximates the full Index in terms of key risk factors and other characteristics. All of the Fund’s investments will be selected through the sampling process, and at least 80% of the Fund’s assets will be invested in bonds held in the Index. The Fund maintains a dollar-weighted average maturity consistent with that of the Index, which generally ranges between 5 and 10 years.

Through its investment in Vanguard Total International Bond Index Fund, the Portfolio also indirectly invests in international bonds. The Fund employs an indexing investment approach designed to track the performance of the Bloomberg Barclays Global Aggregate ex-USD Float Adjusted RIC Capped Index (USD Hedged), which provides a broad-based measure of the global, investment-grade, fixed-rate debt markets. The Index includes government, government agency, corporate, and securitized non-U.S. investment-grade fixed income investments, all issued in currencies other than the U.S. dollar and with maturities of more than one year. The Index is capped to comply with investment company diversification standards of the Internal Revenue Code, which state that, at the close of each fiscal quarter, a fund’s (1) exposure to any particular bond issuer may not exceed 25% of the fund’s assets, and (2) aggregate exposure to issuers that individually constitute 5% or more of the fund may not exceed 50% of the fund’s assets. To help enforce these limits, if the Index, on the last business day of any month, were to have greater than 20% exposure to any particular bond issuer, or greater than 48% aggregate exposure to issuers that individually constitute 5% or more of the Index, then the excess would be reallocated to bonds of other issuers represented in the Index. The Index methodology is not designed to satisfy the diversification requirements of the Investment Company Act of 1940. The Fund will attempt to hedge its foreign currency exposure, primarily through the use of foreign currency exchange forward contracts, in order to correlate to the returns of the Index, which is U.S. dollar hedged. Such hedging is intended to minimize the currency risk associated with investment in bonds denominated in currencies other than the U.S. dollar. The Fund invests by sampling the Index, meaning that it holds a range of securities that, in the aggregate, approximates the full Index in terms of key risk factors and other characteristics. All of the Fund’s investments will be selected through the sampling process and, under normal circumstances, at least 80% of the Fund’s assets will be invested in bonds included in the Index. The Fund maintains a dollar-weighted average maturity consistent with that of the Index, which generally ranges between 5 and 10 years.

Through its investment in Vanguard Institutional Total Stock Market Index Fund, the Portfolio also indirectly invests in U.S. stocks. The Fund employs an indexing investment approach designed to track the performance of the CRSP US Total Market Index, which represents approximately 100% of the investable U.S. stock market and includes large-, mid-, small-, and micro-cap stocks regularly traded on the New York Stock Exchange (“NYSE”) and Nasdaq. The Fund invests by sampling the Index, meaning that it holds a broadly diversified collection of securities that, in the aggregate, approximates the full Index in terms of key characteristics. These key characteristics include industry weightings and market capitalization, as well as certain financial measures, such as price/earnings ratio and dividend yield.

Through its investment in Vanguard Total International Stock Index Fund, the Portfolio also indirectly invests in international stocks. The Fund employs an indexing investment approach designed to track the performance of the FTSE Global All Cap ex US Index, a float-adjusted, market-capitalization-weighted index designed to measure equity market performance of companies located in developed and emerging markets, excluding the United States. As of October 31, 2017, the Index includes approximately 5,902 stocks of companies located in 46 countries. The largest markets covered in the Index as of October 31, 2017, were Japan, the United Kingdom, Canada, France, Germany, and China (which made up approximately 17%, 13%, 7%, 7%, 7%, and 6%, respectively, of the Index’s market capitalization). The Fund invests all, or substantially all, of its assets in the common stocks included in its target index.

Investment Risks The Portfolio invests 87.5% of its assets in bond funds and the remaining 12.5% in stock funds. Through its U.S. and international bond holdings, the Portfolio is subject to interest rate risk, income risk, prepayment risk, extension risk, call risk, credit risk, country/regional risk, liquidity risk, currency hedging risk, and derivatives risk. Through its U.S. and international stock holdings, the Portfolio is subject to stock market risk, country/regional risk, currency risk, and emerging markets risk. The Portfolio is also subject to investment style risk and index sampling risk, and, through its investment in Vanguard Total International Bond Index Fund, nondiversification risk.

Balanced Income Portfolio

Investment Objective The Portfolio seeks to provide current income.

Investment Strategy The Portfolio invests in three Vanguard bond funds and a Vanguard Short-Term Reserves Account, resulting in an allocation of 50% of

11 CSNDD-05666

its assets to investment-grade bonds and 50% of assets to short-term investments. The percentages of the Portfolio’s assets allocated to each Underlying Fund are:

Vanguard Total Bond Market II Index Fund 23.00% Vanguard Total International Bond Index Fund 15.00% Vanguard Short-Term Inflation-Protected Securities Index Fund 12.00% Vanguard Short-Term Reserves Account 50.00%

Through its investment in Vanguard Total Bond Market II Index Fund, the Portfolio indirectly invests in U.S. bonds. The Fund employs an indexing investment approach designed to track the performance of the Bloomberg Barclays U.S. Aggregate Float Adjusted Index. This Index represents a wide spectrum of public, investment-grade, taxable, fixed income securities in the United States—including government, corporate, and international dollar-denominated bonds, as well as mortgage-backed and asset-backed securities—all with maturities of more than 1 year. The Fund invests by sampling the Index, meaning that it holds a broadly diversified collection of securities that, in the aggregate, approximates the full Index in terms of key risk factors and other characteristics. All of the Fund’s investments will be selected through the sampling process, and at least 80% of the Fund’s assets will be invested in bonds held in the Index. The Fund maintains a dollar-weighted average maturity consistent with that of the Index, which generally ranges between 5 and 10 years.

Through its investment in Vanguard Total International Bond Index Fund, the Portfolio also indirectly invests in international bonds. The Fund employs an indexing investment approach designed to track the performance of the Bloomberg Barclays Global Aggregate ex-USD Float Adjusted RIC Capped Index (USD Hedged), which provides a broad-based measure of the global, investment-grade, fixed-rate debt markets. The Index includes government, government agency, corporate, and securitized non-U.S. investment-grade fixed income investments, all issued in currencies other than the U.S. dollar and with maturities of more than one year. The Index is capped to comply with investment company diversification standards of the Internal Revenue Code, which state that, at the close of each fiscal quarter, a fund’s (1) exposure to any particular bond issuer may not exceed 25% of the fund’s assets, and (2) aggregate exposure to issuers that individually constitute 5% or more of the fund may not exceed 50% of the fund’s assets. To help enforce these limits, if the Index, on the last business day of any month, were to have greater than 20% exposure to any particular bond issuer, or greater than 48% aggregate exposure to issuers that individually constitute 5% or more of the Index, then the excess would be reallocated to bonds of other issuers represented in the Index. The Index methodology is not designed to satisfy the diversification requirements of the Investment Company Act of 1940. The Fund will attempt to hedge its foreign currency exposure, primarily through the use of foreign currency exchange forward contracts, in order to correlate to the returns of the Index, which is U.S. dollar hedged. Such hedging is intended to minimize the currency risk associated with investment in bonds denominated in currencies other than the U.S. dollar. The Fund invests by sampling the Index, meaning that it holds a range of securities that, in the aggregate, approximates the full Index in terms of key risk factors and other characteristics. All of the Fund’s investments will be selected through the sampling process and, under normal circumstances, at least 80% of the Fund’s assets will be invested in bonds included in the Index. The Fund maintains a dollar-weighted average maturity consistent with that of the Index, which generally ranges between 5 and 10 years.

Through its investment in Vanguard Short-Term Inflation-Protected Securities Index Fund, the Portfolio also indirectly invests in inflation-indexed bonds. The Fund employs an indexing investment approach designed to track the performance of the Bloomberg Barclays U.S. Treasury Inflation-Protected Securities (TIPS) 0-5 Year Index. The Index is a market-capitalization-weighted index that includes all inflation-protected public obligations issued by the U.S. Treasury with remaining maturities of less than 5 years. The Fund attempts to replicate the target index by investing all, or substantially all, of its assets in the securities that make up the Index, holding each security in approximately the same proportion as its weighting in the Index. The Fund maintains a dollar-weighted average maturity consistent with that of the target index, which generally does not exceed 3 years.

Through its investment in Vanguard Short-Term Reserves Account, the Portfolio indirectly invests in funding agreements issued by one or more insurance companies, synthetic investment contracts, and shares of Vanguard Federal Money Market Fund. Funding agreements are interest-bearing contracts that are structured to preserve principal and accumulate interest earnings over the life of the investment. The agreements pay interest at a fixed minimum rate and have fixed maturity dates that normally range from 2 to 5 years. Vanguard Federal Money Market Fund invests primarily in high-quality, short-term money market instruments. Under normal circumstances, at least 80% of the Fund’s assets are invested in securities issued by the U.S. government and its agencies and instrumentalities. Although these securities are high-quality, most of the securities held by the Fund are neither guaranteed by the U.S. Treasury nor supported by the full faith and credit of the U.S. government. To be considered high quality, a security must be determined by Vanguard to present minimal credit risk based in part on a consideration of maturity, portfolio diversification, portfolio liquidity, and credit quality. The Fund maintains a dollar-weighted average maturity of 60 days or less and a dollar-weighted average life of 120 days or less. Under money market reforms, government money market funds are required to invest at least 99.5% of their total assets in cash, government securities, and/or repurchase agreements that are collateralized solely by government securities or cash (collectively, government securities). The Fund generally invests 100% of its assets in government securities and therefore will satisfy the 99.5%

12 CSNDD-05666

requirement for designation as a government money market fund.

Note: It is possible to lose money by investing in Vanguard Federal Money Market Fund. Although the Fund seeks to preserve the value of a shareholder’s investment at $1.00 per share, it cannot guarantee it will do so. An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The Fund’s sponsor has no legal obligation to provide financial support to the Fund, and shareholders should not expect that the sponsor will provide financial support to the Fund at any time.

Investment Risks The Portfolio is subject to interest rate risk, income risk, prepayment risk, extension risk, call risk, credit risk, liquidity risk, currency hedging risk, country/regional risk, and derivatives risk. The Portfolio is also subject to nondiversification risk (through its investment in Vanguard Total International Bond Index Fund), income fluctuation risk (through its Investment in Vanguard Short-Term Inflation-Protected Securities Index Fund), and manager risk (through its investment in Vanguard Short-Term Reserves Account, which invests a portion of its assets in Vanguard Federal Money Market Fund).

Conservative Income Portfolio

Investment Objective The Portfolio seeks to provide current income and some inflation protection as well as income consistent with the preservation of principal.

Investment Strategy The Portfolio invests in three Vanguard bond funds and a Vanguard Short-Term Reserves Account, resulting in an allocation of 25% of its assets to investment-grade bonds and 75% of assets to short-term investments. The percentages of the Portfolio’s assets allocated to each Underlying Fund are:

Vanguard Total Bond Market II Index Fund 11.50% Vanguard Total International Bond Index Fund 7.50% Vanguard Short-Term Inflation-Protected Securities Index Fund 6.00% Vanguard Short-Term Reserves Account 75.00%

Through its investment in Vanguard Total Bond Market II Index Fund, the Portfolio indirectly invests in U.S. bonds. The Fund employs an indexing investment approach designed to track the performance of the Bloomberg Barclays U.S. Aggregate Float Adjusted Index. This Index represents a wide spectrum of public, investment-grade, taxable fixed income securities in the United States—including government, corporate, and international dollar-denominated bonds, as well as mortgage-backed and asset-backed securities—all with maturities of more than 1 year. The Fund invests by sampling the Index, meaning that it holds a broadly diversified collection of securities that, in the aggregate, approximates the full Index in terms of key risk factors and other characteristics. All of the Fund’s investments will be selected through the sampling process, and at least 80% of the Fund’s assets will be invested in bonds held in the Index. The Fund maintains a dollar-weighted average maturity consistent with that of the Index, which generally ranges between 5 and 10 years.

Through its investment in Vanguard Total International Bond Index Fund, the Portfolio also indirectly invests in international bonds. The Fund employs an indexing investment approach designed to track the performance of the Bloomberg Barclays Global Aggregate ex-USD Float Adjusted RIC Capped Index (USD Hedged), which provides a broad-based measure of the global, investment-grade, fixed-rate debt markets. The Index includes government, government agency, corporate, and securitized non-U.S. investment-grade fixed income investments, all issued in currencies other than the U.S. dollar and with maturities of more than one year. The Index is capped to comply with investment company diversification standards of the Internal Revenue Code, which state that, at the close of each fiscal quarter, a fund’s (1) exposure to any particular bond issuer may not exceed 25% of the fund’s assets, and (2) aggregate exposure to issuers that individually constitute 5% or more of the fund may not exceed 50% of the fund’s assets. To help enforce these limits, if the Index, on the last business day of any month, were to have greater than 20% exposure to any particular bond issuer, or greater than 48% aggregate exposure to issuers that individually constitute 5% or more of the Index, then the excess would be reallocated to bonds of other issuers represented in the Index. The Index methodology is not designed to satisfy the diversification requirements of the Investment Company Act of 1940. The Fund will attempt to hedge its foreign currency exposure, primarily through the use of foreign currency exchange forward contracts, in order to correlate to the returns of the Index, which is U.S. dollar hedged. Such hedging is intended to minimize the currency risk associated with investment in bonds denominated in currencies other than the U.S. dollar. The Fund invests by sampling the Index, meaning that it holds a range of securities that, in the aggregate, approximates the full Index in terms of key risk factors and

13 CSNDD-05666

other characteristics. All of the Fund’s investments will be selected through the sampling process and, under normal circumstances, at least 80% of the Fund’s assets will be invested in bonds included in the Index. The Fund maintains a dollar-weighted average maturity consistent with that of the Index, which generally ranges between 5 and 10 years.

Through its investment in Vanguard Short-Term Inflation-Protected Securities Index Fund, the Portfolio also indirectly invests in inflation-indexed bonds. The Fund employs an indexing investment approach designed to track the performance of the Bloomberg Barclays U.S. Treasury Inflation-Protected Securities (TIPS) 0-5 Year Index. The Index is a market-capitalization-weighted index that includes all inflation-protected public obligations issued by the U.S. Treasury with remaining maturities of less than 5 years. The Fund attempts to replicate the target index by investing all, or substantially all, of its assets in the securities that make up the Index, holding each security in approximately the same proportion as its weighting in the Index. The Fund maintains a dollar-weighted average maturity consistent with that of the target index, which generally does not exceed 3 years.

Through its investment in Vanguard Short-Term Reserves Account, the Portfolio indirectly invests in funding agreements issued by one or more insurance companies, synthetic investment contracts, and shares of Vanguard Federal Money Market Fund. Funding agreements are interest-bearing contracts that are structured to preserve principal and accumulate interest earnings over the life of the investment. The agreements pay interest at a fixed minimum rate and have fixed maturity dates that normally range from 2 to 5 years. Vanguard Federal Money Market Fund invests primarily in high-quality, short-term money market instruments. Under normal circumstances, at least 80% of the Fund’s assets are invested in securities issued by the U.S. government and its agencies and instrumentalities. Although these securities are high-quality, most of the securities held by the Fund are neither guaranteed by the U.S. Treasury nor supported by the full faith and credit of the U.S. government. To be considered high quality, a security must be determined by Vanguard to present minimal credit risk based in part on a consideration of maturity, portfolio diversification, portfolio liquidity, and credit quality. The Fund maintains a dollar-weighted average maturity of 60 days or less and a dollar-weighted average life of 120 days or less. Under money market reforms, government money market funds are required to invest at least 99.5% of their total assets in cash, government securities, and/or repurchase agreements that are collateralized solely by government securities or cash (collectively, government securities). The Fund generally invests 100% of its assets in government securities and therefore will satisfy the 99.5% requirement for designation as a government money market fund.

Note: It is possible to lose money by investing in Vanguard Federal Money Market Fund. Although the Fund seeks to preserve the value of a shareholder’s investment at $1.00 per share, it cannot guarantee it will do so. An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The Fund’s sponsor has no legal obligation to provide financial support to the Fund, and shareholders should not expect that the sponsor will provide financial support to the Fund at any time.

Investment Risks The Portfolio is subject to interest rate risk, income risk, prepayment risk, extension risk, call risk, credit risk, liquidity risk, currency hedging risk, country/regional risk, and derivatives risk. The Portfolio is also subject to nondiversification risk (through its investment in Vanguard Total International Bond Index Fund), income fluctuation risk (through its Investment in Vanguard Short-Term Inflation-Protected Securities Index Fund), and manager risk (through its investment in Vanguard Short-Term Reserves Account, which invests a portion of its assets in Vanguard Federal Money Market Fund).

1 CSNDD-05165

Please file this Supplement to the College SAVE Plan Disclosure Statement and Participant Agreement with your records.

SUPPLEMENT DATED MARCH 2018 TO THE COLLEGE SAVE

PLAN DISCLOSURE STATEMENT AND PARTICIPATION AGREEMENT DATED DECEMBER 2015

This Supplement describes important changes affecting College SAVE.

Federal Law Updates. Major tax changes approved by Congress in the Tax Cuts and Jobs Act became law on December 22, 2017. The following is an overview of those changes applicable to 529 Plans:

Expanded Definition Of Qualified Higher Education Expenses. Effective for distributions made after December 31, 2017, the definition of “qualified higher education expenses” under Section 529 is expanded to include expenses for tuition in connection with enrollment or attendance at an elementary or secondary public, private, or religious school (not to exceed $10,000 per tax year in the aggregate across all qualified tuition programs for a beneficiary) (“K-12 Tuition Expenses”). As such, earnings on distributions from a 529 Plan Account used for K-12 Tuition Expenses will be free of federal income tax. It is the Participant’s responsibility to ensure that distributions for K-12 Tuition Expenses do not exceed the aggregate limit for a Designated Beneficiary.

Certain Rollovers From 529 Plans To ABLE Programs Not Be Subject To Federal Income Tax. Effective for periods prior to January 1, 2026, rollovers from a 529 Plan Account to an ABLE account for the same Designated Beneficiary or to another beneficiary who is a Member of the Family will be free of federal income tax, subject to the annual contribution limits for ABLE accounts. Amounts withdrawn from a 529 Plan Account may be treated as a rollover to an ABLE account for federal tax purposes if the amount withdrawn is re-deposited within 60 days into an ABLE account, subject to the limitations in the immediately preceding sentence. You should consult your tax advisor regarding your individual situation, including whether to rollover to an ABLE account. An ABLE account is an account as defined in Section 529A(e)(6) of the Code that is generally used to pay for qualified disability expenses of a designated beneficiary in accordance with a program established under Section 529A of the Code and sponsored by a state or state agency.

North Dakota Tax Implications. For purposes of North Dakota state income taxes, North Dakota will follow the federal law updates as they relate to 529 Plan distributions made for K-12 Tuition Expenses and rollovers from 529 Plan Accounts to ABLE accounts, subject to the details and limitations described above.

If you are not a North Dakota resident, the state(s) where you pay income tax may differ in its state income tax treatment of K-12 Expenses and rollovers from 529 Plans to ABLE plans. You should consult with your tax advisor regarding your individual situation.

Important Information Regarding Age-Based Options. Certain investment options may be less suitable for short-term investment goals. The Age-Based Options are designed to take into account a Designated Beneficiary’s age and the number of years before the Designated Beneficiary is expected to attend higher education and are not designed for saving for K-12 Expenses. You should consider your investment time horizon before you select your investment options.

1. Effective as of January 1, 2018, throughout the Program Disclosure Statement, all references to “Ascensus Broker Dealer Services, Inc.” shall be deleted and replaced with “Ascensus Broker Dealer Services, LLC.”

2 CSNDD-05165

2. The following replaces the section entitled Contributions on page 27 of the Program Disclosure Statement: Contributions

You may contribute money to the Plan by any of the following methods: check, money order, recurring contribution, payroll direct deposit, EBT, transfer from a Upromise Service account, third-party checks payable to a Participant or a Designated Beneficiary and properly endorsed to the Plan, Ugift, or a rollover. The Plan will not accept Contributions made with cash, traveler’s checks, starter checks, bank courtesy checks, credit cards, credit card checks, instant loan checks, third-party checks over ten-thousand dollars ($10,000.00), checks drawn on banks located outside the U.S., checks not in U.S. dollars, checks dated more than one-hundred eighty (180) days before the Plan receives it, postdated checks, checks with unclear instructions, other checks the Plan deems unacceptable, stocks, securities, or other non-bank account assets.

1 CSNDD-04624

Please file this Supplement to the College SAVE Plan Disclosure Statement and Participant Agreement with your records.

SUPPLEMENT DATED JANUARY 2018 TO THE COLLEGE SAVE

PLAN DISCLOSURE STATEMENT AND PARTICIPATION AGREEMENT DATED DECEMBER 2015

This Supplement describes important changes affecting College SAVE. Portfolio Performance The following tables replace the “Average Annual Total Returns” table on page 21 of the Plan Disclosure Statement as supplemented in the January 2017 Supplement: AVERAGE ANNUAL TOTAL RETURNS AS OF SEPTEMBER 30, 2017 – Advisor Class

Name 1 Year 3 Year 5 Year 10 Year Since

Inception Inception

Date

Aggressive Growth Portfolio - Advisor 18.04% 8.30% 11.37% 5.24% 6.15% 11/03/06

Growth Portfolio - Advisor 13.03% 6.81% 8.93% 5.59% 6.15% 11/03/06

Moderate Growth Portfolio - Advisor 8.14% 5.33% 6.42% 4.84% 5.28% 11/03/06

Conservative Growth Portfolio - Advisor 3.14% 3.63% 3.87% 3.92% 4.26% 11/03/06

Income Portfolio - Advisor -0.67% 1.25% 0.47% 2.53% 2.71% 11/03/06

Interest Accumulation Portfolio - Advisor 0.40% --- --- 5.24% 0.30% 06/03/16

AVERAGE ANNUAL TOTAL RETURNS AS OF SEPTEMBER 30, 2017 – Direct Class

Name 1 Year 3 Year 5 Year 10 Year Since

Inception Inception

Date

Aggressive Growth Portfolio - Direct --- --- --- --- 6.60% 05/05/17

Growth Portfolio - Direct --- --- --- --- 5.20% 05/05/17

Moderate Growth Portfolio - Direct --- --- --- --- 3.90% 05/05/17

Conservative Growth Portfolio - Direct --- --- --- --- 2.60% 05/05/17

Income Portfolio - Direct --- --- --- --- 0.80% 05/05/17

Interest Accumulation Portfolio - Direct --- --- --- --- 0.30% 05/05/17

IRS Increases Annual Federal Gift Tax Exclusion

As of January 1, 2018, the federal annual gift tax exclusion increased to $15,000 for a single individual, $30,000 if married filing jointly (and spouses elect to split gifts). For 529 Plans, contributions of up to $75,000 for a single individual, $150,000 if married filing jointly (and spouses elect to split gifts) can be made in a single year and applied against the annual gift tax exclusion equally over a five-year period. Accordingly, all references to the exclusion of contributions from federal gift tax found in the “College SAVE Plan Highlights” section on page 7 of the Plan Disclosure Statement and in the first paragraph of the “Federal and State Tax Treatment” section on page 34 of the Plan Disclosure Statement are updated to reflect the increase beginning January 1, 2018 and

2 CSNDD-04624

these increased amounts.

Name Changes to Grant Programs

Effective December 21, 2017, the name of the Children FIRST Program changed to New Baby Match and the name of the Matching Grant Program changed to BND Match. Accordingly, all references in the Plan Disclosure Statement to Children FIRST or the Children First Program are updated to New Baby Match and all references in the Plan Disclosure Statement to Matching Grant or the Matching Grant Program are updated to BND Match.

Military Families May Participate in BND Match (formerly, the Matching Grant Program)

The North Dakota residency eligibility requirement for BND Match is waived for active duty military families who are either (i) currently stationed on a military base located in North Dakota or (ii) former North Dakota residents stationed on a military base located outside of North Dakota.

Accordingly, the following replaces the first sentence of the first paragraph of the section entitled “Matching Grant Program” on page 26 of the Plan Disclosure Statement:

The Bank has created BND Match, a program that will award matching grant(s) to North Dakota resident(s) and active duty military families that meet the eligibility requirements set forth below. Active duty Military families must be either (i) currently stationed on a military base located in North Dakota or (ii) former North Dakota residents stationed on a military base located outside of North Dakota.

Accordingly, the following replaces the third bullet point of the second paragraph of the section entitled “Matching Grant Program” on page 26 of the Plan Disclosure Statement:

The Participant must have recently filed a North Dakota state income tax return as a North Dakota resident prior to submitting a BND Match Application. (If the Participant has not recently filed a North Dakota state income tax return or the Participant does not have a copy of his/ her most recently filed North Dakota state income tax return (or a copy of the spouse’s North Dakota state income tax return because he/she filed separately) at this time, the Participant will provide other evidence of eligibility upon request.) This requirement does not apply to active duty military families; however active duty military families may be asked to provide federal tax returns or other supporting documentation evidencing prior residency in North Dakota or current residency on a military base located in North Dakota.

Other Changes

The following replaces: (i) the second paragraph of the section entitled “Tax Considerations” on page 2 of the Plan Disclosure Statement; (ii) the section entitled “State tax and other benefits” on page 12 of the Plan Disclosure Statement; and (iii) the fourth paragraph in the section entitled “Federal and State Tax Treatment” on page 33 of the Plan Disclosure Statement:

If you are not an North Dakota taxpayer, consider before investing whether your or the Beneficiary’s home state offers a 529 Plan that provides its taxpayers with favorable state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that may only be available through investment in the home state’s 529 Plan. Since different states have different tax provisions, this Plan Disclosure Statement contains limited information about the state tax consequences of investing in College SAVE. Therefore, please consult your financial, tax, or other advisor to learn more about how state-based benefits (or any limitations) would apply to your specific circumstances. You also may wish to contact your home state’s 529 Plan(s), or any other 529 Plan, to learn more about those plans’ features, benefits, and limitations. Keep in mind that state-based benefits should be one of many appropriately weighted factors to be considered when making an investment decision.

1 CSNDD-02940

Please file this Supplement to the College SAVE Plan Disclosure Statement and Participant Agreement with your records.

SUPPLEMENT DATED APRIL 2017 TO THE COLLEGE SAVE

PLAN DISCLOSURE STATEMENT AND PARTICIPATION AGREEMENT DATED DECEMBER 2015

This Supplement describes important changes affecting College SAVE. Launch of Advisor and Direct Class Units Effective May 5, 2017, College SAVE will offer the following two different fee structures: Direct Class and Advisor Class. Units invested under the Direct Class are referred to as “Direct Class Units” and Units invested under the Advisor Class are referred to as “Advisor Class Units”. Advisor Class Units are only available to Participants who utilize the services of a Financial Advisor to invest in the Plan. Direct Class Units are only available to Participants who do not use a Financial Advisor to invest in the Plan. The Underlying Fund Expenses, State Administrative Fee, Plan Management Fee and Annual Account Maintenance Fee are the same for both Classes. The Advisor Class includes a 0.30% Distribution and Service Fee that is paid to Financial Advisors for certain distribution and Account related services. The Distribution and Service Fee will be waived on assets in the Interest Accumulation Portfolio. The Advisor Class Units will be subject to the same Total Annual Asset-Based Fee of 0.85% that was charged to Portfolios prior to the fee structure change. The Direct Class Units will be subject to a Total Annual Asset-Based Fee of 0.55%. Effective May 5, 2017, Units owned by Participants with a Financial Advisor on file with the Plan will be designated as Advisor Class Units and Units owned by Participants without a Financial Advisor will be designated as Direct Class Units. Please note that there will be no change in the Portfolio allocations currently held by Participants in their Accounts. Accordingly, effective May 5, 2017, the following replaces the row entitled “Fees & Expenses” in the “College SAVE Plan Highlights” table on page 6 of the Plan Disclosure Statement:

Fees & Expenses Annual Account Maintenance Fee:

$20 (waived for certain qualifying Accounts)

Total Annual Asset-Based Fee:

Advisor Class Units: 0.85% for each Portfolio (0.55% for Interest Accumulation Portfolio)

Direct Class Units: 0.55% for each Portfolio

Participants will bear fees and expenses at the Plan level and also bear the cost of investing in the Underlying Funds. The fees and expenses are described in detail in this Plan Disclosure Statement.

See Part IV. Plan Fees and Expenses, page 21

Accordingly, effective May 5, 2017, the following terms are added to the “Key Terms” section on page 9 of the Plan Disclosure Statement: Dealer – A distributor of the College SAVE who is registered as a broker-dealer under the Securities Exchange Act of 1934, as amended, and a member of both the Financial Industry Regulatory Authority and the Municipal Securities Rulemaking Board. Financial Advisor – Certain broker-dealers, financial advisors, or properly licensed investment advisers that offer College SAVE to investors. Accordingly, effective May 5, 2017, the following replaces the first paragraph of the section entitled “Asset Based Fees” on page 21 of the Plan Disclosure Statement: The Plan charges an expense ratio (Total Annual Asset-Based Fee) for each Portfolio as specified in the Plan Fee and Expense Information tables below. This fee includes the Underlying Fund Expenses, the State Administrative Fee, the Distribution and Marketing

2 CSNDD-02940

Fee (applicable only to Advisor Class), and the Plan Management Fee, which are charged daily against the assets in each Portfolio. The expense ratio of a Portfolio, and that of an Underlying Fund, may change at any time without notice. Accordingly, effective May 5, 2017, the following is added as a new section under the section entitled “Plan Management Fee” on page 22 of the Plan Disclosure Statement: Distribution and Service Fee. The Advisor Class Units are subject to an ongoing annual Distribution and Service Fee of 0.30% of Portfolio assets attributable to such Unit class. This fee is accrued daily, is factored into the Portfolio’s Unit Value, and is paid quarterly to Dealers. The Dealers may pay some portion or the entire amount received to third parties, such as your Financial Advisor, that provide distribution and Account servicing functions. See the Advisor Class Units table below. Accordingly, effective May 5, 2017, the section entitled “Other Compensation” on page 22 of the Plan Disclosure Statement is hereby deleted. Accordingly, effective May 5, 2017, the following replaces the “Plan Fee and Expense Information “table on page 22 of the Plan Disclosure Statement as supplemented in the April 2016 Supplement.

PLAN FEE AND EXPENSE INFORMATION

Direct Class Units

Annual Asset Based Fee1 Additional Investor

Expenses

Portfolio Underlying Fund

Expenses2 State

Administrative Fee Plan Management

Fee3 Total Annual

Asset-Based Fee4 Annual Account

Maintenance Fee5

Aggressive Growth Portfolio 0.04% 0.10% 0.41% 0.55% $20.00

Growth Portfolio 0.04% 0.10% 0.41% 0.55% $20.00

Moderate Growth Portfolio 0.04% 0.10% 0.41% 0.55% $20.00

Conservative Growth Portfolio 0.03% 0.10% 0.42% 0.55% $20.00

Income Portfolio 0.05% 0.10% 0.40% 0.55% $20.00

Interest Accumulation Portfolio 0.08%6 0.10% 0.37% 0.55% $20.00 1 Expressed as an annual percentage of the average daily net assets of each Portfolio. 2 Derived from each Underlying Fund’s most recent prospectus. The Underlying Fund Expenses include investment advisory fees, administrative, and other expenses. Expenses for multiple-fund Portfolios represent a weighted average of the expenses of the Portfolio’s Underlying Funds. 3 ABD and Vanguard have agreed to a specific formula for the allocation of the Plan Management Fee. 4 The Total Annual Asset-Based Fee is the fee charged to Participants for their ownership of Portfolio Units, and includes the Underlying Fund Expenses, the State Administrative Fee, and the Plan Management Fee. 5 The Annual Account Maintenance Fee may be waived in certain circumstances. 6 Expense ratio of the Interest Accumulation Portfolio may include a stable value wrap fee of between 0.20% and 0.30%, which could reduce the return of the Portfolio.

3 CSNDD-02940

Advisor Class Units

Annual Asset Based Fee1 Additional Investor

Expenses

Portfolio Underlying

Fund Expenses2

State Administrative

Fee

Distribution and Service

Fee

Plan Management

Fee3

Total Annual Asset-Based

Fee4

Annual Account Maintenance

Fee5

Aggressive Growth Portfolio 0.04% 0.10% 0.30% 0.41% 0.85% $20.00

Growth Portfolio 0.04% 0.10% 0.30% 0.41% 0.85% $20.00

Moderate Growth Portfolio 0.04% 0.10% 0.30% 0.41% 0.85% $20.00

Conservative Growth Portfolio 0.03% 0.10% 0.30% 0.42% 0.85% $20.00

Income Portfolio 0.05% 0.10% 0.30% 0.40% 0.85% $20.00