SuperWHAT IS Activity 1 ears 7-10 SUPERANNUATION? · PDF fileSuperWHAT IS Activity 1...

45

Tax, Super+You. Page 1 Take Control. Super Activity 1 WHAT IS SUPERANNUATION? Fact sheet Years 7-10 The materials in Super have been designed to be used in a variety of ways. Each topic is designed as a stand-alone section to be explored by a whole class, small groups or individual students WHAT IS SUPER? Have you ever saved up to buy something? Maybe you are putting money aside at the moment to buy a car or something that is important to you. Superannuation, often called super, is money you set aside during your working life to provide an income to live on when you retire from work. Most people start to contribute to super when they begin work and keep contributing until they retire. The money is invested in one or more super funds of your choice. You must leave your super in your fund until you either reach a minimum age or meet strict requirements set by the government. Your super is invested in assets such as bank accounts, property or shares, which earn an income. This income is reinvested in your super fund and then earns more income. This process, where you can generate earnings from previous earnings, is called compounding and greatly increases your final super payout. The government encourages super savings by offering tax concessions that are not available with other forms of saving. In addition, no tax is charged for most people when they retire at 60 or older and take their super as a regular pension or a lump sum. WHY IS SUPER IMPORTANT TO ME? Super is important for you because the more super you accumulate during your working life, the higher your standard of living will be in retirement. In general, most Australians would like to have a higher income in retirement than that offered by the government age pension. Over time, the age pension will provide a basic safety net for older Australians, which will be supplemented or even replaced by the income generated from superannuation. Demographic changes and greater life expectancy have increased the proportion of the Australian population in the retirement age group. Currently there are five people of working age for every person aged 65 and over but by 2047 that will reduce to just 2.4. The demand for government pensions and services will increase, and the number of people in the working age groups will fall. There will be significantly less people in the workforce contributing through taxes to government revenue and there will be a higher demand for government services. Currently there are five people of working age for every person aged 65 and over but by 2047 that will reduce to just 2.4

Transcript of SuperWHAT IS Activity 1 ears 7-10 SUPERANNUATION? · PDF fileSuperWHAT IS Activity 1...

Tax, Super+You.

Page 1

Take Control.

Super Activity 1

WHAT ISSUPERANNUATION?

Fact sheet

Years 7-10

The materials in Super have been designed to be used in

a variety of ways. Each topic is designed as a stand-alone

section to be explored by a whole class, small groups or

individual students

WHAT IS SUPER?Have you ever saved up to buy something? Maybe you are putting money aside at the moment to buy a car or something that is important to you. Superannuation, often called super, is money you set aside during your working life to provide an income to live on when you retire from work. Most people start to contribute to super when they begin work and keep contributing until they retire. The money is invested in one or more super funds of your choice.

You must leave your super in your fund until you either reach a minimum age or meet strict requirements set by the government. Your super is invested in assets such as bank accounts, property or shares, which earn an income. This income is reinvested in your super fund and then earns more income. This process, where you can generate earnings from previous earnings, is called compounding and greatly increases your final super payout.

The government encourages super savings by offering tax concessions that are not available with other forms of saving. In addition, no tax is charged for most people when they retire at 60 or older and take their super as a regular pension or a lump sum.

WHY IS SUPER IMPORTANT TO ME?Super is important for you because the more super you accumulate during your working life, the higher your standard of living will be in retirement. In general, most Australians would like to have a higher income in retirement than that offered by the government age pension. Over time, the age pension will provide a basic safety net for older Australians, which will be supplemented or even replaced by the income generated from superannuation.Demographic changes and greater life expectancy have increased the proportion of the Australian population in the retirement age group. Currently there are five people of working age for every person aged 65 and over but by 2047 that will reduce to just 2.4. The demand for government pensions and services will increase, and the number of people in the working age groups will fall. There will be significantly less people in the workforce contributing through taxes to government revenue and there will be a higher demand for government services.

Currently there are five people

of working age for every person aged 65 and over but by

2047 that will reduce to just 2.4

Tax, Super+You.

Page 2

Take Control.

HOW MUCH SUPER DO I NEED?Australians are living longer, so we will need more super savings to support ourselves for that longer period after retirement. Life expectancy in Australia is currently 84.5 years for women and 80.4 years for men. (Australian Bureau of Statistics, 3302.0.55.001 - Deaths, Australia, 2015). The Association of Superannuation Funds of Australia (ASFA) Retirement Standard benchmarks the annual budget needed by Australians to fund either a comfortable or modest standard of living in the post-work years. It is updated quarterly to reflect inflation and provides estimates of what singles and couples would need to spend to support their chosen lifestyle. This standard has been calculated for two income levels – a 'modest' basic lifestyle and a 'comfortable' lifestyle. The income required for these lifestyles as at December 2016 is shown in Table 1. Both budgets assume that the retirees own their own home outright and are relatively healthy.

Budgets for various households and living standards for those aged around 65(December quarter 2016, national)

Modest lifestyle Comfortable lifestyleSingle Couple Single Couple

Total per year $24,108 $34,687 $43,538 $59,808

Source: ASFA accessed at: www.superannuation.asn.au/resources/retirement-standard

Budgets for various households and living standards for those aged around 85(December quarter 2016, national)

Modest lifestyle Comfortable lifestyleSingle Couple Single Couple

Total per year $23,603 $34,992 $39,171 $54,960Source: ASFA accessed at: www.superannuation.asn.au/resources/retirement-standard

THE GROWTH OF SUPER IN AUSTRALIAThe system of saving through super has existed in Australia for a long time.

� Before 1970 super was generally limited to a minority of workers, such as higher paid white collar staff, public servants and members of the Defence Forces.

� From the 1970s super became more widely available as more industrial awards started to include superannuation clauses. � From 1986 the Conciliation and Arbitration Commission approved industrial agreements that provided for contributions of up to

3% of wages and salaries to be put into approved super funds. � By the early 1990s, 79% of employees had super coverage, including 68% of private sector employees.

I'm young. Why do I think of retirement

now?

� The government introduced the superannuation guarantee system in July 1992 to address issues with some employees having no super and some employers not complying fully with the legislation. This extended employee coverage and made it possible for employer contributions to be increased over time.

� By 2002–03 the contribution rate reached 9%. Despite the exceptions to the super guarantee scheme (see How super works for more details) recent years have seen widespread super contributions among the working population.

� On 1 July 2014 the super guarantee was increased to 9.5%.

The Australian Bankers' Association (ABA), the Financial Planning Association (FPA) and the Investment and Financial Services Association (IFSA) have produced a guide called Smarter Super – Invest in your future and make the most of your retirement (www.smartersuper.com.au/pdf-content.html), which provides information on investing for your future and retirement.

Tax, Super+You.

Page 3

Take Control.

YOU WILL: � interpret data to identify trends in relation to age and life

expectancy � predict future trends in relation to life expectancy � make a judgment on the impact of Australia’s demographic

profile on your own retirement � develop a persuasive speech

YOU WILL NEED: � Fact sheet: What is superannuation?

TASK 1SUPER IS SO WHYSuper Activity 1: What is superannuation?

Worksheet

Years 7-10

INTERPRET DATA TO IDENTIFY TRENDS1. Review Figure 1 and identify trends in relation to the proportion of the population of 65 years of age over time (including

projections into the future).

2. Review Figure 2 and identify trends in life expectancy in the last 30 years.

3. Based on these trends, predict the changes to life expectancy in the next 50 years.

4. Explain how you think Australia’s ageing population and longer life expectancy will affect your chances of receiving an age-pension when you retire. Use statistics and your predictions to justify your decision.

Tax, Super+You.

Page 4

Take Control.

Figure 1: Australia’s population 65 and over, at 30 June (over time)

Figure 2: Life expectancy at birth – 1985-2015

DEVELOP A PERSUASIVE TEXT5. In 1992, the Australia Government introduced a superannuation guarantee system to ensure that all working Australians had

savings for their retirement. You have been asked to develop a short speech to persuade an audience of young people entering the workforce about why this was an important initiative. When developing your speech, use information in the Fact Sheet and the data in Figure 1 and Figure 2. In developing your speech, consider what would happen to your generation at retirement if saving for retirement through the superannuation guarantee did not exist.

Tax, Super+You.

Page 5

Take Control.

Guidelines for your persuasive speechUse a Simple Structure – Have a clear beginning, middle and end to your speech and focus on key messages.

Know Your Audience – The most important aspect of creating a powerful speech is addressing who will be hearing it.

Use Creative, Visual Language – Use rhetorical questions (such as ‘Can you imagine a life with no money?) that will intrigue the audience. Use statistics to convince them. Choose words that give them the message you are conveying.

Tax, Super+You.

Page 6

Take Control.

YOU WILL: � make decisions on how you will budget if you have not

saved enough for a modest retirement � reflect on the consequences of not saving for retirement and

consider action that you might take to avoid these

YOU WILL NEED: � Fact sheet: What is superannuation?

TASK 2SUPER IS SO WHATSuper Activity 1: What is superannuation?

Worksheet

Years 7-10

Scenario You have reached the age of retirement and have had an interrupted working life, so there were times when no contributions were being made to your superannuation fund. Because of this, and the fact that you did not make any voluntary contributions to your superannuation, you have less saved for retirement than you would like. You are single and your superannuation will provide you with an annual income of $14,000 a year, considerably less than the ASFA predicts you need for a modest lifestyle. Imagine there is no age-pension.

You have less money than you need to live modestly in retirement. You will have to spend less money and make choices about what not to spend money on. What will you spend less money on? Will there be items you forgo completely? These are decisions you will have to make if you do not save enough for retirement through superannuation.

MAKE DECISIONS OR TRADE-OFFS1. Make decisions on what you will spend your money on in retirement by completing the blank column in Table 1. This table,

developed by ASFA, benchmarks the annual budget needed by Australians to fund either a comfortable or modest standard of living in the post-work years. You may have a zero entry against some items, or reduced expenditure against others. For example, you might have no travel expenses and use public transport instead of owning a motor vehicle. Remember you only have $14,000 a year to live off and a modest retirement requires at least $24,000.

Super is so what?

Tax, Super+You.

Page 7

Take Control.

Comfortable retirement Modest retirement Poor retirement

One annual holiday in Australia One or two short breaks in Australia near where you live each year

Regularly eat out at restaurants. Good range and quality of food

Infrequently eat out at restaurants that have cheap food. Cheaper and less food than a ‘comfortable’ lifestyle standard

Owning a reasonable car Owning an older, less reliable car

Afford bottled wine Afford cask wine

Good clothes Reasonable clothes

Afford regular haircuts at a good hairdresser

Afford regular haircuts only at a basic salon or pensioner special day

Take part in a range of regular leisure activities

Take part in one paid leisure activity infrequently. Some trips to the cinema

A range of electronic equipment Not much scope to run air conditioner

Replace kitchen and bathroom over 20 years

No budget for home improvements. Can do repairs, but can’t replace kitchen or bathroom

Private health insurance Use public health system

Table 1: Lifestyle choices based on retirement income

REFLECT2. Reflect on the consequences of not saving enough for retirement. Explain what action you might take to avoid these consequences.

Tax, Super+You.

Page 8

Take Control.

YOU WILL: � create short, powerful microblogs or ‘tweets’ promoting the

importance of superannuation

YOU WILL NEED: � Fact sheet: What is superannuation?

TASK 3SUPER IS SO TWEETSuper Activity 1: What is superannuation?

Worksheet

Years 7-10

TwitterTwitter is a very popular social tool. Through Twitter and 'tweeting' you can broadcast short burst messages, or microblogs to the world, with the hope that the messages are useful and interesting to someone.

The big appeal of Twitter is that is rapid and scan-friendly – you can track interesting tweeters and read their content at a glance. This is because every ‘tweet’ entry is limited to 280 characters or less.

The size of a ‘tweet’ means that the language you use has to be focused and clever so that they the message is powerful and easy to read.

Write short powerful microblogsWrite at least two tweets about why super is so important. Assume your tweets will be read by everybody.

Tax, Super+You.

Page 9

Take Control.

There are two types of contributions to super: � Concessional – which are contributed before tax. These

come from your employer and are not taxed before being contributed to super, but are taxed after the contribution is in your super fund at 15% .

� Non-concessional – which are contributed into super after being taxed. They are not subject to be taxed again when put into super. Types of after-tax contributions include:

� contributions an employer makes from an employee’s after-tax income

� contributions a spouse makes to a super fund � some personal contributions.

The ATO imposes significant penalties, to encourage employers to meet their obligations. If an employer doesn’t pay an employee's super on time and to the right fund, they may have to pay the superannuation guarantee charge. This is interest on the outstanding amount (currently 10%), an administration fee ($20 per employee, per quarter) as well as the outstanding amount of super.

Super Activity 2

WHERE DOES SUPER MONEY COME FROM?

Fact sheet

Years 7-10

When must super be paid?Employers must pay super guarantee contributions into a super fund at least every three months. They have 28 days after the end of each quarter to make the payment. Previously, this payment was made annually. The quarterly payment requirement has been designed to ensure contributions are invested as soon as possible and to give employees earlier opportunity to check their employer is making the correct contributions for them.

How can you ensure financial wellbeing when you retire? Discover

the various ways your super can grow.

THE SUPER GUARANTEESuperannuation can grow through funds that come from:

� an employer � government super contributions � voluntary contribution � salary sacrifice.

EmployersCurrently Australian employers must by law contribute 9.5% of an eligible employee's ordinary time earnings into a super fund. This contribution is called the superannuation guarantee.

Ordinary time earnings are what you generally earn for ordinary hours of work, including over-award payments, bonuses, allowances and some paid leave. Overtime is not included. For example, if your ordinary time earnings are $15,000 per quarter (three-monthly), your employer must pay $1,425 into your super fund. This amount must come directly from your employer, not from your gross salary.

Who is eligible for a super guarantee contribution?Your employer must make super guarantee payments on your behalf unless:

� you are under 18 years old and do 30 hours or less of work per week for the employer

� you are paid less than $450 (before tax) in a calendar month from the employer

� the work is of a domestic or private nature, for example as a part-time babysitter or nanny, and is 30 hours or less per week.

Even if you are employed on a casual or part-time basis, you may still be eligible for super guarantee contributions by your employer.

Self-employed people Super is not compulsory for self-employed people, although many do make contributions.

To learn more about adding to your super, go to www.ato.gov.au and search for 'personal super contributions'

There is an annual cap on concessional and non-concessional contributions. If you contribute beyond the cap, the excess will be added back to your tax return and taxed at your marginal tax rates. These caps may change from time to time so it is important to keep aware of the rules and manage your contributions wisely.

Tax, Super+You.

Page 10

Take Control.

EXTRA CONTRIBUTIONS TO SUPERIf you want to retire comfortably, your employer's 9.5% super guarantee contributions may not be enough to build the lifestyle you want for retirement. By making extra contributions, you will boost the amount of super you have when you stop working. The key is to start as soon as possible so you can relax later.

Many Australians save more in super than the required amount in the following ways:

� Some employers choose to contribute more than 9.5% for their employees as a form of added benefit.

� Employees may choose to personally contribute extra money into super from their after-tax income or pay.

� Employees may salary sacrifice super contributions. � Some people are eligible for the Australian Government

super contribution.

Personal super contributionsEmployees can boost their super by adding their own contributions to their super fund or into their spouse’s super fund. Personal super contributions are the amounts contributed to their super fund from after-tax income (that is, from their take-home pay), so it is not taxed again unless they exceed the cap.

If a person is not working and under 65, he or she can also make personal after-tax contributions to their super fund.

Salary sacrificeSalary sacrifice is an arrangement between an employee and their employer to forego part of their salary or wages in return for

the employer providing benefits of a similar value. One example of a salary sacrifice arrangement is to have some of the salary or wages paid into an employee’s super fund instead of to the employee.

When super contributions are made through a salary sacrifice agreement, these contributions are taxed in the super fund at a maximum rate of 15%. Generally, this tax rate is less than the marginal tax rate and the sacrificed part of the total salary package is not counted as assessable income for tax purposes.

The Australian government super contributionsA co-contribution from the Australian government is designed to help eligible people boost their retirement savings.

If you are a low or middle-income earner and you make a personal (after-tax) contribution to your super fund, the government also makes a contribution (called a super co-contribution) up to a maximum amount of $500. The amount of government super co-contribution you receive depends on your income and how much you contribute.

The ATO will work out if you are eligible for a super co-contribution when you lodge your tax return. If the super fund has your tax file number (TFN), the ATO will pay the government co-contribution to your super account automatically.

Some low or middle income earners might also be eligible for the low income super income tax offset (LISTO). When an employer makes a super guarantee contribution to an employee’s super account, the Australian government may make a LISTO payment which equals 15% of the contributions.

RETIREMENT AND SUPERGenerally, you will not be able to access your super until you reach your earliest retirement age, which is called your 'preservation age'. The preservation age is 60 for anyone born after 30 June 1964.There are only a few other circumstances in which a person may be able to access their super before retirement. These include severe financial hardship, compassionate grounds, a terminal medical condition, and permanent incapacity.

Once you become eligible to access your super, you have three options: � take it all as a lump sum � invest it in a superannuation pension or annuity that provides you with a regular income stream � do a combination of both depending on the rules of the fund.

Given that many people live 20 to 30 years in retirement, it is important that your super lasts as long as possible.

The MoneySmart website

also provides helpful advice about growing your super for a comfortable

retirement. Go to www.moneysmart.gov.au

and search 'super contributions'

Tax, Super+You.

Page 11

Take Control.

TASK 1 MY EMPLOYER, ME AND SUPER CONTRIBUTIONS Super Activity 2: Where does my super money come from?

Worksheet

Years 7-10

YOU WILL: � interpret information and make calculations to answer super

contribution questions

YOU WILL NEED: � Fact sheet: Where does my super money come from? � Answer sheet: Task 1 — My employer, me and super

contributions

INTERPRET SCENARIOFrankie and Sarah want to know more about their superannuation. They know that their employer, BeachCrazi, should make a super guarantee contribution on their behalf. Read the three scenarios below and provide answers for their questions.

Scenario 1: FrankieFrankie, aged 25, is employed part-time (33 hours per week) in the office as an administration assistant grade 1. He is responsible for sending out invoices and preparing sales records. His pay is $825 per week before tax. Frankie also gets a weekly allowance of $15 because he has been trained to use certain programs.

Answer Frankie’s questions

1. Does the company need to contribute to my super?

2. Why do you think this?

3. If the company must pay my super, how much super should BeachCrazi contribute over three months (13 weeks). Show me your calculations.

Tax, Super+You.

Page 12

Take Control.

Scenario 2: SarahSarah, aged 30, is employed fulltime as a salesperson for BeachCrazi on a gross salary of $1,550 a week. She visits surf shops selling the company products. Since she began working for the company seven months ago, she has sold $200,000 worth of goods. The company gave her a bonus after six months for her hard work, which equalled 5% of her sales. After seven months, Sarah checked her super account and noticed there had been no deposits made in that time.

Answer Sarah’s questions:

4. Does the company need to put money to my super?

5. Explain why you think this?

6. If the company must pay my super, how much super should have been contributed by BeachCrazi after my first three months (13 weeks) employment. Show me your calculations.

7. What do you think I should do about the missing super contributions?

Scenario 3: BeachCraziThe ATO investigated Sarah’s claim that BeachCrazi failed to pay her super. The ATO found that no super guarantee contributions were made after her first three months in the job plus 28 days, nor since. BeachCrazi admitted there was an administrative error when Sarah commenced her job. The ATO ordered BeachCrazi to pay all outstanding super guarantee contributions, plus interest and a penalty. Beachcrazi paid the outstanding fees nine months (39 weeks) after Sarah began employment with them.

Answer BeachCrazi’s question:

8. How much money should our company deposit into Sarah’s account in her ninth month (39th week) of employment? How much money should our company pay to the ATO in penalties and interest? Show me your calculations.

Tax, Super+You.

Page 14

Take Control.

Super Activity 3

WHAT DO I NEED TO DO ABOUT SUPER?

Fact sheet

Years 7-10

Find out how you can actively manage your super to ensure a comfortable

retirement. You can keep track of your super, access the government’s co-contribution

and access information to make decisions throughout your life to retirement.

GETTING STARTEDCheck that you are eligible for super by going to the ATO or MoneySmart websites.

Refer to these websites to assist you: www.ato.gov.au www.moneysmart.gov.au

Check what super fund your super contributions will be paid into.

In many jobs, your employer is required by law to allow you to choose either the employer's nominated fund or your own preferred super fund. They must give you a standard choice form to choose your fund. This form is also available from the ATO website at www.ato.gov.au.

Choose a complying fund that is best for you.

You will usually be able to choose where you want your employer to pay your super. If you have the choice, it is important to choose a fund that is best for your situation. Make sure your super fund is a complying fund, one which complies with certain rules set by the government.

Read the product disclosure statement (PDS) issued by a super fund to all new members.

The product disclosure statement lists all the features and benefits of the fund, and the fees and costs they charge.

Some other factors that might influence your decision are considered in Activity 3: How do I choose a super fund?

Make sure you include your tax file number (TFN) on your standard choice form.

When you start work, your employer will give you a tax file number declaration form to complete. Your employer will use the completed form to pass on your TFN to the super fund they pay your super into. It isn't compulsory for you to provide your TFN to your fund, but if you don't provide it:

� your fund is liable to pay extra income tax on contributions your employer makes for you (including salary sacrificed contributions) and may take this extra money out of your super account

� your fund must not accept any member contributions and you will miss out on super co-contributions even if you're otherwise eligible.

You can check if your super fund has your TFN by looking at the statements they send you. If your statements show that your TFN is not held by your fund, you should contact them. The super fund needs to know this so that your super account receives the correct tax treatment and other benefits. This also makes it easier to keep track of your super over your lifetime.

Check if you are receiving the correct amount of super from your employer.

Use the employer contributions calculator on the MoneySmart website or the ATO’s employee superannuation guarantee (SG) calculator tool on the ATO website as a guide.

If you think your employer isn’t paying the correct super guarantee contributions, you can follow the steps below:

1. Check you are entitled to super guarantee before taking any further steps.

2. Use the Estimate my super tool on the ATO website to see how much super guarantee your employer should be paying. Print the report if the calculator shows you have not received the right amount of super into your fund. Go to www.ato.gov.au and search for 'estimate my super'.

3. Confirm how much super guarantee you have received by checking super fund statements, contacting your super fund, or checking your myGov account.

4. Show the report to your employer.5. If the matter is not resolved, you can lodge an enquiry

with the ATO.

þ

Tax, Super+You.

Page 15

Take Control.

Check your super statements regularly.

You should also check the statements from your super fund regularly to be sure your employer is paying the correct amount into the right fund. Try to resolve any errors with your employer or the ATO as soon as possible; the longer these issues are left hanging, the greater the risk of an unfavourable outcome for you. Make sure your super fund has your current address so they can keep in touch with you.

Investigate the benefits of the Australian government co-contribution scheme.

When an eligible person makes extra (after-tax) super payments, the Australian government can make a 'co-contribution' in their super fund or retirement savings account. The amount of the government co-contribution, up to a maximum of $500, depends on the amount they contribute and their income.

This scheme relies on information contained in your tax return and on information provided by your super fund. Find more information about the super co-contribution scheme from the ATO website or the MoneySmart website.

Combine (consolidate) different super accounts.

Over your lifetime, you will probably work in a number of jobs, including casual and part-time jobs. If super has been paid into your various employer-nominated funds, you could end up with super in a number of accounts in various super funds. It is usually better if these amounts are combined into one, so you pay only one set of fees and costs. This means you can keep track of your super more easily and help maximise how much money you will have to live on when you retire.

Before combining super funds, find out if a fund will charge you to close your account with them and whether you'll lose any other benefits. Your fund may also insure you against death, illness or an accident. If you choose to leave your current fund you may lose any insurance entitlements you may have: this is especially important if you have a pre-existing medical condition. Make sure you get an appropriate level of insurance in your chosen fund. You may also consider which fund or account is suitable from a risk/rate of return point of view. To maximise your investment and understand the risks it may be worthwhile seeking appropriate independent professional advice.

For more information on choosing a fund go to moneysmart.gov.au and search "choosing a super fund".

Find lost and unclaimed super.

Generally super can become 'lost' if you change your job, address or name and forget to tell your super fund. The ATO has a lost member register of people who have been reported by their super funds as lost. Usually, the super fund that reports you as a lost member continues to hold onto the money.

To protect your lost super from fees, super funds may be required to transfer your money to the ATO. This is known as unclaimed super and is held by the ATO for you to claim at any time.

A myGov account allows individuals to view all their super accounts including ‘Lost’ and ‘Unclaimed’ super and consolidate by transferring their super to an existing fund account or making a direct claim for payment (where eligible).

Monitor your super account.

The level of fees charged and the rate of return on your funds can make a very big difference to the amount built up in your super fund when you retire.

Plan retirement.

Deciding when and how to take your superannuation is a complex decision, as there are many tax and welfare implications. You can seek advice from someone who can help, such as a financial advisor or other qualified professional.

Set up a myGov account.

Use your myGov account to:

� see a list of all your super accounts and request a transfer of your super from one account to another

� look for lost or ATO-held super as well as view all your super accounts

� request a transfer of any lost or ATO-held super into your preferred super account.

Find out more on the ATO website at: www.ato.gov.au by searching 'how to create a myGov account'.

If you change jobs,

consider keeping the

same superannuation

account.

Tax, Super+You.

Page 16

Take Control.

TASK 1 THE GOVERNMENT SUPER CO-CONTRIBUTION Super Activity 3: What do I need to do about super?

Worksheet

Years 7-10

YOU WILL: � interpret information about super � identify the costs and benefits of personal super

contributions � calculate compound interest � describe the mutual roles of government and individuals in

growing super

YOU WILL NEED: � Fact sheet: What do I need to do about super? � Answer sheet: Task 1 –The government super co-contribution � MoneySmart compound interest calculator:

go to moneysmart.gov.au and search 'compound interest calculator'.

Find out about the government super co-contribution scheme, its positives and negatives, and who is eligible.

Income thresholdsThere are two co-contribution income thresholds:

� a lower threshold ($36,021 for 2016–17) � a higher threshold ($51,021 for 2016–17).

If you earn $36,021 or less (for the 2016/2017 year), the federal government pays $0.50 (50 cents) for every dollar you contribute to your super fund in after-tax dollars, up to a maximum of $500 a year.

For example, if you make a $1000 non-concessional contribution and your income is less than $36,021 (for the 2016/2017 year), then your super fund account receives a $500 tax-free contribution from the Government. If you make a $600 contribution, the Government pays $300 into your super fund.

If your total income is between the two thresholds, your maximum entitlement will reduce progressively as your income rises. You will not receive any co-contribution if your income is equal to or greater than the higher threshold.

APPLY YOUR KNOWLEDGEUse your knowledge about the government super co-contribution scheme to work out the advantages and disadvantages for Susie, Alim and the government.

Tax, Super+You.

Page 17

Take Control.

SusieWhen Susie was 16, she worked regularly at her part-time job in a hardware store. Susie's father was keen for her to develop the habit of saving. He suggested that Susie put $10 each week from her wage into a super fund. Her father promised that if Susie saved regularly from 1 July so that she had $500 by mid-June the next year, her parents would give her $500 to contribute to her account, bringing the total to $1,000.

Susie considered whether this was worthwhile. Susie’s father explained that if she had $1,000 in the account by the end of the tax year, the government would deposit a further $500 into her account.

Susie decided to give it a go. She saved $500 each financial year and her parents matched her savings. Each year she was able to obtain the maximum government super co-contribution amount. When Susie left school and took up a three-year apprenticeship with a wage of $32,000 to $35,000 each year, she decided to make the effort to keep adding to her super. In fact, Susie expects to have accumulated a lot of super savings (from herself, her parents and the government) within five years. By that time, Susie will decide whether she wants to continue this saving. If she doesn't, she will be able to leave her savings in the account to grow at compound interest until she retires.

1. Over five years, while working part-time then earning apprentice wages, how much super co-contribution will Susie have gained from the government if her personal contributions are over $1,000 a year?

2. Use the compound interest calculator on the MoneySmart website (www.moneysmart.gov.au) to calculate how much the $1500 a year super contribution will be worth in 5 years. To do this, assume the $1500 is paid annually, interest is calculated annually and the interest rate is 8%. (note that the answer to this question and question 3 ignore the fees charged by super funds. The reality is that the money accumulated would reduce substantially over time unless more contributions are made to the fund).

3. What difference would a contribution of $1500 a year to super make over: a. 20 years ________________ b. 30 years ________________ c. 40 years? _______________

4. What would inhibit Susie from gaining all or part of the government super co-contribution?

Complete a cost benefit analysis5. Susie is young and her income is low. What are the costs and benefits of Susie adding personal contributions to her super over

the next 5 years? Use evidence (facts and calculations) to justify your analysis.

Costs of personal contributions Benefits of personal contributions

6. Conclusion: Is maximising the government super co-contribution an effective financial strategy for for Susie? Justify your conclusion.

Tax, Super+You.

Page 18

Take Control.

AlimAlim, aged 18, is studying to be a doctor at university. He lives at home with his mother, who earns a modest salary but believes that super is important. She is encouraging Alim to study hard and minimise working hours, so that he can graduate without delay and earn a good income. Therefore, he is working casually for only 10 hours per week at the university’s IT department, repairing and maintaining laptops.

Alim has worked for 10 months at the university, earning $2,400 in the last three months, and he expects to continue earning the same. Alim’s mother has advised him to make voluntary contributions to super. Alim feels that he can just afford to add $15 a week as a personal contribution to super. It’s not a lot but he and his mother have seen the power of compound interest in his mother’s super account over time.

7. How much government super co-contribution will Alim receive after one year of employment?

8. Assuming no interest was paid, what was the balance of Alim’s super account after one year of employment?

9. Calculate how much Alim’s small super amount ($1170) will grow over 30 years. The super fund pays interest on Alim’s balance monthly. His fund earns 8% per year. Instructions on how to calculate compound interest is shown in the Instruction Sheet: How to calculate compound interest. (note that the answer to this question ignores the fees charged by super funds. The reality is that the money accumulated would reduce substantially over time unless more contributions are made to the fund).

10. If Alim increased his super contribution by $5 a week, how much government super co-contribution would Alim receive after one year of employment?

11. Assuming no interest was paid, what would be the balance of Alim’s super account after one year of employment?

12. Assuming Alim pays no further superannuation into this super fund, calculate how much his super balance of $1,540 will grow over 30 years. The super fund pays interest on Alim’s balance monthly. His fund earns 8% per year. Instructions on how to calculate compound interest is shown in the Instruction Sheet: How to calculate compound interest. (note that the answer to this question ignores the fees charged by super funds. The reality is that the money accumulated would reduce substantially over time unless more contributions are made to the fund).

13. Conclusion: Is maximising the super co-contribution an effective financial strategy for Alim? Justify your conclusion.

Tax, Super+You.

Page 19

Take Control.

INSTRUCTION SHEET: HOW TO CALCULATE COMPOUND INTERESTThe formula for calculating compound interest is A = P x (1 + r)t

'A' is the accrued amount – that is the end amount of your investment

'P' is the principal, i.e. the starting amount

'r' is the percentage interest rate converted to a decimal rate (e.g. 2% is 0.02 or 2/100)

't' is the number of time periods (for example, 5 years or 60 months) – NOTE THAT THIS IS EXPRESSED AS A POWER

Using a scientific calculator to calculate to the powerEnter the base of the expression you want to calculate. For example, if you wanted to compute 1.0067 raised to the power of 24, you would enter "1.0067."

Press the exponent key on the calculator, usually "^" or "y^x" or “xy” depending on your calculator. The function for a calculator on a smart phone is highlighted in Figure 1.

Enter the power in your expression. Continuing the example, to compute 1.0067 raised to the power of 24, you would enter "24."

To recap:

1. Enter the number you want to calculate to the power (1.0067).

2. Press the exponent key on the calculator (highlighted in Figure 1 below)

3. Enter the power in your expression (24).4. You may have to press equal to reveal your answer.

Using Excel to calculate to the powerThe formula in Excel is:

=POWER(x,y)

Where x = the number you want to calculate to the power Where y = the power in your expression

When you have entered your data, press enter to reveal the answer.

Example 1 - Annual compoundingWork out what $2,000 will grow to over 2 years for an investment or savings that grows at 8% per annum compounding annually.

Imagine that the interest is paid annually (in reality the interest compounds monthly).

A = $2000 (P) x (1+0.08)2

A = $2,000 x (1.08)2

A = $2,000 x 1.1664

A = $2,333

Example 2 - Monthly compoundingWork out what $5,000 will grow to over 2 years for an investment or savings that grow at 8% per annum compounding monthly.

First you need to divide the annual interest rate by 12, which is 0.08/12 = .0067

Second you need to calculate the number of time periods (‘t’) in months, which is 24.

A = $5,000 x (1+.0067)

A = $5,000 x (1.0067)24

A = $5,000 x 1.1738

A = $5,869

Tax, Super+You.

Page 20

Take Control.

MAKE THE CONNECTION

14. Why do you think the government chooses to contribute money to an individuals’ super?

15. Write a paragraph that links the role of both the ATO and an individual in growing the individual’s super. Use the word “mutual”.

Tax, Super+You.

Page 23

Take Control.

TASK 2 CONSOLIDATING YOUR FUNDS Super Activity 3: What do I need to do about super?

Worksheet

Years 7-10

YOU WILL: � consider the impact on super growth when funds are

consolidated � represent data to model scenarios for analysis and

evaluation � develop advice for young people about super

YOU WILL NEED: � Fact sheet: What do I need to do about super?

WHAT HAPPENS WHEN YOU HAVE SUPER IN A NUMBER OF FUNDS? COMPARE

HOW MULTIPLE FUNDS CAN AFFECT YOUR EARNINGS.

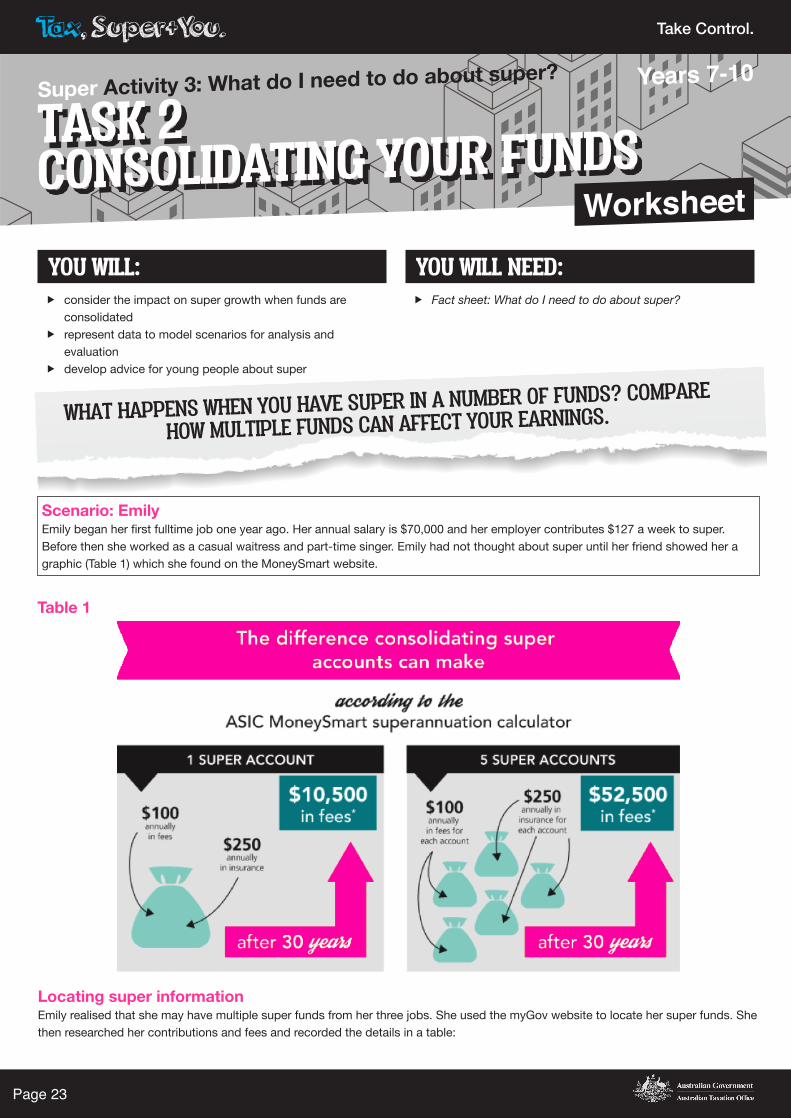

Scenario: EmilyEmily began her first fulltime job one year ago. Her annual salary is $70,000 and her employer contributes $127 a week to super. Before then she worked as a casual waitress and part-time singer. Emily had not thought about super until her friend showed her a graphic (Table 1) which she found on the MoneySmart website.

Locating super informationEmily realised that she may have multiple super funds from her three jobs. She used the myGov website to locate her super funds. She then researched her contributions and fees and recorded the details in a table:

Table 1

Tax, Super+You.

Page 24

Take Control.

Emily’s super accounts

Current balancePerformance per

month (based on past 3 Year Return*)

Annual admin fees and other charges

Insurance

Nova Super $14,000 6.35% 2% $320

CFI Super $5,275 8.9% 1% $260

First Class $6,650 5.8% 1.3% $175

* Note: past performance is not a reliable indicator of future performance

REPRESENT DATA FOR ANALYSIS1. Create a model, digital or non-digital, to show how much super Emily will have at the end of one year if:

� she keeps her super in the different funds � if she consolidates into Nova � if she consolidates into one of the other funds.

EVALUATE INFORMATION TO MAKE DECISIONS2. Emily has to decide what she will do with her three super accounts. Based on your models, recommend what Emily should do

and explain why.

Create advice3. What advice about super would you offer young people who

are in the early stage of their working life?

4. Write some simple tips. Then elaborate with information they can consider to ensure they have super and that it grows well. Things to consider when making super decisions:

Tax, Super+You.

Page 25

Take Control.

Super Activity 4

HOW DO I CHOOSE A SUPER FUND?

Fact sheet

Years 7-10

Explore what factors affect super decisions and

calculate how much money you might need to accumulate in order to retire.

DECIDING ON A SUPER FUNDChoosing a super fund and choosing an investment strategy can be very important financial decisions. There are three broad factors you should consider:

� what type of fund to choose � the benefits/fees and costs of a fund � what investment strategy you should apply to your money.

WHAT TYPES OF SUPER FUNDS ARE AVAILABLE?There are five common types of funds.

Type of super fund

Features

Industry funds These funds are open to people working in a particular industry or under a particular industrial

award. Some industry funds allow anyone to join. Their features may be particularly suited to

workers in that industry.

Retail funds These funds are operated by financial institutions and are open to everyone. They allow a large

number of people and companies to operate their super arrangements as a single group.

Corporate funds These are generally open to people who work for a particular company or employer and are

usually tailored to meet the requirements of the particular company and its employees.

Self-managed super funds (SMSFs)

These are also known as do-it-yourself or DIY funds and are used by people who want to

create and operate their own super fund. It must have less than five members who are solely

responsible for the management and operation of the fund within a strict legal and regulatory

framework. They are generally unsuitable for people with small amounts of money.

Public sector funds These funds are provided by the government for public sector employees.

Each type of fund can have features that one person might see as a strength and another see as a weakness. For example,

a SMSF to one person might offer greater investment flexibility, but to another, it means too much responsibility and risk. You

need to consider which features are important to you when making your choice of fund.

Tax, Super+You.

Page 26

Take Control.

Investment mix Typical characteristics

Below are typical characteristics of different types of investment options within super.TYPES OF INVESTMENT OPTIONSSuper funds invest your money to grow your nest egg over your working life. Your super fund will invest your super in different types of assets, such as cash, bonds, Australian shares, property and international shares. Most super funds will package these assets into different investment options which have varying degrees of risk. Usually, super funds let members choose their investment options.

Below are typical characteristics of different types of investment options within super.

Source: Super investment options, MoneySmart

www.moneysmart.gov.au/superannuation-and-retirement/how-super-works/super-investment-options

Reproduced with permission of ASIC.

Tax, Super+You.

Page 27

Take Control.

WHAT TO CONSIDER WHEN CHOOSING A FUND1. Fees and costs

All super funds charge fees. Every dollar paid in fees will reduce the amount in your super account. Super funds must show all significant fees in a table in the fund's product disclosure statement (PDS). These fees can make a large difference to the amount you accumulate over your working life, and hence the income you will have in retirement. Industry and corporate funds may be set up on a not-for-profit basis and they can charge lower fees. However, you should compare the costs with the returns — If a fund makes a higher return, it may be worthwhile to pay its higher charges.

2. Additional features Some funds will provide access to personal loans or the services of a financial advisor because they can obtain a group discount for members. Some funds allow you to open and make contributions to a spouse account. You need to decide whether these services are important to you.

3. Insurance cover Many super funds provide life and disability cover to their members. Super funds typically have three types of insurance for members:

� Death cover (also known as life insurance) - pays a benefit to your beneficiaries when you die, either as a lump sum or as an income stream

� Total and permanent disability (TPD) cover - pays you a benefit if you become seriously disabled and are unlikely to ever work again

� Income protection (IP) cover - pays you an income stream for a specified period if you can't work due to temporary disability or illness

You can usually increase, decrease, or cancel your default insurance cover. The insurance premium is paid through your super fund and the premiums are deducted from your super account balance.

4. Extra contributions Sometimes an employer offers to pay more than 9.5%, for example, when an employee joins the default fund. This might be worthwhile, but you should find out about the details of the fund first. For example, does the fund allow you to take advantage of the government's super contribution scheme?

5. Investment options and performance You can make your own decisions about how your super is invested.

Check the investment options available in your super fund. If you want the flexibility to change or concentrate on particular asset types, you need to check what the fund offers. Find out the returns the fund has earned for members over the last five or more years. Don't make a decision based on the performance of one year — you need to consider a longer period of time to get a better picture of how effectively the fund is performing.

MoneySmart provides advice on how to judge a super fund’s performance. Go to: www.moneysmart.gov.au and search 'judging a super fund'.

6. Regulation Check the super provider is licensed and complies with super rules and regulations. If the fund is complying, your money will get tax concessions. Individual funds must be able to provide evidence of whether they are complying. For more information about the super fund, check the Super Fund Lookup services at: www.superfundlookup.gov.au

SELECTING A SUPER STRATEGYMost super funds offer you a choice about which assets to invest your super in. When making this choice, super members should consider a strategy to manage their super and its performance, by considering available asset options and performance, risks, returns and their personal risk profile.

Remember, how a fund performs in one year is no guarantee of future

return.

Tax, Super+You.

Page 28

Take Control.

Risk and returnSome assets, such as cash investments or fixed interest deposits, offer the potential for lower returns over time but provide less risk of the asset going down in value (known as a capital loss). Other assets such as shares are the opposite in that they offer greater potential returns but also a much higher chance of capital loss. The relationship between risk and return is often seen as positive – greater returns come with higher risk, while low returns mean lower risks.

You can use the compound interest calculator on the MoneySmart website as a guide to the expected rate of return. Go to: www.moneysmart.gov.au and search 'compound interest calculator'.

Differing rates of return on a final super payout

Rate of return over 45 years, reinvesting fund Start Finish

6% $10,000 $137,646

8% $10,000 $319,204

Difference over 45 years* $181,558

*Source: Compound interest calculator, MoneySmart, Reproduced with permission of ASIC.

Know your risk profileGenerally, the higher the risk you take with your investments, the greater the return you would expect. Not everyone is comfortable with taking such risks, and they will choose a lower return, but with less risk. The diagram illustrates this relationship.

Relationship between returns and risksIt is important for you to work out your risk profile. You need to know how you feel about risk to be able to select an investment option that meets your needs.

Someone who has a long time to invest will often accept higher risk. As you approach retirement age, you are closer to withdrawing your super and you want to be sure about the amount of super you will have. Your risk tolerance may fall sharply. Remember, at retirement your super may need to last another 20 to 30 years.

Do you feel

comfortable when you risk potential loss in order to hopefully gain

higher returns? INVESTING IN YOUR FUTURE

Compound interest and your investment options will determine your future. The magic of

compound interest means your super account

will grow while you work as your employer continues to pay a contribution into your account. The more money you contribute early

on, the more money you will have when you

retire. Also you can consider the investment

options offered to you by your fund. Your choice

of investment can have an impact on how much

money you have down the track.

Tax, Super+You.

Page 29

Take Control.

TASK 1 MAKING A DIFFERENCE TO MY SUPERSuper Activity 4: How do I choose a super fund?

Worksheet

Years 7-10

YOU WILL: � interpret data to develop conclusions about how different

actions impact on super � draw conclusions about factors that affect super fees � draft a plan for a text designed to inform youth about

actions they could take to improve their retirement

YOU WILL NEED: � Fact sheet: How do I choose a super fund?

There are many decisions you can make that will impact the amount of superannuation you have for retirement. These include:

� making contributions sooner � earning a higher income � delaying retirement � making payments to your superannuation through salary sacrificing (before tax) � the fees charged by your super fund � the investment performance of your super fund.

The superannuation estimates and fees in Tables 1-6 were calculated using the MoneySmart Superannuation calculator (www.moneysmart.gov.au ). Tables 1-4 assume an 8% annual investment return and a 1% contribution fee.

INTERPRET DATA TO DEVELOP CONCLUSIONSIn this task, you will interpret projected superannuation amounts at retirement based on these decisions.

Table 1: The effect of making super contributions earlierJane Miguel Sunil

Age now 20 25 35

Age at retirement 67 67 67

Super accumulated now $5,000 $5,000 $5,000

Annual salary $50,000 $50,000 $50,000

Fees paid $23,871 $18,248 $10,300

Estimated super (after fees) $893,289 $683,366 $386,651

1. Conclude: What conclusions can you make about starting super at a young age? Use statistics to justify your conclusion.

Tax, Super+You.

Page 30

Take Control.

Table 2: The effect of earning a higher incomeKwong Pearl Ali

Age now 23 23 23

Age at retirement 67 67 67

Super accumulated now $5,000 $5,000 $5,000

Annual salary $40,000 $60,000 $80,000

Fees paid $18,876 $21,701 $24,618

Estimated super (after fees) $614,774 $903,906 $1,195,815

2. Conclude: What conclusions can you make about the effect of earning a higher income? Use statistics to justify your conclusion.

Table 3: The effect of delaying retirementTim Thomas Tanya

Age now 23 23 23

Age at retirement 67 69 72

Super accumulated now $5,000 $5,000 $5,000

Annual salary $50,000 $50,000 $50,000

Fees paid $20,339 $22,638 $26,519

Estimated super (after fees) $761,442 $847,250 $992,151

3. Conclude: What conclusions can you make about the effect of delaying retirement on superannuation? Use statistics to justify your conclusion.

Table 4: The effect of making additional payments above your employer's 9.5% contributionRosa Will Vince

Age now 23 23 23

Age at retirement 67 67 67

Super accumulated now $5,000 $5,000 $5,000

Annual salary $50,000 $50,000 $50,000

Make voluntary contribution (before tax salary sacrifice $ amount per month)

$60 $120 $180

Fees paid $21,166 $22,091 $23,015

Estimated super (after fees) $854,625 $947,285 $1,039,945

Tax, Super+You.

Page 31

Take Control.

4. Conclude: What conclusions can you make about the effect of earning a higher income? Use statistics to justify your conclusion.

Table 5: The difference fees can makeFund A Fund B Fund C

Age now 23 23 23

Age at retirement 67 67 67

Super accumulated now $5,000 $5,000 $5,000

Annual salary $50,000 $50,000 $50,000

Contribution fee 1% 2% 3%

Fees paid $20,339 $27,655 $34,971

Estimated super (after fees) $761,442 $754,126 $746,810

5. Conclude: What conclusions can you make about the difference fees can make? Use statistics to justify your conclusion.

Table 6: The difference super fund performance can make

Fund A Fund B Fund C

Age now 23 23 23

Age at retirement 67 67 67

Super accumulated now $5,000 $5,000 $5,000

Annual salary $50,000 $50,000 $50,000

Contribution fee 1% 1% 1%

Fees paid $15,569 $20,339 $26,812

Average annual performance 7% 8% 9%

Estimated super (after fees) $580,557 $761,442 $1,008,074

Tax, Super+You.

Page 32

Take Control.

The statistics on the previous page show how the performance of 3 different super funds affects estimated super at retirement. When selecting a super fund, it is important that you compare the performance of each fund over at least 5 years and consider the charges applied to the fund.

6. Conclude: What conclusions can you make about the difference super fund performance can make? Use statistics to justify your conclusion.

7. Look at the fees that different individuals paid on their superannuation in Tables 1-4 and Table 6. A contribution fee of 1% was charged on each superannuation account. What conclusions can you make about the impact that the following has on the fees charged:

a. the time the super fund has been in place b. the value of the super fund.

Use evidence from the tables to justify your conclusions.

CREATE AN INFORMATION TEXT OR INFOGRAPHIC8. Use the conclusions you have made from your interpretation of the data above to plan a flyer or infographic promoting the action

young people could take to maximise their super.

Tax, Super+You.

Page 33

Take Control.

DRAFT IDEAS

Tax, Super+You.

Page 34

Take Control.

TASK 2 DECIDING ON A SUPER INVESTMENT STRATEGYSuper Activity 4: How do I choose a super fund?

Worksheet

Years 7-10

YOU WILL: � identify the criteria that influence superannuation investment

decisions � identify the financial risks and rewards of different

superannuation investment asset options � conduct a cost-benefit analysis of superannuation

investment strategies � design and justify a course of action to achieve given

retirement goals

YOU WILL NEED: � Fact sheet: How do I choose a super fund?

In this task, you are to conduct a cost-benefit analysis of different superannuation investment options to propose a course of action for two hypothetical clients. You will then identify financial risks and rewards of different superannuation investment options, and match these to your hypothetical clients’ circumstances. You will then create and justify advice about a course of action for each client to achieve their retirement goal.

Advice should acknowledge the client’s:

� retirement goals � stage in life � risk profile � available funds � investment options.

ScenarioYou are a qualified financial advisor for a reputable financial planning company. You have two clients, with unique circumstances, each seeking superannuation advice. Having gathered information about their risk profiles and goals, your task is to analyse each client’s circumstances and propose a course of action for superannuation investment over the short, medium and long-term, to assist them to meet their retirement goals.

DECIDE A COURSE OF ACTION

Client AClient A is a 24 year-old nurse, early in her working career. She has been earning about $70,000 a year but expects her salary will increase with experience. She also has overtime opportunities and thinks her salary could reach $95,000 next year. She is not a risk-taker although she wants to make the most of her superannuation.

She believes she has a long-term career in nursing and is interested in soon working overseas for some years. Later, she hopes to have a family. She assumes she will not be eligible for a government pension when she retires. However, by retirement, she would like a comfortable life that includes overseas travel.

Her employer pays her super to an industry fund. The fund is known to consistently perform well, although the fees and charges can be high. The fund packages its investment asset types (cash, fixed interest securities and shares) into four options — growth, balanced, ethical and conservative.

Client BClient B is a plumber, aged 60, who is currently earning $85,000 a year. He is planning to retire at 65. He has been contributing to super since he began work. He currently has enough for a very modest retirement.

By nature, he enjoys action sports such as skiing and skydiving. But he hopes to enjoy a quiet retirement life with his partner who has very little super due to mostly unpaid work in the home. They hope for a modest to comfortable lifestyle in retirement.

While he has had no breaks in his career, he has not volunteered extra payments. He has worked for four employers in his career and his super is in three different super funds, two of which are industry funds and one being a retail fund. The industry funds charge few fees but they are high and the retail fund charges many types of fees, which are not too high. One of the industry funds is performing better than the other two funds. The fund packages its investment asset types into three options — high growth, balanced and conservative.

Identify the objective

Tax, Super+You.

Page 35

Take Control.

Your process will involve:

1. creating a client profile2. deciding a super investment strategy using a cost-benefit analysis3. proposing a course of action to inform an investment strategy4. writing an evaluation of your course of action proposal.

Create a client profile1. Create a profile to understand the unique circumstances of your clients.

Client AA nurse aged 24

Client BA plumber aged 60

Clients’ goal/s for retirement

Client’s stage in life

Client’s financial risk profile (low, medium, high)

Client’s available super funds and their type

Tax, Super+You.

Page 36

Take Control.

Decide a super investment strategy using a cost-benefit analysis2. Analyse the risks and rewards (costs and benefits) of different investment strategies with the clients in mind.

Client AA nurse aged 24

Client BA plumber aged 60

Super investment asset types/investment options available to client

Potential risk/s of the investment options

Potential reward/s of the investment options

Potential risk/s in the client’s life events

Potential reward/s in the client’s life events

Possible suitable super investment option/s for:

� short-term � medium-term � long-term

Tax, Super+You.

Page 37

Take Control.

Propose a course of action to inform an investment strategy3. To help your clients make investment decisions, use the template below to show investment advice including objectives, investment

options (asset type combination), short, medium and/or long-term strategies, and expected outcomes. Justify your advice.

Short-term objective/s

Strategy: Investment option/s

Expected outcomes

Justification for these conclusions

Retirement goal

Medium-term objective/s

Strategy: Investment option/s

Expected outcomes

Justification for these conclusions

Long-term objective/s

Strategy: Investment option/s

Expected outcomes

Justification for these conclusions

Client A: Course of action

Tax, Super+You.

Page 38

Take Control.

Client B: Course of action

Short-term objective/s

Strategy: Investment option/s

Expected outcomes

Justification for these conclusions

Retirement goal

Medium-term objective/s

Strategy: Investment option/s

Expected outcomes

Justification for these conclusions

Long-term objective/s

Strategy: Investment option/s

Expected outcomes

Justification for these conclusions

Tax, Super+You.

Page 39

Take Control.

Evaluate your course of action proposal4. Write a paragraph that describes your proposed course of action for Client A and evaluates how effectively your proposed plan

meets Client A’s goal. Do another paragraph for Client B.

Alternatively, write a comparative piece explaining why your courses of action vary for Client A and Client B.

DESCRIPTION (OR COMPARISON) AND EVALUATION OF COURSES OF ACTION

Tax, Super+You.

Page 40

Take Control.

WHAT ROLE DOES THE ATO PLAY IN RELATION TO SUPER? DISCOVER WHAT RESPONSIBILITIES THE ATO HAS FOR

YOUR SUPER LIFE CYCLE AND LINK THESE RESPONSIBILITIES TO BOTH INDIVIDUAL AND BUSINESS SUPER.

Super Activity 5

SUPER, THE ATO AND YOU

Fact sheet

Years 7-10

ATO REGULATION AND ADVICEThe ATO regulates super and provides a great deal of advice to assist individuals and businesses to take responsibility in complying with super rules and to manage super. The ATO’s work includes regulation and advice about:

� super guarantee contributions � government super contributions (co-contribution and low

income super tax offset) � other contributions � salary sacrificing � keeping track of your super – including lost and ATO-held

unclaimed super

� accessing super early or at retirement � consolidating super or transferring between funds � using myGov � self-managed superannuation funds (SMSFs).

Know about accessing your superGenerally you cannot access your super until you reach your earliest retirement age, which is called your 'preservation age'. The preservation age is 60 for anyone born after 30 June 1964.

Once you become eligible to access your super, you can either take it all as a lump sum or invest it in a superannuation pension or annuity to provide you with a regular income stream, or a combination of both depending on the rules of the fund. Given that many people live 20 to 30 years in retirement, it is important that your super lasts as long as possible.

Early access to your super There are only a few other circumstances in which you may be able to access your super before retirement. These include severe financial hardship, compassionate grounds, a terminal medical condition and permanent incapacity.

Deciding when and how to take your superannuation is a complex decision, as there are many tax and welfare implications. You can seek advice from someone who can help, such as a financial advisor or other qualified professional.

When you access your super, how tax applies to your super benefits depends on a number of factors, such as your age, the source of your benefit and how your benefit is paid. You can find out more on the ATO’s website.

Cautionary adviceThe ATO also investigates and seeks to penalise illegal practices in relation to super, and also offers cautionary advice.

An example:

Illegal super schemes often target people who are under financial pressure or who do not understand the super laws. Some people promoting illegal super schemes will tell you that they can help you access your super early to pay off credit card debt, buy a house or car, or go on holiday. They claim they can offer early access to your super savings by transferring your super into a self-managed super fund (SMSF).

These schemes are illegal. If you participate in one of these schemes, they will cost you a lot more than the super you access and may get you into a lot of trouble. For example:

� These schemes are illegal and heavy penalties apply if you participate.

� You may become a victim of identity theft. Identity theft happens when someone uses your personal details to commit fraud or other crimes. Once your identity has been stolen and misused, it can take years to fix.

� They may charge high fees and you risk losing some or all of your super to the scammer.

For more information, go to the ATO website at www.ato.gov.au and search for 'illegal super schemes'.

Tax, Super+You.

Page 41

Take Control.

TASK 1 WHO IS RESPONSIBLE FOR SUPER?Super Activity 5: Super, the ATO and you

Worksheet

Years 7-10

YOU WILL: � identify the responsibilities of the ATO and businesses in

relation to super � make conclusions about the role of the ATO in Australian

society

YOU WILL NEED: � Fact sheet 1: What is superannuation � Fact sheet 2: Where does my super money come from? � Fact sheet 3: What do I need to do about super? � Fact sheet 4: How do I choose a super fund? � Fact sheet 5: Super, the ATO and you

What role does the ATO play in relation to super? And what responsibilities do individuals and businesses have in supporting individuals’ superannuation?

LOCATE INFORMATION AND IDENTIFY RESPONSIBILITIES1. Review Super Fact Sheets 1, 2, 3, 4 and 5 to identify responsibilities of the ATO, businesses and individuals in relation to super.

Record them in the table below.

What responsibilities do we all play in relation to super?Responsibilities

Aspect of super ATO Businesses Individuals

Example: Educating about super

Keeping businesses and individuals informed about super

Seeking information from ATO sources such as the website and helplines

Seeking information from ATO sources such as the website and helplines

Tax, Super+You.

Page 42

Take Control.

Develop a conclusion about super, the ATO and you2. Now that you have explored the world of super and the role played by the ATO, respond to the statement:

“The ATO is working for all Australians”.

Use the criteria below to guide your development of an informed and justified response.

Conclusion

Point State your conclusion in response to the statement (one sentence)

Elaboration Explain in a little more detail why you conclude this (one or two sentences)

Evidence/Example Provide evidence or arguments based on your analysis of findings (several sentences)

Relate Restate your conclusion (one sentence)

Criteria – Your conclusion:

� is concise and to the point � explains big understandings about the role of the ATO in Australian society � identifies key ideas, for example, who 'all Australians' are, the ATO’s role in super, aspects of super � uses facts or examples to support big ideas.

An evidence-based conclusion is a conclusion that is based on research and analysis of data

and information.

Tax, Super+You.

Page 43

Take Control.

TASK 2 EARLY ACCESS AND ATO SCAM ADVICESuper Activity 5: Super, the ATO and you

Worksheet

Years 7-10

YOU WILL: � research and create informed advice about early access to

super and avoiding scams � research the responsibilities of the ATO in relation to super

and scams

YOU WILL NEED: � Fact sheet: Super, the ATO and you

EARLY RELEASE SCHEMES FOR SUPER MAY BE SCAMS. INVESTIGATE THE RISKS AND BENEFITS OF PEOPLE ACCESSING

THEIR SUPER BEFORE THEY ARE ENTITLED TO. SEE HOW THE ATO CAN ASSIST PEOPLE TO AVOID BEING SCAMMED.

DEVELOP INFORMED ADVICEInvestigate the following scenario and prepare a presentation which offers informed advice about scams and how the ATO can assist.

ScenarioYou are the president of a sports club. One of your members found this flyer when they parked at your local sporting ground last weekend. A number of members are talking about getting early release of their super.

EarlyRelease Super

� Do you need money? � Pay off your bills! � The share market is not recovering this year! � Your super money is not making enough for you!

� ERS can help you get hold of your lazy super money for a small fee.

ERS

Contact: 1300 123 456

Tax, Super+You.

Page 44

Take Control.

Your roleYou have studied super at school in business studies. Club members ask you for advice about how

someone can access their super before retirement.

Club members are in a range of financial situations:

� employed and accumulating super � unemployed or working reduced hours in their jobs � struggling to pay off their credit card bills, loans and mortgages.

You realise there is a lot of misinformation about the benefits and risks of applying to the EarlyRelease

Super company in the flyer. You begin some research and find material on the ATO and MoneySmart

websites: www.ato.gov.au and www.moneysmart.gov.au

You record the important points about:

� when the early release of super is legal � how these superannuation scams operate � who they target � warning signs � schemes against which the ATO and ASIC have taken action.

Your task1. Research the issue and how the ATO can assist, using the important points above as a guide.

2. Prepare a presentation for your club members, outlining the situation in relation to the early

release of super. Prepare a presentation that sets out the facts simply but accurately. Include the

important points you have identified.

3. You can select any appropriate and interesting format for your presentation. It could be:

� a multi-media presentation � an article for the club newsletter � page for Facebook or another form of social media � another format.

4. If you have created a digital presentation you can embed it or upload it to the Tax Super and You

forum in a new discussion topic.

See the full range of super information, online tools and videos

support on the ATO website at: www.ato.gov.au

Tax, Super+You.

Page 45

Take Control.

INTERACTIVE WATCH YOUR SUPER GROWSuper

Worksheet

Years 7-10

YOU WILL: � analyse how life events can have negative and positive

effects on super and retirement � consider consequences of life events for the short, medium

and long-term in relation to retirement � propose strategies to manage the effects of life events on

super � present and share creative ideas about managing life events

and super

YOU WILL NEED: � Watch your super grow: Life event cards – two from the set

per group � butchers’ paper � marker pens

Choices made over a 40-year period have an impact on the quality of life in retirement. What decisions do people make at different stages in life that affect their super for retirement?

COLLABORATIVELY BRAINSTORM AND PRESENT – SUPER AND LIFE EVENTS

Your task: Create a hypothetical person and make decisions about how to respond to events at various stages of their life so as to maximise his/her super for retirement.

Work collaborativelyIn a group, plan to assist a hypothetical person achieve the long-term goal of maximising their super funds for retirement at 65 years of age.

1. Identify a person as the focus of your life scenario. Describe him or her — gender, job, annual income, family, needs and wants. Is he/she a saver or a spender? Does he/she want a modest or comfortable retirement?

2. Refer to the Super fact sheets and worksheets to inform your thinking.

Discuss 3. Discuss the two life event cards issued to you.

4. Brainstorm possible effects of these life events on the person’s financial circumstances:

� Be sure to consider and predict how this would affect their super in the short-term, medium-term and long-term. � Propose strategies or actions your person may use to manage the negative effects of life events on their super in the

short-term, medium-term and long-term.

Design a representation 5. Create a visual representation on your chart paper that shows:

� the possible short, medium and long-term effects of life events on retirement and super. � strategies your person could use to manage these effects. � the possible short, medium and long-term effects of these strategies on retirement.

Short-term: 1–5 years Medium-term: 6–20 years Long-term: 21 years on