SUNY Student Loan Service Center Update - National Credit ... · PDF filePERKINS 101 Karen...

41

PERKINS 101 Karen Reddick National Credit Management Jan Hnilica Wheaton College 1

Transcript of SUNY Student Loan Service Center Update - National Credit ... · PDF filePERKINS 101 Karen...

PERKINS 101

Karen Reddick National Credit Management

Jan Hnilica

Wheaton College

1

History of the Perkins Program

2

• Soviet’s launch Sputnik I Satellite on October 4, 1957 during Cold War

• President Eisenhower and Congress pass the National Defense Education Act on

September 2, 1958 to help solidify US economic shortcomings in the areas of

math, science and technological expertise

• Originally called the National Defense Student Loan Program

• In 1972, it was renamed as the National Direct Student Loan Program

• Renamed in 1987 in honor of Carl D. Perkins, a former

Kentucky Congressman (In Office from 1949-1984)

• It was the 1st Federal Financial Aid Program specifically

designed for disadvantaged, low-income students

• Do you know anyone famous that had a Perkins Loan?

Making A Perkins Loan

3

• General Regulations for Perkins is 34 CFR Part 674

• School must participate in the Federal Perkins Loan Program and complete a PPA per 34

CFR 674.8

• Revolving Fund that needs to be monitored closely to ensure no excess cash and proper

Level of Expenditure (LOE)

• (FCC + ICC + collections + cancellation reimbursements + cash on hand =

LOE)

• Matching ICC and FCC

• Schools Receive Administrative Cost Allowance to Administrate the Program

• Complete Annual FISAP

• Keep Subsidiary Records to enforce the loans and retain up to 3 years

• Update NSLDS

• Schools need to comply with FTC Red Flag Rules on Identity Theft and Perkins Loans (E-

Announcement June 14, 2010)

Making A Perkins Loan

• Student must demonstrate financial need

• 75% of loan recipients had a combined family income less than $60,000 per year 1

• Student must be enrolled at least half-time and must maintain good grades

• Eligible undergraduate students can receive up to $5,500 per year ($27,500 total)

• Graduate students can receive up to $8,000 per year ($60,000 total Average loan amount if $2,166 per student

• Interest rate is fixed at 5%

• No Origination Fees for receiving a Perkins Loan

• Repayment does not start until 9 months after graduation/separation

• Borrowers have up to 10 years to repay the balance and interest

• Loans can be forgiven if the student pursues a public service career

4

Making A Perkins Loan

Master Promissory Note (MPN) ◦ Multi Year (1o years) ◦ Single Year

Disbursement ◦ Notification to the student 30 days prior to

or 30 days after account has been credited Amount Date Right to cancel

Disclosure Requirements 34 CFR 674.16(a) ◦ Rights and responsibilities prior to

disbursement

5

Promissory Note

• A Promissory Note is the legally binding document per 34 CFR 674.31.

• Paper or Electronic

• Evidence of a borrower’s indebtedness to a school.

• Includes information about:

Loan’s Interest Rate

Repayment Terms

Fixed Monthly Payment

Entitlement Provisions

Credit Bureau Reporting

Penalty / Late Charges

Consequences of Default

Collection Costs

Etc.

6

Annual Disclosure

Before making the first Perkins Loan or NDSL disbursement for an award year,

the school must inform the student of his or her rights and responsibilities under the

Federal Perkins Loan Program and must disclose all information to the student in

writing.

• Remind the student that the loan may be used only for educational expenses

• Loan must be repaid

• Review all of the repayment terms in the Promissory Note

7

Annual Disclosure

• Provide following information to the student

− Name and address of the school to which the debt is owed

− Name and address of the official or servicing agent to whom communications should be

sent

− Maximum annual and aggregate amounts the student may borrow

− Effect that accepting the loan will have on the borrower’s eligibility for other types of

student aid

− Statement of the total cumulative balance owed by the student to that school and an

estimate of the monthly payment amount needed to repay that balance

− Options the borrower may have to consolidate or refinance

− Brief notice about the Department of Defense program for repaying loans based on certain

military service

− Complete list of charges connected with making the loan, including whether those charges

are deducted from the loan or whether the student must pay them separately

− Notice that the school will report the outstanding balance of the loan to a national credit bureau at least annually

8

Entrance and Exit Counseling

• Entrance and Exit Interview Counseling are Federal Requirements

• 34 CFR 674.42(a) and 34 CFR 674.42(b)

• It is designed to facilitate the borrower‘s understanding of the financial assistance that has been

extended by the School (i.e. Financial Literacy) and reduce default

• It must also provide detailed information concerning the borrower’s Rights and Responsibilities

• Options include:

• Print & Mail

• Within 30 day of separation

• Face-To-Face

• 3rd Party Websites

• School’s Website

• Your Current Student Loan Servicer

9

Entrance Counseling

• Entrance Interview Counseling – Suggested Elements

• Repayment Obligations

• Review Terms and Conditions

• Consequences of Default

• Effects of Acceptance-Program Specific

• Master Prom Note

• NSLDS Info

• Budgeting

• Updating Contact Info

• Refund Policies

• Keeping Loan Records

• Requirements of Existing Counseling

10

Exit Counseling • Exit Interview Counseling - Required Elements

• Terms and Conditions

• Average Anticipated Monthly Payment

• Debt Management

• Repayment Obligations

• Tax Benefits

• Change Repayment Plans

• MPN

• Options to Prepay

• Forbearance

• Cancellations

• Consequences of Default

• Obligation to pay in full

• Current Information

• Student Loan Ombudsman

• NSLDS

• Loan Consolidation

11

Credit Bureau Reporting

As of 7/23/92, Credit Bureau Reporting must be initiated on all accounts from the

Date of Disbursement to at least one National Credit Bureau. All Credit Bureau

Updates must be made within (30) days of any account status change. 34 CFR

674.45(a)(1) and (b)

National Credit Bureaus:

• Trans Union Corp.

• Experian (formerly TRW)

• Equifax

12

Grace Periods 34 CFR 674.2, 34 CFR 674.31 and 32 Initial Grace Period

9 months Post Deferment

6 months

Terms 10 years 5% interest on loans after July 1, 1981 Disclosure terms before student drops to less than ½ time enrollment Monthly/Bimonthly/Quarterly Calculation of payment

Multiply the principal by the constant multiplier

◦ Monthly - .0106065 (120 payments) ◦ Bimonthly - .0212470 (60 payments) ◦ Quarterly - .0319214 (40 payments)

Incentive Repayment Plan 34 CFR 674.33(f) 1% reduction after 48 consecutive payments Discount up to 5% of the balance owed if paid in full by repayment period With Secretary approval establish repayment options that reduce default All costs need to be repaid to the fund

13

Repayment

Repayment

Calculating Payments 34 CFR 674.33(a)

$5000 Perkins Loan with monthly payments

5000 x .0106065 = $53.03

Payment would be $55

$3500 Perkins Loan with monthly payments

3500 x .0106065 = $37.12

Payment would be $40

Minimum payment requirement of $40

Establish Repayment Dates Most prefer fixed repayment date

Extension of Repayment 34CFR 674.33(c)

14

Repayment

Posting Payments

◦ Order of Posting

1. Collection Cost

2. Late Charges

3. Accrued Interest

4. Principal

◦ Payments applied to the oldest past due dollars first

15

Forbearance 34 CFR 674.33

Temporary postponement of payment

Doesn’t have to be in writing

Period of 1 year not to exceed 3

Types

Hardship

◦ Loans = 20% of Total Income

Poor Health

AmeriCorps Volunteer

National military mobilization

National emergency

16

Deferments 34 CFR 674.38

No interest accrues Post grace period of 6 months Grant deferments based on other FSA Loans Reaffirm yearly Types:

In school Graduate fellowship VR training program Unemployment Economic hardship Military service and active duty

17

Cancellations 34 CFR 674.52

Law Enforcement and Public Defender Early Childhood Education (Pre K, Child Care, and Head Start) Public Service

◦ Firefighter ◦ Early Intervention ◦ Child or Family Services ◦ Speech Pathologist at Title 1 School ◦ Librarian at Title 1 School ◦ Faculty Member at a tribal college

Military Service Different schedule prior to August 2008

Elementary/Secondary Teacher ◦ Low income school or education service agency ◦ Teaching in teacher shortage field ◦ Special Ed

Volunteer Service Cancellation (Peace Corps or AmeriCorps)

Only 70% Forgiveness

18

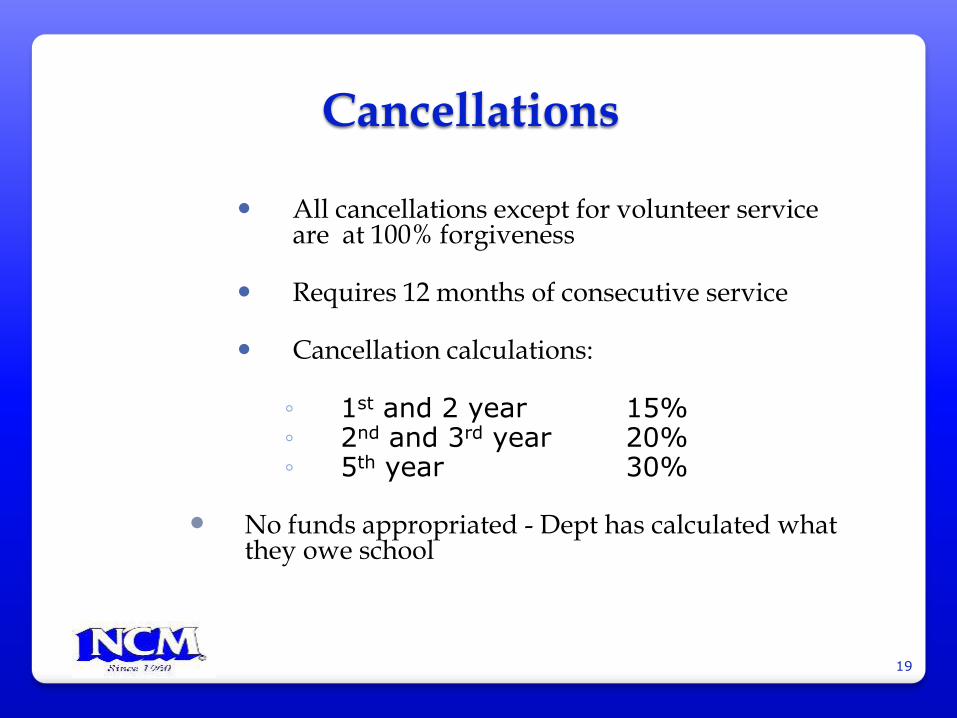

Cancellations

All cancellations except for volunteer service

are at 100% forgiveness Requires 12 months of consecutive service Cancellation calculations:

◦ 1st and 2 year 15% ◦ 2nd and 3rd year 20% ◦ 5th year 30%

No funds appropriated - Dept has calculated what

they owe school

19

Discharging Loans 34 CFR 674.61

Total and permanent Disability - Department of Ed handles

Physician needs to certify within 90 days of application

Veterans disability VA determines disability School closing

Bankruptcy discharge Undue hardship

9/11 Spouse Victims

Closed school Due to death

Original or certified copy of death certificate CFO can approve without death certificate

20

Total & Permanent Disability

• Individuals seeking a TPD discharge will submit a single TPD discharge application directly to the

Department of Education (the Department) rather than to their individual loan holders.

• Throughout the new TPD discharge process, there will be several points when the Nelnet Total and

Permanent Disability Servicer will notify loan holders of actions the loan holder must take related to a

borrower’s account. The Nelnet Total and Permanent Disability Servicer will notify loan holders of the

following:

o That a loan holder must suspend collection activity on a borrower’s loans for up to 120 days while

the borrower completes and submits the TPD discharge application.

o That a loan holder must suspend collection activity on the borrower’s loans indefinitely while the

Department reviews TPD discharge application to determine whether the borrower qualifies for

discharge.

o That the TPD discharge application has been rejected, including the reason that the application has

been rejected.

o That the TPD discharge application has been approved.

• The Department will implement the notifications to loan holders described above through the use of the

TPD LHN File that the Nelnet Total and Permanent Disability Servicer will send to loan holders in a comma

separated values (*.csv) file.

21

Total & Permanent Disability

IFAP May 24, 2013 Electronic Announcement for TPD: http://www.ifap.ed.gov/eannouncements/052413TPDDITPDLHNFileforUseBeginning070113.html.

For additional information about the new TPD discharge process that is effective July 1, 2013, please see the June 20, 2013 Electronic Announcement on this subject. The announcement is available at http://ifap.ed.gov/eannouncements/062013TPDDischargeInfoReminder070113EffectChangeTPDDischargeRegulations.html.

Servicer: Nelnet

US Department of Education 3015 South Parker Road, Suite 400 Aurora, CO 80014 888-303-7818 www.disabilitydischarge.com

22

Billing Procedures Requirements at end of enrollment

◦ Exit Interviews 34 CFR (674.42(b) ◦ Disclosure of Repayment 34 CFR 674.42(a)

Contact information to get copy of prom note Name and address of school Contact information on where to send payments Estimated balance Total interest charges Repayment schedule

◦ Due date ◦ Rate of interest ◦ Number of payments ◦ Amount of payments ◦ Frequency of payments

◦ Grace Period Contact

9 month initial grace period ◦ 90 days ◦ 150 days ◦ 240 days (first billing notice)

6 month grace period ◦ 90 days ◦ 150 days (first billing notice)

23

Billing Procedures

Statements • 30 days prior to 1st payment • 15 days prior for all subsequent payments

Coupon Books

• 30 days before 1st payment

24

Collection Procedures

Overdue payments

◦ 1st notice-15 days ◦ 2nd notice-45 days ◦ 3rd notice-60 days

(final demand) Late charges

◦ Not to exceed 20% ◦ Optional

Telephone contact ◦ No response within 30 days of final demand ◦ At least two attempts

Loan acceleration Entire amount due Written notification -30 days prior (final demand) Written notification when the loan was accelerated total

amount due

25

Collection Procedures

Credit Bureau Reporting 34 CFR 674.5

Two efforts to collect 1st Effort - In house or outside collection agency, if

not returned to regular payment status by 12 months and does not qualify for benefits you need to either litigate or make a second effort

2nd Effort - If 1st effort is your own personnel, then you need to send to an outside collection agency

Collection agency 34 CFR 668.25(c) - Attestation Audit Required to return account at 12 months if there is

no cure

26

Collection Procedures

Yearly attempt

Bi-Yearly Address Searches Can cease collections under $200

Litigation Minimum $500 and review every 2 years

Compromise Waive collection cost Up to 10% of principle balance

Write Off Balances $25 or less $50 or less after two years of billing

27

Collection Procedures Collection Cost

34 CFR 674.48 and 34 CFR 674.45(e) Required to charge reasonable cost

◦ 1st Referral - Up to 30% ◦ 2nd Referral, subsequent referrals including litigation-Up to

40% ◦ Rehabilitation - capped at 24%

Rehabilitation

◦ 9 month consecutive on time payments (Neg Reg) ◦ Sufficient to satisfy outstanding balance ◦ Can not require the balance paid in full if causes an undue

hardship ◦ Within 30 days of last payment Return borrower to regular repayment status(decelerate) Treat 1st payment as the 1st payment of a new 10 year

payment schedule Remove default status from credit bureaus Borrower regains benefits Can only complete one time, but can try as many times as

needed

28

Assignments 34 CFR 674.50

Assignments 34CFR 674.50 Balance of $25 or more Unable to collect after completing the proper due diligence Loan is accelerated Recall 60 days from agencies and withdraw from credit bureaus Send notification 90 days prior Required Assignment Documents:

29

1.Submission Package Manifest 2. Perkins Assignment Form 3. Original Promissory Note and Certification/Audit of E-Signature Process 4. Judgment Information (If Applicable) 5. Bankruptcy Information (If Applicable) 6. Due Diligence Documentation (If applicable) 7. Complete Repayment History

Assignments

Procedures: www.ifap.ed.gov/ifap/cbp.jsp

School Contact Information:

ECSI Servicer (415) 486-5655

Borrower Contact: US Department of Education

ECSI Federal Perkins Loan Servicer PO Box 105765

Atlanta, GA 30348-5765 (866) 313-3797

30

COHORT Default Rate 34 CFR 674.5(b)

30 or fewer borrowers ◦ The percentage of those current and former students

who entered in repayment on loans received for attendance at the school in any of the three most recent years and who defaulted on those loans before the end of the award year immediately following the year in which they entered in repayment

30 or more borrowers ◦ The percentage of those current and former students

who enter in repayment in that award year on loans received for attendance at the school and who default before the end of the following award year

Sample ◦ 25 defaulted loans/1000 borrowers = 2.5% default

rate Penalties 25% or higher no FCC 50% or higher no funding

31

COHORT Default Rate How to Reduce Cohort Default Rate ◦ 6 monthly consecutive payments ◦ Bring loan current ◦ PIF – Consolidation ◦ Deferment/Forbearance Utilize NSLDS ◦ Rehabilitation ◦ Default management ◦ DRAP

32

Loan Consolidation

33

• Up to 30 years for repayment (depending on your loan balance)

• One monthly payment

• May lower the interest rate on some or all of your loan debt (Extending the term beyond the 10 years increases total interest paid)

• Interest rates on consolidation loans are fixed rates that do not change over time rather than variable rates that do change over time.

Advantages • Extending the term beyond the 10 years

increases total interest paid

• Loss of certain deferment and forbearance options

• Loss of all Perkins Loan cancellations provisions

• Loss of Perkins 9 month grace period

Disadvantages

Loan Consolidation

34

New Process Implemented as of January 2, 2014.

Four Direct Loan Servicers (TIVAS):

• PHEAA

• Great Lakes

• Nelnet

• Sallie Mae

Processing Options:

• TIVAS Portals

• Files Via Email or Secure FTP

• Paper or Fax???

• Outsource

FISAP- Fiscal Operations Report

Annual report that the school is required to submit to Department of Education by September 30th, and then an update on October 31 for cash on hand for Perkins.

2015-2016 FISAP in PDF Format, 154KB, 12 Pages

Financial Aid completes FSEOG and FWS part.

Business office completes the Perkins part.

35

FISAP: Continued

Perkins portion of FISAP, what do you need before you start?

FISAP directions : 2015-206 Instructions for FISAP in PDF Format, 436KB, 77 Pages

Perkins Balance sheet from school’s General Ledger.

If a 3rd party servicer is used, a FISAP report dated 6/30.

All accounting adjustments and entries should be complete.

Reconciliation should be complete between 3rd party servicer and school’s General Ledger.

This report should be done in August, early September.

36

FISAP: Continued

FISAP step by step for Perkins: ◦ Part III section A

◦ Cash on Hand as of 6/30:

◦ GL Balance Sheet

◦ Principal/Interest Collected

◦ Loan Advances

◦ Cancelations

◦ Collection Costs

◦ ACA

37

FISAP: Continued ◦ Part lll Section A Continued: Numbers 2-57:

Combination of FISAP report and GL numbers.

Remember to use CULMATIVE numbers, not just past fiscal year.

If properly reconciled from the past year, this is

mostly a plugging in numbers from GL and Fisap

report. ◦ Line 58: Two columns from the above numbers

need to match. If they do not match, your FISAP cannot be submitted!

38

FISAP : Continued

Part III Section B Highlights: ◦ Advance Loans from the past award year.

◦ ACA from past award year.

◦ Your FISAP report has these numbers.

◦ Part III Section C: Status of Borrowers: FISAP Report

Cohort Default Rate: FISAP Report

39

FISAP : Continued

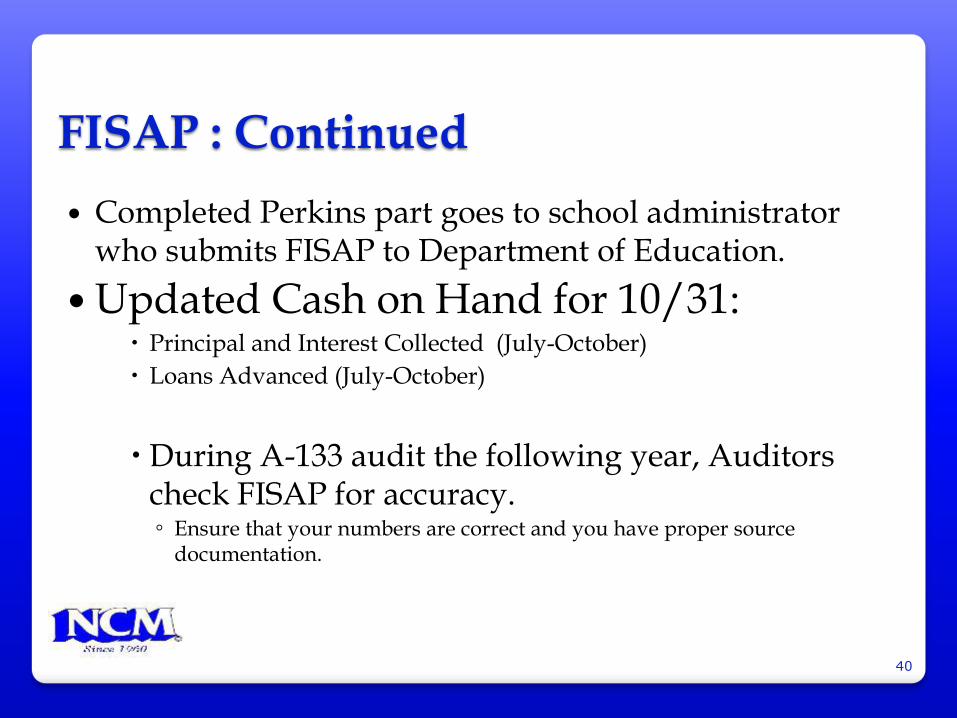

Completed Perkins part goes to school administrator who submits FISAP to Department of Education.

Updated Cash on Hand for 10/31: Principal and Interest Collected (July-October)

Loans Advanced (July-October)

During A-133 audit the following year, Auditors check FISAP for accuracy. ◦ Ensure that your numbers are correct and you have proper source

documentation.

40

CONTACT INFORMATION

Karen Reddick [email protected]

Jan Hnilica

IFAP Website www.ifap.ed.gov

FSA Ombudsman contact info: US Department of Education

830 First St NE Washington, DC 20202

877-557-2575

41