Sunsuper for life Insurance guide · p1 Important information This is the Sunsuper for...

35

Sunsuper for life Insurance guide Preparation date: 7 September 2017 Issue date: 30 September 2017

Transcript of Sunsuper for life Insurance guide · p1 Important information This is the Sunsuper for...

Sunsuper for life Insurance guidePreparation date: 7 September 2017

Issue date: 30 September 2017

p1

Important information This is the Sunsuper for life Insurance guide. The information in this guide forms part of the Sunsuper for life Product Disclosure Statement (PDS) issued 30 September 2017. The PDS references important information contained in this guide by ! . This guide may reference important information contained in the Sunsuper for life Investment guide and Sunsuper for life guide. The PDS, this guide, the Sunsuper for life Investment guide and Sunsuper for life guide should be read in their entirety before making a decision to acquire or continue to hold an interest in the product.

General advice disclaimer The information in the PDS and guides is general information only and doesn’t take into account your personal objectives, financial situation or needs. You should consider the appropriateness of any general information in the PDS and guides having regard to your own personal objectives, financial situation and needs. You should obtain financial advice tailored to your personal circumstances. Call us if you would like to speak to a qualified financial adviser.

Protecting your privacy Sunsuper respects the privacy of the information you give us. If you require a copy of our Privacy Policy visit sunsuper.com.au/privacy or call 13 11 84.

Financial Services Guide (FSG) Visit sunsuper.com.au/fsg or call us on 13 11 84 for a copy of the FSG. The FSG provides you with information about the financial services Sunsuper Pty Ltd provides and will help you decide whether to use these services.

The insurerInsurance cover is provided through group life policies for Death and TPD, and Income Protection, issued by AIA Australia Limited (AIA Australia) ABN 79 004 837 861 to the Trustee of the Sunsuper Superannuation Fund. In the event of a dispute the policy will override the information in the PDS and this guide.

In conjunction with either a disablement claim application or an application for additional cover, Sunsuper members may be contacted directly by an AIA Australia representative on behalf of the Fund to discuss or gather information relating to their application.

AIA Australia Privacy AIA Australia also respects your privacy. AIA Australia’s handling and exchange of your personal and sensitive information is outlined in the AIA Australia Privacy Policy available at www.aia.com.au or by calling AIA Australia on 1800 333 613.

Refund of premiums to the TrusteeAs part of the Trustee of the Sunsuper Superannuation Fund’s arrangements with AIA Australia to provide insurance to Fund members, the Trustee may receive a refund of premiums, depending on the level of claims against the insurance policies. The Trustee may use any refunded premiums to help meet insurance offering costs or to fund insurance related enhancements. Any refunded premiums which are received and not yet used for these purposes are allocated to an insurance reserve.

Contents

1 Why have insurance? 2

2 What types of insurance can I have throughSunsuper?

4

3 How much cover do I need? 6

4 Am I eligible for insurance cover? 7

Other important eligibility terms and conditions 8

When does my insurance cover start? 9

5 Death and TPD cover 10

Death and TPD Assist 10

New Member options — Increase your Death and TPD Assist cover by 50% 15

White Collar cover 16

Life and Age Event Options 17

Tailored Death and TPD cover 19

Conditions and Exclusions 23

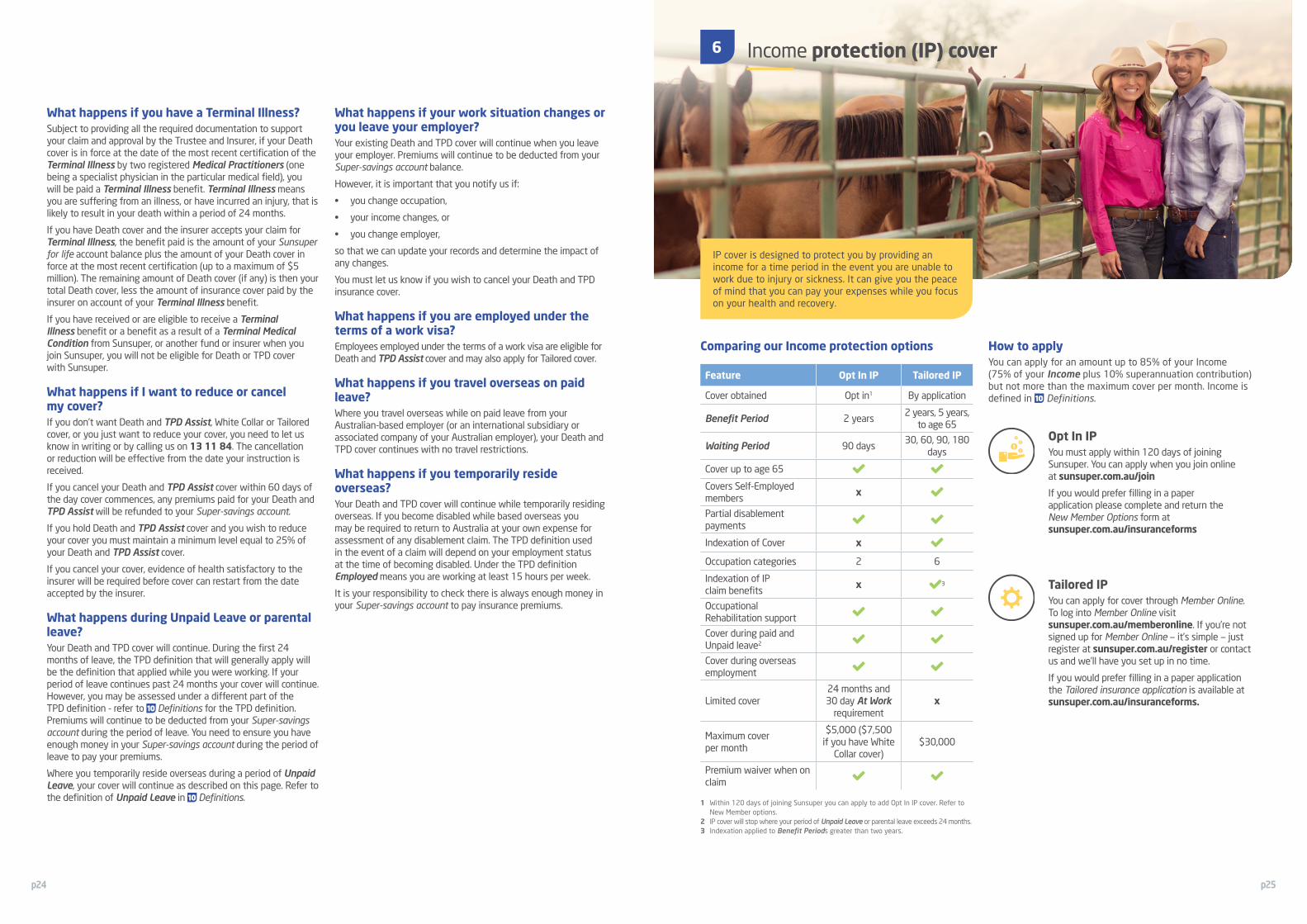

6 Income Protection (IP) cover 25

New Member options — Opt In IP cover 26

White collar IP cover 27

Tailored IP cover 28

Conditions and Exclusions 32

7 How do I apply? 36

8 Premium Rates 38

9 Facts about making a claim 46

10 Definitions 49

Insurance in your super

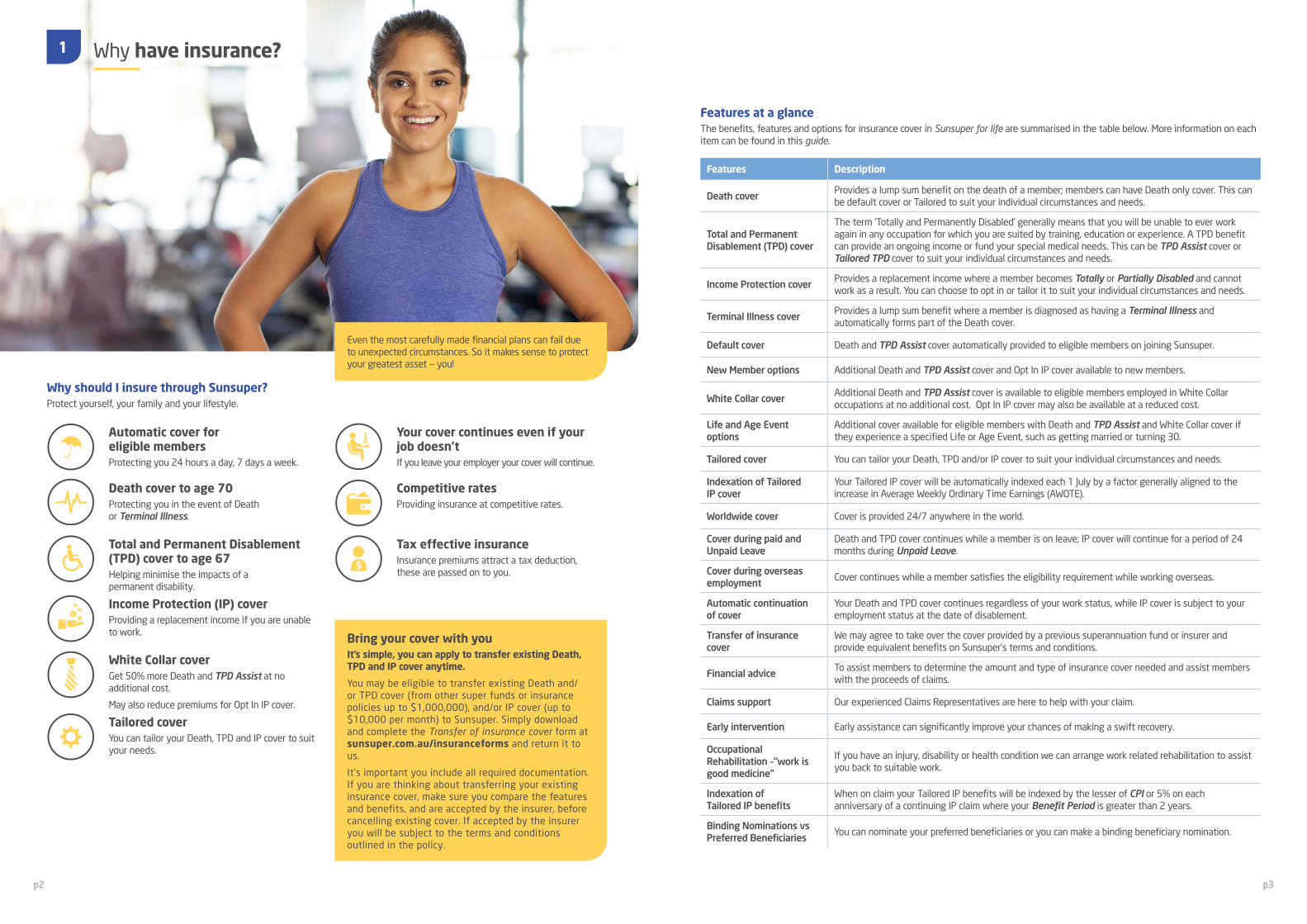

Why should I insure through Sunsuper?Protect yourself, your family and your lifestyle.

Automatic cover for eligible membersProtecting you 24 hours a day, 7 days a week.

Death cover to age 70Protecting you in the event of Death or Terminal Illness.

Total and Permanent Disablement (TPD) cover to age 67Helping minimise the impacts of a permanent disability.

Income Protection (IP) coverProviding a replacement income if you are unable to work.

White Collar coverGet 50% more Death and TPD Assist at no additional cost.

May also reduce premiums for Opt In IP cover.

Tailored coverYou can tailor your Death, TPD and IP cover to suit your needs.

Features at a glanceThe benefits, features and options for insurance cover in Sunsuper for life are summarised in the table below. More information on each item can be found in this guide.

Features Description

Death coverProvides a lump sum benefit on the death of a member; members can have Death only cover. This can be default cover or Tailored to suit your individual circumstances and needs.

Total and Permanent Disablement (TPD) cover

The term ‘Totally and Permanently Disabled’ generally means that you will be unable to ever work again in any occupation for which you are suited by training, education or experience. A TPD benefit can provide an ongoing income or fund your special medical needs. This can be TPD Assist cover or Tailored TPD cover to suit your individual circumstances and needs.

Income Protection coverProvides a replacement income where a member becomes Totally or Partially Disabled and cannot work as a result. You can choose to opt in or tailor it to suit your individual circumstances and needs.

Terminal Illness coverProvides a lump sum benefit where a member is diagnosed as having a Terminal Illness and automatically forms part of the Death cover.

Default cover Death and TPD Assist cover automatically provided to eligible members on joining Sunsuper.

New Member options Additional Death and TPD Assist cover and Opt In IP cover available to new members.

White Collar coverAdditional Death and TPD Assist cover is available to eligible members employed in White Collar occupations at no additional cost. Opt In IP cover may also be available at a reduced cost.

Life and Age Event options

Additional cover available for eligible members with Death and TPD Assist and White Collar cover if they experience a specified Life or Age Event, such as getting married or turning 30.

Tailored cover You can tailor your Death, TPD and/or IP cover to suit your individual circumstances and needs.

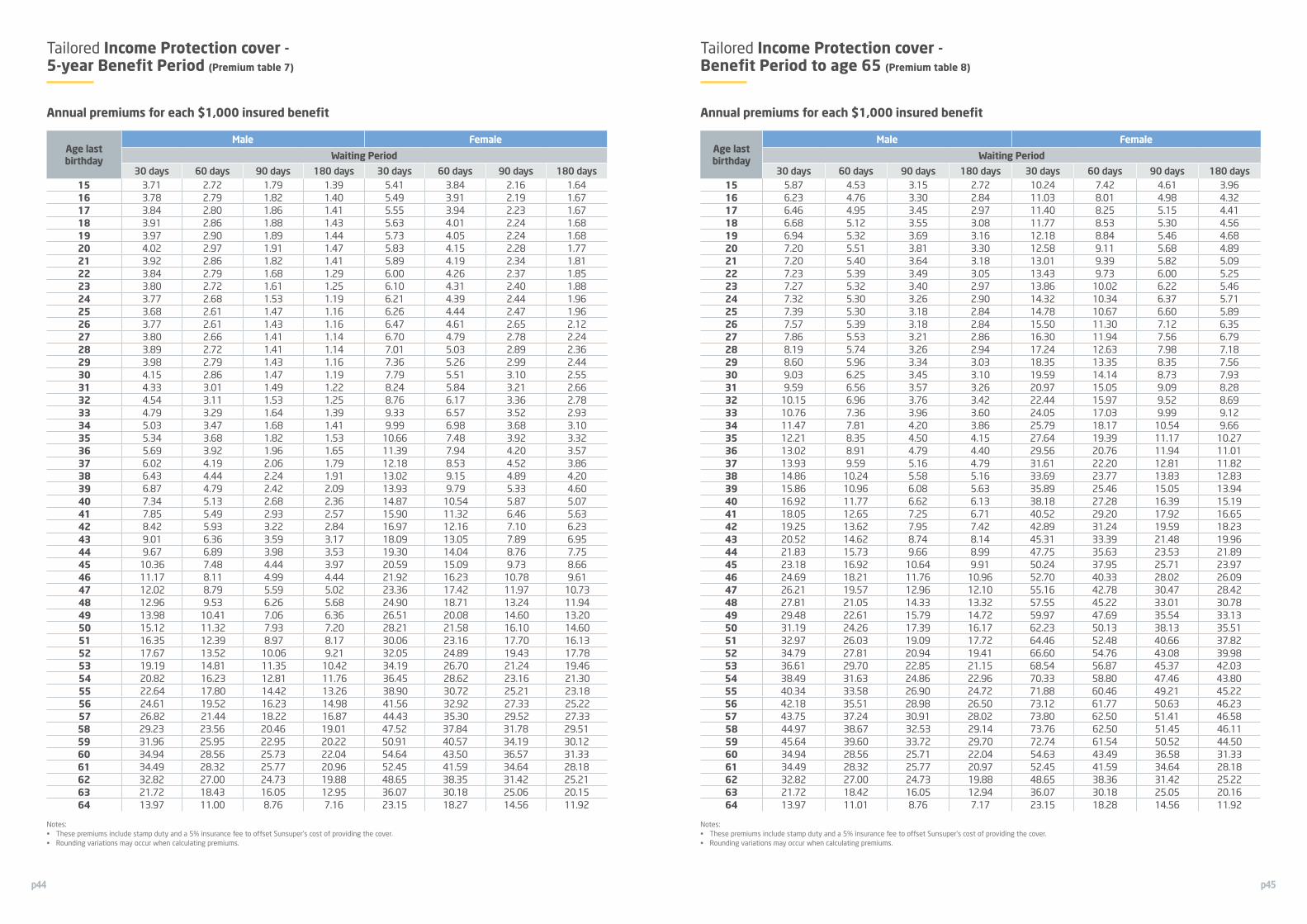

Indexation of Tailored IP cover

Your Tailored IP cover will be automatically indexed each 1 July by a factor generally aligned to the increase in Average Weekly Ordinary Time Earnings (AWOTE).

Worldwide cover Cover is provided 24/7 anywhere in the world.

Cover during paid and Unpaid Leave

Death and TPD cover continues while a member is on leave; IP cover will continue for a period of 24 months during Unpaid Leave.

Cover during overseas employment

Cover continues while a member satisfies the eligibility requirement while working overseas.

Automatic continuation of cover

Your Death and TPD cover continues regardless of your work status, while IP cover is subject to your employment status at the date of disablement.

Transfer of insurance cover

We may agree to take over the cover provided by a previous superannuation fund or insurer and provide equivalent benefits on Sunsuper’s terms and conditions.

Financial adviceTo assist members to determine the amount and type of insurance cover needed and assist members with the proceeds of claims.

Claims support Our experienced Claims Representatives are here to help with your claim.

Early intervention Early assistance can significantly improve your chances of making a swift recovery.

Occupational Rehabilitation –“work is good medicine”

If you have an injury, disability or health condition we can arrange work related rehabilitation to assist you back to suitable work.

Indexation of Tailored IP benefits

When on claim your Tailored IP benefits will be indexed by the lesser of CPI or 5% on each anniversary of a continuing IP claim where your Benefit Period is greater than 2 years.

Binding Nominations vs Preferred Beneficiaries

You can nominate your preferred beneficiaries or you can make a binding beneficiary nomination.

Your cover continues even if your job doesn’tIf you leave your employer your cover will continue.

Competitive ratesProviding insurance at competitive rates.

Tax effective insuranceInsurance premiums attract a tax deduction, these are passed on to you.

p2 p3

1 Why have insurance?

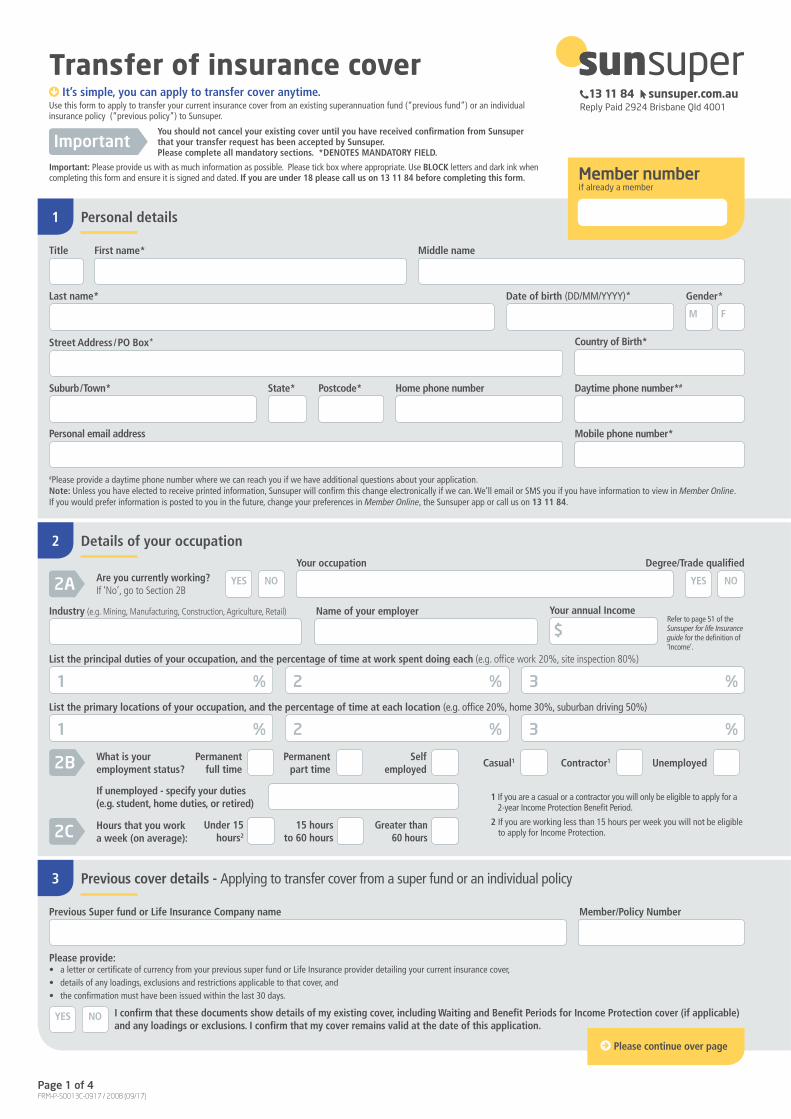

Bring your cover with youIt’s simple, you can apply to transfer existing Death, TPD and IP cover anytime.

You may be eligible to transfer existing Death and/or TPD cover (from other super funds or insurance policies up to $1,000,000), and/or IP cover (up to $10,000 per month) to Sunsuper. Simply download and complete the Transfer of insurance cover form at sunsuper.com.au/insuranceforms and return it to us.

It’s important you include all required documentation. If you are thinking about transferring your existing insurance cover, make sure you compare the features and benefits, and are accepted by the insurer, before cancelling existing cover. If accepted by the insurer you will be subject to the terms and conditions outlined in the policy.

Even the most carefully made financial plans can fail due to unexpected circumstances. So it makes sense to protect your greatest asset — you!

p4 p5

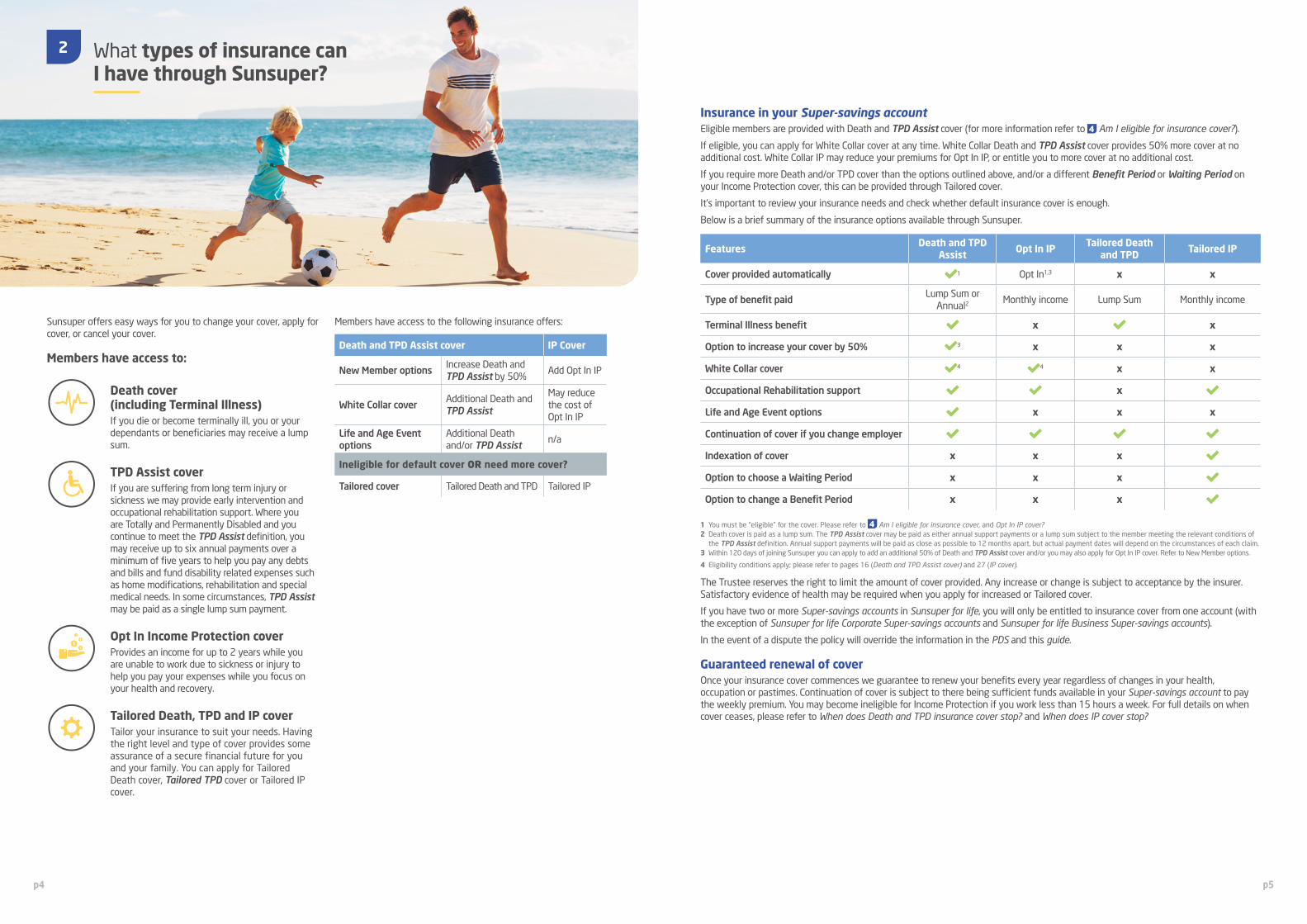

2 What types of insurance can I have through Sunsuper?

Sunsuper offers easy ways for you to change your cover, apply for cover, or cancel your cover.

Members have access to:

Death cover (including Terminal Illness)If you die or become terminally ill, you or your dependants or beneficiaries may receive a lump sum.

TPD Assist coverIf you are suffering from long term injury or sickness we may provide early intervention and occupational rehabilitation support. Where you are Totally and Permanently Disabled and you continue to meet the TPD Assist definition, you may receive up to six annual payments over a minimum of five years to help you pay any debts and bills and fund disability related expenses such as home modifications, rehabilitation and special medical needs. In some circumstances, TPD Assist may be paid as a single lump sum payment.

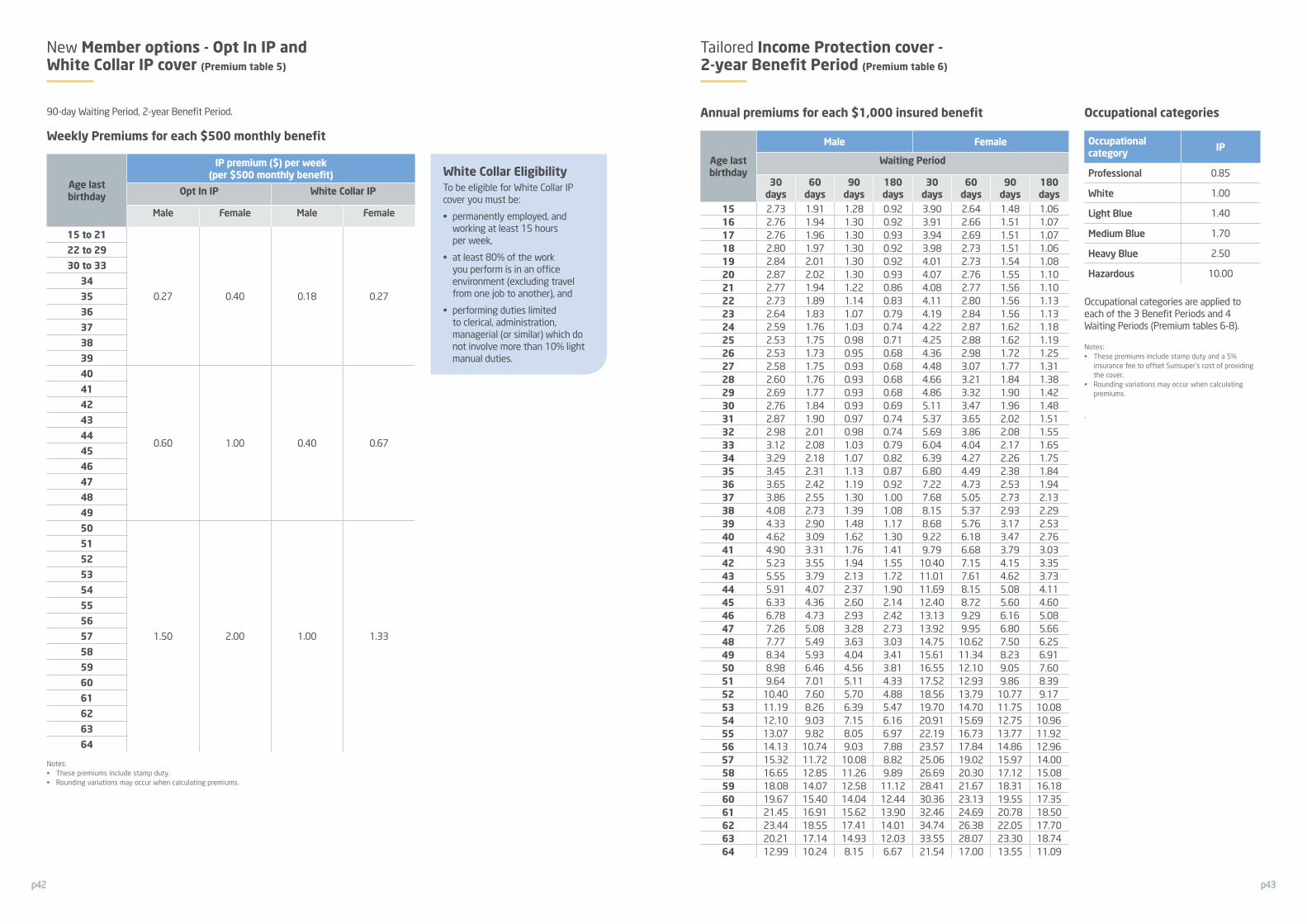

Opt In Income Protection coverProvides an income for up to 2 years while you are unable to work due to sickness or injury to help you pay your expenses while you focus on your health and recovery.

Tailored Death, TPD and IP coverTailor your insurance to suit your needs. Having the right level and type of cover provides some assurance of a secure financial future for you and your family. You can apply for Tailored Death cover, Tailored TPD cover or Tailored IP cover.

Members have access to the following insurance offers:

Death and TPD Assist cover IP Cover

New Member optionsIncrease Death and TPD Assist by 50%

Add Opt In IP

White Collar coverAdditional Death and TPD Assist

May reduce the cost of Opt In IP

Life and Age Event options

Additional Death and/or TPD Assist

n/a

Ineligible for default cover OR need more cover?

Tailored cover Tailored Death and TPD Tailored IP

Insurance in your Super-savings accountEligible members are provided with Death and TPD Assist cover (for more information refer to 4 Am I eligible for insurance cover?).

If eligible, you can apply for White Collar cover at any time. White Collar Death and TPD Assist cover provides 50% more cover at no additional cost. White Collar IP may reduce your premiums for Opt In IP, or entitle you to more cover at no additional cost.

If you require more Death and/or TPD cover than the options outlined above, and/or a different Benefit Period or Waiting Period on your Income Protection cover, this can be provided through Tailored cover.

It’s important to review your insurance needs and check whether default insurance cover is enough.

Below is a brief summary of the insurance options available through Sunsuper.

Features Death and TPD Assist Opt In IP Tailored Death

and TPD Tailored IP

Cover provided automatically 1 Opt In1,3 x x

Type of benefit paidLump Sum or

Annual2Monthly income Lump Sum Monthly income

Terminal Illness benefit x x

Option to increase your cover by 50% 3 x x x

White Collar cover 4 4 x x

Occupational Rehabilitation support x

Life and Age Event options x x x

Continuation of cover if you change employer

Indexation of cover x x x

Option to choose a Waiting Period x x x

Option to change a Benefit Period x x x

1 You must be “eligible” for the cover. Please refer to 4 Am I eligible for insurance cover, and Opt In IP cover? 2 Death cover is paid as a lump sum. The TPD Assist cover may be paid as either annual support payments or a lump sum subject to the member meeting the relevant conditions of

the TPD Assist definition. Annual support payments will be paid as close as possible to 12 months apart, but actual payment dates will depend on the circumstances of each claim.3 Within 120 days of joining Sunsuper you can apply to add an additional 50% of Death and TPD Assist cover and/or you may also apply for Opt In IP cover. Refer to New Member options.

4 Eligibility conditions apply; please refer to pages 16 (Death and TPD Assist cover) and 27 (IP cover).

The Trustee reserves the right to limit the amount of cover provided. Any increase or change is subject to acceptance by the insurer. Satisfactory evidence of health may be required when you apply for increased or Tailored cover.

If you have two or more Super-savings accounts in Sunsuper for life, you will only be entitled to insurance cover from one account (with the exception of Sunsuper for life Corporate Super-savings accounts and Sunsuper for life Business Super-savings accounts).

In the event of a dispute the policy will override the information in the PDS and this guide.

Guaranteed renewal of coverOnce your insurance cover commences we guarantee to renew your benefits every year regardless of changes in your health, occupation or pastimes. Continuation of cover is subject to there being sufficient funds available in your Super-savings account to pay the weekly premium. You may become ineligible for Income Protection if you work less than 15 hours a week. For full details on when cover ceases, please refer to When does Death and TPD insurance cover stop? and When does IP cover stop?

Working out how much insurance is right for you can be a difficult task. The amount of insurance you need will depend on a combination of things such as your liabilities, assets, ongoing expenses and your expected standard of living. Once you have read through this guide for details on the insurance we offer you can work through the following steps to work out how much insurance is right for you.

1

23

4

5

p6 p7

It is important to understand that using your superannuation account now for the payment of insurance premiums before retirement will impact upon your future balance when you do retire.

Need some financial advice?Speak to your adviser or contact Sunsuper to get the advice you need. Call 13 11 84 to speak to one of our qualified financial advisers1 who can give you simple advice about your Sunsuper account at no additional cost, quickly over the phone. For more comprehensive advice, we may refer you to an accredited external financial adviser.2 Advice of this nature may incur a fee.1 Sunsuper employees provide advice as representatives of Sunsuper Financial Services Pty Ltd (ABN 50 087 154 818 AFSL No. 227867) (SFS), wholly owned by the Sunsuper

Superannuation Fund.2 Sunsuper has established a panel of accredited external financial advisers who are not employees of Sunsuper. Sunsuper is not responsible for the advice provided by these

advisers and does not receive or pay any referral fees. These advisers will explain to you how their fees are determined.

3 4How much cover do I need? Am I eligible for insurance cover?

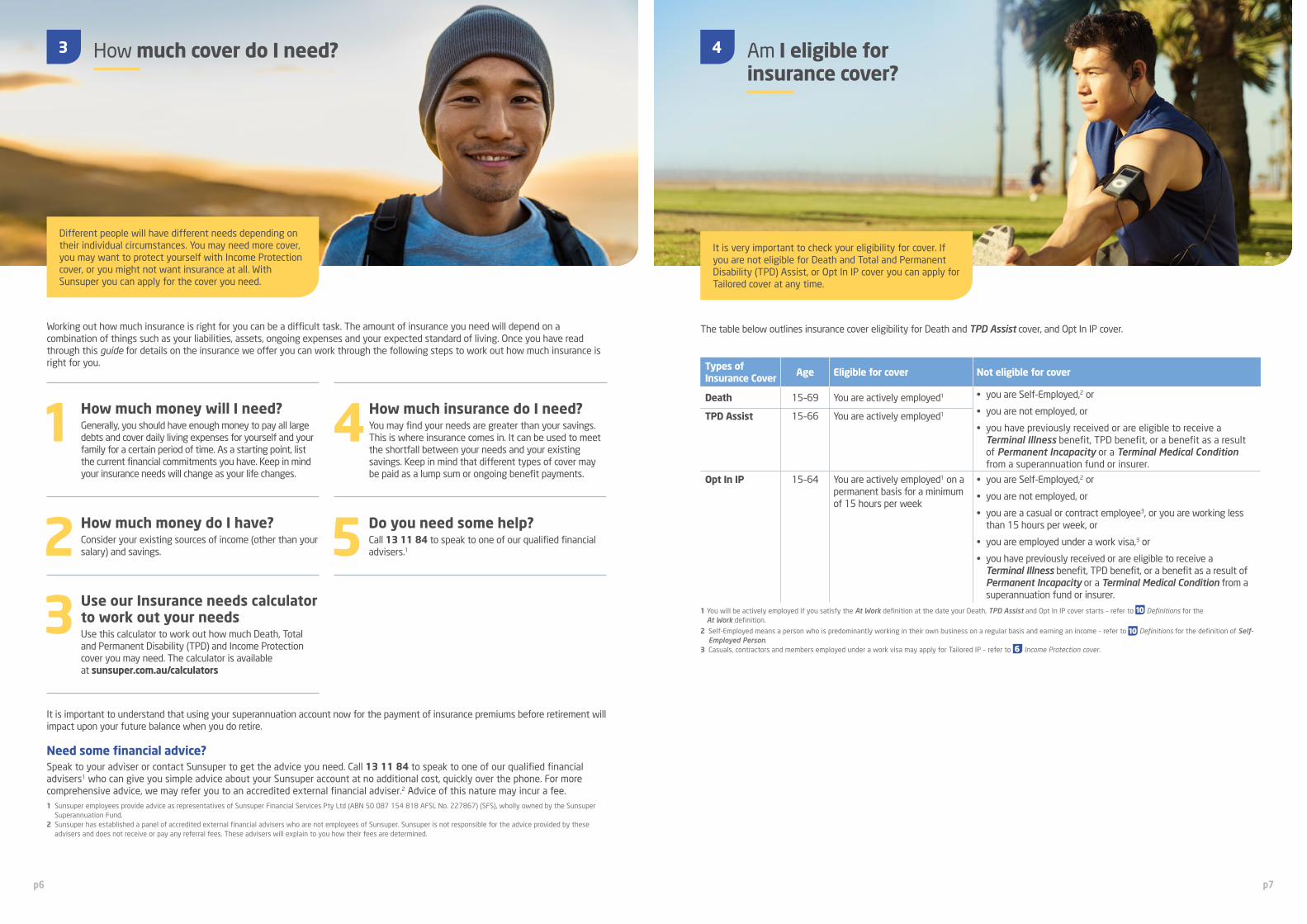

Different people will have different needs depending on their individual circumstances. You may need more cover, you may want to protect yourself with Income Protection cover, or you might not want insurance at all. With Sunsuper you can apply for the cover you need.

It is very important to check your eligibility for cover. If you are not eligible for Death and Total and Permanent Disability (TPD) Assist, or Opt In IP cover you can apply for Tailored cover at any time.

How much money will I need?Generally, you should have enough money to pay all large debts and cover daily living expenses for yourself and your family for a certain period of time. As a starting point, list the current financial commitments you have. Keep in mind your insurance needs will change as your life changes.

How much money do I have?Consider your existing sources of income (other than your salary) and savings.

Use our Insurance needs calculator to work out your needsUse this calculator to work out how much Death, Total and Permanent Disability (TPD) and Income Protection cover you may need. The calculator is available at sunsuper.com.au/calculators

How much insurance do I need?You may find your needs are greater than your savings. This is where insurance comes in. It can be used to meet the shortfall between your needs and your existing savings. Keep in mind that different types of cover may be paid as a lump sum or ongoing benefit payments.

Do you need some help?Call 13 11 84 to speak to one of our qualified financial advisers.1

The table below outlines insurance cover eligibility for Death and TPD Assist cover, and Opt In IP cover.

Types of Insurance Cover Age Eligible for cover Not eligible for cover

Death 15–69 You are actively employed1 • you are Self-Employed,2 or

• you are not employed, or

• you have previously received or are eligible to receive a Terminal Illness benefit, TPD benefit, or a benefit as a result of Permanent Incapacity or a Terminal Medical Condition from a superannuation fund or insurer.

TPD Assist 15–66 You are actively employed1

Opt In IP 15–64 You are actively employed1 on a permanent basis for a minimum of 15 hours per week

• you are Self-Employed,2 or

• you are not employed, or

• you are a casual or contract employee3, or you are working less than 15 hours per week, or

• you are employed under a work visa,3 or

• you have previously received or are eligible to receive a Terminal Illness benefit, TPD benefit, or a benefit as a result of Permanent Incapacity or a Terminal Medical Condition from a superannuation fund or insurer.

1 You will be actively employed if you satisfy the At Work definition at the date your Death, TPD Assist and Opt In IP cover starts – refer to 10 Definitions for the At Work definition.

2 Self-Employed means a person who is predominantly working in their own business on a regular basis and earning an income – refer to 10 Definitions for the definition of Self-Employed Person.

3 Casuals, contractors and members employed under a work visa may apply for Tailored IP – refer to 6 Income Protection cover.

p8 p9

Other important eligibility terms and conditions

Death and TPD• As a general rule, your eligibility for Death and TPD Assist or

White Collar cover will not be assessed until you make a claim.

• Limited Cover will apply until you satisfy the At Work requirements for 30 consecutive days where you have joined Sunsuper and a Superannuation Guarantee (SG) contribution is received within 120 days of the date you joined your employer.

• Where you joined Sunsuper and an SG contribution is received more than 120 days after the date you joined your employer Limited Cover will apply to your cover for a period of 24 months and will cease to apply once you satisfy the At Work requirements for 30 consecutive days after the end of the 24 month period.

• If you become totally and permanently disabled you will only be eligible to make a TPD claim if you notify Sunsuper of your TPD claim within five years from your Date of Disablement. Warning: If you notify Sunsuper of your TPD claim outside this period you will be ineligible for an insurance benefit payment under TPD.

• If you were under age 15 when you joined Sunsuper, your Death and TPD Assist cover will commence upon receipt of an SG contribution after you turn age 15.

• If your insurance cover start date is more than 120 days from the date you joined your employer or you have White Collar cover, New Member Options or Life and Age Events, a Death or TPD Assist benefit will not be paid where Death or Total and Permanent Disablement is caused by suicide or any intentional self-inflicted act within 12 months of your insurance cover start date.

• If you have Tailored Death or TPD cover a benefit will not be paid where Death or Total and Permanent Disablement is caused by suicide or any intentional self-inflicted act within 12 months of your insurance cover start date.

• Members whose financial affairs are under the supervision of a third party due to their medical condition or incapacity, such as a Public Trustee Office, are entitled to Death only cover subject to satisfying the At Work requirements. Members not satisfying the At Work requirements will not be eligible for Death or TPD Assist cover. They will also not be able to apply for New Member options, Life and Age Event options or for White Collar cover.

• If you ceased employment with your employer due to sickness or injury Death and TPD cover transferred from either Sunsuper for life Corporate or Sunsuper for life Business will be Limited Cover. Limited Cover will apply until you have been At Work for 30 consecutive days.

Income Protection• As a general rule, your eligibility for Opt In IP or White Collar IP

cover will not be assessed until you make a claim.

• If you have Opt In IP or White Collar IP cover, Limited Cover will apply for the first 24 months and will apply until you satisfy the At Work requirements for 30 consecutive days after the initial 24 month period.

• An Income Protection benefit will not be paid if the injury or sickness is caused, wholly or partly, directly or indirectly, from:

a. deliberate self-inflicted injury, or attempted suicide, or self destruction while sane or insane,

b. uncomplicated pregnancy, childbirth or miscarriage,

c. your deployment to a hostile environment as part of active military service,

d. a criminal act committed by you, or

e. a fraudulent claim is made.

• You are not eligible for Opt In IP or White Collar IP cover if your financial affairs are under the supervision of a third party such as the Public Trustee Office, due to your medical condition or incapacity.

Not eligible for coverIf you are not eligible for Death and TPD Assist or Opt In IP cover you can apply for Tailored cover. Any application will be subject to acceptance by the insurer (satisfactory evidence of health will be required).

To avoid being charged premiums for cover that you are ineligible for, please ensure that you notify us if you are ineligible, or contact us if you would like to discuss whether you are eligible for Death and TPD Assist cover or Opt In IP cover. Premiums paid for the period you were deemed ineligible for cover will be refunded to your Super-savings account.

Premiums will not be refunded in the instance you are ineligible to claim a TPD Assist or Tailored TPD claim due to Sunsuper not being notified of a TPD claim within five years from your Date of Disablement.

Self-Employed, unemployed or unpaid Domestic DutiesIf you are Self-Employed, unemployed or are engaged in unpaid Domestic Duties in your own home you are eligible to apply for Tailored cover.

Special offersSome members may have other insurance offers made to them from time to time or you may be part of a group transfer from another fund. Your insurance arrangements and eligibility may differ from those contained in this guide. You will be advised if this applies to you.

When does my insurance cover start?

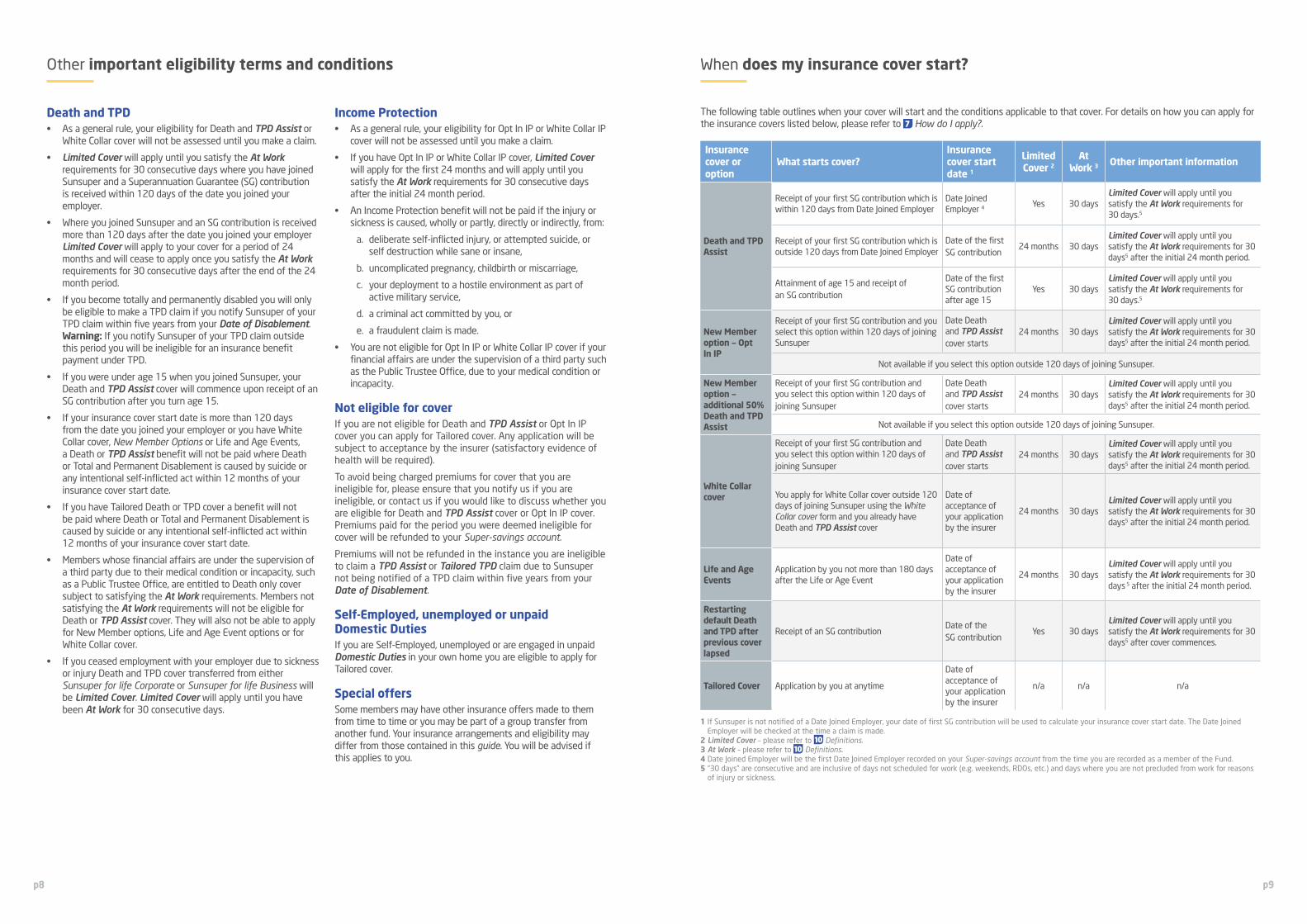

The following table outlines when your cover will start and the conditions applicable to that cover. For details on how you can apply for the insurance covers listed below, please refer to 7 How do I apply?.

Insurance cover or option

What starts cover?Insurance cover start date 1

Limited Cover 2

At Work 3 Other important information

Death and TPD Assist

Receipt of your first SG contribution which is within 120 days from Date Joined Employer

Date Joined Employer 4 Yes 30 days

Limited Cover will apply until you satisfy the At Work requirements for 30 days.5

Receipt of your first SG contribution which is outside 120 days from Date Joined Employer

Date of the first SG contribution

24 months 30 daysLimited Cover will apply until you satisfy the At Work requirements for 30 days5 after the initial 24 month period.

Attainment of age 15 and receipt of an SG contribution

Date of the first SG contribution after age 15

Yes 30 daysLimited Cover will apply until you satisfy the At Work requirements for 30 days.5

New Member option — Opt In IP

Receipt of your first SG contribution and you select this option within 120 days of joining Sunsuper

Date Death and TPD Assist cover starts

24 months 30 daysLimited Cover will apply until you satisfy the At Work requirements for 30 days5 after the initial 24 month period.

Not available if you select this option outside 120 days of joining Sunsuper.

New Member option — additional 50% Death and TPD Assist

Receipt of your first SG contribution and you select this option within 120 days of joining Sunsuper

Date Death and TPD Assist cover starts

24 months 30 daysLimited Cover will apply until you satisfy the At Work requirements for 30 days5 after the initial 24 month period.

Not available if you select this option outside 120 days of joining Sunsuper.

White Collar cover

Receipt of your first SG contribution and you select this option within 120 days of joining Sunsuper

Date Death and TPD Assist cover starts

24 months 30 daysLimited Cover will apply until you satisfy the At Work requirements for 30 days5 after the initial 24 month period.

You apply for White Collar cover outside 120 days of joining Sunsuper using the White Collar cover form and you already have Death and TPD Assist cover

Date of acceptance of your application by the insurer

24 months 30 daysLimited Cover will apply until you satisfy the At Work requirements for 30 days5 after the initial 24 month period.

Life and Age Events

Application by you not more than 180 days after the Life or Age Event

Date of acceptance of your application by the insurer

24 months 30 daysLimited Cover will apply until you satisfy the At Work requirements for 30 days 5 after the initial 24 month period.

Restarting default Death and TPD after previous cover lapsed

Receipt of an SG contributionDate of the SG contribution

Yes 30 days Limited Cover will apply until you satisfy the At Work requirements for 30 days5 after cover commences.

Tailored Cover Application by you at anytime

Date of acceptance of your application by the insurer

n/a n/a n/a

1 If Sunsuper is not notified of a Date Joined Employer, your date of first SG contribution will be used to calculate your insurance cover start date. The Date Joined Employer will be checked at the time a claim is made.

2 Limited Cover – please refer to 10 Definitions.3 At Work – please refer to 10 Definitions. 4 Date Joined Employer will be the first Date Joined Employer recorded on your Super-savings account from the time you are recorded as a member of the Fund. 5 “30 days” are consecutive and are inclusive of days not scheduled for work (e.g. weekends, RDOs, etc.) and days where you are not precluded from work for reasons

of injury or sickness.

p10 p11

5 Death and TPD cover

Death and TPD Assist

If you die your dependants or your beneficiaries may receive a lump sum. If you become Totally and Permanently Disabled (TPD) you may receive a benefit to help you pay any debts and bills and fund disability related expenses such as home modifications, rehabilitation, and special medical needs.

Death coverIf you die, your dependants or beneficiaries may receive a lump sum. This includes Terminal Illness.

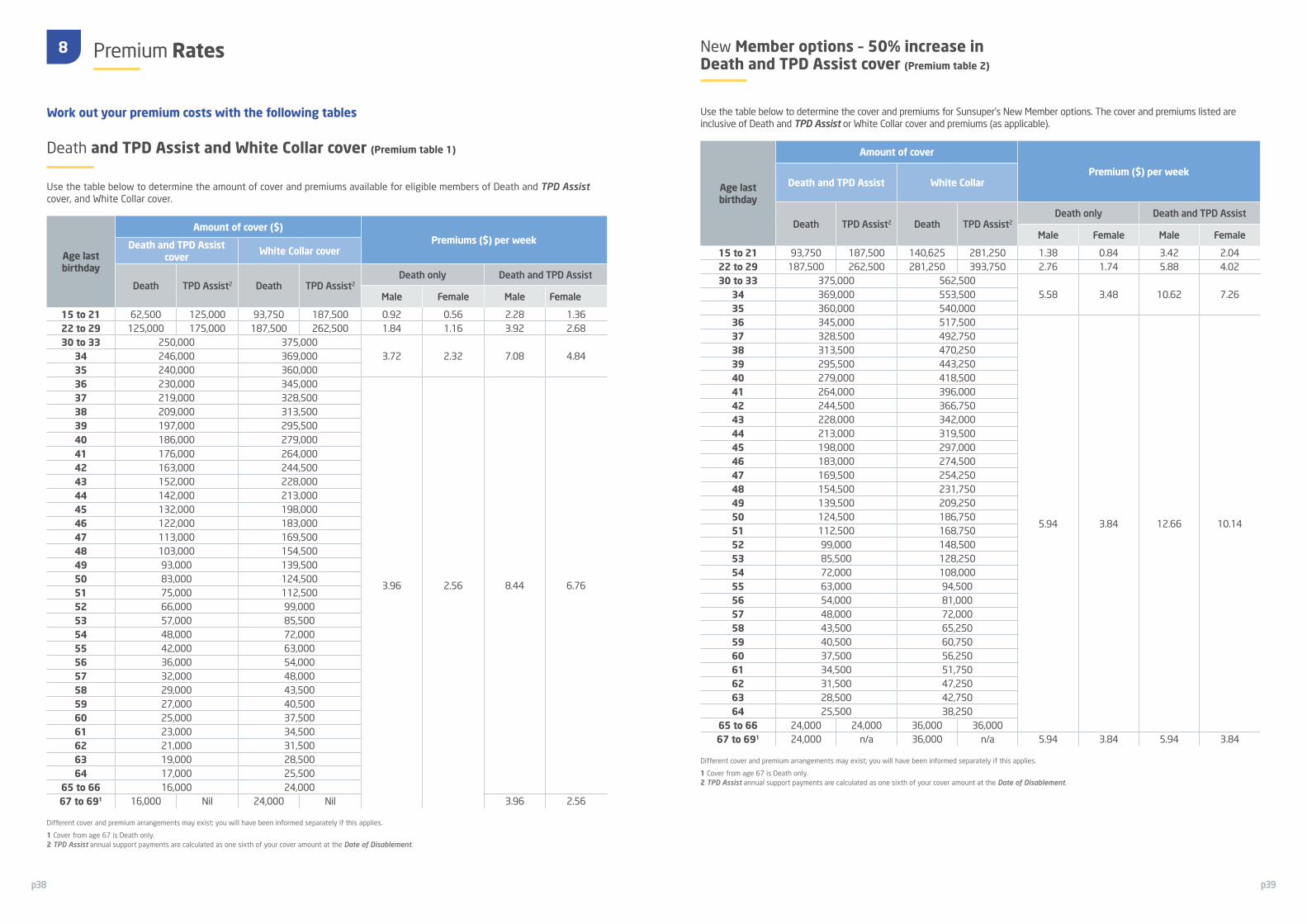

How much cover do you get and what does it cost?The amount and cost of cover depends on your age and type of cover and will alter at certain ages.

Death and TPD Assist cover levels (example)

Your age

Cover ($) Cost per Week ($)

Death TPD Assist Male Female

15 62,500 125,000 2.28 1.36

25 125,000 175,000 3.92 2.68

35 240,000 240,000 7.08 4.84

45 132,000 132,000 8.44 6.76

55 42,000 42,000 8.44 6.76

65 16,000 16,000 8.44 6.76

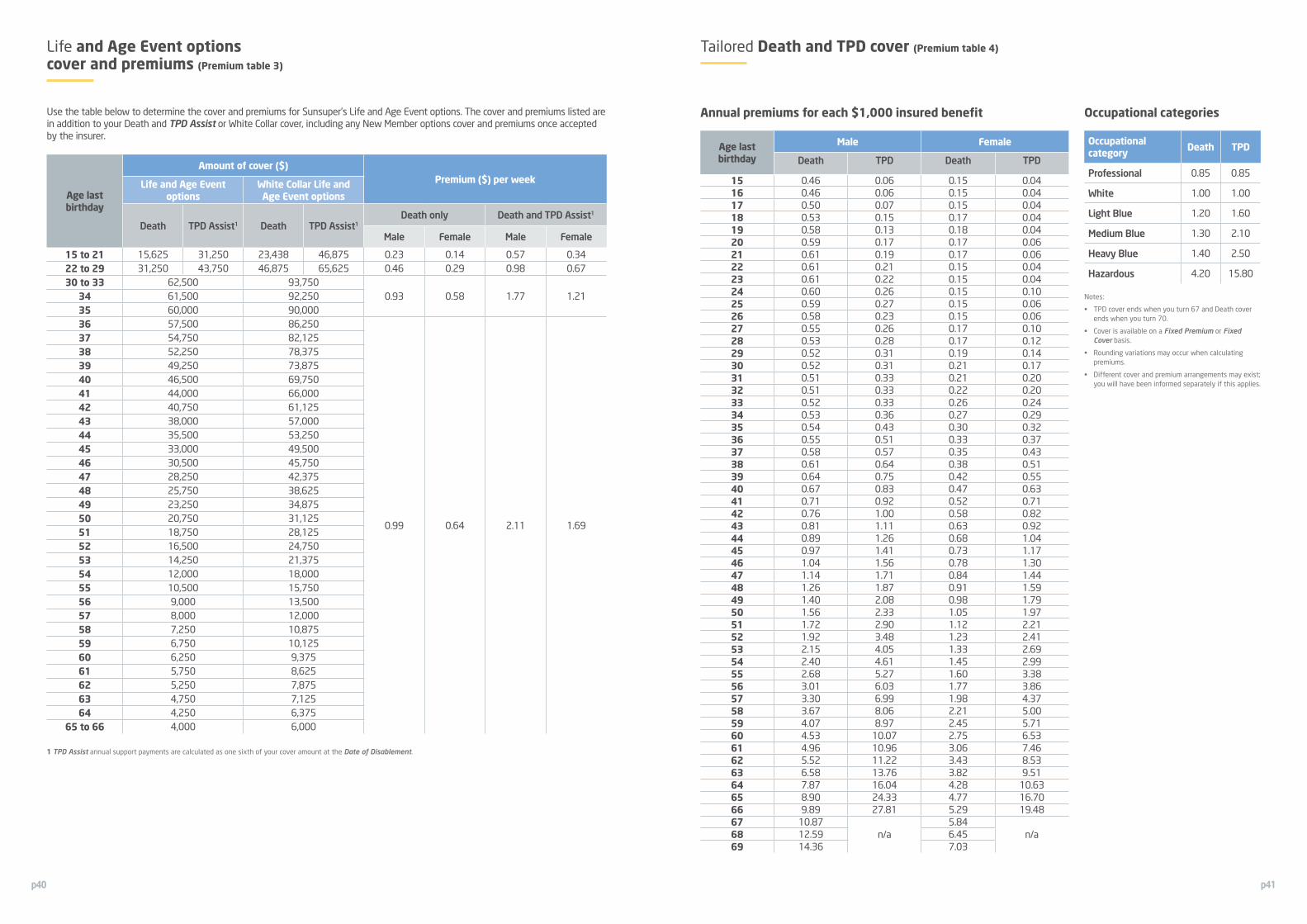

To find out which level of cover and premium applies to you take a look at Premium table 1. TPD Assist cover ends at age 67.

Premiums are calculated weekly and normally deducted from your Super-savings account each month so it doesn’t impact your take-home pay.

Will my cover change as I get older? Yes, the amount and cost of cover will generally alter at certain ages.

We will confirm your cover each year in your Annual statement. To confirm your cover amount at any time just visit Member Online, the Sunsuper app or call us on 13 11 84.

TPD AssistIf you are permanently disabled, you may receive occupational rehabilitation support and up to six annual support payments or in some circumstances a lump sum payment.

Exclusions and restrictionsA Death, TPD or Terminal Illness benefit will not be paid:

• where caused by suicide or any intentional self-inflicted act within 12 months of your insurance cover start date where it is more than 120 days after the date you joined your employer,

• where you become TPD and notify Sunsuper of a claim more than five years after your Date of Disablement,

• if you are deployed to a hostile environment as part of active military service,

• if you are employed under the terms of a work visa and it expires, or you permanently depart Australia (whichever is earlier),

• if benefits have ceased after a second TPD Assist claim period, or• prior to joining Sunsuper you had received a Terminal Illness

benefit, TPD benefit or a benefit as a result of Permanent Incapacity or a Terminal Medical Condition.

If your insurance cover start date is within 120 days of the date you joined your employer, Limited Cover will apply until you have been At Work for 30 consecutive days.

Limited Cover will also apply to your Death and TPD Assist cover where your insurance cover start date is more than 120 days after the date you joined your Employer. Limited Cover will be for a period of 24 months and until you having been At Work for 30 consecutive days after the end of the 24 month period. Please refer to the definition of Limited Cover and At Work in 10 Definitions.

What is TPD Assist cover? At Sunsuper we recognise the importance of supporting members who are sick or injured, and where appropriate, providing assistance in enabling them to return to work where they are able to. Sunsuper’s TPD Assist cover is here to help minimise the impacts of long term injury or sickness that leaves you unable to ever work again.

The road to recovery can be a difficult path both financially and emotionally. As your ability to earn a living is the cornerstone to your standard of living it’s important to regain your capability to earn a living. Where permanent disablement prevents this, it’s important to have a safety net in place.

The term ‘totally and permanently disabled’ generally means that you will be unable to ever work again in any occupation for which you are suited by training, education or experience. If your TPD claim is accepted, you are usually able to withdraw your superannuation account balance and either begin to receive your insured benefit as annual support payments, or receive it as a one-off lump sum, allowing you to pay debts or bills, provide an ongoing income or fund your special medical needs.

Sunsuper’s TPD Assist cover provides several unique features:

• no waiting period – with TPD Assist cover there is no waiting period, with the exception of Part C of the definition relating to Activities and Part A relating to Cognitive Function. If you’re employed, assistance within the first three months of your injury or sickness is essential in successful occupational rehabilitation. Not having a waiting period also avoids any delays where a specified Medical Condition or loss of limb has occurred,

• rehabilitation and retraining – provides occupational rehabilitation support and guidance where deemed appropriate, and may be a compulsory part of the claims process. Our occupational rehabilitation consultants will collaboratively work with you, your treating health professionals, rehabilitation provider and employer to assist you in returning to work,

• annual support payments or lump sum payment – if you are assessed as TPD your insured cover may be paid as annual support payments as long as you continue to meet the TPD Assist definition. If you are diagnosed with a specific long term debilitating injury or sickness (specified Medical Conditions) with no chance of recovery, suffer loss of limbs or loss of Cognitive Function or are unable to undertake specified Activities, your insured cover may be paid as a single lump sum payment following the initial assessment,

• no premium required – while on a TPD Assist claim you don’t have to worry about paying your Death and TPD Assist premiums.

The definition of TPD Assist you will be assessed against in the event of a claim is linked to your employment status immediately prior to the Date of Disablement.

In limited circumstances you will not be eligible to claim on the Death and TPD Assist insurance cover through Sunsuper. See 4 Am I eligible for insurance cover? and 10 Definitions for the Employed (TPD) definition.

What happens if you believe you are totally and permanently disabled? If you believe that you may be eligible to apply for a TPD Assist claim, we are here to help you along the way.

In order to lodge a claim you would need to be under the care of a Medical Practitioner and suffering from an ongoing and serious injury or sickness that is permanently preventing you from working or from performing specified Activities. See 10 Definitions for the TPD Assist definition.

Our Claims Representatives are here to help you every step of the way and will confirm your eligibility to lodge a claim. Following lodgement of your claim application, the insurer will assess whether your claim is successful and whether occupational rehabilitation services would assist you in a successful return to work.

Eligibility to claimIf you become totally and permanently disabled you will only be eligible to make a TPD claim if you notify Sunsuper of your TPD Assist claim within five years from your Date of Disablement. Warning: If you notify Sunsuper of your TPD Assist claim outside this period you will be ineligible for an insurance benefit payment under TPD Assist.

Early Intervention and occupational rehabilitationYour chances of a swift recovery and making a successful return to work are significantly improved if you have access to effective rehabilitation and support services. The sooner you are able to seek assistance from a health professional the higher the chance of a successful outcome.

The approach we take will be dependent on your injury or sickness and whether rehabilitation is appropriate. For complex illnesses such as Depression, Anxiety, Back Pain and Musculoskeletal injuries early assistance can prove invaluable. Early assistance for certain illnesses such as Stroke or Cancer may not be appropriate.

Where deemed appropriate, we will engage with our insurer who will help determine what, if any, occupational rehabilitation and retraining services will assist. Occupational rehabilitation may be a compulsory part of the claims process (where you are assessed against Part B of the TPD Assist definition).

White collar coverWhite collar cover entitles you to 50% more Death and TPD Assist cover at no additional cost to you. Refer to page 16 for more details.

Death and TPD Assist Cover is provided to eligible members, without needing to undergo any medical examinations.

p12 p13

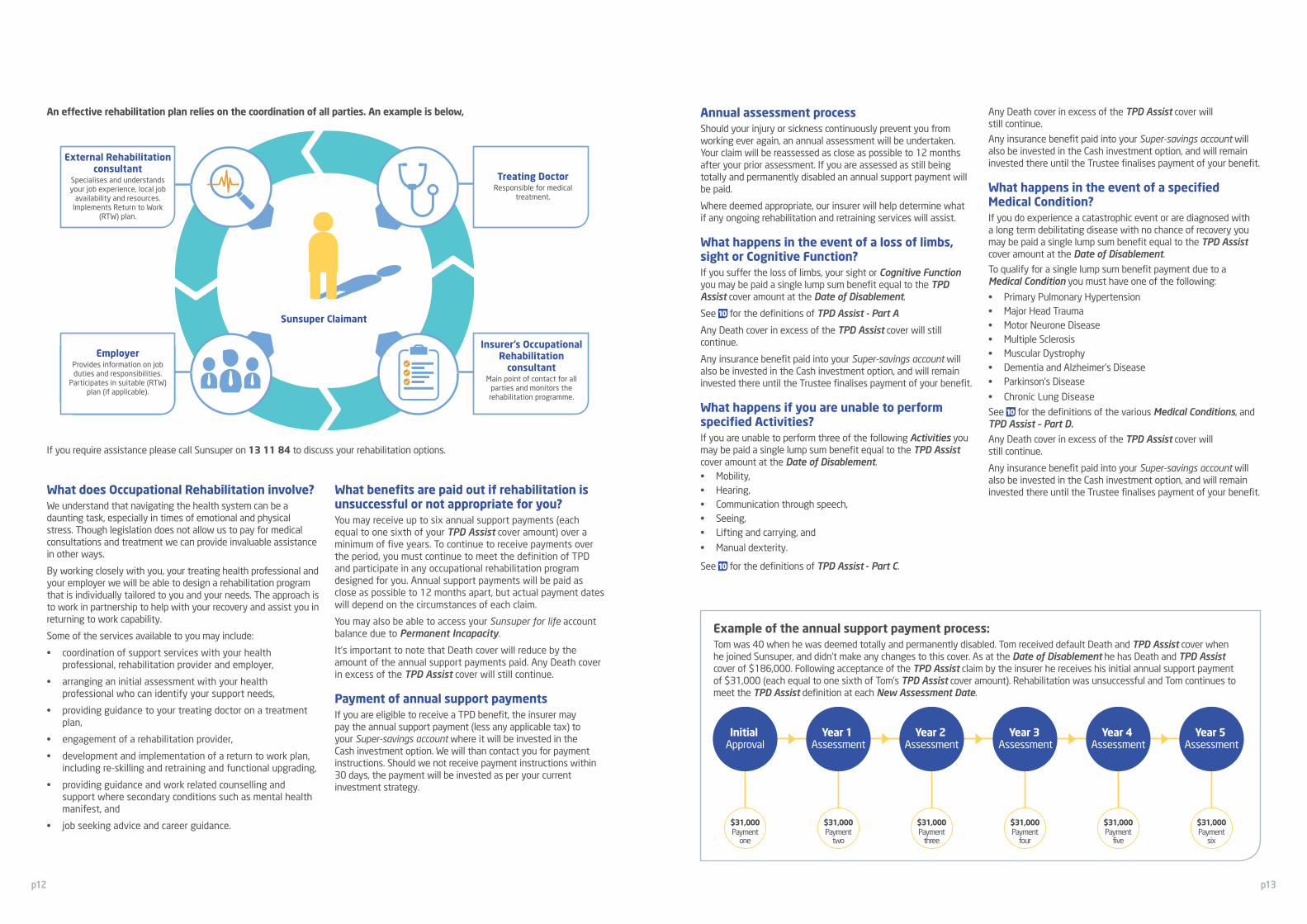

What does Occupational Rehabilitation involve?We understand that navigating the health system can be a daunting task, especially in times of emotional and physical stress. Though legislation does not allow us to pay for medical consultations and treatment we can provide invaluable assistance in other ways.

By working closely with you, your treating health professional and your employer we will be able to design a rehabilitation program that is individually tailored to you and your needs. The approach is to work in partnership to help with your recovery and assist you in returning to work capability.

Some of the services available to you may include:

• coordination of support services with your health professional, rehabilitation provider and employer,

• arranging an initial assessment with your health professional who can identify your support needs,

• providing guidance to your treating doctor on a treatment plan,

• engagement of a rehabilitation provider,

• development and implementation of a return to work plan, including re-skilling and retraining and functional upgrading,

• providing guidance and work related counselling and support where secondary conditions such as mental health manifest, and

• job seeking advice and career guidance.

Insurer’s Occupational Rehabilitation

consultantMain point of contact for all

parties and monitors the rehabilitation programme.

Treating DoctorResponsible for medical

treatment.

External Rehabilitation consultant

Specialises and understands your job experience, local job

availability and resources.Implements Return to Work

(RTW) plan.

Sunsuper Claimant

EmployerProvides information on job duties and responsibilities.

Participates in suitable (RTW) plan (if applicable).

An effective rehabilitation plan relies on the coordination of all parties. An example is below,

If you require assistance please call Sunsuper on 13 11 84 to discuss your rehabilitation options.

What benefits are paid out if rehabilitation is unsuccessful or not appropriate for you?You may receive up to six annual support payments (each equal to one sixth of your TPD Assist cover amount) over a minimum of five years. To continue to receive payments over the period, you must continue to meet the definition of TPD and participate in any occupational rehabilitation program designed for you. Annual support payments will be paid as close as possible to 12 months apart, but actual payment dates will depend on the circumstances of each claim.

You may also be able to access your Sunsuper for life account balance due to Permanent Incapacity.

It’s important to note that Death cover will reduce by the amount of the annual support payments paid. Any Death cover in excess of the TPD Assist cover will still continue.

Payment of annual support paymentsIf you are eligible to receive a TPD benefit, the insurer may pay the annual support payment (less any applicable tax) to your Super-savings account where it will be invested in the Cash investment option. We will than contact you for payment instructions. Should we not receive payment instructions within 30 days, the payment will be invested as per your current investment strategy.

Annual assessment processShould your injury or sickness continuously prevent you from working ever again, an annual assessment will be undertaken. Your claim will be reassessed as close as possible to 12 months after your prior assessment. If you are assessed as still being totally and permanently disabled an annual support payment will be paid.

Where deemed appropriate, our insurer will help determine what if any ongoing rehabilitation and retraining services will assist.

What happens in the event of a loss of limbs, sight or Cognitive Function?If you suffer the loss of limbs, your sight or Cognitive Function you may be paid a single lump sum benefit equal to the TPD Assist cover amount at the Date of Disablement.

See 10 for the definitions of TPD Assist - Part A

Any Death cover in excess of the TPD Assist cover will still continue.

Any insurance benefit paid into your Super-savings account will also be invested in the Cash investment option, and will remain invested there until the Trustee finalises payment of your benefit.

What happens if you are unable to perform specified Activities?If you are unable to perform three of the following Activities you may be paid a single lump sum benefit equal to the TPD Assist cover amount at the Date of Disablement. • Mobility,• Hearing,• Communication through speech,• Seeing,• Lifting and carrying, and

• Manual dexterity.

See 10 for the definitions of TPD Assist - Part C.

Any Death cover in excess of the TPD Assist cover will still continue.

Any insurance benefit paid into your Super-savings account will also be invested in the Cash investment option, and will remain invested there until the Trustee finalises payment of your benefit.

What happens in the event of a specified Medical Condition?If you do experience a catastrophic event or are diagnosed with a long term debilitating disease with no chance of recovery you may be paid a single lump sum benefit equal to the TPD Assist cover amount at the Date of Disablement.

To qualify for a single lump sum benefit payment due to a Medical Condition you must have one of the following:

• Primary Pulmonary Hypertension• Major Head Trauma• Motor Neurone Disease• Multiple Sclerosis• Muscular Dystrophy• Dementia and Alzheimer’s Disease• Parkinson’s Disease

• Chronic Lung Disease

See 10 for the definitions of the various Medical Conditions, and TPD Assist – Part D.

Any Death cover in excess of the TPD Assist cover will still continue.

Any insurance benefit paid into your Super-savings account will also be invested in the Cash investment option, and will remain invested there until the Trustee finalises payment of your benefit.

Example of the annual support payment process:Tom was 40 when he was deemed totally and permanently disabled. Tom received default Death and TPD Assist cover when he joined Sunsuper, and didn’t make any changes to this cover. As at the Date of Disablement he has Death and TPD Assist cover of $186,000. Following acceptance of the TPD Assist claim by the insurer he receives his initial annual support payment of $31,000 (each equal to one sixth of Tom’s TPD Assist cover amount). Rehabilitation was unsuccessful and Tom continues to meet the TPD Assist definition at each New Assessment Date.

Paymentsix

Paymentfive

Paymentfour

Initial Approval

Year 1 Assessment

Year 2 Assessment

Year 3 Assessment

Year 4 Assessment

Paymentthree

Paymenttwo

$31,000 $31,000 $31,000 $31,000 $31,000 $31,000Payment

one

Year 5 Assessment

p14 p15

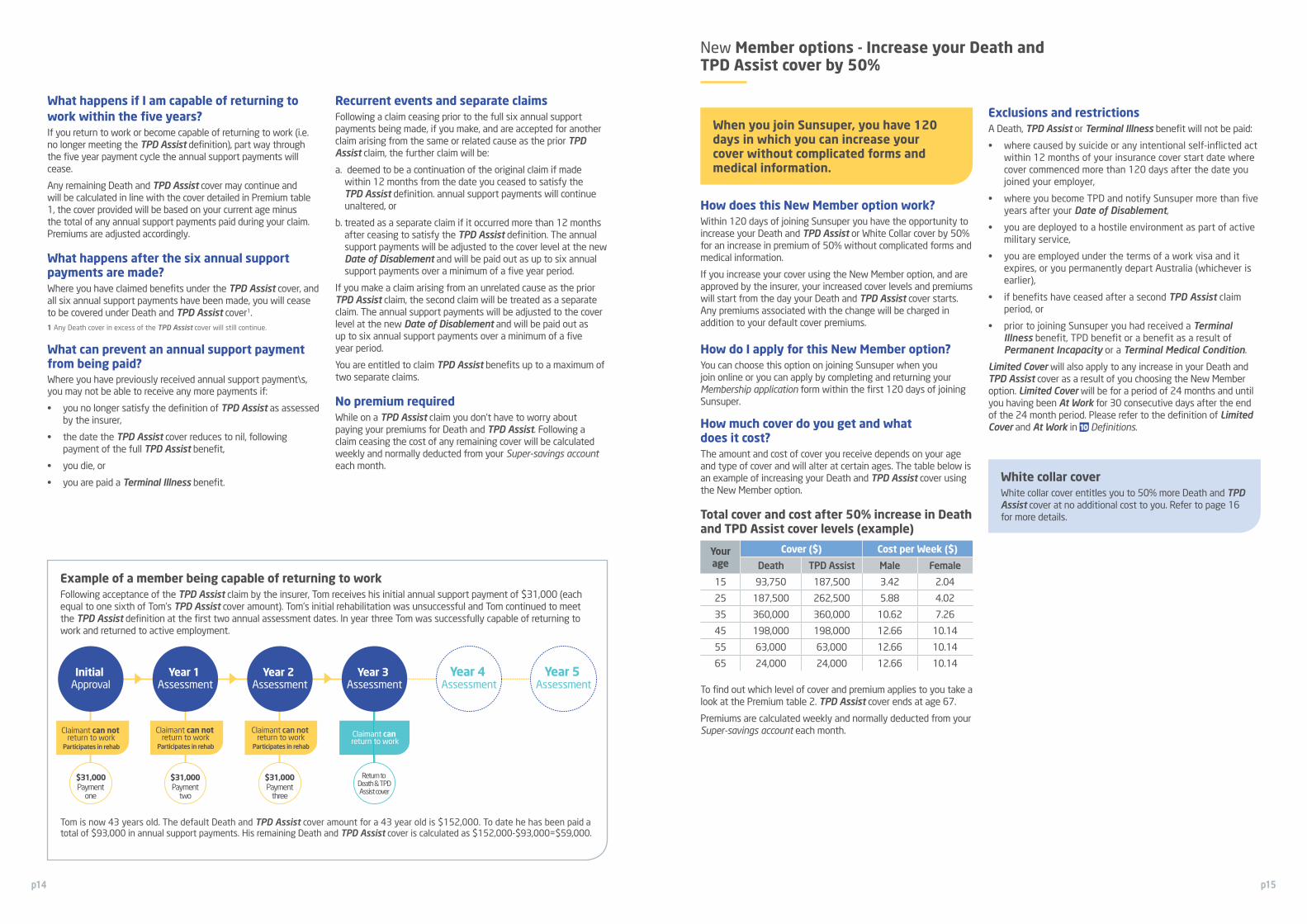

Example of a member being capable of returning to workFollowing acceptance of the TPD Assist claim by the insurer, Tom receives his initial annual support payment of $31,000 (each equal to one sixth of Tom’s TPD Assist cover amount). Tom’s initial rehabilitation was unsuccessful and Tom continued to meet the TPD Assist definition at the first two annual assessment dates. In year three Tom was successfully capable of returning to work and returned to active employment.

Tom is now 43 years old. The default Death and TPD Assist cover amount for a 43 year old is $152,000. To date he has been paid a total of $93,000 in annual support payments. His remaining Death and TPD Assist cover is calculated as $152,000-$93,000=$59,000.

Initial Approval

Year 1 Assessment

Year 2 Assessment

Year 3 Assessment

Year 4 Assessment

Claimant can not return to work

Participates in rehab

Claimant can return to work

Return to Death & TPDAssist coverPayment

threePayment

twoPayment

one

Year 5 Assessment

Claimant can not return to work

Participates in rehab

Claimant can not return to work

Participates in rehab

$31,000 $31,000 $31,000

What happens if I am capable of returning to work within the five years?If you return to work or become capable of returning to work (i.e. no longer meeting the TPD Assist definition), part way through the five year payment cycle the annual support payments will cease.

Any remaining Death and TPD Assist cover may continue and will be calculated in line with the cover detailed in Premium table 1, the cover provided will be based on your current age minus the total of any annual support payments paid during your claim. Premiums are adjusted accordingly.

What happens after the six annual support payments are made?Where you have claimed benefits under the TPD Assist cover, and all six annual support payments have been made, you will cease to be covered under Death and TPD Assist cover1.1 Any Death cover in excess of the TPD Assist cover will still continue.

What can prevent an annual support payment from being paid?Where you have previously received annual support payment\s, you may not be able to receive any more payments if:

• you no longer satisfy the definition of TPD Assist as assessed by the insurer,

• the date the TPD Assist cover reduces to nil, following payment of the full TPD Assist benefit,

• you die, or

• you are paid a Terminal Illness benefit.

Recurrent events and separate claimsFollowing a claim ceasing prior to the full six annual support payments being made, if you make, and are accepted for another claim arising from the same or related cause as the prior TPD Assist claim, the further claim will be:

a. deemed to be a continuation of the original claim if made within 12 months from the date you ceased to satisfy the TPD Assist definition. annual support payments will continue unaltered, or

b. treated as a separate claim if it occurred more than 12 months after ceasing to satisfy the TPD Assist definition. The annual support payments will be adjusted to the cover level at the new Date of Disablement and will be paid out as up to six annual support payments over a minimum of a five year period.

If you make a claim arising from an unrelated cause as the prior TPD Assist claim, the second claim will be treated as a separate claim. The annual support payments will be adjusted to the cover level at the new Date of Disablement and will be paid out as up to six annual support payments over a minimum of a five year period.

You are entitled to claim TPD Assist benefits up to a maximum of two separate claims.

No premium requiredWhile on a TPD Assist claim you don’t have to worry about paying your premiums for Death and TPD Assist. Following a claim ceasing the cost of any remaining cover will be calculated weekly and normally deducted from your Super-savings account each month.

New Member options - Increase your Death and TPD Assist cover by 50%

How does this New Member option work? Within 120 days of joining Sunsuper you have the opportunity to increase your Death and TPD Assist or White Collar cover by 50% for an increase in premium of 50% without complicated forms and medical information.

If you increase your cover using the New Member option, and are approved by the insurer, your increased cover levels and premiums will start from the day your Death and TPD Assist cover starts. Any premiums associated with the change will be charged in addition to your default cover premiums.

How do I apply for this New Member option? You can choose this option on joining Sunsuper when you join online or you can apply by completing and returning your Membership application form within the first 120 days of joining Sunsuper.

How much cover do you get and what does it cost? The amount and cost of cover you receive depends on your age and type of cover and will alter at certain ages. The table below is an example of increasing your Death and TPD Assist cover using the New Member option.

Total cover and cost after 50% increase in Death and TPD Assist cover levels (example)

Your age

Cover ($) Cost per Week ($)

Death TPD Assist Male Female

15 93,750 187,500 3.42 2.04

25 187,500 262,500 5.88 4.02

35 360,000 360,000 10.62 7.26

45 198,000 198,000 12.66 10.14

55 63,000 63,000 12.66 10.14

65 24,000 24,000 12.66 10.14

To find out which level of cover and premium applies to you take a look at the Premium table 2. TPD Assist cover ends at age 67.

Premiums are calculated weekly and normally deducted from your Super-savings account each month.

Exclusions and restrictionsA Death, TPD Assist or Terminal Illness benefit will not be paid:

• where caused by suicide or any intentional self-inflicted act within 12 months of your insurance cover start date where cover commenced more than 120 days after the date you joined your employer,

• where you become TPD and notify Sunsuper more than five years after your Date of Disablement,

• you are deployed to a hostile environment as part of active military service,

• you are employed under the terms of a work visa and it expires, or you permanently depart Australia (whichever is earlier),

• if benefits have ceased after a second TPD Assist claim period, or

• prior to joining Sunsuper you had received a Terminal Illness benefit, TPD benefit or a benefit as a result of Permanent Incapacity or a Terminal Medical Condition.

Limited Cover will also apply to any increase in your Death and TPD Assist cover as a result of you choosing the New Member option. Limited Cover will be for a period of 24 months and until you having been At Work for 30 consecutive days after the end of the 24 month period. Please refer to the definition of Limited Cover and At Work in 10 Definitions.

White collar coverWhite collar cover entitles you to 50% more Death and TPD Assist cover at no additional cost to you. Refer to page 16 for more details.

When you join Sunsuper, you have 120 days in which you can increase your cover without complicated forms and medical information.

p16 p17

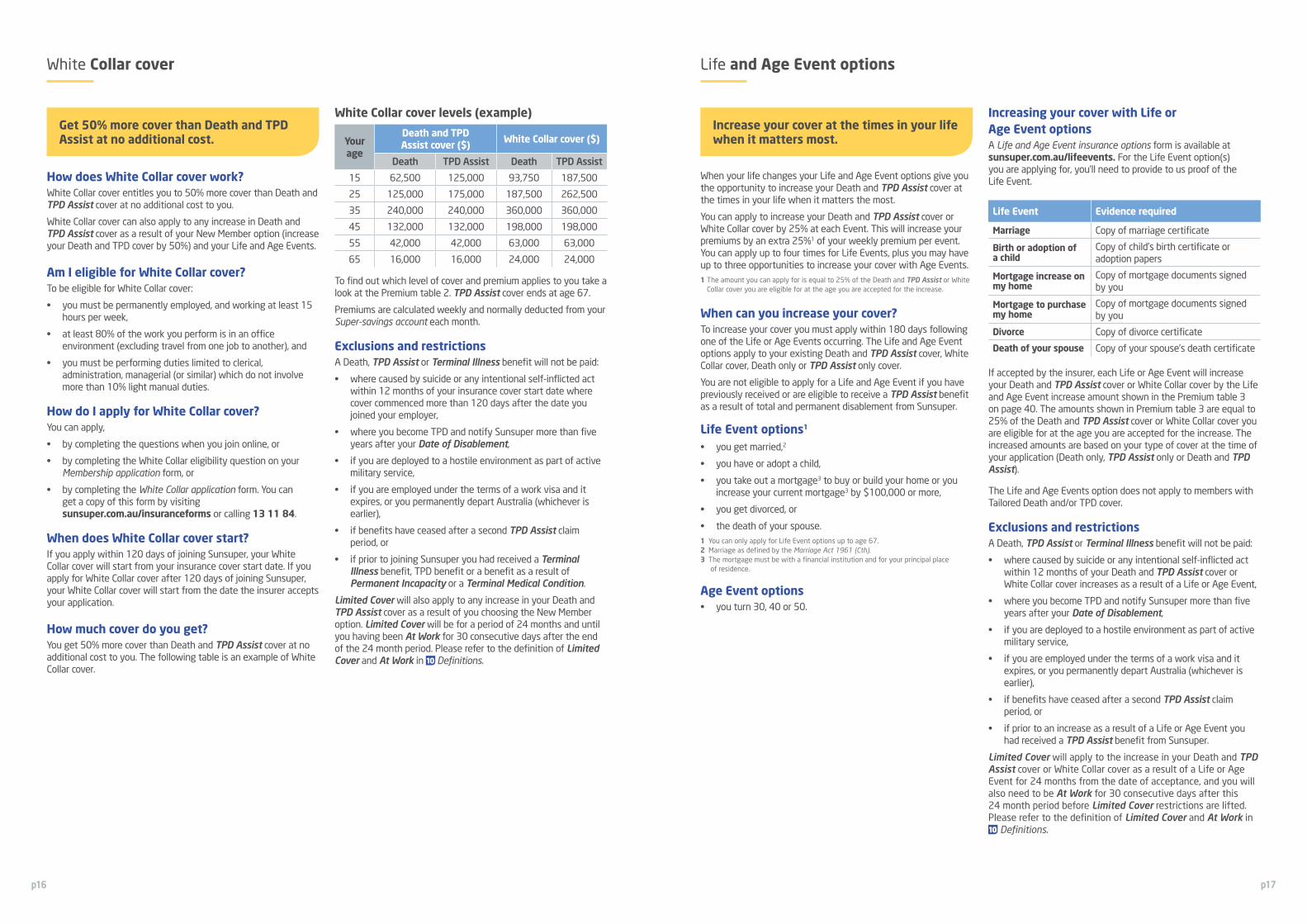

White Collar cover Life and Age Event options

How does White Collar cover work? White Collar cover entitles you to 50% more cover than Death and TPD Assist cover at no additional cost to you.

White Collar cover can also apply to any increase in Death and TPD Assist cover as a result of your New Member option (increase your Death and TPD cover by 50%) and your Life and Age Events.

Am I eligible for White Collar cover? To be eligible for White Collar cover:

• you must be permanently employed, and working at least 15 hours per week,

• at least 80% of the work you perform is in an office environment (excluding travel from one job to another), and

• you must be performing duties limited to clerical, administration, managerial (or similar) which do not involve more than 10% light manual duties.

How do I apply for White Collar cover?You can apply,

• by completing the questions when you join online, or

• by completing the White Collar eligibility question on your Membership application form, or

• by completing the White Collar application form. You can get a copy of this form by visiting sunsuper.com.au/insuranceforms or calling 13 11 84.

When does White Collar cover start? If you apply within 120 days of joining Sunsuper, your White Collar cover will start from your insurance cover start date. If you apply for White Collar cover after 120 days of joining Sunsuper, your White Collar cover will start from the date the insurer accepts your application.

How much cover do you get? You get 50% more cover than Death and TPD Assist cover at no additional cost to you. The following table is an example of White Collar cover.

White Collar cover levels (example)

Your age

Death and TPD Assist cover ($) White Collar cover ($)

Death TPD Assist Death TPD Assist

15 62,500 125,000 93,750 187,500

25 125,000 175,000 187,500 262,500

35 240,000 240,000 360,000 360,000

45 132,000 132,000 198,000 198,000

55 42,000 42,000 63,000 63,000

65 16,000 16,000 24,000 24,000

To find out which level of cover and premium applies to you take a look at the Premium table 2. TPD Assist cover ends at age 67.

Premiums are calculated weekly and normally deducted from your Super-savings account each month.

Exclusions and restrictionsA Death, TPD Assist or Terminal Illness benefit will not be paid:

• where caused by suicide or any intentional self-inflicted act within 12 months of your insurance cover start date where cover commenced more than 120 days after the date you joined your employer,

• where you become TPD and notify Sunsuper more than five years after your Date of Disablement,

• if you are deployed to a hostile environment as part of active military service,

• if you are employed under the terms of a work visa and it expires, or you permanently depart Australia (whichever is earlier),

• if benefits have ceased after a second TPD Assist claim period, or

• if prior to joining Sunsuper you had received a Terminal Illness benefit, TPD benefit or a benefit as a result of Permanent Incapacity or a Terminal Medical Condition.

Limited Cover will also apply to any increase in your Death and TPD Assist cover as a result of you choosing the New Member option. Limited Cover will be for a period of 24 months and until you having been At Work for 30 consecutive days after the end of the 24 month period. Please refer to the definition of Limited Cover and At Work in 10 Definitions.

When your life changes your Life and Age Event options give you the opportunity to increase your Death and TPD Assist cover at the times in your life when it matters the most.

You can apply to increase your Death and TPD Assist cover or White Collar cover by 25% at each Event. This will increase your premiums by an extra 25%1 of your weekly premium per event. You can apply up to four times for Life Events, plus you may have up to three opportunities to increase your cover with Age Events.1 The amount you can apply for is equal to 25% of the Death and TPD Assist or White

Collar cover you are eligible for at the age you are accepted for the increase.

When can you increase your cover? To increase your cover you must apply within 180 days following one of the Life or Age Events occurring. The Life and Age Event options apply to your existing Death and TPD Assist cover, White Collar cover, Death only or TPD Assist only cover.

You are not eligible to apply for a Life and Age Event if you have previously received or are eligible to receive a TPD Assist benefit as a result of total and permanent disablement from Sunsuper.

Life Event options1

• you get married,2

• you have or adopt a child,

• you take out a mortgage3 to buy or build your home or you increase your current mortgage3 by $100,000 or more,

• you get divorced, or

• the death of your spouse.1 You can only apply for Life Event options up to age 67. 2 Marriage as defined by the Marriage Act 1961 (Cth). 3 The mortgage must be with a financial institution and for your principal place

of residence.

Age Event options • you turn 30, 40 or 50.

Increasing your cover with Life or Age Event options A Life and Age Event insurance options form is available at sunsuper.com.au/lifeevents. For the Life Event option(s) you are applying for, you’ll need to provide to us proof of the Life Event.

Life Event Evidence required

Marriage Copy of marriage certificate

Birth or adoption of a child

Copy of child’s birth certificate or adoption papers

Mortgage increase on my home

Copy of mortgage documents signed by you

Mortgage to purchase my home

Copy of mortgage documents signed by you

Divorce Copy of divorce certificate

Death of your spouse Copy of your spouse’s death certificate

If accepted by the insurer, each Life or Age Event will increase your Death and TPD Assist cover or White Collar cover by the Life and Age Event increase amount shown in the Premium table 3 on page 40. The amounts shown in Premium table 3 are equal to 25% of the Death and TPD Assist cover or White Collar cover you are eligible for at the age you are accepted for the increase. The increased amounts are based on your type of cover at the time of your application (Death only, TPD Assist only or Death and TPD Assist).

The Life and Age Events option does not apply to members with Tailored Death and/or TPD cover.

Exclusions and restrictionsA Death, TPD Assist or Terminal Illness benefit will not be paid:

• where caused by suicide or any intentional self-inflicted act within 12 months of your Death and TPD Assist cover or White Collar cover increases as a result of a Life or Age Event,

• where you become TPD and notify Sunsuper more than five years after your Date of Disablement,

• if you are deployed to a hostile environment as part of active military service,

• if you are employed under the terms of a work visa and it expires, or you permanently depart Australia (whichever is earlier),

• if benefits have ceased after a second TPD Assist claim period, or

• if prior to an increase as a result of a Life or Age Event you had received a TPD Assist benefit from Sunsuper.

Limited Cover will apply to the increase in your Death and TPD Assist cover or White Collar cover as a result of a Life or Age Event for 24 months from the date of acceptance, and you will also need to be At Work for 30 consecutive days after this 24 month period before Limited Cover restrictions are lifted. Please refer to the definition of Limited Cover and At Work in 10 Definitions.

Get 50% more cover than Death and TPD Assist at no additional cost.

Increase your cover at the times in your life when it matters most.

p18 p19

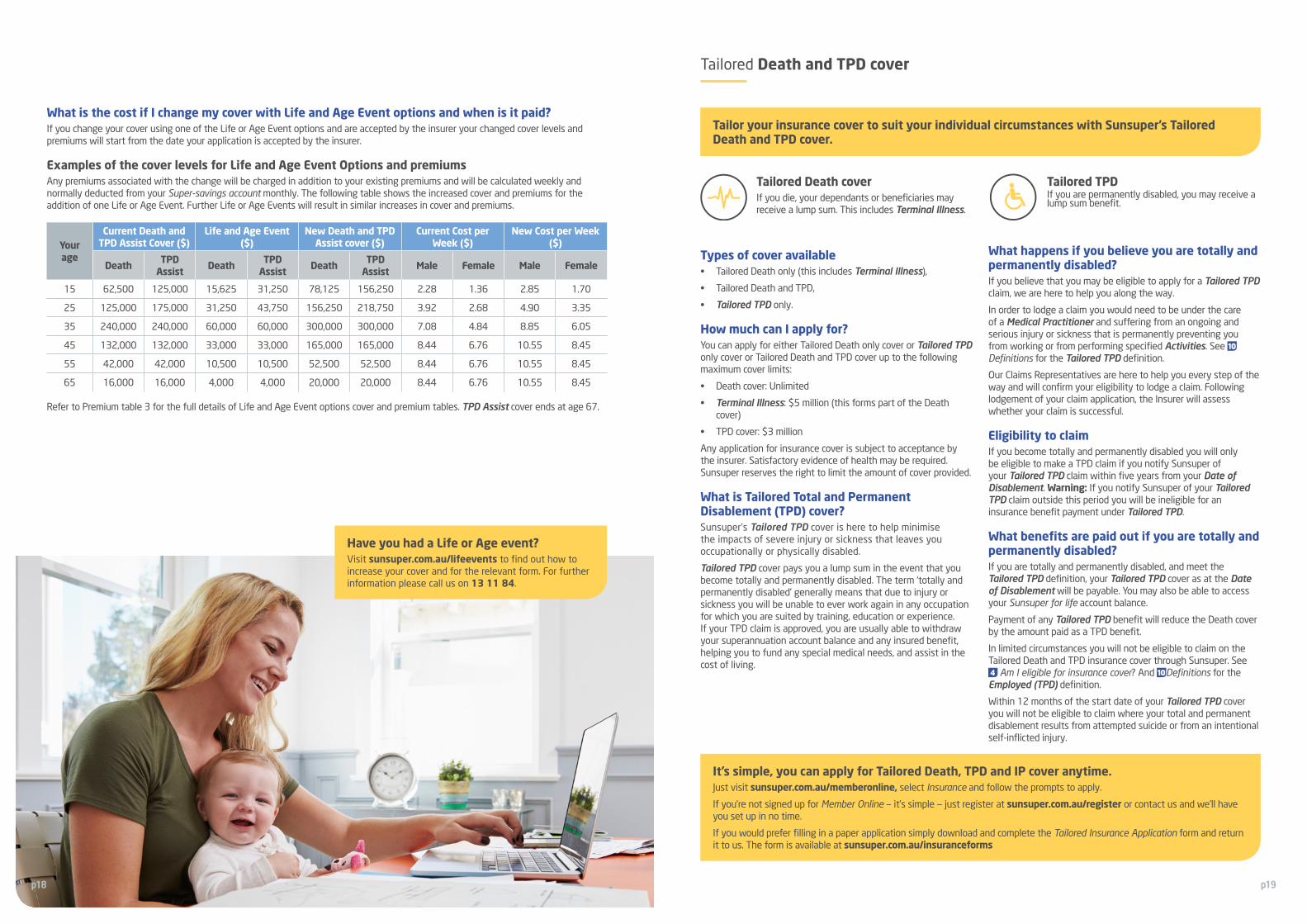

What is the cost if I change my cover with Life and Age Event options and when is it paid? If you change your cover using one of the Life or Age Event options and are accepted by the insurer your changed cover levels and premiums will start from the date your application is accepted by the insurer.

Examples of the cover levels for Life and Age Event Options and premiumsAny premiums associated with the change will be charged in addition to your existing premiums and will be calculated weekly and normally deducted from your Super-savings account monthly. The following table shows the increased cover and premiums for the addition of one Life or Age Event. Further Life or Age Events will result in similar increases in cover and premiums.

Your age

Current Death and TPD Assist Cover ($)

Life and Age Event ($)

New Death and TPD Assist cover ($)

Current Cost per Week ($)

New Cost per Week ($)

Death TPD Assist Death TPD

Assist Death TPD Assist Male Female Male Female

15 62,500 125,000 15,625 31,250 78,125 156,250 2.28 1.36 2.85 1.70

25 125,000 175,000 31,250 43,750 156,250 218,750 3.92 2.68 4.90 3.35

35 240,000 240,000 60,000 60,000 300,000 300,000 7.08 4.84 8.85 6.05

45 132,000 132,000 33,000 33,000 165,000 165,000 8.44 6.76 10.55 8.45

55 42,000 42,000 10,500 10,500 52,500 52,500 8.44 6.76 10.55 8.45

65 16,000 16,000 4,000 4,000 20,000 20,000 8.44 6.76 10.55 8.45

Refer to Premium table 3 for the full details of Life and Age Event options cover and premium tables. TPD Assist cover ends at age 67.

Have you had a Life or Age event?Visit sunsuper.com.au/lifeevents to find out how to increase your cover and for the relevant form. For further information please call us on 13 11 84.

Tailored Death and TPD cover

Tailored Death coverIf you die, your dependants or beneficiaries may receive a lump sum. This includes Terminal Illness.

Types of cover available • Tailored Death only (this includes Terminal Illness),

• Tailored Death and TPD,

• Tailored TPD only.

How much can I apply for?You can apply for either Tailored Death only cover or Tailored TPD only cover or Tailored Death and TPD cover up to the following maximum cover limits:

• Death cover: Unlimited

• Terminal Illness: $5 million (this forms part of the Death cover)

• TPD cover: $3 million

Any application for insurance cover is subject to acceptance by the insurer. Satisfactory evidence of health may be required. Sunsuper reserves the right to limit the amount of cover provided.

What is Tailored Total and Permanent Disablement (TPD) cover? Sunsuper’s Tailored TPD cover is here to help minimise the impacts of severe injury or sickness that leaves you occupationally or physically disabled.

Tailored TPD cover pays you a lump sum in the event that you become totally and permanently disabled. The term ‘totally and permanently disabled’ generally means that due to injury or sickness you will be unable to ever work again in any occupation for which you are suited by training, education or experience. If your TPD claim is approved, you are usually able to withdraw your superannuation account balance and any insured benefit, helping you to fund any special medical needs, and assist in the cost of living.

What happens if you believe you are totally and permanently disabled?If you believe that you may be eligible to apply for a Tailored TPD claim, we are here to help you along the way.

In order to lodge a claim you would need to be under the care of a Medical Practitioner and suffering from an ongoing and serious injury or sickness that is permanently preventing you from working or from performing specified Activities. See 10 Definitions for the Tailored TPD definition.

Our Claims Representatives are here to help you every step of the way and will confirm your eligibility to lodge a claim. Following lodgement of your claim application, the Insurer will assess whether your claim is successful.

Eligibility to claim If you become totally and permanently disabled you will only be eligible to make a TPD claim if you notify Sunsuper of your Tailored TPD claim within five years from your Date of Disablement. Warning: If you notify Sunsuper of your Tailored TPD claim outside this period you will be ineligible for an insurance benefit payment under Tailored TPD.

What benefits are paid out if you are totally and permanently disabled?If you are totally and permanently disabled, and meet the Tailored TPD definition, your Tailored TPD cover as at the Date of Disablement will be payable. You may also be able to access your Sunsuper for life account balance.

Payment of any Tailored TPD benefit will reduce the Death cover by the amount paid as a TPD benefit.

In limited circumstances you will not be eligible to claim on the Tailored Death and TPD insurance cover through Sunsuper. See 4 Am I eligible for insurance cover? And 10Definitions for the Employed (TPD) definition.

Within 12 months of the start date of your Tailored TPD cover you will not be eligible to claim where your total and permanent disablement results from attempted suicide or from an intentional self-inflicted injury.

Tailored TPDIf you are permanently disabled, you may receive a lump sum benefit.

It’s simple, you can apply for Tailored Death, TPD and IP cover anytime.Just visit sunsuper.com.au/memberonline, select Insurance and follow the prompts to apply.

If you’re not signed up for Member Online — it’s simple — just register at sunsuper.com.au/register or contact us and we’ll have you set up in no time.

If you would prefer filling in a paper application simply download and complete the Tailored Insurance Application form and return it to us. The form is available at sunsuper.com.au/insuranceforms

Tailor your insurance cover to suit your individual circumstances with Sunsuper’s Tailored Death and TPD cover.

p20 p21

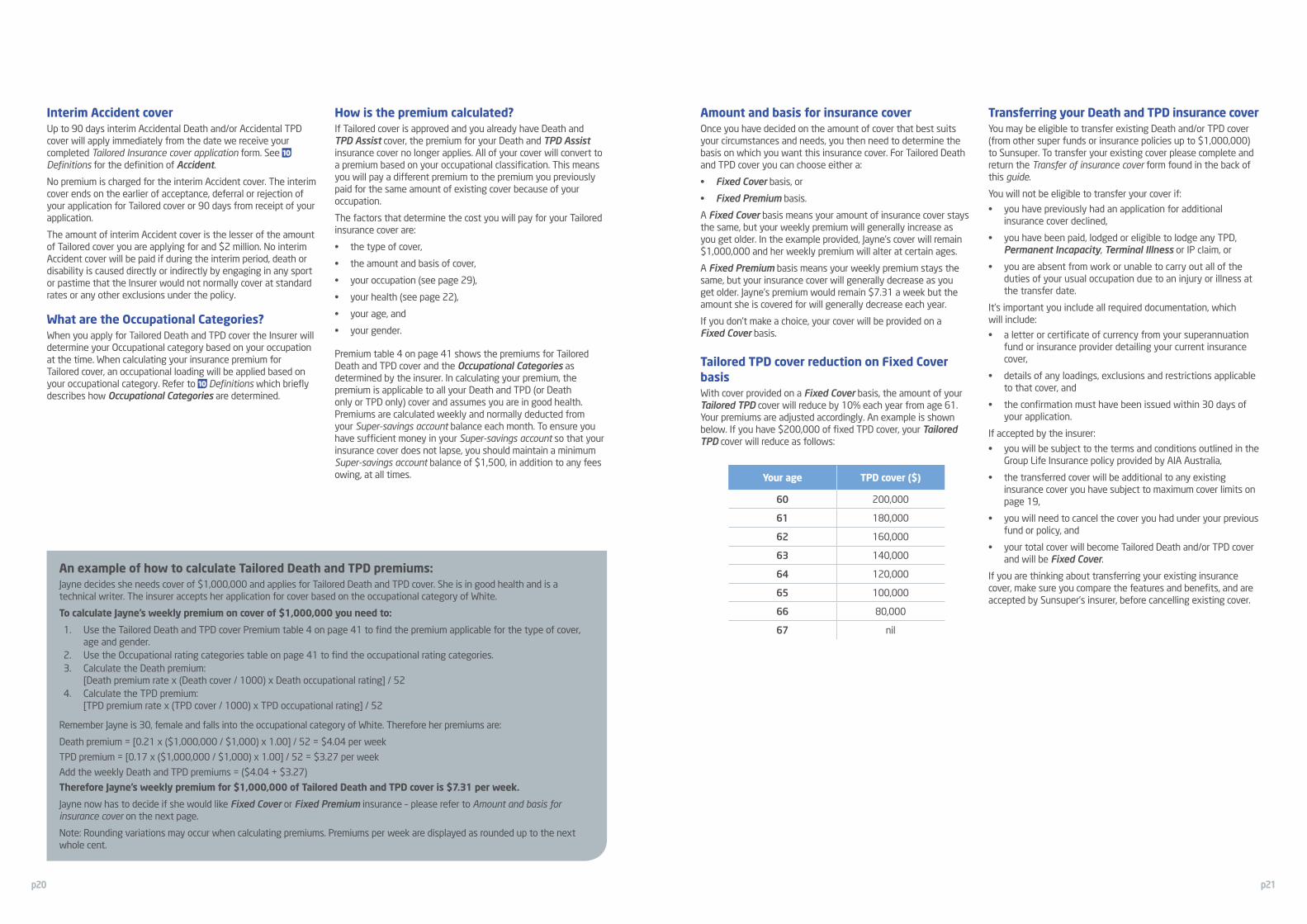

Interim Accident coverUp to 90 days interim Accidental Death and/or Accidental TPD cover will apply immediately from the date we receive your completed Tailored Insurance cover application form. See 10 Definitions for the definition of Accident.

No premium is charged for the interim Accident cover. The interim cover ends on the earlier of acceptance, deferral or rejection of your application for Tailored cover or 90 days from receipt of your application.

The amount of interim Accident cover is the lesser of the amount of Tailored cover you are applying for and $2 million. No interim Accident cover will be paid if during the interim period, death or disability is caused directly or indirectly by engaging in any sport or pastime that the Insurer would not normally cover at standard rates or any other exclusions under the policy.

What are the Occupational Categories?When you apply for Tailored Death and TPD cover the Insurer will determine your Occupational category based on your occupation at the time. When calculating your insurance premium for Tailored cover, an occupational loading will be applied based on your occupational category. Refer to 10 Definitions which briefly describes how Occupational Categories are determined.

How is the premium calculated?If Tailored cover is approved and you already have Death and TPD Assist cover, the premium for your Death and TPD Assist insurance cover no longer applies. All of your cover will convert to a premium based on your occupational classification. This means you will pay a different premium to the premium you previously paid for the same amount of existing cover because of your occupation.

The factors that determine the cost you will pay for your Tailored insurance cover are:

• the type of cover,

• the amount and basis of cover,

• your occupation (see page 29),

• your health (see page 22),

• your age, and

• your gender.

Premium table 4 on page 41 shows the premiums for Tailored Death and TPD cover and the Occupational Categories as determined by the insurer. In calculating your premium, the premium is applicable to all your Death and TPD (or Death only or TPD only) cover and assumes you are in good health. Premiums are calculated weekly and normally deducted from your Super-savings account balance each month. To ensure you have sufficient money in your Super-savings account so that your insurance cover does not lapse, you should maintain a minimum Super-savings account balance of $1,500, in addition to any fees owing, at all times.

An example of how to calculate Tailored Death and TPD premiums: Jayne decides she needs cover of $1,000,000 and applies for Tailored Death and TPD cover. She is in good health and is a technical writer. The insurer accepts her application for cover based on the occupational category of White.

To calculate Jayne’s weekly premium on cover of $1,000,000 you need to:

1. Use the Tailored Death and TPD cover Premium table 4 on page 41 to find the premium applicable for the type of cover, age and gender.

2. Use the Occupational rating categories table on page 41 to find the occupational rating categories.3. Calculate the Death premium:

[Death premium rate x (Death cover / 1000) x Death occupational rating] / 52 4. Calculate the TPD premium:

[TPD premium rate x (TPD cover / 1000) x TPD occupational rating] / 52

Remember Jayne is 30, female and falls into the occupational category of White. Therefore her premiums are:

Death premium = [0.21 x ($1,000,000 / $1,000) x 1.00] / 52 = $4.04 per week

TPD premium = [0.17 x ($1,000,000 / $1,000) x 1.00] / 52 = $3.27 per week

Add the weekly Death and TPD premiums = ($4.04 + $3.27)

Therefore Jayne’s weekly premium for $1,000,000 of Tailored Death and TPD cover is $7.31 per week.

Jayne now has to decide if she would like Fixed Cover or Fixed Premium insurance – please refer to Amount and basis for insurance cover on the next page.

Note: Rounding variations may occur when calculating premiums. Premiums per week are displayed as rounded up to the next whole cent.

Amount and basis for insurance coverOnce you have decided on the amount of cover that best suits your circumstances and needs, you then need to determine the basis on which you want this insurance cover. For Tailored Death and TPD cover you can choose either a:

• Fixed Cover basis, or

• Fixed Premium basis.

A Fixed Cover basis means your amount of insurance cover stays the same, but your weekly premium will generally increase as you get older. In the example provided, Jayne’s cover will remain $1,000,000 and her weekly premium will alter at certain ages.

A Fixed Premium basis means your weekly premium stays the same, but your insurance cover will generally decrease as you get older. Jayne’s premium would remain $7.31 a week but the amount she is covered for will generally decrease each year.

If you don’t make a choice, your cover will be provided on a Fixed Cover basis.

Tailored TPD cover reduction on Fixed Cover basisWith cover provided on a Fixed Cover basis, the amount of your Tailored TPD cover will reduce by 10% each year from age 61. Your premiums are adjusted accordingly. An example is shown below. If you have $200,000 of fixed TPD cover, your Tailored TPD cover will reduce as follows:

Your age TPD cover ($)

60 200,000

61 180,000

62 160,000

63 140,000

64 120,000

65 100,000

66 80,000

67 nil

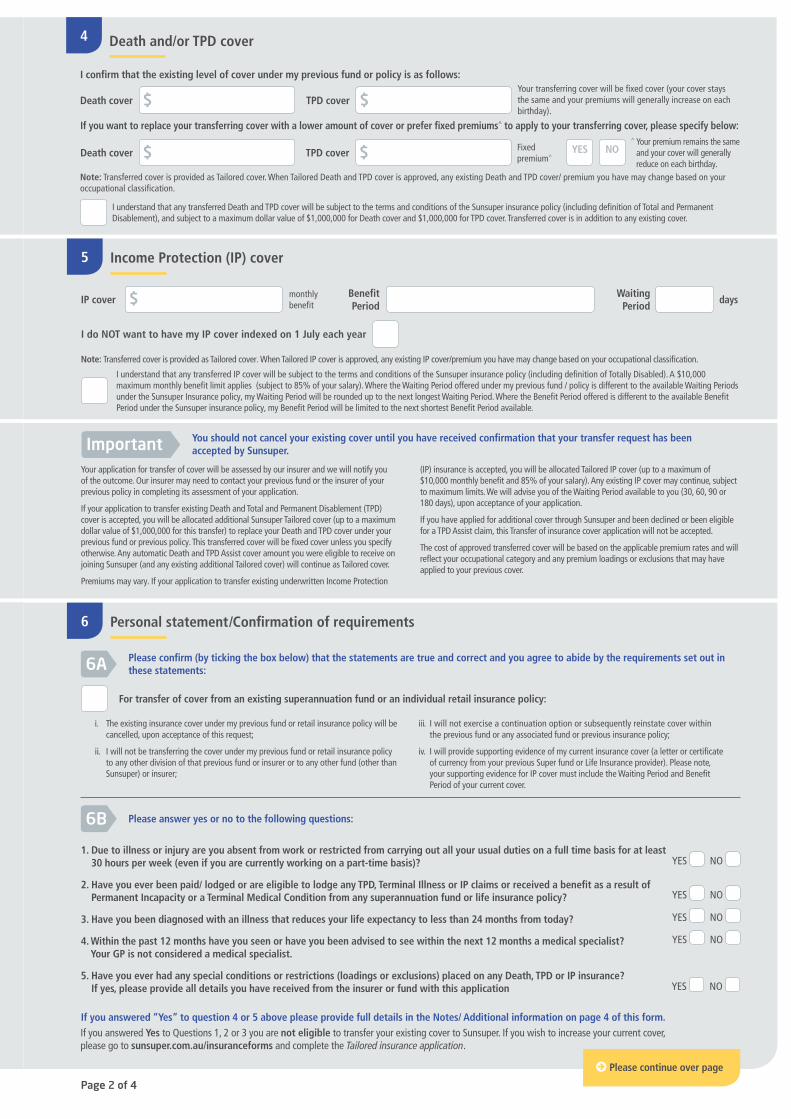

Transferring your Death and TPD insurance coverYou may be eligible to transfer existing Death and/or TPD cover (from other super funds or insurance policies up to $1,000,000) to Sunsuper. To transfer your existing cover please complete and return the Transfer of insurance cover form found in the back of this guide.

You will not be eligible to transfer your cover if:

• you have previously had an application for additional insurance cover declined,

• you have been paid, lodged or eligible to lodge any TPD, Permanent Incapacity, Terminal Illness or IP claim, or

• you are absent from work or unable to carry out all of the duties of your usual occupation due to an injury or illness at the transfer date.

It’s important you include all required documentation, which will include:

• a letter or certificate of currency from your superannuation fund or insurance provider detailing your current insurance cover,

• details of any loadings, exclusions and restrictions applicable to that cover, and

• the confirmation must have been issued within 30 days of your application.

If accepted by the insurer:

• you will be subject to the terms and conditions outlined in the Group Life Insurance policy provided by AIA Australia,

• the transferred cover will be additional to any existing insurance cover you have subject to maximum cover limits on page 19,

• you will need to cancel the cover you had under your previous fund or policy, and

• your total cover will become Tailored Death and/or TPD cover and will be Fixed Cover.

If you are thinking about transferring your existing insurance cover, make sure you compare the features and benefits, and are accepted by Sunsuper’s insurer, before cancelling existing cover.

p22 p23

Can your health affect your insurance cover?When the insurer assesses your application for Tailored insurance cover, they may ask for further details in relation to the information you disclose in your Tailored insurance application.

As a condition of acceptance of the Tailored insurance cover, the insurer may apply a loading (a higher premium) for the increased amount of Death and/or TPD insurance cover. The insurer may also specify a benefit exclusion that will apply if a claim for the increased amount of insurance is related to a specified condition or pastime.

Any premium loadings or benefit exclusions will be advised to you at the time the insurer accepts your application for Tailored insurance cover. Any premium loading or benefit exclusion will apply to your total insured amount. You should advise Sunsuper within 30 days if you decide that you do not wish to proceed with the application for Tailored cover.

Can you change your Occupational Category?If your occupation changes so you are in a less manual or less hazardous occupation, you can apply for a new occupational category by completing an Occupational rating form (visit sunsuper.com.au/insuranceforms). This may result in a reduction in your premiums (Fixed Cover) or increased cover (Fixed Premium). Where you currently have Fixed Premium and have an occupational category of Hazardous, a change in your occupational category may result in a lower premium; however your levels of cover will remain the same.

When does Tailored Death and TPD insurance cover start?Your Tailored Death and TPD insurance cover will start from the date the insurer accepts your application, provided you have enough money in your Super-savings account to pay insurance premiums. If you do not have enough money in your Super-savings account to pay premiums, you will be notified of the conditions that apply to you. The assessment process, known as “underwriting”, usually takes some time especially where additional medical information is required. The “underwriting” process depends on your level of cover and the amount of health evidence required.

Exclusions and restrictionsA Tailored Death, TPD or Terminal Illness benefit will not be paid:

• where caused by suicide or any intentional self-inflicted act within 12 months of the insurer’s acceptance of the additional Tailored cover. This restriction applies only to the amount above your previous level of cover,

• where you become TPD and notify Sunsuper more than five years after your Date of Disablement,

• if you are deployed to a hostile environment as part of active military service,

• if you are employed under the terms of a work visa and the term of the visa expires, or you permanently depart Australia (whichever is earlier), or

• if subject to any restriction or exclusion imposed as a condition of acceptance by the insurer at time of application for Tailored cover.

Any restrictions or exclusions on your previous cover amounts will continue.

Conditions and Exclusions

When does Death and TPD insurance cover stop?Cover will stop when:

• you cancel it,

• you turn 70 years of age for Death cover,

• you turn 67 years of age for TPD Assist or Tailored TPD cover,1

• you die,

• you are paid a Tailored TPD insurance benefit2,

• you are paid all six annual support payments under the TPD Assist benefit,2

• the total of annual support payments paid under the TPD Assist benefit exceed your Death cover. Death cover will cease, TPD Assist cover will continue while you continue to meet the TPD Assist definition,

• in respect to TPD Assist cover, the date benefits cease due to you no longer meeting the TPD Assist definition during a second claim period (with the exception of a Recurrent Event within 12 months),

• you withdraw all monies from Sunsuper,

• the policy issued to the Trustee is cancelled or terminated for any reason,

• you are paid a Terminal Illness benefit2 where the full Death benefit cover is paid,

• you are employed under the terms of a work visa and the term of the visa expires, or you permanently depart Australia (whichever is earlier),

• your Super-savings account balance is low and inactive (normally this will be when your balance is less than $1,500 and employer contributions have not been received for 12 months, unless we have agreed otherwise). Where we have valid contact details, we will contact you advising the date your cover will stop. To avoid your cover stopping in this way, you should maintain your Super-savings account balance above $1,500 or ensure regular employer contributions are paid into your Super-savings account, or

• the premium is due and there is not enough money in your Super-savings account to pay the premiums, and it remains unpaid for 4 months.

1 Special conditions may apply to some members.

2 Death cover in excess of the TPD Assist or Tailored TPD cover or Terminal Illness benefit will still continue.

It is your responsibility to check there is always enough money in your Super-savings account to pay insurance premiums.

Can Death and TPD cover restart if it lapses?Where insurance cover has stopped because:

• your Super-savings account balance is low and inactive, and/or

• there was insufficient money in your Super-savings account to pay the premiums,

the receipt of an SG contribution will restart Death and TPD Assist cover from the date of receipt of the SG contribution. Death and TPD Assist cover will restart as per the cover levels detailed in Premium table 1. Limited Cover will apply until you satisfy the At Work requirements for 30 consecutive days.

If you cancelled your cover or have cover in excess of the default Death and TPD Assist cover (i.e. Tailored Death and TPD cover), satisfactory evidence of health will be required to restart cover.

What benefits are paid out if you die?Your Death benefit is the amount of your Sunsuper for life account balance plus the total amount of your Death cover.

Any benefit payment for your Death cover is subject to acceptance of the claim by the insurer.