sunil kumar gupta & co. - Dakshin Haryana Bijli Vitran Nigam€¦ · SUNIL KUMAR GUPTA & CO....

64

1 SUNIL KUMAR GUPTA & CO. Chartered Accountants ____________________________________________________ 3-STATE BANK COLONY, NEAR I.T.I. GIRLS GATE, ROHTAK-124001 Revised Auditor’s Report to the members of Dakshin Haryana Bijli Vitran Nigam Limited In connection with the above, we had issued the Auditor’s report dated 11-10-2012 and signed the financial statement as authenticated by the Chairman-cum-Managing Director, Director/ Operations, Director/Projects and Chief General Manager/Accounts as authorized by the Board of Directors on 01-10-2012. It has been decided in the BOD meeting held on 30-11-2012 that the Annual Accounts of the Company for FY 2011-12 may be re-opened and main observations raised in the draft comments by PAG/Audit, Haryana and Statutory Auditors be carried out and necessary adjustments be made in the accounts for FY 2011-12. Moreover, the Company has made some adjustments in the accounts and a suitable disclosure has been made at Sr. No. 52 of Schedule 30 to the Notes on Accounts. The BOD has now re-approved the Revised Balance Sheet as at 31 st 1. We have audited the attached Revised Balance Sheet of Dakshin Haryana Bijli Vitran Nigam Limited as at 31 March, 2012 and the Revised Profit and Loss account and also Revised Cash Flow Statement for the year ended on that date by Board of Directors dated 24-12-2012. After taking the effects of entries discussed above para and the same has disclosed by the management in Para 52 of schedule 30 to the notes to accounts. Since there are revisions / amendments in financial statements. So we submit our Revised Auditors’ Report. The Company has not returned the entire original copies of accounts and report dated 11-10- 2012 to us. Subject to the above and report that : st March 2012, the Revised Profit and Loss Account and also the Revised Cash Flow Statement of the Company for the year ended on that date, annexed thereto. As the Company is governed by The Electricity Act, 2003, the provisions of the Act (including for provision of depreciation at rates different from those prescribed in Schedule XIV to The Companies Act, 1956) have prevailed wherever they have been inconsistent with the provisions of The Companies Act, 1956. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audit. 2. We conducted our audit in accordance with auditing standards generally accepted in India. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

Transcript of sunil kumar gupta & co. - Dakshin Haryana Bijli Vitran Nigam€¦ · SUNIL KUMAR GUPTA & CO....

1

SUNIL KUMAR GUPTA & CO. Chartered Accountants ____________________________________________________ 3-STATE BANK COLONY, NEAR I.T.I. GIRLS GATE, ROHTAK-124001 Revised Auditor’s Report to the members of Dakshin Haryana Bijli Vitran Nigam Limited In connection with the above, we had issued the Auditor’s report dated 11-10-2012 and signed the financial statement as authenticated by the Chairman-cum-Managing Director, Director/ Operations, Director/Projects and Chief General Manager/Accounts as authorized by the Board of Directors on 01-10-2012. It has been decided in the BOD meeting held on 30-11-2012 that the Annual Accounts of the Company for FY 2011-12 may be re-opened and main observations raised in the draft comments by PAG/Audit, Haryana and Statutory Auditors be carried out and necessary adjustments be made in the accounts for FY 2011-12. Moreover, the Company has made some adjustments in the accounts and a suitable disclosure has been made at Sr. No. 52 of Schedule 30 to the Notes on Accounts. The BOD has now re-approved the Revised Balance Sheet as at 31st

1. We have audited the attached Revised Balance Sheet of Dakshin Haryana Bijli Vitran Nigam Limited as at 31

March, 2012 and the Revised Profit and Loss account and also Revised Cash Flow Statement for the year ended on that date by Board of Directors dated 24-12-2012. After taking the effects of entries discussed above para and the same has disclosed by the management in Para 52 of schedule 30 to the notes to accounts. Since there are revisions / amendments in financial statements. So we submit our Revised Auditors’ Report. The Company has not returned the entire original copies of accounts and report dated 11-10-2012 to us. Subject to the above and report that :

st

March 2012, the Revised Profit and Loss Account and also the Revised Cash Flow Statement of the Company for the year ended on that date, annexed thereto. As the Company is governed by The Electricity Act, 2003, the provisions of the Act (including for provision of depreciation at rates different from those prescribed in Schedule XIV to The Companies Act, 1956) have prevailed wherever they have been inconsistent with the provisions of The Companies Act, 1956. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audit.

2. We conducted our audit in accordance with auditing standards generally accepted in India. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

2

3. As required by the Companies Auditor’s Report (Amendment) Order, 2004 issued by the

Central Government of India in terms of Sub-Section (4A) of Section 227 of the Companies Act, 1956 and on the basis of such checks of the books and records as we considered appropriate and the information and explanations given to us during the course of the audit, we enclose in the Annexure ‘1’ a statement on the matters specified in the paragraphs 4 and 5 of the said order.

4. Further to our comments in the Annexure-1 referred to in paragraph above, we further report

that: -

a. Subject to para 4(f) i) to 4(f) viii) of this report, we have obtained all the information and explanation which to the best of our knowledge and belief were necessary for the purpose of our audit;

b. In our opinion, proper books of accounts as required by law have been kept by the

Company so far as appears from our examination of the books;

c. The Revised Balance Sheet, Revised Profit and Loss Account and Revised Cash Flow Statement dealt with by this report are in agreement with the books of accounts;

d. Subject to para 4(f) i) to 4(f) viii) of this report, in our opinion, the Revised Balance

Sheet, Revised Profit and Loss Account and Revised Cash Flow Statement dealt with by this report comply with the Accounting Standards referred to in sub-section (3C) of Section 211 of the Companies Act, 1956; .

e. Since the provision regarding disqualification of directors under clause (g) of sub-section (1) of Section 274 of the Companies Act, 1956 are not applicable to company in terms of Notification no. GSR 829(E) dated 21.10.2003, no comments are offered on the questions of disqualification of Directors under the said provision of the Act.

f.

i) The Company is having sundry debtors of Rs. 2178.57 crores (before considering provisions of Rs.926.42 crores) out of which debtors of Rs. 2021.88 crores are outstanding for more than 6 months as at 31st March 2012. Further the company is having security deposit including interest on security deposits of Rs. 720.48 crores as at 31st March 2012. . We are unable to form an opinion on the provision for debts, age wise debtors break-up and segregation of the sundry debtors and security deposits into secured, or otherwise, due to under mentioned reasons: a) The company has segregated debtors secured and considered good on the

basis of total customer security received for which the individual details of sundry debtors and their corresponding security deposits are not made available to us.

3

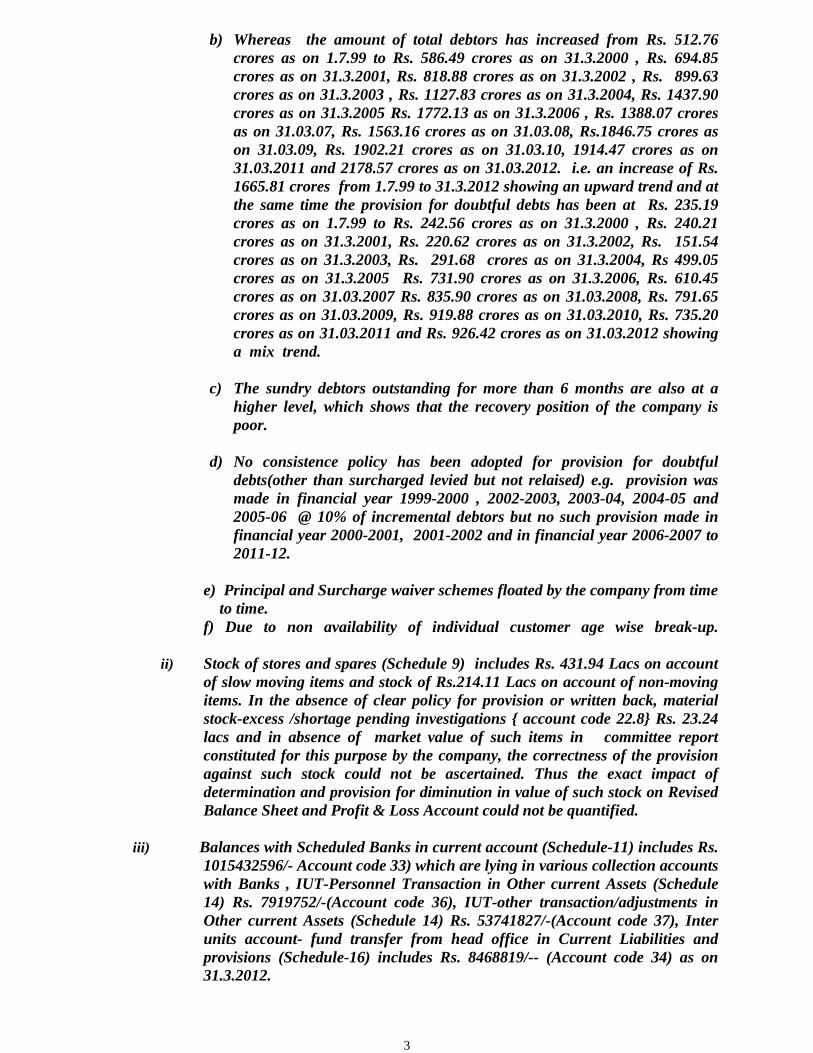

b) Whereas the amount of total debtors has increased from Rs. 512.76

crores as on 1.7.99 to Rs. 586.49 crores as on 31.3.2000 , Rs. 694.85 crores as on 31.3.2001, Rs. 818.88 crores as on 31.3.2002 , Rs. 899.63 crores as on 31.3.2003 , Rs. 1127.83 crores as on 31.3.2004, Rs. 1437.90 crores as on 31.3.2005 Rs. 1772.13 as on 31.3.2006 , Rs. 1388.07 crores as on 31.03.07, Rs. 1563.16 crores as on 31.03.08, Rs.1846.75 crores as on 31.03.09, Rs. 1902.21 crores as on 31.03.10, 1914.47 crores as on 31.03.2011 and 2178.57 crores as on 31.03.2012. i.e. an increase of Rs. 1665.81 crores from 1.7.99 to 31.3.2012 showing an upward trend and at the same time the provision for doubtful debts has been at Rs. 235.19 crores as on 1.7.99 to Rs. 242.56 crores as on 31.3.2000 , Rs. 240.21 crores as on 31.3.2001, Rs. 220.62 crores as on 31.3.2002, Rs. 151.54 crores as on 31.3.2003, Rs. 291.68 crores as on 31.3.2004, Rs 499.05 crores as on 31.3.2005 Rs. 731.90 crores as on 31.3.2006, Rs. 610.45 crores as on 31.03.2007 Rs. 835.90 crores as on 31.03.2008, Rs. 791.65 crores as on 31.03.2009, Rs. 919.88 crores as on 31.03.2010, Rs. 735.20 crores as on 31.03.2011 and Rs. 926.42 crores as on 31.03.2012 showing a mix trend.

c) The sundry debtors outstanding for more than 6 months are also at a

higher level, which shows that the recovery position of the company is poor.

d) No consistence policy has been adopted for provision for doubtful

debts(other than surcharged levied but not relaised) e.g. provision was made in financial year 1999-2000 , 2002-2003, 2003-04, 2004-05 and 2005-06 @ 10% of incremental debtors but no such provision made in financial year 2000-2001, 2001-2002 and in financial year 2006-2007 to 2011-12.

e) Principal and Surcharge waiver schemes floated by the company from time to time. f) Due to non availability of individual customer age wise break-up.

ii) Stock of stores and spares (Schedule 9) includes Rs. 431.94 Lacs on account of slow moving items and stock of Rs.214.11 Lacs on account of non-moving items. In the absence of clear policy for provision or written back, material stock-excess /shortage pending investigations { account code 22.8} Rs. 23.24 lacs and in absence of market value of such items in committee report constituted for this purpose by the company, the correctness of the provision against such stock could not be ascertained. Thus the exact impact of determination and provision for diminution in value of such stock on Revised Balance Sheet and Profit & Loss Account could not be quantified.

iii) Balances with Scheduled Banks in current account (Schedule-11) includes Rs.

1015432596/- Account code 33) which are lying in various collection accounts with Banks , IUT-Personnel Transaction in Other current Assets (Schedule 14) Rs. 7919752/-(Account code 36), IUT-other transaction/adjustments in Other current Assets (Schedule 14) Rs. 53741827/-(Account code 37), Inter units account- fund transfer from head office in Current Liabilities and provisions (Schedule-16) includes Rs. 8468819/-- (Account code 34) as on 31.3.2012.

4

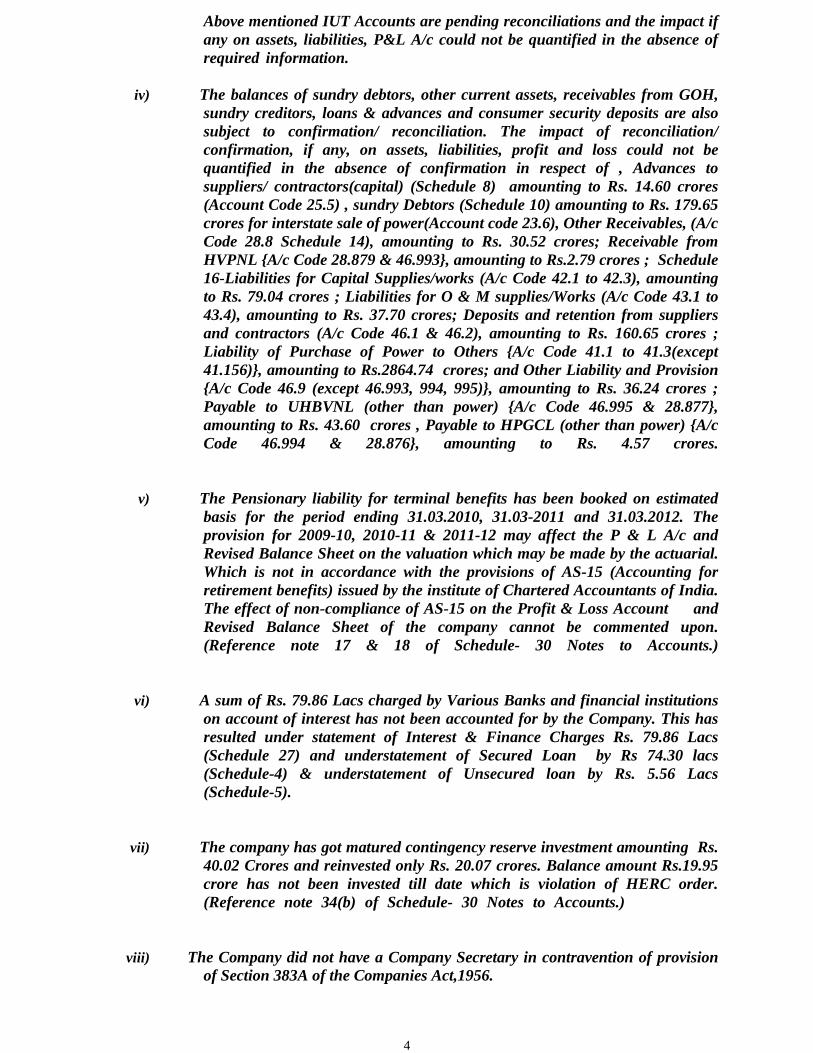

Above mentioned IUT Accounts are pending reconciliations and the impact if any on assets, liabilities, P&L A/c could not be quantified in the absence of required information. .

iv) The balances of sundry debtors, other current assets, receivables from GOH, sundry creditors, loans & advances and consumer security deposits are also subject to confirmation/ reconciliation. The impact of reconciliation/ confirmation, if any, on assets, liabilities, profit and loss could not be quantified in the absence of confirmation in respect of , Advances to suppliers/ contractors(capital) (Schedule 8) amounting to Rs. 14.60 crores (Account Code 25.5) , sundry Debtors (Schedule 10) amounting to Rs. 179.65 crores for interstate sale of power(Account code 23.6), Other Receivables, (A/c Code 28.8 Schedule 14), amounting to Rs. 30.52 crores; Receivable from HVPNL {A/c Code 28.879 & 46.993}, amounting to Rs.2.79 crores ; Schedule 16-Liabilities for Capital Supplies/works (A/c Code 42.1 to 42.3), amounting to Rs. 79.04 crores ; Liabilities for O & M supplies/Works (A/c Code 43.1 to 43.4), amounting to Rs. 37.70 crores; Deposits and retention from suppliers and contractors (A/c Code 46.1 & 46.2), amounting to Rs. 160.65 crores ; Liability of Purchase of Power to Others {A/c Code 41.1 to 41.3(except 41.156)}, amounting to Rs.2864.74 crores; and Other Liability and Provision {A/c Code 46.9 (except 46.993, 994, 995)}, amounting to Rs. 36.24 crores ; Payable to UHBVNL (other than power) {A/c Code 46.995 & 28.877}, amounting to Rs. 43.60 crores , Payable to HPGCL (other than power) {A/c Code 46.994 & 28.876}, amounting to Rs. 4.57 crores. .

v) The Pensionary liability for terminal benefits has been booked on estimated basis for the period ending 31.03.2010, 31.03-2011 and 31.03.2012. The provision for 2009-10, 2010-11 & 2011-12 may affect the P & L A/c and Revised Balance Sheet on the valuation which may be made by the actuarial. Which is not in accordance with the provisions of AS-15 (Accounting for retirement benefits) issued by the institute of Chartered Accountants of India. The effect of non-compliance of AS-15 on the Profit & Loss Account and Revised Balance Sheet of the company cannot be commented upon. (Reference note 17 & 18 of Schedule- 30 Notes to Accounts.) . .

vi) A sum of Rs. 79.86 Lacs charged by Various Banks and financial institutions on account of interest has not been accounted for by the Company. This has resulted under statement of Interest & Finance Charges Rs. 79.86 Lacs (Schedule 27) and understatement of Secured Loan by Rs 74.30 lacs (Schedule-4) & understatement of Unsecured loan by Rs. 5.56 Lacs (Schedule-5). .

vii) The company has got matured contingency reserve investment amounting Rs. 40.02 Crores and reinvested only Rs. 20.07 crores. Balance amount Rs.19.95 crore has not been invested till date which is violation of HERC order. (Reference note 34(b) of Schedule- 30 Notes to Accounts.) . .

viii) The Company did not have a Company Secretary in contravention of provision of Section 383A of the Companies Act,1956.

5

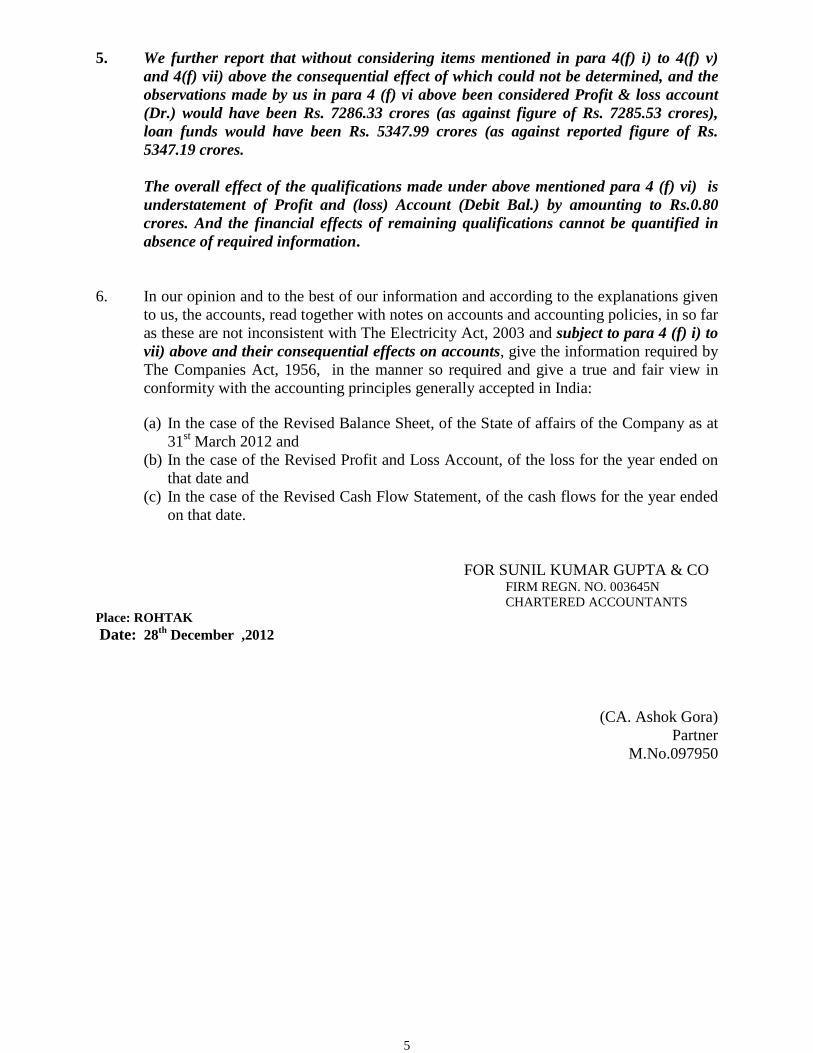

5. We further report that without considering items mentioned in para 4(f) i) to 4(f) v)

and 4(f) vii) above the consequential effect of which could not be determined, and the observations made by us in para 4 (f) vi above been considered Profit & loss account (Dr.) would have been Rs. 7286.33 crores (as against figure of Rs. 7285.53 crores), loan funds would have been Rs. 5347.99 crores (as against reported figure of Rs. 5347.19 crores.

The overall effect of the qualifications made under above mentioned para 4 (f) vi) is understatement of Profit and (loss) Account (Debit Bal.) by amounting to Rs.0.80 crores. And the financial effects of remaining qualifications cannot be quantified in absence of required information.

6. In our opinion and to the best of our information and according to the explanations given

to us, the accounts, read together with notes on accounts and accounting policies, in so far as these are not inconsistent with The Electricity Act, 2003 and subject to para 4 (f) i) to vii) above and their consequential effects on accounts, give the information required by The Companies Act, 1956, in the manner so required and give a true and fair view in conformity with the accounting principles generally accepted in India:

(a) In the case of the Revised Balance Sheet, of the State of affairs of the Company as at

31st

(b) In the case of the Revised Profit and Loss Account, of the loss for the year ended on that date and

March 2012 and

(c) In the case of the Revised Cash Flow Statement, of the cash flows for the year ended on that date.

FOR SUNIL KUMAR GUPTA & CO FIRM REGN. NO. 003645N CHARTERED ACCOUNTANTS Place: ROHTAK Date: 28th

December ,2012

(CA. Ashok Gora) Partner

M.No.097950

6

i. (a) The company is maintaining proper records showing full particulars including quantitative details and situation of fixed assets.

ANNEXURE ‘1’ TO THE AUDITOR’S REPORT (Referred to in Paragraph (3) thereof)

(b) All the assets have not been physically verified by the management during the year but

there is a regular programme of verification which, in our opinion, is reasonable having regard to the size of the company and the nature of its assets. No material discrepancies were noticed on such verification.

(c) Fixed assets disposed off during the year were not substantial. According to information

and explanations given to us, we are of the opinion that the disposal of fixed assets has not affected the going concern status of the company.

ii. (a) It has been reported that the inventories i.e. stores and spares have been physically verified during the year by the management and the frequency of the verification is reasonable.

(b) In our opinion and according to the information and explanation given to us the

procedures of physical verification of inventories followed by the management are reasonable and inadequate in relation to the size of the company and the nature of its business.

(c) On the basis of our examination of the records of inventory, we are of the opinion that the

company is maintaining proper records of inventory i.e. stores & spares. However we were not provided with any report of physical verification and the discrepancy between the physical stock and book records. Hence we are unable to comment on it materiality.

iii. The Company had not taken or granted loan Secured or Unsecured from/to companies listed in

the Register maintained under section 301.

iv. The internal control system for the purchase of stores, components and machinery or spare parts are commensurate with the size of the Company and nature of its business. However in respect of level of inventory we report that the Company has not fixed maximum and minimum level of stock holding and Economic Order Quantity. Stores valuing Rs 646.05 Lacs are reported as slow moving & non-moving.

v. As regards our comments for the sale of goods & services the internal control over sale of

power is lacking as reflected by high distribution losses, high percentage of Un-metered consumption and defective/worn out meters, high element of cross subsidization, poor collection efficiency seen from rising level of debtors, non-classification of debtors into good, doubtful and bad, amount recoverable from untraceable consumers, connections in the premises of defaulting consumers and not acting timely for recovery from permanently disconnected consumers and non-compliance of procedure for disconnection in case of default.

vi. (a) In our opinion and according to the information and explanation given to us, there are no

transactions that need to be entered into the register maintain u/s 301 of the Companies Act, 1956.

(b) In view of above point, paragraph (v) (b) is not applicable to the company.

7

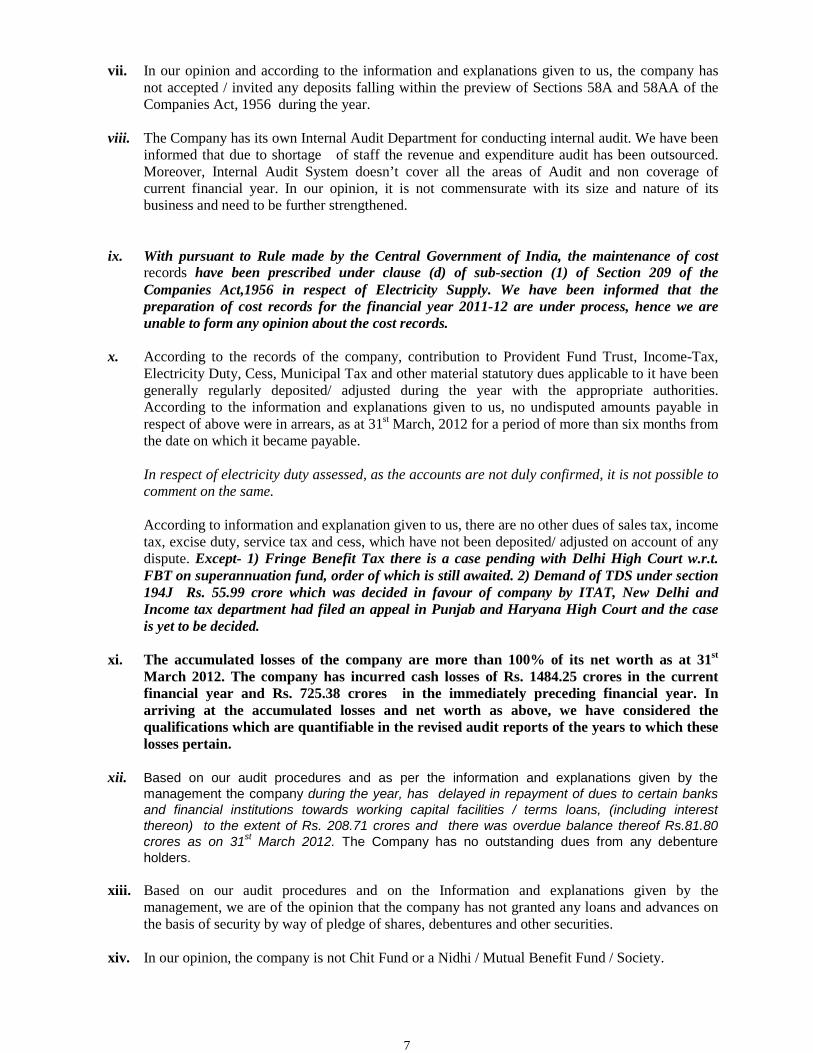

vii. In our opinion and according to the information and explanations given to us, the company has

not accepted / invited any deposits falling within the preview of Sections 58A and 58AA of the Companies Act, 1956 during the year.

viii. The Company has its own Internal Audit Department for conducting internal audit. We have been

informed that due to shortage of staff the revenue and expenditure audit has been outsourced. Moreover, Internal Audit System doesn’t cover all the areas of Audit and non coverage of current financial year. In our opinion, it is not commensurate with its size and nature of its business and need to be further strengthened.

ix. With pursuant to Rule made by the Central Government of India, the maintenance of cost records have been prescribed under clause (d) of sub-section (1) of Section 209 of the Companies Act,1956 in respect of Electricity Supply. We have been informed that the preparation of cost records for the financial year 2011-12 are under process, hence we are unable to form any opinion about the cost records.

x. According to the records of the company, contribution to Provident Fund Trust, Income-Tax,

Electricity Duty, Cess, Municipal Tax and other material statutory dues applicable to it have been generally regularly deposited/ adjusted during the year with the appropriate authorities. According to the information and explanations given to us, no undisputed amounts payable in respect of above were in arrears, as at 31st

In respect of electricity duty assessed, as the accounts are not duly confirmed, it is not possible to comment on the same. According to information and explanation given to us, there are no other dues of sales tax, income tax, excise duty, service tax and cess, which have not been deposited/ adjusted on account of any dispute. Except- 1) Fringe Benefit Tax there is a case pending with Delhi High Court w.r.t. FBT on superannuation fund, order of which is still awaited. 2) Demand of TDS under section 194J Rs. 55.99 crore which was decided in favour of company by ITAT, New Delhi and Income tax department had filed an appeal in Punjab and Haryana High Court and the case is yet to be decided.

March, 2012 for a period of more than six months from the date on which it became payable.

xi. The accumulated losses of the company are more than 100% of its net worth as at 31st

March 2012. The company has incurred cash losses of Rs. 1484.25 crores in the current financial year and Rs. 725.38 crores in the immediately preceding financial year. In arriving at the accumulated losses and net worth as above, we have considered the qualifications which are quantifiable in the revised audit reports of the years to which these losses pertain.

xii. Based on our audit procedures and as per the information and explanations given by the management the company during the year, has delayed in repayment of dues to certain banks and financial institutions towards working capital facilities / terms loans, (including interest thereon) to the extent of Rs. 208.71 crores and there was overdue balance thereof Rs.81.80 crores as on 31st

March 2012. The Company has no outstanding dues from any debenture holders.

xiii. Based on our audit procedures and on the Information and explanations given by the management, we are of the opinion that the company has not granted any loans and advances on the basis of security by way of pledge of shares, debentures and other securities.

xiv. In our opinion, the company is not Chit Fund or a Nidhi / Mutual Benefit Fund / Society.

8

xv. In our opinion the company is not dealing in or trading in shares, securities, debentures and other investments.

xvi. In our opinion, and according to the information and explanation given to us, the Company has

not given any guarantees for loans taken by others from banks or financial institutions.

xvii. The term loans have been applied for the purpose for which they were raised. xviii. According to the information and explanations given to us and on an overall examination of the

Revised Balance Sheet of the company, we report that no funds raised on short-term basis have been used for long-term investment. No long-term funds have been used to finance short-term assets.

xix. The company has not made any preferential allotment of shares to parties and companies covered

in the register maintained under section 301 of the Act during the year. xx. In our opinion and according to the information and explanations given to us, the company has

not created any secured charge in respect of debentures during the period covered by our report. xxi. During the period covered by our audit report, the company has not raised any money by public

issues. xxii. According to the information and explanations given to us, no fraud on or by the company has

been noticed or reported during the course of our audit except reported in Notes 20, 21, 22 & 23 of Notes on accounts Schedule 30.

FOR SUNIL KUMAR GUPTA & CO FIRM REGN. NO. 003645N CHARTERED ACCOUNTANTS Place: ROHTAK Date: 28th

(CA. Ashok Gora)

December, 2012

Partner M.No.097950

DHBVNL

REVISED ANNUAL STATEMENT OF ACCOUNTSFINANCIAL YEAR 2011-12

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITEDRegistered Office : Vidyut Sadan, Vidyut Nagar, Hisar :- 125005 (Haryana)

www.dhbvn.com

Particulars Reference of Schedule

31-3-2012 `

31-3-2011 `

Sources of FundsShare holders fundsShare capital 1 14,065,677,461 12,604,677,461 Reserves and surplus 2 272,320,700 272,320,700 Sub Total 14,337,998,161 12,876,998,161 Capital Consumer Contribution and grants 3 7,805,272,219 6,616,673,933 Loan FundsSecured Loans 4 46,332,775,641 44,368,818,361 Unsecured Loans 5 7,139,091,044 3,848,802,065 Sub Total 53,471,866,684 48,217,620,426 Consumers Security Deposits 6 7,204,825,925 6,210,858,996 Total 82,819,962,989 73,922,151,516 Application of FundsFixed AssetsGross Block 41,136,984,157 35,041,012,565 Less : Accumulated Depreciation 11,342,102,779 9,989,951,823 Net Block 29,794,881,378 25,051,060,742 Capital work in Progress 8 5,208,820,620 7,884,053,591 Total Fixed Assets 35,003,701,998 32,935,114,334 Contingency Reserve Investment 12 200,747,383 365,409,143 Current Assets ,Loans & advancesStores and spares 9 1,095,520,293 754,841,414 Sundry Debtors 10 12,521,472,417 11,792,659,323 Cash and Bank Balances 11 2,613,333,221 2,177,698,912 Loans and Advances 13 536,218,217 449,636,746 Other Current Assets 14 682,667,188 19,854,978,214 Receivable From GOH 15 - 5,945,459,555 Total : Current Assets 17,449,211,337 40,975,274,164 Less : Current Liabilities and Provisions 16 42,689,039,545 28,614,331,529 Net Current Assets (25,239,828,208) 12,360,942,635 Miscellaneous Expenditure 17 - 236,304,000 Regulatory Assets not written off - 1,163,448,000

Profit and (Loss) Account ( Debit Bal.) 72,855,341,816 26,860,933,405 Total 82,819,962,989 73,922,151,516

Cash Flow Statement 29Significant Accounting Policies and 30Notes on Accounts :

For and on behalf of Board of Directors

As per our report of even date attached (V.K.CHAUDHARY) (DEVENDER SINGH)FOR SUNIL KUMAR GUPTA & CO. Director/Projects Chairman cumChartered Accountants Managing DirectorF.R No.: 003645N

(R.V.BARI)(ASHOK GORA) CGM/Accounts

M. No. 097950

Place : Place : Date : Date :

Partner

7

Schedules 1 to 17 & 30 referred to above form an integral part of Balance Sheet

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITED

REVISED BALANCE SHEET AS AT MARCH 31,2012

Sr. No.

Head of Account Particulars Ref. of

Schedule 31-3-2012 `

31-3-2011 `

INCOME1 61 Revenue from sale of power 18 52,258,987,200 44,702,023,514

61 Fuel Surcharge Adjustment 18 3,664,625,855 3,474,666,000 2 62 Other revenue 19 953,778,208 1,099,316,602

Revenue subsidies &grants 13,792,600,000 12,837,500,000 4 Sub Total 70,669,991,263 62,113,506,116

EXPENDITURE5 70 Purchase of power 22 73,660,567,673 56,036,882,845

70 Fuel Surcharge Adjustment 22 - 3,474,666,000 6 74 Repairs & Maintenance 23 390,278,745 364,728,051 7 75 Employees cost 24 5,422,553,728 4,977,978,092 8 76 Administrative & general expenses 25 488,578,709 369,487,297 9 77 Depreciation & related debits 26 861,010,365 684,286,007

10 78 Interest & finance charges 27 5,447,750,805 3,776,415,422 11 Sub Total 86,270,740,025 69,684,443,715 12 79 Other debits 28 101,696,757 371,301,174 13 Net expenditure total 86,372,436,782 70,055,744,888 14 Profit /(Loss) before tax (15,702,445,519) (7,942,238,772)

Fringe Benefit Tax - Profit /(Loss) after FBT (15,702,445,519) (7,942,238,772)

15 Provision for income tax - 16 Profit/(Loss)after tax (15,702,445,519) (7,942,238,772) 17 65/83 Net Prior Period Credit/(Charges) 20 (29,128,514,892) 313,665,890 18 Transfer to/(from) Regulatory Assets (Net) (1,163,448,000) (290,862,000) 19 Profit/(Loss) available for Appropriation (45,994,408,411) (7,919,434,882) 20 Statutory Appropriation22 Profit /(Loss) after appropriation (45,994,408,411) (7,919,434,882) 23 Loss brought forward from previous year (26,860,933,405) (18,941,498,522) 24 Loss carried to Balance Sheet (72,855,341,816) (26,860,933,405)

Earning per Share (on nominal value of ` 1000 per Share)Basic (`) (3,788.57) (758.49) Diluted (`) (3,448.26) (652.91) Cash Flow Statement 29Significant Accounting Policies and 30Notes on Accounts :

As per our report of even date attached (V.K.CHAUDHARY) (DEVENDER SINGH)FOR SUNIL KUMAR GUPTA & CO. Director/Projects Chairman cumChartered Accountants Managing DirectorF.R No.: 003645N

(ASHOK GORA) (R.V.BARI)CGM/Accounts

M. No. 097950

Place : Place : Date : Date :

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITED

REVISED PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED ON 31st MARCH, 2012

213 63

For and on behalf of Board of Directors

Partner

Schedules 18 to 28 & 30 referred to above form an integral part of Profit and Loss Account

Particulars Account Code

31-3-2012 `

31-3-2011 `

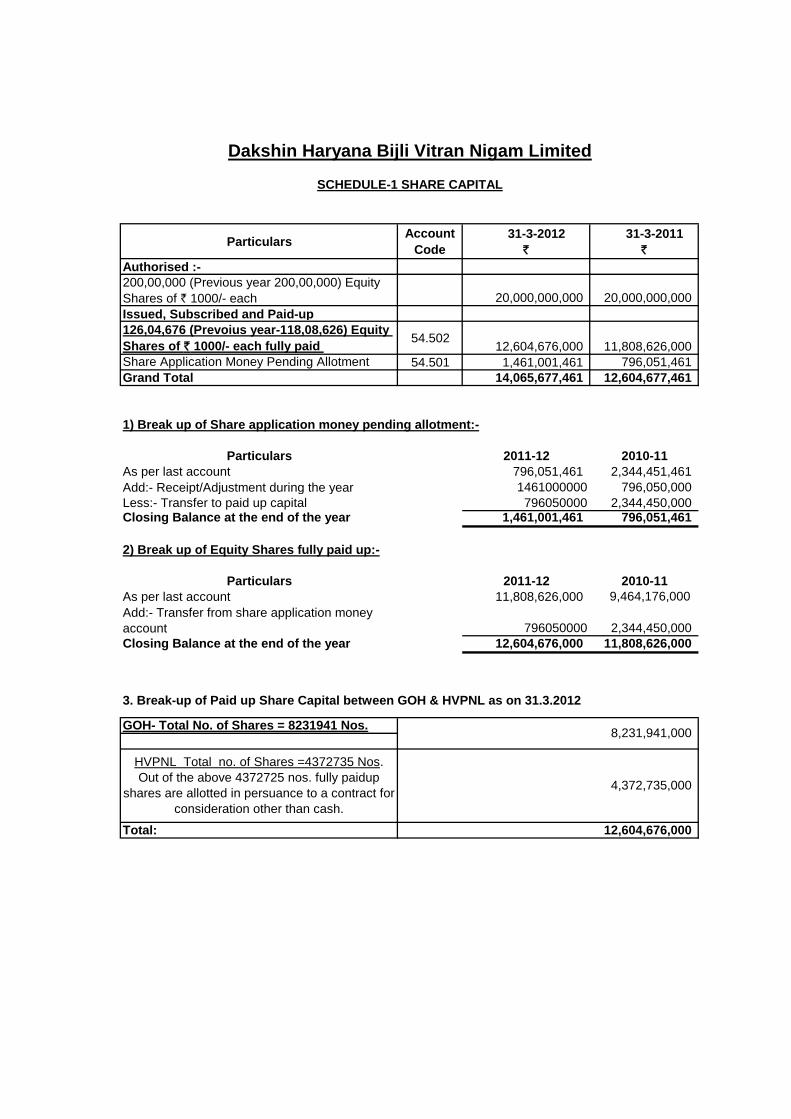

Authorised :-200,00,000 (Previous year 200,00,000) Equity Shares of ` 1000/- each 20,000,000,000 20,000,000,000 Issued, Subscribed and Paid-up 126,04,676 (Prevoius year-118,08,626) Equity Shares of ` 1000/- each fully paid 54.502 12,604,676,000 11,808,626,000 Share Application Money Pending Allotment 54.501 1,461,001,461 796,051,461 Grand Total 14,065,677,461 12,604,677,461

1) Break up of Share application money pending allotment:-

Particulars 2011-12 2010-11As per last account 796,051,461 2,344,451,461 Add:- Receipt/Adjustment during the year 1461000000 796,050,000 Less:- Transfer to paid up capital 796050000 2,344,450,000 Closing Balance at the end of the year 1,461,001,461 796,051,461

2) Break up of Equity Shares fully paid up:-

Particulars 2011-12 2010-11As per last account 11,808,626,000 9,464,176,000 Add:- Transfer from share application money account 796050000 2,344,450,000 Closing Balance at the end of the year 12,604,676,000 11,808,626,000

GOH- Total No. of Shares = 8231941 Nos.

Total: 12,604,676,000

Dakshin Haryana Bijli Vitran Nigam Limited

SCHEDULE-1 SHARE CAPITAL

HVPNL Total no. of Shares =4372735 Nos. Out of the above 4372725 nos. fully paidup

shares are allotted in persuance to a contract for consideration other than cash.

3. Break-up of Paid up Share Capital between GOH & HVPNL as on 31.3.2012

8,231,941,000

4,372,735,000

Particulars Account Code 31-3-2012 `

31-3-2011 `

Contingency Reserve 56.680 272,320,700 272,320,700 Cost Variance Reserve 56.610 - - Grand Total 272,320,700 272,320,700

Dakshin Haryana Bijli Vitran Nigam Limited

SCHEDULE-2 RESERVES AND SURPLUS

Particulars Account Code 31-3-2012 `

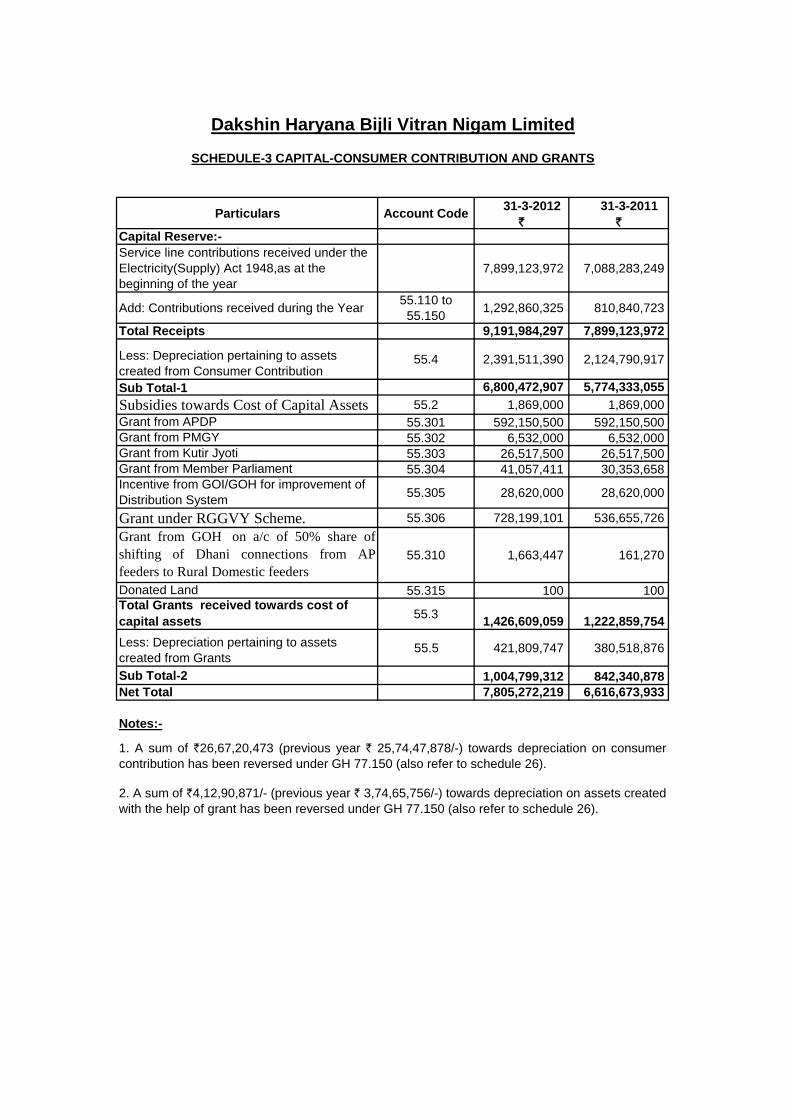

31-3-2011 `

Capital Reserve:-Service line contributions received under the Electricity(Supply) Act 1948,as at the beginning of the year

7,899,123,972 7,088,283,249

Add: Contributions received during the Year 55.110 to 55.150 1,292,860,325 810,840,723

Total Receipts 9,191,984,297 7,899,123,972

Less: Depreciation pertaining to assets created from Consumer Contribution

55.4 2,391,511,390 2,124,790,917

Sub Total-1 6,800,472,907 5,774,333,055 Subsidies towards Cost of Capital Assets 55.2 1,869,000 1,869,000 Grant from APDP 55.301 592,150,500 592,150,500 Grant from PMGY 55.302 6,532,000 6,532,000 Grant from Kutir Jyoti 55.303 26,517,500 26,517,500 Grant from Member Parliament 55.304 41,057,411 30,353,658 Incentive from GOI/GOH for improvement of Distribution System 55.305 28,620,000 28,620,000

Grant under RGGVY Scheme. 55.306 728,199,101 536,655,726 Grant from GOH on a/c of 50% share ofshifting of Dhani connections from APfeeders to Rural Domestic feeders

55.310 1,663,447 161,270

Donated Land 55.315 100 100 Total Grants received towards cost of capital assets 55.3 1,426,609,059 1,222,859,754 Less: Depreciation pertaining to assets created from Grants

55.5 421,809,747 380,518,876

Sub Total-2 1,004,799,312 842,340,878 Net Total 7,805,272,219 6,616,673,933

Notes:-

2. A sum of `4,12,90,871/- (previous year ` 3,74,65,756/-) towards depreciation on assets createdwith the help of grant has been reversed under GH 77.150 (also refer to schedule 26).

Dakshin Haryana Bijli Vitran Nigam Limited

SCHEDULE-3 CAPITAL-CONSUMER CONTRIBUTION AND GRANTS

1. A sum of `26,67,20,473 (previous year ` 25,74,47,878/-) towards depreciation on consumercontribution has been reversed under GH 77.150 (also refer to schedule 26).

Particulars Account Code

31-3-2012 `

31-3-2011 `

Cash credit limits with banks 50.1 4,426,289,060 1,794,673,312 Bank Over drafts 50.2Sub Total (A) 4,426,289,060 1,794,673,312 Loans for capital projectLoan from REC for Re-financing of IBRD Loans 53.302 & 53.303 101,061,305 119,885,250 Loan from PFC under R-APDRP 53.306 271,408,500 271,408,500 Loans from REC 53.300 & 53.301 9,713,308,207 9,243,406,557 Loans from Commercial Banks for Electrification Schemes 53.510 & 53.511 1,885,196,249 2,426,815,271 Repayment due to Commercial Banks for elect. Schemes

51.11033,333,334 -

Loan from REC for Procurement of material 53.518 & 53.519 2,348,484,848 - Add:-Repayment Due 51.138Add:-Interest Accrued and Due 51.238Sub Total-(B) 14,352,792,443 12,061,515,578 Secured Working Capital Loans from Commercial Banks 53.547 & 53.548

26,788,594,228 30,512,629,470 Repayment due 51.139 459,852,628 0 Interest accrued & due 51.239 305,247,281 Sub Total-(C) 27,553,694,137 30,512,629,470 Total (A+B+C) 46,332,775,641 44,368,818,361

Detail of Secured Working Capital Loans from Commercial Banks : -- 31-3-2012

` 31-3-2011

`- 17,104,298

3,332,163,003 3,468,059,632 1,776,469,191 2,115,730,702 2,027,262,194 1,983,429,322 1,950,711,261 2,370,746,323 1,631,970,749 796,191,109 4,723,115,586 5,654,355,327 1,898,419,382 2,231,748,844 2,133,468,669 2,833,275,369 4,318,303,355 5,558,665,883 1,245,598,278 1,400,893,411 1,999,963,382 1,999,876,434

211,001,807 82,552,816 27,248,446,857 30,512,629,470 305247281 - 27,553,694,138 30,512,629,470

Sanctioned LimitCredit Limit

availed 1,000,000,000 751,995,255 1,000,000,000 744,256,519

20,000,000 - 1,770,000,000 1,188,365,874 1,000,000,000 239,409,604 2,000,000,000 1,502,261,808

6,790,000,000 4,426,289,060

Central Bank of India, HisarDena Bank, HisarUCO Bank, Zirakpur

Punjab National Bank, HisarIndian Overseas Bank Panchkula

Oriental Bank of Commerce, Panchkula

Note 1:- Working Capital loans from the following Commercial Banks are secured against hypothecationof Book Debts/Receivables of the Nigam.

Note 3 :- Loans from commercial banks for electrification schemes is against the security of T&D assets of the Nigam.Note 4 :- Loan from REC for procurement of material is secured against hypothecation of T&D stores.

Note 2 :- Loan from REC for Refinancing of IBRD loan is secured against hypothecation of existing fixed assets of Operation Division Ch. Dadri to the extent of 130% of the loan amount.

Allahabad Bank, HisarCanara Bank, Hisar

Vijaya Bank HisarIndian Bank HisarHDFC Bank, Hisar

Name of Banks

State Bank of Patiala Hisar

In addition to this the following cash credit limits are arranged from commercial banks against the security of hypothecation of book debts/receivables of the Nigam

Name of Banks

Bank of Inida, Chandigarh

Interest accrued and due on W/Capital Loans

Dakshin Haryana Bijli Vitran Nigam Limited

SCHEDULE-4 SECURED LOANS

Total

Allahabad Bank Hisar

Total

Canara Bank, Hisar

Syndicate Bank HisarIndian Bank Hisar

Vijay Bank Hisar

OBC Panchkula

Particulars Account Code

31-3-2012 `

31-3-2011 `

A) State Government Loansi) World Bank Project 53.100 & 53.101 641,789,648 641,789,648 ii) Add: Interest Accured & due 51.261 20,755 1,552,753 iii)) NABARD Projects 53.400 & 53.401 7,343,800 23,030,400 iv) APDRP Projects 54.212 & 54.213 384,122,825 418,664,965 v)) PMGY Projects 53.516 & 53.517 10,155,535 11,044,710

vi) Repayment of loans-State Govt. 51.101 - 29,089,190 vii) Interest accrued and due on State Govt. Loans 51.207 - 25,409,533 Sub Total A 1,043,432,563 1,150,581,199 B) Loans from financial institution Loan from PFC 53.527 & 53.537 2,617,017,500 143,687,500 iii) Loan from NCR Planning Board 53.514 & 53.515 1,130,210,965 636,289,947 iv) Loan from REC against RGGVY Scheme 53.551 & 53.552 84,278,423 66,076,364 Sub Total B 3,831,506,888 846,053,811 Un-Secured Loans from Commercial Banks for working capital

53.512 & 53.5132,244,514,124 1,852,167,054

Add:-Repayment Due 51.221 19,637,468 - Sub Total C 2,264,151,592 1,852,167,054 Grand Total (A+B+C) 7,139,091,044 3,848,802,065

31-3-2012 `

31-3-2011 `

2,244,514,124 590,362,918 - 999,809,831 - 90,983,272 - 171,011,033

2,244,514,124 1,852,167,054

Detail of Un-Secured Loans from Commercial Banks for working capital.

Dakshin Haryana Bijli Vitran Nigam Limited

SCHEDULE-5 UNSECURED LOANS

Note:-1. The above loans have been classified as unsecured loans as no tangible security given to thelendersNote:-2 Repayment due within one year i.e during FY 2012-13 is ` 493.00 crore (previous year actualrepayment made ` 1109.61 crore)

Total

Name of Banks

Indian Overseas Bank HisarIndian Bank, HisarAllahabad Bank PanchkulaBank of India Panchkula

Particulars Account Code

31-3-2012 `

31-3-2011 `

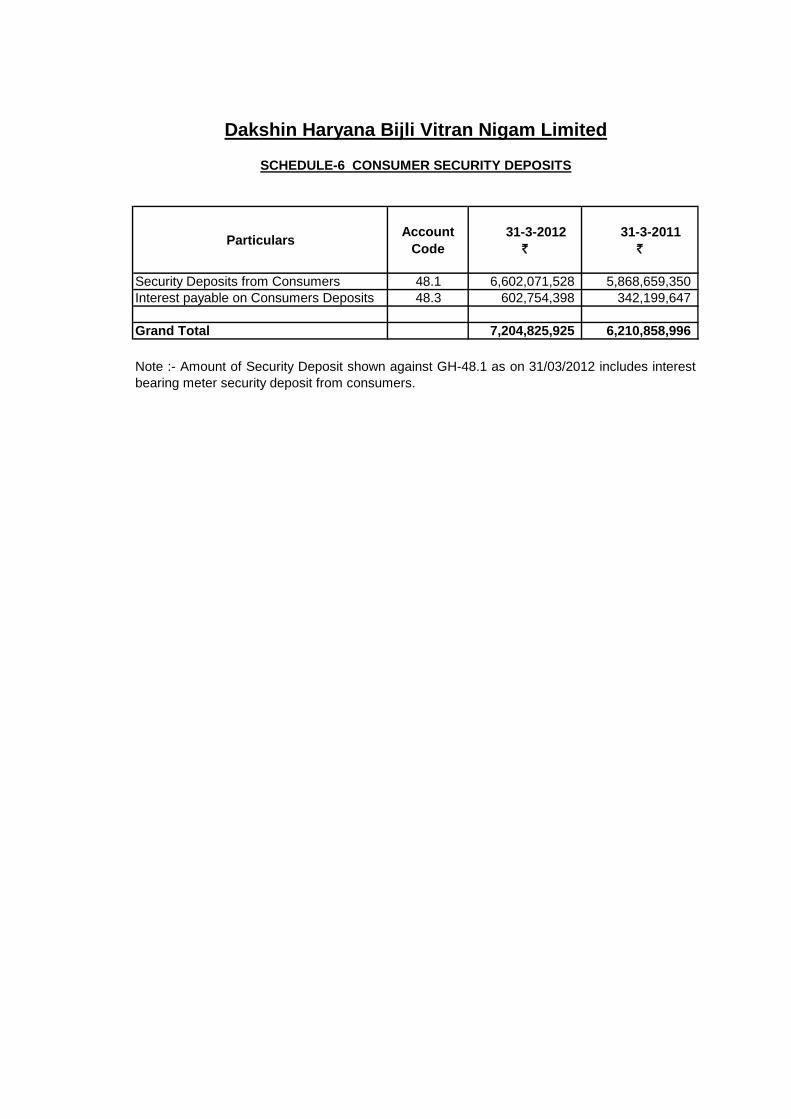

Security Deposits from Consumers 48.1 6,602,071,528 5,868,659,350 Interest payable on Consumers Deposits 48.3 602,754,398 342,199,647

Grand Total 7,204,825,925 6,210,858,996

Dakshin Haryana Bijli Vitran Nigam Limited

SCHEDULE-6 CONSUMER SECURITY DEPOSITS

Note :- Amount of Security Deposit shown against GH-48.1 as on 31/03/2012 includes interestbearing meter security deposit from consumers.

Sr.N

o.

Asset CategoryOpening Balances as on 1-4-2011

`

Addition during the year

Disposal during the year

At the end of year March 2012 `

Opening Balances as on

1-4-2011 `

Addition during the year

Disposal during the

year

At the end of year March 2012

Closing as on 31-3-2012

Closing as on 31-3-2011

1 2 3 4 5 6 7 8 9 10 11 12

1 Land 250,670,541 - - 250,670,541 - - - 250,670,541 250,670,541

2 Building and Civil St t

1,032,709,866 192,884,872 - 1,225,594,738 235,591,162 26,061,915 261,653,077 963,941,660 797,118,703

3Plant & Machinery-T&D

33,513,585,814 5,977,586,663 102,969,185 39,388,203,291 9,615,470,514 1,354,014,023 34,841,063 10,934,643,474 28,453,559,817 23,898,115,300

4 Vehicles 122,483,163 1,584,429 4,617,892 119,449,699 94,936,324 5,241,826 4,156,103 96,022,047 23,427,652 27,546,838

5Furniture & Fixtures and Office Equipments 121,563,182 32,042,603 539,897 153,065,888 43,953,822 6,103,945 273,587 49,784,180 103,281,708 77,609,360

Total 35,041,012,565 6,204,098,567 108,126,975 41,136,984,157 9,989,951,823 1,391,421,709 39,270,753 11,342,102,779 29,794,881,379 25,051,060,742

Previous Year 27,357,699,512 7,794,676,635 111,363,582 35,041,012,565 9,041,621,485 979,199,641 30,869,303 9,989,951,823

Working Note of Depreciation charged during the year 2011-12

Total depreciation during the year 1169021709

2224000001391421709

Note-3:-The Assets created with the help of Govt. Grant amounting to ` 142,66,09,059/-(Prevoius Year `122,28,59,654/-) included in the gross block against Plant & Machinery (T&D) category and depreciation of` 4,12,90,871/- @ 3.38% average rate of depreciation on T&D category of assets (Previous Year ` 3,74,65,756/- @ 3.63%) Charged on the opening balance of assets.

Depreciation accounted for during the year on the assets put into use in the earlier years and capitalised in the books of accounts in later years. Total depreciation during the year

Note-5:- An additional depreciation amounting to ` 4,91,726/- has been provided on Assets providing 33 KV S/Stn. Nagthala, (under (OP) Divn, No.-II Hisar) energised during FY 2008-09 but capitialized during FY 2009-10.

Note-4:- The Land for 33 KV Sub Station Chang donated by Gram Panchayat, Village Chang is recorded at nominal value of ` 100/- in above assets.

Note-1:-Since the Company is engaged in the Electricity Distribution business and all the assets are used in this business only, the function-wise details of assets are not required.

Note-2:-The Assets created out of consumers contribution amounting to ` 919,19,84,297/-(Prevoius Year `789,91,23,972/-) included in the gross block against Plant & Machinery (T&D) category and depreciationof ` 26,67,20,473,/- @ 3.38% average rate of depreciation on T&D category of assets (Previous Year ` 25,74,47,878/- @ 3.63%) Charged on the opening balance of assets.

Dakshin Haryana Bijli Vitran Nigam Limited

SCHEDULE-7 CATEGORY-WISE BREAKUP OF FIXED ASSETS

Net Block

(Amount in `)

Gross Block Provision for Depreciation

Particulars Account Code

31-3-2012 `

31-3-2011 `

DistributionCapital Work in progress 14 5,062,838,260 7,370,813,342 Total GH-14 5,062,838,260 7,370,813,342 2. Advances to Suppliers/Contractors(capital)a) Interest bearing 25.1 12,949 12,949 b) Interest free 25.5 145,988,553 513,246,443 c) Material received but not taken in books

25.6 1,442 1,442

d) Less : Provisions 46 20,584 20,584 Total(a+b+c-d) 145,982,360 513,240,250 4. Grand Total (1+2) 5,208,820,620 7,884,053,591

Working Note on Capital Work-in-Progress:2011-12 2010-2011

7,370,813,342 8,945,637,072 3,222,053,653 5,312,888,339

10,592,866,994 14,258,525,411

- 2,595,180 192,884,872 85,730,795

5,977,586,663 7,697,659,899 1,584,429 1,750,796

32,042,603 6,939,966 6,204,098,567 7,794,676,636 4,388,768,427 6,463,848,775

674,069,833 906,964,567 5,062,838,260 7,370,813,342

Added during the YearTotal (A):

Less: Transfer to Fixed Assets

CWIP at the beginning of the year

Dakshin Haryana Bijli Vitran Nigam Limited

SCHEDULE-8 CAPITAL WORK IN PROGRESS

1. Land2. Building and Civil Structures3. Plant & Machinery-T&D4. Vehicles

Closing CWIP at the year end

5. Furniture and FixturesTotal Transferred to Fixed Assets (B):

Net CWIP (C=A-B): Add: Interest Capitalized during the Year

Particulars Account Code

31-3-2012 `

31-3-2011 `

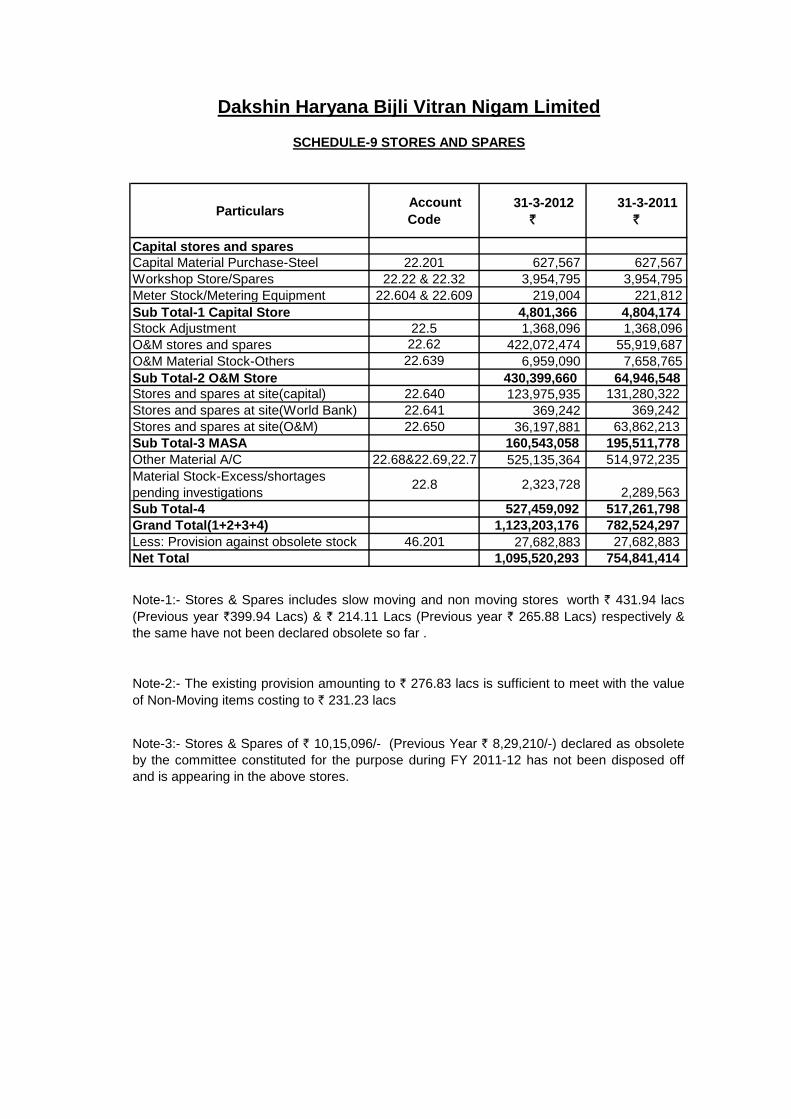

Capital stores and sparesCapital Material Purchase-Steel 22.201 627,567 627,567 Workshop Store/Spares 22.22 & 22.32 3,954,795 3,954,795 Meter Stock/Metering Equipment 22.604 & 22.609 219,004 221,812 Sub Total-1 Capital Store 4,801,366 4,804,174 Stock Adjustment 22.5 1,368,096 1,368,096 O&M stores and spares 22.62 422,072,474 55,919,687 O&M Material Stock-Others 22.639 6,959,090 7,658,765 Sub Total-2 O&M Store 430,399,660 64,946,548 Stores and spares at site(capital) 22.640 123,975,935 131,280,322 Stores and spares at site(World Bank) 22.641 369,242 369,242 Stores and spares at site(O&M) 22.650 36,197,881 63,862,213 Sub Total-3 MASA 160,543,058 195,511,778 Other Material A/C 22.68&22.69,22.7 525,135,364 514,972,235 Material Stock-Excess/shortages pending investigations 22.8 2,323,728 2,289,563 Sub Total-4 527,459,092 517,261,798 Grand Total(1+2+3+4) 1,123,203,176 782,524,297 Less: Provision against obsolete stock 46.201 27,682,883 27,682,883 Net Total 1,095,520,293 754,841,414

Note-1:- Stores & Spares includes slow moving and non moving stores worth ` 431.94 lacs(Previous year `399.94 Lacs) & ` 214.11 Lacs (Previous year ` 265.88 Lacs) respectively &the same have not been declared obsolete so far .

Note-3:- Stores & Spares of ` 10,15,096/- (Previous Year ` 8,29,210/-) declared as obsoleteby the committee constituted for the purpose during FY 2011-12 has not been disposed offand is appearing in the above stores.

Dakshin Haryana Bijli Vitran Nigam Limited

SCHEDULE-9 STORES AND SPARES

Note-2:- The existing provision amounting to ` 276.83 lacs is sufficient to meet with the valueof Non-Moving items costing to ` 231.23 lacs

Particulars Account Code 31-3-2012 `

31-3-2011 `

Sundry Debtors for Sale of Power23.1001-81,

3001-81& 3101-81

2,599,512,919 2,985,715,814

Sundry Debtors for Fixed Charges23.1101-81, .3201-81 &

3301-81 403,616,670 141,739,906

Sundry Debtors for Electricity Duty23.2001-

81,3401-81& 3501-81

658,880,133 724,601,638

Sundry Debtors for Municipal Tax23.2301-81,

23.3601-81&3701-81

206,101,567 176,728,762

Sundry Debtors for Surcharge

23.1701-81, 23.7701-

81,7801-81 & 5301-81

11,880,875,393 9,976,673,836

Provision for Un-billed Revenue 23.4 1,440,752,491 1,379,665,135 Sundry Debtors for Inter State Sale of power 23.6 1,796,499,110 1,637,459,475

Dues from Permanently Disconnected consumersA) Sale of Power 23.5001-81 1,114,822,409 683,548,441 B) Electricity Duty 23.5401-81 109,124,929 100,028,781 C) Municipal Tax 23.5601-81 14,478,880 13,736,159 Sundry Debtors for Misc. Receipts from consumers 23.7 - 11,243,550

Debtors for FSA

23.1301-81, 23.7301-

81,7401-81 & 5201-81

1,561,026,108 1,313,544,589

Sub Total 21,785,690,608 19,144,686,085 Less: Provision for doubtful dues from consumers other than surcharge (Except 23.9301 to 23.9334)

23.9 1,796,123,851 1,796,123,851

Less: Surcharge levied but not realised 23.934 7,468,094,340 5,555,902,910 Net Total 12,521,472,417 11,792,659,323 Out of the aboveDebtors for more than six months 20,218,758,697 17,478,150,004 Other Debtors 1,566,931,911 1,666,536,081 Sub Total 21,785,690,608 19,144,686,085 Less: Provision for doubtful dues from consumers 9,264,218,191 7,352,026,761

Net Debtors 12,521,472,417 11,792,659,323

(a) Debts considered good and in respect of which company is fully Secured 7,204,825,925 6,210,858,996

(b) Debts considered good for which the company holds no security other than debtors personal security

5,316,646,492 5,581,800,327

(c) Debts considered doubtful or bad 9,264,218,191 7,352,026,761 Total 21,785,690,608 19,144,686,085

Notes:-

2.The Sundry Debtors for surcharge prior to 9/2003 includes in the Sundry Debtors for Sale of Power.

Dakshin Haryana Bijli Vitran Nigam Limited

SCHEDULE-10 SUNDRY DEBTORS

1. Existing provision for bad & doubtful debts in respect of Sale of Power is sufficient to meet with theamount of bad debts on this account.

Particulars Account Code

31-3-2012 `

31-3-2011 `

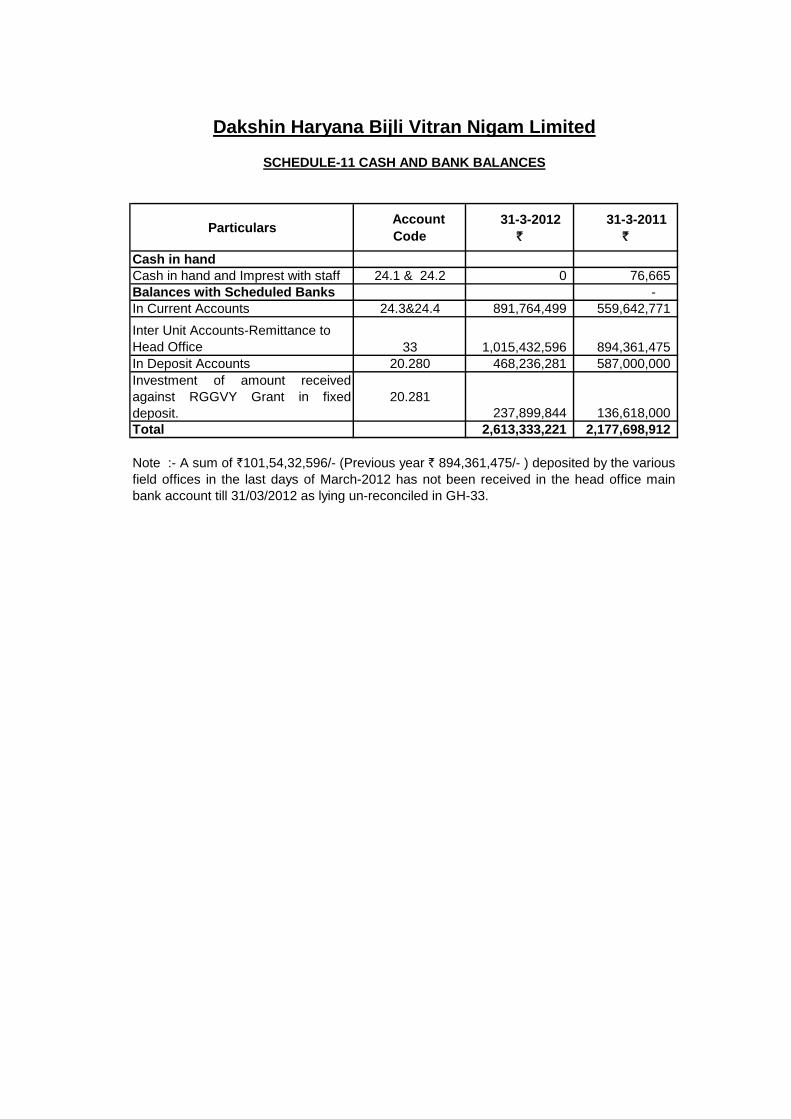

Cash in handCash in hand and Imprest with staff 24.1 & 24.2 0 76,665 Balances with Scheduled Banks - In Current Accounts 24.3&24.4 891,764,499 559,642,771 Inter Unit Accounts-Remittance to Head Office 33 1,015,432,596 894,361,475 In Deposit Accounts 20.280 468,236,281 587,000,000 Investment of amount receivedagainst RGGVY Grant in fixeddeposit.

20.281237,899,844 136,618,000

Total 2,613,333,221 2,177,698,912

Note :- A sum of `101,54,32,596/- (Previous year ` 894,361,475/- ) deposited by the variousfield offices in the last days of March-2012 has not been received in the head office mainbank account till 31/03/2012 as lying un-reconciled in GH-33.

Dakshin Haryana Bijli Vitran Nigam Limited

SCHEDULE-11 CASH AND BANK BALANCES

Particulars Account Code 31-3-2012 `

31-3-2011 `

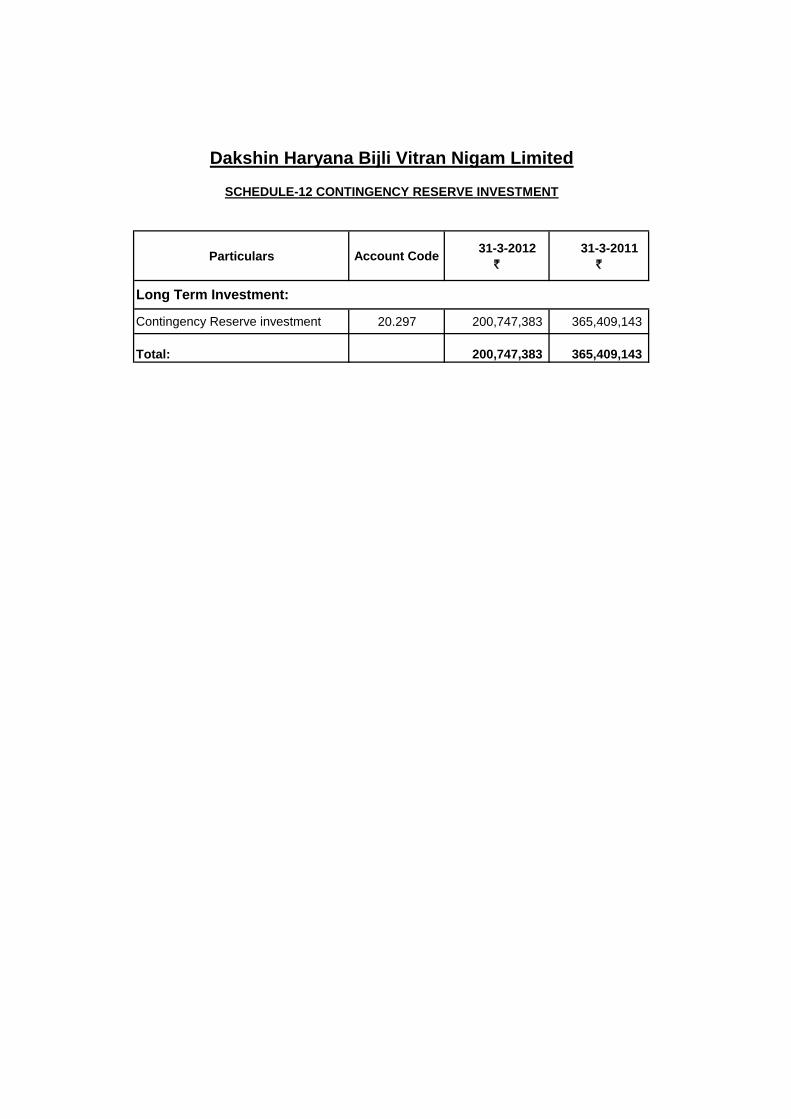

Contingency Reserve investment 20.297 200,747,383 365,409,143

Total: 200,747,383 365,409,143

Long Term Investment:

Dakshin Haryana Bijli Vitran Nigam Limited

SCHEDULE-12 CONTINGENCY RESERVE INVESTMENT

Particulars Account Code 31-3-2012 `

31-3-2011 `

House Building Advance 27.101 225,652,210 150,694,277 Scooter Advance 27.102 17,598,130 13,544,188 Car Advance 27.103 20,213,002 13,966,310 Total Secured Loans & Advances 263,463,342 178,204,775

Advances for Operation & Mtc. Supplies 26.1 to 26.9 11,589,722 34,391,643

Cycle, Marriage & Computer Advance27.104, 107,

108&109 129,710,054 117,485,561 TA & Pay Advance (interest free) 27.201&202 319,885 197,105 Festival, Wheat advance, Other loans & Adv. Of GIS Premium (interest free)

27.203,204,207, 208 & 209 18,299,099

12,400,005 Loans and advances to Licensees 27.3 814,604 814,604 Advance income Tax Deduction at source except 27.411

27.4 Except 27.411 27,767,212 21,951,754

Advance Fringe Benefit Tax deposited with I.T. Deptt. 27.411 85,986,715 85,986,715 Loans and advances -others 27.8 581,653 518,653 Total Un-Secured Loans & Advances 275,068,945 273,746,041 Less:Provision for doubtful loans and advances

27.9 & 46.218-221 2,314,070

2,314,070 Net Un-Secured Loans & Advances 272,754,875 271,431,971 Total Loan & Advances (A & B) 536,218,217 449,636,746

( A) Secured Loans & Advances

Dakshin Haryana Bijli Vitran Nigam Limited

SCHEDULE-13 LOANS AND ADVANCES(Considered good unless otherwise stated)

Particulars Account Code

31-3-2012 `

31-3-2011 `

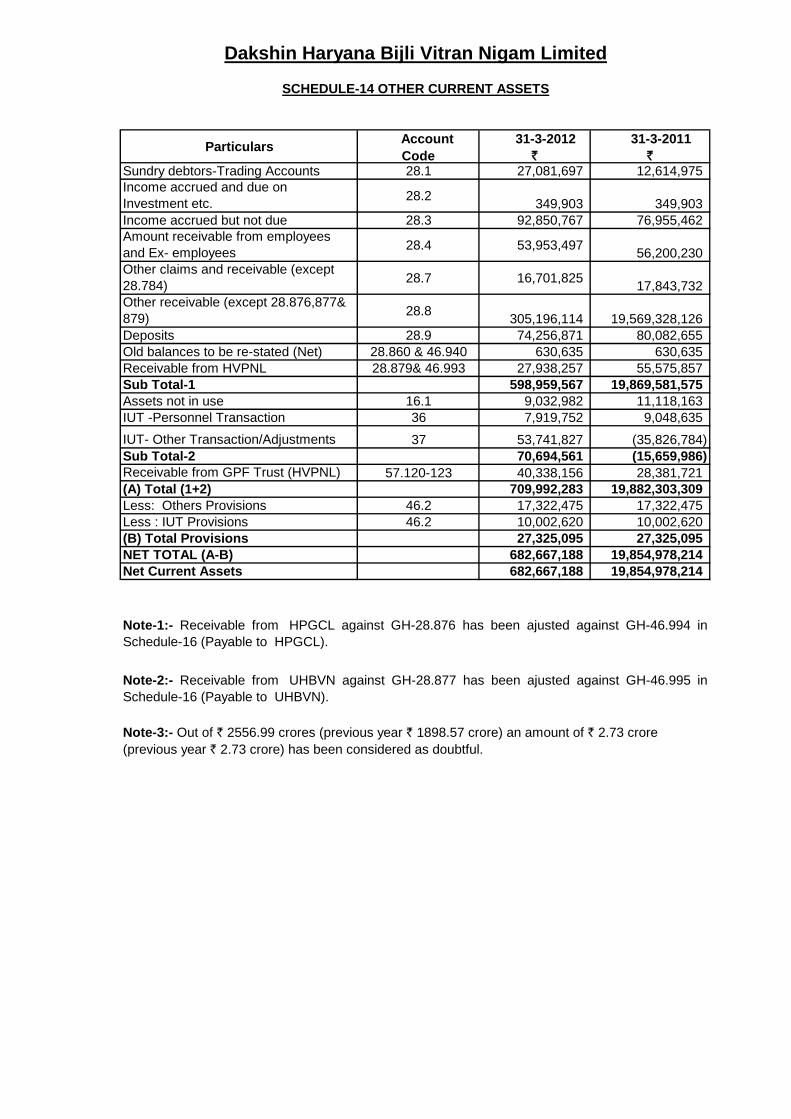

Sundry debtors-Trading Accounts 28.1 27,081,697 12,614,975 Income accrued and due on Investment etc. 28.2 349,903 349,903 Income accrued but not due 28.3 92,850,767 76,955,462 Amount receivable from employees and Ex- employees 28.4 53,953,497 56,200,230 Other claims and receivable (except 28.784) 28.7 16,701,825 17,843,732 Other receivable (except 28.876,877& 879) 28.8 305,196,114 19,569,328,126 Deposits 28.9 74,256,871 80,082,655 Old balances to be re-stated (Net) 28.860 & 46.940 630,635 630,635 Receivable from HVPNL 28.879& 46.993 27,938,257 55,575,857 Sub Total-1 598,959,567 19,869,581,575 Assets not in use 16.1 9,032,982 11,118,163 IUT -Personnel Transaction 36 7,919,752 9,048,635 IUT- Other Transaction/Adjustments 37 53,741,827 (35,826,784) Sub Total-2 70,694,561 (15,659,986) Receivable from GPF Trust (HVPNL) 57.120-123 40,338,156 28,381,721 (A) Total (1+2) 709,992,283 19,882,303,309 Less: Others Provisions 46.2 17,322,475 17,322,475 Less : IUT Provisions 46.2 10,002,620 10,002,620 (B) Total Provisions 27,325,095 27,325,095 NET TOTAL (A-B) 682,667,188 19,854,978,214 Net Current Assets 682,667,188 19,854,978,214

Note-3:- Out of ` 2556.99 crores (previous year ` 1898.57 crore) an amount of ` 2.73 crore (previous year ` 2.73 crore) has been considered as doubtful.

Dakshin Haryana Bijli Vitran Nigam Limited

SCHEDULE-14 OTHER CURRENT ASSETS

Note-1:- Receivable from HPGCL against GH-28.876 has been ajusted against GH-46.994 inSchedule-16 (Payable to HPGCL).

Note-2:- Receivable from UHBVN against GH-28.877 has been ajusted against GH-46.995 inSchedule-16 (Payable to UHBVN).

Particulars Account Code

31-3-2012 `

31-3-2011 `

Deffered subsidy receivable from GOH 28.641 - 5,936,031,540 Amount receivable from GOH on account of EAWS-2005 28.890 - 9,428,015

Total - 5,945,459,555

Dakshin Haryana Bijli Vitran Nigam Limited

SCHEDULE-15 RECEVIABLE FROM GOH FOR SUBSIDY INCLUDING INTEREST

Particulars Account Code

31-3-2012 `

31-3-2011 `

Liability for purchase of power to HVPNL (Wheeling Chaeges) 41.156 1,724,289,419 968,655,970

Liability for purchase of power to others41.1, 41.2& 41.3 (except 41.156 28,647,427,976 11,909,213,025

Total liability for purchase of power (Sub Total-1) 30,371,717,395 12,877,868,995 Liability for Capital supplies/Works 42.1 to 42.3 790,395,796 752,279,413 Liability for O&M supplies/Works 43.1 to 43.4 377,001,090 223,707,542 Staff related Liabilities and provisions 44.1 to 44.4 1,720,182,367 1,697,106,618 Interest due on staff security 51.209 15,059 17,004 Sub Total-2 2,887,594,312 2,673,110,577 Deposits and retention from suppliers and contractors 46.1,46.2 1,606,532,805 1,840,949,326

Electricity Duty Payable to Govt. 46.3 720,474,822 641,046,530 Liability for expenses 46.4 145,625,435 109,238,154 Municipal Tax payable 46.501 374,971,513 266,727,248 Amount payable to Govt. on account of componding of offence in case theft of elecy. 46.502

155,646,322 107,628,434

Interest accrued but not due on borrowings 46.7 268,227,646 150,035,817 Other Liabilities and provision (except 46.993, 994 & 995) 46.9 362,364,802 3,722,817,463

Payable to HPGCL(Other than Power Purchase) 46.994& 28.876 45,745,165 44,945,165

Payable to UHBVNL(Other than Power Purchase) 46.995 & 28.877 435,960,769 869,318,783

Sub Total-3 4,115,549,280 7,752,706,921

Deposits for electrification/ service connection 47 1,183,310,305 994,522,466 Inter Units Accounts - Funds Transfer from Head Office 34 8,468,819 110,246,337 Payable to Pension Trust (HVPNL) 57.131 & 28.784 4,076,151,972 4,176,806,927 Payable to GPF Trust (DHBVNL) 57.160-163 6,248,463 9,069,308 Payable to Pension Trust (DHBVNL) 57.141&142 39,999,000 20,000,000 Sub Total-4 5,314,178,558 5,310,645,037 Grand Total (1 to 4) 42,689,039,545 28,614,331,529

Note-1:- Payable to HVPNL against GH-46.993 has been ajusted against GH-28.879-Schedule-14(Receivable from HVPNL).

Dakshin Haryana Bijli Vitran Nigam Limited

SCHEDULE-16 CURRENT LIABILITIES AND PROVISIONS

Particulars Account Code

31-3-2012 `

31-3-2011 `

Deffered expenditure (to the extent yet to be written off) 18.4 - 236,304,000

Total: - 236,304,000

Regulatory Assets (Not written off) 18.3 - 1,163,448,000 Total: - 1,163,448,000

Dakshin Haryana Bijli Vitran Nigam Limited

SCHEDULE-17 MISCELLANEOUS EXPENDITURE

Sr.No. Particulars Account Code 31-3-2012 `

31-3-2011 `

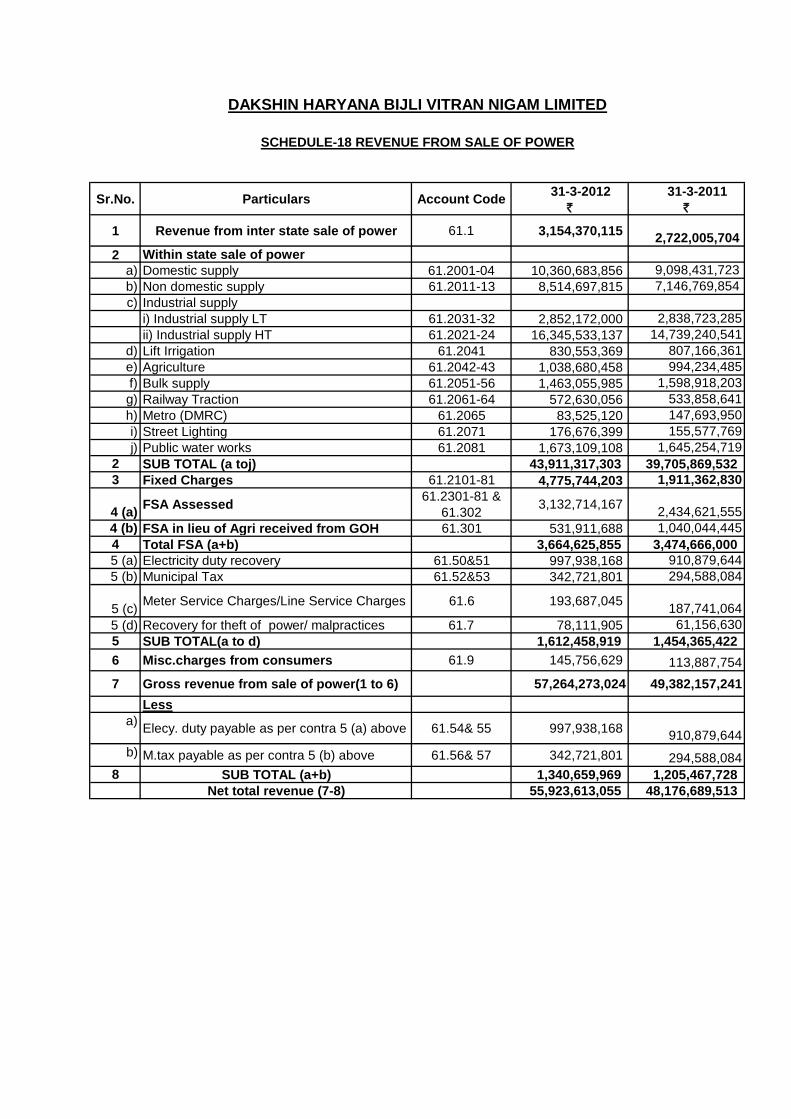

1 Revenue from inter state sale of power 61.1 3,154,370,115 2,722,005,704 2 Within state sale of power

a) Domestic supply 61.2001-04 10,360,683,856 9,098,431,723 b) Non domestic supply 61.2011-13 8,514,697,815 7,146,769,854 c) Industrial supply

i) Industrial supply LT 61.2031-32 2,852,172,000 2,838,723,285 ii) Industrial supply HT 61.2021-24 16,345,533,137 14,739,240,541

d) Lift Irrigation 61.2041 830,553,369 807,166,361 e) Agriculture 61.2042-43 1,038,680,458 994,234,485 f) Bulk supply 61.2051-56 1,463,055,985 1,598,918,203 g) Railway Traction 61.2061-64 572,630,056 533,858,641 h) Metro (DMRC) 61.2065 83,525,120 147,693,950 i) Street Lighting 61.2071 176,676,399 155,577,769 j) Public water works 61.2081 1,673,109,108 1,645,254,719

2 SUB TOTAL (a toj) 43,911,317,303 39,705,869,532 3 Fixed Charges 61.2101-81 4,775,744,203 1,911,362,830

4 (a) FSA Assessed 61.2301-81 & 61.302 3,132,714,167 2,434,621,555

4 (b) FSA in lieu of Agri received from GOH 61.301 531,911,688 1,040,044,445 4 Total FSA (a+b) 3,664,625,855 3,474,666,000 5 (a) Electricity duty recovery 61.50&51 997,938,168 910,879,644 5 (b) Municipal Tax 61.52&53 342,721,801 294,588,084

5 (c) Meter Service Charges/Line Service Charges 61.6 193,687,045 187,741,064 5 (d) Recovery for theft of power/ malpractices 61.7 78,111,905 61,156,630 5 SUB TOTAL(a to d) 1,612,458,919 1,454,365,422 6 Misc.charges from consumers 61.9 145,756,629 113,887,754 7 Gross revenue from sale of power(1 to 6) 57,264,273,024 49,382,157,241

Lessa) Elecy. duty payable as per contra 5 (a) above 61.54& 55 997,938,168 910,879,644 b) M.tax payable as per contra 5 (b) above 61.56& 57 342,721,801 294,588,084

8 SUB TOTAL (a+b) 1,340,659,969 1,205,467,728 Net total revenue (7-8) 55,923,613,055 48,176,689,513

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITED

SCHEDULE-18 REVENUE FROM SALE OF POWER

Sr. No. Particulars Account Code

31-3-2012 `

31-3-2011 `

1 Interest on staff loans & advances 62.210 26,992,417 22,588,742

2 Interest on fixed deposits with banks & company etc. 62.222 49,038,925 12,201,370

3 Interest on other investments 62.229 38,762,540 37,812,335

4 Delayed payment charges from consumers (surcharge levied) 62.2401-2481 494,328,820 394,882,363

7 Income from trading/sale of scrap 62.3 - 24,597,967 8 Income from staff welfare activities 62.6 518,417 492,232 9 Misc.receipts(except 62.901&62.908) 62.8 & 62.9 340,344,764 603,331,099 10 Rent from Residential Building 62.901,62.908 3,792,325 3,410,494

Grand Total: 953,778,208 1,099,316,602

Note:-1

Note:-2

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITED

SCHEDULE -19 OTHER INCOME

Interest on fixed deposit with banks amounting to ` 4,90,38,925/- (previous year ` 1,22,01,370/-) represents gross amount and includes an amount of TDS of `35,03,995/-Interest on investment relating to contingency reserve invested with commercial banks amounting to `3,87,62,540/- (previous year ` 2,25,88,742/-) respresents gross amount and includes an amount of TDS `38,75,946/- .

Sr. No. Particulars Account

Code 31-3-2012

` 31-3-2011

`

1 Prior Period Income Other excess provision in prior periods 65.8 742,409,441 313,687,100 Sub Total-1 742,409,441 313,687,100

2 Prior period Expensesa)Short provision for power purchased in previous years 83.1 22,725,686,221 -

a) Employee Cost relating to Previous Year 83.5 - 21,210 b) Prior period depreciation charges 83.6 222,400,000 - c) Other charges relating to previous years 83.8 6,723,438,112 - d) Refund of Income to Prior Period 83.9 199,400,000 - Sub Total-2 (a to d) 29,870,924,333 21,210 Net Prior Period Credit/(Charges) (1-2) (29,128,514,892) 313,665,890

Detail of (83.1) Short provision for power purchase

16,864,386,221 5,861,300,000

22,725,686,221

Detail of (83.8) Other charges relating to previous years

6,702,731,540

9,428,015 35,007

11,243,550 6,723,438,112

Detail of (83.9) Refund of income to prior periodi) Excess subsidy booked in previous year 4,000,000

195,400,000 Total 83.9 199,400,000

Amount of FSA excluded from power purchase cost in previous years

Total 83.1

Subsidy shown as receivable from GOH but not provided in the budget by GOH.

Interest on provident fund lessor provided in FY 2009-10

Amount waived off under EAWS-2005 but not paid or provided in budget by GOH.

Difference of power purchase on reconciliation with HPGCL

Amount of sundry debtors (misc. receipt from consumers) lying un-identified since formation of companyTotal 83.8

ii) Delay in penalty treated as Rev. income during FY 2009-10

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITED

SCHEDULE-20 Prior Period Adjustment

Sr. No. Particular Account Code

31-3-2012 `

31-3-2011 `

Revenue subsidies & grants 63.1

1 Subsidies from State Govt. for supply to agriculture tubewells at subsidised tariff 63.140 13,792,600,000 12,803,300,000

SUB TOTAL-1 -

2 Subsidies against loss on a\c of flood,fire cyclone etc. 63.2 - 34,200,000

TOTAL 13,792,600,000 12,837,500,000

SCHEDULE -21 REVENUE SUBSIDIES & GRANT

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITED

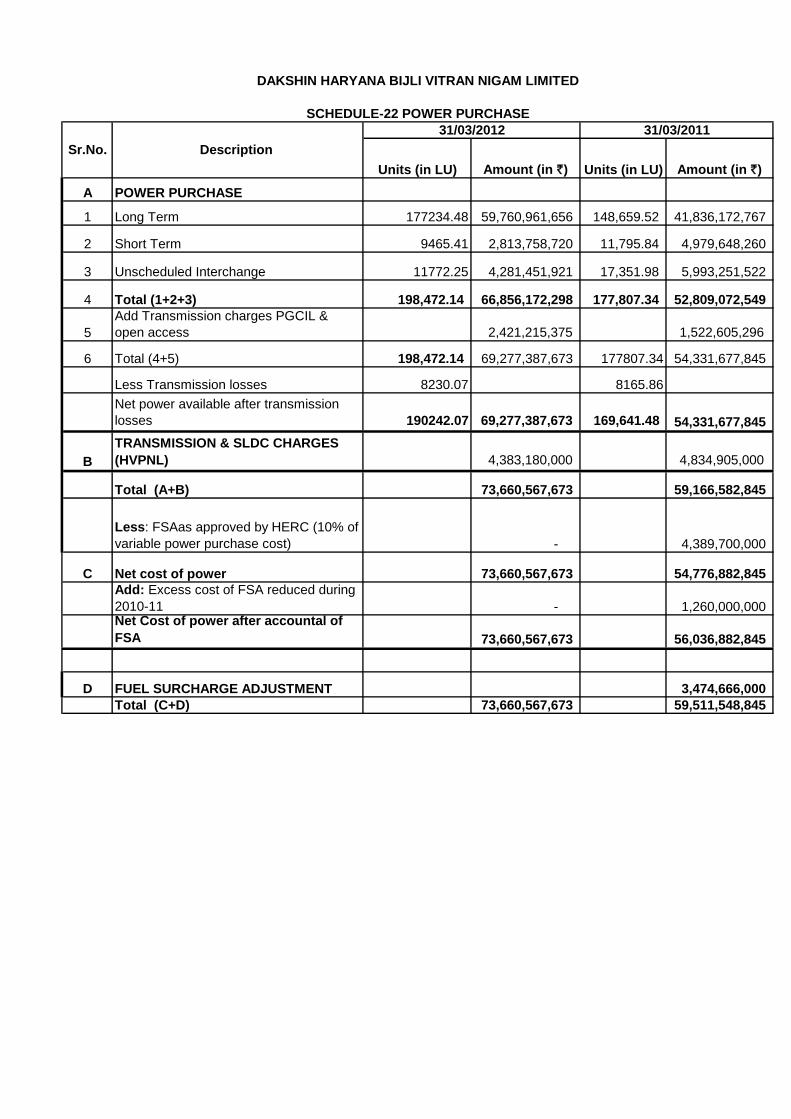

Units (in LU) Amount (in `) Units (in LU) Amount (in `)

A POWER PURCHASE

1 Long Term 177234.48 59,760,961,656 148,659.52 41,836,172,767

2 Short Term 9465.41 2,813,758,720 11,795.84 4,979,648,260

3 Unscheduled Interchange 11772.25 4,281,451,921 17,351.98 5,993,251,522

4 Total (1+2+3) 198,472.14 66,856,172,298 177,807.34 52,809,072,549

5Add Transmission charges PGCIL & open access 2,421,215,375 1,522,605,296

6 Total (4+5) 198,472.14 69,277,387,673 177807.34 54,331,677,845

Less Transmission losses 8230.07 8165.86Net power available after transmission losses 190242.07 69,277,387,673 169,641.48 54,331,677,845

BTRANSMISSION & SLDC CHARGES (HVPNL) 4,383,180,000 4,834,905,000

Total (A+B) 73,660,567,673 59,166,582,845

Less: FSAas approved by HERC (10% of variable power purchase cost) - 4,389,700,000

C Net cost of power 73,660,567,673 54,776,882,845 Add: Excess cost of FSA reduced during 2010-11 - 1,260,000,000 Net Cost of power after accountal of FSA 73,660,567,673 56,036,882,845

D FUEL SURCHARGE ADJUSTMENT 3,474,666,000 Total (C+D) 73,660,567,673 59,511,548,845

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITED

SCHEDULE-22 POWER PURCHASE

Sr.No. Description 31/03/201131/03/2012

Sr.No. Particulars Account Code

31-3-2012 `

31-3-2011 `

1 Plant & machinery-T&D 74.1 150,720,810 115,076,543 2 Buildings 74.2 17,844,941 28,194,827 3 Civil works 74.3 2,019,841 1,376,518 4 Lines cable net work etc. 74.5 211,187,277 211,302,429 5 Vehicles 74.6 8,354,252 7,826,085 6 Furniture & fixture 74.7 40,100 13,275 7 Office equipments 74.8 111,524 938,375

Grand Total: 390,278,745 364,728,051

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITED

SCHEDULE -23 REPAIR & MAINTENANCE

Sr. No. Particulars Account

Code 31-3-2012

` 31-3-2011

`

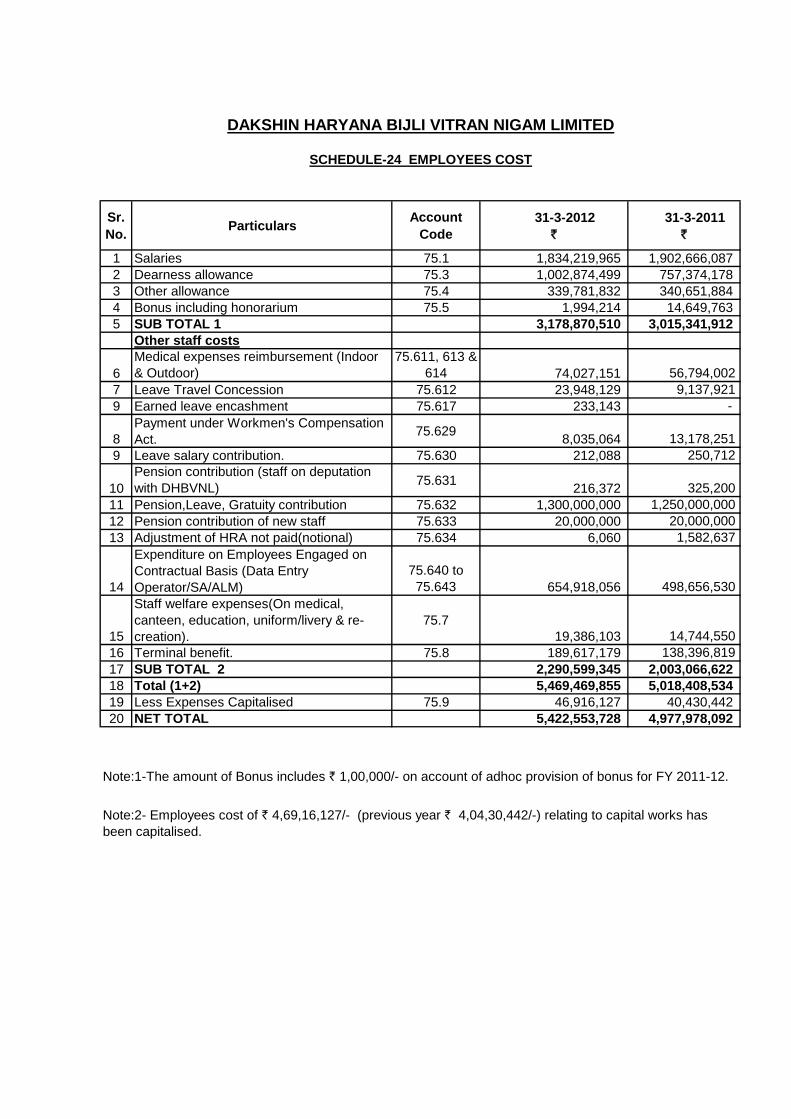

1 Salaries 75.1 1,834,219,965 1,902,666,087 2 Dearness allowance 75.3 1,002,874,499 757,374,178 3 Other allowance 75.4 339,781,832 340,651,884 4 Bonus including honorarium 75.5 1,994,214 14,649,763 5 SUB TOTAL 1 3,178,870,510 3,015,341,912

Other staff costs

6Medical expenses reimbursement (Indoor & Outdoor)

75.611, 613 & 614 74,027,151 56,794,002

7 Leave Travel Concession 75.612 23,948,129 9,137,921 9 Earned leave encashment 75.617 233,143 -

8Payment under Workmen's Compensation Act. 75.629 8,035,064 13,178,251

9 Leave salary contribution. 75.630 212,088 250,712

10Pension contribution (staff on deputation with DHBVNL) 75.631 216,372 325,200

11 Pension,Leave, Gratuity contribution 75.632 1,300,000,000 1,250,000,000 12 Pension contribution of new staff 75.633 20,000,000 20,000,000 13 Adjustment of HRA not paid(notional) 75.634 6,060 1,582,637

14

Expenditure on Employees Engaged on Contractual Basis (Data Entry Operator/SA/ALM)

75.640 to 75.643 654,918,056 498,656,530

15

Staff welfare expenses(On medical, canteen, education, uniform/livery & re-creation).

75.719,386,103 14,744,550

16 Terminal benefit. 75.8 189,617,179 138,396,819 17 SUB TOTAL 2 2,290,599,345 2,003,066,622 18 Total (1+2) 5,469,469,855 5,018,408,534 19 Less Expenses Capitalised 75.9 46,916,127 40,430,442 20 NET TOTAL 5,422,553,728 4,977,978,092

Note:2- Employees cost of ` 4,69,16,127/- (previous year ` 4,04,30,442/-) relating to capital works has been capitalised.

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITED

SCHEDULE-24 EMPLOYEES COST

Note:1-The amount of Bonus includes ` 1,00,000/- on account of adhoc provision of bonus for FY 2011-12.

Sr. No. Particulars Account Code 31-3-2012

` 31-3-2011

`

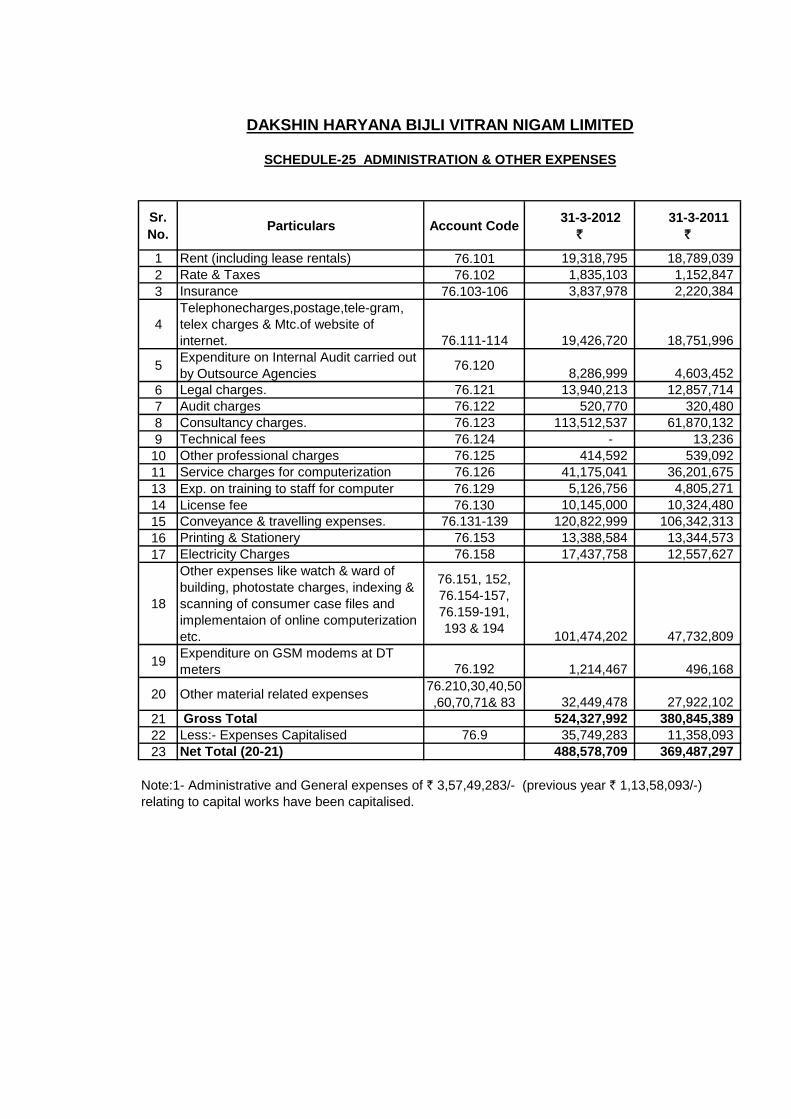

1 Rent (including lease rentals) 76.101 19,318,795 18,789,039 2 Rate & Taxes 76.102 1,835,103 1,152,847 3 Insurance 76.103-106 3,837,978 2,220,384

4Telephonecharges,postage,tele-gram, telex charges & Mtc.of website of internet. 76.111-114 19,426,720 18,751,996

5 Expenditure on Internal Audit carried out by Outsource Agencies 76.120 8,286,999 4,603,452

6 Legal charges. 76.121 13,940,213 12,857,714 7 Audit charges 76.122 520,770 320,480 8 Consultancy charges. 76.123 113,512,537 61,870,132 9 Technical fees 76.124 - 13,236 10 Other professional charges 76.125 414,592 539,092 11 Service charges for computerization 76.126 41,175,041 36,201,675 13 Exp. on training to staff for computer 76.129 5,126,756 4,805,271 14 License fee 76.130 10,145,000 10,324,480 15 Conveyance & travelling expenses. 76.131-139 120,822,999 106,342,313 16 Printing & Stationery 76.153 13,388,584 13,344,573 17 Electricity Charges 76.158 17,437,758 12,557,627

18

Other expenses like watch & ward of building, photostate charges, indexing & scanning of consumer case files and implementaion of online computerization etc.

76.151, 152, 76.154-157, 76.159-191, 193 & 194 101,474,202 47,732,809

19 Expenditure on GSM modems at DT meters 76.192 1,214,467 496,168

20 Other material related expenses 76.210,30,40,50,60,70,71& 83 32,449,478 27,922,102

21 Gross Total 524,327,992 380,845,389 22 Less:- Expenses Capitalised 76.9 35,749,283 11,358,093 23 Net Total (20-21) 488,578,709 369,487,297

SCHEDULE-25 ADMINISTRATION & OTHER EXPENSES

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITED

Note:1- Administrative and General expenses of ` 3,57,49,283/- (previous year ` 1,13,58,093/-) relating to capital works have been capitalised.

Sr. No. Particulars Account Code 31-3-2012

` 31-3-2011

`

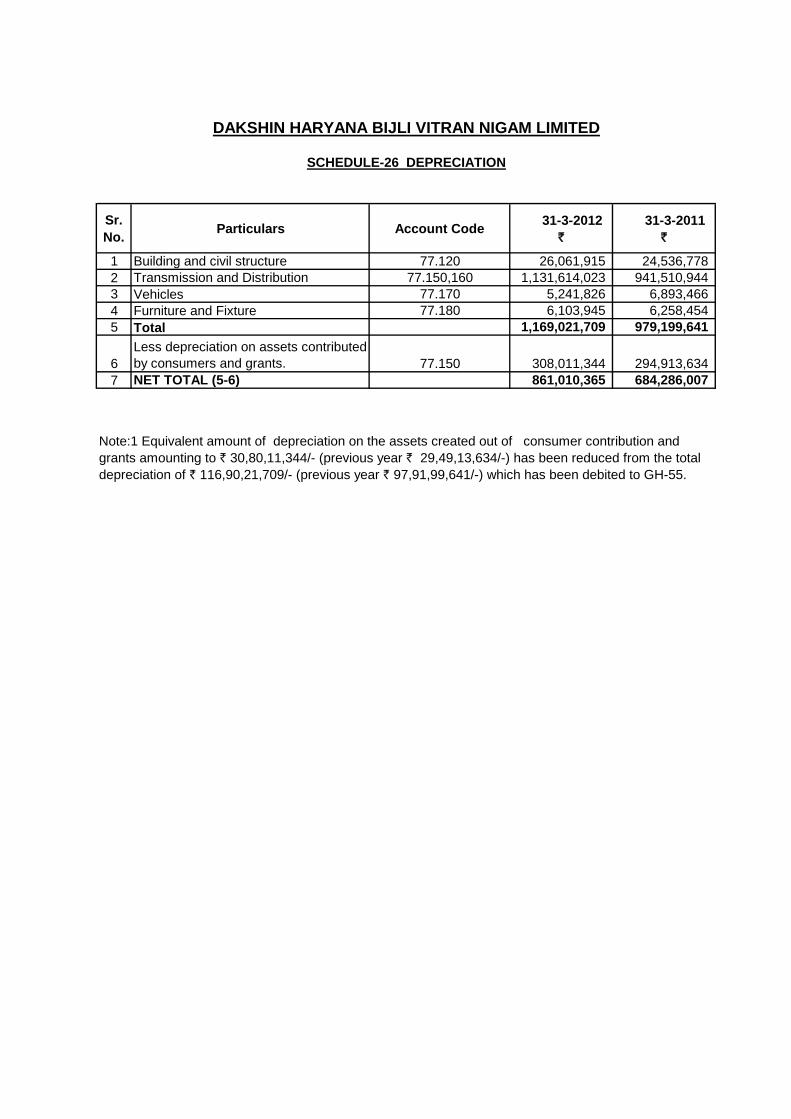

1 Building and civil structure 77.120 26,061,915 24,536,778 2 Transmission and Distribution 77.150,160 1,131,614,023 941,510,944 3 Vehicles 77.170 5,241,826 6,893,466 4 Furniture and Fixture 77.180 6,103,945 6,258,454 5 Total 1,169,021,709 979,199,641

6Less depreciation on assets contributed by consumers and grants. 77.150 308,011,344 294,913,634

7 NET TOTAL (5-6) 861,010,365 684,286,007

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITED

SCHEDULE-26 DEPRECIATION

Note:1 Equivalent amount of depreciation on the assets created out of consumer contribution and grants amounting to ` 30,80,11,344/- (previous year ` 29,49,13,634/-) has been reduced from the total depreciation of ` 116,90,21,709/- (previous year ` 97,91,99,641/-) which has been debited to GH-55.

Sr. No. Particulars Account

Code 31-3-2012

` 31-3-2011

`

1 Interest on loansa) Rural Electrification Corp. 78.502 1,088,381,224 961,624,636 b) State Govt. for NABARAD Projects 78.505 772,674 2,070,409 c) Power Finance Corp. 78.515 14,641,625 13,744,602 d)Payment of interest on loan from commercial bank for Electrification schemes 78.518 221,585,475 143,584,704 e)Interest on loans from Comml. Banks for working capital . 78.527 3,509,458,096 2,813,345,465 f) State Govt. under APDP/APDRP Projects 78.535 45,163,595 48,921,258 g)Interest on Loan from NCR 78.536 111,817,067 70,012,289 h)State Govt. under PMGY Projects 78.537 1,184,637 1,280,650 i)Interest on Loan from RECfor procurement of material 78.538 137,120,175 38,098,776 j)Interest on Loan from REC for re-financing of IBRD loans. 78.539 12,815,123 14,094,609

k)Interest on REC Loan against RGGVY scheme 78.542 2,979,754 - l) Interest on loan from PFC under R-APDRP 78.545 34,885,479 42,966,549 Sub Total (a to l) 5,180,804,924 4,149,743,947

2 Interest on consumers security 78.6 372,288,396 327,698,759 3 Interest on OD/CC from banks for working capital 78.7 509,359,674 188,979,355

4Other interest and finance charges (except 78.884) 78.8 59,367,643 16,957,928 Gross Total 6,121,820,637 4,683,379,989

5 Less: Interest Capitalised 78.9 674,069,833 906,964,567 Net Total 5,447,750,805 3,776,415,422

Note:- A portion of interest payable on interest bearing borrowings relatings to financing of capital assets at construction stage i.e. till the point of commissioning of assets has been capitalised amounting to ` 67.41 crores (Prev. year ` 90.70 crores). Interest is not being capitalised on the assets commenced and completed during the same year.

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITED

SCHEDULE-27 INTEREST & FINANCE CHARGES

Sr. No. Particulars Account Code 31-3-2012

` 31-3-2011

`

1 Cost of trading/manufacturing activities 79.3 - 264,124,940 2 Refund of Revenue 79.480 to 483 1,009,150 1,224,439 3 Misc. losses and write off 79.5 93,749,510 92,054,142

4Losses on account of flood,cyclone,fire to fixed assets 79.881 6,938,097 13,897,653

5 Sub Total 101,696,757 371,301,174 6 Add Provision for bad and doubtful debts 79.460 - -

GRAND TOTAL (9+10) 101,696,757 371,301,174

1 Regulatory Assets written off 79.710 1,163,448,000 290,862,000

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITED

SCHEDULE-28 OTHER DEBITS TO REVENUE

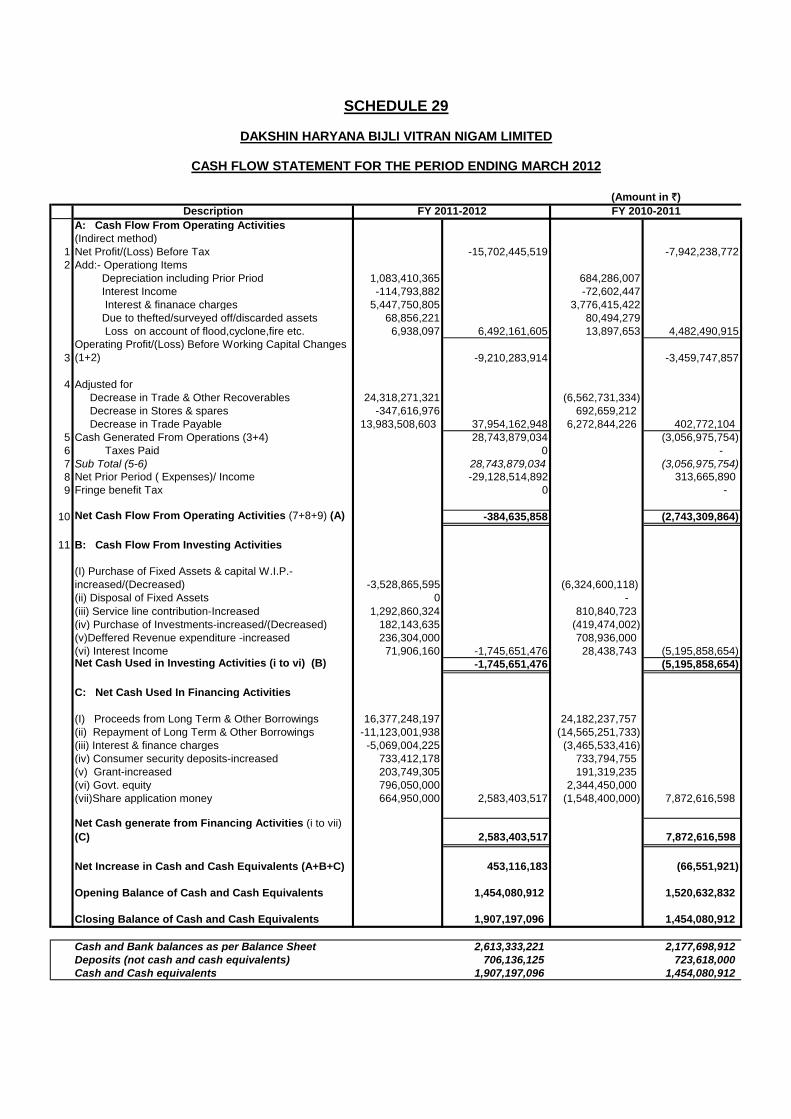

DescriptionA: Cash Flow From Operating Activities(Indirect method)

1 Net Profit/(Loss) Before Tax -15,702,445,519 -7,942,238,7722 Add:- Operationg Items

Depreciation including Prior Priod 1,083,410,365 684,286,007 Interest Income -114,793,882 -72,602,447 Interest & finanace charges 5,447,750,805 3,776,415,422 Due to thefted/surveyed off/discarded assets 68,856,221 80,494,279 Loss on account of flood,cyclone,fire etc. 6,938,097 6,492,161,605 13,897,653 4,482,490,915

3Operating Profit/(Loss) Before Working Capital Changes (1+2) -9,210,283,914 -3,459,747,857

4 Adjusted for Decrease in Trade & Other Recoverables 24,318,271,321 (6,562,731,334) Decrease in Stores & spares -347,616,976 692,659,212 Decrease in Trade Payable 13,983,508,603 37,954,162,948 6,272,844,226 402,772,104

5 Cash Generated From Operations (3+4) 28,743,879,034 (3,056,975,754) 6 Taxes Paid 0 - 7 Sub Total (5-6) 28,743,879,034 (3,056,975,754) 8 Net Prior Period ( Expenses)/ Income -29,128,514,892 313,665,890 9 Fringe benefit Tax 0 -

10 Net Cash Flow From Operating Activities (7+8+9) (A) -384,635,858 (2,743,309,864)

11 B: Cash Flow From Investing Activities

(I) Purchase of Fixed Assets & capital W.I.P.-increased/(Decreased) -3,528,865,595 (6,324,600,118)(ii) Disposal of Fixed Assets 0 - (iii) Service line contribution-Increased 1,292,860,324 810,840,723 (iv) Purchase of Investments-increased/(Decreased) 182,143,635 (419,474,002) (v)Deffered Revenue expenditure -increased 236,304,000 708,936,000 (vi) Interest Income 71,906,160 -1,745,651,476 28,438,743 (5,195,858,654) Net Cash Used in Investing Activities (i to vi) (B) -1,745,651,476 (5,195,858,654)

C: Net Cash Used In Financing Activities

(I) Proceeds from Long Term & Other Borrowings 16,377,248,197 24,182,237,757 (ii) Repayment of Long Term & Other Borrowings -11,123,001,938 (14,565,251,733) (iii) Interest & finance charges -5,069,004,225 (3,465,533,416) (iv) Consumer security deposits-increased 733,412,178 733,794,755 (v) Grant-increased 203,749,305 191,319,235 (vi) Govt. equity 796,050,000 2,344,450,000 (vii)Share application money 664,950,000 2,583,403,517 (1,548,400,000) 7,872,616,598

Net Cash generate from Financing Activities (i to vii) (C) 2,583,403,517 7,872,616,598

Net Increase in Cash and Cash Equivalents (A+B+C) 453,116,183 (66,551,921)

Opening Balance of Cash and Cash Equivalents 1,454,080,912 1,520,632,832

Closing Balance of Cash and Cash Equivalents 1,907,197,096 1,454,080,912

Cash and Bank balances as per Balance Sheet 2,613,333,221 2,177,698,912 Deposits (not cash and cash equivalents) 706,136,125 723,618,000 Cash and Cash equivalents 1,907,197,096 1,454,080,912

FY 2011-2012

SCHEDULE 29

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITED

CASH FLOW STATEMENT FOR THE PERIOD ENDING MARCH 2012

(Amount in `)FY 2010-2011

Statement pursuant to part IV of schedule VI to Company Act-1956Balance sheet abstract and Company General Business profile.

I.

Registration No. 05-34165State Code 5Balance sheet date 31.3.2012

II.

Authorised share capital ` 20,000,000,000 Share allotted ` 12,604,676,000 Share application money pending allotment ` 1,461,001,461 Bonus issue ` - Right issue ` - Public issue ` -

III.

Total Liabilities ` 125,509,002,534 Total Assets ` 125,509,002,534

` 14,065,677,461 ` 272,320,700 ` 46,332,775,641 ` 7,139,091,044 ` 7,204,825,925 ` 7,805,272,219

IV

` 35,003,701,998 ` - ` 200,747,383 ` (25,239,828,208) ` - ` 72,855,341,816

Secured loan

Total fixed assets

Profit and loss account -Losses

Net Current assetsMisc. expenditure

Un-Secured loans

InvestmentsRegulatory Assets

Consumer security deposit Consumer contribution & grantApplication of funds

Reserve and surplus

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITED

Registration details

Capital raised during the year

Source of funds

Position of mobilization and deployment of funds

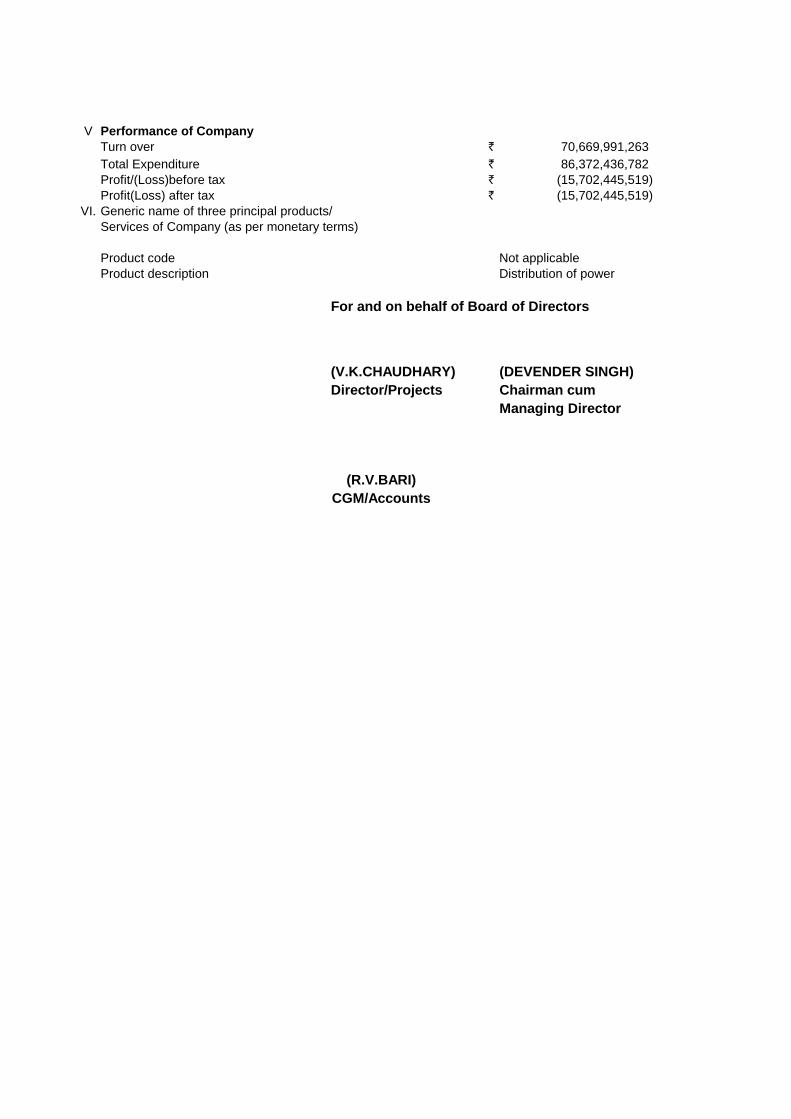

Share capital

VTurn over ` 70,669,991,263 Total Expenditure ` 86,372,436,782 Profit/(Loss)before tax ` (15,702,445,519) Profit(Loss) after tax ` (15,702,445,519)

VI. Generic name of three principal products/Services of Company (as per monetary terms)

Product code Not applicableProduct description Distribution of power

For and on behalf of Board of Directors

(V.K.CHAUDHARY) (DEVENDER SINGH)Director/Projects Chairman cum

Managing Director

(R.V.BARI)CGM/Accounts

Performance of Company

SIGNIFICANT ACCOUNTING POLICIES & NOTES ON ACCOUNTS FOR FY 2011-12:-

SCHEDULE-30

1. The Nigam is governed by the provisions of the Electricity Act, 2003. The provisions

of that Act prevails in preparing the Accounts wherever they are inconsistent with the

provisions of the Companies Act, 1956. 2. BASIS OF ACCOUNTING:

Accounts of the Nigam are being prepared on accrual basis based on the historical

cost convention except in case of surcharge levied on delayed payments which are

on actual realization basis.

3. USE OF ESTIMATES: The preparation of financial statements requires estimates and assumptions to be

made that affect the reported amount of assets and liabilities on the date of the

financial statements and the reported amount of revenues and expenses during the

reporting period. Difference between the actual results and estimates are recognized

in the period in which the results are known / materialized. 4. FIXED ASSETS AND DEPRECIATION:

a) The Fixed Assets are carried at the original cost including appropriate

expenses capitalized less depreciation thereof.

b) The interest on borrowed funds attributable to acquisition/construction of fixed

assets, till commissioning of such assets, is being capitalized.

c) Consumer’s contribution, grants and subsidies towards cost of capital assets

are not reduced from the cost of assets but being treated as ‘Capital

Reserves’ and shall be amortized with the amount of depreciation over the

useful life of fixed assets created out of consumer

contribution/grants/subsidies. The average rate of depreciation of plant &

machinery (T&D) is taken for amortization.

d) The expenditure on capital work in progress is transferred to appropriate

asset at the end of month irrespective of the date of commissioning of

project/work during that month.

e) Depreciation on Fixed Assets is provided in the accounts on Straight Line

Method as per rates provided in HERC Tariff regulation notified vide its

notification dated 19.12.2008 on assets created after 31.03.2005.

Depreciation on assets acquired upto 31.03.2005 is provided on the basis of

Notification made by Central Electricity Authority vide its No. SO/266(E) dated

29.3.1995 as hereto. Where rates for a particular asset are not provided for in

the Notification, the same are taken as per Companies Act, 1956.

f) The accounting policies relating to depreciation followed by the Nigam during

the year under consideration in accordance with the “HERC Tariff Regulation

notified vide its notification dated 19.12.2008” is reproduced here under:

• The value base for the purpose of depreciation shall be the historical

cost of the asset.

• Depreciation shall be calculated annually, based on straight line Method

over the useful life of the asset and at the rates prescribed in Appendix

II to these regulations.

The residual life of the asset shall be considered as 10% and

depreciation shall be allowed upto maximum of 90% of the historical

capital cost of the asset. Land is not a depreciable asset and its cost

shall be excluded from the capital cost while computing 90% of the

historical cost of the asset. The historical capital cost of the asset shall

include additional capitalization on account of Foreign Exchange Rate

Variation upto 31.3.2007 already allowed by the Commission.

• On repayment of entire loan, the remaining depreciable value shall be

spread over the balance useful life of the asset.

• Depreciation shall be chargeable from the first year of operation. In

case of operation of the asset for part of the year, depreciation shall be

charged on pro rata basis.

5. INVENTORIES VALUATION:

a) Inventory valued at cost or net realizable value whichever is lower.

b) Cost is determined on Weighted Average Method. Cost includes duties,

taxes, freight, octroi, insurance, handling, clearing charges and other

incidental expenses. Cost of Material at Site is, however, determined as per

issue price.

c) Provision against obsolete stock has been made for all non-moving items

(assets considered more than 3 years).

d) Scraps are accounted for as and when these are sold.

6 REVENUE RECOGNITION:

a) Revenue from sale of power is being accounted for on accrual basis, in

addition to this the unbilled revenue equivalent to 50% of the amount billed

during the month of March is also added in revenue from sale of power.

However, differences on account of adjustments of undercharge /

overcharged billing with actual billing are adjusted in the year of rectification.

b) The subsidy from Govt. of Haryana is to be accounted for on the basis of

budget provision of the GOH as well as its actual realization.

c) Material known liabilities are provided for on the basis of available information/

estimates.

7. FUEL SURCHARGE ADJUSTMENT

The amount of difference between the actual power purchase rate and the rate

approved by HERC vide its orders on Annual Revenue Requirement for the relevant

year is being filed with Commission to claim as FSA in accordance with mechanism

devised by the Commission for computing FSA, which is being allowed to recover

from the consumers in subsequent period i.e. in monthly installments over a period

of 2 to 4 year The expenditure on account of Fuel Surcharge Adjustment (FSA) is

being accounted when its incurred and revenue on its actual billing.

8. RETIREMENT BENEFITS:

The retirement benefits are being provided on actuarial valuation basis and as per

the certificate of the Actuary in accordance with the provision of Accounting