Summer 2013 out-of-town retail & leisure · goods remained weak, falling by 0.5% and 3.4%...

8

Highlights • While overall economic growth is expected to be weak for 2013, recent data suggests that the macro outlook for the UK is improving. • However, in the out-of-town retail market, headline rents have fallen and continue to edge down in many locations. This is due to general market weakness and also to the increasing dominance of discount retailers, who take a more aggressive approach to property costs. • Yields for better quality retail park assets have been hardening; conversely, values for more secondary assets have fallen. Yields for prime leisure assets meanwhile are now within 75-100bps of their prime retail equivalents. • Out-of-town retail investment volumes for the year to May 2013 are in line with 2012, while leisure investment volumes (excluding hotels but including pubs) almost reached £500 million. research Summer 2013 out-of-town retail & leisure Occupational & investment markets

Transcript of Summer 2013 out-of-town retail & leisure · goods remained weak, falling by 0.5% and 3.4%...

Highlights• Whileoveralleconomicgrowthisexpectedtobeweakfor2013,recentdatasuggeststhatthemacrooutlookfortheUKisimproving.

• However,intheout-of-townretailmarket,headlinerentshavefallenandcontinuetoedgedowninmanylocations.Thisisduetogeneralmarketweaknessandalsototheincreasingdominanceofdiscountretailers,whotakeamoreaggressiveapproachtopropertycosts.

• Yieldsforbetterqualityretailparkassetshavebeenhardening;conversely,valuesformoresecondaryassetshavefallen.Yieldsforprimeleisureassetsmeanwhilearenowwithin75-100bpsoftheirprimeretailequivalents.

• Out-of-townretailinvestmentvolumesfortheyeartoMay2013areinlinewith2012,whileleisureinvestmentvolumes(excludinghotelsbutincludingpubs)almostreached£500million.

research

Summer 2013

out-of-town retail & leisureOccupational&investmentmarkets

2

Summer 2013OUT-OF-TOWN RETAIL AND LEISURE Occupational&investmentmarkets

Economic overviewThe second estimate for Q1 2013 GDP confirmed that the UK economy grew by 0.3%, driven by a strong contribution from the service sector (0.6%) and a smaller contribution from production (0.2%). On the downside, the construction data was weak (-2.4%), as was manufacturing, which declined for the second successive quarter (-0.3%).

However,onapositivenote,thelatestforward-lookingPMIsurveyshavebeenmoreupbeatacrossthemanufacturing,constructionandservicesectors.Therearealsosignsthatconsumerconfidenceisreturning,followingalongperiodofgloom,withGfK’sconsumerconfidenceindexrisingby5pointsinMay.Whiletheoverallfigureremainsnegativeat-22,therecentimprovementcontinuesamoreupbeattrendseensincethestartof2013,whichhasbeenreflectedinthelatestretailsalesdata.

Theinflationpicturehasmarginallyimprovedinrecentmonths,butremainsabovetargetandsomewhat“sticky”.Indeed,ONSdatashowedthatCPIinflationrosefrom2.4%to2.7%inMay,higherthanmostforecasts,onthebackofariseintransportandclothingcosts.TheincreasetakestheheadlinerateofinflationbacktothelevelsseenbetweenOctober2012andMarch2013.

Recentpaygrowthfiguresmeanwhileshowamarginalimprovement–albeitstillrunningathalftherateofinflation–withthethree-monthaveragefigurerisingto1.3%forApril.Whilethepressureonconsumers

hasthereforeeased,realincomesarestillbeingsqueezed.

UnemploymentremainsoneofthebrighterspotsoftheUKeconomyandremainsverylowincomparisonwithmanyEuropeancountries.TheunemploymentrateforFebruarytoAprilwas7.8%,unchangedonthepreviousthreemonths,withthenumberofpeopleoutofworkdecliningbyjust5,000to2.5million.ThemoreprecisecountofJobseeker’sAllowanceshowedafallof8,600to1.51millioninMay.

TheoutlookcontinuestoimproveformostpartsoftheUK,althoughthepathtoamoresustainedrecoverywillremainslowandbumpyandwillvarybyregion.MediumtermforecastssuggestthatthestrongesteconomicgrowthwillbeinLondonandtheSouthEast.Relativelyhighlevelsofemploymentandimprovingconsumerconfidenceshouldfilterthroughtoconsumerspendingastheyearprogresses.

TheEurozoneremainsweakbutatleastappearsmorestableand,despitehighunemployment,positivegrowthhasreturnedtotheUS.

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

%

Q1-Q42008

Q1-Q42009

Q1-Q42010

Q1-Q42011

Q1-Q32012

Q12013

Figure 1

Quarterly GDP growth

Source: ONS

-45-40-35-30-25-20-15-10-505

10

2009 20112010 2012 2013

Consumer Confidence

Index

Personal financial situation over

next 12 months

General economic situation over

next 12 months

Figure2GfK consumer confidence

Source:GfKNOPConsumerConfidence

-8

-6

-4

-2

0

2

4

6

8

May13

May12

May11

May10

May09

May08

May07

May06

May05

May04

Ann

ual %

cha

nge

Annual changeCPI All Items

Average weeklyearnings growth

Figure 3

CPI and pay growth

Source: ONS

3

Trends – Discount retailers

KnightFrank.com

The out-of-town retail landscape has changed significantly in recent years, with the balance of power now firmly in the hands of the discounters. While the property industry may have reservations about some of these brands, consumers have clearly embraced the value end of the market.

Anumberofdiscountershaveundergonedramaticexpansion.TheseincludeoperatorssuchasPoundworld,whichwasfoundedin1997andnowhasover170stores,ofwhicharound120areout-of-town,withanother170storestargeted.Similarly,99pStores,whichwasfoundedin2001,nowhasover190stores,aidedbytheadditionofover40formerWoolworthsstores.Thecompanyalsotradesout-of-townasFamilyBargains.Bothcompanieshaveachievedverystrongsalesgrowthinanenvironmentoflowmarginsandfiercecompetition.Indeed,Poundlandrecentlyreducedsomepricesto97ptoundercutits99privals.

Inthediscountfoodsector,Aldi’ssalesgrowthhaseasilyoutpaceditslargerrivals,withgrowthof31.5%in2012.Ithasgainedsignificantmarketsharethroughitsofferofcheaperversionsofclassicproducts,withoutcompromisingonquality.

Analysissuggeststhattheleadingdiscountershavesomeofthehighestprofitmarginsintheretailsector,withDunelmat15.8%(source:OrielSecurities).Whilethestrengthofdemandfromtheseoperatorsshouldintheorydrivehigherrents,therealityisthattheyareveryfocusedonmarginsandcostsinthecurrentenvironment–includingproperty.

Figure4aboveshowstherentspaidbysomeofthemoreaggressiveretailersin

recentyears,includingfourofthetopfivespacetakersin2012.Acomparisonofthisdataagainstsomeofthemoreestablishedout-of-townplayerssuggeststhatheadlinerentshavefallensteadily.Therefore,whilelandlordshavebeenabletofillthevoidsleftbyretailerclosures,thishasbeenattheexpenseoflowerrents.TheonlyestablishedplayerinthetopfivespacetakersisTKMaxx,whichisexpandingtotakeadvantageofstrongconsumerdemandforqualityproductsatlowprices.However,theaveragerentontheirexistingstoreportfolioishigherthanthemorerecentlyestablishedplayers.

AveragerentsforTheRangeacrossasampleof54storesis£10.55persqft,whileB&Mpaysjust£11.71persqftacrossasampleof91stores.Thesefiguresaremuchlowerthanforthemoreestablishedoperatorswhichexpandedbeforetherecession.Carpetrightforexamplepays£18.64persqftonaverage(basedonasampleof294),whileMothercare’saveragerentacrossasampleof85storesis£23.26persqft.

Discount retailers take over

1 million sq ft of new space in 2012

Top 5 increases in floor space in 2012

• B&M–410,000sqft

• Kiddicare–350,000sqft

• Dunelm–250,000sqft

• TKMaxx–240,000sqft

• HomeBargains–230,000sqft

0

5

10

15

20

25

Mot

herc

are

(85)

TK M

axx

(111

)

Argo

s (2

32)

Carp

etrig

ht (2

94)

Hal

ford

s (3

21)

Stap

les

(94)

Hom

e Ba

rgai

ns (5

4)

Poun

dstr

etch

er (9

1)

Mat

alan

(184

)

Dun

elm

Mill

(87)

B&M

(91)

The

Rang

e (5

4)

Aver

age

rent

s £/s

q ft

per p

ortfo

lio

Figure4Discount retailers

Source:TrevorWoodAssociatesNumbersinbracketrelatetosamplesizeofstoreforeachretailer

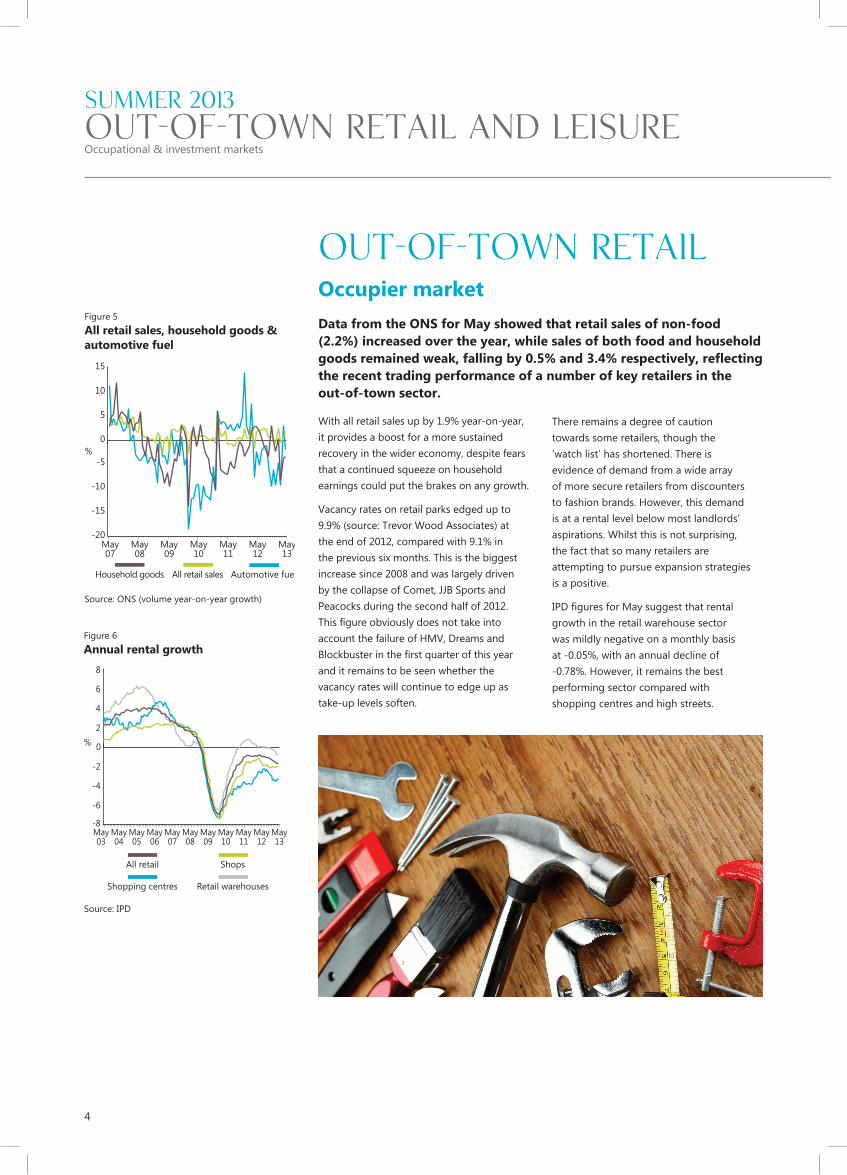

Withallretailsalesupby1.9%year-on-year,itprovidesaboostforamoresustainedrecoveryinthewidereconomy,despitefearsthatacontinuedsqueezeonhouseholdearningscouldputthebrakesonanygrowth.

Vacancyratesonretailparksedgedupto9.9%(source:TrevorWoodAssociates)attheendof2012,comparedwith9.1%intheprevioussixmonths.Thisisthebiggestincreasesince2008andwaslargelydrivenbythecollapseofComet,JJBSportsandPeacocksduringthesecondhalfof2012.ThisfigureobviouslydoesnottakeintoaccountthefailureofHMV,DreamsandBlockbusterinthefirstquarterofthisyearanditremainstobeseenwhetherthevacancyrateswillcontinuetoedgeupastake-uplevelssoften.

Data from the ONS for May showed that retail sales of non-food (2.2%) increased over the year, while sales of both food and household goods remained weak, falling by 0.5% and 3.4% respectively, reflecting the recent trading performance of a number of key retailers in the out-of-town sector.

Thereremainsadegreeofcautiontowardssomeretailers,thoughthe‘watchlist’hasshortened.Thereisevidenceofdemandfromawidearrayofmoresecureretailersfromdiscounterstofashionbrands.However,thisdemandisatarentallevelbelowmostlandlords’aspirations.Whilstthisisnotsurprising,thefactthatsomanyretailersareattemptingtopursueexpansionstrategiesisapositive.

IPDfiguresforMaysuggestthatrentalgrowthintheretailwarehousesectorwasmildlynegativeonamonthlybasisat-0.05%,withanannualdeclineof-0.78%.However,itremainsthebestperformingsectorcomparedwithshoppingcentresandhighstreets.

Out-of-town retail Occupier market

4

-20

-15

-10

-5

0

5

10

15

%

May07

May08

May09

May10

May11

May12

May13

Household goods All retail sales Automotive fuel

Figure5All retail sales, household goods & automotive fuel

Source:ONS(volumeyear-on-yeargrowth)

Summer 2013OUT-OF-TOWN RETAIL AND LEISURE Occupational&investmentmarkets

-8

-6

-4

-2

0

2

4

6

8

%

May03

May04

May05

May06

May07

May08

May09

May10

May11

May12

May13

All retail Shops

Shopping centres Retail warehouses

Figure6Annual rental growth

Source:IPD

The second quarter saw approximately £444m worth of out-of-town investment deals (although 27% was made up of large portfolio sales), showing a 146% increase in volume on the previous quarter and a 25% increase in the number of transactions. RecentkeytransactionsincludethesaleofColiseumShoppingParkinEllesmerePort.TheCrownpurchasedtheparkfromEquitableLifefor£81m,reflectingareportedNIYof5.25%.Inaddition,KKRandQuadrantEstatesrecentlycompletedthepurchaseoftheTuscanyretailparkportfoliofromResolutionfor£112.5m.

WhilstthegoodsecondaryOpenA1markethasbeenquietinthelast18months,Q2witnessedtwodeals,includingtheacquisitionofGalaRetailParkinGalashielsbyPrudentialforc.£11.2m(reflectingaNIYof6.25%)andthepurchaseofSuffolkRetailParkinIpswichbyOrchardStreetfor£18.75m(reflectingaNIYof7.10%).

GallionsReachShoppingParkinBecktoncametothemarketinMaywithaquotingpriceof£110m,reflectinganetinitialyieldof6.00%.Theavailabilityofprimesolusstockhasbeenlimited,althoughtherehavebeentwobenchmarktransactions,namelytheWickesinBicesterwhichsoldfor£5.7m,reflectinganetinitialyieldof6.15%,andtheB&QunitinSouthend-on-Seawhichsoldfor£24.25m,reflectinganetinitialyieldof6.50%.

Overallinvestorsentimentismorepositivethanearlierthisyear.However,thereis

stilladegreeofyieldpolarisationbetweenprimeandsecondaryassets,inparticularthebulkygoodssectorwhererentsareunderpressure.YieldsforprimeOpenA1schemeshardenedfrom5.35%to5.25%inJune,whileyieldsforprimeBulkyGoodsparksmovedoutto6.50%.Weexpectthistrendtocontinue.

Major retail investment transactions

Retail Park Purchaser Vendor Price NIY (£m) (%)TuscanyPortfolio KKRandQuadrantEstates Resolution 112.5 7.50

StoneLakeRetailPark,London Aberdeen LXB 32.95 6.50

PurleyWay,Croydon StandardLife Aviva 31.70 5.90

AngliaRetailPark,Ipswich StarwoodCapital ELAS 29.50 7.80

SuffolkRetailPark,Ipswich OrchardStreet Aberdeen 18.75 7.10

LadyBayRetailPark, Threadneedle LaSalleIM 16.30 8.80Nottingham

GalaRetailPark,Galashiels Prudential Aviva 10.87 6.40Source:Propertydata.com,KnightFrank

Investment market

KnightFrank.com

5

0

100

200

300

400

500

600

700

800£m

2008 2009 2010 2011 2012 20130

10

20

30

40

50

60

Num

ber o

f tra

nsac

tions

£m Number of transactions

Figure9Retail warehouse investment transactions

Source:Propertydata

%

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

Jun2008

Jun2009

Jun2010

Jun2011

Jun2013

Jun2012

Food Store Open A1/Fashion Park

Bulky GoodsRetail Park

Figure7Prime out-of-town retail yields

Source:KnightFrank

%

2

4

6

8

10

May03

May04

May05

May06

May07

May08

May09

May10

May11

May12

May13

Initial yield Equivalent yield

Figure8Long-term retail warehouse yields

Source:IPD

Unsurprisingly,openingsinbothsectorsdeclinedin2009.However,2012sawatleastfourtimesthenumberofnewA3(casualdining)openingsonretailparks,comparedwithfastfoodoutlets.

Operatorsarecurrentlyfacedwithhowtogrowturnoverinaweakconsumerenvironment.Theanswerhasmainlybeenorganicgrowth,particularlyamongstthecasualdiningoperatorssuchasASK,PizzaExpress,Nando’s,Frankie&Benny’sandTGIFridays.Thesebrandshavetraditionallybeenseeninthehighstreet,shoppingcentresand/orleisureschemes.

Mostofthesecompanieshavechosentolocateonshoppingparks,wherethetypeofconsumersandlongopeninghourscreateanattractivelocationforrestaurants.Indeed,

unlikesomeout-of-townleisureschemes,shoppingparksoftentradesuccessfullythroughouttheday.Ouranalysisshowsthattheaveragerentacrossasampleof206restaurantsonretailparksis£24.36persqft,withtheaveragesizeofunitsbeing3,450sqft.

Therapidincreaseofrestaurantoperatorsonout-of-townretailparksreflectstheirdesiretogroworganicallyandchangingconsumerhabits,wherebyeatingouthasbecomeamoreimportantpartoftheshoppingexperience.

Tesco’srecentacquisitionofGiraffemightsetatrendformorerestaurantsinout-of-townsuperstores.Thiscouldallowsupermarketstomakeuseofspacenolongerrequiredforelectricalgoods,aswellasmeetingconsumerdemandforcasualdiningwhileshopping.

Fastfoodopeningshavefallensignificantly,inpartduetosaturationincertainlocations.Itisalsobecauseofchangingconsumerpreferencesandlandlordsseekingabetterqualityofferwhichcomplementstheretailexperience–notjust‘grab&go’.Thedrive-thrumodeladdslimitedvaluetotheretailmixandisunlikelytoimprovefootfalland/ordwelltime.

The expansion of the casual dining restaurants such as Frankie & Benny’s and Nando’s into out-of-town retail parks began in earnest in 2007 – somewhat behind the traditional fast food outlets such as McDonald’s, which peaked over ten years ago.

Summer 2013OUT-OF-TOWN RETAIL AND LEISURE Occupational&investmentmarkets

6

Casual dining on retail parks

BIRMINGHAM FORT add value wITH

RECENT LETTINGS to HARVESTER AND FRANKIE & BENNY’S

*Relatesonlytoopeningssince1997,asdataisnotavailablebeforethisdate

Occupier marketTheleisureoccupationalmarketcontinuestogofromstrengthtostrength,perhapswiththeexceptionofpubsandthelatelicence/nightclubvenues.Theformerarefeelingtheeffectsofthedebtstructureandpropertylegacyissues,whilethelatterareexperiencingchangesinconsumerpreferences(AtmosphereBarsandClubshavegoneintoadministration).

Themajorcinemachains,ledbyVUE,CineworldandOdeon,continuetoseeknewopportunities,oftenincompetition.Thismightbeseenasanattempttoboosttheirmarketvalue,asmuchasadesiretogroworganically,especiallyinthecaseofOdeon.However,themainthreeplayersareexpectedtoopennewcinemasandover50newscreensinplacessuchasBroughton(Cheshire),CramlingtonandGatesheadinthenortheast,QuaysideGloucesterandNewport(SouthWales).InthecaseofCramlington,theheadlinerentis£15persqftandGatesheadat£14persqft.

Activityinthehealthandfitnesssectorispolarisingtowardsthe“value”sector,drivenbythelikesofPureGym,EasyGymandGymGroup.ThelatterwasrecentlysoldtoPhoenixEquityPartnersforjustunder£100mandexpectstoaddatleastnew20clubstotheirportfolio.FitnessFirst,whichhasrecentlyemergedfromitsCVAprocess,iscommittedtospending£20mCAPEXonrefurbishingtheir85-strongportfolio.

Continuedgrowthisalsobeingseeninthecasualdiningsector.TheRestaurantGroup,havingreportedmoreencouragingsalesgrowthfigures,isontargettoopen35newunitsin2013(including5CoasttoCoast).TGIFridayshavealsorecentlycommittedtotheoldAromaunitinBraintreeat£34persqft.Incontrasttothetraditionalpubestate,

Leisure Market

KnightFrank.com

7

thelikesofTobyCarveryandHungryHorsecontinuetoseeknewopportunities(GreeneKinghassuggesteditmaydoubletheHorseestateto400+).Slug&Lettuceisalsolookingforupto40newsites,mainlyinprimeretaillocationssuchasWestfieldandBluewater–inanacknowledgementoftheever-increasingsynergyofleisureandretail.

Investment marketWhilethemostrecentbenchmarkyieldforaprimeleisureassetremainsc.6.20%paidforBurySt.Edmundslatelastyear,marketsentimenthasimprovedin2013.Consumersappeartohaveresistedthetemptationtoreduceleisurespending–albeit“value”isparamount–whichinturnhasledtooccupationaldemandandhigherrentsforthebetterschemes.

MajorinvestorsintheleisuresectorsuchasLandSecuritieshavebeenattractedbythelengthandstabilityofincome(longleases)andrentalgrowthprospects(openmarketandindexation).Earlypurchasessuggestedagreaterdemandforin-townassetswithstrongretailsynergy,suchasCornerhouse(Nottingham)andKingsmead(Bath).However,LandSecurities’purchaseofthemajoritystakeinX-Leisureprovidesexposuretotheout-of-townmarket,aswellasanexperiencedmanagementteamandaccesstokeyoccupiers.Obsolescenceandcompetitionmaybeachallengeforsomeoftheschemes,forexamplePoolewillbethreatenedbynewin-townsupplyinBournemouth.

Wewouldexpectthatthenextdominantprimeleisurescheme(15-yearincome,withindexationandsub-£20m)willtradeat,oraround,6%.Thiswilltakeprimeleisureyieldstowithin75bpsoftheirprimeequivalentintheout-of-townretailsector.

Coffeeshopshaveshownanevengreaterappetiteforretailparks,havingonlystartedtobreakintothismarketin2006/2007.Inthelast10yearsthenumberofCostaandStarbucksunitsopeningonretailparkshasincreasedexponentially,fromoneortwounitsayear,toover20newunitsin2012.TheaveragerentpaidbyCostaandStarbucksacrossasampleof67unitsis£37persqft.

ThefoodandbeverageofferisbecominganessentialpartoftheretailexperienceintheUK.Itisnowwidelyacknowledgedthatanattractiveleisuremixleadstoincreaseddwelltime,aswellasanimprovedconsumerexperience.

0

5

10

15

20

25

No

of C

osta

/Sta

rbuc

ks u

nits

ope

ned

Tota

l num

ber o

f uni

ts

2008

2007

2006

2005

2004

2003

2009

2010

2011

2012

2013

0

20

40

60

80

100

120

140

No of Costa/Starbucksunits opened each year

Total numberof units

Figure13Growth of Costa and Starbucks on retail parks

Source:TrevorWoodAssociates

0

3

6

9

12

15

Num

ber

2008

2007

2006

2005

2004

2003

2000

2001

2002

2009

2010

2011

2012

2013

ASK, Bella Italia, Café Rouge, Caffe Uno, Chiquito,Frankie & Bennys, GBK, Harvester, Nandos,

Pizza Express, Prezzo, TGI Fridays, Zizzi

Figure12Growth of casual dining on retail parks

Source:TrevorWoodAssociates

HEADING

Leisure park Purchaser Vendor Price (£m) NIY (%)Odeon,Richmond Available Odeon 9.975 5.75JunctionLeisurePark,Llandudno U/O Prupim 8.25 6.50i-Scene,Ilford U/O Santander 19.50 8.40TheLight,Leeds Legal&General KamesCapital 91.80 n/aCineworld,Cardiff HendersonUKPUT SpectrumAsset 18.96 6.89 ManagementLarksWood,Chingford BAPensionFund Private 6.78 8.25Source:KnightFrank

KnightFrankResearchprovidesstrategicadvice,consultancyservicesandforecastingtoawiderangeofclientsworldwideincludingdevelopers,investors,fundingorganisations,corporateinstitutionsandthepublicsector.Allourclientsrecognisetheneedforexpertindependentadvicecustomisedtotheirspecificneeds.

© Knight Frank LLP 2013

Thisreportispublishedforgeneralinformationonly.Althoughhighstandardshavebeenusedinthepreparationoftheinformation,analysis,viewsandprojectionspresentedinthisreport,nolegalresponsibilitycanbeacceptedbyKnightFrankResearchorKnightFrankLLPforanylossordamageresultantfromthecontentsofthisdocument.Asageneralreport,thismaterialdoesnotnecessarilyrepresenttheviewofKnightFrankLLPinrelationtoparticularpropertiesorprojects.ReproductionofthisreportinwholeorinpartisallowedwithproperreferencetoKnightFrankResearch.

KnightFrankLLPisalimitedliabilitypartnershipregisteredinEnglandwithregisterednumberOC305934.Ourregisteredofficeis55BakerStreet,London,W1U8AN,whereyoumaylookatalistofmembers’names.

AmericasUSABermudaBrazilCanadaCaribbeanChile

AustralasiaAustraliaNewZealand

EuropeUKBelgiumCzechRepublicFranceGermanyHungaryIrelandItalyMonacoPolandPortugalRomaniaRussiaSpainTheNetherlandsUkraine

AfricaBotswanaKenyaMalawiNigeriaSouthAfricaTanzaniaUgandaZambiaZimbabwe

Asia CambodiaChinaHongKongIndiaIndonesiaMacauMalaysiaSingaporeThailandVietnam

The Gulf AbuDhabi,UAEBahrainDubai,UAEQatar

KnightFrankResearchReportsareavailableatwww.KnightFrank.com/Research

Recent market-leading retail and leisure research publications

ShoppingCentreInvestmentQuarterlyQ22013

UKRetailWarehousingReportWinter2012

CentralLondonRetailReportSummer2013

LeisureReportAutumn/Winter2012

RESEARCH

Commercial ResearchAnthea To, Associate [email protected]

Darren Yates, Partner [email protected]

Investment and Asset ManagementAndrew McGregor, Partner [email protected]

Dominic Walton, Partner [email protected]

Ellie Awford [email protected]

ValuationsRobert Gray, Partner [email protected]

Peter Youngs, Partner [email protected]

Tom Withey, Associate [email protected]