Sue Milton, Adviser, Strategy, Risk & Corporate Governance [email protected] 6th Annual...

19

Sue Milton, Adviser, Strategy, Risk & Corporate Governance [email protected] 6th Annual International Regulatory Affairs Symposium “Risk Governance in Regulation” Analysing Regulatory Failure • Structural, Cultural and Political Contributors to Regulatory Failure. • (Un)Predictable Role of Combinations in Risk Management Failure.

-

Upload

lizeth-freese -

Category

Documents

-

view

226 -

download

10

Transcript of Sue Milton, Adviser, Strategy, Risk & Corporate Governance [email protected] 6th Annual...

Sue Milton, Adviser, Strategy, Risk & Corporate [email protected]

6th Annual International Regulatory Affairs Symposium “Risk Governance in Regulation”

Analysing Regulatory Failure • Structural, Cultural and Political Contributors to Regulatory Failure.• (Un)Predictable Role of Combinations in Risk Management Failure.

2

CONCLUSIONS FIRST “THE GAME IS STILL BEING PLAYED, BUT PERHAPS IT IS BEING PLAYED WITH MORE RULES.” LÉON COURVILLE

WE REQUIRE BETTER GOVERNANCE THAT RECOGNISES:

REGULATION SETS ONLY THE BASELINE FOR WHAT IS EXPECTED. WE SHOULD ALL AIM HIGHER.

REGULATION WILL NOT STOP BAD THINGS FROM HAPPENING. WE STILL NEED TO MANAGE THE RISKS.

REGULATION MAY BE OUT-OF-DATE. COMMUNICATE WITH THE REGULATOR.

REGULATION, AT BEST, WILL DELAY OR MINIMISE FAILURE, AND REDUCE THE COST TO THE INNOCENT.

NAIVETY AND APATHY ARE NOT SYNONYMOUS WITH INNOCENCE.

EACH SIGNIFICANT FAILURE PROVIDES OPPORTUNITY TO DO BETTER. BUT THE END OF ONE CRISIS SOWS THE SEEDS OF THE NEXT.

3

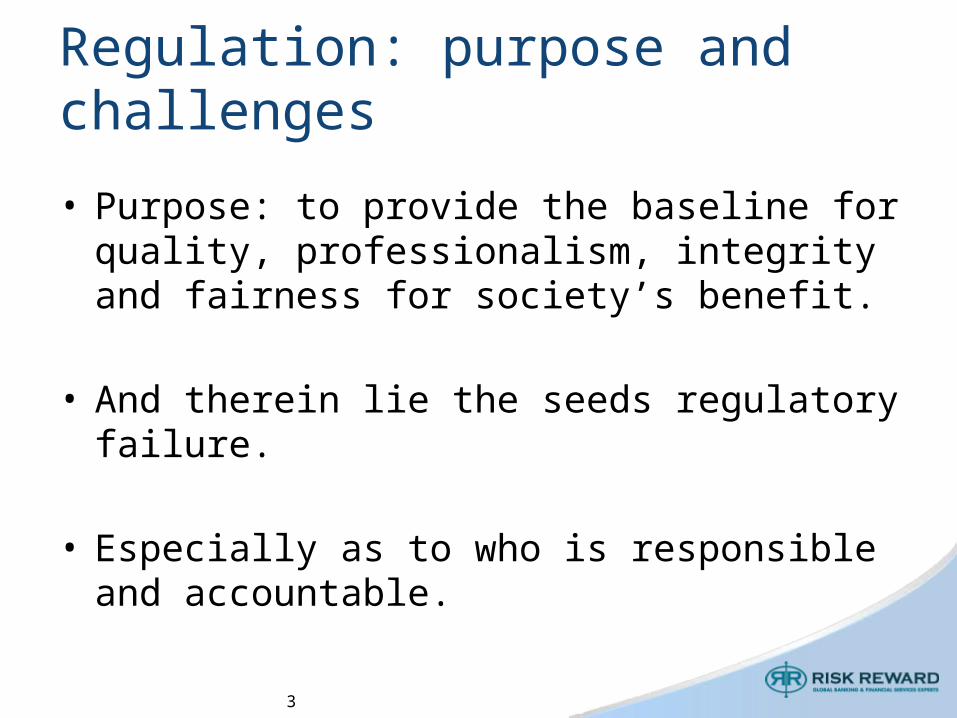

Regulation: purpose and challenges

• Purpose: to provide the baseline for quality, professionalism, integrity and fairness for society’s benefit.

• And therein lie the seeds regulatory failure.

• Especially as to who is responsible and accountable.

4

Governance and regulation• Governance: behaviour and relationships.• Intangible.

• Regulation: codifies.• Tangible.

• Compliance: with regulation.• Performance.

• Reward: for performance.• But not merit.

• ‘Performance’ against the regulation becomes what matters.

5

Regulation as the baseline

• Commonly acceptable standard.

• Comprehensible and understandable.

• Applicable?

• Measurable?

6

Regulation as a risk mitigant.

• Can regulation be a risk mitigant?

• Which risks can be managed by regulation?

• Creating risk?• The letter versus the spirit.• Games people play.

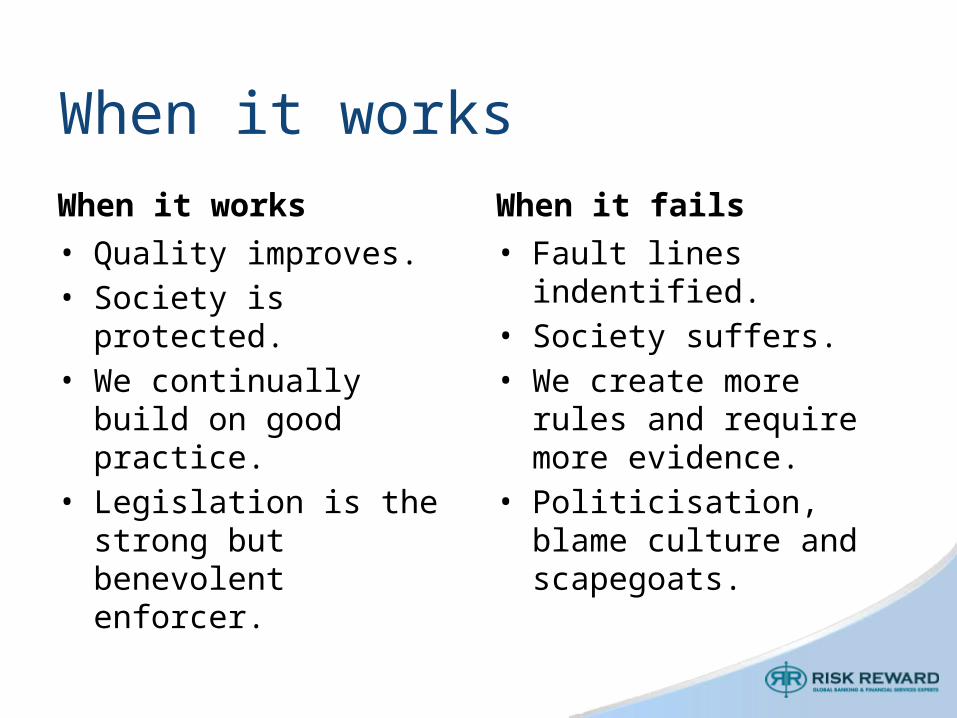

When it worksWhen it works• Quality improves.• Society is protected.• We continually build on

good practice. • Legislation is the strong but

benevolent enforcer.

When it fails• Fault lines indentified.• Society suffers.• We create more rules and

require more evidence.• Politicisation, blame culture

and scapegoats.

8

Cultural, social and political tensions• Cultural and national norms influence behaviour.• Societies fall somewhere between free-market and

centrally controlled, each with ideals, each with imperfections.

• Consensus of ‘right versus wrong’ is difficult to establish, leading to compromise solutions.

• ‘Right behaviour’ – but for whom? Corporate governance models and codes vary. Who should get the most benefit? Who pays, and how, when things go wrong?

9

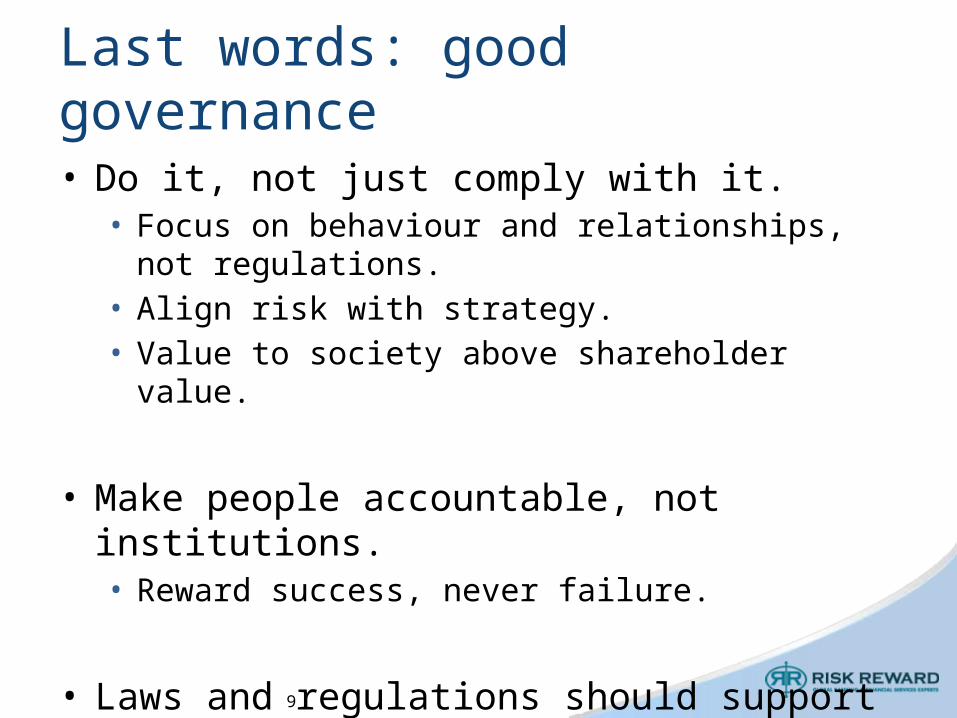

Last words: good governance

• Do it, not just comply with it.• Focus on behaviour and relationships, not regulations.• Align risk with strategy.• Value to society above shareholder value.

• Make people accountable, not institutions.• Reward success, never failure.

• Laws and regulations should support the above and must be enforceable and enforced.

10

Case study: the great recession

11

Can we predict risk?• ‘Yes’ versus ‘no’.• Yes: experience and evidence help predictions (e.g.

Insurance).• No: because we can not predict everything (e.g. Flight

MH370).

• Controlling risk: appetite, tolerances, compliance, assumptions.

• What we can and cannot control.• ‘perfect storm’ versus the avoidable.

• Given the above, could we have foreseen the 2007- 9 crisis?

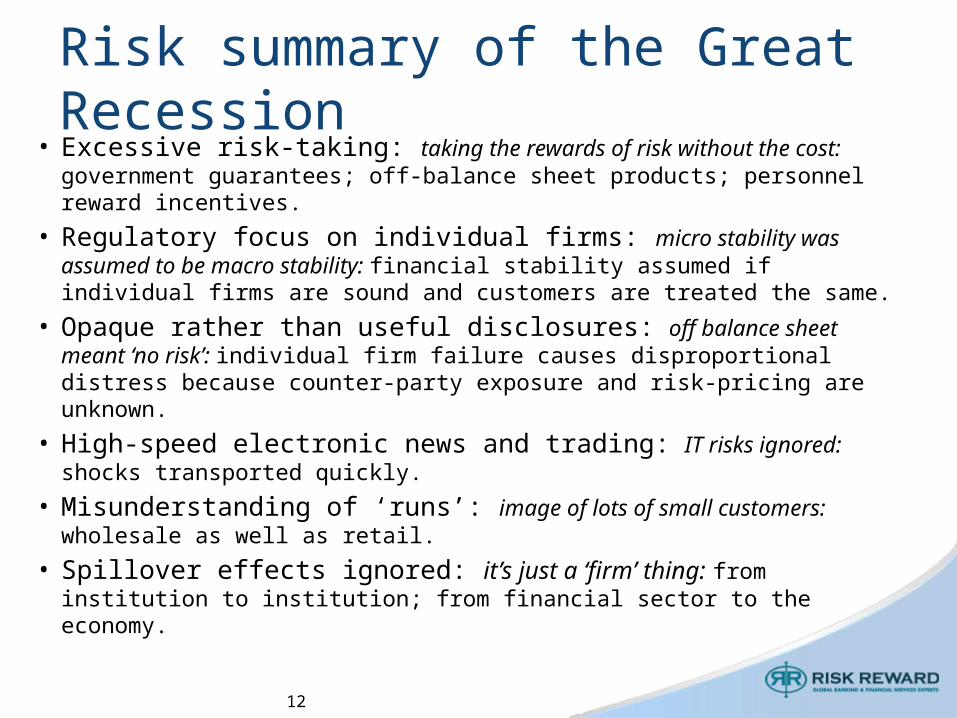

12

Risk summary of the Great Recession• Excessive risk-taking: taking the rewards of risk without the cost:

government guarantees; off-balance sheet products; personnel reward incentives.

• Regulatory focus on individual firms: micro stability was assumed to be macro stability: financial stability assumed if individual firms are sound and customers are treated the same.

• Opaque rather than useful disclosures: off balance sheet meant ‘no risk’: individual firm failure causes disproportional distress because counter-party exposure and risk-pricing are unknown.

• High-speed electronic news and trading: IT risks ignored: shocks transported quickly.

• Misunderstanding of ‘runs’: image of lots of small customers: wholesale as well as retail.

• Spillover effects ignored: it’s just a ‘firm’ thing: from institution to institution; from financial sector to the economy.

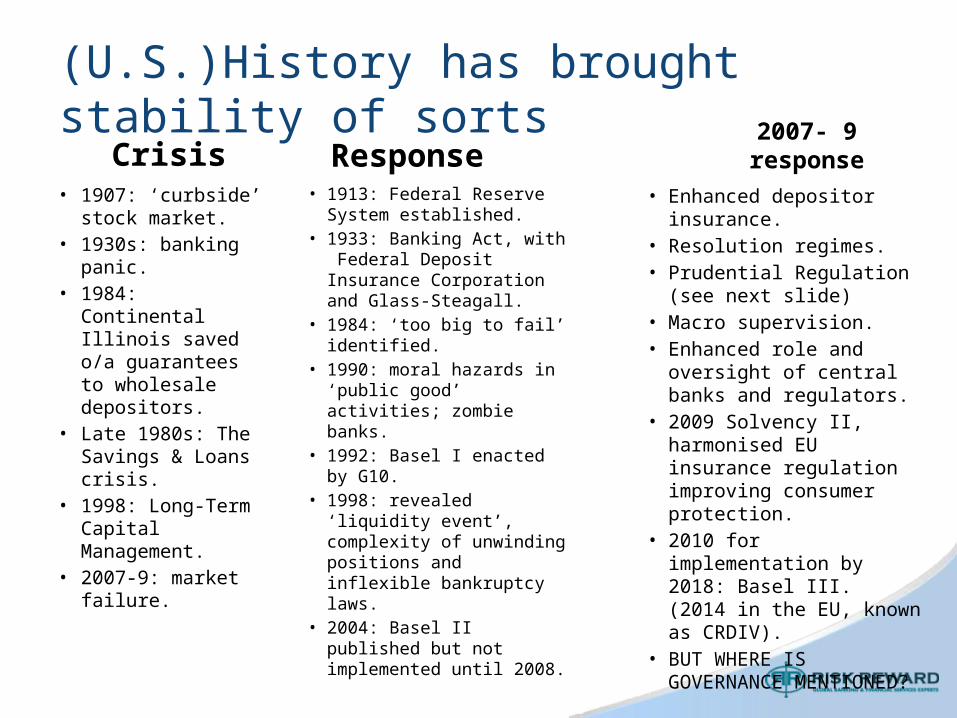

(U.S.)History has brought stability of sorts Crisis

• 1907: ‘curbside’ stock market.

• 1930s: banking panic.

• 1984: Continental Illinois saved o/a guarantees to wholesale depositors.

• Late 1980s: The Savings & Loans crisis.

• 1998: Long-Term Capital Management.

• 2007-9: market failure.

Response• 1913: Federal Reserve

System established.• 1933: Banking Act, with

Federal Deposit Insurance Corporation and Glass-Steagall.

• 1984: ‘too big to fail’ identified.

• 1990: moral hazards in ‘public good’ activities; zombie banks.

• 1992: Basel I enacted by G10.

• 1998: revealed ‘liquidity event’, complexity of unwinding positions and inflexible bankruptcy laws.

• 2004: Basel II published but not implemented until 2008.

2007- 9 response• Enhanced depositor

insurance.• Resolution regimes.• Prudential Regulation (see

next slide)• Macro supervision.• Enhanced role and

oversight of central banks and regulators.

• 2009 Solvency II, harmonised EU insurance regulation improving consumer protection.

• 2010 for implementation by 2018: Basel III. (2014 in the EU, known as CRDIV).

• BUT WHERE IS GOVERNANCE MENTIONED?

14

Prudential regulation – the new solution

15

The future: deja vue?Source: CITY A.M. 17th April 2014

• (p7) Bank deposits shrink as mortgages expand because of high loan to value mortgages.

• (P13) Euro inflation at lowest level since late 2009: the fear of deflation and the demand for monetary stimulus.

Source: the FT 17 April 2014

• (P1) “Face of Irish crisis cleared of loan fraud”.• (P32) “When use of pseudo-maths adds up to fraud”.

16

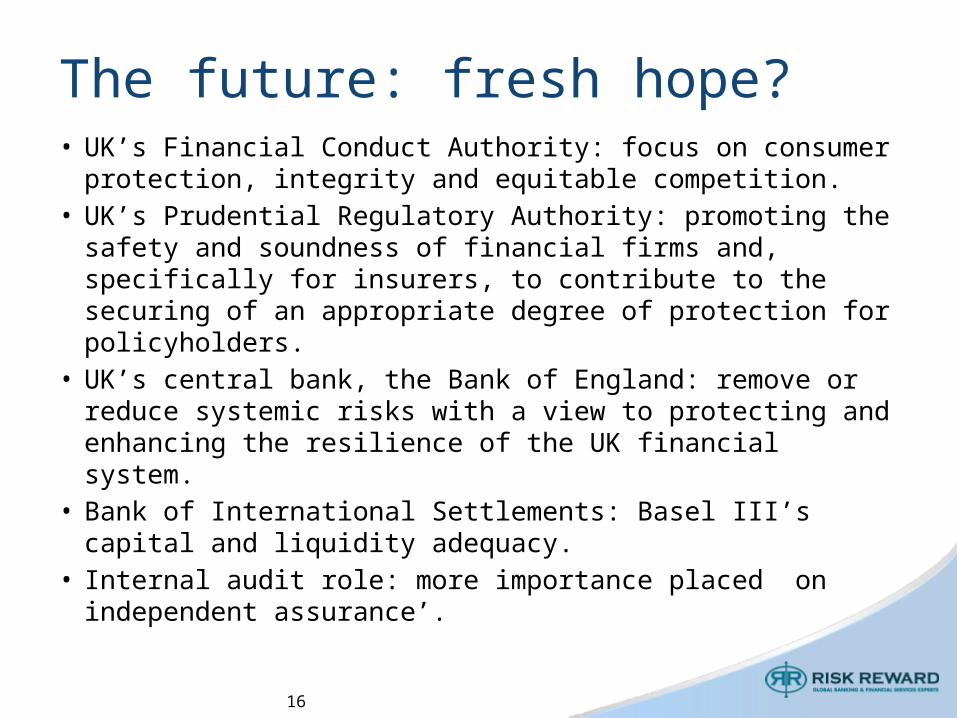

The future: fresh hope?• UK’s Financial Conduct Authority: focus on consumer

protection, integrity and equitable competition.• UK’s Prudential Regulatory Authority: promoting the safety

and soundness of financial firms and, specifically for insurers, to contribute to the securing of an appropriate degree of protection for policyholders.

• UK’s central bank, the Bank of England: remove or reduce systemic risks with a view to protecting and enhancing the resilience of the UK financial system.

• Bank of International Settlements: Basel III’s capital and liquidity adequacy.

• Internal audit role: more importance placed on independent assurance’.

17

QUESTIONS?

18

Case study references• How the Financial Conduct Authority will investigate and report on regulatory failure April 2013

http://www.fca.org.uk/static/fca/documents/how-fca-will-investigate-and-report-regulatory-failure.pdf

• Viral V. Acharya, Thomas Cooley, Matthew Richardson and Ingo Walter, MARKET FAILURES AND REGULATORY FAILURES: LESSONS FROM PAST AND PRESENT FINANCIAL CRISES FIRST DRAFT: 5 DECEMBER 2009 http://pages.stern.nyu.edu/~sternfin/vacharya/public_html/market_failures.pdf

• Financial Crisis: a perfect storm or regulatory failure by Léon Courville http://www.hec.ca/iea/seminaires/120508_leon_courville.pdf

• The failure of financial regulation by Michael Pomerleano http://blogs.ft.com/economistsforum/2009/01/the-failure-of-financial-regulation/#

• Dodd–Frank Wall Street Reform and Consumer Protection Act http://en.wikipedia.org/wiki/Dodd%E2%80%93Frank_Wall_Street_Reform_and_Consumer_Protection_Act

• Volcker Rule http://en.wikipedia.org/wiki/Volcker_rule

• A review of corporate governance in UK banks and other financial industry entities. Final recommendations. 26 November 2009 http://webarchive.nationalarchives.gov.uk/+/http:/www.hm-treasury.gov.uk/d/walker_review_261109.pdf

• Dysfunctions in economic policymaking Part I: simple stories, complex systems and corrupted economics George Yarrow http://rpieurope.org/Publications/Essays_New_Series/Yarrow_Dysfunctions_in_economic_policymaking.pdf

• Lessons from the crisis for central bank management by John Mendzela http://www.mendhurst.com/download/Management-Lessons-from-the-2007-Crisis.pdf

• “Bankers’ Banks”: the Role and Function of Central Banks in Banking Crises By: Sam Vaknin, Ph.D. http://samvak.tripod.com/nm018.html

19

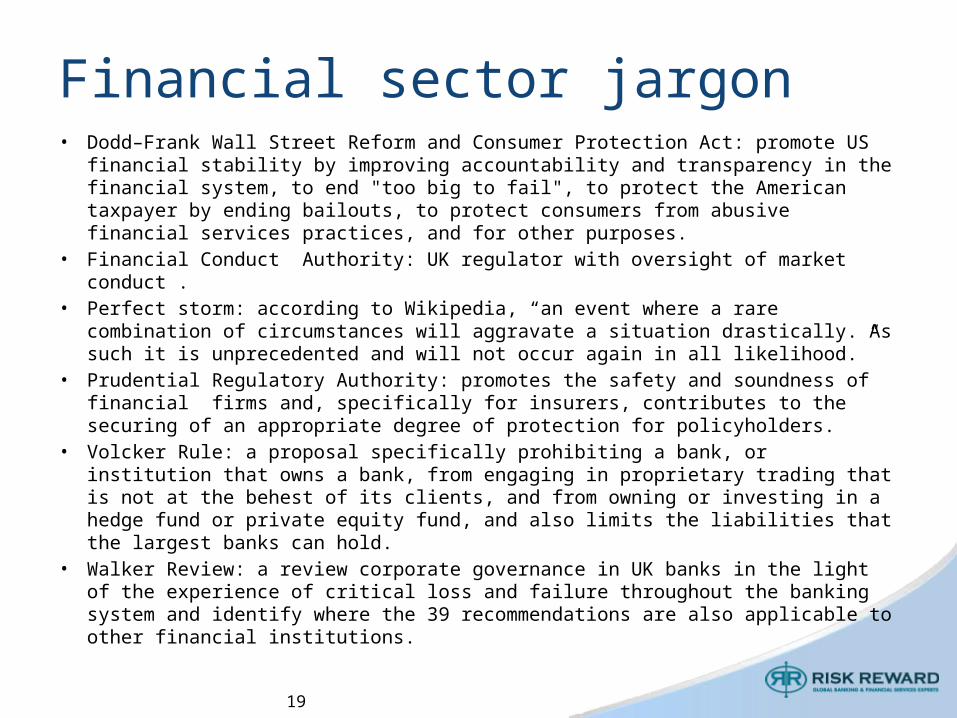

Financial sector jargon• Dodd–Frank Wall Street Reform and Consumer Protection Act: promote US financial

stability by improving accountability and transparency in the financial system, to end "too big to fail", to protect the American taxpayer by ending bailouts, to protect consumers from abusive financial services practices, and for other purposes.

• Financial Conduct Authority: UK regulator with oversight of market conduct . • Perfect storm: according to Wikipedia, “an event where a rare combination of

circumstances will aggravate a situation drastically. As such it is unprecedented and will not occur again in all likelihood.”

• Prudential Regulatory Authority: promotes the safety and soundness of financial firms and, specifically for insurers, contributes to the securing of an appropriate degree of protection for policyholders.

• Volcker Rule: a proposal specifically prohibiting a bank, or institution that owns a bank, from engaging in proprietary trading that is not at the behest of its clients, and from owning or investing in a hedge fund or private equity fund, and also limits the liabilities that the largest banks can hold.

• Walker Review: a review corporate governance in UK banks in the light of the experience of critical loss and failure throughout the banking system and identify where the 39 recommendations are also applicable to other financial institutions.