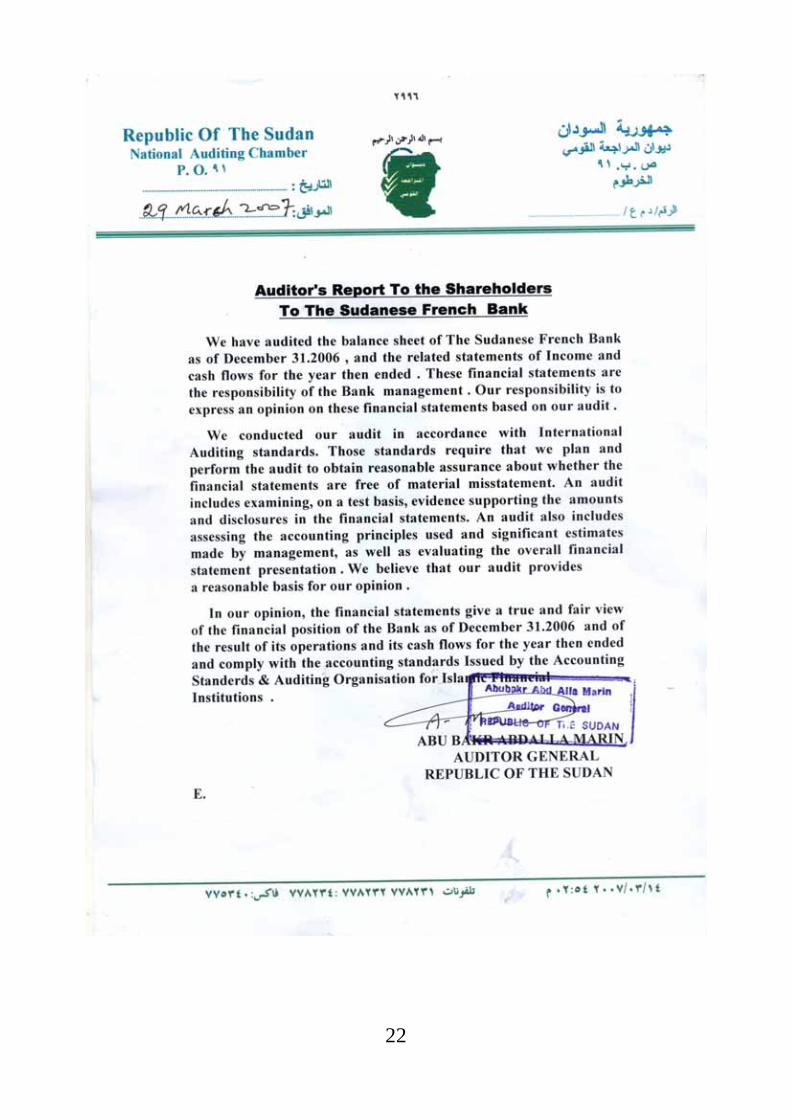

Sudanese French Banksfbank.net/pdfiles/Annual_2006_eng.pdf · Tag Elsir Hamid Abdul kareem Assist....

36

1 Sudanese French Bank Annual Report 2006

Transcript of Sudanese French Banksfbank.net/pdfiles/Annual_2006_eng.pdf · Tag Elsir Hamid Abdul kareem Assist....

1

Sudanese French Bank

Annual Report 2006

2

أعوذ باهللا من الشيطان الرجيم

:قال تعاىل )ينبئُكُم بِما كُنتم تعملُونَوقُلِ اعملُواْ فَسيرى اللّه عملَكُم ورسولُه والْمؤمنونَ وستردونَ إِلَى عالمِ الْغيبِ والشهادة فَ(

صدق اهللا العظيم

) 105(سورة التوبة

3

Nominal Capital is (7) billion Sudanese Dinnar Paid Up Capital : 33,782,307,540 Shares at a value of 5,067,346,131 Sudanese Dinnar Head Office : Al Qasr Street – Khartoum P.O. Box : 2775 Khartoum – Sudan Telephone : (+249)1 83771730 - 83776542 – 83787868 Fax : (+249)1 83790391 – 83774832 – 83771740 Web Site : www.sfbank.net E-Mail : [email protected] Swift code: SUFRSDKH Member of Union of Arab Banks Member of Bank Deposits Guarantee Fund Member of Arab Trade Financing Program

Contents

4

- Board of Directors - Executive Administration

- Bank Branches

- Bank’s Share Capital in Companies

- Chairman’s Report

- Ordinary Meeting Decisions

- Executive Management Report

- Auditors Report

- Financial Statements 2006

- Sharia Board Report

- List of Forgien Correspondents

Board of Directors Dr. Izz El Din Ibrahim Hassan Chairman Mr. Al Nur Abdul Salam AL Hilo Member Mr. Osman Hamad Mohamed Kheir Member

5

Mr. Abdul Gadir Suleiman Hag Hussien Member Mr. Abdul A’l Al Dawi Abdul A’l Member Mr. Victor Hakim Maximos Member Mr. Sidig Al Sadig Al Sidig Al Mahdi Member Mr. Hussein Fadul Ali Member Mr. Bahr Al Din Dawod Ismail Member Mr. Ahmed Mansour Al agab Member Mr. Musaad Mohamed Ahmed Abdul Kareem (G. M.) Member Company Secretary : Ismail Abdullah Mohamed Saleh Legal Adviser : Dr.Tag Alsir Ibrahiem Alshoush Certified Accountants : General Auditing Chamber – Khartoum Tel : 83778232 – 83778231 P.O. Box 91 Khartoum Sharia Supervisory Board : Sheikh. Al Tayib Al Faki Musa Chairman Dr. Hassan Abdullah Al Amin Member Mr. Al Bagir Yousif Mudawi Member

Executive Management General Manager : Musaad Mohamed Ahmed Abdul Kareem Deputy Manager : Kamal Abdul Gadir Saeed Assistant General Manager : Farah Haj Nur Tahir

6

Assist. G. M. For Investment, Marketing & Research Abd Ulmonaim Elhaj Mohammed Assist. G. M. For Administration Affairs Tag Elsir Hamid Abdul kareem Assist. G. M. For Financial Affairs Department Managers :

Adil Salih Bilal Internal Auditor Dept. Suad Yousif Zimrawy Human Resources Dept. Mohamed Batran Hamad Computer & Information Technology Dept. Mohamed Nory Mohamed Foreign Dept.

Alawia Mohamed Ahmed Suliman Investment Dept. Muhsain Abdul Hameed Ali Khalil Administration Affairs Dept. Nayra Abd Alla Sharfi Marketing & Research Dept. Osman Ahmed Osman Elhassan Financial Affairs Dept. Sief Eldin Elfakki Mohammed Legal Dept. Mutwakel Yousif Mustafa Risk Management Dept. Ibrahiem Elhiber Babiker Reconciliation Unit Ishraga Gafar Abdul Raheem Electronic Services Unit

Bank Branch Branch P.O.

Box Area Code

Tel. No. Fax No.

Main Branch-Khartoum 2775 +249-1 83785250 - 83776542 83779300 Algamhouria 1950 +249-1 83781735 -83778600 83773696 Khartoum(2) 6640 +249-1 83472833 - 83461107 83471627 Alsaggana 87 +249-1 83462545 - 83463905 83460589 Khartoum North 1591 +249-1 85339907 -85339908 85339910 Omdurman 1055 +249-1 87568729 - 87555068 87554643 Souk Libya 45 +249-1 87609203 - 87609201 87609202 Alsouk Almahali 12606 +249-1 83438840-83414580 83438838 AlRiyadh Khartoum - +249-1 83520022-83520025 83520024 Port Sudan 871 +249-311 820945 - 824440 826280 Qadariff 191 +249-441 843303 - 833069 843352 New Halfa 134 +249-421 822153 - 822383 822522 Madani 305 +249-511 842307 - 843076 843725 Sinnar 122 +249-561 823203 -822280 823116

7

Rabak 108 +249-572 825070 825145 Almanagil 12 +249-517 872112 - 879999 873200 Hasahissa 86 +249-541 832165 831050 Aldamazin 45 +249-551 822094 - 822394 822394 Obeid 432 +249-611 824333 - 823246 822670 Nyala 456 +249-711 832305 - 833280 832889

Sub-branches :

- Khartoum Airport - Jinaid Sugar Factory

Hasahissa - Tel: 0541840061 - Duty Free Area

Port Sudan – Tel: 0311849045 - Hilton Port Sudan

Port Sudan – Tel: 0311398800 ATM :

Khartoum Branch Qasr Avenue Khartoum(2)Branch Khartoum (2) Gamhouria Branch Cross Of Qasr Avenue With Gamhouria Avenue Omdurman Branch Mawrada Street Alriyadh Branch Almashtal Street Khartoum Land Port Alsouk Almahali Wad Madani Branch Wad Madani Port Sudan Branch Port Sudan

The Participations of the Bank in the Companies and Corporations The bank, since its incorporation in 1978, participated in the capital of the companies and public corporations. The purpose was to project its national role and make the development projects a success. These companies are considered one of the investment channels of the resources of the bank, for achieving a suitable return. In this core, the bank participated in a number of projects, which have a direct impact on the economy of the Sudan. Of these are the following: - 1/ The Sudanese Investment and projects co. Ltd. (SIPCO)- owned by a ratio of 100%. This Company operates in the various fields of investment. It played an effectives role in the import of strategic goods and the export of the Sudanese crops, at a very high efficiency. This Company (SIPCO) owns the following: - - The International Silos and Grain Development Co. (ISOCO): which is a pioneering company

in the field of grain storage, with a long experience in the work of sifting, cleaning, steaming and cleaning crops. The Company own modern silos at Gedarif town, which cost of construction amounted to seven millions US dollars, with a storage capacity of 50 thousands tons.

(SIPCO) also participates in the following companies: - (a) Juba Insurance Company. (b) The Sudanese telecommunications Co. (SUDATEL). (c) The Sudanese Rural Development Co. (d) The Arab Financial Services Co- Bahrain. (e) The Sudanese Horticultural Exports Co. (f) The Gezira and Managil Cotton Textile Co.

8

(g) The Sudan Oil Seeds Co. 2/ The 'Faransi' Financial Services Co. Ltd The bank coped with the development of investment in stocks exchange, by establishing this Company, to be its assisting arm, together with its clients, in the field of investment in stocks and shares. It operates as an approved agent in Khartoum stock Exchange, in the following fields: - - Purchase and sale of stocks and shares, for the interest of the clients. - The management of the clients, Investment Portfolios, to a lucrative return, through a selected

basket of the stocks and shares, which are recorded at the Khartoum stock Exchange. - The marketing and promotion of the issues of stocks and shares for the interest of the clients. - The provision of the information about the prices of the stocks of the companies, which are

recorded in the stock Exchange. - Assist in the monetization of the stocks, in the suitable time.

3/ Transworld Petroleum Investment Co. Ltd. 4/ The Financial Investment Bank. 5/ The National Gulf Flour Mills Co. 6/ The Milk Products Factory- Kenana. 7/ Al- Rai Al-Am Printing and Publishing Co. 8/ The Banking Electronic Services Co. Ltd. 9/ The Exports Insurance and Financing National Agency. Report of the Chairman of the Board of Directors To the 35th Annual General Meeting of the Shareholders of Sudanese-French Bank Dr. Izaddin Ibrahim Chairman of the Board of Directors Brothers and Sisters, I greet you in this blessed night and, on behalf of my colleagues, members of the Board of Directors I welcome you to this meeting and would like to thank you very much for accepting the invitation to attend this 35th annual general meeting, during which I will present to you a general preview of the work of the Board during its present term which will end by the conclusion of this meeting. I will also review before the activities of the Bank and new developments until the present day to enable you to include them in your deliberations and discussions. It has always been our practice to explain everything to you in complete clarity and transparency aiming at reinforcing the development of the Bank, while looking forward to listening to your comments and views which guide us to confront all difficulties and inspire us towards excellence in an ever changing environment. Brothers and Sisters, Have that noticed, after perusal of the report before you , the remarkable growant & diversification of activities and volume of business of the Bank in all banking, financial and investment fields, within systematic frameworks and through specific programs and targets that were formulated by the Board, its specialized committees and the executive management with all its departments and branches all over the Sudan. Our approach of consultations based on planning and follow-up has resulted in an increased confidence of clients in dealing with our Bank in all fields of activities inside the country and abroad.

9

This has been clearly manifested in increases in resources, revenues, net profits and shareholders’ rights. And it reflects full execution of the comprehensive reform program and formulation of rules and regulations that govern the work of our Bank, a task continuous demanded relentless efforts exerted by the Board and its specialized committees, including the Administrative Committee, Finance and Investment Committee, Audit and Control Committee, Legal Affairs Committee and Constructions Committee it is worthmentioning that the Board and its committees have issued about 365 decisions during 2006. Brothers and Sisters, The policy of the Bank is built on three pillars, namely, shareholders, clients and staff. As an acknowledgment of our gratitude towards shareholders who put their confidence in us by electing us as a board, we always reserve to them some of the fruits of the successes of the Bank; in 2003 we have distributed 15% of the paid capital (amounting to SDD 2.2billion.) as cash dividends; in the following year percentage was raised to 16%; in 2005 the same percentage was paid in addition to distributing bonus shares amounting to 127% of the paid capital. As for this year and as per the recommendation raised to the Board the distribution will be raised to 22%, (12% as cash dividend and 10% as bonus shares). This will raise the paid up capital from SDD 2.2 billion. to SSD 5.6 billion. by the end of 2006 in addition to reserves amounting to SSD 1.8 billion., i.e. shareholders rights will raise to SSD 7.4 b. To make it easier for our clients in their dealings with bank we have established two new branches; reinforced the use of the electronic network between Bank HQ and branches to facilitate speedy and convenient services, installed ATMs at accessible locations and provided our clients, Electronic Cards free of charge, to enable them to withdraw cash from their accounts at anytime. In addition to all of this we gave great attention to improving the work environment at our branches to enable them to finalize transactions speedily and conveniently within the context of excellence. We have also established Al-Faransi Financial Services Company to facilitate dealings with the Khartoum Stock Exchange. It became one of the main companies in its field within a very short time. Externally, the network of the Bank correspondents’ have expanded in addition to sizable facilities obtained from correspondents facilities granted to the Bank at reasonable margins that enabled us to attract more distinguished clients. Brothers and Sisters, As for the Bank staff, which constitutes the third pillar in our organization beside the shareholders and the clients, good improvements have been made in their terms of service through salary increase, training and good working condition. I am honored today to tell you that an agreement has been reached with the Bank Staff Association on pay improvements for five years starting as of this year. This has meant and will lead to more stability, which will create common grounds for trust and cooperation between Bank management and the Association. Brothers and Sisters, The Board has been preoccupied throughout the past three years trying to settle the issue of the nominal value of our shares which have been corroded as a result of the inflation of the 1990s. Moreover, the introduction of the Dinar to replace the Pound reduced the nominal value to meager figures, yet the situation has exacerbated even further by the announcement of the Government to introduce the new Pound which equals one thousand old Pounds. On top of that the number ofshares have grown to reach 33 billion, which meant extreme complications in their management. To allow for the settlement to be effected in correct and legal manners, an extra-ordinary meeting was held in December 2004 whereby the Board had secured an authorization from you to do what was required to settle the issue of shares. After a careful study; and after thoughtful discussions of all available options; and to implement the decisions of your said extra-ordinary meeting the Board decided to amalgamate shares in units of one thousand shares each. The value of each of these units will be one and a half new Pounds. Accordingly, the number of shares will be 33 millions instead of 33 billions without any significant change in the total value of the shares.

10

When amalgamating shares there will be some shareholders whose shares are less than the required number for the new unit and the Board has decided in this regard to consummate these to become full units. The cost of this operation will not exceed one million SDD for all shares. Dealing with the new unit shares will start on 1st of July 2007, i.e. the same date the SDD ceases to be the official currency of the Sudan. Brothers and Sisters, 2006 has witnessed remarkable and noticeable developments in all aspects of the business of the Bank and in its financial performance, as you can see in the report handed out to you. I would like to refer, generally, to the following:

1- The year has witnessed the establishment of two branches in suk-mahali and Riyadh in Khartoum at locations of good diversified economic activities, bringing the total number of branches to 20 besides four offices, all linked through a banking data network.

2- All branches have been linked through a modern digital exchange to facilitate communication, speed up and improve services to clients and make the best of the data network linking all branches of the Bank.

3- An increase in the volume of Bank transactions in the operations of foreign exchange and external trade, including letters of credit and collections, in addition to money-changing and external transfers. This increase amounted to US$ 1.8 billion. in 2006 compared to US$ 1.5 billion. in 2005, at a growth rate of 20%.

4- In the field of human resources management, 2006 has witnessed a remarkable activity through continuation of the comprehensive reform program, especially in its parts relating to accumulated balances of annual leaves and the widespread rotation of staff at different levels and grades. The year has also seen appointment of new staff members at the beginning of the service ladder, a move that helped in the implementation of the rotations and annual leaves programs. Widespread promotions have also been effected during the past three years to diffuse bottlenecks and stalemates in the organizational structures approved by the Board. General manager

Assistants’ posts have been filled through promotion of leaders within the Bank itself. Great emphases during the same year have been placed on the aspect of training to the extent that the number of those who trained reached 491 as compared to 280 in the previous year, not including those who trained abroad within the context of our cooperation with foreign correspondents. 5- The Bank has met all requirements of restructuring required by the Central Bank. The

capital adequacy ratio of our bank amounted to 18.9% compared to only 8% demanded by the Central Bank.

6- Attention has been given to the follow up and collection of non performing debts to reduce their percentage and to build up enough provision to cater for bad and doutfull debts by about sdd 900 m. in addition to the continuation of building up the special reserve which amounted now to Sdd 716 m. to cover any unforeseen debts. As a result of this the percentage of non –performing loans dropped to 5.6% compared to 6% last year, which is within international standards.

7- The Bank has stood up for its national and social roles by contributing to benevolent projects by giving donations to hospitals, educational institutions and worship shrines; providing support to those who suffered from rains and floods in the State of Sinnar, the Nile and the Northern States. The Bank has also provided support to the Lebanese people during the last war in Southern Lebanon. Donations during 2006 amounted to SdD 23 m. compared to Sdd 21.5 m. in the previous year.

8- Direction of Bank financing towards development projects and national financing in agricultural, industrial and services sectors through financing major operations. Our Bank has the biggest share in financing irrigated agricultural sector and building of strategic reserve of sorghum. The Bank continued financing of renovation of Khartoum State Water

11

Network Project and financing National Electricity Corporation projects. Our Bank has also recently agreed to finance development projects in a number of States with excellent guarantees.

9- Efforts have continued in improving work environment within the context of the reform program going on for a number of years now, which have been manifested in renovation and maintenance of estates owned by the Bank. The Bank has also endeavored to own new locations for branches in areas witnessing growth in economic activities, and has already approved funds to establish branches in Hasahisa, Rabak, and Khartoum 2. A building has already been bought in Managil for the same purpose.

10- 2006 has also witnessed an expansion in the Bank’s marketing activity through various publications promoting services, sign boards, performance evaluation studies for some branches and field tours to various locations of branches to follow up upgrading of services process and to provide assistance to some branches to enable them attract new clients. The Bank’s internet site has been updated to reflect all information relating to its history, services, branches inside the Sudan and network of correspondents abroad and companies owned by the Bank. The Bank is currently working to develop and update the website to reflect all developments concerning the Bank and banking in general.

11- Our Bank has always been one of the first banks chosen by the Central Bank to test national projects relating to banking technology. The Bank has participated, right from the beginning, in the national transfer project, electronic clearinghouse and electronic returns. This has enabled the Bank to provide banking services accountly in punctuality. The number of ATMs has reached to 8, including 6 in Khartoum and one at each of Medani and Port Sudan while 25 additional ATMs have been ordered, bringing the total number of ATMs to 33 by the end of 2007. The Bank is intending to embark on a central data base to pool in all data from all branches in a unified central data base to facilitate dealings in all banking services, especially modern electronic services, which will greatly reduce cost.

Brothers and Sisters, As the term of this Board will come to an end by the conclusion of this meeting we would like to refer to our achievements compared to what has been the case in 2003 when the Board began its term:

a) Total assets increased by SdD 35.9billion. from SdD 43.8 billion. to SdD 79.7billion., in rate of increase82%.

b) Deposits increased by SdD 29.4billion. from SSD 29.9 b. to SdD 59.4billion, amounting to 98%.

c) Net profits increased by SdD 1.7billion. from SdD 326million. to SdD 2billion., amounting to 521%.

d) Capital adequacy ratiorose from 15.6% to 18.9%. e) Current rate remained at 1:1 (one to one), which means that the Bank didn’t face any

liquidity problems and was able to meet all current commitments at their specified time, which in turn means optimum use of liquidity.

f) Paid up capital rose by SDD 3.4 billion from SDD 2.2 billion in 2003 to SDD 5.6 billion. in 2006, i.e rate of increase equal to 154%. This means that the Bank, judging from its present performance, will be able to raise its paid capital to the level specified by the Central Bank, of SDD 6billion., by the end of 2007. It is worthy of note that the grace period given by the Central Bank extends to 2009.

g) The total ownership rights rose by SDD 3.4billion. from SDD 3.7billion. in 2003 to SDD 7.4billion. in 2006i.e rate of Increase equal to 100%.

h) The percentage of profits distributed to shareholders during the period 2003-2006 amounted to 196%, 59% as cash dividend and 137% as paid shares.

i) The Board continued its relentless efforts to follow up the performance of the companies wholly or partly owned by the Bank. The Bank has also established Al-Faransi Financial

12

Services Company which managed to occupy a distinguished position within financial services companies accredited by Khartoum Stock Exchange Market. As a result of these efforts the Bank received profits amounting to SDD 118.7 m. compared to SDD 23.7 in the previous year, i e. an increase of SDD 95 m. Moreover, Al-Faransi and cipco companies earned the Bank profits amounting to SDD 103 m. that will be added to profits of the Bank for the 2006 financial year. This in addition to the proceeds of the lease contract of the Gulf Flour Mills, in which the Bankowns a 49% shares will earn the Bank decent profits during 2007 financial year. The Bank has recently established Window Electronic Services Company to deal in pre-paid coupons/cards and have already secured a contract with the National Electricity Corporation to provide it with services, while contracts with major communication companies are currently being finalized for the same purpose.

Brothers and Sisters, Please allow me to extend, in your name, sincere thanks to the Governor of the Central Bank and his deputies and assistants for the support and help extended to this Bank during the past period until it surpassed the difficult situation we all know. Thanks in your name are also extended to the auditor general chamber, the Sharia Controls Board and observers to this meeting from the Central Bank, Commercial Registrar and Khartoum Stock Exchange Market. Brothers and Sisters, In conclusion, on behalf of myself and my brothers in the Board, I would like to thank you for the confidence you vested in the Board during the past three years. My special thanks go to those shareholders who communicated with us offering their advice both verbally and in writing. I would also like to thank members of the Board for their cooperation, and I must commend the spirit of togetherness and harmony between all members of the Board, which contributed greatly to success we achieved. This success wouldn’t have bee possible without the cooperation of the excuting management apparatus headed by the General Manager and his deputy and Assistants, and without the great cooperation we found from the Bank Staff Associations, the previous and current, who participated in securing the stability required for success. Brothers and Sisters, During the last few months big shareholders have joined the Bank, namely Fly Overseas Lubwan Company and Bank of Beirut. This will strengthen the Bank and reinforce confidence in it, and will, we hope, add new qualitative dimensions and expertise that will enable it to make remarkable strides both internally and externally. As this meeting represents a demarcation line between a Board whose term is ending and another Board for the new term, I would like to wish the new Board every success and I must reiterate to them that we will hand over to them a Bank that has fully recovered and is enjoying a reputable position in the Sudanese economy. I do hope that they will keep on the success and will move on to new high horizons. Brothers and Sisters, At the end of this report, and after we listen to your views and suggestions, will you please endorse the agenda of this meeting contained in the pamphlet distributed to you prior to this meeting, by voting on them. The items are:

1) Endorsement of the Board of Directors’ Report for 2006. 2) Approval of the of the balance sheet, income statement, distribution of profits account and

reports of the certified auditor and sharia controls board for the year ending on 31 December 2006 as per the recommendation of the Board.

3) Endorsement of the recommendation of the Board of Directors on the profits of 2006. 4) Approval of the remunerations of members of the Board for 2006 in accordance with Article

61 of the Bank article of association. 5) Authorization of the Board to appoint a certified auditor in consultation with the Central

Bank of Sudan, and set out their remunerations for auditing the 2007 accounts.

13

6) Appointment of the Sharia Controls Board for 2007 and authorization for the Board to set out their remunerations.

7) Election of members of the Board of Directors for the term 2007-2009 in accordance with Article 95 of the Bank Chart.

8) Any othermatter that could be discussed in an Ordinary General Meeting upon recommendation from the Board of Directors.

May God guide us all to success Dr. Izaddin Ibrahim Hasan Chairman of the Board of Directors

Decisions Of The 35th Ordinary General Meeting Held on 10 May 2007

Decision No. (1): Approval of the report of the Board of Directors, the consolidated financial status statement, the income statement and the reports of the auditor and the Sharia Supervisory Board, for the year ending on 31/12/2006.

Decision No. (2): Approval of the recommendation of the Board of Directors on distribution of profits, including payment of dividends in cash to shareholders by ratio of 12% and the allotment of new shares by ratio of 10% of the shares of every shareholder as on 31/12/2006.

Decision No. (3): Approval of the recommendation of the Board of Directors on payment of remunerations to members of the Board of Directors for the year 2006 . Decision No. (4): Appointment of a certified Auditor, to audit the bank accounts for the year 2007, in consultation with the Central Bank and authorizing the Board of Directors to fix and pay his fees.

Decision No. (5): Appointment of the following, as members of the Sharia Supervisory Board:-

1- Sheikh El- Tayeb El-Faki Musa Chairman 2- DR. Hassan Abdallah El- Amin Member 3- Sayed Al-Bagir Yousif Modawi Member

Decision No. (6):

14

Ismail Abdallah Mohamed Salah, Secretary of the Company

Performance Report and Financial Statement for 2006

Mr. Musaad M.A.Abdulkarim Managing Director

Bank Performance Indicators during 2006:

The bank activity continued to grow remarkably as reflected by indicators of performance in different administrative and banking fields. Thanks to the stability, planning and careful follow up by the Board of Directors and the executive management and the relentless efforts of the bank staff. All this resulted in a remarkable expansion in the bank activities and sizable returns to shareholders and clients. 2006 has witnessed the following:

First; Financial Position Statement:

a) Assets: The total value of financial position statement (assets) of the bank amounted to SDD

79.68 b. during 2006 as compared to SDD 71.87 b. in 2005, rising by SDD 7.81 b. i.e. 11%. The value of current assets during 2006 amounted to SDD 76.26 b., the value of the current liabilities amounted to SDD 72.31 b. during the same period, i.e. at current ratio of (1.06:1.00), which means that the bank is in a good financial position and is able to meet all commitments as and when required, because the value of the current assets is higher than the value of the current liabilities by SDD 3.95 b., and the amounts used in short term investments rose from SDD 16.33 b. to SDD 17.12 b. during 2006, i.e. growing by 5% (SDD 0.79 b.), reflecting optimum use of available resources.

Growth of Assets during the period 2002-2006 (in SDD b.)

15

b) Cash and Cash equivalent

Cash and Cash alike amounted to about SDD 26.01b.during 2006 compared to SDD 26.87 b. in 2005, with a minor drop of SDD 0.86 b. amounting to 3%. Compared to last year the balance in local currency (treasury + Central Bank) rose by 28% from SDD 10.01 b. in 2005 to SDD 12.86 b. in 2006. On the other hand the local equivalent of the foreign exchange balance (treasury + Central Bank) dropped by 37% from SDD 4.05 b. in 2005 to SDD 2.56 b. in 2006. Foreign currency deposits dropped from SDD 12.80 b. in 2005 to SDD 10.58 b. in 2006, i.e. by 17% (SDD 2.22b.). This is attributed to the rise in the value of the local currency against foreign currencies by about 13% during 2006 as compared with 2005.

Components of Cash and Cash equivalent during the period 2002-2006 (in SDD b.)

c) Financing:

Total value of financing extended in both local and foreign currencies during 2006 amounted to SDD 33.84 b. compared to SDD 27.08 b. in 2005, i.e. an increase of 25%

16

amounting to SDD 6.76 b. This may be broken down to a) local currency financing and b) foreign currency financing. Hereunder we are providing some analyses of financing extended during 2006 compared to previous years:

1- Local Currency Financing: Financing extended during 2006 amounted to SDD 30.44 b. as compared to

SDD 28.89 b. in 2005, i.e. rising by 5% (SDD 1.55 b.), while recovered financing, during the same period, amounted to SDD 23.69 b. as compared to SDD 17.33 b. in 2005, i.e. rising by 37% (SDD 6.36 b.), which indicates high efficiency in collection and follow up, and securing good guarantees for financing operations. Current financing balance in 31 December 2006 amounted to SDD 31.39 b. compared to SDD 24.81 b. in 2005, i.e. rising by 26% (SDD 6.58 b.).

Total Local Currency Financing during 2006 (in SDD b.)

Hereunder is a breakdown of the Financing forms used during 2006: - Murabaha: constituted 59.9% of the total value of financing extended during 2006

compared to 43.94% in 2005. - Musharaka: constituted 8.5% of the total value of financing extended during 2006

compared to 5.75% in 2005. - Mudharaba: constituted 9.5% of the total value of financing extended during 2006

compared to 0.69% in 2005. - Salam: constituted 1.4% of the total value of financing extended during 2006 compared

to 0.61% in 2005. - Mugawala: constituted 0.3% of the total value of financing extended during 2006

compared to 5.94% in 2005. - Shahama Certificates: constituted 6.3% of the total value of financing extended during

2006 compared to 16.94% in 2005 - Government Bonds: constituted 1.6% of the total value of financing extended during

2006 compared to 21% in 2005. - Others*: constituted 12% of the total value of financing extended during 2006

compared to 4.33% in 2005. (* includes consortium funds and stocks - goods)

17

Financing per Economic Sectors: Bank management took into consideration the principle of equitable distribution of financing resources amongst various economic sectors commensurable to the policies of the Central Bank and objectives of the national economy. The chart below shows distribution of funding per economic sectors during 2006: the agricultural sector constituted 17.83%, industrial 17.19%, export 2.57%, transport and storage 4.50%, professionals and craftsmen 1.88%, local trade 29.72%, import 0.76%, shahama 6.33%, government bonds 1.66%, others 5.01%, real estate and services 12.55%.

Funding by Economic Sectors for 2006

2- Foreign Currency Financing:

18

The volume of foreign currency financing during 2006 amounted to US$ 15.14 m. compared to 17.94 m. in 2005, dropping by 16% (US$ 2.8). Foreign currency financing balance during 2005 amounted to US$ 9.99 m. compared to US$ 11.20 in 2006, i.e. an increase of 12% (US$ 1.21 m.). Profits earned from foreign currency financing during 2006 amounted to US$ 1.01 m. equaling SDD 222.69 m. as compared to US$ 1.11 m. in 2005, i.e. a drop of 9%. It is worthy of note that the drop in profits earned in foreign currency was 9% while the increase in profits earned in local currency was 18%, and this is attributed to the drop in the value of US$ against the SDD during 2006.

Total Financing In Foreign Currency 2002-2006 (In Million USD)

d) Fixed Assets:

The book value of fixed assets, before depreciation calculation, has risen from SDD 3.95 b. in 2005 to SDD 4.22 b. in 2006. After calculation of extras and eliminations and after deduction of depreciations the net nominal value amounted to SDD 2.6 b. in 2006 as compared to SDD 2.47 in 2005. The net value of real estate is SDD 1.37 b. representing 52% of the total net value of fixed asset

Fixed Assets During the Period 2002-2006(in SDD b.)

e) Dues and Shareholders Rights:

19

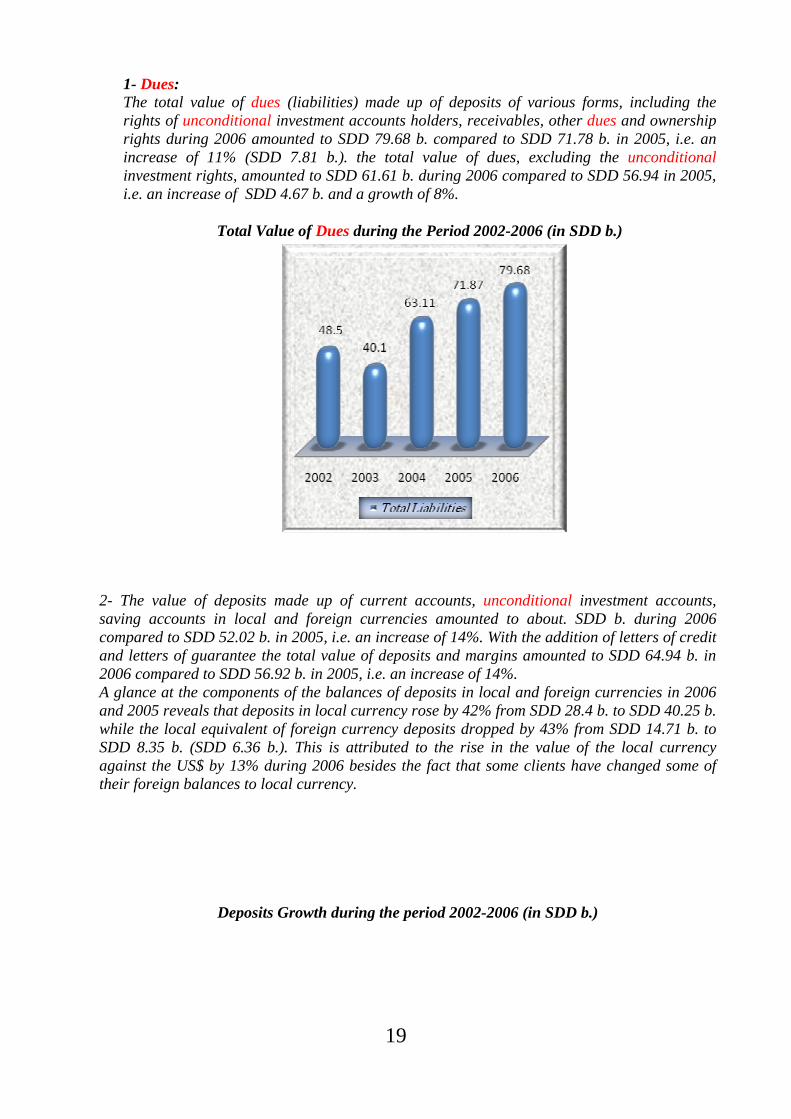

1- Dues: The total value of dues (liabilities) made up of deposits of various forms, including the rights of unconditional investment accounts holders, receivables, other dues and ownership rights during 2006 amounted to SDD 79.68 b. compared to SDD 71.78 b. in 2005, i.e. an increase of 11% (SDD 7.81 b.). the total value of dues, excluding the unconditional investment rights, amounted to SDD 61.61 b. during 2006 compared to SDD 56.94 in 2005, i.e. an increase of SDD 4.67 b. and a growth of 8%.

Total Value of Dues during the Period 2002-2006 (in SDD b.)

2- The value of deposits made up of current accounts, unconditional investment accounts, saving accounts in local and foreign currencies amounted to about. SDD b. during 2006 compared to SDD 52.02 b. in 2005, i.e. an increase of 14%. With the addition of letters of credit and letters of guarantee the total value of deposits and margins amounted to SDD 64.94 b. in 2006 compared to SDD 56.92 b. in 2005, i.e. an increase of 14%. A glance at the components of the balances of deposits in local and foreign currencies in 2006 and 2005 reveals that deposits in local currency rose by 42% from SDD 28.4 b. to SDD 40.25 b. while the local equivalent of foreign currency deposits dropped by 43% from SDD 14.71 b. to SDD 8.35 b. (SDD 6.36 b.). This is attributed to the rise in the value of the local currency against the US$ by 13% during 2006 besides the fact that some clients have changed some of their foreign balances to local currency.

Deposits Growth during the period 2002-2006 (in SDD b.)

20

3- Shareholders Rights:

The total value of shareholders rights (in paid capital, various reserves and retained earnings) amounted to SDD 7.37 b. by the end of 2006 compared to SDD 6.02 in 2005, i.e. growing by 22%. The Bank have managed during the past year to raise the paid capital to SDD 5 b. as a result of capitalization of reserves and retained earnings. As for this year the Board has recommended to distribute cash dividend to shareholders valued at 10% of the paid capital (SDD 506 m.) bringing the total paid capital to SDD 5.5 b. Shareholders’ Rights during the Period 2002-2006 (in SDD b.)

Second: Income Statement: Comparative analysis of the 2006 and 2005 income statements reveals the following:

1) The total value of revenues (after deduction of returns of unconditional investment accounts) rose by 4% from SDD 6.23 b. in 2005 to SDD 6.50 b. in 2006. Returns of

21

investments and forward sales (after deduction of returns of unconditional investment accounts) constituted 36% of total revenues (SDD 2.32 b.), banking services returns 38% (SDD 2.47 b.) and other returns/banking transactions returns 26%.

2) The total value of general and administrative expenses, including depreciation and qualification expenses, during 2006 amounted to SDD 6.04 b. compared to SDD 3.47 b. in 2005, rising by 17% (SDD 590 m.). This is attributed to a 20% pay rise, an increase in the contribution to the deposits guarantee fund, an increase in the cost of the national social security fund and depreciations.

3) The value of the net income after deduction of taxes and zakat amounted to SDD 2.04 b. in 2006 compared to SDD 2.21 b. in 2005, dropping by 8%. This happened despite the increase of revenues during 2006 as compared to 2005 from SDD 6.2 b. to 6.5 b. because of increases in expenses and depreciation. The percentage of net income (after deduction of taxes and zakat) to the paid capital has also dropped from 73% in 2005 to 40% in 2006. This is attributed to the increase of the paid capital during 2006 (capitalization of reserves and retained profits) from SDD 3 b. at the beginning of 2006 to SDD 5.07 b. by the end of 2006, an increase of 69%.

Revenues and Expenses during the period 2002-2006 (in SDD b.)

22

23

24

25

26

27

Sudanese French Bank

Notes To The Financial Statements

1. Status And Operations :-

- S.F.B. was established in 1978 and started its banking activity in 1979 under the name

Sudanese Investment Bank , with a capital of Sudanese pound 7.5 million. - In 1981 the name was changed to be Sudanese International Bank. - In 1993 the name was again changed to be The Sudanese French Bank . - Authorized capital increased to 7 billion Sudanese dinar in January 2005. - Paid up capital and reserves equal 7.3 billion Sudanese dinar as at 31/12/2006. - Total assets 79.6 billion Sudanese dinar ( 397 million in US dollar ) as at 31/12/2006 .

Objective & Purposes Of The Bank :- - Aims of SFB are summarized in the recognition of development and investment potentialities

, encouragement of private and public economic sectors and provision of the required fund and other facilities to attain such purpose .

- To contribute to modernize and innovate existing establishment . - To encourage the flow of local and foreign capital to investment , and contribute to the

financing of foreign trade business either directly or through institutions to be established for such purpose .

- SFB activity concentrates mainly on provision of banking services , financing through a network branches covering all parts of the Sudan , beside a number of correspondents all over the world .

Services Provided By SFB Include :-

- To utilize banking technology for providing better services for clients . - Acceptance of different deposits . - Provision of the fund required by individuals , companies , corporations and consortiums ,

and to provide capital for standing and new companies . - Financing of foreign trade transactions . - Management of investment deposits . - Investing and applying of financial surpluses for the sake of participation in country

development .

28

2. Significant Accounting Policies :- The financial statement have been prepared under the historical cost convention in accordance

with generally accepted accounting principles .

2-1. Revenue Recognition :- Income from investment operations is recognized on liquidation . Revenue from other banking operations is calculated on accrual basis .

2-2. Fixed Assets :- Fixed assets are valued at cost less accumulated depreciation . Routine repairs and maintenance are treated as expenses when incurred. 2-3. Foreign Currency Translation :- 1/ Transactions in foreign currency recorded at exchange rates ruling at the date they took place any differences are treated in the profit and loss A/C. 2/ Assets and liabilities in foreign currencies at balance sheet date are converted to Sudanese Dinar at the exchange rate ruling at that date and any differences in exchange are treated as follows :- a/ If the difference (credit) more than one hundred thousand US dollars , an amount equal to one hundred thousand dollar is treated in the balance sheet and any excess is to be treated in the income statement . b/ If the difference (credit) is equal to one hundred thousand US dollar or less it is to be treated in the balance sheet . 2-4. Return on investment deposits :- 1/ The Return of investment deposit is calculated on the basis agreed upon by the bank management and the Islamic Sheriah Board . 2/ It is considered that all investment deposits are completely used in the bank investment . Operations before the bank starts to used its own resources . 3/ The ratios of investment account from usage point of view are considered to be the same as the classification of investment operations ratios .(Sales debtors , Morabaha , Mudaraba …… ect) 4/ The owners of the investment deposits share in all revenues except revenues from banking services and other revenues . 5/ Investment operations expenses are directly charged to the return from investments operations before distribution . 6/ All administrative expenses are borne by the bank . 2-5. Provision for bad debts :- The provision for bad debts is charged according to the Bank of Sudan regulations . 2-6. Inventory :- The year end inventory is valued at the lower of cost or market value.

29

30

31

32

33

34

35

36

Report of Sharia Supervisory Board To: Sudanese French Bank Shareholders Bank Financial Statements For the Year Ended 31/12/2006 All praise be to Allah and peace and blessings be upon Prophet Mohammed and all Prophets and Messengers 1. The Board has looked into all transactions submitted to it this year and issued Fatwas based on the ruling of Islamic Sharia. 2.The Board conducted filed visits to some branches, reviewing transactions and ordered the submission of files of a number of investment operations from other branches to ensure that the contracts conform with the rulings of Islamic Sharia. The Board has issued the necessary directives and replied to inquires by some staff to raise their awareness on these transactions. 3.The Board reviewed bank’s financial accounts up to 31/12/2006 and ensured that investment and saving deposits and revenues obtained from foreign Banks and exchange were in conformity with Islamic Sharia. 4. It gives the Board pleasure to announce that Bank operations be consistent with Islamic Sharia. 5.The Board extend thanks to Bank officials for facilitating its job and pray to Allah, the Almighty to help them continue on the road to progress and prosperity. Sheikh. Al Tayib Al Faki Musa

Chairman, Board of Sharia Control