SUBMITTE D TO: Centre for Microfinance Resaerch...

78

1 | Page SCOPE OF BUSINESS CORRESPONDENTS FOR FINANCIAL INCLUSION IN RURAL AREAS SUBMITTED TO: Centre for Microfinance Resaerch Bankers Institute of Rural Development, LUCKNOW SUBMITTED BY: NEHA, Intern CHANDRAGUPT INSTITUTE OF MANAGEMENT, PATNA DATE: 1/07/2010

Transcript of SUBMITTE D TO: Centre for Microfinance Resaerch...

1 | P a g e

SCOPE OF BUSINESS CORRESPONDENTS FOR FINANCIAL INCLUSION IN

RURAL AREAS

SUBMITTED TO:

Centre for Microfinance Resaerch

Bankers Institute of Rural Development, LUCKNOW

SUBMITTED BY:

NEHA, Intern

CHANDRAGUPT INSTITUTE OF MANAGEMENT, PATNA

DATE: 1/07/2010

2 | P a g e

DECLARATION

I hereby declare that this dissertation entitled “Scope for business

correspondents for financial inclusion in rural areas” submitted in partial

fulfilment for the Award of Post Graduate Diploma in Business Administration

to Chandragupt Institute of Management Patna, was a record of independent

research work carried out by me.

I also declare that this dissertation was a result of my own efforts and has not

been submitted earlier for the award of any degree/ diploma to any other

University.

Neha

Chandragupt Institute of Management Patna.

3 | P a g e

ACKNOWLEDGEMENT

First and foremost, I extend my heartfelt gratitude towards Chandragupt

Institute of Management, Patna and BIRD, Luknow for giving me opportunity

to work on this project.

It had been an enriching experience for me to undergo my summer internship

under BIRD, which would have not been possible without help and support of

all the people around. I would like to express my sincere thanks to all the people

who supported me during the project.

I extend my sincerest gratitude and thank to Sri B.L.Mishra, Dr. Manesh

Chaubey and Prof. S.Dinda for mentoring and guiding me throughout my

internship. Without their constant guidance and support it would have been

impossible for me to complete the project in time. I would also like to thank the

Director of my institute Dr. V. Mukundadas for guiding me during my project.

I also take this opportunity to thank all the people from various Banks, SLBC

Government departments, Companies and clients for giving their valuable time,

suggestion and prompt answers for the questions intended for primary data

collection.

Last but not the least I thank all my friends and members of my family for

encouragement and moral support they had provided.

However, I accept the sole responsibility for any possible error and would be

extremely grateful to the readers of this project report if they bring such

mistakes to my notice.

Neha

Intern,

Chandragupt Institute of Management Patna.

4 | P a g e

CONTENTS

CONTENTS PAGE NO.

Chapter 1

Chapter 2

Chapter 3

Chapter 4

Chapter 5

Chapter 6

Chapter 7

Chapter 8

List of Tables

List of graphs

Abbreviations Used

Executive Summary

Introduction

Methodology

BC Model in India : An Insight

Bihar: Empowering the state through financial inclusion

Bihar Socio –Economic and Banking Profile

Present status of Banking and Financial Services and Banking

Profile of Bihar

Extent of Coverage of BC model in Bihar

Bank wise spread of BCs

CASE STUDIES:

CASE 1 :

Eko Aspire Foundation-SBI

CASE 2 :

Zero Mass Foundation-SBI

CASE 3 :

India Post-SBI

Clients Profile

Stakeholder analysis

Client’s Perspective

Conclusion and Recommendations

Annexures

Annexure I: details regarding number of BCs appointed and

accounts opened by banks (Public and private) Annexure II:

List of 19 districts and banks which successfully completed

100% financial inclusion.

Annexure III: Account opening form of Zero Mass

Foundation and Post Office

Bibliography

5

5

6-7

8-13

14-17

18-20

21-25

26-30

27-28

29-30

31-35

33-35

36-43

44-53

54-58

59-62

63-68

69-73

74-78

74-75

76

77-78

79

5 | P a g e

LIST OF TABLES

LIST OF GRAPHS

SERIAL

NO.

NAME PAGE

7.1.1 Age group wise classification of clients 59

7.2.1 Occupation pattern 59

7.3.1 Educational profile of clients 60

7.3.2 Classification of New and Old accounts 61

7.3.4 Number of new/old accounts for all the

three BCs

62

Table

No.

Name Page No.

2.3.1 Sample CSPs 20

4.2.1 Comparative data of Bihar and India for various socio

economic indicators

29

4.2.2 Banking profile of Bihar 30

5.1.1 Banks and their BCs working in different areas of

Bihar

32

5.2.2 Business of different BCs as on 31st May 2010. 33

6.1.1.6.1 Remuneration paid by Bank to BC(Eko Aspire) 42

6.1.1.6.2 Remuneration by BC to CSP 42

6.1.2.8.1 Remuneration paid by Bank to BC(Zero Mass) 52

6.1.2.8.2 Remuneration by BC to CSP 52

6.1.3.5.1 Remuneration paid by bank to PO 57

7.2.1 Crosstab of Occupational pattern and banking history

of clients

61

6 | P a g e

ABBRIVIATIONS USED

ALW A Little World

BC Business Correspondent

BC Business Correspondent

BF Business Facilitator

BIRD Bankers Institute of Rural Development

CSC Customer Service Centers

CSP Customer Service Points

EDGE Enhanced Data rates for GSM Evolution

EKO Eko Foundation

FI Financial Inclusion

FIF Financial Inclusion Fund

FITF Financial Inclusion Technology Fund

GOI Government Of India

GPRS General Packet Radio Service

KYC Know Your Customer

mFI Micro Finance Institution

MOU Memorandum Of Understanding

NABARD National Bank for Agriculture and Rural Development

NBFC Non Banking Financial Company

NGO Non Governmental Organization

PNB Punjab National Bank

7 | P a g e

PO Post Office

RBI Reserve Bank Of India

SBI State Bank of India

SLBC State Level Bankers Committee

ZMF/ZERO Zero Microfinance and Savings Support Foundation

8 | P a g e

EXECUTIVE SUMMARY

In order to meet the objective of financial inclusion and increasing outreach of

the banking sector to the unbanked, Reserve Bank of India, in January 2006

permitted banks to use intermediaries as Business Facilitators (BF) or Business

Correspondents (BC) for providing financial and banking services. The BCs

were allowed to conduct banking business as agents of the banks at places other

than the bank premises. The categories of entities that could act as BCs were

also specified. Since its inception in 2006, various banks had started promoting

the BC Model in all corners of the country. The Reserve Bank vide its circular

DBOD.No.BL.BC.58/22.01.001/2005-06 dated January 25, 2006 permitted

banks to utilize the services of non-governmental organizations (NGOs), micro-

finance institutions (other than Non-Banking Financial Companies) and other

civil society organizations as intermediaries in providing financial and banking

services through the use of Business Facilitator (BF) and Business

Correspondent (BC) models. Before analyzing the existing business

correspondent model as an effective tool for financial inclusion, let us examine

numerous key issues:

Were BCs bringing unbanked into formal banking system?

Were clients accepting the BC Model for opening bank account and to

what extent?

Reach and scope of BCs.

Various incentives and regulations for the banks, BC’s and other entities

involved?

How efficient and scalable were the Institutional set up between BC’s and

the promoting banks?

What other entities can be considered for becoming BC to increase the

reach of banking services.

9 | P a g e

The objective of the present study was to study the spread of BCs in Bihar,

acceptance of BCs by clients, problems faced by different stakeholders in

implementation of BC model and scope of BC in financial inclusion in rural

areas. The data were collected from 90 clients, seven CSPs, five banks, RBI,

NABARD and Government Department. Total number of sample size was 112.

Major findings and recommendations of the study are as under:

MAJOR FINDINGS:

Interview with BCs and clients revealed that BCs were not charging any

fees from clients. It was observed during interview that the payment to

the BCs was not being done regularly

It was seen during the interaction with BCs that they were using

technology except Post Office.

Interview with bankers revealed that the banks at state level had not

constituted the Grievance Redressal Committee as yet.

During the interview it was observed that KYC form was simplified by

the bank for BCs clients and BCs and the KYC norms were being

followed by the BCs

The common service points were tagged with the specific branch locally.

Transit cash insurance for BCs/CSPs was not taken by banks

A closer look of the attempts of Banks in financial inclusion revealed that

these inclusions were through “no frill accounts” which were lying in an

inoperative state as there was no transaction in almost all the accounts.

Thus the bank had paid only lip service to the cause of financial inclusion

by opening only savings account in the form of “no frill accounts” and

had not cared for other aspects like credit needs, financial literacy,

financial advice, credit, insurance and remittance.

10 | P a g e

Average population per branch is very high (18,395) in Bihar as

compared to all India figure (12,470). Even in districts where the number

of rural branches was high, most of them were poorly manned and poorly

managed

RECOMMENDATIONS:

The banks may act positively on regulatory framework on two specific

points of risk mitigation by taking transit cash insurance for BCs/CSPs

and setting up of grievance redressal committee.

As yet only three banks had appointed BCs. All the banks (commercial

banks and RRB) should appoint BCs for providing banking services to

unbanked area. Bihar Government has already created a wide network of

well equipped Vasudha Kendras under e-governance initiative of Central

Government. Three agencies were taking care of it. These were

SRE Infrastructure Finance Ltd.

In Patna, Magadh, Purnea, Munger and Tirhut commissionery.

Zoom Developers working in

Darbhanga and Bhagalpur.

SARK System Ltd. Working in

Saran and Kosi belt.

5798 Vasudha Kendras had already been opened by the above three agencies

against the target of 8463.

Similarly, primary agricultural cooperative societies (8463), Milk Producing

Cooperative Society (6200), Milk booth of COMPFED (6000), Angan Badi

Kendra (80797) may be used by the banks as BCs.

Banks must utilize these wide networks to scale up the BC model in Bihar.

11 | P a g e

Banks should simplify the procedure for appointment of BCs. Release of

fees to the BCs and simultaneously the charge should be reasonable so

that BC model should be viable.

Banks must take this initiative as one of their main business rather than

taking it as a social responsibility. BCs may scale up the business to earn

profit and in turn make financial inclusion a reality.

Efforts must be taken by banks to cover all the major components of

financial inclusion i.e. providing bank account, savings, affordable credit,

insurance, financial advice and payment and remittance.

Banks should make sincere effort to increase network of their branches in

the state to implement financial inclusion in true sense.

SBI may sort out the problem with India Post to continue the account

opening process which had been stopped by India Post at present.

Cash handling issues can be solved by adopting the “MILK ROUTE”

method COMPFED had adopted to collect milk from villages to district.

As technology was a necessity for

scaling up the BC Model, banks can help BC to bear the initial cost on

account of introducing technology which BC can pay back after a certain

time period.

Banks may be permitted to

collect reasonable service charge from the customer for delivering

services through BC model.

Banks may bear the initial set up

cost of the BCs and extend a handholding support to the BCs, at least

during the initial stages.

Banks should utilize the fund sanctioned by NABARD for financial

inclusion for capacity building of BC and increase financial inclusion.

12 | P a g e

It had been found that India Post was not utilizing technology for its BC

business. BCs must use technology to make the business more viable and

scalable.

BCs must take initiatives to build up confidence amongst people. It can

do so by conducting meeting/seminar with local people and make them

understand the concept of BC model.

BCs must start scaling up the business with operational effectiveness.

BCs have already identified the clients and thus can utilize this

information to make JLGs and SHGs and in turn avail the financial

support from NABARD through their bank. This will provide financial

sustainability to the system.

The Government of Bihar/banks may telecast advertisement of the BC

model and its benefits on the local Radio/TV channels which will create a

feel of confidence among the public.

Financial literacy and Credit Counseling Centers(FLCCs) may be utilized

to make the illiterate mass familiar with the practices of the BC to create

confidence among the general public.

NABARD should play proactive role in awareness creation, publicity,

improving financial literacy and use of technology for the financial

inclusion. Till the completion of this time of study report no disbursal had

been made by NABARD out of its two funds in the state of Bihar.

NABARD should launch aggressive marketing of BC products.

RBI should reconsider a few guidelines for BC operations such as:

Relaxing the limitation of area

for setting up a CSP

Limitation of time of one day for

depositing the money in bank

13 | P a g e

Though within strict review and guidelines companies offering BC

services should be allowed to work for profit rather than Section 25

companies only then scaling up of business can happen making financial

inclusion possible.

Presently not much feedback was available on implementation of BC as

nobody was monitoring it. Review and monitoring mechanism for the BC

model should be started in SLBC and DLCC meetings.

14 | P a g e

CHAPTER 1

INTRODUCTION

In the broader perspective, Financial Inclusion aimed at ‘connecting’ excluded

people including vast sections of disadvantaged and low income groups at an

affordable cost with the banking system. Access to formal financial system was

of critical importance for economic upliftment of the common man. Such access

was especially powerful for the poor as it provides them opportunities to build

savings, make investments and avail credit. Despite rapid expansion of the

banking network over the last four decades, majority of people in our country

especially the underprivileged sections of the society, did not have access to

basic banking services resulting in financial exclusion. In its landmark research

work titled “Building Inclusive Financial Sectors for Development”,(2006),

more popularly known as the Blue Book, the United Nations (UN) had raised

the basic question: “why were so many bankable people unbanked?”An

inclusive financial sector, the Blue Book says, would provide access to credit

for all “bankable” people, to insurance for all insurable people and to

remittances services for everyone. Access to finance by the poor and vulnerable

groups has to be recognized as a pre requisite for poverty reduction and social

cohesion. Apart from these benefits, financial inclusion imparts formal identity,

provides access to the payments system and to savings safety net like deposit

insurance.

15 | P a g e

FINANCIAL INCLUSION

According to 59th round NSSO Survey, 51.4% of farmer household were

financially excluded from formal / informal sources of credit (549 lakh

household out of 893 lakh). Even if the remaining population of farmer was

taken into consideration only 27% of agricultural household had access to

formal sources of credit. So it can be said that about 73% of the farmer

household had no access to formal sources of credit in the country.

A region wise study showed that the situation was most critical in Central,

Eastern and North-Eastern regions- having a concentration of 64% of all

financially excluded farmer households (from formal sources) in the country

(415.61 lakh households out of 649.54 lakh households). Overall indebtedness

to formal sources of finance alone was only 19.66% in these three regions

(4.09% for North-Eastern Region, 18.74% for Eastern Region and 22.41% for

Central Region)

16 | P a g e

Marginal farmer households constituted 66% of total farm households. Only

45% of these households were indebted to either formal or non formal sources

of finance (small farmers – 51%, medium farmers – 65.1% and large farmers –

66.4%). About 20% of indebted marginal farmer households had access to

formal sources of credit (medium farmers – 57.6% and large farmers – around

65%). Among non-cultivator households nearly 80% did not access credit from

any source.

In Bihar only 33%of agricultural household were indebted, out of which 23%

were from Institutional finance. It clearly indicated the severity of exclusion in

Bihar.

As per latest BPL survey the state (Bihar) was having 1.34 crore BPL families

(1.26 crore rural and .8 crore urban).The total population of Bihar is around 8.3

crore, 55% o population lying under poverty line.

The SHG movement could credit link 1.50 lakh SHGs (18lakh members) as on

March 2010. Similarly mFIs could provide credit to 6 lakh people in the state. It

meant that out of 1.34 crores BPL family only 24 lakh family were included by

formal sources, leaving a vast gap of 1.10 crores family. Hence the task for

financial inclusion in the state was gigantic and would be difficult and time

taking for inclusion of the excluded people from existing Banking system.

Hence there was need for alternate strategy and the RBI on the recommendation

of Rangarajan Committee implemented the use of BCs for financial inclusion.

(Source: Extent of Exclusion – NSSO Survey 59th Round in the situation assessment

survey on Indebtedness of Farmer Households (2003))

As shown in Annexture I, till May 2010, 129 BCs were identified by 48 banks

covering throughout the country covering 88.50 lakh clients. The details

position as pertaining to Bihar was indicated in Annexure II. In Bihar the pace

of implementation of BC model was poor and is in initial phase. Only three

banks namely SBI, Canara bank, and PNB had appointed BCs. Total number of

17 | P a g e

BCs appointed were only 10. Till 31st May 2010 they had opened 81902

accounts only. Although Canara and PNB had appointed BCs, but BCs had not

started their work at ground level.

To know the entire gamut of implementation of BC model in Bihar, a study

namely “scope of business correspondents for financial inclusion in rural areas”

was planned and conducted with following objectives:

1. Find out the reach and performance level of the BC model

2. Find out the acceptance level of BCs by clients

3. To study the problems being faced by various stakeholders

4. To study the scope of BC for financial inclusion in rural areas

18 | P a g e

CHAPTER 2

METHEDOLOGY

2.1 We deployed four step methodology i.e. Prepare, Observe, Analyse and

Report for collection of data as detailed below.

2.2 DATA COLLECTION

2.2.1. Secondary data/Information collection.

Secondary data had been collected from three different channels.

1. Reading materials: different articles available on internet and other sources.

2. Banks: Banks such as RBI, NABARD, SLBC, SBI, PNB, Canara bank,

Madhya Bihar Grameen Bank, Central bank and Union bank.

RBI being the Central Bank of country was the first one to be approached for

basic information. Some of very vital information such as the guidelines to

different banks by RBI, expected degree of seriousness with which different

Step I

Prepare

Step II

Observe

Developed detailed project

Plan including sampling.

Discussion with RBI,

NABARD, Banks, SLBC,

BCs, CSPs.

Finalized data collection

format and mechanism for

information capture.

Pretesting of framework of

in depth interview.

Conducted field

interviews.

Collected field data.

Monitored field data

periodically for accuracy.

Conducted periodic

process checks and

verifications.

Converted field data into

desired soft format.

Step III

Analyze

Summarized field data.

Conducted detailed data

analysis.

Step IV

Report

Developed detailed reports and

summary.

Prepared recommendations and

policy matrix.

19 | P a g e

banks had been asked to take up the project, number and names of bank which

had already initiated the projects, governing body for implementation and

monitoring of the projects were obtained from RBI.

The next visit was to State Level Bankers Committee, SLBC (SBI, Patna).

Various information and data regarding the present scenario of the Business

Correspondent Model in Bihar were collected from SLBC. After collection of

the required data from SLBC, visits were conducted to all the banks which had

undertaken the BC Model as a means for Financial Inclusion in rural Bihar.

3. Different BC: Information from the Business Correspondents, appointed by

the banks to open accounts on their behalf were collected by making visits to

their zonal office and centers.

2.2.2 Primary data/information collection

Primary data through a well designed pretested questionnaire were collected

from Customer Service Points of BCs and clients.

2.3 SAMPLING Out of three Banks, banks with highest number of BCs

were identified as sample. In this case SBI was having highest number of BCs.

Three BCs of SBI having opened the maximum number of accounts were

sampled. Accordingly the sampled BCs were

1. Eko Aspire Foundation

2. Zero Mass foundation

3. India Post

Based on the coverage of BCs, their following CSPs were sampled.

Table no. 2.3.1: Sample CSPs

Serial no. BCs CSP

20 | P a g e

1 EKO Aspire Deoghar(Sarath and Sarawan)

2 Zero Mass Foundation Purnia( Maranga)

3 India Post Bhagalpur( Amarpur and

Ghogha)

13 clients of each CSP were randomly selected for collection of data.

Total sample size was 107. Comprising Beneficiaries-90, CSP-7, Banks-5, RBI-

1, NABARD-1.

2.4 TABULATION AND ANALYSIS

The data collected were tabulated to facilitate easier sharing, referencing and

analysis.

2.5 SOFTWARE

We deployed MS Excel and SPSS for storing and analyzing the data.

2.6 REPORT WRITING Based on data and its analysis, detailed report was developed.

2.7 LIMITATION OF STUDY

1. It is only a sample study and the

results have been generalized. There can be a change in results if a

census is done.

2. Due to time constraint only one

bank and three BCs have been studied in details.

3. Most of the projects had just

started so real potential could not be concluded.

4. Only a limited no. of clients had

been interviewed.

21 | P a g e

CHAPTER 3

BC MODEL IN INDIA: AN INSIGHT Government of India launched Third party banking in 2006 with the intent of

achieving the milestone “Financial Inclusion” which included increasing the

sphere of formal banking sector to include unbanked .It build on the regulatory

inertia of prioritizing financial inclusion, particularly the RBI’s ‘no frill account

drive’ which began in November2005. For the drive, Dr. C.Rangarajan,

chairman of the PM’s Economic Advisory Committee, had advised that each

semi-urban / rural bank branch should open 250 such bank accounts annually

which, if implemented, would result in approximately 11.5 million customers

country wide. (Dr. C.Rangarajan 2008).

To further the objective of Financial Inclusion as well to leverage banking

services, two kinds of third party banking agents were created – Business

Facilitators(BF) who would primarily be involved in processing and opening

accounts and Business Correspondents who would , in addition to the BC

functions mobilize deposits and disburse credit on behalf of the bank.

Further RBI permitted banks to utilize the services of nongovernmental

organizations, mFI (except NBFCs) and other civil society organizations,

intermediateries in providing financial and banking services through the use of

above mentioned two models. As per the extant guidelines, the following

entities mentioned below can act as BCs of banks.

NGOs/ MFIs set up under Societies/ Trust Acts;

Societies registered under Mutually Aided Cooperative Societies Acts or

the Cooperative Societies Acts of States;

22 | P a g e

Section 25 companies that were stand alone entities or in which NBFCs,

banks, telecom companies and other corporate entities or their holding

companies do not had equity holdings in excess of 10%;

Post Offices and Retired bank employees, ex-servicemen and retired

government employees.

Individual owners of kirana/medical /Fair Price shops

Individual Public Call Office (PCO) operators

Agents of Small Savings schemes of Government of India/Insurance

Companies

Individuals who own Petrol Pumps

Retired teachers

Authorized functionaries of well run Self Help Groups (SHGs) which

were linked to banks

Non-deposit taking NBFCs in the nature of loan companies whose

microfinance portfolio was not less than 80% of their loan outstanding,

in the financially excluded districts as identified by the Committee on

Financial Inclusion(Chairman: Dr.C.Rangarajan)

While appointing individuals as BCs, banks had to ensure that these individuals

were permanent residents of the area in which they propose to operate as BCs

and also institute additional safeguards as appropriate to minimize agency risk.

3.2 Key components of the regulatory framework surrounding BCs

include:

3.2.1 Payment of commission/fees for engagement of BFs/BCs

While doing so the rate and the quantum of the same may be reviewed

periodically. Agreement with the BF/BC should specifically prohibit them from

23 | P a g e

charging any fee to the customers directly. Interview with BCs and clients

revealed that BCs were not charging any fees from clients. It was observed

during interview that the payment to the BCs was not being done regularly.

3.2.2 Risk mitigation

Since the service agreement involves legal and operational risks, inter alia,

sincere effort to adopt technology based solutions for managing the risks should

be in place. All agreements/contracts with the customer shall clearly specify that

the bank was responsible to the customer for acts of omission and commission

of the BF/BC. It was seen during the interaction with BCs that they were using

technology, Post Office being an exception. It was observed during the study

that Banks had not fulfilled the basic regulatory framework of risk mitigation as

transit cash insurance was not taken.

3.2.3 Grievance redressal

Such machinery within the bank premises for redressing complaints about

services rendered by BFs/BCs was advised to be constituted. Interview with

bankers revealed that the banks at State Level had not constituted the

Grievance Redressal Committee as yet.

3.2.4 Know Your Customer (KYC) norm

Such norms will continue to be the responsibilities of banks. Banks may

adopt a flexible approach within the parameters of such guidelines issued on

KYC from time to time. During the interview it was observed that KYC

form was simplified by the bank for BCs clients and BCs were adopting the

KYC norms.

Over the Operations and activities of the BCs by banks it has been stipulated

that every BC would be attached to and be under the oversight of specific

24 | P a g e

bank branch to be designated as the base branch. The common service points

were tagged with the specific branch locally.

The banks may act positively on regulatory framework on two specific

points of risk mitigation by taking transit cash insurance for BCs/CSPs and

setting up of Grievance Redressal Committee.

3.3 Financial Inclusion Fund created with NABARD

Two funds had been created by GOI with NABARD for financial inclusion of

the excluded population. These were Financial Inclusion Fund (FIF) and

Financial Inclusion Technology Fund (FITF). Each of the Funds shall consist of

an overall corpus of Rs. 500 crore, with initial funding to be contributed by the

GOI, Reserve Bank of India (RBI) and NABARD in a ratio of 40:40:20. The

funding would be contributed in a phased manner over a maximum period of

five years, depending upon utilisation of funds. A large number of activities had

been allowed to be funded with this fund including capacity building of BC/BF.

The agencies eligible to get this fund were

3.3.1. Eligible Institutions for FIF

Financial Institutions, viz., NABARD, Commercial Banks, Regional

Rural Banks and Cooperative Banks;

NGOs, MFIs, SHGs, Farmers’ Clubs, Local Level Associations, etc.;

Training and research organisations, academic institutions, universities;

Service providers like Insurance Companies (providing micro insurance

services), Post Offices, Railways, etc.;

Any other organisation whose objectives were in conformity with the

overall objectives of the FIF and were approved by the Advisory Board

from time to time.

25 | P a g e

3.3.2 Eligible Institutions for FITF

Financial Institutions, viz., NABARD, Commercial Banks, Regional

Rural Banks and Cooperative Banks;

NGOs, MFIs, SHGs, Farmers’ Clubs, Local Level Associations, etc.;

Technology Service providers and other service providers like Insurance

Companies (providing micro insurance services), Post Offices, Railways,

etc.;

Any other institution/ organisation whose objectives were in conformity

with the overall objectives of the FITF and were approved by the

Advisory Board.

3.3.3 Progress in Bihar:

Interview with NABARD official indicated that the progress of implementation

of this project in Bihar was very poor. Only one Proposal for technology in

Financial Inclusion of Rs 88 lakh has been sanctioned to Uttar Bihar Gramin

Bank in April 2010 The disbursement against these sanctions was nil.

NABARD should market these funds aggressively by organizing

seminar/meetings and distributing leaflets to speed up financial inclusion in the

State. NABARD may also use publicity mode for popularizing this scheme.

26 | P a g e

CHAPTER 4

BIHAR: EMPOWERING THE STATE

THROUGH FINANCIAL INCLUSION

As the financial exclusion was very high in Bihar, there was every need for the

formal banking system to provide better and integrated financial services to the

vast majority of the unbanked population in the state of Bihar. Given the natural

and human resource endowments, Bihar had a tremendous potential for growth

and development in general and financial inclusion in particular. There was a

need for partnership, innovative strategies and dedicated approach to harness the

potential. Various flagship programmes and key projects had been supporting

wide ranging developmental interventions in the State which were brainchild of

Central Government, various institutions including RBI regulated financial

inclusion through BC/BF model on pan India basis including Bihar.

A very wide network had been already created in Bihar by e-governance

scheme of Government of India. 5798 Common Service Centers (CSPs) had

already been set up known as “Vasudha Kendra” by the government against the

target of 8463 CSCs. This network could be leveraged upon by the Government

to increase the pace of financial inclusion.

Dairy cooperative COMPFED too was a very successful entity and had a very

wide network and reach in Bihar and this could also be considered for taking the

project further.

Financial Inclusion envisaged the provision of comprehensive financial services

including credit, to at least 50% of such households, by 2012 through

commercial banks and RRBs and the remaining households by

2015.Accordingly the vision statement for the State of Bihar was to achieve

financial inclusion by serving 6.5million mainly poor families in Bihar in

27 | P a g e

support of their livelihood through a range of financial services provided by the

formal banking system and mFIs. The banking system had already geared itself

to bring about financial inclusion to cover all families in the state by 2012

through opening of no frill accounts. In the first stage SLBC identified 19

districts for 100% financial inclusion, the details of which had been enclosed in

Annexure II. It was observed from the Annexure I, that overall achievement

stands at 95.61% in all the districts. A closer look of the attempts of Banks in

financial inclusion revealed that these inclusions were through no frill accounts.

A further enquiry in the field during the visits of CSP, it was observed that there

was no transaction in almost all accounts. The banks had provided only one

component of financial inclusion and had not cared for financial literacy,

financial advice, credit, insurance and remittance but not taking care of other

components, the banks had provided only lip service to the cause of financial

inclusion. In order to have effective financial inclusion efforts should be made

to cover all the components.

4.2Bihar Socio-Economic and Banking profile:

The decadal population growth rate of the state during 1991-2001was the

highest in the country at 28.62%.Of its total population, 89.5% lived in rural

areas. In terms of human development index, Bihar was at the lowest position

among all the major states. The State ranked at the 7th poorest with 57.22% of

its population under the poverty line (as per 2008 survey). Demographic

indicators like high birth rate and infant mortality rate, poor social service

delivery, and lack of economic opportunities due to limited infrastructure

development all point to a highly disadvantaged social and economic

conditions. Table below gives comparative data for Bihar and all India in

respect of several socio economic indicators.

Table no.4.2.1: Comparative data of Bihar and India for various socio

economic indicators

28 | P a g e

Classification of Work Cultivators 29.3% 31.7%

Agricultural Labourers 48% 26.55

Artisans NA NA

Household/Cottage Industries 3.9% 4..2%

Other Workers 18.8% 37.6%

(source:Stat

e Focus Paper, NABARD, 2011-12)

To emerge as a developed state, focus was mandatory on infrastructural

improvement, industrial investments and other necessary fundamental needs

and corresponding opportunities for the people. The Government of Bihar’s

vision (as per white paper on state finances and development, 2006) was to

reduce the poverty headcount from 39% (1999) to 28% by 2015. Instead of

decreasing the poverty level has increased to 55% Present five year plan (2007-

2012) focused investment for socio-economic empowerment of women,

enhancing livelihood opportunities in the farm and nonfarm sectors and

participation of local level institutions to make service delivery more

accountable.

4.3 Present Status of Banking and Financial Services & Banking Profile of

Bihar:

As far as outreach and development of banking services were concerned, Bihar

was one of the most undeveloped states. The formal banking infrastructure

SOCIO-ECONOMIC PROFILE BIHAR INDIA Population 82.87m 1028.6m

Rural population 74.19m 742.4m

Population Density 880/sqkm 324/sqkm

Poverty Ratio 42.56% 26%

Overall Literacy Rate 47.50 65.20

Average land holding .75ha 1.57ha

Human development Index .367 .472

Infrastructure development index .260 .660

Per Capita Income 9214 25716

29 | P a g e

available in the State is presented in the Table no.4.3 .Banking network in the

state comprised of only 5% of the all bank branches in the country, despite

being third largest in population. Out of a total of 4505 branches of various

banking entities, 56.85% of the branches were in the rural areas, 20.13% in

semi-urban areas and 16.82% were located in the urban centers (Source: State

Focus Paper, 2011-12, NABARD).This translated to a bank branch on average

every 20.9 square kilometers. In terms of population, branch population per

bank in Bihar was approximately 18,395 in comparison to the national average

of 12,470.The rural urban divide in Bihar was also very stark with each rural

branch serving 31,000 people as compared to 18,000 people in the urban areas.

Formal banking data shows another face of low penetration, as 37 out of 538

blocks in the state had no bank branch. Further private commercial banks were

concentrated in only a few urban centers in Bihar.

Table No. 4.3.1: Banking profile of Bihar compared to India

(Source:

Economic Survey Report2008-09)

(State

Focus Paper, NABARD, 2011-12)

Average population per branch was very high (18,395) in Bihar as compared to

all India figure (18,395). Banks should make sincere effort to increase network

of bank branches in the State to implement financial inclusion in true sense.

Even in districts where the number of rural branches was high, most of them

Banking profile Bihar India

Total no. Of bank

branches(including RRBs and co-

operative banks)

4505 82485

Per Branch Population 18,395 12,470

Credit deposit ratio 2009-10 32.13% 74.20%

Per capita bank deposit(2007)(Rs.) 5035 23382

Per capita credit (2007)(Rs) 1518 17541

30 | P a g e

were poorly manned and poorly managed. The main reason for low CD ratio

was the absence of infrastructure facilities such as power, transport,

communication, agriculture extension services in the state. One of the factors

contributing to the low credit flow has been the weak loan recovery rates due to

lack of follow up, poor infrastructure and flood drought situation. The

cumulative recovery percentage for all banks in the state was still as low as

53.48%. Despite all the above challenges, Government of Bihar had taken many

initiatives to induce banks to address the issue of flow of credit .

31 | P a g e

CHAPTER 5

EXTENT OF COVERAGE OF BC MODEL IN

BIHAR

In Bihar only 3 Banks namely SBI, PNB and Canara bank had appointed the

BCs which were as under:

Table 5.1.1: Banks and their BCs working in different areas of Bihar

It was apparent from the above table that only 10 BCs were appointed by the

only three banks. Out of these 10 BCs, 5 BCs of SBI had started operation at

ground level. Similarly the BCs of PNB had started operation on pilot basis.

BC of Canara bank had not yet started operation at field level.

5.2 The Bank wise coverage of BCs in the state is appended below

Banks

BC Operational Area

1. SBI 1. EkoAspire

Foundation

Gaya,Madhubani, Darbhanga

Samastipur,Siwan,Deoghar

2. ZeroMass

Foundation

Purnia,Supaul,Athmalgola,Patna,Gopalganj,W.

Champaran

3. India Post Every district

4. Swagram Madhubani

5. Drishtee Patna

6. Save Gaya

2. PNB 1. Samman

Foundation

2. Swagram

3. Kaushalya

Patna, Tinehri in Jehanabad, Ara, Gaya, Bihar

Sharif

3. Canara

bank

I25 Rural Middle

Services

Shekhpura

32 | P a g e

Table No.5.2.1: Business of different BCs on 31st May 2010

Name of Bank

Name of BC No.of CSP Service offered

Total no of accounts

Deposit in lakh

Loan in Lakh

SBI Eko Aspire Foundation

174 A/c opening 31,000 49.05 -

Zero Mass 29 A/c opening Remittances

20,778 - -

Drishtee 4 A/c opening 143 2.41 -

SAVE 24 A/c opening 6,125 62 7

India Post 658 A/c opening 2,872 168 57

Total 865 60,918 281.46 64

PNB Samman Foundation

NA A/c opening 4,984 - -

Swagram NA A/c opening 11,000 - -

Kaushaliya NA A/c opening 5,000 - -

Total 20,984

TOTAL 81,902 281.46 64

The total number of accounts opened by all the BCs in state was 81902. Only

two BCs namely SAVE and India Post had given credit and that too a nominal

amount of Rs 64 lakh. It meant presently BCs were concentrating on opening of

savings accounts only. The operation BCs would not be viable by simply

opening the SB Accounts, as income generated through these operations was at

low ebb. The banks and BCs had to adopt followed two fold strategy to make

BCS operation viable:

1. Scale up the existing business of opening of accounts and banking

2. Diversifying business

3. Use of information and communication technology applications which

would reduce hassles and cost.

During the interaction with the stake holders it transpired that integration of

SHGs/LJGs model with financial inclusion would provide platform to BCS for

diversifying business. It was opined that BCs had already identified the clients

in the process of opening of Accounts. BCs should endeavour to form JLGs of

33 | P a g e

male members of identified clients’ family and SHGs for women members. The

BCs can also avail financial support for SHGs/JLGs promotion from NABARD

through their bank. This would not only enlarge their business but also help in

economic development of clients.

5.2 Bank wise spread of BCs

5.2.1. State Bank of India:

5.2.1.1. Post Offices had been appointed as BC on pan India basis. Being a

government organization no security deposit had been taken. The MOU had

been signed with department of Posts wherein 658 Post Offices were

working as BC in Bihar/Jharkhand.

5.2.1.2. SAVE: Internet enabled Kiosks banking. It was operational in

Chakand block, Gaya district. There were 29 kiosks of SAVE till 30 July

2010.

5.2.1.3. EKO ASPIRE Foundation: Low cost banking by mobile phone. The

project was operational in 5 districts i.e., Madhubani, Darbhanga,

Samastipur, Siwan, Deoghar. They had opened more than 31,000 accounts

with approximate deposits of 49.05lakh. Total number of Customer Service

Points (CSP) in Bihar/Jharkhand was 174.

5.2.1.4. Zero Mass Foundation: Smart card based banking –The project was

functional since 2007-08.They were working in three districts Purnia, Supaul

and Patna. Total no of accounts opened till date was 20,778.

Taking together all the BCs of SBI had covered 5,495 no of villages and opened

60,918 accounts. The BCs were having 865 CSPs in the state. Their deposits

34 | P a g e

were to the tune of Rs 281.46 lakh. They had provided credit to the tune of Rs

64.00 lakh.

Punjab National Bank:

There was a three tier system to appoint BC. They can be appointed at 1) circle

level, 2) Field GM level, 3) Head office level. The main function of BC was to

open savings account. Three BCs had been appointed by PNB:

1) Samman Foundation

2) Swagram Foundation

3) Kaushalya Foundation

Technology providers for PNB were 1) IL and FS, 2) TCS.

Places of operation of BCs of PNB in Bihar were:

• Patna: The project was operational in two areas of Patna i.e., Mussodi and

Teneri. Smart card based technology was used for opening the account

and operating it.

• ARA: The project was operational in two areas of ARA i.e. Koneria and

Udwanth Nagar.

• Gaya: The project was operational in two areas of Gaya i.e. Guraru and

Amraut.

• Bihar Sharif.

The BCs of PNB had opened 20984 savings bank accounts. Presently they were

not providing other facilities.

5.2.3. Canara Bank:

Canara Bank has started this project on pilot basis in a district near Patna called

Shekhkpura. A Bangalore based NGO, I25 Rural Middle Services had been

appointed as BC. The technology used by them was Biometric Smart Card and

technology partner was Ms Integra 62.

35 | P a g e

The pilot project had been launched in January 2010, but could not start opening

of accounts till the date of visit in May 2010.

36 | P a g e

CHAPTER 6

CASE STUDY OF SOME BCs

6.1 Case studies of 3 BCs of SBI has been attempted during the study which is

given ahead.

6.1.1. EKO ASPIRE FOUNDATION- SBI

6.1.1.1. Introduction: Eko Aspire Foundation and Eko India Financial Services

Pvt. Ltd. were formed in September 2007 to extend banking facilities in

unbanked areas via mobile phone-based technology and a network of retail

outlets called customer service points (CSPs). Eko Aspire Foundation was a

Section 25company, which had Bharti Airtel Ltd. one of Asia’s leading

integrated telecom service providers, as its technology partner. The Eko model

worked on the fundamental premise of giving everyone a bank account. It was

building a low cost financial services infrastructure to increase the reach of

financial institutions to the un-banked and to democratize financial services for

the un-banked in urban as well as rural areas: powered by innovation and

technology.

37 | P a g e

Eko was leveraging existing distribution networks, existing behavior and

interaction mechanisms to ensure that the barriers for adoption were very low.

The endeavor was to build a rapidly scalable model by addressing the

challenges of the existing models and by using mobile technology to help bring

down significantly the network cost. The Eko system, was aiming at providing

secure, simple and convenient financial services in a cost - effective and

scalable manner to the target segment.

6.1.1.2. Model: Public sector bank in collaboration with a section 25 company

as BC to make basic financial services available to the un-banked.

In the capacity of BC, appointed on February 23rd 2009, of SBI prime activity of

EKO was, to open no frill account for the rural unbanked clients and provide

them basic financial facility of deposit and withdrawals from this account. For

the purpose of opening the accounts EKO appoints CSPs, which in this case was

a local cloth merchant and a cement shop (Hansa Cloth Shop, Nirmal Cement

Agency).The area for operation was decided by the bank concerned. It had also

provided training to the CSP on usage of technology.

6.1.1.3. Location:

A visit to the EKO ASPIRE centers located at Sarwan and Sarath block of

Deoghar district was undertaken to make depth study of BC model.

38 | P a g e

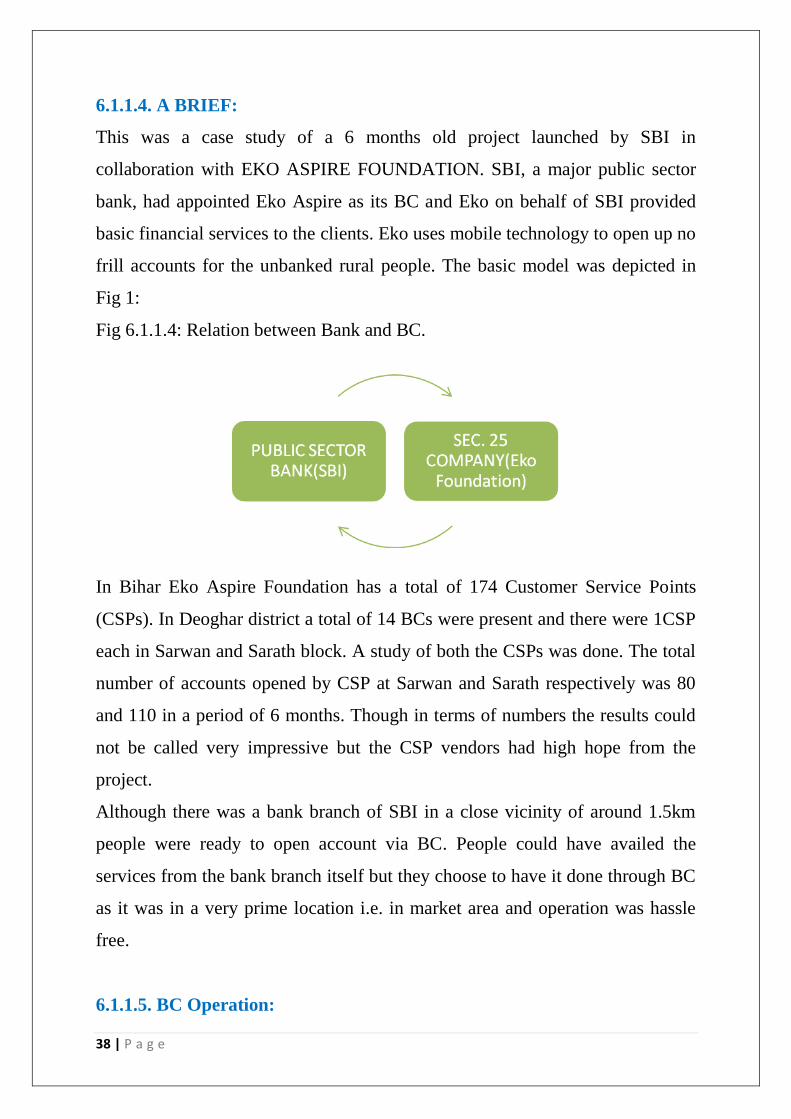

6.1.1.4. A BRIEF:

This was a case study of a 6 months old project launched by SBI in

collaboration with EKO ASPIRE FOUNDATION. SBI, a major public sector

bank, had appointed Eko Aspire as its BC and Eko on behalf of SBI provided

basic financial services to the clients. Eko uses mobile technology to open up no

frill accounts for the unbanked rural people. The basic model was depicted in

Fig 1:

Fig 6.1.1.4: Relation between Bank and BC.

In Bihar Eko Aspire Foundation has a total of 174 Customer Service Points

(CSPs). In Deoghar district a total of 14 BCs were present and there were 1CSP

each in Sarwan and Sarath block. A study of both the CSPs was done. The total

number of accounts opened by CSP at Sarwan and Sarath respectively was 80

and 110 in a period of 6 months. Though in terms of numbers the results could

not be called very impressive but the CSP vendors had high hope from the

project.

Although there was a bank branch of SBI in a close vicinity of around 1.5km

people were ready to open account via BC. People could have availed the

services from the bank branch itself but they choose to have it done through BC

as it was in a very prime location i.e. in market area and operation was hassle

free.

6.1.1.5. BC Operation:

39 | P a g e

Zonal office of BC (Eko foundation) located at state headquarter appointed field

officer in each district. Field officer kept a check over all the CSP which were

appointed by the zonal office. Field Officer used to send the information to the

Zonal office.

The forms were filled by the CSP and then these completed forms were sent to

the nearest bank branch (Sarwan, Sarath), and also the zonal office of the

company. The branch office (bank) as well as zonal office of the company

maintains the database of clients.

The project being in inception phase the bank had delegated the power to the

branch manager of the implementing branch. So that operations could be carried

out without any hurdle.

As far as withdrawal from the savings account was concerned, paucity or

availability of little liquid cash (maximum Rs10,000) with the CSP , was a

hurdle in case withdrawal transactions increases arithmetically.

Technology used: The technology partner for EKO was Airtel. Eko uses mobile

based technology to open as well as operate the account. Mobile numbers issued

by the service provider, itself got converted as a saving account number for the

users and such arrangement eliminated the formal necessity of providing unique

number to clients. The account holder could carry on the transactions through

this account number. The procedure for opening the account had become very

easy and fast due to the usage of mobile banking. Such technology usage was

highly cost effective and the current tele density including the future forecast

would increase the scope of account opening exponentially. At present, the

instrument did not facilitate the transfer of electronic data to the server at the

receiving end which includes either the bank or the BC concerned.

40 | P a g e

6.1.1.6. BC Services: Financial Structure

The SBI had appointed EKO as BC. Bank commissions were the primary

source of revenue for BCs. They were usually based on the number of new

clients enrolled, the volume of transactions, and client balances. Eko

foundation had entered into a contract with SBI. The decision has been taken by

SLBC branch of SBI (Patna) to appoint Eko as their Business Correspondent. A

consensus decision had been taken on the operational area and then the

respective local bank branches were informed about the project. The service

charge given to Eko by SBI is given in the Table no. 6.1.1.6.1. below.

Table no. 6.1.1.6.1: Remuneration by bank to BC

Service Remuneration

Opening bank account Rs 55 /Account

Transaction(debit/withdrawal) Rs 500/10,000

Eko had its own setup and staff to handle the business. The CSP which it

appoints were paid commissions for their service. The agreed amount for

payment of Sarwan CSP was given in table no. 6.1.1.6.1

41 | P a g e

Table no. 6.1.1.6.1: Remuneration by BC to CSP

Service Remuneration

Opening bank account Rs 13 /Account

Transaction(debit/withdrawal) .03% of every transaction.

As a necessary condition for account opening, a client requires:

Voter I-Card( or any other government identity card)

Mobile and mobile no.

Photograph

6.1.1.7. Financial services offered:

While performing the task of a BC in Sarwan and Sarath, Eko Aspire opened

only basic no frill savings accounts. As of May 2010, total no. of accounts

opened were 80and 110 by Sarwan and Sarath CSPs respectively. In contrast to

other BCs, the regular transactions in accounts were observed.

6.1.1.8. Challenges Involved and clients Observations

While interacting with the clients, challenges and observations were mainly as

under:

Information about the BC Model/Financial services available for clients

Hassles in operations

Clients’ behavioral pattern

42 | P a g e

1. Information about the BC Model/Financial services available for

clients: Authentic information regarding BC was not given in the area.

2. Beneficiaries lacked confidence and trust on BCs: As many chit funds

had already cheated the people in past they were not able to trust this new

model.

3. Hassles in operation: One of the most important benefits of this model

was mobile banking that means a client can check his/her account by

himself. One of the basic problems was to make the customers learn the

process. Though very simple the basic fact of them being illiterate makes

the implementation part difficult. The clients having Airtel mobile no.

had the facility of calling a toll free no. (18001025432) and checking the

mini statement of the account but other people having numbers of other

mobile operator has to get the details through SMS which makes the

process difficult for them.

4. Client’s behavioral pattern: Socio-economic condition, low literacy

rates, vicious cycle of daily subsistence stress acted as a blockade in

implementation of the model.

43 | P a g e

6.1.2 Zero Microfinance and Savings

Support Foundation-SBI

6.1.2.1. Introduction: A Little World (ALW) was the developer of ZERO,

India’s first domestic payment system with specific focus on reaching out to

masses with lowest available communication infrastructure. Zero Microfinance

and Savings Support Foundation, a Section 25 Company closely affiliated to

ALW, had been appointed as a Business Correspondent by 22 Banks, in 21

states of India, and provides field operations for the ZERO platforms. ZMF

manages the field force, account creation, appointment of Customer Service

Points (CSPs), management of cash and other logistics at the last mile. ZMF in

turn collaborated with strongly placed local organizations, district and state

administration to ensure smooth deployment and operations. ZMF created the

last mile operations network in villages, under pre-defined service agreements

with Banks and front-ends the delivery of full-featured transactional services on

behalf of Banks for Financial Inclusion on the ground.

6.1.2.2. Model: Public sector bank(SBI) in collaboration with a Section 25

company(ZMF) to make basic financial services available to the un-banked

area. The technology for operation was provided by A Little World. The

details of the model as under:-

Zero Mass Foundation (ZMF): Company Details

44 | P a g e

Functions of ZMF:

As per a typical agreement between ZMF and a bank, ZMF’s scope of

services includes: Enrolment of customers for no-frills zero-balance

savings accounts and other account types that may be specified by the

Bank.

Enrolling, training and equipping of Customer Service Points (CSPs) in

villages to provide various kinds of transaction services including cash

deposit, cash withdrawal, transfer of money, payment of utility bills,

disbursal of loans, collection of loan installments, and cashless payments

at local remote merchant..

3rd party cash collection

Cashless payments at local and remote merchant establishments.

Management of cash

Functions of ALW:

A Little World is the technology provider for ZMF. It managed front-end

technology, back-end systems and 24x7 centralized Data Centre operations,

including:

Opening accounts with fingerprint + photo capture, using mobiles

End-to-end security and key management. Biometric de-duplication

Free open-source end-to-end account management system OR option of

connectivity to any Core Banking system

Headquarters Mumbai, India

Industry Financial Services

Type Non-Profit

Company Size 400 employees

Website http://www.alittleworld.com.

45 | P a g e

Card issuance and card management (photo-ID / smart cards)

Variety of transaction options at front end.

Web services.

Daily reporting to financial institutions, Government and others.

Predictive Cash Management System

6.1.2.3. Location:

A visit of Zero Mass center located at Maranga in Purnia District was

undertaken to make depth study of BC model.

The nearest bank branch i.e., Purnia Bazaar Branch was nearly 2-3kms from the

CSP. As the nearest bank branch was not at a distance local people would feel

convenient to go daily for depositing or withdrawing money.

Fig 6.1.2.3: CSP of Zero Mass

6.1.2.4. A Brief

Based on the agreement between zero mass foundation, a Section 25 company

and a public sector entity, SBI, ZMF overtook the role of BC and offered

financial services to clients. A sister company of ZMF, A little world provided

the technology for said operations. Case study included operational details,

client’s observation, challenges involved per se. It also unfolds critical issues

that surround BCs operations.

46 | P a g e

Fig 6.1.2.4: Relation between Bank, BC and Technology partner.

6.1.2.5. BC Operation:

ZMF recruited and trained village based operators. Manned outlets for

transactions (incl. deposit, withdrawal, transfer).For performing operational

task, Zero Mass foundation appointed field officer who supervised and

controlled entire assigned activities of all the CSPs which were appointed by the

concerned Zonal Office, Patna. Further field officer sent entire activity

information both to the zonal office and nearest controlling bank branch.

The forms were filled by the CSP and then these completed forms were sent to

the nearest bank branch (SBI, Purnia Bazaar Branch), and also the zonal office

of the company. The Purnia branch office (bank) as well as zonal office of the

company maintains the database of clients.

Such project was under the supervision and control of the bank manager of the

assigned local bank branch.

The financial sustainability issue did not arise even when the primary result of

opening saving account was not very successful. Below mentioned data reveales

struggling status of entire model.

47 | P a g e

All the CSPs working under Purnia Bazar Branch were not having any

information about 2900 requisition for account opening, as out of 3500 only 600

met the fate of being open and functional. The role of concerned zonal office

was not performed well.

There was also an evidence of deviation of BC from the service agreement

especially on account of commission paid to CSP by the BC. In this case,

evidence showing commission paid (Rs 4/account opening) and agreement for

commission was Rs 8/account opening. Further, grievances of CSPs majorly

included non-cooperation of Bank in making arrangement of cash for

withdrawals exceeding Rs 10,000. In one case, even issues regarding

remittances were noticed as the account balance for deposit from outside base

branch were not paid on time from the agency concerned.

6.1.2.6. CSP Field activities and norms for opening account:

Below mentioned were the steps involved for opening of an Account:

In the first step, all the necessary information of a client was gathered and

stored on a system.

Secondly, requisition form for account opening was filled and it included

ZSN no. and form id. The ZSN no. itself acted as an account number for

further financial transaction and services.

Complete filled form for account opening was sent to the bank.

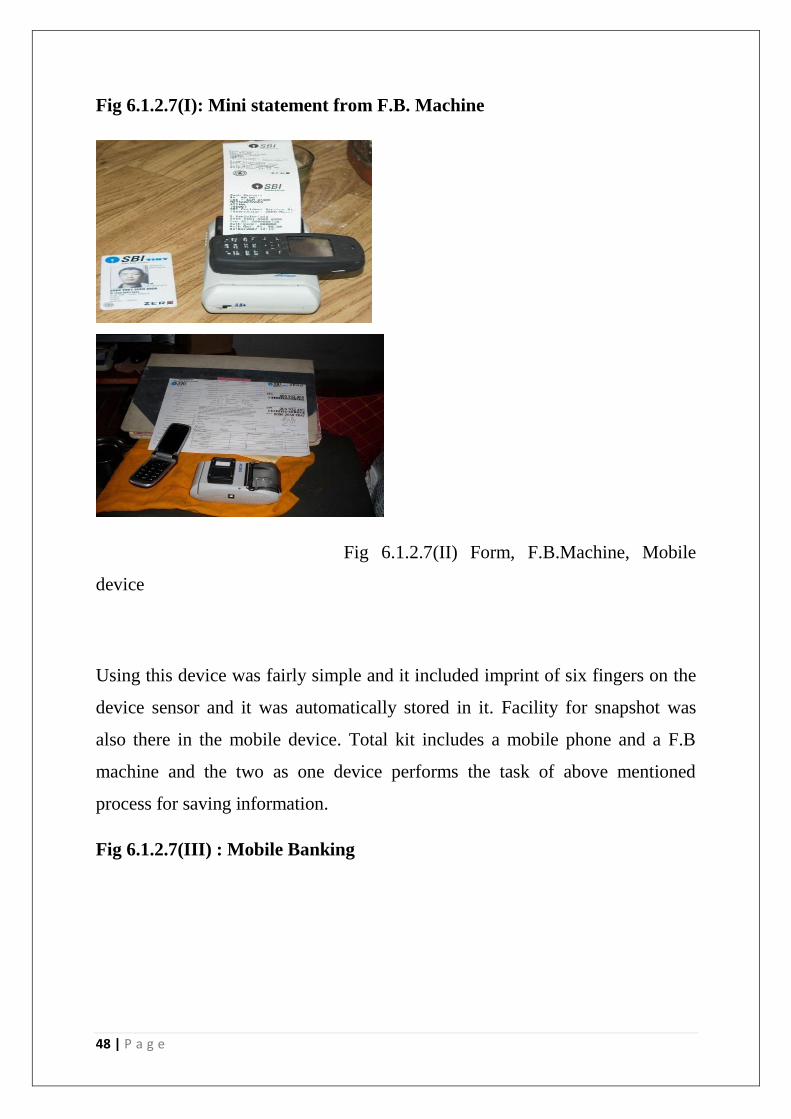

6.1.2.7. Technology used: While performing BC Operations ZMS customer

service provider were heavily dependent on ALWs mobile phone specially

designed for agent banking.This device had the capacity to store customers’

information. In addition biometric data like finger prints and photographs were

also stored in the device.Its technology transmits transactions to the ALW back

end server.The technology used in the device was GPRS or EDGE and it has the

capacity to transmitt data very fast.

48 | P a g e

Fig 6.1.2.7(I): Mini statement from F.B. Machine

Fig 6.1.2.7(II) Form, F.B.Machine, Mobile

device

Using this device was fairly simple and it included imprint of six fingers on the

device sensor and it was automatically stored in it. Facility for snapshot was

also there in the mobile device. Total kit includes a mobile phone and a F.B

machine and the two as one device performs the task of above mentioned

process for saving information.

Fig 6.1.2.7(III) : Mobile Banking

49 | P a g e

Mobile transaction Finger print taken on F.B Smart Card

Machine

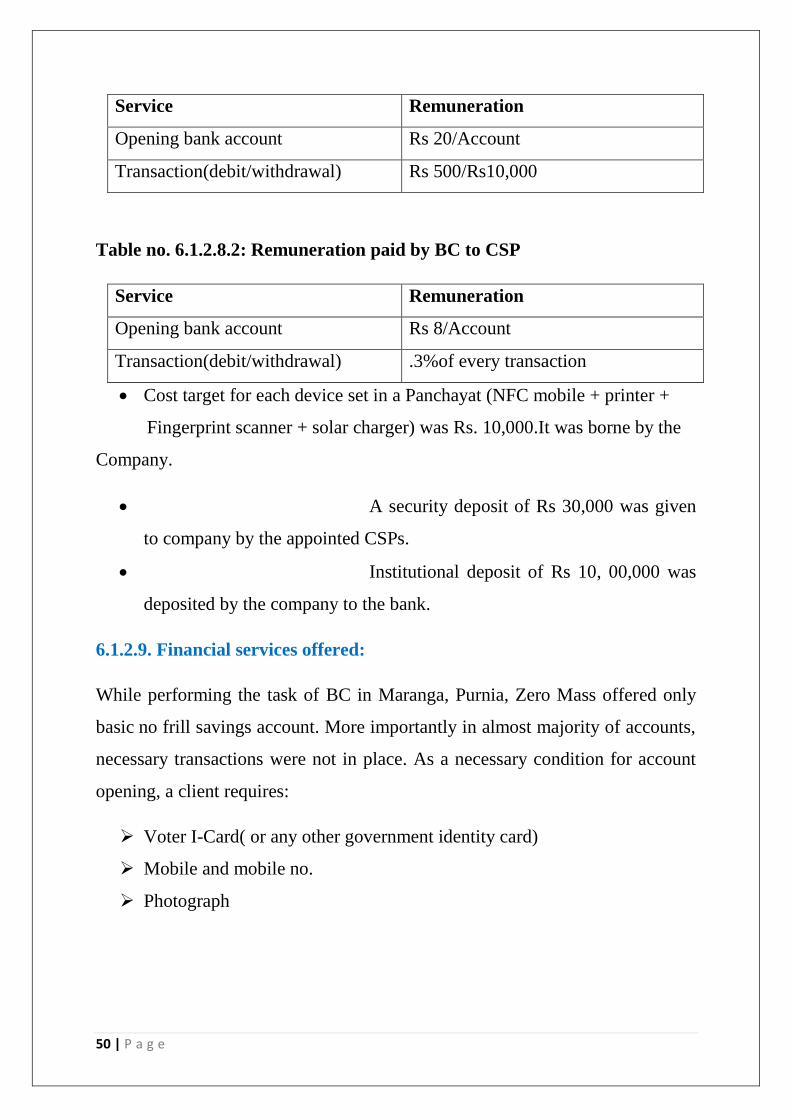

6.1.2.8. BC Services: Financial Structure

Bank commissions were the primary source of revenue for BCs. They were

usually based on the number of new clients enrolled, the volume of transactions,

and client balances. Zero Mass foundation has entered into a contract with

senior management of SBI. SLBC in the state approved Zero Mass to carry out

Business Correspondent role. A joint decision in this regard for the operational

areas and subsequent role of local bank branch regarding the project was taken.

The commission given to by SBI was given in the table 6.1.

Zero Mass has its own setup and staff to handle the business. The CSP which it

appoints were paid commissions for their service. The agreed amount for

payment of CSP in Maranga, Purnia is given in Table no. 6.1.2.8.1.

Table no. 6.1.2.8.1: Remuneration paid by Bank to BC

50 | P a g e

Service Remuneration

Opening bank account Rs 20/Account

Transaction(debit/withdrawal) Rs 500/Rs10,000

Table no. 6.1.2.8.2: Remuneration paid by BC to CSP

Service Remuneration

Opening bank account Rs 8/Account

Transaction(debit/withdrawal) .3%of every transaction

Cost target for each device set in a Panchayat (NFC mobile + printer +

Fingerprint scanner + solar charger) was Rs. 10,000.It was borne by the

Company.

A security deposit of Rs 30,000 was given

to company by the appointed CSPs.

Institutional deposit of Rs 10, 00,000 was

deposited by the company to the bank.

6.1.2.9. Financial services offered:

While performing the task of BC in Maranga, Purnia, Zero Mass offered only

basic no frill savings account. More importantly in almost majority of accounts,

necessary transactions were not in place. As a necessary condition for account

opening, a client requires:

Voter I-Card( or any other government identity card)

Mobile and mobile no.

Photograph

51 | P a g e

Challenges Involved and clients Observations

While interacting with the clients challenges and observations were mainly as

under:

Information about the BC Model/Financial services available for clients

Hassles in operations

Clients’ behavioral pattern

1. Information about the BC Model/Financial services available for

clients: Though in earlier case it was found that clients information level

were abysmally low here in case of Zero mass the situation was different.

The clients understood the need of bank account and were interested in

having their account opened in nearby vicinity. They had accepted the

concept of branchless banking and wanted to avail the service.

2. Hassle free operation: One of the most important benefits of this model

was that client didn’t have to visit bank for getting mini statement. He/Se

could get a mini statement from the nearest CSP. The customer just had

to provide the ZSN no. and the mini statement was provided in a printed

form to them by CSP.A hard copy of the statement helped the clients to

develop a kind of faith on the company.

3. Client’s behavioral pattern: In this case also socio-economic condition,

low literacy rates, vicious cycle of daily subsistence stress acted as a

blockade in implementation of the model.

6.1.3. INDIA POST-SBI

52 | P a g e

6.1.3.1. Model: Public sector bank in collaboration with an Agency of

the Government of India to make basic financial services available to the un-

banked.

6.1.3.2. Location: BCs were located at Amarpur and Ghogha. Amarpur was a

block of Banka district in Bihar. The district, a part of Bhagalpur Division, has

its headquarters at Banka town. The district occupies an area of 3018 km² and

has a population of 1,608,773 (2001 census). Ghogha was located in Bhagalpur

district. The district occupies an area of 2570 km² and has a total population of

1,909,967 and rural population of 1,566,518(Bihar.nic.in).

Although a bank branch of SBI was operational in the immediate next building,

people were ready to open accounts through P.O. In this case the problem was

not of unavailability of bank branch but tedious and complicated process of

opening bank account. The procedure for opening bank account was very easy

through BC and so people especially from rural background felt more

comfortable with opening a bank account through BC. There were two other

factors which attracted people to open account through PO, one was the kind of

reputation it had built and other was its vast network.

6.1.3.3. A BRIEF:

This was a case study of a 1year old project launched by SBI in collaboration

with India Post. SBI a major public sector bank had appointed India Post as its

BC and P.O on behalf of SBI provides basic financial services to the clients.

The technology usage was not found in this case. P.O. still was working on

paper and conventional mode of opening the account was used.

Fig 6.1.3.3: Relation between Bank and BC

53 | P a g e

6.1.3.4. BC Operations:

The operational structure of BC in this case was very simple. The top

management of both bank and PO has mutually taken a decision to leverage

upon the network of PO in India to open accounts and fasten the pace of

financial inclusion. PO in every district of India was acting as a BC of SBI. For

the bank, motive was very clear that they want to cut cost by not opening new

branches and for PO, it has become a new source of revenue.

The KYC forms were filled up by the PO in the block and the filled up form

was sent to the assigned bank branch. The data was maintained by both bank as

well as PO. After the account was opened bank gave the passbook to the client

and they could do further transactions from bank.

6.1.3.5. BC Services: Financial Structure

As for the other BC in the case of PO also remuneration by bank was paid in

terms of commission. They were based on the number of new clients enrolled,

the volume of transactions, and client balances. The decision has been taken

jointly by higher managerial level of both bank and P.O. A joint decision has

been taken on the operational area and then the respective local bank branches

were informed about the project. The remuneration given to P.O was given in

the table no. 6.1.3.5.1.

Table 6.1.3.5.1 : Remuneration paid by bank to PO

Service

Remuneration

Opening bank account Rs 50 /Account

54 | P a g e

Transaction(debit/withdrawal) Rs 500/10,000

6.1.3.6. Financial services offered:

While performing the task of a BC in Amarpur and Ghogha, Bhagalpur, PO

offered services of only opening of basic no frill savings accounts. As of May

2010, total no. of accounts opened at Amarpur and Ghogha were 115 and 95

respectively. After opening the above mentioned number of accounts PO

stopped opening the accounts. The problem faced according to them was non

cooperative attitude of banks. On the other hand while the visit to bank was

conducted it was found that they were already overloaded with work and there

was no possibility they could open the account in less than 15days, while PO

asked them to open the account within 2 days.

Requirement for the account opening are:

Voter I-Card (or any other government identity card, even id

confirmation from sarpanch can also be accepted as proof for

identification)

Photograph

Signature/thumb impression.

6.1.3.7. Challenges Involved and clients Observations

This relatively unsuccessful pilot has shown that cooperation between the bank

and the BC was essential. Post Office being one of the most trusted institutions

in India could be instrumental in making BC Model successful. The trust P.O

enjoys together with their vast network can be leveraged to further accelerate

the growth of Business Correspondent Model and convert the dream of financial

inclusion into reality.

55 | P a g e

Clients in this case were ready to open account through P.O. The only complain

they had was slow processing (15 days to open account) but compared to other

cases their processing time was much lower. On this observation one could

conclude that there was a high demand from the customers’ side and P.O must

resume the process without any further delay. The misunderstanding between

bank branch and the P.O. may be removed by higher-ups in the banks and the

P.O.

56 | P a g e

CHAPTER 7

CLIENTS PROFILE

7.1. AGE GROUP PROFILE

Age group wise disbursement of the sampled clients was given below in the

Pie-chart.

Graph no. 7.1.1. Age group wise classification of clients

From the above chart it was evident that 86% of the clients were in working age

group.

7.2. Occupational Pattern

The occupational pattern of the clients was given below in the Pie-chart

Graph 7.2.1: Occupational pattern of clients

It appeared from the above graph that sampled beneficiaries were well

distributed among major occupation.

57 | P a g e

Table no 7.2.1: Crosstab of Occupational pattern and banking history of

clients.

occupation

account Total New(Throu

gh BC)

Old

(Banks)

farmer 12 4 16

labour 22 1 23

shopkeeper 12 7 19

vendor 29 3 32

Total 75 15 90

The table above tries to establish a relationship between the types of occupation

the observed clients were in and banking history of the client. It has been found

that except for the shopkeepers, clients into other occupation majorly opened

accounts(new account holder) through BCS. Thus it can be safely assumed that

the model was being successful in including financially excluded people.

7.3. EDUCATIONAL PROFILE

The education profiles of the sampled beneficiaries are given below.

Graph no. 7.3.1: Education profile of the clients

It was observed from the educational profile that 67% of the sampled clients

were illiterate. It meant BCs were also giving due importance to illiterate

clients.

58 | P a g e

7.4. No. of accounts opened after the BC operation (new) and no. of old

accounts:

The classification of client based on new accounts and old account is given

below in the Pie-chart.

Graph no. 7.3.2: Classification of new and old accounts

It was evident from the above chart that 83% of the clients had new accounts i.e.

they had opened the accounts for the first time. 17% of the clients although

were having accounts, but opened accounts again with the help of BCs to save

time and cost of travel.

The Bar Chart of the three sampled BCs for the new and old account is given

below.

Graph no.7.3.4 : Classification of new and old accounts for all the three

BCs.

59 | P a g e

60 | P a g e

CHAPTER 8

STAKEHOLDER ANALYSIS

8.1. This part of the study was done to analyse various pros and cons of the

model, according to different stakeholders. The purpose of the analysis was to

enumerate all the factors which were playing role to make BC model a success

or failure. To start with first of all it was important to mention various

stakeholders of the project. There were broadly four stakeholders who can be

associated with this model, they were:

Government

Banks

Business Correspondents

Clients

8.1.1. Government: Through discussions was held with Government

departments particularly Department of Institutional finance, Rural

Development Dept., Science and technology Dept. and Cooperative Dept.

Government was giving much thrust for financial inclusion and reviewing the

progress in each SLBC meeting particularly regarding appointment of BC by

banks. Government Dept pointed out that 100% financial inclusion had been

achieved in 19 districts. The detail of the same is provided in ANNEXTURE II.

Rest of 19 districts has been selected for 100% financial inclusion by the year

2012. The Government Dept. further pointed out that banks were achieving

target of financial inclusion by opening simply no frill savings accounts, which

also turned into non-operative/dormant accounts in due course. Government

officials were of the view that BC model would prove effective in achieving

61 | P a g e

100% financial inclusion. For scaling up the BC model concepts State

Government officials offered following suggestions:

Opening of commercial Bank

branches in unbanked block and other rural area to be at par with national

average of serving population per branch.

Use of strength of Bihar such as

Common Service Center(Vasudha Kendra) under e-governance scheme,

milk producers co-operative society, Angan Bari and PACS

a) Common Service Center(Vasudha

Kendra) set up under e-governance Scheme.

S.No. Name of organisation Area of operation

1. SRE Infrastructure Patna,Magadh,Purnea,Munge and Trihut

commissionary

2. Zoom Developers Darbhanga and Bhagalpur

3. SARK System Ltd. Saran and Kosi region

b) Milk producing co-operative

society (COMPFED) :

Total number of milk producers cooperatives : 6200

Villages covered : 7750

Retail outlet of Sudha(COMPFED) : 6000

Towns covered : 84

c) Angan Bari Kendra: 80797 angan

bari centers have been established across the state

under ICDS program.

d) PACS: 8463 PACS were working

in Bihar.

62 | P a g e

Change of mindset of bankers

towards financial inclusion concept is essential. Presently bankers think

opening of no frill accounts as financial inclusion. They have to change

their mindset and engage them in actual financial inclusion by providing

at least saving, credit, insurance and financial advice.

Pro active role by banks in

appointing BC. The pro-active role is required from all the banks i.e.

Commercial Bank, RRB and Co-operative. At the time of study only 3

commercial banks had appointed in total 7 BCs. All the banks are

required to expedite their effort and develop suitable strategy for

enlarging BC model concept.

Regular reviews of progress

although done in SLBC. There is need to review progress of bank

controlling office level, BLBC and DLCC.

Capacity building of staff of

banks

Simplification of procedure in

appointing BCs.

Use of technology