Study Renewable Energies Maghreb

34

A Friedrich Naumann Foundation Policy Brief Authors: Dennis Kumetat and Nassima Hamiane

-

Upload

ffn-alger-alexander-knipperts -

Category

Documents

-

view

179 -

download

20

description

A Friedrich Naumann Foundation Policy Brief Authors: Dennis Kumetat and Nassima HamianePrefaceWith the Maghreb region in the midst of the most profound political changes in recent history, the eyes of the world have finally turned to Europe’s southern neighbours. And the nuclear incident following the recent earthquake in Japan reignited the debate about renewable energies as an alternative to nuclear fuel based electricity generation. Two profound reasons that highlight the strategic releva

Transcript of Study Renewable Energies Maghreb

A Friedrich Naumann Foundation Policy BriefAuthors: Dennis Kumetat and Nassima Hamiane

01

PrefaceWith the Maghreb region in the midst of the most profound political changes in recent history, the eyes of the world have finally turned to Europe’s southern neighbours. And the nuclear incident following the recent earthquake in Japan reignited the debate about renewable energies as an alternative to nuclear fuel based electricity generation. Two profound reasons that highlight the strategic relevance of the current study as a starting point of both closer economic cooperation between Europe and the Maghreb and as a roadmap of the changes needed to make cooperation in renewable energies economically viable.

The concept for the three Workshops in Algeria, Tunisia and Morocco was developed on the basis of the realisation that most of the initiatives in the field lack a visible private sector component in the countries of North Africa, where most of the technical installations are to be based. Not only does a lot of local entrepreneurial potential remain unused but the projects lack the local ownership as a key precondition for their political feasibility and economic viability from the point of view of the Maghreb countries.

The objective of the three meetings was therefore to unite businessmen and private entrepreneurs from the Maghreb in the three countries to discuss the economic potential, the opportunities and strategic challenges, which local entrepreneurs are faced with in the much discussed “Megapro-jects” in renewable energies.

The result of these discussions is summarised in the present study which highlights the many opportunities that exist for technology transfer and the generation for economic growth in the Maghreb countries while pointing out the many hurdles that still need to be taken, not least in the countries of the European Union, to make these projects an economically viable alternative source of energy both within the Maghreb and for European consumer countries. We hope that it may be a step towards closer economic cooperation between neighbours, whose interdependence and proximity has become all the more visible in recent months.

Algiers, March 2011

Project Director Maghreb

02

1. Introduction

In recent years, several large-scale renewable energy projects have been announced in the Maghreb. Desertec, Transgreen, the Mediterranean Solar Plan, as well as the World Bank’s Clean Technology Fund have presented billion-dollar renewable energy projects in the region. While the international power industry forms an integral part of these schemes, the renewable energy sector in the Maghreb itself is often not as strongly involved.

Particularly small and medium enterprises lack well-structured networks and are thus hardly capable of shaping the current process or of supplying political stakeholders with concepts of how such terms as “technology transfer” or “local content factor” can actually be implemented.

This study1 summarizes the results of three workshops held in Tunisia, Algeria and Morocco in November 2010, bringing together relevant stakeholders from small, medium-size and large-scale renewable energy companies, as well as energy experts and decision-makers from government and administration2. The workshops were held by the Friedrich Naumann Foundation in partnership with the German Chamber of Commerce and Industry in Morocco (Casablanca), the Institut Arabe des Chefs d’Entreprises (IACE – Tunis) and with the German-Algerian Chamber of Commerce and Industry (Algiers).

It aims to analyse domestic industry structures and to identify ways of how Maghreb energy com-panies can fruitfully cooperate with the multinationals in the renewable energy sector, what their contribution to the success of the projects could be and how they could benefit from them in an optimal way. Further, the workshops attempted to identify the legal, technical and commercial areas of a potential renewableelectricity export that could benefit from the existing export experiences in the oil and gas sector.The key messages of the workshops can be summarized as follows:

- While more clarity on the EU’s renewable energy policy is needed, the North African stake-holders should not focus too strongly on future green energy export opportunities to EU. Rather, meeting domestic energy policies should be their key drivers for developing the RE field in the Maghreb.

- The application of long-term renewable energy delivery contracts suchtake-or-pay should be further investigated with price baskets reflecting the costs of electricity produced from renewables. Parallel to that, international feed-in-tariffs should also be explored.

1 About the authors: Dennis Kumetat (lead author), LSE Kuwait Programme PhD Scholar, Department of Geography andEnvironment, London School of Economics and Political Science ([email protected]); Nassima Hamiane MSc (Imperial College London), freelance consultant, Algiers ([email protected]). 2 The authors and the Friedrich Naumann Foundation wish to express their gratitude for the valuable input and thepro-bono-participation of the following experts and project partners (in alphabetical order): Tahar Achour, Ayadi Ben Aïssa, Walid Bel Haj Ali, Abdelkrim Benghanem, Abdelaziz Bennouna, Tarek Chaabouni, Boubker Chatre, Hakim Darbouche, Justin Dargin, Alex Dhina, Janis Folkmanis, Roger Gaillard, Sadok Guellouz, Salah Hannachi, Toufik Hasni, Ali Kanzari, Alexander Knipperts, Taoufik Laabi, Ulrich Laumanns, Mustapha Mekideche, Silvia Morgenroth, Andreas Reinhardt, Stefan Rist,

03

- The Maghreb countries should seek to develop stronger and more transparent regulatory regimes favouring national (and international) competition in the renewables sector

- Small and medium enterprise(SME) penetration of the renewable power market should be encouraged through a further liberalization of the power sector and the implementation of more integrated policy (market and grid) between the three countries.

- In addition to a focus on the large-scale projects there are many business opportunities for SMEs stemming from bottom–up, small-scale programmes like the solar water heater programme in Tunisia. These areas could provide essential niches for the Maghreb renewable energy SMEs to gain expertise and that can be scaled up to an industrial level at a later point in time.

- To facilitate the concern of the Maghreb countries regarding adequate technology transfer through the development of major renewable projects on their lands a more sustained effort on the part of the host countries is required. A strong and independent regional technology innovation system would need to be put in place and more support (public and also private) should be given to the local R&D sector introducing a wide range of training programmes on with RE policies and technology-related aspects.

- Efforts for having a common North African voice should be intensified in order to strengthen the position of the three countries in the international discussions about trans-regional renewable electricity plans and in order to be more likely to meet domestic expectations in term of jobs creation and technology transfer. A possible forum for this could be COMELEC or the energy ministers’ conference of the AMU.

04

2. Current (Renewable) Energy Policies in the Maghreb

2. 1. Morocco

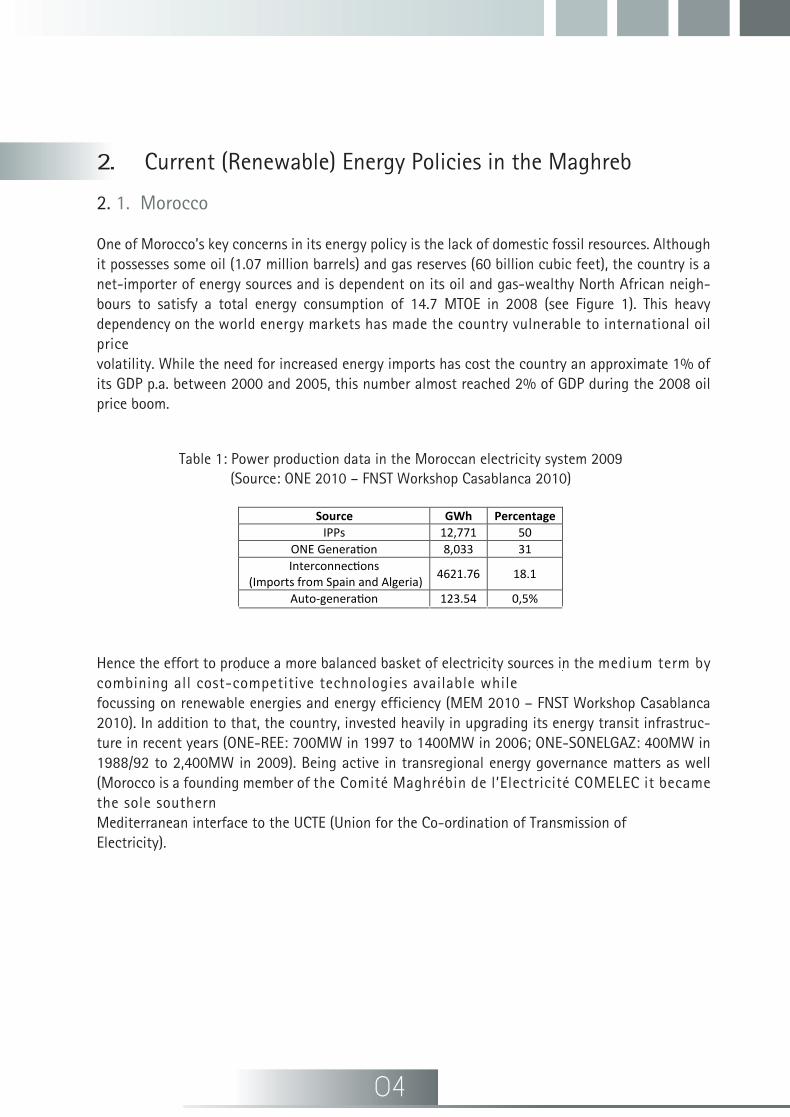

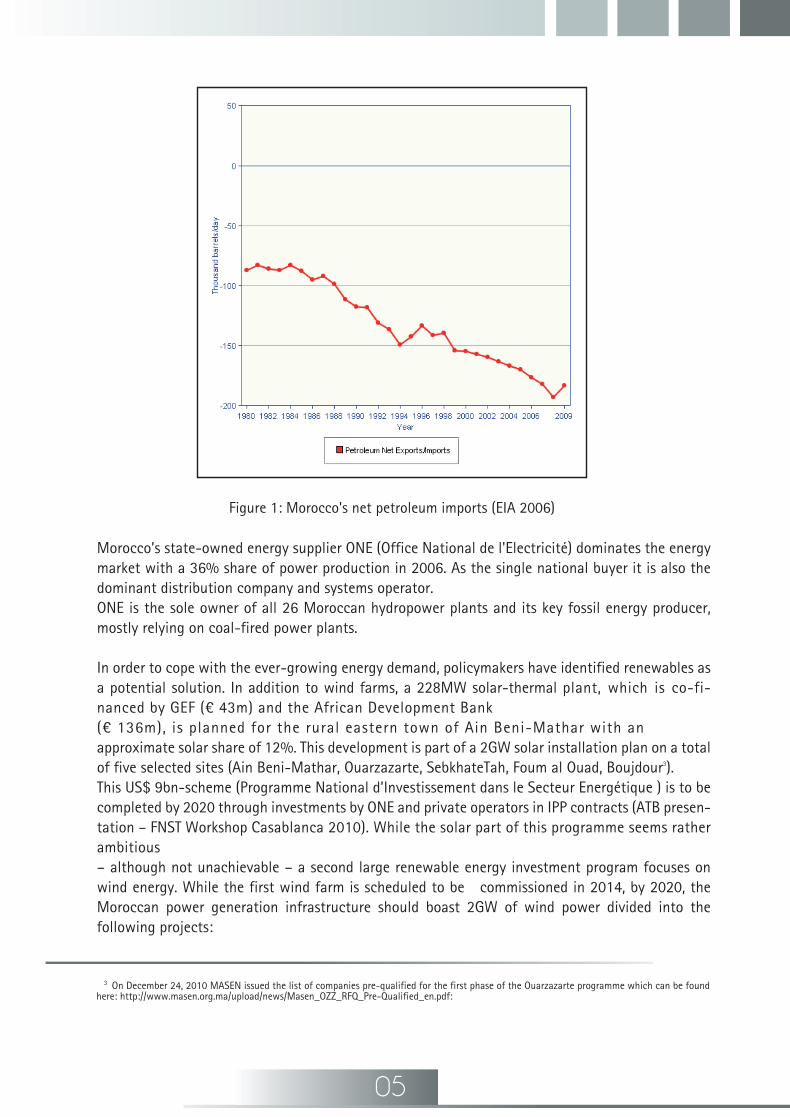

One of Morocco’s key concerns in its energy policy is the lack of domestic fossil resources. Although it possesses some oil (1.07 million barrels) and gas reserves (60 billion cubic feet), the country is a net-importer of energy sources and is dependent on its oil and gas-wealthy North African neigh-bours to satisfy a total energy consumption of 14.7 MTOE in 2008 (see Figure 1). This heavy dependency on the world energy markets has made the country vulnerable to international oil price volatility. While the need for increased energy imports has cost the country an approximate 1% of its GDP p.a. between 2000 and 2005, this number almost reached 2% of GDP during the 2008 oil price boom.

Hence the effort to produce a more balanced basket of electricity sources in the medium term by combining all cost-competitive technologies available while focussing on renewable energies and energy efficiency (MEM 2010 – FNST Workshop Casablanca 2010). In addition to that, the country, invested heavily in upgrading its energy transit infrastruc-ture in recent years (ONE-REE: 700MW in 1997 to 1400MW in 2006; ONE-SONELGAZ: 400MW in 1988/92 to 2,400MW in 2009). Being active in transregional energy governance matters as well (Morocco is a founding member of the Comité Maghrébin de l’Electricité COMELEC it became the sole southern Mediterranean interface to the UCTE (Union for the Co-ordination of Transmission of Electricity).

Source GWh Percentage IPPs 12,771 50

ONE Generation 8,033 31 Interconnections

(Imports from Spain and Algeria) 4621.76 18.1

Auto-generation 123.54 0,5%

Table 1: Power production data in the Moroccan electricity system 2009 (Source: ONE 2010 – FNST Workshop Casablanca 2010)

05

Morocco’s state-owned energy supplier ONE (Office National de l'Electricité) dominates the energy market with a 36% share of power production in 2006. As the single national buyer it is also the dominant distribution company and systems operator. ONE is the sole owner of all 26 Moroccan hydropower plants and its key fossil energy producer, mostly relying on coal-fired power plants.

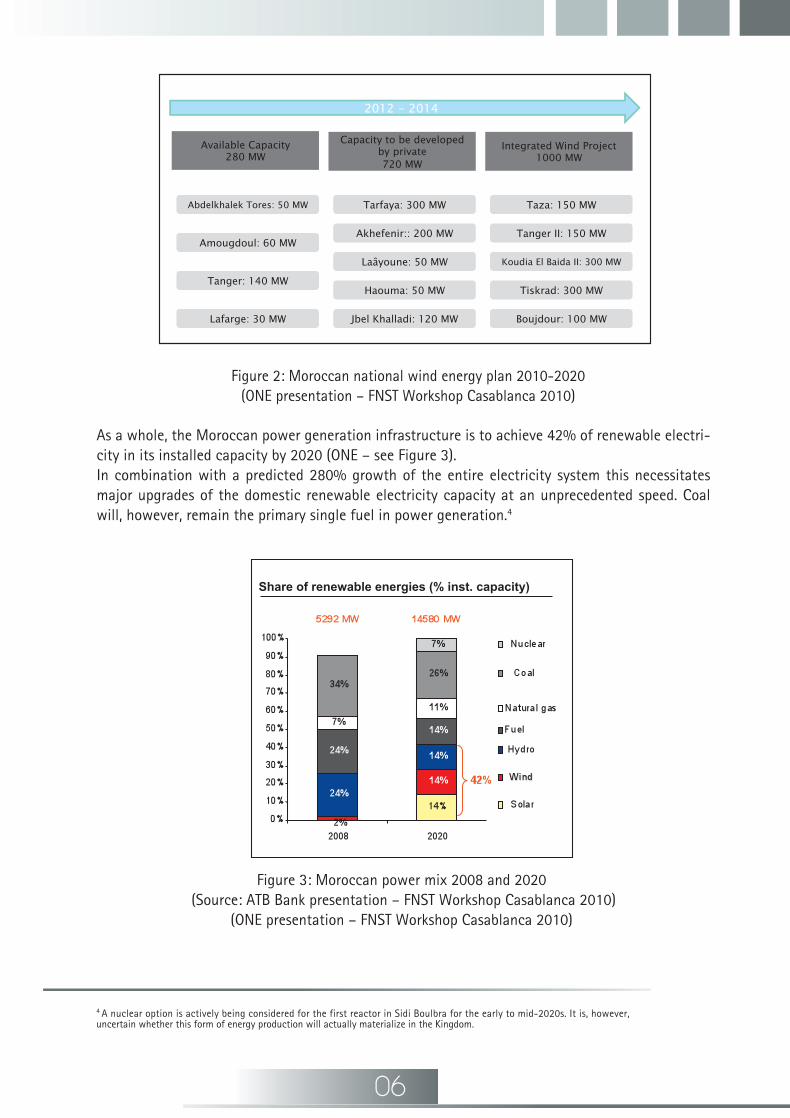

In order to cope with the ever-growing energy demand, policymakers have identified renewables as a potential solution. In addition to wind farms, a 228MW solar-thermal plant, which is co-fi-nanced by GEF (¤ 43m) and the African Development Bank (¤ 136m), is planned for the rural eastern town of Ain Beni-Mathar with an approximate solar share of 12%. This development is part of a 2GW solar installation plan on a total of five selected sites (Ain Beni-Mathar, Ouarzazarte, SebkhateTah, Foum al Ouad, Boujdour3). This US$ 9bn-scheme (Programme National d’Investissement dans le Secteur Energétique ) is to be completed by 2020 through investments by ONE and private operators in IPP contracts (ATB presen-tation – FNST Workshop Casablanca 2010). While the solar part of this programme seems rather ambitious– although not unachievable – a second large renewable energy investment program focuses on wind energy. While the first wind farm is scheduled to be commissioned in 2014, by 2020, the Moroccan power generation infrastructure should boast 2GW of wind power divided into the following projects:

3 On December 24, 2010 MASEN issued the list of companies pre-qualified for the first phase of the Ouarzazarte programme which can be found here: http://www.masen.org.ma/upload/news/Masen_OZZ_RFQ_Pre-Qualified_en.pdf:

Figure 1: Morocco's net petroleum imports (EIA 2006)

Figure 2: Moroccan national wind energy plan 2010-2020 (ONE presentation – FNST Workshop Casablanca 2010)

06

As a whole, the Moroccan power generation infrastructure is to achieve 42% of renewable electri-city in its installed capacity by 2020 (ONE – see Figure 3). In combination with a predicted 280% growth of the entire electricity system this necessitates major upgrades of the domestic renewable electricity capacity at an unprecedented speed. Coal will, however, remain the primary single fuel in power generation.4

4 A nuclear option is actively being considered for the first reactor in Sidi Boulbra for the early to mid-2020s. It is, however, uncertain whether this form of energy production will actually materialize in the Kingdom.

Figure 3: Moroccan power mix 2008 and 2020 (Source: ATB Bank presentation – FNST Workshop Casablanca 2010)

(ONE presentation – FNST Workshop Casablanca 2010)

Share of renewable energies (% inst. capacity)

07

As will be analysed further below, Morocco has also been active in promoting the TREC concept, Dii and the Mediterranean Solar Plan. The fact that the Moroccan Nareva Group became a shareholder of Dii is indicative of that. While most of the large-scale renewable energy potential in the country has yet to be realized, in terms of legislation, regulatory and institutional environment as well of (international) funds the country fulfils most major preconditions for a successful domestic renewable energy sector.

2. 2. Algeria

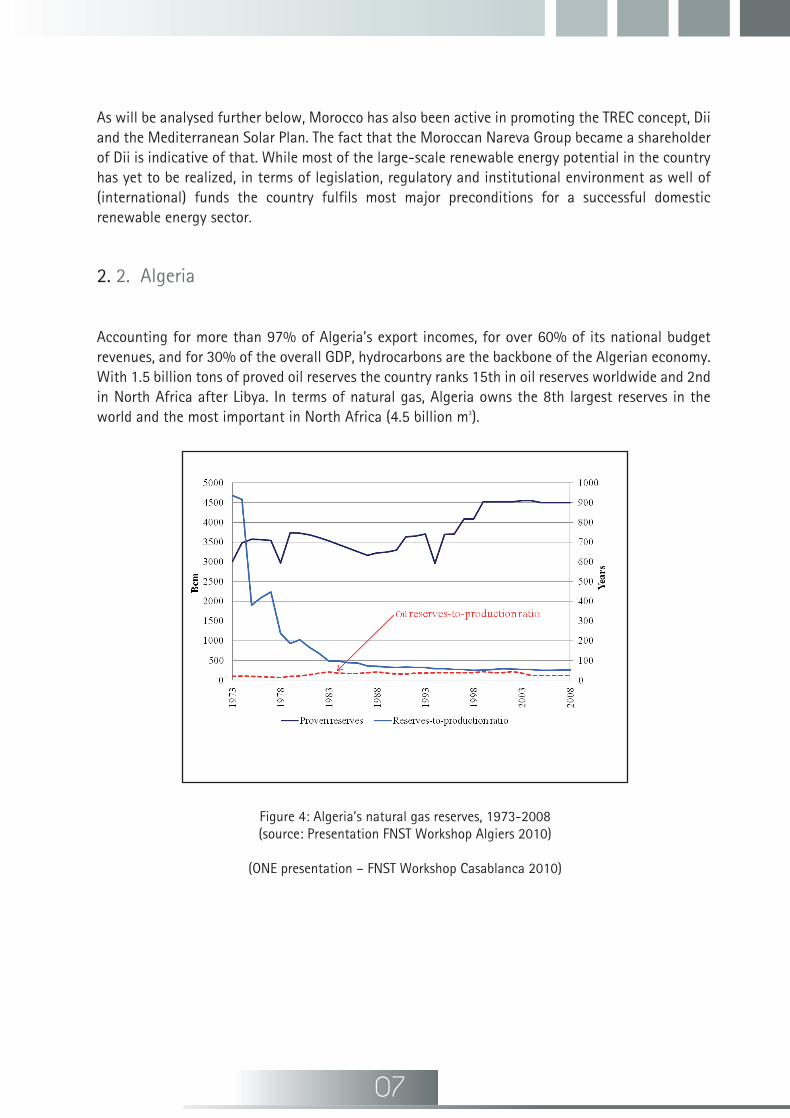

Accounting for more than 97% of Algeria’s export incomes, for over 60% of its national budget revenues, and for 30% of the overall GDP, hydrocarbons are the backbone of the Algerian economy. With 1.5 billion tons of proved oil reserves the country ranks 15th in oil reserves worldwide and 2nd in North Africa after Libya. In terms of natural gas, Algeria owns the 8th largest reserves in the world and the most important in North Africa (4.5 billion m3).

Figure 4: Algeria’s natural gas reserves, 1973-2008 (source: Presentation FNST Workshop Algiers 2010)

(ONE presentation – FNST Workshop Casablanca 2010)

Figure 5: Share of hydrocarbons in Algeria’s economy (source: Presentation FNST Workshop Algiers 2010)

08

In light of this, Algeria’s energy policy remains to date oriented toward theexploitation and export of these fossil resources. In terms of national energy supply, natural gas occupies a central position: over 65% of the national energy needs are met by gas, which also supplies almost the total of the country’s electricityrequirements (about 98%).

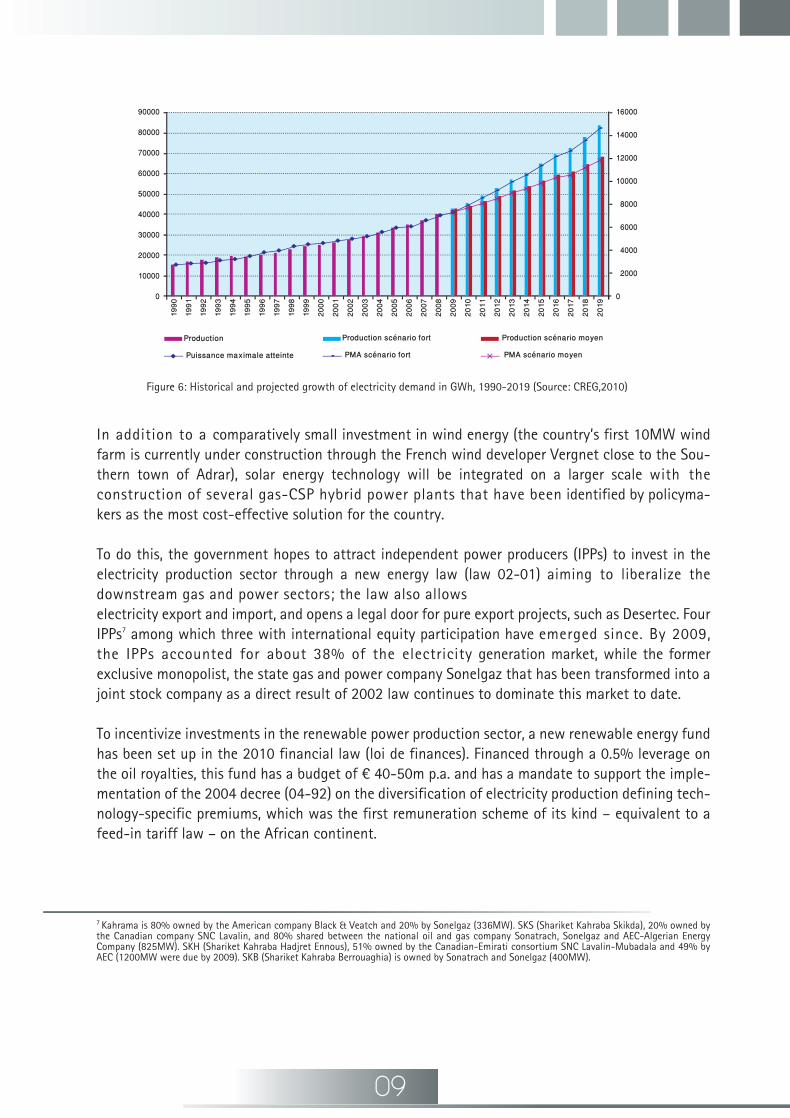

The remaining 2% are shared equitably between diesel and hydraulic sources. The share of power based on non-hydro renewable energy sources is negligible; in 2007, it represented as low as 0.006% of the national energy production mix. With a growth rate of 5.6% between 2000 and 2009, electricity demand reached 33.8TWh by the end of 2009, while the total installed capacity reached 8,411MW. In order to meet the increasing electricity demand of the rapidly growing popu-lation (1.43% population growth rate predicted between 2009-2019) and a healthy economic development5 , the Electricity and Gas Regulatory Commission (CREG) has forecasted a need for an additional capacity of 6,500MW from 2013 in the case of a strong economic growth scenario and 2,940MW starting 2016 for an average economic growth scenario according to the 2010-2019 Programme Indicatif des Moyens en Besoins de Production d’Electricité6. To be able to expand the national power production capacity, Algerian stakeholders intend on the one hand to make the most of the country’s gas reserves, and on the other hand to assign a greater role to renewable energies.

5 An average annual economic growth rate of 4.4% between 2007 and 2035 is forecasted for non-OECD countries as per the International Energy Outlook 2010 reference case, US EIA. 6 Available from CREG’s website: www.creg.gov.dz

Figure 6: Historical and projected growth of electricity demand in GWh, 1990-2019 (Source: CREG,2010)

7 Kahrama is 80% owned by the American company Black & Veatch and 20% by Sonelgaz (336MW). SKS (Shariket Kahraba Skikda), 20% owned by the Canadian company SNC Lavalin, and 80% shared between the national oil and gas company Sonatrach, Sonelgaz and AEC-Algerian Energy Company (825MW). SKH (Shariket Kahraba Hadjret Ennous), 51% owned by the Canadian-Emirati consortium SNC Lavalin-Mubadala and 49% by AEC (1200MW were due by 2009). SKB (Shariket Kahraba Berrouaghia) is owned by Sonatrach and Sonelgaz (400MW).

09

In addition to a comparatively small investment in wind energy (the country’s first 10MW wind farm is currently under construction through the French wind developer Vergnet close to the Sou-thern town of Adrar), solar energy technology will be integrated on a larger scale with the construction of several gas-CSP hybrid power plants that have been identified by policyma-kers as the most cost-effective solution for the country.

To do this, the government hopes to attract independent power producers (IPPs) to invest in the electricity production sector through a new energy law (law 02-01) aiming to liberalize the downstream gas and power sectors; the law also allows electricity export and import, and opens a legal door for pure export projects, such as Desertec. Four IPPs7 among which three with international equity participation have emerged since. By 2009, the IPPs accounted for about 38% of the electricity generation market, while the former exclusive monopolist, the state gas and power company Sonelgaz that has been transformed into a joint stock company as a direct result of 2002 law continues to dominate this market to date.

To incentivize investments in the renewable power production sector, a new renewable energy fund has been set up in the 2010 financial law (loi de finances). Financed through a 0.5% leverage on the oil royalties, this fund has a budget of ¤ 40-50m p.a. and has a mandate to support the imple-mentation of the 2004 decree (04-92) on the diversification of electricity production defining tech-nology-specific premiums, which was the first remuneration scheme of its kind – equivalent to a feed-in tariff law – on the African continent.

0

30000

20000

10000

Production

Puissance maximale atteinte PMA scénario fort PMA scénario moyen

Production scénario fort Production scénario moyen

60000

50000

40000

90000

70000

80000

0

6000

4000

2000

12000

10000

8000

16000

14000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

8 In place since 2002 and under MEM supervision, NEAL is meant to be the principal point of contact in Algeria for all major renewable related projects; it is 45% owned by Sonatrach, 45% by Sonelgaz and 10% by the Algerian private investor SIM.

10

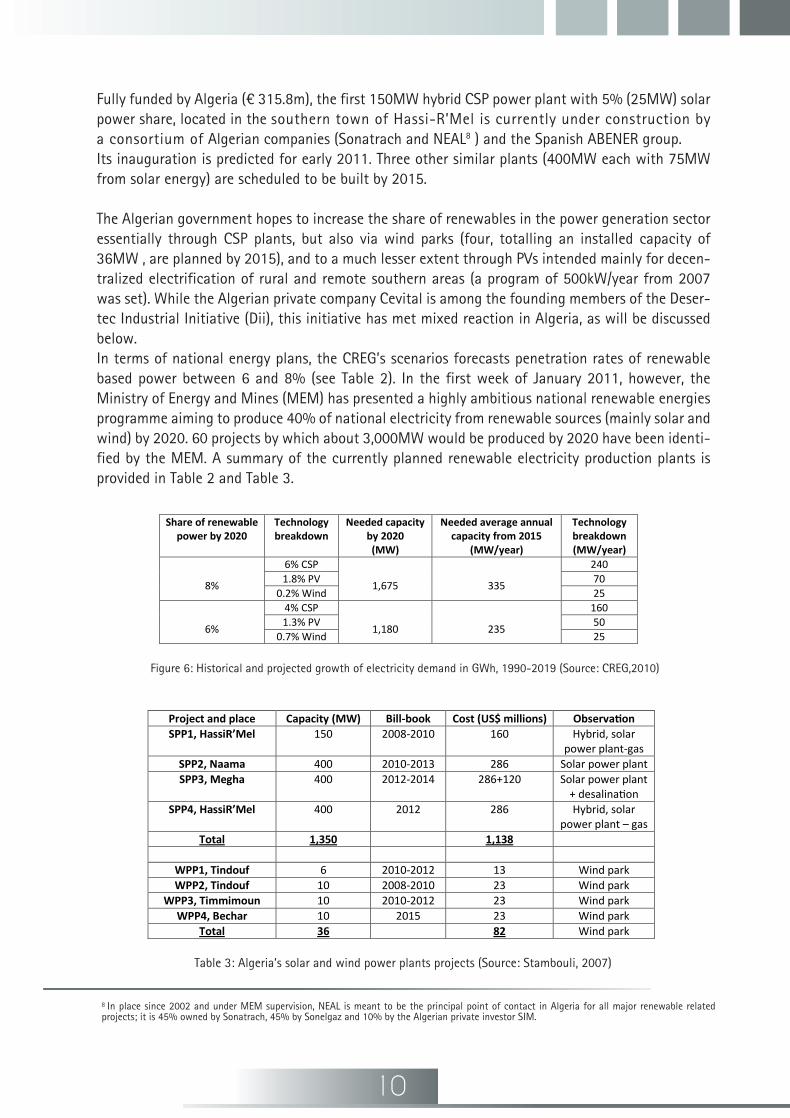

Fully funded by Algeria (¤ 315.8m), the first 150MW hybrid CSP power plant with 5% (25MW) solar power share, located in the southern town of Hassi-R’Mel is currently under construction by a consortium of Algerian companies (Sonatrach and NEAL8 ) and the Spanish ABENER group. Its inauguration is predicted for early 2011. Three other similar plants (400MW each with 75MW from solar energy) are scheduled to be built by 2015.

The Algerian government hopes to increase the share of renewables in the power generation sector essentially through CSP plants, but also via wind parks (four, totalling an installed capacity of 36MW , are planned by 2015), and to a much lesser extent through PVs intended mainly for decen-tralized electrification of rural and remote southern areas (a program of 500kW/year from 2007 was set). While the Algerian private company Cevital is among the founding members of the Deser-tec Industrial Initiative (Dii), this initiative has met mixed reaction in Algeria, as will be discussed below.In terms of national energy plans, the CREG’s scenarios forecasts penetration rates of renewable based power between 6 and 8% (see Table 2). In the first week of January 2011, however, the Ministry of Energy and Mines (MEM) has presented a highly ambitious national renewable energies programme aiming to produce 40% of national electricity from renewable sources (mainly solar and wind) by 2020. 60 projects by which about 3,000MW would be produced by 2020 have been identi-fied by the MEM. A summary of the currently planned renewable electricity production plants is provided in Table 2 and Table 3.

Figure 6: Historical and projected growth of electricity demand in GWh, 1990-2019 (Source: CREG,2010)

Share of renewable power by 2020

Technology breakdown

Needed capacity by 2020 (MW)

Needed average annual capacity from 2015

(MW/year)

Technology breakdown (MW/year)

8%

6% CSP

1,675

335

240 1.8% PV 70

0.2% Wind 25

6%

4% CSP

1,180

235

160 1.3% PV 50

0.7% Wind 25

Table 3: Algeria’s solar and wind power plants projects (Source: Stambouli, 2007)

Project and place Capacity (MW) Bill-book Cost (US$ millions) Observation SPP1, HassiR’Mel 150 2008-2010 160 Hybrid, solar

power plant-gas SPP2, Naama 400 2010-2013 286 Solar power plant SPP3, Megha 400 2012-2014 286+120 Solar power plant

+ desalination SPP4, HassiR’Mel 400 2012 286 Hybrid, solar

power plant – gas Total 1,350 1,138

WPP1, Tindouf 6 2010-2012 13 Wind park WPP2, Tindouf 10 2008-2010 23 Wind park

WPP3, Timmimoun 10 2010-2012 23 Wind park WPP4, Bechar 10 2015 23 Wind park

Total 36 82 Wind park

9 Due to the current phase of political transition, the short-term plans for renewable energies in Tunisia are unlikely to be adhered to. However, this study highlights the more structural issues with regards to Tunisian energy markets, business sectors and industry policy. These trends and observa-tions are likely to apply in future as well.

10 Report published by GTZ (Energy-policy Framework Conditions for Electricity Markets and Renewable Energies) available at: www2.gtz.de/dokumente/bib/04-0110.pdf

11

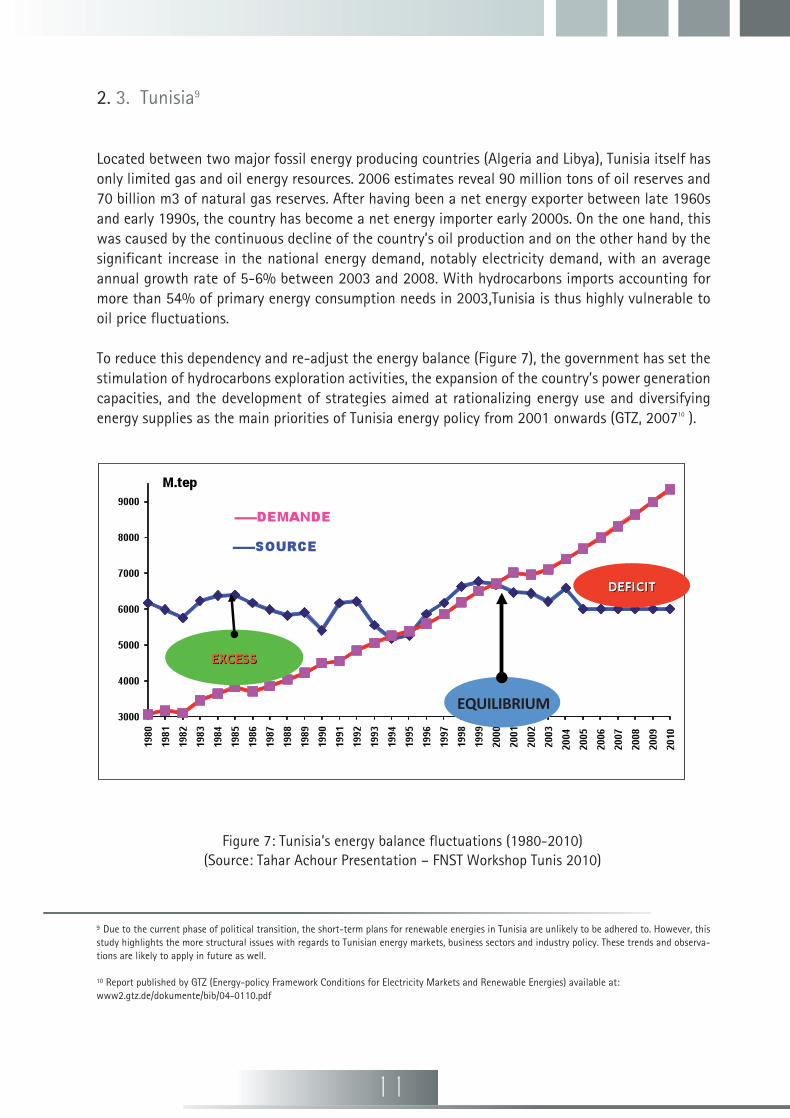

2. 3. Tunisia9

Located between two major fossil energy producing countries (Algeria and Libya), Tunisia itself has only limited gas and oil energy resources. 2006 estimates reveal 90 million tons of oil reserves and 70 billion m3 of natural gas reserves. After having been a net energy exporter between late 1960s and early 1990s, the country has become a net energy importer early 2000s. On the one hand, this was caused by the continuous decline of the country’s oil production and on the other hand by the significant increase in the national energy demand, notably electricity demand, with an average annual growth rate of 5-6% between 2003 and 2008. With hydrocarbons imports accounting for more than 54% of primary energy consumption needs in 2003,Tunisia is thus highly vulnerable to oil price fluctuations.

To reduce this dependency and re-adjust the energy balance (Figure 7), the government has set the stimulation of hydrocarbons exploration activities, the expansion of the country’s power generation capacities, and the development of strategies aimed at rationalizing energy use and diversifying energy supplies as the main priorities of Tunisia energy policy from 2001 onwards (GTZ, 200710 ).

Figure 7: Tunisia’s energy balance fluctuations (1980-2010) (Source: Tahar Achour Presentation – FNST Workshop Tunis 2010)

EQUILIBRIUM

11 Gas supplied from Tunisia’ own resources and imports from Algeria whom provide Tunisia with more than one million tons/year of oil equivalent as a transit fee.

12

In the power sector, Tunisia has currently an installed capacity of 3,470MW where 97% of the elec-tricity comes from gas11 fired thermal power plants, 2% from hydroelectric stations, and 1% from the 20MW Sidi Daoud wind park that was expanded in 2009 with an additional capacity of 35MW. According to the International Energy Agency, Tunisia’s national electricity production totalled 15,311GWh in 2008. In order to meet the rapidly growing demand for electricity, Tunisia will have to expand its power production capacity to 4,400MW by 2011 and to 7,500MW by 2021.

To achieve this, the government envisages building additional conventional power plants (predominantly gas and potentially coal) and developing solar and wind capacities. In the light of this, the liberalization of the power generation sector formed an integral part of the major sector reforms adopted by the Tunisian government. Open to IPPs since 1996, this market was still domi-nated (over 70%) by the state-owned power utility Société Tunisienne d’Electricité et du Gaz (STEG) in 2009. Today, there are two IPPs in Tunisia: brought to service in 2002, the 471MW combined cycle plant at Rades (Rades II) was the first IPP in the country, while the second one is the 30MW gas-fired power plant at El Bibane, which began operating in 2004.

During the last decade, wind power and solar thermal energy for water heating have been the two focal areas of Tunisia’s renewable energy strategy. With regard to solar water heaters, the country announced in 2005 the objective to expand the total collector area to 700,000m2 by 2011 against 30,000m2 in the mid-1990s. The program has become a major success and could raise the collector area to 400,000 m2 in the residential sector by the end of 2009. Also, it could create an industrial and commercial structure formed from more than 1000 small and medium enterprises.

In 2009, the Tunisian government released the Tunisian Solar Plan, according to which Tunisia plans to increase the share of renewable energies in the electricity sector to 10% of the total capacity by 2011 and to 4% in the national energy mix by 2016. Covering the 2010-2016 period, the pro-gramme will cost ¤ 2,300m, of which ¤ 1,530m are intended to be covered by private funds, the rest will be split between the public sector, mainly STEG (¤ 560m), international cooperation (¤ 65m), and the National Fund for Energy Control (FNME) (¤ 145m). The TSP contains 40 projects aimed at promoting solar thermal and photovoltaic energies, wind energy, as well as energy efficiency mea-sures. The plan also incorporates the ELMED project; a 400KV submarine cable interconnecting Tunisia and Italy.

Overall however, the Tunisian Solar Plan remains fairly modest compared to its Moroccan and Algerian counterparts in terms of added capacity. Indeed until 2016, projects in CSP and centralized PV plants will only add about 130MW to the total capacity. With regard to wind capacity, around 280MW are planned by 2016, while 1130MW shall be reached in 2020 and 1,840MW by 2030 as per the scenario of the 2010-2030 development strategy report issued by the Tunisian Energy Control Agency (ANME) responsible for the promotion of renewable energies.

13

The TSP also stipulated the creation of STEG-Renewable Energy (STEG-ER), a new subsidiary of STEG, a project that may suggest the will to maintain a certain state control over power generation from renewable energies. It remains to be seen in how far the currently small structure of STEG-ER can become a major renewable energy actor within Tunisia. On the international front, however, STEG-ER asserted its key role by joining Dii as the first Tunisian shareholder company in October 2010.

In conclusion, the plans to increase the share of renewable electricity are similarly structured and motivated by energy economics (minimizing energy import dependence in Morocco and Tunisia; achieving greater oil & gas export quotas in Algeria). It is the combination of the regulatory and financial fine-tuning and the local entrepreneurial environment that will decide on the success or failure of the respective national renewable energy scheme.

2. 4. International renewable energy initiatives with relevance to the Maghreb The European Union

In terms of power production and grid structures, energy policy largely belongs into the domain of the EU member states. However, since most of the large-scale renewable energy projects that are currently under discussion have a strongly European dimension, this section has been added to the policy brief.

TREC and the Desertec Industrial Initiative

Apart from ambitious and successful domestic programmes in several EU member states, European research and policy-making have increasingly taken interest in power production and transport to the EU from outside Europe.

In addition to the researchers involved, civil society and industry stakeholders promote the construction of large-scale renewable energy power plants in North Africa. One major group was the international political lobby group TREC (Trans-Mediterranean Renewable Energy Corporation) that began working with the German section of the Club of Rome. Its plans have been in the German political discourse for well over a decade. TREC contributed to the discussions by launching its “Desertec White Book”, which has recently appeared in its fourth edition. The TREC concept was taken up by various committed individuals and a series of national groups (e.g. TREC-UK, Deser-tec-Méditerrané, etc.) was founded. In 2008, the group transformed and renamed itself Desertec Foundation and registered in Berlin as an incorporated association.

These activities have sparked the interest of German industry: on July 13, 2009, a group of major German and international corporations (ABB, Abengoa Solar, Desertec Foundation, Deutsche Bank, E.ON, HSH Nordbank, MAN Solar Millennium, Munich Re, M+W Zander, RWE, SCHOTT Solar, Siemens and the Algerian company Cevital announced in a press conference a memorandum of understanding seeking to promote the above-mentioned Desertec initiative and intending to found a Desertec Industrial Initiative (Dii).

14

The formal registration of the consortium as a limited company took place in October 2009.

In its founding declaration, Dii announced overall investments of ¤ 400 billion, which it claimed to be willing and able to invest over the next 20 years into large-scale renewable power projects in the MENA region. In 2010, various other companies joined the consortium (Enel, Terna, Nareva, RED Electrica de Espana, Saint-Gobain Solar, STEG Energies Renouvelables).

The enrolment of these Italian, Spanish, Italian, Tunisian and Moroccan groups was an important step for Dii both in terms of its outreach to the Mediterranean countries as well as to move public perception away from the misconception that the Dii is exclusively a German initiative.

The 2009 announcements met very different responses in Europe and in North Africa respectively. While the former Algerian energy Minister Chakib Khelil voiced criticism towards the project, his successor Youcef Yousfi highlighted that his support depended on three conditions: a genuine tech-nology partnership on all levels; the production of key elements on Algerian soil, and the opening of the European power markets for potential production surpluses. This position has also been put forward by the Algerian President Bouteflika during his visit in Berlin in December 2010. In spite of this, for reasons to be discussed below, international investment in the renewables sector in Algeria is considered as rather difficult in comparison to its two neighbour states:

In Morocco, support for national and regional renewable energy projects has been voiced at the highest level by King Mohamed VI. In that vein, Moroccan energy minister Amina Benkhadra gene-rally conveyed the notion that Morocco wanted to become a major Desertec partner and advoca-ted for investment in her country. In February 2010, for instance, minister Benkhadra gave a semi-nar in the British House of Commons that was attended by the UK energy minister Lord Hunt. In this meeting, she advocated Morocco’s Ouarzazate plant and invited power companies to bid on that US$9 billion project.

A similar notion has also been conveyed by Tunisian authorities: while Morocco is arguably the most visible Maghreb state in terms of renewable energy policies in Europe, Tunisia has managed to place itself well on the international scene through its recent high-level Tunisian Solar Energy conference (November 2010) during which the Desertec University Network (DUN) was founded (see below for a further discussion of DUN). Apart from welcoming statements by parties, environmental NGOs and research institutions, there have also been critical voices in Europe. Eurosolar, a German solar energy lobby group, dubbed the plans “mirages in the Sahara desert” and “centralistic plans of the German power sector” that were designed to perpetuate the dominance of a few corporations in the national power sector.

15

At the time of writing, the Dii is working on a detailed implementation strategy that defines a roadmap until 2020. This roadmap is to be finalised by 2012 and it will entail a long-term vision beyond 2020. In talks and press announcements, Dii partners the Mediterranean for at least the last 15 years, first through the Barcelona Process as of 1995 then through the European Neighbou-rhood and Partnership Instrument (ENPI) in 2007. Parallel to this, the Union for the Mediterranean (UfM) was founded in 2008. One of its flagship projects is the Mediterranean Solar Plan (MSP), which has been designed as an instrument to be driven primarily by private investment considera-tions targeting mainly renewable energy projects in North Africa and interconnectors to Europe while a EU Directorate General Europe-Aid project strengthens market and legal framework condi-tions in the region simultaneously.

The bureau of the MSP distinguishes between public and private projects. Integrating wind energy and both PV and CSP, the scope of the MSP is wide, which explains the roughly 200 projects regis-tered. In general, projects are registered on the MSP list (that remains unpublished) through the member states’ ministries or executing energy agencies. This implies that the registered projects differ strongly in terms of scope, size, and feasibility.

In spite of this, the MSP secretariat has chosen not to introduce a binding trans-regional methodo-logy, as the multilateral process to agree on such a mechanism would have taken years and would have been a difficult undertaking given the large number of member states and heterogeneous renewable energy policy frameworks, technology preferences and funding schemes. Thus, flexibility and transparency, rather than a total control of the projects, is what is achieved by the MSP admi-nistration.

Concerning the overall investment costs, a total sum of ¤ 45 billion is forecast until 2020. While various projects have been registered with the CTF and other investment banks, the financing of most projects should not be the key problem. Instead, it is the differing funding conditions, loan times and other details of the financial architecture for the larger projects in this scheme that currently needs attention on behalf of the MSP. This analysis has been confirmed by a study published by the European Investment Bank in October 2010 assessing current projects all over the Arab Mediterranean states. It concluded that if all pronounced targets were met, the region could reach 26GW of additional renewable electricity capacity by 2020 – which would mean it would comfortably fulfil the 20GW by 2020 the MSP originally planned. However, this study came to the rather dramatic conclusion that the actual projects in the national pipelines amount to only 10.3GW by 2020 while out of those 10.3GW only 2.2GW are projects that are at an advanced stage of development, and only 600MW have a financial plan. Evidently, although not negating the continuous and valuable high-level efforts of the MSP, doubts about the final implementation potential of the MSP must be raised.

16

Furthermore, the study demonstrated that out of the mentioned 2.2GW 80% are wind projects, while most of the less mature projects as a whole are solar projects of both PV and CSP technolo-gies. Given the maturity of the wind energy industry this cannot be too surprising.

However, it shows that all forms of solar or thermo-solar power generation still need strong tech-nology-push measures to become price-competitive in the mid-term future. It needs to be kept in mind that the MSP itself can only work as a facilitator of the national initiatives and can assist member states in developing a conducive regulatory framework and in acquiring funds. The genuine initiative, however, must come from the member states themselves, which is why the MSP secreta-riat also welcomes the developments such as the Moroccan or Tunisian solar plans as a step in the right direction. It would be desirable for Algeria to develop a plan similar to the ones of its neigh-bours, as the Algerian programme indicatif cannot yet be seen as a fully-fledged national renewable energy policy programme. The recent ambitious Algerian announcements can, however, be seen as a step in this direction.

The EU Renewable Energy Directive

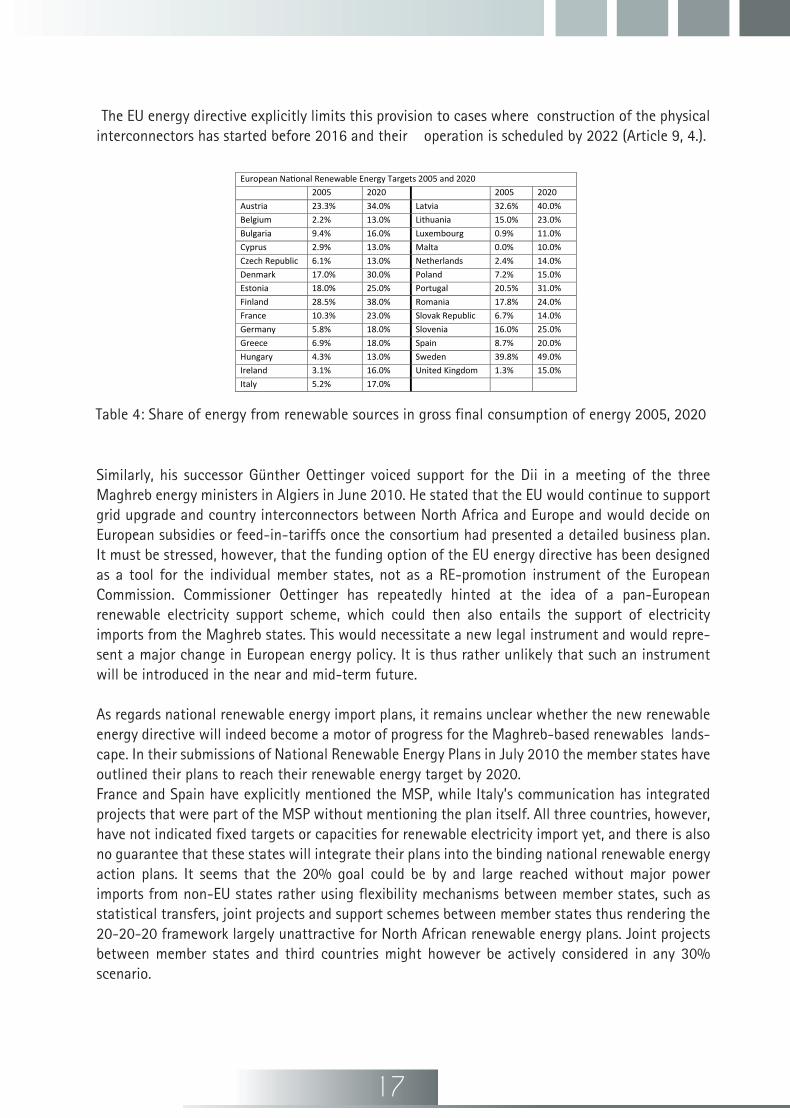

In December 2008, the member states of the European Union signed an agreement about the increased use of renewable energies in the community’s energy supply. In the Directive on the Promotion of the Use of Energy from Renewable Sources all member states committed themselves to binding renewable energy shares in their national energy balance (see Table 4). Each member is obliged to present an individual roadmap outlining how the state intends to meet its renewable energy goal. It is up to the member states to choose their own means for the goal’s implementation. These could include various sectors, such as transport, industry, or heating, but also renewable electricity production.

As a remarkable innovation, the EU renewable energy directive facilitates the import of renewable electricity generated by third countries. Such a third country could, for instance, be any Maghreb country. The third country provision is given in Article 9 of the directive, which stipulates that energy produced outside the EU can be financially supported through laws promoting renewable energies as long as this energy export does not lower the previous RE quota of the country of origin. Also, this power can be added to the respective countries’ quotas for renewable energy power.

An interesting feature of the directive is that it also allows non-physical electricity export. For this, it has to be proven that actual power lines will be built within a realistic time frame. In that regard, Morocco and Tunisia are currently ahead of Algeria.

However, according to the directive, any Maghreb country could promote the construction of renewable energy power plants before their electricity physically reaches the EU. It remains to be seen whether this energy trade option could develop into a key element of kick-starting large-scale electricity exports from North Africa to Europe.

17

The EU energy directive explicitly limits this provision to cases where construction of the physical interconnectors has started before 2016 and their operation is scheduled by 2022 (Article 9, 4.).

Similarly, his successor Günther Oettinger voiced support for the Dii in a meeting of the three Maghreb energy ministers in Algiers in June 2010. He stated that the EU would continue to support grid upgrade and country interconnectors between North Africa and Europe and would decide on European subsidies or feed-in-tariffs once the consortium had presented a detailed business plan. It must be stressed, however, that the funding option of the EU energy directive has been designed as a tool for the individual member states, not as a RE-promotion instrument of the European Commission. Commissioner Oettinger has repeatedly hinted at the idea of a pan-European renewable electricity support scheme, which could then also entails the support of electricity imports from the Maghreb states. This would necessitate a new legal instrument and would repre-sent a major change in European energy policy. It is thus rather unlikely that such an instrument will be introduced in the near and mid-term future.

As regards national renewable energy import plans, it remains unclear whether the new renewable energy directive will indeed become a motor of progress for the Maghreb-based renewables lands-cape. In their submissions of National Renewable Energy Plans in July 2010 the member states have outlined their plans to reach their renewable energy target by 2020. France and Spain have explicitly mentioned the MSP, while Italy’s communication has integrated projects that were part of the MSP without mentioning the plan itself. All three countries, however, have not indicated fixed targets or capacities for renewable electricity import yet, and there is also no guarantee that these states will integrate their plans into the binding national renewable energy action plans. It seems that the 20% goal could be by and large reached without major power imports from non-EU states rather using flexibility mechanisms between member states, such as statistical transfers, joint projects and support schemes between member states thus rendering the 20-20-20 framework largely unattractive for North African renewable energy plans. Joint projects between member states and third countries might however be actively considered in any 30% scenario.

European National Renewable Energy Targets 2005 and 2020

2005 2020 2005 2020

Austria 23.3% 34.0% Latvia 32.6% 40.0%

Belgium 2.2% 13.0% Lithuania 15.0% 23.0%

Bulgaria 9.4% 16.0% Luxembourg 0.9% 11.0%

Cyprus 2.9% 13.0% Malta 0.0% 10.0%

Czech Republic 6.1% 13.0% Netherlands 2.4% 14.0%

Denmark 17.0% 30.0% Poland 7.2% 15.0%

Estonia 18.0% 25.0% Portugal 20.5% 31.0%

Finland 28.5% 38.0% Romania 17.8% 24.0%

France 10.3% 23.0% Slovak Republic 6.7% 14.0%

Germany 5.8% 18.0% Slovenia 16.0% 25.0%

Greece 6.9% 18.0% Spain 8.7% 20.0%

Hungary 4.3% 13.0% Sweden 39.8% 49.0%

Ireland 3.1% 16.0% United Kingdom 1.3% 15.0%

Italy 5.2% 17.0%

Table 4: Share of energy from renewable sources in gross final consumption of energy 2005, 2020

18

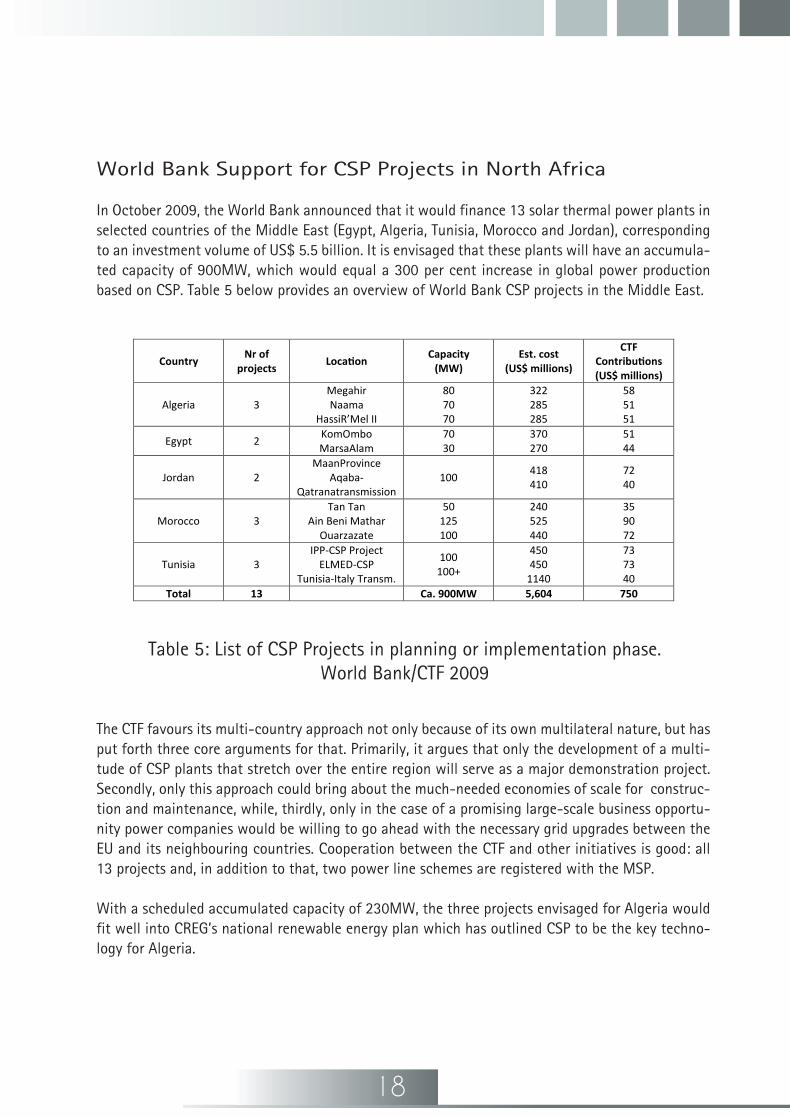

World Bank Support for CSP Projects in North Africa

In October 2009, the World Bank announced that it would finance 13 solar thermal power plants in selected countries of the Middle East (Egypt, Algeria, Tunisia, Morocco and Jordan), corresponding to an investment volume of US$ 5.5 billion. It is envisaged that these plants will have an accumula-ted capacity of 900MW, which would equal a 300 per cent increase in global power production based on CSP. Table 5 below provides an overview of World Bank CSP projects in the Middle East.

The CTF favours its multi-country approach not only because of its own multilateral nature, but has put forth three core arguments for that. Primarily, it argues that only the development of a multi-tude of CSP plants that stretch over the entire region will serve as a major demonstration project. Secondly, only this approach could bring about the much-needed economies of scale for construc-tion and maintenance, while, thirdly, only in the case of a promising large-scale business opportu-nity power companies would be willing to go ahead with the necessary grid upgrades between the EU and its neighbouring countries. Cooperation between the CTF and other initiatives is good: all 13 projects and, in addition to that, two power line schemes are registered with the MSP.

With a scheduled accumulated capacity of 230MW, the three projects envisaged for Algeria would fit well into CREG’s national renewable energy plan which has outlined CSP to be the key techno-logy for Algeria.

Country Nr of

projects Location

Capacity (MW)

Est. cost (US$ millions)

CTF Contributions (US$ millions)

Algeria 3 Megahir Naama

HassiR’Mel II

80 70 70

322 285 285

58 51 51

Egypt 2 KomOmbo MarsaAlam

70 30

370 270

51 44

Jordan 2 MaanProvince

Aqaba-Qatranatransmission

100 418 410

72 40

Morocco 3 Tan Tan

Ain Beni Mathar Ouarzazate

50 125 100

240 525 440

35 90 72

Tunisia 3 IPP-CSP Project

ELMED-CSP Tunisia-Italy Transm.

100 100+

450 450

1140

73 73 40

Total 13 Ca. 900MW 5,604 750

Table 5: List of CSP Projects in planning or implementation phase. World Bank/CTF 2009

19

The Transgreen/MedGrid Consortium

While the Dii has begun to work on the realisation of its projects during the last year, it has not always been welcomed by all European countries. Particularly in France, where the government has worked hard to establish the Union for the Mediterranean and the Mediterranean Solar Plan, Deser-tec has since been perceived as a German initiative that might endanger the “French” Solar Plan. In light of this context, a recent development is particularly noteworthy.

On 25 May 2010, the Transgreen project was founded in Cairo during an energy ministers’ meeting of the Union for the Mediterranean. Led by the French utility EDF, the project brings together power companies, network operators and high-tension equipment makers. The consortium itself is struc-tured in a very similar way to the Dii. It likewise plans to launch a feasibility study as a first phase before actually constructing any lines. In total, eleven mostly French companies, such as ABB, Alstom/Areva, Nexans, Prysmian, Cap Gemini or Atos Origin, RTE have joined the consortium; Spa-nish and North African companies are expected to join in due course as well. In addition to these, Transgreen has also taken in Siemens and the French group Saint-Gobain, both also part of the Dii.

At a first glance, the Transgreen project appears to be a competitor to Desertec – this, however, seems to be a misconception as both sides have announced strong cooperation and excellent inte-raction with each other on the working level.

Thus, there is full potential that the two consortia add to each other in a mutually beneficial way: Transgreen could deliver to Europe the energy (or part of it) that has been generated by the Dii in North Africa. After feasibility studies, a first step of Transgreen might be the upgrade of what is currently the only power connection between the two continents, linking Morocco and Spain, with a capacity of 1,400MW. This – in addition to another power cable (the Tunisian-Italian ELMED) – could facilitate the work of the Dii in a major way.

In conclusion, the most pressing issues renewable energy schemes in the Maghreb face with regard to Europe seem to be the combination of still unclear financial and pricing issues; a lack of clarity on the European side regarding the new energy directive and the possibility of electricity exports to Europe; grid issues and a not yet fully developed legal framework and power market condition in North Africa.

20

3. Main Findings of the workshops

The next section will focus on the results of the workshops held. Participants discussed lively various aspects of how to create enabling conditions for the Maghreb’s private renewable energy sector. Two key aspects have become evident:

a) The Maghreb’s renewable energy sector is very heterogeneous. Companies involved cover the entire range from the former parastatal monopolist utilities to micro-sized enterprises based on the workforce of one or very few. It is evident that in this environment, companies follow very different development strategies and can hardly be grouped under the same category. Thus, in opposition to the country-by-country approach chosen in the first part of this study, the following section will work along trans-regional issues rather focussing on a division by company size (large-scale vs. SMEs) than by country.

b) Identifying measures to unlock the North African renewable energies potential for local and regional businesses is a complex undertaking. As argued above, there is no one-size-fits-all solution as problems are multi-layered and multi-scalar. Thus, the following discussion has been divided into several subsections that have been identified as key areas for local business development.

3. 1. Legislative and institutional framework

The electricity sector needs a strong and transparent regulatory system of the power sector as well as a clear financial incentive to invest in comparatively costly renewable energy production capaci-ties. Morocco, Algeria and Tunisia show relatively advanced policies aimed at diversifying their national energy mix through the liberalization of their electricity markets and the integration of commercial scale renewable power generation to their current fossil-dominated electricity produc-tion systems. Despite these reforms, the three states still remain far from a fully liberalized electri-city sector; the market operations (transmission, distribution, and purchase) remain today under the control of the omnipresent state utilities.

Even though Morocco is on the verge of introducing a fairly innovative legal framework for promo-ting renewable energies by adapting a feed-in tariff model, most of its momentum is likely to be lost by cutting out its integral parts. So does the draft law not give any details about the targeted height of financial support. It also remains unclear whether only wind power will be supported or if other forms of energy production, e.g. solar thermal power production, will be included. There are therefore severe doubts regarding the scope of this law. It might be true that smaller, private opera-tors will benefit for a limited, regional off-grid use of renewables; any major on-grid projects that might be able to challenge ONE’s dominant market position are subject to government agreement and thus unlikely to happen.

With regards to funding, despite the fact that Morocco’s international credit rating has been upgraded in March 201012, the availability of capital in the Maghreb is not comparable with major European economies like Germany or Spain, where the feed-in-tariff model has proven to be successful. Thus, countries need to rely on international development banks for both large projects.

12 According to Standard and Poor’s Morocco’s new rating is now BBB+ for long-term local currency credits and BBB-/A-3 to long and short-term foreign currency sovereign credit ratings.

21

Although various favourable credit lines are on offer, it might still remain difficult to encourage sufficient momentum to attract private capital: if the height of the feed-in tariff is unclear, no rate of return can be given and other key financial indicators can only be approximated. The financial engineering of the planned projects, their contractual forms and transparency of tenders is thus an issue that needs to be improved in future.

In Algeria, the feed-in tariff scheme introduced through decree 04-92 has so far not had the expec-ted impact of boosting the renewable energy market in the country. One major impediment concerns the already highlighted uncertainties about the return on investment which large-scale private investors face. The missing definition of a base price upon which the calculation of the feed-in bonuses is based as well as the more structural market distortions through electricity subsi-dies (three times less than the average price, electricity in Algeria is the cheapest in the Euro-Medi-terranean region) tend to discourage private investments.

The restrictive procedures, that the new power plants are subject to constitute another obstacle for private investors. Beyond the 25MW generation capacity allowed for power production for own demand (French: autoproduction), a consent from CREG or the Ministry of Energy is required limi-ting therefore the right of accessing the Algerian electricity grid. Potential renewable power plants that are meant for export exclusively would not exempt from this requirement, unless the law would be changed for that case. A further barrier is related to the transmission network. Next to the fact that it cannot be owned by a third party, the national grid monopolist, Sonelgaz GRTE (a subsi-diary of Sonelgaz group) has no legal obligations to construct transmission lines for private electri-city generation projects.

Today it remains unclear whether the electricity law passed in 2002 (law 02-01) prohibiting natio-nal and foreign entities to have independent transmission lines applies or not to power generation plants exclusively dedicated for export. Also, the 2009 financial law requiring all foreign develop-ments in the country to be partnered by an Algerian majority shareholder (51%) is widely perceived as a barrier against foreign investments in potential large-scale renewable power projects. The 2004 renewable energies law (law 04-09) that foresaw the introduction of a new market based mechanism (renewable certificate system) is currently under reformulation, a process that may take several years before a new text comes into force. It should however be underlined that from an economic point of view, a competitive electricity market is a prerequisite for the success of such scheme.

By liberalizing its electricity market since more than a decade (1996), promulgating its energy control law (2004) and 2009 by introducing a feed in tariff mechanism for self-generation (2009), Tunisia has made important steps toward the promotion of renewable energies on all scales. However, as discussed earlier, the Tunisian electricity sector is still largely state-controlled and only geared to competition to a limited extent.

22

Similarly to the fossil-based power plants, the electricity produced from renewable energy sources can be fed into the national grid under STEG monopoly only through tendering processes and indivi-dual contracts between private producers and STEG. The latter can purchase up to 30% of electricity surplus from private producers for which power generation is not their primary business. Although STEG is not obliged to purchase electricity from purely power producing companies, the purchase can be done through individual contractual arran-gements. To date, there is no RET-specific legislation in place aimed at promoting power production from these sources. However, private investors can benefit from tax and customs duty reductions, which can be reduced to a minimum rate of 10%. Also, the state can make the land available at a symbolic price for projects considered as strategic in the view of engaged capitals and jobs creation opportunities.

Decisions on concessions of this nature are taken by the Commission Supérieure de la Production Indépendante d’Electricité (CSPIE).In conclusion, all Maghreb states have made significant adjustments in their institutional and regu-latory electricity systems on the surface. It seems however, that in all three states, major issues that are more deeply engrained in the economic or political structures of the countries currently remain that prevent the well-designed new frameworks from making a breakthrough in the renewables sector.

3. 2. Relationship to the EU

Discussions in the three workshops reflected the different national experiences the Maghreb states have made with the European Union. While Moroccan and Tunisian entrepreneurs were keenly aware of the Brussels machinery and expectations for fruitful business cooperation were rather high, the focus of the Algerian workshop lay more on the country’s own energy experience and in how far a meaningful technology and energy interrelationship could be forged between Algeria and the EU. This touches upon the key questions where a renewable energy production should be physi-cally based (EU vs. Maghreb) and for whom (for the EU member states or for domestic use) such a production should be erected. Only when this has been decided on, the questions of how to achieve the respective domestic or international goals and how the private sector in the Maghreb could gain the maximum from such an undertaking can be answered in a meaningful way.

i. Import-export issues

This can be demonstrated in the question of EU-Maghreb electricity market issues. As shown above, it remains uncertain in how far EU member states will make use of the existing framework to import renewable electricity from the Maghreb to fulfil their 2020 quotas. Although the EU’s and the Maghreb’s power markets are already integrated to a large extent (grid synchronisation with UCTE, the Spanish-Moroccan electricity trade, as well as the listing of Algerian and Tunisian utilities at the Spanish electricity exchange), the EU’s renewable energy policy could constitute a forceful pull factor for renewable energies in the Maghreb.

23

Although various favourable credit lines are on offer, it might still remain difficult to Given the lack of clarity of the European policy side, however, North African stakeholders should not focus their interests too strongly on this opportunity. Instead, a more promising way might be to lobby domes-tically for the proclamation and actual implementation of strong domestic renewable energies targets. In addition to that, a common regional power market in the Maghreb under the roof of COMELEC might yield considerable synergy effects for the North African renewable energy markets that might be an excellent first step towards a larger regional electricity interconnection. This step might arguably also be less rigged by economic and political imbalances, such as an EU-Maghreb power market integration could possibly become.

ii. Problem of access to information and lack of clarity in EU policy for Maghreb stakeholders

Another frequently mentioned issue was the apparent lack of access to information on the EU even on a senior level. In the Maghreb, the European Union continues to be seen as a political behemoth that is a key actor for the countries themselves, but that its actual policy decisions are also hardly predictable. While state institutions already at times fail to understand the intricacies of the Euro-pean system and have difficulties addressing the right stakeholders in the complex power rela-tionships between Brussels and the 27 member states, this is significantly harder for a small or medium-sized private enterprise from any Maghreb country that lacks experience and human medium-sized private enterprise from any Maghreb country that lacks experience and human resources to do so.

In the renewable energies field, the many initiatives of the last years, such as Desertec, have been wrongly ascribed to the EU. Others, such as the new Renewable Energy Directive have nurtured great business expectations for Maghreb entrepreneurs. This is the reason why the cautious steps taken by many European decision-makers in the trans-regional renewable field has thus caused great disappointment with the EU. A greater degree of openness would serve EU institutions in the Maghreb well; not least in order to manage expectations that tend to grow out of proportion the less intimate the contact between the EU and the business (and political) environment becomes.

3. 3. Regional integration in the Maghreb

As discussed earlier, there is no doubt that the electricity markets of the Maghreb countries have undergone major transformations in the recent years. The steadily growing domestic electricity demand necessitates these states to significantly enlarge their power generation capacities and upgrade their electricity grids, both involving heavy investments. However, the partial power market liberalisation achieved to date tends to hamper the realisation of the needed large-scale projects that often encounter major financing issues. In addition to the general move towards a more competitive power market, the Maghreb governments have expressed their will

24

to integrate their national electricity markets. This goal was first expressed in 1989 by the Arab Maghreb Union (AMU) governments and led to the creation of the Maghreb Electricity Committee (COMELEC).

During the three workshops held this issue has emerged as one of the fundamental aspects in order for DESERTEC or MSP to become a reality. In the light of this, the Maghreb countries have agreed to launch a major electricity market harmonization project. The cooperation protocol was signed in Rome in December 2003 at the Euro-Mediterranean Conference of Ministers of Energy, where the Maghreb states set up a regional electricity market that would progressively be integrated into the EU.

Being technically interconnected with the European Network of Transmission System Operators for Electricity (ENTSO-E) since 1997 (see Figure 8), Morocco, Algeria and Tunisia have all shown parti-cular adhesion to this Euro-Maghreb regional power market project, which explains the role occu-pied by the state power companies of both Morocco and Algeria (ONE and Sonelgaz) as licensed traders on the Spanish electricity exchange platform Operador del Mercado Ibérico de Energía (OMEL) since 2001 as well as the agreement of these two companies to create a joint venture for the installation of a power distribution network from Algeria to Spain. More recently during the first council of AMU energy ministers held in Algiers in June 2010, the wish for a closer Maghreb-EU energy cooperation and market integration by 2020/2025 has been reiterated by the different ministers. They consider such an integration not only as a real opportu-nity for the creation of a free trade area between the two shores of the Mediterranean but also as a means to encourage the European Union to put more efforts in the field of technology transfer. Despite being liberalised, the EU power market remains difficult to access for the Maghreb countries. Sonelgaz, for instance, had been prohibited in 2009 from acting as an electricity producer and seller in Spain, obstacles that are not yet entirely removed today.

Since its creation, the AMU remains deeply weakened by the political divergences that exist between Morocco and Algeria. It remains to be seen if the recently expressed willingness to work toward the creation of a strong common economic platform rather than toward political integra-tion would push forward the Maghreb-EU power markets integration set target.

25

In addition to the need for the adaptation of regulatory frameworks within and between the EU and the Maghreb countries, other challenges facing the regional power market integration need to be addressed. Amongst them, the heavily subsidized energy prices tend to undermine the commercial attractiveness of renewable energy projects and to reduce effectiveness of market mechanisms such as feed-in-tariffs when introduced. Lastly, the lack of private investments in the absence of adequate support policies and regulatory stability form the most relevant regional barriers to a quick spread of renewable electricity in the Maghreb (see Figure 9).

Figure 8: Existing and future electrical interconnections in EU-Maghreb region (Source: COMELEC 2008)

Figure 9: Main aspects required for the creation of an integrated electricity market

(Source: COMELEC 2008)

1

2

3

IWith regard to the latter point, experts from the workshop panels argued that long term take-or-pay contracts currently used in the oil and gas sector may minimise regulatory uncertainty and reduce risk for private investors. In the hydrocarbon sector, the take-or-pay clause requires that gas has to be paid for whether it is taken or not, and the clause specifies an obligation for the seller to make available defined volumes of gas. The take amount can be specified in two ways:

1) By allowing the buyer to take a quantity which is a specified percentage of the production within a given lifetime.

2) By basing it on a percentage of production capacity of the well. With both the reserves and the capacity are tested periodically, these indicate from changes, the buyer can be asked to modify the take quantity, though the percentage itself is fixed. In order to absorb seasonal demand fluctua-tions, annual take requirements may be modified and complemented by monthly or daily with-drawals (Presentation J. Dargin – FNST workshops Casablanca & Tunis 2010).

Indeed, for scaling up renewable energies it will be key to design support schemes that protects investors from regulatory and commercial uncertainty that might be caused by future develop-ments in terms of grid access, load management and cost calculations. These risks could be over-come by the use of take-or-pay contracts through which revenue streams would remain unchanged regardless of unpredictable market developments. Also, they would allow for efficient system operation and are generally compatible with the tradition of state directed development in the region.

Long-term prices in the hydrocarbon take-or-pay contracts are usually tied to a basket reflecting price developments on the oil and gas markets. For a long-term renewable energy delivery contract, other price baskets reflecting electricity production costs could be developed.However, it remains an open question whether the specific contractual form of a take-or-pay model would be a necessary and adequate instrument for the promotion of renewable electricity or whether long-term price guarantees in the form of national or international feed-in-tariffs would not cause the same effects with significantly smaller efforts.

3. 4. Renewable energy industry structures: former monopolists vs. SMEs?

As highlighted above, the prevailing dominance of the former national champions remains a major issue in all three Maghreb countries. In all of them powerful formerly national utilities (ONE – Sonelgaz – STEG) have long enjoyed a position of state monopolists. With the spread of the mar-ket-liberal European acquis communautaire across the Mediterranean, these three parastatals are now independent companies that have, however, retained strong linkages and good relationships with the state.

26

27

While the three utilities mentioned come from a non-renewables power sector background, all of them have been exposed to the recent renewables boom and have opened themselves to it by either founding subsidiaries (NEAL, Algeria; STEG-ER, Tunisia) or by launching large-scale renewable energies programmes by themselves (ONE).

This combination of excellent government relations as well as their international connections and decades of experience in the domestic power sector (indeed, it is fair to say that these companies were one with the respective domestic sectors until very recently), causes major hurdles for domes-tic and international SMEs to enter profitable sectors of the domestic markets, as several CEOs of SMEs confirmed in the FNST-Maghreb workshops this study is based on.

In addition to the fact that the former monopolists are to some extent stalling an actual liberaliza-tion of the power markets and dominate market structures these companies also have the advan-tage that they can attract international partnerships much more easily as they can (rightfully) advertise themselves to foreign consortia as gate openers to the domestic power markets. This is for instance reflected in the recent memorandum of understanding of STEG-ER with Dii. Furthermore, the former monopolists can often react quicker than private companies and thus capitalize on first-mover advantages and special state support as can be seen in the case of the state-sponsored effort to establish a domestic solar industry in Algeria with Rouiba Eclairage or the Tunisian project of establishing a solar panel factory in Bousalem in the Jendouba governorate by the company Energie Industrie.

Only very large and politically well-connected private companies such as Cevital (Algeria) or Nareva (Morocco) are able to counterbalance the weight of the utilities in a structural way. Of course, SMEs can often gain market advantages through a site- or technology-specific expertise or the filling of other niches in which larger companies do not operate. These companies have to develop more pointedly from a bottom-up-ap-proach, which might, in the mid term, be the key to regional success in the business in a scaled-up way.

Although it should not be forgotten that a true liberalization of power markets and industries has hardly ever been fully realized, the domestic private sector struggles under the dominance of few large companies that have been able to retain control over large areas of the domestic power market. A stronger regulatory regime favouring national (and international) competition is needed in all three Maghreb countries and would certainly create very positive externalities in terms of transparency, technology deployments and cost structure of projects.

28

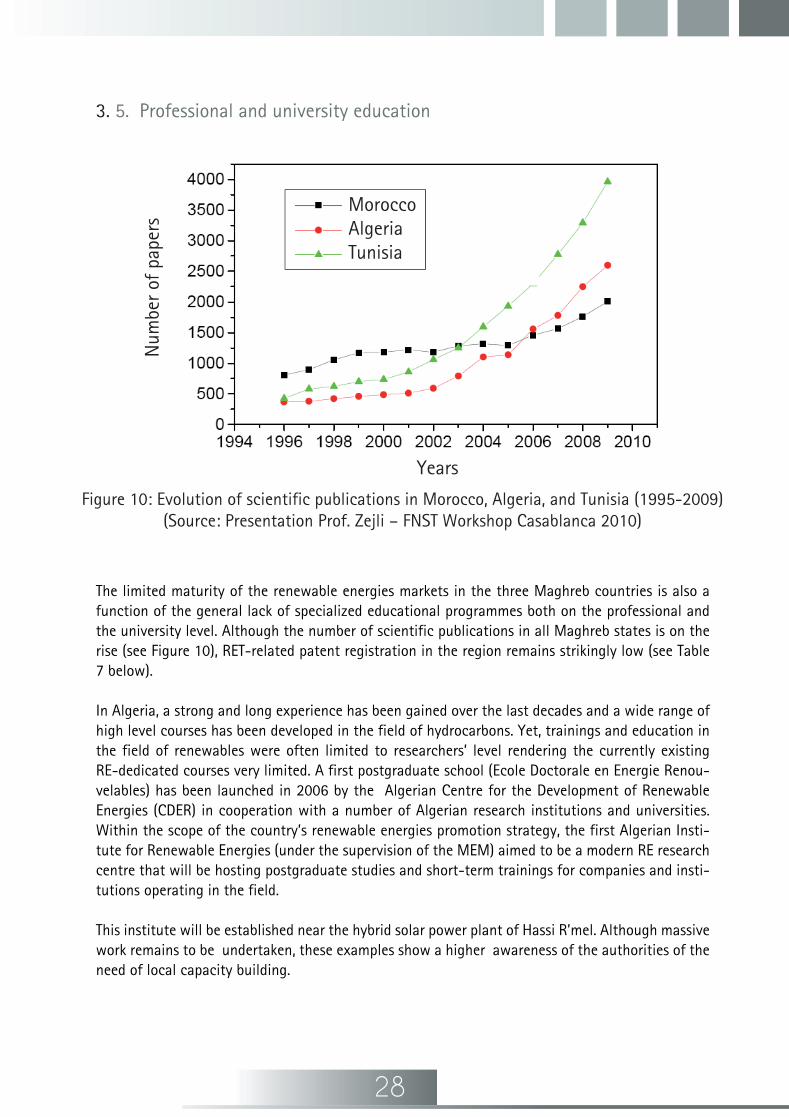

3. 5. Professional and university education

The limited maturity of the renewable energies markets in the three Maghreb countries is also a function of the general lack of specialized educational programmes both on the professional and the university level. Although the number of scientific publications in all Maghreb states is on the rise (see Figure 10), RET-related patent registration in the region remains strikingly low (see Table 7 below).

In Algeria, a strong and long experience has been gained over the last decades and a wide range of high level courses has been developed in the field of hydrocarbons. Yet, trainings and education in the field of renewables were often limited to researchers’ level rendering the currently existing RE-dedicated courses very limited. A first postgraduate school (Ecole Doctorale en Energie Renou-velables) has been launched in 2006 by the Algerian Centre for the Development of Renewable Energies (CDER) in cooperation with a number of Algerian research institutions and universities. Within the scope of the country’s renewable energies promotion strategy, the first Algerian Insti-tute for Renewable Energies (under the supervision of the MEM) aimed to be a modern RE research centre that will be hosting postgraduate studies and short-term trainings for companies and insti-tutions operating in the field.

This institute will be established near the hybrid solar power plant of Hassi R’mel. Although massive work remains to be undertaken, these examples show a higher awareness of the authorities of the need of local capacity building.

Figure 10: Evolution of scientific publications in Morocco, Algeria, and Tunisia (1995-2009)(Source: Presentation Prof. Zejli – FNST Workshop Casablanca 2010)

Num

ber o

f pap

ers

MoroccoAlgeriaTunisia

Years

29

With almost 30% of the state budget (about 7.5% of GDP) allocated to the education sector (including higher learning and professional training), Tunisia has become a regional frontrunner in educational policy, a sector that has undergone major reforms since the early 1990s. In addition to that, the country’s concerns related to the energy balance improvement has led the authorities from 2001 to take a number of short and medium term actions; awareness raising, information dissemi-nation, local capacities building, and research and development support in the field of RE & EE were among the top priorities. As a consequence, Tunisia has in place a conducive education support policy throughout which the courses needed for an RE expanding market can be developed.

However, the challenge today still consists of designing programmes that would be able to bring to market qualified and operational labour. The High Institute of Environmental Science and Techno-logy hosted by Borj-Cédria (see below) attempts to meet that objective by involving professionals in the educational programs development and implementation phases.

Within the Moroccan context, arguably, the long-term issue is less related to the dissemination of information than to capacity building: for sustainable growth, the country needs to rely on its own engineers and scientists with much less foreign-based consultancy and technical cooperation than there is today. A recent study however, maintains that in the field of fossil energy production, Morocco has a diversified set up of education and training institutions on all skill levels. Thus, the potential for the development of new programs and modules for RE and EE is there. As soon as the education and training infrastructure is getting clearer signals from the labour market, the existing institutions would be able to develop upgrading and new initial training programs for RE and EE – with international assistance.

Another important regional initiative is the newly founded Desertec University Network (DUN). Combining the scientific community that is interested in Desertec-related research DUN was foun-ded on the Tunisian Solar conference in October 2010. Headed by veteran Desertec supporter Mouldi Miled DUN could make an important contribution to the overall trans-regional renewable energy discourse, particularly due to its own international character with members from most Arab Mediterranean and key European states. DUN could also develop into a key enabler for businesses if it took in a decidedly local business perspective. This could be a real value added to this network that, should it choose to focus on academia exclusively, could run the danger of limiting itself to Ia purely academic audience during the power sector realizing renewable projects in the Maghreb.

Another result of the workshop’s debates on the integration of research and business is the recom-mendation for a strong government attention on the creation of local technology clusters. Equipped with research facilities, universities, and technology-oriented businesses these clusters can stand at the forefront of these efforts.

30

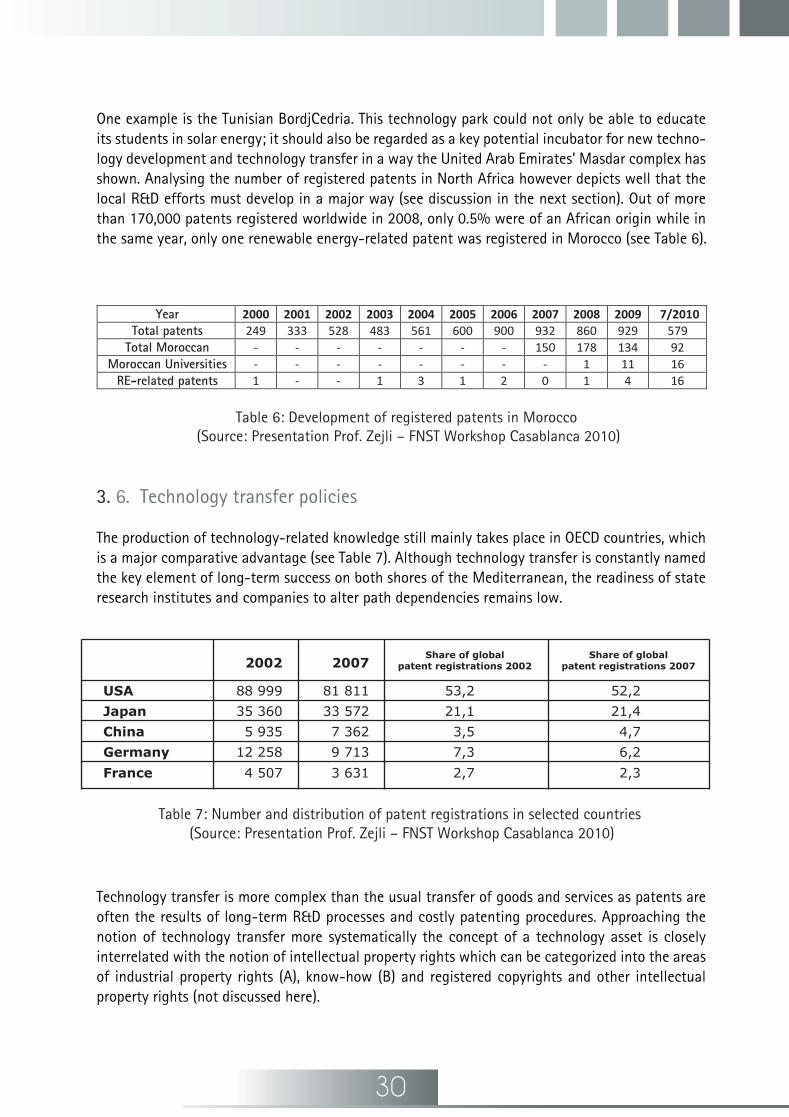

One example is the Tunisian BordjCedria. This technology park could not only be able to educate its students in solar energy; it should also be regarded as a key potential incubator for new techno-logy development and technology transfer in a way the United Arab Emirates’ Masdar complex has shown. Analysing the number of registered patents in North Africa however depicts well that the local R&D efforts must develop in a major way (see discussion in the next section). Out of more than 170,000 patents registered worldwide in 2008, only 0.5% were of an African origin while in the same year, only one renewable energy-related patent was registered in Morocco (see Table 6).

3. 6. Technology transfer policies

The production of technology-related knowledge still mainly takes place in OECD countries, which is a major comparative advantage (see Table 7). Although technology transfer is constantly named the key element of long-term success on both shores of the Mediterranean, the readiness of state research institutes and companies to alter path dependencies remains low.

Technology transfer is more complex than the usual transfer of goods and services as patents are often the results of long-term R&D processes and costly patenting procedures. Approaching the notion of technology transfer more systematically the concept of a technology asset is closely interrelated with the notion of intellectual property rights which can be categorized into the areas of industrial property rights (A), know-how (B) and registered copyrights and other intellectual property rights (not discussed here).

Year 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 -7/2010 Total patents 249 333 528 483 561 600 900 932 860 929 579

Total Moroccan - - - - - - - 150 178 134 92 Moroccan Universities - - - - - - - - 1 11 16

RE-related patents 1 - - 1 3 1 2 0 1 4 16

Table 6: Development of registered patents in Morocco (Source: Presentation Prof. Zejli – FNST Workshop Casablanca 2010)

Table 7: Number and distribution of patent registrations in selected countries (Source: Presentation Prof. Zejli – FNST Workshop Casablanca 2010)

2002 2007Share of global

patent registrations 2002Share of global

patent registrations 2007

USA 88 999 81 811 53,2 52,2

Japan 35 360 33 572 21,1 21,4

China 5 935 7 362 3,5 4,7

Germany 12 258 9 713 7,3 6,2

France 4 507 3 631 2,7 2,3

31

The definitions of these terms are those of the UN’s Asian and Pacific Centre for Transfer of Technology (APCTT)13. Applied to the Maghreb RE situation, elements of technology transfer, as well as know-how transfer on the level below that of a patent seem to be the key issues. Three points can be made here

1) As stated, multinationals will not be willing to forego income they could make through patents or long-term R&D advantages for political reasons. Either there is a striking market incen-tive for such companies to take this step (as in the case of China in other technology areas such as car manufacturing, high-speed trains or aerospace) or well-intentioned political claims will not lead far. The Maghreb however would have the potential to represent such a business incentive for large companies if major renewable energy plans in all three countries indeed go ahead. Particularly a Maghreb power sector speaking with one voice would have a strong negotiating position towards foreign companies; such a negotiation strategy would also have the advantage that companies could not play out one Maghreb state against the other.

2) Should that not be possible, the option of technology licensing or outsourcing in the form of subsidiary companies in the Maghreb seems a likely option which could be beneficial for Maghreb companies of any size.

3) In the long run however, only a strong and independent own regional technology innovation system can work against this trend. This will only be possible through increased public R&D expenses and a strong domestic industry sector (as most business-relevant patents are currently developed and registered through companies, not through public research institutes) that can build up its own experience with the respective technologies can innovate on its own and will thus attain a real technology ownership. Yet, it is evident that this can only be achieved in a mid- to long-term national (and regional) technology and industry policy.

13 Patents: A patent is a right given to the inventor when objects or methods, which did not exist before, are invented for the first time ever. An invention is an idea that enables the actual resolution of special problems in the technology field, and in line with its characteristics it is protected by the “invention patent”.