Structural Aspects of Competitiveness - Startseite6f34fd8e-6018-42b6-b360-744e567ca3a1/... · TIG2...

33

Wiener Institut für Internationale Wirtschaftsvergleiche The Vienna Institute for International Economic Studies www.wiiw.ac.at Structural Aspects of Competitiveness Julia Woerz Conference on European Economic Integration Vienna 2007

Transcript of Structural Aspects of Competitiveness - Startseite6f34fd8e-6018-42b6-b360-744e567ca3a1/... · TIG2...

Wiener Institut für Internationale Wirtschaftsvergleiche

The Vienna Institute forInternational EconomicStudies

www.wiiw.ac.at

Structural Aspects of Competitiveness

Julia Woerz

Conference on European Economic IntegrationVienna 2007

2

Outline

General remarks about competitiveness

Indicators of competitiveness

- Traditional

- Structural

- Location factors

Determinants of competitivenessConclusions

3

Definition of Competitiveness

Concept of competitiveness is not unambiguously defined in economics (Krugman 1994, Aiginger and Landesmann 2000, etc.)

Level of analysis

Firm level: well defined! = Ability to survive and strengthen your position vis-à-vis your competitors

All other levels: sectors, regions, countries: not well defined objectives of agents inside these entities may differ

4

Definition of Competitiveness

OECD (Hatzichronoglou 1996):

‘... the ability of companies, industries, regions, nations or supranational regions to generate, while being exposed to international competition, relatively high factor income and factor employment levels on a sustainable basis.’

EU: output growth and high rates of employment in a sustainable environment

5

Competitiveness

Ability to sell goods and services

Ability to grow

Ability to attract FDI

6

Indicators of CompetitivenessTraditional Indicators:- Trade balances - Market shares in export markets- Price and cost indicators

Structural Indicators:- Industry and product composition- Trade specialization- Quality indicators

Location factors:- Infrastructure, human capital- Business environment- Investor perceptions

7EU 15Advanced OECDNMS 10Russia

Turkey, Mexico1st Tigers2nd TigersChina, India

8

Global Convergence

05000

1000015000200002500030000350004000045000

EU15

EU12

advO

ECD

catc

hOEC

D

USA JP

N

RU

S

CH

N

IND

TIG

1

TIG

2

0.0

2.0

4.0

6.0

8.0

10.0

12.0GDP p.c. (USD) GDP (bio USD) GDP growth

9

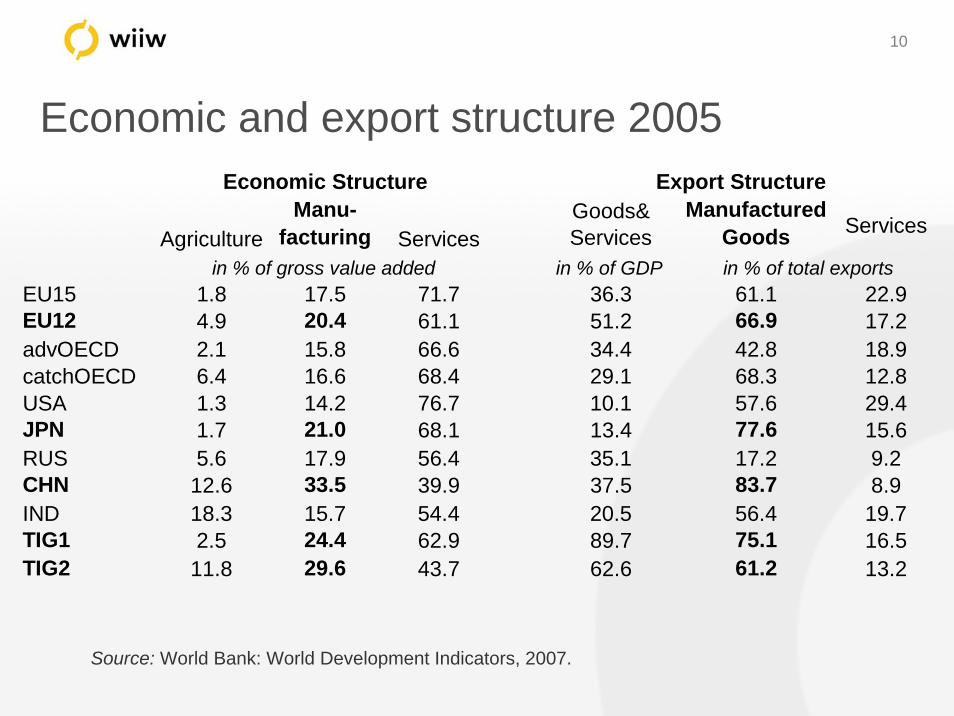

Economic and export structure 2005

Source: World Bank: World Development Indicators, 2007.

AgricultureManu-

facturing ServicesGoods& Services

Manufactured Goods Services

in % of GDPEU15 1.8 17.5 71.7 36.3 61.1 22.9EU12 4.9 20.4 61.1 51.2 66.9 17.2advOECD 2.1 15.8 66.6 34.4 42.8 18.9catchOECD 6.4 16.6 68.4 29.1 68.3 12.8USA 1.3 14.2 76.7 10.1 57.6 29.4JPN 1.7 21.0 68.1 13.4 77.6 15.6RUS 5.6 17.9 56.4 35.1 17.2 9.2CHN 12.6 33.5 39.9 37.5 83.7 8.9IND 18.3 15.7 54.4 20.5 56.4 19.7TIG1 2.5 24.4 62.9 89.7 75.1 16.5TIG2 11.8 29.6 43.7 62.6 61.2 13.2

in % of total exports

Export StructureEconomic Structure

in % of gross value added

10

Economic and export structure 2005

Source: World Bank: World Development Indicators, 2007.

AgricultureManu-

facturing ServicesGoods& Services

Manufactured Goods Services

in % of GDPEU15 1.8 17.5 71.7 36.3 61.1 22.9EU12 4.9 20.4 61.1 51.2 66.9 17.2advOECD 2.1 15.8 66.6 34.4 42.8 18.9catchOECD 6.4 16.6 68.4 29.1 68.3 12.8USA 1.3 14.2 76.7 10.1 57.6 29.4JPN 1.7 21.0 68.1 13.4 77.6 15.6RUS 5.6 17.9 56.4 35.1 17.2 9.2CHN 12.6 33.5 39.9 37.5 83.7 8.9IND 18.3 15.7 54.4 20.5 56.4 19.7TIG1 2.5 24.4 62.9 89.7 75.1 16.5TIG2 11.8 29.6 43.7 62.6 61.2 13.2

in % of total exports

Export StructureEconomic Structure

in % of gross value added

11

Economic and export structure 2005

Source: World Bank: World Development Indicators, 2007.

AgricultureManu-

facturing ServicesGoods& Services

Manufactured Goods Services

in % of GDPEU15 1.8 17.5 71.7 36.3 61.1 22.9EU12 4.9 20.4 61.1 51.2 66.9 17.2advOECD 2.1 15.8 66.6 34.4 42.8 18.9catchOECD 6.4 16.6 68.4 29.1 68.3 12.8USA 1.3 14.2 76.7 10.1 57.6 29.4JPN 1.7 21.0 68.1 13.4 77.6 15.6RUS 5.6 17.9 56.4 35.1 17.2 9.2CHN 12.6 33.5 39.9 37.5 83.7 8.9IND 18.3 15.7 54.4 20.5 56.4 19.7TIG1 2.5 24.4 62.9 89.7 75.1 16.5TIG2 11.8 29.6 43.7 62.6 61.2 13.2

Economic Structure Export Structure

in % of gross value added in % of total exports

12

Location Factors

13

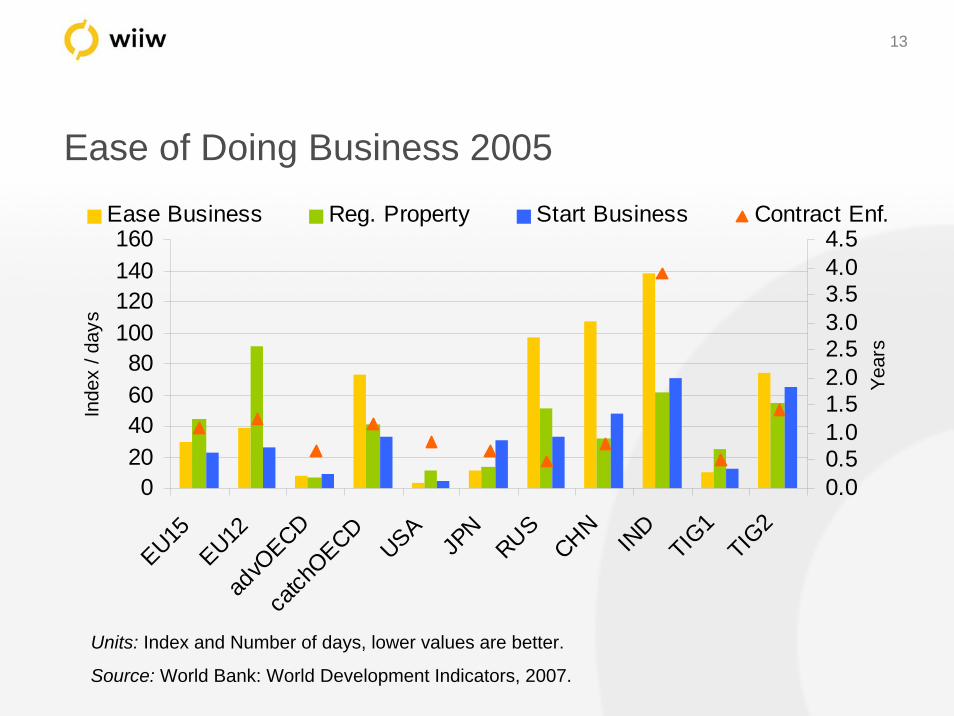

Ease of Doing Business 2005

Units: Index and Number of days, lower values are better.

Source: World Bank: World Development Indicators, 2007.

020406080

100120140160

EU15EU12

advO

ECDca

tchOECD

USA

JPN

RUSCHN

IND

TIG1

TIG2

Inde

x / d

ays

0.00.51.01.52.02.53.03.54.04.5

Year

s

Ease Business Reg. Property Start Business Contract Enf.

14

Major business constraints, Governance 2005

Units: per cent of managers perceiving this as constraint, lower values are better.

Source: World Bank: World Development Indicators, 2007.

05

101520253035

EU15

EU12ad

vOECD

catch

OECD

USA

JPN

RUS

CHN

IND

TIG1

TIG2

Corruption Courts Policy Uncertainty

15

Major business constraints, structural 2005

Units: per cent of managers perceiving this as constraint, lower values are better.

Source: World Bank: World Development Indicators, 2007.

05

10152025303540

EU15

EU12ad

vOECD

catch

OECD

USA

JPN

RUS

CHN

IND

TIG1

TIG2

Labour Skills Tax Rates

16

Structural Features: ICT & High Tech, 2005

Units: ICT Expenditure in % of GDP, HT Export in % of total exports

Source: World Bank: World Development Indicators, 2007.

05

1015202530354045

EU15

EU12ad

vOECD

catch

OECD

USA

JPN

RUS

CHN

IND

TIG1

TIG2

ICT expenditure HT Exports

17

Traditional & Structural Indicators

18

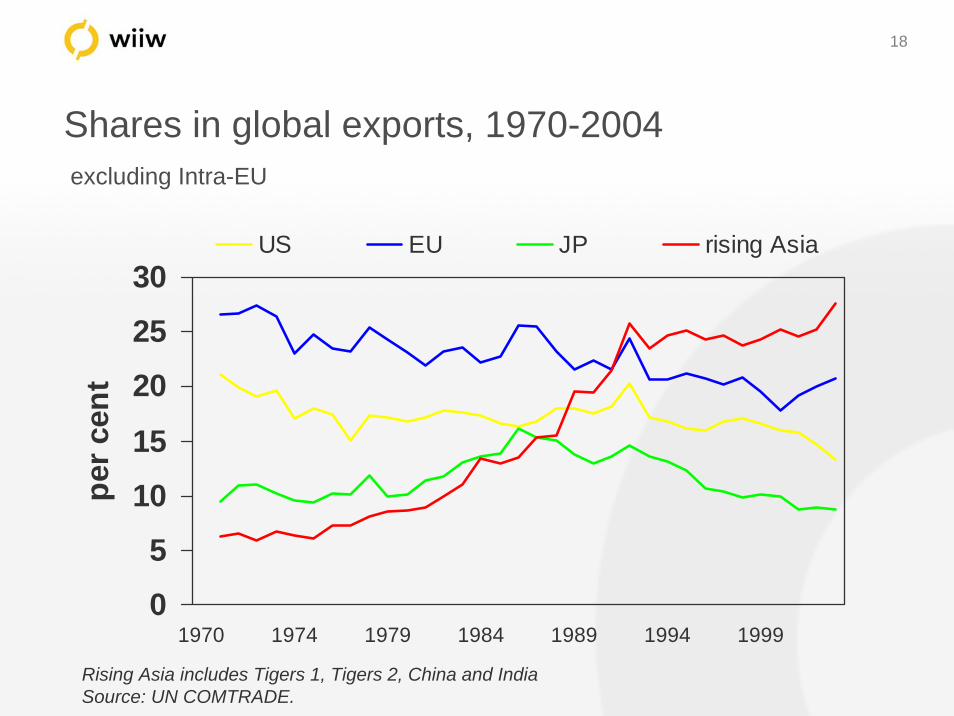

Shares in global exports, 1970-2004excluding Intra-EU

0

5

10

15

20

25

30

1970 1974 1979 1984 1989 1994 1999

per c

ent

US EU JP rising Asia

Rising Asia includes Tigers 1, Tigers 2, China and IndiaSource: UN COMTRADE.

19

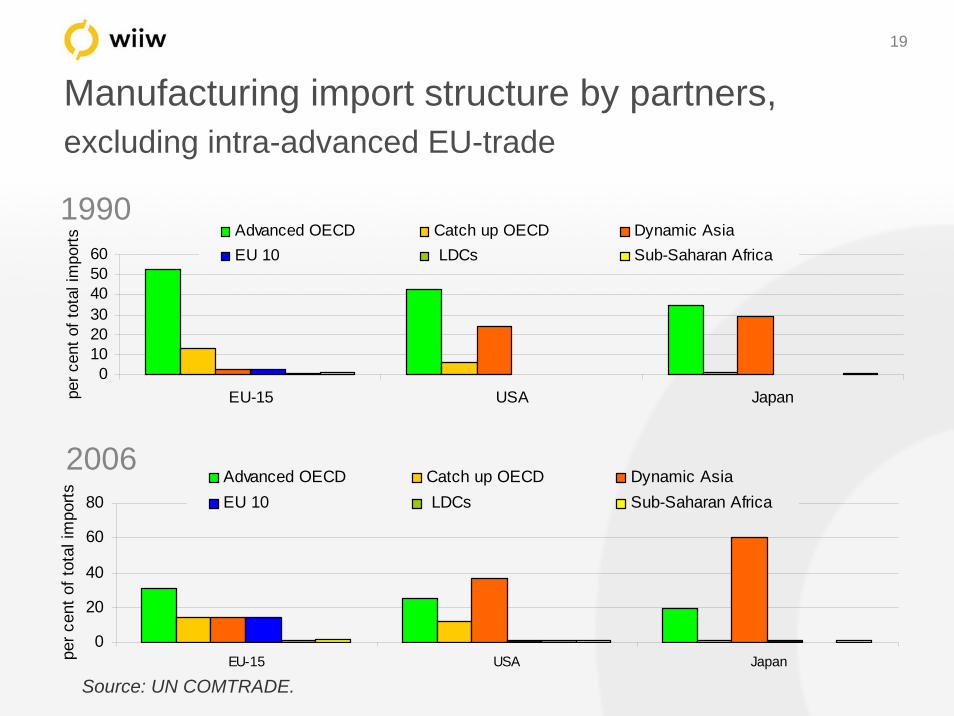

Manufacturing import structure by partners, excluding intra-advanced EU-trade

1990

2006

0102030405060

EU-15 USA Japanper c

ent o

f tot

al im

ports

Advanced OECD Catch up OECD Dynamic AsiaEU 10 LDCs Sub-Saharan Africa

0

20

40

60

80

EU-15 USA Japanper c

ent o

f tot

al im

ports

Advanced OECD Catch up OECD Dynamic AsiaEU 10 LDCs Sub-Saharan Africa

Source: UN COMTRADE.

20

Shares of CHINA in imports of EU-North, USA and Japan (%)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

1 2 3 4 5 1 2 3 4 5 1 2 3 4 5

1990 1995 2000 2005

42.7 5545.3

EU-North USA Japan

technology: 1: low tech industries, 2: medium-low industries, 3: medium-high industries, 4: high industries, 5: office machinery and computers, Source: wiiw

21

Shares of EU10, Cohesion and Tigers 1 in imports of EU-North, USA and Japan (%)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

1 2 3 4 5 1 2 3 4 5 1 2 3 4 5

1990 1995 2000 2005EU-North USA JAPAN

technology: 1: low tech industries, 2: medium-low industries, 3: medium-high industries, 4: high techindustries, 5: office machinery and computers; Source: wiiw

22

Global Trade in Goods, 2005Billion USD

Importer

Exporter

EU 2

5

Oth

er E

urop

e

Rus

sia

Oth

er C

IS

Uni

ted

Stat

es

Can

ada

Latin

Am

eric

a

Japa

n

Chi

na

Oth

er A

sia

AUS&

NZL

Mid

dle

East

Afric

a

EU 25

Other Europe

Russia

Other CIS

United States

Canada

Latin America

Japan

China

Other Asia

AUS&NZL

Middle East

Africa400-500

300-400

200-300

100-200

0-100

23

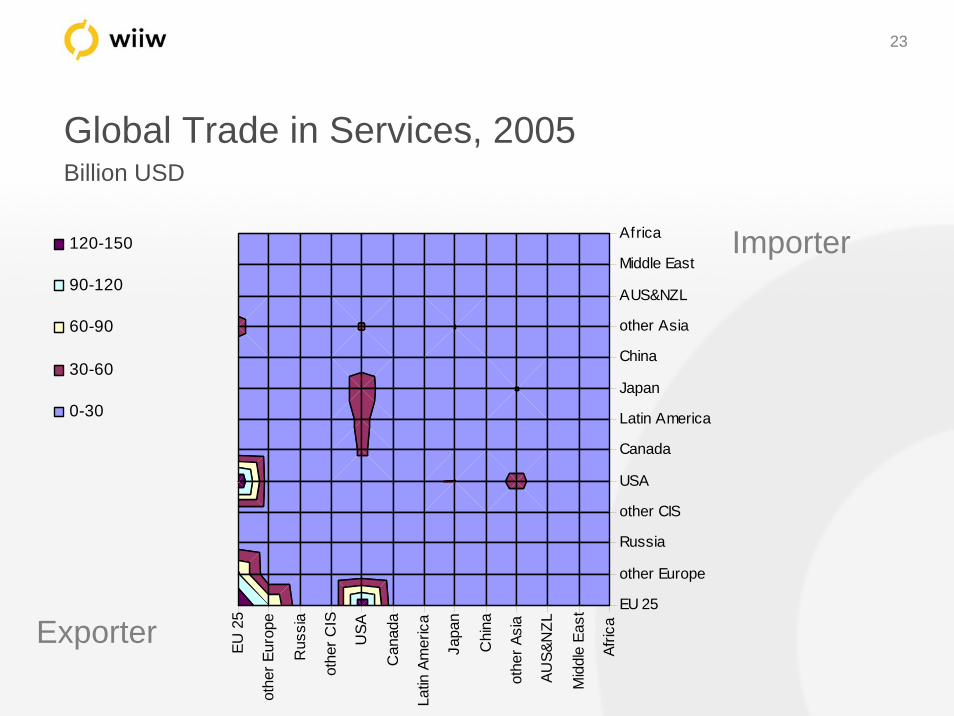

Global Trade in Services, 2005Billion USD

EU 2

5

othe

r Eur

ope

Rus

sia

othe

r CIS

USA

Can

ada

Latin

Am

eric

a

Japa

n

Chi

na

othe

r Asi

a

AUS&

NZL

Mid

dle

East

Afric

aEU 25

other Europe

Russia

other CIS

USA

Canada

Latin America

Japan

China

other Asia

AUS&NZL

Middle East

Africa120-150

90-120

60-90

30-60

0-30

Importer

Exporter

24

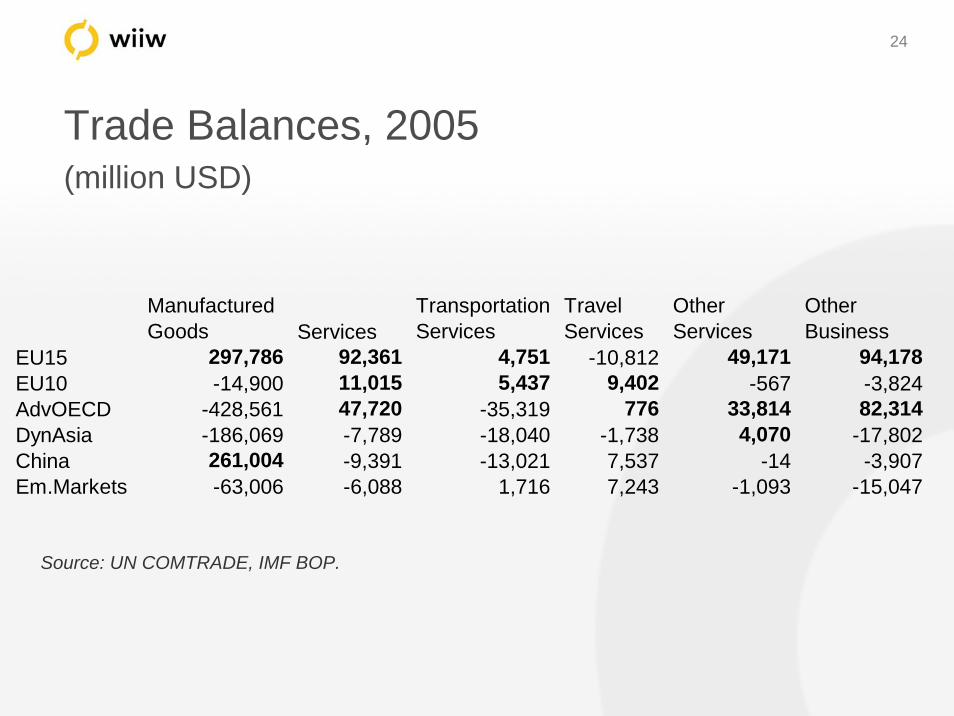

Trade Balances, 2005(million USD)

Source: UN COMTRADE, IMF BOP.

Manufactured Goods Services

Transportation Services

Travel Services

Other Services

Other Business

EU15 297,786 92,361 4,751 -10,812 49,171 94,178EU10 -14,900 11,015 5,437 9,402 -567 -3,824 AdvOECD -428,561 47,720 -35,319 776 33,814 82,314DynAsia -186,069 -7,789 -18,040 -1,738 4,070 -17,802 China 261,004 -9,391 -13,021 7,537 -14 -3,907 Em.Markets -63,006 -6,088 1,716 7,243 -1,093 -15,047

25

Market Shares, 1995 and 2005

Goods

Services

Source: UN COMTRADE, IMF BOP.

0.00

0.10

0.20

0.30

0.40

0.50

EU15 EU10 AdvOECD DynAsia CHN EmergingMarkets

1995 2005

0.00

0.10

0.20

0.30

0.40

0.50

EU15 EU10 AdvOECD DynAsia CHN EmergingMarkets

1995 2005

26

Revealed Comparative Advantages in Services, 2005

Source: IMF BOP, wiiw calculations.

Transportation Services

Travel Services Other Services

Other Business

EU15 0.12 -0.17 -0.15 0.04EU10 0.41 0.30 -0.89 -0.33 AdvOECD -0.11 -0.12 0.35 0.15DynAsia -0.07 -0.04 0.16 -0.18 China -0.34 0.45 -0.03 -0.04 Em.Markets 0.36 0.46 -0.69 -0.43

27

Determinants of service sector competitivenessin EU10

kit

ki

kit

kit

kit

kit

kit

kit

SkillsOpen

SizeULCLPRCA

εγββ

βββα

++++

++++=

54

321

LP … labour productivity growth in euro

ULC … unit labour costs

Size … size of an industry in terms of employment

Open … openness of the respective industry

Skill … skill intensity of the industry

t … time (year), k … countries, i …service items

28

Determinants of service sector competitivenessin EU15 (1) (2) (3)

Labour Productiv 0.038 0.014 0.0960.38 0.14 0.87

Unit Labour Costs 0.206 *** 0.192 *** 0.203 ***2.95 2.83 2.91

Size of industry -0.151 *** -0.115 *** -0.090 ***-4.17 -3.2 -2.41

Openness 0.280 *** 0.335 *** 0.335 *** 10.78 11.96 11.15Sector dummies:Communication 1.009 *** 1.037 ***

4.38 4.4Construction 1.033 *** 1.064 ***

4.48 4.54Insurance 0.552 *** 0.680 *** 2.28 2.63Computer&Information 0.521 *** 0.587 *** 2.26 2.29tertiary education share 0.011

0.3white collar, high skill workers share 0.033 1.17overall R2 0.11 0.30 0.34Observations 782 782 720Obs. per group 91 91 91

29

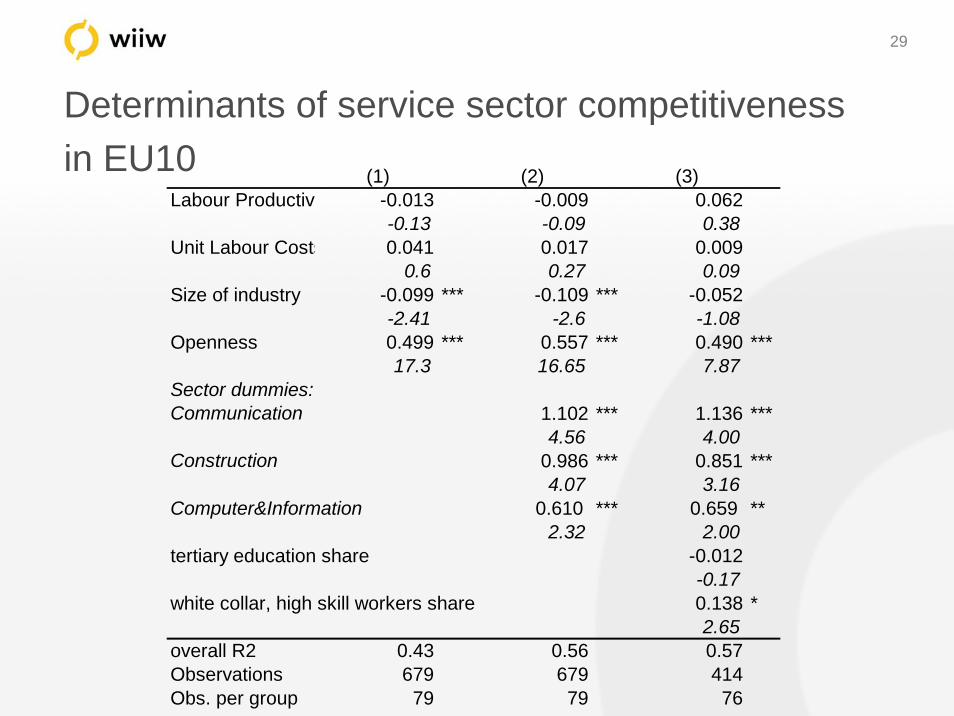

Determinants of service sector competitivenessin EU10 (1) (2) (3)

Labour Productiv -0.013 -0.009 0.062-0.13 -0.09 0.38

Unit Labour Costs 0.041 0.017 0.0090.6 0.27 0.09

Size of industry -0.099 *** -0.109 *** -0.052-2.41 -2.6 -1.08

Openness 0.499 *** 0.557 *** 0.490 ***17.3 16.65 7.87

Sector dummies:Communication 1.102 *** 1.136 ***

4.56 4.00Construction 0.986 *** 0.851 ***

4.07 3.16Computer&Information 0.610 *** 0.659 **

2.32 2.00tertiary education share -0.012

-0.17white collar, high skill workers share 0.138 *

2.65overall R2 0.43 0.56 0.57Observations 679 679 414Obs. per group 79 79 76

30

Conclusions

The world has changed dramatically over the past decadesAsia’s share in world merchandise trade has risen strongly Trade in services concentrated predominantly in EU The most export oriented countries still show a relative dominance of the manufacturing sector

31

What determines competitiveness?

Mostly structural featuresLess so locational / soft factorsAsia (China + Tigers 2) and EU10 show good structural characteristics, high competitiveness in manufacturing despite low rankings in business environmentThey also show a good performance in low- and high tech industries

32

What determines competitiveness?

Determinants differ between competitiveness in goods versus servicesCost factors (unit labour costs and labour productivity) play a stronger role for goodsFor services, soft factors appear to be more important, also general export orientation matters stronglySome service sectors are more competitive than others: communication, construction, computer&information services.

Wiener Institut für Internationale Wirtschaftsvergleiche

The Vienna Institute forInternational EconomicStudies

www.wiiw.ac.at

Structural Aspects of Competitiveness

Julia Woerz

Conference on European Economic IntegrationVienna 2007