Strengthening You Organization a Series of Modules and Reference Materials for NGO and CBO Managers...

51

Series 2 ORGANIZATIONAL MANAGEMENT Module Financial Management 3 3 Financial Management • •STRUCTURE • Management Information Systems • SUSTAINABLE DEVELOPMENT • Impact • Assessment • Career Development • Strategic Planning • SYSTEMS • Supervision • Objectives • Program Series 2 MODULE 2/

-

Upload

darwin-manalo-etang -

Category

Documents

-

view

231 -

download

2

description

ss

Transcript of Strengthening You Organization a Series of Modules and Reference Materials for NGO and CBO Managers...

Series 2ORGANIZATIONAL

MANAGEMENT

Modu leFinancialManagement

33

FinancialManagement ••STRUCTURE •ManagementInformation Systems •SUSTAINABLEDEVELOPMENT •Impact • Assessment• Career Development •Strategic Planning •SYSTEMS • Supervision •Objectives • Program

Series 2

MO

DU

LE

2 /

x

Financial Management

Introduction 1Before you Begin 2Budgets and blueprints for your organization 3Characteristics of good budgets 3Step by step: Preparing a budget 4Tips and tools: Some standard budget categories 6Monitoring your budget 8Variances 11Vexing financial management issues 11

❐ Travel expenses❐ Petty cash❐ Income generation❐ Procurement❐ Inventories

Instituting effective financial controls 16❐ Accounting controls❐ Segregation of duties❐ Managerial supervision

Figures, Tables, and Exercises

Figure 1: Financial management cycle 1Exercise A: Using a format to facilitate budget monitoring 9Exercise B: Identifying the types of costs your organization incurs 10

Annexes

Annex A: Model budget formatsAnnex B: Travel authorization and expense report formatsAnnex C: Petty Cash vouchers and ledgersAnnex D: Cash collection and contraceptive receipt/distribution formatsAnnex E: Requisition forms and local purchase ordersAnnex F: Internal questionnaires and checklistsAnnex G: Model financial reports

1

For many managers, financial management is a mystery best left to those who toil with dustyledgers, sharp pencils, even sharper eyesight, and the word “No” to many seemingly “simple”requests omnipresent in their conversations. While it is true that every organization needsstrong financial management – and dedicated staff to provide it – effective managers mustknow basic information about, and have basic skills for, monitoring the fiscal health of theirorganization and each of its programs. This module will not make every manager a financialexpert. This module will enable managers to:

☛ Review financial documents (budgets, reports, forecasts, procurement requests, incomeand expenditure statements) with comprehension.

☛ Understand budget preparation and monitoring.☛ Recognize the importance of implementing sound financial controls.☛ Monitor the impact of changing program plans on resource requirements and

communicate effectively with financial staff.☛ Use financial data and information for decision-making.☛ Calculate realistic funding needs and identify appropriate sources.☛ Minimize risks of financial difficulties for the organization.

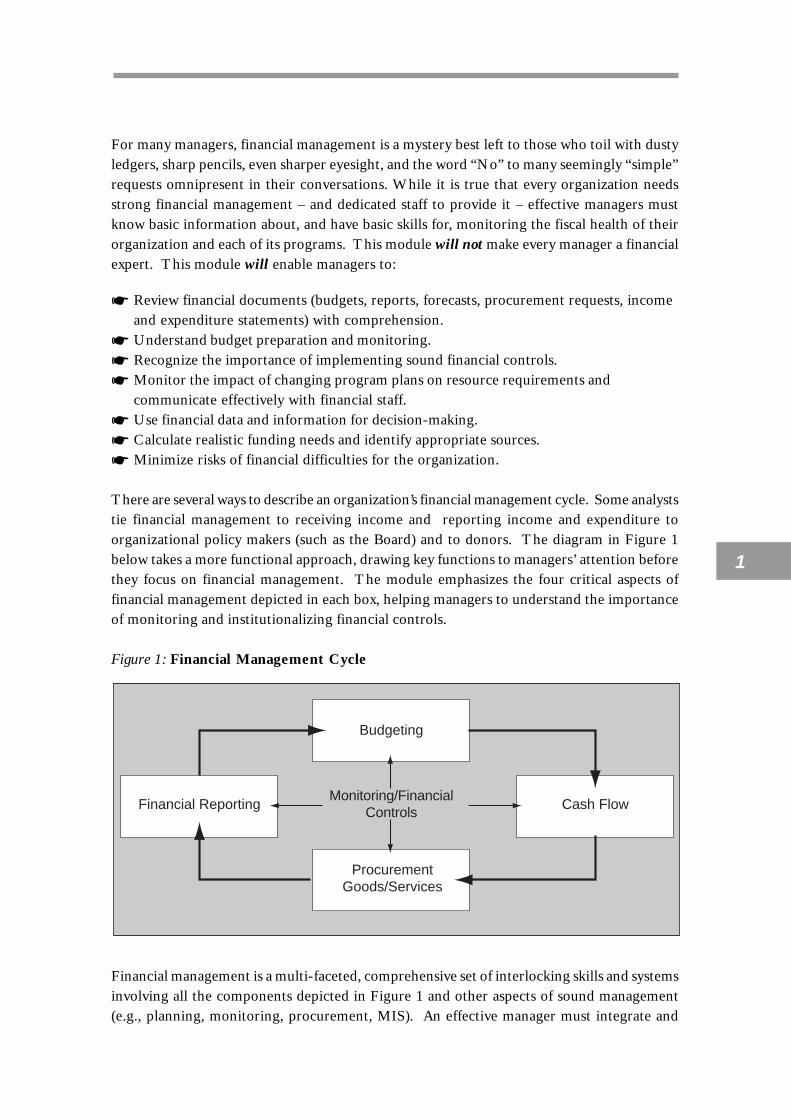

There are several ways to describe an organization’s financial management cycle. Some analyststie financial management to receiving income and reporting income and expenditure toorganizational policy makers (such as the Board) and to donors. The diagram in Figure 1below takes a more functional approach, drawing key functions to managers’ attention beforethey focus on financial management. The module emphasizes the four critical aspects offinancial management depicted in each box, helping managers to understand the importanceof monitoring and institutionalizing financial controls.

Figure 1: Financial Management Cycle

Monitoring/Financial Controls

Financial management is a multi-faceted, comprehensive set of interlocking skills and systemsinvolving all the components depicted in Figure 1 and other aspects of sound management(e.g., planning, monitoring, procurement, MIS). An effective manager must integrate and

Budgeting

Monitoring/FinancialControls

ProcurementGoods/Services

Cash FlowFinancial Reporting

2

carefully monitor these aspects of an organization’s operations, balancing competing processesand concerns to ensure that the organization has adequate resources at all times.

Clearly, financial management goes beyond traditional bookkeeping and accounting.Financial management is about analyzing financial performance, identifying waysto use resources efficiently, and finding creative means to use resources in order togenerate additional resources. Financial management activities include:1

✔ Matching available resources to planned activities.✔ Ensuring effective teamwork, interdependent activities and systems, and good

communication or information flow between financial and program staff.✔ Monitoring the efficiency of resource use.✔ Identifying ways to reduce and recover costs.✔ Developing, monitoring, updating, and reporting on operational budgets.✔ Finding ways to finance new initiatives.✔ Tracking resource use trends in order to determine future budget requirements, project

cash needs, and forecast financial growth.✔ Developing long-term financial plans to meet future resource needs.✔ Managing and investing future resources to make them profitable.✔ Controlling and attempting to prevent major financial risks.

Before You Begin…Some Questions for Managers. Tickyour responses to gather clues about priorities forimprovement.

❐ Do you have a financial system that providesadequate information about yourorganization’s income and expenditures on anas-needed basis? Are you collecting data youtruly need or it is excessive?

❐ Are your financial reports accurate, clear,complete, timely, and coordinated with yourprogrammatic reports?

❐ Do you have an integrated organizationalbudget that reflects income and expendituresfrom all sources?

❐ Do you regularly review and update yourbudget?

❐ Can your accounting system monitor costcenters and segregate costs (includingdetermining cost per unit)?

❐ Are you able to project and forecast resourceneeds or shortfalls before they occur?

1 Adapted from FPMD. The Manager Series. “Understanding and Using Financial Management Systems toMake Decisions,” Winter 1999 /2000, Volume VIII, Number 4. Boston, MA.

3

❐ Do you bring your financial and program staff together when preparing proposals ordesigning new initiatives and for regular consultations or operational plan reviews?

❐ Can the same person request, approve, and sign a check for goods or services?❐ Does your organization have annual audits by a professional outside accounting firm?❐ Do you monitor or review all systems involved in financial management on a regular basis?❐ Have you linked your financial management system to monitoring indicators and to

your organization’s strategic plan?❐ Do you have a handbook or written policies that explain procedures and formats for

routine financial transactions (e.g., accounting for travel or imprest funds, petty cash,requisitions or procurement, grants disbursements) to all staff? Do you regularly reviewand provide training regarding these policies?

If the answer to any of these questions is No, you and your management team need to reviewfinancial management policies and procedures in great detail and develop plans to improveand strengthen them.

Budgets as Blueprints for Your Organization

Your organization’s budget is perhaps the most basic tool for sound financial management. Abudget encompasses several related financial management issues: specific costs for activitiesor staff members; a plan of action for making expenditures; the number and kinds of humanresources required to implement the program, and, implicitly, the amount of money neededto support an organization as it seeks to achieve its goals and objectives. Annex A containstwo types of budgets: a budget allocating specific costs to budget categories and line items,and a cash flow budget.

Every good manager should institutionalize a rigorous budget monitoring and review process,usually involving monthly income and expenditure reports (See an example in Annex G) orspreadsheets. These reports can serve as a basis for quarterly or other reports required byBoards and Directors or donors. The best managers also ensure that financial and programstaff meet together regularly and provide inputs that help a manager make appropriate decisionsabout revising budgets, seeking increased revenues, or reallocating resources.

Characteristics of GoodBudgets2

A budget is a dynamic tool. It should reflectmanagement decisions regarding allocation ofresources, However, since a budget must beviewed in the context of an organization’sinternal and external environments, it shouldbe altered according to changes in thoseenvironments. Budgets and reports are usedby managers to review projected costs againstactual costs, to forecast cash needs, and even

2Adapted from The Manager, Winter 1999/2000 op. cit.

4

as a marketing tool to leverage funds to ensure coverage of all expenses. The following arecharacteristics of a good budget:

✔ Budgets cover a defined set of activities. This means that every separate project orprogram should have its own budget. It is important, however, for program managersto combine all separate budgets into an organization-wide operations budget, and theadvent of computers makes this a relatively simple action. Monitoring the entireorganization’s fiscal health pays dividends because it allows a manager to determineopportunities for becoming more cost-effective, to estimate cash flow more efficiently,to use excess funds in one area to subsidize another under-funded area, and to predictwhere additional resources may be needed.

✔ Budgets state the time period covered. It is advisable for managers to prepare annualbudgets, and to prepare them in tandem with annual work or operations plans.However, from time to time, dividing the budget into months or quarters may facilitatemonitoring.

✔ Budgets are realistic about expected revenues and expected costs. A budgetshould be based on prudent cost estimates. Too often, managers under- or over-estimate the costs of particular line items or budget categories. Consequently, someorganizations experience cash shortfalls or improper allocation of resources thatdemoralize staff and compromise program implementation. Ask financial staff to seekpro-forma invoices or cost estimates for major expenses (vehicles, computers, clinicequipment, etc.) and recurring costs (office stationery, telephone and bank charges, staffsalaries, etc.) your office is likely to incur annually. This is one way to ensure goodcosting as a basis for preparing a budget.

✔ Budgets include indirect costs. One of managers’ most frequent problems withbudgeting is that they only capture direct costs such as salaries, rent, supplies, andequipment. Yet, there are many indirect costs that influence how well an organizationor a program operates. Fringe benefits – e.g., leave, pensions, insurance – andoverhead (e.g., administration, services shared among various programs such asphotocopying, telephones). Even the costs of financial management and administration(which cover several programs or functions simultaneously) are the two most commonkinds of indirect costs. They are often hard to estimate, However, as an organization’smanagement structure becomes more complex, it is often advisable to hire a publicaccounting firm to calculate an appropriate overhead rate. This rate can be applied as apercentage of the entire budget, and is especially useful when preparing or negotiatingbudgets with donors who may also not have considered some important indirect costsrequired for supporting an effective program.

Step by Step: Preparing a Budget

Budgeting needs to be as precise as possible. This means that a manager and his or her teamshould have all available information about the program, unit, or activity to be budgeted.When preparing a budget, some key assumptions are always made. For example, financialmanagers may assume that costs will remain relatively static during the period covered by thebudget. Or it may be assumed that the funds available are adequate for program ororganizational needs. Or planners may develop a budget and recognize that they must raise

5

adequate funds before implementation. These scenarios fall under two basic budgetingtechniques: zero-based budgeting (creation of an “ideal” budget before allocating availablefunds) and allocation budgeting (basing the budget on funds already allocated).

STEP 1: Always begin by reviewing your plans – strategic, work, and operational. Theseplans will tell you what activities are scheduled, what resources (human, financial, andmaterial) are needed, and when they must be available. Your budget and your formalplans must be absolutely synchronized. That is, no activity or staff should appear in thework plan that does not appear in the budget, and vice versa.

STEP 2: Always have up-to-date cost figures. For example, have your organization’sAdministrator or Human Resource Manager provide current salary and fringe benefitsfor all full- and part-time staff. If you are planning major purchases, get three pro-formainvoices from suppliers and select the one in which you have the most confidence. (Thisis not always the lowest invoice; some suppliers are unreliable or have hidden costs likeshipping. Use your best judgement.) Ask your financial staff to conduct a “mini” auditof administrative costs over the last year; assume that they will increase byapproximately 10-20%. Review what is happening to local currency. Is it losing orgaining value? Since most donors expect local budgets to be in local currency, it may beprudent to prepare your budget in a convertible currency (e.g., pounds sterling, dollars,Deutsche marks, yen, French francs). Then apply a conversion rate you think is rationaland reflects currency inflation or deflation based on your experience over the last yearor two. This is one way of avoiding shortfalls due to currency fluctuations.

STEP 3: Always express your budget clearly so that anyone who is reading or workingwith it understands what you are trying to fund or achieve. Calculate line items in thefollowing ways:

☛ For salaries and fringe benefits, calculate the line item 3 this way:N20,000/month x 12 months plus 15% of the total salary as employer paymentstowards pension as a fringe benefit: N20,000/month x 12 months x 0.15.

☛ For supervisory visits or travel for regularly scheduled meetings:Travel: N8,000 x 4 trips (1 trip/quarter)Per diem: N4,000/day x 3 days/trip x 4 trips

☛ For recurring administrative expenses: Bank charges: N1,000/monthx 12 months x 2 accounts

☛ For education and training, don’t forget to calculate each line item basedon the number of participants except for meeting rooms, resource persons,and equipment rental:

❐ Travel and per diem: N2,500 travel allowance x 50 participantsPer diem: N 500/day for dinner and incidentals4

❐ Materials: N1,000 x 50 participants❐ Hotel (bed and breakfast): N4,000 x 50 participants x 6 days5

2Adapted from The Manager, Winter 1999/2000 op. cit.3 For the purpose of this section, the currency being used is the Nigerian Nira. It is connoted by an “N.”4Often, at workshops, conference venues offer bed and breakfast, and lunch and teas are served to participants.Remember these possibilities when you are budgeting.5 Often, conference planners want participants to arrive early to attend the start of the conference, workshop, ortraining. Always factor this indicating, for example, six days instead of five.

6

☛ For purchased services (e.g., vehicle maintenance, audits, printing,construction if your organization is renovating), examine the contract anddetermine expected levels of service. For example, if your photocopier hasa contract, you can choose to make the line item an annual figure or breakit down into monthly costs through dividing it by “12”. Sometimes monthlytotals are easier to monitor and evaluate.

STEP 4: Always make sure your math is correct. Now, with computerized spreadsheets,there are virtually no excuses for mathematical errors. Even if you are preparing yourbudget manually, make sure that one or two people – especially from your finance staff –review the budget for mathematical accuracy. Remember some of the “hidden” costs,especially overhead or indirect costs. Apply them to the budget as a separate line itemafter all costs and categories have been calculated to ensure that you apply the indirectcost rate to all your organization’s administration and activities.

STEP 5: Always follow the guidelines or formats provided by donors. Nothing can bemore disruptive – or perhaps disqualify your organization from receiving support – thanchoosing your own “approach” to budgeting. Donors often design their formats toprovide crosscutting information about all of the organizations they support.Therefore, if you are not following the format, you may not be entered into theirmanagement information or monitoring systems. A good manager is able to interprethis or her normal financial management or budgeting categories in line with those ofdonors.

Below, coverage or contents of some standard budget categories are suggested but youmust conform to donor guidelines in order to raise funds. For successful organizationswith multiple donors, it may be useful to have a donors coordination meeting. There,donors, management, and staff can discuss harmonizing some of the varying donorrequirements to reduce the burdens caused by complying with multiple, and varying,formats, requirements, and stipulations. Many donors appreciate this pro-activeinitiative.

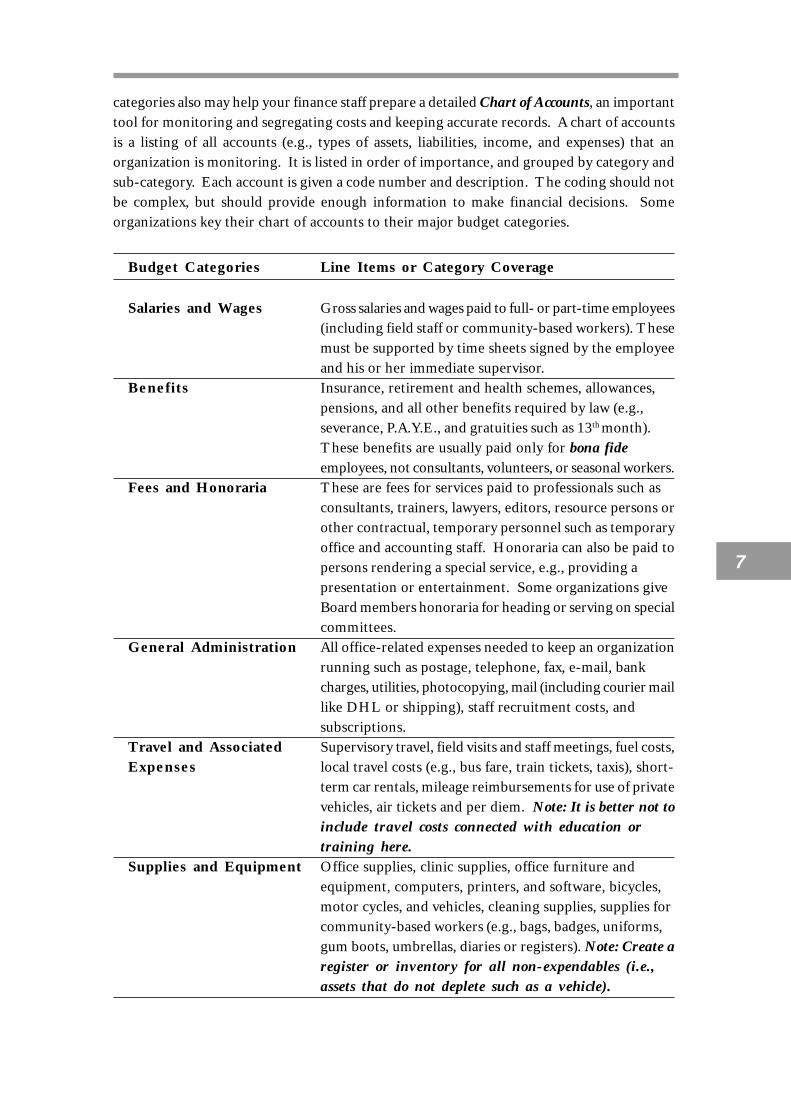

Tips and Tools…Some Standard Budget Categories

Although it may seem redundantbecause donor requirements oftenappear to be paramount, it is helpfulfor an effective manager to befamiliar with budget categories andtheir corresponding activities or lineitems. The following are somesuggested budget categories thatcan – and should – be modified basedon your type of organization andprograms. You may also find thatthere are several additional routine

or recurring items that should appear under each category. You should discuss, with yourprogram and financial staff sitting together as a team, what line items you might add . These

7

categories also may help your finance staff prepare a detailed Chart of Accounts, an importanttool for monitoring and segregating costs and keeping accurate records. A chart of accountsis a listing of all accounts (e.g., types of assets, liabilities, income, and expenses) that anorganization is monitoring. It is listed in order of importance, and grouped by category andsub-category. Each account is given a code number and description. The coding should notbe complex, but should provide enough information to make financial decisions. Someorganizations key their chart of accounts to their major budget categories.

Budget Categories Line Items or Category Coverage

Salaries and Wages Gross salaries and wages paid to full- or part-time employees(including field staff or community-based workers). Thesemust be supported by time sheets signed by the employeeand his or her immediate supervisor.

Benefits Insurance, retirement and health schemes, allowances,pensions, and all other benefits required by law (e.g.,severance, P.A.Y.E., and gratuities such as 13th month).These benefits are usually paid only for bona fideemployees, not consultants, volunteers, or seasonal workers.

Fees and Honoraria These are fees for services paid to professionals such asconsultants, trainers, lawyers, editors, resource persons orother contractual, temporary personnel such as temporaryoffice and accounting staff. Honoraria can also be paid topersons rendering a special service, e.g., providing apresentation or entertainment. Some organizations giveBoard members honoraria for heading or serving on specialcommittees.

General Administration All office-related expenses needed to keep an organizationrunning such as postage, telephone, fax, e-mail, bankcharges, utilities, photocopying, mail (including courier maillike DHL or shipping), staff recruitment costs, andsubscriptions.

Travel and Associated Supervisory travel, field visits and staff meetings, fuel costs,Expenses local travel costs (e.g., bus fare, train tickets, taxis), short-

term car rentals, mileage reimbursements for use of privatevehicles, air tickets and per diem. Note: It is better not toinclude travel costs connected with education ortraining here.

Supplies and Equipment Office supplies, clinic supplies, office furniture andequipment, computers, printers, and software, bicycles,motor cycles, and vehicles, cleaning supplies, supplies forcommunity-based workers (e.g., bags, badges, uniforms,gum boots, umbrellas, diaries or registers). Note: Create aregister or inventory for all non-expendables (i.e.,assets that do not deplete such as a vehicle).

8

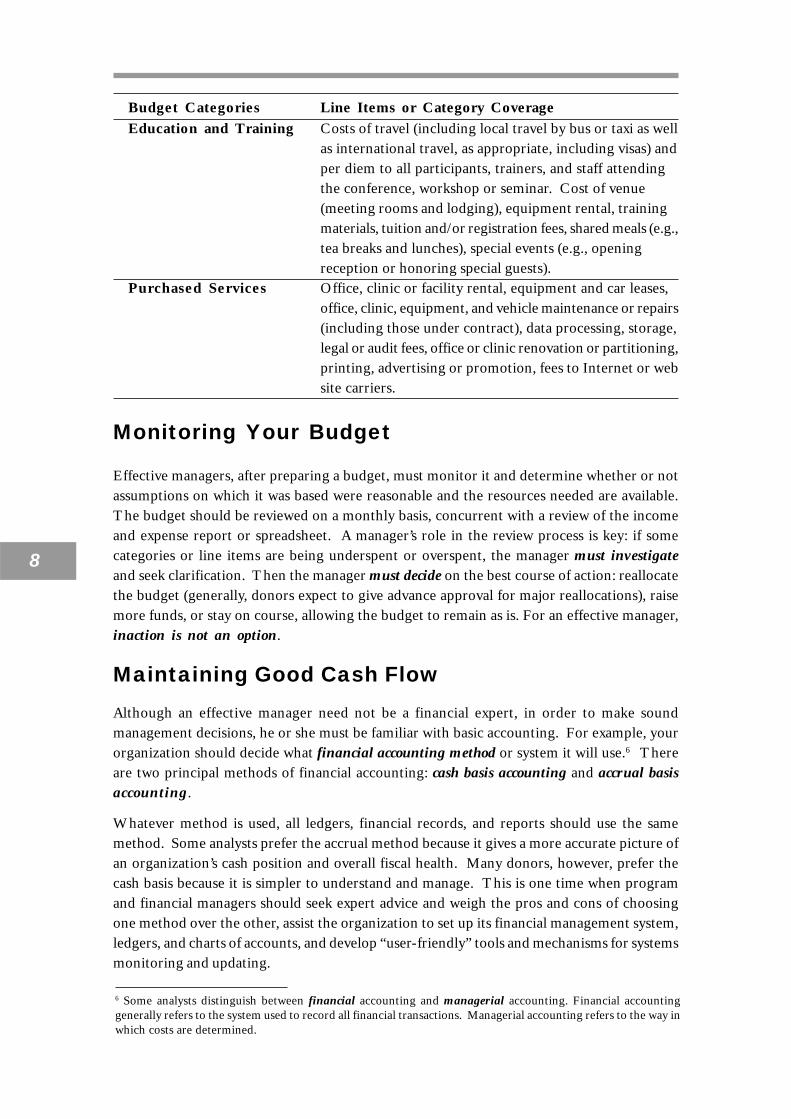

Budget Categories Line Items or Category CoverageEducation and Training Costs of travel (including local travel by bus or taxi as well

as international travel, as appropriate, including visas) andper diem to all participants, trainers, and staff attendingthe conference, workshop or seminar. Cost of venue(meeting rooms and lodging), equipment rental, trainingmaterials, tuition and/or registration fees, shared meals (e.g.,tea breaks and lunches), special events (e.g., openingreception or honoring special guests).

Purchased Services Office, clinic or facility rental, equipment and car leases,office, clinic, equipment, and vehicle maintenance or repairs(including those under contract), data processing, storage,legal or audit fees, office or clinic renovation or partitioning,printing, advertising or promotion, fees to Internet or website carriers.

Monitoring Your Budget

Effective managers, after preparing a budget, must monitor it and determine whether or notassumptions on which it was based were reasonable and the resources needed are available.The budget should be reviewed on a monthly basis, concurrent with a review of the incomeand expense report or spreadsheet. A manager’s role in the review process is key: if somecategories or line items are being underspent or overspent, the manager must investigateand seek clarification. Then the manager must decide on the best course of action: reallocatethe budget (generally, donors expect to give advance approval for major reallocations), raisemore funds, or stay on course, allowing the budget to remain as is. For an effective manager,inaction is not an option.

Maintaining Good Cash FlowAlthough an effective manager need not be a financial expert, in order to make soundmanagement decisions, he or she must be familiar with basic accounting. For example, yourorganization should decide what financial accounting method or system it will use.6 Thereare two principal methods of financial accounting: cash basis accounting and accrual basisaccounting.

Whatever method is used, all ledgers, financial records, and reports should use the samemethod. Some analysts prefer the accrual method because it gives a more accurate picture ofan organization’s cash position and overall fiscal health. Many donors, however, prefer thecash basis because it is simpler to understand and manage. This is one time when programand financial managers should seek expert advice and weigh the pros and cons of choosingone method over the other, assist the organization to set up its financial management system,ledgers, and charts of accounts, and develop “user-friendly” tools and mechanisms for systemsmonitoring and updating.

6 Some analysts distinguish between financial accounting and managerial accounting. Financial accountinggenerally refers to the system used to record all financial transactions. Managerial accounting refers to the way inwhich costs are determined.

9

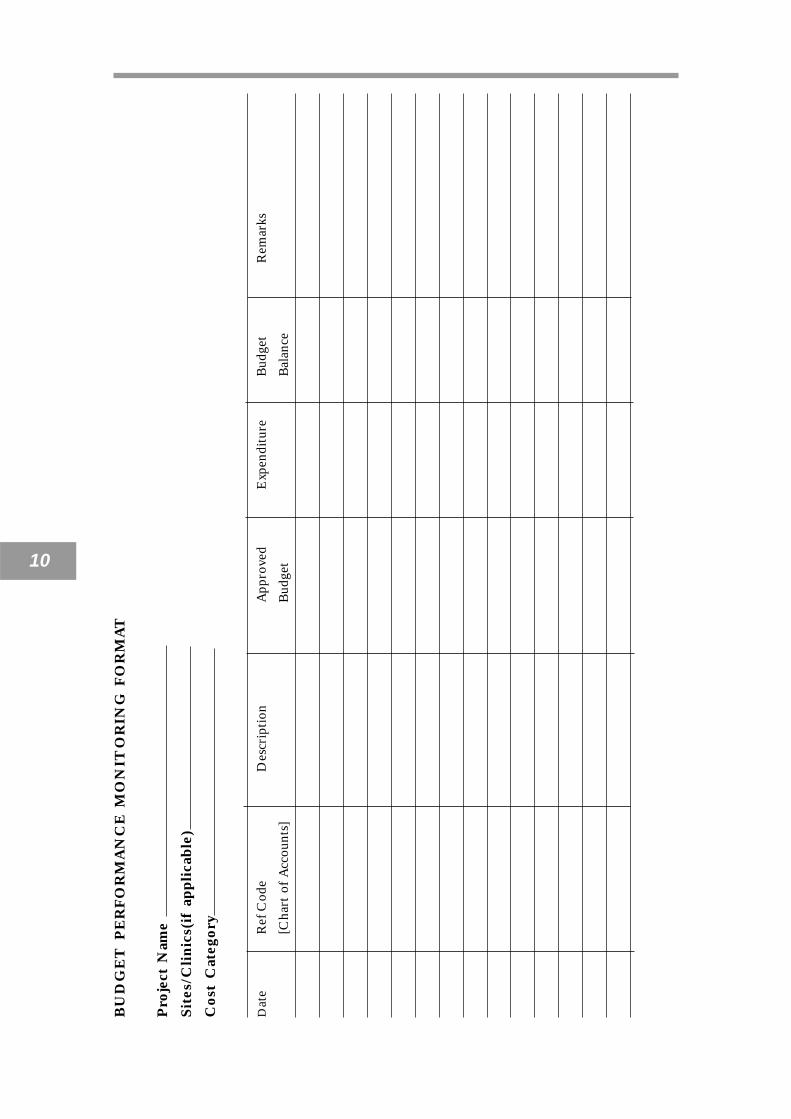

Exercise…Using a format to facilitate budgetmonitoring

This format can be used to facilitate budget monitoring and review. A prudent manager mayrequest that financial staff institutionalize it and fill it in on a monthly basis. Format reviewcan be a major agenda item at regular staff meetings.

Cash Basis Accounting

Cash basis accounting is the mostsimple: revenue is recorded whenreceived and expenses recorded whenpaid. However, it can distort the truecash position of an organizationbecause income may not be related tothe appropriate expenses, or paymentscan be manipulated to make anorganization look more “cash rich”(e.g., delay in paying bills so the balancesheet looks better).

Accrual Basis Accounting

Under accrual basis accounting, revenue isrecorded when earned and expenses arerecorded when incurred without regard towhen cash changes hands. For example, ifan organization prepays its rent annually, itis “expensed” in the ledger on a monthlybasis although it was paid earlier. Similarly,an accrual system spreads depreciationequally over the useful life on an asset. Inthe accrual system, two ledgers are main-tained: Accounts Receivable and Ac-counts Payable. These are updated as in-come is actually received or payments areactually made.

Remember...There are two main types of accountingsystems

10

BU

DG

ET

PE

RF

OR

MA

NC

E M

ON

ITO

RIN

G F

OR

MA

T

Pro

ject

Nam

e

Site

s/C

lini

cs(i

f ap

plic

able

)

Cos

t C

ateg

ory

Dat

eR

ef C

ode

Des

crip

tion

App

rove

dE

xpen

ditu

reB

udge

tR

emar

ks

[Cha

rt o

f A

ccou

nts]

Bud

get

Bal

ance

11

As mentioned earlier, a manager must monitor several kinds of costs. Among these are directversus indirect costs or fixed versus variable costs. An example of a direct cost is paymentto a trainer or for a venue for conducting a training course. An example of an indirect costmay be headquarters rent or the assistance of a financial officer, because both must cover theentire operations of an organization and cannot be specifically attributed to one project orprogram. Most managers are able to easily quantify direct costs because they are specific.Yet, indirect costs often contribute substantially to administration and management.Therefore, financial staff should be encouraged to determine the indirect costs – or the costof doing business – for the organization. Usually, an accounting firm can provide the appropriatetechnical support to determine the indirect costs and express it as an average rate, orpercentage, of normal operational costs. The indirect rate can then be included in budgetssubmitted to donors or in projecting annual operating costs.

An example of fixed costs are those in a contract that specifies a monthly charge for a particularservice. On an annual basis, staff salaries are generally a fixed cost (the term “generally” isused because it may be that a staff member receives a promotion or an increment as an incentiveduring a year). Variable costs are those that may depend on market forces or fluctuations. Asimple example is the costs of stationery and information technology that may increase, oreven decrease, based on demand, currency fluctuations, and the costs of production.

Exercise…Identifying the types of costs yourorganization incurs

Sometimes, financial terminology seems confusing or overly theoretical. Sitting togetherwith your financial and program staff, conduct a simple exercise that can help everyone tobetter understand these terms.

1. Divide a piece of paper into four sections.2. Label each quarter as follows: at the top of the page, write “direct” in one quarter and

“indirect” in the other. Do the same thing at the bottom of the page, writing “ fixed” inthe first quarter and “variable” in the other.

3. Brainstorm about your organization’s routine expenses that fall into each category.4. Note those expenses that may fall into more than one category. Are your systems

capable of monitoring and providing accurate data on all of these categories? Are therelinkages or patterns among them that suggest the need to monitor some categoriessimultaneously?

5. How do these categories compare with your organization’s chart of accounts? Do youneed more or different categories to capture all the financial data you are monitoring?

12

Variances

If you are carefully and systematically monitoring your budget, you will discern income andexpenditure patterns that must be watched carefully. Among the most critical are variances;that is, the difference between what was planned and the actual results. A manager must actwhen variances appear. Managers should ask questions, conduct a variance analysis (see below)and adopt a plan of action for addressing the variance. A variance is not always negative. Forexample, an organization may generate more income or attract more donor support than wasoriginally assumed in designing the budget. Alternatively, an organization may receive an in-kind donation, such as a building, eliminating the need to rent or renovate a facility. Mostoften, however, a variance involves a shortfall or miscalculation that must be addressed inorder to ensure smooth operations.

Remember…Conduct a variance analysis when resultsdiffer from plans.7

There are three primary types of variance analyses:

✔ Comparison of budgeted costs and actual costs orexpenditures.

✔ Comparison of the planned quantity of an activity orpurchase with the actual quantity.

✔ Comparison of the planned output with the actualoutput.

As a manager, when you realize there is a variance, ask questions and act. Bring in yourprogram and finance directors, or your accountant, to analyze the situation. Then, decideupon and implement a concrete plan of action.

Vexing Financial Management Issues

Some recurring financial transactions can truly influence the “bottom line” and complicatefinancial management. Among these are travel advances, petty cash, income or revenuegenerated, requisition or procurement of goods and services, contraceptives and inventoriesof supplies or non-expendable assets. Each will be discussed separately.

Travel Expenses

Program managers, staff members, volunteers or Board members, and even programparticipants travel in furtherance of organizational programs, goals, and strategic objectives.Travel expenses are often among the most troubling and difficult aspects of controlling anorganization’s budget and expenditures. Following are a few simple rules that, if implemented,can reduce these problems:

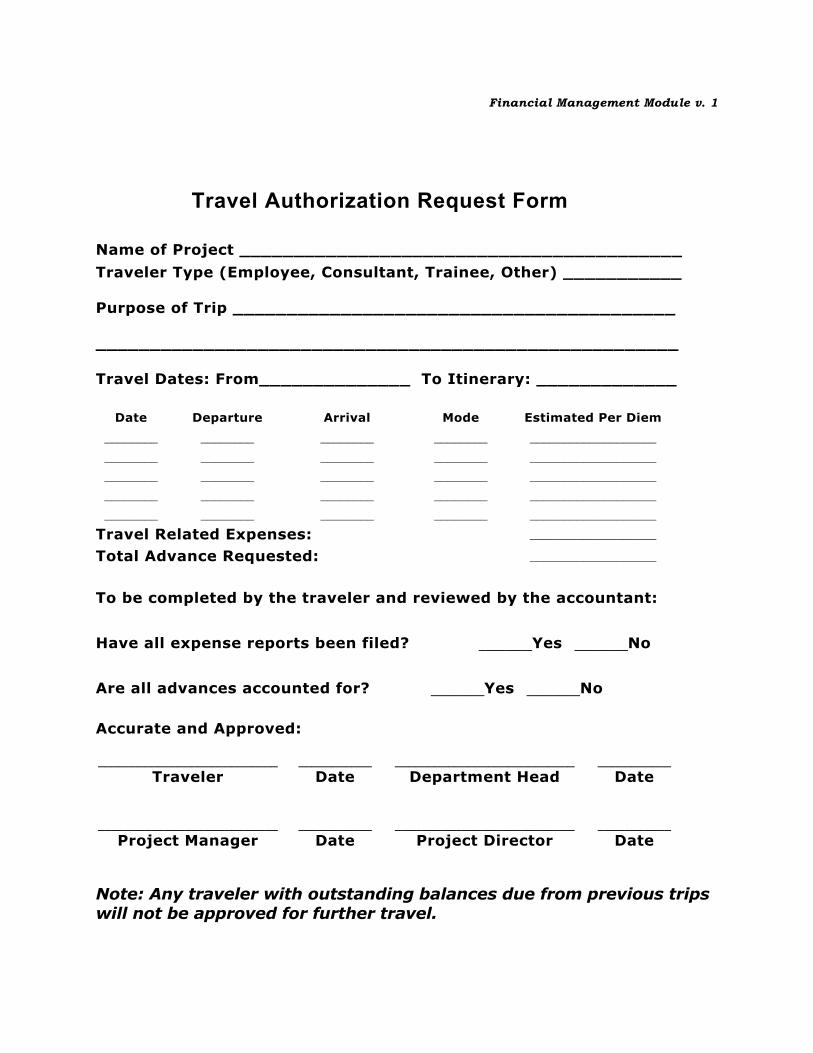

Always insist that a supervisor or manager approve travel before funds are allocatedand the trip is taken. The Travel Authorization Form in Annex B is designed tofacilitate the approval process.

7 The Manager. “Understanding and Using Financial Management Systems to Make Decisions, “ op. cit.

13

Always make sure that the travel is included in the budget. Very often, a staff personwill want to make a “spot check” or emergency trip that was not budgeted. This doesnot mean that travel should be summarily denied. It does mean that if the trip is notincluded in the budget, its importance should be determined and funds reallocated.

Always insist that the travel advance is retired or liquidated before new funds arereleased to the traveler. A good rule of thumb is that the travel expense report (seeAnnex B) should be submitted within 10 days of the travelers’ return. Sometimes,travelers have back-to-back trips and it is difficult to prepare and submit the form. Inany case, no traveler should take more than two trips without submitting a complete,and approved, travel expense report.

Always set rules for documentation of travel expenses. Receipts for lodging andtransportation should be appended to the travel expense report. Receipts should beattached to document any other major expenses (visas, airport taxes, communication,local transportation, business meals, photocopying or faxing, car rentals, etc.).Generally, it is acceptable to set a threshold amount (i.e., the equivalent of $10-20)below which a receipt is not required.

Always ask the traveler to prepare a trip report so that you as a manager have additionaldocumentation of the trip and expenditures. If the purpose of the trip was to prepare amajor document (e.g., an assessment or curriculum), it may be produced in lieu of a tripreport. A good trip report will give you clues about program performance and potentialresource shortfalls, needs, or opportunities.

With regard to travel, clear rules and regulations are extremely important and they must becommunicated to all staff persons or others who are traveling. Procedures regarding accountingfor travel should also be included in employee handbooks or personnel policies.

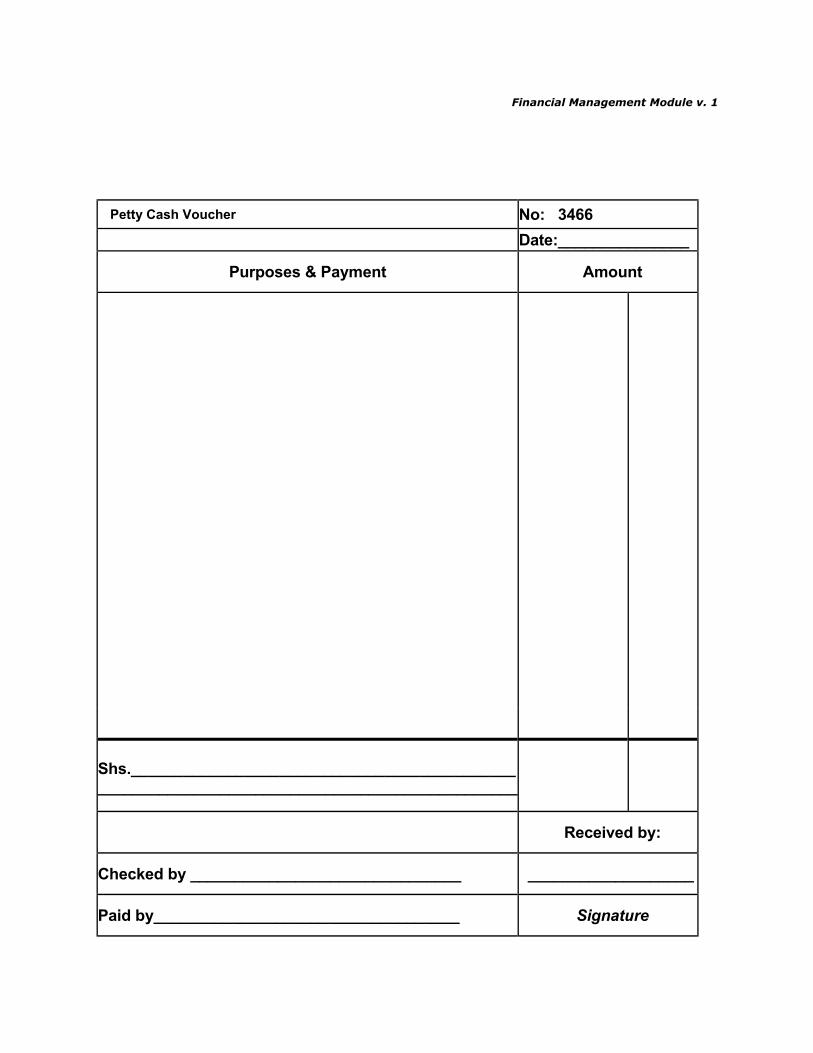

Petty Cash

Petty cash is just what it says: “petty.” In other words, petty cash is not a slush fund or asource for large payments. Petty cash is a small amount of money and should be used forminor expenditures. A staff member should request reimbursement from petty cash if theexpenditure is ordinary and reasonable, and within the scope of the staff member’s duties(e.g., taking a taxi to deliver a document, staying late and taking a taxi home to comply with adeadline, paying for small-scale outside color photocopying, etc.).

Some organizations use imprests as a supplement to the petty cash system (e.g., giving aclinic in-charge a small amount of money to replace expendable supplies such as Jik, gauze,bandages, soap, and gloves). Usually it is prudent to require prior supervisors’ approval beforeundertaking any activity for which petty cash or an imprest will be required. In any case, allpetty cash or imprests must be reimbursed only upon production of original receipts.

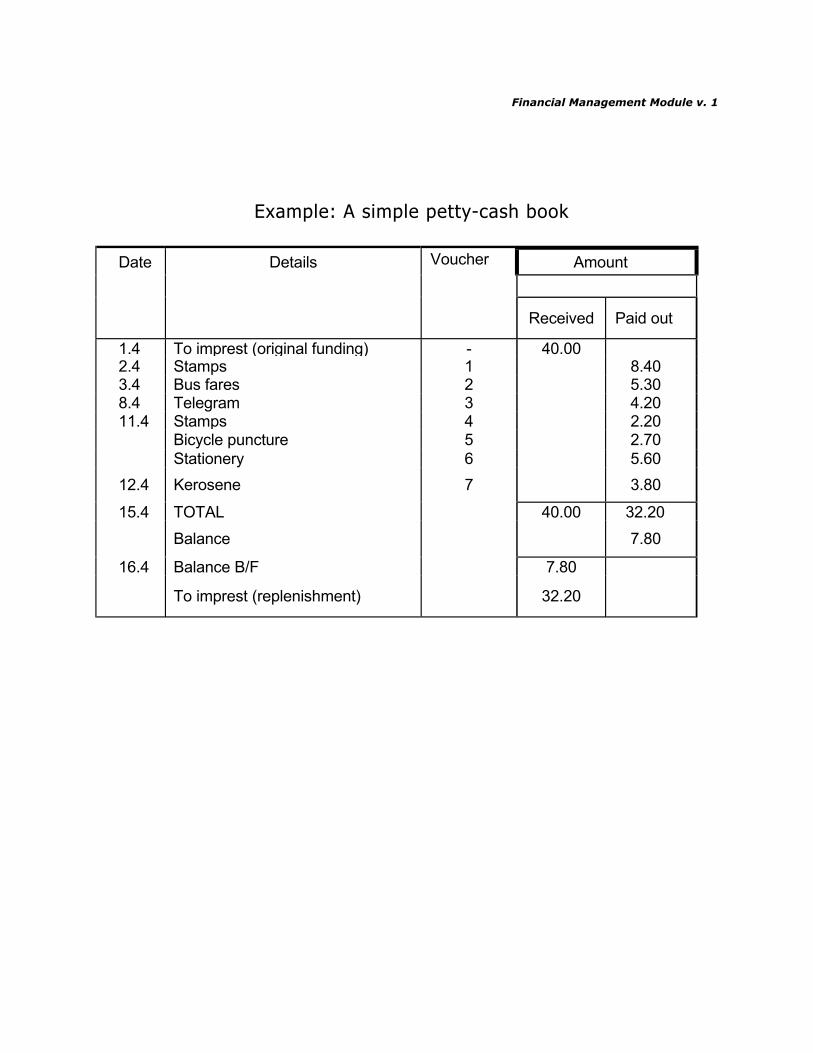

It is advisable to keep a simple petty cash or imprest book. Annex C contains examples ofpetty cash ledgers and vouchers. With both systems, all accounts should be reconciled on aweekly or bi-weekly basis since the amounts are small but critical to smooth operations. Amonthly petty cash or imprest report should be included in the overall income and expenditurestatement.

14

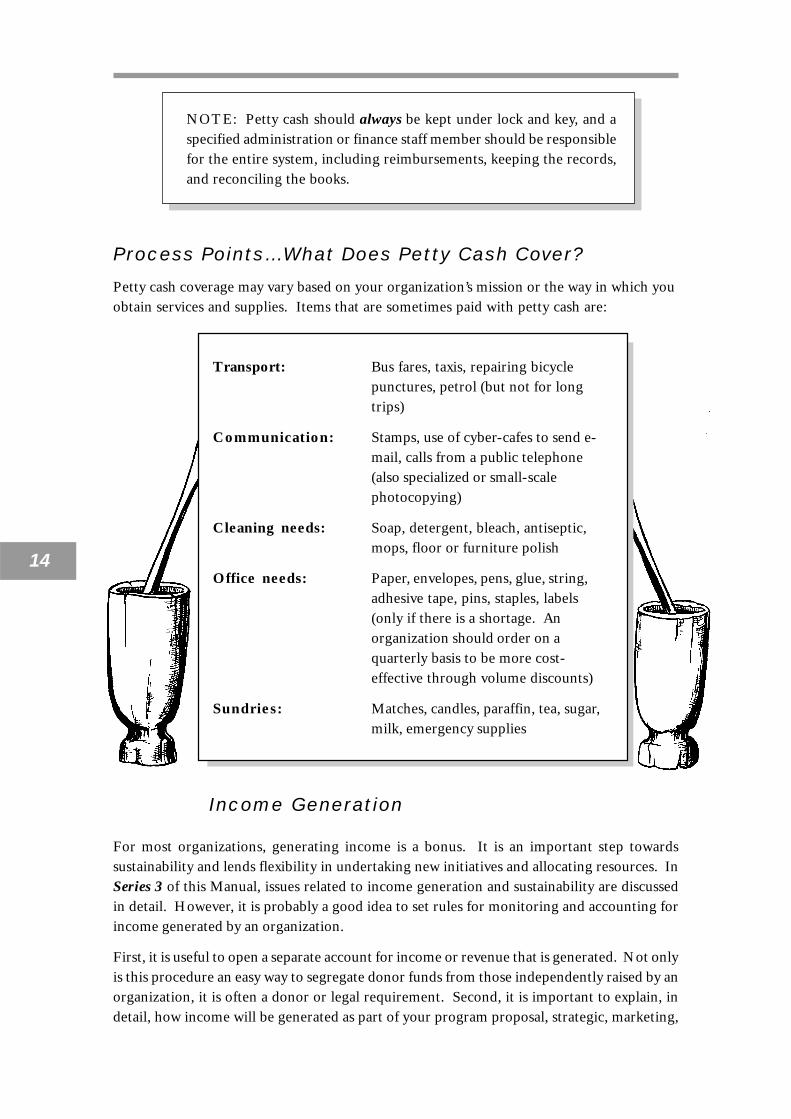

Process Points…What Does Petty Cash Cover?

Petty cash coverage may vary based on your organization’s mission or the way in which youobtain services and supplies. Items that are sometimes paid with petty cash are:

NOTE: Petty cash should always be kept under lock and key, and aspecified administration or finance staff member should be responsiblefor the entire system, including reimbursements, keeping the records,and reconciling the books.

Transport: Bus fares, taxis, repairing bicyclepunctures, petrol (but not for longtrips)

Communication: Stamps, use of cyber-cafes to send e-mail, calls from a public telephone(also specialized or small-scalephotocopying)

Cleaning needs: Soap, detergent, bleach, antiseptic,mops, floor or furniture polish

Office needs: Paper, envelopes, pens, glue, string,adhesive tape, pins, staples, labels(only if there is a shortage. Anorganization should order on aquarterly basis to be more cost-effective through volume discounts)

Sundries: Matches, candles, paraffin, tea, sugar,milk, emergency supplies

Income Generation

For most organizations, generating income is a bonus. It is an important step towardssustainability and lends flexibility in undertaking new initiatives and allocating resources. InSeries 3 of this Manual, issues related to income generation and sustainability are discussedin detail. However, it is probably a good idea to set rules for monitoring and accounting forincome generated by an organization.

First, it is useful to open a separate account for income or revenue that is generated. Not onlyis this procedure an easy way to segregate donor funds from those independently raised by anorganization, it is often a donor or legal requirement. Second, it is important to explain, indetail, how income will be generated as part of your program proposal, strategic, marketing,

15

or business plan, and in your regular financial reports. Some of the critical details includemethods of generating income, price per unit, source and amount of financial inputs fromthe organization (e.g., commodities, fees for services, membership cards, per trainee cost fora training course, etc.), and profitability ratios (e.g., the profit or revenue divided by thefinancial inputs).

For some NGOs offering specific services,such as health services, it is useful to have acash book or ledger to record cashcollections, income generated by fees, andpurchases. As a manager, you should shortenthe intervals for collecting and accountingfor cash as much as possible. For example,for nearby facilities, a weekly cash collectionand report is advisable. Similarly, whenevercommodities and supplies are distributed,they are the same as “cash.” Therefore, thesedistributions should also be entered into a

ledger and kept as a form of inventory. Annex D contains sample formats or ledger sheetsfor cash collections and contraceptive receipt or distribution. Non-health organizations canadapt these formats to reflect their primary products or mission, such as IEC materials oragricultural and environmental protection input kits.

Procurement

Although it appears to be a simple matter, procurement of goods and services is often amajor stumbling block for even a well-run organization. Procurement is an area requiringvery specific, written procedures and guidelines. Procurement procedures are very oftenlinked to financial control procedures to prevent fraud or waste of organizational resources.Clearly, procurements are tied to the budget, and the larger the expenditure, the greater theneed for control.

Procurement ranges from the routine, day-to-day acquisition of supplies to tenders forlarge- scale supply orders or long-term services. The stages in the procurement process shouldbe the same no matter what is being ordered:

Managers should make sure that funds are available for procurement.A strict process should be followed – with specific criteria for evaluating pro-formainvoices or responses to tender offers – that ensures the organization gets the bestvalue for its expenditures, or the best qualified vendor.Finally, a clear paper trail should be created so that an organization’s decision-makingprocess is documented and defensible.

16

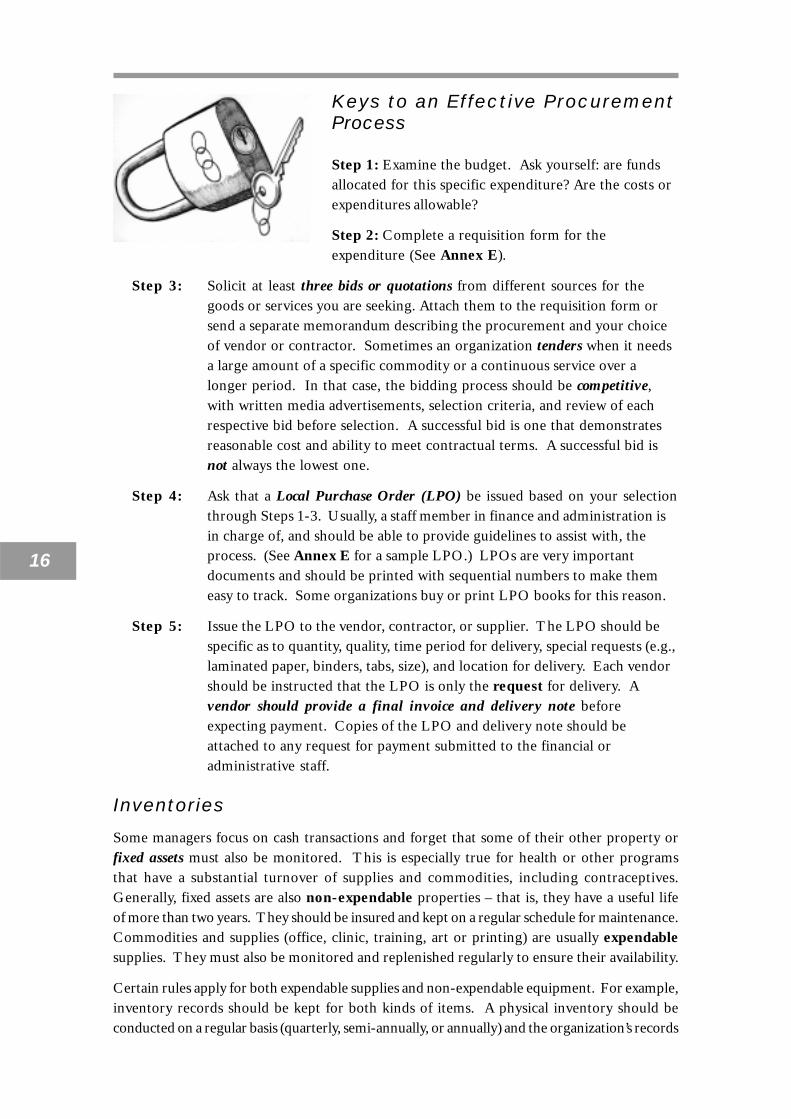

Keys to an Effective ProcurementProcess

Step 1: Examine the budget. Ask yourself: are fundsallocated for this specific expenditure? Are the costs orexpenditures allowable?

Step 2: Complete a requisition form for theexpenditure (See Annex E).

Step 3: Solicit at least three bids or quotations from different sources for thegoods or services you are seeking. Attach them to the requisition form orsend a separate memorandum describing the procurement and your choiceof vendor or contractor. Sometimes an organization tenders when it needsa large amount of a specific commodity or a continuous service over alonger period. In that case, the bidding process should be competitive,with written media advertisements, selection criteria, and review of eachrespective bid before selection. A successful bid is one that demonstratesreasonable cost and ability to meet contractual terms. A successful bid isnot always the lowest one.

Step 4: Ask that a Local Purchase Order (LPO) be issued based on your selectionthrough Steps 1-3. Usually, a staff member in finance and administration isin charge of, and should be able to provide guidelines to assist with, theprocess. (See Annex E for a sample LPO.) LPOs are very importantdocuments and should be printed with sequential numbers to make themeasy to track. Some organizations buy or print LPO books for this reason.

Step 5: Issue the LPO to the vendor, contractor, or supplier. The LPO should bespecific as to quantity, quality, time period for delivery, special requests (e.g.,laminated paper, binders, tabs, size), and location for delivery. Each vendorshould be instructed that the LPO is only the request for delivery. Avendor should provide a final invoice and delivery note beforeexpecting payment. Copies of the LPO and delivery note should beattached to any request for payment submitted to the financial oradministrative staff.

Inventories

Some managers focus on cash transactions and forget that some of their other property orfixed assets must also be monitored. This is especially true for health or other programsthat have a substantial turnover of supplies and commodities, including contraceptives.Generally, fixed assets are also non-expendable properties – that is, they have a useful lifeof more than two years. They should be insured and kept on a regular schedule for maintenance.Commodities and supplies (office, clinic, training, art or printing) are usually expendablesupplies. They must also be monitored and replenished regularly to ensure their availability.

Certain rules apply for both expendable supplies and non-expendable equipment. For example,inventory records should be kept for both kinds of items. A physical inventory should beconducted on a regular basis (quarterly, semi-annually, or annually) and the organization’s records

17

with regard to stock should be updated. In fact, the records can serve as a checklist so that noitem is overlooked in the inventory. The forms in Annex D can also be used as inventoryformats to be adapted for your specific use.

Some tips about expendable supplies andcontraceptives:

Instituting Effective Financial Controls

This is among the most challenging aspects of financial management for the manager andfinancial professional alike. This is, in part, because financial controls are essentially rules,policies, and procedures that must be consistently applied, adhered to, and enforced.Management’s attitude toward controls – that is, whether management promotes anenvironment in which controls are valued or is lax in their enforcement – can make a significantdifference in the effectiveness of an organization’s financial management. Control policiesand procedures are designed primarily to:

Ensure that accounting records are complete and accurate.Institute safeguards, checks, and balances so that expenditures are properly approvedand made as budgeted.Safeguard assets and curtail misappropriation or theft.Prevent and detect fraud and errors.

Expendable supplies should be:

✔ Stored in a clean, well lighted, wellventilated area.

✔ Kept off the floor on shelves or palettes.✔ Logged in based on a FEFO system, that is

First Expired, First Out.✔ Kept in a locked area to which only

authorized personnel have access.✔ Kept on separate register pages or on

cards to facilitate stock taking andinventories.

✔ Accounted and signed for by all staffwho receive them. Formats should bedeveloped for this purpose.

18

Protect staff.Ensure proper utilization of resources.Support the preparation of reliable and timely financial reports.

Control procedures generally involve some comparisons of information from different sourcesto verify and validate requests, expenditures, and reports. Usually, organizations have threekinds of control procedures: accounting controls, segregation of duties, and managerialsupervision.

Accounting controls

Accounting controls are usually maintained by the financial management staff and involvecomparisons between data sources to verify the accuracy of transactions and recording. Someof the comparisons8 that should routinely be conducted include:

Comparing cash receipts as recorded by a cashier or cash clerk with information on thenumbers of patients or clients recorded in a register or ledger.Comparing total receipts with the amount deposited in the bank.Counting cash to verify that the cash on hand agrees with the cash balance recorded inthe cash book.Reconciling bank statements to compare cash book entries with entries in the bankstatement.Controlling stock inventory by comparing the physical stock with the accountingrecords or stock cards.Comparing actual expenditures and revenues with budgets.

Any variances or discrepancies should be immediately documented and reported to seniormanagement. Senior managers should undertake a review of the circumstances and any actionneeded, being fair, but firm.

Segregation of duties

The concept is simple, but its applications are often difficult. Basically, segregation of dutiesmeans that one person should never be responsible for all aspects of a transaction. Inother words, one person checks the work of another. For example, one person should notorder or make a requisition for purchase, review the pro forma invoices, approve the selectionof the vendor, and sign the check for payment. Also, the person who keeps cash should notmaintain the cash book or do bank reconciliations. The person who prepares the payrollshould not pay salaries, while the person who makes payments should not approve them.Three important financial management functions that should routinely be handled by differentpeople are:

Custody – physical responsibility for cash, stores, commodities, vehicles, majorequipment, etc.Recording – making entries into the main accounts or ledgers from which reports aremade.Authorizing – approving purchases and other uses of resources.

8 Based on materials from Abt Associates, Bethesda, MD, Cambridge, MA and Johannesburg, RSA.

19

Managerial supervision

An effective manager will ensure that staff members at all levels and members of the Boardunderstand an organization’s internal controls, policies, and procedures. He or she will insiston written policies and procedures, and regularly review controls for currency and effectiveness.The manager should also not circumvent or ignore controls or problems that they uncover.

Most important, an effective manager should be a model of compliance. In fact, he or sheshould be a primary advocate, adhering to sytems disciplines, reviewing reports systematically,and asking questions about any discrepancies or ambiguities. Annex F contains some veryuseful checklists, prepared by Abt Associates, to monitor internal controls and theireffectiveness.

Remember…There are some “Thou Shalt Nots…”

Here are some simple principles formaintaining internal controls.

✔ Thou shalt not have a financialmanagement system without writtenprocedures that are regularly reviewed andupdated.✔ Thou shalt not enter into transactionswithout supporting documentation such asoriginal receipts, invoices, LPOs, andinternal approval documents (e.g.,requisitions, travel authorization forms).✔ Thou shalt not leave cash and checkbooksunsecured. A few specific persons should be

given the responsibility for maintaining secure physical custody of these items.✔ Thou shalt not manage an entire transaction without cross-checking by another person.✔ Thou shalt not forget to thoroughly review requests for approval and financial reports

as received and to ask about any variances between the budget or prior reports and thecurrent requests or reports.

✔ Thou shalt not ignore evidence of abuse of physical assets such as vehicles or majorequipment.

Reporting on Your Organization’s Finances

Reporting on an organization’s finances generally takes two forms: reports needed for soundinternal financial management, controls, and decision-making and reports required by externaldonors (See Annex G “Grantee Financial Report”). Both are extremely important, butoften managers focus more on the external than the internal reports. Yet, the internal reportingsystem may be even more critical because it will help a manager avoid small problems becomingmajor ones.

Organizations must conduct an annual audit, both for their own internal fiscal disciplineand also to comply with donor requirements. Audit results will provide important insightsinto areas of successful financial management, or areas needing improvement. Although most

20

financial reports required by donors are formatted, it is often useful to provide a more detailednarrative to explain some of the financial issues or changes that have occurred since preparingthe budget or the first report. The audit report may provide useful information for this purpose.

Annex G also contains a good internal report format such as an income and expendituresstatement. This sample is manually prepared but the advent of spreadsheets or softwareapplications means that a manager should be able to receive accurate and timely reports at amonthly interval. A manager should also provide regular (at least quarterly) reports to anorganization’s Board to inform them about the organization’s cash position and needs. If theBoard has a Finance Committee, a prudent manager will engage them in reviewing financialdata, making forecasts of potential revenues or shortfalls, and identifying new donors.

Internal monthly financial reports can be issued with any frequency or combined in anyconfiguration required by donors: quarterly, semi-annually, or annually. A prudent manager,however, will ask for internal biweekly or monthly reports as a matter of course. Frequentreports help monitor and protect against downturns in the organization’s fiscal health.

Sometimes, donors ask that key data and information be appended to the financial report.Data may include copies of bank statements and bank reconciliation exercises; lists of salariesand benefits paid from donor funds; acknowledgement of contraceptives or other suppliesreceived; reports on the currency exchange rates over a period; and a list of unpaid obligationsfor the period covered by the report. Whatever the stipulations, follow the donors’guidelines. If there are no guidelines, you may wish to review Annex G for a model financialreport.

Bright Idea… Avoid some of these managerial pit-falls:9

✔ Chronic crisis management, leading to last-minute,often more expensive, solutions that contribute toinefficient management and missed opportunities.

✔ Unrealistic price setting that may create a situationin which an organization cannot recover its costs orincurs greater losses.

✔ Inaccurate analyses of the real cost of doingbusiness, such as a failure to consider fixed or indirectcosts when preparing budgets or forecasting resourceneeds.

✔ Dependency on a single funding source or donor,which leaves the organization vulnerable if the donorreduces or suspends funding.

✔ Failure to react to environmental changes that canlead to missed opportunities to generate or attract newfunding or failure to budget for new regulatory or otherrequirements (e.g., licenses).

✔ Lack of managerial skill in analyzing, using, andcommunicating financial information such that amanager is unable to recognize potential risks or makeappropriate decisions about the use of scarce resourcesor the generation of new ones.

9 Adapted from The Manager, op. cit.

21

Annex AModel Budget Formats

Financial Management Module v. 1

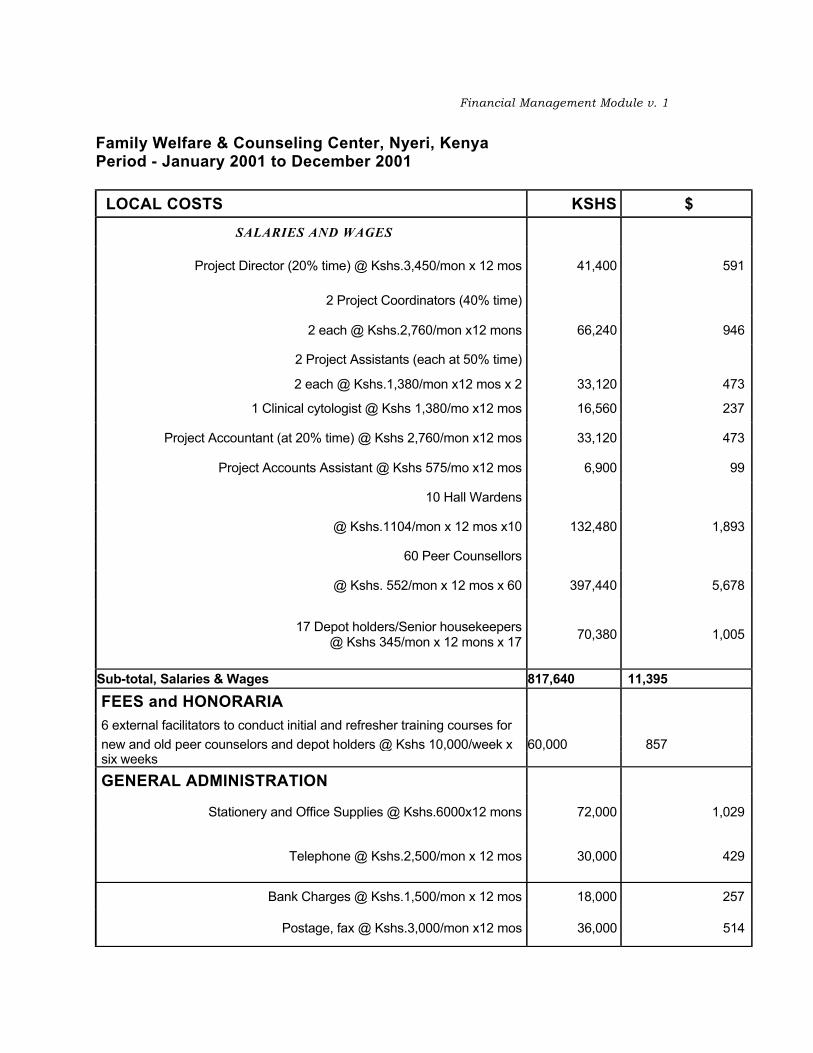

Family Welfare & Counseling Center, Nyeri, Kenya Period - January 2001 to December 2001

LOCAL COSTS KSHS $ SALARIES AND WAGES

Project Director (20% time) @ Kshs.3,450/mon x 12 mos 41,400 591

2 Project Coordinators (40% time)

2 each @ Kshs.2,760/mon x12 mons 66,240 946

2 Project Assistants (each at 50% time)

2 each @ Kshs.1,380/mon x12 mos x 2 33,120 473

1 Clinical cytologist @ Kshs 1,380/mo x12 mos 16,560 237

Project Accountant (at 20% time) @ Kshs 2,760/mon x12 mos 33,120 473

Project Accounts Assistant @ Kshs 575/mo x12 mos 6,900 99

10 Hall Wardens

@ Kshs.1104/mon x 12 mos x10 132,480 1,893

60 Peer Counsellors

@ Kshs. 552/mon x 12 mos x 60 397,440 5,678

17 Depot holders/Senior housekeepers @ Kshs 345/mon x 12 mons x 17 70,380 1,005

Sub-total, Salaries & Wages 817,640 11,395 FEES and HONORARIA 6 external facilitators to conduct initial and refresher training courses for new and old peer counselors and depot holders @ Kshs 10,000/week x 60,000 857 six weeks GENERAL ADMINISTRATION

Stationery and Office Supplies @ Kshs.6000x12 mons 72,000 1,029

Telephone @ Kshs.2,500/mon x 12 mos 30,000 429

Bank Charges @ Kshs.1,500/mon x 12 mos 18,000 257

Postage, fax @ Kshs.3,000/mon x12 mos 36,000 514

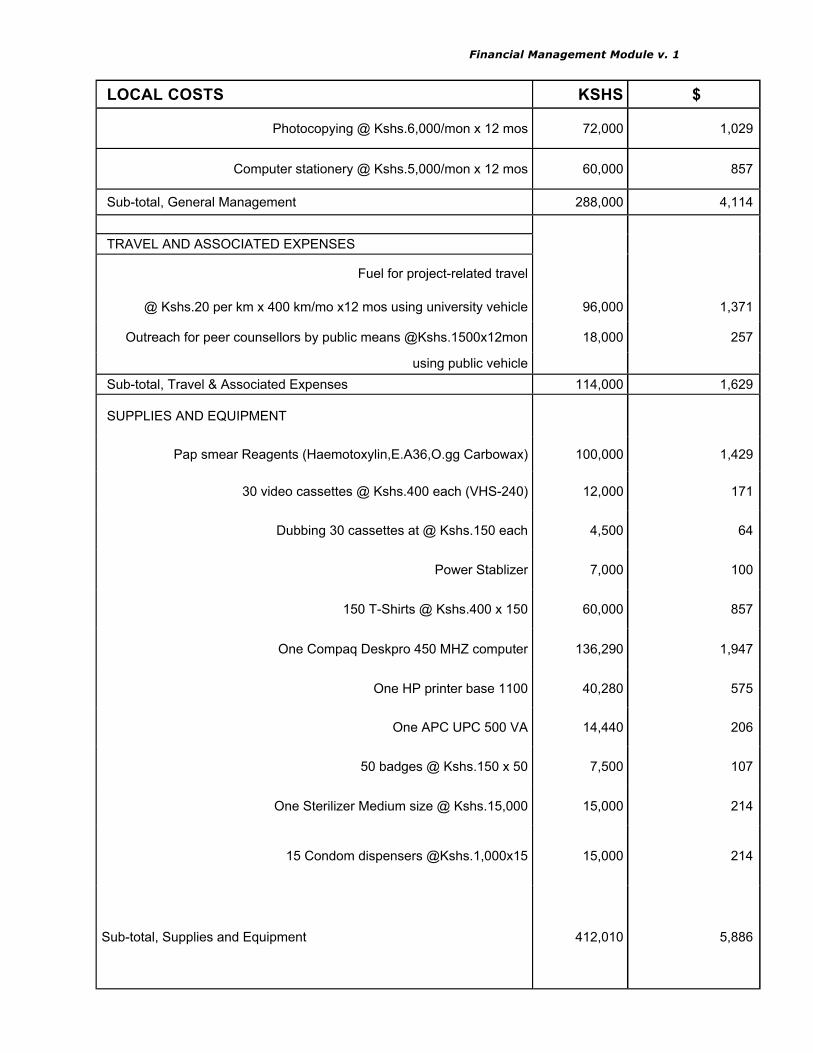

Financial Management Module v. 1

LOCAL COSTS KSHS $

Photocopying @ Kshs.6,000/mon x 12 mos 72,000 1,029

Computer stationery @ Kshs.5,000/mon x 12 mos 60,000 857

Sub-total, General Management 288,000 4,114

TRAVEL AND ASSOCIATED EXPENSES

Fuel for project-related travel

@ Kshs.20 per km x 400 km/mo x12 mos using university vehicle 96,000 1,371

Outreach for peer counsellors by public means @Kshs.1500x12mon 18,000 257

using public vehicle Sub-total, Travel & Associated Expenses 114,000 1,629

SUPPLIES AND EQUIPMENT

Pap smear Reagents (Haemotoxylin,E.A36,O.gg Carbowax) 100,000 1,429

30 video cassettes @ Kshs.400 each (VHS-240) 12,000 171

Dubbing 30 cassettes at @ Kshs.150 each 4,500 64

Power Stablizer 7,000 100

150 T-Shirts @ Kshs.400 x 150 60,000 857

One Compaq Deskpro 450 MHZ computer 136,290 1,947

One HP printer base 1100 40,280 575

One APC UPC 500 VA 14,440 206

50 badges @ Kshs.150 x 50 7,500 107

One Sterilizer Medium size @ Kshs.15,000 15,000 214

15 Condom dispensers @Kshs.1,000x15 15,000 214

Sub-total, Supplies and Equipment 412,010 5,886

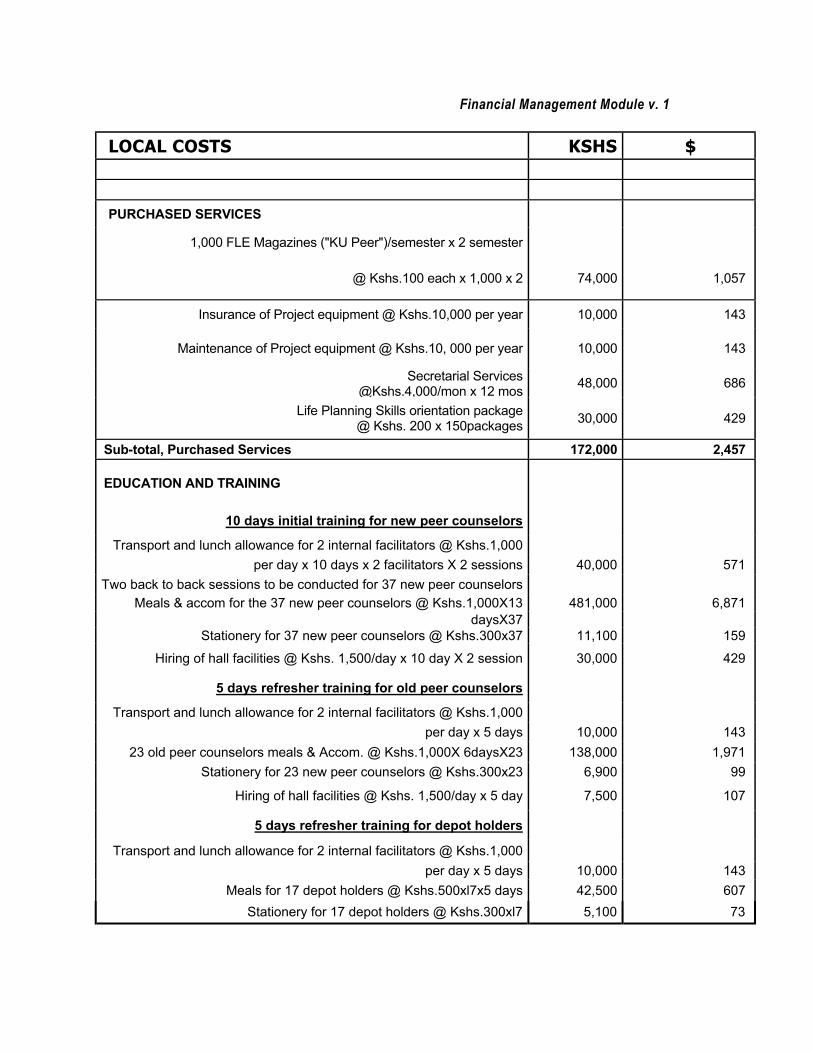

Financial Management Module v. 1

LOCAL COSTS KSHS $

PURCHASED SERVICES

1,000 FLE Magazines ("KU Peer")/semester x 2 semester

@ Kshs.100 each x 1,000 x 2 74,000 1,057

Insurance of Project equipment @ Kshs.10,000 per year 10,000 143

Maintenance of Project equipment @ Kshs.10, 000 per year 10,000 143

Secretarial Services @Kshs.4,000/mon x 12 mos 48,000 686

Life Planning Skills orientation package @ Kshs. 200 x 150packages 30,000 429

Sub-total, Purchased Services 172,000 2,457

EDUCATION AND TRAINING

10 days initial training for new peer counselors

Transport and lunch allowance for 2 internal facilitators @ Kshs.1,000 per day x 10 days x 2 facilitators X 2 sessions 40,000 571

Two back to back sessions to be conducted for 37 new peer counselors Meals & accom for the 37 new peer counselors @ Kshs.1,000X13 481,000 6,871

daysX37 Stationery for 37 new peer counselors @ Kshs.300x37 11,100 159

Hiring of hall facilities @ Kshs. 1,500/day x 10 day X 2 session 30,000 429

5 days refresher training for old peer counselors

Transport and lunch allowance for 2 internal facilitators @ Kshs.1,000 per day x 5 days 10,000 143

23 old peer counselors meals & Accom. @ Kshs.1,000X 6daysX23 138,000 1,971 Stationery for 23 new peer counselors @ Kshs.300x23 6,900 99

Hiring of hall facilities @ Kshs. 1,500/day x 5 day 7,500 107

5 days refresher training for depot holders

Transport and lunch allowance for 2 internal facilitators @ Kshs.1,000 per day x 5 days 10,000 143

Meals for 17 depot holders @ Kshs.500xl7x5 days 42,500 607 Stationery for 17 depot holders @ Kshs.300xl7 5,100 73

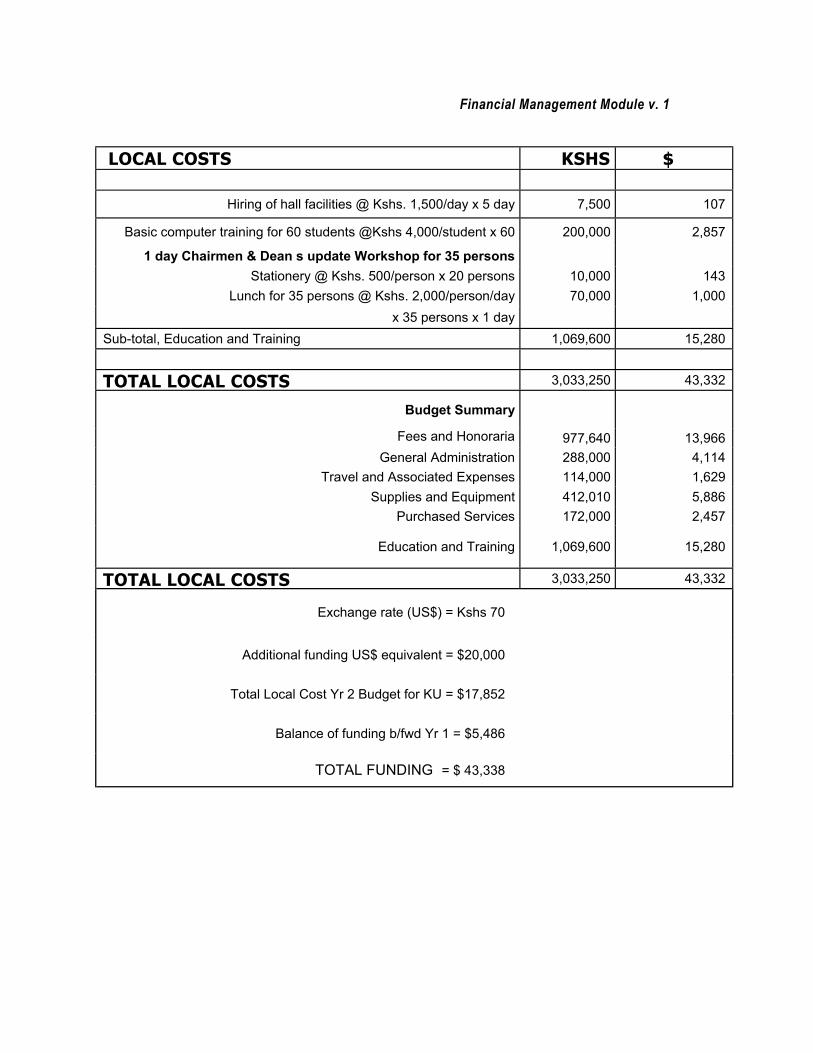

Financial Management Module v. 1

LOCAL COSTS KSHS $

Hiring of hall facilities @ Kshs. 1,500/day x 5 day 7,500 107

Basic computer training for 60 students @Kshs 4,000/student x 60 200,000 2,857

1 day Chairmen & Dean s update Workshop for 35 persons Stationery @ Kshs. 500/person x 20 persons 10,000 143

Lunch for 35 persons @ Kshs. 2,000/person/day 70,000 1,000 x 35 persons x 1 day

Sub-total, Education and Training 1,069,600 15,280

TOTAL LOCAL COSTS 3,033,250 43,332

Budget Summary

Fees and Honoraria 977,640 13,966 General Administration 288,000 4,114

Travel and Associated Expenses 114,000 1,629 Supplies and Equipment 412,010 5,886

Purchased Services 172,000 2,457

Education and Training 1,069,600 15,280

TOTAL LOCAL COSTS 3,033,250 43,332

Exchange rate (US$) = Kshs 70

Additional funding US$ equivalent = $20,000

Total Local Cost Yr 2 Budget for KU = $17,852

Balance of funding b/fwd Yr 1 = $5,486

TOTAL FUNDING = $ 43,338

Financial Management Module v. 1

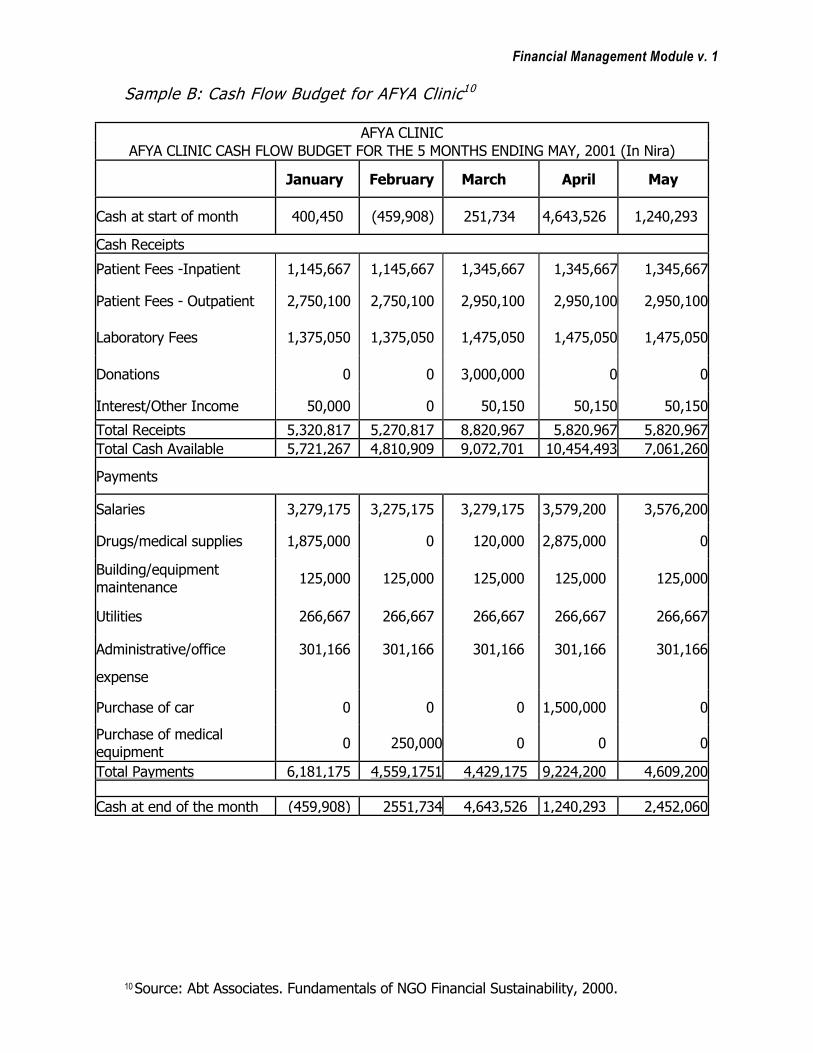

Sample B: Cash Flow Budget for AFYA Clinic10

AFYA CLINIC AFYA CLINIC CASH FLOW BUDGET FOR THE 5 MONTHS ENDING MAY, 2001 (In Nira)

January February March April May

Cash at start of month 400,450 (459,908) 251,734 4,643,526 1,240,293

Cash Receipts

Patient Fees -Inpatient 1,145,667 1,145,667 1,345,667 1,345,667 1,345,667

Patient Fees - Outpatient 2,750,100 2,750,100 2,950,100 2,950,100 2,950,100

Laboratory Fees 1,375,050 1,375,050 1,475,050 1,475,050 1,475,050

Donations 0 0 3,000,000 0 0

Interest/Other Income 50,000 0 50,150 50,150 50,150

Total Receipts 5,320,817 5,270,817 8,820,967 5,820,967 5,820,967 Total Cash Available 5,721,267 4,810,909 9,072,701 10,454,493 7,061,260

Payments

Salaries 3,279,175 3,275,175 3,279,175 3,579,200 3,576,200

Drugs/medical supplies 1,875,000 0 120,000 2,875,000 0

Building/equipment maintenance 125,000 125,000 125,000 125,000 125,000

Utilities 266,667 266,667 266,667 266,667 266,667

Administrative/office 301,166 301,166 301,166 301,166 301,166

expense

Purchase of car 0 0 0 1,500,000 0

Purchase of medical equipment 0 250,000 0 0 0

Total Payments 6,181,175 4,559,1751 4,429,175 9,224,200 4,609,200

Cash at end of the month (459,908) 2551,734 4,643,526 1,240,293 2,452,060

10 Source: Abt Associates. Fundamentals of NGO Financial Sustainability, 2000.

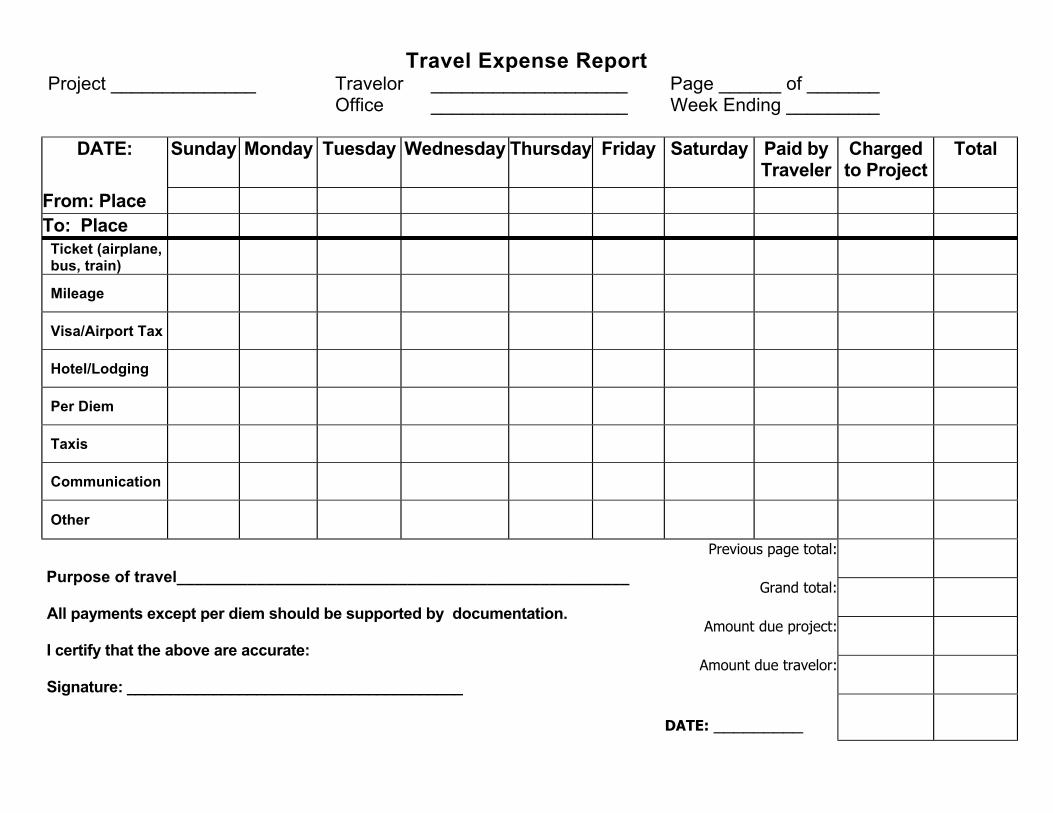

Annex BTravel Authorization

and Expense Report Formats

Travel Expense Report Project ______________ Travelor ___________________ Page ______ of _______

Office ___________________ Week Ending _________

DATE: Sunday Monday Tuesday Wednesday Thursday Friday Saturday Paid by Traveler

Charged to Project

Total

From: Place To: Place

Ticket (airplane, bus, train)

Mileage

Visa/Airport Tax

Hotel/Lodging

Per Diem

Taxis

Communication

Other

Previous page total:

Grand total:

Amount due project:

Amount due travelor:

Purpose of travel___________________________________________________ All payments except per diem should be supported by documentation. I certify that the above are accurate: Signature: _______________________________________

DATE: _________

Financial Management Module v. 1

Travel Authorization Request Form

Name of Project _________________________________________

Traveler Type (Employee, Consultant, Trainee, Other) ___________

Purpose of Trip _________________________________________

______________________________________________________

Travel Dates: From______________ To Itinerary: _____________

Date Departure Arrival Mode Estimated Per Diem ________ ________ ________ ________ ___________________ ________ ________ ________ ________ ___________________ ________ ________ ________ ________ ___________________ ________ ________ ________ ________ ___________________ ________ ________ ________ ________ ___________________

Travel Related Expenses: ___________________

Total Advance Requested: ___________________

To be completed by the traveler and reviewed by the accountant:

Have all expense reports been filed? ________Yes ________No

Are all advances accounted for? ________Yes ________No

Accurate and Approved:

___________________________ ___________ ___________________________ ___________ Traveler Date Department Head Date

___________________________ ___________ ___________________________ ___________ Project Manager Date Project Director Date

Note: Any traveler with outstanding balances due from previous trips will not be approved for further travel.

Annex CPetty Cash Vouchers and Ledgers

Financial Management Module v. 1

Example: A simple petty-cash book

Date Details Voucher Amount

Received Paid out

1.4 To imprest (original funding) - 40.00 2.4 Stamps 1 8.40 3.4 Bus fares 2 5.30 8.4 Telegram 3 4.20 11.4 Stamps 4 2.20

Bicycle puncture 5 2.70 Stationery 6 5.60

12.4 Kerosene 7 3.80

15.4 TOTAL 40.00 32.20 Balance 7.80

16.4 Balance B/F 7.80

To imprest (replenishment) 32.20

Financial Management Module v. 1

Petty Cash Voucher No: 3466 Date:_______________

Purposes & Payment Amount

Shs.____________________________________________________________________________________________

Received by:

Checked by _______________________________ ___________________

Paid by___________________________________ Signature

Annex DCash Collection

and Contraceptive Receipt/DistributionFormats

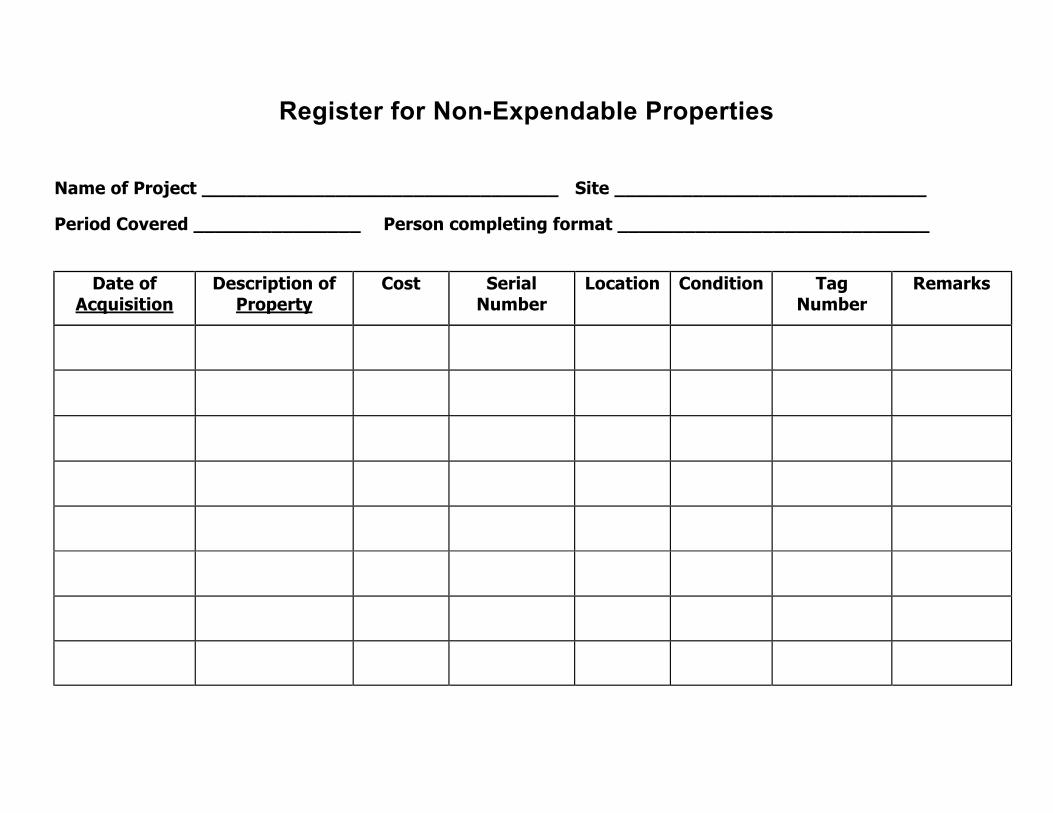

Register for Non-Expendable Properties

Name of Project ________________________________ Site ____________________________

Period Covered _______________ Person completing format ____________________________

Date of Acquisition

Description of Property

Cost SerialNumber

Location Condition

Tag Number

Remarks

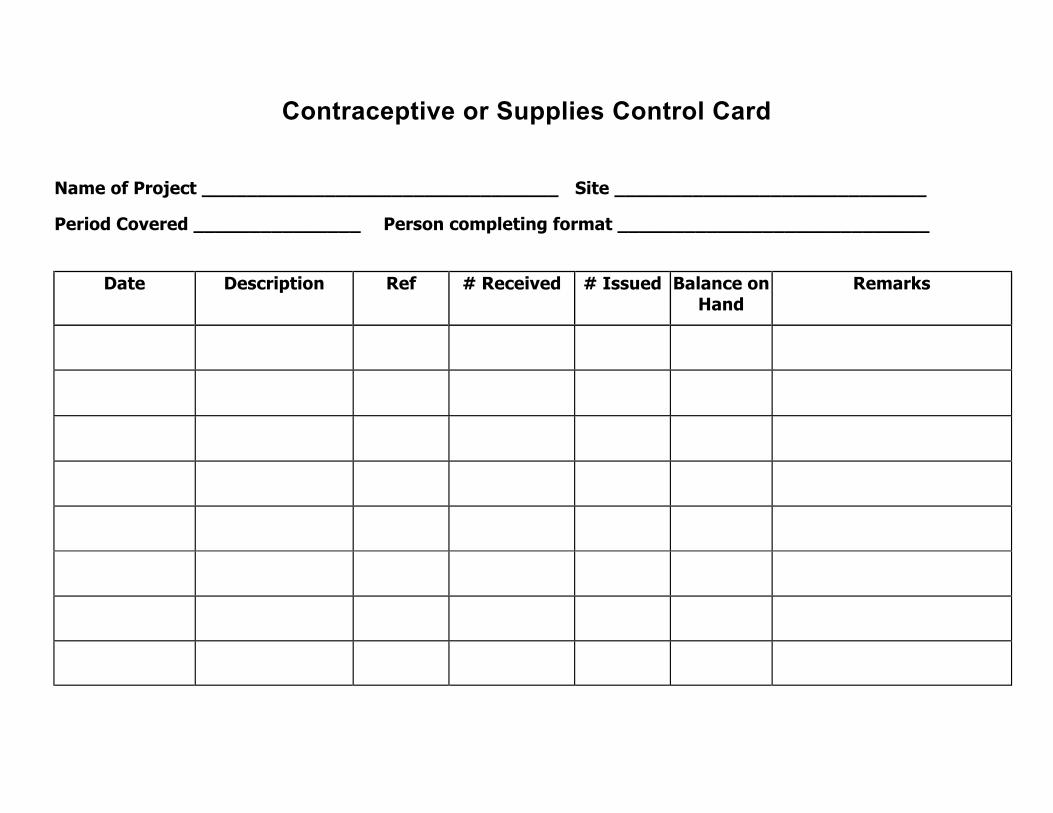

Contraceptive or Supplies Control Card

Name of Project ________________________________ Site ____________________________

Period Covered _______________ Person completing format ____________________________

Date Description Ref # Received # Issued Balance on Hand

Remarks

Annex ERequisition Forms and Local Purchase Orders

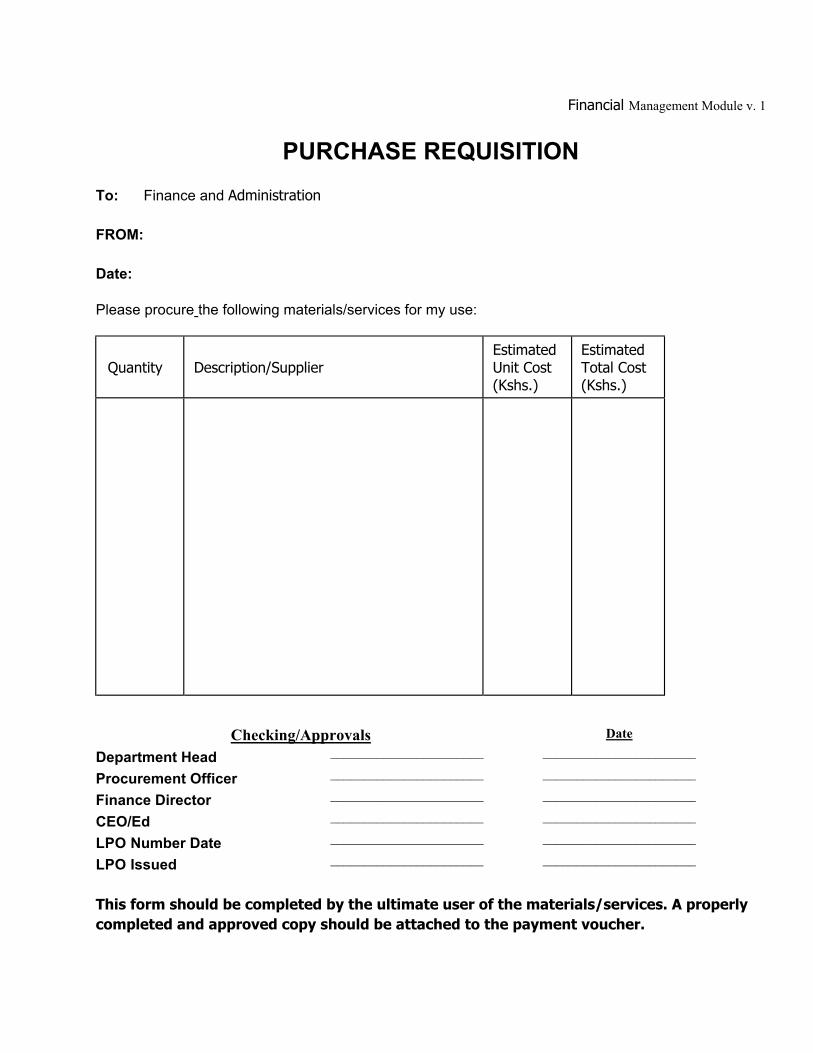

Financial Management Module v. 1

PURCHASE REQUISITION

To: Finance and Administration

FROM:

Date:

Please procure the following materials/services for my use:

Quantity Description/Supplier Estimated Unit Cost (Kshs.)

Estimated Total Cost (Kshs.)

Checking/Approvals Date

Department Head _______________________ _______________________

Procurement Officer _______________________ _______________________

Finance Director _______________________ _______________________

CEO/Ed _______________________ _______________________

LPO Number Date _______________________ _______________________

LPO Issued _______________________ _______________________

This form should be completed by the ultimate user of the materials/services. A properly completed and approved copy should be attached to the payment voucher.

Financial Management Module v. 1

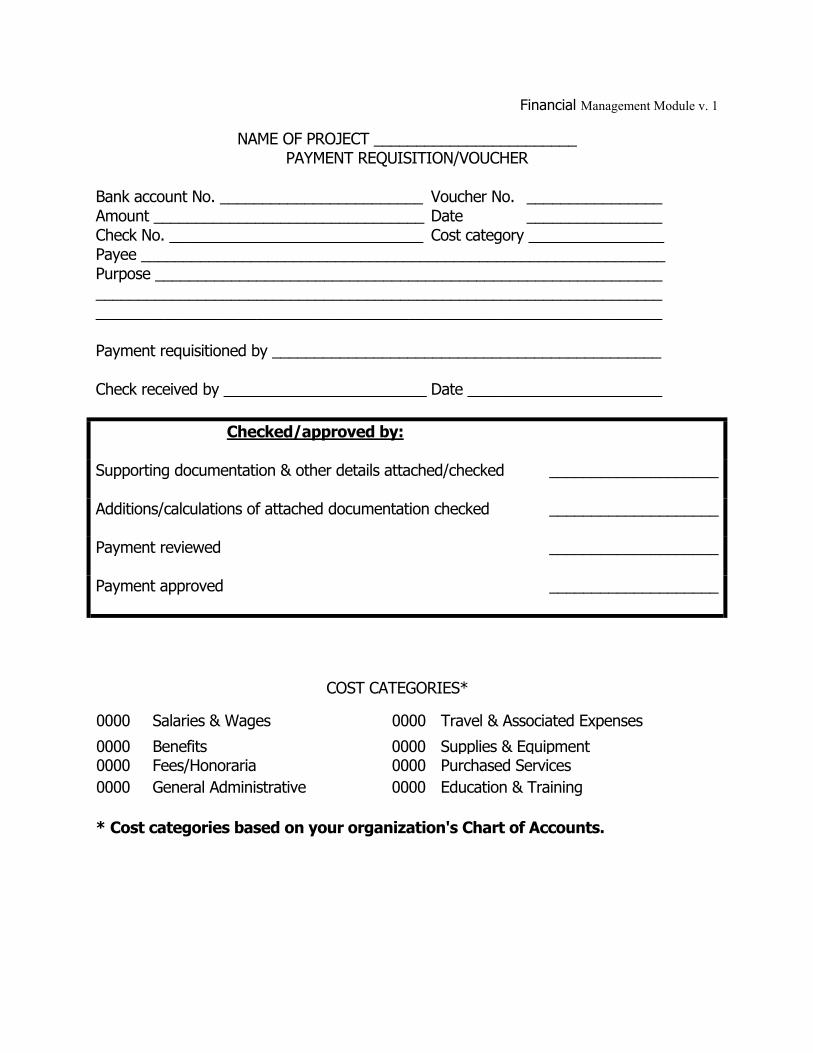

NAME OF PROJECT ________________________ PAYMENT REQUISITION/VOUCHER

Bank account No. ________________________ Voucher No. ________________ Amount ________________________________ Date ________________ Check No. ______________________________ Cost category ________________ Payee ______________________________________________________________ Purpose ____________________________________________________________ ___________________________________________________________________ ___________________________________________________________________ Payment requisitioned by ______________________________________________

Check received by ________________________ Date _______________________

Checked/approved by:

Supporting documentation & other details attached/checked ____________________

Additions/calculations of attached documentation checked ____________________

Payment reviewed ____________________

Payment approved ____________________

COST CATEGORIES*

0000 Salaries & Wages 0000 Travel & Associated Expenses

0000 Benefits 0000 Supplies & Equipment 0000 Fees/Honoraria 0000 Purchased Services 0000 General Administrative 0000 Education & Training * Cost categories based on your organization's Chart of Accounts.

Financial Management Module v. 1

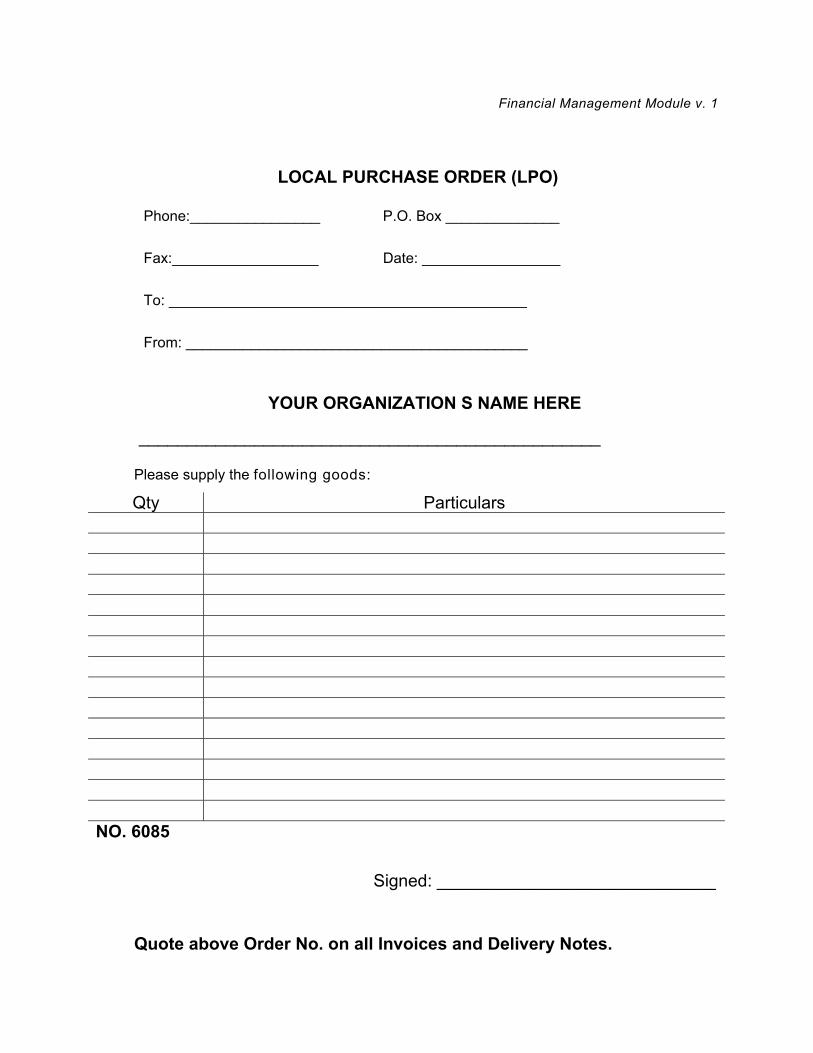

LOCAL PURCHASE ORDER (LPO)

Phone:________________ P.O. Box ______________

Fax:__________________ Date: _________________

To: ____________________________________________

From: __________________________________________

YOUR ORGANIZATION S NAME HERE

________________________________________________

Please supply the following goods:

Qty Particulars NO. 6085

Signed: _____________________________

Quote above Order No. on all Invoices and Delivery Notes.

Annex FInternal Questionnaires and Checklists

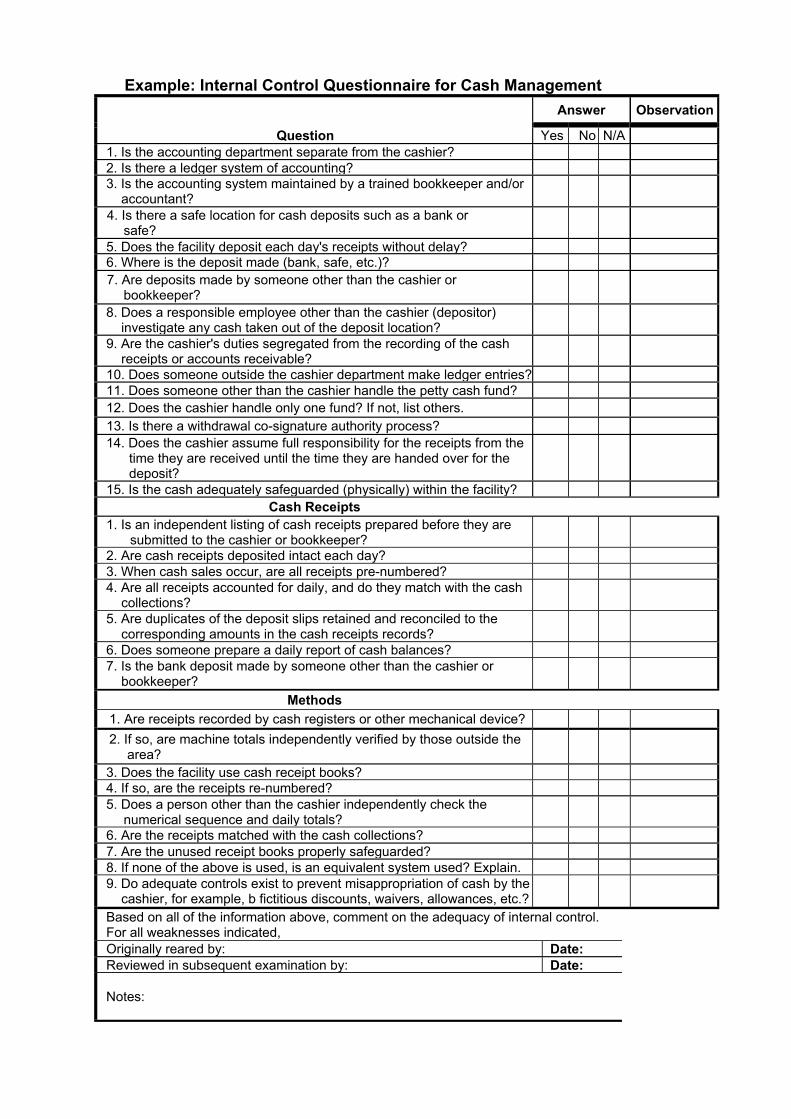

Example: Internal Control Questionnaire for Cash ManagementAnswer Observation

Question Yes No N/A1. Is the accounting department separate from the cashier?2. Is there a ledger system of accounting?3. Is the accounting system maintained by a trained bookkeeper and/or

accountant?4. Is there a safe location for cash deposits such as a bank or

safe?5. Does the facility deposit each day's receipts without delay?6. Where is the deposit made (bank, safe, etc.)?7. Are deposits made by someone other than the cashier or

bookkeeper?8. Does a responsible employee other than the cashier (depositor)

investigate any cash taken out of the deposit location?9. Are the cashier's duties segregated from the recording of the cash

receipts or accounts receivable?10. Does someone outside the cashier department make ledger entries?11. Does someone other than the cashier handle the petty cash fund?12. Does the cashier handle only one fund? If not, list others.13. Is there a withdrawal co-signature authority process?14. Does the cashier assume full responsibility for the receipts from the

time they are received until the time they are handed over for thedeposit?

15. Is the cash adequately safeguarded (physically) within the facility?Cash Receipts

1. Is an independent listing of cash receipts prepared before they aresubmitted to the cashier or bookkeeper?

2. Are cash receipts deposited intact each day?3. When cash sales occur, are all receipts pre-numbered?4. Are all receipts accounted for daily, and do they match with the cash

collections?5. Are duplicates of the deposit slips retained and reconciled to the

corresponding amounts in the cash receipts records?6. Does someone prepare a daily report of cash balances?7. Is the bank deposit made by someone other than the cashier or

bookkeeper?Methods

1. Are receipts recorded by cash registers or other mechanical device?2. If so, are machine totals independently verified by those outside the

area?3. Does the facility use cash receipt books?4. If so, are the receipts re-numbered?5. Does a person other than the cashier independently check the

numerical sequence and daily totals?6. Are the receipts matched with the cash collections?7. Are the unused receipt books properly safeguarded?8. If none of the above is used, is an equivalent system used? Explain.9. Do adequate controls exist to prevent misappropriation of cash by the

cashier, for example, b fictitious discounts, waivers, allowances, etc.?Based on all of the information above, comment on the adequacy of internal control.For all weaknesses indicated,Originally reared by: Date:Reviewed in subsequent examination by: Date:

Notes:

12

3

4

5

6

7

8

9

1

1

1

1

Bit

O

R

N

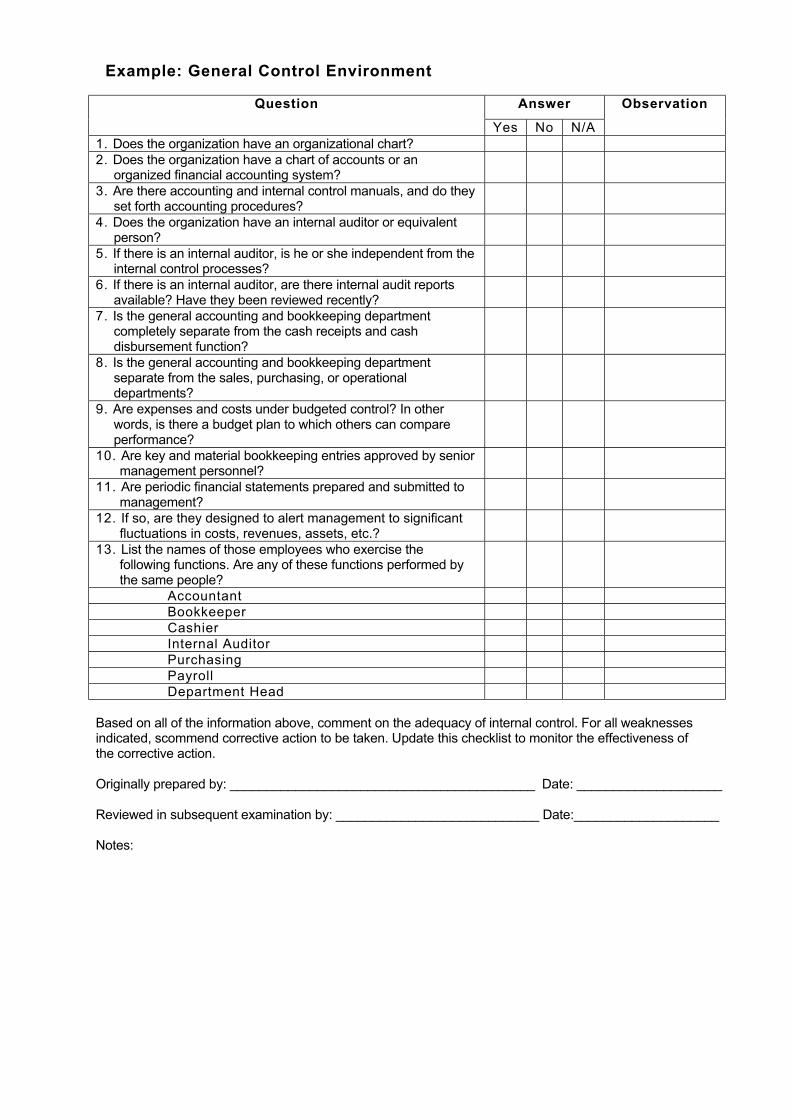

Example: General Control Environment

AnswerQuestion

Yes No N/A

Observation

. Does the organization have an organizational chart?

. Does the organization have a chart of accounts or anorganized financial accounting system?

. Are there accounting and internal control manuals, and do theyset forth accounting procedures?

. Does the organization have an internal auditor or equivalentperson?

. If there is an internal auditor, is he or she independent from theinternal control processes?

. If there is an internal auditor, are there internal audit reportsavailable? Have they been reviewed recently?

. Is the general accounting and bookkeeping departmentcompletely separate from the cash receipts and cashdisbursement function?

. Is the general accounting and bookkeeping departmentseparate from the sales, purchasing, or operationaldepartments?

. Are expenses and costs under budgeted control? In otherwords, is there a budget plan to which others can compareperformance?

0. Are key and material bookkeeping entries approved by seniormanagement personnel?

1. Are periodic financial statements prepared and submitted tomanagement?

2. If so, are they designed to alert management to significantfluctuations in costs, revenues, assets, etc.?

3. List the names of those employees who exercise thefollowing functions. Are any of these functions performed bythe same people?

AccountantBookkeeperCashierInternal AuditorPurchasingPayrollDepartment Head

ased on all of the information above, comment on the adequacy of internal control. For all weaknessesndicated, scommend corrective action to be taken. Update this checklist to monitor the effectiveness ofhe corrective action.

riginally prepared by: __________________________________________ Date: ____________________

eviewed in subsequent examination by: ____________________________ Date:____________________

otes:

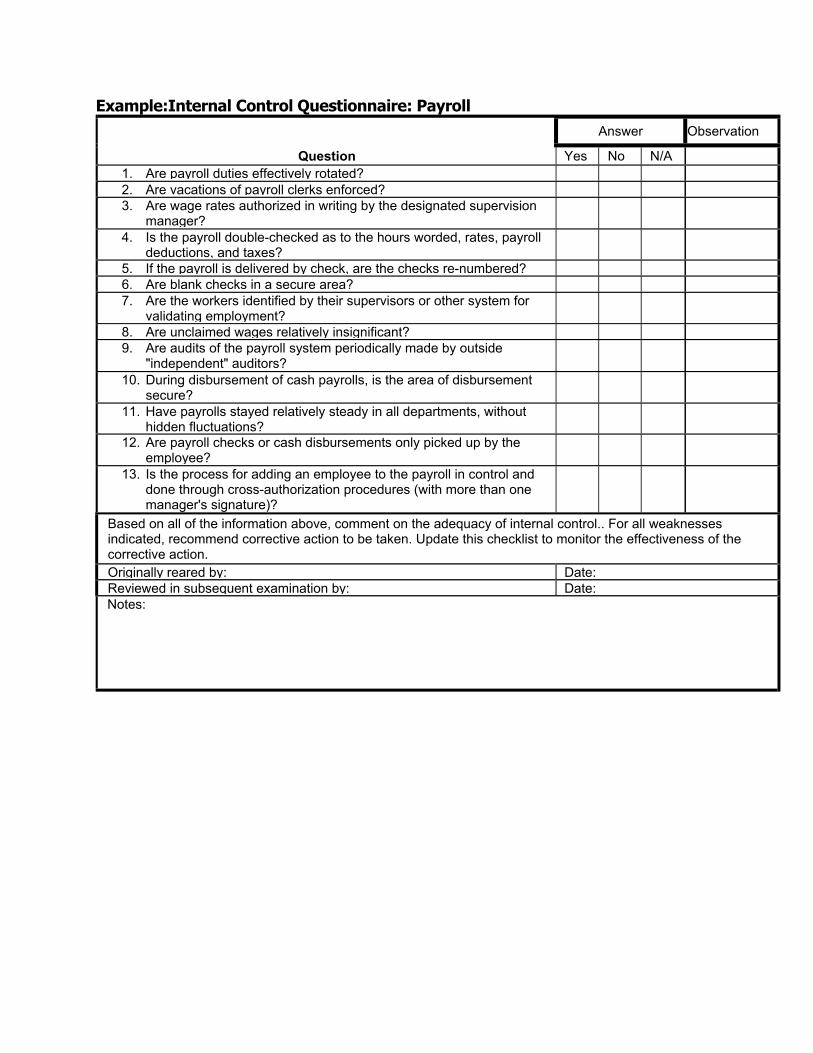

Example:Internal Control Questionnaire: Payroll

Answer Observation

Question Yes No N/A 1. Are payroll duties effectively rotated? 2. Are vacations of payroll clerks enforced? 3. Are wage rates authorized in writing by the designated supervision

manager?

4. Is the payroll double-checked as to the hours worded, rates, payroll deductions, and taxes?

5. If the payroll is delivered by check, are the checks re-numbered? 6. Are blank checks in a secure area? 7. Are the workers identified by their supervisors or other system for

validating employment?

8. Are unclaimed wages relatively insignificant? 9. Are audits of the payroll system periodically made by outside

"independent" auditors?

10. During disbursement of cash payrolls, is the area of disbursement secure?

11. Have payrolls stayed relatively steady in all departments, without hidden fluctuations?

12. Are payroll checks or cash disbursements only picked up by the employee?

13. Is the process for adding an employee to the payroll in control and done through cross-authorization procedures (with more than one manager's signature)?

Based on all of the information above, comment on the adequacy of internal control.. For all weaknesses indicated, recommend corrective action to be taken. Update this checklist to monitor the effectiveness of the corrective action. Originally reared by: Date: Reviewed in subsequent examination by: Date: Notes:

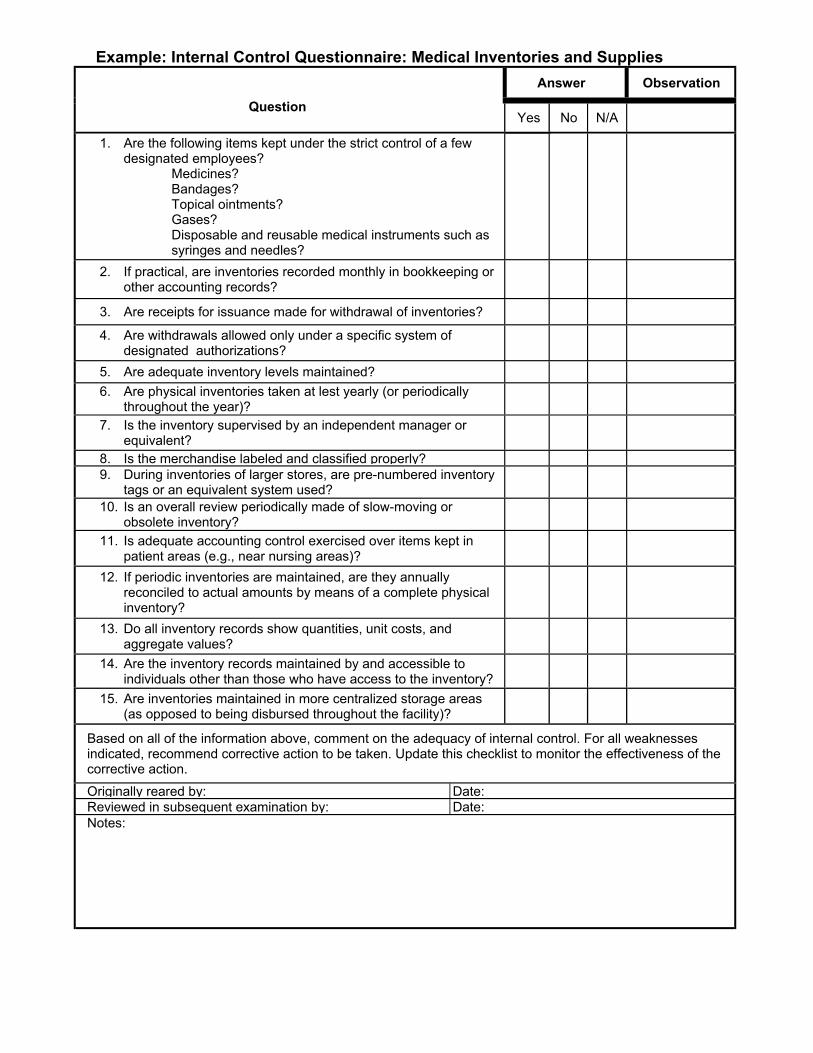

Example: Internal Control Questionnaire: Medical Inventories and Supplies Answer Observation

Question Yes No N/A

1. Are the following items kept under the strict control of a few designated employees?

Medicines? Bandages? Topical ointments? Gases? Disposable and reusable medical instruments such as syringes and needles?

2. If practical, are inventories recorded monthly in bookkeeping or other accounting records?

3. Are receipts for issuance made for withdrawal of inventories?

4. Are withdrawals allowed only under a specific system of designated authorizations?

5. Are adequate inventory levels maintained? 6. Are physical inventories taken at lest yearly (or periodically

throughout the year)?

7. Is the inventory supervised by an independent manager or equivalent?

8. Is the merchandise labeled and classified properly? 9. During inventories of larger stores, are pre-numbered inventory

tags or an equivalent system used?

10. Is an overall review periodically made of slow-moving or obsolete inventory?

11. Is adequate accounting control exercised over items kept in patient areas (e.g., near nursing areas)?

12. If periodic inventories are maintained, are they annually reconciled to actual amounts by means of a complete physical inventory?

13. Do all inventory records show quantities, unit costs, and aggregate values?

14. Are the inventory records maintained by and accessible to individuals other than those who have access to the inventory?

15. Are inventories maintained in more centralized storage areas (as opposed to being disbursed throughout the facility)?

Based on all of the information above, comment on the adequacy of internal control. For all weaknesses indicated, recommend corrective action to be taken. Update this checklist to monitor the effectiveness of the corrective action. Originally reared by: Date: Reviewed in subsequent examination by: Date: Notes:

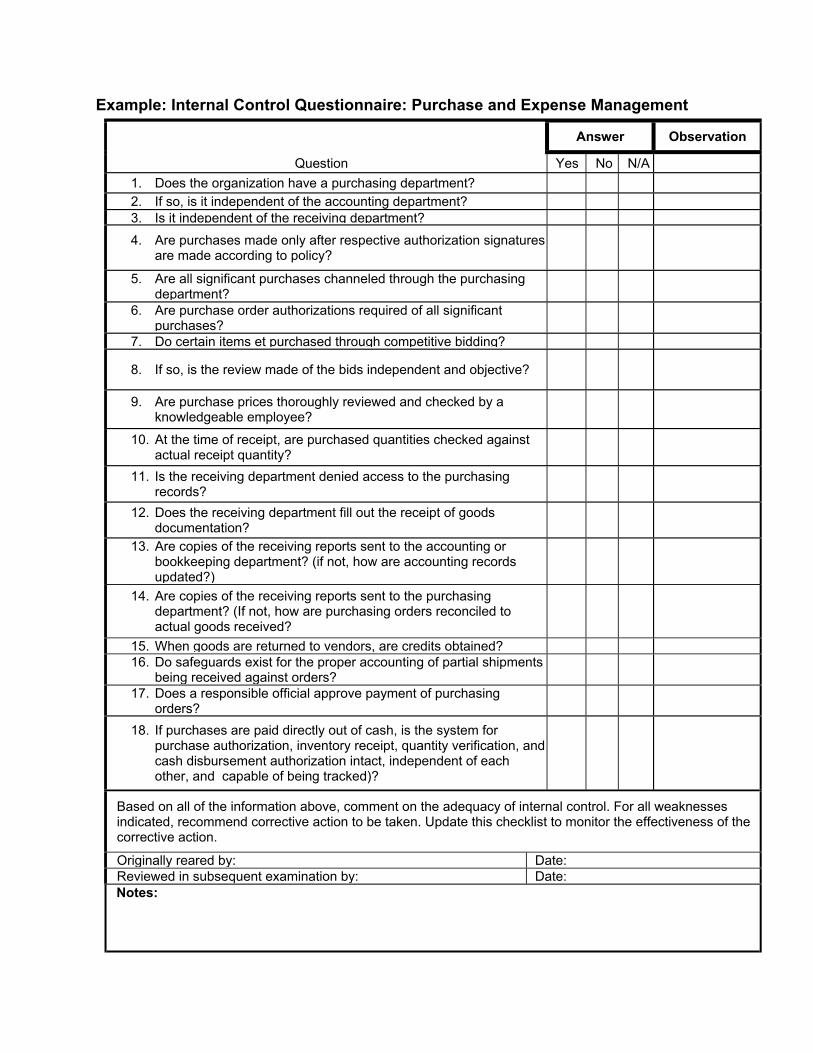

Example: Internal Control Questionnaire: Purchase and Expense Management

Answer Observation

Question Yes No N/A 1. Does the organization have a purchasing department? 2. If so, is it independent of the accounting department? 3. Is it independent of the receiving department? 4. Are purchases made only after respective authorization signatures

are made according to policy?

5. Are all significant purchases channeled through the purchasing department?

6. Are purchase order authorizations required of all significant purchases?

7. Do certain items et purchased through competitive bidding?

8. If so, is the review made of the bids independent and objective?

9. Are purchase prices thoroughly reviewed and checked by a knowledgeable employee?

10. At the time of receipt, are purchased quantities checked against actual receipt quantity?

11. Is the receiving department denied access to the purchasing records?

12. Does the receiving department fill out the receipt of goods documentation?

13. Are copies of the receiving reports sent to the accounting or bookkeeping department? (if not, how are accounting records updated?)

14. Are copies of the receiving reports sent to the purchasing department? (If not, how are purchasing orders reconciled to actual goods received?

15. When goods are returned to vendors, are credits obtained? 16. Do safeguards exist for the proper accounting of partial shipments

being received against orders?

17. Does a responsible official approve payment of purchasing orders?

18. If purchases are paid directly out of cash, is the system for purchase authorization, inventory receipt, quantity verification, and cash disbursement authorization intact, independent of each other, and capable of being tracked)?

Based on all of the information above, comment on the adequacy of internal control. For all weaknesses indicated, recommend corrective action to be taken. Update this checklist to monitor the effectiveness of the corrective action.

Originally reared by: Date: Reviewed in subsequent examination by: Date: Notes:

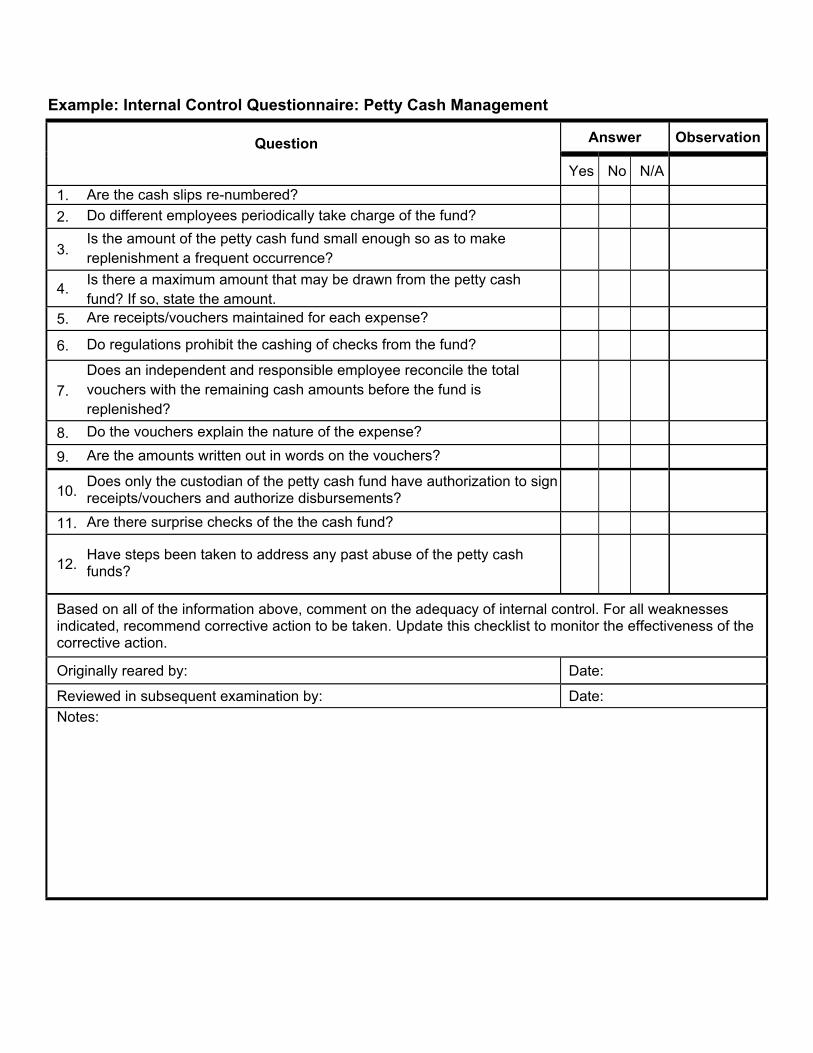

Example: Internal Control Questionnaire: Petty Cash Management

Answer Observation

Question

Yes No N/A 1. Are the cash slips re-numbered? 2. Do different employees periodically take charge of the fund?

3. Is the amount of the petty cash fund small enough so as to make replenishment a frequent occurrence?

4. Is there a maximum amount that may be drawn from the petty cash fund? If so, state the amount.

5. Are receipts/vouchers maintained for each expense?

6. Do regulations prohibit the cashing of checks from the fund?

7. Does an independent and responsible employee reconcile the total vouchers with the remaining cash amounts before the fund is replenished?

8. Do the vouchers explain the nature of the expense? 9. Are the amounts written out in words on the vouchers?

10. Does only the custodian of the petty cash fund have authorization to sign receipts/vouchers and authorize disbursements?

11. Are there surprise checks of the the cash fund?

12. Have steps been taken to address any past abuse of the petty cash funds?

Based on all of the information above, comment on the adequacy of internal control. For all weaknesses indicated, recommend corrective action to be taken. Update this checklist to monitor the effectiveness of the corrective action.

Originally reared by: Date:

Reviewed in subsequent examination by: Date: Notes:

Annex GModel Financial Reports

Financial Management Module v. 1

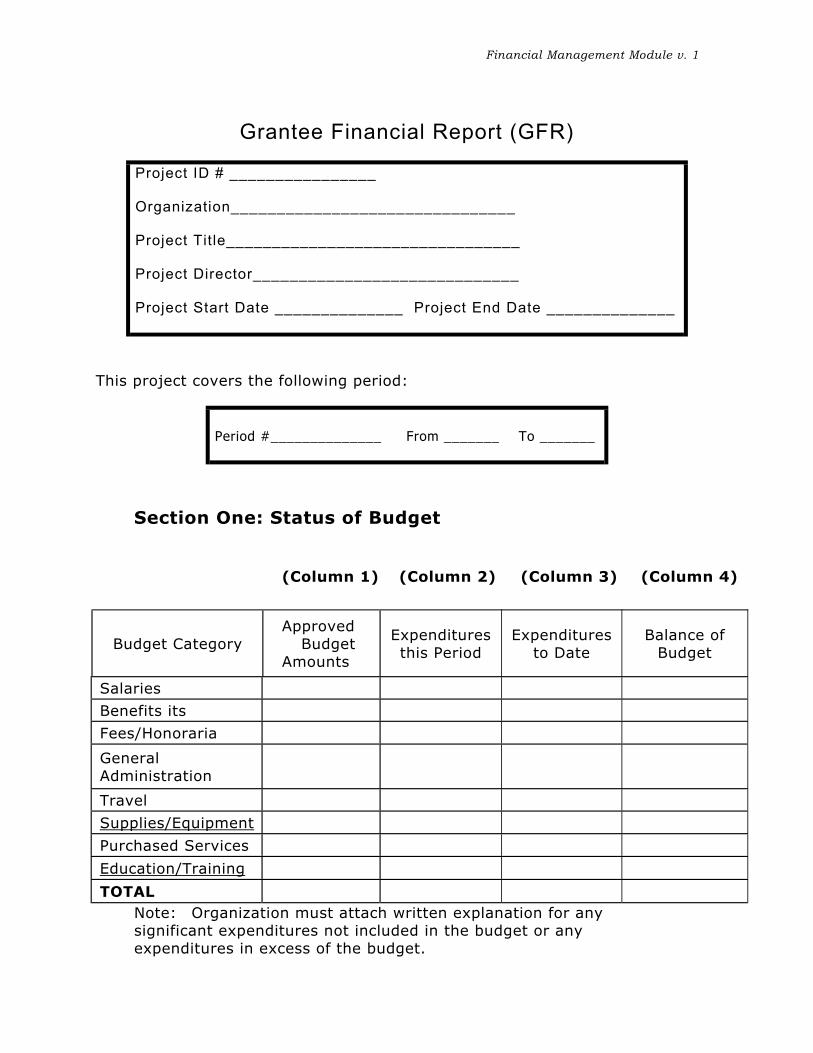

Grantee Financial Report (GFR)

Project ID # ________________ Organization_______________________________ Project Title________________________________ Project Director_____________________________ Project Start Date ______________ Project End Date ______________

This project covers the following period:

Period #______________ From _______ To _______

Section One: Status of Budget

(Column 1) (Column 2) (Column 3) (Column 4)

Budget Category Approved

Budget Amounts

Expenditures this Period

Expenditures to Date

Balance of Budget

Salaries

Benefits its

Fees/Honoraria

General Administration

Travel

Supplies/Equipment

Purchased Services

Education/Training

TOTAL Note: Organization must attach written explanation for any significant expenditures not included in the budget or any expenditures in excess of the budget.

Financial Management Module v. 1

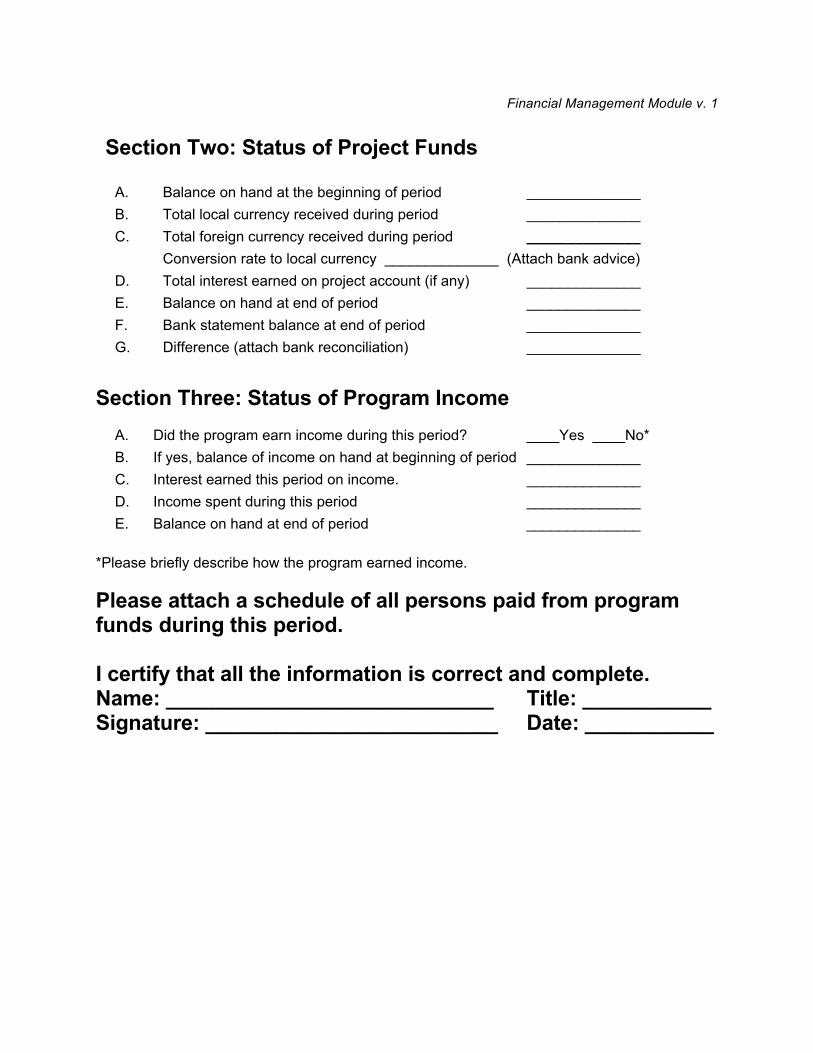

Section Two: Status of Project Funds

A. Balance on hand at the beginning of period ______________ B. Total local currency received during period ______________ C. Total foreign currency received during period ______________

Conversion rate to local currency ______________ (Attach bank advice) D. Total interest earned on project account (if any) ______________ E. Balance on hand at end of period ______________ F. Bank statement balance at end of period ______________ G. Difference (attach bank reconciliation) ______________

Section Three: Status of Program Income

A. Did the program earn income during this period? ____Yes ____No* B. If yes, balance of income on hand at beginning of period ______________ C. Interest earned this period on income. ______________ D. Income spent during this period ______________ E. Balance on hand at end of period ______________

*Please briefly describe how the program earned income. Please attach a schedule of all persons paid from program funds during this period. I certify that all the information is correct and complete. Name: ____________________________ Title: ___________ Signature: _________________________ Date: ___________