STRATEGIC MANAGEMENT ACCOUNTING - {$SEO … - Strat… · · 2015-09-01STRATEGIC MANAGEMENT...

24

STRATEGIC MANAGEMENT ACCOUNTING (BB315009S) Prepared by: MISS NURAZRIN BINTI JUPRI

Transcript of STRATEGIC MANAGEMENT ACCOUNTING - {$SEO … - Strat… · · 2015-09-01STRATEGIC MANAGEMENT...

STRATEGIC MANAGEMENTACCOUNTING

(BB315009S)

Prepared by:

MISS NURAZRIN BINTI JUPRI

Chapter 7:

Divisional Performance & Transfer Pricing 2

Purposes of transfer pricing

1. To provide information that motivates divisional managers to make good economic decisions.

2. To provide information that is useful for evaluating the managerial and economic performance of the divisions.

3. To intentionally move profits between divisions or locations.

4. To ensure that divisional autonomy is not undermined.

Information for making good decisions

• Intermediate products = Goods transferred from the supplying toreceiving division.

• Final products = Products sold by the receiving division to the outside world

Alternative transfer pricing methods

1. Market-based2. Marginal cost3. Full cost4. Cost-plus a mark-up5. Negotiated transfer prices

Market-based transfer prices

• Where there is a perfectly competitive market for the intermediateproduct, the current market price is the most suitable basis for setting the transfer prices.

• TP ’s will motivate sound decisions and form a suitable basis forperformance evaluation

Difficulties in determine market price:

• Comparable product

• Different suppliers – initial prices

• Different buyers - discounts, credit terms

• Internal transfer – involve savings

Marginal cost transfer prices

• Economic theory indicates TP based on the MC of producing theintermediate product at the optimum output level for the company as awhole will encourage total organizational optimality

• Adopting a short-run perspective to derive MC results in MC = VC and the assumption that MC is constant per unit throughout the relevant output range.

• MC not widely used:1. Provides poor information for performance evaluation2. MC may not be constant over entire range of output3. Measuring MC beyond short-term is difficult4. Managers reject short-term perspective

Figure 21.1 An illustration of cost-based transfer prices

Full cost transfer prices

• Widely used because managers require an estimate of long-runmarginal cost for decision-making.

• Traditional costing systems tend to provide poor estimates of longrun MC.

• Does not enable supplying division to report a profit on goodstransferred.

Cost-plus a mark-up transfer prices

• Attempts to meet the performance evaluation purpose of transfer pricing (profit allocated to the supplying division)

• Results in non-optimal decisions because TP exceeds short-run or long-run MC.

• Enormous mark-ups can result when goods/services are transferredbetween several divisions.

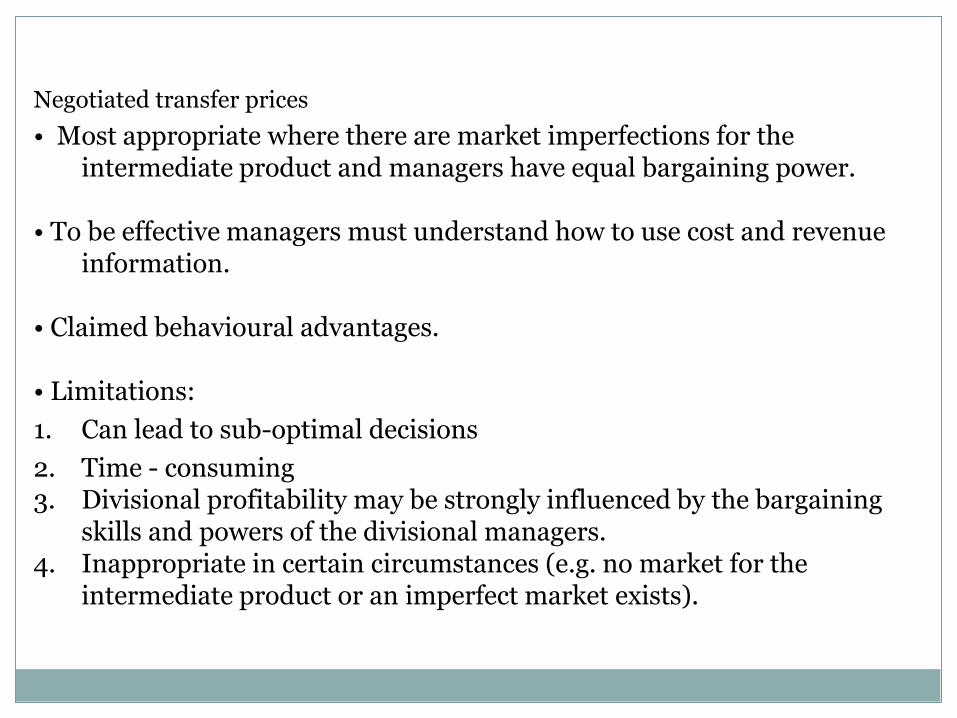

Negotiated transfer prices

• Most appropriate where there are market imperfections for theintermediate product and managers have equal bargaining power.

• To be effective managers must understand how to use cost and revenue information.

• Claimed behavioural advantages.

• Limitations:

1. Can lead to sub-optimal decisions

2. Time - consuming3. Divisional profitability may be strongly influenced by the bargaining

skills and powers of the divisional managers.4. Inappropriate in certain circumstances (e.g. no market for the

intermediate product or an imperfect market exists).

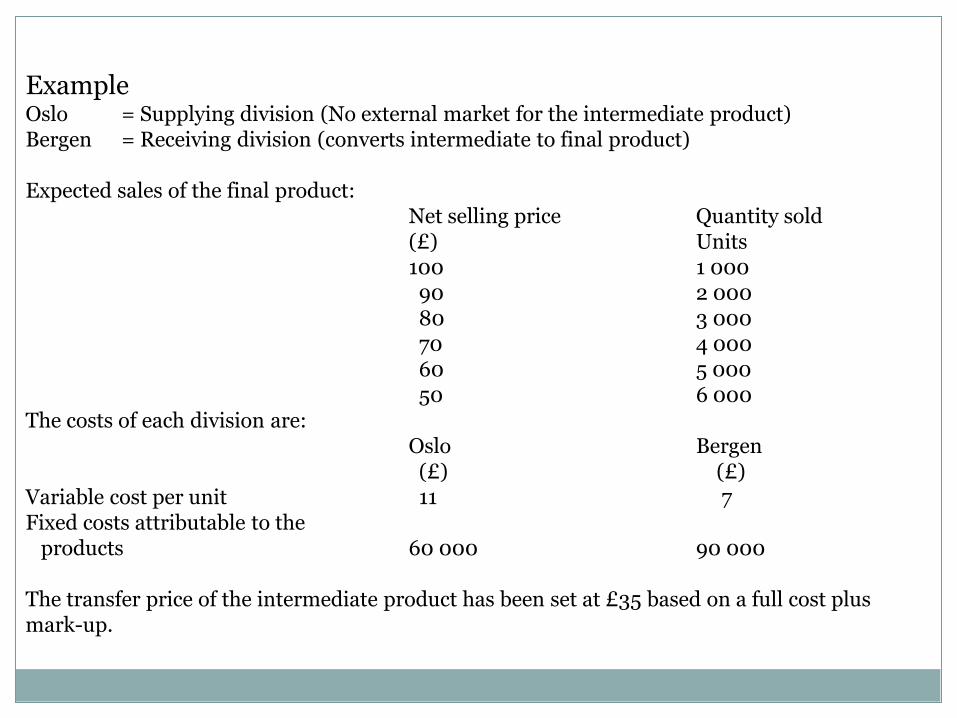

ExampleOslo = Supplying division (No external market for the intermediate product)Bergen = Receiving division (converts intermediate to final product)

Expected sales of the final product:Net selling price Quantity sold(£) Units100 1 00090 2 00080 3 00070 4 00060 5 00050 6 000

The costs of each division are:Oslo Bergen(£) (£)

Variable cost per unit 11 7Fixed costs attributable to the

products 60 000 90 000

The transfer price of the intermediate product has been set at £35 based on a full cost plus mark-up.

• £35 TP does not motivate optimum output level for the company as a whole.

• To ensure overall company optimality the TP must be set at MC of the intermediate product (i.e VC of £11 per unit or £11,000 per batch of 1,000 units).

• The receiving division will face the following net marginal revenue (NMR)schedule:

Units net marginal revenue (£)1 000 93 000 (100 000 – 7000)2 000 73 000 (80 000 – 7 000)3 000 * 53 000 (60 000 – 7 000)4 000 33 000 (40 000 – 7 000)5 000 13 000 (20 000 – 7 000)6 000 –7 000 (0 – 7 000)

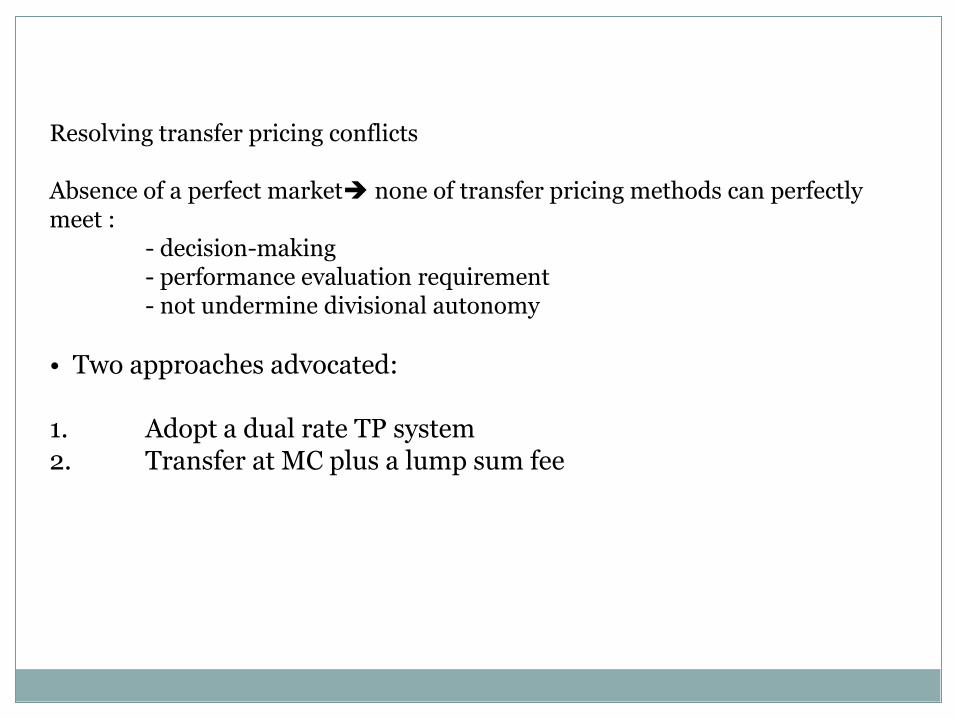

Resolving transfer pricing conflicts

Absence of a perfect market none of transfer pricing methods can perfectly meet :

- decision-making- performance evaluation requirement- not undermine divisional autonomy

• Two approaches advocated:

1. Adopt a dual rate TP system2. Transfer at MC plus a lump sum fee

Resolving transfer pricing conflicts (contd.)

Dual rate TP system

• Uses two transfer prices

1. Supplying division may receive full cost plus a mark-up so that it makes a profit on inter-divisional transfers

2. Receiving division charged at MC of transfers thus motivating managers to operate at the optimum output level for the company as a whole.

3. Profit on inter-group trading removed by an accounting adjustment.

• Not widely used because:

1. Use of two TP ’s causes confusion2. Seen as artificial3. Divisions protected from competition4. Reported inter-divisional profits can be misleading

Resolving transfer price conflicts (contd.)

Marginal cost plus a lump sum fee

• Intended to motivate receiving division to equate MC of transfers with its net marginal revenue to determine optimum company profit maximizing output level.

• Enables supplying division to cover its fixed costs and earn a profit on inter-divisional transfers through the fixed fee charged for the period.

• Motivates receiving division to consider full cost of providing intermediate products/services (.TP = £11 MC plus £60,000 lump sum plus a profit contribution in the example).

Domestic TP conclusions/recommendations

• Competitive market for the intermediate product — Use market prices.

• No market for the intermediate product — Transfer at MC plus a lump sum

• An imperfect market - negotiation may be appropriate in certain circumstances.

• Use standard costs for cost-based TP ’s

International transfer pricing

• Where divisions are located in different countries taxation implications become important and TP has the potential to ensure that most of the profits on inter-divisional transfers are allocated to the low taxation country.

Example

Supplying division in country A (Tax rate = 25%)

Receiving division in country B (Tax rate = 40%)

Motivation is to use highest possible TP so receiving division will have high costs and low profits whereas supplying division will have high revenues and high profits.

• Taxation authorities in most countries are wise to companies using TP to manipulate profits and seek to apply OECD guidelines based on arm ’s length pricing principles.

• TP can also have an impact on import duties and dividend repatriations.