Stocktake and Analysis of Australia's Water … Stocktake and Analysis of Australia’s Water...

306

Stocktake and Analysis of Australia's Water Accounting Practice FINAL REPORT Final 13 October 2006

Transcript of Stocktake and Analysis of Australia's Water … Stocktake and Analysis of Australia’s Water...

Stocktake and Analysis of Australia's Water Accounting Practice

FINAL REPORT

Final 13 October 2006

Stocktake and Analysis of Australia's Water Accounting Practice

FINAL REPORT Final 13 October 2006

Sinclair Knight Merz 12-14 William St PO Box 260 Tatura VIC 3616 Australia Tel: +61 3 5824 6400 Fax: +61 3 5824 6444 Web: www.skmconsulting.com COPYRIGHT: The concepts and information contained in this document are the property of Sinclair Knight Merz Pty Ltd. Use or copying of this document in whole or in part without the written permission of Sinclair Knight Merz constitutes an infringement of copyright.

LIMITATION: This report has been prepared on behalf of and for the exclusive use of Sinclair Knight Merz Pty Ltd’s Client, and is subject to and issued in connection with the provisions of the agreement between Sinclair Knight Merz and its Client. Sinclair Knight Merz accepts no liability or responsibility whatsoever for or in respect of any use of or reliance upon this report by any third party.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE i

Acknowledgements

The Stocktake and Analysis of Australia’s Water Accounting Practice and the recommendations for the development of water accounting in Australia were completed with the close assistance of the project’s Expert Advisory Panel and staff of organisations that participated in the stocktake.

The contributions by the members of the Expert Advisory Panel both at meetings and in providing written comment is particularly acknowledged as is the specific assistance from Maryanne Slattery and Dr. Lindsay White in making proactive contributions and assistance in relation to material about development of water accounting as a discipline.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE ii

Contents

Executive Summary 1

1 Introduction 12 1.1 Background 12 1.2 Project and report overview 13

2 Information Requirements 14 2.1 Approach 14 2.2 Desired outcomes and water accounting reports 17 2.3 The chart of water accounts 22 2.3.1 Information elements 22 2.3.2 Accounting entities for water 23 2.3.3 Using the chart of water accounts 26 2.3.4 Aggregating accounts to the state and national level 26 2.3.5 Moving to standard water accounting conventions 28 2.4 Standards 29 2.5 Accounting for environmental water 29 2.5.1 Instream environmental rights 29 2.5.2 Extractive environmental rights 30 2.5.3 Reporting on all environmental water 31

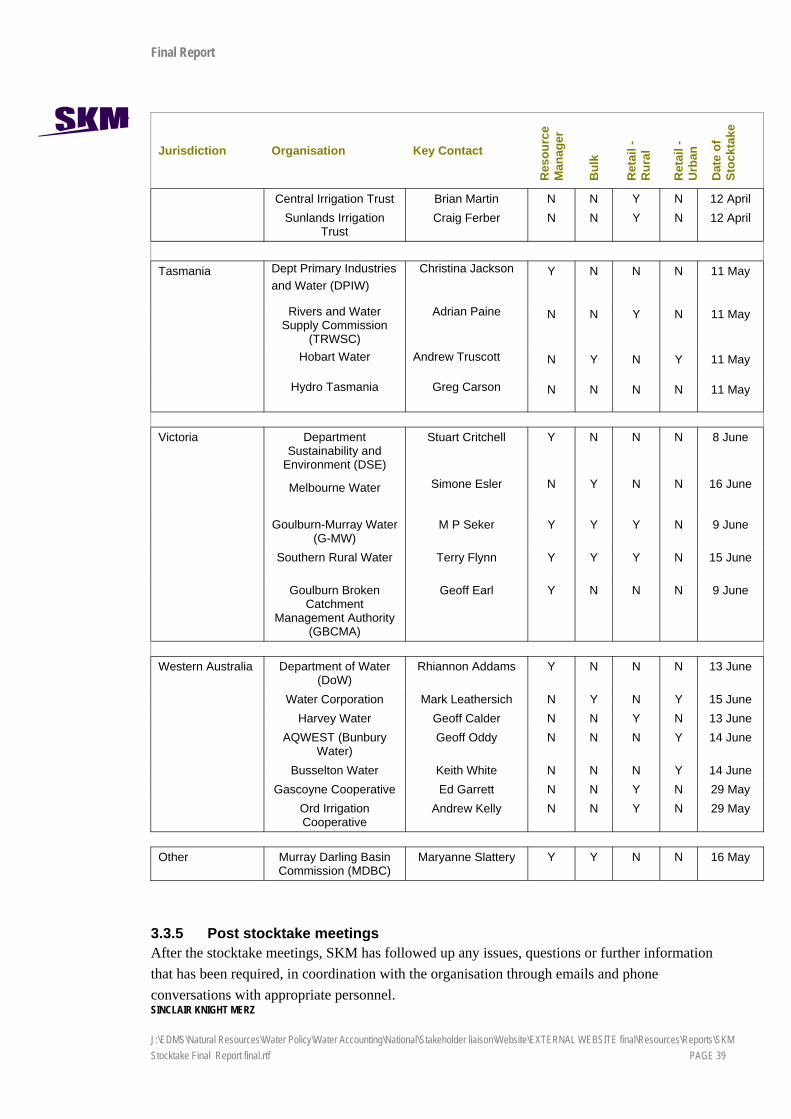

3 The Stocktake 32 3.1 Purpose 32 3.2 Scope 32 3.3 Method 33 3.3.1 Commitment building and stocktake inception 34 3.3.2 Adaptive approach 34 3.3.3 Stocktake forms 35 3.3.4 Stocktake meetings 37 3.3.5 Post stocktake meetings 39 3.4 Definition of water accounting 40

4 Stocktake Findings 41 4.1 Measuring physical water parameters 41 4.1.1 River levels and flows 42 4.1.2 Pipe flows 42 4.1.3 Artificial channel flows 43 4.1.4 Rainfall, evaporation and transpiration 44 4.1.5 Groundwater levels 44

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE iii

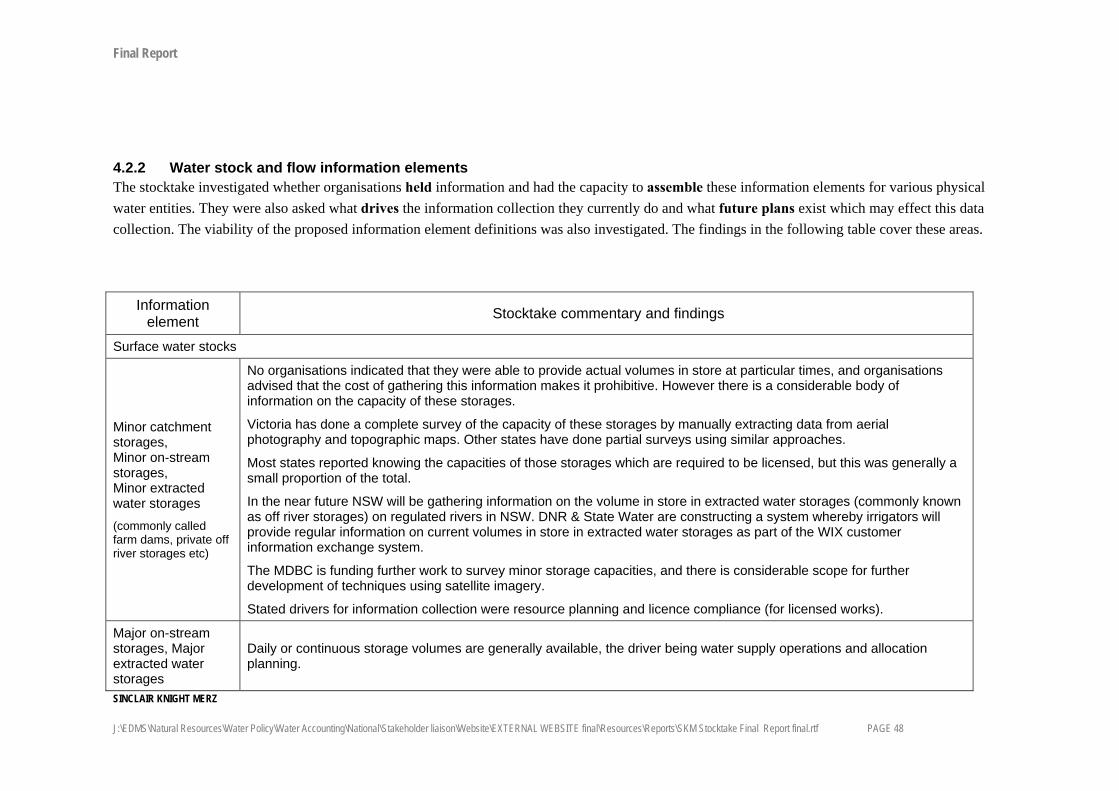

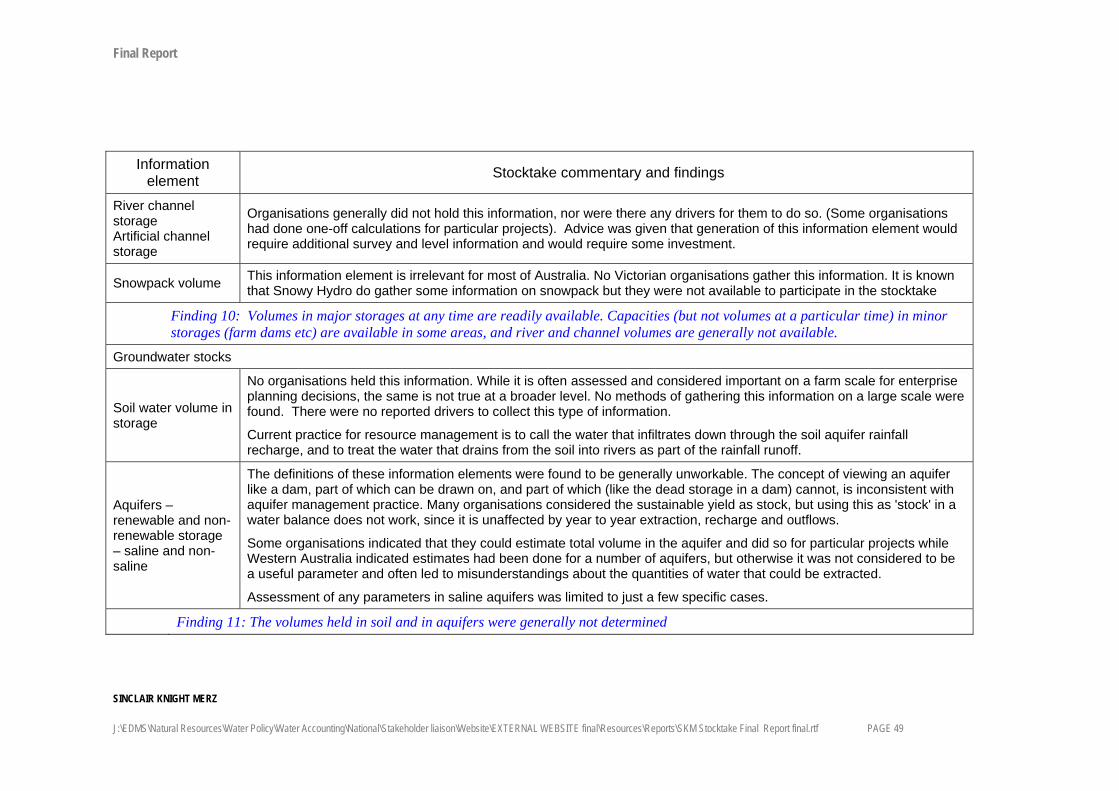

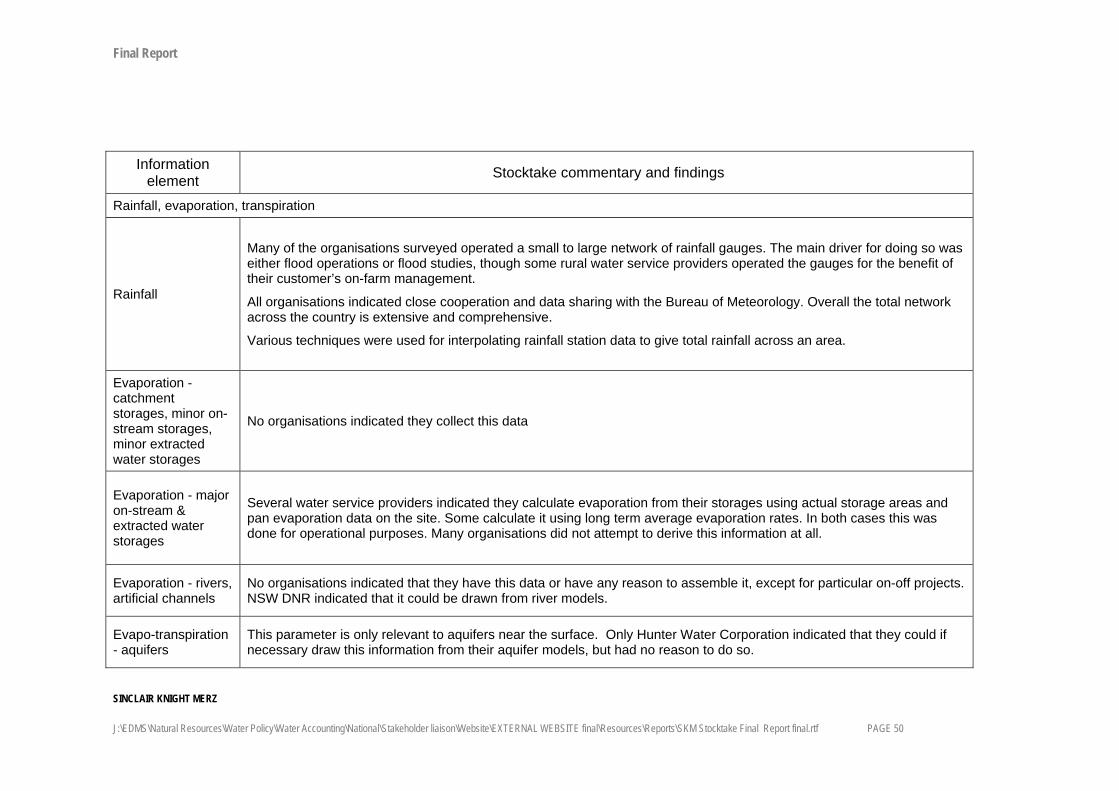

4.1.6 Broadscale charting of farm dams 45 4.2 Assembling chart of accounts information 45 4.2.1 Reporting units - use of physical water entities 45 4.2.2 Water stock and flow information elements 48 4.2.3 Water use information elements 57 4.2.4 Water entitlements and allocations information elements 59 4.2.5 Environmental rules information elements 61 4.2.6 Terminology 62 4.2.7 Standards 64 4.3 Recording water information 65 4.3.1 Information store types 65 4.3.2 Recording of information elements 67 4.3.3 Use of standards and quality assurance 71 4.3.4 Access and security 72 4.3.5 Application of accounting principles 75 4.4 Reporting water information 77 4.4.1 Existing reports including water accounting information 77 4.4.2 Capacity to prepare proposed water cycle reports 78 4.4.3 Capacity to prepare proposed surface water reports (water balances) 78 4.4.4 Capacity to prepare proposed groundwater reports 82 4.4.5 Capacity to prepare proposed water access entitlement, water allocation and trade reports 82 4.4.6 Capacity to prepare proposed water use reports 87 4.4.7 Capacity to prepare proposed environmental rules reports 88 4.4.8 Aggregation of reporting information 89 4.5 General findings 91 4.5.1 Potential for reporting overload 91 4.5.2 Cooperation of participating organisations 91 4.5.3 Organisational capability 92 4.5.4 Functional management levels 92 4.6 Stocktake conclusion 92 4.7 Summary of stocktake findings 93 4.7.1 Measuring physical water parameters 93 4.7.2 Assembling chart of accounts information 93 4.7.3 Recording water information 95 4.7.4 Reporting water information 97 4.7.5 General findings 98

5 Analysis of water accounting as a discipline 99 5.1 Context 99 5.2 What is water accounting? 101 5.3 Proposed National Water Accounting Process 102

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE iv

5.4 Institutional arrangements 104 5.5 Identification of user requirements 110 5.6 Conceptual framework 112 5.7 Procedure for setting of water accounting standards 116 5.8 Common chart of water accounts 118 5.9 Accounting systems 121 5.9.2 Starting points for water information system standardisation 124 5.10 Water accounting standards 125 5.11 Reporting, obligations and compliance 126 5.12 Assurance 128 5.13 Capacity building 129

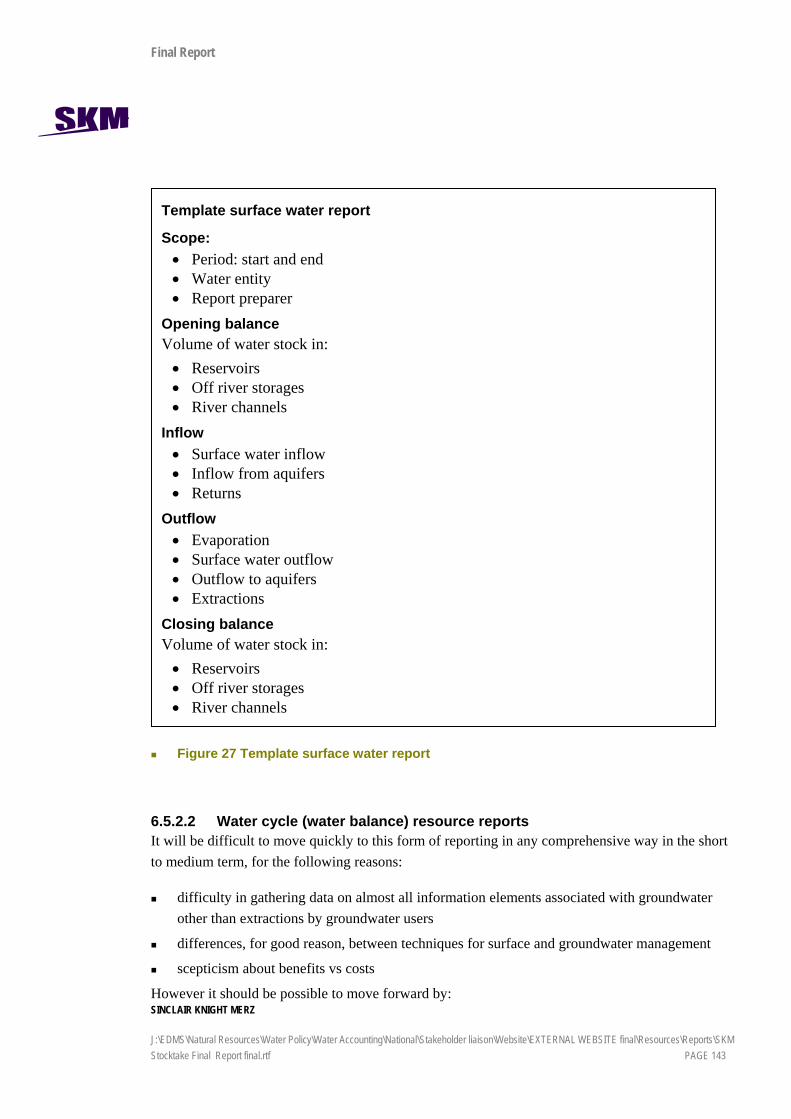

6 Analysis of water resource accounting 130 6.1 Description and scope of theme 130 6.2 Objective 130 6.3 Current drivers 131 6.4 Concepts and definitions 132 6.4.1 Water resource accounting 132 6.4.2 Environment vs economy, public and private water 134 6.4.3 Modified water cycle reports 137 6.5 Reporting 139 6.5.1 Reporting obligations 139 6.5.2 Standard reports 142 6.5.3 Water entities for reporting 148 6.5.4 Report periods 148 6.6 Measurement 149 6.6.1 Standards and methods 149 6.6.2 Resolving ‘balancing items’ in reports 150 6.6.3 Information elements in surface water resource accounts 150 6.6.4 Additional information elements in full water cycle accounts 154 6.7 Recording water resource information 157 6.7.1 Starting points for standardisation 158 6.7.2 Quality labelling 159 6.7.3 Quality assurance 159

7 Analysis of water market accounting 161 7.1 Water access entitlements 161 7.1.1 Description and scope of theme 161 7.1.2 Objective 161 7.1.3 Current drivers 162 7.1.4 Concepts and definitions 162

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE v

7.1.5 Water systems 165 7.1.6 Reporting 167 7.1.7 Measuring 172 7.1.8 Recording 173 7.2 Water Allocations 175 7.2.1 Description and scope of theme 175 7.2.2 Objective 175 7.2.3 Current drivers 175 7.2.4 Concepts and definitions 176 7.2.4.3 Regulated river allocated and unallocated stock and the consumptive 178 7.2.5 Allocation reporting levels 178 7.2.6 Reporting 182 7.2.7 Recording 190 7.2.8 Measurement 193

8 Analysis of environmental water accounting 195 8.1 Scope of environmental water accounting 195 8.2 Objective 200 8.3 Discussion of environmental water concepts 202 8.3.1 Unregulated streams 202 8.3.2 Regulated streams 202 8.4 Types of environmental right 205 8.4.1 Instream environmental rights 206 8.4.2 Extractive environmental rights 207 8.5 Recording and reporting 208 8.5.1 Instream environmental rights 208 8.5.2 Extractive environmental rights 210 8.6 Environment as a unique holder of rights 211 8.7 Measurement 211 8.8 Recording 212 8.9 Opportunities for improvement 212 8.9.1 Consistency of language 212 8.9.2 Consistency of methods of estimation 213 8.9.3 Consistent presentation 213 8.9.4 Annual plans 213

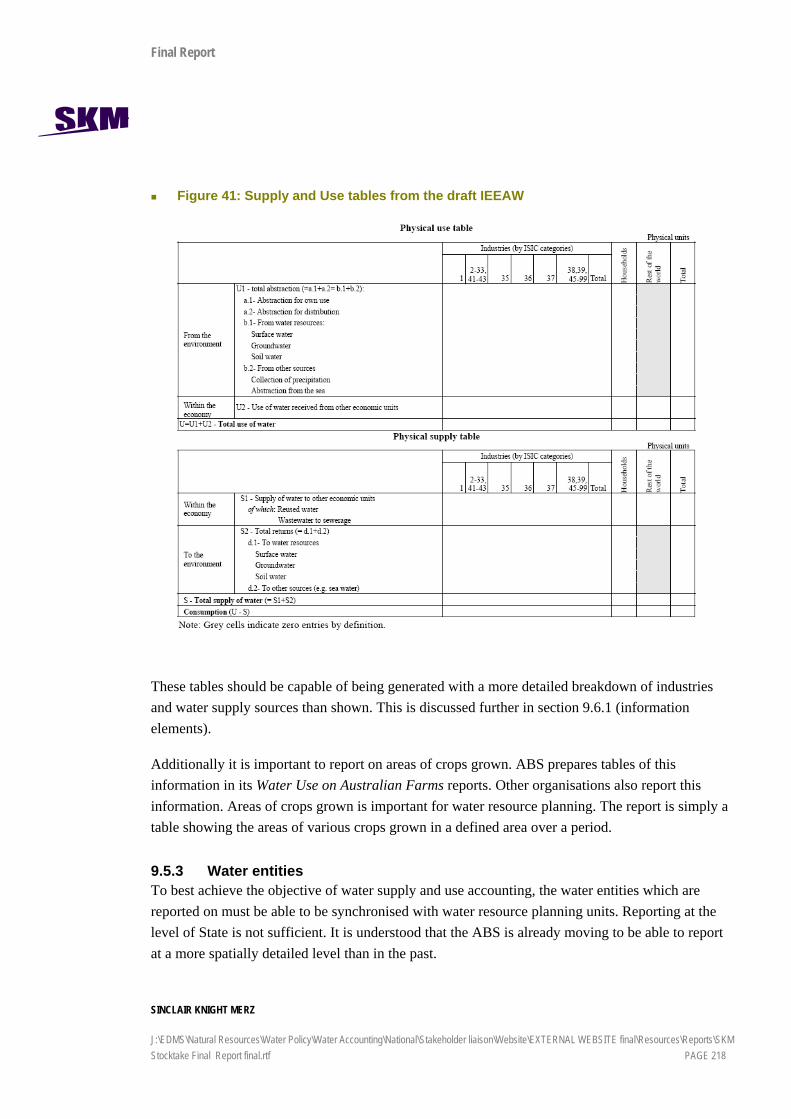

9 Analysis of water use accounting 215 9.1 Description and scope of theme 215 9.2 Objective 215 9.3 Current drivers 216 9.4 Concepts and definitions 217

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE vi

9.5 Reporting 217 9.5.1 Reporting obligations 217 9.5.2 Standard reports 217 9.5.3 Water entities 218 9.5.4 Reporting periods 219 9.5.5 Aggregation 219 9.6 Measuring 219 9.6.1 Information elements 219 9.6.2 Information gaps 220 9.6.3 Standards and methods 220 9.7 Recording 221 9.7.1 System features 221 9.7.2 Reconciliation 222

10 Recommendations 223 10.1 Context 223 10.2 The way forward 224 10.3 What is water accounting? 225 10.4 Proposed National Water Accounting Process 225 10.5 Institutional arrangements 227 10.6 Capacity building 229 10.7 Identification of user requirements 230 10.8 Conceptual framework 232 10.9 Procedure for setting of water accounting standards 233 10.10 Common chart of water accounts 234 10.11 Arrangements for water accounting development 236 10.12 Priorities for development of water accounting standards 238 10.13 Water accounting information systems 244 10.14 Work plan and resourcing estimates 248

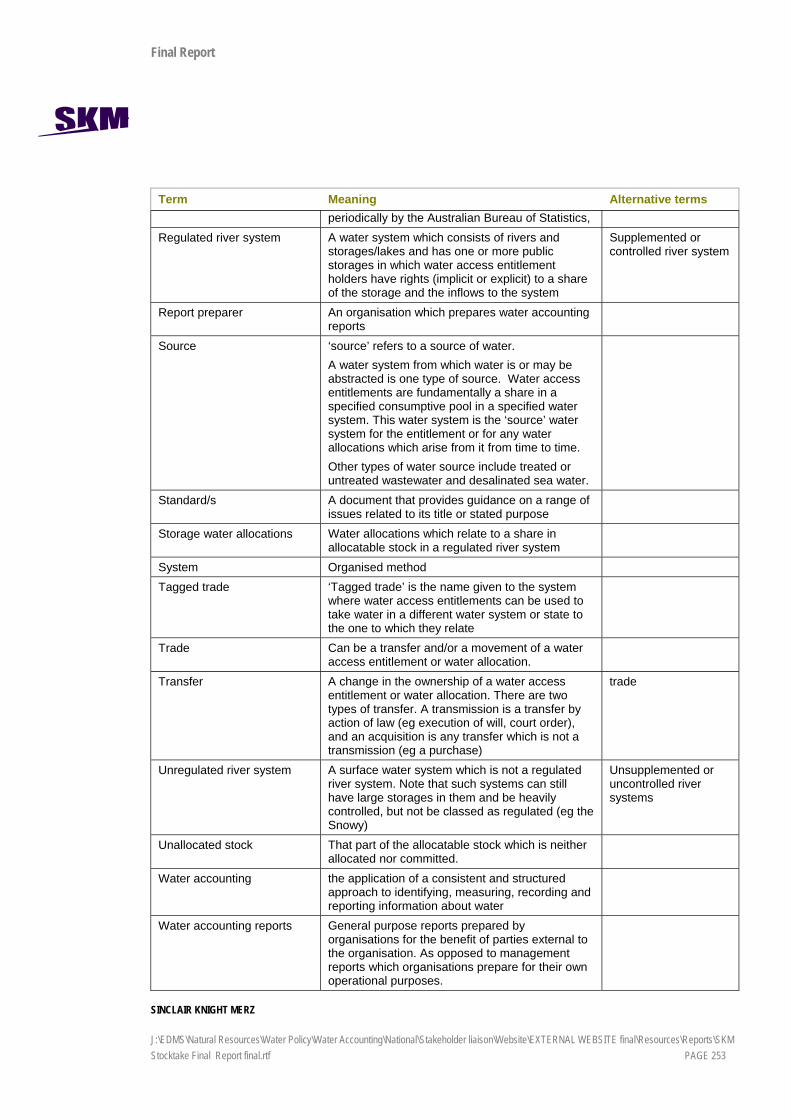

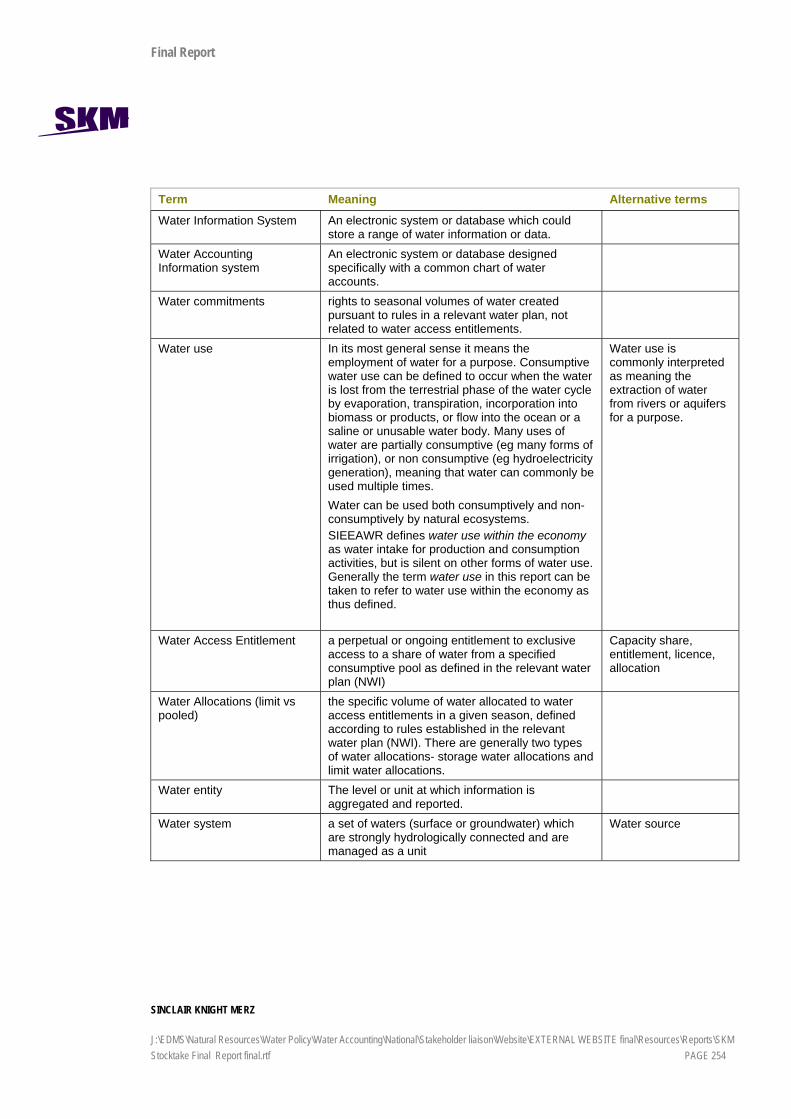

Appendix A Glossary of Terms 252

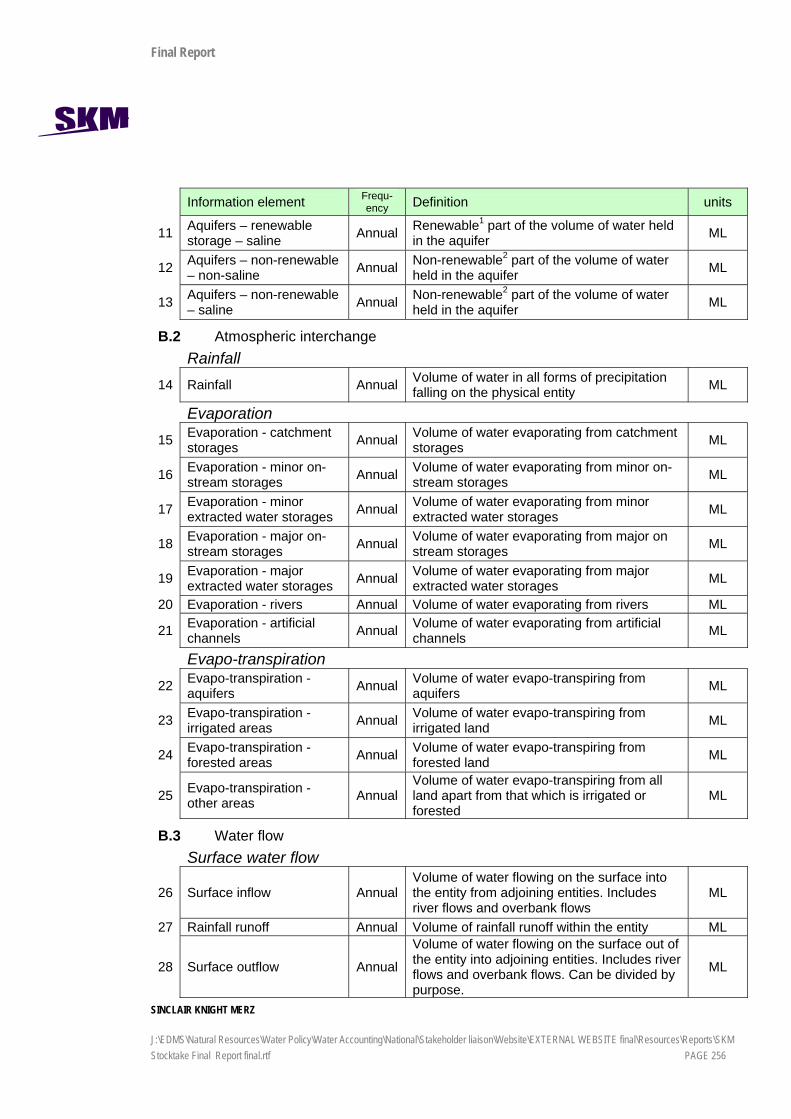

Appendix B Information elements 255 B.1 Water stock 255 B.2 Atmospheric interchange 256 B.3 Water flow 256 B.4 Water use 258 B.5 Water access entitlement 260 B.6 Water allocation 261 B.7 Environmental water rules 262

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE vii

Appendix C Water information systems 264

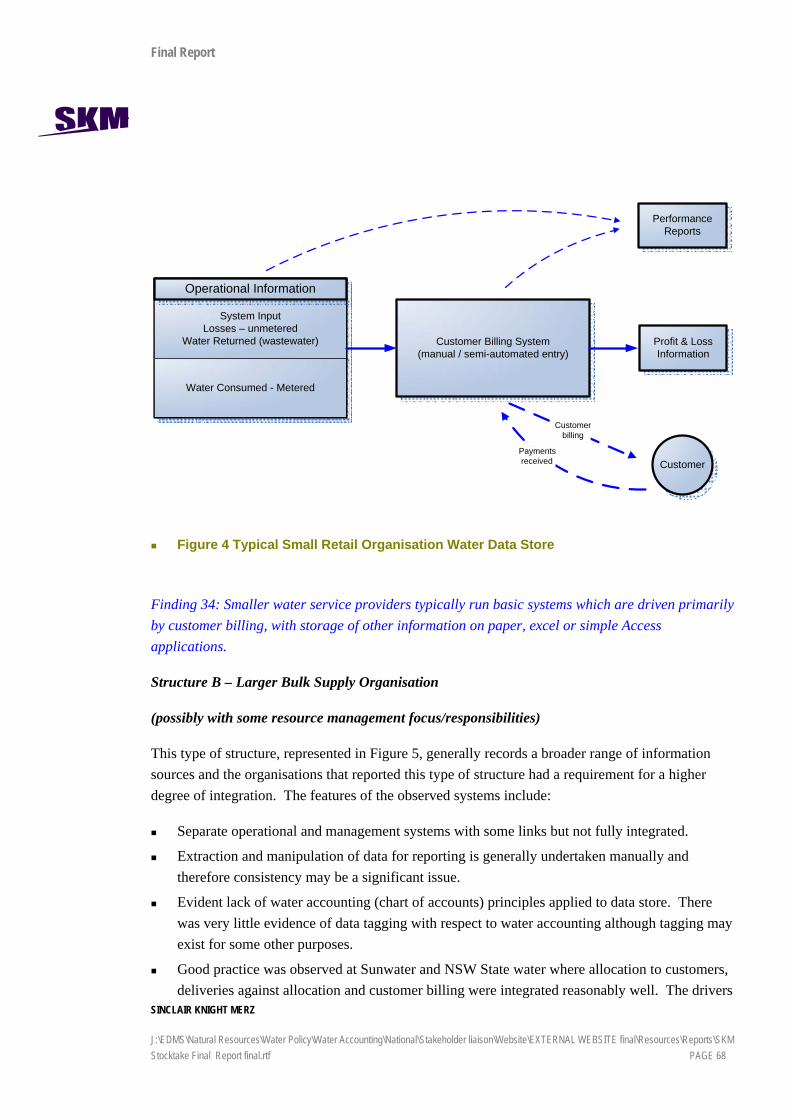

Appendix D Examples of published water accounting information – urban water service providers 273

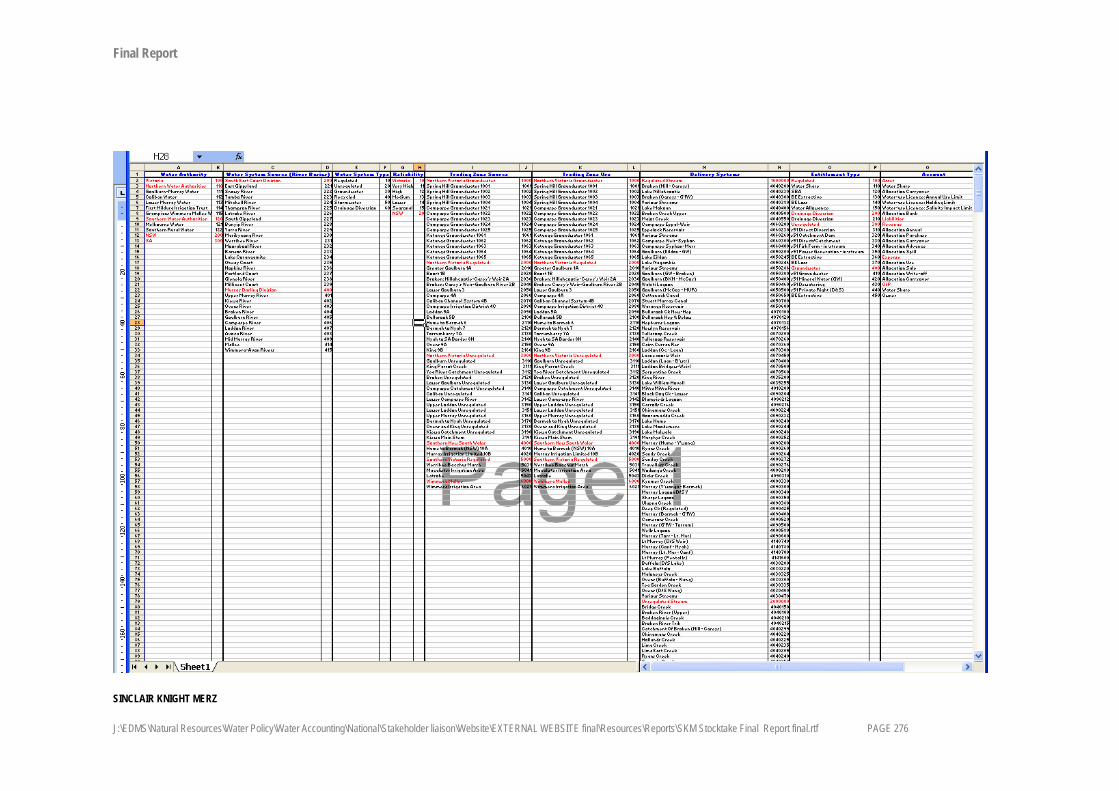

Appendix E Example chart of water accounts 275

Appendix F Example water accounting standard for materiality 277

Appendix G Murray Darling Basin case study 282 G.1 Background 282 G.2 Classes of environmental water 282 G.3 Conversion between instream and extractive rights 284 G.3.1 Conversion of extractive use to instream use 284 G.3.2 Conversion of instream use to extractive use 285 G.4 River loss or environmental use? 286

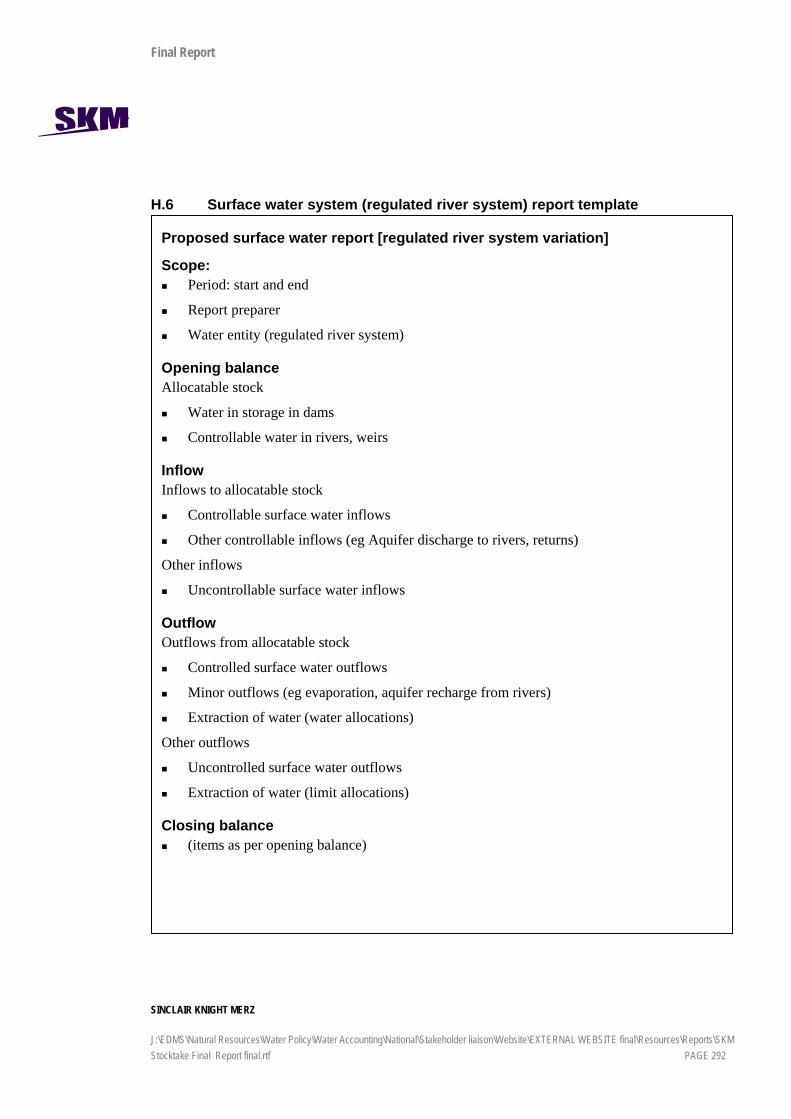

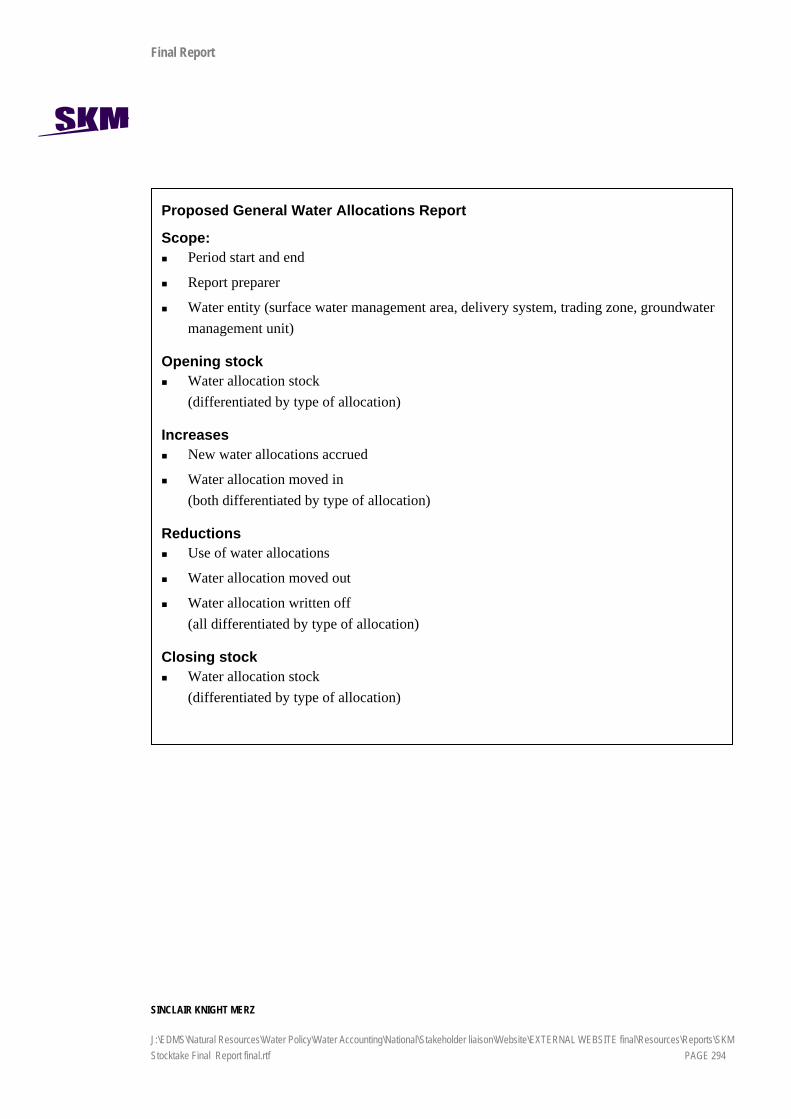

Appendix H Consolidated report templates 287 H.1 Surface water report template 287 H.2 Water cycle report template 288 H.3 Groundwater report template 289 H.4 Water access entitlement source report template 290 H.5 Water access entitlement destination report 291 H.6 Surface water system (regulated river system) report template 292 H.7 Allocatable stock report template 293 H.8 General water allocation trade report template 295

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE viii

Document history and status

Revision Date issued

Reviewed by Approved by Date approved Revision type

First Draft Stocktake Report

Draft 1 23/6/06 D Flett D Flett 23/6/06 Draft for information

Draft 2 29/6/06 D Flett D Flett 29/6/06 Draft for distribution to EAP

Draft 3 Draft including EAP comments

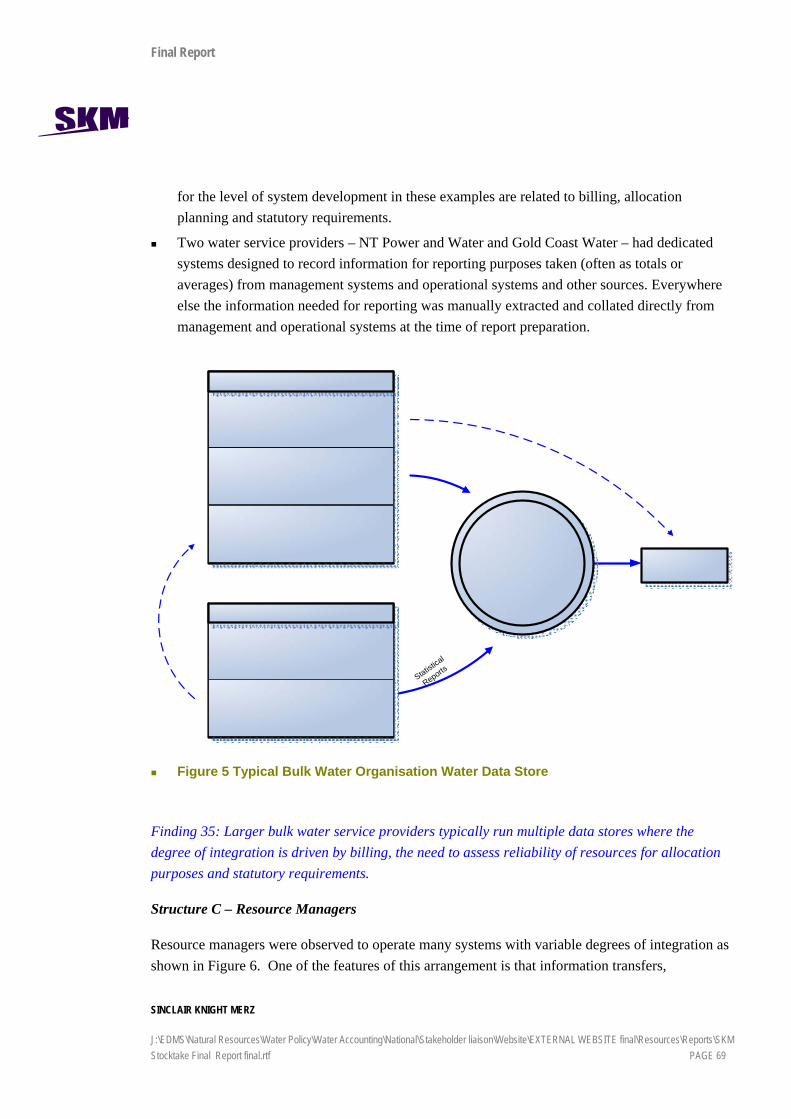

Second Draft Stocktake Report

Draft 1 2/8/06 D Flett D Flett 2/8/06 Draft for distribution to EAP

Final Report

Draft 1 31/8/06 D Flett D Flett 31/8/06 Draft for distribution to EAP

Draft 2 3/10/06 D Flett D Flett 3/10/06 Draft for distribution to NWIC

Final 13/10/06 D Flett D Flett 13/10/06 Final report

Distribution of copies Revision Copy no Quantity Issued to

First Draft Stocktake Report

Draft 1 1 Elec. D. Victorsen

Draft 2 1 Elec. D. Victorsen

File

Second Draft Stocktake Report

Draft 1 1 Elec. D Victorsen

File

Final Report

Draft 1 1 Elec. D Victorsen

Draft 2 1 Elec. D Victorsen

Final 1 Elec. D Victorsen

File

Printed: 25 March 2008

Last saved: 19 March 2008 08:52 AM

File name: I:\Wtat\Projects\WT01936\Deliverables\Final Report\Final Report final.doc

Author: Dean Delahunty, Mark Hamstead, Chris Scriven, Clarke Ballard

Project manager: Denis Flett

Name of organisation: Department of Agriculture, Fisheries and Forestry

Name of project: Stocktake and Analysis of Australia's Water Accounting Practice

Name of document: Final Report

Document version: Final v1

Project number: WT01936.300

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE ix

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 1

Executive Summary Stocktake and Analysis of Australia’s Water Accounting Practice

Sinclair Knight Merz was engaged by the Department of Agriculture, Forestry and Fisheries to undertake a stocktake and analysis of Australia’s water accounting practice. The aim of the project was to guide the development of standards and guidelines to underpin a national water accounting system, and processes which would support consistent water measurement, monitoring, accounting and reporting at all levels of water management.

The project was overseen by the multi-jurisdictional National Water Initiative Committee (NWI Committee) of the Natural Resource Management Ministerial Council, with advice from an Expert Advisory Panel, established by the NWI Committee. Day to day management was undertaken by the Department of Agriculture, Forestry and Fisheries with the assistance of the National Water Commission.

An information requirements framework was prepared to facilitate and add value to the stocktake, to enable comparison between current practice and what could be in the future. As anticipated, both the structure and detail of the information requirements framework was challenged and as a result reviewed and changed throughout the project.

The Stocktake involved 38 organisations nominated by the jurisdictional representatives of the Expert Advisory Panel to ensure adequate exposure to current practices and systems. Participating organisations included the central water agency in each State and Territory and a range of water service providers. It was made clear that the stocktake was about gaining a snapshot and appreciation of practice and was not about assessing performance or gathering actual data or information elements.

There were 60 stocktake findings, which overall demonstrated that while showing signs of some good practice, water accounting in Australia is at an immature phase and being developed in an ad-hoc fashion.

An analysis of best practice, information gaps and areas for improvement focussed on:

The development of the intellectual infrastructure necessary to develop water accounting as a discipline; and

Four themes which cover the anticipated scope of water accounting in Australia – water market, water resource, water for the environment and water use accounting

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 2

A disciplinary approach was recognised as the most appropriate way forward and the most likely to achieve a nationally consistent result to maximise the benefits from the considerable efforts and resources being directed to water accounting.

Key drivers for water accounting to be established as a discipline include:

1. With the exception of the Australian Bureau of Statistics (ABS), external users of accounting information cannot command information directly from the provider.

2. Policy makers and water markets will require that information is assembled and reported according to consistent standards.

3. Public confidence in water accounting is required, as the availability of the resource will have social, economic and environmental consequences as policy makers and water markets react to water accounting information.

A significant number of observations and conclusions were documented throughout the analysis phase and substantial bodies of work were developed and drawn together as starting points for further development. Twelve recommendations to progress water accounting were prepared through interaction between the project team and the Expert Advisory Panel.

A working definition of water accounting was developed to explain what water accounting is:

Water accounting is the application of a consistent and structured approach to identifying, measuring, recording and reporting information about water

Recommendation 1: That the working definition of water accounting be adopted.

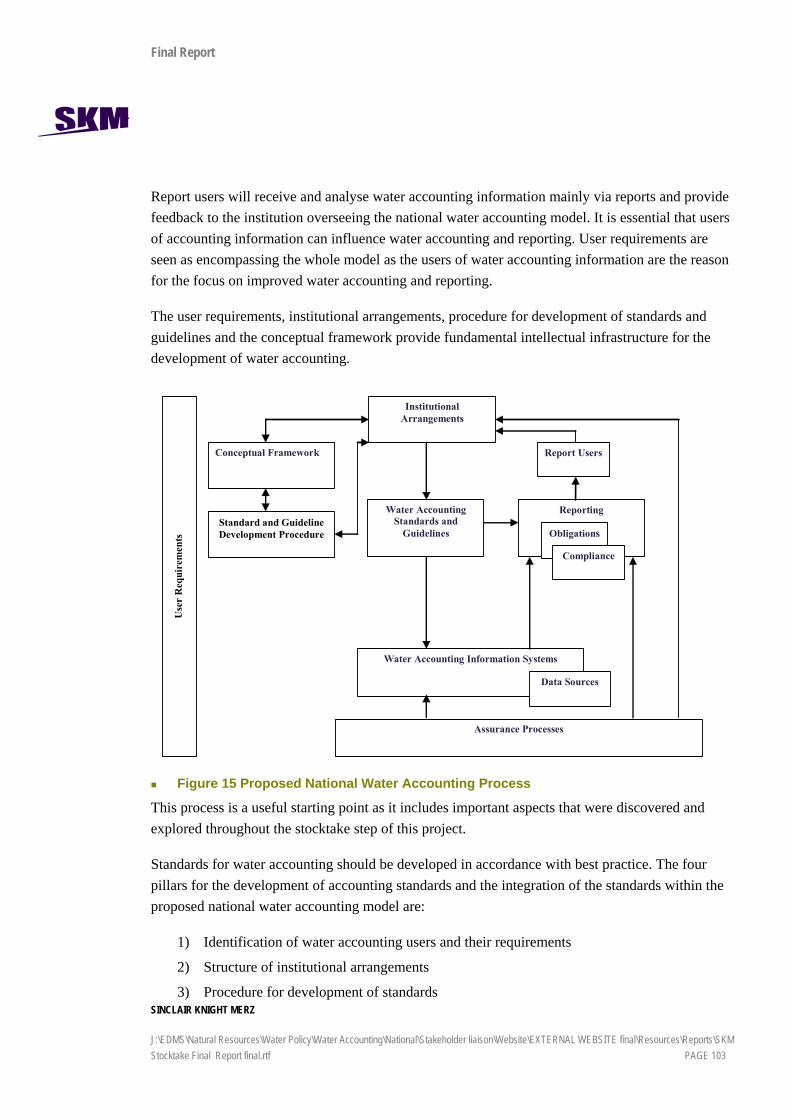

A proposed national water accounting process was developed as shown in Figure E1. The user requirements, institutional arrangements, procedure for development of standards and guidelines and the conceptual framework provide fundamental intellectual infrastructure to ensure the rigor and logical consistency needed to produce useful water accounting information and to instil the necessary confidence among the users of water accounting reports.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 3

.

Conceptual Framework

Institutional Arrangements

Water Accounting Standards and

Guidelines

Reporting

Obligations

Compliance

Assurance Processes

Water Accounting Information Systems

Data Sources

Report Users

Standard and Guideline Development Procedure

Use

r R

equi

rem

ents

Figure E1 Proposed National Water Accounting Process

Application of the level of discipline inherent in the process will enable progressive building of knowledge, limit the need for revision and iteration and reduce cost in the long run.

Recommendation 2: That the process for developing and maintaining water accounting as a discipline be adopted as indicated in Figure E1.

A Water Accounting Development Committee comprised of an independent chair, other independent experienced water and accounting experts and jurisdictional water representatives is proposed to ensure appropriate governance and decision making for the first phase development of water accounting. The Development Committee would be the prime body to determine water accounting standards and guidelines and would be linked to the Natural Resource Management Ministerial Council via the NWI Committee for resolution of any matters that may be required in accordance with the provisions of the NWI Agreement.

The Water Accounting Development Committee would have a support team and oversee technical working groups (TWGs) developing the intellectual infrastructure necessary to establish water accounting as a discipline and water accounting and reporting standard and guideline development. It is also proposed that all development work be progressively tested in practice through pilot projects aimed at demonstrating the application of proposed standards and guidelines and informing the essential disciplinary development work through iterative processes.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 4

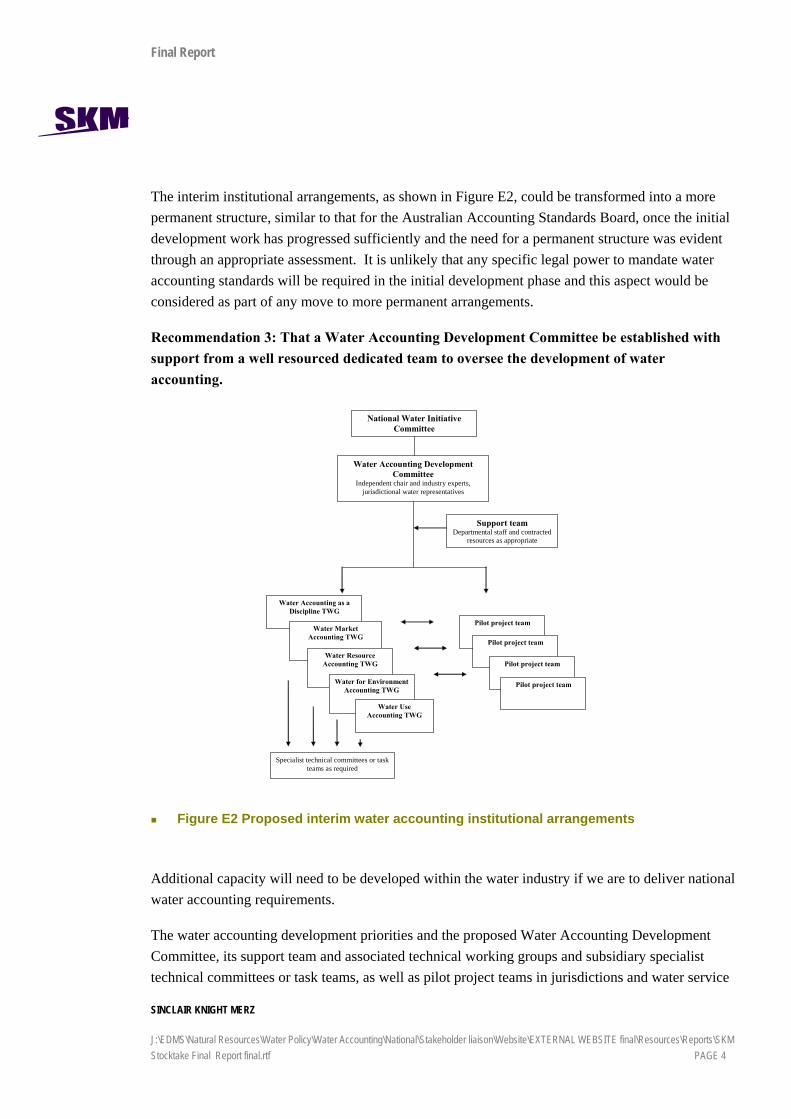

The interim institutional arrangements, as shown in Figure E2, could be transformed into a more permanent structure, similar to that for the Australian Accounting Standards Board, once the initial development work has progressed sufficiently and the need for a permanent structure was evident through an appropriate assessment. It is unlikely that any specific legal power to mandate water accounting standards will be required in the initial development phase and this aspect would be considered as part of any move to more permanent arrangements.

Recommendation 3: That a Water Accounting Development Committee be established with support from a well resourced dedicated team to oversee the development of water accounting.

Pilot project team

Water Accounting Development Committee

Independent chair and industry experts, jurisdictional water representatives

Support team Departmental staff and contracted

resources as appropriate

Water Accounting as a Discipline TWG

Specialist technical committees or task teams as required

Pilot project team

Water Market Accounting TWG

Pilot project team

National Water Initiative Committee

Water Resource Accounting TWG

Water for Environment Accounting TWG

Water Use Accounting TWG

Pilot project team

Figure E2 Proposed interim water accounting institutional arrangements

Additional capacity will need to be developed within the water industry if we are to deliver national water accounting requirements.

The water accounting development priorities and the proposed Water Accounting Development Committee, its support team and associated technical working groups and subsidiary specialist technical committees or task teams, as well as pilot project teams in jurisdictions and water service

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 5

provider organisations, will provide significant opportunities to build water accounting capacity. An infusion of qualified accountants and the integration of their skills and perspectives with water industry practitioners and policy formulators is to be encouraged, as is the building of capacity of specialist expertise in such areas as groundwater modelling and associated accounting development.

Recommendation 4: That capacity building, aligned with water accounting development priorities, be addressed as early as practicable.

If water accounting is to emerge as a discipline then water accounting information must serve the needs of external users of water accounting information as well as the management requirements of water businesses.

The development of a detailed user requirements definition is considered essential if we are to support the development of a meaningful national chart of water accounts and to identify water accounting standard development priorities.

Such a task is required to inform the initial stage of water accounting development and could be carried out partially in parallel with and linked to other processes designed to develop an agreed common chart of water accounts for water accounting and agreed reporting formats for key reports.

Recommendation 5: That the detailed requirements of water information users be defined, assessed and reported to inform the scope and development of water accounting.

A conceptual framework is a consistent reminder of the requirements needed to develop rigorous and relevant standards. Any conceptual framework for water accounting must complement the standard setting procedure and facilitate high quality water accounting standards.

The theoretical aspects included in a conceptual framework for water accounting are expected to take some time to develop. Realistically the conceptual framework may not be fully developed for some years, and in the interim it is proposed that work on high priority accounting standards proceed in parallel with the development of the conceptual framework, and that lessons learned during the development of these standards influence the conceptual framework. An outline conceptual framework has been developed as a starting point to assist this iterative process.

Recommendation 6: That a conceptual framework be progressively developed based on the starting point identified in this project and integrated with the development of the initial priority water accounting standards, to facilitate the development of consistent and relevant water accounting standards.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 6

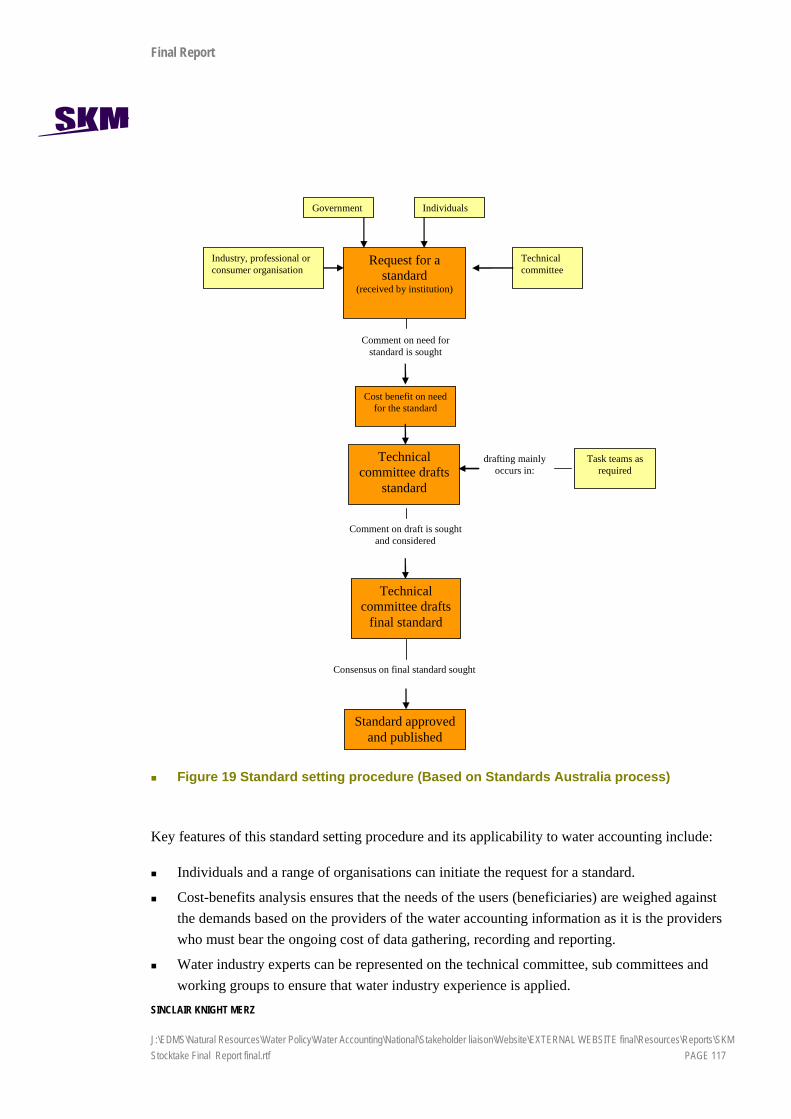

There are advantages in having a structured, transparent procedure for the development of water accounting standards and one based on the process used by Standards Australia is proposed. Whilst the procedure is initiated by a request, initial standard and guideline development may be accelerated by modifying the procedure through active priority setting by the Water Accounting Development Committee and by some concentrated resourcing provision.

Recommendation 7: That a procedure for standard and guideline development be adopted by the Water Accounting Development Committee based on the standards development process applied by Standards Australia.

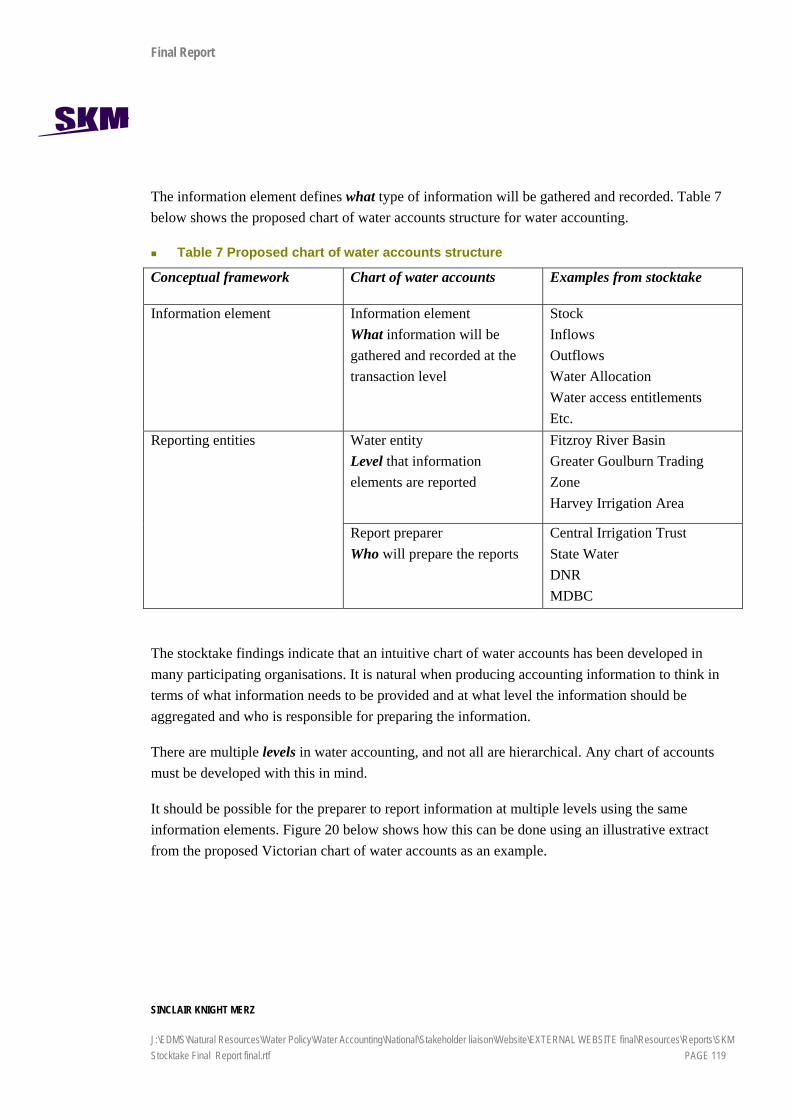

Accounting information systems cannot function without a chart of accounts. The chart of water accounts for a water accounting information system should define what type of information must be gathered and recorded (the information element) and the level that the information element is to be aggregated and reported (the water entity) and who prepares the water accounting reports (the report preparer).

It is proposed that a national chart of water accounts be developed based on input from all States and Territories. The common chart of water accounts has a direct relationship with the conceptual framework.

Recommendation 8: That a common chart of water accounts be developed based on the starting points identified in this project and including work within jurisdictions.

The development of standards and guidelines is seen as one of the key areas where water accounting practices can be significantly improved in this country. Water accounting standards will address particular subjects and explain and prescribe the treatment of various water accounting issues. Typically, the standards will address the concepts that are listed in the conceptual framework.

There is potential for many standards to be required for water accounting and development of standards is likely to take some years. This time horizon should not inhibit development and it is recommended the focus should initially be on the development of reporting standards as they directly relate to the information user requirements. An initial focus on reporting standards would in turn lead to a focus on the associated information element standards, which in turn links to measuring standards.

The focus should also initially be in agreed target areas where management approaches are settled and development of standards can be both rapid and most beneficial. Proposed standard report templates have been developed as starting points for initial reporting standards development for the water market and water resource accounting themes.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 7

Coordination of work to develop water accounting and reporting standards and guidelines is essential. Technical working groups overseen by the Water Accounting Development Committee are proposed as the main work vehicles as shown in Figure E2 and will have an important coordination role which would be assisted by some common membership.

Testing in practice proposed standards and guidelines through targeted and representative pilot projects, using iterative processes to inform both standards development and the work to develop water accounting as a discipline, is also proposed.

The technical working groups, along with associated technical committees or task teams and the pilot project teams will provide an opportunity to include people with an appropriate mix of skills and perspectives and to build commitment to water accounting development.

Recommendation 9: That nationally coordinated development projects which use a pilot approach in multiple representative areas and which progressively interact with and test other developmental work (user requirements definition, common chart of water accounts, conceptual framework and standards development procedure) be initiated by the Water Accounting Development Committee to progressively develop water accounting and reporting standards or guidelines for:

water market accounting including water access entitlements, water allocations, use and trading; and

water resource accounting including surface water, groundwater, water cycle and connected surface and groundwater resource accounting.

Further work is required to progress the key principles and concepts for management and accounting for water for the environment and the extent of the contribution from water for the environment accounting. This includes reconciling approaches to managing and accounting for environmental provision via water planning and indirect rules, which is the most prevalent method throughout Australia, as well as for the wider suite of provisions for the regulated and interconnected and over-allocated systems in the southern Murray Darling basin. It is evident that a particular focus on water for the environment is warranted and a number of proposed starting points have been developed for further consideration.

Recommendation 10: That a technical working group be established to further develop and pilot accounting principles and standards for water for the environment and that the principles and standards resolve the accounting treatment of:

indirect rules;

volumetric rights (extractive and in stream); and

direct rules.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 8

Further work building on and adapting the work of the ABS and practice within industry, is required to progress both management and accounting for water use, for which it is evident that a particular focus is warranted.

Recommendation 11: That a technical working group, building on the ABS Water Statistics User Group, be established by the Water Accounting Development Committee to further develop water use accounting principles and guidelines.

Information sharing is seen as one of the key methods of achieving a higher degree of consistency, transparency and accountability within the water sector. Existing water information systems are not necessarily efficient at producing standard information or reports required by the wider audience.

Most jurisdictions have made significant financial investments in existing water information systems.

Joint ventures or partnerships in water accounting information system development projects that can make rapid advances in national water accounting and reporting are to be encouraged. It is proposed that projects be initiated to develop examples of water accounting information systems that demonstrate to a range of water businesses the potential benefits of applying accounting principles and that have the potential for rapid expansion to relevant parts of the industry. It is envisaged that these will be integrated with pilot projects.

Recommendation 12: That demonstration water accounting information systems projects be supported as soon as the water accounting benefits have been determined.

The integration of water accounting development work over the next three years is problematic in that specific project plans have not yet been identified or developed. This is a task to be undertaken by the Water Accounting Development Committee and associated technical working groups.

The following development principles were developed through consultation with the EAP:

Use appropriate starting points wherever practicable, picking up on relevant work undertaken nationally and within jurisdictions, best practice examples within water businesses and specific developments that have been documented during this project, as a cost effective base on which to build.

Develop the essential intellectual infrastructure or theoretical base to ensure discipline and rigour in a manner which both learns from and informs practice and practicable developments, through targeted pilot projects which test the application of proposed standards and guidelines and maximises the integration of development work.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 9

Focus on agreed priorities for development of standards, build on current or proposed good practice reporting and support research and development projects that are effective or offer significant potential in developing national standards for identifying, measuring and recording water information.

Involve stakeholder representatives and develop business cases as part of each project or priority action initiated to develop water accounting nationally.

Concentrate on development of a few demonstration water accounting information systems – make real progress on development of information systems with the intent of effective and expandable application of water accounting functionality.

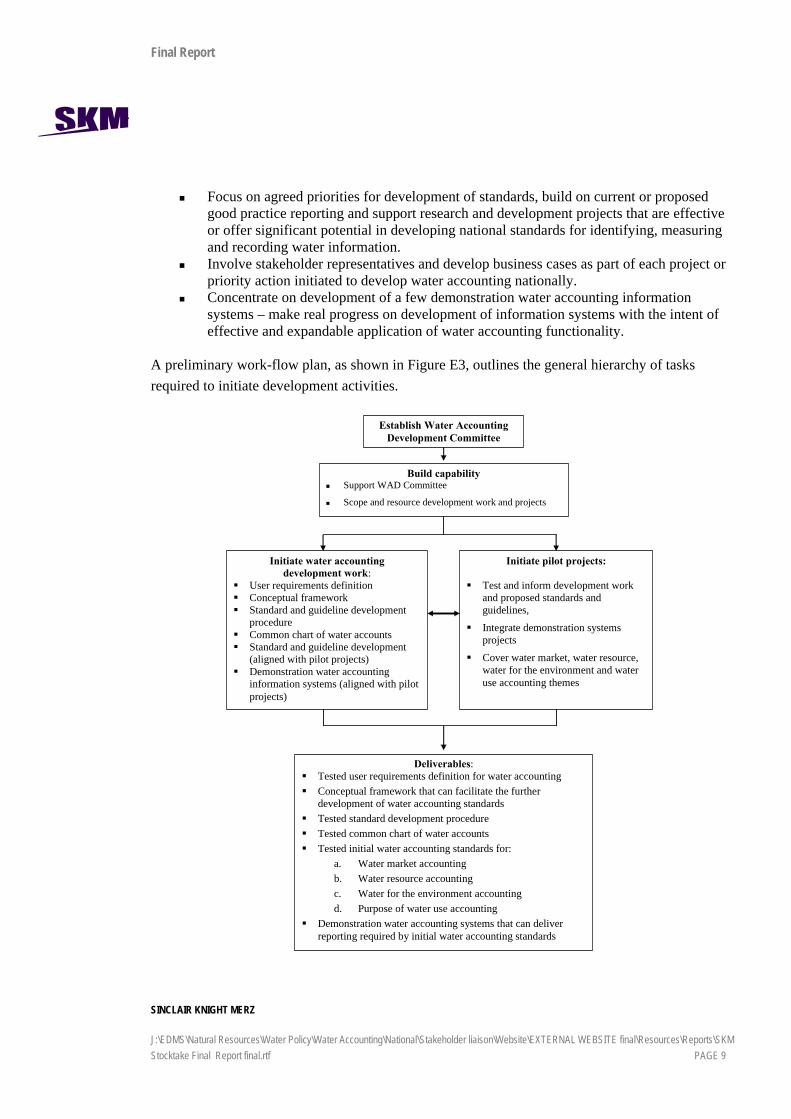

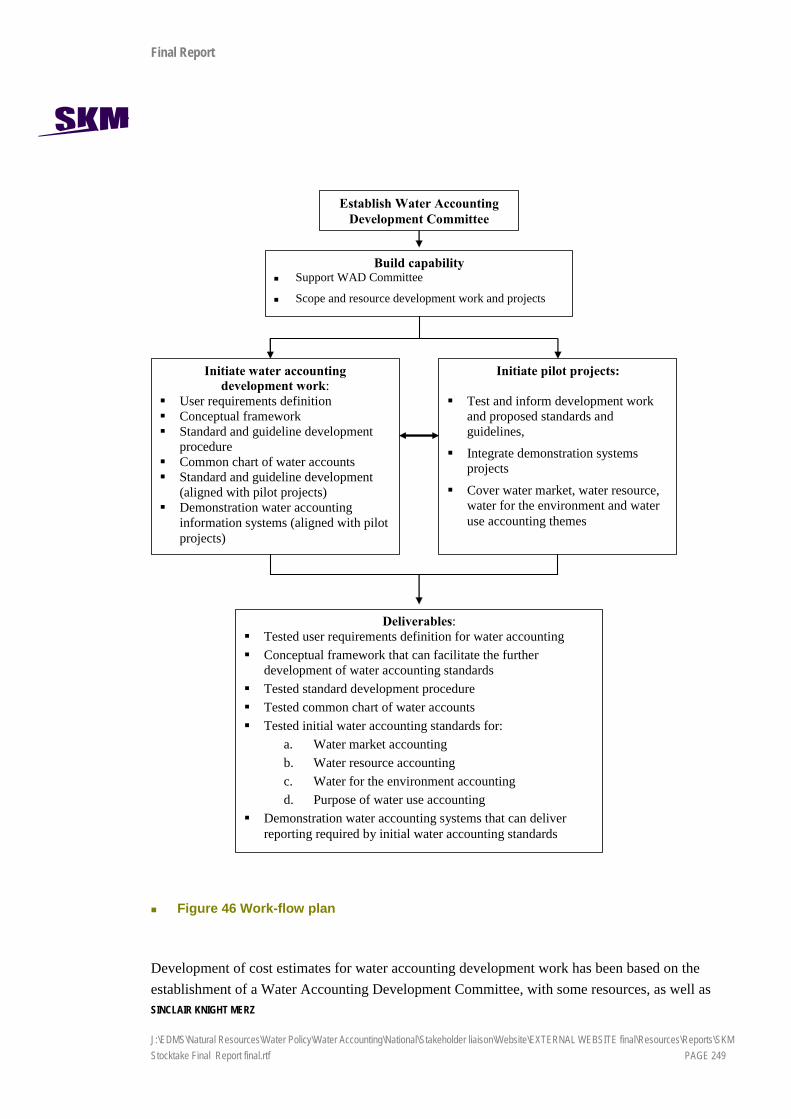

A preliminary work-flow plan, as shown in Figure E3, outlines the general hierarchy of tasks required to initiate development activities.

Establish Water Accounting Development Committee

Build capability Support WAD Committee

Scope and resource development work and projects

Initiate pilot projects:

Test and inform development work and proposed standards and guidelines,

Integrate demonstration systems projects

Cover water market, water resource, water for the environment and water use accounting themes

Initiate water accounting development work:

User requirements definition Conceptual framework Standard and guideline development

procedure Common chart of water accounts Standard and guideline development

(aligned with pilot projects) Demonstration water accounting

information systems (aligned with pilot projects)

Deliverables: Tested user requirements definition for water accounting Conceptual framework that can facilitate the further

development of water accounting standards Tested standard development procedure Tested common chart of water accounts Tested initial water accounting standards for:

a. Water market accounting b. Water resource accounting c. Water for the environment accounting d. Purpose of water use accounting

Demonstration water accounting systems that can deliver reporting required by initial water accounting standards

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 10

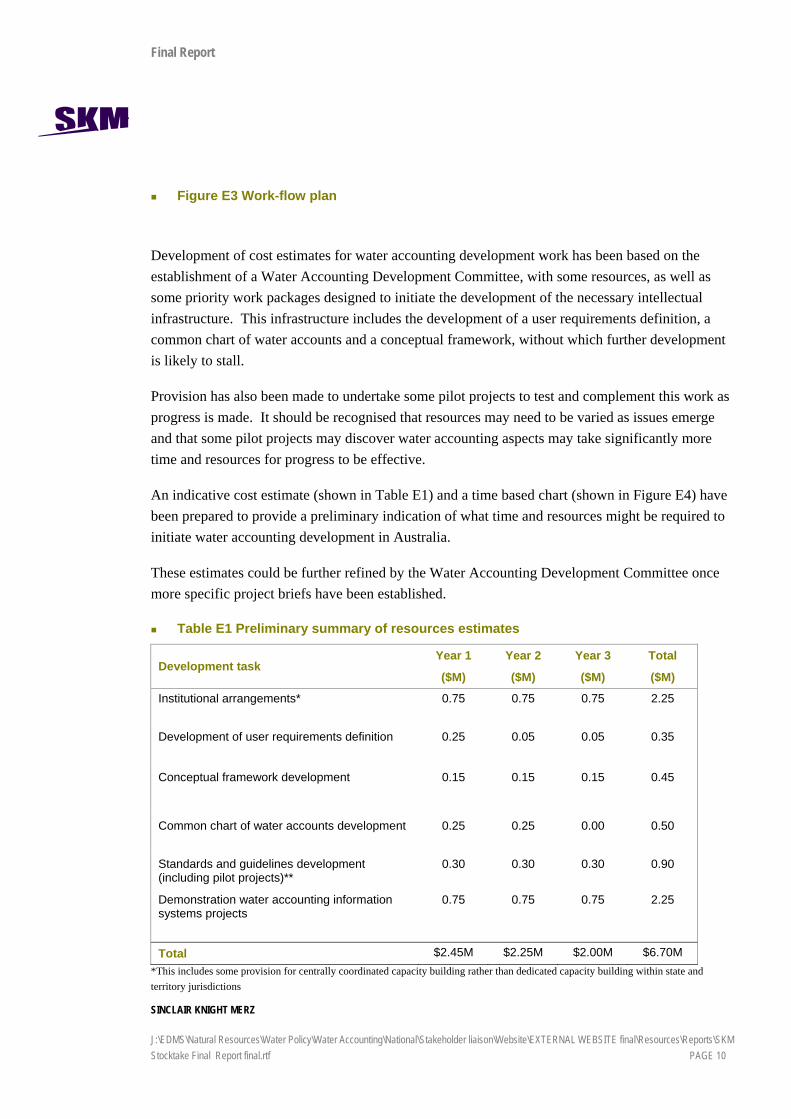

Figure E3 Work-flow plan

Development of cost estimates for water accounting development work has been based on the establishment of a Water Accounting Development Committee, with some resources, as well as some priority work packages designed to initiate the development of the necessary intellectual infrastructure. This infrastructure includes the development of a user requirements definition, a common chart of water accounts and a conceptual framework, without which further development is likely to stall.

Provision has also been made to undertake some pilot projects to test and complement this work as progress is made. It should be recognised that resources may need to be varied as issues emerge and that some pilot projects may discover water accounting aspects may take significantly more time and resources for progress to be effective.

An indicative cost estimate (shown in Table E1) and a time based chart (shown in Figure E4) have been prepared to provide a preliminary indication of what time and resources might be required to initiate water accounting development in Australia.

These estimates could be further refined by the Water Accounting Development Committee once more specific project briefs have been established.

Table E1 Preliminary summary of resources estimates

Development task Year 1

($M)

Year 2

($M)

Year 3

($M)

Total

($M)

Institutional arrangements*

0.75 0.75 0.75 2.25

Development of user requirements definition 0.25 0.05 0.05 0.35

Conceptual framework development 0.15 0.15 0.15 0.45

Common chart of water accounts development

0.25 0.25 0.00 0.50

Standards and guidelines development (including pilot projects)**

0.30 0.30 0.30 0.90

Demonstration water accounting information systems projects

0.75 0.75 0.75 2.25

Total $2.45M $2.25M $2.00M $6.70M *This includes some provision for centrally coordinated capacity building rather than dedicated capacity building within state and territory jurisdictions

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 11

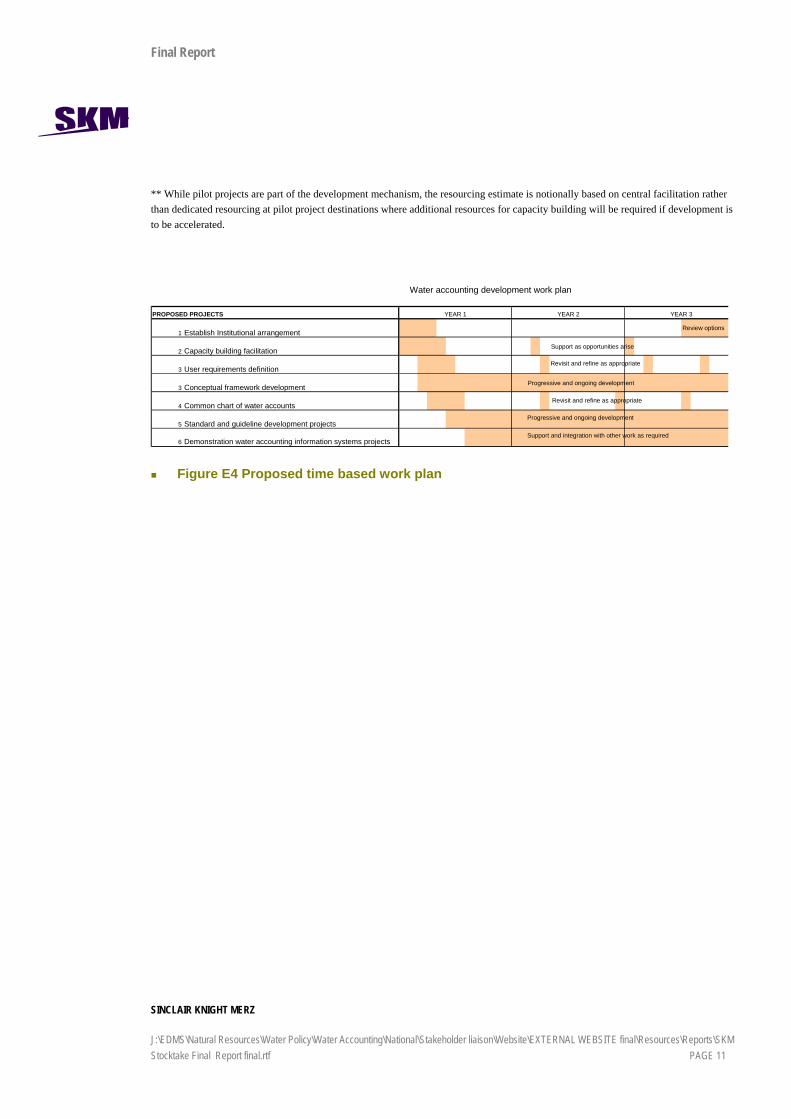

** While pilot projects are part of the development mechanism, the resourcing estimate is notionally based on central facilitation rather than dedicated resourcing at pilot project destinations where additional resources for capacity building will be required if development is to be accelerated.

Water accounting development work plan

PROPOSED PROJECTS

1 Establish Institutional arrangementReview options

2 Capacity building facilitation

3 User requirements definition

3 Conceptual framework development

4 Common chart of water accounts

5 Standard and guideline development projects

6 Demonstration water accounting information systems projects

YEAR 1 YEAR 2 YEAR 3

Support and integration with other work as required

Support as opportunities arise

Revisit and refine as appropriate

Progressive and ongoing development

Revisit and refine as appropriate

Progressive and ongoing development

Figure E4 Proposed time based work plan

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 12

1 Introduction

1.1 Background SKM was engaged by the Department of Agriculture, Forestry and Fisheries to undertake a stocktake and analysis of Australia’s water accounting practices.

The aim of this project was to guide the development of standards and guidelines to underpin a national water accounting system, and processes which would support consistent water measurement, monitoring, accounting and reporting at all levels of water management. The project was undertaken to assist the parties to the National Water Initiative (NWI) to achieve the outcome for water accounting as stated in Clause 80 of the NWI, namely to “ensure that adequate measurement, monitoring and reporting systems are in place in all jurisdictions, to support public and investor confidence in the amount of water being traded, extracted for consumptive use, and recovered and managed for environmental and other public benefit outcomes.”

The project was divided into 4 steps, as follows:

Step 1. develop the information requirements of accounting systems at the different levels of water management, against which the initial stocktake of the nation’s water accounting systems can be undertaken,

Step 2. in all States and Territories, undertake a stocktake of jurisdictions’ and water service providers’ current water accounting systems (including current arrangements to account for environmental water), focusing on the agreed information requirements, and having regard to the links between existing registration and accounting systems;

Step 3. analyse the information collected in the stocktake to identify best practice, information gaps and areas for improvement;

Step 4. make recommendations for development of water accounting standards, principles for environmental water accounting and guidelines for reporting and information, including priorities for standards, guidelines and systems development.

The project was overseen by the multi-jurisdictional NWI Committee of the Natural Resource Management Ministerial Council, with advice from an Expert Advisory Panel (EAP), established by the NWI Committee. Day to day management was undertaken by the Department of Agriculture, Forestry and Fisheries with the assistance of the National Water Commission.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 13

1.2 Project and report overview Project Step 1, the development of information requirements for the stocktake occurred between January and March 2006. Step 2, the undertaking of a stocktake of water accounting systems and practices, were completed between April and June 2006 and presented to the EAP in early July 2006. Step 3, analysis, was undertaken by the project team in July 2006 and presented in the Second Draft Stocktake Report for consideration by and value adding from the EAP in early August 2006. The Final Report was prepared in August and finalised via meeting with the EAP and NWIC in September and October 2006.

A Water Accounting Information Requirements Framework was developed in Step 1 and used in the Step 2 stocktake, in an attempt to help envisage what a national water accounting system might look like. The information requirements framework was prepared to facilitate and add value to the stocktake, to enable comparison between current practice and what could be in the future. As anticipated, both the structure and detail of the information requirements framework was challenged and as a result reviewed and changed throughout the project.

The Final Report recaps the information requirements used in undertaking the stocktake in Chapter 2, and covers the stocktake scope and method developed in consultation with the EAP along with comment on the conduct of the stocktake in Chapter 3.

Chapter 4 sets out the findings from the stocktake and includes some modifications from the First and Second Draft Stocktake Reports as a result of completion of the stocktake in the Northern Territory and a review by the project team of comments received from EAP members.

Inconsistency in terminology occurred as the project progressed, primarily due to proposing an information requirements framework for the purpose of the stocktake and the adaptive approach taken. This has been addressed to a degree in this report through the provision of a glossary of key terms in Appendix A and more consistent use of terminology in the analysis and recommendation chapters.

Chapter 5 presents an analysis of the development of water accounting as a discipline and Chapters 6 to 9 include an analysis of each of four water accounting themes identified in consultation with the EAP – water resource, water market, environmental water and water use accounting.

Chapter 10 presents recommendations arising from the analysis and a work plan outlining priority development to progress water accounting practice in Australia.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 14

2 Information Requirements

2.1 Approach The approach taken to identifying the information requirements to underpin a national water accounting system was to:

1. consider and synthesise the purpose and outcomes desired from this project and the relevant provisions of the NWI and then to develop the envisaged types of standard water accounting reports which could contribute to those outcomes being achieved,

2. consider the accounting principles and the chart of accounts necessary to support the production of standard water accounting report types and underpin the development of a national water accounting system.

3. develop templates for the standard water accounting report types and examples of the type of reports proposed

4. identify the information elements needed to populate the proposed standard water accounting reports and consider how the information elements are derived or obtained.

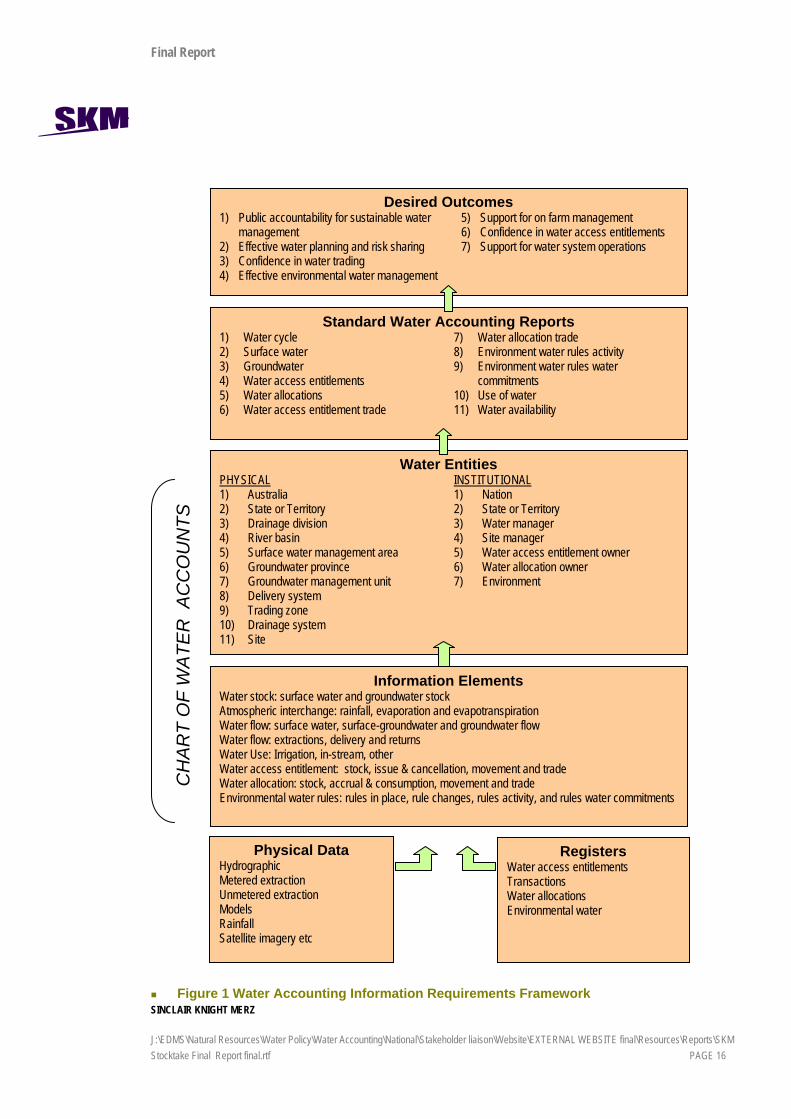

A Water Accounting Information Requirements Framework as shown in Figure 1 was developed for use in the stocktake. The framework was agreed by the NWI Committee at its meeting on 22 March 2006 for the purposes of conducting a stocktake of water accounting systems within jurisdictions. Figure 1 shows how Information Elements, which are derived or obtained from Physical Data or from Registers, combine with Physical Water Entities and Institutional Water Entities in a proposed Chart of Water Accounts, which could be used to produce proposed Standard Water Accounting Reports, which in turn contribute to the Desired Outcomes from the project.

It is recognised that the Water Accounting Information Requirement Framework would need to be compatible with broader frameworks for holistic integrated water resource management, which adequately represents the physical water cycle. SKM is confident that the Water Accounting Information Requirement Framework would be compatible with broader frameworks such as SEEA 2003 (System of Integrated Environmental and Economic Accounts, joint publication of the United Nations, European Commission, International Monetary Fund, Organisation for Economic Co-operation and Development, and the World Bank). The important thing is that all relevant information elements can be captured and are consistent so that arrangement and aggregation of the information elements at appropriate levels is effective.

From a philosophical perspective, it is recognised that while water accounting practices will reflect the prevailing water management regime, it can also influence the management regime through the

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 15

methodical presentation of information and associated analysis and help bring about beneficial change. For a national water accounting system to be effective the purposes and benefits of its development and use will need to be obvious and relevant to users of the system and an emphasis will be placed on this aspect throughout the project.

The developed Water Accounting Information Requirements Framework will be scrutinised in the analysis Step 3. Each part of the framework, aspects relating to it and how it is envisaged to work are described in the remaining sections of this chapter.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 16

Figure 1 Water Accounting Information Requirements Framework

CH

AR

T O

F W

ATE

R A

CC

OU

NTS

Desired Outcomes

1) Public accountability for sustainable water management

2) Effective water planning and risk sharing 3) Confidence in water trading 4) Effective environmental water management

5) Support for on farm management 6) Confidence in water access entitlements 7) Support for water system operations

Standard Water Accounting Reports 1) Water cycle 2) Surface water 3) Groundwater 4) Water access entitlements 5) Water allocations 6) Water access entitlement trade

7) Water allocation trade 8) Environment water rules activity 9) Environment water rules water

commitments 10) Use of water 11) Water availability

Water Entities PHYSICAL 1) Australia 2) State or Territory 3) Drainage division 4) River basin 5) Surface water management area 6) Groundwater province 7) Groundwater management unit 8) Delivery system 9) Trading zone 10) Drainage system 11) Site

INSTITUTIONAL 1) Nation 2) State or Territory 3) Water manager 4) Site manager 5) Water access entitlement owner 6) Water allocation owner 7) Environment

Information Elements Water stock: surface water and groundwater stock Atmospheric interchange: rainfall, evaporation and evapotranspiration Water flow: surface water, surface-groundwater and groundwater flow Water flow: extractions, delivery and returns Water Use: Irrigation, in-stream, other Water access entitlement: stock, issue & cancellation, movement and trade Water allocation: stock, accrual & consumption, movement and trade Environmental water rules: rules in place, rule changes, rules activity, and rules water commitments

Physical Data Hydrographic Metered extraction Unmetered extraction Models Rainfall Satellite imagery etc

Registers Water access entitlements Transactions Water allocations Environmental water

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 17

2.2 Desired outcomes and water accounting reports A set of desired outcomes, which a national water accounting system would serve, were identified, based on those stated in the NWI agreement and further advice provided by the Expert Advisory Panel. Water accounting systems on their own would not deliver these outcomes, but they could contribute substantially to their achievement. The seven desired outcomes are summarised in the top box in Figure 1.

Standard water accounting report types relevant to these outcomes were identified and are described and explained in Table 1. Detailed templates and descriptions for the eleven proposed standard water accounting reports were developed and were included in the Step 1 Status Report. The reports could be done at various scales, defined by the water accounting entities in the proposed chart of accounts. These entities are discussed in Section 2.3.

In developing these templates financial reporting models were considered and applied, with appropriate modifications, to water accounting. Some templates combine the concept of a financial position statement (balance sheet) and a financial cash flow statement. In some cases assets are replaced with water in storage; revenue is replaced with inflows of water; expenditure is replaced with outflows of water. In other cases revenue and expenditure are replaced with such things as increases and decreases in water allocations or water access entitlements. Water allocations under entitlements and commitments of water under environmental rules can be considered to be unmet liabilities, which are reduced when the water is taken or supplied.

Worked examples of the water cycle, surface water and water availability type of reports were also developed and included in the Step 1 Status Report.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 18

Table 1 Proposed Standard Types of (Water Accounting) Reports

Report type Description Physical water entities

Institutional water entities

Comments

Water cycle Quantifies the elements of the water cycle (rainfall, evapo-transpiration, runoff etc) for a designated water entity for a designated period.

Australia Drainage division River basin Surface water

management area Site

Nation State or

territory Water

manager Site manager

This report type shows the total picture of the movement and/or position of water from rainfall to the soil, rivers and aquifers, to the economy, to the atmosphere via evapo-transpiration, or to the sea. This report type will primarily be used for planning and monitoring purposes. Theoretically this report can show the effects of land use change and climate change on inflows to rivers and aquifers. It is however not easy to quantify all the elements of this report type and simplifying assumptions may be needed. Errors in measuring or estimating parameters may hamper its value but if progress is to be made toward holistic integrated water resource management and accounting, including surface water and groundwater interaction, then this report type offers value.

Surface water Quantifies the inflow, outflows, extraction and storage of water for designated water entity over a designated period.

Surface water management area

Delivery system Drainage system

Water manager

For any surface water system this report type shows the movement and/or position of water in and out. This type of report is already being produced for many river systems, and is relatively straightforward to prepare. It is important for planning, annual and day-to-day operations and could be used to deal with surface water and groundwater interaction.

Groundwater Quantifies the inflow, outflows, extraction and storage of water for a designated groundwater entity over a designated period.

Groundwater management unit

Water manager

For any aquifer system this report type shows the movement of water in and out. While such reports are available for specific cases, they are not easy to prepare and not generally available. Many of the parameters are estimated or modelled rather than measured. It is essentially used for planning and could be used to help deal with surface water and groundwater interaction.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 19

Report type Description Physical water entities

Institutional water entities

Comments

Water access entitlements

Sets out the types and quantity of share units held under water access entitlements, and the increases and decreases in them, for a designated water entity and institutional entity over a designated period.

Surface water management area

Delivery system Trading zone Groundwater

management unit Drainage system

State or territory

Water manager

Water access entitlement owner

Environment

Water access entitlements give the holder a right to an ongoing share of a consumptive pool. The size of the share varies from entitlement to entitlement. The total quantity of share units is the essential factor. This report types essentially shows share units held in a water entity and changes in the share units in that water entity over time. Used for planning, public accountability and to support public and investor confidence.

Water allocations

Quantifies the water allocated under water access entitlements and how it is extracted, traded or cancelled from time to time, for a designated physical water entity and institutional water entity over a designated period.

Surface water management area

Delivery system Trading zone Groundwater

management unit

Nation State or

territory Water

manager Water

allocation owner

Environment

For rights to extract water allocated under entitlements to persons, this report type shows the amount allocated and what happens to it. These types of reports are already commonly produced. A record (a water allocation bank) is normally kept in relation to each person or persons with a right to take water allocated under entitlements. These reports can be rolled up to a range of levels. They are used on a day to day basis by individuals to monitor their available allocation and by institutions to monitor the compliance of persons with their allocations. On a rolled up basis they are used for operational decision making, and for planning.

Water access entitlement trade

For a designated period, quantifies trading activity in water access entitlements for a designated water entity and institutional entity.

Surface water management area

Delivery system Trading zone Groundwater

management unit

State or territory

Water manager

Water access entitlement owner

Environment

This report type shows the effect of water trading activity on the locations where water is extracted in the longer term. It can be prepared at a variety of levels such as trading zone, water source. On a day to day basis it is needed for operation of trading rules which limit such movements between trading zones. On a long term basis it is used to review whether trading rules are achieving desired results and to analyse trends Iin trading of water access entitlements.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 20

Report type Description Physical water entities

Institutional water entities

Comments

Water allocation trade

For a designated period, quantifies movement of water allocations into, out of and within the designated entities, resulting from trade.

Surface water management area

Delivery system Trading zone Groundwater

management unit

Nation State or

territory Water

manager Water

allocation owner

Environment

This report type shows the effect of water trading activity on the locations where water can be extracted in the short term. It can be prepared at a variety of levels such as trading zone, water source etc On a day to day basis it is needed for operation of trading rules which limit such movements between trading zones. On a long term basis it is used to review whether trading rules are achieving desired results and to analyse trends in trading of water allocation.

Environment water rules

For a designated period, specifies environmental water rules in place and at the start and finish and what rules have been commenced, terminated or modified.

Surface water management area

Groundwater management unit

Site

State or territory

Water manager

Site manager

This report type is a textual rather than numerical report, showing in summary form the environmental water rules that apply

Environment water rules activity

For a designated period, for environmental water rules in place specifies whether they were activated and complied with or not.

Surface water management area

Groundwater management unit

Site

State or territory

Water manager

Site manager

This report type is a textual rather than numerical report, showing in summary form the compliance status of environmental water rules during the specified period

Environment water rules water commitments

Quantifies water committed under environmental water rules and the quantities of water supplied or protected from extraction under those rules, for designated waters over a designated period.

Surface water management area

Delivery system Groundwater

management unit Site

State or territory

Water manager

Site manager

This report type is similar in concept to the water allocations and use of water report types. Rather than dealing with water allocated under entitlements, it shows water committed under environmental water rules, and rather than recording use of that water, it records the supply or protection of that water, as the case may be. It is used operationally for implementation of the rules, and longer term to demonstrate delivery of environmental water, and for planning purposes. It is only applicable to some environmental water rules.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 21

Report type Description Physical water entities

Institutional water entities

Comments

Use of water Tabulates the volumes of water used by purpose and by source for a specified area over a designated period. (Most of the information for these reports will not be available from the water accounting system)

Australia Drainage division River basin Surface water

management area

Nation State or

territory Business Household Environment

These are the type of reports already being prepared by the Australian Bureau of Statistics, who are currently expanding and refining them. They show the uses of water by standard industry groupings, and the sources of water for those uses. These reports demonstrate the economic value being derived from the use of water. They are primarily useful for planning purposes. Linked with other reports such as water access entitlement or water allocation trade report they can show the economic benefits of water reforms over time.

Water availability

Shows the availability of water, which is the water stored less the water committed or allocated, for designated waters over a designated period

Surface water management area (regulated)

Groundwater management unit

Water manager

This report type brings together some elements of the surface water, environmental water rules, and water allocation report types into one report. They are designed to show the way water stored and received into storage is allocated or committed over time, and the extent to which water held is available to be committed. The report type can also apply to groundwater.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 22

2.3 The chart of water accounts In financial accounting, the chart of accounts provides the basis for the accounting information to be recorded, summed, analysed and reported.

Water accounting should be based on a chart of water accounts that meets the needs of water managers, governments, farmers, environmental interests, other owners of water and people interested in water accounting, including researchers, journalists, water brokers, etc.

A financial chart of accounts consists of natural accounts and accounting entities. A similar structure can usefully be applied to water accounting systems.

2.3.1 Information elements In financial accounts the natural accounts are the various asset, liability, equity, revenue and expense accounts. The ‘natural accounts’ for water can be grouped into descriptors such as water stocks, atmospheric interchanges, water flows, water use, water access entitlements, water allocations and environmental water rules. The more generic term ‘information elements’ is being used rather than ‘natural water accounts’ because to many the term ‘natural water accounts’ implies information on the natural or untouched state of the water resources, which is not the case for the information elements.

A water stock is the volume of water in a physical water entity at a particular time, held in such things as storages, channels and aquifers. Stock can be conveniently grouped into surface water stock (storages, channels, snowpack) and groundwater stock (soil water, aquifers).

Atmospheric interchanges are the volumes of water moving between land and the atmosphere. The information elements within this group include rainfall, evapo-transpiration and evaporation.

Water flows represent movements of water into or within a physical water entity, over a specified period. The information elements within this group include surface water flows, groundwater flows, surface-groundwater flows, extractions, deliveries and returns.

These first three categories of information elements relate to the physical water cycle, whereas the next four categories relate more to how water is managed and used.

Water use shows the purposes for which water is used, and the volumes associated with that use. Purposes are categorised in accordance with the ABS groupings of ANZSIC standard classifications.

Water access entitlements are the entitlements issued to persons for a share of the water in a consumptive pool, as per the NWI. The water access entitlements information element group includes share stock, as shown on registry systems at a particular date, and the various changes to water access entitlements such as issue of new entitlements, movements of entitlements in or out of the entity, and trade of entitlements.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 23

Water allocations are volumes of water that are made available for extraction or delivery under water access entitlements. Water allocations can be recorded in water allocation banks, which, like financial bank accounts, are ‘owned’ by persons, can have ‘deposits’ (water allocation announcements), ‘withdrawals’ (physical extraction of water) and ‘transfers’ (assignment of water allocations from one person to another). The water allocations information elements group includes water allocation stock at a particular date, accrual and consumption, movement into or out of the entity and trade.

Environmental water rules are the various rules in water plans which commit water to environmental purposes. They do not include water access entitlements which are committed to environmental purposes, nor the water allocations accruing under those entitlements. The environmental water rules information element group includes schedules of the rules in place, changes to those rules, the activity status of those rules, the water committed under environmental water rules, the use of that water (e.g. by allowing to flow downstream or flow into an environmental asset) over a period of time, and the write-off of committed water which is not used.

The information elements are the individual elements, or lines of reporting, envisaged in the standard water accounting reports outlined in previous sections. They are the key ‘building blocks’ of the envisaged national water accounting system.

The information elements are tabulated in Appendix B. This shows the groups of information elements, the name of each individual information element, (required reporting) frequency, definition of each information element and units.

2.3.2 Accounting entities for water In a financial chart of accounts, the natural accounts will be joined with entities like cost centres and lines of business.

For example a business might have three regional outlets, five city outlets and a head office. These would all be cost centres. Each of the city and regional cost centres could have multiple lines of business, or profit centres such as hardware, furniture, garden ornaments etc. The cost centres can have multiple lines of business and the managers of these cost centres can be held responsible for each line of business and the overall performance of their cost centre.

Some businesses have multiple entities and use coding to group and sort information within lines of business and related lines of business and cost centres. All city based cost centres may have a code of 1nn while regional cost centres may have a code of 2nn etc. The chart of accounts design controls the recording, summing, analysis and reporting of financial information.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 24

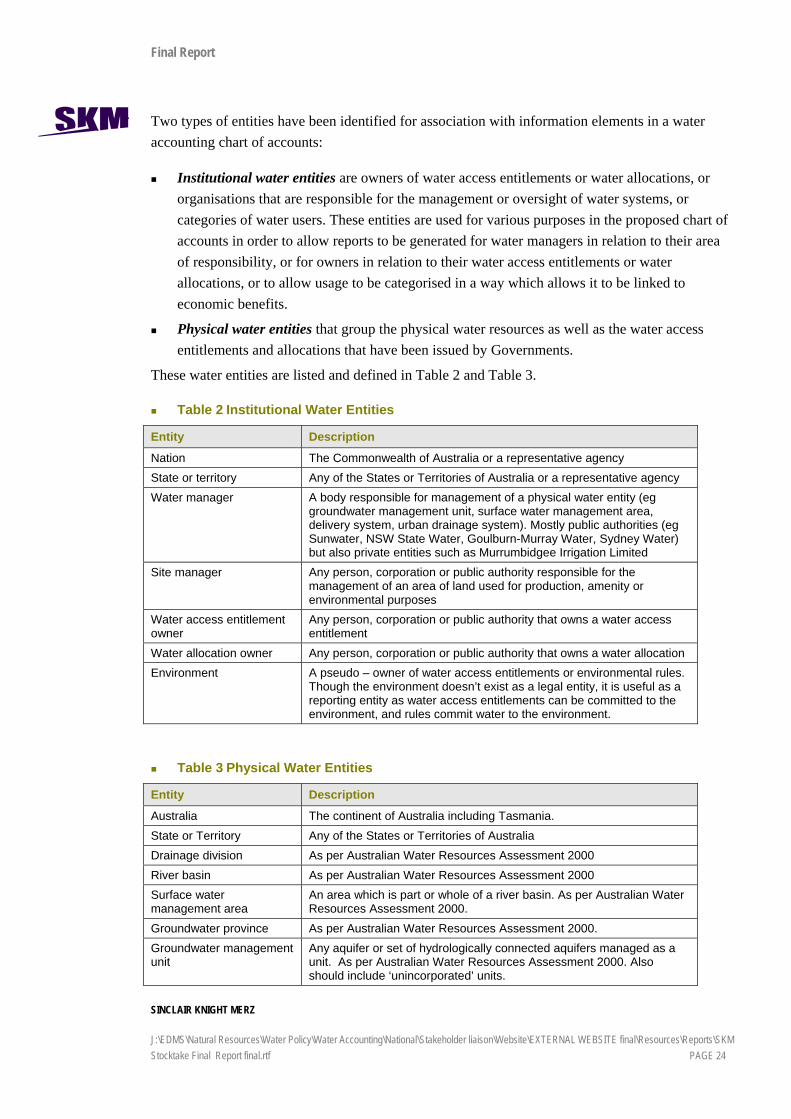

Two types of entities have been identified for association with information elements in a water accounting chart of accounts:

Institutional water entities are owners of water access entitlements or water allocations, or organisations that are responsible for the management or oversight of water systems, or categories of water users. These entities are used for various purposes in the proposed chart of accounts in order to allow reports to be generated for water managers in relation to their area of responsibility, or for owners in relation to their water access entitlements or water allocations, or to allow usage to be categorised in a way which allows it to be linked to economic benefits.

Physical water entities that group the physical water resources as well as the water access entitlements and allocations that have been issued by Governments.

These water entities are listed and defined in Table 2 and Table 3.

Table 2 Institutional Water Entities

Entity Description

Nation The Commonwealth of Australia or a representative agency State or territory Any of the States or Territories of Australia or a representative agency Water manager A body responsible for management of a physical water entity (eg

groundwater management unit, surface water management area, delivery system, urban drainage system). Mostly public authorities (eg Sunwater, NSW State Water, Goulburn-Murray Water, Sydney Water) but also private entities such as Murrumbidgee Irrigation Limited

Site manager Any person, corporation or public authority responsible for the management of an area of land used for production, amenity or environmental purposes

Water access entitlement owner

Any person, corporation or public authority that owns a water access entitlement

Water allocation owner Any person, corporation or public authority that owns a water allocation Environment A pseudo – owner of water access entitlements or environmental rules.

Though the environment doesn’t exist as a legal entity, it is useful as a reporting entity as water access entitlements can be committed to the environment, and rules commit water to the environment.

Table 3 Physical Water Entities

Entity Description

Australia The continent of Australia including Tasmania. State or Territory Any of the States or Territories of Australia Drainage division As per Australian Water Resources Assessment 2000 River basin As per Australian Water Resources Assessment 2000 Surface water management area

An area which is part or whole of a river basin. As per Australian Water Resources Assessment 2000.

Groundwater province As per Australian Water Resources Assessment 2000. Groundwater management unit

Any aquifer or set of hydrologically connected aquifers managed as a unit. As per Australian Water Resources Assessment 2000. Also should include ‘unincorporated’ units.

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 25

(Individual) Sites

Human physical water entities

Groundwater mgt unit

Surface water management area

River basin

Drainage division

Groundwater province

Australia

Drainage system(s)

Delivery system

Groundwater mgt unit

River basin

Delivery system

Water Accounting

Water manager

Nation

Institutional water entities

State or Territory

Environment

Site manager

Surface water management area

States & Territories

Natural physical water entities

Delivery system A set of connected channels, pipes, storages used to deliver water taken from water sources to properties or other delivery systems.

Trading zone A zone used for management of trading of water access entitlements or water allocations.

Drainage system A system of works used for the purpose of collecting and draining water from irrigation areas, water from rural areas outside irrigation areas, or storm water from urban areas.

Site Any land parcel, rural or urban.

Figure 2 is a simplified architecture diagram showing how the physical and institutional water entities relate to each other.

Figure 2 Water Entity Architecture

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 26

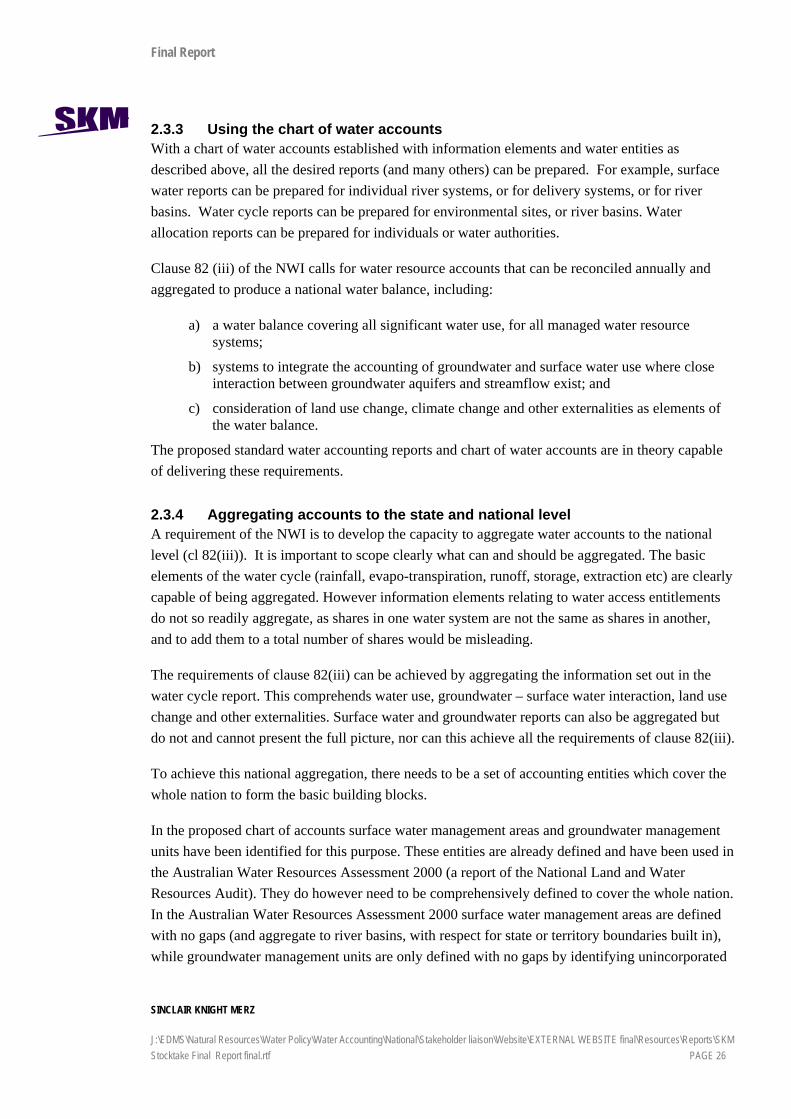

2.3.3 Using the chart of water accounts With a chart of water accounts established with information elements and water entities as described above, all the desired reports (and many others) can be prepared. For example, surface water reports can be prepared for individual river systems, or for delivery systems, or for river basins. Water cycle reports can be prepared for environmental sites, or river basins. Water allocation reports can be prepared for individuals or water authorities.

Clause 82 (iii) of the NWI calls for water resource accounts that can be reconciled annually and aggregated to produce a national water balance, including:

a) a water balance covering all significant water use, for all managed water resource systems;

b) systems to integrate the accounting of groundwater and surface water use where close interaction between groundwater aquifers and streamflow exist; and

c) consideration of land use change, climate change and other externalities as elements of the water balance.

The proposed standard water accounting reports and chart of water accounts are in theory capable of delivering these requirements.

2.3.4 Aggregating accounts to the state and national level A requirement of the NWI is to develop the capacity to aggregate water accounts to the national level (cl 82(iii)). It is important to scope clearly what can and should be aggregated. The basic elements of the water cycle (rainfall, evapo-transpiration, runoff, storage, extraction etc) are clearly capable of being aggregated. However information elements relating to water access entitlements do not so readily aggregate, as shares in one water system are not the same as shares in another, and to add them to a total number of shares would be misleading.

The requirements of clause 82(iii) can be achieved by aggregating the information set out in the water cycle report. This comprehends water use, groundwater – surface water interaction, land use change and other externalities. Surface water and groundwater reports can also be aggregated but do not and cannot present the full picture, nor can this achieve all the requirements of clause 82(iii).

To achieve this national aggregation, there needs to be a set of accounting entities which cover the whole nation to form the basic building blocks.

In the proposed chart of accounts surface water management areas and groundwater management units have been identified for this purpose. These entities are already defined and have been used in the Australian Water Resources Assessment 2000 (a report of the National Land and Water Resources Audit). They do however need to be comprehensively defined to cover the whole nation. In the Australian Water Resources Assessment 2000 surface water management areas are defined with no gaps (and aggregate to river basins, with respect for state or territory boundaries built in), while groundwater management units are only defined with no gaps by identifying unincorporated

Final Report

SINCLAIR KNIGHT MERZ

J:\EDMS\Natural Resources\Water Policy\Water Accounting\National\Stakeholder liaison\Website\EXTERNAL WEBSITE final\Resources\Reports\SKM Stocktake Final Report final.rtf PAGE 27

areas as “groundwater management units” (in which case aggregation to groundwater province is achieved).

If the accounts are set up so that the reports can be done for these entities, then the information from these reports can be rolled up through different paths to the national level. This is illustrated in Figure 3. The most important aggregation, if it can be achieved, will be the aggregation of water cycle information. Note that this includes both surface and groundwater information. It is recommended that the best entities for water cycle reports are surface water management area (and then river basin). To achieve this it means that groundwater information will need to be accounted within surface water management area (or river basin) boundaries as well as within groundwater management units. In some situations this presents difficulties as groundwater management units cross surface water management area boundaries. However such a protocol is sensible, given the vertical and lateral flow characteristics of groundwater (vertical flows are generally much greater than lateral flows), as well as necessary if holistic and integrated water resource management and accounting is to occur.

Figure 3 Aggregation of accounts to national level

Australia

Drainage Division

Groundwater province

State or territory

River basin

Surface water management

area