Stochastic Review

55

Stochastic Models in Finance and Insurance Script by Ilya Molchanov and Michael Schmutz [email protected] Recommended books: Primary • J.C. Hull, Options, Futures and other Derivatives, Prentice-Hall, 2009. • M. Baxter, A. Rennie, Financial Calculus, Cambridge University Press, 2001. • J. Cvitani´ c, F. Zapatero, Introduction to the Economics and Mathematics of Financial Markets, MIT Press, 2004. • W. Hausmann, K. Diener, J. K¨asler, Derivate, Arbitrage und Portfolio-Selektion, Vieweg, 2002. • A. Irle, Finanzmathematik. Die Bewertung von Derivaten, Teubner, 2003. Secondary • R. Dobbins, S. Witt, J. Fielding, Portfolio Theory and Investment Management, Blackwell, 1994. • E. Straub, Non-Life Insurance Mathematics, Springer, 1988. • H.U. Gerber, Life Insurance Mathematics, Springer, 1990. • S.N. Neftci, An Introduction to the Mathematics of Financial Derivatives, Academic Press, 1996. • P. Wilmott, Derivatives. The Theory and Practice of Financial Engineering, Wiley, 1998. • J.Y. Campbell, A.W. Lo, A.C. MacKinlay, The Econometrics of Financial Markets, Princeton University Press, 1997. • H. B¨ uhlmann, Mathematical Methods in Risk Theory, Springer, 1970. Further reading More economical/actuarial ... • R. Korn, E. Korn, Option pricing and Portfolio Optimization, Amer. Math. Society, 2001. • R.W. Kolb, Understanding Futures Markets, Blackwell, 1997. • R.W. Kolb, Practical Readings in Financial Derivatives, Blackwell, 1998. • D. Winstone, Financial Derivatives, Chapman & Hall, 1995. • E.J. Elton, M.J. Gruber, Modern Portfolio Theory and Investment Analysis, Wiley. • C.D. Daykin, T. Pentik¨ ainen, M. Pesonen, Practical Risk Theory for Actuaries, Chapman & Hall, 1994.

-

Upload

isaiah-eng -

Category

Documents

-

view

110 -

download

0

Transcript of Stochastic Review

Stochastic Models in Finance and InsuranceScript by Ilya Molchanov and Michael Schmutz [email protected] Recommended books:Primary J.C. Hull, Options, Futures and other Derivatives, Prentice-Hall, 2009. M. Baxter, A. Rennie, Financial Calculus, Cambridge University Press, 2001. J. Cvitani, F. Zapatero, Introduction to the Economics and Mathematics of Financial Markets, MIT c Press, 2004. W. Hausmann, K. Diener, J. Ksler, Derivate, Arbitrage und Portfolio-Selektion, Vieweg, 2002. a A. Irle, Finanzmathematik. Die Bewertung von Derivaten, Teubner, 2003. Secondary R. Dobbins, S. Witt, J. Fielding, Portfolio Theory and Investment Management, Blackwell, 1994. E. Straub, Non-Life Insurance Mathematics, Springer, 1988. H.U. Gerber, Life Insurance Mathematics, Springer, 1990. S.N. Neftci, An Introduction to the Mathematics of Financial Derivatives, Academic Press, 1996. P. Wilmott, Derivatives. The Theory and Practice of Financial Engineering, Wiley, 1998. J.Y. Campbell, A.W. Lo, A.C. MacKinlay, The Econometrics of Financial Markets, Princeton University Press, 1997. H. Bhlmann, Mathematical Methods in Risk Theory, Springer, 1970. u Further reading More economical/actuarial ... R. Korn, E. Korn, Option pricing and Portfolio Optimization, Amer. Math. Society, 2001. R.W. Kolb, Understanding Futures Markets, Blackwell, 1997. R.W. Kolb, Practical Readings in Financial Derivatives, Blackwell, 1998. D. Winstone, Financial Derivatives, Chapman & Hall, 1995. E.J. Elton, M.J. Gruber, Modern Portfolio Theory and Investment Analysis, Wiley. C.D. Daykin, T. Pentikinen, M. Pesonen, Practical Risk Theory for Actuaries, Chapman & Hall, 1994. a

FS 2011

Stoch Modelle FV

More mathematical ... R. Korn, Optimal Portfolios, World Scientic, 1997. P. Wilmott, J. Dewynne, S. Howison, Option Pricing, Oxford Financial Press, 1993 (mostly deterministic approach). P. Wilmott, S. Howison, J. Dewynne, The Mathematics of Financial Derivatives, Cambridge University Press, 1995. S.P. Pliska, Introduction to Mathematical Finance, Blackwell, 1997 (mostly discrete). S.E. Shreve, Stochastic Calculus for Finance, Springer, 2004. T. Mikosch, Elementary Stochastic Calculus with Finance in View, World Scientic, 1998. N.H. Bingham, R. Kiesel, Risk-Neutral Valuation. Pricing and Hedging of Financial Derivatives, Springer, 1998. Y.K. Kwok, Mathematical Models of Financial Derivatives, Springer, 1998. D. Lamberton, B. Lapeyre, Introduction to Stochastic Calculus Applied to Finance, Chapman & Hall, 1996. M. Musiela, M. Rutkowski, Martingale Methods in Financial Modelling, Springer, 1997. T. Rolski et al, Stochastic Processes for Insurance and Finance, Wiley, 1999.

Plan Chapter Chapter Chapter Chapter

1. 2. 3. 4.

Basic concepts of nancial derivatives Stochastic models for stock prices Portfolios Risk and insurance.

2

1. Basic concepts of asset returns, futures, options and other financial instruments

A nancial derivative is an instrument whose value depends on, or is derived from, the value of another asset. The underlying assets include stocks, currencies, interest rates, commodities, debt instruments, electricity, insurance payos, the weather, etc.

1. Asset returns1.1. Interest rates Consider an amount a invested for n years at an interest rate r per annum. If the rate is compounded once per annum, the terminal value of the investment is a(1 + r)n . If it is compounded m times per annum, the terminal rate of the investment is a(1 + r/m)mn . The limit as m tends to innity corresponds to continuous compounding aern . Let rc be the rate of continuous compounding and rm be the rate with compounding m times per annum. Then aerc n = a(1 + rm /m)mn , whence rc = m log(1 + rm /m) , rm = m(erc /m 1) .

For instance, with a single annual compounding m = 1 and r = r1 rc = log(1 + r) , 1.2. Forward rates The forward interest rate is the interest rate for a future period of time implied by the rates prevailing in the market today. r = erc 1 .

3

FS 2011

Stoch Modelle FV

Year 1 2 3 4 5

Zero rate 10.0 10.5 10.8 11.0 11.1

Forward rate 11.0 11.4 11.6 11.5

Example: if $100 invested for one year and then for another year, then 100e0.10 e0.11 = 123.37 = 100e10.52 .

2. Forwards and futures2.1. Forward contacts A forward contract is a contract that obligates the holder to buy or sell an asset for a predetermined delivery price at a predetermined future time. The main features of a Forward contract are: initiated now, performed later; involves exchange of assets; price set at time of contracting. 2.2. Some important words and concepts

buyer = long position; buying = going long seller = short position; selling = going short

portfolio = combination of several assets/securities, etc.Short selling involves selling an asset that is not owned with the intention of buying it later. Example: An investor contacts a broker to short 500 IBM shares. The broker borrows the shares from another client and sells them depositing the proceeds to the investors account. At some stage the investor instructs the broker to close out the position, the broker uses the funds from the investor to purchase 500 IBM shares and replaces them. If at any time, the broker runs out of shares, the investor is short-squeezed and must close the position immediately, even if not ready to do so. 2.3. Futures A futures contract is a standardised contract that obligates the holder to buy or sell an asset at a predetermined delivery price during a specied future period. The contract is settled daily.

4

FS 2011

Stoch Modelle FV

Futures: Futures Futures Futures Futures Futures Futures

started at Chicago Board of Trade, opened 1848 trade on organised exchanges. contracts have standardised contract terms. exchanges have associated clearinghouses to guarantee fullment of futures contract obligations. trading requires margin payment and daily settlement. positions can be closed easily. markets are regulated by identiable agencies, while forward markets are self-regulating.

Standardised contract terms cover the following issues: quantity quality expiration months delivery terms delivery dates (normally any day in a month) minimum price uctuation (tick is the smallest change in the price of a futures contract permitted by the exchange) daily price limit (restricts price movements in a single day) trading days and hours Clearinghouse guarantees fullment of the contract, acting as the seller to the buyer and as the buyer to the seller. Thus, the buyer and seller do not have to check credit worthiness. Margin provides a nancial safeguard to ensure that traders will perform on their contract obligations. Initial margin (deposit requested from trader before trading any futures, usually 5% of the commoditys value). Maintenance margin. If the trader sustains a loss, it is taken from his margin. When the value of the funds on deposit reaches the maintenance margin (usually 75% of the initial margin), the trader is required to replenish the margin (this demand is known as margin call). Closing a futures position Delivery or cash settlement (usually not more than 1% of all contracts end this way, for currencies this may be about 2%). Oset or reversing trade (the trader enters the reverse contract, so his net position is zero which is recognised by the clearinghouse; the reverse contract should match exactly the original contract entered). Types of futures contracts: agricultural and metallurgical contracts interest-earning assets (bonds, treasury bills, etc.) foreign currencies stock indices (they do not admit a possibility of actual delivery) Combination of several related futures is called a spread intramarket spread, also called calendar spread or time spread intermarket spread (dierent but closely related commodities) Abusive trading practices and manipulations Example: (The Hunt Silver Manipulation) Prices (per ounce in US dollars): 6 (1979), over 50 (Jan 1980), 12 (Mar 1980), 5-6 (1996). Amassed gigantic futures contracts and demanded delivery as they came due; at the same time, they bought big quantities of physical silver and held it o the market. The exchange imposed 5

FS 2011

Stoch Modelle FV

liquidation-only trading, meaning trade to only close existing futures positions. The exchange increased the margins on silver, then Hunts defaulted on their margin obligations. They tried to issue bonds backed by their physical silver holdings, which the market interpreted as act of desperation and the price crashed. Sued by their co-conspirators, became bankrupt by 1990. 2.4. Traders A speculator is a trader who enters the futures market in pursuit of prot, accepting the risk. A hedger is a trader who trades futures to reduce some preexisting risk exposure. They are often producers or major users of a given commodity (e.g., a farmer may hedge by selling his anticipated harvest even before the farmer plants). They often trade through a brokerage rm. Arbitrageurs enter several contracts in dierent markets to exploit price uctuations. If a good had two prices, a trader can get an arbitrage prot a sure prot with no investment. But prices may dier because of transportation costs, etc.

Arbitrage = trading without investment that guarantees no loss with probability one and potential income with a non-zero probabilityTrading orders: market order (buy or sell at the best price currently available); limit order (maximum and minimum prices specied); short sale; stop order (activated when the price of a stock reaches a predetermined limit).

3. Hedging using futuresA company that is due to sell an asset takes a short futures position (short hedge). If the price goes down, the company loses on the sale, but makes a gain on the short futures position. If the price goes up, the company loses on futures and gains on sales. A company that is due to buy an asset takes a long hedge. Note: a futures hedge does not necessarily improve the nal outcome, it even makes it worse roughly 50% of the time. But it reduces the risk by making the outcome more certain. Example. Italian company expects to receive 50 million USD at the end of July. USD contracts have deliveries Mar, Jun, Sep, Dec. The company shorts four 12.5 million Sep USD contracts. In the end of Jul the company receives USD and closes out futures position. If the Sep futures price in Mar was 0.78 and the spot and futures price in Jul are 0.72 and 0.7250, then the gain on futures is 0.78-0.725=0.055 cents per USD. The eective price per USD will be 0.72+0.055=0.775. Rolling the hedge forward is achieved by entering successive futures contracts and closing out previous contracts. Optimal hedge ratio Hedge ratio h is the ratio of the size of the position taken in futures contracts to the size of the exposure. Let S be the change in spot price, S, during the life of the hedge; let F be the change in futures price, F , S , F are standard deviations of S and F and is the coecient of correlation.

6

FS 2011

Stoch Modelle FV

For a short hedge the eective price obtained is S2 + h(F1 F2 ), so that change of total value S hF (and hF S for a long hedge). The variance of the change of value (in either case) is2 2 S + h2 F 2hS F ,

which is minimised if h=

S . F

The optimal h = 1 if the futures prices mirror the spot price perfectly.

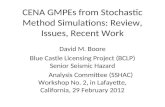

4. Futures pricesNewspaper quotes First line: nearby contract, then distant or deferred contracts; opening, high, low prices; settlement price (at the close of trading); change in the settlement price from the previous day; open interest (the number of futures contracts for which delivery is currently obligated). Example. A buys and B sells one contract, the open interest is one; C buys and D sells 3 contracts, the open interest is 4; then A sells and D buys 1 contract, the open interest is 3. Basis is current cash price minus futures price. In a normal market the prices for more distant futures are higher, while in the inverted market the distant future prices are lower.

Figure 1.1: Converging cash and futures prices (normal market) Assume that the market is perfect (no transaction costs and no restrictions on free contracting). The cost-of-carry or carrying charge is the total costs to carry a good forward in time: storage, insurance, transportation and nancing costs. We will mostly consider the nancing costs. 4.1. Examples Assume that interest rate is 10%

7

FS 2011

Stoch Modelle FV

Cash-and-Carry strategy Spot price of gold 1800; Future price of gold (delivery in 1 year) 2000 Transaction: t=0 Borrow 1800 for one year at 10% Buy 1 ounce of gold in the spot market for 1800 Short a futures contract for delivery in 1 year for 2000 t=1 Remove the gold from storage Deliver the ounce of gold, repay the loan, including interest Total cash flow: .... Reversed Cash-and-Carry Strategy Spot price of gold 1800; Future price of gold (delivery in 1 year) 1950 Transaction: t=0 Sell ounce of gold short Lend 1800 for 1 year at 10% Enter a long position in a future for buying 1 ounce of gold in one year t=1 Collect proceeds from the loan Accept delivery of the futures contract Total cash flow: .... 4.2. Pricing rule The futures price must equal the spot price plus the cost of carrying the spot commodity forward to the delivery date of the futures contract F0,T = S0 (1 + C) or F0,T = S0 ecT ,

where C (resp. c) measures the storage cost plus the interest that is paid to nance the asset less the income earned on the asset. If the above equations hold, the market is a full carry market. Example: Silver Sep 41.20, Silver Dec 41.95, Bankers Acceptance Rate 90 days 7.5%. Then (41.95/41.20)4 = 1.0748 corresponds roughly to the interest rate. If an asset provides income I during the life of a contract, then F0,T = (S0 I)erT . It is important to remember that I is the discounted price (i.e. price at time zero) of all future cash ows. Reason: buy one unit of the asset and enter a short forward contract to sell it for F0,T . This costs S0 and should match cash inow I + F0,T erT . 4.3. Pricing under transaction costs The transaction costs and other market imperfections lead to the appearance of two prices: the ask price at which the goods are sold and the bid price at which they are purchased. The ask price is always greater than or equal to the bid price. For nancing purposes, this corresponds to the two interest rates: the lending rate and the borrowing rate. If T denotes transaction costs, then S0 (1 + CL )(1 T ) F0,T S0 (1 + CB )(1 + T ) , 8

FS 2011

Stoch Modelle FV

where CL is the lending rate and CB is the borrowing rate. There are normally restrictions on short selling. If only a part f of the funds may be used, then S0 (1 + f CL )(1 T ) F0,T S0 (1 + CB )(1 + T ) .

5. BondsInterest rates: Treasury rates - risk-free. LIBOR rates (London Interbank Oer Rate) - not necessarily risk-free (usually quoted on loans expressed in dollars; used by numerous nancial institutions). Repo rate (repurchase agreement) - very little risk (one party sells a security to another party and agrees to buy it back at a specied time/price). 5.1. Pure discount bonds A pure discount bond promises to pay a certain amount (face value) at a specied time in the future and is sold for less than this promised future payment. Its price: P = C (1 + r)T or P = erT C ,

where C is the cash to be paid at the maturity of the bond at time T , r is the annualised (resp. continuously compounded) yield to maturity (yield: a return provided by an instrument). 5.2. Coupon bonds Coupon bonds make regular scheduled payments between the date of issue and the maturity date. Treasury bills (T-bills) (up to one year maturity). Treasury bonds and Treasury notes (longer maturity). Eurodollar CD (Certicate of Deposit) - issued by banks outside the US to attract dollar denominated funds (US$ deposited in foreign banks). Repurchase agreement or repos, when one party sells a security to another part and agrees to buy it back at a specied time/price. Example: Treasury zero rates are rates for investments that start today and last some time without intermediate payments and with continuous compounding. For example, 0.5 years - 5.0%, 1.0 - 5.8%, 1.5 - 6.4%, 2.0 - 6.8%. Consider two-year treasury bond of $100 with coupons at rate 6% p.a. with the coupons being paid semiannually. The theoretical price of this bond is 3e0.050.5 + 3e0.0581.0 + 3e0.0641.5 + 103e0.0682.0 = 98.39 . To nd the yield on the bond we have to solve 3ey0.5 + 3ey1.0 + 3ey1.5 + 103ey2.0 = 98.39 that gives y = 6.76%. 9

FS 2011

Stoch Modelle FV

To nd its par yield c solve c 0.050.5 c 0.0581.0 c 0.0641.5 c e + e + e + (100 + )e0.0682.0 = 100 2 2 2 2 that gives c = 6.87 per annum with semiannual compounding. 5.3. Currency futures The futures price is given by

F0,T = S0 e(rrf )T ,

where rf is the risk-free interest rate in the foreign country. Reason: the holder may invest the foreign currency in a foreign-denominated bond, which brings extra income.

6. Major Market IndicesA stock index tracks changes in the value of a hypothetical portfolio of stocks. The weight of a stock in the portfolio equals the proportion of the portfolio invested in the stock. The percentage increase in the stock index over a small interval of time is set equal to the percentage increase in the value of the hypothetical portfolio. Dividends are usually not included in the calculation so that the index tracks the capital gain/loss from investing in the portfolio (an exception to this is a total return index, which is calculated by assuming that dividends on the hypothetical portfolio are reinvested in the portfolio). If the hypothetical portfolio of stocks remains xed, the weights assigned to individual stocks in the portfolio do not remain xed. When the price of one particular stock in the portfolio rises more sharply than others, more weight is automatically given to that stock. Some indices are constructed from a hypothetical portfolio consisting of one of each of a number of stocks. The weights assigned to the stocks are then proportional to their market prices, with adjustments being made when there are stock splits. Other indices are constructed so that wights are proportional to market capitalization (stock price number of shares outstanding). Important market indices: Dow Jones Industrial Average (DJIA); S&P 100 and S&P 500 Indices; FTSE 100 (25 pounds per index point, a tick is 12.50); The Nikkei index (225 largest Japanese rms); and naturally SMI. 6.1. Pricing and hedging with indices The index can be considered as an asset providing a continuous dividend yield at rate q. Then F0,T = S0 e(rq)T .

10

FS 2011

Stoch Modelle FV

Example. Hedging the value of a portfolio (vanishing cost of carrying) Cash market Futures market 5 April Holds a balanced portfolio of UK Sells eight June FTSE 100 contracts shares valued at 1 million pounds at a price of 5000 each (25x5000x8), so but fears a fall in its value. committing himself to the notional sale The current FTSE is 5000. of 1 million of stock at equity prices implied by the futures price on 5 Apr 10 May The FTSE 100 index has fallen Closes out the futures position buying to 4750. The value of portfolio eight June FTSE 100 contracts at a price declines to 950,000. of 4750. Loss of 50,000 Gain of 50,000 The other action can be undertaken if the hedger anticipates receipt of cash and fears a rise in the index. Then one buys futures index contracts.

11

FS 2011

Stoch Modelle FV

7. Options

Call option gives the owner the right to buy a particular good at a certain price. Put option gives the owner the right to sell a particular good at a certain price.The seller of an option is also known as the writer of an option. The act of selling is called writing an option. Each option contract stipulates a price that will be paid if the option is exercised, known as exercise price or strike price. Options are usually valid for only a limited time (until maturity). Every option involves a payment from the buyer to seller (price or premium of an option).

American options can be executed at any time prior to maturity. European options can be executed only at maturity.In the USA, options are traded at the Chicago Board Options Exchange, Philadelphia Exchange, the American Stock Exchange and the Pacic Stock Exchange. Stock options on over 500 dierent stocks (in lots of 100 shares) mostly American; foreign currency options (depending on currency, e.g. 31,250 pounds per option) American and European; index options (S&P 100 American and S&P 500 European at 100 times the index); options on futures (the underlying asset is a futures contract - when the holders of a call/put option exercise they acquire a long/short position in the futures contract plus a cash amount equal to the excess of the futures/strike price over the strike/futures price). Newspaper quotes on stock options: the rst column - the company and the closing stock price (per share, so it is to be multiplied by 100). The strike price and maturity appear in the second and third columns. If traded before, then the volume and, nally, the prices for call and put options are included. Margin accounts are always required for writers. When the option is purchased the option price must be paid in full (and not from margin accounts). The Options Clearing Corporation (OCC) performs the same role as clearinghouses for futures. When the option is exercised, the broker noties the OCC; it randomly selects a member with an outstanding short position in the same option. The member using an established procedure, elects a particular client who has written an option. The client is said to be assigned.Profit/Loss

Profit/Loss

0 17

240 Price

0 9

240 Price

Figure 1.2: Prot/loss prole of a call/put option at expiry. The strike price is 240. For writers of an option the graphs are opposite.

12

FS 2011

Stoch Modelle FV

7.1. Hedging with options Positions in options trading: A long position is a call position. A long position is a put position. A short position is a call position. A short position is a put position.Profit/Loss Profit/Loss

0

Price

0

Price

(a) Long position in a Stock and (b) Short position in a Stock and short position in a Call long position in a CallProfit/Loss Profit/Loss

0

Price

0

Price

(c) Long position in a Stock and (d) Short position in a Stock and Long position in a Put short position in a Put

Figure 1.3: Strategies involving a single option and a stock

7.2. Spreads A spread trading strategy involves taking a position in two or more options of the same type. A bull spread can be created by buying a call option on a stock with a certain strike price and selling a call option on the same stock with a higher strike price. Both options have the same expiration date. (It can be also created by buying a put with a low strike price and selling a put with a higher strike price). Reason: Limits the traders upside as well as downside risk. The trader gives up some upside potential by selling a call option with higher strike price X2 . If ST X2 , then the total payo is X2 X1 ; if X1 < ST < X2 , then the payo is ST X1 ; if ST X1 , the payo is zero. The gain is obtained as payo minus the price of option bought plus the price of option sold. Bull spread with calls involves an initial investment, as the price of the option sold is less than the price of the option purchased. A trader who enters into a bear spread is hoping that the stock price will decline. Then the price of an option purchased is greater than the price of the option sold. 13

FS 2011

Stoch Modelle FV

Profit/Loss

Profit/Loss

0

Price

0

Price

Figure 1.4: Bull/bear spread created using two call options

A buttery spread is created by buying a call option with a relatively low strike price X1 , buying a call option with a relatively high strike price X3 and selling two call options with a strike price X2 , half-way between X1 and X3 . It provides a modest return when the market is stable. A reversed strategy produces a modest prot if there is a signicant change in the stock price.

Profit/Loss

0

Price

Figure 1.5: Buttery spread created using call options Combinations involve taking a position in both calls and puts on the same stock. A straddle involves buying a call and a put with the same strike price and expiration date. In a strangle a trader buys a put and a call with the same expiration date and dierent strike prices. They can be useful if the trader is betting that there will be a large price move but is uncertain whether it will be an increase or a decrease.

14

FS 2011

Stoch Modelle FV

Profit/Loss

Profit/Loss

0

Price

0

Price

Figure 1.6: Straddle and strangle

7.3. Other derivatives (exotic derivatives) Standard Oils Bond (1986). There is no interest, but when the bond matures, the holders will receive a supplement based on the oil price at maturity. Range forward contract. E.g., a three month sterling contract with dollar exchange rate between 1.6 and 1.64. If the rate lies outside the limits, then the lower/upper limit applies. Weather derivatives have payos depending on the average temperature at particular locations. Insurance derivatives have payo dependent on the dollar amount of insurance claims. Electricity derivatives have payo dependent on the spot price of electricity, etc. etc. etc.

15

2. Stochastic models for stock market prices

1. Properties of option pricesFactors aecting option prices the current stock price and the strike price (call options are more valuable if the stock price increases and less valuable if the strike price increases) the time to expiration (put and call American options are more valuable as time to expiration increases; European options are not necessarily more valuable) the volatility of the stock price, , so that t is the st. deviation of the return on the stock in a short length of time t (the owner of a call benet from price increases but has limited downside risk; the owner of a put benets from price decreases but has limited risk if price increases; therefore, the value of both calls and puts increases as volatility increases) the risk-free interest rate (if the rate increases, the expected growth rate of the stock price tends to increase, however, the present value of any future cash ows decreases, therefore the value of a put option decreases; for call options the rst eect tends to increase the price, while the second tends to decrease it, but the rst always dominates, so the value increases) the dividends expected during the life of an option (reduce the stock price on the ex-dividend date, decrease the value of a call option, but increase the value of a put option) Assumptions: no transaction costs; all trading prots (losses) are subject to the same tax rate; borrowing and lending at the risk-free interest rate is possible.

NotationS0 current stock price St stock price at time t X strike price of option T time of expiration of option r risk-free rate of interest C value of American call option to buy one share P value of American put option to sell one share c value of European call option to buy one share p value of European put option to sell one share

16

FS 2011

Stoch Modelle FV

1.1. Upper bounds

c S0 , p XerT

C S0 , P X.

,

1.2. Lower bounds for non-dividend paying stocks European calls c S0 XerT . Example. S0 = 20, X = 18, r=10% p.a., T=1 year. Then S0 XerT = 3.71. Assume that the option costs $3. Then an arbitrageur buys the call and shorts the stock. This provides cash 20 3 = 17, invested for one year risk-free, it gives 17e0.1 = 18.79. Then the option expires. If the stock price is greater than $18, the arbitrageur exercises the option and makes a prot of 18.79 18 = 0.79. If the stock price is less than $18, say $17, then the stock is bought in the market and the prot is 18.79 17 = 1.79. Proof of the lower bound. Consider two portfolios: A (one European call option and cash XerT ) and B (one share). At time T , portfolio A is worth max(ST , X), while portfolio B is worth ST . Thus A must be worth more than B today, meaning that c + XerT S0 . European puts p XerT S0 . For the proof consider two portfolios: A (one put option and one share) and B (cash XerT ). 1.3. Put-call parity for European options on non-dividend paying stock Consider two portfolios: A - one call option plus an amount of cash equal to XerT ; B - one put option plus one share. At time T both portfolios are worth max(ST , X), so (because they are European) they must have identical values today: c + XerT = p + S0 . This is known as put-call parity. 1.4. Dividends-paying stock Let D be the present (time zero) value of the future dividends, i.e. the future dividends are discounted. Consider two portfolios: A - one European call option and cash D + XerT , where D is the present value of dividends; B - one share. 17

FS 2011

Stoch Modelle FV

Then Similarly Put-call parity for European options

c S0 D XerT . p D + XerT S0 . c + D + XerT = p + S0 .

1.5. American options (Early exercise) Example. A trader owns a call option on a non-dividend paying stock with strike price $40 and the current stock price $50 with one month to expiry. It is better not to exercise early, because $40 can earn interest for a month, and also the option is a protection against falling price of a stock. It is better to sell the option (or keep the option and short the stock). Thus C S0 XerT . For dividends paying stock, it may be optimal to exercise a call option early. In contrast to call options, it can be optimal to exercise a put option early. For example, let X = 10 and let the stock price be zero. Then it is better to exercise immediately to get the maximal prot and invest it. Thus P X S0 . There is no put-call parity for American options.

2. Binomial trees2.1. Example (a wrong approach to option pricing) Assume that now 1 Euro=$1.15 and in a month it will be worth either $0.75 or $1.45 with equal probabilities. Assume that interest rates are zero. Let a European call option have strike price $1.15. Then the expected gain on the option will be V = (1.45 1.15) 0.5 + 0 0.5 = 0.15 . One might be tempted to think that this is the fair price of an option. However an arbitrageur may do the following Buy the option at price 0.15; lend x dollars; borrows y Euros at $1.15. His balance at time zero is 0.15 x + 1.15y. In case of zero initial investment, the balance at time zero should be zero too, i.e. 0.15 x + 1.15y = 0 so that x = 1.15y 0.15 .

Starting with zero investment, in a month there are two possibilities. If the Euro has risen, the option is exercised, he buys y Euros at 1.45 and pays back the loan, so that his balance is 0.30 1.45y + x = 0.3 1.45y + 1.15y 0.15 = 0.15 0.3y . 18

FS 2011

Stoch Modelle FV

If the Euro has fallen, option is worthless, he buys y Euros at 0.75 and pays back the loan, so his balance is 0.75y + x = 0.75y + 1.15y 0.15 = 0.4y 0.15 . Then there are some values of y, so that the end balance is positive in any case. For this, solve 0.15 0.3y > 0, i.e. the choice3 8

0.4y 0.15 > 0 ,

1 and d < 1) with option values fu and fd . Then S0 u fu = S0 d fd ,

19

FS 2011

Stoch Modelle FV

S0 u fu S0 f

S0 d fd

Figure 2.2: A general one-step binomial tree

whence =

fu fd . S0 u S0 d

Let r be the risk-free interest rate. Then the present value of the portfolio should be equal to the cost of setting up the portfolio (S0 u fu )erT = S0 f . Then After substituting the value of where q= f = S0 (S0 u fu )erT . f = erT [qfu + (1 q)fd ] , erT d . ud

Note that if the value of q lies outside [0, 1], one has an immediate arbitrage opportunity.

This option price f does not refer to the probabilities of the stock moving up or down. The probabilities are incorporated into the price of the stock. Then q can be interpreted as the probability of up movement, (1 q) is the probability of a down movement, and qfu + (1 q)fd is the expected payo from the option.The expectation with respect to the risk-free probabilities will be denoted by E Q , while the expectation in the real world is E P . Then the expected stock price is E Q (ST ) = qS0 u + (1 q)S0 d = S0 erT , meaning that the price grows, on average, risk-free. 2.4. Risk-neutral valuation In a risk-neutral world all individuals are indierent to risk, require no compensation for risk, and the expected return on all securities is the risk-free interest rate. Thus the value of an option is its expected payo in a riskneutral world discounted at the risk-free rate.

20

FS 2011

Stoch Modelle FV

Risk-neutral valuation principle states that it is valid to assume the world is risk-neutral when pricing options. The resulting option prices are correct in the real world as well.Example. Let q be a probability of up movement in Figure 2.1 (in the risk-neutral world). Then 22q + 18(1 q) = 20e0.120.25 , so that q = 0.6523. The expected value of the option is then also $0.6523, it should be discounted at the risk-free rate as 0.6523e0.120.25 = 0.633. 2.5. Two-step binomial trees Figure 2.3 shows a two-step tree with two steps of three months long. The value of an option at node B is given by (u = 1.1, d = 0.9, so that q = 0.6523) e0.120.25 [0.6523 3.2 + 0.3477 0] = 2.0257 . In a similar way it is possible to do calculations backwards.

D

24.2 3.2

22

B 2.0257

A 20 1.2823

E 19.8 0.0

18 0.0

C F 16.2 0.0

Figure 2.3: Stock and option prices in a two-step tree. The strike price is $21. For a general two-step tree shown in Figure 2.4, u and d remain the same, so is q. Then, if each step takes time t, fu = ert [qfuu + (1 q)fud ] , fd = ert [qfud + (1 q)fdd ] , f = ert [qfu + (1 q)fd ] . Thus f = e2rt [q 2 fuu + 2q(1 q)fud + (1 q)2 fdd ] . 21

FS 2011

Stoch Modelle FV

S 0 u2 fuu S0 u fu S0 f S0 d fd S0 d2 fddFigure 2.4: A general two-step tree

S0 ud fud

A general step on a multi-step tree with a slightly dierent but related argument is obtain with the help of a replicating portfolio based on the asset and on a bond. Notation t is the length of the time period (of the step) Si stock price at time i, Siu (Sid ) stock price after an up (down) movement i+1 stock holding for the step from i to (i + 1) in the replication protfolio i+1 bond holding for the step from i to (i + 1) in the replication portfolio fi claim value at time i, fiu (fid ) claim value after an up (down) movement erit bond value at time i q arbitrage probability of up-jump Q measure made up of the qs By ensuring i+1 Si u + i+1 er(i+1)t = fiu i+1 Si d + i+1 er(i+1)t = fid , i.e. i+1 = fiu fid , Si (u d) i+1 = ufid dfiu r(i+1)t (u e ,

d)

we know that the replication portfolio yields the same value as the claim value not depending on the direction of the stock movement. In order to avoid arbitrage in any time step we obtain fi = i+1 Si + i+1 erit = ert (qfiu + (1 q)fid ) , with q= Finally, i+1 can be rewritten as ert d . ud

i+1 = erit fi i+1 Si erit .

Note that by backward induction the value of the derivative is given by the discounted expectation of the claim payo where the expectation is calculated with respect to Q. 22

FS 2011

Stoch Modelle FV

2.6. Put options Similarly, put options can be priced. For them, there is a dierence between American and European options, as early exercise may be protable, see Figure 2.5. Here the interest rate is 5%, and the strike price is 52$. There are two time steps of one year, and in each step the price goes up or down by 20%.

D 72 0 B 1.4147 50 A 4.1923 (5.0894) 40 60

E 48 4

C 9.4636 (12.0)

F

32 20

Figure 2.5: Two-step tree for European and American put options (if dierent, American option prices are given in parentheses)

2.7. Delta hedging Delta is the ratio of the change in the price of the derivative to the change in the price for the underlying asset, e.g., for Figure 2.1, 10 = = 0.25 . 22 18 Note that may change over time. Mathematically, = f . S

Delta hedging requires buying (the value) shares of the stock. Example. Stock price $100, = 0.6, the option price is $10. An investor sells 20 option contracts (i.e. options to buy 20 100 = 2000 shares). His position could be hedged by buying 0.6 2000 = 1200 shares. The gain/loss on the option position would then tend to be oset by the loss/gain on the shares purchased. For example, if the stock price goes up by $1, the option price will tend to go up by $0.6, so loss=gain. NOTE. Because changes, the investors position remains delta hedged for only a relatively short period of time. The hedge has to be adjusted (known as rebalancing).

23

FS 2011

Stoch Modelle FV

3. Stochastic processes on binomial trees3.1. Main concepts The set of possible stock values is a stochastic process S, it depends on time as Si (discrete time) or St (continuous time). The set of probabilities pj or qj associated with nodes of the tree is a measure P or Q. They describe how likely is to jump up or down. A ltration (Fi ), Fi is the history of the stock up until tick-time t = i on the tree. A claim X (on a nite tree) is an FT -measurable function. The conditional expectation operator E P (|Fi ). For example, E P (X|Fi ) is the expectation of X along the latter position of paths which have initial segment Fi . This expectation depends on Fi and so is a random variable itself. The claim X can be converted into a process E P (X|Fi ) or E Q (X|Fi ) if the measure P or Q is given. A predictable process is a process on the same tree whose value at any given node at time tick i depends only on the history up to one time-tick earlier Fi1 (F1 = F0 ). Predictable processes play the part of trading strategies where we cannot tell in advance where prices are going to go. A process S is a martingale with respect to a measure Q and a ltration (Fi ) if Sj is Fj -measurable for all j and E Q (Sj |Fi ) = Si for all i j . This means that S has no drift under Q. Then Q is called a martingale measure for S and S is called a Q-martingale (if the underlying probability space is not nite we also need E |Sj | < for all j in the denition). NOTE: For any claim X, the process E Q (X|Fi ) is a Q-martingale . 3.2. Binomial representation theorem Theorem. If S is Q-martingale and E is any other Q-martingale, then there exists a predictable process such thati

Ei = E0 +k=1

k Sk ,

where Sk = Sk Sk1 . Proof. Consider a typical node. As there are two values only, the random variables can be transformed to eachSup Eup

Snow

Enow

Sdown

Edown

Figure 2.6: Process S on left; process E on right

24

FS 2011

Stoch Modelle FV

other by scaling and oset Ei = i Si + k , for i and k known by Fi1 . The conditional expectation given Fi1 of Si and Ei should be zero, as they are martingales. Thus, k = 0. 3.3. The bond process The bond process Bi represents the value of $1 at time i. It is a predictable and positive process, B0 = 1.1 The process Bi is another predictable process called the discount process. 1 Zi = Bi Si is the discounted stock process. 1 BT X is the discounted claim.

3.4. Self-nancing strategies1 1 Let the discounted stock process Zi = Bi Si be a Q-martingale. Another Q-martingale is Ei = E Q (BT X|Fi ). Then there exists a predictable process such that i

Ei = E0 +k=1

k Zk .

At time i buy the portfolio i with i+1 units of stock;1 i+1 = (Ei i+1 Bi Si ) units of the cash bond.

Note that and are predictable. At time i, the portfolio is worth Vi = i+1 Si + i+1 Bi . At time zero, portfolio 0 is worth 1 1 S0 + 1 B0 = E0 = E Q (BT X) . After one time tick 0 is worth1 1 1 S1 + 1 B1 = B1 (E0 + 1 (B1 S1 B0 S0 )) = B1 (E0 + 1 Z1 ) = B1 E1

by the binomial representation theorem. On the other hand, the portfolio 1 scheduled to be acquired at time 1 costs also B1 E1 , so we can cash 0 to buy 1 . This strategy is called self-nancing, since the change in value V of the portfolio dened by the strategy obeys the dierence equation Vi+1 Vi = Vi = i+1 Si + i+1 Bi 1 (the general step follows below). At the end the portfolio will be worth BT BT X = X, as required. Thus the 1 claim price is E Q (BT X). For a general step i, note that Vi = i+1 Si + i+1 Bi = i+1 Si + Bi Ei i+1 Si = Bi Ei . Therefore,1 i+1 Si+1 + i+1 Bi+1 = Bi+1 (i+1 + Bi+1 i+1 Si+1 ) 1 1 = Bi+1 (Ei i+1 Bi Si + Bi+1 i+1 Si+1 )

= Bi+1 (Ei + i+1 Zi ) = Bi+1 (Ei + Ei ) = Bi+1 Ei+1 . 25

FS 2011

Stoch Modelle FV

Repeating this until day T , we see that the value of the portfolio will be equal to BT ET . Option price formula The value at time i of a claim X maturing at date T is1 Bi E Q (BT X|Fi ) .

A martingale measure Q (i.e. a measure such that Bi1 Si is a Q matringale) always exists in the binomial model (and it is unique). The real measure P (which S follows) is irrelevant.

4. More general discrete-time modelsConsider a discrete-time nancial model with time horizon N dened on a nite and ltered probability space (, F, (Fn )n=0,...,N , P) (recall that a ltration is an increasing sequence of -subelds of F), with the additional assumptions that F0 = {, }, FN = F = P(), and P({}) > 0 for .0 1 d The (d + 1)-dimensional vector of prices at time n is denoted by Sn = (Sn , Sn , . . . , Sn ) and contains positive random variables being measurable with respect to Fn . The zero-coordinate contains the riskless asset and we 0 0 set S0 = 1 and Sn = (1 + r)n , while the assets indexed by i = 1, . . . , d are called risky assets.

Important denitions are A trading strategy is a predictable (i.e. i is Fj1 -measurable for all i, and j 1 and i is F0 0 j measurable for all i) Rd+1 -valued stochastic process = ((0 , 1 , . . . , d ))0nN , where i stands for n n n n the quantity of asset i held in the portfolio at time n. The (discounted) value of the corresponding portfolio is the scalar productd

Vn () = n Sn =i=0

i i Sn n

S S 0 Vn () = (Sn )1 (n Sn ) = n Sn , Sn = 1, n , . . . , n 0 0 Sn Sn

1

d

.

A strategy is self-nancing if the equation n Sn = n+1 Sn (equivalently, Vn+1 () Vn () = n+1 (Sn+1 Sn )) holds for all for all 0 n N 1. A strategy is admissible if it is self-nancing and if Vn () 0 for any n {0, 1, . . . , N }. An arbitrage is an admissible strategy with V0 = 0 and P(VN > 0) > 0. A real-valued adapted (for any n, Mn is Fn -measurable) process (Mn )0nN (being automatically integrable on our nite probability space) is a martingale if E (Mn+1 |Fn ) = Mn for all n N 1. Furthermore, we denote an Rd -valued process (Mn )0nN to be a martingale if each component is a real-valued martingale. A market is viable if there is no arbitrage opportunity. The following result is often called the Fundamental Theorem of Asset pricing. Theorem The market is viable if and only if there exists a probability measure Q equivalent to P such that the discounted prices of assets are Q-martingales. 26

FS 2011

Stoch Modelle FV

Some more denitions A contingent claim is a non-negative FN -measurable random variable X (here automatically integrable). The contingent claim dened by X is attainable if there exists an admissible strategy worth X at time N . The market is complete if every contingent claim is attainable. The following result is often called the Second Fundamental Theorem of Asset pricing. Theorem A viable market is complete if and only if there exists a unique probability measure Q equivalent to P, under which discounted prices are martingales.0 0 It follows that in a complete market it is quite natural to call Sn E Q ((SN )1 X|Fn ) the value of the option at time n.

An example for a complete market is the Binomial model, while the Trinomial model is an example for an incomplete market. The above results also have dierent (more complicated) formulations depending on the level of generality.

27

FS 2011

Stoch Modelle FV

5. Continuous processes5.1. Heuristic arguments Let Bt = ert and let S0 be the initial stock price. Single small step. Assume that over a small time interval t the stock moves to either value S0 et+ t

(if up) or to S0 et t (if down). Here denotes the return on the stock, so that the expected price after time t is Set . Further is the volatility. The probability of up-movement is S0 et Sdown S0 et S0 et t 1 e t p= = = Sup Sdown S0 et+ t S0 et t e t e t 1 1 1 t , 2 2 where the exponentials is decomposed using the Taylor expansion up to the second order. Many steps. Real world. If n = t/t, then St = S0 exp t + t 2Xn n n ,

where Xn is the total number of up-jumps. The random variable Xn has the binomial distribution Bi(n, p). Thus, (2Xn n)/ n has mean 2np n = 1 nt = 1 t 2 2 n and the variance 4np(1 p) 1 1 = (1 1 t)(1 + 2 t) = (1 2 2 t) 1 . 2 n

1 By the central limit theorem, (2Xn n)/ n converges to N( 1 t, 1), which can be represented as Z 2 t 2 for the standard normal random variable Z. Thus, St can be expressed as St = S0 exp t + t(Z 1 t) = S0 exp ( 1 2 )t + tZ . 2 2 Thus log(St ) has the normal distribution and so St has the log-normal distribution.

Stock prices are widely believed to be log-normally distributed.Many steps. Risk-neutral world. In the risk-neutral world, the probability of up-movement is 1 + 1 2 r S0 ert Sdown 2 1 t . Sup Sdown 2 1 Then Xn Bi(n, q), and (2Xn n)/ n has mean t( + 2 2 r)/ and the variance 1, and so converges to 1 2 N( t( + 2 r)/, 1). Finally, log St N(log S0 + (r 1 2 )t, 2 t) or 2 St = S0 exp{ tZ + (r 1 2 )t} , 2 q= where Z N(0, 1) under the risk-neutral probability measure Q. 28

FS 2011

Stoch Modelle FV

5.2. Stock price process Assume that the volatility vanishes, i.e. = 0. In this case dS = Sdt , where is the expected return on the stock. Then dS = dt S and St = S0 et .

The randomness of stock prices is modelled using the Brownian motion (also called Wiener process). The standard Brownian motion Wt is a stochastic process (family of random variables), such that W0 = 0; Wt Ws is normally distributed with mean zero and the variance t s for t s; Wt has independent increments, i.e. Wtn Wtn1 , . . . , Wt2 Wt1 are jointly independent for any time moments t1 t2 tn . The Brownian motion has continuous but nowhere dierentiable paths. Let Wt be the standard Brownian motion. Then dS = Sdt + SdW or with time as subscript dSt = St dt + St dWt , is a classical way to model the price process of an underlying instrument. 5.3. Stochastic dierential equations In a more general case Xt is a general stochastic process (not necessarily stock price process) such that dXt = t dt + t dWt . The drift t and the volatility t may be random (note that the term volatility is sometimes also used in t 2 a slightly dierent way), but they must be suitably regular ( 0 (s + |s |)ds < a.s. for all t) and adapted to the same ltration, so depend on the the events up to the current time (i.e. Ft ), but not on the future. Given X0 the drift and volatility determine uniquely the underlying process and can be determined uniquely from Xt . Stochastic dierential equation for Xt dXt = (Xt , t)dt + (Xt , t)dWt . A stochastic dierential equation need not have a solution, and if it does it might not be unique. Example: A stock pays dividends at 15% p.a. with continuous compounding and has a volatility of 30% p.a. Then dS = 0.15Sdt + 0.30SdW . In other words, where Z N(0, 1). 29 S = 0.15t + 0.30Z t S

FS 2011

Stoch Modelle FV

5.4. Its formula o If dXt = t dt + t dWt and f is a deterministic twice continuously dierentiable function, then Yt = f (Xt ) satises 2 dYt = (t f (Xt ) + 1 t f (Xt ))dt + (t f (Xt ))dWt . 2 More generally, let Yt = F (Xt , t) for a twice continuously dierentiable function F . Then dYt = F 1 2F 2 F dXt + dt + 2 dt Xt t 2 Xt t F F 1 2F 2 F = t + + dt + t dWt . 2 Xt t 2 Xt t Xt

This formula transforms a stochastic dierential equation for Xt into a stochastic dierential equation for Yt . Example. X = W , Y = X 2 . Then dYt = d(Wt2 ) = dt + 2Wt dWt . This can be used to ndT 0

Wt dWt , sinceT T T

dYt =0 0

dt +0

2Wt dWt ,

whence

T 2 1 Wt dWt = 1 WT 2 T . 2 0

Exercise. Let dSt = Sdt + SdWt for the (non-dividend paying) stock price. Find the dierential for the forward price Ft = St er(T t) . 5.5. Geometric Brownian motion Consider dSt = St dt + St dWt . Its solution (prove it using Its formula) is o St = S0 exp{Wt + ( 1 2 )t} 2 called the geometric (or exponential) Brownian motion. It can be shown that this solution is unique.

This formula gives the stock price in the real world if the stock follows the Geometric Brownian motion with given and .Note: Wt has the normal distribution with mean zero and the variance t, so that St = S0 e , where has the normal distribution with mean ( 1 2 )t and the variance 2 t. 2

30

FS 2011

Stoch Modelle FV

5.6. Estimating volatility Take a sample of daily returns for i = 1, . . . , n and then the standard deviation of this sample will estimate , where = 1/252 is the length of time interval in years (a year is assumed to have 252 trading days). The choice of n is crucial, more observations do not necessarily mean a better estimate as the volatility may change over time. When dealing with ui it is appropriate to give latter observations more weights, for example, use exponentially decreasing weights. It is possible to use various models from Time Series. ui = log(Si /Si1 )

6. Martingales and BlackScholesA process Mt is called a Q-martingale if Mt is Ft -measurable for all t, E Q |Mt | < for all t;

E Q (Mt |Fs ) = Ms for all s t. Examples: (1) A constant process is a martingale. (2) Q-Brownian motion is a Q-martingale. (3) Mt = exp{Wt 1 2 t} is a martingale. 2 (4) For any random variable X (with E Q |X| < ), the process Nt = E Q (X|Ft ) is a Q-martingale. For pricing options, the central point was to ensure that the discounted price process is a martingale with respect to some measure. The price of derivatives then becomes the discounted expectation of the claim with respect to this martingale measure. In this Section a claim will always be a non-negative, FT -measurable, and square-integrable (under Q) random variable. 6.1. Change of measure If is a constant, and Wt is a P-Brownian motion, then there exists a measure Q such that Wt = Wt + t is a Q-Brownian motion. This change of measure theorem is a particular case of the Cameron-MartinGirsanov theorem from stochastic calculus. The change of measure changes only the drift; the volatility remains the same. Example. Xt = Wt + t, where Wt is a P-Brownian motion. Then, with = /, there exists a measure Q such that Wt = Wt + (/)t is a Q-Brownian motion up to time T , i.e. Xt = Wt .

Idea: take the stock model, use the change of measure to change it into a martingale and then use the martingale representation theorem to create a replicating strategy for each claim.

31

FS 2011

Stoch Modelle FV

6.2. Black-Scholes model Published in 1973, later Scholes and Merton received the Nobel Prize in Economics. Assumptions: Bt = ert , dSt = St dt + St dWt . Short-selling is permitted, no transaction costs or taxes, all securities are perfectly divisible, there are no dividends, there are no arbitrage opportunities, security trading is continuous, the risk-free interest rate is constant and the same for all maturities.1 1 1 Take the discount process Bt and form a discounted stock Zt = Bt St and a discounted claim BT X.

Step 1. Make Zt into a martingale.1 Zt = Bt St = S0 exp{Wt + ( r 1 2 )t} 2 r 2 1 t) 2 t} = S0 exp{(Wt + = S0 exp{ Wt 1 2 t} 2

for a Q-Brownian motion Wt , so that Zt is a Q-martingale. Then St = Bt Zt = ert Zt and so St = S0 exp{ Wt + (r 1 2 )t} 2 determines the stock price process in the risk-neutral world. The corresponding stochastic dierential equation is dSt = rSt dt + St dWt .1 Step 2. Et = E Q (BT X|Ft ) is the discounted claim time t and is also a Q-martingale.

Step 3. By martingale representation theorem, dEt = t dZt . Replicating strategy. hold t units of the stock at time t hold t = Et t Zt units of the bond The value of the corresponding portfolio at time t is Vt = t St + t Bt = Bt Et . Let us check that so dened portfolio is self-nancing, i.e. its value only depends on the change of the asset prices dVt = t dSt + t dBt . We have dVt = Bt dEt + Et dBt = t Bt dZt + Et dBt = t Bt dZt + (t Zt + t )dBt = t (Bt dZt + Zt dBt ) + t dBt = t d(Bt Zt ) + t dBt = t dSt + t dBt . 32

FS 2011

Stoch Modelle FV

Thus, (t , t ) is self-nancing. Note that we have used the following fact: if Bt is zero volatility process, then d(Bt Xt ) = Xt dBt + Bt dXt . Since we also know that VT = X we have that the price of X at time t must be Vt .

All claims X, knowable up to some horizon T , have associated replicating strategies. The arbitrage price of such a claim at time t is given by1 Vt = Bt E Q (BT X|Ft ) = er(T t) E Q (X|Ft )

where Q is a measure that makes the discounted stock a martingale.

6.3. Example: pricing of a call option Consider a call option with the exercise date T and strike price k. Then the claim is X = max(ST k, 0) . Find V0 , the value of the replicating strategy (and thus the option) at time zero as V0 = erT E Q (max(ST k, 0)) . We should nd the marginal distribution of ST under Q ST = S0 exp{ WT + (r 1 2 )T } . 2 Since WT N(0, T ) under Q, where Z N( 1 2 T, 2 T ). Then 2 so that the claim price is V0 = erT1 WT + (r 2 2 )T = Z + rT ,

ST = S0 eZ+rT ,

E Q ((S0 e

Z+rT

k) ) =

+

1 2 2 T

(S0 ex kerT ) exp log(k/S0 )rT

1 (x + 2 2 T )2 2 2 T

dx .

Change of variables v = (x + 1 2 T )/ T leads to 2 1 V0 = 2a

S0 e

T v 1 2 T 2

kerT e 2 v dv ,

1

2

where a = (log(S0 /k) + (r 1 2 )T )/ T . Then writing 2 ( T v 1 2 T 1 v 2 ) = 1 (v + T )2 2 2 2 yields S0 V0 = 2 This leads to Black-Scholes formula V0 = S 0 logS0 k a+ T a

e

1 v2 2

kerT dv 2

e 2 v dv .

1

2

+ (r + 1 2 )T 2 T

kerT

log

S0 k

+ (r 1 2 )T 2 T

.

33

FS 2011

Stoch Modelle FV

We only need that the drift of the stock price is constant, its exact value is immaterial.The Black-Scholes formula may be written as c = S0 (d1 ) kerT (d2 ) . Note that d2 = d1 T . The corresponding price formula for a European put is p = kerT (d2 ) S0 (d1 ) . Implied volatility can be derived from option prices for a particular stock. They can be used to monitor the markets opinion about the volatility of a particular stock. NOTE. A variant of Black-Scholes formula for call price on a general asset with futures price F V0 = erT {F (d1 ) k (d2 )} , where d1 = log(F/k) + 1 2 T 2 . T

This formula has wider applicability, also for indices, dividend paying stocks and currencies.

6.4. Foreign exchange For foreign currency options consider three instruments dollar bond Bt = ert (domestic) sterling bond Dt = eut , where u is the sterling interest rate (foreign) exchange rate Ct = C0 exp{Wt + ( 1 2 )t} 2 Sterling cash bond is not directly tradable, what is tradable is St = Ct Dt . Then we can use the Black-Scholes 1 1 approach, nd Q that makes Zt = Bt St = Bt Ct Dt a martingale. Implementing this: By the change of measure theorem1 and Ct = Bt Dt Zt , whence

Zt = C0 exp{Wt + ( + u r 1 2 )t} . 2 Zt = C0 exp{ Wt 1 2 t} 2 Ct = C0 exp{ Wt + (r u 1 2 )t} , 2

under Q. Then the forward price is F = e(ru)T C0 and the price for a European call is V0 = erT F log(F/k) + 1 2 T 2 T 34 k1 log(F/k) 2 2 T T

.

FS 2011

Stoch Modelle FV

6.5. Dividend paying stock Example (European call option on a dividend paying stock). Ex-dividend dates in two months and ve months. The dividend on each ex-dividend date is expected to be $0.50. The current share price is $40, the volatility is 30% p.a., the risk-free interest rate is 9% p.a. The time of maturity is 6 months. The present rate of the dividends is 0.5e2/120.09 + 0.5e5/120.09 = 0.9741 . The option price can be calculated from the Black-Scholes formula with S0 = 39.0259, k = 40, r = 0.09, = 0.3, and T = 0.5. The result is $3.67. Stocks paying dividends continuously. If the stock is paying dividends at rate q (continuously), then the Black-Scholes formula is applicable with S0 replaced by the dividend-adjusted stock price S0 eqT . This is also applicable for options on stock indices. Alternatively, options on shares paying dividends continuously can be regarded as options on foreign currency with the foreign risk-free interest rate u replaced by the dividends yield q. Then the forward price is F = e(rq)T S0 and the price for for a European call is again V0 = erT F log(F/k) + 1 2 T 2 T k1 log(F/k) 2 2 T T

.

NOTE. The same result is obtained if one adjusts S0 for the dividends and uses the standard Black-Scholes formula on non-dividend paying stock with S0 replaced by S0 eqT .

6.6. Finding the replicating strategy The value of the claim X at time t is equal to V (St , t), e.g. for a European call as in Black-Scholes formula with St (stock price at time t) instead of S0 and (T t) (the remaining time) instead of T . Since dSt = St dWt + rSt dt, Its formula yields o dV (St , t) = V dSt + St2 V 2 V 1 + 2 2 St 2 t St

dt .

On the other hand, the self-nancing condition gives dVt = t dSt + t dBt . By equalling coecients of dSt , we get t = V (St , t) St

meaning that the amount of stock at any stage is the derivative of the option price with respect to the stock price. Compare the values of the replicating strategy V (St , t) = t St + t Bt with option price given by the BlackScholes formula V (St , t) = St log(St /k) + (r + 1 2 )(T t) 2 T t ker(T t) 1 log(St /k) + (r 2 2 )(T t) T t

35

FS 2011

Stoch Modelle FV

to see that the replicating strategy is given by t = and Bt t = ker(T t) log(St /k) + (r + 1 2 )(T t) 2 T t .

1 log(St /k) + (r 2 2 )(T t) T t

.

The value of t for the European call is always between zero and one. The amount of borrowing is bounded by the exercise price k. 6.7. Black-Scholes dierential equation (alternative approach) A short option hedging portfolio starts with some initial capital V0 and invests in the stock and in the money market account so that the portfolio value Vt at each time t [0, T ] agrees with f (t, St ), where f (t, x) is the value of the derivative at time t if St = x. This happens if and only if ert Vt = ert f (t, St ) for all t. In order to ensure this ensure d(ert Vt ) = d(ert f (t, St )) for all t [0, T ) (2.1) and V0 = f (0, S0 ). By integrating ert Vt V0 = ert f (t, St ) f (0, S0 ) If V0 = f (0, S0 ) we get the desired equality. If t is the investment in the share (suitably regular and adapted to the ltration associated with the Brownian motion), while the reminder of the portfolio value, Vt t St , is invested in the money market account, we obtain that dVt is due to t dSt (capital gain on the stock) and r(Vt t St )dt (interest earnings). Hence, dVt = t dSt + r(Vt t St )dt = t (St dt + St dWt ) + r(Vt t St )dt = rVt dt + t ( r)St dt + t St dWt , so that by using this and that ert is a zero volatility process the l.h.s. of (2.1) is d(ert Vt ) = rert Vt dt + ert dVt = rert Vt dt + ert (rVt dt + t ( r)St dt + t St dWt ) = ert (t ( r)St dt + t St dWt ) . For the r.h.s. of (2.1) we have (again by using that ert is a zero volatility process) d(ert f (t, St )) = rert f (t, St )dt + ert df (t, St ) = ert ((rf (t, St ) + St2 f f 1 f 2 f (t, St ) + (t, St ) + 2 St 2 (t, St ))dt + St S (t, St )dWt ) . St t 2 St t

for all t [0, T ) .

(2.2)

(2.3)

(2.4)

By comparing (2.3) and (2.4) we see that (2.1) holds if and only if t ( r)St dt + t St dWt = (rf (t, St ) + St2 f f 1 f 2 f (t, St ) + (t, St ) + 2 St 2 (t, St ))dt + St S (t, St )dWt . St t 2 St t

(2.5)

36

FS 2011

Stoch Modelle FV

Hence, by equating the dWt terms we obtain t = f (t, St ) St for all t [0, T ) .

This is called delta-hedging rule. By equating the dt terms we end up with2 f f f 1 2 f (t, St )( r)St = rf (t, St ) + St (t, St ) + (t, St ) + 2 St 2 (t, St ) , St St t 2 St

or equivalently, rf (t, St ) =2 f f 1 2 f (t, St ) + rSt (t, St ) + 2 St 2 (t, St ) t St 2 St

for all t [0, T ) .

(2.6)

In conclusion, we should look for a continuous function f (t, x) that is a solution of the BlackScholesMerton partial dierential equation rf (t, x) = f f 1 2f (t, x) + rx (t, x) + 2 x2 2 (t, x) t x 2 x for all t [0, T ) , x 0 , (2.7)

that satises terminal condition appropriate to the choice of the payo function, e.g. f (T, x) = (x k)+ for a European call. Assume that we have found this function for the European call. If an investor starts with V0 = f (0, S0 ) and uses f f t = St (t, St ) then (2.5) will hold for all t [0, T ). Indeed the dWt terms agree because t = St (t, St ) and the dt terms agree because (2.7) guarantees (2.6). Equality in (2.5) gives us (2.2). By cancelling V0 = f (0, S0 ) and ert we see that Vt = f (t, St ) for all t [0, T ). By t T and using that Vt and f (t, St ) are continuous, we conclude that VT = f (T, ST ) = (ST k)+ . 6.8. The Greek letters of a portfolio is a portfolio dependent on a single asset S. = = Sn

wi i ,i=1

where i = = ; t 2 . = S 2

ci is the Delta of particular options ; S

They satisfy the Black-Scholes dierential equation1 2

2 S 2 + rS + = r .

The following characteristics are also often used: V= = r 37 Vega , rho .

FS 2011

Stoch Modelle FV

6.9. American options The buyer of an American option has the choice when to stop and this choice can only use price information up to the present moment. Such a random time is called a stopping time. Then the payo for a call option is (S k)+ . The cost of hedging that payo will be E Q (er (S k)+ ) . But the writer does not know which time will be used, so he has to prepare for the worst and charge V0 = max E Q (er (S k)+ ) .

Pricing derivatives with optionality If A is a set of possible choices and Xa is the payo under a A, then the option writer should charge V0 = max E Q (erT Xa ) .aA

If the purchaser does not exercise the option optimally, then the issuers hedge will produce a surplus by date T. American calls on non-dividend paying stock should not be exercised early. 6.10. Exotic options It is often possible to represent some complicated derivatives as combinations of call and put options. Example. A ve-year contract pays out 90% times the ratio of the terminal and initial values of FTSE. Or it pays out 130% if otherwise it would be less or 180% if otherwise it would be more. Assume FTSE drift = 7%, FTSE volatility = 15%, FTSE dividend rate q = 4% (the compound dividends payments from 100 stocks used to compose the FTSE), UK interest rate r = 6.5%. The claim X = min(max(1.3, 0.9ST ), 1.8) , where T = 5 and S0 = 1. Rewrite X as X = 1.3 + 0.9((ST 1.44)+ (ST 2)+ ) . Thus, X is the dierence of the two FTSE calls plus some cash. The forward price F = e(rq)T S0 = 1.133. The two calls can be valued at 0.0422 and 0.0067, so that V0 = 1.3erT + 0.9(0.0422 0.0067) = 0.9712 . forward start options (start at-the-money at some time in the future; used in employee incentive schemes) compound options (e.g., a call on a call with two strike prices) chooser options (the holder can choose whether the option is a call or a put at some point during its life) barrier options (the payo depends on whether the assets price reaches a certain level during a certain period of time) binary options (pays nothing if the stock price ends up below the strike price and pays a xed amount if it ends above the strike price) 38

FS 2011

Stoch Modelle FV

lookback options (payo depends on the maximum or minimum stock price during the life of an option) a shout option (a European option where the holder can shout to the writer once; at the end the option holder receives either the usual payo or the intrinsic value at the time of the shout, whichever is greater) Asian options (the payo depends on the average price of the asset during at least some part of the life of an option) basket options (the payo depends on the value of a portfolio of assets), etc.

39

3. Optimal portfolios

If properly hedged, derivatives provide riskless returns. This is used by banks who sell their products for a bit more than it is worth. Fund managers buy and sell assets (and also derivatives) with the aim of beating the banks rate of return. This often involves taking a degree of risk.

1. Mean-variance approachThe mean-variance approach was developed by H. Markowitz (Nobel Prise winner in economics). Let Pi (t) be the price of security i at time t, so that Pi (0) is its initial price. The returns Ri = (Pi (t) Pi (0))/Pi (0) are modelled as random variables with i = E (Ri ) , ij = Cov(Ri , Rj ) .

The variance-covariance matrix of returns is denoted by . If the rst asset is risk-free, then the corresponding variance and covariances are zeros. Let i be the fraction of initial wealth X of the investor invested in security i at time t = 0 i = i Pi (0) , X

where i is the number of shares of security i held by investor at time t = 0. = (1 , . . . , d ) is called the portfolio vector. Note that 1 + 2 + + d = 1 . If short-selling is not allowed, portfolios should have all non-negative components. Such portfolios are called admissible. The total return is given byd

R=i=1

i Ri .

Thend

E(R) = E (R) =i=1 d

i i , i ij j .i,j=1

V (E) = Var(R) =

1.1. Mean-variance principle2 A For a given upper bound max on 2 , choose an admissible portfolio such that () is maximal.

40

FS 2011

Stoch Modelle FV

B For a given lower bound low on for the mean of the portfolio, choose an admissible portfolio with the smallest variance. Mathematical formulations of this principle is possible as a quadratic programming problem.

return

max

risk2 min

2

Figure 3.1: Mean-variance ecient set (shown as a thick line)

1.2. Two assets portfolios Then = (1 , 2 ) with 1 + 2 = 1. For simplicity, denote 1 = x and 2 = 1 x. Then E(R) = x1 + (1 x)2 ,2 2 V (R) = x2 1 + (1 x)2 2 + 2x(1 x)1 2 ,

where is the correlation coecient between the two individual returns. If short sales are forbidden, then 0 x 1, otherwise x can be an arbitrary number. Then V (R) is a quadratic function of E(R), namely2 2 V (R)(1 2 )2 = (E(R) 2 )2 1 + (1 E(R))2 2 + 2(E(R) 2 )(1 E(R))1 2 .

If the short sales are allowed, then the minimum variance is achieved at x =2 1 2 2 1 2 2 + 2 21 2

(derive it!). Note that the corresponding x may be negative or greater than 1. If short sales are forbidden, then the optimal x can be found as either 0 or 1 or x given above (if x (0, 1)). The objective function may be written as f () = AE(R) + V (R) , where A is a risk aversion index. If A = 0, the portfolio with the lowest variance of return will be selected. As A increases, the investor becomes more willing to accept risk in order to achieve a higher expected return, and 41

FS 2011

Stoch Modelle FV

return

risk2 min

2

Figure 3.2: Mean-variance relationship and the ecient frontier for a two-asset portfolio

if A = the portfolio with the highest expected return will be optimal. In application to two asset portfolios, this gives 2 2 f (x) = A(x1 + (1 x)2 ) + x2 1 + (1 x)2 2 + 2x(1 x)1 2 . Then The derivative is zero if x =1 2

df 2 2 = A(1 2 ) + 2x1 2(1 x)2 + 2(1 2x)1 2 . dx2 A(1 2 ) + 2 1 2 . 2 + 2 2 1 1 2 2

If short sales are forbidden, then the optimal value of x is either 0 or 1 or x above (if x (0, 1)).

2. Risk-free assets and the capital market lineAssume the portfolio Rp has two assets, and one is risk-free. The other (risky asset) may be interpreted as a portfolio R of several risky assets with return E(R) and variance V (R). Let x be the share of the fund invested in the rst (risky) asset. Assume that the risk-free asset provides return r. Then the asset of the combined portfolio Rp will be E(Rp ) = xE(R) + (1 x)r , V (Rp ) = x2 V (R) . Then, if (R) = V (R) is the standard deviation of the risky portfolio and (Rp ) = E(Rp ) = r + E(R) r (Rp ) . (R) V (Rp ),

Thus, the set of portfolios comprising a combination of the risk-free asset and a risky portfolio is a straight line. The tangent point M to the set of admissible portfolios represents the market portfolio or the best combination of risky assets. The optimal position on the capital market line corresponds to the degree of risk preferred. If continued beyond M , it represents a borrowing portfolio. 42

If the borrowing rate rB is dierent from the lending rate rL , then two tangent points are to be determined, see Figure 3.4.

FS 2011

M

E (RM )

Attainable portfolios

r

Figure 3.3: Capital market line

M

PB

rB

PL

Attainable portfolios

rL

Figure 3.4: Dierent borrowing and lending rates

43

capital market lineStoch Modelle FV

FS 2011

Stoch Modelle FV

3. Capital Asset Pricing Model (CAPM)Assume that the return of a security is determined entirely by the market index and random factors Rj = j + j RM + j , where RM is the return of the market portfolio and j is a random error term. Note that,2 Cov(Rj , RM ) = E (j RM + j RM + j RM ) E (j + j RM + j )E (RM ) 2 = j (E (RM ) (E (RM ))2 ) = j Var(RM ) .

Therefore, the beta of an asset Rj can be also dened as j =

Cov(Rj ,RM ) Var(RM )

.

The following is a very important representation of the expected returns E (Rj ) = r + j [E (RM ) r] , where r is the risk-free rate; E (Rj ) is the expected return of asset j; E (RM ) is the expected return on the market portfolio; j is the beta of asset j. In order to prove this representation, consider a portfolio M with the asset Aj taken out of it. The convex combinations of Aj and M can be drawn on (, )-plane as a curve that joints the points corresponding to Aj and M . This curve passes through point M such that the tangent to the curve at M coincides with the capital market line. This slope equals (E (RM ) r)/M . The part of this curve that joins M and Aj has the following parametric representation as rt = (1 t)E (RM ) + tE (Rj ) t =2 2 (1 t)2 M + t2 j + 2(1 t)t Cov(Rj , RM ) .

After dierentiation at point t = 0 we nd rt = E (RM ) + E (Rj ) t = M + j M . Since rt E (RM ) r = t M at t = 0,

we immediately obtain that E (Rj ) = r + j [E (RM ) r]. The betas can be estimated from the following linear model: rj,t = j + j rM,t + j,t , where rj,t is the return of asset j in the tth period, rM,t is the return of the market portfolio in the tth period, j is the intercept, j,t is the residual error for period t. Further,2 Var(Rj ) = j Var(RM ) + Var(j )

and, for i = j, Cov(Ri , Rj ) = i j Var(RM ) . The beta of a portfolio can be found as the weighted sum of betas of individual assetsd

=i=1

i i .

44

FS 2011

Stoch Modelle FV

4. Hedging the value of a portfolio describes relationship between the expected return of a portfolio and market performance. The correct number of contracts to hedge the value of a portfolio is P A where P is the value of a portfolio and A is the value of assets underlying one futures contract (on stock indices). Example. A company hedges a portfolio worth $2,100,000 over the next three months using S&P 500 index futures with 4 months to maturity. The current level of S&P is 900 and = 1.5. The value of assets underlying one futures contract is 900x250=$225,000. The number of contracts to short 1.5 2, 100, 000 = 14 . 225, 000

Suppose the risk-free rate is r=4% per year (so 1% per three months), while the market provides return of -7% in the course of the next three months. Thus, the return on portfolio is 1.58%=12% below the risk-free rate or -11%. Assume that the stocks underlying the index provide a dividend of 2% per annum (0.5% per three months). This means that the index declined by 7.5%, from 900 to 832.5. The initial futures price is 900e(0.040.02)1/3 = 906.02, the nal futures price is 832.5e(0.040.02)1/12 = 833.89. The gain on the futures position is (906.02 833.89) 250 14 = 252, 455 . The total gain/loss on the portfolio is 0.11 2, 100, 000 = 231, 000. The net gain from the hedged position is 21,455 or about 1% of the value of the portfolio (the risk-free rate). Why hedge and not to invest risk-free? Because the hedger feels that the stocks in the portfolio have been chosen well. A hedge removes the risk from market moves and leaves the hedger exposed only to the performance of the portfolio relative to the market.

5. Risk-assessment of a portfolioThe Value-at-Risk (VaR) at level is the maximal loss, which is not exceeded at a given time point with probability . If X is the random variable representing the loss, then V@R (X) = inf{x : P {X > x} 1 } . The value of is typically chosen to be large, e.g. 0.99. Note that if X represents a gain, then one should consider its lower tail. If X is normally distributed with mean zero, then its Value-at-Risk is proportional to the standard deviation, i.e. the volatility. Assume that the loss is normally distributed. Let yr be the volatility per annum. Then the daily volatility (assuming 252 trading days) is day = yr / 252 0.06yr . Here all volatilities are daily. They correspond to the standard deviation of the price change in a day. In the geometric Brownian motion model we have dS = Sdt + SdWt . The rst return term is much small than the volatility contribution and is typically neglected. Thus, the change S in the value of the asset is approximated by SZ t, so that dWt is written as the product of the standard 45

FS 2011

Stoch Modelle FV

normal variable Z and the time interval t. If the daily volatility is used, then the time should be also measured in days. Thus, the Value-at-Risk of the price change is the product of S t and the corresponding quantile of the standard normal distribution. V@R calculation Example. Portfolio $10 million shares of IBM, day = 0.02. We can ignore expected returns of shares as they are smaller than the volatility (say 13% p.a.=0.05% p.day.). The standard deviation of the value of a portfolio over N = 10 days is 10 10 106 =$632,456. As (2.33) = 0.01 (c.d.f. of N(0, 1)), the value at risk 99% of the portfolio is 2.33 632, 456 = $1, 473, 621. For two-asset portfolio X+Y =2 2 X + Y + 2X Y .

This shows that the diversication of normally distributed assets reduces V@R. Linear model. Recall that the change of value for an option satises f = , S where if called the Delta of the option f . Thus, f = S = SZ t . If the portfolio contains various options, then the linear model involves Delta of options:n

=i=1

i Si xi ,

where i is the delta of the portfolio with respect to the ith market variable (the partial derivative of the value with respect to the ith stock price), Si is the value of the ith market variable, and xi = i Zi t is the (random) relative change of value of the ith variable. Note that xi may be dependent. Example. Consider portfolio that consists of options on IBM shares with = 1, 000 at $120 per share and options on AT&T shares with = 20, 000 at $30 per share. Then = 120 1, 000 x1 + 30 20, 000 x2 = 120, 000x1 + 600, 000x2 assuming that the daily volatility of IBM is 2%, and AT&T is 1% and the correlation is 0.7, the st. deviation of (in thousands of USD) (120 0.02)2 + (600 0.01)2 + 2 120 0.02 600 0.01 0.7 7.869 . The 5-day 95% V@R is 1.65 5 7, 869 = $29, 033 .

Quadratic model involves s of options and their cross-gammas ij = 2 /Si Sjn n n

=i=1

Si i xi +i=1 j=1

1 Si Sj ij xi xj . 2

In case of options on a single-stock we obtain 1 = Sx + S 2 (x)2 . 2 46

FS 2011

Stoch Modelle FV

6. Risk measuresIt should be noted that the diversication reduces the Value-at-Risk not for all underlying distributions of the loss. Example. Consider 100 independent bonds, which all have the same default probability q = 0.02 and the current price 100. In case of no default until maturity, each of these bonds will pay back 105 and nothing otherwise. The loss of bond i is thus Li = 100 5 with probability 0.02 with probability 0.98

Two portfolios, each with an initial value 10 000 are compared. Portfolio A is fully concentrated in one single bond. Portfolio B is diversied and invests the same amount in each of the 100 bonds. The Value-at-Risk at level = 0.95 for A is given by V@R(LA ) = V@R(100L1 ) = 100V@R(L1 ) = 500, meaning that at level 0.95 we do not see any loss, but only a gain from A. In order to calculate the loss on B, let Yi be one if bond i defaults and zero otherwise. Then Li = 100Yi 5(1 Yi ) = 105Yi 5 and the loss on B is given by100 100

LB =i=1

Li = 105i=1

Yi 500 .

Thus, V@R(LB ) = 105V@R(S) 500 , where S =100 i=1

Yi has the binomial distribution Bi(100, 0.02). Thus, V@R(S) = 5, so that V@R(LB ) = 525 500 = 25 .