Sticky Wages and Prices: Aggregate Expenditure and...

71

5 Topic Sticky Wages and Prices: Aggregate Expenditure and the Multiplier

Transcript of Sticky Wages and Prices: Aggregate Expenditure and...

5TopicSticky Wages and Prices:

Aggregate Expenditure and the

Multiplier

Questioning the Classical Position and

the Self-Regulating Economy

John Maynard Keynes, an English economist, changed how

many economists viewed the economy.

Keynes’s major work, The General Theory of employment,

Interest and Money, was published in 1936.

Just prior to its publication, the Great Depression had plagued

many countries of the world.

Unemployment was sky-high in many countries, and many

economies had been contracting.

Questioning the Classical Position and

the Self-Regulating Economy

Where was Say’s law, with its promise that there would be no

general gluts?

When was the self-regulating economy going to heal itself of

its depression illness?

Where was full employment?

And, given the depressed state of the economy, could anyone

any longer believe that laissez-faire was the right policy?

With the Great Depression as recent history, Keynes and the

Keynesians thought that although their theory might not be right in

every detail, they certainly had enough evidence to say that the

classical view of the economy was wrong.

Keynes challenged all four of the following classical position beliefs:

(1) Say’s law holds, so that insufficient demand in the economy is

unlikely.

(2) Wages, prices, and interest rates are flexible.

(3) The economy is self-regulating.

(4) Laissez-faire is the right and sensible economic policy.

Questioning the Classical Position and

the Self-Regulating Economy

Keynes’s Criticism of Say’s Law in a

Money Economy

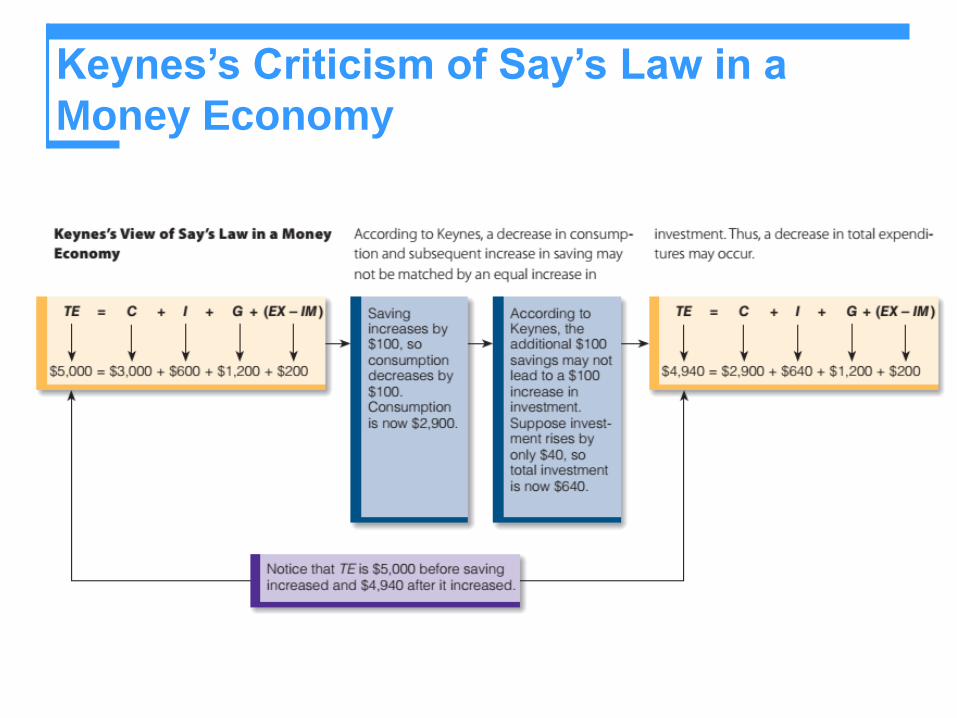

According to classical economists and Say’s law, if consumption

spending falls because saving increases, the added saving will put

downward pressure on the interest rate, and at a lower interest rate

businesses will borrow and invest more. As a result, total spending will

not fall.

Keynes disagreed. He didn’t think that added saving would necessarily

stimulate an equal amount of added investment spending.

According to Keynesian view, the fall in interest rate would increase

investment but not by enough to prevent a decline in aggregate

spending.

And if, at a given price level, total spending falls, so will aggregate

demand. In other words, according to Keynes, aggregate demand

could fall if saving increases.

Keynes’s Criticism of Say’s Law in a

Money Economy

Keynes’s Criticism of Say’s Law in a

Money Economy

The classical economists believed that saving and investment

depend on the interest rate.

Keynes believed that both saving and investment depend on a

number of factors that may be far more influential than the interest

rate.

Saving is more responsive to changes in income than to

changes in the interest rate.

Investment is more responsive to technological changes,

business expectations, and innovations than to changes in the

interest rate.

Keynes’s Criticism of Say’s Law in a

Money Economy

Consider the difference between Keynes and the classical

economists on saving.

The classical economists held that saving is directly related to the

interest rate: As the interest rate goes up, saving rises; as the

interest rate goes down, saving falls, ceteris paribus.

Keynes thought this assumption might not always be true. Suppose

individuals are saving for a certain goal—say, a retirement fund of

$100,000. They might save less per period at an interest rate of 10

percent than at an interest rate of 5 percent because a higher

interest rate means that they can save less per period and still meet

their goal by retirement.

Keynes’s Criticism of Say’s Law in a

Money Economy

As for investment, Keynes believed that the interest rate is

important in determining the level of investment, but not as

important as other variables, such as the expected rate of

profit on investment.

Keynes argued that if business expectations are

pessimistic, then much investment is unlikely, regardless

of how low the interest rate is.

Keynes on Wage Rates

As explained in the last chapter, if the unemployment rate in the

economy is greater than the natural unemployment rate, a surplus

exists in the labor market. Consequently, according to classical

economists, wage rates will fall.

According to Keynesian economists, wage rates may be inflexible in a

downward direction.

Employees will naturally resist an employer’s efforts to cut

wages.

Labor unions may resist wage cuts.

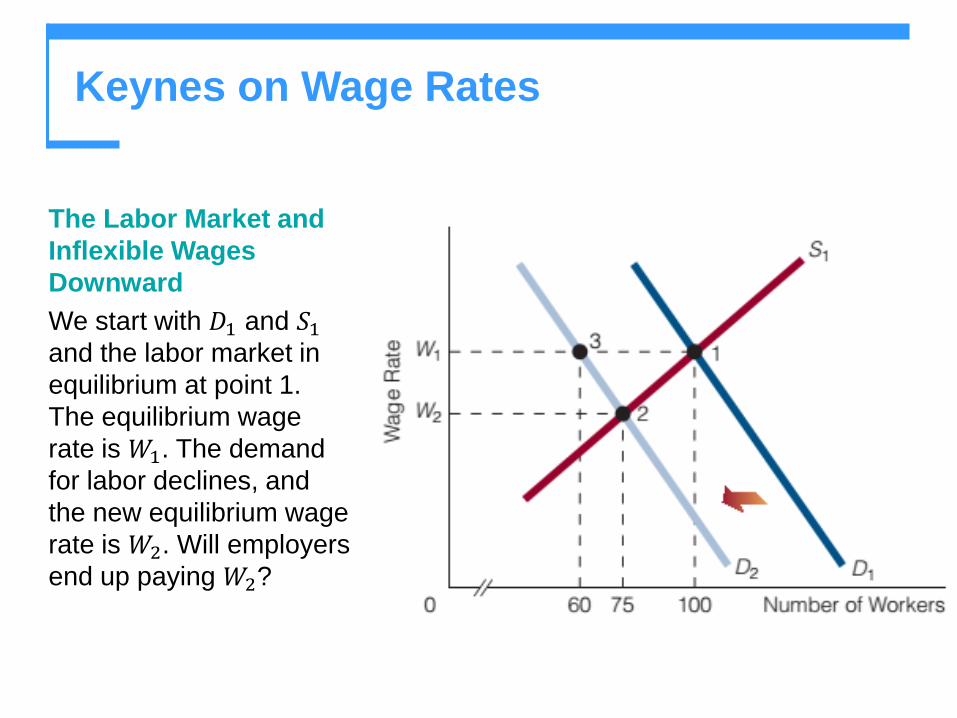

The Labor Market and

Inflexible Wages

Downward

We start with 𝐷1 and 𝑆1and the labor market in

equilibrium at point 1.

The equilibrium wage

rate is 𝑊1. The demand

for labor declines, and

the new equilibrium wage

rate is 𝑊2. Will employers

end up paying 𝑊2?

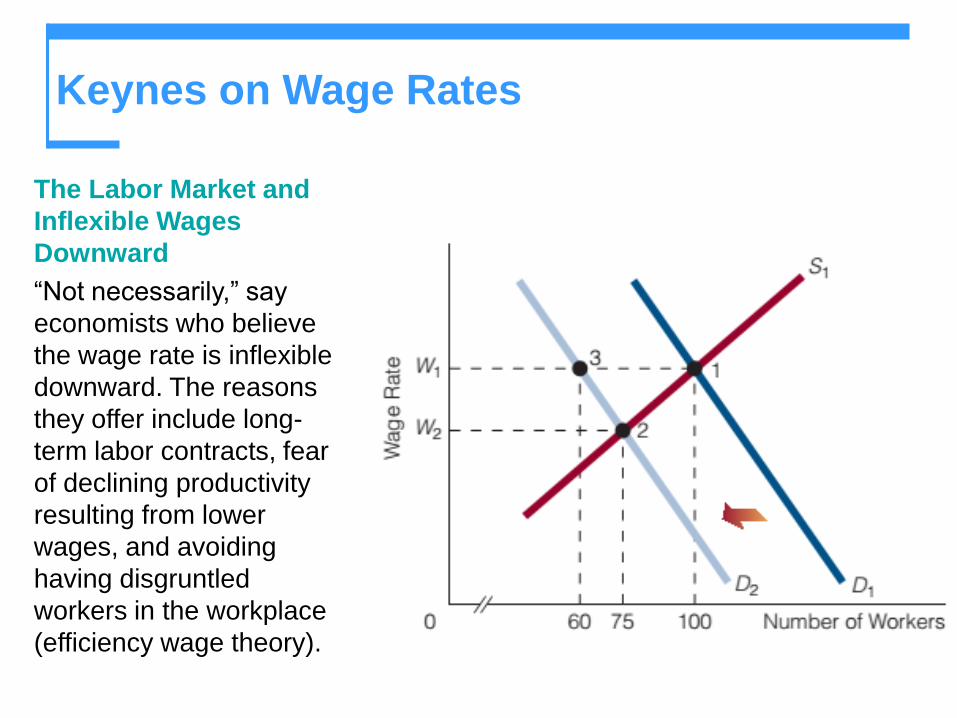

Keynes on Wage Rates

The Labor Market and

Inflexible Wages

Downward

“Not necessarily,” say

economists who believe

the wage rate is inflexible

downward. The reasons

they offer include long-

term labor contracts, fear

of declining productivity

resulting from lower

wages, and avoiding

having disgruntled

workers in the workplace

(efficiency wage theory).

Keynes on Wage Rates

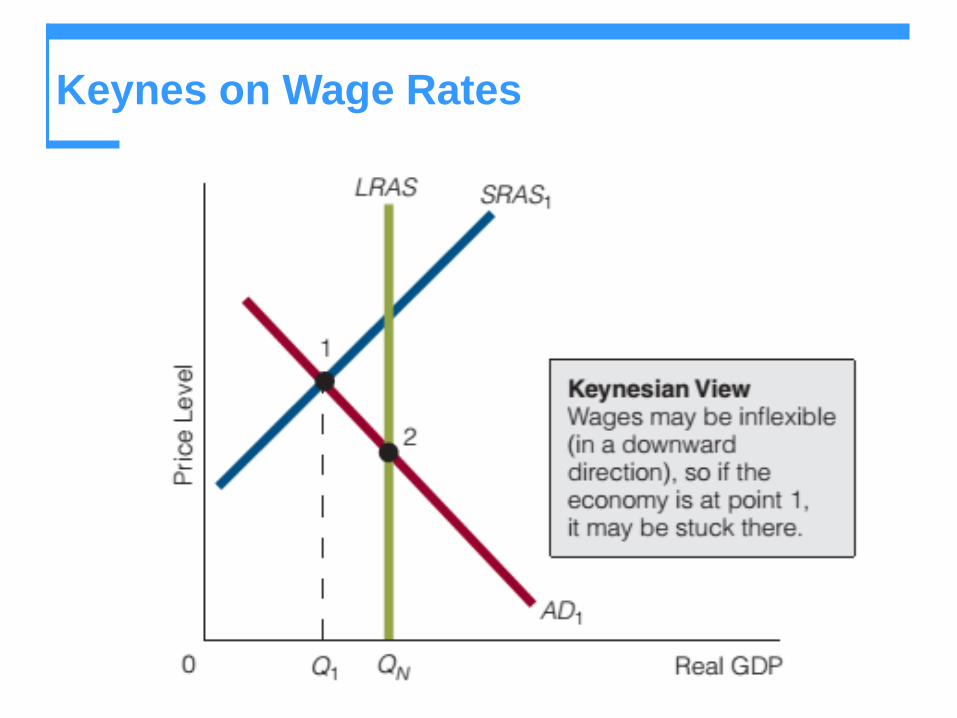

Keynes on Wage Rates

If Keynes is correct and wage rates will not fall, is the

economy then unable to get itself out of a recessionary gap?

The unequivocal answer is yes.

If employee and labor union resistance prevents wage rates

from falling, then the SRAS curve will not shift to the right. If it

does not shift to the right, the price level won’t come down. If

the price level does not come down, buyers will not purchase

more goods and services and move the economy out of a

recessionary gap.

Keynes believed that the economy is inherently unstable and

that it may not automatically cure itself of a recessionary gap.

It may not be self-regulating.

Keynes on Wage Rates

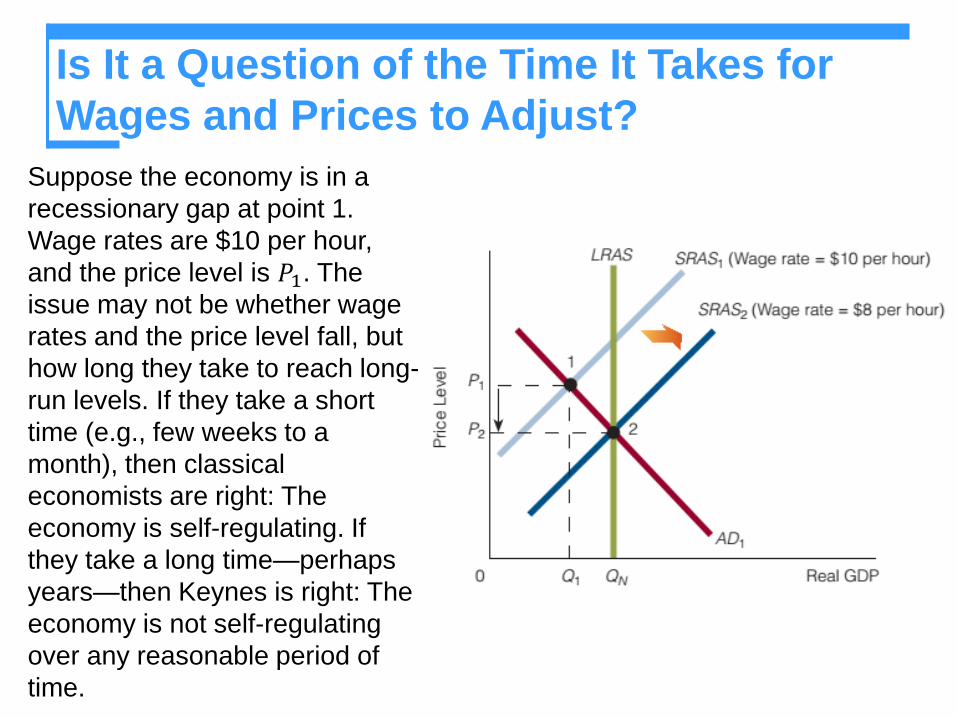

Is It a Question of the Time It Takes for

Wages and Prices to Adjust?

Suppose the economy is in a

recessionary gap at point 1.

Wage rates are $10 per hour,

and the price level is 𝑃1. The

issue may not be whether wage

rates and the price level fall, but

how long they take to reach long-

run levels. If they take a short

time (e.g., few weeks to a

month), then classical

economists are right: The

economy is self-regulating. If

they take a long time—perhaps

years—then Keynes is right: The

economy is not self-regulating

over any reasonable period of

time.

Keynes on Prices

Again, recall what classical economists believe occurs when a

recessionary gap exists: Wage rates fall, the SRAS curve shifts to the

right, and the price level begins to decrease—stop right there! The

phrase “the price level begins to decrease” tells us that classical

economists believe that prices in the economy are flexible: They move

up and down in response to market forces.

Keynes said that the internal structure of an economy is not always

competitive enough to allow prices to fall. Anticompetitive or

monopolistic elements in the economy sometimes prevent price from

falling.

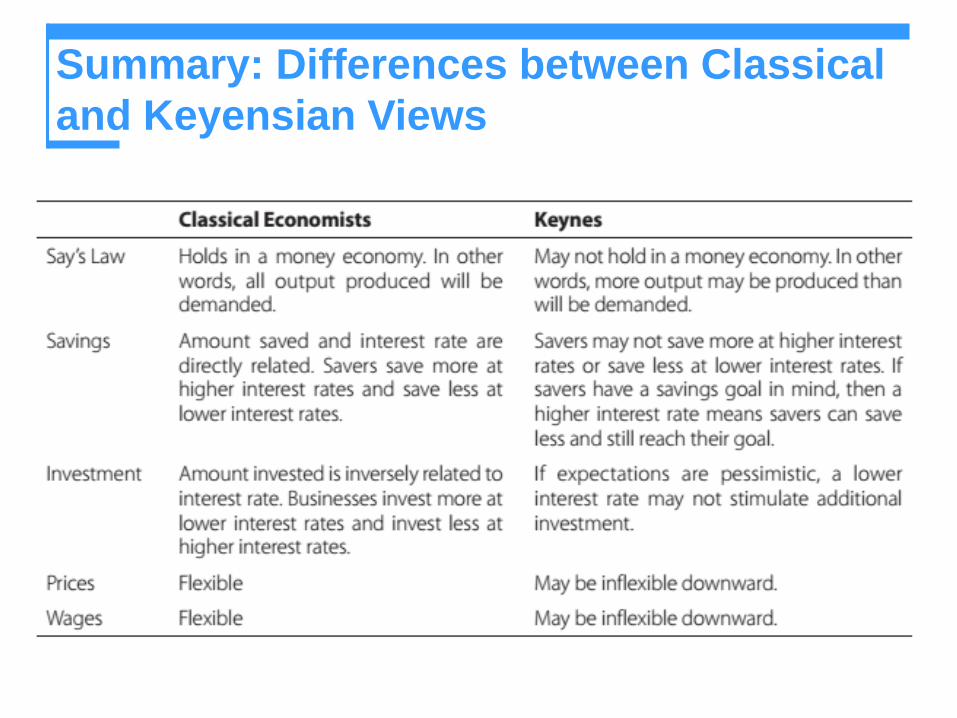

Summary: Differences between Classical

and Keyensian Views

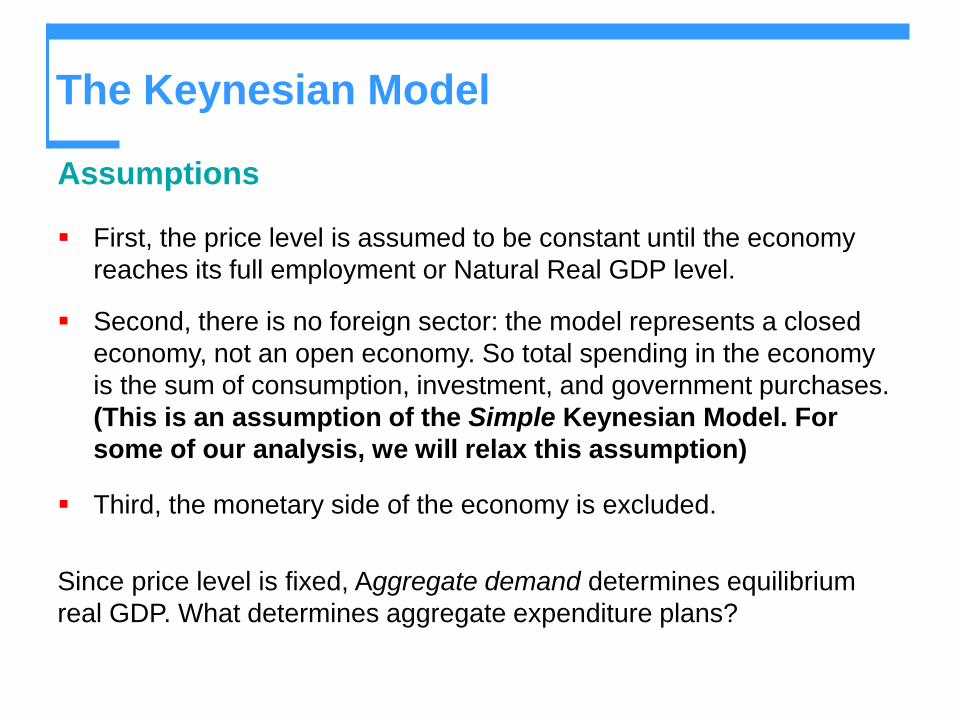

The Keynesian Model

Assumptions

First, the price level is assumed to be constant until the economy

reaches its full employment or Natural Real GDP level.

Second, there is no foreign sector: the model represents a closed

economy, not an open economy. So total spending in the economy

is the sum of consumption, investment, and government purchases.

(This is an assumption of the Simple Keynesian Model. For

some of our analysis, we will relax this assumption)

Third, the monetary side of the economy is excluded.

Since price level is fixed, Aggregate demand determines equilibrium

real GDP. What determines aggregate expenditure plans?

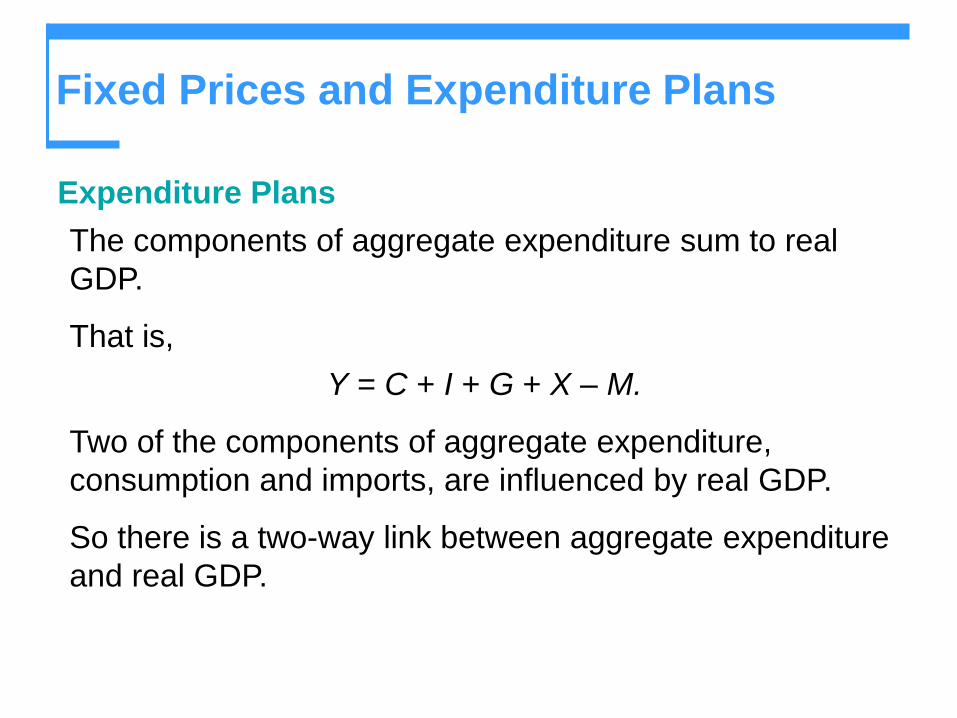

Fixed Prices and Expenditure Plans

Expenditure Plans

The components of aggregate expenditure sum to real

GDP.

That is,

Y = C + I + G + X – M.

Two of the components of aggregate expenditure,

consumption and imports, are influenced by real GDP.

So there is a two-way link between aggregate expenditure

and real GDP.

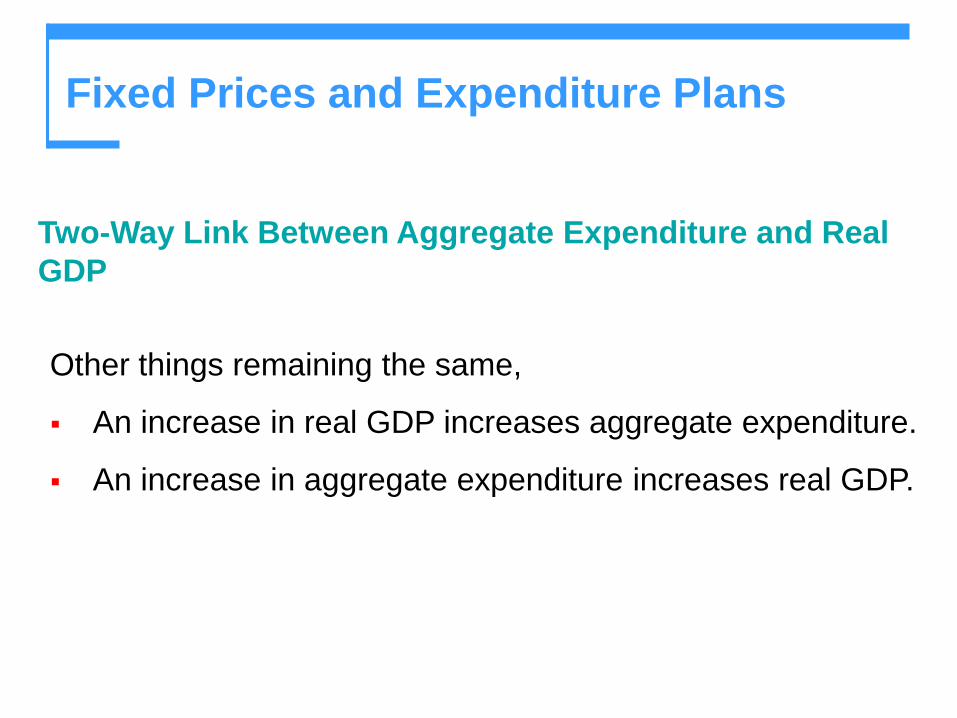

Fixed Prices and Expenditure Plans

Two-Way Link Between Aggregate Expenditure and Real

GDP

Other things remaining the same,

An increase in real GDP increases aggregate expenditure.

An increase in aggregate expenditure increases real GDP.

Fixed Prices and Expenditure Plans

Consumption and Saving Plans

Consumption expenditure is influenced by many factors

but the most direct one is disposable income.

Disposable income is aggregate income or real GDP, Y,

minus net taxes, T.

Call disposable income YD.

The equation for disposable income is

YD = Y – T

Fixed Prices and Expenditure Plans

Disposable income, YD, is either spent on consumption

goods and services, C, or saved, S.

That is,

YD = C + S.

The relationship between consumption expenditure and

disposable income, other things remaining the same, is

the consumption function.

The relationship between saving and disposable income,

other things remaining the same, is the saving function.

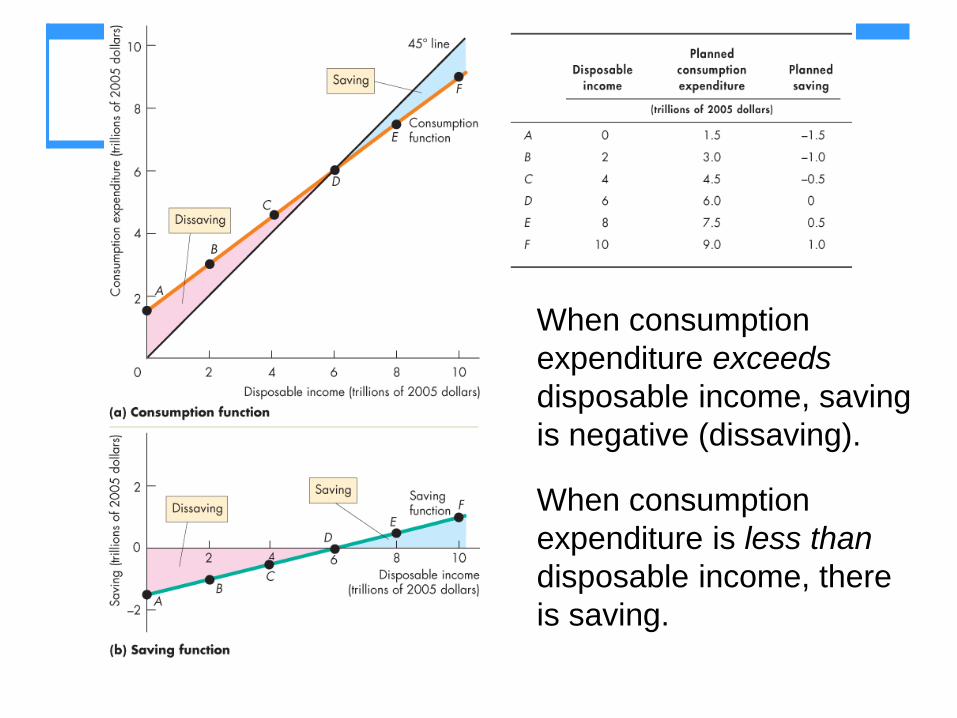

Figure in the next slide illustrates the consumption function

and the saving function.

When consumption

expenditure exceeds

disposable income, saving

is negative (dissaving).

When consumption

expenditure is less than

disposable income, there

is saving.

Fixed Prices and Expenditure Plans

Marginal Propensities to Consume and Save

The marginal propensity to consume (MPC) is the

fraction of a change in disposable income spent on

consumption.

It is calculated as the change in consumption expenditure,

C, divided by the change in disposable income, YD,

that brought it about.

That is, MPC = C

YD

Fixed Prices and Expenditure Plans

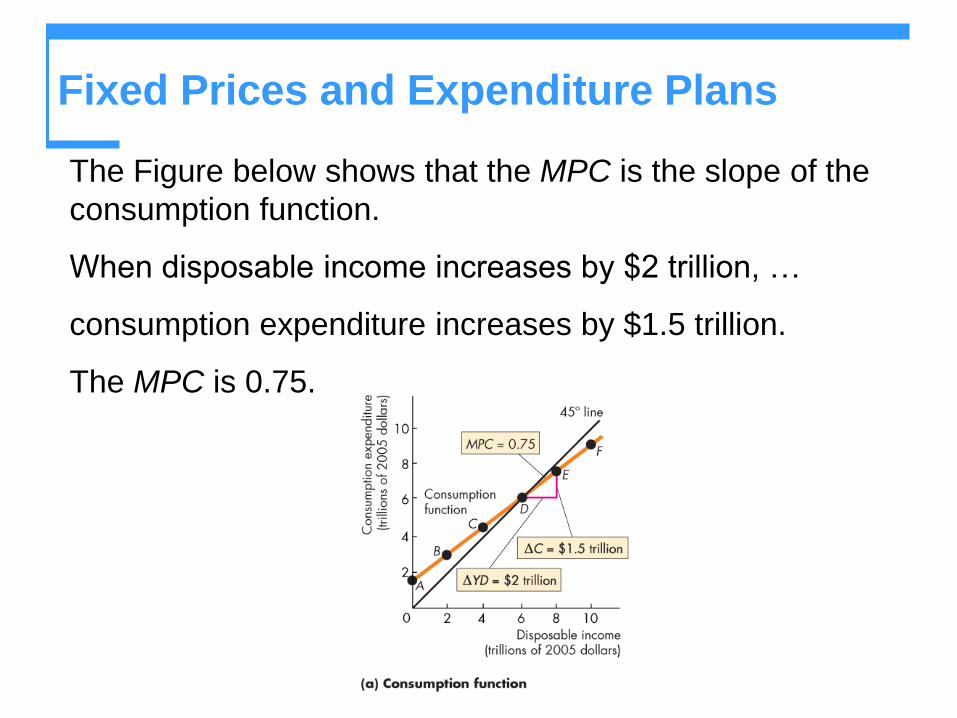

The Figure below shows that the MPC is the slope of the

consumption function.

When disposable income increases by $2 trillion, …

consumption expenditure increases by $1.5 trillion.

The MPC is 0.75.

Fixed Prices and Expenditure Plans

The marginal propensity to save (MPS) is the fraction of a change in disposable income that is saved.

It is calculated as the change in saving, S, divided by the change in disposable income, YD, that brought it about.

That is,

MPS = ∆𝑆

∆𝑌𝐷

Fixed Prices and Expenditure Plans

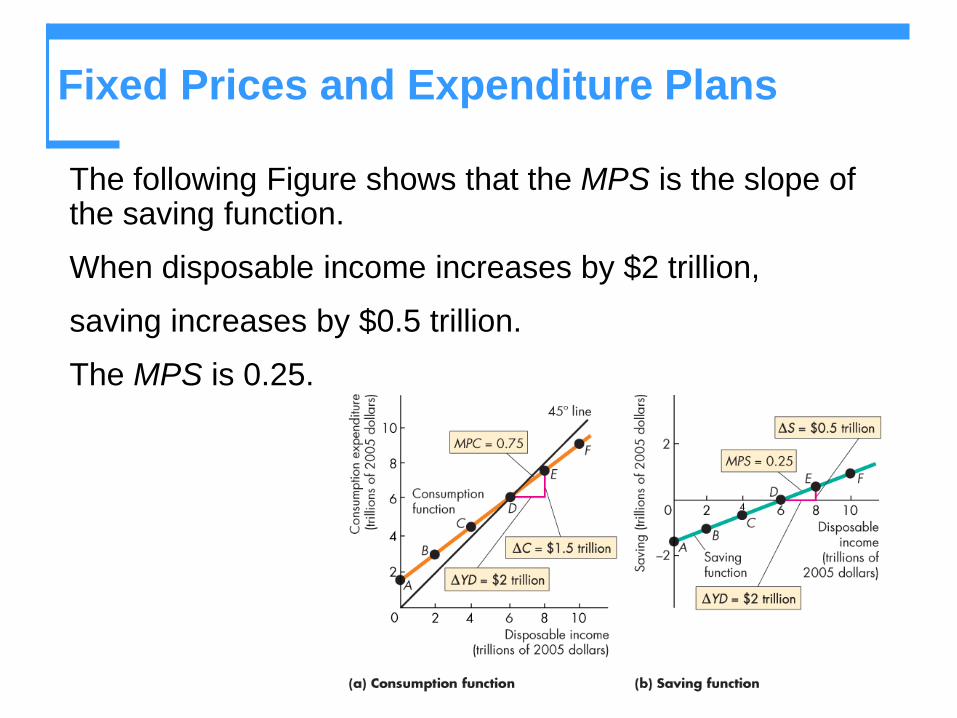

The following Figure shows that the MPS is the slope of the saving function.

When disposable income increases by $2 trillion,

saving increases by $0.5 trillion.

The MPS is 0.25.

Fixed Prices and Expenditure Plans

The MPC plus the MPS equals 1.

To see why, note that,

C + S = YD.

Divide this equation by YD to obtain,

C/YD + S/YD = YD/YD

or

MPC + MPS = 1.

Fixed Prices and Expenditure Plans

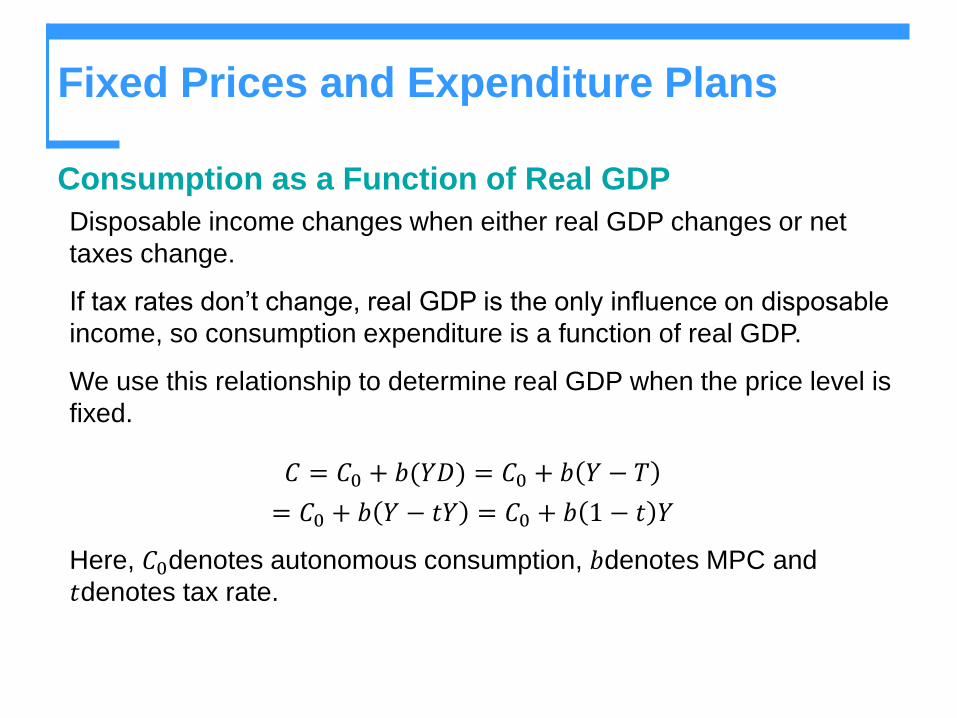

Consumption as a Function of Real GDP

Disposable income changes when either real GDP changes or net

taxes change.

If tax rates don’t change, real GDP is the only influence on disposable

income, so consumption expenditure is a function of real GDP.

We use this relationship to determine real GDP when the price level is

fixed.

𝐶 = 𝐶0 + 𝑏(𝑌𝐷) = 𝐶0 + 𝑏 𝑌 − 𝑇

= 𝐶0 + 𝑏 𝑌 − 𝑡𝑌 = 𝐶0 + 𝑏 1 − 𝑡 𝑌

Here, 𝐶0denotes autonomous consumption, 𝑏denotes MPC and

𝑡denotes tax rate.

Fixed Prices and Expenditure Plans

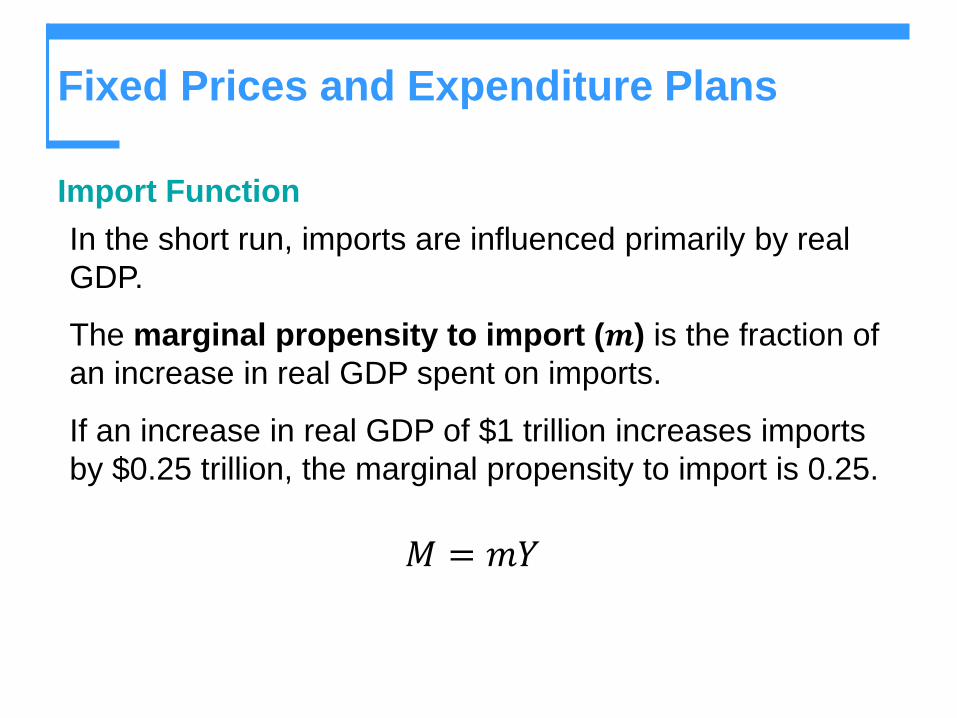

Import Function

In the short run, imports are influenced primarily by real

GDP.

The marginal propensity to import (𝒎) is the fraction of

an increase in real GDP spent on imports.

If an increase in real GDP of $1 trillion increases imports

by $0.25 trillion, the marginal propensity to import is 0.25.

𝑀 = 𝑚𝑌

Real GDP with a Fixed Price Level

Consumption expenditure minus imports, which varies with

real GDP, is induced expenditure.

The sum of investment, government expenditure, and

exports, which does not vary with GDP, is autonomous

expenditure.

Consumption as explained before also has an autonomous

component.

Real GDP with a Fixed Price Level

Aggregate Planned Expenditure

The relationship between aggregate planned expenditure

and real GDP can be described by an aggregate

expenditure schedule, which lists the level of aggregate

expenditure planned at each level of real GDP.

The relationship can also be described by an aggregate

expenditure curve, which is a graph of the aggregate

expenditure schedule.

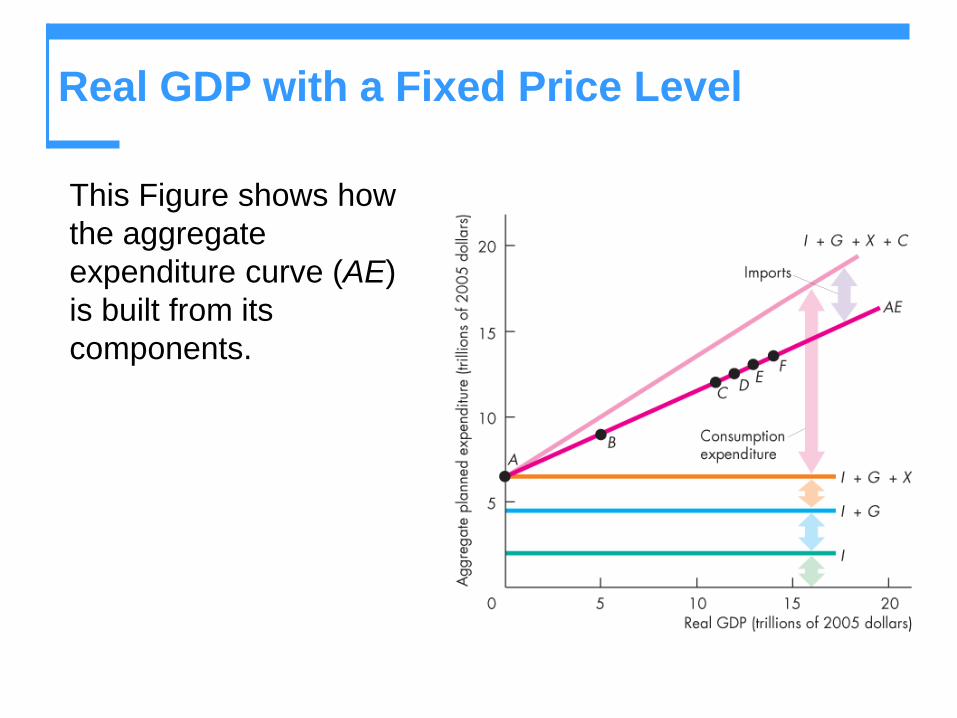

Real GDP with a Fixed Price Level

This Figure shows how

the aggregate

expenditure curve (AE)

is built from its

components.

Real GDP with a Fixed Price Level

Businesses produce the goods and services that are bought by household,

business, government and the rest of the world (ROW). Sometimes, though,

businesses produce too much or too little in comparison to what these

sectors buy.

For example, Assume that business firms hold an optimum inventory level of

$300 billion worth of goods and they produce $11 trillion worth of goods and

services (GDP = $11 trillion), but the four sectors buy only $10.8 trillion

worth (Planned expenditure = $10.8 trillion). In this case, businesses have

produced too much relative to what the four sectors buy and inventory levels

rise unexpectedly to $500 billion, which is $200 billion more than the $300

billion that firms see as optimal.

This unexpected rise in inventories signals to firms that they have

overproduced. Consequently, they cut back on the quantity of goods they

are producing. The cutback in production causes Real GDP to fall, bringing

Real GDP closer to the (lower) output level that the three sectors of the

economy and the ROW are willing and able to buy. Ultimately, GDP will

equal Aggregate Planned Expenditure.

Real GDP with a Fixed Price Level

Assume that business firms hold their optimum inventory level ($300

billion worth of goods), that they produce $10.4 trillion worth of goods

(GDP = $10.4 trillion), and that the four sectors buy $10.6 trillion worth of

goods (Planned expenditure = $10.6 trillion).

How can individuals buy more than businesses produce? Firms make up

the difference out of inventory. In our example, inventory levels fall from

$300 billion to $100 billion because individuals purchase $200 billion

more of goods than firms produced (to be sold). This is why firms

maintain inventories in the first place: to be able to meet an unexpected

increase in sales. The unexpected fall in inventories signals to firms that

they have underproduced.

Consequently, they increase the quantity of goods they produce. The rise

in production causes Real GDP to rise, in the process bringing Real GDP

closer to the (higher) real output that the four sectors are willing and able

to buy. Ultimately, GDP will equal Aggregate Planned Expenditure.

Real GDP with a Fixed Price Level

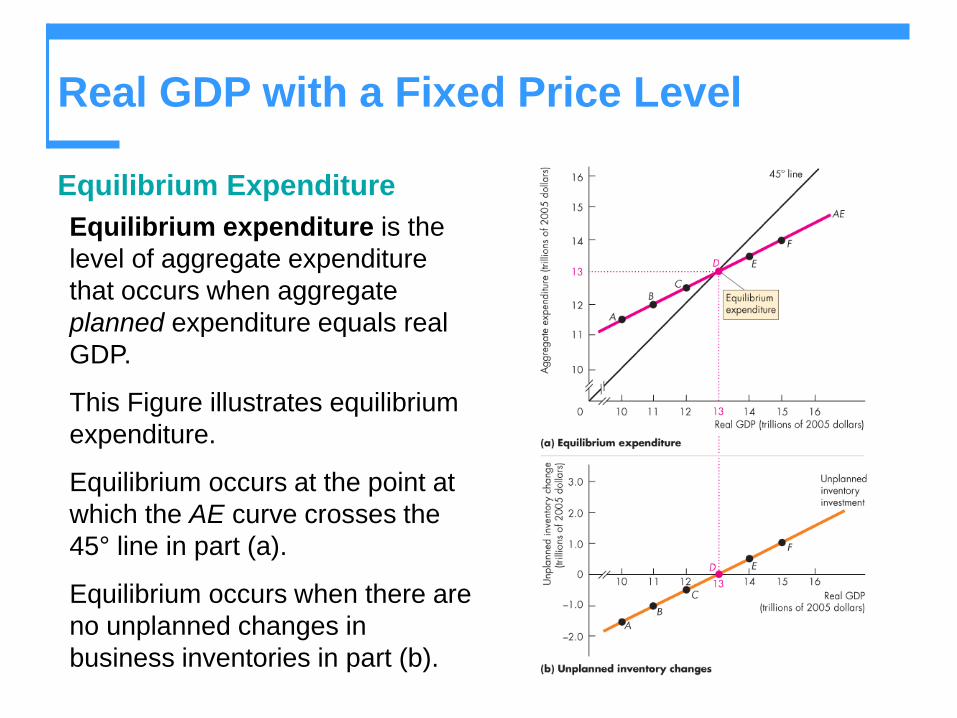

Equilibrium Expenditure

Equilibrium expenditure is the

level of aggregate expenditure

that occurs when aggregate

planned expenditure equals real

GDP.

This Figure illustrates equilibrium

expenditure.

Equilibrium occurs at the point at

which the AE curve crosses the

45° line in part (a).

Equilibrium occurs when there are

no unplanned changes in

business inventories in part (b).

Real GDP with a Fixed Price Level

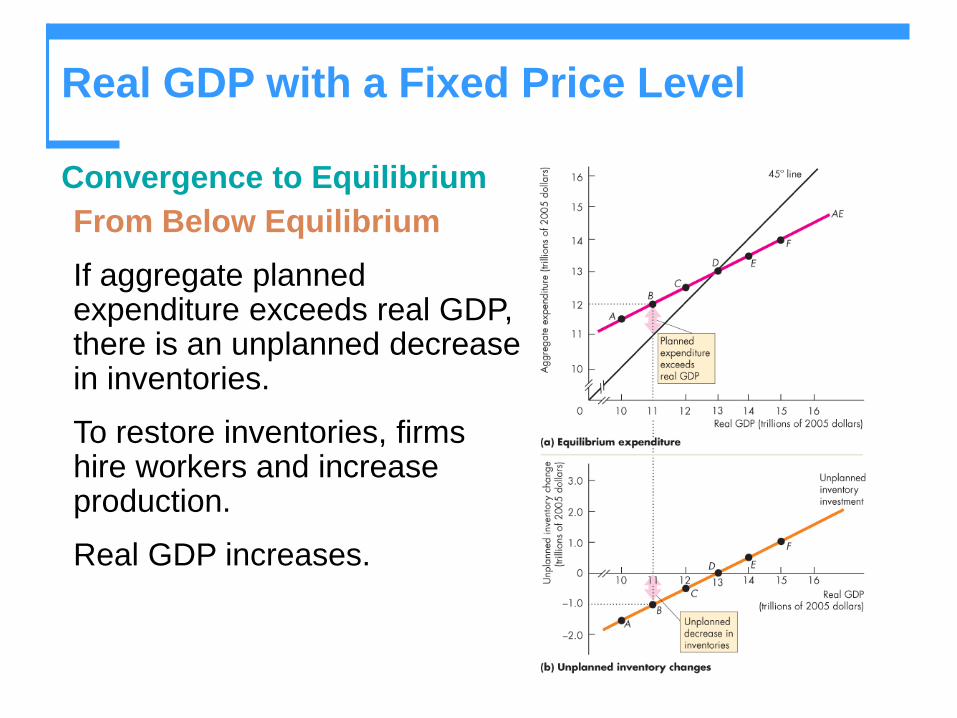

Convergence to Equilibrium

From Below Equilibrium

If aggregate planned expenditure exceeds real GDP, there is an unplanned decrease in inventories.

To restore inventories, firms hire workers and increase production.

Real GDP increases.

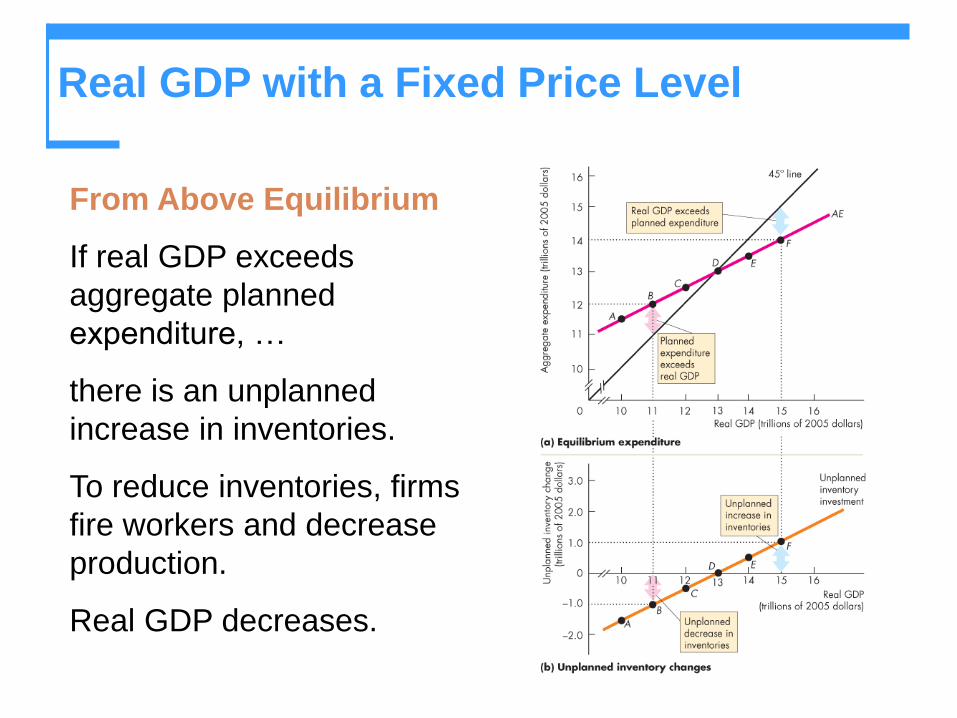

Real GDP with a Fixed Price Level

From Above Equilibrium

If real GDP exceeds

aggregate planned

expenditure, …

there is an unplanned

increase in inventories.

To reduce inventories, firms

fire workers and decrease

production.

Real GDP decreases.

Real GDP with a Fixed Price Level

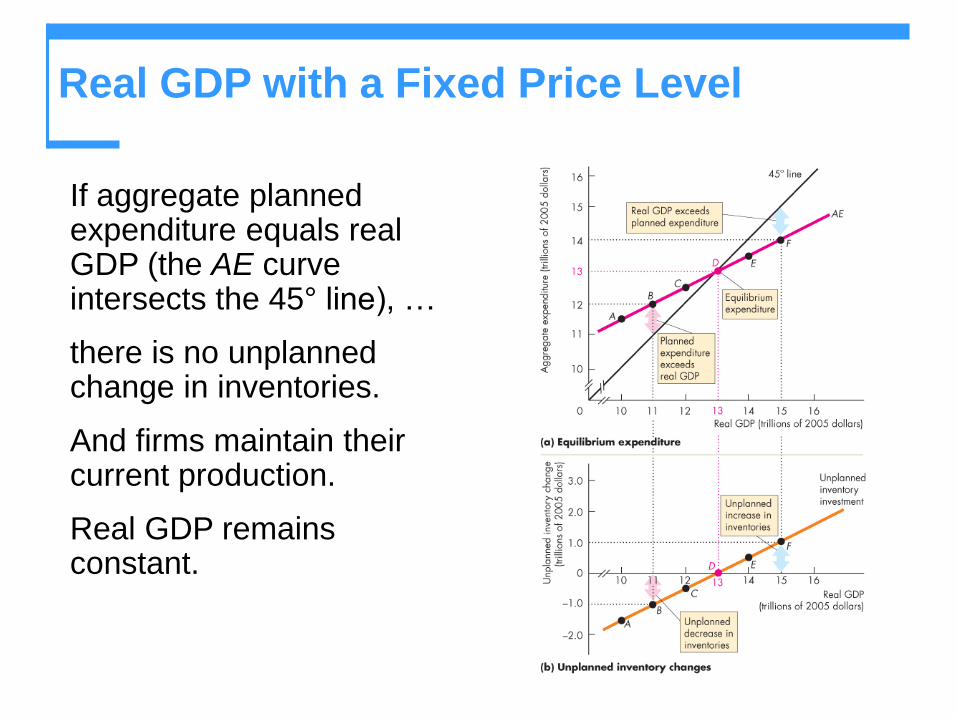

If aggregate planned expenditure equals real GDP (the AE curve intersects the 45° line), …

there is no unplanned change in inventories.

And firms maintain their current production.

Real GDP remains constant.

The Multiplier

When autonomous expenditure changes, so does

equilibrium expenditure and real GDP.

But the change in equilibrium expenditure is larger than

the change in autonomous expenditure.

The multiplier is the amount by which a change in

autonomous expenditure is magnified or multiplied to

determine the change in equilibrium expenditure and real

GDP.

The Multiplier

The Basic Idea of the Multiplier

An increase in investment (or any other component of

autonomous expenditure) increases aggregate

expenditure and real GDP.

The increase in real GDP leads to an increase in induced

expenditure.

The increase in induced expenditure leads to a further

increase in aggregate expenditure and real GDP.

So real GDP increases by more than the initial increase in

autonomous expenditure.

The Multiplier

Why Is the Multiplier Greater than 1?

The multiplier is greater than 1 because an increase in

autonomous expenditure induces further increases in

aggregate expenditure.

The Size of the Multiplier

The size of the multiplier is the change in equilibrium

expenditure divided by the change in autonomous

expenditure.

The Multiplier

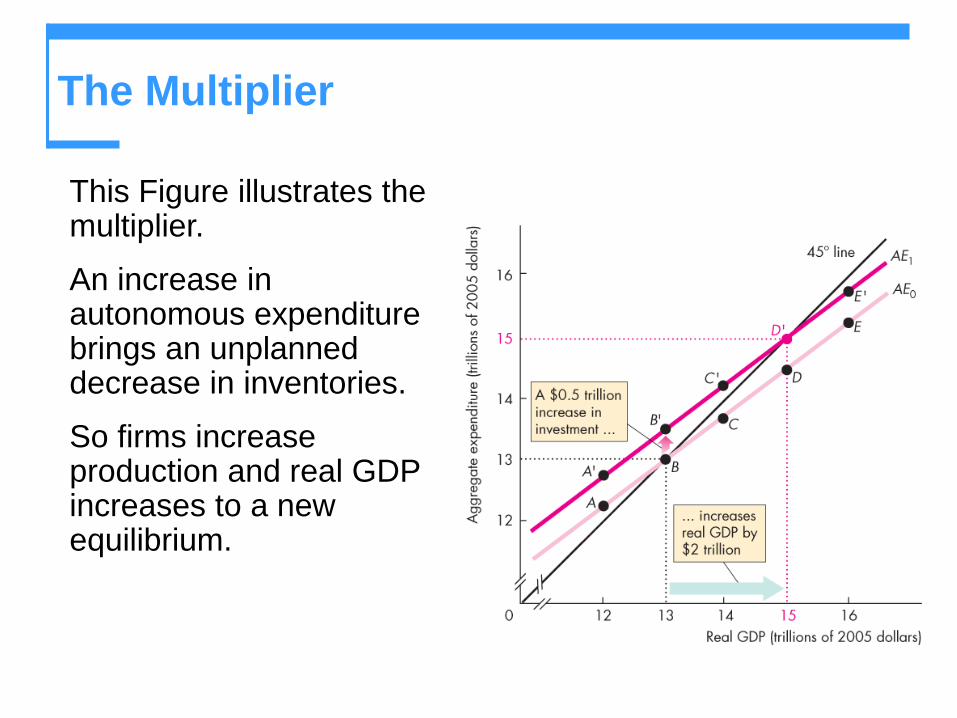

This Figure illustrates the multiplier.

An increase in autonomous expenditure brings an unplanned decrease in inventories.

So firms increase production and real GDP increases to a new equilibrium.

The Multiplier

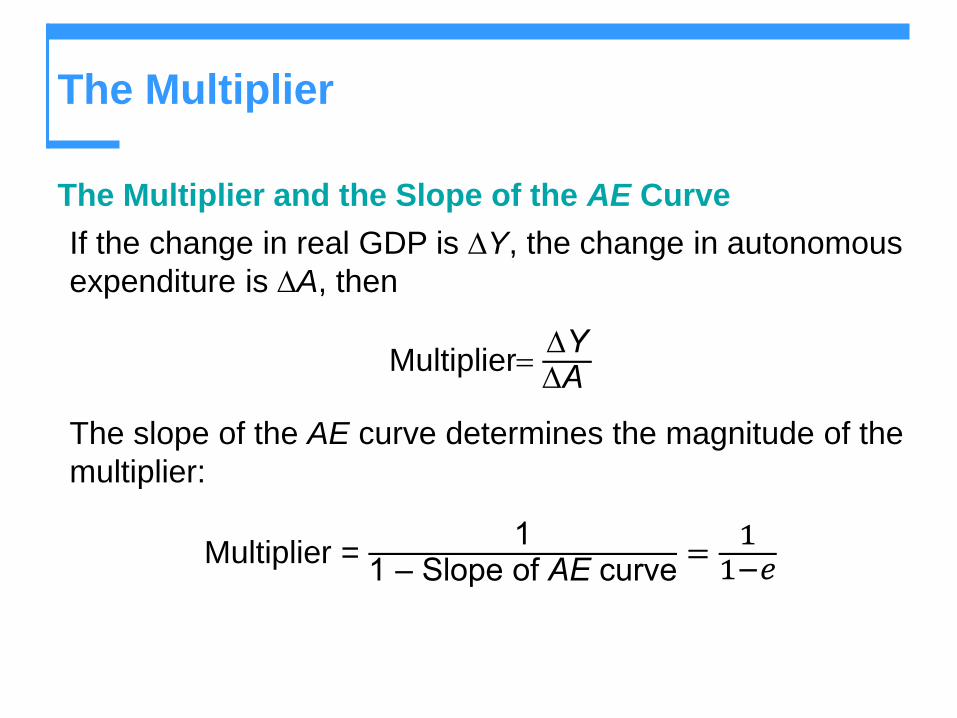

The Multiplier and the Slope of the AE Curve

If the change in real GDP is Y, the change in autonomous

expenditure is A, then

Multiplier= YA

The slope of the AE curve determines the magnitude of the

multiplier:

Multiplier = 1

1 – Slope of AE curve=

11−𝑒

The Multiplier

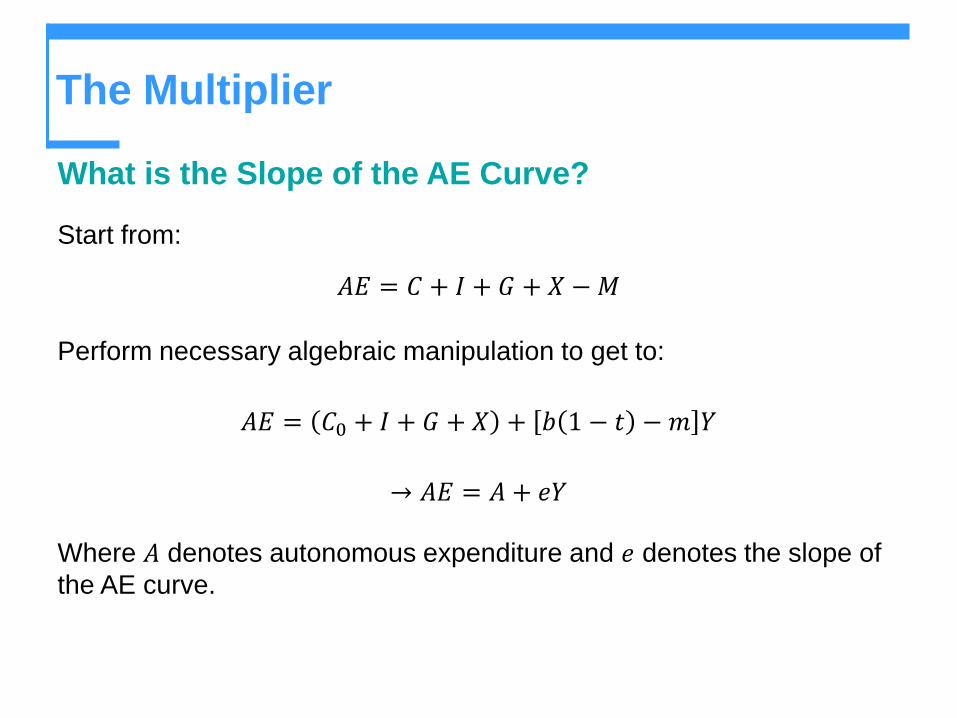

What is the Slope of the AE Curve?

Start from:

𝐴𝐸 = 𝐶 + 𝐼 + 𝐺 + 𝑋 −𝑀

Perform necessary algebraic manipulation to get to:

𝐴𝐸 = 𝐶0 + 𝐼 + 𝐺 + 𝑋 + 𝑏 1 − 𝑡 − 𝑚 𝑌

→ 𝐴𝐸 = 𝐴 + 𝑒𝑌

Where 𝐴 denotes autonomous expenditure and 𝑒 denotes the slope of

the AE curve.

The Multiplier

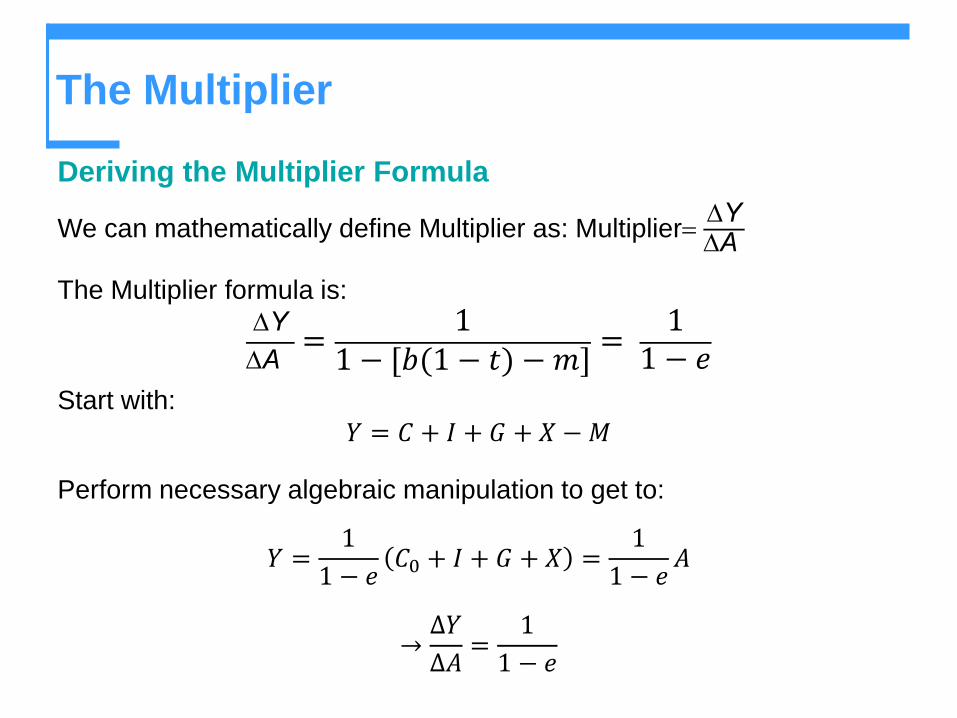

Deriving the Multiplier Formula

We can mathematically define Multiplier as: Multiplier= YA

The Multiplier formula is:

Y

A=

11 − 𝑏 1 − 𝑡 − 𝑚

=1

1 − 𝑒

Start with:

𝑌 = 𝐶 + 𝐼 + 𝐺 + 𝑋 −𝑀

Perform necessary algebraic manipulation to get to:

𝑌 =1

1 − 𝑒𝐶0 + 𝐼 + 𝐺 + 𝑋 =

1

1 − 𝑒𝐴

→∆𝑌

∆𝐴=

1

1 − 𝑒

The Multiplier

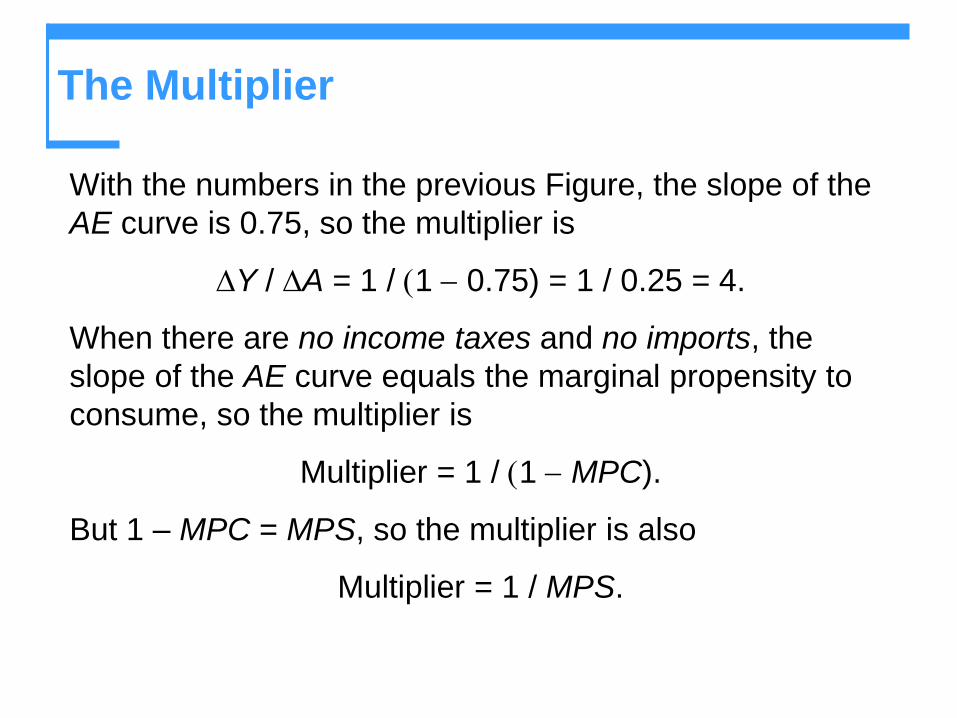

With the numbers in the previous Figure, the slope of the

AE curve is 0.75, so the multiplier is

Y / A = 1 / (1 - 0.75) = 1 / 0.25 = 4.

When there are no income taxes and no imports, the

slope of the AE curve equals the marginal propensity to

consume, so the multiplier is

Multiplier = 1 / (1 - MPC).

But 1 – MPC = MPS, so the multiplier is also

Multiplier = 1 / MPS.

The Multiplier

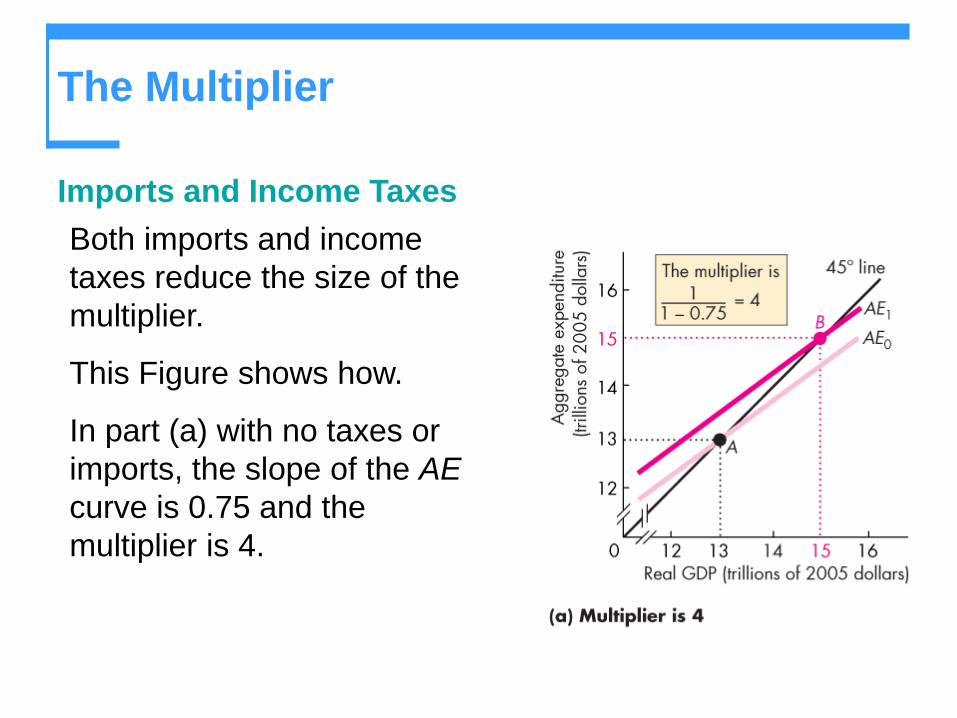

Imports and Income Taxes

Both imports and income

taxes reduce the size of the

multiplier.

This Figure shows how.

In part (a) with no taxes or

imports, the slope of the AE

curve is 0.75 and the

multiplier is 4.

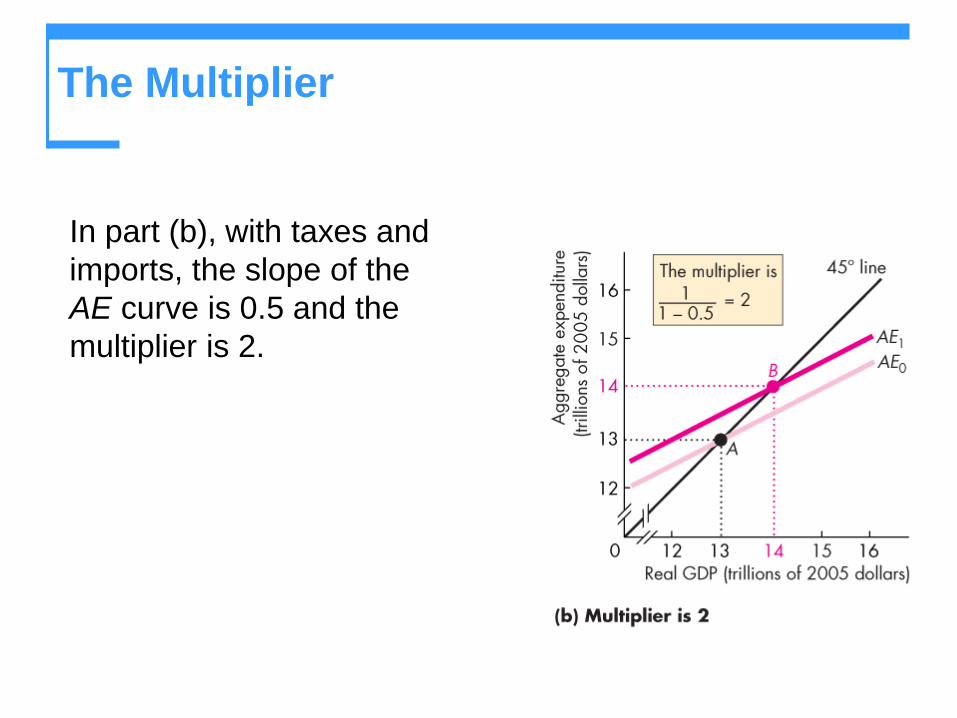

The Multiplier

In part (b), with taxes and

imports, the slope of the

AE curve is 0.5 and the

multiplier is 2.

The Multiplier

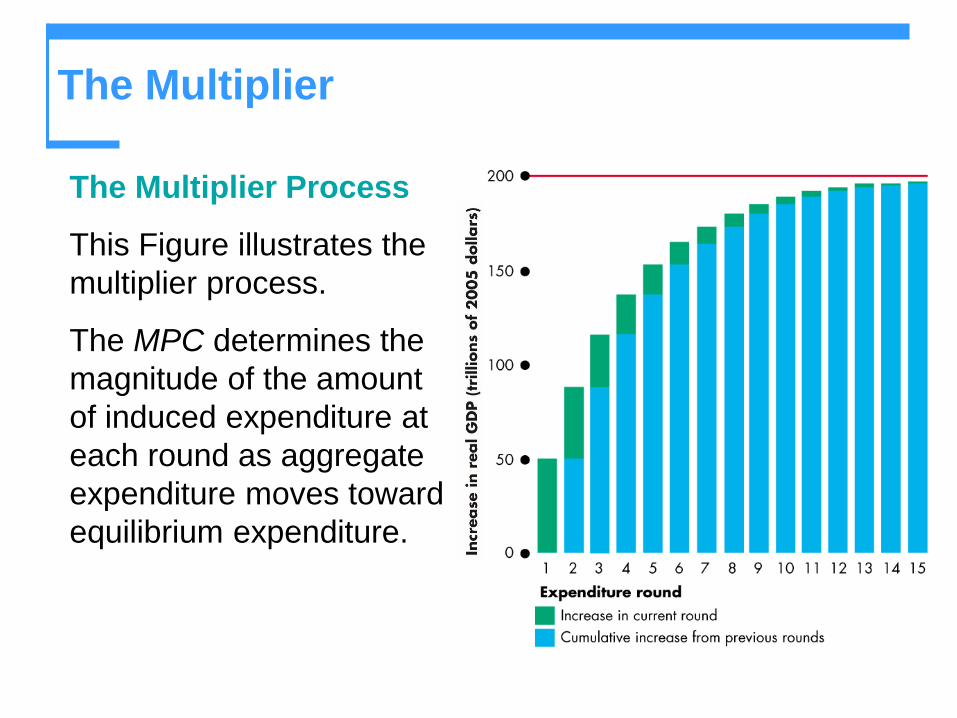

The Multiplier Process

This Figure illustrates the

multiplier process.

The MPC determines the

magnitude of the amount

of induced expenditure at

each round as aggregate

expenditure moves toward

equilibrium expenditure.

The Multiplier and Reality

So, in simple terms, a change in autonomous spending leads

to a greater change in total spending.

Also, in the Keynesian model, the change in total spending is

equal to the change in Real GDP (assuming that the economy

is operating below Natural Real GDP).

The reason is that, in the model, prices are assumed to be

constant until Natural GDP is reached; so any change in

nominal total spending is equal to the change in real total

spending.

However, two reality checks are necessary.

The Multiplier and Reality

First, the multiplier takes time to have an effect. In a textbook, going

from an initial increase in autonomous spending to a multiple

increase in either total spending or Real GDP takes only seconds. In

the real world, this process takes many months.

Second, for the multiplier to increase Real GDP, idle resources must

exist at each spending round. After all, if Real GDP is increasing

(output is increasing) at each spending round, idle resources must

be available to be brought into production. If they are not available,

then increased spending will simply result in higher prices without an

increase in Real GDP. Simply put, GDP will increase, but not Real

GDP.

The Simple Keynesian Model in the AD–

AS Framework

Shifts in the Aggregate Demand Curve

Now, we will assume a closed economy (no export or import) to be

consistent with the Text.

Because there is no foreign sector in the simple Keynesian model,

total spending consists of consumption (C), investment (I), and

government purchases (G). Because the economy has no monetary

side, changes in any of these variables (C, I, G) can shift the AD

curve.

For example, a rise in consumption will shift the AD curve to the

right; a decrease in investment will shift it to the left.

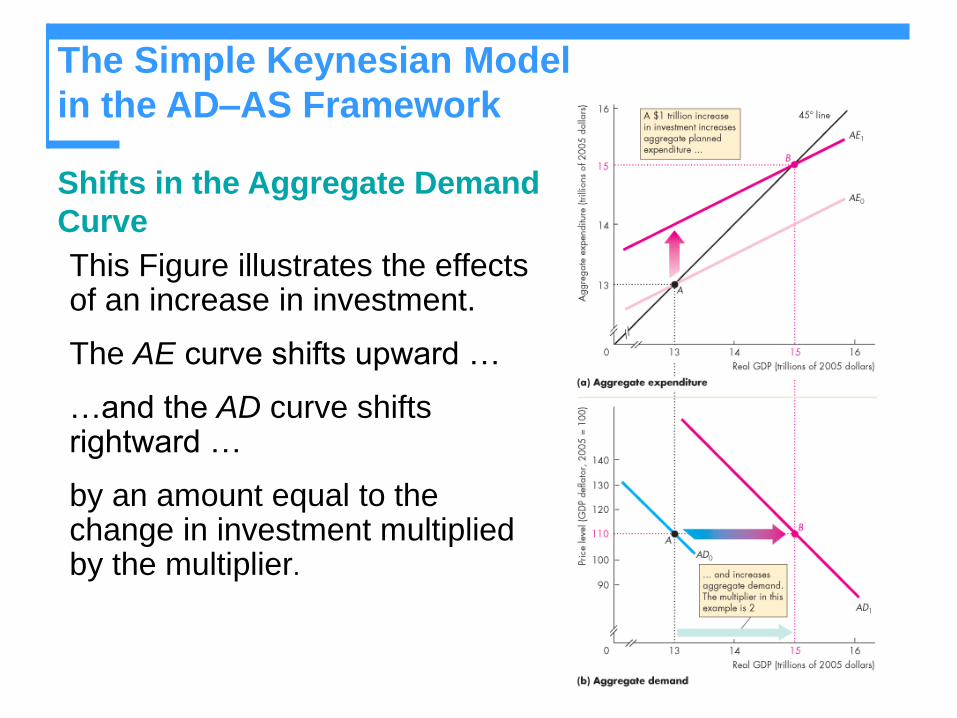

The Simple Keynesian Model

in the AD–AS Framework

Shifts in the Aggregate Demand

Curve

This Figure illustrates the effects of an increase in investment.

The AE curve shifts upward …

…and the AD curve shifts rightward …

by an amount equal to the change in investment multiplied by the multiplier.

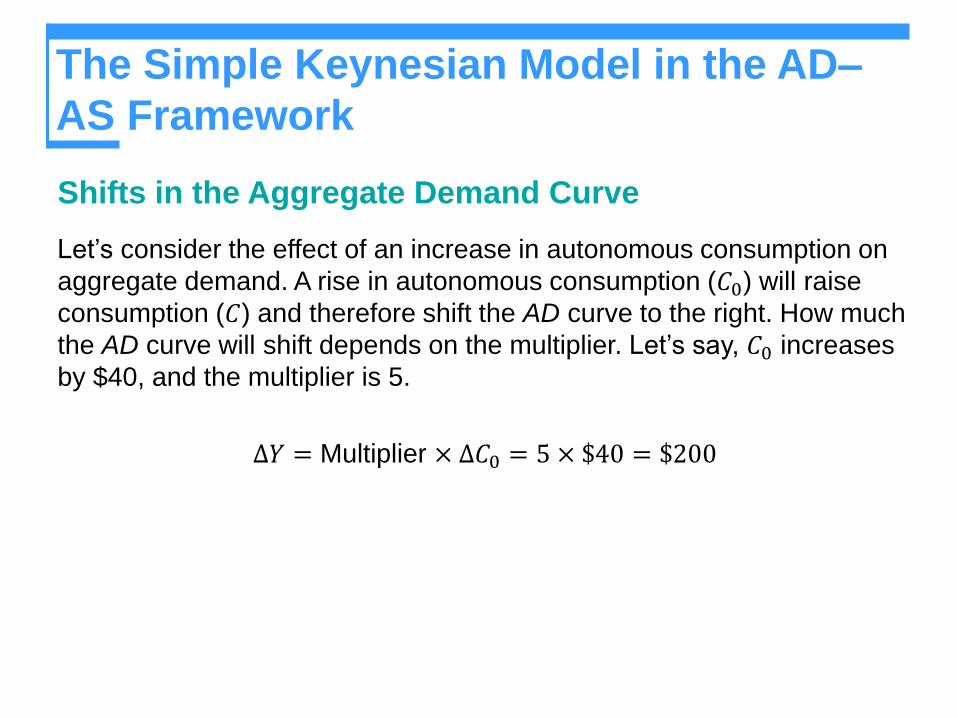

The Simple Keynesian Model in the AD–

AS Framework

Shifts in the Aggregate Demand Curve

Let’s consider the effect of an increase in autonomous consumption on

aggregate demand. A rise in autonomous consumption (𝐶0) will raise

consumption (𝐶) and therefore shift the AD curve to the right. How much

the AD curve will shift depends on the multiplier. Let’s say, 𝐶0 increases

by $40, and the multiplier is 5.

∆𝑌 = Multiplier × ∆𝐶0 = 5 × $40 = $200

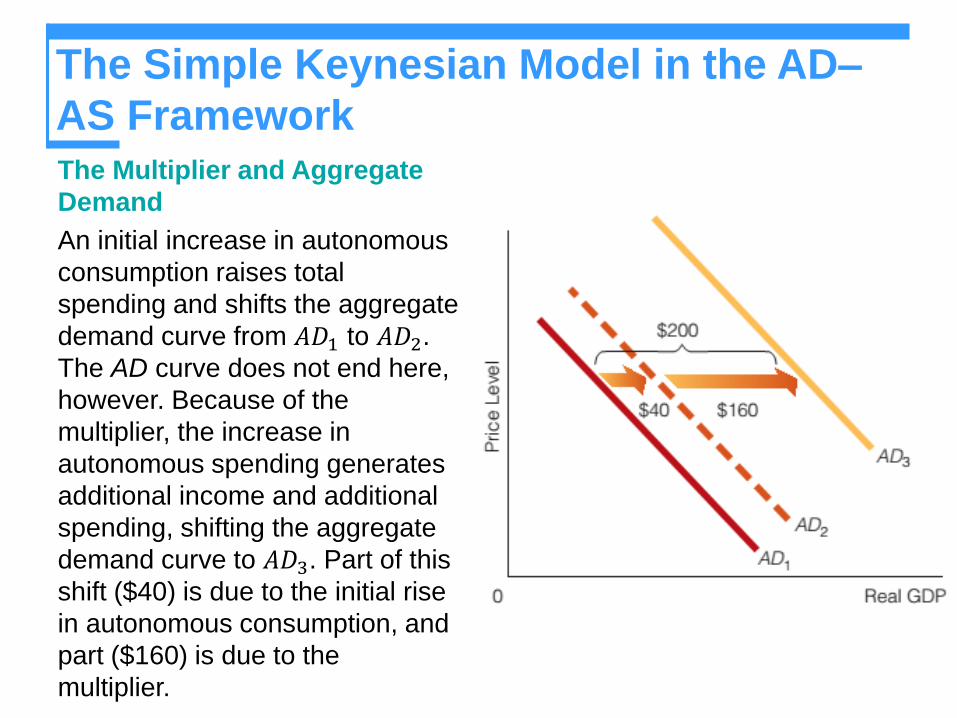

The Simple Keynesian Model in the AD–

AS FrameworkThe Multiplier and Aggregate

Demand

An initial increase in autonomous

consumption raises total

spending and shifts the aggregate

demand curve from 𝐴𝐷1 to 𝐴𝐷2. The AD curve does not end here,

however. Because of the

multiplier, the increase in

autonomous spending generates

additional income and additional

spending, shifting the aggregate

demand curve to 𝐴𝐷3. Part of this

shift ($40) is due to the initial rise

in autonomous consumption, and

part ($160) is due to the

multiplier.

The Simple Keynesian Model in the AD–

AS Framework

The Keynesian Aggregate Supply Curve

As noted, in the simple Keynesian model, the price level is assumed

to be constant until it reaches its full-employment or Natural Real

GDP level.

What does this assumption say about the Keynesian aggregate

supply curve?

Think back to the discussions of aggregate demand and aggregate

supply.

The AD curve is downward sloping, and the SRAS curve is upward

sloping. Therefore, any shift in the AD curve (rightward or leftward)

will automatically change (raise or lower) the price level.

If the price level is assumed to be constant, then the Keynesian

aggregate supply curve must have a horizontal section.

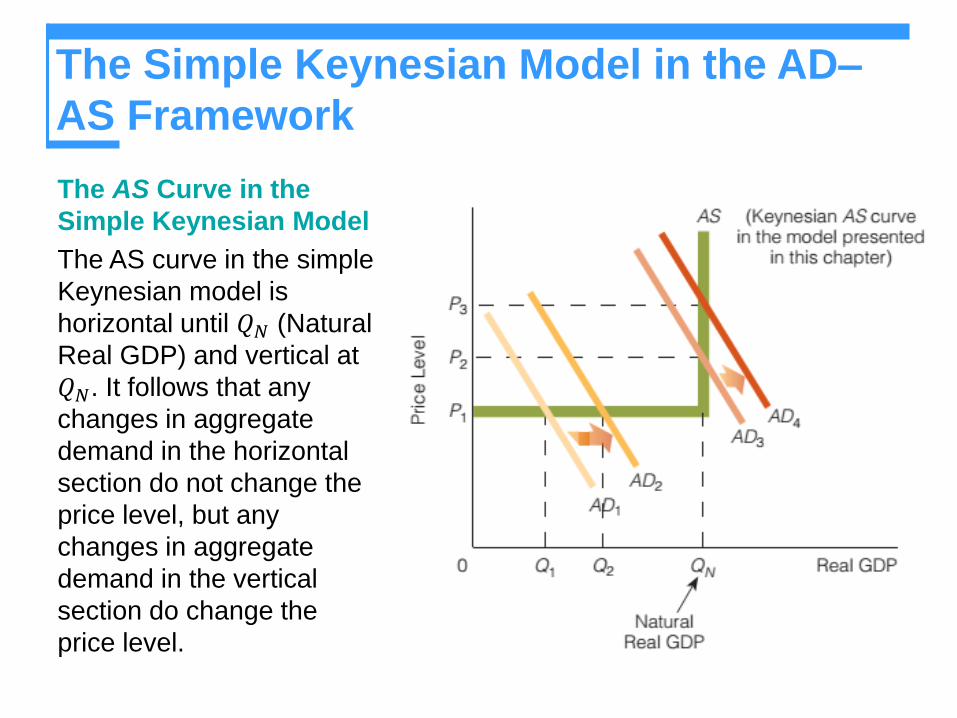

The Simple Keynesian Model in the AD–

AS Framework

The AS Curve in the

Simple Keynesian Model

The AS curve in the simple

Keynesian model is

horizontal until 𝑄𝑁 (Natural

Real GDP) and vertical at

𝑄𝑁. It follows that any

changes in aggregate

demand in the horizontal

section do not change the

price level, but any

changes in aggregate

demand in the vertical

section do change the

price level.

The Simple Keynesian Model in the AD–

AS Framework

The AS Curve in the

Simple Keynesian Model

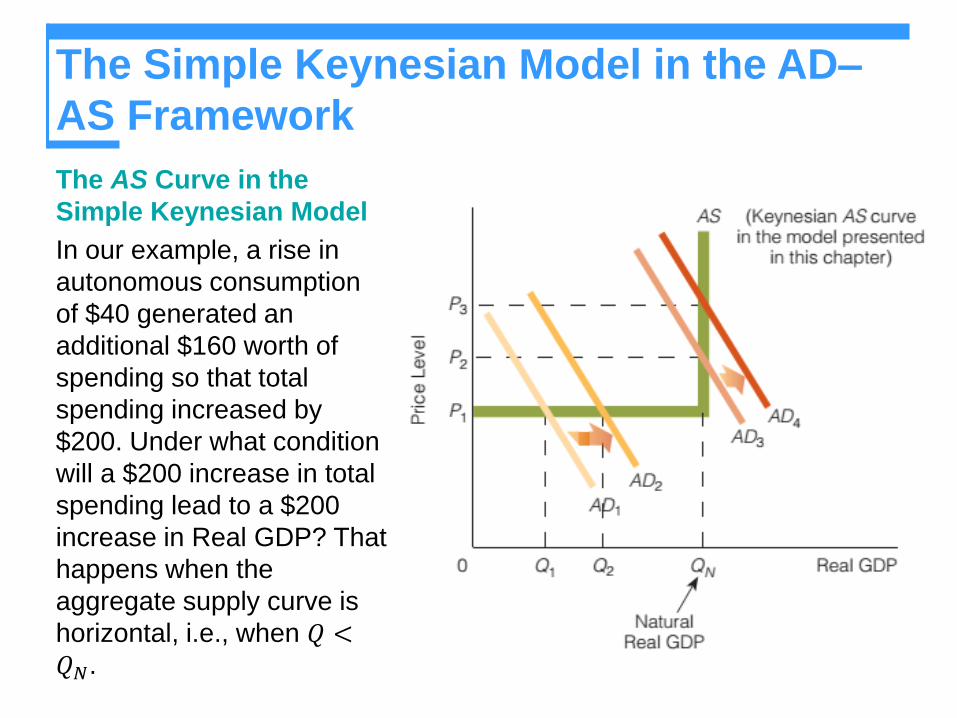

In our example, a rise in

autonomous consumption

of $40 generated an

additional $160 worth of

spending so that total

spending increased by

$200. Under what condition

will a $200 increase in total

spending lead to a $200

increase in Real GDP? That

happens when the

aggregate supply curve is

horizontal, i.e., when 𝑄 <𝑄𝑁.

The Simple Keynesian Model in the AD–

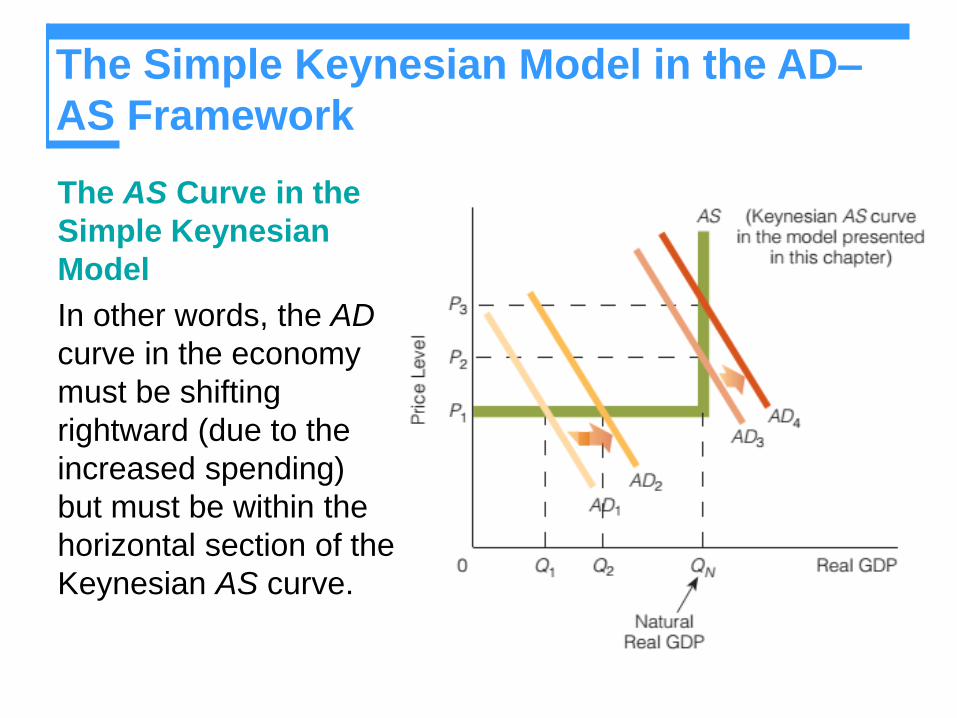

AS Framework

The AS Curve in the

Simple Keynesian

Model

In other words, the AD

curve in the economy

must be shifting

rightward (due to the

increased spending)

but must be within the

horizontal section of the

Keynesian AS curve.

The Simple Keynesian Model in the AD–

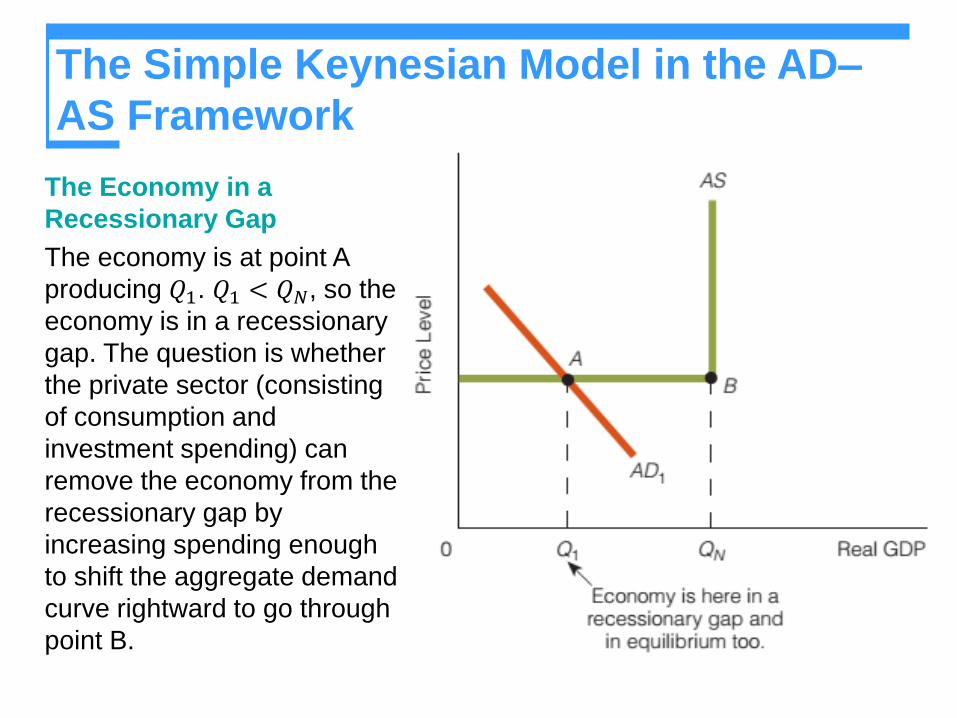

AS Framework

The Economy in a

Recessionary Gap

The economy is at point A

producing 𝑄1. 𝑄1 < 𝑄𝑁, so the

economy is in a recessionary

gap. The question is whether

the private sector (consisting

of consumption and

investment spending) can

remove the economy from the

recessionary gap by

increasing spending enough

to shift the aggregate demand

curve rightward to go through

point B.

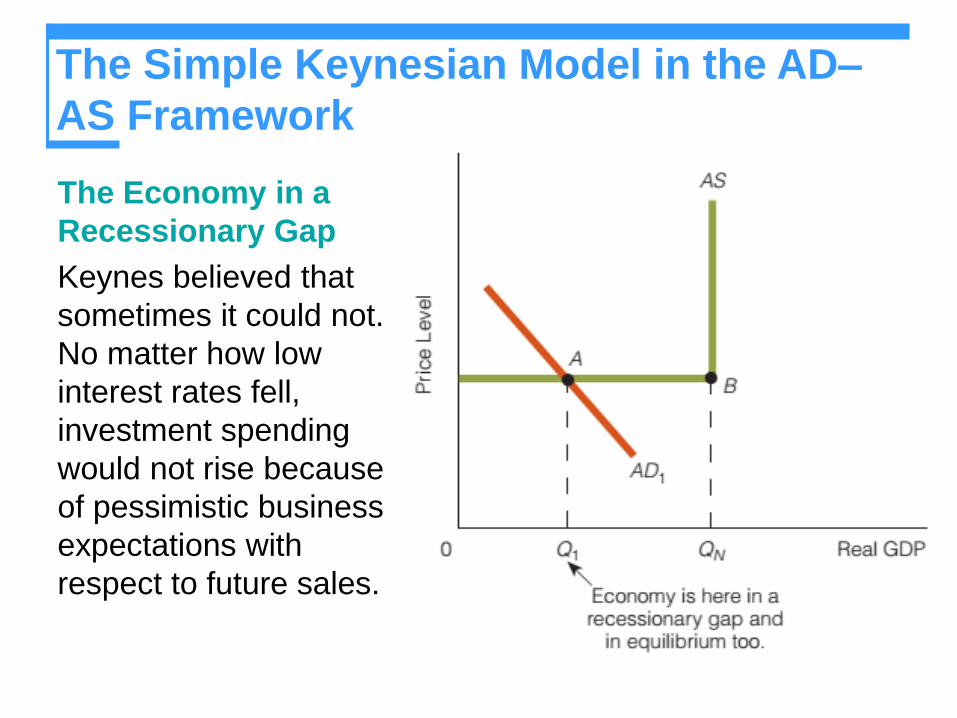

The Simple Keynesian Model in the AD–

AS Framework

The Economy in a

Recessionary Gap

Keynes believed that

sometimes it could not.

No matter how low

interest rates fell,

investment spending

would not rise because

of pessimistic business

expectations with

respect to future sales.

The Simple Keynesian Model in the AD–

AS Framework

Government’s Role in the Economy

In the self-regulating economy of the classical economists,

government does not have a management role to play. The

private sector (households and businesses) is capable of self-

regulating the economy at its Natural Real GDP level.

On the other hand, Keynes believed that the economy is not

self-regulating and that economic instability is a possibility. In

other words, the economy could get stuck in a recessionary gap.

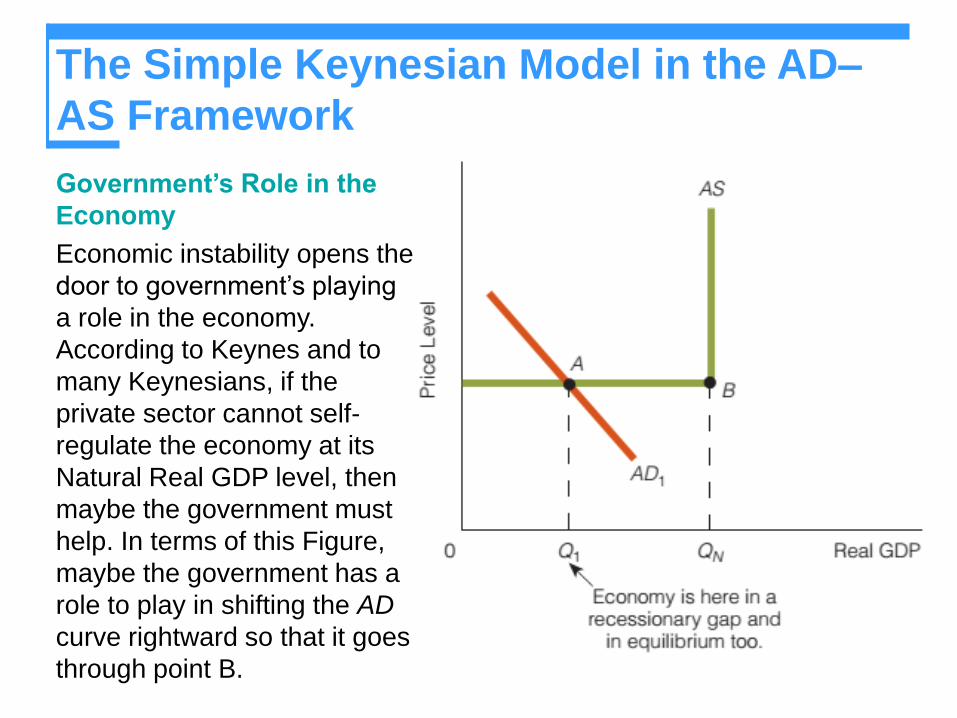

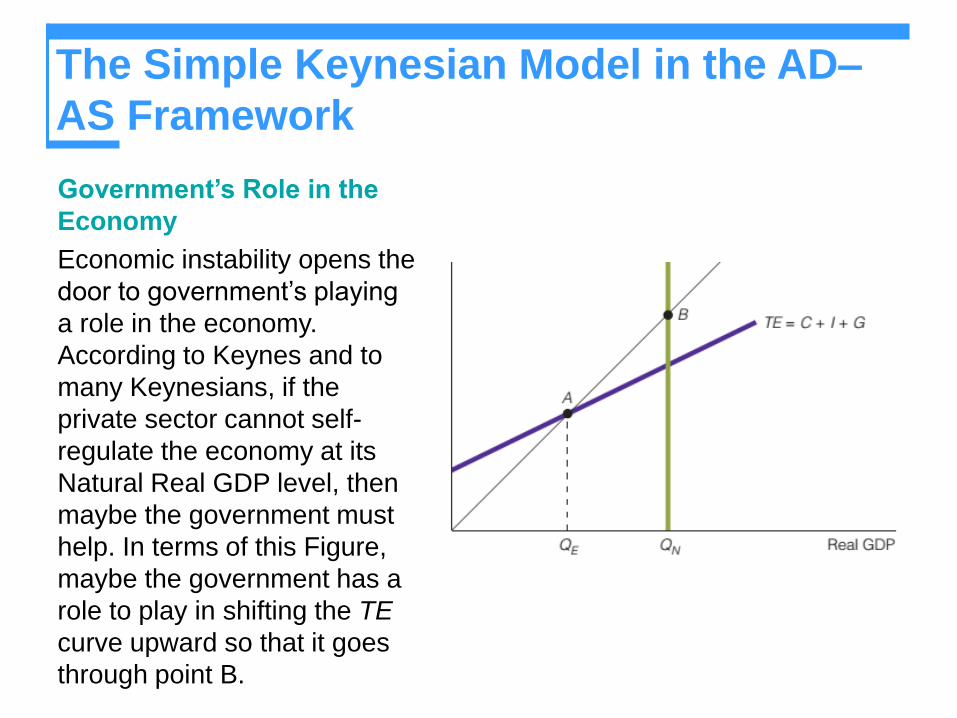

The Simple Keynesian Model in the AD–

AS Framework

Government’s Role in the

Economy

Economic instability opens the

door to government’s playing

a role in the economy.

According to Keynes and to

many Keynesians, if the

private sector cannot self-

regulate the economy at its

Natural Real GDP level, then

maybe the government must

help. In terms of this Figure,

maybe the government has a

role to play in shifting the AD

curve rightward so that it goes

through point B.

Government’s Role in the

Economy

Economic instability opens the

door to government’s playing

a role in the economy.

According to Keynes and to

many Keynesians, if the

private sector cannot self-

regulate the economy at its

Natural Real GDP level, then

maybe the government must

help. In terms of this Figure,

maybe the government has a

role to play in shifting the TE

curve upward so that it goes

through point B.

The Simple Keynesian Model in the AD–

AS Framework

The Theme of the Simple Keynesian Model

In terms of AD and AS, the essence of the simple Keynesian model can

be summarized in five statements:

1. The price level is constant until Natural Real GDP is reached.

2. The AD curve shifts if there are changes in C, I, or G.

3. According to Keynes, the economy could be stuck in a recessionary

gap.

4. The private sector may not be able to get the economy out of a

recessionary gap.

5. The government may have a management role to play in the economy.

According to Keynes, government may have to raise aggregate

demand enough to stimulate the economy to move it out of the

recessionary gap and to its Natural Real GDP level.

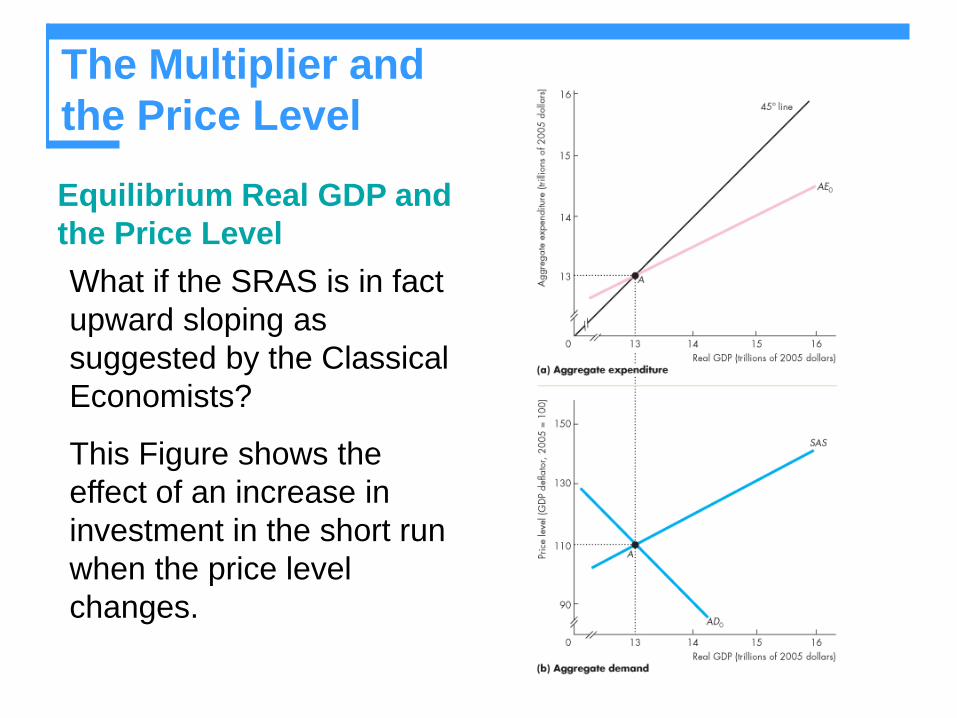

The Multiplier and

the Price Level

Equilibrium Real GDP and

the Price Level

What if the SRAS is in fact

upward sloping as

suggested by the Classical

Economists?

This Figure shows the

effect of an increase in

investment in the short run

when the price level

changes.

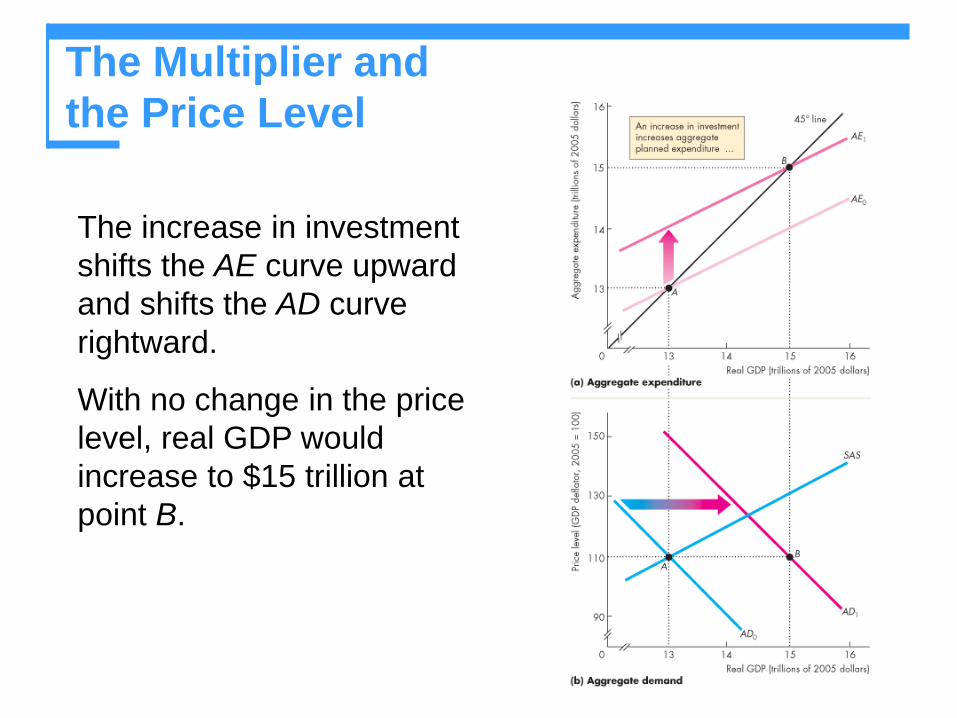

The Multiplier and

the Price Level

The increase in investment

shifts the AE curve upward

and shifts the AD curve

rightward.

With no change in the price

level, real GDP would

increase to $15 trillion at

point B.

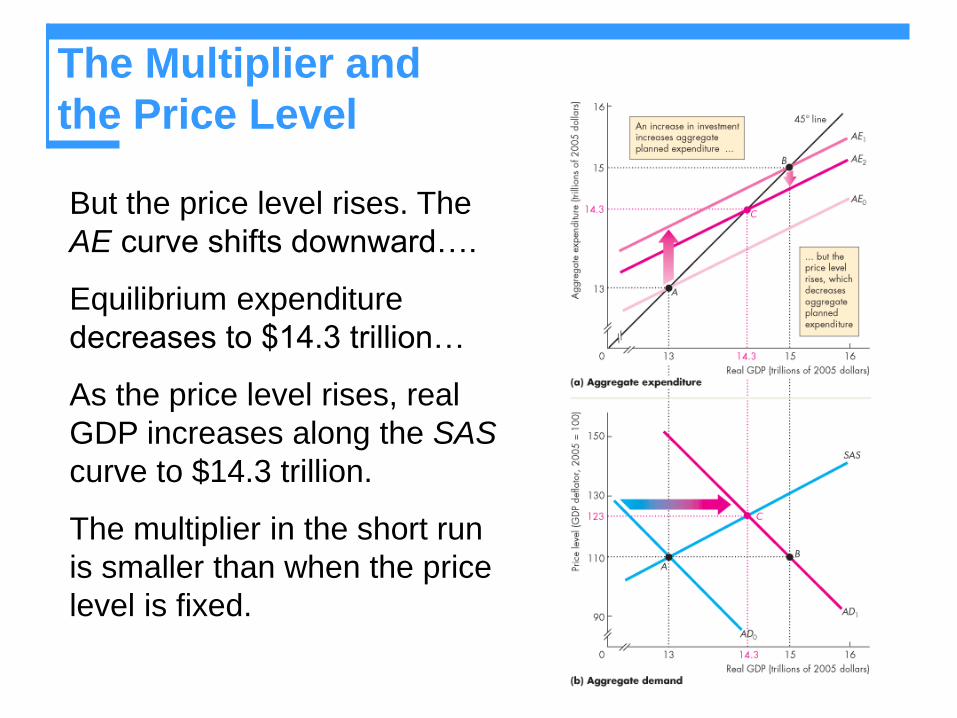

The Multiplier and

the Price Level

But the price level rises. The

AE curve shifts downward….

Equilibrium expenditure

decreases to $14.3 trillion…

As the price level rises, real

GDP increases along the SAS

curve to $14.3 trillion.

The multiplier in the short run

is smaller than when the price

level is fixed.

The Multiplier and

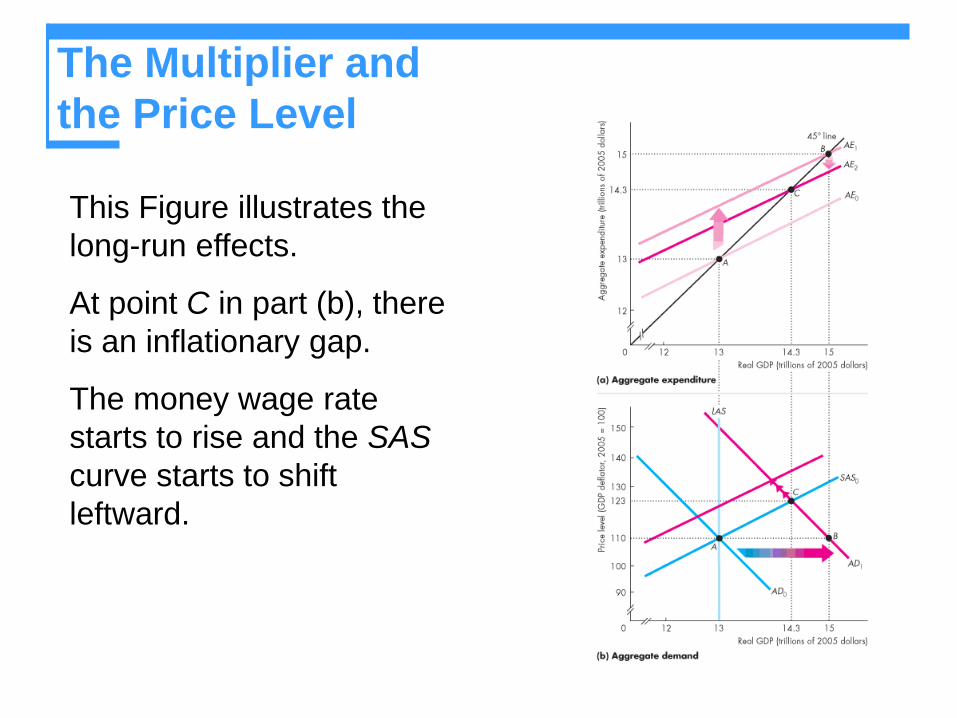

the Price Level

This Figure illustrates the

long-run effects.

At point C in part (b), there

is an inflationary gap.

The money wage rate

starts to rise and the SAS

curve starts to shift

leftward.

The Multiplier and

the Price Level

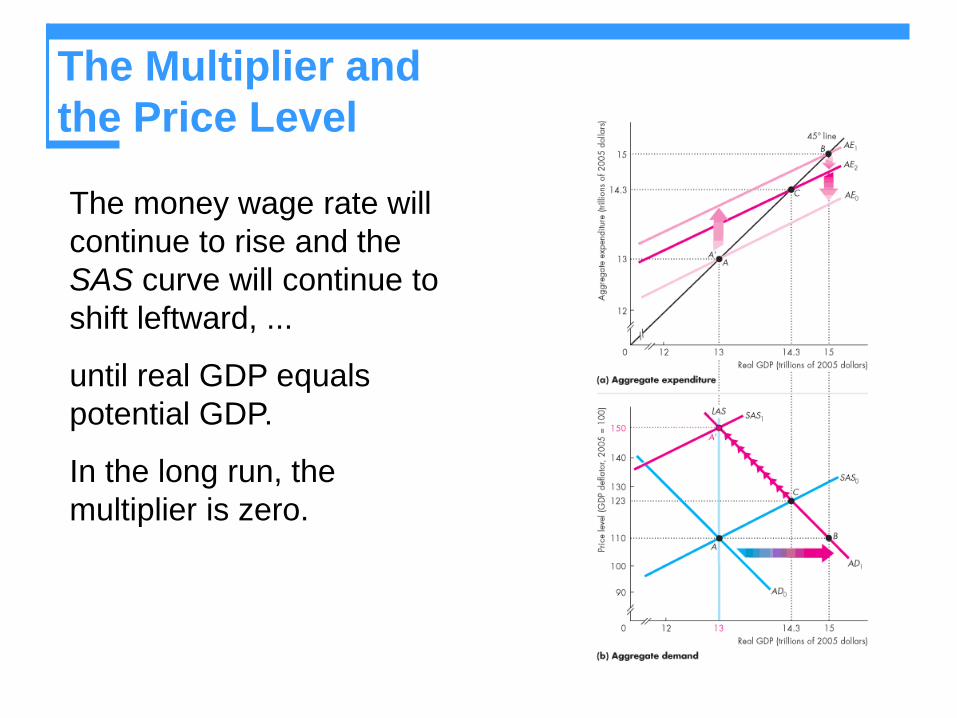

The money wage rate will

continue to rise and the

SAS curve will continue to

shift leftward, ...

until real GDP equals

potential GDP.

In the long run, the

multiplier is zero.