STEVE WOLOZ & ASSOCIATES INC. MANAGEMENT CONSULTANTS Connaître Vos Compétiteurs AECQ Le 1...

58

S S TEVE WOLOZ & TEVE WOLOZ & ASSOCIATES ASSOCIATES INC. INC. MANAGEMENT CONSULTANTS MANAGEMENT CONSULTANTS www.swaassoc.com Connaître Vos Compétiteurs AECQ Le 1 Novembre , 2003

-

Upload

augusta-thomas -

Category

Documents

-

view

214 -

download

0

Transcript of STEVE WOLOZ & ASSOCIATES INC. MANAGEMENT CONSULTANTS Connaître Vos Compétiteurs AECQ Le 1...

SSTEVE WOLOZ & TEVE WOLOZ & ASSOCIATES INC.ASSOCIATES INC.

MANAGEMENT CONSULTANTSMANAGEMENT CONSULTANTSwww.swaassoc.com

Connaître Vos

Compétiteurs

AECQLe 1 Novembre , 2003

SSTEVE WOLOZ & TEVE WOLOZ & ASSOCIATES INC.ASSOCIATES INC.

MANAGEMENT CONSULTANTSMANAGEMENT CONSULTANTSwww.swaassoc.com

?Connaître

Vos Compétiteurs

SSTEVE WOLOZ & TEVE WOLOZ & ASSOCIATES INC.ASSOCIATES INC.

MANAGEMENT CONSULTANTSMANAGEMENT CONSULTANTSwww.swaassoc.com

SWA Experience •Brasil ; Colombia•Ecquador ; Guyana •Honduras;Mexico•Mongolia; Salvador•United States

SWA Recherche

SSTEVE WOLOZ & TEVE WOLOZ & ASSOCIATES INC.ASSOCIATES INC.

MANAGEMENT CONSULTANTSMANAGEMENT CONSULTANTSwww.swaassoc.com

Format

•Discussion Interactive ( francais / englais) •Video

•Notes Disponible sur Demande

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 55

OverviewOverview INTRODUCTIONINTRODUCTION

MAJOR TRADE TREATIES AND THEIR IMPLICATIONSMAJOR TRADE TREATIES AND THEIR IMPLICATIONS

GLOBAL COMPETITIONGLOBAL COMPETITION

COMPETING REGIONS & COUNTRIES: STRENGTHS AND WEAKNESSES COMPETING REGIONS & COUNTRIES: STRENGTHS AND WEAKNESSES

VIDEO PRESENTATIONSVIDEO PRESENTATIONS

SUCCESS FACTORS AND PRESENT OPPORTUNITIESSUCCESS FACTORS AND PRESENT OPPORTUNITIES

MARKET INTELLIGENCEMARKET INTELLIGENCE

BASIS OF PRESENTATION / ACTUAL EXPERIENCE / STATISTICAL BASIS OF PRESENTATION / ACTUAL EXPERIENCE / STATISTICAL RESEARCHRESEARCH

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 66

IntroductionIntroductionDynamics

COMPETITOR

CUSTOMER

SUPPLIER

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 77

OverviewOverview INTRODUCTIONINTRODUCTION

MAJOR TRADE TREATIES AND THEIR IMPLICATIONSMAJOR TRADE TREATIES AND THEIR IMPLICATIONS

GLOBAL COMPETITIONGLOBAL COMPETITION

COMPETING REGIONS & COUNTRIES: STRENGTHS AND COMPETING REGIONS & COUNTRIES: STRENGTHS AND WEAKNESSES WEAKNESSES

VIDEO PRESENTATIONSVIDEO PRESENTATIONS

SUCCESS FACTORS AND PRESENT OPPORTUNITIESSUCCESS FACTORS AND PRESENT OPPORTUNITIES

MARKET INTELLIGENCEMARKET INTELLIGENCE

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 88

Trade TreatiesTrade Treaties

What are Trade Treaties ?What are Trade Treaties ?

Exclusive Agreements Between Exclusive Agreements Between Trading Partners To promote Trading Partners To promote

Trade Trade

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 99

Major Trade TreatiesMajor Trade TreatiesGATT 1947; 1986-DEC 1990; 1994GATT 1947; 1986-DEC 1990; 1994

WTO 1994 ; 2005WTO 1994 ; 2005NAFTA 1994NAFTA 1994

US Preference Programs for Apparel:US Preference Programs for Apparel:CBTPA Caribbean Basin Trade Partnership Act : CBTPA Caribbean Basin Trade Partnership Act : Oct 2000 – Oct 2000 –

Sep 2008Sep 2008

AGOA Africa Growth and Opportunity Act :AGOA Africa Growth and Opportunity Act :Oct 2000 – Sep 2008Oct 2000 – Sep 2008

ATPDEA Andean Trade Promotion and Drug Eradication ATPDEA Andean Trade Promotion and Drug Eradication Act : Act : Oct 2002 – Dec 2006Oct 2002 – Dec 2006

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 1010

Major Trade TreatiesMajor Trade Treaties

807 Outward Processing ?807 Outward Processing ?

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 1111

History of the CBI-NAFTAHistory of the CBI-NAFTA

NAFTA : 1994NAFTA : 1994==

Progressive and CompleteProgressive and CompleteElimination ofElimination of

Duty and QuotaDuty and QuotaBetween Trading PartnersBetween Trading Partners

United States; Mexico; CanadaUnited States; Mexico; CanadaRules of OriginRules of Origin

For Trading PartnersFor Trading Partners

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 1212

History of the CBI-NAFTAHistory of the CBI-NAFTA

Rules of OriginRules of Origin

“ “ yarn forward”yarn forward”

MeansMeans

Textile and Apparel goods must be Textile and Apparel goods must be produced from yarn made in a produced from yarn made in a

Nafta Country Nafta Country

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 1313

Chief Criterion of the Chief Criterion of the CBICBI

American Made FabricAmerican Made Fabric

Yarn Forward Yarn Forward

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 1414

Main Difference Main Difference CBICBI / NAFTA / NAFTA

NAFTANAFTAFABRIC CAN BE MADE IN ANY MEMBER NATION FABRIC CAN BE MADE IN ANY MEMBER NATION

CBICBIFABRIC & THREAD MUST BE MADE IN UNITED FABRIC & THREAD MUST BE MADE IN UNITED

STATESSTATES

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 1515

Chief Objectives of the Chief Objectives of the CBICBI

Repatriation of Apparel Production Repatriation of Apparel Production

From Asia to Western HemisphereFrom Asia to Western Hemisphere

Revitalisation of US Textile IndustryRevitalisation of US Textile Industry

Promotion of Trade with Neighbouring Promotion of Trade with Neighbouring

NationsNations

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 1616

Chief Advantages of the Chief Advantages of the CBICBI

Outward ProcessingOutward ProcessingDuty Free Duty Free

AndAndQuota Free Access to US Quota Free Access to US

Providing Providing Made With US Fabric Made With US Fabric

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 1717

CBTPA Trade Benefits

Office of Textiles and ApparelInternational Trade AdministrationU.S. Department of Commerce

US Market

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 1818

Treaties =Treaties =Opportunity + ChallengeOpportunity + Challenge

Heated race for more Heated race for more investment $$$ and new investment $$$ and new

strategic partnershipsstrategic partnerships

Existing trade treaties (e.g. NAFTA)Existing trade treaties (e.g. NAFTA)

New trade treaties (e.g. FTAA and WTO 2005)New trade treaties (e.g. FTAA and WTO 2005)

Opportunity to Opportunity to accelerate tradeaccelerate trade

Help finance full Help finance full package expansionpackage expansion

Develop Develop Manufacturing Manufacturing

expertise in all areasexpertise in all areas

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 1919

CBTPA SummaryCBTPA Summary

(i)(i) US Fabric Cut in US, Assembled in CBI US Fabric Cut in US, Assembled in CBI

(ii) (ii) US Fabric Cut and Assembled in CBIUS Fabric Cut and Assembled in CBI

(iii)(iii)Knit Apparel: Knit-to-Shape/Cut & SewKnit Apparel: Knit-to-Shape/Cut & Sew

(iv)(iv)Brassieres: Cut & Assembled in US or Brassieres: Cut & Assembled in US or CBICBI

(v) (v) Short Supply Yarns and FabricsShort Supply Yarns and Fabrics

(vi)(vi)Handloomed, Handmade & Folklore Handloomed, Handmade & Folklore Art.Art.

(vii)(vii)Special Rules: (Exceptions to the Special Rules: (Exceptions to the Rules)Rules)

(viii)(viii)Luggage: Cut in US/CBI, Assembled Luggage: Cut in US/CBI, Assembled in CBIin CBI

Section 211(b)(2)(A): Eligible Countries:

BarbadosBarbados

BelizeBelize

Costa RicaCosta Rica

Dominican RepublicDominican Republic

El SalvadorEl Salvador

GuatemalaGuatemala

GuyanaGuyanaHaitiHaitiHondurasHondurasJamaicaJamaicaNicaraguaNicaraguaPanamaPanamaSaint LuciaSaint LuciaTrinidad and TobagoTrinidad and Tobago

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 2020

CBTPA Trade TreatyCBTPA Trade Treaty

Total U.S. textile and apparel imports from Total U.S. textile and apparel imports from CBI increased by 8% CBI increased by 8%

CBPTA-qualifying trade accounts for 68 % CBPTA-qualifying trade accounts for 68 % of total exportsof total exports

88% of CBPTA Qualifying Apparel Use US 88% of CBPTA Qualifying Apparel Use US Yarn and US FabricYarn and US Fabric

10% of CBPTA Qualifying Apparel Use 10% of CBPTA Qualifying Apparel Use Regionally Formed Fabric of US YarnRegionally Formed Fabric of US Yarn

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 2121

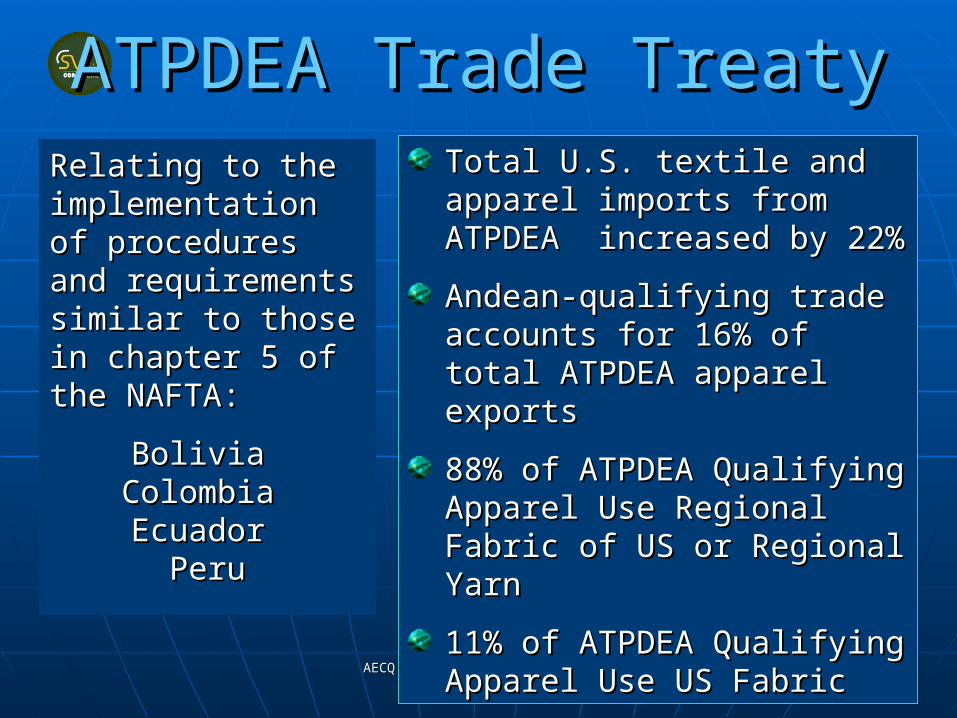

ATPDEA Trade TreatyATPDEA Trade TreatyRelating to the Relating to the implementation of implementation of procedures and procedures and requirements requirements similar to those in similar to those in chapter 5 of the chapter 5 of the NAFTA: NAFTA:

Bolivia Bolivia Colombia Colombia Ecuador Ecuador

PeruPeru

Total U.S. textile and Total U.S. textile and apparel imports from apparel imports from ATPDEA increased by 22%ATPDEA increased by 22%

Andean-qualifying trade Andean-qualifying trade accounts for 16% of total accounts for 16% of total ATPDEA apparel exportsATPDEA apparel exports

88% of ATPDEA Qualifying 88% of ATPDEA Qualifying Apparel Use Regional Fabric Apparel Use Regional Fabric of US or Regional Yarnof US or Regional Yarn

11% of ATPDEA Qualifying 11% of ATPDEA Qualifying Apparel Use US FabricApparel Use US Fabric

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 2222

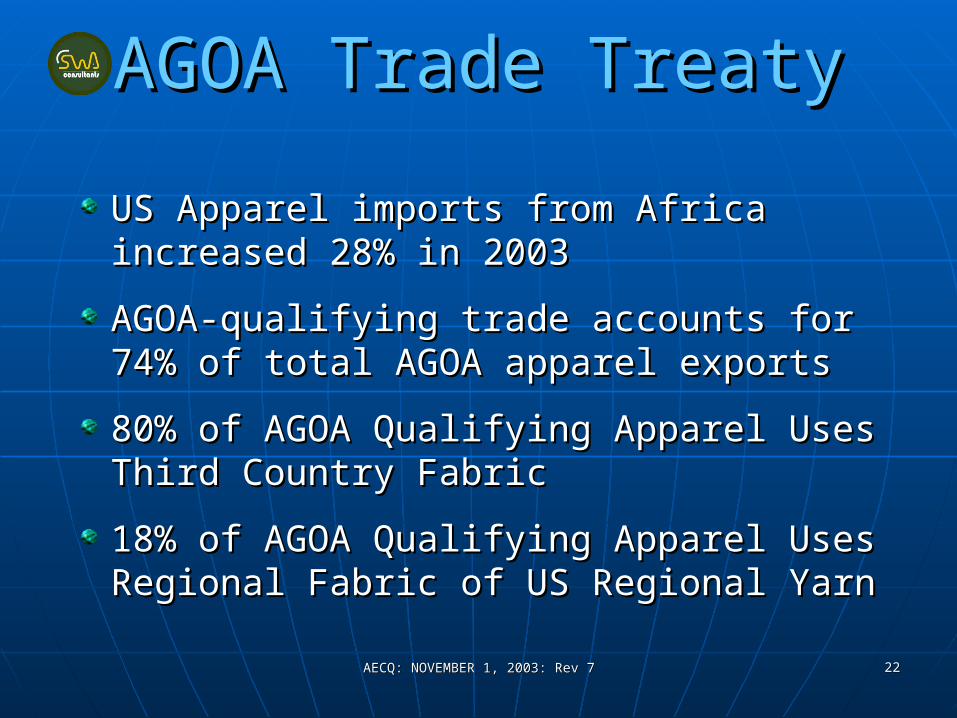

AGOA Trade TreatyAGOA Trade Treaty

US Apparel imports from Africa US Apparel imports from Africa increased 28% in 2003increased 28% in 2003

AGOA-qualifying trade accounts for 74% AGOA-qualifying trade accounts for 74% of total AGOA apparel exportsof total AGOA apparel exports

80% of AGOA Qualifying Apparel Uses 80% of AGOA Qualifying Apparel Uses Third Country FabricThird Country Fabric

18% of AGOA Qualifying Apparel Uses 18% of AGOA Qualifying Apparel Uses Regional Fabric of US Regional YarnRegional Fabric of US Regional Yarn

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 2323

OverviewOverview INTRODUCTIONINTRODUCTION

MAJOR TRADE TREATIES AND THEIR IMPLICATIONSMAJOR TRADE TREATIES AND THEIR IMPLICATIONS

GLOBAL COMPETITIONGLOBAL COMPETITION

COMPETING REGIONS & COUNTRIES: STRENGTHS AND COMPETING REGIONS & COUNTRIES: STRENGTHS AND WEAKNESSES WEAKNESSES

VIDEO PRESENTATIONSVIDEO PRESENTATIONS

SUCCESS FACTORS AND PRESENT OPPORTUNITIESSUCCESS FACTORS AND PRESENT OPPORTUNITIES

MARKET INTELLIGENCEMARKET INTELLIGENCE

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 2424

Global CompetitorsGlobal CompetitorsTop US SuppliersTop US Suppliers

March 31, 2003March 31, 2003

% Share% ShareGrowthGrowth

1.1. MEXICOMEXICO 11.8811.88 -2.44-2.442.2. CHINACHINA 10.0010.00 78.6878.683.3. HONDURASHONDURAS 6.31 6.31 14.6714.674.4. BANGLADESHBANGLADESH 5.17 5.17 -0.97-0.975.5. HONG KONGHONG KONG 4.51 4.51 -9.20-9.206.6. EL SALVADOREL SALVADOR 4.42 4.42 8.498.497.7. DOMINICAN REPUBLICDOMINICAN REPUBLIC 4.09 4.09 -0.50-0.508.8. KOREAKOREA 3.53 3.53 0.800.809.9. INDONESIAINDONESIA 3.48 3.48 7.827.8210.10. TAIWANTAIWAN 3.21 3.21 -5.40-5.40

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 2525

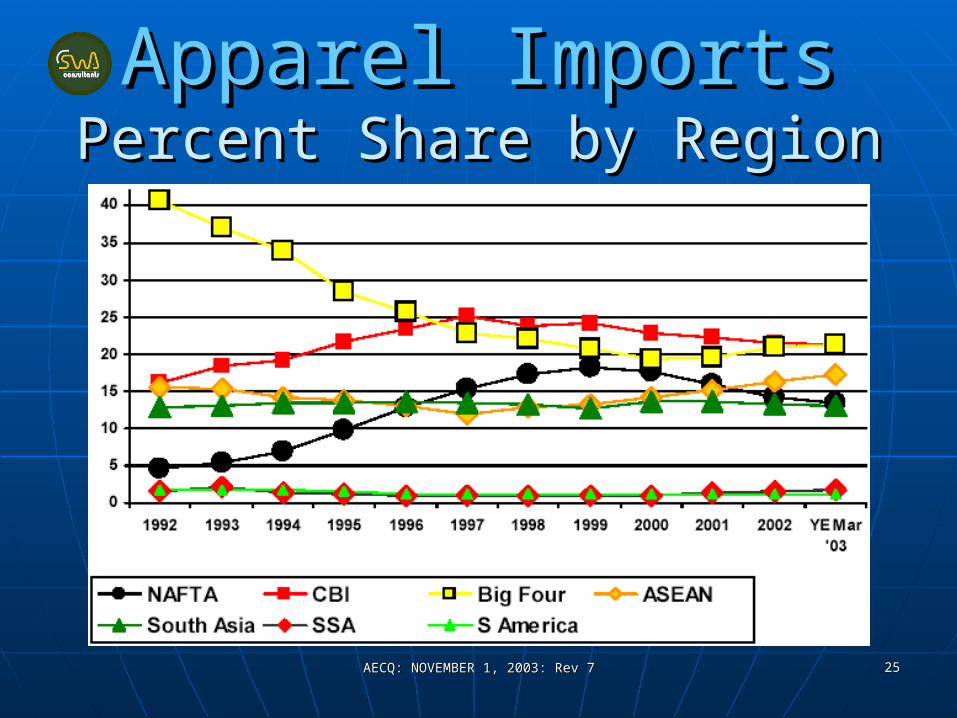

Apparel ImportsApparel ImportsPercent Share by RegionPercent Share by Region

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 2626

The Apparel Commodity The Apparel Commodity Supply ChainSupply Chain

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 2727

Apparel Imports From Apparel Imports From Asia Soar:Asia Soar:

1995-2002 1995-2002 (Billion SME)(Billion SME)

Trade-weighted Index of 21 Asian Currencies vs.Textile Imports from the Same 21 Asian Nations

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 2828

US Apparel Imports US Apparel Imports Central America & Dominican RepublicCentral America & Dominican Republic

20002000

$337

$831

$1,499$1,634

$2,365 $2,456

$0

$500

$1,000

$1,500

$2,000

$2,500

Nicaragua Costa Rica GuatemalaEl Salvador Honduras Rep. Dominicana

(U.S.$ Millones)

Source: OTEXA - 2001

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 2929

US Apparel ImportsUS Apparel Imports Shifts in Regional ImportsShifts in Regional Imports

1986 - 19961986 - 1996

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 3030

OverviewOverview INTRODUCTIONINTRODUCTION

MAJOR TRADE TREATIES AND THEIR IMPLICATIONSMAJOR TRADE TREATIES AND THEIR IMPLICATIONS

GLOBAL COMPETITIONGLOBAL COMPETITION

COMPETING REGIONS & COUNTRIES: STRENGTHS COMPETING REGIONS & COUNTRIES: STRENGTHS AND WEAKNESSESAND WEAKNESSES

VIDEO PRESENTATIONSVIDEO PRESENTATIONS

SUCCESS FACTORS AND PRESENT OPPORTUNITIESSUCCESS FACTORS AND PRESENT OPPORTUNITIES

MARKET INTELLIGENCEMARKET INTELLIGENCE

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 3131

Mexico:Mexico:HistoryHistory

Until the early 90s: almost exclusively Until the early 90s: almost exclusively an assembler, operating primarily as an assembler, operating primarily as

an 807 supplier to the US.an 807 supplier to the US.

By the mid 90s the non-807 By the mid 90s the non-807 exports rose significantlyexports rose significantly

Qualitative leap to more Qualitative leap to more value added production value added production

through cutting primarily through cutting primarily NAFTA sourced fabrics. NAFTA sourced fabrics.

In 1996, Mexico surpassed In 1996, Mexico surpassed

China to become the #1 China to become the #1

apparel exporter to the U.S.A. apparel exporter to the U.S.A.

In 1997, it made the top 10 In 1997, it made the top 10

list of apparel exporters to list of apparel exporters to

Canada for the 1Canada for the 1stst time time

Since NAFTA, Mexico's U.S. Since NAFTA, Mexico's U.S.

exports of apparel increased exports of apparel increased

nearly eight-foldnearly eight-fold

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 3232

Mexico:Mexico:HistoryHistory

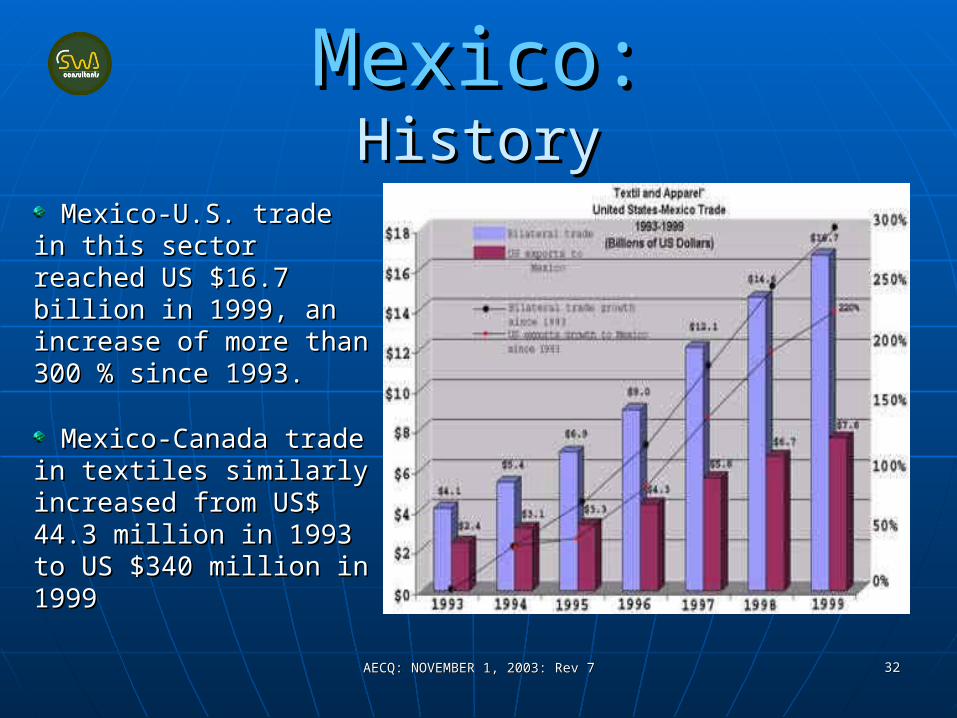

Mexico-U.S. trade in Mexico-U.S. trade in this sector reached US this sector reached US $16.7 billion in 1999, an $16.7 billion in 1999, an increase of more than increase of more than 300 % since 1993. 300 % since 1993.

Mexico-Canada trade in Mexico-Canada trade in textiles similarly textiles similarly increased from US$ 44.3 increased from US$ 44.3 million in 1993 to US million in 1993 to US $340 million in 1999$340 million in 1999

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 3333

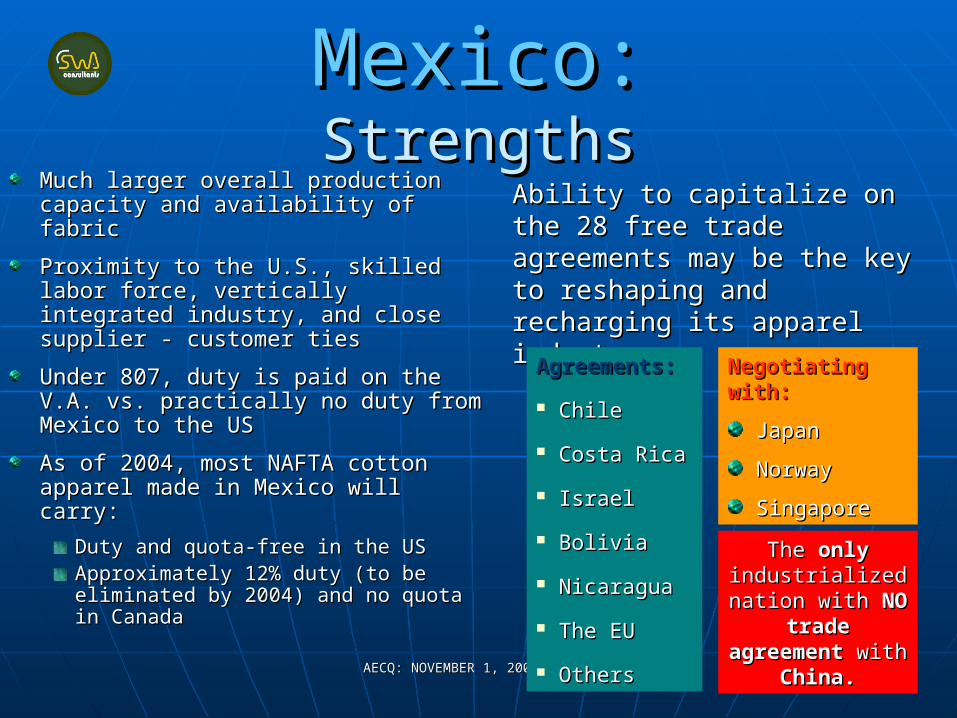

Mexico:Mexico:StrengthsStrengths

Much larger overall production Much larger overall production capacity and availability of fabriccapacity and availability of fabric

Proximity to the U.S., skilled labor Proximity to the U.S., skilled labor force, vertically integrated force, vertically integrated industry, and close supplier - industry, and close supplier - customer tiescustomer ties

Under 807, duty is paid on the V.A. Under 807, duty is paid on the V.A. vs. practically no duty from Mexico vs. practically no duty from Mexico to the USto the US

As of 2004, most NAFTA cotton As of 2004, most NAFTA cotton apparel made in Mexico will carry:apparel made in Mexico will carry:

Duty and quota-free in the USDuty and quota-free in the USApproximately 12% duty (to be Approximately 12% duty (to be eliminated by 2004) and no quota eliminated by 2004) and no quota in Canadain Canada

Ability to capitalize on the 28 Ability to capitalize on the 28 free trade agreements may be free trade agreements may be the key to reshaping and the key to reshaping and recharging its apparel recharging its apparel industry:industry:

Agreements:Agreements:

ChileChile

Costa RicaCosta Rica

IsraelIsrael

BoliviaBolivia

Nicaragua Nicaragua

The EUThe EU

OthersOthers

Negotiating Negotiating with:with:

JapanJapan

NorwayNorway

SingaporeSingapore

TheThe only only industrialized industrialized

nation withnation with NO NO trade trade

agreement agreement withwith China. China.

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 3434

Mexico:Mexico:WeaknessesWeaknesses

High rate of rejects: 1.43 %High rate of rejects: 1.43 % vs. 1.12 % in Costa Rica vs. 1.12 % in Costa Rica (Speer 2000)(Speer 2000)

High labor force turnover:High labor force turnover: 70% (Speer 2000)70% (Speer 2000)

High income taxes High income taxes

Shortages of electricityShortages of electricity

Piracy and smugglingPiracy and smuggling

97.5 % of 40,000 97.5 % of 40,000 businesses operating in the businesses operating in the textile sector are micro or textile sector are micro or small businessessmall businesses

They just took advantage of They just took advantage of FTA rather than investing in the FTA rather than investing in the engineering and the know-howengineering and the know-how

Passage of the TDA in 2000 Passage of the TDA in 2000 with CBI countries makes them with CBI countries makes them more threatening competitorsmore threatening competitors

Farther away, but no less Farther away, but no less menacing, China is in a position menacing, China is in a position to regain its U.S. apparel to regain its U.S. apparel market share in 2005, when market share in 2005, when the World Trade Organization the World Trade Organization (WTO) implements the final (WTO) implements the final phase-out of quotasphase-out of quotas

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 3535

AsiaAsia

Asia's significant investment in recent Asia's significant investment in recent years in Central America will years in Central America will accelerate:accelerate:

In Guatemala, Asian ownership of In Guatemala, Asian ownership of apparel facilities is up to 17 %, while apparel facilities is up to 17 %, while in other countries, this level of in other countries, this level of ownership ranges from 28% to 45%. ownership ranges from 28% to 45%.

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 3636

Asia:Asia:StrengthsStrengths

The key exporting nations of the Orient have The key exporting nations of the Orient have developed unquestionable high levels of:developed unquestionable high levels of:

Raw Materials AvailabilityRaw Materials Availability Quick Development CapabilityQuick Development Capability FlexibilityFlexibility Quality workmanshipQuality workmanship All are considered by import experts as the All are considered by import experts as the

strongest strategic advantages influencing strongest strategic advantages influencing the sourcing decision.the sourcing decision.

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 3737

Asia:Asia:WeaknessesWeaknesses

The long lead-time required for The long lead-time required for production in the Orientproduction in the Orient

The complexities of doing business The complexities of doing business offshore (language, distance)offshore (language, distance)

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 3838

Combating ChinaCombating China2005 Massacre2005 Massacre

A two-year window of opportunity before quotas A two-year window of opportunity before quotas expire under the WTO in 2005.expire under the WTO in 2005.

During this period, it will be important for During this period, it will be important for countries to develop a well-rounded sourcing countries to develop a well-rounded sourcing matrix that includes:matrix that includes:

High quality/price ratioHigh quality/price ratioFull package productionFull package productionRapid turnaround capabilitiesRapid turnaround capabilitiesExcellent customer serviceExcellent customer service

FlexibilityFlexibility

Over the long term, these capabilities will be Over the long term, these capabilities will be necessary for Latin America to compete with the necessary for Latin America to compete with the Far East.Far East.

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 3939

ChinaChina

Heavy investment in CBI countries Heavy investment in CBI countries (e.g., Nicaragua)(e.g., Nicaragua)

Impossibility to compete with China Impossibility to compete with China in terms of costin terms of cost

Necessity to offset that with:Necessity to offset that with:shorter cycle timesshorter cycle times

quicker response timesquicker response times

changing styles with the market. changing styles with the market.

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 4040

Caribbean CountriesCaribbean Countries::StrengthsStrengths

NAFTA made it almost impossible for other NAFTA made it almost impossible for other Latin American countries to compete with Latin American countries to compete with Mexico simply by offering cheap laborMexico simply by offering cheap labor

To remain competitive, manufacturers in To remain competitive, manufacturers in the CBI region responded by:the CBI region responded by:

Building state-of-the-art facilitiesBuilding state-of-the-art facilities

Offering high-quality goods and quick Offering high-quality goods and quick turnaroundturnaround

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 4141

Caribbean CountriesCaribbean Countries: : StrengthsStrengths

Absence of quota and duty under 807A Absence of quota and duty under 807A

Positive relationships with the U.S. Positive relationships with the U.S.

Outstanding productivity Outstanding productivity

Proximity to market Proximity to market

The infrastructureThe infrastructure

The know-howThe know-how

CostCostPerception in the importer community:Perception in the importer community:

Shorter lead times on fashion ordersShorter lead times on fashion orders

Higher levels of quality and Higher levels of quality and productivity than Mexicoproductivity than Mexico

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 4242

Caribbean CountriesCaribbean Countries: : WeaknessesWeaknesses

Lack of cooperation between countriesLack of cooperation between countriesJamaica's apparel industry:Jamaica's apparel industry:

Contractions over the past few yearsContractions over the past few years LLoss of business to other CBI beneficiary countries (Speer 2000)oss of business to other CBI beneficiary countries (Speer 2000)

Lack of fabricsLack of fabricsLack of non-cotton apparel production (30% of U.S. exports, vs. Lack of non-cotton apparel production (30% of U.S. exports, vs. balanced Mexico's exports)balanced Mexico's exports)A small, inexperienced woven goods baseA small, inexperienced woven goods baseA shortage of skilled pattern makersA shortage of skilled pattern makersA lack of financial capital A lack of financial capital Potential U.S. investors, such as textile mills, are not familiar with Potential U.S. investors, such as textile mills, are not familiar with the CBI region. the CBI region.

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 4343

OverviewOverview INTRODUCTIONINTRODUCTION

MAJOR TRADE TREATIES AND THEIR IMPLICATIONSMAJOR TRADE TREATIES AND THEIR IMPLICATIONS

GLOBAL COMPETITIONGLOBAL COMPETITION

COMPETING REGIONS & COUNTRIES: STRENGTHS AND COMPETING REGIONS & COUNTRIES: STRENGTHS AND WEAKNESSES WEAKNESSES

VIDEO PRESENTATIONSVIDEO PRESENTATIONS

SUCCESS FACTORS AND PRESENT OPPORTUNITIESSUCCESS FACTORS AND PRESENT OPPORTUNITIES

MARKET INTELLIGENCEMARKET INTELLIGENCE

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 4444

HondurasHonduras

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 4545

MexicoMexico

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 4646

El SalvadorEl Salvador

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 4747

GuyanaGuyana

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 4848

Honduras: Honduras: Pride Mfg.Pride Mfg.

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 4949

OverviewOverview INTRODUCTIONINTRODUCTION

MAJOR TRADE TREATIES AND THEIR IMPLICATIONSMAJOR TRADE TREATIES AND THEIR IMPLICATIONS

GLOBAL COMPETITIONGLOBAL COMPETITION

COMPETING REGIONS & COUNTRIES: STRENGTHS AND COMPETING REGIONS & COUNTRIES: STRENGTHS AND WEAKNESSES WEAKNESSES

VIDEO PRESENTATIONSVIDEO PRESENTATIONS

SUCCESS FACTORS AND PRESENT OPPORTUNITIESSUCCESS FACTORS AND PRESENT OPPORTUNITIES

MARKET INTELLIGENCEMARKET INTELLIGENCE

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 5050

Factors For SuccessFactors For Success

FULL PACKAGE SERVICE FULL PACKAGE SERVICE

SPEED TO MARKETSPEED TO MARKET

TOTAL COSTTOTAL COST

SECURITYSECURITY

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 5151

Factors For SuccessFactors For SuccessNEW BUSINESS MODEL NEW BUSINESS MODEL

FOR SUCCESS FOR SUCCESS

Total Supply Chain Total Supply Chain IntegrationIntegration

Elimination Of MiddlemenElimination Of Middlemen Minimization of Overheads, Minimization of Overheads,

Lead Times (Birnbaum; Pg Lead Times (Birnbaum; Pg 40)40)

2 Link Paradigm: Factory - 2 Link Paradigm: Factory - CustomerCustomer

Full Value Garment Sourcing Full Value Garment Sourcing ModelModel

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 5252

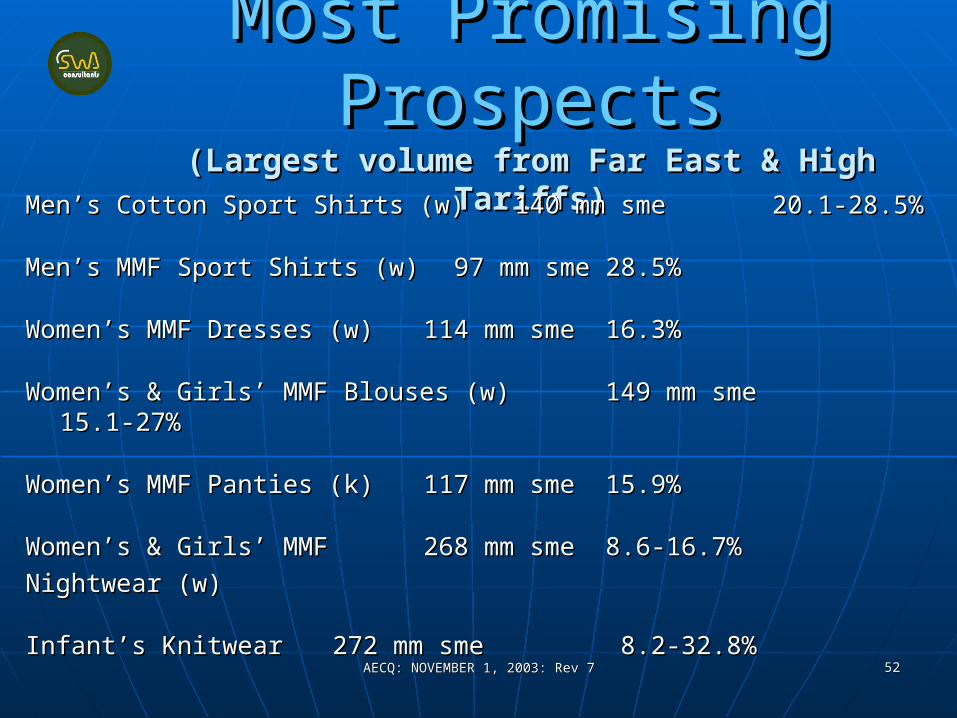

Most Promising ProspectsMost Promising Prospects(Largest volume from Far East & High Tariffs)(Largest volume from Far East & High Tariffs)

Men’s Cotton Sport Shirts (w)Men’s Cotton Sport Shirts (w) 140 mm sme140 mm sme 20.1-28.5% 20.1-28.5%

Men’s MMF Sport Shirts (w)Men’s MMF Sport Shirts (w) 97 mm sme 97 mm sme 28.5%28.5%

Women’s MMF Dresses (w)Women’s MMF Dresses (w) 114 mm sme114 mm sme 16.3%16.3%

Women’s & Girls’ MMF Blouses (w) Women’s & Girls’ MMF Blouses (w) 149 mm sme 149 mm sme 15.1-15.1-27%27%

Women’s MMF Panties (k)Women’s MMF Panties (k) 117 mm sme117 mm sme 15.9%15.9%

Women’s & Girls’ MMF Women’s & Girls’ MMF 268 mm sme268 mm sme 8.6-16.7%8.6-16.7%

Nightwear (w)Nightwear (w)

Infant’s KnitwearInfant’s Knitwear 272 mm sme 8.2-32.8%272 mm sme 8.2-32.8%

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 5353

OverviewOverview INTRODUCTIONINTRODUCTION

MAJOR TRADE TREATIES AND THEIR IMPLICATIONSMAJOR TRADE TREATIES AND THEIR IMPLICATIONS

GLOBAL COMPETITIONGLOBAL COMPETITION

COMPETING REGIONS & COUNTRIES: STRENGTHS AND COMPETING REGIONS & COUNTRIES: STRENGTHS AND WEAKNESSES WEAKNESSES

VIDEO PRESENTATIONSVIDEO PRESENTATIONS

SUCCESS FACTORS AND PRESENT OPPORTUNITIESSUCCESS FACTORS AND PRESENT OPPORTUNITIES

MARKET INTELLIGENCEMARKET INTELLIGENCE

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 5454

Trade DataTrade Data

WHERE TO FIND MORE WHERE TO FIND MORE

INFORMATION INFORMATION

PROGRAMS TO HELP PROGRAMS TO HELP

EXPORT MARKET DEVELOPMENTEXPORT MARKET DEVELOPMENThttp://www.swaassoc.comhttp://www.swaassoc.com

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 5555

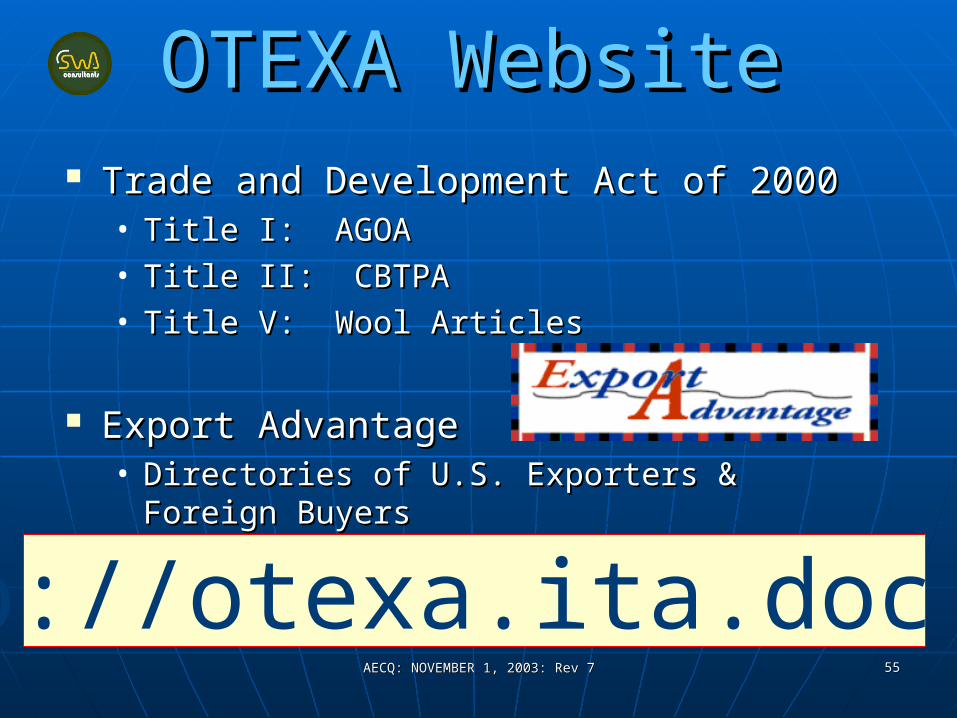

Trade and Development Act of 2000Trade and Development Act of 2000• Title I: AGOATitle I: AGOA• Title II: CBTPATitle II: CBTPA• Title V: Wool ArticlesTitle V: Wool Articles

Export AdvantageExport Advantage• Directories of U.S. Exporters & Foreign Directories of U.S. Exporters & Foreign

BuyersBuyers

OTEXA WebsiteOTEXA Website

http://otexa.ita.doc.gov

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 5656

Apparel AssociationsApparel AssociationsMATERIAL WORLDMATERIAL WORLD

http://www.material-world.com http://www.material-world.com

2 X YEAR2 X YEARNEXT EVENTNEXT EVENT

MAY 18-20, 2004MAY 18-20, 2004MIAMI BEACH, FlaMIAMI BEACH, Fla

Co Hosted ByCo Hosted By

American Apparel and Footwear Association American Apparel and Footwear Association http://http://www.americanapparel.orgwww.americanapparel.org//

American Apparel Producers' NetworkAmerican Apparel Producers' Networkhttp://http://www.usawear.orgwww.usawear.org//

AECQ: NOVEMBER 1, 2003: Rev 7AECQ: NOVEMBER 1, 2003: Rev 7 5757

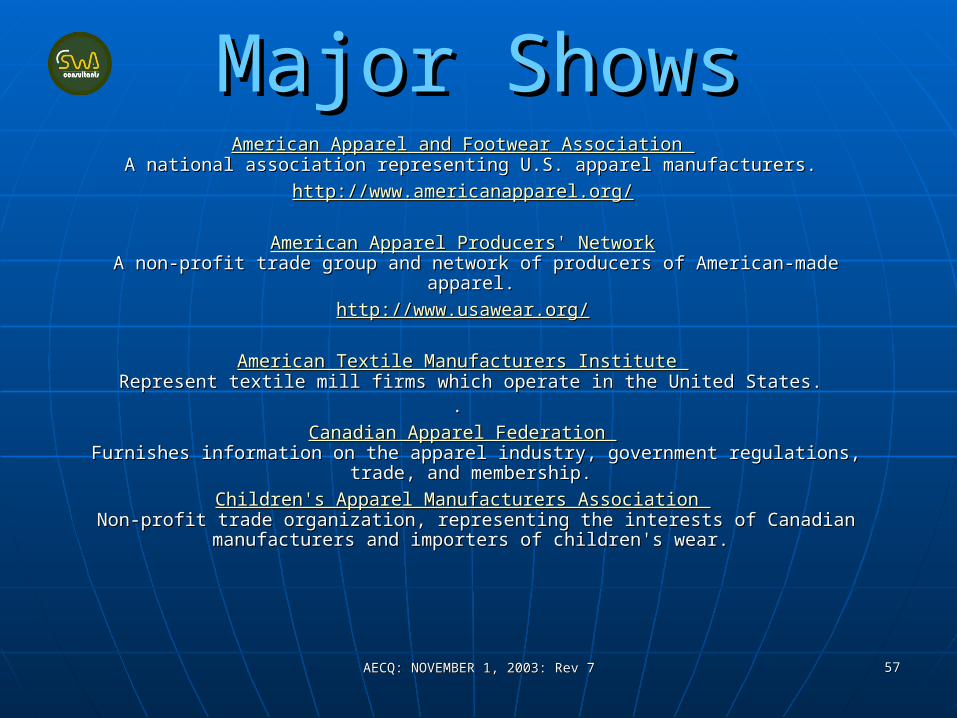

Major ShowsMajor ShowsAmerican Apparel and Footwear Association American Apparel and Footwear Association

A national association representing U.S. apparel manufacturers. A national association representing U.S. apparel manufacturers. http://http://www.americanapparel.orgwww.americanapparel.org//

American Apparel Producers' NetworkAmerican Apparel Producers' NetworkA non-profit trade group and network of producers of American-made A non-profit trade group and network of producers of American-made

apparel. apparel. http://http://www.usawear.orgwww.usawear.org//

American Textile Manufacturers Institute American Textile Manufacturers Institute Represent textile mill firms which operate in the United States. Represent textile mill firms which operate in the United States.

. . Canadian Apparel Federation Canadian Apparel Federation

Furnishes information on the apparel industry, government regulations, trade, Furnishes information on the apparel industry, government regulations, trade, and membership. and membership.

Children's Apparel Manufacturers Association Children's Apparel Manufacturers Association Non-profit trade organization, representing the interests of Canadian Non-profit trade organization, representing the interests of Canadian

manufacturers and importers of children's wear. manufacturers and importers of children's wear.

SSTEVE WOLOZ & TEVE WOLOZ & ASSOCIATES INC.ASSOCIATES INC.

MANAGEMENT CONSULTANTSMANAGEMENT CONSULTANTSwww.swaassoc.com