Status of Network roll outs and applications

19

Update on IoT – Status of Network roll outs and applications CME Sharing Initiative Prepared by Youssef El Shaarany, Robert Knechtel, José Alejandro Rojas and Astrid Soufflay September 21 th , 2017

Transcript of Status of Network roll outs and applications

Update on IoT – Status of Network roll outs and applications

CME Sharing Initiative

Prepared by Youssef El Shaarany, Robert Knechtel, José Alejandro

Rojas and Astrid Soufflay

September 21th, 2017

© 2017 BearingPoint France SAS | 2

Definition of the “Internet of Things” (IoT)

What is the hype all about?

THE INTERNET OF THINGS:MAPPING THE VALUE BEYOND THE HYPE

McKinsey Global InstituteJune 2015

We define the Internet of Things as sensors and

actuators connected by networks to computing

systems. These systems can monitor or manage the

health and actions of connected objects and

machines. Connected sensors can also monitor the

natural world, people, and animals.

The objective of this sharing is to :• Understand the roles of alternative LPWA IoT technologies• And the impact on telecom operators of main unlicensed LPWA technologies*:

LPWA: Low Power Wide Area technologies are a type of wireless communication technologies designed to allow long range communicationsat a low bit rate. Two main categories of LPWA exist: licensed and unlicensed (not requiring a telecom operator). Source ARCEP

© 2017 BearingPoint France SAS | 3

ContentsContents

Today’s IoT market environment1

2 Deep dive on LPWA networks

3 Conclusions

© 2017 BearingPoint France SAS | 4

ContentsContents

Today’s IoT market environment1

2 Deep dive on LPWA networks

3 Conclusions

© 2017 BearingPoint France SAS | 5

IoT market size – Expect strong growth ahead

I. Today’s IoT market environment

Global IoT market size and forecast

2015

304.3

778.4

2018 2019

543.8

20172014

241.6196.3

401.1

2016

CAGR+31.7%

Number of connected devices

3,32

4,54

6,25

8,71

12,22

17,22

20192017

CAGR+39,0%

2018201620152014

• Today’s IoT market is at valued around US$ 400 billion, more than doubled its original size in 2014

• With a CAGR of 31.72 % it is expected to reach US$ 778,43 billion in 2019

• Strong market growth is mainly driven by a high adoption rate from companies entering the IoT market

• Device interoperability solutions represents 40% of IoT value creation potential, compared to 5% for connectivity solutions

• Current forecasts predict 17.22 billion devices connected in use, starting from 3.32 billion devices back in 2014 and growing with a CAGR of 39%

billion unitsUS$ billion

Data source on this slide: TechNavio report “Global Internet of Things (IOT) Market 2015-2019”

© 2017 BearingPoint France SAS | 6

IoT market – drivers, challenges and market segmentation

I. Today’s IoT market environment

Drivers & Tends

Market Challenges

48.9%

15.7%

35.8% 35,8%

15,2%

49,1%

• APAC constitutes largest regional market of the global IoT market• Although total market volume almost triples, the relative

geographical distribution remains the same

2017 2019Geographical distribution

US$ billionKey market drivers:

• Decline in Cost of Communication Devices -> faster adoption on B2B and B2C segments :

• Increased Adoption of Smart Devices by Consumers-> Enhanced services and customer experience

• Increased Adoption of IoT by Enterprises -> Value chain optimization and data gathering capabilities

IoT blurs industry barriers allowing to develop new business models

Major challenges for further IoT market growth:

• Data protection and security concerns

• Lack of standardization

• High cost of implementation

• Monetization remains challenging for TelCos, with an ARPC of US$ 1.6 in the IoT business

Market size2017 196.322019 778.43

Growth path for telcos

Telcos can increase their IoT revenue generating potential by:

• Moving up the value chain : entering the market for platform services. Roughly 80% of the value of IoT applications is in this segment.

• Embracing more connectivity choices (licensed and unlicensed LPWA, Wi-Fi …)

• Enabling interoperability across application silos

AmericasAPACEMEA

Source: TechNavio report “Global Internet of Things (IOT) Market 2015-2019” , McKinsey Global Institute, “The Internet of Things, mapping the value beyond the hype, 2015, and “ Digital Ecosystem Management for Telco IoT by BearingPoint.

© 2017 BearingPoint France SAS | 7

IoT market – Star End user applications

I. Today’s IoT market environment

Smart HomeHome controllers andsecurity systems

Energy and UtilitiesSmart grids &predictive maintenance

Connected VehiclesAutonomous vehicles & predictive maintenance

Industry 4.0Operation & equipmentoptimization

Human: Healthcare & fitness Maintain human wellness, manage disease

Retail environmentsAutomated checkout surface optimization

Transportation andlogistics:Merchandisetracking

Smart CitiesPublic transportationoptimization

IoT helps to generate value by:• Transforming business process• Enabling new business models

Source: McKinsey Global Institute, “The Internet of Things, mapping the value beyond the hype, 2015

© 2017 BearingPoint France SAS | 8

Value chain and key technologies (non exhaustive list of actors)

I. Today’s IoT market environment

Device manufacturers Connectivity layer Platform layer Solution layer

OEMs

Telecom Operators

Unlicensed LPWA technologies

We focus on the impact of LPWA networks on telecom operators

Software companies/integrators

deploys

deploys

developed

developed LTE-M

Application mgmt. platforms including API services for B2B clients

Private network solutions for corporate and public sector customers

deploys LTE-M and NB IoT

deploys NB IoT Smart object services (m-health, smart home…)

SAMI platform allowsto connect devices from different OEMs

Source: BearingPoint Telecom practice

Application mgmt. platforms including API services for B2B clients

© 2017 BearingPoint France SAS | 9

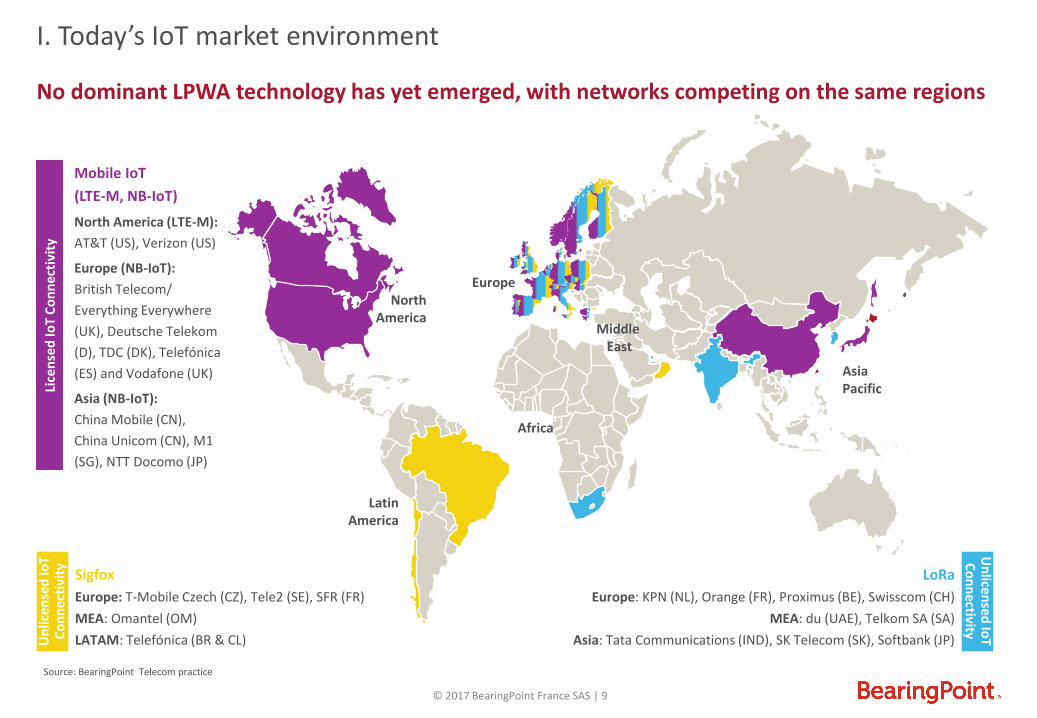

No dominant LPWA technology has yet emerged, with networks competing on the same regions

Mobile IoT

(LTE-M, NB-IoT)

North America (LTE-M):

AT&T (US), Verizon (US)

Europe (NB-IoT):

British Telecom/

Everything Everywhere

(UK), Deutsche Telekom

(D), TDC (DK), Telefónica

(ES) and Vodafone (UK)

Asia (NB-IoT):

China Mobile (CN),

China Unicom (CN), M1

(SG), NTT Docomo (JP)

Lice

nse

d Io

TC

on

ne

ctiv

ity

Sigfox

Europe: T-Mobile Czech (CZ), Tele2 (SE), SFR (FR)

MEA: Omantel (OM)

LATAM: Telefónica (BR & CL)Un

lice

nse

d Io

TC

on

nec

tivi

ty LoRa

Europe: KPN (NL), Orange (FR), Proximus (BE), Swisscom (CH)

MEA: du (UAE), Telkom SA (SA)

Asia: Tata Communications (IND), SK Telecom (SK), Softbank (JP)

Un

license

d Io

TC

on

ne

ctivity

North America

AsiaPacific

Latin America

Africa

Middle East

Europe

Source: BearingPoint Telecom practice

I. Today’s IoT market environment

© 2017 BearingPoint France SAS | 10

ContentsContents

Today’s IoT market environment1

2 Deep dive on LPWA networks

3 Conclusions

© 2017 BearingPoint France SAS | 11

Low Power Wide Area (LPWA) networks are designed to answer industrial IoT connectivity needs. Two competing approaches exist:

II. Deep dive on LPWA networks

Licensed LPWAUnlicensed LPWA

NB-IoT: (LTE Derivative)Direct competitor of LoRa. Co-developed by both equipment manu-facturers (Ericsson, Huawei, Intel) and operators (Vodafone, AT&T, DT). Collaborating within the 3GPP standardization body

SigfoxA French startup created in 2009, developing low-cost LPWA devices.

LoRaA 330 member alliance that specified the “LoRaWAN“ protocol. This standard ensures inter-operability LoRa devices

LTE-M: (LTE derivative)Its larger bandwidth targets IoT applications with a demand for large data volumes, e.g. managing industrial processes, machinery or infrastructure

EC – GPRS: Based on 2G networks, this LPWA technology is especially suitable for deploying IoT services in the absence 3G/ 4G net-works, e.g. emerging countries

Unlicensed LPWA are the narrowband, low-energy consumption equivalents of WiFi and satellite communications. Main features are: wide area coverage, low power consumption, low unit cost and the use of unlicensed spectrum

As competing technologies to Sigfox and LoRa, operators developed cellular-based LPWA-alternatives. Since these technologies use the operator’s spectrum, they are also referred to as licensed LPWA.So far two LTE-based technologies are available and one based on the 2G/ GSM networks:

Sources: SigFox and Lora websites

© 2017 BearingPoint France SAS | 12

Comparison of the four major LPWA network technologies: Sigfox vs. LoRa vs. EC-GPRS vs. LTE-derivatives

Company or service

description

Bandwidth spectrumand range

Maturity (TTM)

Use cases

• NB –IoT (Narrowband IoT) is a SIM based alternative to LoRaand SigFox. It features:

• Lower device cost and battery consumption than regular SIM devices

• Carrier grade connectivity• Spectrum use optimization

(high device density)

• From 20 to 80 kb/s• Licensed 700 – 900 MHz• Range <15 KM

• Currently deployed by DT in the NL and GER

• Vodafone installation in ES

LTE-derivatives

• Maintenance monitoring of utilities

• Point of sale terminals• Vehicle fleet management• Asset tracking

• Proven technology, with 19 clients in 26 countries

SigFox

• Sigfox manufactures low-cost LPWA devices featuring:

• Low cost transparent and simple pricing policy. Price decreases as the customer adds devices

• Utilities (metering)• Agriculture: irrigation, silo

monitoring, livestock mgmt.• Smart home :monitoring • Industry: prev. maintenance

• Proven technology with 22 clients in 19 countries

LoRa Alliance

• LoRa shares Sigfox LPWA features. Other features are:

• Coverage of all network elements: devices, software and terminals

• Adaptive data rate maximizes battery life and network capacity

• Secured encrypted connectivity

• Intelligent building mgmt. • Logistics: inventory mgmt.,

route optimization • Agriculture: soil monitoring

and water use optimization

• Extended Coverage-GSM (EC-GSM)

• Up to 7-times extension of range, especially well suited for remote area locations or indoor scenarios

• Software upgrade of existing 2G networks

• Supports extended battery lifetime

• Up- & downlink 500 kb/s• 900 Mhz band• Range <15 km

• Ericsson, Intel and Orange completed live trials in 2016

EC-GPRS

• Smart meters/ smart grids• Fleet management

• <100 bit/s• Unlicensed 868 MHz • Range <13 KM

• From 300 bit/s to 100 kb/s • Unlicensed 868 MHz• Range <11 KM

Network at glance

• Carrier grade NB & BB IoTconnectivity

• Cost controlled no frills NB connectivity

• Secured, carrier compatible unlicensed IoT alternative

• Licensed NB alternative for emerging countries

II. Deep dive on LPWA networks

© 2017 BearingPoint France SAS | 13

• Implemented as a software upgrade to existing GPRS networks

• Improved coverage at challenging locations, e.g. deep indoor basements

• Already existing standards and infrastructure -> easy and fast deployment in LTE equipped areas

• Support from large telecom operators and equipment manufacturers

• Proven 3GPP characteristics: QoS, roaming capabilities, secured communications

• Devices can operate in private or public networks

• Full data emitting and receiving capabilities

• Network and battery optimization capabilities according to device/application needs

• High security standards (encryption)

Which are the advantages of each technology from the customer’s perspective?

II. Deep dive on LPWA networks

Pros

LTE-derivativesSigFox LoRa Alliance EC-GPRS

• Low cost devices and services, starting 10 EUR year

• Ability to cover a large geographical scope and industries

• Wide existing geographical coverage

• Useful for private networks requiring only local connectivity needs.

• Open system

We will focus on SigFox, currently the most widely spread technology due to it simplicity and low cost

Sources slides 12&13: BearingPoint Telecom practice

© 2017 BearingPoint France SAS | 14

II. Deep dive on LPWA networks

Indicators which SigFox is looking at during transactions Increase of volume of connected devices

• Type of traffic per device

• Number of maximum messages uplink/downlink

• Duration of the average subscription

Low subscription prices and pay for use

• Subscription : between 1 and 14 euros per year for each

connected device

• Degressive tarification : the more devices there are, the

cheaper it is

SigFox’s Business Model

• In every country Sigfox starts business by setting up a partnership with a telco operator. It’s already deployed in 15 countries.

• In USA and Europe, its used a non licensed bandwidth of 868MHz in Europe and 915MHz in the US

• In 2015, Sigfox used a public fundraising in order to extend its business, and several telco operators answered the call like Telefonica and SK Telecom.

SigFox and Telco Operators

In France, SigFox signed a deal with SFR in 2016 which praised its innovative technology and broad network existing in 15 countries. The main arguments for choosing the company were

• Global coverage

• Absence of SIM card

• Overall simplicity of the system

The deal implies that SFR will accompany SigFox in developing its infrastructures in countries were it is not yet present such as Israel or the United States.

Examples of applications

SigFox’s low subscription price and wide network is reinforced by alliances the company made with Telco operators across the globe

Sources : BearingPoint Telecom practice

© 2017 BearingPoint France SAS | 15

• Telecom operators offering IoT connectivity

• End users B2B or B2C customers requiring low latency and high QoS

• Telecom operators

• End users: B2B customers (private networks) requiring low device cost and a secured connection

• Telecom operators

• Increased indoor coverage• Very simple roll-out by

installing software-only updates to existing 2G networks

• Fast deployment potential (uses already existing networks)

• End-device mobility (connectivity is not limited to on site networks)

• Carrier grade connectivity

• Ability to operate in public, private and hybrid network modes

• Deep indoor (and underground) coverageDifferentiators

Target customers and differentiating characteristics

II. Deep dive on LPWA networks

Target customers

LTE-derivativesSigFox LoRa Alliance EC-GPRS

• End users: B2B customers (private networks) requiring low device cost

• Telecom operators

• Existing national coverage in various countries (France, UK, Italy, Spain)

• Optimized energy consumption

• Suits companies requiring basic connectivity needs

Unlicensed networks are suitable for local connectivity needs while licensed networks allow higher data transmission rates higher security standards

Sources: BearingPoint Telecom practice; and ICT Express “A Survey on LPWA Technology”, March 2017, publisher Elsevier.

© 2017 BearingPoint France SAS | 16

Key takeaways. Which network technology should I choose if I need:

II. Deep dive on LPWA networks

Low operating costs

High QoS

LTE-derivativesSigFox LoRa Alliance EC-GPRS

Secured private networks (industrial

applications)

Latency / performance

Reaching rural or suburban areas

Sources : ICT Express “A Survey on LPWA Technology”, March 2017, publisher :Elsevier.

© 2017 BearingPoint France SAS | 17

A look at the potential of 5G networks

What next ?

What is 5G?

5G is 10 times faster than 4G. It decreases significateviely the latency in cellphone networks which currently limits IoT applications. It was designed for IoT use. It will strongly increase

the efficiency and the number of connected devices.

This increase in latency could bring a whole new world of IoT devices. The needs of IoT devices have been taken into consideration when constructing 5G. By 2022 it is expected

that 5G will allow low bandwidth usage. The viability of connectivity will also significantly increase allowing usage of IoT restricted until now, especially in health, transport and

industry.

The fifth generation mobile networks (5G) will be composed of a new interface radio, but also of LTE and Wi-FI while still being handled by the same heart of network. 5G is predicted

to arrive by 2020 . Ericsson plans that by 2022, 5G will make up to 12% of the networks.

What is its potential?

What does it meanfor IoT?

Sources: Ericson mobility report, November 2017

© 2017 BearingPoint France SAS | 18

ContentsContents

Today’s IoT market environment1

2 Deep dive on LPWA networks

3 Conclusions

© 2017 BearingPoint France SAS | 19

• Telcos experience great challenges creating new business models to monetize the IoT business opportunities. As classical connectivity revenue declines (ARPC) over the next years TelCos must adapt their market approach and business models in order to stay competitive

• Staying competitive in an adaptive and increasingly dense market as that of IoT implies a change of mindset and culture for Telco actors which might be difficult faced with startups which are extremely reactive and adaptive

• Rise of the various new low power network technologies means it can be difficult to select the the “right” technology. However, licensed and unlicensed LPWA-technologies should be seen as complementary to each other. There is no “right or wrong” answer !

Our conclusion and areas where BearingPoint could support TelCos with the IoT-challenges ahead

Challenges for Telcos in today’s IoT environment