State Tax Laws Amendment (Budget and Other Measures) Act 2013

35

i State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013 TABLE OF PROVISIONS Section Page PART 1—PRELIMINARY 1 1 Purposes 1 2 Commencement 2 PART 2—CONGESTION LEVY ACT 2005 4 3 Purpose 4 4 Definitions 4 5 Amount of levy 4 6 How is levy assessed 5 7 Statutory ratio repealed 5 8 Exemptions 5 9 New section 20 substituted 6 20 Parking for people attending special events 6 10 Further exemptions 6 11 Part year concession for parking spaces in a public car park 6 12 New section 40 inserted 7 40 State Tax Laws Amendment (Budget and Other Measures) Act 2013 7 PART 3—DUTIES ACT 2000 8 13 Definitions—New Zealand Exchange included in definitions of listed company and listed trust 8 14 Definitions—other amendments 8 15 Definition of eligible first home buyer in section 57G repealed 9 16 What is a PPR transfer? 9 17 Concessional rate of duty for certain PPR transfers 9 18 Section 57JA substituted 9 57JA Reduction of duty for certain first home buyers on PPR transfers 9 19 Exemption or concession for young farmers 10 20 Section 69AE substituted 10 69AE Calculation of exemption or concession on transfer of single parcel of land or partial interest in single parcel of land 10

Transcript of State Tax Laws Amendment (Budget and Other Measures) Act 2013

i

State Tax Laws Amendment (Budget and Other Measures) Act 2013

No. 41 of 2013

TABLE OF PROVISIONS Section Page

PART 1—PRELIMINARY 1 1 Purposes 1 2 Commencement 2

PART 2—CONGESTION LEVY ACT 2005 4 3 Purpose 4 4 Definitions 4 5 Amount of levy 4 6 How is levy assessed 5 7 Statutory ratio repealed 5 8 Exemptions 5 9 New section 20 substituted 6

20 Parking for people attending special events 6 10 Further exemptions 6 11 Part year concession for parking spaces in a public car park 6 12 New section 40 inserted 7

40 State Tax Laws Amendment (Budget and Other Measures) Act 2013 7

PART 3—DUTIES ACT 2000 8 13 Definitions—New Zealand Exchange included in definitions

of listed company and listed trust 8 14 Definitions—other amendments 8 15 Definition of eligible first home buyer in section 57G repealed 9 16 What is a PPR transfer? 9 17 Concessional rate of duty for certain PPR transfers 9 18 Section 57JA substituted 9

57JA Reduction of duty for certain first home buyers on PPR transfers 9

19 Exemption or concession for young farmers 10 20 Section 69AE substituted 10

69AE Calculation of exemption or concession on transfer of single parcel of land or partial interest in single parcel of land 10

Section Page

ii

21 What is a relevant acquisition? 11 22 Acquisition of economic entitlement 11 23 Conversion of a private unit trust scheme into a public unit

trust scheme 12 24 Conversion of a private company to a listed company 12 25 Definitions—Registration of unit trust schemes 12 26 Private vehicle used to convey incapacitated person 12 27 Transitional provision—Duties Amendment (Landholder)

Act 2012 13

PART 4—FIRE SERVICES PROPERTY LEVY ACT 2012 14 28 New section 8 substituted 14

8 Property that is subject to the levy 14 29 Treatment of parcels of land for levy purposes 14 30 New section 9A inserted 15

9A Single farm enterprise exemption 15 31 Land that is not subject to the levy 17 32 Determination of levy rates 18 33 Councils to pay only fixed charge in respect of specified

leviable land 18 34 Revised assessment of liability to pay levy amount 18 35 Delegation 18 36 Permitted disclosures to particular persons 19

PART 5—FIRST HOME OWNER GRANT ACT 2000 20 37 Extension of residence requirement 20 38 Definitions 20 39 Eligible transaction 20 40 Special eligible transactions 21 41 Amount of grant 21 42 Protection of confidential information 22

PART 6—LIQUOR CONTROL REFORM ACT 1998 23 43 New section 178A inserted 23

178A Delegation 23

PART 7—PAYROLL TAX ACT 2007 24 44 Relevant contracts 24 45 Transitional provision 25

18 State Tax Laws Amendment (Budget and Other Measures) Act 2013 25

Section Page

iii

PART 8—TAXATION ADMINISTRATION ACT 1997 27 46 Section 66 substituted 27

66 Deputy and Assistant Commissioners 27 47 Section 67 substituted 27

67 Other staff 27 48 Section 69 substituted 28

69 Delegation by the Commissioner 28 49 Permitted disclosures to particular persons or for particular

purposes 28 50 New section 92A inserted 28

92A Permitted disclosures—dutiable transactions in relation to land 28

51 Permitted disclosures to particular persons 29

PART 9—WATER ACT 1989 30 52 Waiver of service charges 30 53 Reimbursement by State 30

PART 10—REPEAL OF AMENDING ACT 31 54 Repeal of amending Act 31

═══════════════

ENDNOTES 32

1

State Tax Laws Amendment (Budget

and Other Measures) Act 2013† No. 41 of 2013

[Assented to 28 June 2013]

The Parliament of Victoria enacts:

PART 1—PRELIMINARY

1 Purposes The purposes of this Act are—

(a) to amend the Congestion Levy Act 2005 to increase the amount of the levy and extend it to short stay parking spaces in the central business district and inner Melbourne;

Victoria

Part 1—Preliminary

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

2

(b) to amend the Duties Act 2000 in relation to eligible first home buyers, young farmers, the landholder provisions and motor vehicle duty;

(c) to amend the Fire Services Property Levy Act 2012 to clarify how the levy is assessed;

(d) to amend the First Home Owner Grant Act 2000—

(i) to increase the residence requirement from 6 months to 12 months and in relation to the disclosure of information;

(ii) to limit the availability of the first home owner grant to the purchase or construction of new homes and to increase the amount of the grant;

(e) to amend the Liquor Control Reform Act 1998 to provide for the delegation of certain powers by the Treasurer to the Commissioner of State Revenue;

(f) to amend the Payroll Tax Act 2007 in relation to the contractor and owner-driver exemption provisions;

(g) to amend the Taxation Administration Act 1997 in relation to staffing, delegation and disclosure of information;

(h) to amend the Water Act 1989 so that certain functions can be performed by the Commissioner of State Revenue.

2 Commencement (1) This Act (except Part 2, sections 13 and 27 and

Parts 5 and 7) comes into operation on the day after the day on which it receives the Royal Assent.

s. 2

Part 1—Preliminary

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

3

(2) Section 27 is taken to have come into operation on 1 July 2012.

(3) Section 13 is taken to have come into operation on 8 May 2013.

(4) Parts 5 and 7 come into operation on 1 July 2013.

(5) Part 2 comes into operation on 1 January 2014.

__________________

s. 2

Part 2—Congestion Levy Act 2005

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

4

PART 2—CONGESTION LEVY ACT 2005

3 Purpose In section 1 of the Congestion Levy Act 2005, omit "long stay".

4 Definitions (1) In section 3(1) of the Congestion Levy Act

2005—

(a) in the definition of leviable parking space, omit "long stay";

(b) the definition of long stay parking space is repealed.

(2) Section 4 of the Congestion Levy Act 2005 is repealed.

5 Amount of levy (1) In section 10(3) of the Congestion Levy Act

2005, after "subsequent year" insert "up to and including 2013".

(2) After section 10(3) of the Congestion Levy Act 2005 insert—

"(3A) The amount of the levy for 2014 is $1300 for each leviable parking space.

s. 3

See: Act No. 74/2005. Reprint No. 1 as at 17 October 2012 and amending Act No. 13/2013. LawToday: www. legislation. vic.gov.au

Part 2—Congestion Levy Act 2005

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

5

(3B) The amount of the levy for 2015 and each subsequent year is the CPI adjusted levy for that year for each leviable parking space.".

6 How is levy assessed At the foot of section 13 of the Congestion Levy Act 2005 insert— "Note

See section 40 for the application of this section to the levy for 2014.".

7 Statutory ratio repealed Sections 14 and 15 of the Congestion Levy Act 2005 are repealed.

8 Exemptions (1) In sections 16(1) and 17(1) of the Congestion

Levy Act 2005, omit "set aside or".

(2) For section 17(2) of the Congestion Levy Act 2005 substitute—

"(2) A parking space is an exempt parking space if—

(a) it is owned by or leased to a hospital; and

(b) it is used exclusively for the parking of a motor vehicle by a person while a patient of the hospital or while visiting or accompanying a patient of the hospital.".

s. 6

Part 2—Congestion Levy Act 2005

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

6

9 New section 20 substituted For section 20 of the Congestion Levy Act 2005 (including the example at the foot of the section) substitute—

"20 Parking for people attending special events A parking space is an exempt parking space if—

(a) it is used exclusively for the parking, without charge, of a motor vehicle in conjunction with a particular event; and

(b) at all other times it is not available for the parking of a motor vehicle.".

10 Further exemptions In sections 22, 23 and 24 of the Congestion Levy Act 2005, omit "set aside or".

11 Part year concession for parking spaces in a public car park

In section 26 of the Congestion Levy Act 2005—

(a) in subsection (2), omit ", taking into account the statutory ratio for the public car park under section 14 or 15 (as the case may be)";

(b) for the example at the foot of subsection (2) substitute— "Example

A parking space in a public car park comes into existence on 1 June 2014 and remains a parking space for the rest of 2014 except for the month of September, when it is used as a loading bay. Therefore, the space did not exist, or was exempt, for a total of 6 months in 2014, or half the year, and the levy for 2015 in respect of the space is reduced by half.".

s. 9

Part 2—Congestion Levy Act 2005

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

7

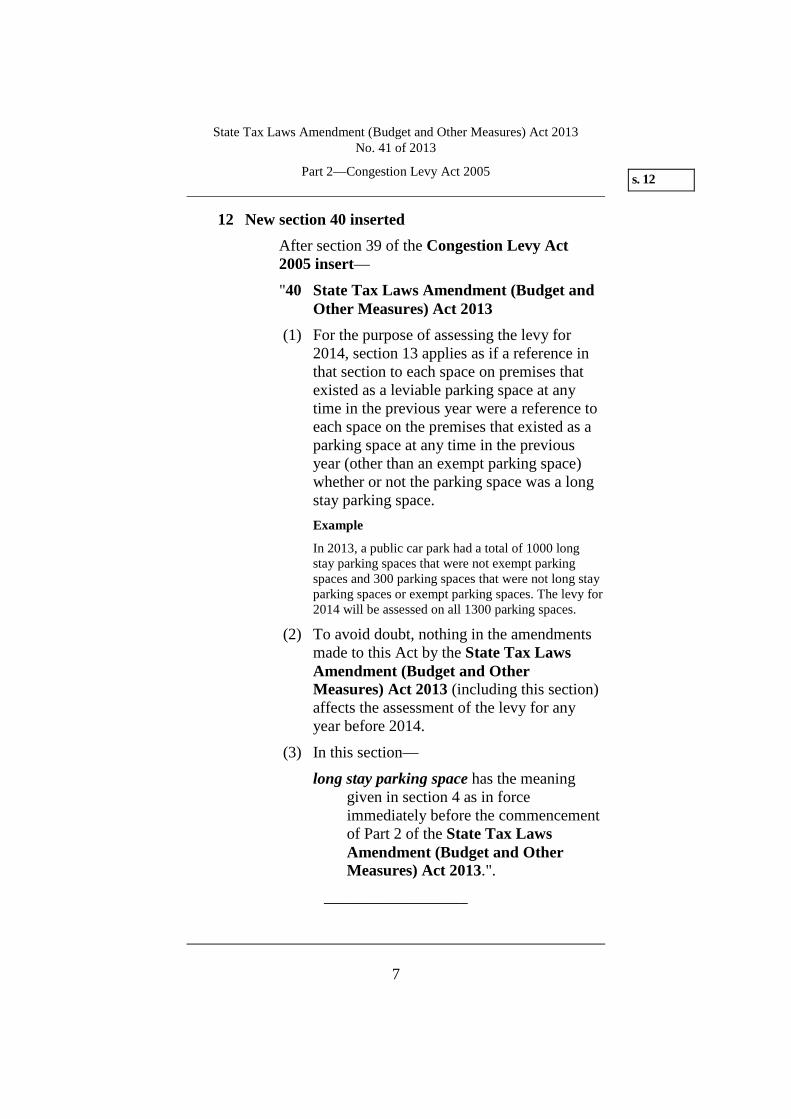

12 New section 40 inserted After section 39 of the Congestion Levy Act 2005 insert—

"40 State Tax Laws Amendment (Budget and Other Measures) Act 2013

(1) For the purpose of assessing the levy for 2014, section 13 applies as if a reference in that section to each space on premises that existed as a leviable parking space at any time in the previous year were a reference to each space on the premises that existed as a parking space at any time in the previous year (other than an exempt parking space) whether or not the parking space was a long stay parking space. Example

In 2013, a public car park had a total of 1000 long stay parking spaces that were not exempt parking spaces and 300 parking spaces that were not long stay parking spaces or exempt parking spaces. The levy for 2014 will be assessed on all 1300 parking spaces.

(2) To avoid doubt, nothing in the amendments made to this Act by the State Tax Laws Amendment (Budget and Other Measures) Act 2013 (including this section) affects the assessment of the levy for any year before 2014.

(3) In this section—

long stay parking space has the meaning given in section 4 as in force immediately before the commencement of Part 2 of the State Tax Laws Amendment (Budget and Other Measures) Act 2013.".

__________________

s. 12

Part 3—Duties Act 2000

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

8

PART 3—DUTIES ACT 2000

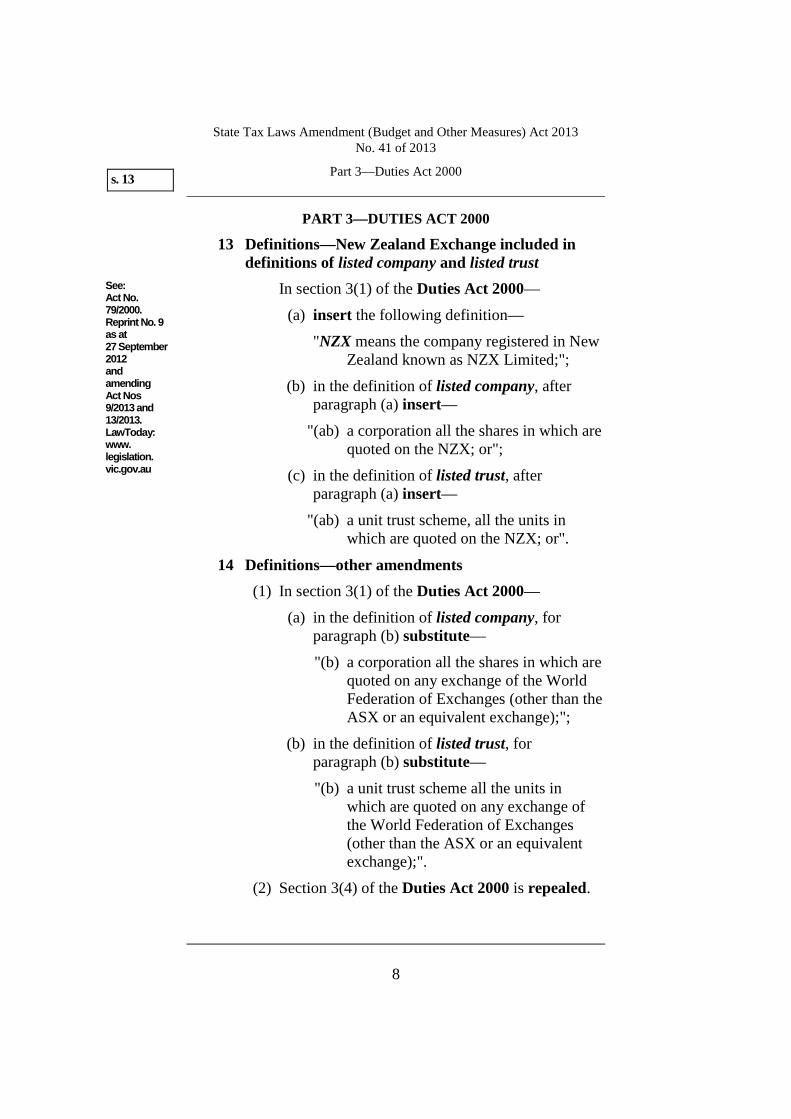

13 Definitions—New Zealand Exchange included in definitions of listed company and listed trust

In section 3(1) of the Duties Act 2000—

(a) insert the following definition—

"NZX means the company registered in New Zealand known as NZX Limited;";

(b) in the definition of listed company, after paragraph (a) insert—

"(ab) a corporation all the shares in which are quoted on the NZX; or";

(c) in the definition of listed trust, after paragraph (a) insert—

"(ab) a unit trust scheme, all the units in which are quoted on the NZX; or".

14 Definitions—other amendments (1) In section 3(1) of the Duties Act 2000—

(a) in the definition of listed company, for paragraph (b) substitute—

"(b) a corporation all the shares in which are quoted on any exchange of the World Federation of Exchanges (other than the ASX or an equivalent exchange);";

(b) in the definition of listed trust, for paragraph (b) substitute—

"(b) a unit trust scheme all the units in which are quoted on any exchange of the World Federation of Exchanges (other than the ASX or an equivalent exchange);".

(2) Section 3(4) of the Duties Act 2000 is repealed.

s. 13

See: Act No. 79/2000. Reprint No. 9 as at 27 September 2012 and amending Act Nos 9/2013 and 13/2013. LawToday: www. legislation. vic.gov.au

Part 3—Duties Act 2000

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

9

15 Definition of eligible first home buyer in section 57G repealed

In section 57G(1) of the Duties Act 2000, the definition of eligible first home buyer is repealed.

16 What is a PPR transfer? In section 57I(1)(d) of the Duties Act 2000 omit "more than $130 000 but".

17 Concessional rate of duty for certain PPR transfers In the note at the foot of section 57J of the Duties Act 2000, for "more than $550 000 but not more than $600 000" substitute "not more than $130 000, or more than $500 000 but not more than $600 000,".

18 Section 57JA substituted For section 57JA of the Duties Act 2000 substitute—

"57JA Reduction of duty for certain first home buyers on PPR transfers

(1) This section applies to—

(a) a transferee to whom a first home owner grant is paid or payable under section 7 of the First Home Owner Grant Act 2000; or

(b) a transferee of an existing home to whom a first home owner grant would be payable under section 7 of the First Home Owner Grant Act 2000 if the home were a new home within the meaning of that Act.

(2) The duty chargeable on a PPR transfer to a transferee to whom this section applies calculated under section 28(1) or 57J is to be reduced by the following percentages—

s. 15

Part 3—Duties Act 2000

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

10

(a) where the dutiable transaction takes place on or after 1 July 2011 and on or before 31 December 2012—20%;

(b) where the dutiable transaction takes place on or after 1 January 2013 and on or before 30 June 2013—30%;

(c) where the dutiable transaction takes place on or after 1 July 2013 and on or before 31 August 2014—40%;

(d) where the dutiable transaction takes place on or after 1 September 2014—50%.".

19 Exemption or concession for young farmers In section 69AD(1)(d)(i) of the Duties Act 2000, for "$400 000" substitute "$750 000".

20 Section 69AE substituted For section 69AE of the Duties Act 2000 substitute—

"69AE Calculation of exemption or concession on transfer of single parcel of land or partial interest in single parcel of land

(1) This section applies for the purposes of section 69AD in the case of one transfer of dutiable property.

(2) If the dutiable value of the dutiable property does not exceed $600 000, the young farmer or young farmer business entity (as the case requires) is entitled to an exemption from duty in respect of $300 000 of the dutiable value of the dutiable transaction. Examples

1 A young farmer enters into a dutiable transaction with a dutiable value of $275 000. No duty is payable as the young farmer is entitled to an

s. 19

Part 3—Duties Act 2000

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

11

exemption in respect of the whole dutiable value (as it is less than $300 000).

2 A young farmer enters into a dutiable transaction with a dutiable value of $550 000. The young farmer is entitled to an exemption from duty in respect of $300 000 of the dutiable value. For the purposes of assessing the young farmer's duty liability, duty is chargeable at the rate set out in section 28(1) on a dutiable transaction of $550 000 and reduced by the amount of duty that would be chargeable on a dutiable transaction of $300 000.

(3) If the dutiable value of the dutiable property exceeds $600 000 but does not exceed $750 000, the young farmer or young farmer business entity (as the case requires) is entitled to a concession from duty of an amount calculated in accordance with the following formula—

1307P$65 35015 000

−

where P is the dutiable value of the dutiable property.".

21 What is a relevant acquisition? In section 78(4) of the Duties Act 2000, for "acquisitions" substitute "the acquisition or holding".

22 Acquisition of economic entitlement In section 81(5) of the Duties Act 2000 omit "in a private landholder".

s. 21

Part 3—Duties Act 2000

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

12

23 Conversion of a private unit trust scheme into a public unit trust scheme

In section 89B(3) of the Duties Act 2000, for "acquisition of the last interest under the agreement or arrangement" substitute "date on which the private unit trust scheme became a public unit trust scheme".

24 Conversion of a private company to a listed company

In section 89C(3) of the Duties Act 2000, for "acquisition of the last interest under the agreement or arrangement" substitute "date on which the private company became a listed company".

25 Definitions—Registration of unit trust schemes In section 89P(2) of the Duties Act 2000, for "paragraph (f)" substitute "paragraph (g)".

26 Private vehicle used to convey incapacitated person (1) In section 233C(1) of the Duties Act 2000—

(a) in paragraph (b), for "minor." substitute "minor; or";

(b) after paragraph (b) insert—

"(c) a person who is a relative of or a carer for an incapacitated person.".

(2) After section 233C(2) of the Duties Act 2000 insert—

"(3) In this section—

carer has the same meaning as in the Carers Recognition Act 2012.".

s. 23

Part 3—Duties Act 2000

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

13

27 Transitional provision—Duties Amendment (Landholder) Act 2012

After clause 31(7) of Schedule 2 to the Duties Act 2000 insert—

"(7A) An acquisition by a person before 1 July 2009 of an interest in a private unit trust scheme, private company, wholesale unit trust scheme or public unit trust scheme that was not land rich under this Act as in force on the date of that acquisition is not to be taken into account in determining whether an acquisition on or after 1 July 2012 of an interest in the scheme or company is a relevant acquisition of a further interest under section 78(1)(b).".

__________________

s. 27

Part 4—Fire Services Property Levy Act 2012

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

14

PART 4—FIRE SERVICES PROPERTY LEVY ACT 2012

28 New section 8 substituted For section 8 of the Fire Services Property Levy Act 2012 substitute—

"8 Property that is subject to the levy The levy is assessable on all land other than land referred to in section 10. Note

Land specified in this section is leviable land—see section 3.".

29 Treatment of parcels of land for levy purposes (1) For the heading to section 9 of the Fire Services

Property Levy Act 2012 substitute—

"How parcels of land are treated for levy purposes".

(2) For section 9(1) of the Fire Services Property Levy Act 2012 substitute—

"(1) This section sets out how parcels of land are to be treated for the purpose of assessing the levy.".

(3) For section 9(8) of the Fire Services Property Levy Act 2012 substitute—

"(8) A collection agency must separately assess the levy in respect of each parcel or portion of a parcel of land for which the collection agency has a separate valuation.".

(4) Section 9(9), (10), (11) and (12) of the Fire Services Property Levy Act 2012 are repealed.

s. 28

See: Act No. 58/2012 and amending Act Nos 58/2012 and 81/2012. LawToday: www. legislation. vic.gov.au

Part 4—Fire Services Property Levy Act 2012

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

15

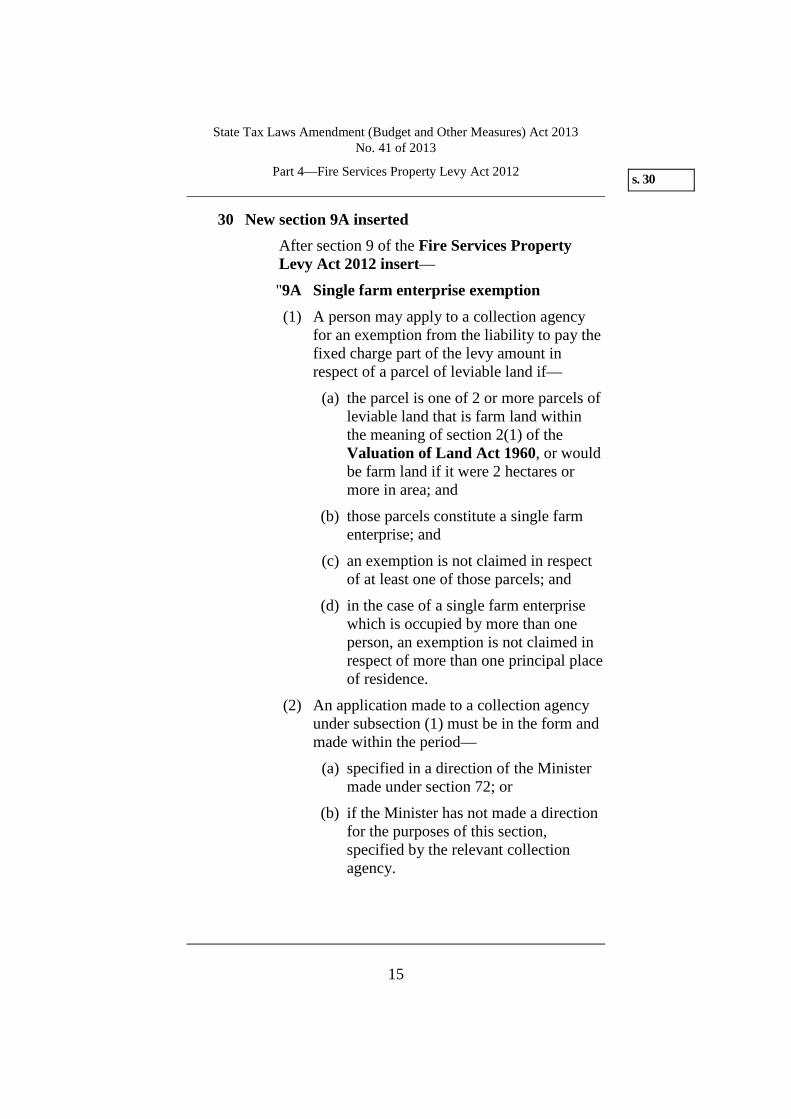

30 New section 9A inserted After section 9 of the Fire Services Property Levy Act 2012 insert—

"9A Single farm enterprise exemption (1) A person may apply to a collection agency

for an exemption from the liability to pay the fixed charge part of the levy amount in respect of a parcel of leviable land if—

(a) the parcel is one of 2 or more parcels of leviable land that is farm land within the meaning of section 2(1) of the Valuation of Land Act 1960, or would be farm land if it were 2 hectares or more in area; and

(b) those parcels constitute a single farm enterprise; and

(c) an exemption is not claimed in respect of at least one of those parcels; and

(d) in the case of a single farm enterprise which is occupied by more than one person, an exemption is not claimed in respect of more than one principal place of residence.

(2) An application made to a collection agency under subsection (1) must be in the form and made within the period—

(a) specified in a direction of the Minister made under section 72; or

(b) if the Minister has not made a direction for the purposes of this section, specified by the relevant collection agency.

s. 30

Part 4—Fire Services Property Levy Act 2012

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

16

(3) A collection agency may require an applicant for an exemption under this section to give further particulars, or to verify particulars, in respect of the person's application.

(4) A person who has made an application for, or who has been granted, an exemption under this section must advise all relevant collection agencies of any change in circumstances that could affect the person's eligibility for an exemption under this section.

(5) In this section—

single farm enterprise means 2 or more parcels of leviable land—

(a) which—

(i) are farm land; and

(ii) are farmed as a single enterprise; and

(iii) are occupied by the same person or persons—

whether or not the parcels of land are contiguous or are located in the same municipal district; or

(b) which—

(i) as to all the properties except one, are farm land farmed as a single enterprise occupied by the same person or persons; and

(ii) as to one property contiguous with at least one of the other properties, is the principal place of residence

s. 30

Part 4—Fire Services Property Levy Act 2012

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

17

of that person or one of those persons.".

31 Land that is not subject to the levy (1) In section 10(1) of the Fire Services Property

Levy Act 2012—

(a) in paragraph (a), for "or licensed to any person" substitute ", subleased, licensed or sublicensed to any person other than the Commonwealth or a public body";

(b) after paragraph (b) insert—

"(ba) land owned by the Director of Housing that is leased to an individual or registered agency for the purpose of public housing;

(bb) land leased to the Director of Housing by the Crown, a public body or the Commonwealth that is subleased to an individual or registered agency for the purpose of public housing;".

(2) In section 10(2) of the Fire Services Property Levy Act 2012—

(a) insert the following definitions—

"Director of Housing means the body corporate established under section 9 of the Housing Act 1983;

public housing has the same meaning as in the Housing Act 1983;

registered agency has the same meaning as in the Housing Act 1983.";

(b) in the definition of public body, in paragraph (b), for "section." substitute "section;".

s. 31

Part 4—Fire Services Property Levy Act 2012

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

18

32 Determination of levy rates (1) After section 12(5) of the Fire Services Property

Levy Act 2012 insert—

"(6) If the Minister does not determine and specify a levy rate by 31 May for the next levy year, the levy rate for the next levy year is the most recent levy rate set by the Minister.".

(2) Section 14(2) of the Fire Services Property Levy Act 2012 is repealed.

33 Councils to pay only fixed charge in respect of specified leviable land

After section 20(1)(c)(ix) of the Fire Services Property Levy Act 2012 insert—

"(ixa) 980–988;".

34 Revised assessment of liability to pay levy amount For section 39(4) of the Fire Services Property Levy Act 2012 substitute—

"(4) If an amount to be refunded under subsection (3) is not refunded within 28 days after the day on which the valuer-general certifies the supplementary valuation to be correct (the supplementary valuation day), interest accrues daily, at the rate specified in section 30(2)(a), from and including the 29th day after the supplementary valuation day until the day the owner is paid the amount to be refunded.".

35 Delegation In section 45 of the Fire Services Property Levy Act 2012, after "of the Commissioner," insert "any function of the Commissioner under this Act,".

s. 32

Part 4—Fire Services Property Levy Act 2012

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

19

36 Permitted disclosures to particular persons In section 65 of the Fire Services Property Levy Act 2012—

(a) omit "(1)";

(b) after paragraph (d)(v) insert—

"(va) the Monitor within the meaning of the Fire Services Levy Monitor Act 2012;".

__________________

s. 36

Part 5—First Home Owner Grant Act 2000

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

20

PART 5—FIRST HOME OWNER GRANT ACT 2000

37 Extension of residence requirement (1) In section 3(1) of the First Home Owner Grant

Act 2000, in the definition of residence requirement, for "6 months" substitute "12 months".

(2) In section 8(2)(a) of the First Home Owner Grant Act 2000, for "6 months" substitute "12 months".

(3) In section 12(1) of the First Home Owner Grant Act 2000, for "6 months" substitute "12 months".

(4) In section 12(2) of the First Home Owner Grant Act 2000, for "6 months" substitute "12 months".

(5) In section 20(1) of the First Home Owner Grant Act 2000, for "6 months" substitute "12 months".

(6) In section 22(3) of the First Home Owner Grant Act 2000, for "6 months" substitute "12 months".

38 Definitions In section 3(1) of the First Home Owner Grant Act 2000 insert the following definitions—

"new home means a home that is a new residential premises;

new residential premises has the same meaning as in section 40–75 of the A New Tax System (Goods and Services Tax) Act 1999 of the Commonwealth;".

39 Eligible transaction (1) In section 13(1)(a) of the First Home Owner

Grant Act 2000, after "1 July 2000" insert "and before 1 July 2013".

s. 37

See: Act No. 5/2000. Reprint No. 3 as at 6 May 2010 and amending Act Nos 36/2010 and 28/2011. LawToday: www. legislation. vic.gov.au

Part 5—First Home Owner Grant Act 2000

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

21

(2) After section 13(1)(a) of the First Home Owner Grant Act 2000 insert—

"(ab) a contract made on or after 1 July 2013 for the purchase of a new home in the State;".

40 Special eligible transactions Section 13A(3) of the First Home Owner Grant Act 2000 is repealed.

41 Amount of grant (1) In section 18(1) of the First Home Owner Grant

Act 2000, for "The amount" substitute "If the commencement date of an eligible transaction is before 1 July 2013, the amount".

(2) After section 18(1) of the First Home Owner Grant Act 2000 insert—

"(1A) If the commencement date of an eligible transaction is on or after 1 July 2013, the amount of a first home owner grant is the lesser of the following—

(a) the consideration for the eligible transaction;

(b) $10 000.".

(3) After section 18(4B) of the First Home Owner Grant Act 2000 insert—

"(4C) Despite anything to the contrary in subsection (1) or (1A), the amount of a first home owner grant is the amount referred to in subsection (1) if the Commissioner is satisfied that the contract that formed the basis of the eligible transaction replaces a contract made before 1 July 2013 (the earlier contract), and the earlier contract was—

(a) a contract for the purchase of the same home; or

s. 40

Part 5—First Home Owner Grant Act 2000

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

22

(b) a comprehensive home building contract to build the same or a substantially similar home.".

(4) In section 18(8) of the First Home Owner Grant Act 2000, the definition of new residential premises is repealed.

42 Protection of confidential information After section 50(4)(ca)(iv) of the First Home Owner Grant Act 2000 insert—

"(v) the Legal Services Board; or

(vi) the Legal Services Commissioner; or".

__________________

s. 42

Part 6—Liquor Control Reform Act 1998

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

23

PART 6—LIQUOR CONTROL REFORM ACT 1998

43 New section 178A inserted After section 178 of the Liquor Control Reform Act 1998 insert—

"178A Delegation (1) The Treasurer may delegate, by instrument,

to the Commissioner of State Revenue—

(a) a power of the Treasurer under section 177(1) or 178(1);

(b) the power to delegate a power delegated under paragraph (a).

(2) If power has been delegated under subsection (1)(b), the Commissioner of State Revenue may, subject to the terms of the instrument of delegation, sub-delegate, by instrument, to a member of staff of the State Revenue Office a power that is the subject of the delegation, other than the power of sub-delegation.

(3) Sections 42 and 42A of the Interpretation of Legislation Act 1984 apply in relation to a sub-delegation in the same manner as they apply in relation to a delegation.

(4) In this section—

member of staff of the State Revenue Office means—

(a) an employee referred to in section 67 of the Taxation Administration Act 1997; or

(b) a consultant or contractor engaged under section 68 of that Act.".

__________________

s. 43

See: Act No. 94/1998. Reprint No. 7 as at 1 May 2013 and amending Act No. 9/2013. LawToday: www. legislation. vic.gov.au

Part 7—Payroll Tax Act 2007

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

24

PART 7—PAYROLL TAX ACT 2007

44 Relevant contracts (1) In section 32(2)(c) of the Payroll Tax Act 2007—

(a) in subparagraph (iii), for "carried on by the contractor—" substitute "carried on by the contractor; or";

(b) omit "unless the Commissioner determines that the contract or arrangement under which the services are so supplied was entered into with an intention either directly or indirectly of avoiding or evading the payment of tax by any person; or".

(2) In section 32(2)(d) of the Payroll Tax Act 2007—

(a) in subparagraph (i), after "services" insert "solely for or";

(b) in subparagraph (iii), for "person—" substitute "person.";

(c) omit "unless the Commissioner determines that the contract or arrangement under which the services are so supplied was entered into with an intention either directly or indirectly of avoiding or evading the payment of tax by any person.".

(3) After section 32(2) of the Payroll Tax Act 2007 insert—

"(2A) Subsection (2)(a), (2)(b)(i), (2)(b)(iv) or (2)(d) does not apply to a contract under which services not referred to in that subsection are supplied in addition to services referred to in that subsection.

s. 44

See: Act No. 26/2007. Reprint No. 1 as at 20 May 2010 and amending Act Nos 36/2010, 28/2011, 29/2011, 69/2011 and 13/2013. LawToday: www. legislation. vic.gov.au

Part 7—Payroll Tax Act 2007

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

25

(2B) Subsection (2)(b)(ii) or (iii) does not apply to—

(a) a contract under which services not referred to in that subsection are supplied in addition to services referred to in that subsection; or

(b) a contract under which services referred to in that subsection are provided for a period exceeding a period referred to in that subsection.

(2C) Subsection (2)(c) does not apply to a contract under which work is performed in a manner other than a manner referred to in that subsection, in addition to work performed in a manner referred to in that subsection.

(2D) Subsection (2) does not apply if the Commissioner determines that the contract under which the services are supplied was entered into with an intention either directly or indirectly of avoiding or evading the payment of tax by any person.".

45 Transitional provision After clause 17 of Schedule 3 to the Payroll Tax Act 2007 insert—

"18 State Tax Laws Amendment (Budget and Other Measures) Act 2013

(1) Section 32, as amended by section 44 of the State Tax Laws Amendment (Budget and Other Measures) Act 2013, applies in respect of work performed on or after 1 July 2013 irrespective of when amounts are paid or become payable in respect of the work.

(2) Section 32 as in force immediately before the commencement of section 44 of the State Tax Laws Amendment (Budget and Other

s. 45

Part 7—Payroll Tax Act 2007

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

26

Measures) Act 2013 continues to apply in respect of work performed before 1 July 2013 irrespective of when amounts are paid or become payable in respect of the work.".

__________________

s. 45

Part 8—Taxation Administration Act 1997

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

27

PART 8—TAXATION ADMINISTRATION ACT 1997

46 Section 66 substituted For section 66 of the Taxation Administration Act 1997 substitute—

"66 Deputy and Assistant Commissioners (1) Any Deputy or Assistant Commissioners of

State Revenue may be employed under Part 3 of the Public Administration Act 2004 who are necessary for—

(a) the administration and execution of taxation laws and other laws under the general administration of the Commissioner; or

(b) the performance of other functions of the Commissioner.

(2) A Deputy or an Assistant Commissioner has the same functions as the Commissioner under a taxation law or any other law.".

47 Section 67 substituted For section 67 of the Taxation Administration Act 1997 substitute—

"67 Other staff Any other employees may be employed under Part 3 of the Public Administration Act 2004 who are necessary for—

(a) the administration and execution of taxation laws and other laws under the general administration of the Commissioner; or

(b) the performance of other functions of the Commissioner.".

s. 46

See: Act No. 40/1997. Reprint No. 5 as at 13 October 2011 and amending Act Nos 69/2011, 76/2012 and 13/2013. LawToday: www. legislation. vic.gov.au

Part 8—Taxation Administration Act 1997

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

28

48 Section 69 substituted For section 69 of the Taxation Administration Act 1997 substitute—

"69 Delegation by the Commissioner The Commissioner, by instrument, may delegate any function of the Commissioner, other than this power of delegation, to—

(a) an employee referred to in section 67; or

(b) a consultant or contractor engaged under section 68.".

49 Permitted disclosures to particular persons or for particular purposes

Insert the following heading to section 92 of the Taxation Administration Act 1997—

"Permitted disclosures to particular persons or for particular purposes".

50 New section 92A inserted After section 92 of the Taxation Administration Act 1997 insert—

"92A Permitted disclosures—dutiable transactions in relation to land

(1) Despite section 92, a tax officer may disclose the minimum information about a dutiable transaction under Chapter 2 of the Duties Act 2000 that is necessary to enable a person to ascertain—

(a) whether duty has been paid or is payable on the dutiable transaction;

(b) the amount of duty that has been paid or is payable on the dutiable transaction;

s. 48

Part 8—Taxation Administration Act 1997

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

29

(c) the basis on which duty was or was not paid, or is or is not payable.

(2) Without limiting subsection (1), a tax officer may disclose the following information—

(a) a reference number allocated to a dutiable transaction by the Commissioner;

(b) the name of a party who lodged a written instrument or statement with the Commissioner in relation to a dutiable transaction;

(c) the date on which an amount of duty was paid;

(d) whether the Commissioner has estimated the amount of duty that is payable on a dutiable transaction;

(e) whether a taxpayer is entitled to a refund of tax in relation to a dutiable transaction;

(f) whether there has been a reassessment of a tax liability in relation to a dutiable transaction.".

51 Permitted disclosures to particular persons (1) In section 92(1)(e)(vi) of the Taxation

Administration Act 1997, for "Authority." substitute "Authority; or".

(2) After section 92(1)(e)(vi) of the Taxation Administration Act 1997 insert—

"(vii) the Legal Services Board; or

(viii) the Legal Services Commissioner; or".

__________________

s. 51

Part 9—Water Act 1989

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

30

PART 9—WATER ACT 1989

52 Waiver of service charges After section 283(3B) of the Water Act 1989 insert—

"(3BA) An Order under subsection (3B) may—

(a) confer a discretionary authority or impose a duty on the Commissioner of State Revenue; and

(b) require any matter affected by the Order to be approved by or to the satisfaction of the Commissioner of State Revenue.".

53 Reimbursement by State (1) After section 284(1) of the Water Act 1989

insert—

"(1A) The Commissioner of State Revenue may pay any amounts required to be reimbursed under subsection (1).".

(2) In section 284(2) of the Water Act 1989—

(a) after "1994" insert "or the Commissioner of State Revenue";

(b) after "subsection (1)" insert "or (1A)".

__________________

s. 52

See: Act No. 80/1989. Reprint No. 10 as at 1 January 2011 and amending Act Nos 50/2010, 29/2011, 50/2011, 63/2011, 17/2012, 4/2013, 22/2013 and 24/2013. LawToday: www. legislation. vic.gov.au

Part 10—Repeal of Amending Act

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

31

PART 10—REPEAL OF AMENDING ACT

54 Repeal of amending Act This Act is repealed on 1 January 2015.

Note

The repeal of this Act does not affect the continuing operation of the amendments made by it (see section 15(1) of the Interpretation of Legislation Act 1984).

═══════════════

s. 54

State Tax Laws Amendment (Budget and Other Measures) Act 2013 No. 41 of 2013

32

ENDNOTES

† Minister's second reading speech—

Legislative Assembly: 8 May 2013

Legislative Council: 13 June 2013

The long title for the Bill for this Act was "A Bill for an Act to amend the Congestion Levy Act 2005, the Duties Act 2000, the Fire Services Property Levy Act 2012, the First Home Owner Grant Act 2000, the Liquor Control Reform Act 1998, the Payroll Tax Act 2007, the Taxation Administration Act 1997 and the Water Act 1989 and for other purposes."

Endnotes