State of the Clean Cooking Energy Sector in Sub-Saharan...

52

Slides for ACCI Report THE WORLD BANK State of the Clean Cooking Energy Sector in Sub-Saharan Africa November 16, 2012 DRAFT FOR DISCUSSION

Transcript of State of the Clean Cooking Energy Sector in Sub-Saharan...

Slides for ACCI Report

THE WORLD BANK

State of the Clean Cooking Energy Sector in Sub-Saharan Africa

November 16, 2012

DRAFT FOR DISCUSSION

What do we mean by clean and improved cooking solutions?

What’s included?

Potential benefits

What is it?

Basic ICS Intermediate ICS Advanced ICS Modern fuels

Small functional improvements over baseline technologies; typically made from local materials by local artisans or self-built

Improved efficiency of combustion of fuel and emission gases, typically with rocket principles and (often) higher end materials.

Gasifier biomass stoves using natural draft principles or with fans, some biochar producing; emerging TEG/charging features.

• LPG

• Electricity

• Kerosene

• Natural gas

High

Renewable fuels

• Biogas digesters

• Biofuels / ethanol

• Solar / retained heat cookers

• Briquettes/Pellets

• Legacy chimney

• Basic efficient wood

• Basic effic. charcoal

• Portable wood rocket

• Fixed rocket chimney

• Highly improved charcoal stoves

• Natural draft gasifier (TLUD or sideload)

• TChar stoves

• Fan gasifiers / fan jet

Non-biomass stoves relying on liquid / gas fossil fuels or electricity.

Sustainable fuel or stove solutions that rely on renewable energy sources. Often part of stove/fuel system.

ISO tier 1 ISO tier 1-2 ISO tier 3 ISO tier 3-4 ISO tier 3-4

IMPROVED SOLUTIONS CLEAN COOKING ENERGY

Moderate High

2

• Solid fuel cooking by 700 million Africans imposes large and growing economic, health, and environmental costs on the region, with a disproportionate impact on women

• Strong and growing evidence that clean fuels and improved stoves can mitigate these costs, save lives, and improve environmental sustainability, but mitigation potential varies by technology

• The potential market is large, but only ~17% of African households rely on clean cooking solutions and, including all non-legacy ICS, penetration of clean and improved stoves and fuels is under 25%

• The convergence of several new demand, supply, and enabling environment trends suggests that the next decade will bring major progress in access to improved cooking energy

• The business as usual scenario for 2020 is encouraging, but still leaves >60% of Africans behind, potential health and environmental benefits largely unrealized, and energy poverty gaps growing

• Key barriers to uptake and use of clean energy include affordability, consumer behavior, distribution to last mile, producer technical capacity, A2F, product quality, and policy constraints

• Faster and more equitable growth is possible via a targeted focus on affordability, consumer education, access to quality products, and investment in sustainable fuel/stove value chains

Executive summary

3

The Case for Clean and Improved Cooking Energy

Sub-Saharan Africa has the highest rate of solid fuel reliance globally

Percentage of developing world population relying on solid fuels by region

6 94

8 92

28 72

48 52

29 71

63 37

Solid fuels Modern fuels

31 69

58 42

71 29

81 19

88 12

95 5

Eastern Europe & Central Asia 83

Latin America & Car.

17

19 81

South-East Asia 53 47

South Asia 71 29

Sub-Saharan Africa 82 18

65 35 East Asia

Total population Rural population Urban population

Source: Dalberg fuel use database drawing on WHO Global Health Observatory Data Repository, DHS, MICS, LSMS, National Census. Uses latest year known (2005-2012) rather than parametric forecast model for missing datapoints. 5

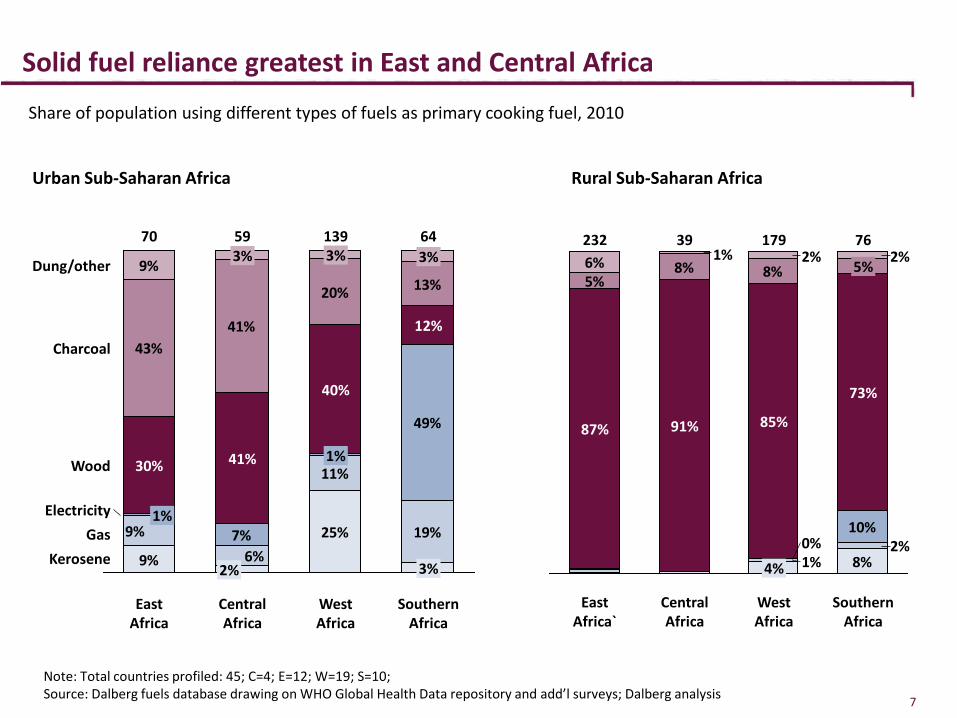

Solid fuel reliance greatest in East and Central Africa

8% 8%

8%2%

1%

10%0%

5%2%1%6% 2%

Central Africa

91%

39

East Africa`

232

87%

West Africa

Southern Africa

85%

179

4%

5%

73%

76

Share of population using different types of fuels as primary cooking fuel, 2010

Note: Total countries profiled: 45; C=4; E=12; W=19; S=10; Source: Dalberg fuels database drawing on WHO Global Health Data repository and add’l surveys; Dalberg analysis

Rural Sub-Saharan Africa

7

25%7%

49%

43%41%

20% 13%

9% 6%9% 19%

11%

9%

Kerosene Gas

Electricity

Wood

64

3%

12%

3% 3%

41%

2%

59

Southern Africa

3% 70

East Africa

30%

1%

West Africa

Charcoal

Dung/other

139

Central Africa

40%

1%

Urban Sub-Saharan Africa

SSA solid fuel dependence will continue to grow quickly

Number of people living in households where the primary fuel is solid fuel (in Millions)

271 287 276

759 840 864 880

1,0511,140 1,144 1,116

252

2000

2,714

546

South East Asia

2015 F

East Asia

884

South Asia

3,150

2020 F

78

Lat Am & Carribean

SSA

3,209

80

787

2010

3,049

82

700

87

∆ 2010-2020 (millions)

+ 184

- 24

+ 40

- 35 - 5

1 Not modeled but known as an important potential driver Source: 2000-2010 data based on Dalberg fuel mix database; projection based on inertial penetration trends for underlying fuels from 2000-2010, adjusted for changes in population and urban/rural mix

Fuel mix drivers • Population growth

• Urbanization

• Inertial modern fuel adoption trends

• Incomes1

• Price differential between fuels1

• Gov’t policy changes1

12

Costs of traditional cooking significant, but improved solutions can help

13

Economics & livelihoods

SSA traditional cooking Mitigation potential via new solutions

Health

Environment

Gender and other social

Stat

e of

our

kno

wle

dge

• USD 50 bn opportunity cost across quantifiable health, environment, and economic impacts\

• 24bn to 41bn growth in fuel spend projected by 2020

• 3-20%+ share of monthly HH expenditure

• Time loss of >40 mn person years

• 12-17 mn jobs in woodfuel value chains

• Strong real world evidence for fuel and time savings (30-80%) depending on solution

• Theoretical impact of clean energy is labor saving, but net impact on jobs likely limited due to demand growth

• Add’l livelihood benefits due to ICS/clean fuel jobs and saved time for income generation (15-35%)

• 570-680k deaths and 18-22 mn DALYS for COPD/ALRI alone due to solid fuel cooking

• Significant unquantified impacts from other IAP-related illnesses, burns, firewood collection, and lifestyle nuisances (e.g., eye irritation)

• Hardest benefit to capture due to steep dose-response curve, behavioral changes needed, long lag time

• 25-60% IAP upper respiratory illness reduction from best-in-class solutions, most other impacts not yet clear

• 120-380 MT CO2 Kyoto GHG (~1% of global)

• Major source of BC emissions (6% ) resulting in local climate changes and potential global warming impact

• Charcoal contributor to forest degradation, with possible local deforestation effects

• Strong theoretical impact case, but difficult to measure

• Little data as of yet on systemic impacts (e.g., total woodfuel demand, degradation, local outdoor pollution)

• Disproportionate impact on women and girls for health, time poverty, and economic wellbeing

• Education, nutrition, and aesthetic impact

• Good evidence for improved (self-reported) health and economic impacts for women and girls

• Evidence for improved VAW outcomes weak

• Nutrition, education, aesthetic impact largely anecdotal

Cooking fuels are a significant share of expenditures for the poor

Source: National household survey data (2000-2011) from multiple sources; Dalberg analysis

6.7%

South Africa

9.0%

Uganda

15.0%

3.0%

11.4%

5.8%

Ethiopia

10.0%

7.0%

Malaw

i

2.5%

20.0% Kenya

5.8% 6.0%

Angola 3.3%

1.8%

5.9% 4.6%

Ghana

Madagascar

Richest Poorest

5%

10%

Cooking and lighting fuel spending as share of total household expenditures (%)

Economic impact

14

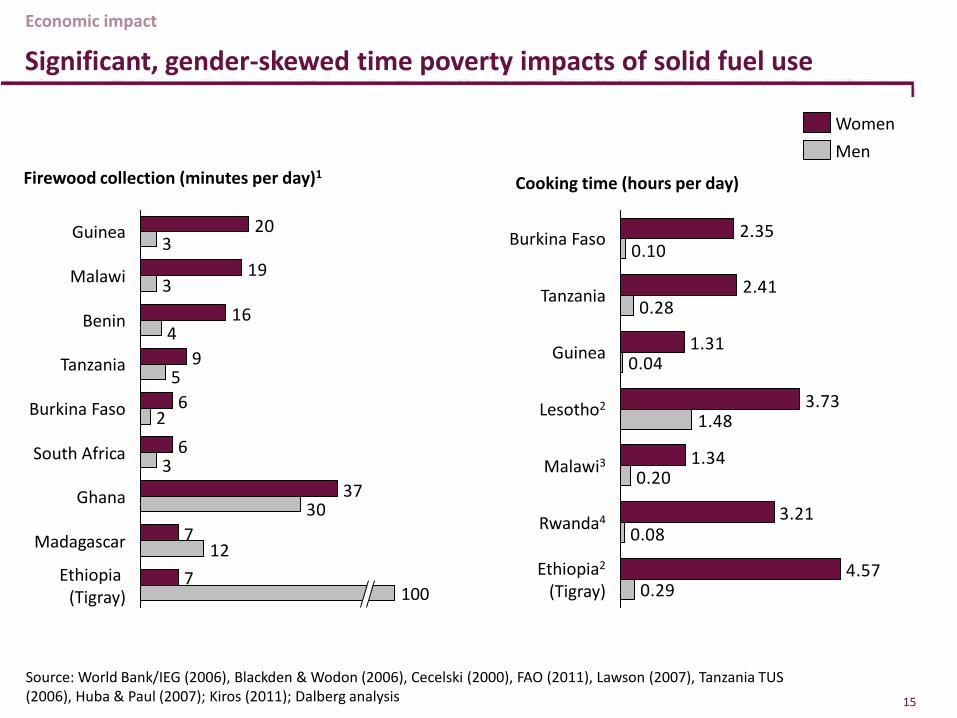

Significant, gender-skewed time poverty impacts of solid fuel use

7

7

37

6

6

9

16

19

20

12

30

3

2

5

4

3

3

Burkina Faso

Madagascar

Ghana

South Africa

Tanzania

Ethiopia (Tigray) 100

Benin

Malawi

Guinea

Men Women

Firewood collection (minutes per day)1 Cooking time (hours per day)

4.57

3.21

1.34

3.73

1.31

2.41

2.35

0.29

0.08

0.20

1.48

0.04

0.28

0.10

Malawi3

Lesotho2

Guinea

Tanzania

Burkina Faso

Ethiopia2

(Tigray)

Rwanda4

Source: World Bank/IEG (2006), Blackden & Wodon (2006), Cecelski (2000), FAO (2011), Lawson (2007), Tanzania TUS (2006), Huba & Paul (2007); Kiros (2011); Dalberg analysis

Economic impact

15

Solid fuel cooking is a fast growing public health crisis

1 Dalberg estimate applying 2004/2005 COPD/ALRI mortality ratio to 2010 solid fuel exposure 2 Pro-rated share of WHO/UNDP 2030 estimates using SSA region share of 2030 solid fuel population 3 Application of 2004/2005 ALRI/COPD mortality ratio from WHO to 2030 F solid fuel dependent population of 900 million Source: WHO, IEA, Dalberg IAP database; Dalberg analysis

Millions of deaths in Sub-Saharan Africa annually 2004-2030F

Solid fuel cooking-linked ALRI and COPD

.57

HIV/AIDS

.67

1.2

1.7

TB

.14 .25 .25

Malaria

.23

.6 .75 .702 .681

2004

2030 F

2010

.873

16

Health

BC emissions and forest degradation impacts could be substantial

1 Assumes fNRB of 90% for firewood and charcoal, share <0.5% if fNRB of 50% is used for charcoal and fNRB of 10% for firewood Source: Hosonuma et al (2012), SEI (2008), EPA (2011), Dalberg impact database, Dalberg analysis

GHG (Kyoto)

95%

4% 1%1

80%

SSA biomass cooking 6%

All other sources globally

14% SSA cooking In other regions

Black carbon

33%

6%

Timber logging

Sub-tropical Asia

Uncontrolled fires

74%

3% 9% 1%

16%

Lat. Am. Africa

8%

52%

Livestock grazing 12% 3%

Charcoal production / firewood collection

84%

Climate change contribution Cooking/charcoal production share of total, %

Drivers of forest degradation – not fully validated % attribution based on R-PIN proposal analyses

17

Environment

Woodfuel demand not the only challenge, supply is unsustainable and inefficient

SOURCE: AFREA (2011); WB (2011); Dalberg woodfuel value chain database; Dalberg analysis

Cross-cutting challenges

• Lack of sustainable forestry management, potentially leading to high rates of resource depletion and localized overharvesting

• Periodic charcoal bans mean that information on sector is limited and ability to influence sustainability is low

• High rates of informality account for 30-50% of end-price instead of being captured as tax revenue

• True economic costs of charcoal production not accounted for as wood seen as a “free” resource

• Disproportionate value capture by large transporters and wholesalers at expense of producers and retailers, especially women

Wood production and harvest Transport Charcoal

production Wholesale Retail

• Waste and GHG from poor efficiency kilns (8-20% vs. 25-40% potential)

• Low capacity

• Health hazards

• Oligopolistic control and often limited value for small transporters

• Significant informal payments

• Health hazards

• Significant informal payments

• Operate in shadow economy and cause tax revenue loss

• Unsustainable livelihoods due to capture of value by upstream intermediaries

• Weak forestry management

• Over-harvesting of “free” resource in public forests

• Land rights issues

Environment

18

Ethanol

Solar

Coal traditional

Biogas

Built-in rocket Portable

rocket

Natural draft gasifier Fan draft stove

Basic efficient wood

High-end charcoal 3 stone fire

Basic efficient charcoal

Kerosene

LPG

Traditional charcoal

Electric

Wide range of theoretical impacts depending on cooking solution

4 3 2 1 0

Health impact

Clim

ate

Impa

ct

Clean

Pollu

ting

Gree

n

1 Index on scale of 1-10 based on stove emissions of tons of GHG CO2-eq including all particles from fuel combustion and charcoal production weighted at GWC100; assumes fNRB of 0.5 2 Index on scale of 1-10 of daily PM 2.5 intake per person and CO mg/ m3 concentration, weighted 50/50 to capture both carbon monoxide and PM emissions health effects

Source: Berkeley Air Monitoring Stove Performance Inventory Report (October 2012); Grieshop et al (2011); Dalberg stove database; Dalberg analysis

185

Unhealthy

Mitigation potential of improved and clean solutions

19

DIRECTIONAL ONLY

State of the Sector

Reach of clean and improved cooking solutions

Reach (# HH)

Legacy & Basic ICS Intermediate ICS Advanced ICS Modern Renewable

IMPROVED CLEAN

21

LPG: 7.8 mn

Electricity: 9.5mn

Kerosene: 11.6 mn

• 150k (excluding 550k+ retained heat cookers)

Legacy: 8mn

Basic ICS: 7.6mn

>4 mn stoves ~50k stoves

Africa examples

Pima gas LPG (Kenya)

Arivi kerosene (S. Africa)

CleanStar (Moz.)

CookIt (multiple)

Inyeyeri (Rwanda)

Lorena chimney

Mud stove (Malawi)

KCJ (Kenya)

Rocket Lorena (Uganda)

Envirofit (multiple)

Jiko Poa (Kenya)

Ugastove (Uganda)

Philips Fan Stove

Awamu (Uganda)

Jiko Bomba (Tanzania)

Source: Press searches, interviews, program M&E data, Dalberg analysis

Clean and improved solutions are under a quarter of the SSA cooking market

Source: Dalberg SSA fue database; ICS penetration database with data for 45 SSA countries from national program, donor, CDM, and individual manufacturer data; WHO chimney stove penetration database; Global Alliance Market Assessments; Dalberg analysis

71%

5%

Traditional stove

Legacy ICS

Non-legacy ICS 7%

Modern 17%

Renewable

<1%

Primary cooking technology mix in Sub-Saharan Africa (2010) 100% = 171 million HH

DIRECTIONAL ESTIMATE

22

Technologies like retained heat cookers not includes as they are not primary stoves

Chimney stoves often not truly improved (Tier 0) but included in broad ICS definition for completeness

Largely basic and intermediate stoves, “Clean” ACS <0.1%,

Substantial but unknown (10-25%?) portion of ICS are actually used by modern fuel households

Basic ICS 7.6 mil

Charcoal artisanal jikos

Wood basic artisanal

Charcoal semi-industrial

>4.4

>2.5

>0.6

38% 17%

<0.1%

59%

Legacy and basic stoves dominate the improved biomass sector, but intermediate solutions beginning to see scale and ACS have entered market

Intermediate ICS 4.1 mil

Rocket chimney

Portable wood rocket

Charcoal industrial

Rocket injera stoves

1.7 mil

<500k

100k

1.8 mil

Legacy stoves

Chimney legacy

Enclosed mud/clay

6.3 mil

1.8 mil

8.1 mil

Source: Dalberg ICS database drawing on public sources, program M&E data, and interview for 45 SSA countries

Household utilizing stove as primary cooking facility (2010) 100% = ~20 million SSA households

23

Advanced ICS

Natural draft gasifier

Fan draft gasifier / fan jet

15-40k

<10k

<50k

The majority of ICS have been distributed in urban areas, are portable, use wood fuel, and are domestically manufactured

100% = 11.8 million (excludes 8 mil legacy stoves)

Portable 66%

Fixed and semi-fixed

34%

Charcoal 44% Wood & multi-fuel

56%

Urban 65%

Rural 35%

24

98% Domestic

2% Imported

DIRECTIONAL ESTIMATE

Source: Dalberg ICS database drawing on public sources, program M&E data, and interview for 45 SSA countries

Sector Trends and Opportunities

• Large and growing demand for clean and improved solutions

Large potential market –50% buys fuels already spending >20bn per year

Only 15-20% cannot or will not buy even basic ICS, but truly clean solutions are unaffordable to many

Demand set to grow with rapid population growth, urbanization, rising incomes, growing fuel prices

• Transformative changes in supply landscape

Advanced biomass solutions entering commercialization (fan gasifiers, TEG fan jet, ND gasifiers)

Continuing evolution in artisanal/semi-industrial sector with frugal design/replication of intermediate ICS

Business model and financing innovation to reach BoP (pay-per-use, fuel-stove packaging, small LPG cylinders)

• Enabling environment

Growing ecosystem of supporting intermediaries and improving, though still limited, funding environment

Evolution in policy landscape with increased recognition of harms and policymaker focus on biomass solutions

Learning from country programs on viable models for scale-up and market support

Emerging testing infrastructure and start of alignment on industry standards

Key sector trends

26

Demand

High

Middle

Low

Large potential market with diverse customer segments

Low

High

Medium

Modern fuels (LPG, Kerosene, Electricity, LNG)

Wood purchasers

Wood collectors Charcoal

Urb

an m

arke

t Ru

ral m

arke

t

Low (<BoP 500) Medium (BoP 500-1500) High (>BoP 1500)

SSA population by customer segment (100% = 164 million households)1

1 Excludes 6.5 million households who use “other” solid fuels including dung, crop waste, coal, or unknown Source: WRI, WB, DHS, WHO, Dalberg consumer segmentation database and analysis 28

Demand

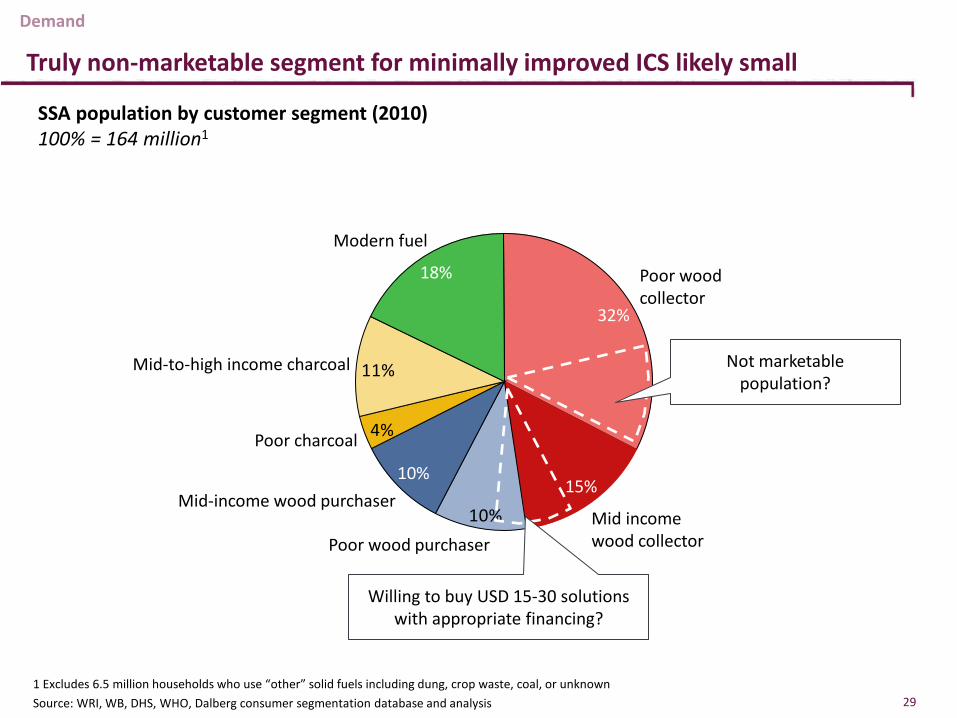

Truly non-marketable segment for minimally improved ICS likely small

1 Excludes 6.5 million households who use “other” solid fuels including dung, crop waste, coal, or unknown Source: WRI, WB, DHS, WHO, Dalberg consumer segmentation database and analysis

SSA population by customer segment (2010)

100% = 164 million1

29

10%

11%

4%

Poor wood purchaser

Poor wood collector

15%

Mid-to-high income charcoal

Mid income wood collector

Mid-income wood purchaser 10%

Poor charcoal

32%

18%

Modern fuel

Not marketable population?

Willing to buy USD 15-30 solutions with appropriate financing?

Demand

Affordability constraint likely to be reduced with growing incomes

1 Purchasing power parity adjusts for price differences in identical goods across countries to reflect differences in purchasing power 2 Includes all of Africa, not just SSA countries Source: McKinsey Global Institute

Share of households in each Africa income bracket (Percent)2

30

Demand

Fuel prices will drive both overall demand and inter-fuel substitution

2006 2005 2004 2003 2002 2001 2000

LPG (kg)

350

300

250

200

150

100

50

2012 2011 2010 2009 2008 2007

Kerosene (l)

Wood (kg)

Charcoal (kg)

Charcoal (w/ 45% poverty premium)

400

Average household cooking by fuel using constant fuel diet (avg. real cost of MJ 320 cooking energy consumption in 2012 USD)

Source: Dalberg SSA fuel price database (22 countries for charcoal, 11 for LPG, 45 for kerosene) 31

Demand

Supply

Wide range of performance with new tech reaching commercialization M

oder

n IC

S Re

new

able

Legacy stoves

Basic efficient stoves

Chimney rocket

Portable rocket

Advanced charcoal

ND gasifier

Fan gasfier/jet

LPG

Electricity

Kerosene

Ethanol

Biogas

Solar

Briquettes/pellets

Retained heat devices

33

Supply

Source: Expert interviews, Berkeley Air Monitoring data, Dalberg analysis

Overview of key production models

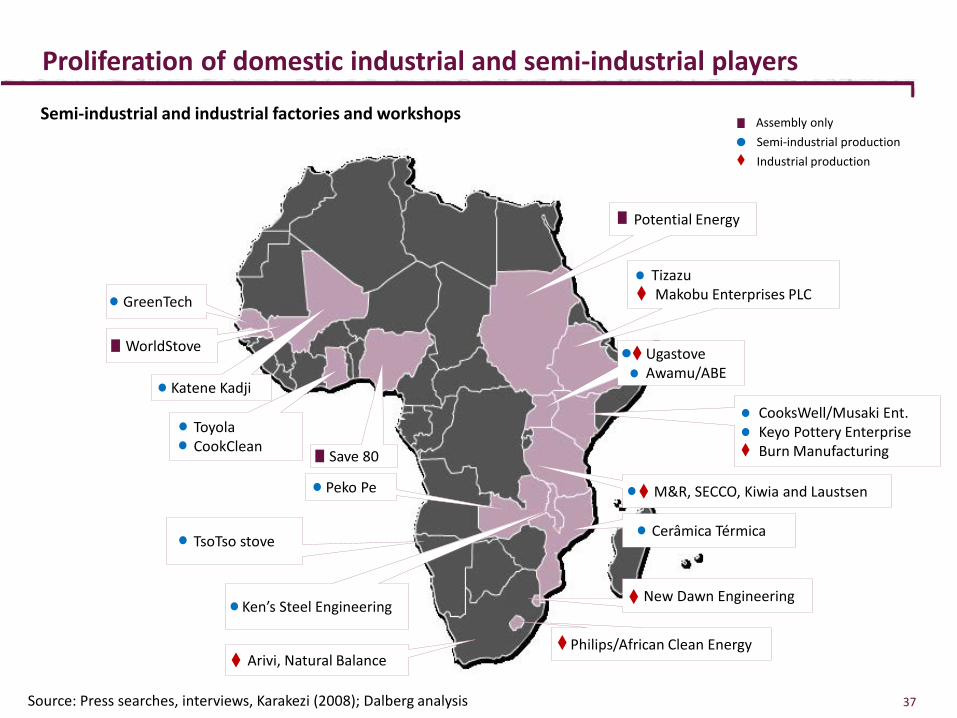

Source: Interviews, press searches, Dalberg analysis

Industrial Semi-industrial Artisanal

Decreasing mechanization and increasing decentralization

34

10-15 firms

200-250k unit sales / year

USD 20-100 per stove

25-40 mid-sized fims

>300k units / year

USD 6-25 per stove

>10k artisans/masons

>3 million units per year

USD 3-15 per stove (portable)

Supply

• High tech , scalable manufacturing outside of SSA

• Mechanized domestic assembly of locally manufactured and imported components

• SSA assembly of imported precision tooled “flatpack” parts

• Individual artisanal producers with support from facilitating programs/ institutions

• Individual unaffiliated artisans and masons

• Local components , moderate levels of automation

• Decentralized workshop production, with central assembly/quality control/and distribution

Multiple new entrants and supporting intermediaries

Source: Interviews, press searches, Dalberg analysis

SolCom

Industrial Semi-industrial Artisanal

Decreasing mechanization and increasing decentralization

Workshop based

Producer networks & individual artisans

35

Mechanized assembly of local and imported components

High tech , scalable manufacturing outside of SSA

Decentralized production, central assembly/quality control

Individual artisanal producers with support from facilitating programs/institutions

Local components , moderate levels of automation

Local low-tech integrated

“Flatpack” assembly of precision tooled parts

International imported

Local hi-tech integrated

Africa assembly

Save80

Supply

Ugastove Awamu/ABE

Tizazu Makobu Enterprises PLC

Semi-industrial and industrial factories and workshops

CooksWell/Musaki Ent. Keyo Pottery Enterprise Burn Manufacturing

M&R, SECCO, Kiwia and Laustsen

Cerâmica Térmica

Katene Kadji

Toyola CookClean

New Dawn Engineering

Philips/African Clean Energy

Ken’s Steel Engineering

Peko Pe

GreenTech

Save 80

WorldStove

Potential Energy

Semi-industrial production Industrial production

Assembly only

Proliferation of domestic industrial and semi-industrial players

TsoTso stove

Source: Press searches, interviews, Karakezi (2008); Dalberg analysis

Arivi, Natural Balance

37

Growing diversification in distribution channels as sector seeks scale Supply – distribution

Source: Press searches, interviews, Dalberg analysis 39

3rd party dealer-distributor networks

Social sector partners Institutional sales Micro-franchisees Direct sales channel

Distributor / dealer networks including both large and small retailer formats

Manufacturer staff, commission-based door-to-door agents, proprietary stores

Bulk purchases and redistribution by institutional clients (e.g., relief agencies)

Sales/order fulfillment via MFI / NGO / gov’t extension agents

Micro-franchisee agents empowered an incented to distribute products

Save80

Innovation in consumer financing models Supply – financing

Overview of finance solutions for driving price reduction Option Details Example

Installment / PAYG plans • Consumers can pay for a stove in installments.

• Pay-as-you-go systems lower upfront costs for consumers and but transaction costs of collection are high and difficult to scale

Carbon finance (CDM) • USD 10-25 carbon credit claimed by the manufacturer as income or passed through to the consumer in lower prices..

• USD 42 million CDM funds channeled to stoves projects last year, but viability at scale unclear given state of carbon credit markets.

Microfinance • Small loans for stove purchase disbursed through MFIs/SACCOs and typically bundled with distribution arrangements

• No demonstrated capacity for scale today due to logistical challenges and low MFI appetite for financing <USD 60 products

Non-carbon “buy-down” performance based grants

• Performance based subsidies provided directly by donors/ governments to lower upfront cost of the stove to the end user.

• Subsidy can go to the manufacture to lower price of stove, or to the user for purchase (e.g. voucher mechanism).

Mobile enabled utility model

• Potential for mobile financing and utility based models with remote stove activation/deactivation (e.g., pay for 2 weeks use)

• Models currently being trialed for solar lighting and potential exists for extending model to cookstoves

Fuel amortization and cross-subsidy models

• Stoves offered for free, at cost, or with partial subsidy but funds collected from fuel revenue stream

• Stoves offered for free in return for fuel collection services

40 Source: Press searches, interviews, Dalberg analysis

Overview of key cost drivers

Source: manufacturer interviews, Dalberg analysis

32% 27%

Improved charcoal stove

USD 22

18%

11%

14%

16%

14%

Wood Rocket stove

USD 21

14%

15%

14%

14%

11%

Semi-industrial production

26%32%

Fan gasifier (pellet)

USD 49

11%

11%

8% 6%

12%

20%

Wood rocket

USD 41

5%

13%

23%

9%

10%

15%

Industrial production Artisanal

40%30%

18%

USD 5 USD 11

23%

Efficient charcoal stove

18%

Efficient charcoal stove

23%

21%

26%

42

Shipping and import duties Distribution costs Manufacturing margin Local transport Labor

Taxes Raw materials

Supply – product economics

Move to frugal design and Africa production for natural draft gasifier

1 Approvecho testing for Africa manufactured stove; self-reported results for India manufactured stove; results from pyrolysis only, not burning resulting charcoal Source: Manufacturer interviews, public value chain data, Dalberg analysis

13

10

10

6

39

Urban Africa end-

consumer price

Distribution costs,

margins, and VAT

Import duties

and shipping

Labor and mfg. margin

Materials

Industrially mfg. ND TLUD imported from India ND TLUD manufactured semi-industrially in Uganda

Recycled metal

8

5

3

Distribution and VAT

16

Urban Africa end-consumer

price

Materials Labor and mfg. margin

Easy to assemble design for low skill labor

Overall performance: ISO Tier 2-3 PM: 89 mg (range unknown)1

CO 8.1 g (range unknown) Fuel savings vs. 3-stone fire: 40%+

Overall performance: ISO Tier 2-3 PM: 25 -180 mg1 CO: 3-8 g Fuel savings vs. 3-stone fire: 45%

Costs across stove value chain, USD

Low VAT due to low baseline product cost; no import duties

Supply – product economics

43

Enabling Environment

Growing eco-system of supporting intermediaries

Source: Organization websites; Literature review; interviews; Dalberg analysis

Coordinating platforms

Testing centers/providers

Fuel & stove suppliers/distributors

Government agency/program

Donors and programs

National/International NGOs

SeTAR Centre

Global LPG Partnership

45

Enabling environment

CERER

Providers of finance / Investors

MEMD

Champions have emerged with focus on specific sectors /technologies

Source: Online websites/resources; Dalberg research and interviews

Modern and renewable fuels and stoves

Kerosene Bio-fuels Biogas Renewable solid fuels

Solar & Retained Heat LPG for the BoP

Global LPG Partnership

Many SMEs (USD 20-300k revenues

46

Enabling environment

Of 11 globally recognized testing centers, only one is in SSA, 3 others in development

Aprovecho Research

Center, USA

Colorado State University Engines and Energy Conversion Lab,

USA Centre for Research in

Energy and Energy consumption (CREEC),

Uganda

Sustainable Energy Technology and Research Centre

(SeTAR), South Africa

Asia Regional Cookstove Program

(ARECOP), Indonesia

EELC Technology Lab (EELC)

and Renewable Resources Lab (RRL), China

GERES, Cambodia

Prakti Design Lab,

India

GIZ – UMSS University of Cochabamba,

Bolivia

SENCICO, Peru

Zomorano University, Honduras

Kenya Industrial Research and Dev’t

Institute (KIRDI), Kenya

Environmental Protection Agency

(EPA), USA

Testing facilities for improved cookstoves around the world

Enabling environment

Centre d'Etudes et de Recherches sur les Energies

Renouvelables (CERER), Senegal

48 Source: Press searches, interviews, Dalberg analysis

Looking ahead

In business as usual case clean and improved access will grow significantly

24%13%

20%

17%

16%

15%

14% 25%

7%14%

17%6%

5%4%

2010

0%

80

2020 Base case

Legacy stoves

Fixed chimney rocket

Portable artisanal ICS Semi-industrial ICS Industrial ICS/ACS

LPG

Kerosene

Renewablessolutions

Electricity

48

0%

0% 1%

Penetration (% of all HH)

2010 2020F

17% 18%

7%

18%

24% 36%

Improved stove and clean fuel penetration of SSA households (Millions of HH, %)

Source: Dalberg ICS penetration forecast model; Dalberg analysis

+25 mil HH

+7 mil HH

50

18%6%

18%

2010

5%

72%

23 45

ICS

62%

2% Legacy improved

2020

Traditional

unimproved

17% Clean stoves/fuels

… but this growth is not sufficiently quick and, likely, insufficiently equitable or sustainable

Source: Dalberg analysis

South Asia

East Asia

Lat Am.

100%

20%

40%

90%

60%

10%

80%

0%

30%

70%

50%

Improved 2010

Traditional cooking

Improved 2020

Would still leave SSA in much worse situation in 2020 than where other developing countries are today

Inertial growth likely to be highly unequal, with many access laggards

SSA countries

51

Major barriers to more rapid uptake

Source: World Bank regional consultations; GACC market assessments; Sector interviews; PCIA; Dalberg analysis PCIA

Consumer demand Supply Cross-cutting enablers

• Affordability (product and fuel)

• Consumer awareness

• Access

• Culturally appropriate design and convenience

• Low product quality

• Cost-effective distribution

• Producer and distributer A2F

• Producer technical capacity

• Lack of after-sales

support

• Policy and regulations

• Quality standards and testing infrastructure

• Lack of consumer/ market intelligence

• R&D and technical innovation barriers

• Lack of sector coordination

• Program monitoring and impact assessment

52

How can the market grow even faster?

• Investment in unlocking demand via consumer education campaigns, consumer finance solutions, and stove price reductions via tech innovation and performance based incentives

• Strategic investments by donors in underserved markets to “kindle” new market growth (e.g., set up of artisanal sector, consumer awareness) in totally unpenetrated geographies

• Acceleration of industrial and semi-industrial solutions (e.g., from 35-50% to 45-70% annual sales growth) via access to finance, market linkages, quality testing support to multiply number of new entrants and help existing players grow faster

• Re-alignment of policy and regulations to support market (e.g., taxes and tarrifs)

• Success of ambitious programs or projects across modern and renewable fuels unrelated to improved biomass cooking solutions, e.g.:

• ABPP – targeting 2 million SSA biogas users by 2020

• Global LPG Partnership – 30 million incremental new HH in SSA by 2018-2020

• Ethanol (Cleanstar)– scaling to 1-2 million HH Africa-wide by 2020

53

The funding gap to improved and clean cooking energy access is large

1 SSA share of USD 70 million estimate by IEA based on SSA proportion of global solid fuel users 2 Dalberg estimate based on tally of known and estimated donor, CDM, and private sector investments in the past year (or, where applicable, historical annual average) 3 IEA funding need estimate showing range from “New Policy Scenario” for the minimum to “Universal Access” for all Source: Dalberg analysis

22

IEA estimate of SSA funding need

(average 2010-30)3

300-1100

Dalberg estimate (2011)2

50-125

IEA estimate 20111

SSA clean/improved cooking energy annual funding gap USD millions

54

Enabling environment

3,833

2,000

217

HIV/AIDS

10-18x

Malaria ALRI/COPD from solid fuel cooking

Annual funding per death (2012)1

9-10x

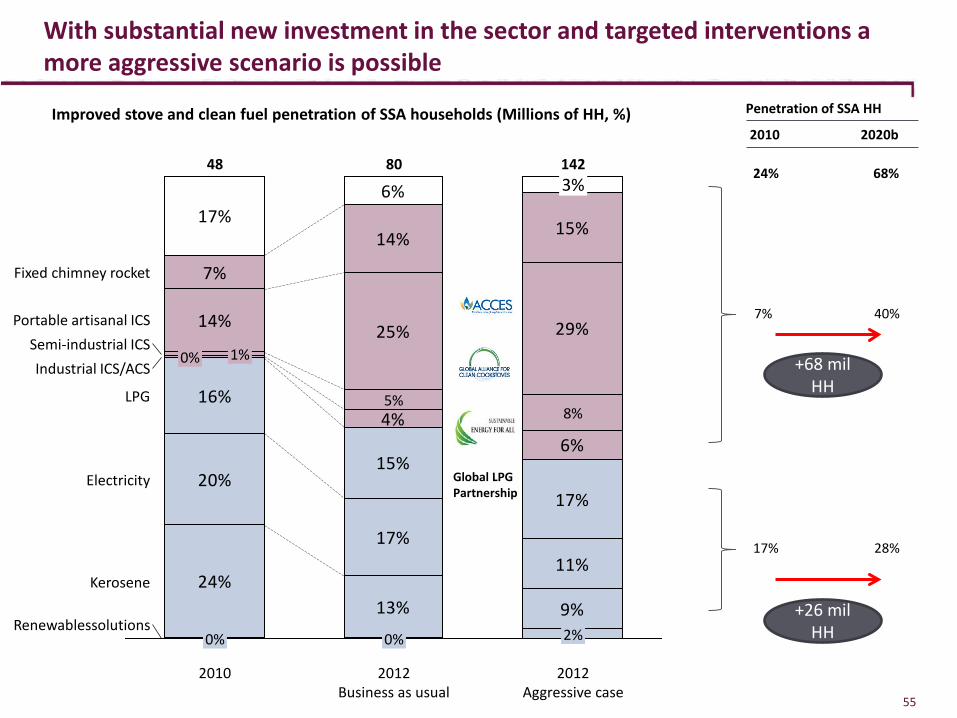

With substantial new investment in the sector and targeted interventions a more aggressive scenario is possible

Penetration of SSA HH

2010 2020b

17% 28%

7%

40%

24% 68%

Improved stove and clean fuel penetration of SSA households (Millions of HH, %)

55

24%13% 9%

20%

17%11%

16%

15%

17%

4%6%

5%8%

14% 25% 29%

7%

14% 15%17%6%

Electricity

LPG

Industrial ICS/ACS Semi-industrial ICS

Portable artisanal ICS

Fixed chimney rocket

2012 Aggressive case

142

2%

48

0%

0% 1%

3%

2012 Business as usual

80

0% Renewablessolutions

Kerosene

2010

+68 mil HH

+26 mil HH

Global LPG Partnership

Recommendations

Recommendations – Private sector

1. The SSA household cooking market is ripe for investment and market entry with increasing commercial opportunities for first mover producer, distributor, and financier entrepreneurs

2. Product quality and consumer orientated design can drive adoption and greater scale

3. Segment-specific customization is important for many end-users but there is also strong demand for relatively standardized products that translate across borders and customers

4. Private sector enterprises serious about building scale in Africa should consider on-shoring the production and/or assembly of stoves in large SSA demand markets or regional hubs due to the significant potential net benefits from a product price and distribution perspective

5. The cooking fuel market is orders of magnitude larger than the market for cooking appliances, highlighting benefits of business models that integrate into fuel supply chains

6. Product bundling and partnerships with existing distribution networks will be critical to scale – building one’s own proprietary distribution is effective, but typically expensive and slow

7. Compelling impact data is relatively scarce, particularly for newer, higher performing technologies, well structured investments in M&E will be important competitive differentiators with public sector, donor, and social impact investor community

57

Recommendations – Governments, NGOs, and Donor Community

1. Cleaner, more efficient production of solid biomass and the development of renewable fuel markets should be pursued alongside efforts to encourage the adoption of modern fuel and improved biomass stoves

2. Artisanal production continues to be an important solution for many consumers even as parallel efforts are being pursued to maximize the environmental and health benefits of cooking interventions through more advanced technologies and benefits of industrial scale production

3. More sustainable and equitable reach of clean cooking energy solutions will require donors, NGOs, and governments to engage both on market acceleration, market creation, and non-market solutions

4. Smart subsidies and incentives linked to performance are therefore an essential tool for clean cooking energy promotion; direct subsidies should be used sparingly to avoid market distortion

5. Access to finance challenges spans upstream and downstream needs, but donor interventions are likely to make the biggest impact on producer and distributor financing bottlenecks

6. Large-scale consumer awareness efforts are needed to drive faster adoption and ongoing use of clean cooking energy solutions

7. Despite growing knowledge on the sector, the donor community must address major gaps in data on the African consumer and real world impacts

8. Investment in standards and quality testing will be critical to help producers and distributors strike appropriate balance between affordability and quality and minimize potential market spoilage

9. Market development must be integrated with policy reforms including rationalization of taxes/duties),integration of sustainable biomass fuels into energy strategy, and regulatory regime for modern fuel and renewable fuel development

58

Appendix

Overview of SSA customer segments

Poor wood collectors

Mid income wood collectors

Poor wood purchasers

Mid income wood purchasers

Poor charcoal users

Mid-high income charcoal

Modern fuel users

Segment size 53 mil (32%) 25 mil (15%) 17 mil (10%) 16 mil (10%) 6 mil (4%) 18 mil (11%) 29 mil (18%)

Current spending Monthly fuel cost (stove cost)

n/a n/a $1-10/month ($ 0–5)

$5-25/month ($ 0-5)

$5-20/month ($1-5)

$5-35 / month ($1-12)

$5-40/month ($10-100)

Household income <BoP 500

BoP 500-1500 <BoP 500 BoP 500-1500 <BoP 500 60% BoP 500-1500, 40% >1500

>95% BoP 1500

Location of consumer 90% rural, 10% urban

90% rural, rest urban

>60% urban, esp. W. Africa

38% urban, 62% rural

50% urban

75% urban, rest peri-urban

>80% urban

Awareness of solid fuel health harms/risks

Awareness of improved fuels/stoves

(Physical) access to improved products

Ability to afford improved solution

Access to finance

Cultural resistance to new technologies

Source: various end-user surveys, Shell Foundation, Global Alliance Market Assessments; Dalberg customer segmentation database; Dalberg analysis 60

The penetration renewable cooking solutions is negligible, but biogas, ethanol, and renewable solid fuel pilots are garnering significant attention

Source: Dalberg Africa ICS and clean energy database

0.65 (<1%)

Biogas digesters <20k Uganda, Burkina Faso, Kenya, Ethiopia, Rwanda, Tanzania

Ethanol / ethanol gel <50k South Africa, Ethiopia, Malawi, Nigeria, Mozambique, Zimbabwe, Botswana

Solar cookers <70k Darfur, Chad, S. Africa, Kenya, Senegal

Retained heat cookers >550k Predominantly South Africa, but some models in Nigeria, Tanzania, Botswana

Briquettes / Pellets <10k Kenya, Tanzania, Uganda, Rwanda, Ethiopia, Senegal

HH reached Key geographies for commercialization

61