State of Small Business Britain conference 2016 presentation.

80

-

Upload

enterpriseresearchcentre -

Category

Business

-

view

37 -

download

0

Transcript of State of Small Business Britain conference 2016 presentation.

10,000 Small Businesses UKCharlotte Keenan

Goldman Sachs, 30th November 2016

Why 10,000 Small Businesses UK

Goldman Sachs is committed to leveraging our capital, people and innovation to help address economic and societal challenges, catalyze markets and transform communities

Since 2001, through its global philanthropic efforts and Investing for Impact business, the firm has deployed grants and investments to help bring economic growth, stability and opportunity to communities around the world

The institutional platform is dedicated to helping entrepreneurs grow their businesses and create jobs by providing them with education, support services and access to capital.

10,000 Small Businesses is an initiative to help small businesses across the UK and the U.S. create jobs and economic growth through access to a practical business education and business support services

— Practical business and management education is delivered through academic partners

— Guided by an advisory council Co-Chaired by Lloyd Blankfein, Michael Bloomberg, Warren Buffett and Dr. Michael Porter

With 28 sites across the U.S. and UK, including the U.S. national cohort, 10KSB has served over 7,300 small business owners in the UK and US

How does 10KSB work? Highly practical course focused on skill development for business

growth co-taught by Oxford Saïd Business School, Aston Centre for Growth, University of Leeds, and Manchester Metropolitan University

Rotates between residential and online sessions to provide ultimate flexibility

— Each participant is assigned a personal business coach

— Over the 12 weeks, participants develop a customised Business Growth Plan to direct business strategy and expansion

— 6-8 hours of online activities per week

Taught in a collaborative, peer-learning setting

Provides tools that can be immediately used in your business

Provided for free to business owners, and fully-funded by the Goldman Sachs Foundation

The success of the program is due to the right balance of formal learning, mentoring, and peer-to-peer support. Participants of the programme will benefit from:

— Specialist workshops

— One-on-one business advising

— Access to professional experts

— Networking opportunities and

— A network of 10,000 Small Business graduates

Who are the participants? 10,000 Small Businesses UK is offered at no cost to small businesses and

social enterprise leaders who want to grow their businesses, create local employment and have scalable business models

The following eligibility criteria also apply:

— Must be the primary owner, co-owner, or the most senior decision-maker of the business

— Operating at least three years, with 5 to 50 employees and annual turnover of at least £250,000

— Must be scalable and capable of generating additional local employment

— Should not have extensive recent management education

— Preference will be given to those businesses operating in or on behalf of disadvantaged communities or regeneration areas

An average of

£1.2m revenue

An average of 21 employees

of participants have no

university-level degree

Since 2010, 10,000 Small Businesses has helped over 1,000 small businesses in UK grow and create jobs

How do we know 10KSB works?

From 2016, the programme has become national, accepting entrepreneurs from across the whole of Great Britain

The programme is proven to drive growth and job creation

10KSB UK graduates are growing their staff at 31% per year and increasing revenue at 81% per year.

They are three times more likely to be creating jobs and two times more likely to be growing revenue than other UK small businesses.

Independent analysis shows that participants create 17% more jobs and generate 19% higher revenues than they would have without the programme.

1 Results taken from November 2016 Impact Report

Social enterprises

One in six 10KSB UK participants run social enterprises, and they collectively employ over 2,500 people with a combined turnover of £112m.

Social enterprises grow faster than other 10KSB UK participants, with a mean employment growth rate of 43%, compared to 29%.

These social enterprises are twice as likely small businesses to be led by women than men

Rana [email protected] 971533

Monster Group UKYork

Manufacturing

Monster Group is an online retailer, established in 2007, that develops products across different sectors, including retail, food, industry and manufacturing. It includes the businesses Monster Chef, Monster Racking, Monster Retail, Monster Scales and Monster Doodles.

Employees: 20 Graduated: 2012Since Graduating: Job Creation: 14 Revenue Turnover: 331% increase

How has 10KSB UK changed your business?

Reformed the company’s structure with Monster Group, which incorporated the existing businesses

Reviewed workflows and productivity of the team

Reduced the order process time to just 2 minutes

Purchased a 90,000 sq. ft. warehouse to increase the group’s product offerings

Opened a Research and Development centre to advance product development and competitiveness

“ I had never dreamed of developing an R&D site before I started the programme – I was focused on driving international sales. The Strategy and Operations Management modules

changed all that.”

Professor Mark Hart

ERC

Dashboard – Focus on Geography of Growing Firms

• Video highlighted the wide range of variations in the well-known OECD High-Growth Firm (HGF)

• However, while useful it is restrictive – need to understand the various types of firms that are growing and where they are concentrated

• Greater granularity in growth metrics better informs the development of local and regional economic policy

Firm Survival and Growth

13

Start-ups achieving at least £1m T/O after 3 years

Established businesses growing from £1-2m to £3m+ T/O

Fast-Growing Firms (2012-15)

• Fast-Growth is defined as annualised average growth in employment of 20% or more over a three year period.

• Overall, Scotland, Wales and the southern and western parts of Northern Ireland perform well with above average proportions of these businesses.

• In England, London has the highest proportions of fast-growing businesses but all the other local areas with above average proportions of fast-growing businesses are in the North, South West and the Midlands.

• The data shows quite clearly that some of the fastest growing businesses in the UK are delivering jobs and revenues for their owners outside London and the South East which has been a consistent finding since we started tracking this metric by local areas in the UK.

Driving Business Support Interventions

• Does confirm the value of locally differentiated policies reflecting the local realities of business dynamics

• Something long recognised in Scotland, Wales and Northern Ireland but constantly being re-worked in England!

A Simple Story of Productivity! – 2008-15Turnover Growth

Job Growth

Zero

Zero

‘Green Zone’

+

+

+

-

-

-

Only one ‘space’ where growth in T/O; Jobs and productivity are all +ve – the ‘green zone’

But sparsely populated with firms – approx. 10%

…and more than half of them where there is very little growth – the blue triangle

Rule of thumb – 3 out of 4 firms which grow turnover grow productivity; 1 in 5 firms which grow jobs grow productivity

Productivity and High-Growth Firms?

• Only 20% of 10+ employee firms in the ‘green zone’ are HGFs (T/O definition)

• Only 5% of 10+ employee firms in the ‘green zone’ are HGFs (Jobs definition)

• So from a productivity perspective HGFs are not an important group of firms – main problem here is both a definitional one and the focus on jobs!

Creating a Growth Pipeline

• A single-minded preoccupation with HGFs may not be a sensible focus for policy-makers - not only is it somewhat arbitrarily defined, it has the disadvantage of rendering invisible the reality of growth for the majority of businesses

• And now we know they are less important for productivity growth than one might have imagined!

• It would be more informative to concentrate on the importance of creating a growth pipeline at local level and monitoring its development over time.

A Fresh Look at the SME Population

• Build a growth pipeline around the following:

– Potential and Nascent Entrepreneurs

– Lone Rangers and the unwilling self-employed

– Steady Eddies – limited entrepreneurial intensity and low risk tolerance

– Rising Stars – strong growth ambition but in need of leadership skills to implement innovation and internationalisation and engage in external networks

– Leading Lights – established firms with sustained growth ambition based on core management competencies

Thank you!

Questions and comments?

More information at http://enterpriseresearch.ac.uk/

Contact us about this research: Mark Hart [email protected]

This work reflects the joint effort by the research team of the ERC, including

Michael Anyadike-Danes, Karen Bonner and Mark Hart.

This work contains statistical data from ONS which is Crown Copyright. The use of these data does not imply the

endorsement of the data owner or the UK Data Service at the UK Data Archive in relation to the interpretation or

analysis of the data. This work uses research datasets which may not exactly reproduce National Statistics aggregates.

Lee Hopley (EEF)

James Phipps (Nesta)

Susanna Lawson (OneFile Ltd & Goldman Sachs 10,000

Small Businesses alumnus)

Sarah Middleton (Black Country Consortium Ltd)

Chair: Professor Mark Hart (ERC)

Liam Byrne, MPAPPG on Inclusive Growth

THE ALL PARTY GROUP ON INCLUSIVE GROWTHReconnecting wealth creation and social justice

www.inclusivegrowth.co.uk

The APPG on Inclusive Growth Mission:

The APPG aims to create a space in parliament to connect

reformers and thinkers in politics, business, trade unions,

finance, churches, faith groups and civil society to forge a

new consensus on inclusive growth and to identify practical

next steps for reform.

We have a problem….

And its bad for workers

In the UK

productivity and

pay link broke

down in 90s

Workers are right to be angry….

Some, however, are doing rather well

Top 1% takes

bigger slice of

national

income

In a democracy anger isn’t abstract: Brexit

The APPG brings together a cross-party group of leading MPs and Peers

Liam Byrne MP

Rushanara Ali MP

Rt Rev Bishop of Birmingham

Members of the APPG include:

Dame Caroline Spelman MP Lord Wrigglesworth

Alison McGovern MP Chris White MP Seema Malhotra MP

Previous events

Our 2014-2015 work programme constituted seminars, private discussions and a distinguished speaker series including:• His Grace the Archbishop of

Canterbury• Angel Gurria, Secretary-

General of the OECD• Sir Charlie Mayfield, CEO of

John Lewis Partnership• Mike Rake, Chairman of the

CBI• Xavier Rolet, CEO of the

London Stock Exchange

His Grace the Archbishop of Canterbury addresses the APPG

Angel Gurria, Secretary General of the OECD Sir Charlie Mayfield, Lord Baker & Lord Wrigglesworth

National media coverage

Current partners

The Group has partnerships with leading cross-party think tanks who jointly published a collection of essays for the group in March.

The Group also has partnerships with leading business and civil society organisations, including Oxfam and the City of London Corporation.

SPERI is the Group’s Secretariat, which aims to develop new ways of thinking about the economic and political challenges posed for the whole world.

Our agenda is shaped around the key reforms required to deliver growth, productivity, and a fairer distribution of wealth

3. Enterprise / Regulation

5. Demand side: trade reform

1. Supply side: science & technology

2. Capital: Patience 4. Labour: skills & pay

6. Place: regional balance 7. Tax: Fair / sustainable

WWW.INCLUSIVEGROWTH.CO.UK

Cliff PriorBig Society Capital

GROWING SOCIAL VENTURES

Cliff Prior, Chief Executive, Big Society Capital

@cliffprior@BigSocietyCap

About Big Society Capital

• Big Society Capital is an independent financial institution with a social mission, set up to help to

develop social investment in the UK.

Champion for Social Investment

Wholesale Social Investor

As a champion

Business Impact Challenge

GET IT Public service reform

Transparency

Research Council Charity Bonds Social Pensions Crowd Funding

Working with charities & social enterprises

Working with investors Social impact tools

CURRENT PROJECTS

CORE ACTIVITIES

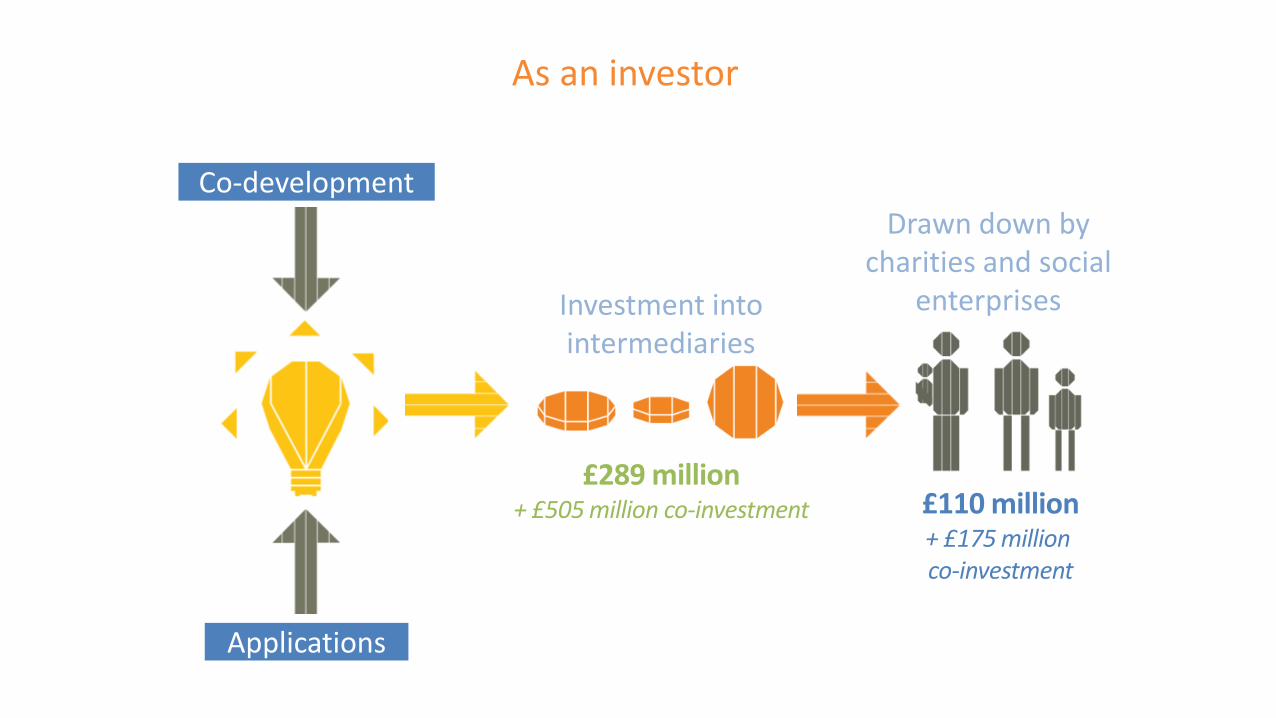

As an investor

Co-development

Applications

Drawn down by charities and social

enterprisesInvestment into intermediaries

£289 million+ £505 million co-investment £110 million

+ £175 million co-investment

Our focus

Finance for small & medium-sized

charities & other social sector organisations

Capital that allows innovation in tackling

social problems to quickly grow and

replicate

Mass participation in social investment

.

Greater financial scale in order to

finance social issues

THE SOCIAL CHALLENGE IN THE UK

Housing & local facilities

Communities Education

Income & financial inclusion

Health & social care

Employment & training

Family, friends and relationships

Criminal justiceArts, heritage, sport

and faith

What is social investment?

Social investment is repayable money to help charities and social enterprises to do more of their important work.

ONE tool for SOCIAL VENTURES

Trading Donations

BankFinance

Contracts/ PaymentBy Results

Social Investment

FINANCIAL TOOLKIT

To build innovation, growth and sustainability

Examples of how it works

48

Social sector info

49

£39bn income£38bn spenddeclined since 2007 peak of £41bn

900k civil society orgs

161k charities

70k social enterprises

Social enterprises contribute

£24bn to economy

and employ 1m people

Charities & social enterprisesare regulated organisations: asset locked / (part) profit locked

52% of social enterprises grew in last year

40% of mainstream sme’s grew in same year

Social Investment Market Size

50

52

£39bn income£38bn spenddeclined since 2007 peak of £41bn

THE RISE OF THE MISSION LED BUSINESS

53

CONTROVERSIES

54

CONTROVERSIES

55

Regulated, no/limited private gainCan’t give equity investment – slows

down growth

Will they still be social tomorrow?

CONTROVERSIES

56

Regulated, no/limited private gainCan’t give equity investment – slows

down growth

Will they still be social tomorrow?

?

57

58

59

Business finance in disadvantaged areas

60

Banks still not reaching disadvantaged areas enough.CDFIs help but are poorlysupported and reliant on EU funds/guarantees which will disappear with Brexit

A CALL TO ACTION

61

• Traditional social sector is struggling but resilient

• Social investment can help some to do more

• Growing movement of social entrepreneurs and profit with purpose businesses

• Increasing interest in inclusive business

• New social needs including the people “left behind”

• SME business finance in disadvantaged areas needs an urgent reboot

www.bigsocietycapital.com

• Big Society Capital Limited is registered in England and Wales at Companies House number 07599565. Our registered office is 4th Floor, New Fetter Place, 8-10 New Fetter Lane, London EC4A 1AZ. Big Society Capital is authorised and regulated by Financial Conduct Authority number 568940.

62

Thanks for listening

@cliffprior@bigsocietycap

www.goodfinance.org.uk#socinv

Professor Jun DuERC

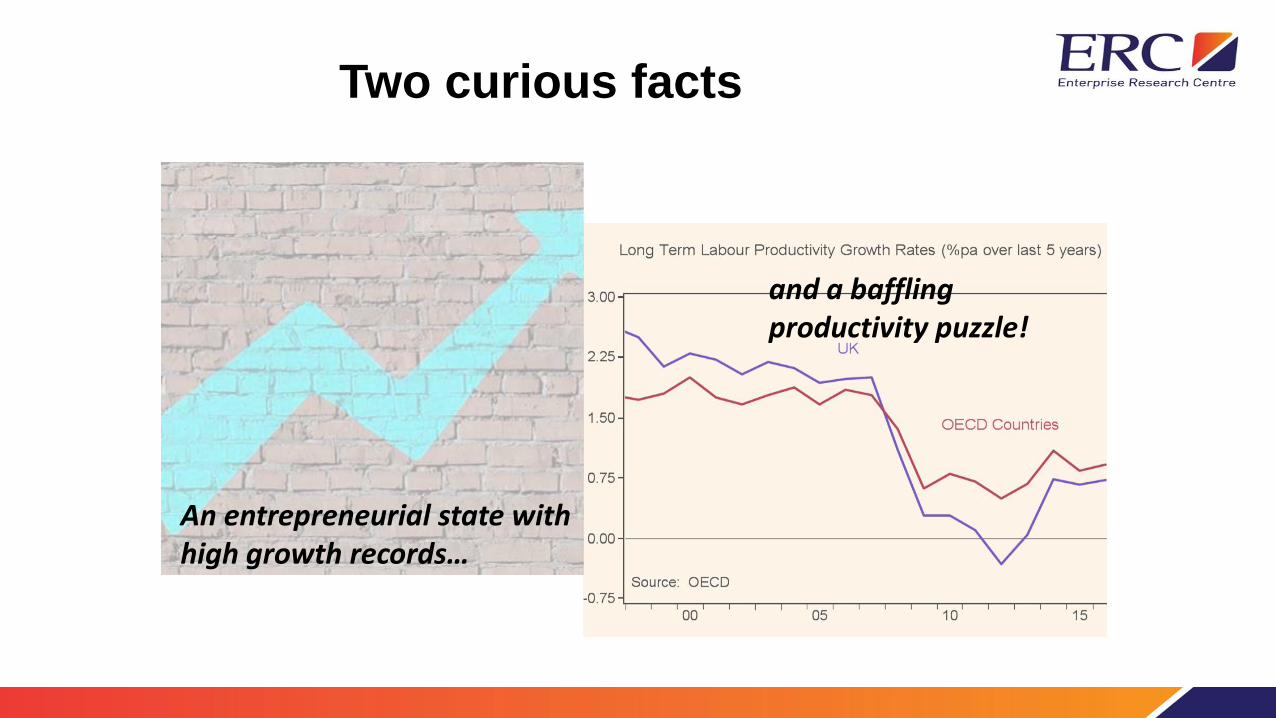

Two curious facts

An entrepreneurial state with high growth records…

and a baffling productivity puzzle!

Fast Growing Firms: to define and identify

High growth firms, in

employment(OECD, 2007)

High impact firms

Growth heroes(Du and Bonner 2015)

Top performers

Millennium 2000 firms(Hart et al 2016)

High growth entrepreneurs

Gazelles

High employment growth

firms

(Clayton et al, 2013)

High growth firms, in value

Employment based Productivity based

Bigger firms

Micro firms

Bigger firms Micro firms

% in total survivors 1.2 1.7 2.1 0.5 5.2 1.2

OECD-HGFs Small HGFs

GrowthHeroes

Super GrowthHeroes

GrowthHeroes

Super GrowthHeroes

Jobs (stock)

Jobs (net job creation)

Turnover (stock) ££££ £ ££ £ £ £

Turnover (growth) ££ £££ ££ ££ £££££ ££££

Productivity (level) ★★★ ★★★★★ ★★ ★★★★ ★★ ★★★★

Productivity (growth) ★★★ ★★★ ★★★★ ★★★

Summary of Findings

Fast-Growing Firms and Productivity: beyond

single firms

• Growth persistence is not at firm level, but at regional

level

– The predictability of high growth episodes remains limited

– firm growth is typically highly discontinuous and high

employment growth is not persistent among firms

– Recent research on growth persistence beyond single firms – at

regional level

• Regional and industrial externalities

– Knowledge spillovers within and across industries

– Localisation externalities

– Urbanisation externalities

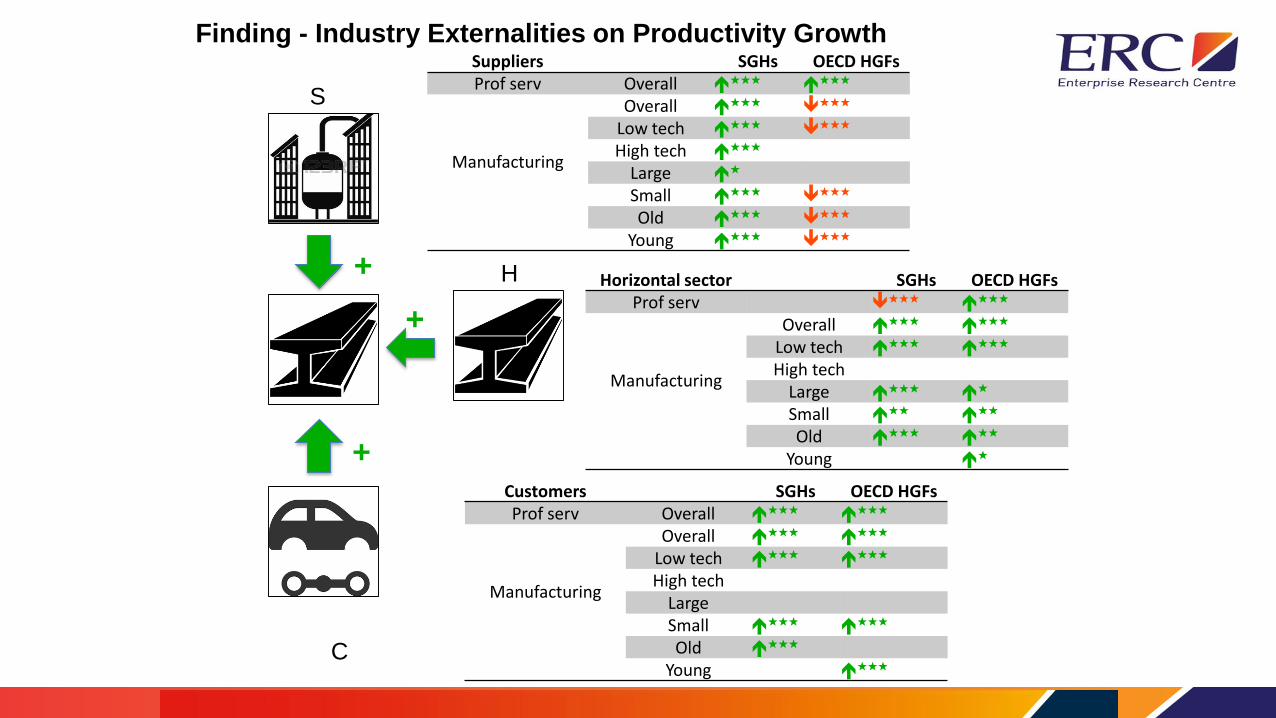

What does it mean for a region to have more fast-growing firms?

Finding - Industry Externalities on Productivity Growth Suppliers SGHs OECD HGFsProf serv Overall

★★★★★★

Manufacturing

Overall ★★★

★★★

Low tech ★★★

★★★

High tech ★★★

Large ★

Small ★★★

★★★

Old ★★★

★★★

Young ★★★

★★★

Horizontal sector SGHs OECD HGFsProf serv

★★★★★★

Manufacturing

Overall ★★★

★★★

Low tech ★★★

★★★

High techLarge

★★★ ★

Small ★★

★★

Old ★★★

★★

Young ★

Customers SGHs OECD HGFsProf serv Overall

★★★★★★

Manufacturing

Overall ★★★

★★★

Low tech ★★★

★★★

High techLargeSmall

★★★★★★

Old ★★★

Young ★★★

H

S

C

++

+

Finding: Regional externalities of super

growth heroes on productivity growth

Key MessagesBeyond job creation and productivity improvement within their own

organizations, fast-growing firms have externalities to other firms in the region,

within and across industrial sectors.

Horizontal effects:

• Competition-led efficiency improvement with positive productivity

spillovers

Vertical effects:

• Improved productivity and efficiency – knowledge spillovers effects

• Increased demand for services and products – positive market creation

effect

• Competition-led crowding out effects for skills and labour in the upstream

sectors

Regional disparity:

• Advantageous urban areas

• Interestingly, the areas of more high growth incidences are not

necessarily those which benefit most from it!

Thank you!

Questions and comments?

More information at http://enterpriseresearch.ac.uk/

Contact us about this research: Jun Du [email protected]

This work reflects the joint effort by the research team of the ERC, including

Jun Du, Karen Bonner, Enrico Vanino, Mark Hart and Michael Anyadike-

Danes.

This work contains statistical data from ONS which is Crown Copyright. The use of these data does not imply the

endorsement of the data owner or the UK Data Service at the UK Data Archive in relation to the interpretation or

analysis of the data. This work uses research datasets which may not exactly reproduce National Statistics aggregates.

Phil Smith (Cisco UK and Ireland)

Professor Stephen Roper (ERC)

The UK Productivity Council

How Good Is Your Business Really?

Phil Smith - Chairman, Cisco UK & Ireland

Jenny Cridland (BAE Systems)

Jun Du (ERC)

Richard Evans (Mechatronic Ltd & Goldman Sachs

10,000 Small Businesses alumnus)

Joe Marshall (NCUB)

Chair: Michael Anyadike-Danes (ERC)

Tony Moody (BEIS)

Matt Adey (BBB)

Tony Moody ( BEIS)

Matt Adey ( BBB)

Kevin Davis (The Vine Trust & Goldman Sachs

10,000 Small Businesses alumnus)

Chair: Ute Stephan (Aston University, ERC)

Stephen Roper (Director, ERC)

Mark Hart (Deputy Director, ERC)

Vicki Belt (Deputy Director, Impact & Engagement,

ERC)