Startup Equity and Stock Options vs 5 22 13

30

Startup Equity 201: Stock Options for Founders and Employees May 22, 2013 by Jamie Lee @jieunjamie with Zeke Vermillion www.adlervermillion.com Thursday, May 23, 13

Transcript of Startup Equity and Stock Options vs 5 22 13

Startup Equity 201: Stock Options

for Founders and Employees

May 22, 2013by Jamie Lee@jieunjamie

with Zeke Vermillion www.adlervermillion.com

Thursday, May 23, 13

Disclaimer

Hi! I’m not an accountant or a lawyer.

The information contained herein and ensuing discussion should NOT be considered tax or legal advice.

The information is intended to help you get familiarized with general concepts in startup finance, which may or may not apply to your situation.

Thank you!

Jamie Lee @jieunjamiejieunjamie.com

Thursday, May 23, 13

Before joining a startup, ask

•Do I trust this team? Is this the right company?

•What is my percentage of ownership?

•What is market rate salary and equity comp?

•What is the estimated valuation at exit?

•Do I need a lawyer or accountant (because devil’s in the details)?

•How long is my vesting schedule?

•What are tax implications?

•Can I make 83b election for restricted stock grants?

•Can I exercise my options early?

Startup Equity: More ART than SCIENCE Key questions to ASK for Founders and Employees

Thursday, May 23, 13

Startup Equity: More ART than SCIENCE but still need to do the MATH

1) Ownership = # Shares Granted to You Total Capitalization

Formulas Example

1) 1% = 100K Shares Granted10M Total Shares Outstanding

2) Dilution Factor = (# Your Future Shares + Future Investor Shares)

Total Cap. + # Your Future + Future Investor Shares

2) 0.17% = (50K + 2M) (10M + 50K + 2M)

1% - 0.17% = 0.83% New Ownership

3) Your Payday at Exit* = (Your Ownership X Company Exit Price)

– (Total Exercise Price)

3) $99K* = (0.83% X $30M) - ($150K)

*Assuming $1 strike price and company acquisition price of $30MBEFORE taxes, very rough est.

Thursday, May 23, 13

Real Life Example: Tumblr Acquisition by Yahoo!How much does Founder David Karp take home?

• David Karp, CEO of Tumblr, is said to have owned about 25% of Tumblr at time of Yahoo! acquisition

• Total acquisition price = $1.1 Billion

• Total funds raised = about $125 Million

• Quick math:

$1.1 Billion total price

- 0.1 Billion returned to investors (assuming 1x liquidation preference)

$1.00 Billion for shareholders

x .25 owned by David Karp

$250 Million payout approximately

Thursday, May 23, 13

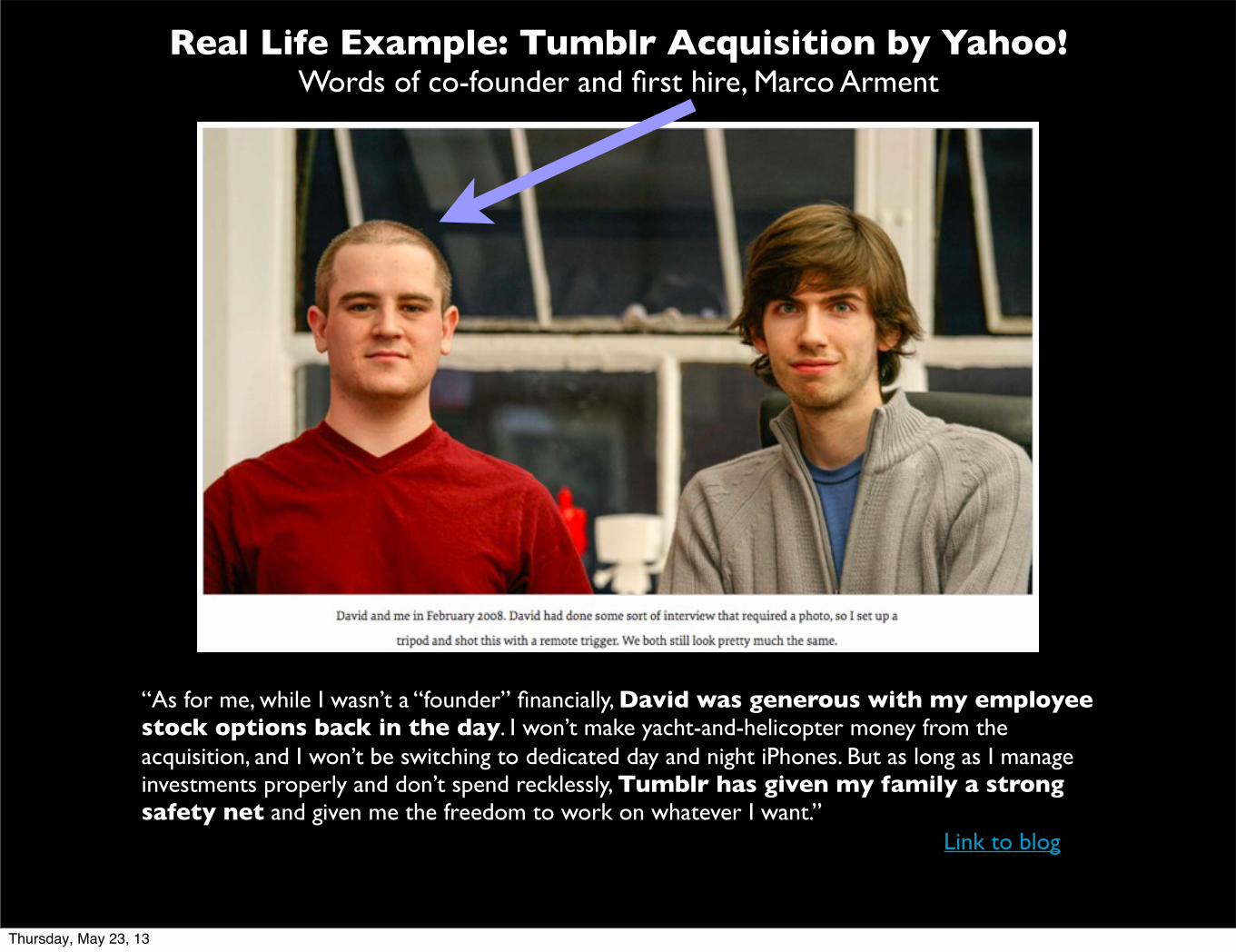

Real Life Example: Tumblr Acquisition by Yahoo!Words of co-founder and first hire, Marco Arment

Link to blog

“As for me, while I wasn’t a “founder” financially, David was generous with my employee stock options back in the day. I won’t make yacht-and-helicopter money from the acquisition, and I won’t be switching to dedicated day and night iPhones. But as long as I manage investments properly and don’t spend recklessly, Tumblr has given my family a strong safety net and given me the freedom to work on whatever I want.”

Thursday, May 23, 13

High(1)

High ReturnLow Risk

(2)High Return

High Risk

Low(3)

Low Return Low Risk

(4)Low Return High Risk

Low High

risk

return

Back to Earth: Think like an investorConsider the risk profile of your investment.

Your startup is like your baby. But let’s face it, most of us won’t work at the next Facebook or Google or Tumblr.

Brave souls featured in Read Write’s “8 Real-World Stories Of Why Startups Fail”

Failure is like a badge of honor, and a great teacher. Financially speaking, it means no return.

Yup, that’s me.

Thursday, May 23, 13

High(1)

High ReturnLow Risk

(2)High Return

High Risk

Low(3)

Low Return Low Risk

(4)Low Return High Risk

Low High

risk

return

Back to Earth: Think like an investorConsider the risk profile of your investment.

Your startup is like your baby. But let’s face it, most of us won’t work at the next Facebook or Google or Tumblr.

Brave souls featured in Read Write’s “8 Real-World Stories Of Why Startups Fail”

Failure is like a badge of honor, and a great teacher. Financially speaking, it means no return.

Yup, that’s me.

Thursday, May 23, 13

High(1)

High ReturnLow Risk

(2)High Return

High Risk

Low(3)

Low Return Low Risk

(4)Low Return High Risk

Low High

risk

return

Back to Earth: Think like an investorConsider the risk profile of your investment.

Your startup is like your baby. But let’s face it, most of us won’t work at the next Facebook or Google or Tumblr.

Brave souls featured in Read Write’s “8 Real-World Stories Of Why Startups Fail”

Failure is like a badge of honor, and a great teacher. Financially speaking, it means no return.

Yup, that’s me.

Thursday, May 23, 13

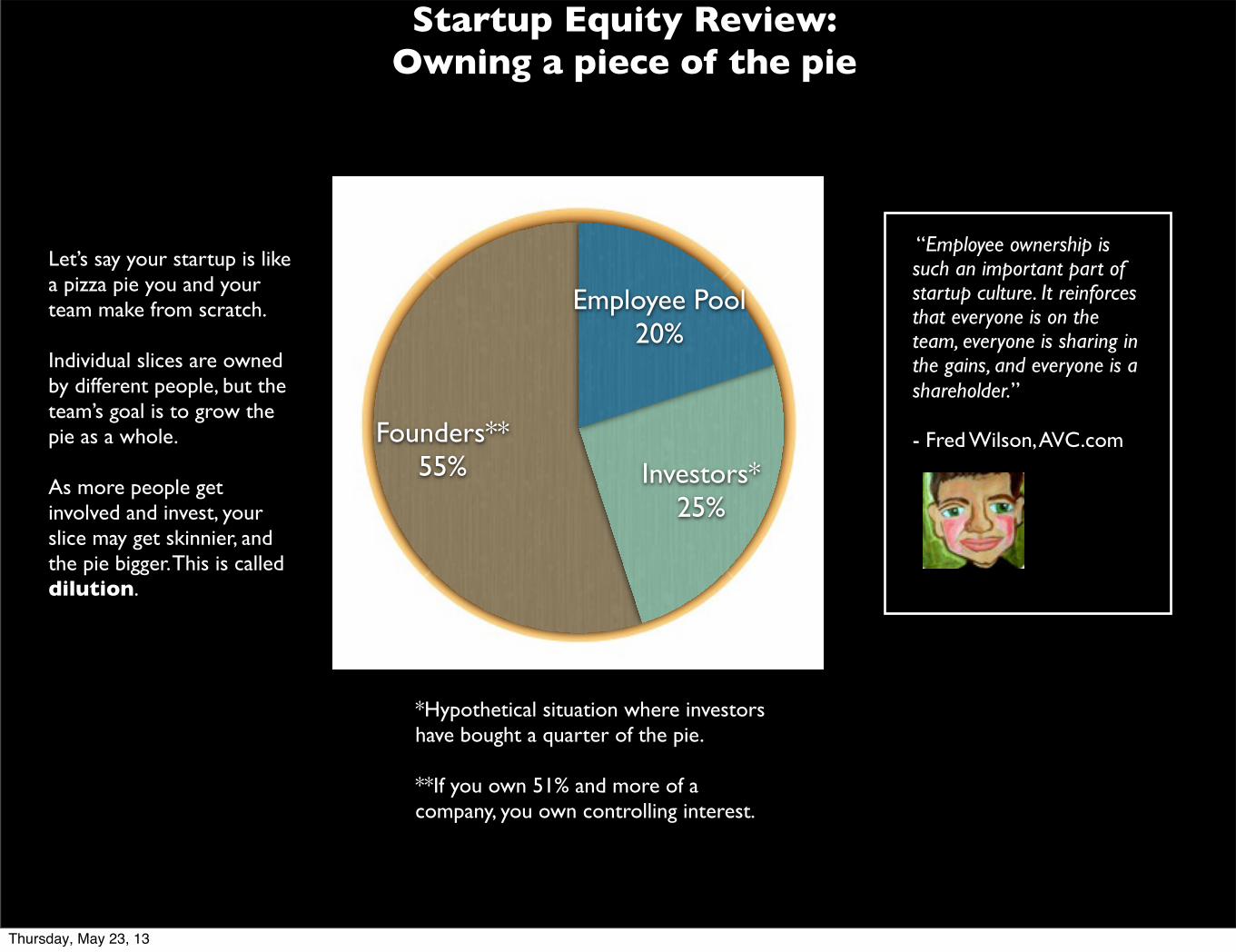

Startup Equity Review: Owning a piece of the pie

Let’s say your startup is like a pizza pie you and your team make from scratch.

Individual slices are owned by different people, but the team’s goal is to grow the pie as a whole.

As more people get involved and invest, your slice may get skinnier, and the pie bigger. This is called dilution.

Founders**55% Investors*

25%

Employee Pool20%

*Hypothetical situation where investors have bought a quarter of the pie.

**If you own 51% and more of a company, you own controlling interest.

“Employee ownership is such an important part of startup culture. It reinforces that everyone is on the team, everyone is sharing in the gains, and everyone is a shareholder.”

- Fred Wilson, AVC.com

Thursday, May 23, 13

Review: Employee Stock Ownership at a VC-funded tech startup

Typically, total non-founder employee equity pool tends to fall between 10% - 20%.

TitleOf

Total Shares

CEO 5.00 - 10.00%

C-level Executives 1.00 - 3.00%

VP, Directors 0.50 - 2.00%

Managers 0.25 - 1.00%

Board Directors 0.50%

The details of who owns what kind of ownership is spelled out in capitalization table, or cap table. It’s considered private and sensitive information.

Thursday, May 23, 13

1. Founders and founding members receive common stock. Special vesting schedule applies. ➡ TIP: draw up and execute a partnership agreement as soon as

humanly possible.

2. Restricted stocks are ownership interest issued to employees at early stage companies while the value of stock is low. Granted with certain restrictions, usually vesting, sometimes performance. Deemed taxable property. ➡ TIP: Make an 83B election within 30 days of grant to limit

future tax liability

3. Stock options are the most common form of employee equity. Options grant the right to buy stock at a pre-determined price, and is deemed taxable property of grantee. Vesting restriction is standard. ➡ TIP: Exercise early. Ask for cash bonus to cover the exercise cost

Types of Employee Equity

Apple Computer, Inc.Incorporated on Jan 3,1977

Stock value: $0

Thursday, May 23, 13

Review: Vesting Schedule

4 year vesting with 1 year cliff is common.

1 year cliff means you don’t vest during the 1st year. If you leave during this period, you leave with no equity.

Unvested equity may be repurchased by the company and returned to the employee pool.

Idea is to avoid a “hit and run” situation and to retain talented employees.

Oops

27.1%

+1 mo.

Day 1 1st year 2nd year 3rd year 4th year

0% 25% 50% 75% 100%

0 2,5002,710

5,000 7,500 10,000Vested Shares

Generally, option strike price will not change throughout vesting schedule.

Thursday, May 23, 13

$0

$25

$50

$75

$100

2013 2014 2015 2016

Company XYZ Share Price

FMV Cost to EE

100 shrs granted to EE at FMV of $1.00 with 4 year vest. EE files

83B Election recognizing income of $1 (FMV) - $1 (shr price) = $0

At end of 1 year anniversary, 25 shares vested to EE.

FMV rose to $5/shr. ($5 - $1) x 25 shares = $100

Don’t owe taxes until you sell.

After 2 years, 50 shares vested to EE. FMV rose to $25/shr.

($25 - $1) x 50 shares = $1,200 value. Don’t owe taxes until you sell.

Restricted Stock Example: 83B Election

Thursday, May 23, 13

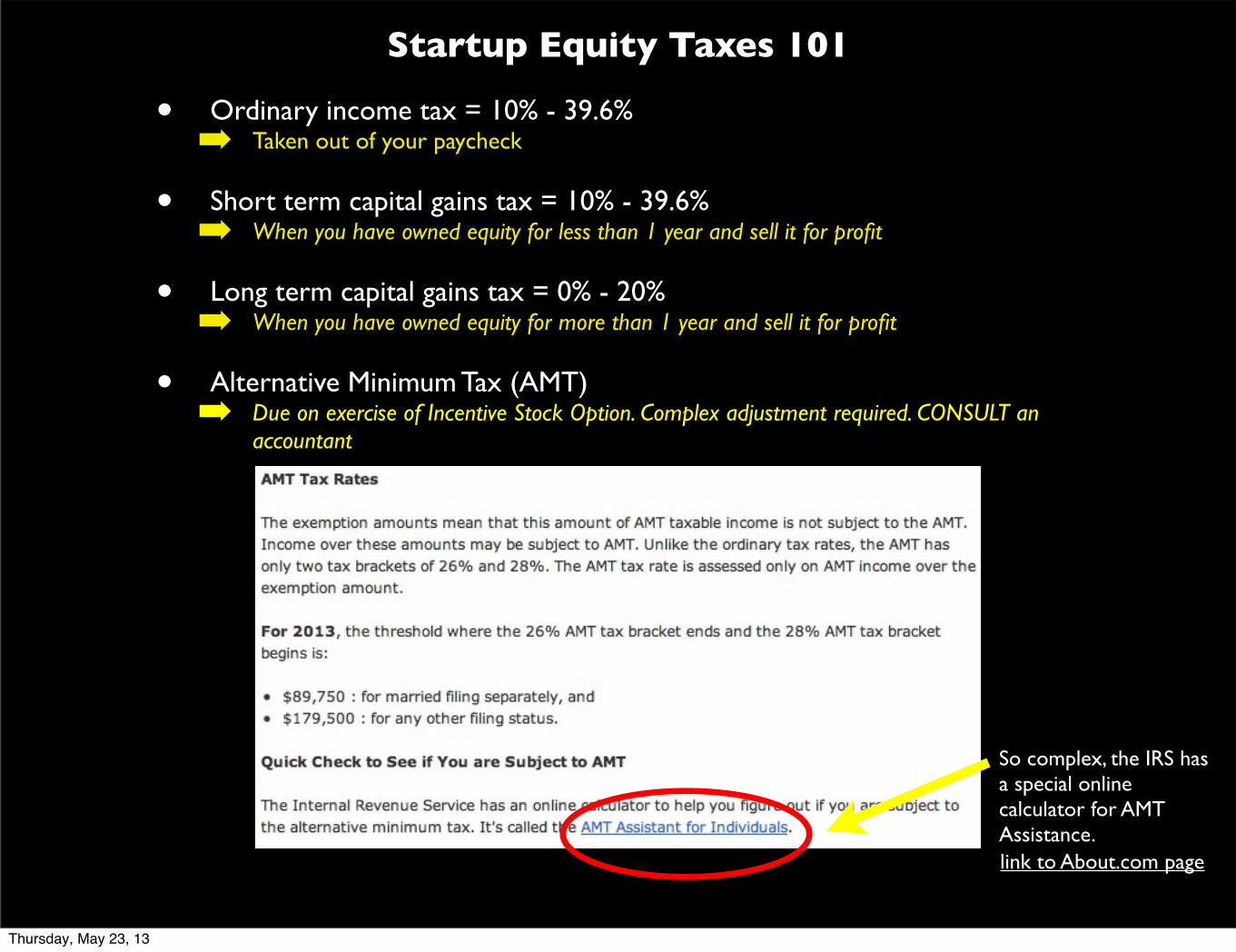

Startup Equity Taxes 101

• Ordinary income tax = 10% - 39.6% ➡ Taken out of your paycheck

• Short term capital gains tax = 10% - 39.6%➡ When you have owned equity for less than 1 year and sell it for profit

• Long term capital gains tax = 0% - 20%➡ When you have owned equity for more than 1 year and sell it for profit

• Alternative Minimum Tax (AMT) ➡ Due on exercise of Incentive Stock Option. Complex adjustment required. CONSULT an

accountant

link to About.com page

So complex, the IRS has a special online calculator for AMT Assistance.

Thursday, May 23, 13

Stock Options

Options give you the right to buy equity, not the equity out right. Exercising your option is when you buy the underlying stock at strike price.

Consider: •Restrictions, such as vesting or performance

•Strike price must equal Fair Market Value at time of grant

•Cost of exercising option

•Tax liability at exercise

•Tax liability at sale of underlying equity

‣Earn or vest it‣Exercise it & pay taxes‣Hold stock ‣Sell stock & pay taxes

Thursday, May 23, 13

$0

$15

$30

$45

$60

$75

$90

2013 2014 2015 2016 2017 2018

Company ABC Share Price and Options

FMV SOP ISO

100 options granted to EE at FMV of $10.00 with 4 year vest. Strike price is

equal to FMV at time of grant, $10. This is called “At the Money”

25 options vested to EE. She can buy 25 shares at $10 and realizes gain: (FMV $25 -

Strike price $10) X 25 shares = $375This spread between FMV and strike price

will be taxed.

If she sells the underlying stock, she will be taxed again for the profit.

2 years in, management decide to incentivize the EE with Incentive Stock Options. Similar 4 year vest. At this time, FMV is $53, so strike

price of ISO set to $53.

“Spread”

Thursday, May 23, 13

ISO vs NSO SummaryCheck out this chart for full comparison

ISO = only employees

•Complex holding periods, annual limitations

•Spread on exercise can incur Alternative Minimum Tax (AMT), a complex minefield best navigated by experienced accountants

•Selling underlying stock at long-term capital gains tax rate ONLY if holding periods are met. If not, then a mix of short-term and long-term capital gains tax rates.

•Not tax deductible to employer

NSO = employees and non-employees

•More straight-forward and less complicated

•Spread on exercise will be taxed at ordinary income tax rate

•Selling underlying stock will incur either short-term or long-term capital gains tax depending on holding period

•Deductible to employer

Thursday, May 23, 13

Equity Compensation: the Negotiables

Best if hire is C-level or executive-level, and company is pre-Series A fundraising. VC’s term sheet details can change what’s negotiable and what’s not.

• Size of grant

• Equity grant upfront (Founders stock, not options)

• Early exercise of options

• Partial vesting on the grant date

• Borrow strike price against proceeds of liquidity event, in order to exercise without being “out-of-pocket”

• Accelerated vesting if terminated without “cause”

• Accelerated vesting if company is acquired and there is change-of-control

• Single and double trigger

• Other negotiables: base salary, title, benefits and other perks

Thursday, May 23, 13

Startup Equity RECAP: More ART than SCIENCE but still need to ASK and do the MATH

Before joining a startup, ask

• Is this the right team and company for my success?

•What is my percentage of ownership?

➡ # shares you own / total shares issued

•How long is my vesting schedule?

➡ 4 years with 1 year cliff is standard

•What are tax implications?

➡Restricted stock: make 83B elections

➡Option holders: liable for capital gains tax at exercise of NSO and when stock is sold for both

•What is total company capitalization?

•What is the estimated valuation at exit?

•What do I need to do when I leave?

If you’re a founder or prospective employee,

•Research market rate salary and equity comp

➡See appendices for references

•Read the partnership and employment agreements

•Negotiate like a business person

•Consult a lawyer or tax accountant

Thursday, May 23, 13

Sources

- Andy Payne, Startup Equity for Employees: http://www.payne.org/index.php/Startup_Equity_For_Employees

- Chris Dixon, The One Number You Should Know About Your Equity http://cdixon.org/2009/08/27/the-one-number-you-should-know-about-your-equity-grant/

- Fred Wilson, MBA Monday Series on Equity: http://www.avc.com/a_vc/2010/09/employee-equity.html

http://www.avc.com/a_vc/2008/11/restricted-stoc.html

- How Stuff Works, Stock Options:

http://money.howstuffworks.com/personal-finance/financial-planning/stock-options1.htm

- Infochachkie, What The Heck Are My Startup Stock Options Worth?! Seven Questions You Should Ask Before Joining A Startup: http://infochachkie.com/options/

- Paul Graham, Equity Equation: http://paulgraham.com/equity.html

- Startup Company Lawyer, What is an 83b Election?

http://www.startupcompanylawyer.com/2008/02/15/what-is-an-83b-election/

- Startup Law Blog, Incentive Stock Options vs Nonqualified Stock Options http://www.startuplawblog.com/2013/05/15/incentive-stock-options-vs-nonqualified-stock-options/#comment-899265747

- Tax & Business Professionals, ISOs Versus Non-statutory Stock Options? http://www.unclefed.com/AuthorsRow/TaxBusProf/stockoptions.html

- Wealthfront, Manage Your Tech Career: https://blog.wealthfront.com/startup-employee-equity-compensation/

- Wealthfront, The 12 Crucial Questions About Stock Options: https://blog.wealthfront.com/stock-options-package-valuation/

- Wikipedia, Restricted Stock: http://en.wikipedia.org/wiki/Restricted_stock

Thank you!

Thursday, May 23, 13

Appendix A: LLC v. C Corp

Thursday, May 23, 13

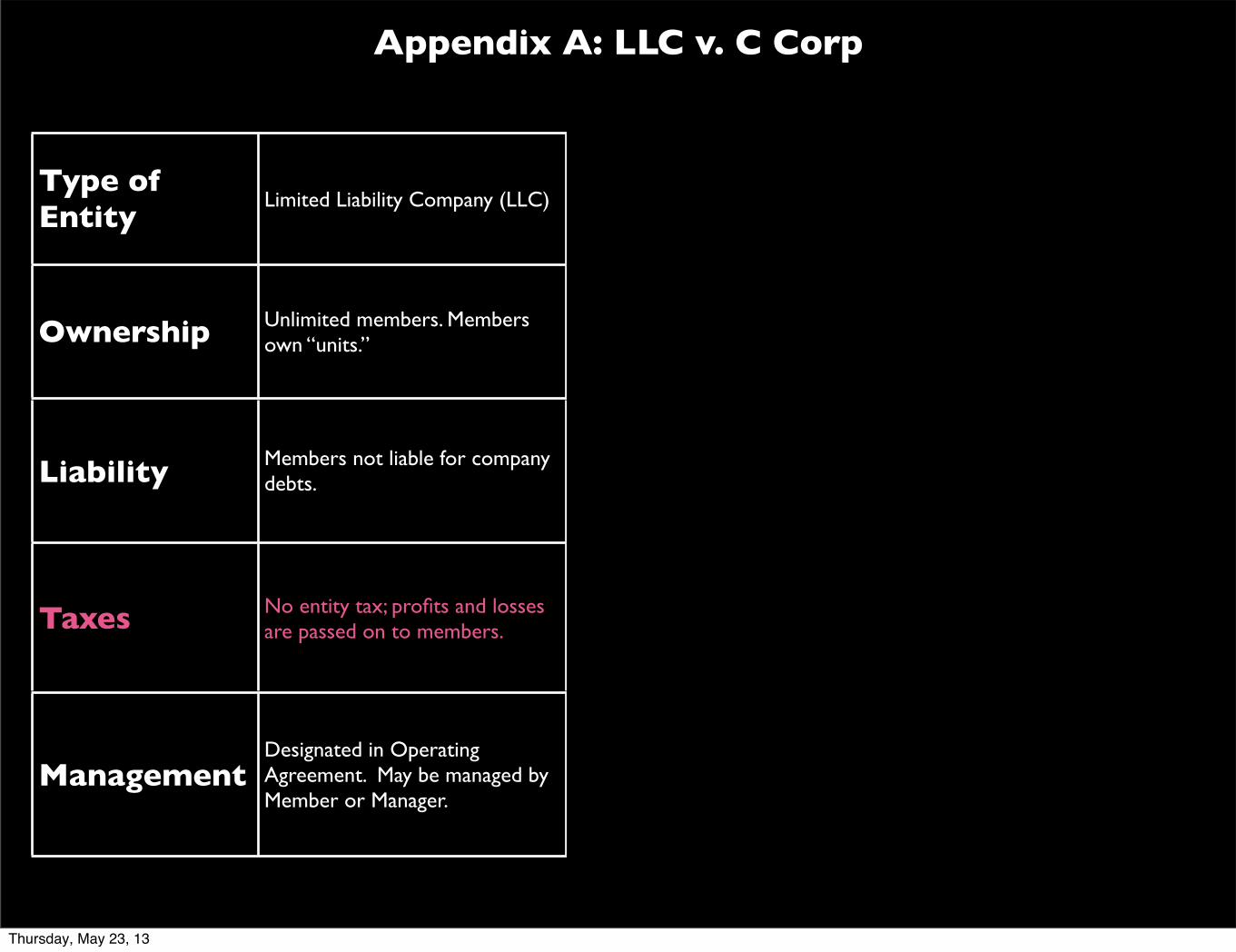

Appendix A: LLC v. C Corp

Type of Entity

Limited Liability Company (LLC) C Corporation S Corporation

Ownership Unlimited members. Members own “units.”

500 shareholders if private. No limit on shareholders if public.

Up to 35 shareholders, one class of stock allowed.

Liability Members not liable for company debts.

Shareholders not liable for company debts. Shareholders not liable

Taxes No entity tax; profits and losses are passed on to members.

“Double taxation” Company is taxed as an entity. Shareholders are also taxed.

“Double taxation” Company is taxed as an entity. Shareholders are also taxed.

ManagementDesignated in Operating Agreement. May be managed by Member or Manager.

Managed overall by Board of Directors. Officers manage day to day.

Managed overall by Board of Directors. Officers manage day to day.

Thursday, May 23, 13

Appendix A: LLC v. C Corp

Type of Entity

Limited Liability Company (LLC) C Corporation S Corporation

Ownership Unlimited members. Members own “units.”

500 shareholders if private. No limit on shareholders if public.

Up to 35 shareholders, one class of stock allowed.

Liability Members not liable for company debts.

Shareholders not liable for company debts. Shareholders not liable

Taxes No entity tax; profits and losses are passed on to members.

“Double taxation” Company is taxed as an entity. Shareholders are also taxed.

“Double taxation” Company is taxed as an entity. Shareholders are also taxed.

ManagementDesignated in Operating Agreement. May be managed by Member or Manager.

Managed overall by Board of Directors. Officers manage day to day.

Managed overall by Board of Directors. Officers manage day to day.

Thursday, May 23, 13

Appendix A: LLC v. C Corp

Type of Entity

Limited Liability Company (LLC) C Corporation S Corporation

Ownership Unlimited members. Members own “units.”

500 shareholders if private. No limit on shareholders if public.

Up to 35 shareholders, one class of stock allowed.

Liability Members not liable for company debts.

Shareholders not liable for company debts. Shareholders not liable

Taxes No entity tax; profits and losses are passed on to members.

“Double taxation” Company is taxed as an entity. Shareholders are also taxed.

“Double taxation” Company is taxed as an entity. Shareholders are also taxed.

ManagementDesignated in Operating Agreement. May be managed by Member or Manager.

Managed overall by Board of Directors. Officers manage day to day.

Managed overall by Board of Directors. Officers manage day to day.

Thursday, May 23, 13

Appendix A: LLC v. C Corp

Type of Entity

Limited Liability Company (LLC) C Corporation S Corporation

Ownership Unlimited members. Members own “units.”

500 shareholders if private. No limit on shareholders if public.

Up to 35 shareholders, one class of stock allowed.

Liability Members not liable for company debts.

Shareholders not liable for company debts. Shareholders not liable

Taxes No entity tax; profits and losses are passed on to members.

“Double taxation” Company is taxed as an entity. Shareholders are also taxed.

“Double taxation” Company is taxed as an entity. Shareholders are also taxed.

ManagementDesignated in Operating Agreement. May be managed by Member or Manager.

Managed overall by Board of Directors. Officers manage day to day.

Managed overall by Board of Directors. Officers manage day to day.

Thursday, May 23, 13

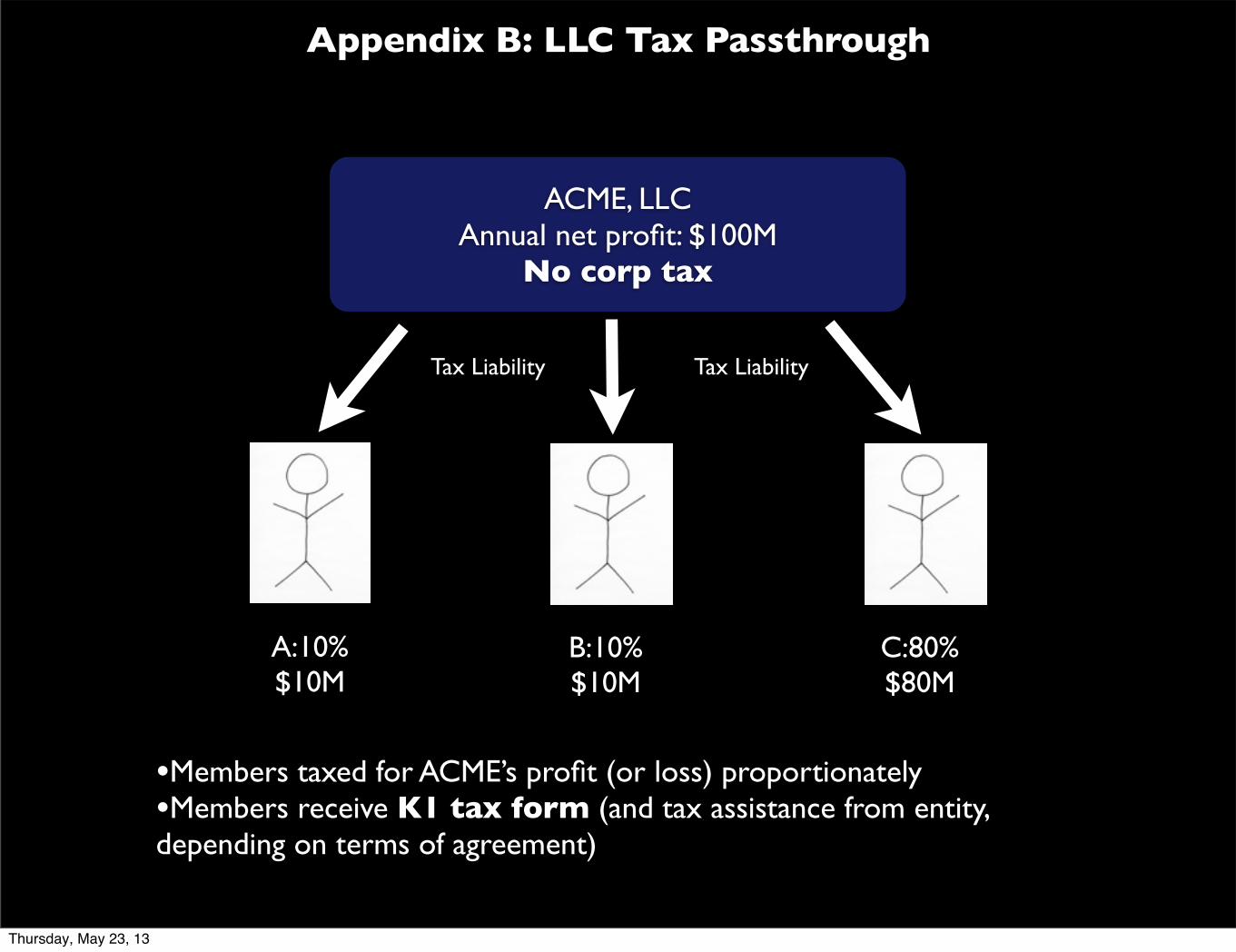

ACME, LLCAnnual net profit: $100M

No corp tax

Appendix B: LLC Tax Passthrough

•Members taxed for ACME’s profit (or loss) proportionately•Members receive K1 tax form (and tax assistance from entity, depending on terms of agreement)

A:10%$10M

B:10%$10M

C:80%$80M

Tax Liability Tax Liability

Thursday, May 23, 13

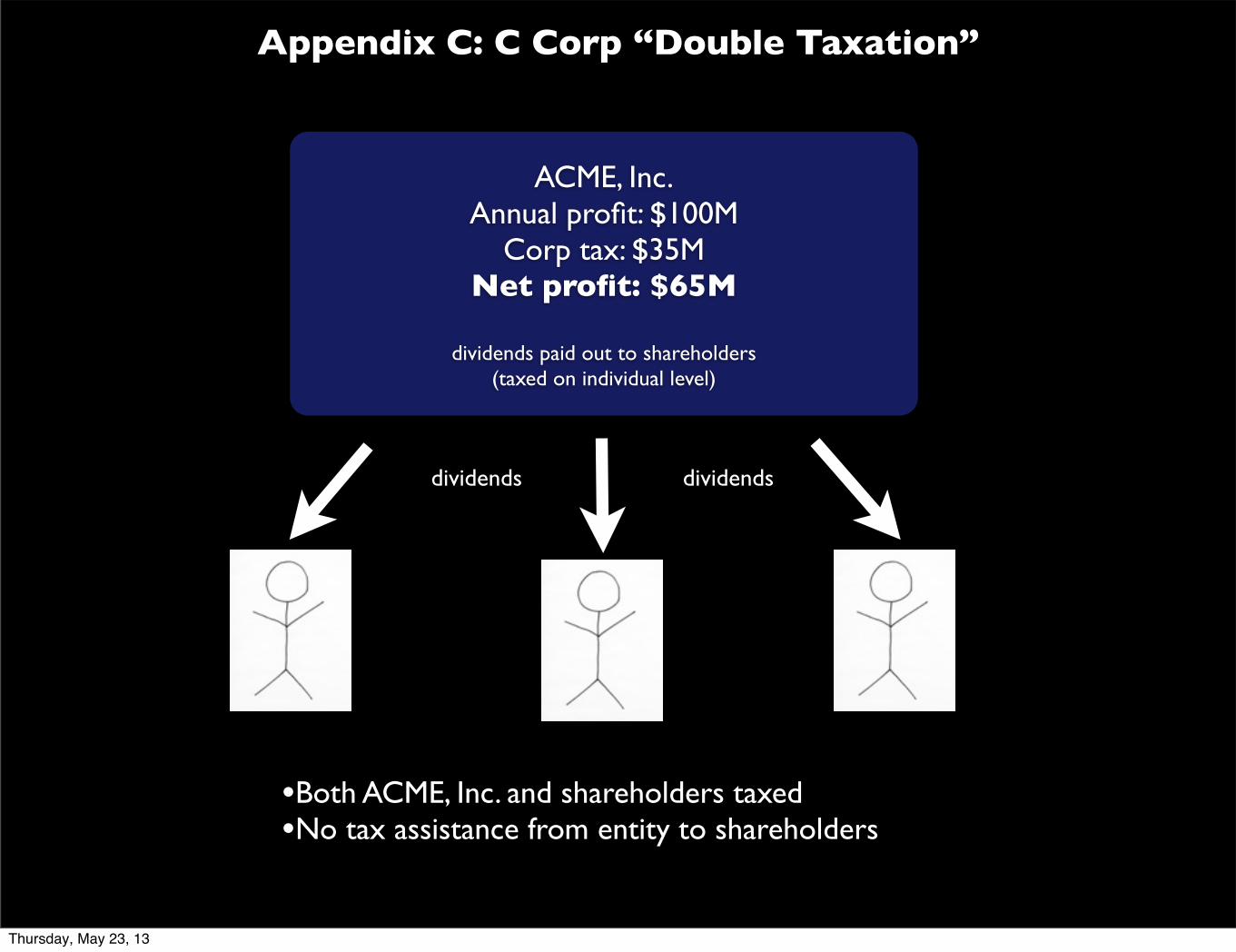

ACME, Inc.Annual profit: $100M

Corp tax: $35M Net profit: $65M

dividends paid out to shareholders(taxed on individual level)

Appendix C: C Corp “Double Taxation”

•Both ACME, Inc. and shareholders taxed •No tax assistance from entity to shareholders

dividends dividends

Thursday, May 23, 13

Appendix D: Recommended Online Resources

• Check out Anonymous Startup Salaries, Stock Options and Equity on Ackwire.com

• Check out Fred Wilson’s Cap Table Template on Google Docs

Thursday, May 23, 13

Appendix E: Recommended Online Resources

• Check out Patrick McKenzie’s Salary Negotiation: Make More Money, Be More

• Check out David Weekly’s An Intro to Stock Options

Thursday, May 23, 13