STARTING A FUND - Gemini Companies … · 2 Structure of a Mutual Fund ... Starting a Fund with...

15

P O O L E D I N V E S T M E N T S O L U T I O N S STARTING A FUND – MUTUAL FUNDS – FUNDS SOLD ON INSURANCE PLATFORMS – EXCHANGE-TRADED FUNDS

Transcript of STARTING A FUND - Gemini Companies … · 2 Structure of a Mutual Fund ... Starting a Fund with...

P O O L E D I N V E S T M E N T S O L U T I O N S

STARTING A FUND– MUTUAL FUNDS

– FUNDS SOLD ON INSURANCE PLATFORMS

– EXCHANGE-TRADED FUNDS

TABLE OFCONTENTS

6775-GFS-4/13/2016

MUTUAL FUNDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Why Advisors Launch Mutual Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Basic Fund Facts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

STARTING A MUTUAL FUND . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Frequently Asked Questions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Structure of a Mutual Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Timeline and Costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

FUNDS SOLD ON INSURANCE PLATFORMS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Similarities to a Traditional Mutual Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Key Differences from a Traditional Mutual Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Challenges of Distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Wholesaling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

EXCHANGE-TRADED FUNDS (ETF) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

ETF Attributes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Challenges of Starting and Managing an ETF . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Getting Started . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Key Players . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

How the Funds Work . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Being Profitable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Starting a Fund with Gemini Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

INDUSTRY TERM DEFINITIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

1

While there are many operational benefits for advisors to start a mutual fund, it is important to realize that mutual funds are an increasingly attractive vehicle for your investors for the following reasons:

DIVERSIFICATION Investors are provided with the benefit of instant diversification and asset allocation without the large amounts of cash needed to create individual portfolios. Typically, through the use of diversification, a reduced portfolio risk may be achieved.

ECONOMIES OF SCALE Mutual funds are able to take advantage of their buying and selling size which leads to a reduction in transaction costs for investors.

LIQUIDITY Mutual funds transact on a daily basis after the close of the stock market, making them a liquid asset.

TRANSPARENCY AND OVERSIGHT Mutual funds have a clearly defined investment objective/strategy with set investment parameters, per the fund prospectus. Investments are monitored on a post trade basis by the fund administrator and Securities and Exchange Commission (SEC) to ensure compliance to the stated investment strategy. Investments, fees, etc. are reported quarterly, semi-annually and annually to shareholders and regulators, which means they have a public record.

PROFESSIONAL MANAGEMENT Investors are able to track their investment periodically, knowing that they have a registered investment advisor dedicating their time to research potential investments and monitoring the strategy.

TAX & PURCHASING SIMPLICITY The purchasing of mutual funds is simplified through a broker, and a 1099 tax filing provides ease and consistency for investors.

Figures in this document are estimates and may not apply to your fund.

WHY ADVISORS LAUNCH MUTUAL FUNDS

Advisors start their own investment vehicles for many reasons. Mutual funds provide advisors with the following advantages:

– New distribution opportunities to market their funds to the retail public, other advisors, and broker-dealers – An increase in operational efficiencies – Reduced transaction costs

MUTUAL FUNDS

BASIC FUND FACTS

Registered as investment companies under the Investment Company Act of 1940 (‘40 Act)

Primarily regulated by the SEC and the Financial Industry Regulatory Authority (FINRA)

Extensive disclosure, reporting, governance and other requirements pursuant to the ‘40 Act

May be advertised and offered to retail investors

Interests must be registered with the SEC pursuant to the Securities Act of 1933, and the mutual fund is subject to the reporting requirements of the Securities Exchange Act of 1934

Past performance information is generally only allowed for offered fund

Hypothetical results cannot be included

Must have a Board of Directors, 40% of which must be independent

Generally, the person or entity who manages the portfolio must be a registered investment advisor under the Investment Advisors Act of 1940

Must have at least $100,000 in seed capital

2

STARTING AMUTUAL FUND

We receive many questions about starting a mutual fund and have narrowed them down here to the most frequently asked questions. Please note that the details given to each question are general representations and Gemini Fund Services, LLC (Gemini Fund) would be delighted to discuss your specific needs on an individual basis.

Which investment strategies work in a ‘40 Act vehicle?The flexibility available often surprises managers. While there are limitations on the amount of leverage available, many strategies work within the ‘40 Act structure. These include tactical asset allocation, managed futures, distress debt, global distressed, long/short equity, market neutral, arbitrage, absolute return, real estate, quantitative, and strategic asset funds.

How long does the process take?It takes typically four months to register a mutual fund. Much of this is taken up by the SEC review process.

Are there minimum assets under management?There is no minimum size restriction for a mutual fund, but unless the manager is willing to cover the fund’s costs themselves, a certain minimum amount of assets under management is recommended to cover administration costs. Mutual funds typically break even around $15 million, which covers the costs of administration, transfer agent, shareholder reporting, board oversight and compliance.

What are the costs for creation and ongoing operating costs?Set up and organizational costs range from $45,000 to $100,000 (not including platform addition fees) depending on the complexity and the structure of the fund.

At a minimum, annual mutual fund operating expenses (not including sales & marketing expenses) are approximately $175,000 to $200,000. These fees cover fund administration, annual audit, shareholder reporting and support, transfer agent, corporate governance and compliance.

What are the management fee options?Mutual fund fees typically approach those of their peer group. A manager would not want his fees to be much higher than those of similar funds, especially if he wants to promote the fund through the broker and RIA distribution channels. Annual management fees typically range from 75 bps up to 150 bps, but can approach 200 bps.

Can performance be ported over from a hedge fund or SMA strategy to the mutual fund for marketing purposes? What are the rules about porting or using past performance? Generally porting performance is an area that requires analysis for any specific strategy or fund. Some hedge fund performance can be ported if the hedge fund meets these criteria:

– The fund must have multiple investors.

– Utilize the same investment strategy; the ‘40 Act fund must generally follow the same investment strategy as the originating hedge fund.

*Porting performance generally requires the original hedge fund to close and convert into a mutual fund. A manager may instead wish to start a mutual fund that mirrors his existing unregistered fund. In both cases, the manager can disclose the performance of the unregistered vehicle or SMA in the mutual fund’s prospectus if the new fund follows similar investment strategies and provided that certain other conditions are met.

*Even though the SMA performance may be allowed in the Fund’s prospectus, it cannot be used in the Fund’s marketing materials.Figures in this document are estimates and may not apply to your fund.

3

How do I stop cannibalization of investors from my existing hedge strategy?Hedge fund managers are obviously concerned that their investors may switch into the less-expensive mutual fund. Hedge funds can mitigate this risk by applying institutional strategies, leverage, and exposure to their alternative investment, thus keeping their more sophisticated investors aligned with the goals of the fund.

How does the Board & Compliance work?Gemini Fund provides the option of a turnkey solution. Our series trusts, the Northern Lights Fund Trusts and Two Roads Shared Trust, provide a board of directors and compliance oversight. The mutual fund benef its from the economies of scale available through the use of these shared resources.

How does distribution work?In today’s market, distribution generally occurs through a platform or broker channel. Most mutual funds charge a 12b-1 fee, typically through an A-share class to help with the compensation of the distributor. Funds can benef it from Gemini Fund’s sister f irm, Northern Lights Distributors, LLC, (NLD) which has more than 500 selling agreements with dif ferent broker and fund platforms and is a member of FINRA. NLD provides a complete suite of supporting services including FINRA compliance oversight, Strategic Relationship Managers and additional distribution opportunities.

Mutual fund managers may want to consider hiring a third party marketing f irm or their own fund wholesaler to market the fund directly to the individual registered representatives.

What are the restrictions?

DIVERSIFICATION: 50% of a mutual fund’s assets must be invested in diversified assets. This means 50% of a fund’s assets must be in holdings of 5% or less. A mutual fund can also satisfy the diversification requirement by investing in other registered investment companies, such as mutual funds or ETFs. Cash and cash products are always considered a diversified investment.

LEVERAGE: Mutual funds cannot exceed 33% leverage. This rule refers to leverage used by the fund itself and not to any underlying funds. The underlying investments can use leverage, and levered ETFs can be a useful part of a portfolio.

DERIVATIVES: Mutual fund investments in derivatives are allowed with some restrictions, although tactical allocation to certain ETFs can provide a pass through.

SHORTING: Mutual funds can sell short. It requires a tri-party collateral account with the bank and broker with assets segregated to cover the positions. An alternative approach could be a tactical allocation to certain ETFs that sell short themselves.

COMMODITIES: While there is no direct limit on commodity investments, a mutual fund must receive 90% of its income through passive investments. Commodities are considered non-passive. However, investments in commodity ETFs can be treated as equity (pass-through) but they may be tax inefficient. This differing tax treatment depends on how the ETF is structured. Most ETFs disclose the expected tax treatment and advisors should consult with the tax department of their administrator. Most Exchange Traded Notes (ETNs) are 1933 Act structures and can be treated as passive income for tax purposes.

DAILY REDEMPTION: Mutual funds have daily net asset value (NAV) calculations and daily redemptions. Because of the possibility of daily redemption, most mutual funds keep a certain amount of cash available at all times.

ILLIQUID ASSETS: Mutual funds must provide daily liquidity, so illiquid assets are limited to 15%. Closed-end funds can have 100% illiquid assets and are traded on the exchange under their own ticker. Another option is a closed-end interval fund which can accept daily inflows, but withdrawals are restricted typically to quarter-ends. Closed-end funds require their own trust and distribution agreements.

INVESTMENTS: There are percentage restrictions on investments into other mutual funds and hedge funds.

Figures in this document are estimates and may not apply to your fund.

7170-NLD-4/4/2016

4

NORTHERN LIGHTS FUND TRUSTS I, II, III, IVPartners with advisors to provide advantages like joint marketing exposure and advisor networking opportunities for mutual funds.

FUNDS: 155+

ASSETS: $13.7 billion+

LAUNCH DATE: 2006, 2011, 2012, 2015

TWO ROADS SHARED TRUSTPartners with advisors to provide support for traditional and alternative mutual funds.

FUNDS: 12 and several in registration

ASSETS: $1.6 billion+

LAUNCH DATE: 2012

NORTHERN LIGHTS VARIABLE TRUSTPartners with advisors to provide support for mutual funds which are sold exclusively through insurance providers

FUNDS: 27+

ASSETS: $3 billion+

LAUNCH DATE: 2006

STRUCTURE OF A MUTUAL FUNDAll mutual funds are registered with the SEC in a trust format. Advisors can choose to launch their funds in either a shared or series trust or they can launch their fund in a stand alone trust.

A shared or series trust is comprised of independent funds, all managed by separate advisors. This means your fund would be registered in a trust with other funds but you are still fully in control of managing your fund as an independent advisor. Gemini Fund offers several series trust options. Your fund would share some costs with other funds in the trust, easing the financial burden for you as the advisor for costs incurred while running a fund. Your fund would also share a board of trustees with every fund in the trust, which saves you as the advisor time and money because you do not have to recruit trustees and form your own board.

A stand alone trust is a trust comprised of only your firm’s mutual fund(s). Your firm is responsible for all costs for your fund(s), however Gemini Fund will help you form your own board of trustees, and align all other services the trust needs.

Gemini offers multiple series trusts, giving you several solutions to meet your needs. They include:

Figures in this document are estimates and may not apply to your fund.

+As of 3/31/16

5

TIMELINE AND COSTSCreation costs, time to market, the SEC review process, various fees and more are different for funds in a series trust or stand alone model. Below highlights some key differences between starting a stand-alone trust vs. joining one of our series trusts.

As you can see above, starting a fund in a series trust takes approximately 120 days, depending on how quickly each stage progresses.

STAND ALONE TRUST SERIES TRUST

CREATION COSTSVariable based upon service provider selection – approx. $60k - $100k

Lower cost because of negotiated agreements – approx. $45k - $75k

TRUSTEES / BOARDAdvisor appoints trustees and establishes new board

Use of existing board and trustees

TRUST INDEPENDENCE Minimum of 40% independent trustees Minimum of 40% independent trustees

TRUSTEE FEES Variable based upon selection Typically lower cost because of shared service

PLATFORM FEES Must establish new agreements for trustMany existing trust level agreements can be shared and can lower additional fees

LEGAL SERVICES Advisor nominates, Trust approves Use established legal counsel

AUDIT SERVICESTrust evaluates and approves with Advisor recommendation

Trust evaluates and approves with Advisor recommendation

CCO Advisors recommends, Trust approves Use established CCO

CUSTODY SERVICESTrust evaluates and approves with Advisor recommendation

Trust evaluates and approves with Advisor recommendation

CREATION TIMELINE Approximately 4 - 6 months Approximately 4 months

SEC REVIEW Variable, no set time 75 days

15C PROCESS AND APPROVAL Yes Yes

CONVERTIBLE Yes Yes

ON-GOING BREAK-EVENVariable based upon service provider selection – typically higher (approx. $25-30 million)

Typically lower cost because of shared service and negotiated agreements(approx. $15-20 million)

SEED AUDIT $100k requirement to begin seed audit No seed audit

ESCROW At Board’s discretion At Board’s discretion

BRANDING Trust and fund level Fund level

Figures in this document are estimates and may not apply to your fund.

6

The cost to launch a mutual fund varies based on whether the fund is created inside a series or stand alone trust. Total costs range from $45,000 to $75,000 for a series trust and $60,000 to $100,000 for a stand alone trust. Through a waiver of their management fee and/or reimbursement by the advisor, the advisor is responsible for all fund expenses until the assets in the fund hit the break-even amount, upon which the fund’s expenses are paid for by shareholder fees. Not including sales and marketing costs for the fund, the operational break-even amount for most funds is $15-20 million for a series trust and $25-30 million for a stand alone trust.

There are multiple costs that make up the fees for creating a fund. These include a consultation fee, paid to Gemini Fund, of $15,000. Once you have engaged an outside legal firm (which includes an engagement letter), they will require you to pay a retainer of approximately $15,000 to $20,000, based on the requirements of your fund.

During days 30-90 of your fund’s creation process, you will be billed the remaining legal fee from your outside counsel, minus the retainer. Costs usually run between $10,000 and $15,000, based on your fund’s requirements; for a total legal creation cost of $25,000 to $35,000. If you engage our sister f irm, Northern Lights Compliance Services, LLC (NLCS), for their chief compliance off icer services, you will be billed for their services also during days 30-90 for your on-site due diligence visit. These costs vary depending on their travel expenses for airfare, hotel, etc. and the complexity of your fund. This cost typically ranges between $2,500 to $5,000.

There are additional out of pocket expenses to be aware of that are fund expenses but will need to be paid out of pocket by the advisor prior to the fund launch. These items are required around the f inal stages of your fund being effective or ready for launch but before you actually choose to go operational and launch the fund. All of the below fees are reimbursed to the advisor once the fund is operational or launched.

The chart below describes each stage and approximate timing of each stage. Please note: If you’re launching a fund in a stand alone trust, the timeline can be longer.

DRAFTING 30 DAYS

Begin Compliance Due Diligence Questionnaire / Visit

Begin 15c Material

Preliminary Board (varies)*/ Drafts Finalized

Custody Call & Accounting Call

Shareholder Servicing Call (optional)

Tax and Compliance Call

CAN NOW LAUNCH( LAUNCH DATE DETERMINED

BY ADVISOR )

DAYS1 - 30

DAY30

DAYS31 - 104

DAYS105 - 119

DAY120

ENGAGEMENT 12 DAYS

TRADING BEGINS

SEC COMMENTS 30-45 DAYS AFTER FILING

QUIET TIME: BEGIN TO THINK ABOUT MARKETING AND DISTRIBUTION CONTINUE WEEKLY

OPERATIONAL CALLS

FINAL WEEKLYOPERATIONAL CALL

BEGIN WEEKLY OPERATIONAL CALLS

LEGAL RETAINER / DRAFTING BEGINS RED HERRING CONTINUES EFFECTIVE WITH SEC( RED HERRING ENDS )

STRIKE NAV/OPERATIONALEngage Gemini / Retainer

Client Services Call

Questionnaires

Red Herring Period Definition: a quiet period of time extended from the time a company files a registration statement with the SEC until SEC staff declared the registration statement effective. During that period, the federal securities laws limit what information a company and related parties can release to the public.

* Board dates and requirements are specific to each board.** Only applicable if (NLD) Northern Lights Distributors, LLC, Member FINRA is the Fund’s named distributor.

FILE WITH SEC

BEGIN RED HERRING (75 DAYS)

NLD DISTRIBUTION CALL**

NLD MARKETING/TECH CALL**

FILE WITH SEC

DAY121

CREATION TIMELINE - SUBJECT TO CHANGE / ALL DATES ARE ESTIMATEDCREATION TIMELINE - SUBJECT TO CHANGE / ALL DATES ARE ESTIMATED

Figures in this document are estimates and may not apply to your fund.

0004-NLCS-4/12/2016

EDGAR FILING FEES

Typically $2500 to $7500 (depending on stand alone vs. series trust)

NASDAQ REGISTRATION FEES

$0. As of January 2016, they no longer charger an initial fee (They do charge an annual maintenance fee)

CUSIP REGISTRATION FEES

Approximately $275 for initial class, $20 for each additional

STATE BLUE SKY REGISTRATION FEES FOR INITIAL TRUST LEVEL STATES

Approximately $1760 for Series Trust and $10,740 for a Stand Alone Trust (Trust Only Filings)

7

FUNDS SOLD ONINSURANCE PLATFORMS

An investment company interested in distributing their separate accounts strategy to an additional audience or a mutual fund company looking to add a distribution channel may want to consider launching a fund that can be offered on insurance platforms. Shares of these funds are offered to separate accounts of participating life insurance companies for the purpose of funding variable annuity contracts and variable life insurance policies. Because these funds are tax-deferred, some investors seek them out in place of their IRA accounts.

SIMILARITIES TO A TRADITIONAL MUTUAL FUNDFunds on insurance platforms, registered as part of a variable insurance trust with the SEC, are very similar to traditional mutual funds. However, there are not as many funds on insurance platforms as there are mutual funds in existence. Because the competition is limited, many investment companies consider launching a fund in this channel. An investor looking to select funds for their variable annuity or variable life insurance policy are only allowed to select from an insurance companies platform, hence providing a captive audience for those funds on their platform.

KEY DIFFERENCES FROM A TRADITIONAL MUTUAL FUNDThere are just a few differences between a traditional mutual fund and a fund on an insurance platform.

A fund inside an insurance wrapper, also known as a variable insurance trust, will have slightly different diversif ication requirements than a mutual fund.

They are also required to have the same year-end close date as the associated insurance carrier.

Because insurance companies are participating in the sales and marketing of funds on their platforms, the 12b-1 fees for these funds are higher.

To stay competitive with other funds on these platforms, management fees and expense limitations are typically lower.

TIMELINE AND COSTSPlease refer to the Mutual Fund timeline and cost sections. These are very similar for a fund on an insurance platform.

CHALLENGES OF DISTRIBUTIONThe main difference between a mutual fund and a fund inside a variable insurance trust, lies in the distribution process. Obtaining a selling agreement between a traditional mutual fund and a broker-dealer platform can be time consuming, costly and involve a very detailed due diligence process. There are many exceptions to this and many broker-dealers that are open to accepting a multitude of mutual funds on their platforms.

In order for a fund inside a variable insurance trust to be offered by an insurance carrier, that fund must be added to that insurance product platform. The insurance carriers, much like the broker-dealers are for a mutual fund, decide which funds to add to their platforms. Their process can also be time consuming and involve a very detailed due diligence process. Insurance carriers only add funds to their line up two times per year, in May and November. Because they do offer a limited amount of funds on their platform, it may be challenging for a new fund to gain entry.

It’s important to note that while there are some open architecture insurance companies who will add your fund to their platform, most of the time, it’s much harder to gain access to insurance company platforms. It’s up to the fund company to develop relationships with insurance carriers in order to be added. And that’s just part of the equation - an insurance company must be receiving demand for your fund in most cases before they will allow your fund to be sold on their platform.

WHOLESALINGDistribution varies in other ways for a fund on an insurance platform. Most investment companies have a wholesaling team just for these funds, which differs from the wholesaling team for their mutual fund. Because the insurance company is offering a limited selection of funds, it’s important a wholesaler develops relationships with the insurance carrier representatives.

To help the fund’s wholesalers maintain visibility with these representatives, they could build a schedule of:• Joint events • Presentations to representatives • Regular office visits • Drip campaigns

Figures in this document are estimates and may not apply to your fund.

8

EXCHANGE-TRADED FUNDS (ETF)

We are partnering with advisors to develop pooled investment solutions, in the form of ETFs, to help them capture the growing demand for ETF products.

ETF ATTRIBUTESTRANSPARENCYETFs are required to publish their holdings at the end of each business day with the Depository Trust & Clearing Corporation (DTCC).

Investors can see which securities and how much of each security the ETF holds and therefore what they are buying into.

DISTRIBUTIONETFs are bought and sold on the open exchange, eliminating the need for traditional mutual fund platforms like Schwab or Pershing.

Eliminating the traditional platforms means there is no need for selling agreements. The fund is available for purchase by the public with no need for the due diligence process required by mutual fund platforms. There is no minimum to buy into ETFs, making them available to many more investors who may not have the stated minimum investment required by most mutual funds.

INTRA-DAY TRADING Because ETFs are traded like stocks, investors can use tools like limit orders to purchase shares only at a certain price. ETFs can be bought using strategies like shorting, which indicates an investor’s prediction the ETF’s underlying securities will decline.

NO MARKET TIMING RULESAnother potential benefit of the stock-like trading structure of ETFs is there are no market timing rules. Investors are not required to hold ETF shares for any length of time.

LIQUIDITYLiquidity is typically measured in daily trading volume, but this does not apply to ETFs. Instead, liquidity can be measured by the degree to which a market maker can create or redeem shares of the ETF without moving the market of the underlying securities.

Typically the market maker creates or redeems a large order of shares without it affecting the value of the underlying securities.

ETF trading specialist firms can also redeem shares, but do so in an effort to optimize your expenses without moving the market.

TAX EFFICIENCY ETFs have the potential to be more tax efficient than mutual funds because sales occur between investors. Through in-kind redemptions between the custodian bank and market maker, capital gains are not realized within the ETF when turnover occurs. If a mutual fund has a large redemption by a shareholder, the manager may need to sell fund holdings that could include appreciated stocks. The capital gains realized from this sale are distributed within the fund. Also, all shareholders of a mutual fund receive their per share portion of the tax burden for the stated year, regardless of how long the investor has owned the fund or even if the investor did not own the fund when the gains were realized.

Figures in this document are estimates and may not apply to your fund.

9

CHALLENGES OF STARTING AND MANAGING AN ETFHigher creation costs and lower expense ratios create a higher break-even point for ETF managers. Gemini offers advisors a solution to combat these higher costs through our ETF Trust. Our shared trust allows advisors to share costs like those incurred through compliance or board services.

Incentivizing investors to purchase your fund is much more difficult and requires a distribution strategy. ETFs are sold to the general public, but ETF transactions do not include the incentive fees of a 12b-1 fee like mutual funds for broker dealer platforms and broker dealer representatives. Your distribution strategy must include a plan for differentiating your ETF through education based on the reason to purchase your ETF and how it could be used within a portfolio.

GETTING STARTEDETF MUTUAL FUND

REGISTRATION

– Investment Company Act of 1940

— or —

– Securities Act of 1933

– Investment Company Act of 1940

— and —

– Securities Act of 1933

UNDERLYING SECURITIES

– Strategy and focus outlined in prospectus

– Tracks index, sector, commodity, or currency

– Can hold securities outside of tracked entity

– Strategy and focus outlined in prospectus

– Can purchase or hold any security that qualifies

under the strategy in prospectus

DOCUMENTATION – Prospectus– Prospectus

– Statement of Additional Information (SAI)

START-UP PROCESS

– Advisor selects or creates index to track

– Advisor works with legal counsel to get SEC approval for prospectus

– Advisor secures seed money

– Advisor engages transfer agent, custodian and authorized participants (AP) or market makers

– Gemini sets up the ETF with its fund accounting and fund administration services

– Advisor drums up demand for ETF

– AP delivers basket of underlying securities to custody bank in return for a specific number of ETF shares, thus making a creation unit

– Advisor secures seed money

– Advisor outlines objectives, strategies, and benchmarks

– Advisor works with legal counsel to get SEC approval for prospectus and SAI

– Advisor meets with trust board of directors for approval

– Gemini sets up the fund with its fund accounting, fund administration, and transfer agent services

– Open accounts with custody bank

START-UP COSTS– $50,000 to $100,000+

– Dependent upon exemptive order used

– $40,000 to $100,000

– Dependent upon creation of fund within series trust or as stand-alone fund

TIMELINE TO CREATE – Variable (can be several months) – Approximately 4 months

Figures in this document are estimates and may not apply to your fund.

10

KEY PLAYERS

HOW THE FUNDS WORK

ETF MUTUAL FUND

CREATION

– Administrator– Legal Counsel– Custody Bank– Authorized Participant (AP) or Market Maker– Board of Directors

– Administrator– Legal Counsel– Custody Bank– Board of Directors

OPERATIONS– Administrator– Fund Accountant– Transfer Agent

– Administrator– Fund Accountant– Transfer Agent

BUYING AND SELLING– Market Makers– ETF Trading Specialists– Investors in secondary market

– Broker/dealer platforms– Wirehouses– Independent broker/dealers– Direct from transfer agent

MARKETING OR DISTRIBUTION

– Advisor’s in-house marketing department – Advertising agency

– Broker/dealers – Third party marketers (3PMs)– Advisor’s in-house marketing department – Advertising agency

ETF MUTUAL FUND

PRICING

– Net asset value (NAV) calculated at end of business day based on value of underlying securities– Inter-day trading is based on bid/ask price, similar to stocks

– NAV calculated at end of business day based on value of underlying securities– Shares purchased today will be purchased at today’s calculated NAV

BENCHMARKS – Own entire index to deliver beta of benchmark – Employ teams of analysts and strategies to outperform beta and generate alpha

DIVIDENDS

– Dividends are paid to investors’ brokerage accounts, then investors must complete another purchase to reinvest the dividends– Often paid quarterly, but frequency is determined by advisor

– Most mutual funds offer an automatic reinvestment option, but shareholders can opt to receive dividend payment– Required to pay dividends at least once a year, frequency is determined by advisor

PURCHASE STRATEGIES

– Can be sold short or held long– Options contracts allow investor to call or put shares in the future at a specific price– Utilize limit orders, like stocks

– Can only be purchased at the NAV of the day the order is placed

BUYING PROCESS

– Investor goes to ETF specialist to browse list of available ETFs– ETF specialist takes investor’s purchase order– Market maker fills order for specialist– If order is larger than number of available shares from market maker, the market maker will have AP bundle more of the underlying securities according to the ETF’s index. – Except for initial purchase of new shares, all trades are between investors on the open market

– Investor browses list of funds available to his brokerage account through the corresponding platform– Investor places order through account– Broker purchased corresponding shares for investor

— or —– Investor can purchase shares directly from fund

Figures in this document are estimates and may not apply to your fund.

11

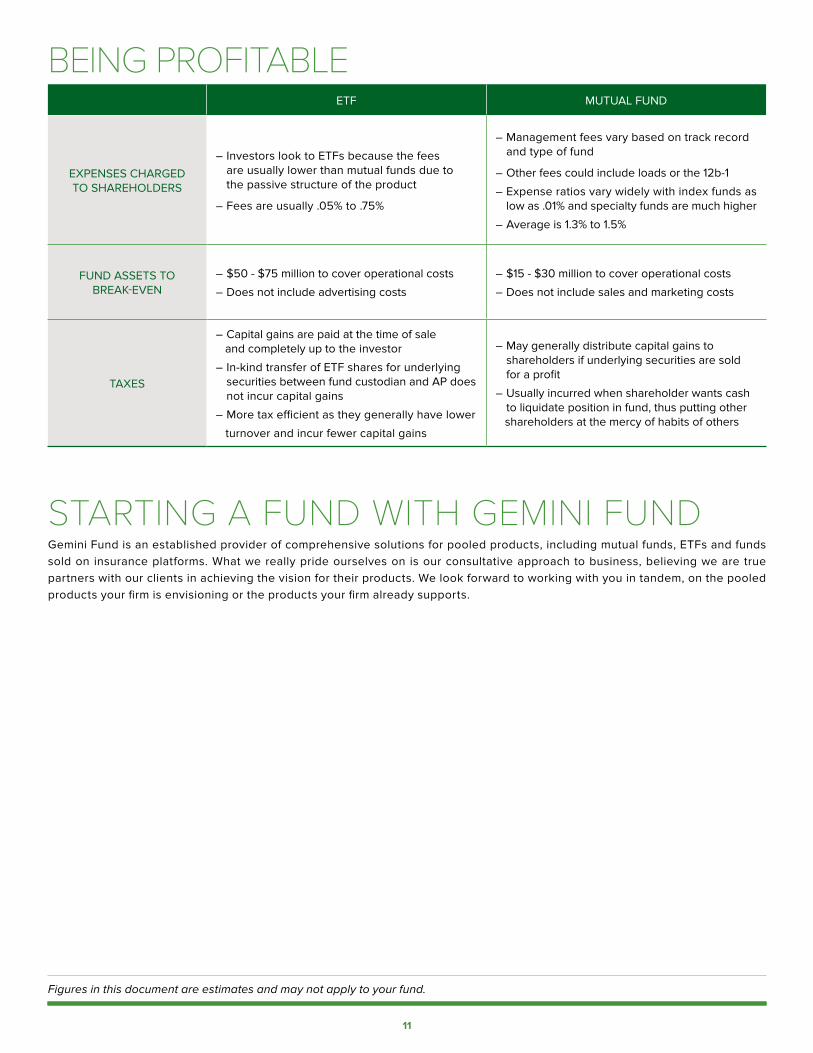

BEING PROFITABLEETF MUTUAL FUND

EXPENSES CHARGED TO SHAREHOLDERS

– Investors look to ETFs because the fees are usually lower than mutual funds due to the passive structure of the product

– Fees are usually .05% to .75%

– Management fees vary based on track record and type of fund

– Other fees could include loads or the 12b-1

– Expense ratios vary widely with index funds as low as .01% and specialty funds are much higher

– Average is 1.3% to 1.5%

FUND ASSETS TO BREAK-EVEN

– $50 - $75 million to cover operational costs

– Does not include advertising costs

– $15 - $30 million to cover operational costs

– Does not include sales and marketing costs

TAXES

– Capital gains are paid at the time of sale and completely up to the investor

– In-kind transfer of ETF shares for underlying securities between fund custodian and AP does not incur capital gains

– More tax efficient as they generally have lower

turnover and incur fewer capital gains

– May generally distribute capital gains to shareholders if underlying securities are sold for a profit

– Usually incurred when shareholder wants cash to liquidate position in fund, thus putting other shareholders at the mercy of habits of others

STARTING A FUND WITH GEMINI FUNDGemini Fund is an established provider of comprehensive solutions for pooled products, including mutual funds, ETFs and funds sold on insurance platforms. What we really pride ourselves on is our consultative approach to business, believing we are true partners with our clients in achieving the vision for their products. We look forward to working with you in tandem, on the pooled products your firm is envisioning or the products your firm already supports.

Figures in this document are estimates and may not apply to your fund.

12

INDUSTRY TERM DEFINITIONS

ALPHAa measure of performance on a risk-adjusted basis that takes the volatility (price risk) of a mutual fund and compares its risk-adjusted performance to a benchmark index (like the S&P 500). The excess return of the fund relative to the return of the benchmark index is a fund’s alpha and essentially represents the value the portfolio manager adds to (or subtracts from) a fund’s return.

AUTHORIZED PARTICIPANT (AP) the entity chosen by an ETF advisor with the responsibility of obtaining the underlying assets needed to create an ETF and then transferring the assets to the custodian bank to create shares of the ETF.

BETAmeasure of volatility corresponding to the security’s response to swings in the market.

BPSbasis point, a unit equal to 1/100th of 1% or .01%

CALLan option contract giving the owner the right (but not obligation) to buy a specified amount of a security at a specified price within a specified time.

CREATION UNITset of shares that makes up one unit of an ETF. One creation unit is the denomination of underlying assets that can be redeemed for a certain number of ETF shares.

ETFexchange-traded fund, a security that tracks an index, a commodity or a basket of assets like an index fund, but trades like a stock on an exchange. ETFs experience price changes throughout the day as they are bought and sold.

ETF TRADING SPECIALISTmember of an exchange who acts as the market maker to facilitate the trading of a given ETF. The specialist holds an inventory of the ETF, posts the bid and ask prices, manages limit orders and executes trades. Specialists are also responsible for managing large movements that influence supply and demand.

EXEMPTIVE ORDERunder current SEC regulations, ETFs must have an order from the SEC to operate that exempts them from certain regulations under the Investment Company Act of 1934 and Investment Company of 1940. The structure of ETFs would not otherwise be allowed under these two acts.

13

GEMINI FUND SERVICES, LLC | 80 Arkay Drive, Suite 110, Hauppauge, NY 11788 | 855.891.0092 | www.geminifund.com

INVESTMENT COMPANY ACT OF 1940defines the responsibilities and limitations of fund companies that offer investment products.

LIMIT ORDERan order placed with a brokerage to buy or sell a set number of shares at a specified price or better. Limit orders also allow an investor to limit the length of time an order can be outstanding before being cancelled.

LONG POSITIONbuying a security with the expectation that the asset will rise in value.

LONG/SHORT EQUITY a mutual fund strategy that mimics some of the trading strategies typically employed by hedge funds. Unlike most mutual funds, long/short funds use leverage, derivatives and short positions in an attempt to maximize total returns, regardless of market conditions. The amount of leverage used and the number of derivatives and short positions that long/short funds may contain are limited by law. These funds invest primarily in stocks.

MARKET MAKERbroker/dealer f irm that assumes the risk of holding a certain number of shares of a security in order to ease the process of trading the security.

NET ASSET VALUE (NAV)a fund’s price per share value. The per-share dollar amount of the mutual fund or ETF is calculated by dividing the total value of all the securities in its portfolio, less any liabilities, by the number of fund shares outstanding.

PASSIVE INVESTMENTmirrors a market index.

PASSIVE MANAGEMENT fund’s portfolio mirrors a market index. Is the opposite of active management in which a fund’s manager attempts to beat the market with various investing strategies and buying or selling decisions.

PUTan option contract giving the owner the right (but not obligation) to sell a specified amount of a security at a specified price within a specified time.

SHORT POSITIONselling a security with the expectation that the asset will fall in value.