Standard presentation August 2005 - coloplast.com · Investor presentation. 2 Coloplast ... • The...

46

Coloplast A/S Investor presentation

Transcript of Standard presentation August 2005 - coloplast.com · Investor presentation. 2 Coloplast ... • The...

Coloplast A/SInvestor presentation

2

Coloplast

Coloplast products and services help patients achieve greater independence from medical challenges in 5 areas:

Ostomy care, continence care, wound care, skin care and breast care.

39%* 24% 12% 5% 7%

*Percentage of total group sales (2003/04)

3

0

1000

2000

3000

4000

5000

6000

7000

1957

1962

1967

1972

1977

1982

1987

1992

1997

2002

History of revenue growth 1957-2004m

DKK

Danish productionand sale through

distributors

Product divisionsand subsidiaries

Acquisitions

Forward integration

4

Sales and production world wide

Austria

BelgiumGermany

Great Britain

Italy

Sweden

Norway

Argentina

Australia

Brazil

Canada

USA

France

Holland

Hungary

Poland

Spain

Japan

Switzerland

Israel RussiaCzech Republic SloveniaSlovakiaCroatia South Africa

Denmark

Costa Rica

Portugal

China

5

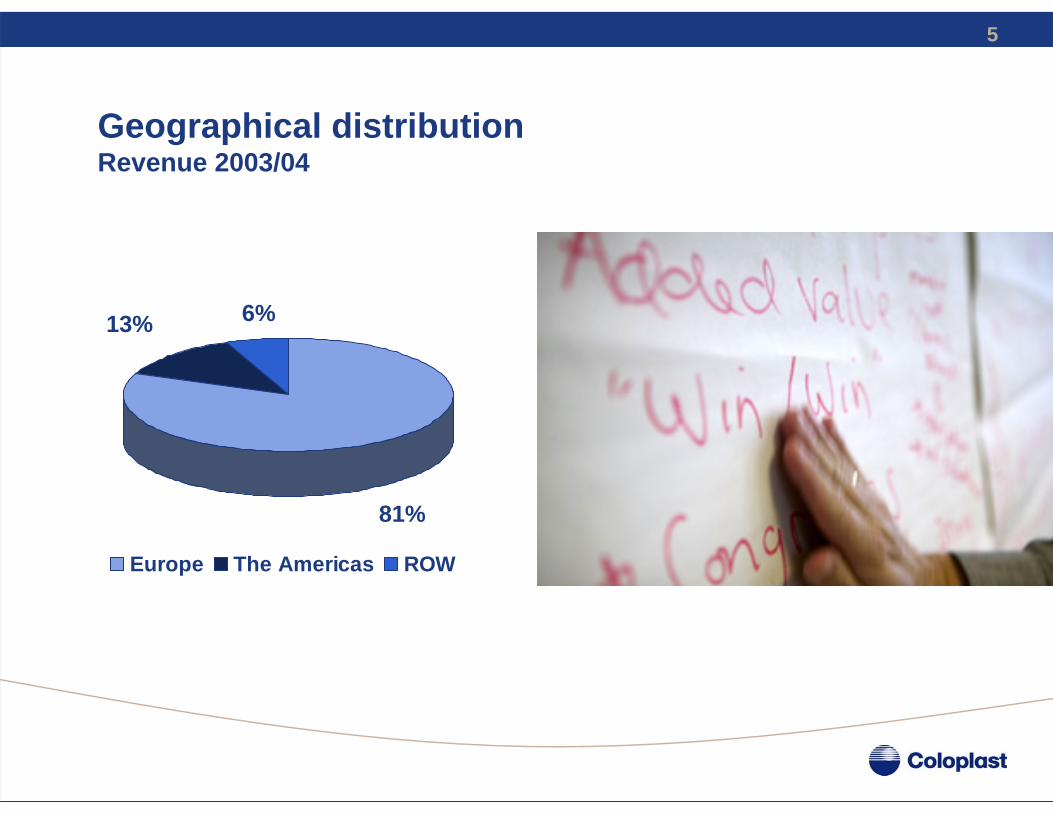

Geographical distribution Revenue 2003/04

Europe The Americas ROW

81%

6%13%

6

Innovation rate*

0

5

10

15

20

25

30

35

98/99 99/00 00/01 01/02 02/03 03/04

% o

f sal

es

Grouptarget

* Share of products in sales with less than 4 years of age

7

Macro trends

Trend

Description

Demographics

Population aged 60 or older is growing steadily in Europe, Asia and North America…

… and with higher demands for health care

Changing lifestyles triggered by improved wealth

Health care reforms

Health care budget constraints…

… lead to the need for cost containment programmes…

… through co-payment and consumption capitation

Power todistribution

The major distributors grow their share...

...through both retail pharmacy, home care and parallel importing...

...changing them to competitors, not customers

All issues have been on the agenda for years

8

Market conditions and response

1. Reimbursement changes• Monitor/influence policy• Product design• Emphasis on clinical

documentation

2. Price pressure• Observe market trends• Improve tendering capabilities

3. Harmonisation of health care systems• Monitor development

Market growth influenced by:• Earlier cancer detection• Improved surgical procedures• Increased longevity• New technologies and treatment

alternatives• Slowdown in conversion from

older products

9

Three key customers

• The end customer• The user, primary concern

is quality of life• The health care professional

• The advisor, primary concerns are user qualityof life and handling

• The payer• Concern is primarily

product pricing

10

Competitor overview

Total corp.

% of total

Turn

over

by

busi

ness

are

a(D

KK

m)

Ostomy care

Continence care

Wound care

Skin care

ConvaTec

Hollister

Mentor

Astra Tec

h

S&N

J&J

Coloplast

4% 80%12%20%67% ½% ¼%

11

Business StructureGroup Management

Woundcare

Breastcare

Skinhealth

Ostomycare

Continencecare

Volume

production

Americas

Europe,South

Europe,North

RoW

Chronic care segment SBU segment

Corporate functions

Sales

12

Ostomy care - for discreet protection

• Normal function of bowel or bladder lost

• Almost 80% related to cancer

• Designed for security, skin-friendliness, discretion, ease of use and comfort

• Wide variety of bags, plugs and accessories

13

Ostomy care - market dataGlobal market value DKK 8-8½bn

Europe (>4bn)

ConvaTec Coloplast Hollister B Braun Other

28%

37%

24%

5%6%

USA (<2bn)

55%

4%

39%

2%

Note: Only markets where Coloplast is present are included

35%

28%

27%

10%

Global (>8bn)

14

Continence care - for independent living

• Spinal cord injured, multiple sclerosis, spina bifida

• Discreet and easy-to-use solutions

• Catheters, urine bags, urisheaths, bowel management, absorbentproducts

15

Continence care - market data

No direct competitors--1.0bn DKK2%

>60%

30% (value)

43%

Coloplast marketshare (Europe)

Maincompetitors

Coloplastgrowth

Marketsize

Productarea

Mentor, Hollister, Rochester, Manfred Sauer

0-3%0.5bn DKK0-3%

Bard, Hollister, Mentor, B Braun, Manfred Sauer, Unomedical

5%1.2bn DKK0-5%

Astra Tech, Porges/Mentor, Rüsch, Rochester, B Braun

15-20%1.5bn DKK15%

16

Chronic care - US market positioning and key goals

• Strong product portfolio• Convex baseplate, EasiClose

• Market access through GPO/IDN• Consorta• Large number of IDN contracts

• Significant growth in new patient discharge• Sustained OC hospital growth > 30%

• Sustained OC/CC growth > 20%• Reach two-digit ostomy market share within 3-5 years• Develop intermittent coated catheter market segment

17

Chronic care - US market value

Ostomy market value 280mn USD Continence market value 370mn USD

Other2%

Coloplast4%

CvT56%

Holl38%

Intermittent Coated Cathetersestimated value potential 60 mill. USD, 16% of total CC

18D

istri

butio

n

Hospital Home Health Agencies Retail DME

Chronic care - US patient path

Payer source - Medicare, Medicaid and private insurance

2-5 Days 90 Days - 20 Years30-90 Days

Patie

nt p

ath

Patient at homeNew patient Convalescent patient(at home or in long-term care inst.)

Direct sales, wholesalers and specialised home care providers

Medical product manufacturerGPO

19

Home care value chain

Coloplast Subs.

Wholesaler Pharmacy

Passive distribution

Active distribution

Homecare

Hospitals

Value PropositionInnovation Relationship

20

Coloplast home care activities

Leading provider in the US of ostomy, wound care, urological, and diabetic products and cost management services. Ownership since 2001.

Distribution of ostomy, continence care and wound care products in the UK. Cutting service for ostomists. Internal merger of Coloplast Direct (1996) and ThackrayCare(2001). Established 2004.

German market leader in active distribution. Distributing 1/3 of all ostomy bags in Germany. Ownership majority since 2001.

21

Effects of changing market conditions in Germany

Jan 05

Oct 04

Jul 0

4Apr 0

4Ja

n 04

CC draft fornew prices

OC finaldecision

CC final decisionpostponed

OC pricereduction

OC draft fornew prices

Implementation ofhealth care reform

Introduction ofpatients‘ co-paymentfor medical devices

Reimbursement onauxiliary productsremoved

CC final decision

Dec 04

Exp 20

06Oct

03

Stockingby users,additionalsales

Mar

ket c

ondi

tions

Mar

ket e

ffect

s Retail anticipateslower prices,dampenedsales.Comparison with Q1 03/04

De-stockingby users,dampenedsales, higheradmin. costs

Alignment tochanged marketconditions

22

German market impact on Coloplast

• Reform impacts 1-1.2bn DKK turnover (ostomy and continence care)

• Coloplast is German market leader in ostomy• HSC is German market leader in distribution

- distributing 1/3 of all ostomy products• Activities will be aligned to changed market

conditions from 2005• Expectations for 2004/05 affected by 1-2

percentage points on top line and profit margin• Objectives for 2008 are maintained

23

Wound care - providing better outcomes

• For difficult to heal wounds• leg ulcers, pressure sores,

diabetic ulcers• Primarily affects the elderly• Portfolio of advanced, active

dressings• Education, information

and service

24

€ 1.0 billion€ 1.0 billion

Wound care - market definition

Moistwound healing

Drywound healing

ChronicAcute

€ 0.5 billion

€ 1.0 billion€ 1.5 billion

Wound type

Pharma and biotech

VAC

€ 0.1 billion

€ 0.4 billion

Active

€ 0.4 billion

€ 0.1 billion

Prod

uct t

echn

olog

y

€ 1.1 billion segment, growth 9-11%

Compression

25

27%

17%14%

11%

21%

10%

Convatec S&NColoplast J&JMölnlycke Others

Wound care - market shares in EuropeMWH and active products

XXMölnlyckeXXXJ&JXXColoplastXXS&NXXConvaTec

ActiveAdvancedTraditionalTechnology

26

Skin health - for medical and personal use

• To treat skin problems arising from medical conditions or related to frequent hand washings

• Designed for cleansing, moisturising, protection and treatment

• Skin health includes US wound care sales

• 3/4 of SBU turnover generated in the US

27

Skin health - product positioningPATIENT INTERVENTIONS

INTACT SKIN

Risk Factors- Dry skin

- Immobility- Incontinence

ALL PATIENTS

Intact Skin

Moisturising

Skin breakdown

Skin repair

+ Barriers

+ Wound care

+ Cleansing

Bathing

+ Wound cleansing

Intact Skin

CLINICIAN

Han

d hy

gien

e

28

Long-term care

Skin health - competitors4bn DKK US market

0

20

40

60

80

100

0 20 40 60 80 100

Sales setting (%)

Acute

Wound

Skin

Prod

uct m

ix (%

)

29

Breast care - for peace of mind

• Attached, lightweight and soft breast forms, partial breast shapers, lingerie and swimwear

• Breast cancer affect approx. 10% of women

30

Breast care business case1bn DKK global market

• 45% total market share (breastforms, partials, textiles)

• >50% market share for breast forms

• 50/50 sales value split between US and Europe

• Incidence of cancer in women is increasing

• Number of breast-saving surgeries increasing

• US market hit by low demandColoplast

Anita

TruLife

AmericanBCAirway

ThämertOthers

Partials

Bras

Swimwear

OthersBreast Forms

Segmentation by product groupColoplast sales value

Competitor overview

31

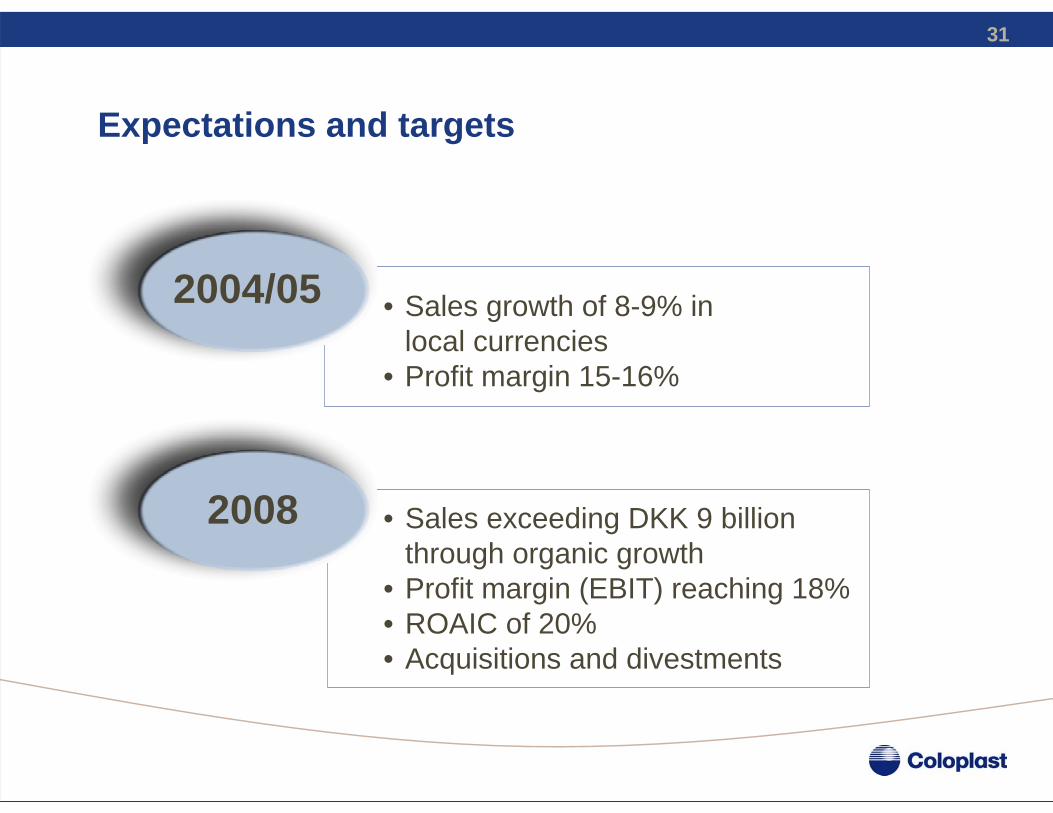

Expectations and targets

• Sales growth of 8-9% inlocal currencies

• Profit margin 15-16%

• Sales exceeding DKK 9 billionthrough organic growth

• Profit margin (EBIT) reaching 18%• ROAIC of 20%• Acquisitions and divestments

2004/05

2008

32

Key figures Q3 2004/05

-0-19Special items

-9633859284

93107

Index vs2003/04

17%433

-3-226662-87

7494,468

9 months2003/04

15%414

-1-192607-73

6994,786

9 months2004/05

EBIT

Profit marginGroup profitMinority interestsTaxProfit before taxFinancial items

RevenuemDKK

33

Growth Q3 2004/05- local currencies

2-6%5-8%

9-11%9-12%

(3)-(1)%

Est. market growth

4%8%

18%

5%

9%8%6%4%

12%(3)%

4%

Growth Q1 2004/05

GrowthH1 2004/05

Growth Q3 2004/05

5%10%23%

7%11%22%

EuropeAmericasROW

7%8%Coloplast total

9%9%8%8%7%

(1)%5%

9%10%

9%9%8%4%7%

Ostomy CareContinence CareChronic Care segment*Wound CareSkin HealthBreast CareSBU segment

Continence Care (24%)Ostomy Care (39%)

Other (13%)

Wound Care (12%)Breast Care (7%)Skin Health (5%)

*Includeshomecare

34

Breast Care sales rebound at 4% growth- Growth in both US and Europe

Wound Care sales increase of 9%- Growth back on track- Biatain Ag and Altreet Ag silver dressings introduced in France

Continence Care growth by 10%- SpeediCath Compact still fuelling growth- New reimbursement prices in Germany expected in 2006

Ostomy Care continues to outperform market growth - Solid US and RoW growth, restructuring in Germany- Corsinel well accepted, Strong Easiflex growth

Highlights markets

35

Profit and margins - how to reach 18%…

• Relocation- Hungary and China

• Efficiency projects / abc

• SBU margin improvement

• Economies of scale0

200

400

600

800

1000

1200

99/00 00/01 01/02 02/03 03/0410

11

12

13

14

15

16

17

EBIT EBIT %

mn %

36

Volume productionProduct life cycle stages

Introductionand

development

Growth Decline

Maturity

Time

Sales

37

Tatabanya, Hungary

• 700 headcounts by Aug. 2005• Construction completed• DKK 1.5bn sales value in 2005/06• EBIT up 5% compared to

Danish manufacturing

• Phase I - finalised: ostomy bags, urisheaths• Phase II - finalised: ostomy bags, dressings, catheters• Phase III - finalised 2005: Assura ostomy bags, baseplates, adhesives

Coloplast, Phase I-III, Tatabanya, Hungary

38

Coloplast’s total staff requirements by geography

Total staff requirements (FTEs) by geography, 2003/04-2010/11

0

500

1.000

1.500

2.000

2003

/0420

04/05

2005

/0620

06/07

2007

/0820

08/09

2009

/1020

10/11

FTEs

DKHUCN

39

Cash flow

-1500

-1000

-500

0

500

1000

1500

96/97

97/98

98/99

99/00

00/01

01/02

02/03

03/04

3Q 04

/05

mD

KK

Acquisitions

Investments

Cash flow

Free cash flow

40

Oil prices

• Energy consumption• Fixed price contract 2006-2008

• Cost of goods sold• Polymer raw material price increase

• Transportation of goods• Diesel oil price increase

41

42

Coloplast consolidated figures

1 EBITDA defined as Profit before depreciation as stated in the Accounts2 Net Interest Expense defined as Interest Expense less Interest Income3 Total Debt defined as Short Term Bank Loans and Mortgages plus Long Term Bank Loans and Mortgages4 Net Debt defined as Total Debt less Cash and cash equivalents

As per 30 September 2004

577567768405292Coloplast’s share of profit for the year

8921603148Net financial expenses2

988909875618498Operating profit

2,3572,0021,5621,2131,637Total equity capital

1,4651,4731,4711,121334Net debt42,2062,3011,7911,395509Total debt3

1,2951,2061,157878720EBITDA1

6,0695,6105,5674,0183,556Net turnover

03/0402/0301/0200/0199/00mDKK

43

Coloplast key financial ratios

1317144448EBITDA/Net interest, ratio

Coverage

2121212220EBITDA margin

10101084Total debt/total capitalisation, %

11312212712846Net debt/EBITDA, ratio

Leverage

1616161514Operating profit margin

Profitability03/0402/0301/0200/0199/00As per 30 September 2004

44

Investments - tangible assets

-100

0

100

200

300

400

500

600

700

97/98 98/99 99/00 00/01 01/02 02/03 03/04

Adjustment, tangible assets under construction

Plant & machineryLand & buildings

mD

KK

45

5 year share price development

46

Shareholders as per 30 September 2004

-2.5592Coloplast A/S*14.824.85,960Foreign instit. investors

97.5100.022,2001,800Total

-1.7405Non-registered shareholders*5.08.42,014Other shareholders

10.918.34,390Danish instit. investors

66.844.38,8391,800Holders of A-shares

Voting rights, %

Owner-ship, %

B-shares1,000 units

A-shares1,000 units

*No voting rights