Stable Value Investment Association (SVIA) Conference Value Investment Association ... Conference...

34

Stable Value Investment Association (SVIA) Conference April 2013 Goldman Sachs Asset Management

Transcript of Stable Value Investment Association (SVIA) Conference Value Investment Association ... Conference...

Stable Value Investment Association

(SVIA) Conference

April 2013

Goldman Sachs Asset Management

Introduction

Four key areas of focus regarding our take on current environment:

1. Global Impact on the US Market

2. Current US Trends

3. Key Risks to GS Outlook

4. GS Investment Recommendations

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice.

1

Global Impact on the US Market

Current US Trends

Key Risks to GS Outlook

GS Investment Recommendations

Outlook on the US Economy

Ripple Effects US economic growth trend should remain positive

We expect to continue to feel the impact of fiscal policies

Tail risk from European financial crisis appears to have been mitigated

for now

Quantitative monetary easing planned by the BOJ is expected to have a

positive impact on markets

Trending US financial system is largely healthy

Improving consumer spending and corporate balance sheet

Healthier housing market

Growing energy boom in the US

Premature / excessive tightening of fiscal and/or monetary policy

Reassertion of the European sovereign crisis

Re-emergence of China growth concerns

Geopolitical shock

Unexpected inflationary pressures

Key Risks

Source: Goldman Sachs. This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or

investment advice. As of March 2013.

2

3

China: While Hard Landing Concerns Have Been Mitigated For Now…

Source: Goldman Sachs. (1) Jim O’Neill, Goldman Sachs Asset Management. Source: Plot Tool. Plot tool is a proprietary analytical tool and database representing developed and emerging markets including the

US, Europe, Asia, and Latin America for their respective Fixed Income, Equity, Foreign Exchange, Commodities, and Credit Markets covering thousands of cash, forward, futures, options, and swap instruments.

Plot tool houses over 20 years of economic data. The views and opinions expressed may differ from those of GSAM or other departments or divisions of Goldman Sachs and its affiliates. This information

discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. Investors are urged to

consult with their financial advisors before buying or selling any securities.

China Real GDP Growth (YoY)

Growth forecasts for the next 10 years are ~7%1, consistent with a view of successful policy

management. These levels should support US growth and are in line with lower concerns about the

Chinese financial sector

6.0

7.0

8.0

9.0

10.0

11.0

12.0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Yo

Y G

DP

Gro

wth

(%

)

China Real GDP YoY Growth

4

…Uncertainty Remains

Source: PBOC, Wind, Gao Hua Securities Research estimates. Plot tool. Plot tool is a proprietary analytical tool and database representing developed and emerging markets including the US, Europe, Asia, and

Latin America for their respective Fixed Income, Equity, Foreign Exchange, Commodities, and Credit Markets covering thousands of cash, forward, futures, options, and swap instruments. Plot tool houses over

20 years of economic data. The views and opinions expressed may differ from those of GSAM or other departments or divisions of Goldman Sachs and its affiliates. This information discusses general market

activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. Investors are urged to consult with their financial

advisors before buying or selling any securities. The economic and market forecasts presented herein are based on proprietary models for informational purposes as of the date of this presentation. There can be

no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation.

Leadership Transition

Proactive Government Policies

China’s Shadow Banking Activity Continues to Grow

Sh

ad

ow

Ba

nkin

g a

s %

of

To

tal C

red

it

China needs to grow consumer demand without excessive reliance on expansion of credit

1.0

1.5

2.0

2.5

3.0

3.5

4.0

-6.0

-5.5

-5.0

-4.5

-4.0

-3.5

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

Jan-2010 Jul-2010 Jan-2011 Jul-2011 Jan-2012 Jul-2012 Jan-2013

Avg of Italian & Spanish 10y Spread to Germany (LHS, Inverted) US 10y (RHS)

5

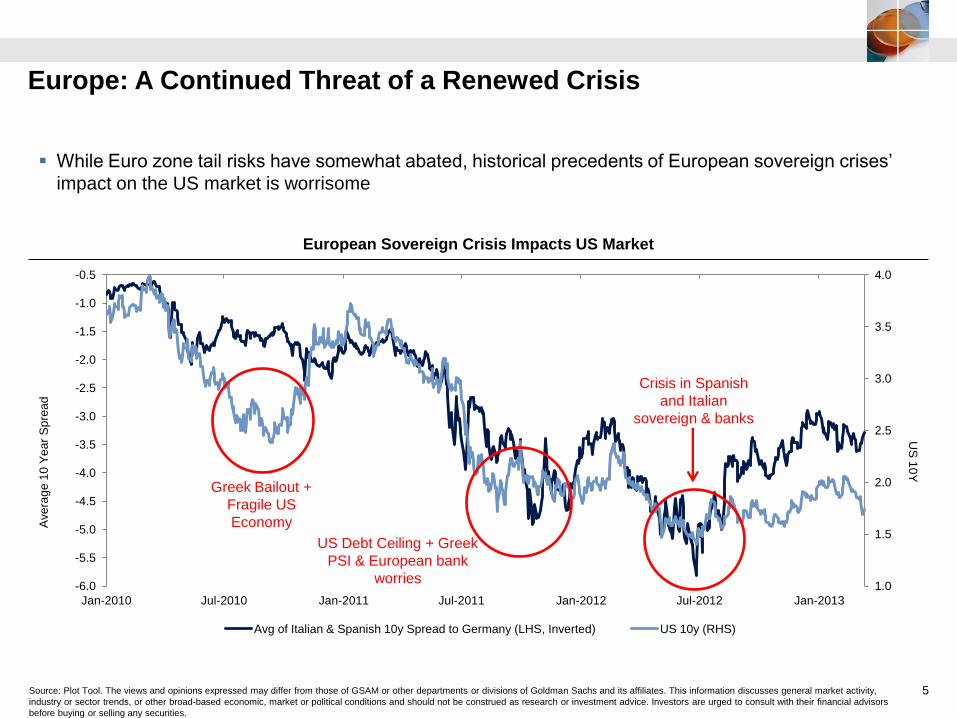

Europe: A Continued Threat of a Renewed Crisis

Source: Plot Tool. The views and opinions expressed may differ from those of GSAM or other departments or divisions of Goldman Sachs and its affiliates. This information discusses general market activity,

industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. Investors are urged to consult with their financial advisors

before buying or selling any securities.

While Euro zone tail risks have somewhat abated, historical precedents of European sovereign crises’

impact on the US market is worrisome

European Sovereign Crisis Impacts US Market

US Debt Ceiling + Greek

PSI & European bank

worries

Greek Bailout +

Fragile US

Economy

Crisis in Spanish

and Italian

sovereign & banks

Ave

rag

e 1

0 Y

ea

r S

pre

ad

U

S 1

0Y

6

Europe: The Banking Crisis Has Had a Prolonged Impact on the US

Source: Goldman Sachs, Plot Tool. Plot Tool is a proprietary analytical tool and database representing developed and emerging markets including the US, Europe, Asia, and Latin America for their respective

Fixed Income, Equity, Foreign Exchange, Commodities, and Credit Markets covering thousands of cash, forward, futures, options, and swap instruments. Plot tool houses over 20 years of economic data. The

views and opinions expressed may differ from those of GSAM or other departments or divisions of Goldman Sachs and its affiliates. This information discusses general market activity, industry or sector trends,

or other broad-based economic, market or political conditions and should not be construed as research or investment advice. Investors are urged to consult with their financial advisors before buying or selling

any securities.

Euro zone 10 Year Treasury Bond Yields

Since last summer, Draghi’s actions have reduced the prospect of a major crisis, but this continues to be

tested

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Apr-08 Oct-08 Apr-09 Oct-09 Apr-10 Oct-10 Apr-11 Oct-11 Apr-12 Oct-12 Apr-13

Germany France Italy Spain

10

Ye

ar

Yie

lds

July 2012, Draghi

announces ECB will

fight to preserve Euro

7

Europe: Is Cyprus a Unique Case?

Source: ECB. The views and opinions expressed may differ from those of GSAM or other departments or divisions of Goldman Sachs and its affiliates. This information discusses general market activity, industry

or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. Investors are urged to consult with their financial advisors before

buying or selling any securities.

Questions raised of a potential Cyprus exit from the Euro, the probability of which is mitigated by the

ECB’s continued support of the euro and statements that the bailout approach is not a blueprint

Foreign and Corporate Deposits in Euro zone

0.00

0.10

0.20

0.30

0.40

0.50

0.00 0.10 0.20 0.30 0.40 0.50 0.60 0.70 0.80

Fore

ign

de

po

sits a

s %

of to

tal d

ep

osits

Euro area corporate deposits as % of household deposits

Italy

Greece

Malta

Cyprus

Ireland

Netherlands

Spain

Luxembourg

Japan: Bolder Than Expected Quantitative Easing

Source: Goldman Sachs, Plot Tool. Plot tool is a proprietary analytical tool and database representing developed and emerging markets including the US, Europe, Asia, and Latin America for their respective

Fixed Income, Equity, Foreign Exchange, Commodities, and Credit Markets covering thousands of cash, forward, futures, options, and swap instruments. Plot tool houses over 20 years of economic data. The

views and opinions expressed may differ from those of GSAM or other departments or divisions of Goldman Sachs and its affiliates. This information discusses general market activity, industry or sector trends, or

other broad-based economic, market or political conditions and should not be construed as research or investment advice. Investors are urged to consult with their financial advisors before buying or selling any

securities. The economic and market forecasts presented herein are based on proprietary models for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will

be achieved. Please see additional disclosures at the end of this presentation.

BOJ announced it aimed to double the monetary base in 2 years, with the goal of ending a long

period of deflation

BOJ Asset and Monetary Base

8

Asse

t a

nd

Mo

ne

tary

Ba

se

(¥

tn)

9

US Government Balance Sheet Was In a Period of Expansion

Source: Goldman Sachs, Plot Tool. Plot tool is a proprietary analytical tool and database representing developed and emerging markets including the US, Europe, Asia, and Latin America for their respective

Fixed Income, Equity, Foreign Exchange, Commodities, and Credit Markets covering thousands of cash, forward, futures, options, and swap instruments. The views and opinions expressed may differ from those

of GSAM or other departments or divisions of Goldman Sachs and its affiliates. This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political

conditions and should not be construed as research or investment advice. Investors are urged to consult with their financial advisors before buying or selling any securities.

The unprecedented fiscal and monetary policy set the foundation for US economic recovery

Asset Side of Federal Reserve’s Balance Sheet ($mm)

Asse

t S

ide

of F

ed

era

l R

ese

rve

’s B

ala

nce

Sh

ee

t

($m

m)

10

Both Private and Public Sectors Beginning to Reduce Their Financial

Balances

Source: Department of Commerce, March 2013; Goldman Sachs. The views and opinions expressed may differ from those of GSAM or other departments or divisions of Goldman Sachs and its affiliates. This

information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. Investors are

urged to consult with their financial advisors before buying or selling any securities.

Public Sector vs. Private Sector Balance as a % of GDP

A close inverse relationship exists between private sector balance and federal government balance,

indicating that a decrease in the financial balance of both the public and private sectors would lead to

GDP growth

-12

-9

-6

-3

0

3

6

9

12

-12.0

-9.0

-6.0

-3.0

0.0

3.0

6.0

9.0

12.0

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Private Sector Financial Balance General Government Budget Balance

1960-2011

Avg = 1.9%

% o

f G

DP

Sequestration Used as a Tool to Enforce Discretionary Spending Cuts

Source: Dept. of Commerce, Congressional Budget Office. *Drawdown scenario assumes troops deployed for overseas military operations declines to 45k by 2015.

Federal Spending is Projected to Decline

While sequestration is projected to reduce spending significantly, it is only one of several sources of

spending restraint that has taken or will soon take effect B

illio

ns o

f 2

00

5 D

olla

rs

Bill

ion

s o

f 2

00

5 D

olla

rs

600

800

1000

1200

1400

1600

600

800

1000

1200

1400

1600

2000 2005 2010 2015 2020

CBO January 2011 Projectionw/ Spring 2011 Reductionsw/ Budget Control Act Spending Capsw/ Sequestrationw/ Other Adjustmentsw/ Military Drawdown*

Billions of 2005 dollars Billions of 2005 dollars

Federal Discretionary Spending:

* Drawdown scenario assumes troops deployed for overseas military operations declines to 45k by 2015.

Actual Projection

11

Impact of the Sequestration Will be Negative, But Manageable

Source: Goldman Sachs. This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or

investment advice. Please see additional disclosures.

Fiscal Policy’s Effect on Real GDP Growth

The sequester cuts, which are less than 3% of spending, are concentrated in discretionary spending in

the second half of the year

12

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

Tax Spending (Ex Sequester) Sequester

Impact of Federal Fiscal Policy on

Real GDP Growth:

2012 2013 2014

Imp

act o

n R

ea

l G

DP

Gro

wth

(%

)

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

1960 1970 1980 1990 2000 2010

Deb

t a

s %

of a

sse

ts

Debt / Asset Ratio for US Households

Trend line (1952-2012)

Government Borrowing Has Supported Private Deleveraging

US Households Debt / Asset Ratio

Source: Goldman Sachs, Plot Tool. Plot tool is a proprietary analytical tool and database representing developed and emerging markets including the US, Europe, Asia, and Latin America for their respective

Fixed Income, Equity, Foreign Exchange, Commodities, and Credit Markets covering thousands of cash, forward, futures, options, and swap instruments. Time series for the Debt/GDP is the longest available.

GSAM, ERWIN, Bloomberg. Plot tool is a proprietary analytical tool and database representing developed and emerging markets including the US, Europe, Asia, and Latin America for their respective Fixed

Income, Equity, Foreign Exchange, Commodities, and Credit Markets covering thousands of cash, forward, futures, options, and swap instruments. Plot tool houses over 20 years of economic data. The views

and opinions expressed may differ from those of GSAM or other departments or divisions of Goldman Sachs and its affiliates. This information discusses general market activity, industry or sector trends, or other

broad-based economic, market or political conditions and should not be construed as research or investment advice. Investors are urged to consult with their financial advisors before buying or selling any

securities.

13

The consumer balance sheet is looking healthier with debt / asset ratios nearing historic trends

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0 Domestic Financial

Non-fin Biz

Household

State & Local Govn't

Federal Govn't

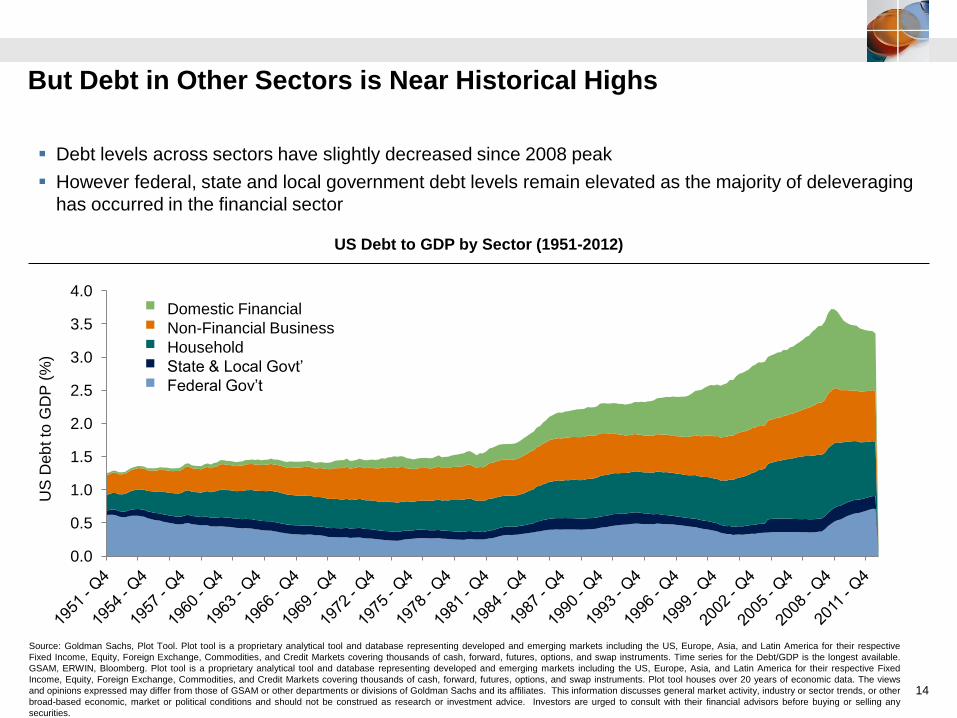

But Debt in Other Sectors is Near Historical Highs

US Debt to GDP by Sector (1951-2012)

Source: Goldman Sachs, Plot Tool. Plot tool is a proprietary analytical tool and database representing developed and emerging markets including the US, Europe, Asia, and Latin America for their respective

Fixed Income, Equity, Foreign Exchange, Commodities, and Credit Markets covering thousands of cash, forward, futures, options, and swap instruments. Time series for the Debt/GDP is the longest available.

GSAM, ERWIN, Bloomberg. Plot tool is a proprietary analytical tool and database representing developed and emerging markets including the US, Europe, Asia, and Latin America for their respective Fixed

Income, Equity, Foreign Exchange, Commodities, and Credit Markets covering thousands of cash, forward, futures, options, and swap instruments. Plot tool houses over 20 years of economic data. The views

and opinions expressed may differ from those of GSAM or other departments or divisions of Goldman Sachs and its affiliates. This information discusses general market activity, industry or sector trends, or other

broad-based economic, market or political conditions and should not be construed as research or investment advice. Investors are urged to consult with their financial advisors before buying or selling any

securities.

14

Debt levels across sectors have slightly decreased since 2008 peak

However federal, state and local government debt levels remain elevated as the majority of deleveraging

has occurred in the financial sector

US

Deb

t to

GD

P (

%)

Domestic Financial

Non-Financial Business

Household

State & Local Govt’

Federal Gov’t

U.S.A

2d

0.425

0.45

0.475

0.5

0.525

0.55

0.575

0.6

0.625

0.65

0.675

0.7

0.725

0.75

0.775

0.8

0.825

0.85

0.875

-2.2

-2.1

-2

-1.9

-1.8

-1.7

-1.6

-1.5

-1.4

-1.3

-1.2

-1.1

Positive US Trends Have Emerged

15 Source: Goldman Sachs. This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or

investment advice. As of March 2013.

Housing Recovery

Factors like affordability, availability of credit and supply are trending

toward normalized levels

Positive growth is expected to have a moderate impact on US growth

Consumer Spending

With more stable finances and the availability of credit, consumer

demand may spur growth

Labor force participation expected to stabilize

Corporate Growth and Capital Spending

Increased corporate investing despite policy uncertainty

Growth of manufacturing sector has been trending positively

Energy Boom

Oil and natural gas production has increased, driving fixed investment

in commodity exploration

Stability of low natural gas prices expected to drive reduced electricity

and manufacturing costs

Estim

ate

d E

ffe

ct o

n H

ou

sin

g o

n R

ea

l G

DP

Gro

wth

(%

)

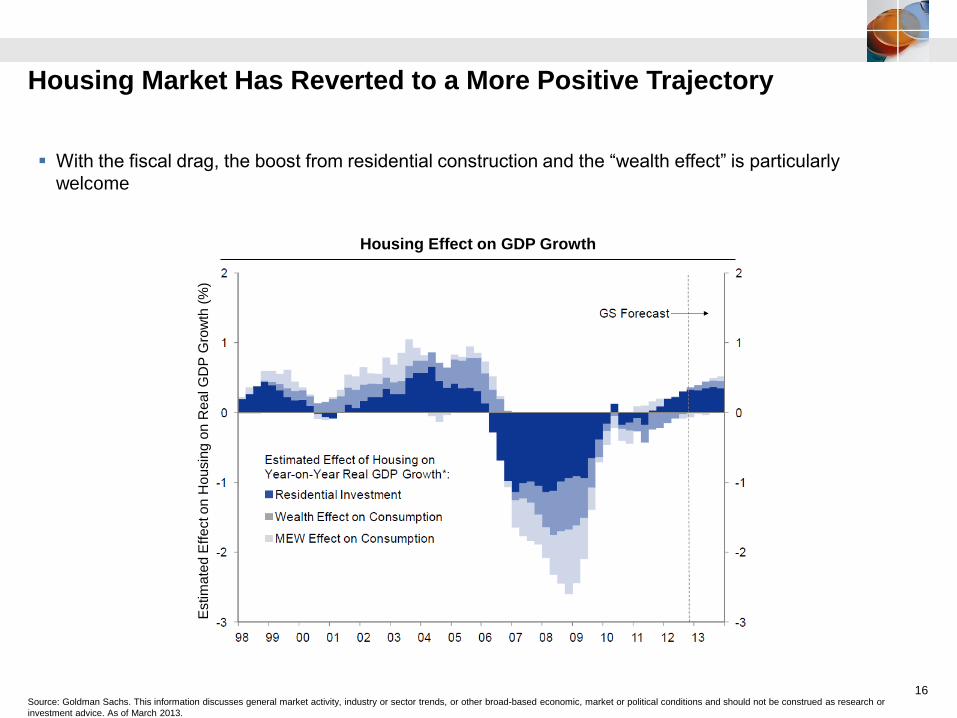

Housing Market Has Reverted to a More Positive Trajectory

Source: Goldman Sachs. This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or

investment advice. As of March 2013.

Housing Effect on GDP Growth

16

With the fiscal drag, the boost from residential construction and the “wealth effect” is particularly

welcome

While Certain Factors Have Returned To Normal….

*Assumed demolition rate of 300,000 per year. Source: Department of Commerce. GS Global ECS Research. March 2013.

Housing Affordability Has Risen Significantly

Pri

ce

to

Ren

t R

atio

(In

de

x)

Hou

sin

g A

fford

ab

ility (In

de

x)

17

The Housing Affordability Index shows that housing is the most affordable in decades, thanks to record

low mortgage rates

…Others Are More Dislocated

Source: Department of Commerce. Goldman Sachs. *Assumed demolition rate of 300,000 per year.

Household Formation Has A Long Way to Rise

Hou

sin

g A

ffo

rda

bili

ty (

Th

ou

sa

nds)

18

Household formation has started to normalize. However, there are still headwinds as exemplified by

housing starts, which are well below demand

0

400

800

1200

1600

2000

2400

2800

0

400

800

1200

1600

2000

2400

2800

86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16

Household Formation Demolitions* Housing Starts

Household

Formation

Forecast

19

Positive Signs Emerging for Consumer Spending

Source: Goldman Sachs, Plot Tool. Plot Tool is a proprietary analytical tool and database representing developed and emerging markets including the US, Europe, Asia, and Latin America for their respective

Fixed Income, Equity, Foreign Exchange, Commodities, and Credit Markets covering thousands of cash, forward, futures, options, and swap instruments. Plot tool houses over 20 years of economic data.

With more stable finances and the availability of credit, consumer demand should spur growth

Fed Senior Loan Officer Survey (% Easing - % Tightening)

-90

-70

-50

-30

-10

10

30

C&L Loans to Large Firms C&L Loans to Small Firms Consumer Loans

% E

asin

g -

% T

igh

ten

ing

20

Unemployment has Been Declining

Source: Plot tool. Plot tool is a proprietary analytical tool and database representing developed and emerging markets including the US, Europe, Asia, and Latin America for their respective Fixed Income, Equity,

Foreign Exchange, Commodities, and Credit Markets covering thousands of cash, forward, futures, options, and swap instruments. Plot tool houses over 20 years of economic data.

Unemployment rate dropped to 7.6%, but this decrease was undermined by news that only 88,000 jobs

where created in March 2013, far below February 2013’s 268,000 gain

Headline Unemployment and Labor Force

Part

tim

e W

ork

/ L

abor

Fo

rce

H

eadlin

e U

nem

plo

ym

ent

-1

1

3

5

7

9

11

0

1

2

3

4

5

6

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Persons Working Part Time for Economic Reasons / Labor Force (LHS)

Headline Unemployment Rate (RHS)

21

Labor Force Participation Has Been on Downward Trend

Source: Goldman Sachs, Plot Tool. Plot Tool is a proprietary analytical tool and database representing developed and emerging markets including the US, Europe, Asia, and Latin America for their respective

Fixed Income, Equity, Foreign Exchange, Commodities, and Credit Markets covering thousands of cash, forward, futures, options, and swap instruments. Plot tool houses over 20 years of economic data.

Labor Force and Average Duration of Unemployment

Unemployment is down, partially as a result of a decline in the number of workers seeking jobs

Avg D

ura

tio

n o

f U

ne

mp

loym

en

t (w

ks) L

ab

or F

orc

e P

artic

ipa

tion

(RH

S)

63.0%

63.5%

64.0%

64.5%

65.0%

65.5%

66.0%

66.5%

67.0%

67.5%

10.0

12.5

15.0

17.5

20.0

22.5

25.0

27.5

30.0

32.5

35.0

37.5

40.0

42.5

Average Duration of Unemployment in Weeks (LHS)

Last Value 37w (LHS)

Labor Force Participation (RHS)

22

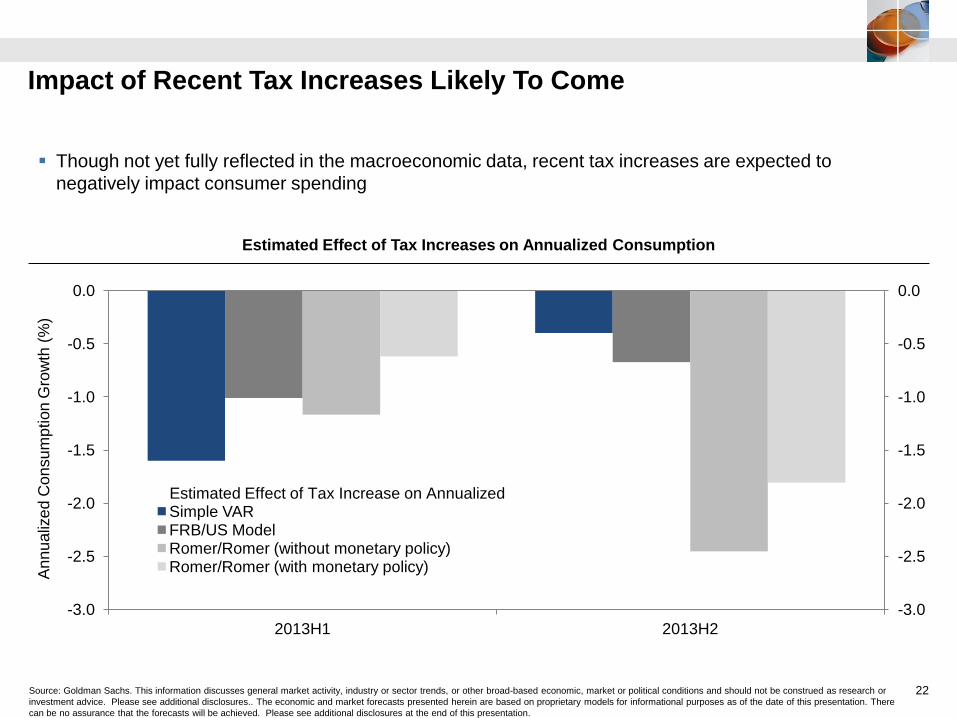

Impact of Recent Tax Increases Likely To Come

Source: Goldman Sachs. This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or

investment advice. Please see additional disclosures.. The economic and market forecasts presented herein are based on proprietary models for informational purposes as of the date of this presentation. There

can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation.

Estimated Effect of Tax Increases on Annualized Consumption

Though not yet fully reflected in the macroeconomic data, recent tax increases are expected to

negatively impact consumer spending

2013H1 2013H2

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

Simple VAR FRB/US Model Romer/Romer (without monetary policy) Romer/Romer (with monetary policy)

Estimated Effect of Tax Increase on Annualized

An

nu

aliz

ed

Co

nsu

mp

tion G

row

th (

%)

23

Corporate Profits Have Been Robust….

Source: Department of Commerce, Goldman Sachs. This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be

construed as research or investment advice. Please see additional disclosures. *After-tax adjusted profits as percent of GDP.

2012 Corporate Profit Margins – Actual and Forecasted

While general market sentiment suggests that capital spending should not accelerate until policy and tax

reforms are resolved, profit margins indicate that companies are positioned to drive demand

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

70 75 80 85 90 95 00 05 10 15

Actual

Corporate Profit Margins*:

Co

rpo

rate

Pro

fit M

arg

ins (

%)

24

…As Corporate Spending Poised to Increase

Source: Department of Commerce, Goldman Sachs. *After-tax adjusted profits as percent of GDP. This information discusses general market activity, industry or sector trends, or other broad-based economic,

market or political conditions and should not be construed as research or investment advice. Please see additional disclosures.

Growth of Real Private Capital and Profit Margins

Capital spending is expected pick up as the profit rate has led investment growth during the last 2

business cycles

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

1950 1960 1970 1980 1990 2000 2010

Profit Margin, Domestic Industries (left)

Growth Rate of Real Private Capital Stock (right)

Pro

fit M

arg

in,

Do

me

stic In

du

str

ies (

%)

Gro

wth

Ra

te o

f Re

al P

riva

te C

ap

ital S

tock (%

)

25

Oil and Natural Gas Production Has Increased…

Source: EIA Annual Energy Outlook 2012. Actual data through 2010, EIA projections beginning in 2011. This information discusses general market activity, industry or sector trends, or other broad-based

economic, market or political conditions and should not be construed as research or investment advice. Please see additional disclosures.The economic and market forecasts presented herein are based on

proprietary models for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation.

Rise in Domestic Oil and Gas Production

Advances in technology have unlocked oil and gas in shale beds across the US, allowing substantially

more energy production and providing modest benefit to employment

26

…Leading to Indirect Stimulus in Other Areas of the Market

Source: Bloomberg, Goldman Sachs. This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as

research or investment advice. Please see additional disclosures.

Natural Gas Prices Across US, UK and Japan

The potential collapse in the price of natural gas, which supports 20-25% of US electricity, could create a

meaningful competitive advantage for US companies that are energy cost sensitive

27

Given These Trends, Outlook Moving Forward

Source: Goldman Sachs. (1) Jim O’Neill, Goldman Sachs Asset Management. This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political

conditions and should not be construed as research or investment advice. As of March 2013.

GDP

GDP growth in the US and Euro zone continues at a slow pace

Forecasts indicate 2.3% and -0.3% GDP growth for the US and the Euro zone

in 2013 respectively1

Interest Rates

Yields are still low, but rising rates may be on the horizon

We expect 10y Treasuries to potentially trade around 2.5% in the next 12

months

Fed guidance on unemployment (6.5% target) indicates potential rates hike in

2015-2016

Inflation

Near-term inflation is benign

We expect both headline and core CPI inflation to remain contained through

2013

Equity Market

Investors are continuing to seek out riskier assets

Threat of tail risks from US fiscal policy and Euro zone crisis has somewhat

abated

Rates Likely to Rise Modestly, However Risk is Asymmetrical

Source: Goldman Sachs. This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or

investment advice.

Downside is still possible:

Renewed European concerns

US fiscal / political mismanagement

Adoption of more dovish Fed policy

Possibility of US growth surprise:

Housing market

Consumer balance sheet

Labor market

Unexpected inflation

2.5% 3.5% 2.0%

1 std 1 std

28

In light of these trends, we expect 10Y treasuries to trade around 2.5% in 6-12 months (somewhat higher

than forwards)

29

Inflation Likely to Remain Below 2.0%

Source: Department of Commerce. Federal Reserve Board. This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should

not be construed as research or investment advice. As of March 2013.

Near Term Inflation Expectations are Benign

Despite small upticks in CPI reports from January and February, ongoing slack in the labor market and

stable inflation expectations continue to keep inflation low

0

1

2

3

4

5

0

1

2

3

4

5

90 92 94 96 98 00 02 04 06 08 10 12 14

Actual Fed Forecast GS Forecast

Core PCE Inflation:

Fed Inflation Target = 2.0%

Pro

fit M

arg

in,

Do

me

stic In

du

str

ies (

%)

Gro

wth

Rate

of R

ea

l Priv

ate

Ca

pita

l Sto

ck (%

)

30

Unexpected Acceleration in Inflation

Expected to be contained, but risk has increased

Several Key Risks Remain

Return of the EMU Crisis

Cyprus highlights the long road ahead

China Credit Concerns

Limited risk of “hard landing”, but withdrawing liquidity earlier than expected

could be a concern

Shadow banking system may create a threat

Geopolitical concerns

Increased possibility of conflict in the Middle East

Recent developments in North Korea pose a tail risk

Source: Goldman Sachs. This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or

investment advice. As of March 2013.

30

Equity valuations are still

generally attractive,

despite strong YTD

performance

In credit, strong corporate

balance sheets give

comfort that defaults

should continue to be low.

Additional spread

compression is likely to be

limited

Relative to other asset

classes, muted returns can

be expected from

Emerging Markets Debt,

Corporate Credit, and

Government Bonds given

their current low yields and

potential for rising rates

A disorderly rise in yields is

unlikely as the 10y

Treasury yield may rise to

about 2.5% by year end

2013 31

Less Attractive More Attractive

Source: Goldman Sachs. As of March 2013. This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be

construed as research or investment advice. Asset class views are relative to the GPS Model Strategic Portfolio.

Where to Invest Today E

qu

ity US Equity

European Equity

Japanese Equity

Fix

ed

Inc

om

e Emerging Markets Debt

Corporate Credit

High Yield

Rea

l

As

se

ts Commodities

Real Estate

Infrastructure

Deve

lop

ed

Go

ve

rnm

en

t

Bo

nd

s

US Gov’t Fixed Income

German Gov’t Fixed Income

European ex-Germany

Gov’t Fixed Income

UK Gov’t Fixed Income

Oth

er

Curve Steepeners

Disclosures

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

This material has been prepared by GSAM and is not a product of Goldman Sachs Global Investment Research. The views and opinions expressed may differ from those of Goldman Sachs Global Investment Research or

other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and GSAM has no

obligation to provide any updates or changes. Views and opinions expressed are for informational purposes only and do not constitute a recommendation by GSAM to buy, sell, or hold any security. Views and opinions are

current as of the date of this presentation and may be subject to change, they should not be construed as investment advice.

References to indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only and do not imply that the portfolio will achieve similar results. The

index composition may not reflect the manner in which a portfolio is constructed. While an adviser seeks to design a portfolio which reflects appropriate risk and return features, portfolio characteristics may deviate from

those of the benchmark.

Indices are unmanaged. The figures for the index reflect the reinvestment of all income or dividends, as applicable, but do not reflect the deduction of any fees or expenses which would reduce returns. Investors cannot

invest directly in indices.

The indices referenced herein have been selected because they are well known, easily recognized by investors, and reflect those indices that the Investment Manager believes, in part based on industry practice, provide a

suitable benchmark against which to evaluate the investment or broader market described herein. The exclusion of “failed” or closed hedge funds may mean that each index overstates the performance of hedge funds

generally.

32

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal

may occur.

Economic and market forecasts presented herein reflect our judgment as of the date of this presentation and are subject to change without notice. These forecasts do not take into account the specific investment

objectives, restrictions, tax and financial situation or other needs of any specific client. Actual data will vary and may not be reflected here. These forecasts are subject to high levels of uncertainty that may affect actual

performance. Accordingly, these forecasts should be viewed as merely representative of a broad range of possible outcomes. These forecasts are estimated, based on assumptions, and are subject to significant revision

and may change materially as economic and market conditions change. Goldman Sachs has no obligation to provide updates or changes to these forecasts. Case studies and examples are for illustrative purposes only.

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

Goldman Sachs does not provide accounting, tax, or legal advice. Notwithstanding anything in this document to the contrary, and except as required to enable compliance with applicable securities law, you may disclose to

any person the US federal and state income tax treatment and tax structure of the transaction and all materials of any kind (including tax opinions and other tax analyses) that are provided to you relating to such tax

treatment and tax structure, without Goldman Sachs imposing any limitation of any kind. Investors should be aware that a determination of the tax consequences to them should take into account their specific

circumstances and that the tax law is subject to change in the future or retroactively and investors are strongly urged to consult with their own tax advisor regarding any potential strategy, investment or transaction.

Confidentiality

No part of this material may, without GSAM’s prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorized

agent of the recipient.

© 2013 Goldman Sachs. First use: April 15, 2013. All rights reserved: 96823.OTHER.TMPL/4/2013

33

Disclosures