![North Western Province Water Resources Development Project in Sri Lanka (Loan 1166-SRI[SF])](https://static.fdocuments.net/doc/165x107/577ce6d91a28abf10393be33/north-western-province-water-resources-development-project-in-sri-lanka-loan.jpg)

North Western Province Water Resources Development Project in Sri Lanka (Loan 1166-SRI[SF])

Completion Report

Project Number: 31382 Loan Numbers: 1800 and 1801 June 2006

Sri Lanka: Private Sector Development Program Loan

CURRENCY EQUIVALENTS

Currency Unit – Sri Lankan rupee (SLRe/SLRs)

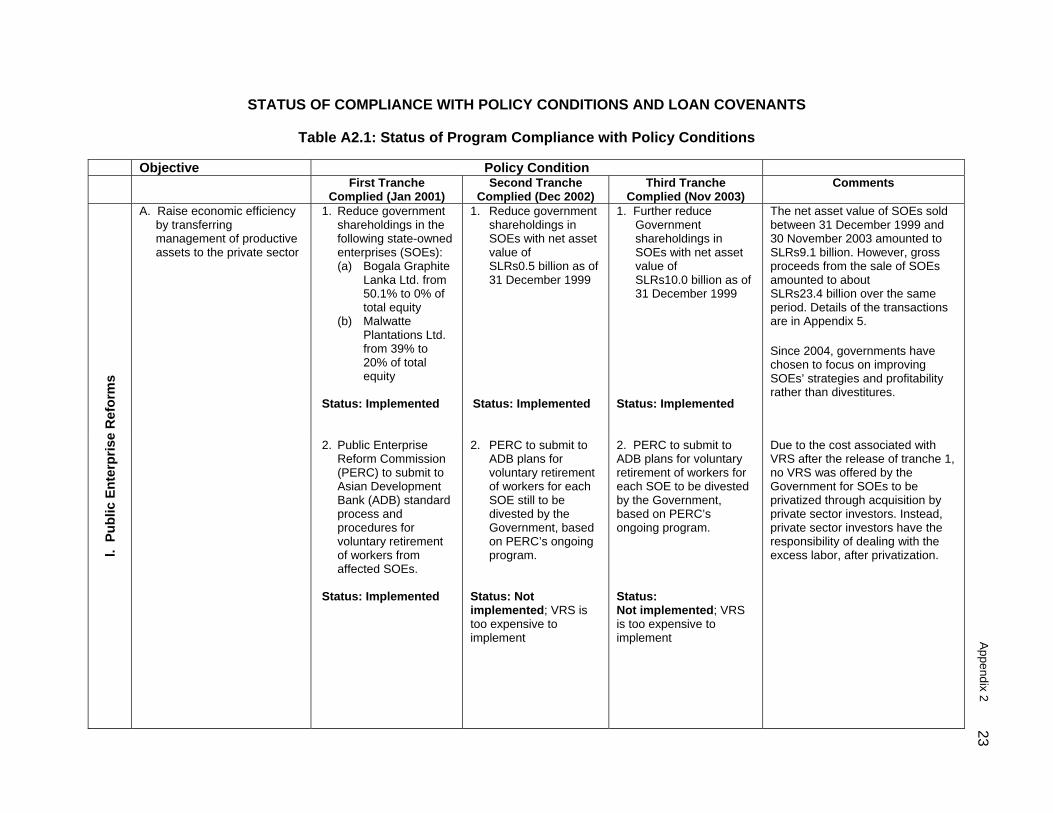

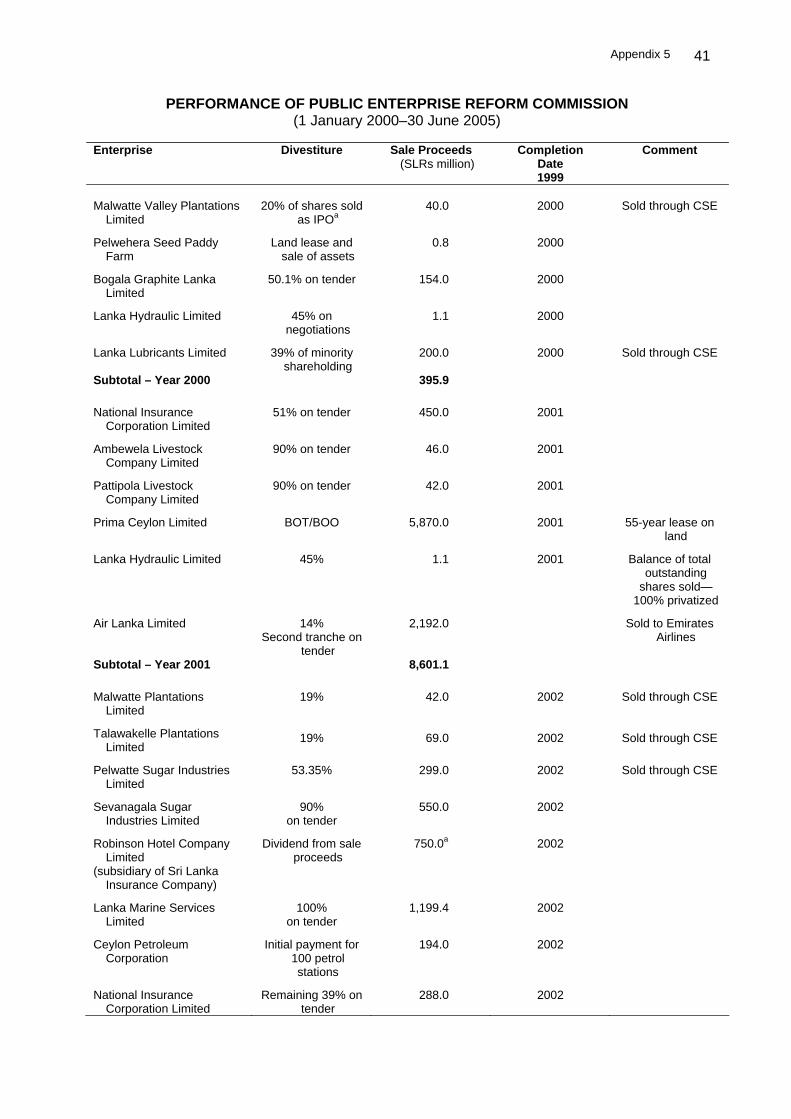

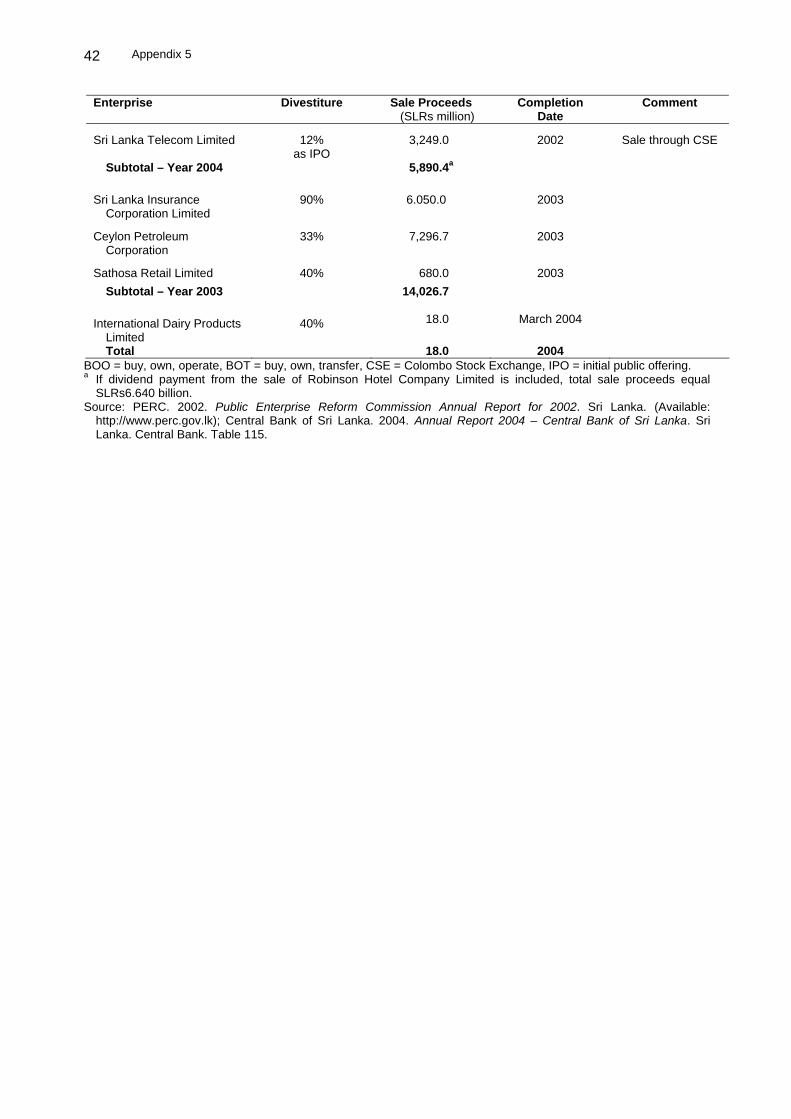

At Appraisal At Program Completion 1 September 2000 31 May 2006

SLRe1.00 = $0.0128 $0.0097 $1.00 = SLRs78.05 SLRs102.96

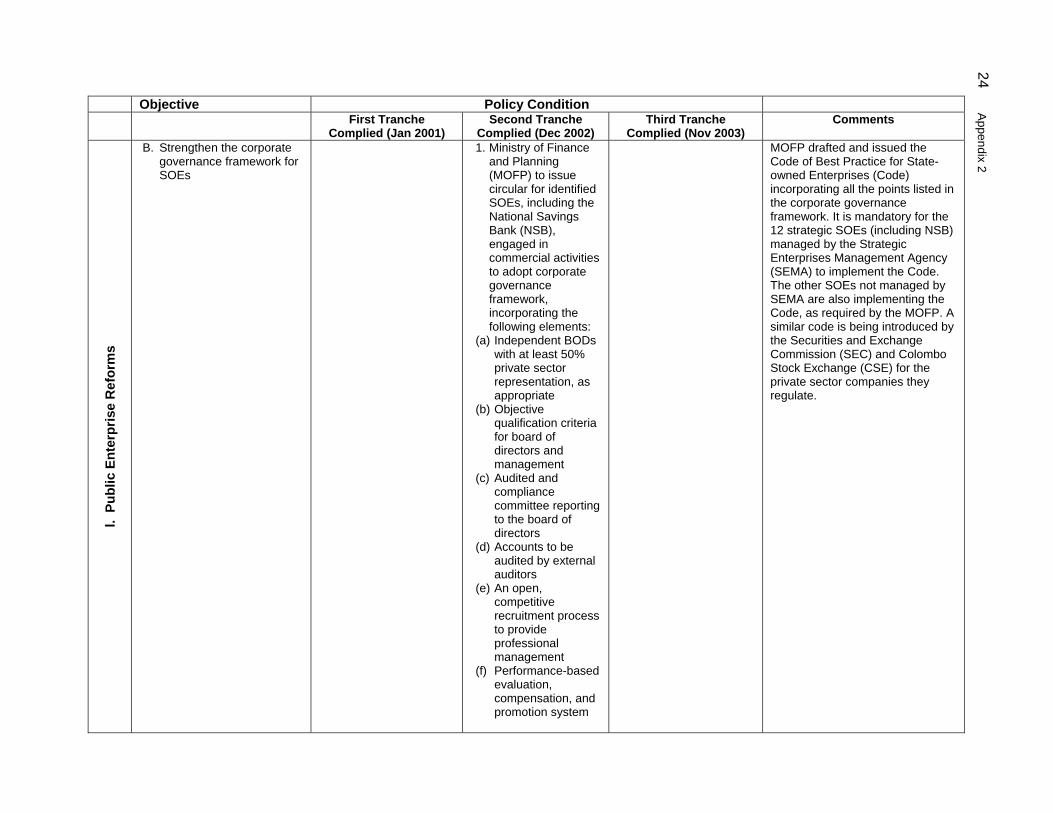

ABBREVIATIONS

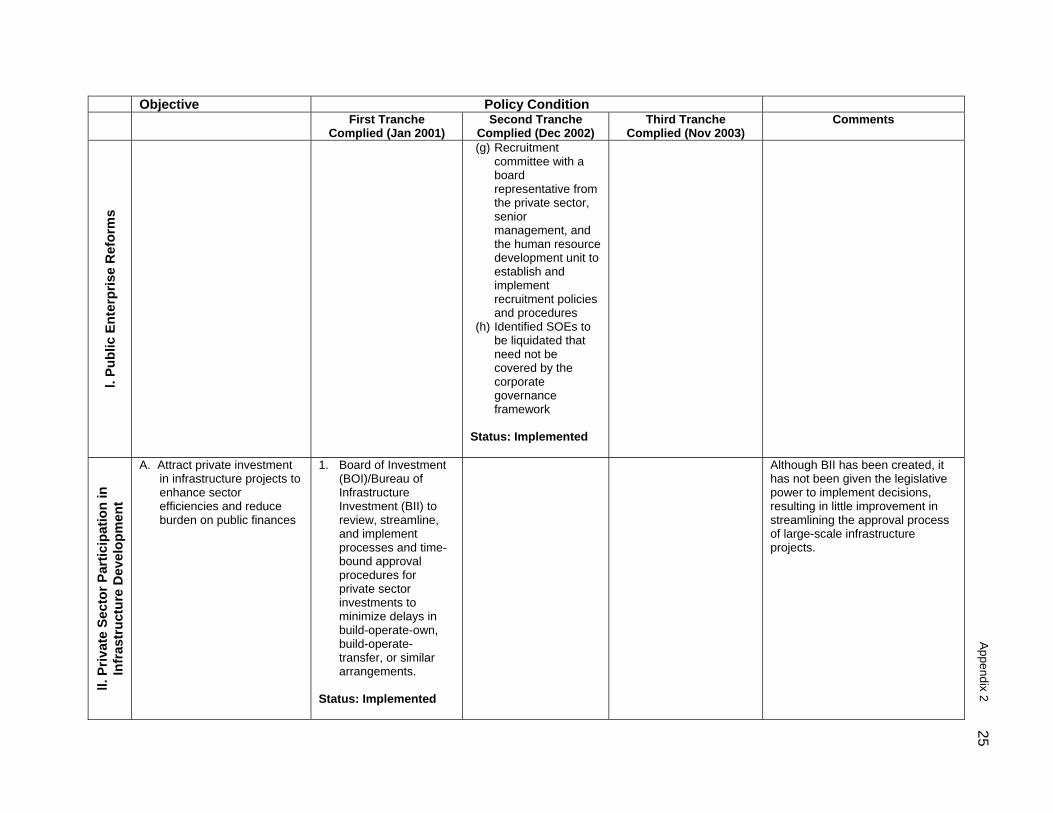

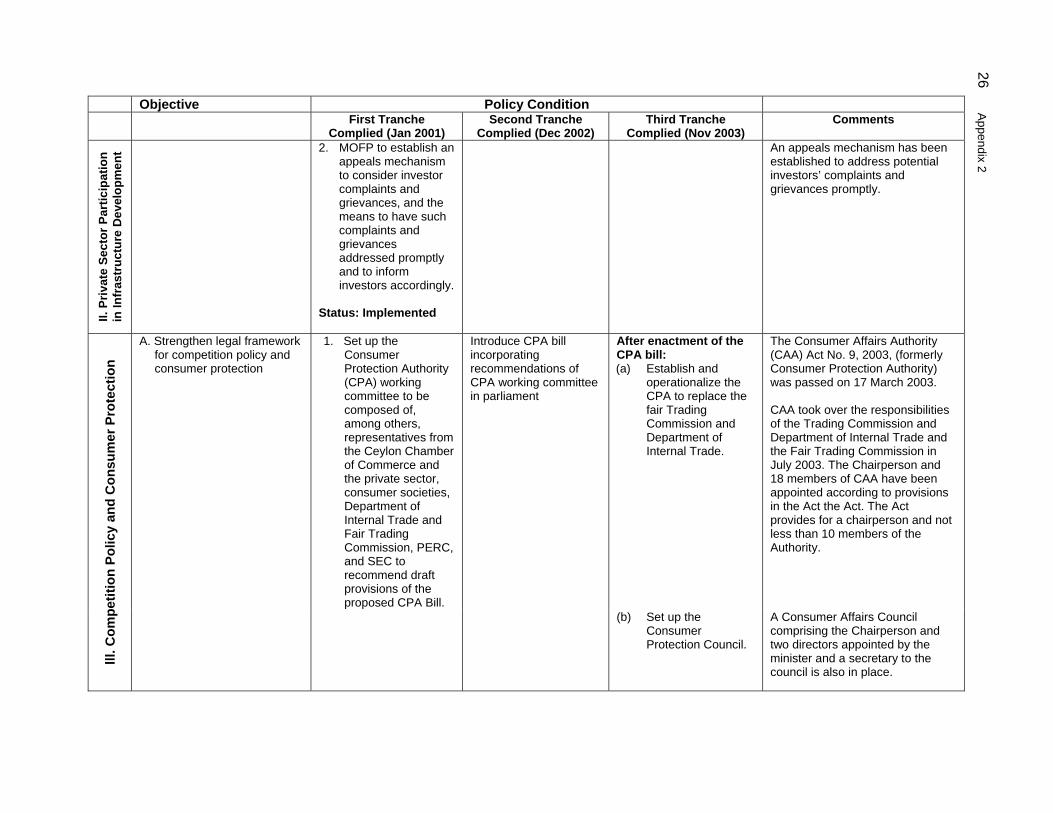

ADB – Asian Development Bank BII – Bureau of Infrastructure Investment BOC – Bank of Ceylon BOD – board of directors BOI – Board of Investment CAA – Consumer Affairs Authority CBSL – Central Bank of Sri Lanka CPA – Consumer Protection Authority CSE – Colombo Stock Exchange EA – executing agency GDP – gross domestic product IA – implementing agency IBSL – Insurance Board of Sri Lanka LCB – licensed commercial bank LIBOR – London interbank offered rate LSB – licensed specialized bank MOFP – Ministry of Finance and Planning NIC – National Insurance Company NPL – nonperforming loan NSB – National Savings Bank PB – People’s Bank PERC – Public Enterprise Reform Commission PSDP – Private Sector Development Program SDR – special drawing rights SEC – Securities and Exchange Commission SEMA – Strategic Enterprise Management Agency SLTL – Sri Lanka Telecom Ltd. SOE – state-owned enterprise TA – technical assistance TEWA – Termination of Employment of Workmen (Special Provisions)

Act No 45, 1971 VRS – voluntary retirement scheme

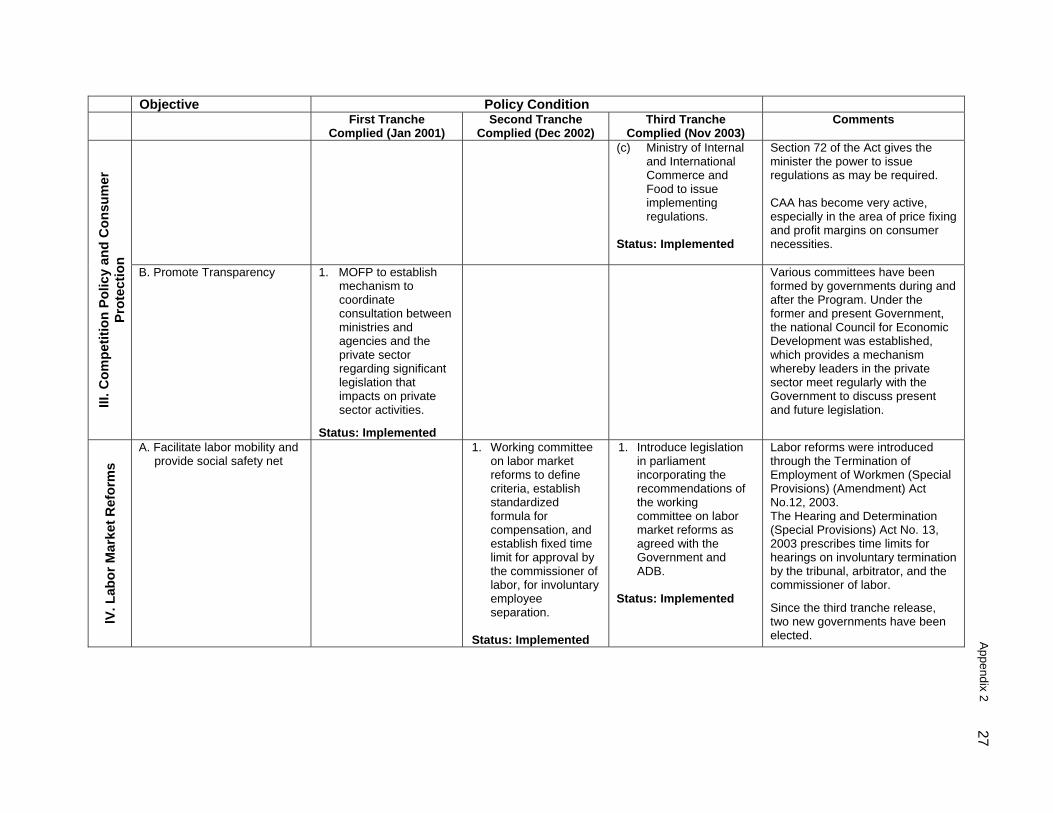

NOTES (i) The fiscal year (FY) of the Government ends on 31 December.

(ii) In this report, "$" refers to US dollars.

Vice President L. Jin, Vice President (Operations 1) Director General K. Senga, South Asia Department (SARD) Director A. Sharma, Governance, Finance and Trade Division, SARD Team leader B. Ericsson, Principal Financial Sector Specialist, SARD

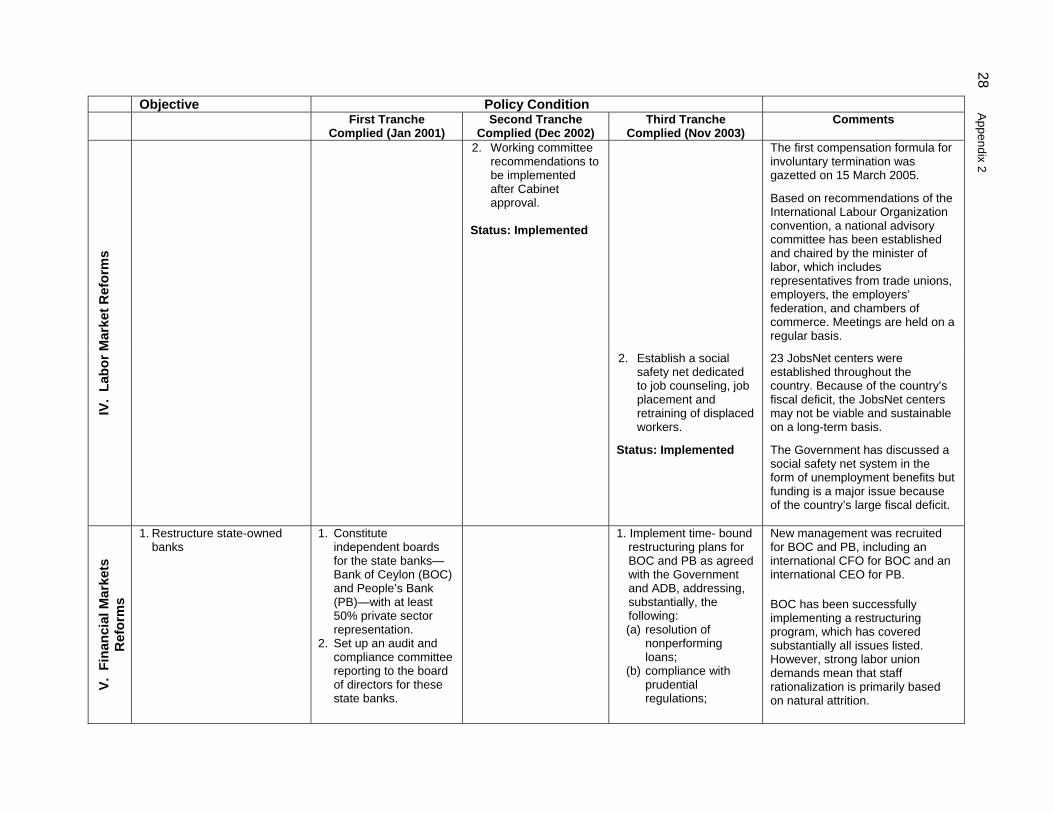

CONTENTS Page

BASIC DATA ii

I. PROGRAM DESCRIPTION 1

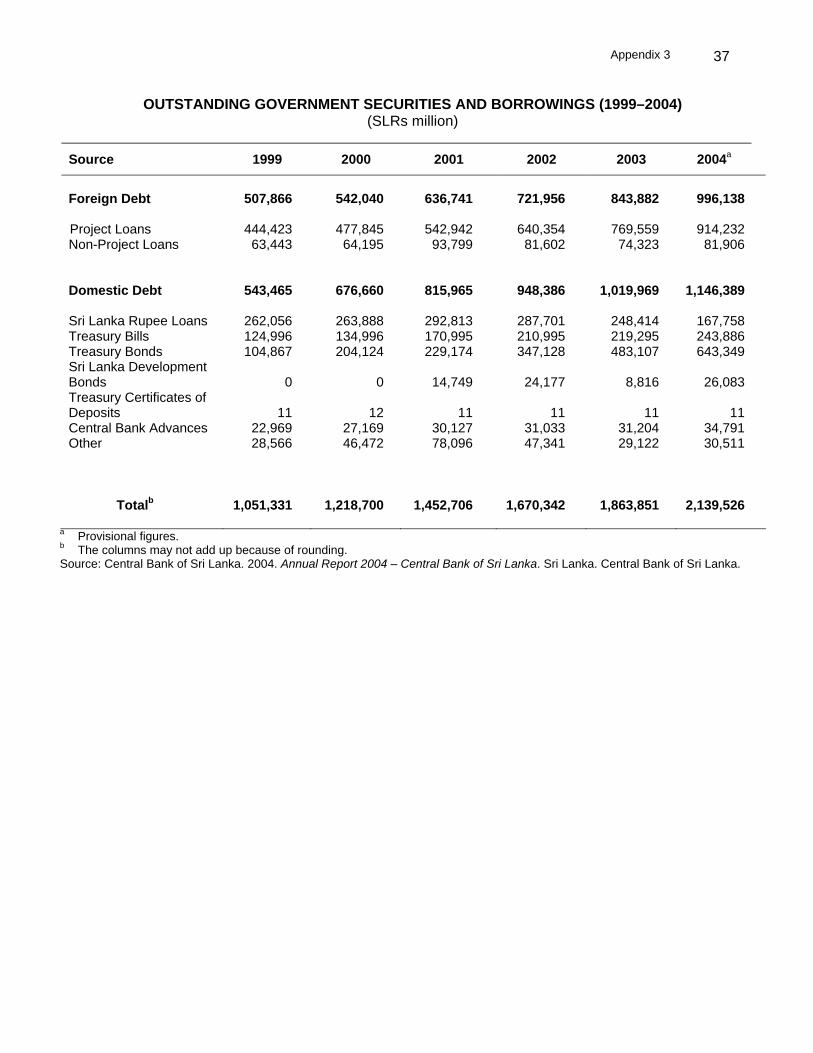

II. EVALUATION OF DESIGN AND IMPLEMENTATION 1 A. Relevance of Design and Formulation 1 B. Program Outputs 2 C. Program Costs 6 D. Disbursements 6 E. Program Schedule 7 F. Implementation Arrangements 7 G. Conditions and Covenants 7 H. Related Technical Assistance 8 I. Performance of the Borrower and the Executing Agency 8 J. Performance of the Asian Development Bank 9

III. EVALUATION OF PERFORMANCE 9 A. Relevance 9 B. Effectiveness in Achieving Outcome 9 2. Private Sector Participation in Infrastructure 10 C. Efficiency in Achievement of Outcome and Outputs 11 D. Preliminary Assessment of Sustainability 12 E. Impact 12

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS 13 A. Overall Assessment 13 B. Lessons Learned 13 C. Recommendations 14

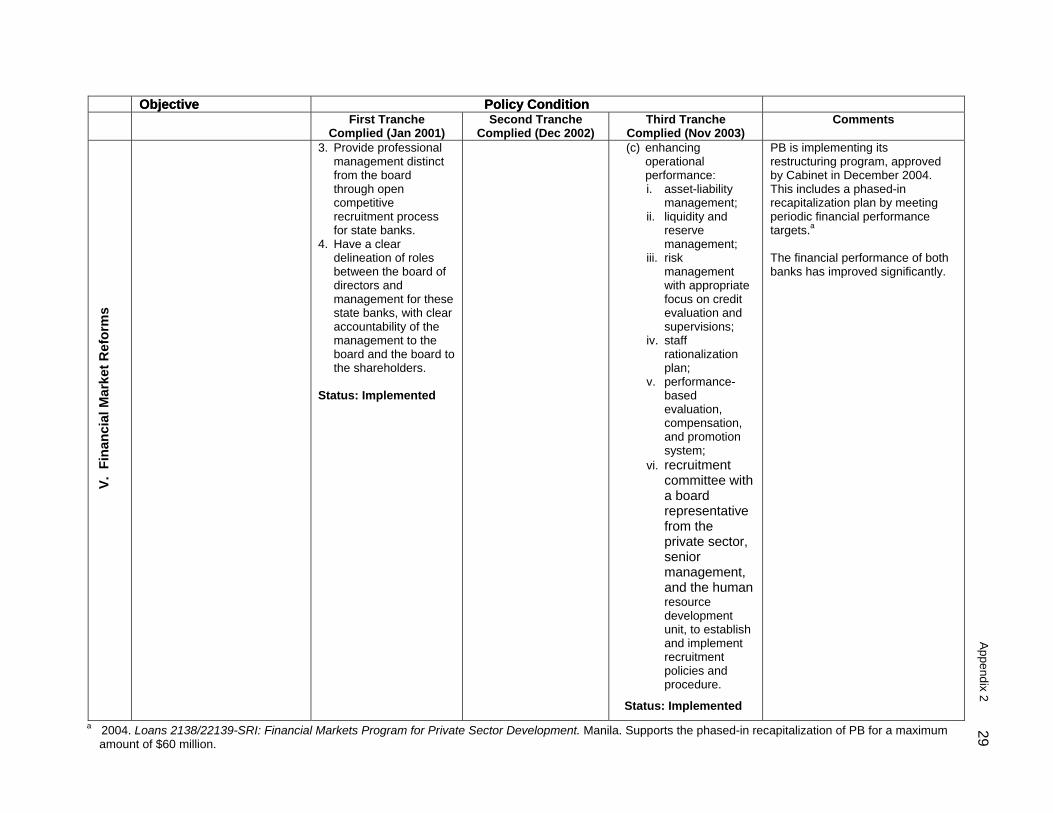

APPENDIXES 1. Program Framework 16 2. Status of Compliance with Policy Conditions and Loan Covenants 23 3. Outstanding Government Securities and Borrowing (1999–2004) 37 4. Sri Lanka Financial Sector Profile 38 5. Performance of Public Enterprise Reform Commission 41 6. Fiscal Accounts of the Central Government of Sri Lanka (1999–2004) 43 7. Savings and Investments in Sri Lanka (1999–2004) 44 8. Financial performance of Bank of Ceylon 45 9. Financial Performance of People’s Bank 46

BASIC DATA A. Loan Identification 1. Country 2. Loan Number 3. Program Title 4. Borrower 5. Executing Agency 6. Amount of Loan 7. Program Completion Report Number

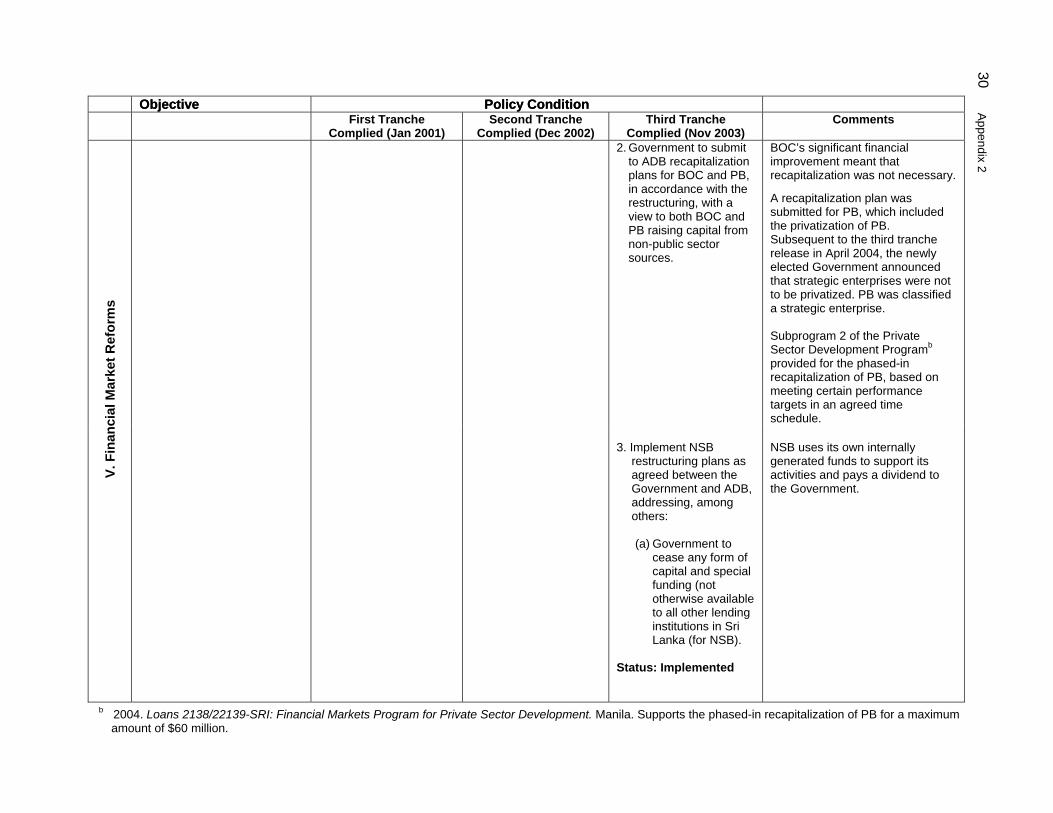

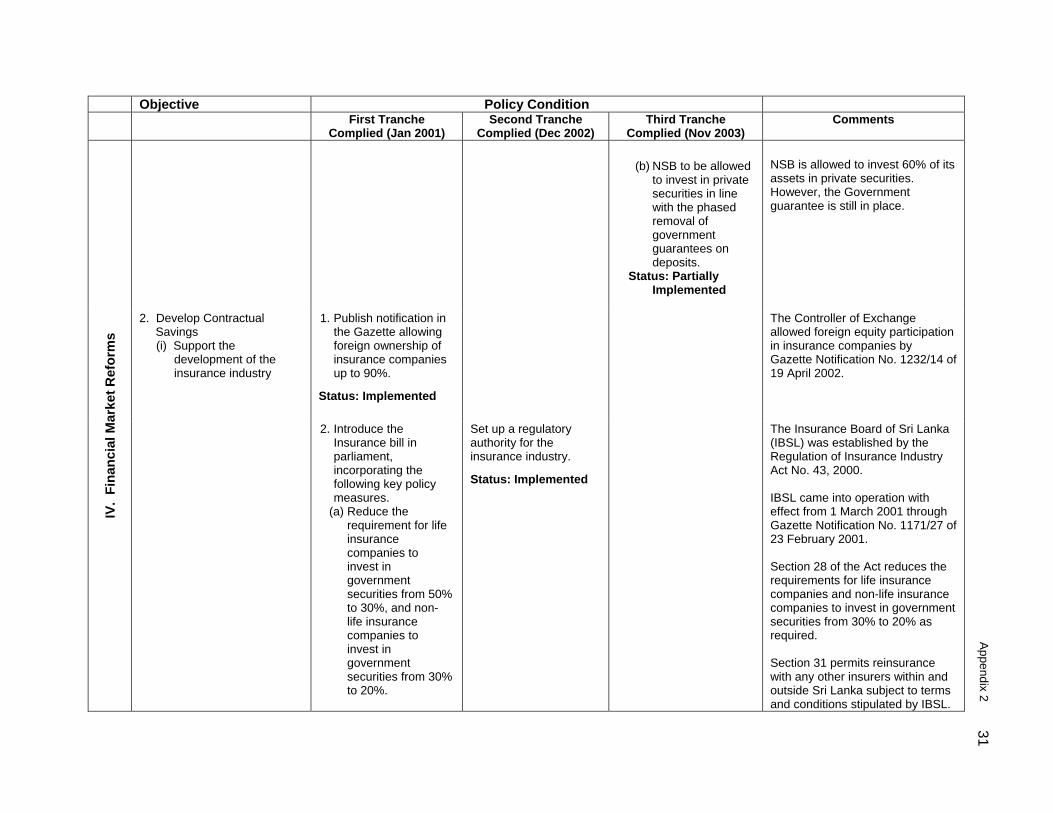

Sri Lanka 1800 and 1801- SRI Private Sector Development Program Democratic Socialist Republic of Sri Lanka Ministry of Finance and Planning $100.0 million SRI 31382

B. Loan Data 1. Appraisal – Date Started – Date Completed 2. Loan Negotiations – Date Started – Date Completed 3. Date of Board Approval 4. Date of Loan Agreement 5. Date of Loan Effectiveness – In Loan Agreement – Actual – Number of Extensions 6. Closing Date – In Loan Agreement – Actual – Number of Extensions 7. Terms of Loans – Interest Rate – Maturity (number of years)

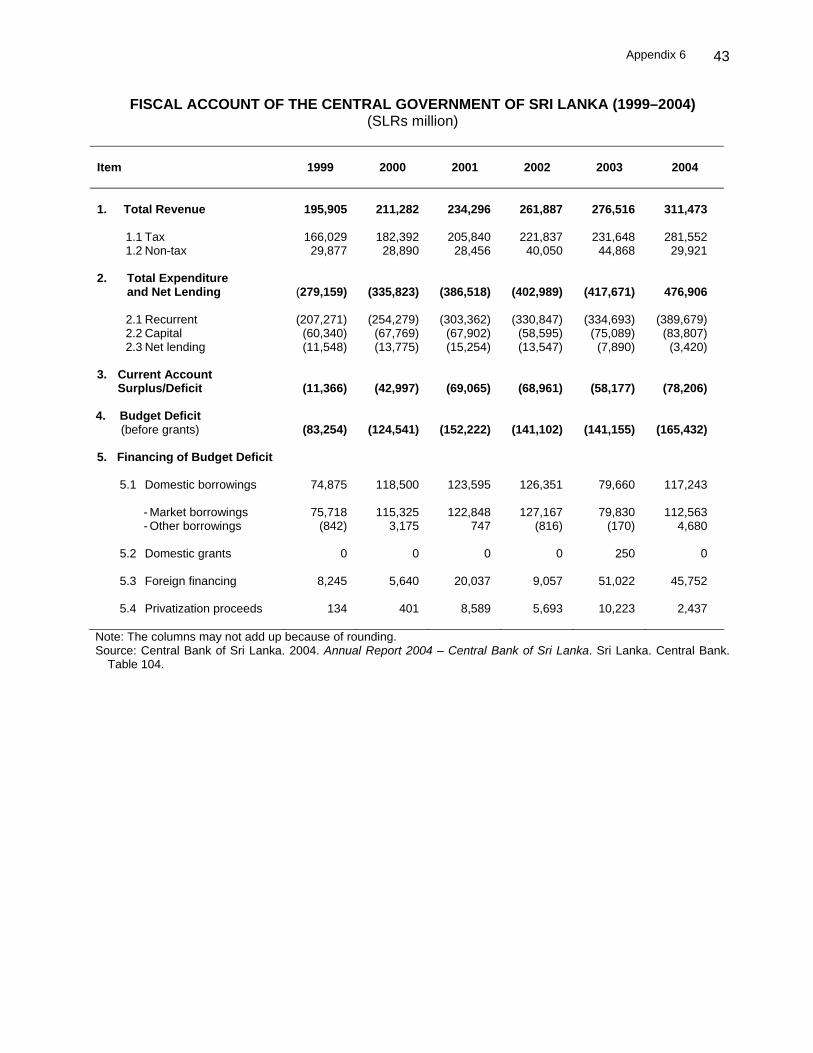

– Grace Period (number of years)

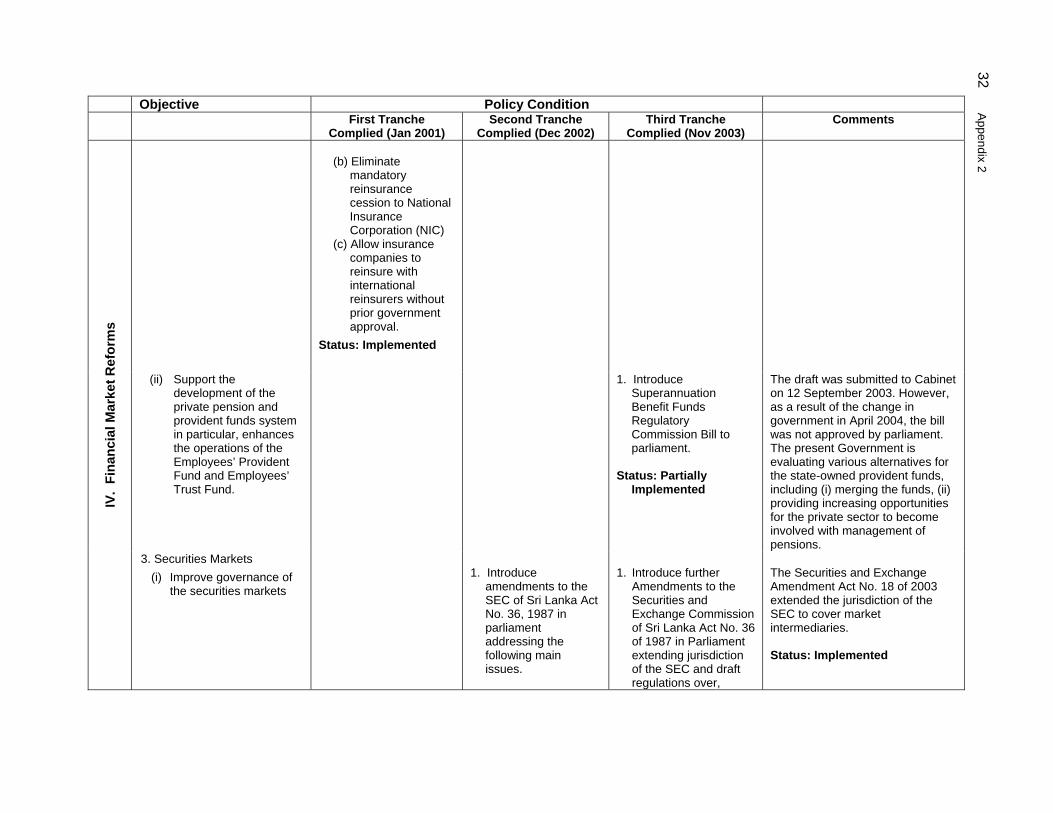

24 Jul 2000 04 Aug 2000 30 Oct 2000 31 Oct 2000 12 Dec 2000 17 Jan 2001 25 Jan 2001 25 Jan 2001 None 30 Jun 2003 24 Nov 2003 3 Loan 1800 Loan 1801 1% and 1.5% Variable 24 15 8 3

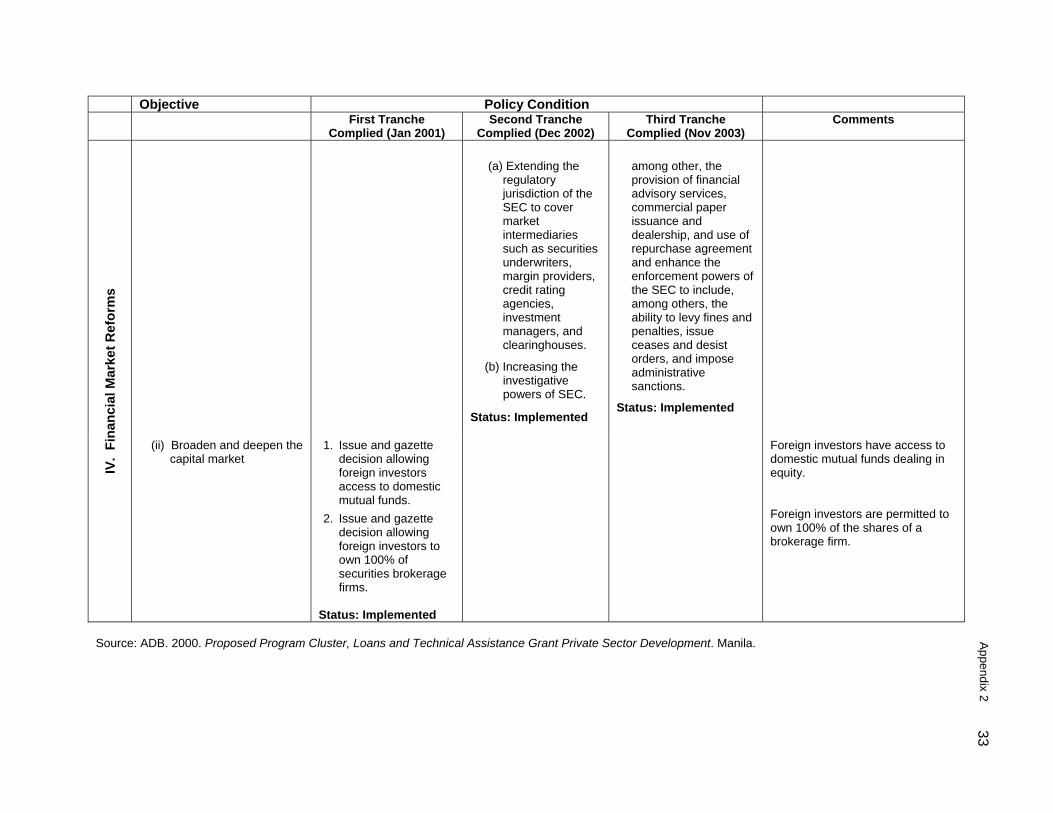

8. Disbursements a. Dates Initial Disbursement

26 Jan 2001

Final Disbursement

24 Nov 2003

Time Interval

32 months

Effective Date

31 Jan 2001

Actual Closing Date

24 Nov 2003

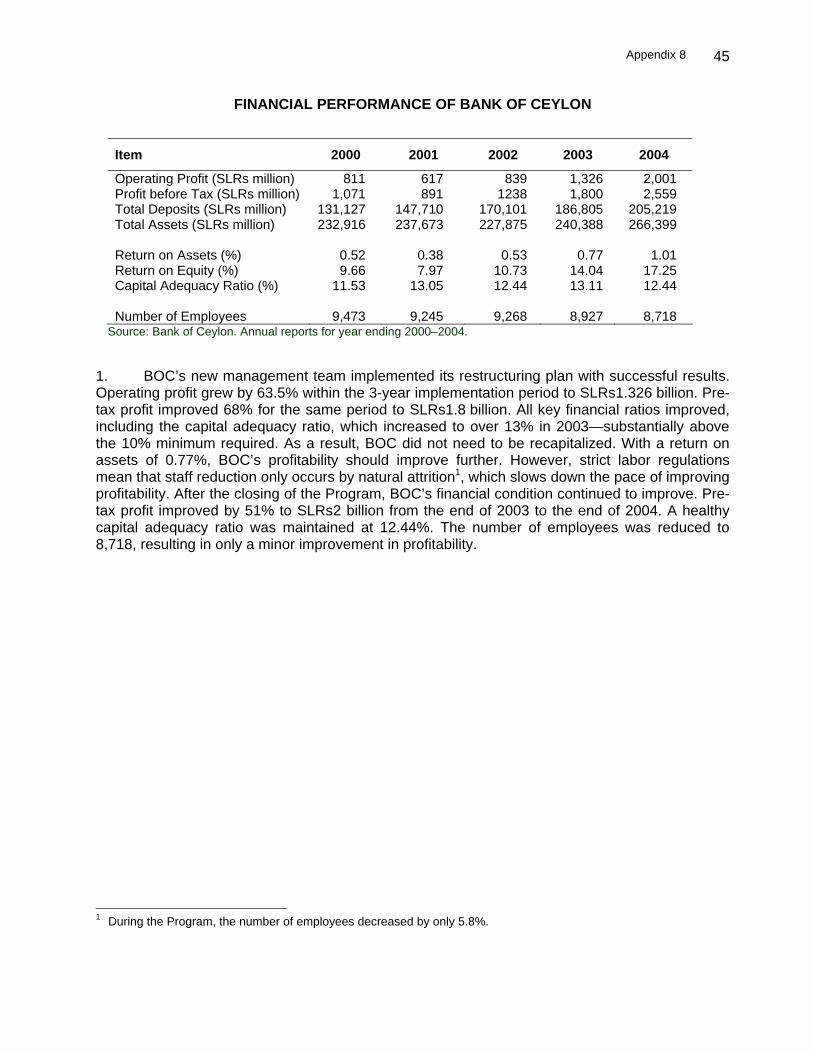

Time Interval

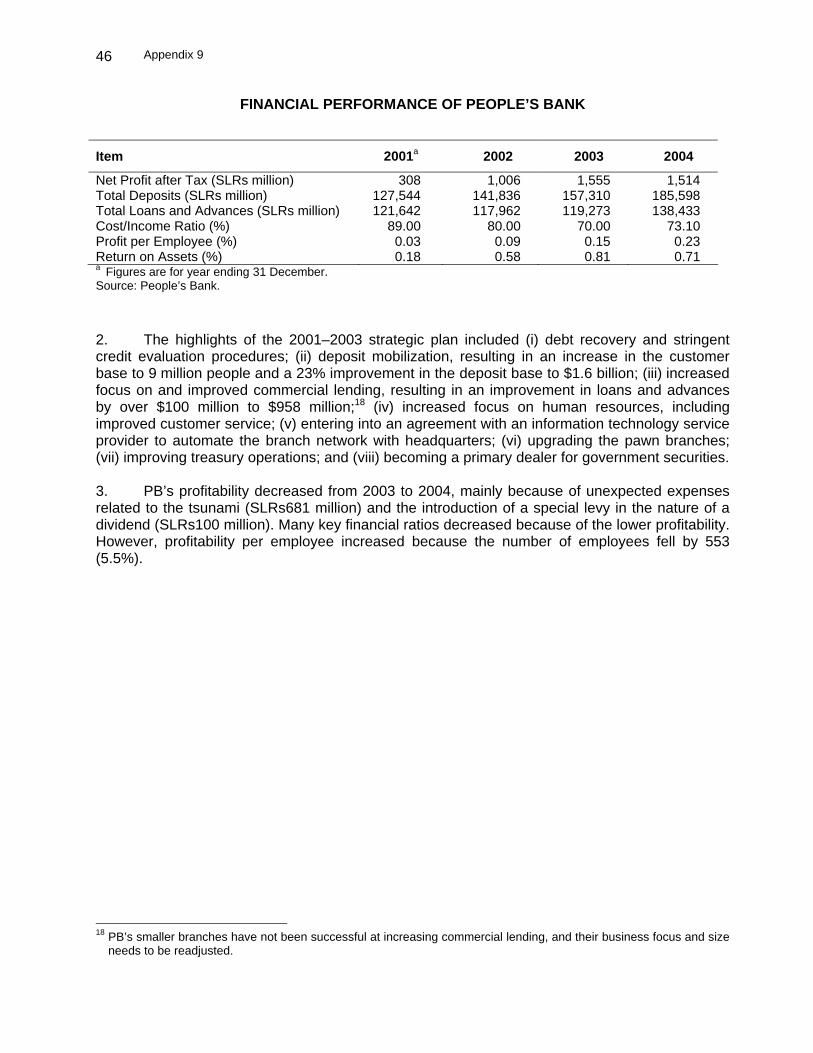

32 months

iii

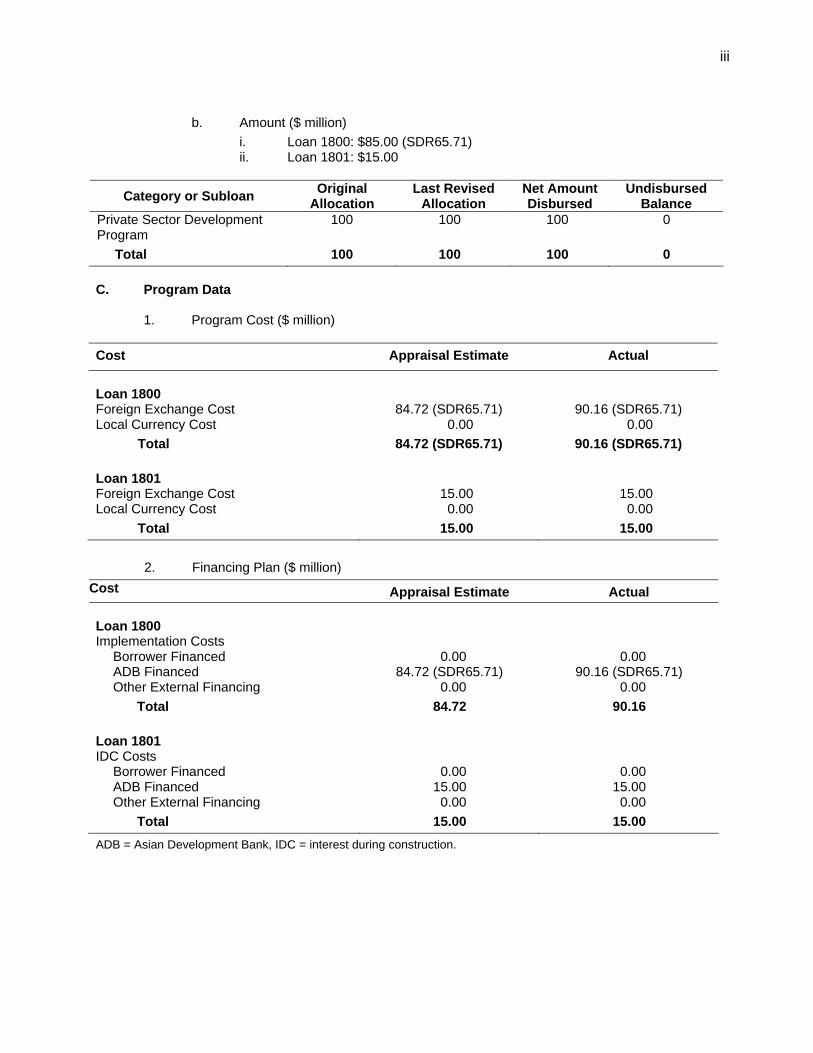

b. Amount ($ million)

i. Loan 1800: $85.00 (SDR65.71) ii. Loan 1801: $15.00

Category or Subloan Original Allocation

Last Revised Allocation

Net Amount Disbursed

Undisbursed Balance

Private Sector Development Program

100 100 100 0

Total 100 100 100 0 C. Program Data

1. Program Cost ($ million) Cost Appraisal Estimate Actual

Loan 1800 Foreign Exchange Cost 84.72 (SDR65.71) 90.16 (SDR65.71) Local Currency Cost 0.00 0.00 Total 84.72 (SDR65.71) 90.16 (SDR65.71) Loan 1801 Foreign Exchange Cost 15.00 15.00 Local Currency Cost 0.00 0.00 Total 15.00 15.00

2. Financing Plan ($ million) Cost Appraisal Estimate Actual Loan 1800 Implementation Costs Borrower Financed 0.00 0.00 ADB Financed 84.72 (SDR65.71) 90.16 (SDR65.71) Other External Financing 0.00 0.00 Total 84.72 90.16 Loan 1801 IDC Costs Borrower Financed 0.00 0.00 ADB Financed 15.00 15.00 Other External Financing 0.00 0.00 Total 15.00 15.00

ADB = Asian Development Bank, IDC = interest during construction.

iv

3. Cost Breakdown by Program Component ($ million)

– not applicable

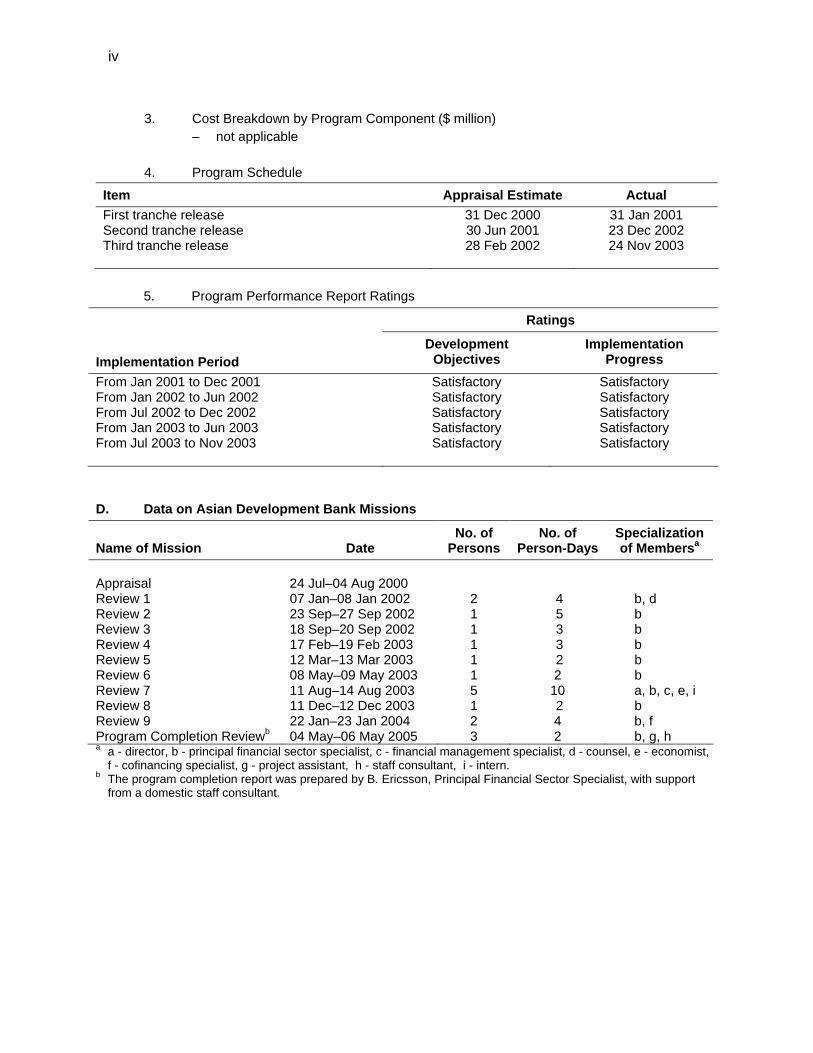

4. Program Schedule

Item Appraisal Estimate Actual First tranche release 31 Dec 2000 31 Jan 2001 Second tranche release 30 Jun 2001 23 Dec 2002 Third tranche release

28 Feb 2002 24 Nov 2003

5. Program Performance Report Ratings

Ratings Implementation Period

Development Objectives

Implementation Progress

From Jan 2001 to Dec 2001 Satisfactory Satisfactory From Jan 2002 to Jun 2002 Satisfactory Satisfactory From Jul 2002 to Dec 2002 Satisfactory Satisfactory From Jan 2003 to Jun 2003 Satisfactory Satisfactory From Jul 2003 to Nov 2003

Satisfactory Satisfactory

D. Data on Asian Development Bank Missions

Name of Mission

Date

No. of Persons

No. of Person-Days

Specialization of Membersa

Appraisal 24 Jul–04 Aug 2000 Review 1 07 Jan–08 Jan 2002 2 4 b, d Review 2 23 Sep–27 Sep 2002 1 5 b Review 3 18 Sep–20 Sep 2002 1 3 b Review 4 17 Feb–19 Feb 2003 1 3 b Review 5 12 Mar–13 Mar 2003 1 2 b Review 6 08 May–09 May 2003 1 2 b Review 7 11 Aug–14 Aug 2003 5 10 a, b, c, e, i Review 8 11 Dec–12 Dec 2003 1 2 b Review 9 22 Jan–23 Jan 2004 2 4 b, f Program Completion Reviewb 04 May–06 May 2005 3 2 b, g, h a a - director, b - principal financial sector specialist, c - financial management specialist, d - counsel, e - economist, f - cofinancing specialist, g - project assistant, h - staff consultant, i - intern. b The program completion report was prepared by B. Ericsson, Principal Financial Sector Specialist, with support

from a domestic staff consultant.

I. PROGRAM DESCRIPTION 1. On 22 December 2000, the Asian Development Bank (ADB) approved the $100 million Private Sector Development Program (PSDP or Program).1The program cluster approach was chosen to provide flexibility for PSDP implementation given the complexity and sensitivities of various reform actions to be undertaken and prevailing uncertainties owing to the civil conflict in Sri Lanka. 2. The objective of the PSDP subprogram 1 was to eliminate impediments to, and develop opportunities for, greater private sector involvement. This included developing an enabling environment conducive to private sector participation, strengthening regulatory and institutional capacity, and improving the public-private interface. The PSDP focused on (i) sustaining and reinforcing the Government’s privatization and public enterprise reform program, (ii) facilitating private sector entry into and participation in infrastructure development, (iii) enhancing the market system by promoting competition and introducing reforms for private sector activity, (iv) increasing labor market mobility and providing protection for workers through a suitable social safety net, and (v) improving private sector access to finance. The PSDP, subprogram I, also undertook preparatory work for subprogram 2.2 This report discusses the results of subprogram I.

II. EVALUATION OF DESIGN AND IMPLEMENTATION A. Relevance of Design and Formulation 3. The Program was Timely and Highly Relevant. The economy grew at an average annual rate of 5.2% during the 1990s despite (i) a suboptimal environment caused by the civil conflict that started in 1983, and (ii) periodic draughts and floods affecting the large agricultural industry. However, the Government faced the challenge of maintaining and improving living standards without resorting to substantial budget outlays. The budget deficit was 7.5% as a percent of gross domestic product (GDP) at the end of 1999, declining from 9.2% in 1998, mainly because of a rise in revenues and reduction in expenditures. A major portion of expenditures was allocated to defense—an average of 3.3% of GDP from 1990 to 1994 and 5.4% from 1995 to 1999. The Government realized that (i) higher levels of economic growth and productivity were needed to allow Sri Lanka to provide adequate employment, and (ii) it would need to attract private investment to generate the resources required to increase development and improve living standards. Aside from a bloating bureaucracy, Sri Lanka had a highly regulated economy that resulted in grossly inefficient business practices. These factors put enormous pressure on the Government to prioritize policy reforms to develop an enabling environment for the private sector. The framework for the PSDP was prepared over a 2-year period with significant participation from the Government, stakeholders, and others. Based on the Government’s goals, the Program was timely and highly relevant. 4. Sector Work. In 1997, the Government asked ADB for assistance with public enterprise and industry sector policy reform and capital market development. ADB performed substantial 1 ADB. 2000. Report and Recommendation of the President to the Board of Directors on a Proposed Program

Cluster for Loans and Technical Assistance Grant to the Democratic Socialist Republic of Sri Lanka for the Private Sector Development Program. Manila (Loan 1800-SRI for $85 million and Loan 1801-SRI for $15 million, approved on 12 December 2000). The PSDP was structured as a cluster loan with two subprograms.

2 ADB. 2004. Report and Recommendation of the President to the Board of Directors on Proposed Loans to the Democratic Socialist Republic of Sri Lanka for the Financial Markets Program for Private Sector Development. Manila (Loan 2138-SRI for $60 million and loan 2139-SRI for $5 million, Subprogram 2 was approved on 15 December 2004).

2

analytical work during the Program’s formulation and found that the main impediment to accelerated growth in Sri Lanka was the country’s incomplete transition to a competitive market system, which prevented the private sector from achieving its full potential. Based on sector studies, mission findings, technical assistance (TA) support,3 and extensive consultation with the Government and other stakeholders, the Program design was sound. 5. Capacity Building. Program implementation was supported by a TA to address key public enterprise reforms resulting from privatization and commercialization of state-owned enterprises (SOEs).4 Capacity building was provided to certain regulatory authorities: (i) Public Enterprise Reform Commission (PERC) to be responsible for privatizing and commercializing SOEs; (ii) Ministry of Finance and Planning (MOFP) to introduce good corporate governance in all SOEs; (iii) Insurance Board of Sri Lanka (IBSL) to regulate the insurance industry, which would be 100% owned by the private sector when the two largest state-owned insurance companies were privatized;5 (iv) Consumer Affairs Authority (CAA) to protect investors and consumers in deregulated industries; and (v) Securities and Exchange Commission (SEC) to support the regulation of the sale of SOE shares through an initial public offering on the Colombo Stock Exchange (CSE) and generally strengthen the capital market to attract much needed private investment capital. B. Program Outputs 6. The Program covered policy reforms for five key areas (para 2). The difficult macroeconomic and political environment in 2001 and early 2002 had a negative impact on several aspects of the PSDP—including a negative GDP of 1.5% in 2001, compared with an average of 4.2% in the 1980s and 5.2% in the 1990s. Afterward, the Government’s overall reform agenda provided positive results, including GDP growth ranging from 4.0% in 2002 to 5.5% in 2004. The details of policy actions under the PSDP, including their implementation status, are in Appendix 1. The major reform efforts that were implemented are discussed below. 7. Privatization and Public Enterprise Reform. One of the Government’s development objectives was to raise economic efficiency by transferring the management of productive SOEs to the private sector. Under the PSDP, 22 SOEs with a net asset value of SLRs9.1 billion were sold by PERC. Net proceeds to the Government amounted to SLRs23.4 billion (See Appendix 5). 8. The country experienced substantial benefits from the public enterprise reform program: (i) the insurance industry became 100% privately owned through the sale of the two dominant state-owned insurance companies, National Insurance Company (NIC) and Sri Lanka Insurance Company; (ii) the majority of shares of the country’s national airline, Sri Lanka Airlines Limited, were sold and a joint venture agreement was entered into between the Government and the majority shareholder. The majority shareholder was responsible for restructuring the airline; its loss-making operations became profitable and yearly dividends are being paid out on the remaining shares owned by the Government; (iii) the telephony monopoly was eliminated through the sale of Sri Lanka Telecom Limited (SLTL), making Sri Lanka one of the most deregulated telecommunications industries in Asia; (iv) CSE’s market capitalization increased substantially (doubled) through the sale of SLTL; and (v) the petroleum distribution monopoly

3 ADB. 1998. Technical Assistance to the Democratic Socialist Republic of Sri Lanka for Preparing a Private Sector

Development Program. Manila (TA 3075-SRI, approved on 23 September 1998). 4 ADB. 2000. Technical Assistance to the Democratic Socialist Republic of Sri Lanka for Governance and

Institutional Strengthening of Non-Bank Financial Institutions. Manila (TA 3567-SRI). 5 Tranche release condition under PSDP.

3

was eradicated through the sale of (a) Lanka Marine Services Limited, an oil bunkering company; and (b) one third of the petroleum sheds and storage facilities of Ceylon Petroleum Corporation. The proceeds of the privatizations were used to service debt, thereby contributing to the reduction of the fiscal deficit. The reduction in debt service6 and simultaneous increase in market liquidity helped ease interest rates. 9. The TA for governance and institutional strengthening of nonbank financial institutions (footnote 4) introduced the Code of Best Practices for Public Enterprises in Sri Lanka (Code) for commercial SOEs to adopt a corporate governance framework. This included (i) the establishment of an independent board of directors with at least 50% private sector representation, (ii) the requirement of audit and compliance committees, and (iii) the introduction of a performance-based compensation and promotion system. 10. Private Sector Participation in Infrastructure. One of the objectives of the PSDP was to attract private investment in infrastructure projects to enhance sector efficiences and reduce the burden on public finances. The Bureau of Infrastructure Investment (BII) was established as a separate division of the Board of Investment (BOI) to (i) facilitate foreign direct private sector investment in infrastructure development; and (ii) ensure proper processing and procedures, including publication of step-by-step checklists and procedures to be used by prospective investors. An appeals mechanism was also established to handle investor complaints and grievances. 11. Introducing Reforms for Private Sector Activity. Proper regulatory authorities and appropriate regulations were put in place before the sale of SOEs (footnote 4) to eliminate or reduce monopolistic behavior, and encourage competition and private sector development. The Telecommunications Regulatory Commission was established before the privatization of SLTL, and the monopoly over telephonic services was eliminated through the issuance of external licenses to 23 independent telephone operators. The multisector Public Utilities Commission of Sri Lanka was created to regulate utilities providing electricity, water, petroleum, and ports services. IBSL was established to regulate the insurance industry. The establishment of a single authority to regulate the nonbanking financial industry, the Financial Supervisory Authority, is being considered to combine the nonbank financial regulators, IBSL, and SEC. 12. Competition Policy and Consumer Protection. The Consumer Affairs Authority (CAA) was established to protect investors and consumers against unfair competition, and it defined a competition policy and regulatory framework for the country. CAA has reviewed complaints and anticompetitive activities, and has implemented stiff measures to eliminate cartel-like behavior in the pricing of certain products deemed consumer necessities. A consumer protection council was also established and made operational to register consumer grievances. 13. Labor Market Reforms. The Termination of Employment of Workmen (Special Provisions) Act No. 45, 1971, (TEWA) establishes specific procedures to be followed when terminating employees other than for disciplinary reasons. TEWA is one of the most rigid labor laws in Asia7 and, for all practical purposes, prevents employees from being terminated. To circumvent the rigidity of the law, many employers have hired fewer employees, encouraging substantial overtime and hiring part-time employees. The labor environment created under

6 Debt service (i.e., repayment of the principal as a percentage of GDP) declined from 14.7% in 2000 to 13.2% in

2002 and 11.6% in 2003. The weighted average prime lending rates for commercial banks decreased from a high of 21.46% (31 December 2000) to 8.95% (31 December 2003).

7 ADB and World Bank. 2004. Investment Climate Study. Manila.

4

TEWA has not been conducive to reducing long-term unemployment, increasing productivity, or encouraging private sector development. 14. As part of the Program’s policy reforms, Parliament approved an amendment to TEWA in which a formula was devised for (i) the time to settle cases involving involuntary employee separation, and (ii) a formula for the maximum compensation payable to an employee who has been retrenched. 15. Reforms complementing the TEWA amendment included the establishment of 23 JobsNet centers throughout the country. JobsNet centers provide counseling, placement, and retraining of displaced employees. 16. An employment services mediation centre was established on the initiative of the Employers’ Federation to resolve employment disputes more rapidly without confrontation. Its members include some of Sri Lanka’s leading businesses and larger labor unions. It focuses on awareness building and providing training mediation. 17. Financial Market Reforms. Effective participation by the private sector in the economy requires adequate access to funding on viable terms. Over the years, the Government needed to finance its large fiscal deficit, which resulted in (i) crowding out the private sector from the financial markets (i.e., over 60% of total lending is government borrowing); and (ii) high interest rates on borrowed funds. Improved access to adequate capital for the private sector is largely dependent on the success of the Government’s fiscal consolidation efforts in reducing government borrowings in the market, increased efficiencies of financial intermediation, and further development of the domestic capital market. 18. To reduce the crowding out of the private sector from the financial market, the Program supported the Government’s shift from direct borrowing from captive institutions (i.e., state-owned savings bank and state-owned provident funds) at lower than market rates. The Government began issuing market-based securities by borrowing through the issuance of domestic Treasury bills and Treasury bonds at “near” market rates. From the introduction of the Program in December 2000 until the end of 2004, direct domestic Sri Lanka rupee government borrowing was reduced by 35%, while the issuance of Treasury bills and bonds together improved by over 160% during the same period (Appendix 3). In 2004, the Central Bank of Sri Lanka (CBSL) created the Public Debt Department, which has been given the responsibility of issuing and managing public debt instruments. A medium-term goal is to establish a National Debt Office, independent from the decisions of the Ministry of Finance and CBSL.8

a. State Banks 19. Until 2001, the two commercial state-owned banks, Bank of Ceylon (BOC) and People’s Bank (PB), followed government instructions that state-owned banks must purchase government-issued securities. The country’s large fiscal deficit caused a strong demand for government funding resulting in the private sector being crowded out from borrowing from state-owned banks. To improve the profitability of state-owned banks, the interest rate margin between deposit and lending rates increased with little adjustment made when interest rates started to decline. Private commercial banks followed the example of state-owned banks and charged higher interest rates, resulting in high lending rates and further crowding out of the private sector. 8 The introduction of a bill to parliament for the Establishment of the National Debt Office is a requirement of the

tranche release of the Financial Market Program for Private Sector Development subprogram (footnote 2).

5

20. Historically, the Government directed BOC and PB to provide loans to certain customers (e.g., financially weak SOEs). This resulted in each bank managing a credit portfolio with a substantial number of nonperforming loans (NPLs). 21. During the Program, credit exposure to the Government and SOEs was reduced to about 30% of loans for BOC (from a peak of 60%) and 21% for PB (from 43%). Based on international standards for classifying NPLs, the percentage of total loans outstanding that were nonperforming was about 40% for BOC and 26% for PB in year 2000. By the end of the Program (end of 2003), NPLs constituted 14% of BOC’s total loans outstanding and 18% for PB; this declined to around 10% for BOC and 14% for PB at the end of 2004. 22. The board of directors of BOC and PB were changed and professional management was recruited through reforms introduced by the Program. Steps were taken toward introducing best practices in governance, reducing the number and volume of NPLs, reducing exposure to SOEs, and introducing credit and treasury risk management. Strategic and corporate business plans were prepared. New computer systems to integrate the extensive branch networks of each of the banks were introduced and are in the process of being installed at all branches to improve efficiency. The profitability of both banks has improved substantially (paras 34–42). 23. The state-owned National Savings Bank (NSB), the country’s second largest, has about 20% market share of the banking system’s total deposits. To improve competition in the banking sector, the Government was supposed to remove its guarantee on NSB deposits as a policy reform under the Program. However, the guarantee has yet to be removed. The guarantee attracts substantial deposits to the bank, so NSB has become a captive source for investing in government securities, which are used to fund the budget deficit. According to a government directive, NSB’s minimum investment in government securities should be 60% of total assets; actual investment is still around 80% of total assets—the same level as at the start of the Program. Therefore, the Program had no impact on the policy reforms envisioned for NSB.

b. Contractual Savings

24. To improve private sector access to finance, among other things, the Program supported the development of (i) contractual savings products, including products from the insurance industry, private pensions, and the provident fund; and (ii) the securities market, including improvement in governance to promote the stability and depth of the capital market. 25. As part of the PSDP’s policy reforms, the Regulation of Insurance Industry Act was passed in 2001, further liberalizing the insurance industry. The Act reduced the requirement for mandated investment in government securities from 50% to 30% for life insurance companies, and 30% to 20% for non-life insurance companies. Private sector money supply and access to finance improved (Appendix 6). The mandatory 15% reinsurance cession to the previously state-owned NIC was eliminated. By liberalizing the reinsurance market, domestic insurance companies could have access to the international market, making reinsurance costs more competitively priced in the domestic market.

26. Under the PSDP, the Government was obliged to (i) adopt a comprehensive strategy to restructure the pension system; and (ii) formulate an overall reform plan to strengthen fund management, especially of the two state-owned provident funds which manage over 75% of the total pension funds. The largest fund, Employees’ Provident Fund, has 98% of its portfolio invested in government securities; the other pension fund, Employees’ Trust Fund, invests over 80% of its portfolio in government securities. Together, the two state-owned provident funds

6

have an investment portfolio equivalent to over 20% of GDP. The objective of the restructuring plan was to (i) improve pension fund yields, (ii) diversify provident fund investments to include private sector securities, (iii) extend coverage to employees, (iv) strengthen administration, and (v) rationalize taxation of the pension funds. In September 2003, the Superannuation Benefit Fund Regulatory Commission Bill was submitted to Cabinet, which recommended that a commission be established to address the strategy to restructure the pension system. However, the Bill was never passed by parliament. Instead, the Government is reviewing the entire structure of the two large state-owned provident funds, including methods of reducing operating costs by possibly merging the funds.

c. Securities Market Development 27. Amendments to the SEC Act passed in January 2003 broadened the scope of securities-related activities open to licensed brokers. This resulted in SEC regulating the entire nonbank financial industry. To strengthen its supervisory role, SEC was also given increased investigative and enforcement powers, including the ability to levy fines and penalties, issue cease and desist orders, and impose administrative sanctions. 28. In the government bond market, primary dealers are given privileged access to auction government securities; in return, primary dealers must be market makers for such securities. To strengthen the system, CBSL made it mandatory for all primary dealers to be established as separate legal entities. The minimum Tier I capital9 requirement for primary dealers was increased from SLRs200 million to SLRs350 million (as of 31 December 2004). The market was strengthened by requiring primary dealers to maintain a minimum capital to assets ratio (capital adequacy) of 5% with Tier 1 capital constituting not less than 70% of total capital funds. The reforms reduced the risk of credit default by primary dealers. To facilitate secondary market trading, CBSL automated the clearing and settlement system of government securities through the introduction of scripless securities trading. As a result, government securities are cleared and settled in real time, reducing the interest rate risk to investors and primary dealers. C. Program Costs 29. ADB supported the Program with a policy loan as described in the development policy letter and policy matrix (Appendix 1 and 2) and an attached TA grant for $1.9 million (footnote 4). The loan was for $100 million, of which $85 million was financed through ADB’s Japan Special Funds and $15 million was financed through ADB’s ordinary capital resources. The program loan size was determined by its strategic significance for private sector development, and the strength and costs of structural reforms.

D. Disbursements

30. The Program was approved on 12 December 2000 and was disbursed in three tranches. The first tranche of $25 million was released on 31 January 2001, when the Program was declared effective. The second tranche of $25 million was disbursed on 23 December 2002 and the third tranche of $50 million was disbursed on 24 November 2003, upon compliance with corresponding tranche conditions.

9 Based on the Regulations established by the CBSL, each licensed primary dealer must maintain a minimum ratio

of shareholders’ equity to total capital of 70%.

7

31. The Government requested that the undisbursed portion of the loan as of July 2003, be subjected to the terms and conditions of ADB’s London interbank offered rate (LIBOR)-based lending facility. Consequently, ADB and the Government agreed that, as of 11 July 2003 (the transformation date), the $50 million undisbursed loan would comprise (i) a pool-based loan of $35 million, and (ii) a LIBOR-based loan in the amount of $15 million. Therefore, the initial Loan Agreement was amended and restated to provide for the application of different terms and conditions to the portion of the loan that remained undisbursed on the transformation date. E. Program Schedule

32. The Program period was envisaged to be from December 2000 to December 2002. However, the release of the second tranche was delayed by 18 months because of factors not foreseen at the time of the Program’s design, including the political turmoil in the second half of 2001 which led to the dissolution of parliament. Following the general election in December 2001, the reform process was revived and the second tranche was disbursed in December 2002. The third tranche, originally scheduled for release by December 2002, was delayed because of the 18-month delay of the second tranche. However, actual implementation of the reform efforts was expedited, and all conditions for the third tranche release were fully or substantially met within 12 months rather than 18 months, as envisaged.

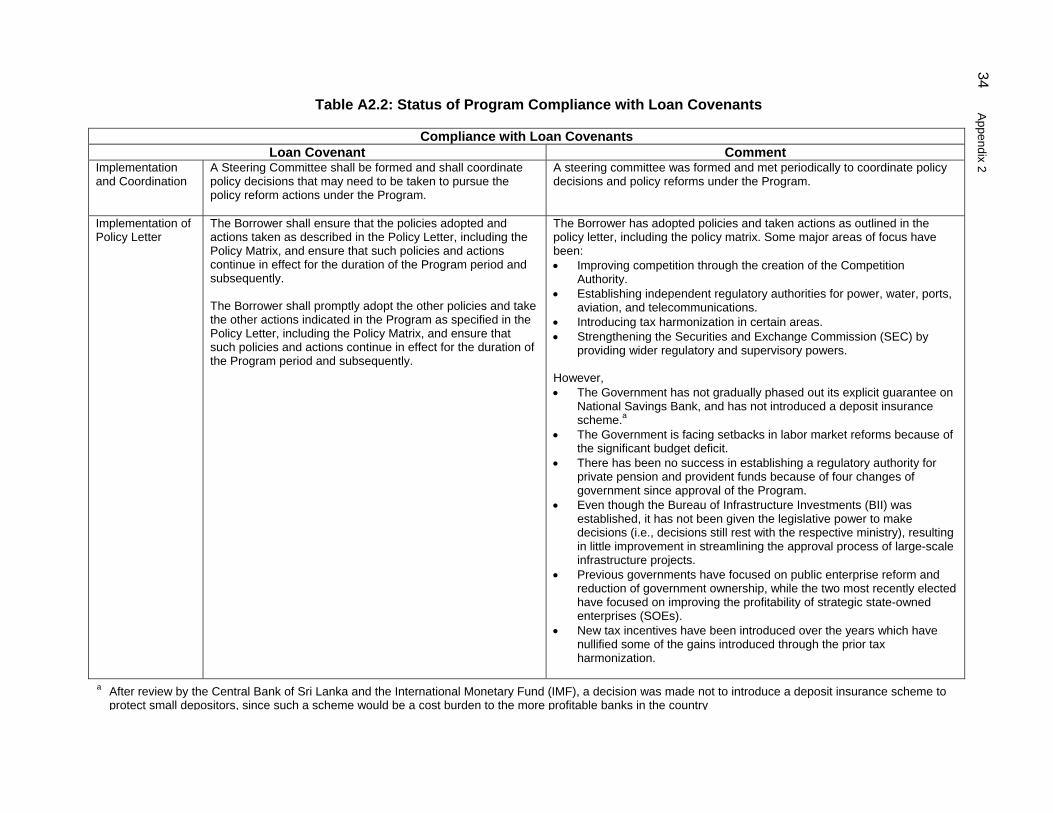

F. Implementation Arrangements 33. ADB staff members closely monitored program implementation. MOFP was the Executing Agency (EA) for the PSDP and its Finance and Planning Department was the Implementing Agency (IA). All participating agencies supported the PSDP—including PERC; BOI; regulatory bodies (SEC, IBSL, and CAA); state-owned banks (BOC, PB, and NSB); and relevant ministries (MOFP, Ministry of Labor and Employment, and Ministry of Trade and Commerce). Overall, implementation arrangements were satisfactory in delivering program outputs and achieving the purpose of the Program (See Appendix 2).

G. Conditions and Covenants

34. The PSDP provided 32 policy conditions to be complied with. Of these, 14 were complied with at the time of approval by ADB’s Board of Directors. Of the 8 policy conditions to be complied with for the release of the second tranche, all were fully complied with (including 2 as amended). A further 10 conditions were specified for the third tranche; 8 were fully complied with (including 2 as amended) and 2 conditions were substantially complied with (Appendix 2).

35. The implementation of voluntary retirement schemes (VRS)—for workers of SOEs to be divested under the PERC program—had to be amended because of a change in circumstances in the second and third tranche release. The objective of this condition was to mitigate the adverse impact of privatization on the employees of affected SOEs when pre-privatization retrenchment was undertaken. The Government found it difficult to selectively target redundant labor and offer a VRS to such workers without opening itself to charges of discrimination. Consequently, the VRS was offered to all workers and the Government frequently faced the problem of adverse selection, as better and more skilled workers took the VRS and left the enterprise. Over time, bargaining by trade unions led to an increase in the average value of the compensation packages. The compensation packages became so attractive that more workers than targeted opted to leave; in several cases, a significant number of the workers were rehired by the enterprise after privatization. In addition, pre-privatization retrenchment did not take into account any plans that the investor might have for capital restructuring, retraining, and changes

8

in production plans after privatization. Given the experience with pre-privatization downsizing in Sri Lanka, labor retrenchment has been left to private sector investors who take over the enterprises. 36. Through PERC activities, the Program supported a reduction in government ownership of SOEs through privatization. Since February 2004, the Government has changed strategy regarding public enterprise reform by focusing on efficiency and improving the profitability of key strategic SOEs10 that remain under state ownership.

37. At the time of Program approval (year-end 2000), BOC and PB faced significant financial instability, including failure to meet prudential regulations set out by the bank regulator, CBSL. As part of the PSDP, the Government agreed that (i) it would not use more public resources to recapitalize BOC and PB, and (ii) any additional capital must be raised from private sources. BOC’s restructuring program is ongoing and substantial progress has been made, reflected by the enhanced financial performance in terms of profitability, asset quality, liquidity, and asset and liability structure (see Appendix 8). 38. Substantive reforms were also made to depoliticize PB, including appointing new board members from the private sector. Top management from the private sector, with significant international banking experience, was hired in 2001, resulting in a significant reduction in political influence on bank management and operations. The new management was given the mandate to restructure PB and introduce operational improvements through the implementation of a strategic plan (2001–2003). Such measures included reducing the bank’s cost structure, introducing risk management techniques, and ensuring sharper customer focus. When structuring the second cluster of the Program (footnote 1), the Government decided not to privatize PB and requested ADB to provide financial support for its recapitalization. ADB provided a program loan (footnote 2) for a phased-in recapitalization of PB, on condition that it meet financial criteria as established in a strategic plan approved by Cabinet. Appendix 9 compares PB’s actual financial results for 2001-2004. H. Related Technical Assistance

39. Under the TA grant (footnote 4) for $1.9 million, included in the Program, $1.715 million has been utilized. The unutilized funds (about $185,000) are scheduled to be fully utilized by the end of September 2006, the final closing date for the TA. Parallel cofinancing grant was organized by ADB for the equivalent of $1 million to focus primarily on labor market reforms and capacity building of the CAA. However, the funding was not provided because of the slow approval of the TEWA amendment, the CAA became operational just before the third tranche release, combined with CAA’s lack of interest in TA at the time. I. Performance of the Borrower and the Executing Agency 40. The Government demonstrated strong ownership during implementation. It fulfilled the conditions of the first tranche on time and significant progress was made on the second and third tranche conditions. Delays were mostly caused by external factors beyond the scope of the Program. The performance of the EA and IA are rated satisfactory. The ministries of finance, 10 PB, BOC, National Savings Bank, State Mortgage and Investment Bank, Ceylon Electricity Board, Ceylon

Petroleum Corporation, Sri Lanka Ports Authority, Airports and Aviation Authority, Sri Lanka Railways, Sri Lanka Central Transport Board (responsibilities include the state-owned bus company), National Water Supply and Drainage Board, and State Pharmaceutical Corporation. SEMA companies have combined total assets of over $10.5 billion and about 125,000 employees.

9

labor and education, and trade and commerce cooperated in implementing the various policy actions. However, policy reforms slowed down (and sometimes reversed) and impediments to reforms developed when there were new elections11 (In addition, some reforms could not be implemented because of contradictory policy decisions. For example, the Government introduced a freeze on hiring new employees at all SOEs in 2002/2003, preventing state-owned banks (BOC and PB) from recruiting the necessary external professional staff to fully implement their restructuring plans.

J. Performance of the Asian Development Bank 41. ADB monitored the PSDP regularly through frequent visits to the EA and the IA, and close supervision. From 2001 to 2003, nine review missions were undertaken, totaling 37 person-days, focusing on the compliance review and implementation of the loan and TA. Implementation of a large and complex program such as the PSDP was very demanding on staff time, both for substantive inputs, guidance and administrative support. Project officers handling the Program changed twice during implementation but the last project officer managed the release of the second tranche, and the third tranche was released 12 months later, instead of the scheduled 18 months. Because of limited staff resources, some review missions were conducted in conjunction with other projects and missions in Sri Lanka to enable close monitoring of program implementation. The Sri Lanka Resident Mission provided valuable support, especially in facilitating timely information. The overall performance rating of ADB is satisfactory.

III. EVALUATION OF PERFORMANCE

A. Relevance 42. The PSDP is assessed as relevant to Sri Lanka. The Program’s goals, purposes, and outputs were consistent with the Government’s development strategy and ADB’s country strategy for Sri Lanka. The Program remained relevant, appropriate, and timely through implementation. The Program’s scope was broad-based and ambitious. However, a balance should have been drawn between broad-based and in-depth policy actions. 43. The Government was closely involved in designing the Program through policy dialogues. Program objectives were defined in accordance with the Government’s development agenda and ADB’s country development strategy for Sri Lanka. The Government owned the Program from the design stage. B. Effectiveness in Achieving Outcome

44. The PSDP loan was successfully implemented. Intended outputs from the policy framework were achieved: (i) proceeds were received from the sale of government shareholdings in SOEs for a total of SLRs24.5 billion; (ii) the Code of Best Practice for SOEs was introduced; (iii) expansion of the telecommunications industry to the private sector was accomplished by privatizing SLTL; (iv) competition policy and consumer protection was strengthened through creation of the CAA; (v) the two state-owned banks, which accounted for about 40% of banking industry assets improved their efficiency and profitability; (vi) the insurance regulator (IBSL) was established; (vii) the insurance industry was liberalized by privatizing all the state-owned insurance companies; (viii) the reinsurance industry was opened 11 There were four changes in government from loan effectiveness until January 2006.

10

to competition in the private sector; and (ix) the securities market was broadened, and deepened and governance was improved by providing more regulatory power to SEC.

1. Privatization and Public Sector Reforms

45. The privatization program was substantially met. PERC also took steps to improve the assessment, monitoring, and transparency of future privatization transactions. There has been acceptance within SOEs to improve their governance, accountability, and efficiency. Steps have been taken to make it mandatory for SOEs to follow codes of governance and best practices in accounting. 46. One of the outputs of the privatization was to improve the liquidity of shares listed on the CSE. However, many of the SOEs were sold to private investors rather than being listed on the CSE, mainly because of the financial weakness of the privatized SOE. Only the larger well-structured SOEs were listed on the CSE (e.g., SLTL). 47. Since February 2004, governments changed the SOE strategy from privatization to focus more on public enterprise reform—by improving the efficiency and profitability of SOEs—with special emphasis on strategic SOEs that provide essential services to the country. Twelve of the larger strategic SOEs were transferred to the Strategic Enterprise Management Agency (SEMA) to provide professional management free from political interference. Many strategic SOEs are sustaining operating losses and are being supported by government subsidies. There are no plans to privatize the strategic SOEs at present. Instead, SEMA’s public enterprise reform and restructuring strategy is to provide additional strength to strategic SOEs to become profitable and achieve strict performance targets.

2. Private Sector Participation in Infrastructure

48. Over the last few years, BII has had to deal with changing policies and direction, and administration of various governments with regard to encouraging private sector investment. Granting tax concessions is the primary incentive for increased private sector participation but is not as effective as it used to be. In addition, the current law does not give BOI the power to address all grievances, particularly where obstructions are created by other agencies for political or other purposes. BII is mandated to support line ministries and government agencies in identifiying, evaluating, negotiating, and implementing private sector infrastructure projects under build-own-operate, build-operate-transfer, and build-own-operate-transfer arrangements. However, there has been considerable delay in processing such projects, mainly because of administrative issues such as poor coordination, lack of procedures, and lack of capacity. Legislative change is required to fully implement the one-stop shop concept to be offered by BII. Private sector investments were also negatively impacted because of the absence of a clear medium-term sector development plan. 49. The Government offered special tax incentives to stimulate private investment but these ad hoc tax measures have had adverse effects on the country’s aggregate fiscal deficit. In the longer term, the Government should identify a flat rate of taxation for all entities (i.e. 15% was once contemplated in 2002). Besides the flat tax rate, other methodologies should be identified to encourage long-term investment.

3. Labor Market Reforms

50. The implication of policy actions associated with the TEWA amendment were too ambitious and did not result in far-reaching reforms for labor issues. The rigidities of the TEWA

11

have been a major cause of inefficiency and substantial cost to all employers, including the private sector. Recruitment policy is impacted by (i) inability to terminate employees for non-disciplinary reasons without the approval of the Commissioner of Labor, (ii) uncertainty of the period during which wages need to be paid, and (iii) compensation that has to be paid. The TEWA amendment was supposed to facilitate labor market mobility. However, the conflicting interests of employees, employers, and Ministry of Labor modified the formulas in the amendment several times; for all practical purposes, it was never implemented. Major changes in labor laws must still be introduced and implemented over a longer period, and a social safety net (e.g., unemployment insurance) must be introduced simultaneously. However, the country’s budget deficit rules out increased spending for a social safety net in the short to medium term. 51. Labor issues are one of the largest deterrents for private sector development in Sri Lanka. The TEWA amendment, the establishment of JobsNet centers, and the Employment Service Mediation Center are only a partial solution to the substantially larger issues involving labor, unemployment, and a social safety net. Resolution of the labor issues requires significantly more work and major restructuring. The Government must be committed to major changes in labor legislation and the resulting costs to resolve the labor issues. Because of the significant issues around labor—including termination, unemployment insurance, training and/or skills development for the unemployed—as well as the substantial commitment by stakeholders, labor issues could be addressed as a separate program rather than trying to implement major changes under a program to improve private sector development. C. Efficiency in Achievement of Outcome and Outputs 52. Public Enterprise Reforms. Public enterprise reform is rated sustainable. However, the emphasis on the type of reform to be implemented—privatization vs. public enterprise reform—depends on the government in power. SEMA was created in May 2004 to professionally manage, restructure, and eventually eliminate budgetary support for 12 strategic SOEs. The following problems are being addressed through implementation of the Code in all SEMA-managed SOEs: (i) governance issues specifically related to SOEs and their relationship with the Government (e.g., the need for an independent board of directors, commercial independence, etc.); (ii) maintaining the distinction between SOEs’ financial objectives and the Government’s political or social objectives; (iii) implementing a strategy and maintaining financial and commercial targets for each SOE; (iv) establishing standards for the quality of service the public can expect from SOEs; and (v) emulating private sector incentives. Through implementation of the Code, each of the SEMA-managed SOEs (i) have board representatives from the public and private sectors, (ii) have developed and are implementing their respective corporate strategy, and (iii) publish timely annual reports with improved disclosure.

53. Private Sector Participation in Infrastructure Development. For private sector participation in infrastructure development to be sustainable, amendments to the BOI laws are needed to obtain the legal backing required for the BOI and/or BII. However, the Government’s support is also needed in the form of consistent policy so that investor confidence is retained and the credibility of BOI and/or BII as an institution and of the Government is not lost. As a result of the country’s fiscal deficit, the Government is focusing on private sector participation as a means to finance the development of the necessary infrastructure. Therefore, the preliminary assessment is that private sector participation in infrastructure development is most likely to be sustainable. Private-public partnerships and joint venture agreements should become a government priority for private sector participation in infrastructure development.

12

54. Competition Policy and Consumer Protection. The need to improve competitiveness and consumer protection are, in principle, accepted by all political parties. CAA needs additional capacity, especially in implementing international best practice standards from a competitive policy and consumer protection standpoint. However, in CAA’s decisions to protect consumers against cartel-like behavior by certain industries, CAA should take into account that (i) the private sector must be profitable to succeed; and (ii) competition, rather than CAA’s regulation of profit margins, will stimulate private sector development and protect the consumer. The Government should also give the necessary power to an appropriate authority to approve mergers and acquisitions from an antitrust perspective. These measures would further improve competition policy and consumer protection. 55. Labor Market Reforms. The long-term sustainability of labor reforms and the introduction of a viable social safety network remain challenging. To resolve the rigidity of the labor laws and develop a modern, more flexible labor market, a major overhaul of the labor laws is needed; labor and its unions must cooperate fully. However, a major part of the problem is due to the fiscal deficit and the Government’s inability to support the social safety net needed to address the labor problems (e.g., social security and unemployment). To resolve this issue, a separate program must be developed to address the entire labor, social safety net, and fiscal deficit supported by all stakeholders. Only then can a time-bound program be implemented to resolve some of the major labor issues. An assessment of the labor market reforms included in the Program is rated unlikely to be sustainable. 56. Financial Market Reforms. Further reforms in the financial services sector should be introduced. Structural and process reforms are being implemented in state-owned banks but rigid labor legislation hinders sweeping reforms. Improved risk management must also be implemented in state-owned and private banks to maintain a sound financial system, and NPLs must decrease in the banking system to reduce interest spreads. The reforms introduced through the Program are sustainable. 57. However, to improve competition and create a more level playing field in the banking sector, the Government’s guarantee on NSB should be withdrawn, and NSB’s investment in government securities should be further reduced. D. Preliminary Assessment of Sustainability 58. The Program’s sustainability was assessed successful.12 Two of the risks identified at the outset of the PSDP were (i) a possible change in government and (ii) lack of political will to carry out the reforms. During program implementation, two changes in government—one soon after the program began and the second less than 6 months after the final disbursement—contributed to implementation delays. Two additional elections have taken place since the final tranche release. However, successive governments’ recognition of the need for reform has, for the most part, remained consistent. E. Impact 59. The Program was categorized as environment category B with no direct environmental impact. There were neither indirect nor long-term negative environmental impacts. The Program did not encounter any unanticipated impact on indigenous people during implementation. The

12 ADB.2000. Guidelines for the Preparation of Project Performance Audit Reports. Manila. (The rating categories are

highly successful, successful, partly successful, and unsuccessful).

13

Program’s design included VRS for workers retrenched because of privatization, and training and rehabilitative services for such employees.

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS

A. Overall Assessment 60. Overall, the PSDP is rated successful (footnote 12). SOEs have been given a code of good governance which is being implemented. Although the Government’s privatization program may have slowed down, public enterprise reform is being enforced through emphasis on efficiency, profitability, and governance in the longer term. Improved processes are in place through the establishment and/or strengthening of regulators to support competition and private sector development. A regulator is in place to ensure that protection is granted to investors and consumers when dealing with competition issues.

61. Steps must be taken to ensure that the process is followed through. The new processes outlined must be communicated to stakeholders. In areas where capacity building is required, sufficient support should be provided as a matter of urgency to ensure that momentum is not lost. At the same time, complementary measures required to fulfill the Government’s ultimate aim to encourage private sector participation in the economy must be identified, considered, and implemented. In this regard, it must also be ensured that such measures comply with the Government’s other economic and fiscal policies and are not counterproductive. For example, using tax benefits as an incentive to prospective investors should be carefully thought through without negatively impacting the Government’s overall revenues. B. Lessons Learned 62. The approved PSDP was presented as a program cluster to provide adequate flexibility in changing circumstances, especially because of civil unrest at the time of approval. Political instability resulting from the dissolution of parliament on two occasions, followed by elections and changes in the macro-environment, had a negative impact on the implementation of the PSDP. Also, given the wide-ranging scope of the PSDP—covering five areas of economic focus, with an upfront identification of detailed conditionalities for each of the three tranches of subprogram 1, inclusive of legislation to be implemented over an anticipated period of 25 months was a challenge for the Government. In the release of the second and third tranche, two conditions were modified because of the change in circumstances would have a negative effect on the country if the conditions were to be implemented. In order to provide adequate flexibility, a program cluster should be designed as a set of single tranche subprograms, with each subprogram comprising clearly defined policy actions that are calibrated to be achievable within a relatively short time frame. 63. Under the program cluster approach, other multilateral institutions may finance programs originally proposed to be included in future subprograms of the cluster loan. The PSDP’s subprogram 1 and proposed follow-on (subprogram 2) were put in place before the World Bank’s Poverty Reduction Strategy Credit was developed. The World Bank program overlaps some of the focus areas of PSDP’s subprogram 2. Organizational restructuring within ADB also shifted responsibility for many of the components that were originally envisioned to be included in subprogram 2 to other departments, which are implementing them. Although the PSDP was structured as a cluster, only 1 of the 15 areas considered in the preparatory work for subprogram 2 were actually included in subprogram 2 (footnote 4).

14

64. Proceeds received from the sale of SOEs are dependent on the economic environment and market conditions. A predetermined mandatory program for privatizations—with a quantified net asset value within a specified period to meet tranche release conditions—may not always optimize proceeds. Instead, it could result in underpricing of shares as demonstrated in the sale of SLTL and Sri Lanka Insurance Corporation Ltd., both of which were sold in order to meet tranche release conditions when the stock markets were plummeting worldwide and the Sri Lanka market was at a relatively low level. In addition, the regulatory authority must be operational to properly regulate the industry (i.e., IBSL) before a privatization takes place. 65. Some measures, such as VRS schemes for the involuntary termination of workers for SOEs that are to be divested, have significant budgetary implications. When including such measures in the policy matrix, it is important to ensure that the fiscal situation can support such measures and the necessary budget allocations are made. C. Recommendations

1. Program Related 66. Future Monitoring. Although the Government is moving towards issuing its public securities at market rates, CBSL must also become more proactive in raising interest rates, especially when the yield curve is rising. A true market yield curve will only develop if CBSL and the Government implement best practices when public debt securities are listed. 67. The capital market, including the debt market, must be further developed. Improved regulations, new products and services must be introduced.13 Issue of corporate debt continues to be limited, with a concentration on the issue of commercial paper bank borrowings. This is largely due to lack of public awareness and, more importantly, a need to harmonize the tax laws pertaining to the issuance and sale of government securities and publicly traded corporate debt. 68. Since SEMA is responsible for ownership and management of the four state-owned banks, the role of all state-owned banks should be further reviewed, particularly with regard to increasing competition in the banking market and strengthening the banking system in general. 69. Covenants. The requirement for PERC to submit to ADB plans for voluntary retirement of workers for each SOE to be divested by the Government based on PERC’s ongoing program should be waived, since voluntary retirement system was too expensive to implement at the onset of the Program. 70. Further Action or Follow-Up. The laws pertaining to BOI and BII should be amended to obtain the required backing for implementing their processes and services. Support is needed in the form of consistent policy to obtain the necessary confidence of private sector investors and the credibility of financial institutions. Steps should also be taken to review tax incentives offered by BII and the Government’s requirements to increase revenue to reduce the fiscal deficit. 71. Improved governance and enhanced capacity in the regulatory bodies of the financial services sector would build public confidence in the financial markets. Improved performance by

13 ADB. 2004. Technical Assistance to the Democratic Socialist Republic of Sri Lanka for Implementing Products and

Services for the Domestic Debt Market. Manila (TA 4421-SRI). This TA is being provided primarily in the form of capacity building for the domestic debt market.

15

state-owned banks would contribute to the strength of the banking system. Stronger banks would provide further funds for development of the country by the private sector. 72. Through its restructuring plan and support from the Program (footnote 2), PB will better serve the private sector, mostly small and medium-sized enterprises in the nonurban and/or rural areas of the country. Although the Government has a conflict of interest by being responsible for a strong financial system on the one hand and owner of a bank on the other, it should make it mandatory for NSB to reduce its investments in government securities. The Government should also eliminate its guarantee, as planned under the Program’s policy reforms. In addition, the Government should readdress the Superannuation Benefits Fund since it could play a major role in capital formation for the private sector. 73. Mergers and acquisitions of commercial enterprises could reduce competition and compromise consumer protection. Therefore, CAA’s scope should be extended to (i) cover these areas, and (ii) work in tandem with SEC’s Mergers and Acquisition Code. CAA must also become more involved with questions related to government subsidies of SOEs, which does not create a fair playing field. 74. Additional Assistance. The Program supported the establishment of key regulatory bodies (CAA and IBSL) and strengthening of others (SEC, BOI, and BII). The operations of institutions such as SEC, BOI, and BII have generated positive impacts, but further capacity building is necessary for long-term sustainability. IBSL must develop additional actuarial capacity to monitor and supervise the insurance industry properly. ADB needs to continue dialogue with the Government, regulatory bodies, and the private sector to ensure that the structural changes and institutional building efforts adopted under the Program are translated to the operational level in order to implement all the objectives of the reforms. 75. To improve corporate governance in SOEs, additional capacity building is needed within the various government authorities to implement the Code—as well as within the SOEs themselves. Corporate governance for companies listed on the CSE should be further strengthened by the SEC to attract more capital to the Sri Lankan financial market, especially foreign capital. 76. Additional assistance could also be used by the Government to (i) overhaul the pension system, and (ii) labor laws. However, due to the immense political implication of such changes, the Government may not be willing to accept such assistance. 77. Further assistance could also be provided to harmonize the tax rules of financial instruments. 78. Timing of the Program Performance Evaluation Report. The Program Performance Evaluation Report should start as soon as the grant TA 3857-SRI (footnote 4) is closed.

2. General 79. The Program supported the Government’s efforts for private sector development and helped initiate reform. ADB has comparative advantage in program implementation through its accumulated expertise. Increasing pressures from global and regional economic integration and the fiscal deficit mean that it is challenging to identify the best way to help Sri Lanka benefit from these opportunities and improve industry competitiveness. ADB should continue its policy and institutional support to sustain the benefits from reforms in the private sector undertaken by the Government, either unilaterally or as agreed in the multilateral framework.

Appendix 1 16

PROGRAM FRAMEWORK

Design Summary

Performance Indicators/Targets

Monitoring Mechanisms Assumptions and Risks

1. Goal • To increase private

sector activity and promote competition to intensify resource mobilization, improve economic efficiency, and raise productivity in order to achieve higher and sustainable economic growth and reduce poverty

• Increased private sector

investment and output • Reduced public enterprise output

share of gross domestic product

• Economic reports, official

statistics • Government budget • Asian Development Bank

(ADB) review missions

• Security situation may

deteriorate • Affected interest groups

may slow down or even derail the reform program

• Government’s

commitment to undertake reforms may waver

2. Purpose (i) Reduce public

sector engagement in financial activities that are commercial in nature

(ii) Strengthen

enabling environment for private sector participation, particularly in infrastructure development

(iii) Foster competition,

promote transparency, and strengthen consumer protection

(iv) Facilitate labor

market mobility and ensure provision for social safety nets

(v) Improve private

sector’s access to financing

• Reduced government budget

deficit resulting from a positive net contribution from the state-owned enterprises (SOEs) sector

• Increased returns of SOEs and reduced budgetary support for SOEs

• Increased private sector investments, particularly in infrastructure projects

• Strengthened competition and consumer protection legal framework and enforcement

• Increased employment

• Increased share of output of the formal sector

• Increased private sector share of financing from banking system and capital markets

• Increased availability of long-term finance to the private sector

• Government borrowings shift to market-based terms

• Government budget

• Annual reports of SOEs, reports from Ministry of Finance and Planning (MOFP) on the revenue from privatization

• Economic reports, official statistics

• ADB review missions

• Labor and employers may

fail to reach agreement on labor reforms

• Political opposition may delay public sector disengagement from commercial activities

• Stakeholders may delay the liberalization of the infrastructure sectors

• Lack of capacity of Consumer Affairs Authority (CAA) to enforce competition and consumer protection

• Government may not be able to contain budget deficits

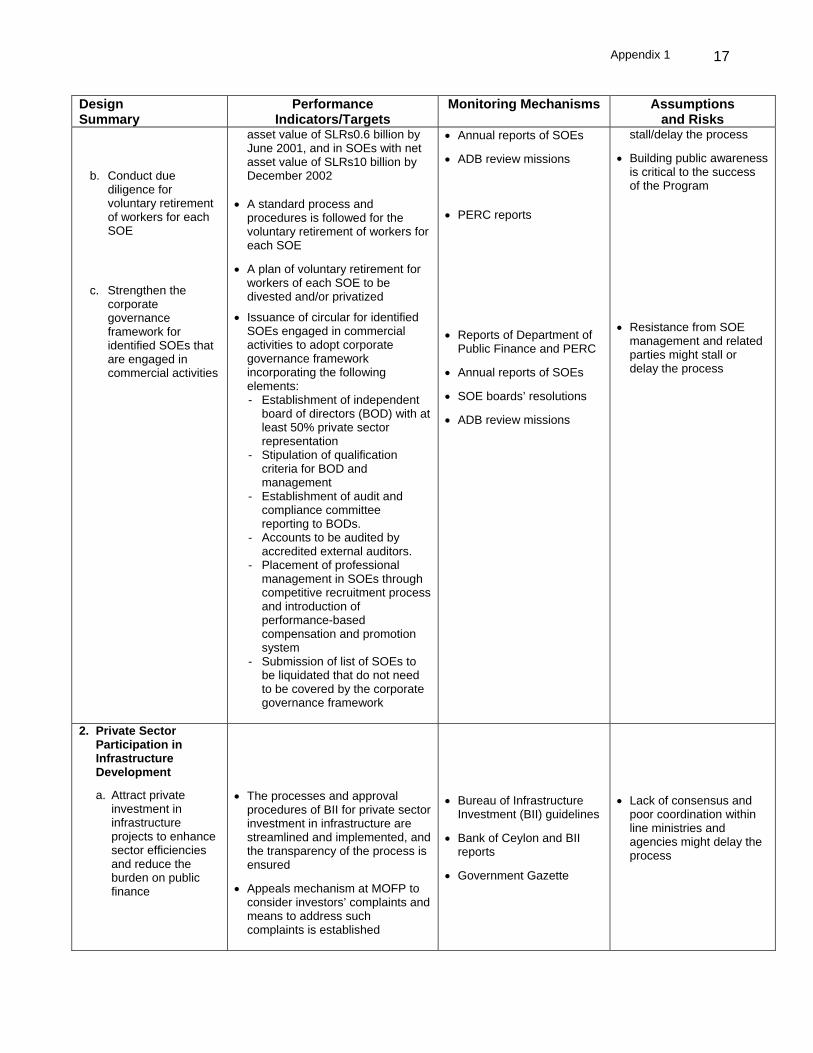

3. Outputs A. Subprogram I 1. Public Enterprise

Reforms

a. Raise economic efficiency by transferring the management of productive assets to the private sector

• Government reduces shareholdings in: - Bogala Graphite Lanka to 0% - Malwatte Plantations to 20%

• Government reduces shareholdings in SOEs with net

• Reports of Department of Finance and Planning and Public Enterprise Reform Commission (PERC)

• Budget speech

• Building public awareness is critical to the success of the Program

• Opposition from SOE employees, management, and related parties might

Appendix 1 17

Design Summary

Performance Indicators/Targets

Monitoring Mechanisms Assumptions and Risks

b. Conduct due

diligence for voluntary retirement of workers for each SOE

c. Strengthen the

corporate governance framework for identified SOEs that are engaged in commercial activities

asset value of SLRs0.6 billion by June 2001, and in SOEs with net asset value of SLRs10 billion by December 2002

• A standard process and

procedures is followed for the voluntary retirement of workers for each SOE

• A plan of voluntary retirement for workers of each SOE to be divested and/or privatized

• Issuance of circular for identified SOEs engaged in commercial activities to adopt corporate governance framework incorporating the following elements: - Establishment of independent

board of directors (BOD) with at least 50% private sector representation

- Stipulation of qualification criteria for BOD and management

- Establishment of audit and compliance committee reporting to BODs.

- Accounts to be audited by accredited external auditors.

- Placement of professional management in SOEs through competitive recruitment process and introduction of performance-based compensation and promotion system

- Submission of list of SOEs to be liquidated that do not need to be covered by the corporate governance framework

• Annual reports of SOEs

• ADB review missions

• PERC reports

• Reports of Department of Public Finance and PERC

• Annual reports of SOEs

• SOE boards’ resolutions

• ADB review missions

stall/delay the process

• Building public awareness is critical to the success of the Program

• Resistance from SOE

management and related parties might stall or delay the process

2. Private Sector Participation in Infrastructure Development a. Attract private

investment in infrastructure projects to enhance sector efficiencies and reduce the burden on public finance

• The processes and approval procedures of BII for private sector investment in infrastructure are streamlined and implemented, and the transparency of the process is ensured

• Appeals mechanism at MOFP to consider investors’ complaints and means to address such complaints is established

• Bureau of Infrastructure

Investment (BII) guidelines

• Bank of Ceylon and BII reports

• Government Gazette

• Lack of consensus and

poor coordination within line ministries and agencies might delay the process

Appendix 1 18

Design Summary

Performance Indicators/Targets

Monitoring Mechanisms Assumptions and Risks

3. Competition Policy and Consumer Protection

a. Strengthen legal framework and institutional support for competition policy and consumer protection

b. Promote

transparency

• (CAA) bill incorporating the recommendations of the working committee is passed

• CAA becomes operational

• Consumer protection council is established

• Implementing regulations for CPA are issued by Ministry of Internal and International Commerce and Food

• Consultation process with private sector is strengthened

• CPA Act

• Government Gazette

• Feedback from private sector organizations

• Lack of consensus among government departments and the private sector might delay the enactment of the bill

• Government will allocate funds for capacity building of the regulatory body

• Building public awareness is critical to the process

4. Labor Market Reforms

a. Facilitate labor market mobility

b. Provide social

safety net

• Criteria and standardized bases of compensation for involuntary employee separation—that are acceptable to employees, employers, and Ministry of Labor—are formulated and legislation is introduced in parliament

• A social safety net dedicated to the counseling, placement, and retraining of displaced workers is established

• Working committee recommendations

• Government pronouncements and/or directives

• Labor legislation

• Government Gazette

• Report of Ministry of Labor

• Consensus building is critical to the success of the Program

• Opposition from labor unions might delay the process

5. Financial Markets Reforms (i) Improve private

sector access to financing

(ii) Restructure state banks, institutionalize corporate governance, and commercialize operations to increase autonomy of state banks, promote competition for funds, and improve the soundness of the operation of these state banks

• Independent BODs for state

banks—Bank of Ceylon (BOC), People’s Bank (PB), and National Savings Bank (NSB)—are constituted with majority private sector representation

• Audit and compliance committees reporting to the BODs are established

• Professional management, distinct from the BODs, is recruited through open competitive recruitment

• A clear delineation of roles between BODs and management of these state banks is established

• Annual reports of state

banks

• Annual reports of Central Bank of Sri Lanka

• ADB review missions

• Government budget

• Deposit insurance regulations

• Government’s resolve to

reform may weaken if fiscal deficits continue to widen

• Opposition from labor unions and management, and the political sensitivity of the reforms might lead to a delay in the process

Appendix 1 19

Design Summary

Performance Indicators/Targets

Monitoring Mechanisms Assumptions and Risks

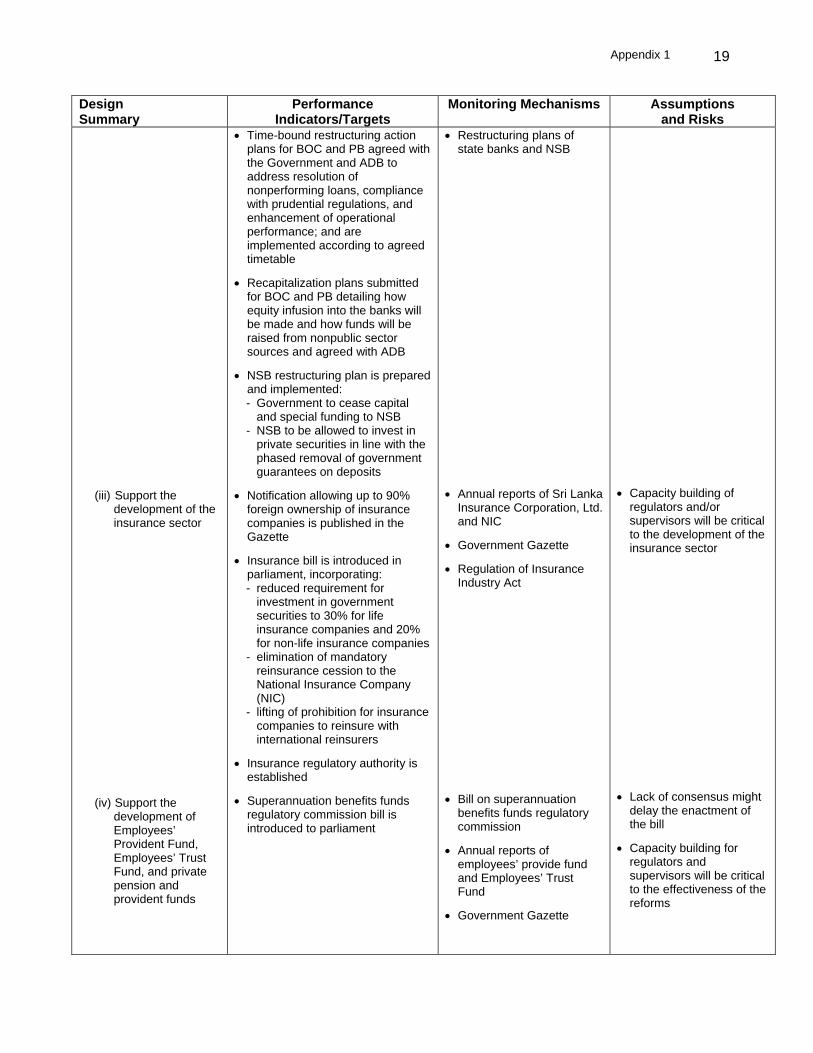

(iii) Support the development of the insurance sector

(iv) Support the

development of Employees’ Provident Fund, Employees’ Trust Fund, and private pension and provident funds

• Time-bound restructuring action plans for BOC and PB agreed with the Government and ADB to address resolution of nonperforming loans, compliance with prudential regulations, and enhancement of operational performance; and are implemented according to agreed timetable

• Recapitalization plans submitted for BOC and PB detailing how equity infusion into the banks will be made and how funds will be raised from nonpublic sector sources and agreed with ADB

• NSB restructuring plan is prepared and implemented: - Government to cease capital

and special funding to NSB - NSB to be allowed to invest in

private securities in line with the phased removal of government guarantees on deposits

• Notification allowing up to 90% foreign ownership of insurance companies is published in the Gazette

• Insurance bill is introduced in parliament, incorporating: - reduced requirement for

investment in government securities to 30% for life insurance companies and 20% for non-life insurance companies

- elimination of mandatory reinsurance cession to the National Insurance Company (NIC)

- lifting of prohibition for insurance companies to reinsure with international reinsurers

• Insurance regulatory authority is established

• Superannuation benefits funds regulatory commission bill is introduced to parliament

• Restructuring plans of state banks and NSB

• Annual reports of Sri Lanka

Insurance Corporation, Ltd. and NIC

• Government Gazette

• Regulation of Insurance Industry Act

• Bill on superannuation benefits funds regulatory commission

• Annual reports of employees’ provide fund and Employees’ Trust Fund

• Government Gazette

• Capacity building of

regulators and/or supervisors will be critical to the development of the insurance sector

• Lack of consensus might

delay the enactment of the bill

• Capacity building for regulators and supervisors will be critical to the effectiveness of the reforms

Appendix 1 20

Design Summary

Performance Indicators/Targets

Monitoring Mechanisms Assumptions and Risks

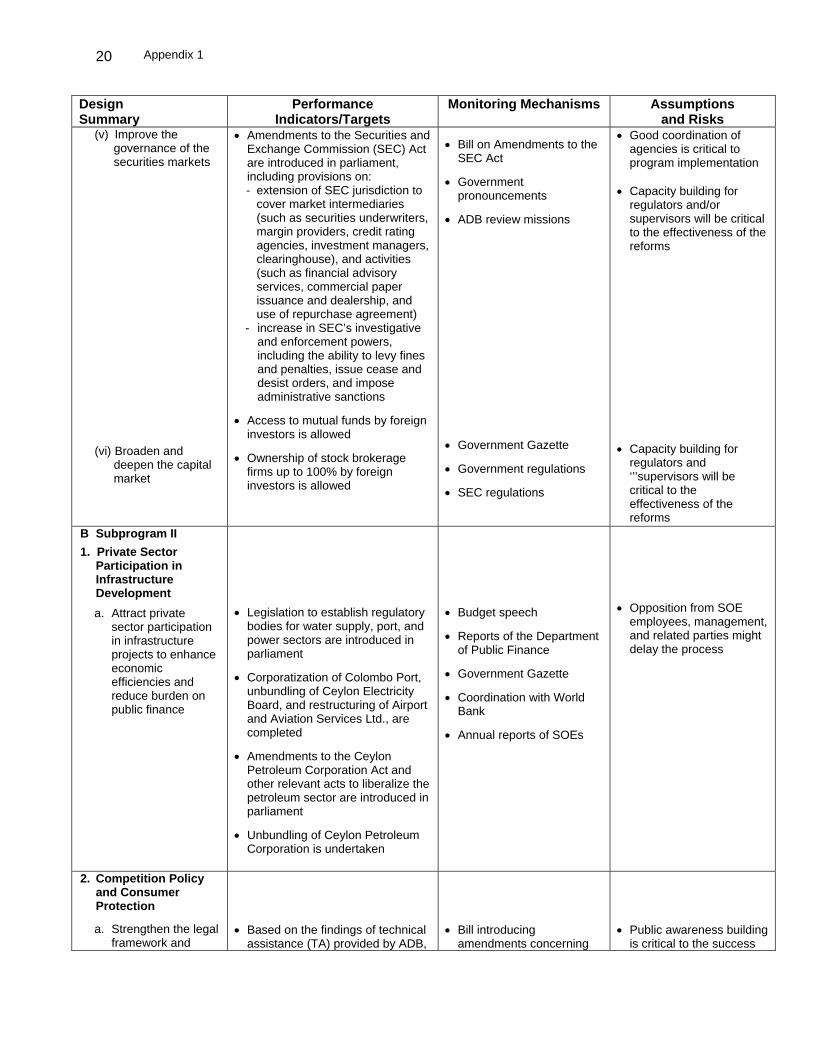

(v) Improve the governance of the securities markets

(vi) Broaden and

deepen the capital market

• Amendments to the Securities and Exchange Commission (SEC) Act are introduced in parliament, including provisions on: - extension of SEC jurisdiction to

cover market intermediaries (such as securities underwriters, margin providers, credit rating agencies, investment managers, clearinghouse), and activities (such as financial advisory services, commercial paper issuance and dealership, and use of repurchase agreement)

- increase in SEC’s investigative and enforcement powers, including the ability to levy fines and penalties, issue cease and desist orders, and impose administrative sanctions

• Access to mutual funds by foreign investors is allowed

• Ownership of stock brokerage firms up to 100% by foreign investors is allowed

• Bill on Amendments to the SEC Act

• Government pronouncements

• ADB review missions

• Government Gazette

• Government regulations

• SEC regulations

• Good coordination of agencies is critical to program implementation

• Capacity building for

regulators and/or supervisors will be critical to the effectiveness of the reforms

• Capacity building for regulators and ‘’’supervisors will be critical to the effectiveness of the reforms

B Subprogram II

1. Private Sector Participation in Infrastructure Development

a. Attract private sector participation in infrastructure projects to enhance economic efficiencies and reduce burden on public finance

• Legislation to establish regulatory bodies for water supply, port, and power sectors are introduced in parliament

• Corporatization of Colombo Port, unbundling of Ceylon Electricity Board, and restructuring of Airport and Aviation Services Ltd., are completed

• Amendments to the Ceylon Petroleum Corporation Act and other relevant acts to liberalize the petroleum sector are introduced in parliament

• Unbundling of Ceylon Petroleum Corporation is undertaken

• Budget speech

• Reports of the Department of Public Finance

• Government Gazette

• Coordination with World Bank

• Annual reports of SOEs

• Opposition from SOE employees, management, and related parties might delay the process

2. Competition Policy and Consumer Protection

a. Strengthen the legal

framework and

• Based on the findings of technical assistance (TA) provided by ADB,

• Bill introducing amendments concerning

• Public awareness building is critical to the success

Appendix 1 21

Design Summary

Performance Indicators/Targets

Monitoring Mechanisms Assumptions and Risks

institutional support for competition policy and consumer protection

b. Enhance domestic

competition

strengthen competition policy and consumer protection, incorporating Sri Lankan experience and best practices

• Action plan for the rationalization

of tax incentives is completed and implemented

competition policy and consumer protection

• Amendment of tax framework and legislation

• ADB review missions

of the process

• Tax incentives offered by neighboring countries might prevent the Government from pursuing the tax rationalization program

• Opposition from management of affected enterprises and related parties might stall or delay the process

3. Labor Market Reforms

a. Strengthen social safety nets

• Study to rationalize existing welfare benefits, that define approaches for incorporating benefits into a formal social security system, is conducted

• Social safety system study

• Further TA might be necessary to support the design and establishment of the social safety system

4. Financial Market Reforms

a. Restructure state banks, institutionalize corporate governance, and commercialize operations to increase the autonomy of state banks, promote competition for funds, and improve the soundness of state banks’ operation

b. Support the development of Employees’ Provident Fund, Employees’ Trust

• After restructuring of the state banks, the Government is to cease funding for them; this will be incorporated in the agreement between the Government and the state banks under the corporate governance framework and based on the recapitalization plan agreed with ADB

• State banks to mobilize capital requirements from non-public sector sources (such as employee stock options or a public offering that may be listed on the stock exchange). The Government may also consider divesting its shareholdings.

• A deposit insurance scheme to protect small depositors to cover all banks is set up

• All forms of government guarantees on deposits are removed

• Reform program for private pension and provident funds is implemented by - adopting an investment policy

defining the phased liberalization of investments of the private

• Reports and/or announcements of the Central Bank of Sri Lanka (CBSL)

• Government budget

• Annual reports of state banks

• ADB review missions • Reports and/or

announcements of MOFP

• Consensus within the

Government on its future role in the financial system

• Resolving the labor issue in state banks

• State banks are satisfactorily restructured

• Consensus is reached

among various stakeholders on the required reforms and future strategic role of private pension and

Appendix 1

22

Design Summary

Performance Indicators/Targets

Monitoring Mechanisms Assumptions and Risks

Fund, and private pension and provident funds