600 Powerpoint business diagrams Powerpoint templates Powerpoint maps Powerpoint shapes

description

The Changing Role of

Managerial Accounting in a

Dynamic Business Environment

Chapter 1

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Managerial accounting is the process of Identifying Measuring Analyzing Interpreting Communicating information

Define Managerial Accounting

1-2

Managing Resources, Activities, and Managing Resources, Activities, and PeoplePeople

An organization . . .

Acquires Resources

Hires People

Organized setOrganized setof activitiesof activities

Organized setOrganized setof activitiesof activities

DecisionMaking

DecisionMaking

PlanningPlanning

DirectingDirecting

ControllingControlling

1-3

How Managerial Accounting Adds Value to the Organization

Providing information for decision making and planning.

Assisting managers in directing and controlling activities.

Motivating managers and other employees towards organization’s goals.

Measuring performance of subunits, activities, managers, and other employees.

Assessing the organization’s competitive position.

Providing information for decision making and planning.

Assisting managers in directing and controlling activities.

Motivating managers and other employees towards organization’s goals.

Measuring performance of subunits, activities, managers, and other employees.

Assessing the organization’s competitive position.

1-4

Managerial versus Financial Managerial versus Financial AccountingAccounting

Accounting SystemAccounting System(accumulates financial and(accumulates financial and

managerial accounting data in the managerial accounting data in the cost accounting system)cost accounting system)

Accounting SystemAccounting System(accumulates financial and(accumulates financial and

managerial accounting data in the managerial accounting data in the cost accounting system)cost accounting system)

Managerial AccountingManagerial AccountingInformation for decisionInformation for decisionmaking, planning, and making, planning, and

controlling an controlling an organizationorganization’’ss

operations.operations.

Managerial AccountingManagerial AccountingInformation for decisionInformation for decisionmaking, planning, and making, planning, and

controlling an controlling an organizationorganization’’ss

operations.operations.

Financial AccountingFinancial AccountingPublished financialPublished financial

statements and otherstatements and otherfinancial reports.financial reports.

Financial AccountingFinancial AccountingPublished financialPublished financial

statements and otherstatements and otherfinancial reports.financial reports.

InternalInternalUsersUsers

ExternalExternalUsersUsers

1-5

Line and Staff PositionsLine and Staff PositionsA line position is

directly involved in achieving the basic objectives of an organization.

Example: A production supervisor in a manufacturing plant.

A line position is directly involved in achieving the basic objectives of an organization.

Example: A production supervisor in a manufacturing plant.

A staff position supports and assists line positions.Example: A cost

accountant in the manufacturing plant.

A staff position supports and assists line positions.Example: A cost

accountant in the manufacturing plant.

1-6

ControllerController The chief managerial and financial accountant

is responsible for:Supervising accounting personnel. Preparation of information and reports,

managerial and financial.Analysis of accounting information.Planning and decision making.

The chief managerial and financial accountant is responsible for:Supervising accounting personnel. Preparation of information and reports,

managerial and financial.Analysis of accounting information.Planning and decision making.

1-7

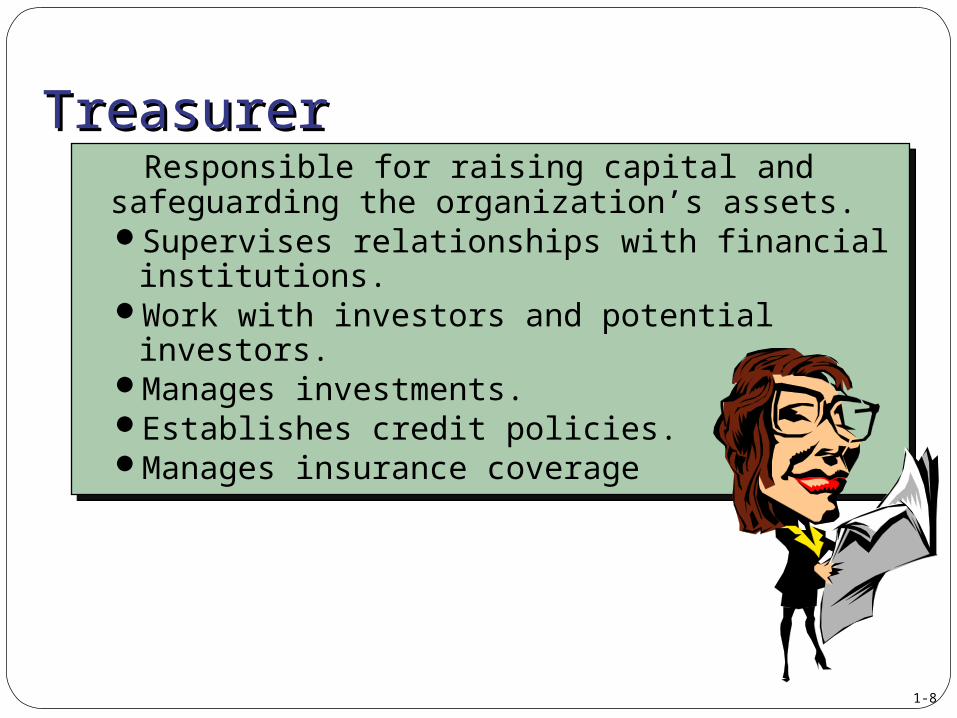

TreasurerTreasurer Responsible for raising capital and safeguarding

the organization’s assets.Supervises relationships with financial

institutions.Work with investors and potential

investors. Manages investments.Establishes credit policies.Manages insurance coverage

Responsible for raising capital and safeguarding the organization’s assets.Supervises relationships with financial

institutions.Work with investors and potential

investors. Manages investments.Establishes credit policies.Manages insurance coverage

1-8

Internal AuditorInternal Auditor Responsible for reviewing accounting procedures,

records, and reports in both the controller’s and the treasurer’s area of responsibility.Expresses an opinion to top

management regarding theeffectiveness of theorganization’s accountingsystem.

Responsible for reviewing accounting procedures, records, and reports in both the controller’s and the treasurer’s area of responsibility.Expresses an opinion to top

management regarding theeffectiveness of theorganization’s accountingsystem.

1-9

ProductProductDesignDesign

ProductProductDesignDesign

ResearchResearchandand

DevelopmentDevelopment

ResearchResearchandand

DevelopmentDevelopment

Strategic Cost Management and the Strategic Cost Management and the Value ChainValue Chain

Securing rawSecuring rawmaterials andmaterials and

other resourcesother resources

Securing rawSecuring rawmaterials andmaterials and

other resourcesother resources

ProductionProductionProductionProduction

MarketingMarketingMarketingMarketing

DistributionDistributionDistributionDistribution

CustomerCustomerServiceService

CustomerCustomerServiceServiceStartStart

1-10

Capacity

Theoretical Capacity is the upper limit on the amount of goods or services if everything works perfectly.

Practical capacity allows for normal occurrences such as cash register downtime and cashier fatigue or illness.

1-11

Cost Management SystemsCost Management Systems

ObjectivesMeasure the cost

of resources consumed.

Identify and eliminate non-value-added costs.

ObjectivesMeasure the cost

of resources consumed.

Identify and eliminate non-value-added costs.

CostManagement

System

1-12

Cost Management SystemsCost Management SystemsObjectives

Determine efficiency and effectiveness of major activities.

Identify and evaluate new activities that can improve performance.

ObjectivesDetermine efficiency

and effectiveness of major activities.

Identify and evaluate new activities that can improve performance.

CostManagement

System

1-13

Managerial Accounting as a Managerial Accounting as a CareerCareer

Professional Organizations

Institute of Management Accountants (IMA)Institute of Management Accountants (IMA)

PublishesManagementAccounting

and researchstudies.

PublishesManagementAccounting

and researchstudies.

AdministersCertified

ManagementAccountant

program

AdministersCertified

ManagementAccountant

program

DevelopsStandards of

EthicalConduct forManagementAccountants

DevelopsStandards of

EthicalConduct forManagementAccountants

1-14

Ethical Climate of BusinessEthical Climate of Business The corporate scandals experienced over the

last few years have shown us that unethical behavior in business is wrong in a moral sense

and can be disastrous in the economy. In addition to Sarbanes-Oxley, there will likely be

more reforms in corporate governance and accounting.

The corporate scandals experienced over the last few years have shown us that unethical

behavior in business is wrong in a moral sense and can be disastrous in the economy. In

addition to Sarbanes-Oxley, there will likely be more reforms in corporate governance and

accounting.

1-15

Professional EthicsProfessional Ethics

CompetenceCompetenceConfidentialityConfidentialityIntegrityIntegrityCredibilityCredibility

1-16