Special report Opportunities and Risks in the Middle East ...

12

StrategicFit - overview to business opportunities in the Middle East Spectrum – maybe have a look at Lebanon PGS – a new opportunity offshore Egypt FGE – Iran has possibilities Event Report, Opportunities and Risk in the Middle East & The Levant , Oct 20, 2015, London Special report Opportunities and Risks in the Middle East & The Levant Oct 20, 2015, London Event sponsored by:

Transcript of Special report Opportunities and Risks in the Middle East ...

StrategicFit - overview to business opportunities in the Middle East

Spectrum – maybe have a look at Lebanon

PGS – a new opportunity offshore Egypt

FGE – Iran has possibilities

Event Report, Opportunities and Risk in the Middle East & The Levant , Oct 20, 2015, London

Special report

Opportunities and Risks in the Middle East & The Levant

Oct 20, 2015, London

Event sponsored by:

+ 44 (0) 20 7637 0324

Opportunities and Risk in the Middle East & The Levant

3

“I've worked now for two direct supervisors, bothCEOs, who said, if you want to be in the oil and gasindustry from 2030 onwards, you need to be in theMiddle East,” said Andrew Lodge, Principal with oil& gas strategy consulting firm StrategicFit, andChairman of the conference, in his opening remarks.

Mr Lodge is a former Exploration Director for Pre-mier Oil and VP Exploration for Hess. The Middle East “has the opportunity, but it has sig-nificant issues.”

The Middle East is the source of 30 per cent of theworld’s oil production, dominated by Saudi Arabia,and the reserves for future oil production are also inthe Middle East, Mr Lodge said.

There may be great potential for unconventional oiland gas operations in the Middle East, given the“wonderful world class source rocks,” he said. Al-though there haven’t been much efforts to try andfind it so far, with so much conventional oil avail-able.

“We could still be, in the oil industry, at the end ofthis century still focussed on Middle East. It is the-oretically a land of opportunity,” he said.

But of course there are plenty of difficulties with oiland gas operations too, including political instabilityand terrorist attacks.

Mr Lodge quoted Espen Barth Eide, Managing Di-rector of the World Economic Forum and formerNorwegian Minister of foreign affairs, who oncesaid. “Energy politics in the region must changefrom being divisive to an enabler of sustainable andinclusive economic growth.”

“We all know it’s unlikely to change,” Mr Lodgesaid.

Given security and instability issues, and limited de-mand for oil, a realistic prediction is that productionfrom the Middle East in 2025 will be roughly thesame as it is today, he said.

Politically, “maybe we can say that the US is less in-terested in the Middle East now it has its own do-mestic supplies of oil, he said. But China is havinga growing interest in the region. The influence ofChina in the Middle East is already there and willcontinue to grow.”

The Chinese have a growing influence in the regionfrom a demand point of view, basically in partner-ship with the National Oil Companies,” he said.

“CNPC (China National Petroleum Corporation)does invest with other companies. So there will berelationship opportunities to partner with CNPC andjoin them. They have the contacts and diplomaticclout.”

The majority of the Middle East has low findingcost, low development cost and low operating cost,with the only exception being offshore deepwaterEgypt, he said.

One particularly interesting area is the Zagros regionof Iran. “That’s where the oil is,” he said.

Apache has a strong position in Egypt. “It has donea fantastic job there, bought it, developed it, foundmore, protected it, got costs down. Having a physicallocation slightly away from main centres of protest-ing has helped it go forward,” he said.

Oxy (Occidental Petroleum Corporation) has “a longhistory of relationship building, investment, invest-ing for growth,” he said. It is one of the few US

Middle East is where the oil isThe Middle East is where the oil is – but producing it is far from easy, as weheard in our Finding Petroleum forum in London on October 20th,“Opportunities and risks in the Middle East & the Levant” – with a specialfocus on Iran, Lebanon, Egypt and the Zagros

Event Report, Opportunities and Risk in the Middle East & The Levant, Oct 20, 2015, London

The conference was sponsored and supported by NeftexExploration Insights (part of Halliburton), Cambridge Car-bonates, Spectrum, PGS, Geospatial Research and Petro-leum Geological Analysis Ltd.

The full agenda and links to download videos and presen-tations (where speakers have agreed to make them avail-able) is www.findingpetroleum.com/event/e03a4.aspx

Also speaking at the conference but not included in thisreport:

Stephen Trueblood, Commercial Manager for Sasol Petro-leum International, gave a presentation on the future ofEgypt’s oil and gas industry. The talk is not included in thisreport, the slides and video were not released.

Richard Jones, CEO of Geospatial Research, gave a presen-tation on the geological structural style of the Zagrosmountain belt through Iran and the Kurdistan Region ofIraq, characterised by world class structural traps andstacked fractured reservoirs. The talk is not included inthis report, but the slides are available on the Finding Pe-troleum website.

Andy Horbury, Director of Cambridge Carbonates, gave apresentation on the geology of the Zagros margin of theArabian plate. The talk is not included in this report, butthe video and slides are on the Finding Petroleum web-site.

John Hurst, recently retired Head of Exploration withGenel Energy, gave a talk on the highs and lows of explo-ration in the Kurdish Region of Iraq. The talk is not in-cluded in this report and the video and slides were notreleased.

Mike Simmons, Technology Fellow with Neftex Explo-ration Insights at Halliburton, gave a geological talk onexploration potential in Iran, including Classic Zagros FoldBelt plays, Extension of the fractured carbonate playsfrom Kurdistan, Resource plays from rock units such as theKazhdumi and Pabdeh shales and the potential of theSouth Caspian. The talk is not included in this report andthe video and slides were not released

This is an Event Report fromour Finding Petroleum

forum in London on Oct 20,2015, " Opportunities and

risks in the Middle East & the Levant”

Event website

www.findingpetroleum.com/event/e03a4.aspx

Some presentations and videos fromthe conference can be downloaded

from the event website.

Conference produced by David Bamford

Report written by Karl Jeffery, editor of Finding Petroleum

[email protected] Tel 44 208 150 5292

Sales manager Richard McIntyre

[email protected] Tel 44 208 150 5291

Conference produced by Karl Jeffery

Layout by Laura Jones, Very Vermilion Ltd

Cover art by Alexandra Mckenzie

Finding Petroleum

www.findingpetroleum.com

Future Energy Publishing, 39-41 North Road,

London, N7 9DP, UK www.fuenp.com

Opportunities and Risk in the Middle East & The Levant

4 Event Report, Opportunities and Risk in the Middle East & The Levant, Oct 20, 2015, London

companies that has continued to invest in theMiddle East.”

Genel Energy has been successful in the Kurdis-tan Region. “A lot of us saw that map with won-derful undrilled folds. But it is one thing to thinkabout them, another thing to get in there and dosomething about it.”

Some oil companies start by trying to work outwhere they can make money – but Genel startedby looking for where the resource (oil) was, onthe basis that if it could find oil, it would be ableto make money, Mr Lodge said.

Egypt

There has been a major discovery by ENI (theZohr field) in offshore Egyptian waters. “It gob-smacked me,” Mr Lodge said.

The field was found in “a published seismicline,” and many people saw the same data. Thisleads to possibilities for other future develop-ments in Egypt and Lebanon.

“Egypt has been a wonderful country, becauseit is most like Western oil industry of any coun-try in the Middle East,” he said.“There is a farm in market, people buy compa-nies, sell companies. But a lot of uncertainty ex-ists.”

If it was his personal choice of where to invest,Mr Lodge said he would not currently invest inEgypt in the current price environment. “It is dif-ficult to do what Apache have done,” he said.

Saudi Arabia

“Saudi Arabia is pivotal to the area, it has themost production and the most reserves and itcontrols OPEC,” he said. “It is essentially at themoment dominating the market, forcing themarket price of oil, to some extent attempting to destroy unconventional resourceof the US.”

“Are they determined to basically bust US un-conventional production - or get it to a certainlevel where they are comfortable US oil stays inthe US [ie the US does not export any oil] andSaudi dominates emerging markets?” he asked.“Saudi Arabia could theoretically changecourse.”

Iraq / Kurdistan

In recent years the most exciting exploration op-portunities have been in the frontal fold belt ofKurdistan. “It’s a great place to find oil.”

“The oil which comes out is not sold at marketprice, it is sold at a discount or sometimes noteven paid for,” he said.

The Kurdistan Regional Government (KRG)has challenges are getting oil to market, withregular damage to their pipelines. “The compa-nies who invest there don't get paid very often,”

he said. “KRG needs that money to fund its ownfight against ISIS.”

“But I'm pleased to see DNO and GENEL havein fact received payments over the last couple ofmonths. KRG did a deal with Baghdad, where it wouldsupply oil to Baghdad in return for cash. But,“Iraq can't give you cash and they claim thatKRG can't give them the oil,” he said.

Current production overall in Iraq is “wellbelow” what it has been in the past, and there’sno quick fix to this in sight.

Iran

Iran is likely to open up, with upcoming liftingof sanctions “theoretically related to the nucleardeal, one suspects also [linked to] to IS threat,”he said.

The Europeans see it as a great opportunity,while Americans are “a little bit more reserved,”he said

“If you listen to the rhetoric of some of the USRepublican candidates, they are for tearing upthe nuclear deal and going back to the way itwas. The Europeans say, yes let's go for it.”

“So there’s an opportunity for oil companiesbased in Europe to take a lead in this, and for theUK.”

Many oil companies including Premier, Hessand BHP were close to signing contracts in Iranbefore the last wave of sanctions. This meansthat many people are ahead of the game in termsof understanding the subsurface, he said. “I seethis primarily as a development opportunity (notan exploration opportunity).”Although the value of the opportunity will de-pend on what sort of contracts the Iran govern-ment is willing to sign, he said.

Lebanon

Looking at the Eastern Mediterranean / Levantregion, many people have evaluated Lebanon,and then been dismayed “that the offshore hasnever opened up,” he said.

“It has been there for 10 years as a potential op-portunity for investment.”The country claims, even on advertising bill-boards, that the country has oil. “But it doesn't,”he said. “It thinks it has.”

However, “some figures suggest it has a signif-icant amount of oil and indeed gas,” he acknowl-edged.

“My own view, having seen the data, is that I’mnot too sure whether offshore Lebanon is amajor opportunity.”

ENI drilled 2 wells in offshore Cyprus, on thesame plays which are present in Lebanon, whichturned out to be dry.

“And if there is an opportunity will there ever bea license round? And if there was a licenseround, and we find oil and generate cash, whatwould happen to it? How would the country be-have?”

“It is probably best for the country to be a littlebit slower, let the whole thing play out and thenopen up to the industry with clear contractual ob-ligations,” he said.

Economics

It is also important to note that oil fuels the econ-omy of Middle Eastern countries, and they needa certain oil price to keep their budgets going.

Even at a $100 oil price, many of the

countries did not meet their own budget require-ments from the cash generatedfrom oil sales,” he said.

“The situation today at $50 is even bleaker. OnlyKuwait generates more funds from oil than itneeds for its own budget.”

Iraq has managed to reduce its requirements fora break-even oil price (ie reduced governmentspending).

If the oil price stays low, that could lead to moretension in the region, especially with Iran in-creasing production. “Will this lead to further in-stability in the region? Probably.”

OPEC has issues enforcing any quotas it makes.“They will do a certain quota but actually domore than that. It undermines the premise of cutsand control.”

Security and contracts

If you are investing in the Middle East, as wellas the subsurface issues, you have to look at thesecurity situation and sanctions, delayed pay-ments and contract uncertainty,” he said.

“All this means - when a company makes anevaluation of Middle East - it has to think muchmore critically about the risks it is prepared totake,” he said.

“Delayed payments are always an issue inEgypt. Generally the money comes but de-layed,” he said.

“For an oil company, the key sanctity is, 'do Ihave a contract to work with',” he said. “Have Isigned something so, if I find the oil I will gainsomething from it - either oil or cash.

Having said all that, companies are successful,he said.

See a link to Andrew’s talk on video and slidesatwww.findingpetroleum.com/event/e03a4.aspx

5

Opportunities and Risk in the Middle East & The Levant

Event Report, Opportunities and Risk in the Middle East & The Levant, Oct 20, 2015, London

Neil Hodgson – maybe have a look at LebanonOffshore Lebanese waters could hold more oil than is commonly thought, said Neil Hodgson - Executive VicePresident Mediterranean and Middle East Region, with seismic company Spectrum

“I strongly believe that the Levant has onlystarted to give its reward, and it will keep giv-ing,” said Neil Hodgson, Executive VP Mul-ticlient with Spectrum and formerlyExploration Director for Matra Petroleum,and with BP, BG and Premier Oil.

By the “Levant,” Mr Hodgson is referring tothe eastern Mediterranean, with areas aroundLebanon, Israel, Egypt and Cyprus.

The North Levant waters, offshore SouthLebanon, is ‘probably an oil play’ as well as abiogenic gas play, and it has bigger and lesscomplex structures than offshore Israel, hesaid. The reservoir rock is 3-4 times thickerthan offshore Israel.

The prospects for gas changed with Eni’sZohr 30 TCF gas discovery earlier in 2015,and there may be other gas fields like it, hesaid. Zohr “not only changes the geopoliticsof the area, but it also changes the geologicalstory quite dramatically. There’s got to be 50TCFs in the Zohr analogues,” he said. “Iheartily encourage you to explore it if youcan.”

Gas

Most people think that there is only gas in theregion, and it is deep and expensive, he said.

Combined with security issues, and commer-cial issues (particularly getting gas from Is-raeli oilfields out to wider markets), and poorresults from two ENI wells drilled offshoreCyprus in 2015, “It leads to a picture that theEastern Med is not a very interesting place atall,” he said.

Offshore Israel is widely considered to be agas basin. “It is, sort of, so far. But is it alwaysgoing to be a gas basin?”

Israel’s 11 TCF Tamar gas field, drilled byNoble Energy in 2009, was “quite a landmarktype of well”, under 1500m of water, whichcounted as deep in 2009, he said.

It was brought online in just 3 years, by tyingit back to a facility in shallower water, usinga 75km tieback. “You don't need a 15 year de-velopment cycle,” he said.

Tamar was followed by a series of roughlysimilar gas discoveries in the region of 14 –15 TCF. So the industry has decided it is a gasbasin, and it is probably dry biogenic gas(caused directly from organisms).

People also believe that the plate (tectonic)structures in the region are quite complicated,and this means you need many wells to gethigh production levels, because the produc-tion for each individual well is lower. If thesands were simpler, you could get the sameproduction from two or three wells as you canget from 30 wells in a complex structure, hesaid, quite a factor when wells can cost $150mto drill.

“All these things point to Eastern Med beingan awkward place to be. But I don't think anyof that is true.”

Alternative story

Mr Hodgson presented a seismic line runningsouthwards, going through the Tamar fieldoffshore Israel, into the Northern Levant basinin offshore Israel.

The Tamar field shows up on the seismic as a‘flat spot’, a horizontal line, indicating a fluidboundary. “This was the thing that made

Tamar so attractive, it reduced the risk ofdrilling,” he said. But “it was still risky be-cause no-one knew what the sand was goingto be.”

There is another area of the seismic line whichshows a light acoustic impedance contrast (ieblurry picture). “That tells you it’s full of clas-tics,” he said.

Clastics are fragments of pre-existing miner-als and rock, which have been deposited on aseabed (sedimentary rock).

This leads to the story of the drainage patternof the Nile Delta during the Cretaceous era,with a large area of hinterland drainingthrough the Nile Delta.

At the end of the Cretaceous (moving into theMiocene era), the Mediterranean was open tothe East, leading into the Tethys Sea. Therewas a rift system moving Northwards, whichbrought Arabian sands into the basin, draggedfrom East to West by water currents.

The seaway to the Tethys Sea closed later, atthe end of the Miocene era (Messinian period)due to Northward movement of the Arabianplate. At this point in geological time, the re-gion was dried out and covered by Messiniansalt. “The Nile Delta starts to develop like anormal delta,” he said.

So if we look at the basin offshore Lebanonand offshore Israel, most of the deposition hascome from the Nile Delta, and we have wehave small sands which may have come fromthe Arabian plate margin.

The water would have been very deep duringthe Cretaceous, and the deposits formed tur-bidite (defined as the geologic deposit of a tur-bidity current, a type of sediment gravity flowresponsible for distributing vast amounts ofclastic sediment into the deep ocean). Thiswould fill up the Northern Levant basin.

The Southern Levant would have been a plat-form. This is where Tamar was found. But most of the sand from the Nile wouldhave bypassed the Southern Levant and beendeposited in the deeper waters of the NorthLevant basin.

6 Event Report, Opportunities and Risk in the Middle East & The Levant, Oct 20, 2015, London

Opportunities and Risk in the Middle East & The Levant

Another thing known by geologists is that inthe early Miocene era there were big carbon-ate reefs developing. Zohr was found in oneof these carbonate reefs.

The flow of clastics kills reefs, so that indi-cates that the sand from the Nile basin musthave been deposited a long way from whereZohr was found.

The sands probably just dropped into theNorthern Levant basin, directly in front of theNile Delta, they didn’t go westwards, towardswhere Zohr was found, and towards Cyprus,he said.

Looking at a seismic line running East toWest, you can see a shelf in the rock, whichwould have been the seabed in the Cretaceous.

The turbidite deposits would have dropped off

the edge of the shelf and been deposited indeepwater.

“There's no reason a turbidite would sit on theedge of the shelf,” he said. “It’s like when youdrop soap in the bath, it ends up on the bottomof the bath, not where the taps are.”

The two wells drilled by ENI in Cypriot wa-ters, which were dry, were on the Western sideof the Northern Levant basin – so probablyaway from where the sands were deposited,he said.

Looking at ENI’s “Onasagoras-1” well, “itseemed to be drilled in a valid structure,” hesaid. But it was drilled into early Miocenesand (Arabian sand which was carried overfrom the East), not sands from the Nile (de-posited in the cretaceous). The well was also drilled into a point wherethe Miocene sands are just about pinched out

(narrowing to nothing). “It is not surprisingthat the well was unsuccessful.

So this dry well does not reveal anythingabout the prospectivity of the Nile sands, hesaid.

And in the centre of the basin, there are a kilo-metre thick (Arabian) Miocene sands. “Thatis the main play offshore Lebanon in my opin-ion,” he said. “We are not looking for strati-graphic play, looking for nice simple sand.

“It is the same geometry as Tamar, rather sim-ple structure.”

So “there may be an argument for a decentreservoir in Northern Levant based on offsetbasin and where the sands may have comefrom,” he said.

7Event Report, Opportunities and Risk in the Middle East & The Levant, Oct 20, 2015, London

Oil not gas?

All the Miocene sands drilled so far have ledto dry gas, thought to be biogenic gas, formeddirectly from organisms, rather than thermo-genic gas, formed from cooking organic mat-ter under high pressure.

Of course, oil can only be produced by ther-mogenic means, so if the gas is biogenic thatmakes it less likely that there will be oil.

“The normal way of finding oil is to under-stand geology and do some basin modelling,trying to work out where the source rocks willbe,” he said.

Looking again at the North South seismic linewhich goes through the Tamar field, there is asection beneath Tamar from the Oligocene(which fills part of the space between the Cre-taceous and Miocene).

“Not much is known about Oligocene becauseit doesn't outcrop in Lebanon,” he said.

Here, “the Oligocene is one or two per centorganic carbon. It is an established sourcerock,” he said. “It is known to be a contributorto deeper structures in the Nile Delta”.

In the Southern Levant, where the Tamar fieldis, “the Oligocene rock is not mature for [ther-mal] generation of oil or gas.” But the biolog-ical activity generates biogenic gas. “That’swhy Tamar is stuffed full of gas.”

But moving to the North Levant, theOligocene rock is deposited at much greaterdepth, so it is at higher temperatures, makingit possible to generate oil.

“The Oligocene source rock sitting under-neath a kilometre of sand is generating oil andthat oil will be migrating into those struc-tures,” he said.

“Maybe the reason we don't see obvious flatspots offshore Lebanon is just because it’s notgas, its oil.”

“Then the question becomes, just how big thisoil play could be.”

There have also been a series of natural oilseeps in the waters above Lebanon, whichshow up on SAR Satellite data, running par-allel to the coast.

Because the seeps appear close to the coast,people think that the oil reservoirs are near thecoast, he said.

But it could be that the Oligocene source rockgenerates oil which starts to migrate beneaththe Messinian salt layer above. “The oil willmigrate along the base of the salt and pop outclose to the coast,” he said

Another interesting discovery is the Karishfield offshore Israel. “It first looked like a bor-ing gas story,” he said. “Then it was reportedthat Karish was slightly different, it was gascondensate.”

Perhaps rather than being gas condensate,Karish is full of oil, which comes from theNorthern Levant basin and migrates up dip tothe Karish structure,” he said. “Karish, I think,has got up dip closure.”

Spectrum has drawn a map of where it thinksthe early Miocene sand is, which could befeeding oil into Karish.

“It may not be exactly right,” he said. “In thisarea, our colleagues PGS have 3D data andprobably nailed that pinch-out better than Ican on 2D.”“So there’s a bit of a story about a potentialoil play.”

North Levant structure

When you try to work out the subsurfacestructures of the North Levant, “the 2D datawould seem to justify the model that NorthLevant is just shattered by faults and its hope-less finding anything, and it’s deepwater,” hesaid.

But if you look at a map of some of the struc-tures, you can see they are less faulted thanTamar.

The Leviathan gas field off the coast of Israelis highly faulted. It actually manages to holdthe gas because there is so much sand. “It’sunlikely you'll get faults sealing,” he said.

So the Lebanon oilfields “will be very easy todevelop, they won't need too many wells, theywill be developed extremely quickly. If it isoil, “these will be billion dollar fields.”

The faults do not break up the Oligoceneshale. “The reason is that Oligocene is sourcerock and it is viscous,” he said.

There are many similar structures, which en-able repeatability in drilling.

“This is what will happen when NorthernLevant is drilled offshore Lebanon

We'll have one well and we'll have the re-peatability

“This is exactly what has happened to theSouth Offshore Israel where Noble drilledwell after well and found 50 TCF.”

Zohr

Looking again at Zohr, in an early Miocenereef. “We understand that the gas is a very drygas, nobody has said it is biogenic,” he said.“But the odds are, it’s the same biogenic gasyou get in Tamar.”

After the Zohr discovery, Spectrum had a lookthrough the seismic data to see how well itcould see Zohr, and if there was anything sim-ilar.

It is possible to see Zohr once you know it isthere. “This fuzzy sort of imaging is not justpoor seismic imaging, it is the reef part,” hesaid. “In the middle you have some more co-herence.”

Perhaps there is a reason why the seismic im-aging in the middle of the field is clearer thanon the left and right edge.

The Spectrum interpreters looked for otherparts of the subsurface which had a “fuzzy re-flectivity on either side, coherent reflectivityin the middle” and found one.

“It’s a 500km carbonate reef, covered byMessinian salt,” he said. “These are probablythe key play areas that we need to thinkabout.”

There are other examples as well. “Presum-ably they all have prospectivity rather similarto Zohr,” he said.

See a link to Neil’s talk on video and slides atwww.findingpetroleum.com/event/e03a4.aspx

Opportunities and Risk in the Middle East & The Levant

8 Event Report, Opportunities and Risk in the Middle East & The Levant, Oct 20, 2015, London

Opportunities and Risk in the Middle East & The Levant

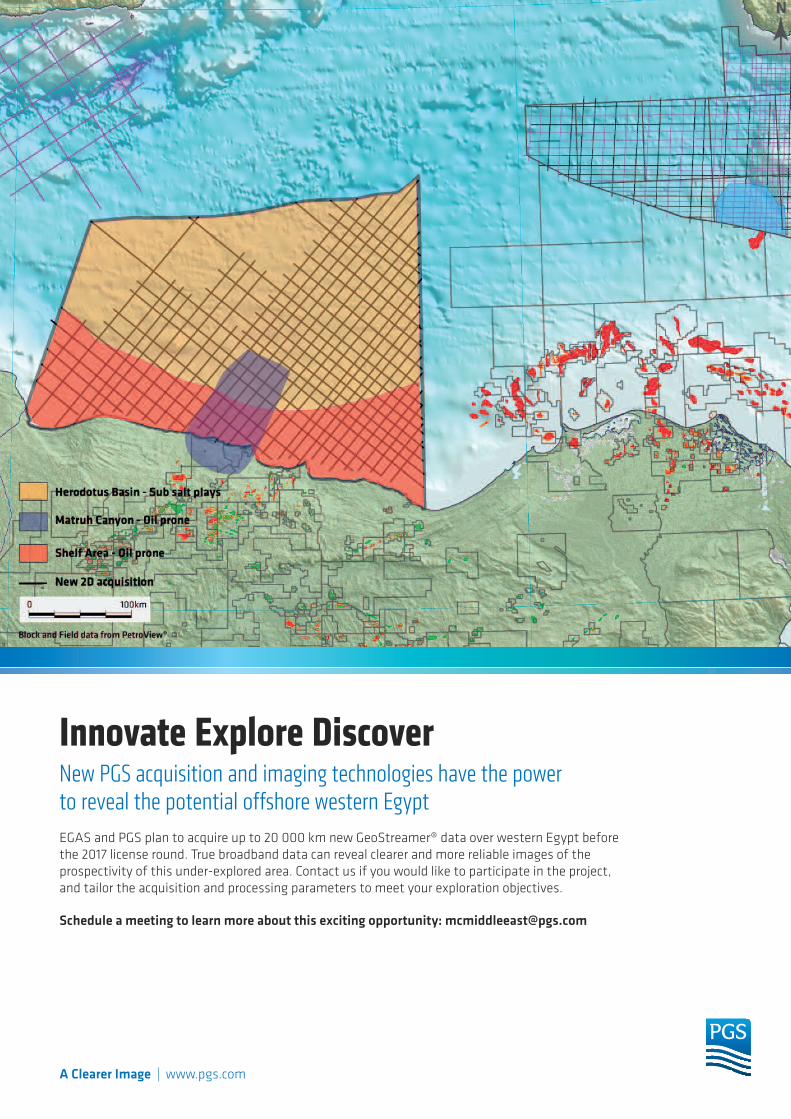

Egypt offshore, west of the Nile Delta, couldbe an exciting new opportunity, said ØysteinLie, Project Manager MultiClient for the Mid-dle East and CIS with seismic company PGS.

He was speaking at Finding Petroleum’sforum on October 20th 2015, “Opportunitiesand risks in the Middle East & the Levant.”

PGS will do a non-exclusive 2D survey of alarge area of the Egypt’s West MediterraneanSea, after winning a contract earlier this yearwith Egyptian Natural Gas Holding CompanyEGAS (the Egyptian state owned companywhich is responsible for issuing of natural gasexploration licenses in Egypt).

The survey will take into consideration all ofthe geological domains known to be present.“Special processing techniques need to beadapted and PSDM imaging will be per-formed,” he said.

PGS is also re-processing all of the legacydata, and will use this together with the newsurvey data.

Some areas, such as the fold belt area, aretricky to illuminate with 2D data, so theymight be followed up by 3D.

The survey will start with infill lines in exist-ing directions (North East to South West), andfollow with the perpendicular (North West toSouth East).

“The density of the grid will be decided basedon industry feedback,” he said.

PGS has also done surveys in neighbouringwaters, including Greek waters (commis-

sioned by the Greek government in 2014) andin Cypriot waters (commissioned by theCypriot government). It has also done Multi-Client 3D surveys, including in Cypriot wa-ters close to the Zohr discovery (Zohr is inEgyptian waters).

EGAS will use the results of the survey to de-fine exploration blocks to be on offer in a bidround planned for 2017.

“It is very important to have your eyes openand to look at new data and new opportuni-ties,” he said. “The 2017 bid round shouldprovide interesting acreage.”

A couple of blocks have been taken up in off-shore West Egypt in the past and been relin-quished, he said.

Zohr

The interest in Egyptian waters begins withENI’s Zohr discovery in ultra-deepwater(1450m depth), discovered in 2015.

Zohr was reported to be biogenic gas, but it islikely to be a thermogenic system in the re-gion as well, he said.

ENI found Zohr using 2D data, he said. MrLie showed the 2D section which ENI used,re-processed and depth imaged.

“If the structure is big enough, you can stilldo exploration based on 2D data,” he said.

Zohr is claimed to be 30 TCF, based on oneexploration well, with a 630m thick hydrocar-bon column.

The structure is a satellite structure of the Er-atosthenes high (an enormous 2000m highmountain on the seabed between Cyprus andEgypt).

It is thought to be biogenic gas from the Ter-tiary source rock, of the same system as gasdiscoveries in Israel.

The question is whether another giant like thiscould be found elsewhere in the EasternMediterranean.

Shelf

Looking at other areas of Egyptian waters, theEgyptian continental shelf area could be inter-esting.

There is already a working petroleum systemonshore Egypt, and we expect this to be con-tinued to the shelf, he said.

There is a canyon in this region, called theMatruh Canyon, which is filled with a thicksedimentary sequence, he said.

Deepwater

Beyond the shelf, it quickly becomes ultra-deepwater where the Herodotus Basin is situ-ated, which is covered with Messinian salt, hesaid.

There is an important exploration well,“Kiwi”, drilled by Statoil about five years ago,in the deepwater basin. They drilled throughthe thick Messinian salt to see what was belowit.

“It was reported as a dry well but they discov-ered high quality sands (below the salt), hesaid. “Of course they could have been unluckywith the location of the well and might havehit hydrocarbons in another location.”

In Cypriot waters, further north, there haveonly been three exploration wells, of whichone was successful, Aphrodite which is a 5Tcfdiscovery

“New geophysical data is needed to do aproper assessment of the whole area, bothseismic and gravity / magnetic data,” he said.

Nile Delta

Further East, the most important feature is theNile Delta. There could be sand lobes comingfrom the Nile Delta, which could extend Westand North.

The main play type for the Nile Delta isPliocene sandstones (Pliocene is part of thetertiary era). There could be reservoirs sealedby Messinian salt above.

Using legacy seismic data, you can see“nicely defined basin floor fans,” he said.“Some are very sparsely sampled by seismicand a better seismic coverage is needed toevaluate the area properly.”

See a link to Øystein’s talk on video anddownload slides atwww.findingpetroleum.com/event/e03a4.aspx

PGS – A new opportunity offshore EgyptOffshore Egyptian waters, west of the Nile Delta, offer a potentially exciting new opportunity for oil and gasexploration, says Øystein Lie of PGS

9Event Report, Opportunities and Risk in the Middle East & The Levant, Oct 20, 2015, London

FGE – Iran has possibilities Siamak Adibi of Middle East consultancy FGE struck a cautious note on Iran – it would like to grow productionbut isn’t necessarily offering good opportunities to outside companies

Opportunities and Risk in the Middle East & The Levant

Iran plans to offer contracts to oil and gas com-panies at a London conference in February2016 – but the terms could be tough, and willbe offered to local companies first, said SiamakAdibi, senior consultant with Middle East fo-cussed consultancy FGE.

He was speaking at the Finding Petroleumforum in London on October 20, 2015, “Oppor-tunities and risks in the Middle East & the Lev-ant.”

Iran is keen to develop more oil, and gain morepower in OPEC. But “Every time they go forexploration they find gas,” he said.

A chart of oil exploration shows that the oil dis-covery rate has dropped to nearly zero for thepast 2 years. Sanctions and the low oil pricehave not helped.

Iran has the largest gas reserves in the world,more than Russia. There are many giganticfields, just one of which would be sufficient forthe Iranian market.

Iran is subject to sanctions from the US and EU,but there have been discussions lately aboutlifting the sanctions based on an agreementover Iran’s nuclear research, he said.

Contracts

Contracts between oil companies and Iran is avery sensitive subject politically - for more in-formation read the Wikipedia page on “Anglo-Persian Oil Company”.

Recently, Iran has only been offering inflexible“service contracts” to oil companies, where theoil company essentially provides a

service to the government, and all costs mustbe agreed in advance.

In the past, these have been a long way short ofa level which will give companies the expected15 to 20 per cent internal rate of return. Somecompanies actually lost money in South Parsprojects phase 6-8, he said.

Production sharing agreements, where oil rev-enues are split between the oil company and theIranian government, are banned under the Iran-ian constitution.

However there could be a contract which is ahybrid of service contract and production shar-ing agreement, Mr Adibi said.

Another option is that the international oil com-pany can form a joint venture with the state-owned National Iranian Oil Company (NIOC). Iran is also considering longer service con-tracts, which could be 35 years rather than 7-8as previously, so a similar time scale to produc-tion sharing agreements. They could also bemore flexible.

The government has also considered systemssuch as paying companies a fixed fee per barrel,Mr Adibi said. “If they want to bring IOCs inthe country they have to bring some kind of at-tractive contracts for them. They understandthis.”]

But there is still political pressure to keep con-tracts tough, he said.

There are 49 contracts which might be readyfor investment post sanction.

Statoil, BP and ENI have already announcedthat they are interested in setting up operationsin Iran again.

Oil

Before the sanctions, Iran’s crude oil produc-tion was 4m bopd, now it is 2.9 m bopd.

The oil fields are well maintained, so once thesanctions are lifted, expected to be around theend of the first quarter of 2016, there could bearound 500,000 barrels of oil per day comingonto the market.

“By end of 2016 they can ramp up productionclose to pre-sanctions level,” he said.

Iran has ambitious plans to get production toover 5m bopd, but this might not be achievable.

“Many of Iran fields are ageing oilfields,” hesaid. “Going beyond 4m bopd is possible, butit means huge investment.”

Gas

The South Pars field is the largest gas field inIran, producing 12 bcf / day. It is also the mostimportant field for gas development projects,he said. There are several development phases

10 Event Report, Opportunities and Risk in the Middle East & The Levant, Oct 20, 2015, London

Opportunities and Risk in the Middle East & The Levant

planned, all numbered. Phase 12 was recentlycompleted, adding another 2 bcf a day.

The plan is to get production to 27 bcf a day by2018. “We believe [this date] is not realistic, butmaybe by 2025, and maybe to 25 bcf a day,” hesaid. “The local contractors are capable of finishingthese projects.”

The gas stream includes condensate, whichcould itself reach 1m bopd. Iran does not planto export the additional condensate, but use itto produce petroleum products for use withinthe country, such as naphtha.

The production could be compared to 17 bcf /day currently being produced from Qatar’sNorth Field, which is liquefied for Asian mar-kets.

“South Pars will probably achieve similar pro-duction level to Qatar around 2020,” he said.

But “they are still far behind Qatar in terms ofcumulative gas production.”

Of the current gas production, 13 per cent isreinjected, 16 per cent is flared or lost, and 71per cent if marketed, he said.

The overall gas production in Iran is planned toincrease from 24-25 bcf /day to over 42 bcf/dayby 2030, mainly by developing large gas fields.

This raises the question of what Iran will dowith the gas.

Up to 8 bcf/day might be injected into the oil-fields, to improve oil recovery.

They may need to install pipelines and com-pressors to send the gas to domestic or exportmarkets.

The Iran domestic market currently consumesabout 17 bcf a day, making it the 4th largestconsumer after US, Russia and China, with ahigher consumption than Italy and France.

The Iranian market could absorb more gas, par-ticularly for power generation, he said.

There has already been a dramatic fuel substi-tution over the past 2 years, equivalent toswitching 200 kbpd oil consumption to gas, hesaid.

The gas is also used in the petrochemical indus-try and for transport, where Iran has the secondlargest compressed natural gas (CNG) fleet inthe world, with 3m cars, planned to be in-creased to 5m.

FGE estimates that if the remaining gas goes toother markets, Iran will be exporting 5 bcf by2030.

This could be 0.5 bcf/day exported across thePersian Gulf to UAE, 0.5 bcf/day to Kuwait,1.5 bcf for Iraq (although that is only temporarybecause Iraq plans to develop its own produc-tion). Some gas could go to Pakistan, which thecountry shares a border with.

Sending Iranian gas to Europe is currently nota viable economic position, with gas prices nothigh enough to support the necessary pipelines.

Liquefying the gas could not be done today dueto the sanctions blocking import of the neces-sary technology, but would still be tough with-out the sanctions.

There is an option of sending gas by pipeline toDas Island, which is around 50 miles offshoreAbu Dhabi, UAE, where there is a gas lique-faction facility.

Political risk

There is always a risk of political instability andsanctions coming back. It has hard to make pre-dictions so it comes down to what sort of riskscompanies are comfortable with.

There are similar risks in all Middle East coun-tries, he said. “The oil is there, the problem ispolitics,” he said. “There is always risk.

Even US politics is very unpredictable. If thenext president is Republican, it could be lesslikely that US sanctions get lifted – but thereare also many US companies lobbying politi-cians to lift sanctions. “Who knows the future,”he said.

See a link to Siamaks’s talk on video and down-load slides atwww.findingpetroleum.com/event/e03a4.aspx

What did you enjoy most about the event?

“ “To get an overviewof important issuesin the Levant andthe Middle East. Olav Nipen, Statoil

“"Good number ofrelevant details Ihadn't beenaware of.M. Al-Chalabi

” ” ”This was the best, most contentfilled event I have attended atFinding Petroleum. Excellentvivid speakers with huge experi-ence and insight, well delivered.

“ “"Very goodpresenta-tionsDavidSendra

Neil Hodgson. Alwaysgood value since I firstsaw him present Triassic 'podology'using a Toblerone 25years ago!

“"Good mixtureof the politicaland economic challenges v the geologyCGG

”” ”“John Hurst's pres-

entation - lots ofinformation,opinion, andinsight

Richard Jones

”

“”

top class presentationsMartin Anderson, Ikon Science

“ “"Good varietyof talks and in-troduction toopportunitiesin the ME andLevant

"Well organised.Diverse and well presentedsubjects."

“Thought provok-ing and good tosee some technicalrather than justmarketing exercises.

”” ”“Good selection of talks, with a

balanced mix of overviews anddetail, in both geotechnicaland the commercial spheres.Well done.

”

“Well organised.Diverseand wellpresentedsubjects.

”

List of attendees - Finding Petroleum: Opportunities and risks in theMiddle East & the Levant, The Geological Society, London, Oct 20 2015

11Event Report, Opportunities and Risk in the Middle East & The Levant, Oct 20, 2015, London

Evi Otobo, Senior GeoscientistStuart Amor, AnalystHugh Ebbutt, Associated DirectorA.T. KearneyChristian Bukovics, Partner, Adamant VenturesRushen Patel, Chief Operating OfficerAfraz AdvisersPaul Murphy, Key Account Manager, Oil and Gas Division, Airbus Defence and SpaceAnil Katyal, AK AssociatesDuncan McSorland, Business Development Manager,Aker SolutionsChris Beech, Business Development Manager - CapitalProjects, Amec Foster WheelerRichard Hedley, Director, International New Ventures,AnadarkoGeoffrey Boyd, Field Development Consultant AntiumFrontfieldChristian Richards, VP Sales, EAME ARKeXNeil Frewin, Exploration Manager - Global New Ven-tures, BG GroupMark Houchen, Global New Venture Manager BGGroupSarah Brazier, Geophysicist, BG GroupMick McCaughey, Exploration Stategy and Portfolio Manager, BG GroupSean Goodman, Geophysicist, BridgeporthRobert FE Jones, Director, Caithness PetroleumRobert Kennedy, Commercial DirectorCaithness Petroleum LimitedAndy Horbury, Director, Cambridge CarbonatesAdam Thomas, Senior Consultant, CGGJames Andrew, Busines Development Mgr EAME CGGMustafa Elsherif, Sales Manager, CGGAli Zolalemin, Head of Business Development, CGGSiebe Breed, Structural GeologistCGG - NPA Satellite MappingTina Brough, Scouting Geologist, CGG RobertsonPaul Logan, Director, Chase GeoscienceJohn Lyle, Senior New Venture Earth Scientist, ChevronJohn Glass, Consultant Geologist, Cloverfield ConsultingLtdPeter Farrington, Geophysicist, Consultant, GeophysicistCorneliu Cosovanu, Senior Geologist, CoreLab Integrated Reservoir Solutions-UKDan Kunkle, Director, Count GeophysicsDavid Boote, DBconsulting LtdPaulo Godinho, Marketing Manager, DigitalGlobeBen James, Sales Coordinator, Dolphin GeophysicalChris Anderson, Marine Sales ManagerDolphin Geophysical Ltd.Ian Blakeley, VP Asia, Drilling InfoMichael Sharman, International Territory Manager - EMEA DrillinginfoJustin Sangster, EMEA Manager, DrillingInfoGavin Mc Aulay, Business Development Manager, Earthworks ReservoirMartin Riddle, Technical Manager, EnvoiMark Lonergan, Senior Business Development ManagerEPI LtdMurray Johnson, Geologist, Europa Oil & GasJohn Hurst, Ex-GenelMarlene Haase, Geologist, ExxonMobilPaul Nicholson, Team Technical Lead North and EastAfrica New Ops, ExxonMobilSiamak Adibi, Senior Consultant, Head of Middle EastGas Team, Facts Global EnergyRob Beckmann, Facts Global EnergyAudrey Dubois-Hebert, Oil analyst, FGERichard McIntyre, Sales Manager,Finding PetroleumAvinga Pallangyo, Conference Coordinator, Finding Petroleum

Karl Jeffery, Editor, Finding PetroleumSalar Golestanian, Managing Director, Finity AssetTom Whittington, Associate, FirstEnergy CapitalNikki Jones, MSc Student, GeoExproRichard Jones, CEO, Geospatial Research LtdStephen Shorey, General Manager, GeotraceJohn Stafford, V.P. OperationsGulf Keystone PetroleumFaouzi Khene, GXTSimon Berkeley, Principal, HalliburtonMike Simmons, Technology Fellow (Geosciences), Halliburton/NeftexDavid Harper, Principal Consultant, Harper AssociatesGiles Middleton, Director, Hermes Datacommunications International LtdLuke Calladine, Exploration Researcher, IHSClaire Woolsey, Analyst, IHSAlastair Reid, Consultant, IHSWilliam Gibson, Legal Analyst, IHSMartin Anderson, Business Development Manager, Ikon ScienceCameron Davis, SVP Sales, Ikon ScienceEhsan Naeini, Senior Research AdvisorIkon ScienceManouchehr Takin, Independent consultantMark Jones, Business Development Manager E&A INTECSEABob Lambert, Founder, Ipex Energy LtdRitchie Wayland, Exploration ManagerJKX Oil & Gas plcChristopher Tiratsoo, Editor, Journal of Petroleum GeologyPeter Knox, Consultant, KTSRichard Handley, Account ManagerLandmark SoftwareQusay Abeed, Petroleum Geologist, Landmark, NeftexRod Makin, Consultant, LK ExplorationDavid Peel, Technical Director, LukoilAhmed Elghorori, LukoilRichard Bootle, LukoilArtem Kotener, Lukoil OverseasAmrit Brar, Marketing and Sales RepresentativeLynx Information SystemsJim Lee, Associate Director, MacquarieRobert Palfrey, Managing Director, Minerva SRMPaul Richardson, Geoscientist, NeftexHarish Pillai, Vice President, Neo EnergyDavid Bamford, New Eyes ExplorationGreg Jones, Team Lead, Europe New Ventures Explo-ration, Nexen-CNOOCFrances Morris-Jones, Non-Executive Director, OGARamesh Shukla, Shareholder of exploration companiesShah Jahan Khandokar, Associate, Norton Rose FulbrightElsa Weatherley-Godard, AssociateNorton Rose Fulbright LLPJodie Cocker, Remote Sensing GeologistNPA Satellite MappingToby Walker, Account Manager, OneSubseaPeter Dolan, Advisor to the Board of Directors OphirEnergy PLCRobert Parker, Consultant, ParkerHoward Dewhirst, Managing Director, Petroalbion P/LJonathan Popper, Vice President Business Development, Petrofac Integrated Energy ServicesGreg Coleman, MD, Petromall LtdDavid Sendra, Associate Consultant, Petrophysical ConsultantM. Al-Chalabi, Head, Petrotech ConsultancyGrenville Lunn, Manging Director, PGA Ltd

Lance Usher, Sales Manager, PGSOystein Lie, PGSJohn Maciver, MultiClient Supervisor, PGSSoraya Derdiri, Private Investor, PIKevin Sylvester, Director, Pinnacle Energy LimitedChris Newton, Sales Manager, Polarcus UK LtdAruna Mannie, Senior Exloration GeoscientistPremier OilTim Davies, Global Portfolio & NV ManagerPremier OilRick Moore, Director, Quad OperationsMike Rego, Managing Director, Rego Exploration (Oil & Gas Consultancy Services)Robert Snashall, Consultant, RGSConsultRobert Stevens, Richmond Energy PartnersAlastair Bee, Partner, Richmond Energy PartnersAndreas Exarheas, Assistant Editor, RigzonePatrick Taylor, Director, RISC (UK) LimitedRobert Waterhouse, Director, Rosha Resources LtdJohn Georgiou, Exploration Consultant GeophysicistRps EnergyJanice Weston, Principal Advisor, RPS Energy Ltd.Matteo Di Lucia, RPS GroupStephen Trueblood, Commercial Manager, SasolRajan Gupta, Principal Geoscientist, SasolJan Nietzer, Senior Geoscientist, Global New VenturesSasolKevin Dale, Exploration Advisor, New VenturesSasol E & P InternationalDavid Webber, Seismic Operations SupervisorSceptre Oil & GasTomi Owodunni, Schlumberger Account ManagerSchlumbergerOddi Aasheim, Managing Director SLP Global Ltd.Neil Hodgson, New Ventures Manager, SpectrumGareth Morris, Account Manager, SpectrumOlav Nipen, Specialist Geology, StatoilDomenico Lodola, Geologist, Sterling EnergyAndrew Lodge, Principal, Strategic Fit, Egdon ResourcesChris Jones, Senior Consultant, StrategicFitDaniel Barnes, Consultant, StrategicFitAdam Mitchell, Principal, StrategicFitDavid Green, Head of Sales, The Energy ExchangePatrick Djuma, Commercial Manager - AfricaThe Energy ExchangeBrian McBeth, Managing PartnerThe Oxford Consultancy GroupAndy Cooper, Sales Director, ThyssenKruppMick Michaelides, General Manager, Troika InternationalSteven McTiernan, Director, Tullow Oil plcPete Brooke-Monti, Recruitment ManagerUpstream Technical Consultants LtdAlec Robinson, President & CEO, Valient EnergyMike Branston, WesternGecoCesar Purchio, Marine MENA Sales ManagerWesternGecoJohn Wood Consultant Geophysicist-GeosciencetistWood Geoscience LimitedChris Gumm, Business Development Manager - Automation Business Unit, Wood Group MustangCaron Howard, New Client Development ManagerWood MackenziePhil Houston, Senior Consultant, WorleyparsonsChris Phillips, General Manager, WorleyParsonsMohammed Khalil, Business Development ManagerXodus GroupAndrew Zolnai, Consultant, zolnai.ca

Opportunities and Risk in the Middle East & The Levant

A Clearer Image | www.pgs.com

Innovate Explore Discover New PGS acquisition and imaging technologies have the power to reveal the potential offshore western Egypt EGAS and PGS plan to acquire up to 20 000 km new GeoStreamer® data over western Egypt before the 2017 license round. True broadband data can reveal clearer and more reliable images of the prospectivity of this under-explored area. Contact us if you would like to participate in the project, and tailor the acquisition and processing parameters to meet your exploration objectives.

Schedule a meeting to learn more about this exciting opportunity: [email protected]