SPECIAL OLYMPICS MARYLAND, INC. FINANCIAL STATEMENTS ... · Olympics Unified Sports to their...

21

SPECIAL OLYMPICS MARYLAND, INC. FINANCIAL STATEMENTS DECEMBER 31, 2016

Transcript of SPECIAL OLYMPICS MARYLAND, INC. FINANCIAL STATEMENTS ... · Olympics Unified Sports to their...

SPECIAL OLYMPICS MARYLAND, INC.

FINANCIAL STATEMENTS

DECEMBER 31, 2016

TABLE OF CONTENTS

Page

Independent auditor's report 1 – 2 Financial statements Statement of financial position 3 Statement of activities 4 Statement of cash flows 5 Notes to financial statements 6 – 17 Supplementary information Schedule of functional expenses 18

-1-

INDEPENDENT AUDITOR’S REPORT

To the Board of Directors of Special Olympics Maryland, Inc. Baltimore, Maryland We have audited the accompanying financial statements of Special Olympics Maryland, Inc. (a non-profit Organization), which comprise the statement of financial position as of December 31, 2016, and the related statements of activities and cash flows for the year then ended, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements

in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and

disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

-2-

Special Olympics Maryland, Inc. Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Special Olympics Maryland, Inc. as of December 31, 2016, and the changes in its net assets and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. Report on Summarized Comparative Information

We have previously audited Special Olympics Maryland, Inc.’s 2015 financial statements, and

our report dated May 17, 2016 expressed an unmodified opinion on those audited financial statements. In our opinion, the summarized comparative information presented herein as of and for the year ended December 31, 2015, is consistent, in all material respects, with the audited financial statements from which it has been derived. Other Matter

Our audit was conducted for the purpose of forming an opinion on the financial statements as a whole. The schedule of functional expenses on page 18 is presented for the purposes of additional analysis and is not a required part of the financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the financial statements. The information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated in all material respects in relation to the financial statements as a whole.

MULLEN, SONDBERG, WIMBISH & STONE, P.A. Annapolis, Maryland May 23, 2017

The accompanying notes are an integral part of these financial statements.

-3-

Special Olympics Maryland, Inc. STATEMENT OF FINANCIAL POSITION

December 31, 2016

2016 2015CURRENT ASSETS

Cash and cash equivalents 919,357$ 975,616$ Contributions receivable 217,357 181,807Prepaid expenses 12,953 4,137

Total current assets 1,149,667 1,161,560

PROPERTY AND EQUIPMENTNet of accumulated depreciation 79,660 69,252

OTHER ASSETSInvestments 1,334,888 1,224,509Deposits and other assets 3,000 3,000

Total other assets 1,337,888 1,227,509

Total assets 2,567,215$ 2,458,321$

CURRENT LIABILITIESAccounts payable and accrued expenses 496,754$ 434,618$ Accrued payroll and related withholdings 81,496 51,994Accrued vacation 63,767 56,454Capital lease obligations 4,925 5,849Deferred rent 5,312 2,557Deferred revenue 3,107 18,750

Total current liabilities 655,361 570,222

LONG TERM LIABILITIESCapital lease obligations 6,778 11,703Deferred rent 44,067 49,379

Total long term liabilities 50,845 61,082

Total liabilities 706,206 631,304

NET ASSETSUnrestricted 526,121 585,091Unrestricted - Board designated 1,334,888 1,224,509Temporarily restricted - 17,417

Total net assets 1,861,009 1,827,017

Total liabilities and net assets 2,567,215$ 2,458,321$

ASSETS

LIABILITIES AND NET ASSETS

The accompanying notes are an integral part of these financial statements.

-4-

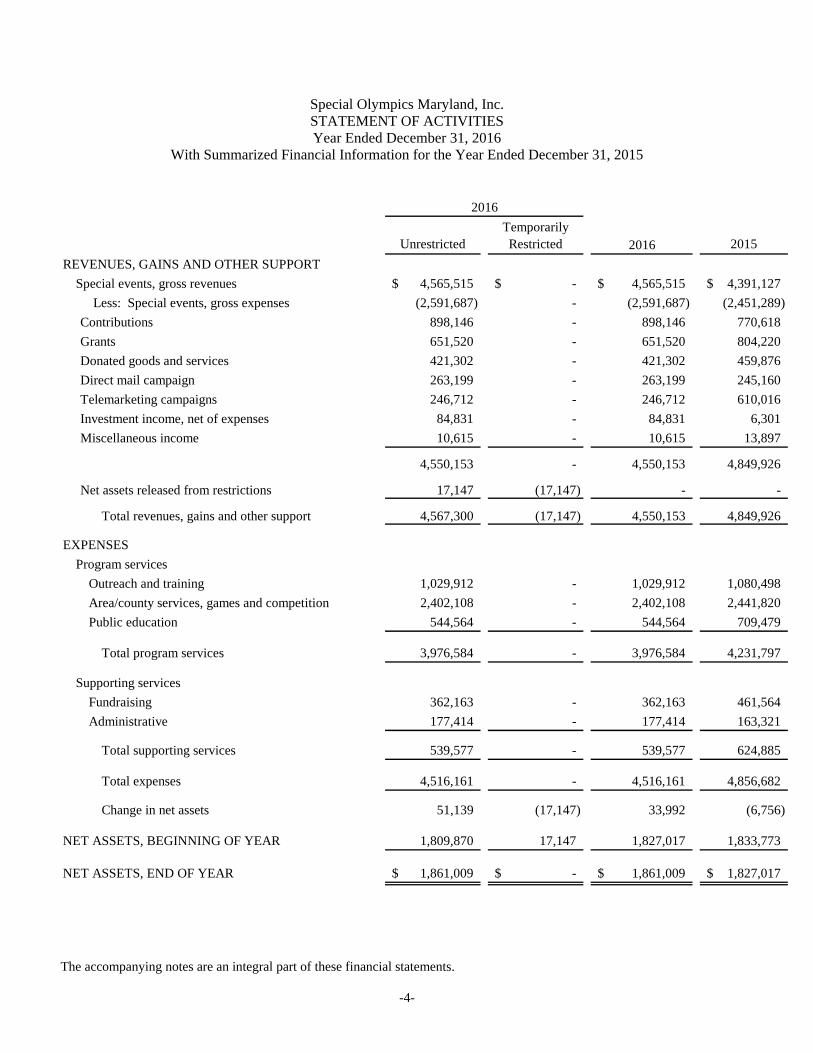

Special Olympics Maryland, Inc. STATEMENT OF ACTIVITIES Year Ended December 31, 2016

With Summarized Financial Information for the Year Ended December 31, 2015

UnrestrictedTemporarily Restricted 2016 2015

REVENUES, GAINS AND OTHER SUPPORT

Special events, gross revenues 4,565,515$ -$ 4,565,515$ 4,391,127$

Less: Special events, gross expenses (2,591,687) - (2,591,687) (2,451,289)

Contributions 898,146 - 898,146 770,618

Grants 651,520 - 651,520 804,220

Donated goods and services 421,302 - 421,302 459,876

Direct mail campaign 263,199 - 263,199 245,160

Telemarketing campaigns 246,712 - 246,712 610,016

Investment income, net of expenses 84,831 - 84,831 6,301

Miscellaneous income 10,615 - 10,615 13,897

4,550,153 - 4,550,153 4,849,926

Net assets released from restrictions 17,147 (17,147) - -

Total revenues, gains and other support 4,567,300 (17,147) 4,550,153 4,849,926

EXPENSES

Program services

Outreach and training 1,029,912 - 1,029,912 1,080,498

Area/county services, games and competition 2,402,108 - 2,402,108 2,441,820

Public education 544,564 - 544,564 709,479

Total program services 3,976,584 - 3,976,584 4,231,797

Supporting services

Fundraising 362,163 - 362,163 461,564

Administrative 177,414 - 177,414 163,321

Total supporting services 539,577 - 539,577 624,885

Total expenses 4,516,161 - 4,516,161 4,856,682

Change in net assets 51,139 (17,147) 33,992 (6,756)

NET ASSETS, BEGINNING OF YEAR 1,809,870 17,147 1,827,017 1,833,773

NET ASSETS, END OF YEAR 1,861,009$ -$ 1,861,009$ 1,827,017$

2016

The accompanying notes are an integral part of these financial statements.

-5-

Special Olympics Maryland, Inc. STATEMENT OF CASH FLOWS

Year Ended December 31, 2016

2016 2015CASH FLOWS FROM OPERATING ACTIVITIES:

Change in net assets 33,992$ (6,756)$ Adjustments to reconcile change in net assets to net cash provided by operating activities:

Depreciation and amortization 30,536 32,242Realized/unrealized (gain) loss on investments (46,044) 53,087 (Increase) decrease in operating assets:

Contributions receivable (35,550) 52,505 Prepaid expenses (8,816) (3,381)

Increase (decrease) in operating liabilities:Accounts payable and accrued expenses 62,136 7,895 Accrued payroll and related withholdings 29,502 23,902 Accrued vacation 7,313 (84) Deferred revenue (15,643) (8,750) Deferred rent (2,557) 237

Net cash provided by operating activities 54,869 150,897

CASH FLOWS FROM INVESTING ACTIVITIES:Purchase of property and equipment (40,944) (29,676) Purchase of investments and reinvested income (94,917) (459,262) Proceeds from the sale of investments 30,582 205,510

Net cash used by investing activities (105,279) (283,428)

CASH FLOWS FROM FINANCING ACTIVITIES:Principal payments on capital lease obligations (5,849) (11,745)

Net change in cash and cash equivalents (56,259) (144,276)

Cash and cash equivalents at beginning of year 975,616 1,119,892

Cash and cash equivalents at end of year 919,357$ 975,616$

SUPPLEMENTAL CASH FLOW INFORMATION:Cash paid during the year for interest 2,020$ 3,842$

-6-

Special Olympics Maryland, Inc. NOTES TO FINANCIAL STATEMENTS

December 31, 2016

Note 1 - Summary of Significant Accounting Policies

Nature of Organization

Special Olympics Maryland, Inc. (the Organization) provides year-round sports training and competition programs for children and adults with intellectual disabilities. The Organization has partnered with twenty-one of the State’s twenty-four School Districts to add Special Olympics Unified Sports to their Interscholastic Sports programs, to help those Districts comply with the 2008 Maryland Fitness and Athletics Equity for Students with Disabilities Act. These financial organization statements reflect the activities of the state office of Special Olympics Maryland, Inc. and the activities of eighteen geographical areas within Maryland that operate under the auspices of Special Olympics Maryland, Inc. These activities are funded primarily by special events, direct mail and telemarketing campaigns, and private contributions.

Basis of Accounting

The Organization prepares its financial statements in accordance with accounting principles generally accepted in the United States of America. This basis of accounting involves the application of accrual accounting; consequently, revenues and gains are recognized when earned, and expenses and losses are recognized when incurred.

Financial Statement Presentation

The financial statements include certain prior year summarized comparative information in total but not by net asset class. Such information does not include sufficient detail to constitute a presentation in conformity with accounting principles generally accepted in the United States of America. The prior year statement of financial position, statement of cash flows, and footnote disclosures are included for comparative purposes only. Accordingly, such information should be read in conjunction with the Organization’s financial statements for the year ended December 31, 2015, from which the summarized information was derived.

Revenue Recognition

Contributions and grants are reported as revenue in the year received and/or when the unconditional promises are made. Special Olympics Maryland, Inc. reports gifts of cash and other assets as temporarily restricted support if they are received with donor stipulations that limit the use of the donated assets. When a donor restriction expires, that is, when the restriction is met, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the statement of activities as net assets released from restrictions. Donor-restricted contributions whose restrictions are met in the same year are reported as unrestricted support. The policy for recognizing revenue for the Polar Bear Plunge was amended to reflect recognition of revenue in the period when the cash is received. Therefore, no pledge receivables were recorded for this event as of December 31, 2016 or 2015.

-7-

Special Olympics Maryland, Inc. NOTES TO FINANCIAL STATEMENTS (Cont.)

December 31, 2016

Note 1 - Summary of Significant Accounting Policies (Cont.)

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingencies at the statement of financial position date and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Cash and Cash Equivalents

For purposes of the statement of cash flows, cash and cash equivalents represent deposits in checking and savings accounts and certificates of deposit with original maturities of ninety days or less, except those that are part of an investment portfolio.

Contributions Receivable

Contributions receivable represent gifts from individuals and corporations for the general support of the Organization. All contributions are due within one year. All contributions are considered fully collectible; therefore no allowance has been established.

Investments

Investments comprise mutual funds and exchange traded funds. These investments are recorded in the financial statements at fair market value. Unrealized gains and losses are included in investment income in the statement of activities.

Property and Equipment

Property and equipment acquisitions in excess of $500 are capitalized and recorded at cost. Depreciation is provided over the estimated useful lives of the assets using the straight-line method.

Deferred Revenue

Deferred revenue consists of grant revenue for which the Organization has not met its obligation. Deferred revenue for the years ended December 31, 2016 and 2015 was $3,107 and $18,750, respectively.

Classification of Net Assets

Unrestricted net assets represent the portion of expendable net assets that are available for support of operations. Unrestricted, board designated net assets represent the portion designated by the Board of Directors to be used as a reserve fund.

-8-

Special Olympics Maryland, Inc. NOTES TO FINANCIAL STATEMENTS (Cont.)

December 31, 2016

Note 1 - Summary of Significant Accounting Policies (Cont.)

Income Tax Status

Special Olympics Maryland, Inc. qualifies as a tax-exempt Organization under Section 501(c)(3) of the Internal Revenue Code and is classified as other than a private foundation. Such organizations are taxed only on unrelated business income. No provision for federal income tax is required as of December 31, 2016 and 2015, as the Organization has no unrelated business income.

Income Tax Position

The Organization follows the guidance of ASC 740-10, “Accounting for Uncertainty in Income Taxes” which clarifies the accounting for the recognition and measurement of the benefits of individual tax positions in the financial statements, including those of non-profit organizations. Tax positions must meet a recognition threshold of more-likely-than-not in order for the benefit of those tax positions to be recognized in the Organization’s financial statements. The Organization analyzes tax positions taken, including those related to the requirements set forth in IRC Sec. 501(c) to qualify as a tax exempt organization, activities performed by volunteers and board members, the reporting of unrelated business income, and its status as a tax-exempt organization under Maryland state statute. The Organization does not know of any tax benefits arising from uncertain tax positions, and there was no effect on the Organization’s financial position or changes in net assets as a result of analyzing its tax positions. Years ending on or after December 31, 2013 remain subject to examination by federal and state authorities.

Donated Goods and Services

Donated services are recognized as a contribution if the services (a) create or enhance nonfinancial assets or (b) require specialized skills, are performed by people with those skills, and would otherwise be purchased by the Organization. Various individuals and organizations contribute goods and services to the Organization’s programs. Donated goods and services are recorded at fair value as of the date of donation and are included in contributions as revenue and assets or expenses in the accompanying financial statements. A significant number of unpaid volunteers contribute time to the Organization. The value of these services are not reflected in the accompanying financial statements in accordance with accounting principles generally accepted in the United States of America because the time contributed was for non-specialized services, and the recognition criteria was not met.

-9-

Special Olympics Maryland, Inc. NOTES TO FINANCIAL STATEMENTS (Cont.)

December 31, 2016

Note 1 - Summary of Significant Accounting Policies (Cont.)

Functional Expenses

The cost of providing the various programs and other activities has been summarized on a functional basis in the accompanying schedule of functional expenses. Accordingly, certain costs have been allocated to programs and supporting services based upon direct costs. Reclassifications Certain amounts in the prior year financial statements have been reclassified for comparative purposes to conform to the presentation in the current year financial statements.

Note 2 - Concentration of Cash Balances

At December 31, 2016 and 2015, and at various times during the year, the Organization maintained cash-in-bank balances in excess of the federally insured limit of $250,000. Amounts held in excess of FDIC insurance coverage at December 31, 2016 and 2015, were approximately $184,000 and $188,000, respectively. The Organization monitors the credit worthiness of these financial institutions and has not experienced any losses on its cash and cash equivalents.

Note 3 - Property and Equipment

Property and equipment consisted of the following at December 31:

Estimated Lives(in years) 2016 2015

Furniture and equipment 3 - 10 145,866$ 129,356$ Computer software 3 - 7 31,246 31,246 Work in progress 24,431 -

201,543 160,602 Less accumulated depreciation (121,883) (91,350)

79,660$ 69,252$

Depreciation expense for the years ending December 31, 2016 and 2015 was $30,536 and $32,242, respectively.

-10-

Special Olympics Maryland, Inc. NOTES TO FINANCIAL STATEMENTS (Cont.)

December 31, 2016

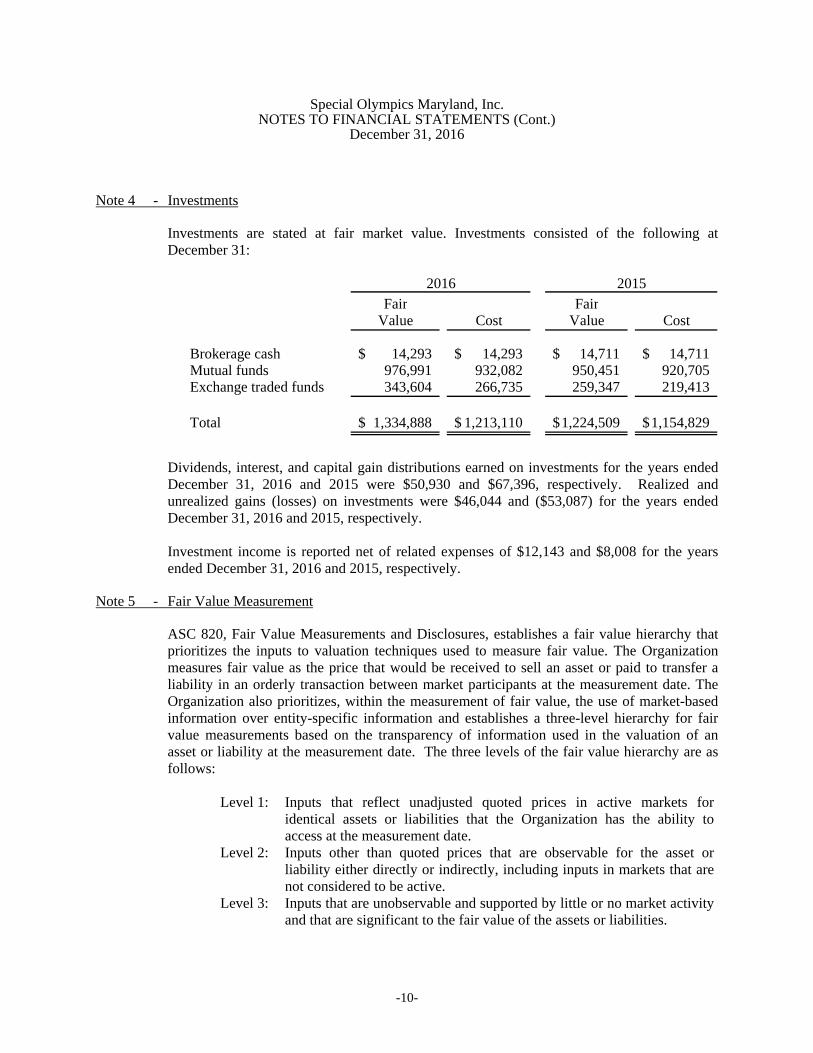

Note 4 - Investments

Investments are stated at fair market value. Investments consisted of the following at December 31:

Fair FairValue Cost Value Cost

Brokerage cash 14,293$ 14,293$ 14,711$ 14,711$ Mutual funds 976,991 932,082 950,451 920,705 Exchange traded funds 343,604 266,735 259,347 219,413

Total 1,334,888$ 1,213,110$ 1,224,509$ 1,154,829$

20152016

Dividends, interest, and capital gain distributions earned on investments for the years ended December 31, 2016 and 2015 were $50,930 and $67,396, respectively. Realized and unrealized gains (losses) on investments were $46,044 and ($53,087) for the years ended December 31, 2016 and 2015, respectively. Investment income is reported net of related expenses of $12,143 and $8,008 for the years ended December 31, 2016 and 2015, respectively.

Note 5 - Fair Value Measurement

ASC 820, Fair Value Measurements and Disclosures, establishes a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The Organization measures fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The Organization also prioritizes, within the measurement of fair value, the use of market-based information over entity-specific information and establishes a three-level hierarchy for fair value measurements based on the transparency of information used in the valuation of an asset or liability at the measurement date. The three levels of the fair value hierarchy are as follows:

Level 1: Inputs that reflect unadjusted quoted prices in active markets for identical assets or liabilities that the Organization has the ability to access at the measurement date.

Level 2: Inputs other than quoted prices that are observable for the asset or liability either directly or indirectly, including inputs in markets that are not considered to be active.

Level 3: Inputs that are unobservable and supported by little or no market activity and that are significant to the fair value of the assets or liabilities.

-11-

Special Olympics Maryland, Inc. NOTES TO FINANCIAL STATEMENTS (Cont.)

December 31, 2016

Note 5 - Fair Value Measurement (Cont.)

Inputs are used in applying the various valuation techniques and broadly refer to the assumptions that market participants use to make valuation decisions including assumptions about risk. Inputs may include price information, volatility statistics, specific and broad credit data, liquidity statistics, and other factors. A financial instrument's level within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement. However, the determination of what constitutes observable requires significant judgment by the Organization's management with the consultation of its investment advisors. Management considers observable data to be market data which is readily available, regularly distributed or updated, reliable and verifiable, not proprietary, and provided by independent sources that are actively involved in the relevant market. The classification of a financial instrument within the hierarchy is based upon the pricing transparency of the instrument.

Investments whose values are based on quoted market prices in active markets, and are, therefore classified with Level 1, include brokerage cash, active listed mutual funds and exchange traded funds. There have been no changes in investment valuation technique or inputs.

-12-

Special Olympics Maryland, Inc. NOTES TO FINANCIAL STATEMENTS (Cont.)

December 31, 2016

Note 5 - Fair Value Measurement (Cont.)

The table below presents the balances of assets measured at fair value on a recurring basis by level within the hierarchy as of December 31:

Level 1 Level 2 Level 3 Total Investments

Brokerage cash 14,293$ -$ -$ 14,293$ Mutual funds

Equity - large cap U.S. funds 383,790 - - 383,790 Equity - short term bonds 308,226 - - 308,226 Equity - small cap funds 130,856 - - 130,856 Equity - mid cap funds 76,580 - - 76,580 Equity - international funds 64,558 - - 64,558 Money market mutual funds 12,981 - - 12,981

Exchange traded fundsLarge value 336,779 - - 336,779 Mid cap value 6,825 6,825

Total investments 1,334,888$ -$ -$ 1,334,888$

Level 1 Level 2 Level 3 Total Investments

Brokerage cash 14,711$ -$ -$ 14,711$ Mutual funds

Equity - large cap U.S. funds 355,719 - - 355,719 Equity - short term bonds 220,105 - - 220,105 Equity - mid cap funds 118,355 - - 118,355 Equity - small cap funds 113,694 - - 113,694 Equity - international funds 59,591 - - 59,591 Equity - world bonds 58,236 - - 58,236 Money market mutual funds 24,751 - - 24,751

Exchange traded fundsLarge value 254,893 - - 254,893 Mid cap value 4,454 - - 4,454

Total investments 1,224,509$ -$ -$ 1,224,509$

2015

2016

-13-

Special Olympics Maryland, Inc. NOTES TO FINANCIAL STATEMENTS (Cont.)

December 31, 2016

Note 6 - Capital Lease Obligations

The Organization obtained two copiers in December 2010 with lease agreements accounted for as capital leases. In January 2014, one of the copiers was replaced with a new copier and lease agreement. All leases are for a period of 63 months. These capital lease obligations have been recorded in the financial statements at the present value of future minimum lease payments, discounted at an interest rate of 8%. At December 31, 2016 and 2015 the capitalized cost of the leased copiers amounted to $55,482. At December 31, 2016 and 2015, the book value of the copiers was $10,371 and $15,974, respectively. Amortization attributable to the copiers for the years ended December 31, 2016 and 2015 amounted to $5,603 and $10,568, respectively, and is included in depreciation and amortization expense on the schedule of functional expenses. The future minimum lease payments under the above capital leases are as follows:

Year Ending December 31

2017 5,733$ 2018 5,733 2019 1,435

Total future minimum lease payments 12,901 Less amount representing interest (1,198)

Present value of future minimum lease payments (including current portion of $4,925) 11,703$

For the years ended December 31, 2016 and 2015 the Organization incurred $2,020 and $3,842, respectively, in interest expense related to these leases.

Note 7 - Compensated Absences

Employees of the Organization are entitled to paid vacation, depending on job classification. At December 31, 2016 and 2015, employees had accrued vacation benefits of $63,767 and $56,454, respectively.

Note 8 - Line of Credit

During the year ending December 31, 2015, the Organization entered into an agreement with a financial institution to obtain a secured, revolving line of credit. The maximum allowable draw on the line is $125,000, bearing interest at LIBOR plus 2.75%. The line of credit expires October 31, 2017. As of December 31, 2016, there were no outstanding draws of the line of credit.

-14-

Special Olympics Maryland, Inc. NOTES TO FINANCIAL STATEMENTS (Cont.)

December 31, 2016

Note 9 - Unrestricted Board Designated Net Assets

The following special purpose funds have been designated by the Board of Directors as of December 31:

2016 2015

Quasi-endowment fund 155,976$ 117,032$ Reserve fund 1,178,912 1,107,477

1,334,888$ 1,224,509$

Note 10 - Net Assets (Unrestricted) – Board Designated / Quasi - Endowment

As of December 31, 2016 and 2015, the Board of Directors designated $155,976 and $117,032, respectively, of unrestricted net assets as a general endowment fund/quasi – endowment to support the Howard County program of Special Olympics Maryland, Inc. Since that amount resulted from internal designations and is not donor-restricted, it is classified and reported in unrestricted net assets.

The Organization has a spending policy that allows the Organization to either use the earnings to support the day-to-day operations of the Howard County program of Special Olympics Maryland, Inc. or reinvest the earnings.

Composition of and changes in board designated endowment net assets were as follows for the year ended December 31:

2016 2015

Board-designated endowment new assets, beginning of year 117,032$ 92,148$ Contributions 30,001 25,000 Investment income, net management fees 3,988 5,172 Net appreciation (depreciation) 4,955 (5,288)

Board-designated endowment net assets, end of year 155,976$ 117,032$

Note 11 - Temporarily Restricted Net Assets

The Organization received a grant to support strategic planning in Frederick County. During the year ended December 31, 2016 all restricted funds related to this grant were fully expended. The temporarily restricted net assets at December 31, 2016 and 2015 were $-0- and $17,417, respectively.

-15-

Special Olympics Maryland, Inc. NOTES TO FINANCIAL STATEMENTS (Cont.)

December 31, 2016

Note 12 - Allocation of Joint Costs

During the years ended December 31, 2016 and 2015, the Organization incurred joint costs of $155,504 and $425,033, respectively, for telemarketing activities that included both a program component and a fundraising appeal. Of these costs, $54,426 was allocated to fundraising and $101,078 was allocated to program services for the year ended December 31, 2016. For the year ended December 31, 2015, $148,762 was allocated to fundraising and $276,271 was allocated to program services.

Note 13 - Retirement Plan

The Organization sponsors a 403(b) defined contribution plan funded through a group annuity contract. Employee contributions to the Plan are discretionary, and the employer may match 100% of the employee contributions up to 4% of gross salary and an additional 4% of gross salary as an employer discretionary contribution. All employees who have completed at least 1,000 hours of services within one year and have reached 21 years of age are eligible to participate in the Plan. Employees become fully vested in the value of their account attributable to employer contributions after three years of service. Pension expenses for the years ended December 31, 2016 and 2015 were $77,291 and $80,238 respectively, and are included in employee benefits in the accompanying schedule of functional expenses.

Note 14 - Accredited Organization

The Organization is accredited by Special Olympics, Inc. Through this relationship, the Organization is allotted a share of the net revenue generated by direct mail fundraising campaigns conducted solely by Special Olympics, Inc. in Maryland. In turn, the Organization pays Special Olympics, Inc. an annual accreditation fee calculated based on a percentage of its total revenue earned, less in-kind donations and revenue earned from Special Olympics, Inc. During the years ended December 31, 2016 and 2015, the Organization received net funding of $183,827 and $170,988, respectively, from Special Olympics, Inc.

-16-

Special Olympics Maryland, Inc. NOTES TO FINANCIAL STATEMENTS (Cont.)

December 31, 2016

Note 15 - Commitments - Operating Leases

Special Olympics Maryland, Inc. has a non-cancelable operating lease for its main office space in Baltimore, Maryland that expires in August 2021. Under the lease, the base rent of $10,712 per month escalates 2% annually and is subject to common area maintenance fees. The Organization leases additional office space in Columbia, Maryland under a non-cancelable operating lease that expires in August 2021. The agreement is for $1,375 per month in base rent and escalates at a rate of 3% annually. Future minimum rental payments under the current leases are as follows for subsequent years ending December 31:

2017 185,676$ 2018 189,585 2019 193,594 2020 197,636 2021 135,712

Total 902,203$

Rent expense for the years ended December 31, 2016 and 2015 totaled $215,339 and $214,064, respectively and is included in occupancy on the schedule of functional expenses.

Note 16 - Donated Goods and Services

Donated goods and services of certain key volunteers and businesses have been recorded at their estimated value as of the date the services or goods were rendered. For the years ended December 31, 2016 and 2015, donated goods and services amounted to $1,340,409 and $1,357,026, respectively. If these goods and services were not provided by a volunteer or donor, they would otherwise have to be performed by paid personnel or subcontractors. Donated goods and services consist of in-kind donations for athletic events, special events, and donated legal services. In-kind contributions of $914,640 and $890,506 was recognized for the Polar Bear Plunge for the years ended December 31, 2016 and 2015 and are included on the statement of activities as special event revenue and expense. Of this amount, approximately $875,000 was donated from local radio and television stations for advertisements and promotions for the years ended December 31, 2016 and 2015.

-17-

Special Olympics Maryland, Inc. NOTES TO FINANCIAL STATEMENTS (Cont.)

December 31, 2016

Note 17 - Subsequent Events

The Organization has evaluated the impact of significant subsequent events. There have been no subsequent events that require recognition or disclosure through May 23, 2017, the date the Organization’s financial statements were available to be issued.

SUPPLEMENTAL INFORMATION

- 18 -

Special Olympics Maryland, Inc. SCHEDULE OF FUNCTIONAL EXPENSES

Year Ended December 31, 2016 With Summarized Financial Information for the Year Ended December 31, 2015

Outreach and Training

Area/County Services,

Games and Competition

Public Education Total Fundraising Administrative Total 2016 2015

Salaries 591,023$ 373,236$ 217,759$ 1,182,018$ 170,263$ 92,913$ 263,176$ 1,445,194$ 1,393,954$ Employee benefits 83,501 39,143 30,765 153,409 24,055 17,709 41,764 195,173 202,200 Payroll taxes 45,362 29,913 16,699 91,974 13,057 6,565 19,622 111,596 116,281

Total salaries and related expenses 719,886 442,292 265,223 1,427,401 207,375 117,187 324,562 1,751,963 1,712,435

Competition and training 39,417 1,684,498 4,703 1,728,618 2,735 4,153 6,888 1,735,506 1,816,951 Occupancy 86,310 94,457 31,801 212,568 24,864 12,500 37,364 249,932 246,555 Professional fees and services 57,345 20,787 105,214 183,346 11,622 30,113 41,735 225,081 268,384 Telemarketing - - 101,078 101,078 54,426 - 54,426 155,504 425,033 Postage and office supplies 22,327 22,723 7,189 52,239 42,480 2,914 45,394 97,633 76,365 Special Olympics, Inc. fee 39,686 39,686 - 79,372 - - - 79,372 74,172 Insurance 23,188 14,106 8,543 45,837 6,680 3,358 10,038 55,875 57,021 Travel and meetings 6,235 23,740 592 30,567 1,071 438 1,509 32,076 36,867 Telephone 12,198 8,997 4,085 25,280 3,558 2,302 5,860 31,140 41,132 Depreciation and amortization 12,059 10,001 3,897 25,957 3,047 1,532 4,579 30,536 32,242 Printing and publications 9,094 9,274 6,114 24,482 2,607 1,305 3,912 28,394 25,769 Fundraising and marketing 907 14,193 5,466 20,566 1,344 87 1,431 21,997 21,672 Miscellaneous 1,260 14,798 659 16,717 354 180 534 17,251 15,677 Interest - 720 - 720 - 1,300 1,300 2,020 3,842 Repairs and maintenance - 1,836 - 1,836 - 45 45 1,881 2,565

Total expenses 1,029,912$ 2,402,108$ 544,564$ 3,976,584$ 362,163$ 177,414$ 539,577$ 4,516,161$ 4,856,682$

Program Services Supporting Services Total