Speakers - WealthEngine | Wealth Data and Solutions for...

22

1

Transcript of Speakers - WealthEngine | Wealth Data and Solutions for...

1

Speakers

Tony Glowacki, Chief Executive Officer

Tony Glowacki‟s history with WealthEngine began over 10 years ago. He first shepherded the company

through a transition phase from what was Prospects of Wealth & Resources, Inc., into what is now

WealthEngine. During this time, his role was both as an angel investor and business strategist. In 2003,

having successfully assisted the company with the transition, Tony assumed the Chief Executive Officer‟s

position, which he has held since. Tony has had a long career in technology, particularly in the area of

information technology and database applications. He served in management roles at Manugistics from

1992 to 1996 before embarking on an entrepreneurial path. He has been both an active and passive early

stage investor in a diverse range of markets including real estate, banking, technology, and franchise

restaurants. Tony graduated with a BS from the University of Iowa and currently serves on their College of

Liberal Arts and Sciences Dean‟s Advisory Board. He is also a strong supporter of local non-profits whose

focus is on improving educational opportunities for under-privileged children.

Sameer Kasargod, SVP, Strategic Data Analytics and Professional Services

Sameer Kasargod joined WealthEngine in May 2010 as Senior Vice President, leading the newly created

Strategic Data Analytics and Professional Services group. Sameer is responsible for developing state of the

art analytics and statistical modeling capabilities to help organizations achieve higher return on investment

in their endeavors. In addition, Sameer also leads the professional services team that delivers consulting

services to nonprofit organizations. Sameer has 12 years of experience in business analytics, having held

senior leadership roles at Capital One, GE Capital and Sallie Mae. Sameer graduated from the University of

Bombay in Mumbai, India, then went on to earn his master‟s degree at the University of Missouri and his

Ph.D. from The Johns Hopkins University.

2

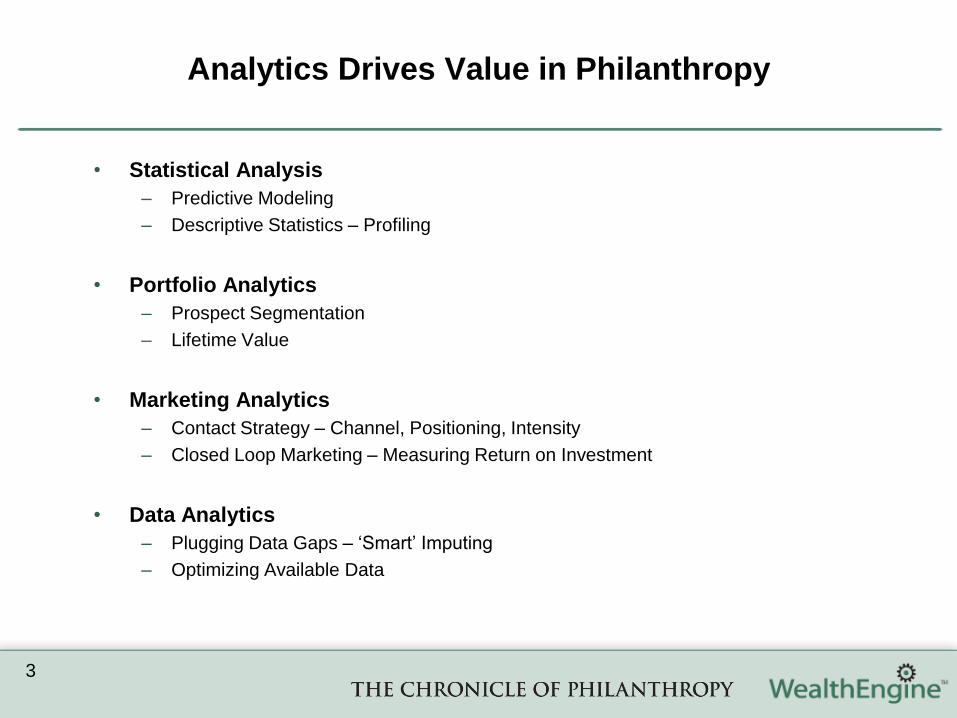

Analytics Drives Value in Philanthropy

3

• Statistical Analysis

– Predictive Modeling

– Descriptive Statistics – Profiling

• Portfolio Analytics

– Prospect Segmentation

– Lifetime Value

• Marketing Analytics

– Contact Strategy – Channel, Positioning, Intensity

– Closed Loop Marketing – Measuring Return on Investment

• Data Analytics

– Plugging Data Gaps – „Smart‟ Imputing

– Optimizing Available Data

Concentration of Wealth in the United States

4

• Wealth is highly concentrated in

the United States

– Top 1% of households own 43% of

total financial wealth

– Next 19% own 50%

– Bottom 80% own only 7%

• The recent recession has further

polarized this distribution

– 36% drop in marketable assets of

the median household compared to

11% for the top 1%

• In this environment, it is more

important than ever for fundraisers

to find wealth

43%

50%

7%

Top 1%

Next 19%

Bottom 80%

1%

19%

80%

Distribution of US Households*

Distribution of Financial Wealth

*Distributions as of 2007

Source: Wealth, Income, & Power by G. William Domhoff, July 2010

Agenda

• Defining Hidden Wealth

• How Analytics Uncovers Hidden Wealth

• Using Analytics to Unlock Hidden Giving

5

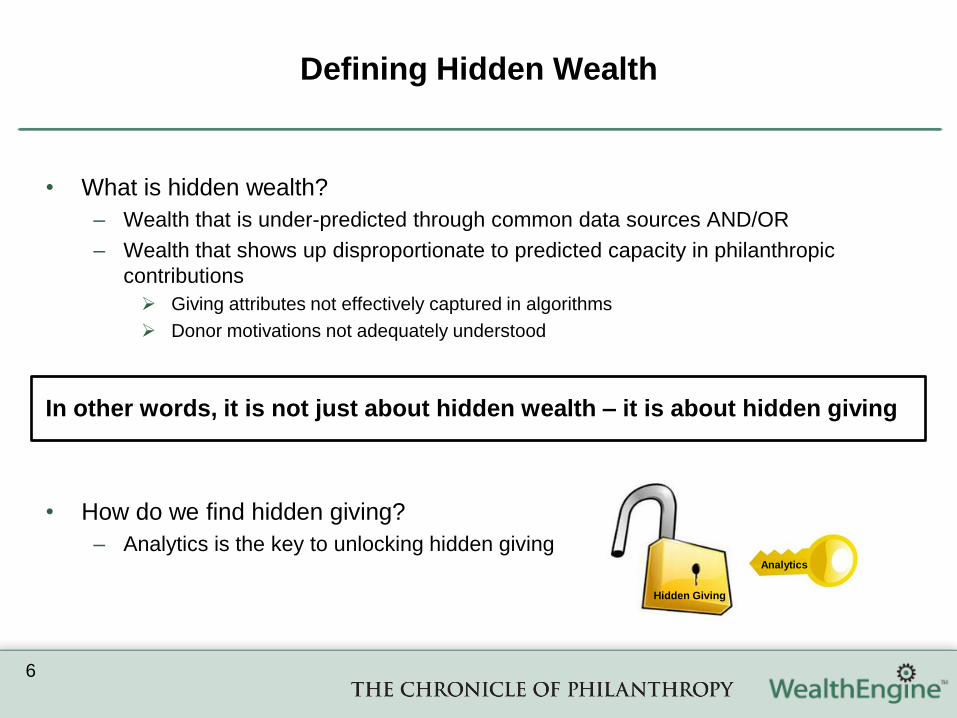

Defining Hidden Wealth

6

• What is hidden wealth?

– Wealth that is under-predicted through common data sources AND/OR

– Wealth that shows up disproportionate to predicted capacity in philanthropic

contributions

Giving attributes not effectively captured in algorithms

Donor motivations not adequately understood

In other words, it is not just about hidden wealth – it is about hidden giving

• How do we find hidden giving?

– Analytics is the key to unlocking hidden givingAnalytics

Hidden Giving

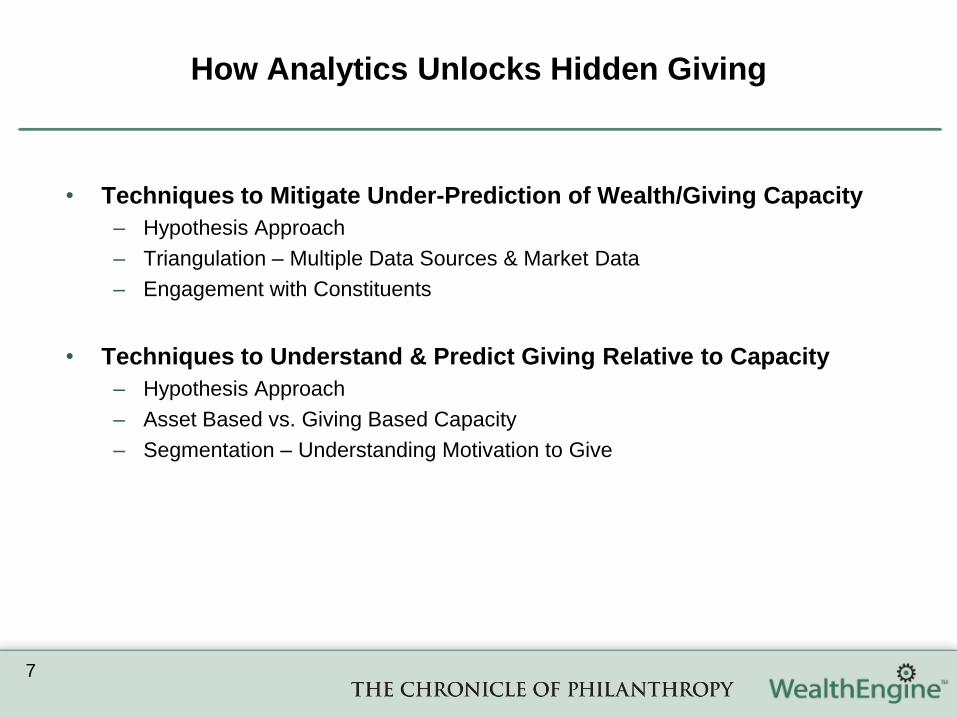

How Analytics Unlocks Hidden Giving

7

• Techniques to Mitigate Under-Prediction of Wealth/Giving Capacity

– Hypothesis Approach

– Triangulation – Multiple Data Sources & Market Data

– Engagement with Constituents

• Techniques to Understand & Predict Giving Relative to Capacity

– Hypothesis Approach

– Asset Based vs. Giving Based Capacity

– Segmentation – Understanding Motivation to Give

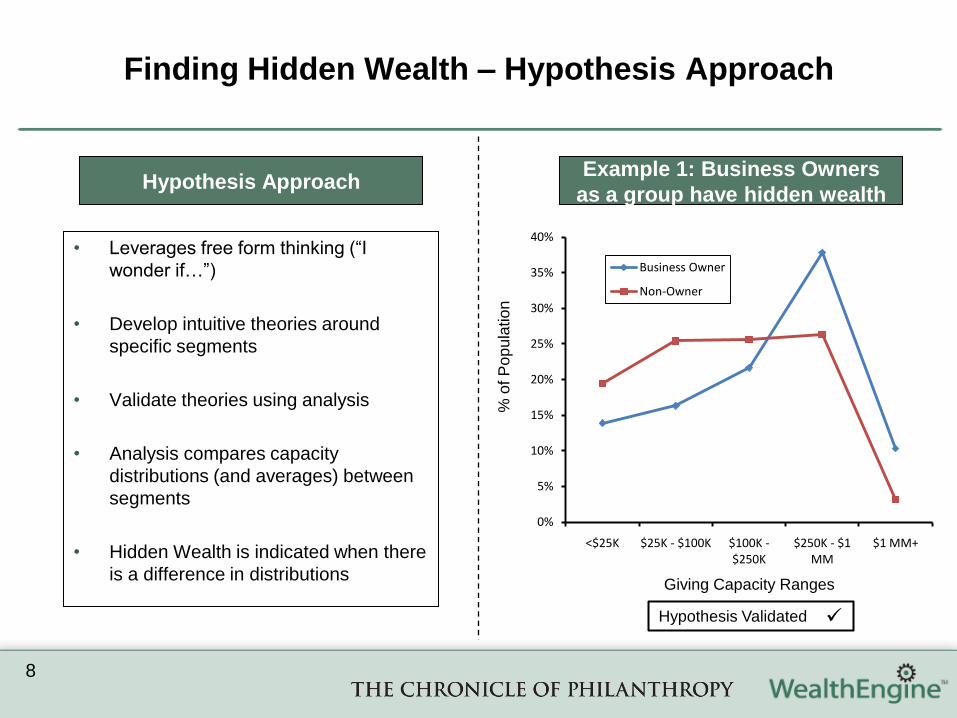

Finding Hidden Wealth – Hypothesis Approach

8

Hypothesis ApproachExample 1: Business Owners

as a group have hidden wealth

• Leverages free form thinking (“I

wonder if…”)

• Develop intuitive theories around

specific segments

• Validate theories using analysis

• Analysis compares capacity

distributions (and averages) between

segments

• Hidden Wealth is indicated when there

is a difference in distributions

0%

5%

10%

15%

20%

25%

30%

35%

40%

<$25K $25K - $100K $100K -$250K

$250K - $1 MM

$1 MM+

Business Owner

Non-Owner

Giving Capacity Ranges

% o

f P

op

ula

tion

Hypothesis Validated

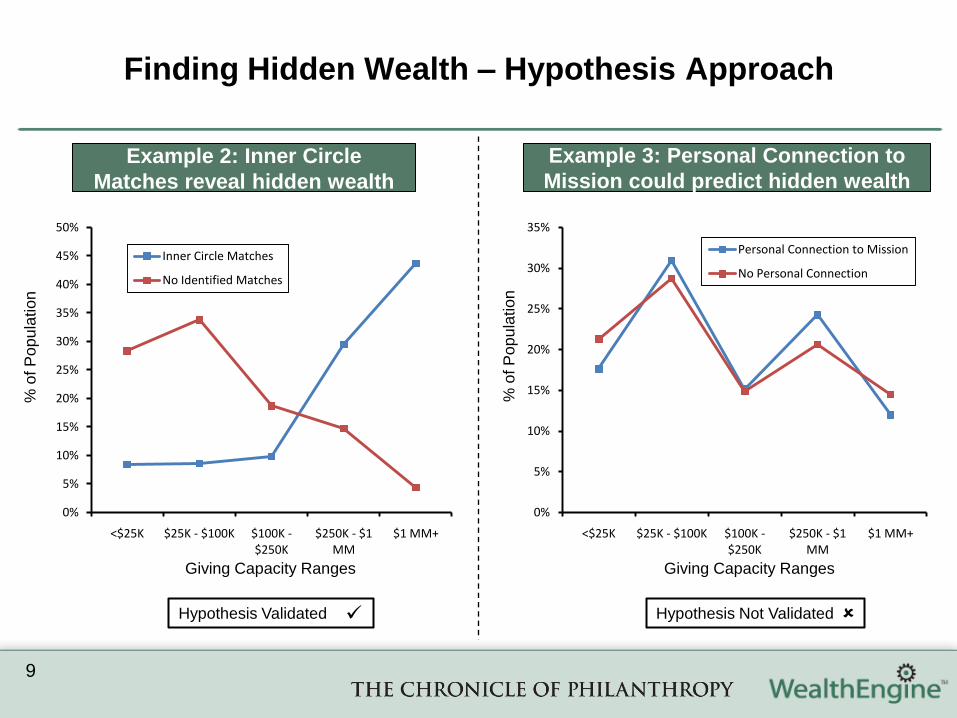

Finding Hidden Wealth – Hypothesis Approach

9

Example 2: Inner Circle

Matches reveal hidden wealth

Example 3: Personal Connection to

Mission could predict hidden wealth

% o

f P

op

ula

tion

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

<$25K $25K - $100K $100K -$250K

$250K - $1 MM

$1 MM+

Inner Circle Matches

No Identified Matches

0%

5%

10%

15%

20%

25%

30%

35%

<$25K $25K - $100K $100K -$250K

$250K - $1 MM

$1 MM+

Personal Connection to Mission

No Personal Connection

% o

f P

op

ula

tion

Giving Capacity Ranges Giving Capacity Ranges

Hypothesis Validated Hypothesis Not Validated

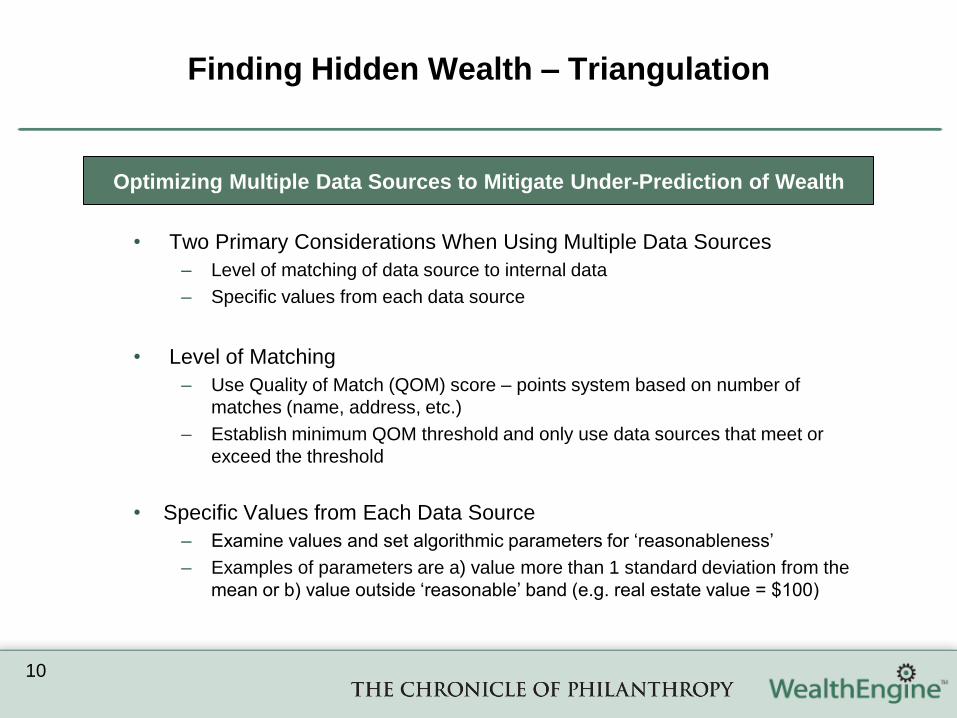

Finding Hidden Wealth – Triangulation

10

Optimizing Multiple Data Sources to Mitigate Under-Prediction of Wealth

• Two Primary Considerations When Using Multiple Data Sources

– Level of matching of data source to internal data

– Specific values from each data source

• Level of Matching

– Use Quality of Match (QOM) score – points system based on number of

matches (name, address, etc.)

– Establish minimum QOM threshold and only use data sources that meet or

exceed the threshold

• Specific Values from Each Data Source

– Examine values and set algorithmic parameters for „reasonableness‟

– Examples of parameters are a) value more than 1 standard deviation from the

mean or b) value outside „reasonable‟ band (e.g. real estate value = $100)

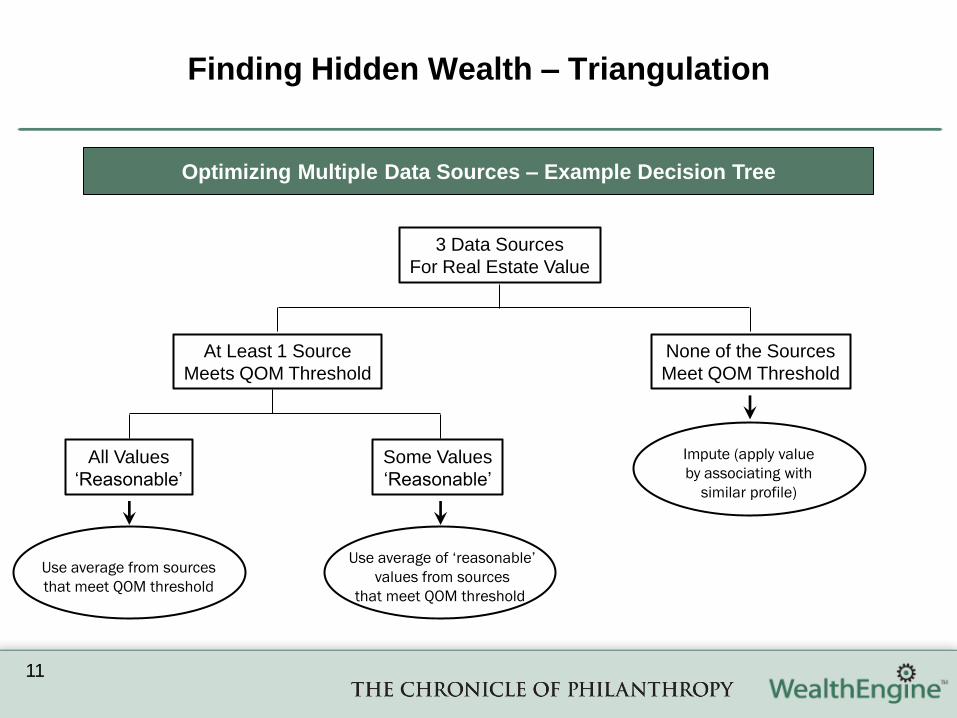

Finding Hidden Wealth – Triangulation

11

Optimizing Multiple Data Sources – Example Decision Tree

3 Data Sources

For Real Estate Value

At Least 1 Source

Meets QOM Threshold

None of the Sources

Meet QOM Threshold

All Values

„Reasonable‟

Some Values

„Reasonable‟

Use average from sources

that meet QOM threshold

Use average of ‘reasonable’

values from sources

that meet QOM threshold

Impute (apply value

by associating with

similar profile)

Finding Hidden Wealth – Triangulation

12

Size of net worth

Total assetsDebts and

mortgagesNet worth Personal residence Other real estate

Number Amount Number Amount Number Amount Number Amount Number Amount

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10)

Total 2,728 11,076,759 2,099 850,622 2,728 10,201,246 2,062 1,185,941 1,5311,402,029

Under $1.5 million 531 736,039 468 231,035 531 480,113 410 176,105 255 134,674

$1.5 million under $2.0 million 746 1,386,077 544 98,187 746 1,287,890 549 229,369 406 206,626

$2.0 million under $3.5 million 846 2,316,701 614 147,370 846 2,169,331 639 342,206 475 329,893

$3.5 million under $5.0 million 247 1,082,889 192 58,950 247 1,023,939 194 127,444 153 152,634

$5.0 million under $10.0 million 231 1,668,002 176 104,811 231 1,563,191 173 148,543 149 230,146

$10.0 million under $20.0 million 79 1,155,326 64 69,849 79 1,085,477 61 76,472 58 137,770

$20.0 million or more 47 2,731,726 40 140,421 47 2,591,305 36 85,802 35 210,286

Using Market Data for Enhancement of Wealth Estimates

• Published market data can be used to confirm internal estimates and/or refine asset calculations

• Reconciling internal asset data with market statistics solidifies estimates (i.e. ensuring that asset

breakouts are aligned with market distributions)

• Market data can also be used to refine asset calculations (i.e. extrapolating individual asset

components using market factors)

Subset of IRS Statistics of Income Data

Finding Hidden Wealth – Engaging with Constituents

13

• Ongoing engagement with constituents can lead

to new insights

– Identifying gaps in available data

– Determining variance in capacity estimates

– Monitoring economic and giving trends

• Periodic constituent research can be used as a

tool for more specific feedback

– Surveys and personal interviews to a randomly

selected constituent population

– Focus on collecting wealth, philanthropic &

demographic data

– Systematic data capture

• Analysis of constituent feedback enhances data

and analytic infrastructure

– Informs new data acquisition

– Strengthens wealth/capacity estimates

– Incorporates trends into projections

When In Doubt, Just Ask!

Integration of Various Approaches – Hidden Wealth

14

Analytics Drives

Continuous

Capacity Rating

Enhancement

New

Hypotheses

Constituent

Research

New

DataMarket

Data

Hidden Wealth

Finding Hidden Giving – Hypothesis Approach

15

Hypothesis ApproachExample 1: Business Owners

practice hidden giving

• Analysis compares percent of capacity

given between segments

• Comparisons are made within capacity

ranges

• Hidden Giving is indicated when there

is a difference in giving between

segments within capacity ranges

Giving Capacity Ranges

% o

f C

ap

acity G

ive

n

Hypothesis Validated

0%

10%

20%

30%

40%

50%

60%

70%

$1+ $100K+ $250K+ $1MM+ $5MM+

Business Owner

Non-Owner

Finding Hidden Giving – Hypothesis Approach

16

Example 2: Inner Circle

Matches reveal hidden giving

Example 3: Personal Connection to

Mission could predict hidden giving

% o

f C

ap

acity G

ive

n

% o

f C

ap

acity G

ive

n

Giving Capacity Ranges Giving Capacity Ranges

Hypothesis Validated Hypothesis Validated

0%

20%

40%

60%

80%

100%

120%

$1+ $100K+ $250K+ $1MM+ $5MM+

Inner Circle Matches

No Identified Matches

0%

10%

20%

30%

40%

50%

60%

70%

80%

$1+ $100K+ $250K+ $1MM+ $5MM+

Personal Connection to Mission

No Personal Connection

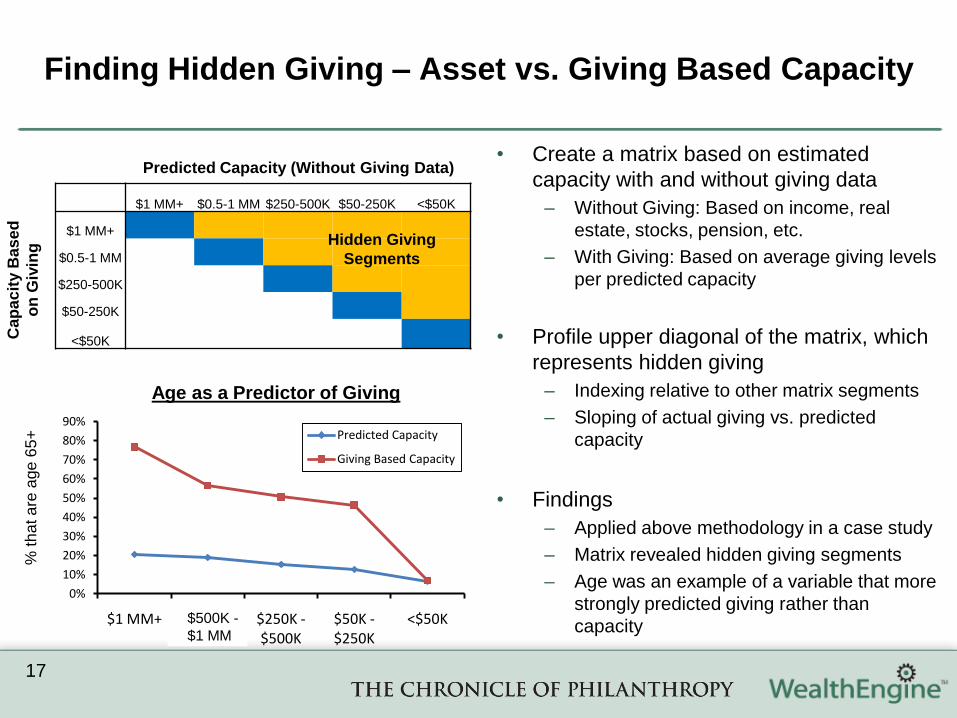

• Create a matrix based on estimated

capacity with and without giving data

– Without Giving: Based on income, real

estate, stocks, pension, etc.

– With Giving: Based on average giving levels

per predicted capacity

• Profile upper diagonal of the matrix, which

represents hidden giving

– Indexing relative to other matrix segments

– Sloping of actual giving vs. predicted

capacity

• Findings

– Applied above methodology in a case study

– Matrix revealed hidden giving segments

– Age was an example of a variable that more

strongly predicted giving rather than

capacity

$1 MM+ $0.5-1 MM $250-500K $50-250K <$50K

$1 MM+

$0.5-1 MM

$250-500K

$50-250K

<$50K

Hidden Giving

Segments

Predicted Capacity (Without Giving Data)

Cap

ac

ity B

as

ed

on

Giv

ing

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

$1 MM+ $500K - $1 MM

$250K -$500K

$50K -$250K

<$50K

Predicted Capacity

Giving Based Capacity

$500K -

$1 MM

Age as a Predictor of Giving

% th

at a

re a

ge

65

+

Finding Hidden Giving – Asset vs. Giving Based Capacity

17

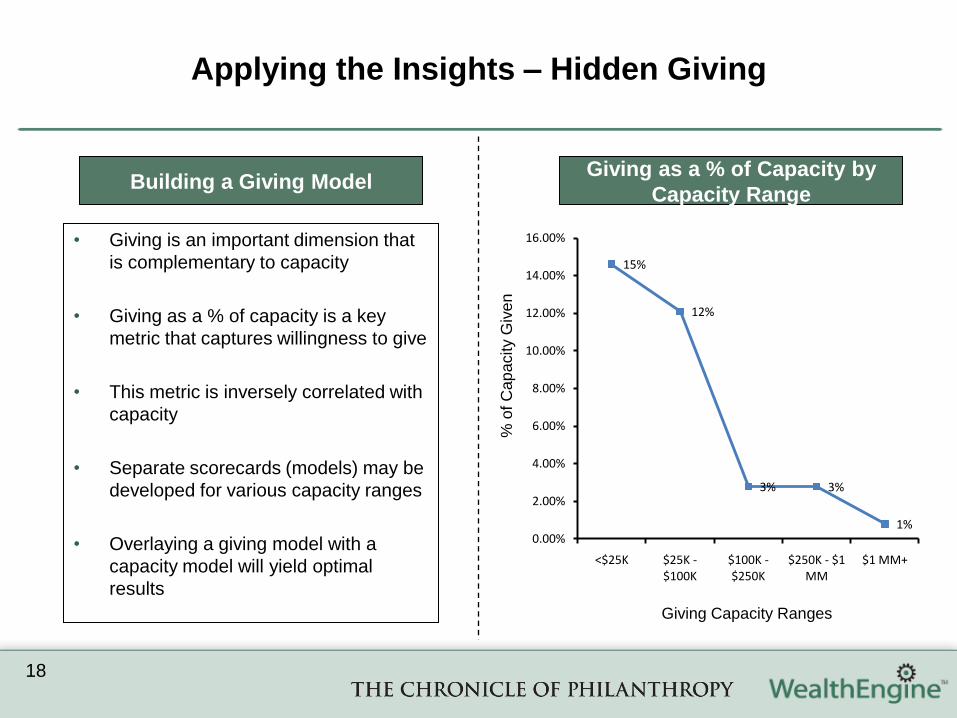

Applying the Insights – Hidden Giving

18

Building a Giving ModelGiving as a % of Capacity by

Capacity Range

• Giving is an important dimension that

is complementary to capacity

• Giving as a % of capacity is a key

metric that captures willingness to give

• This metric is inversely correlated with

capacity

• Separate scorecards (models) may be

developed for various capacity ranges

• Overlaying a giving model with a

capacity model will yield optimal

results

15%

12%

3% 3%

1%0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

<$25K $25K -$100K

$100K -$250K

$250K - $1 MM

$1 MM+

% o

f C

ap

acity G

ive

n

Giving Capacity Ranges

Finding Hidden Giving – Segmentation

19

• Repayers (e.g. Grateful Patients)

• Casual Givers (e.g. Disaster Relief)

• High Impact (e.g. Overlooked Social

Causes)

• Faith Based (e.g. Religious)

• See the Difference (e.g. Local

Community Oriented)

• Personal Ties (e.g. Inner Circle

Members)*From The Chronicle of Philanthropy (8/12/2010), sourced from „Money for Good‟ by Hope Consulting

• What is Segmentation?

– Dividing a large group of constituents into smaller

groups with homogenous needs, attitudes or

behaviors

• Why is it Important?

– Understanding donor motivations

– Developing segment specific messaging

– Prioritizing initiatives based on major segment

preferences

• How is Segmentation Developed?

– Information provided by constituents

Why did you give?

What do you like best about this organization?

Rank ordering of giving motivations

– Statistical Techniques

K-Means Clustering

Hierarchical Clustering

Regression Techniques

Example Segmentation*

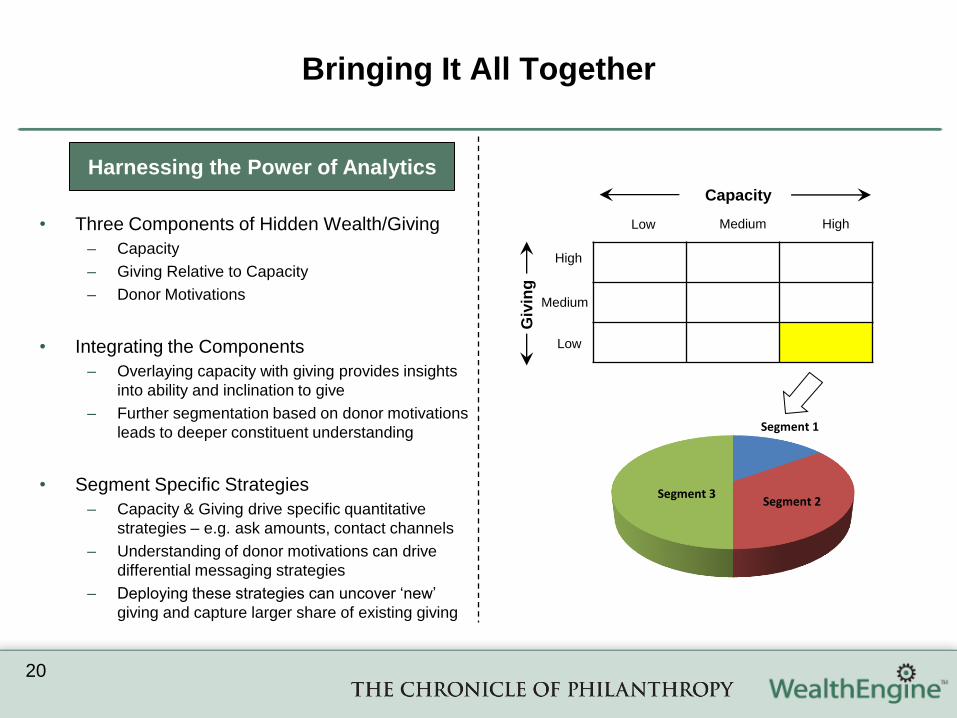

Bringing It All Together

20

Capacity

Giv

ing

Low Medium High

Low

Medium

High

Segment 1

Segment 2Segment 3

• Three Components of Hidden Wealth/Giving

– Capacity

– Giving Relative to Capacity

– Donor Motivations

• Integrating the Components

– Overlaying capacity with giving provides insights

into ability and inclination to give

– Further segmentation based on donor motivations

leads to deeper constituent understanding

• Segment Specific Strategies

– Capacity & Giving drive specific quantitative

strategies – e.g. ask amounts, contact channels

– Understanding of donor motivations can drive

differential messaging strategies

– Deploying these strategies can uncover „new‟

giving and capture larger share of existing giving

Harnessing the Power of Analytics

• We have explored several analytical techniques to find hidden wealth/giving

– Hypothesis Approach

– Triangulation

– Engagement with Constituents

– Asset Based vs. Giving Based Capacity

– Segmentation

• The techniques emphasize independent analysis of the three key aspects of giving

– Ability to Give – Related to Financial Capacity

– Inclination to Give – Related to Giving

– Organization Specific Giving – Related to Donor Motivation

• Integrating these aspects into strategy development can maximize fundraising success

– Uncover New Giving

– Capture Larger Share of Existing Giving

• It is not just about hidden wealth – it is about hidden giving

Key Takeaways

21

Questions?

22