Spanish Digital Startup Ecosystem Overview 2015

30

aquí DIGITAL STARTUP ECOSYSTEM OVERVIEW 2015 1

-

Upload

aleix-valls -

Category

Small Business & Entrepreneurship

-

view

1.780 -

download

0

Transcript of Spanish Digital Startup Ecosystem Overview 2015

aquí

DIGITAL STARTUP ECOSYSTEM OVERVIEW 2015

1

Spanish Startup Ecosystem

Barcelona Digital Hub Opportunity to foster the ecosystem

DIGITAL STARTUP ECOSYSTEM OVERVIEW 2015

2

Spanish Startup Ecosystem 3

STARTUPS IN SPAIN More than 20 years creating tech companies

0

1.500

3.000

4.500

6.000 NASDAQ index & founding date of Spanish startups

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

.com crisis economic crisis vs growth mobile companies

4 Source: Novobrief, Vitamina K

STARTUPS IN SPAIN Spain: The digital sector continues to grow

Digital sector to account for 3.1% of Spain’s GDP in 2016, €34.9 billion Telco-driven sector 2,638 startups +26%Year-on-Year (YoY) 3 main hubs: Barcelona: 26% of all startups,+16% (YoY) Madrid: 27%, +25% (YoY) Valencia: 14%, +32% (YoY)

5 Source: Boston Consulting Group, McKinsey, Startupxplore

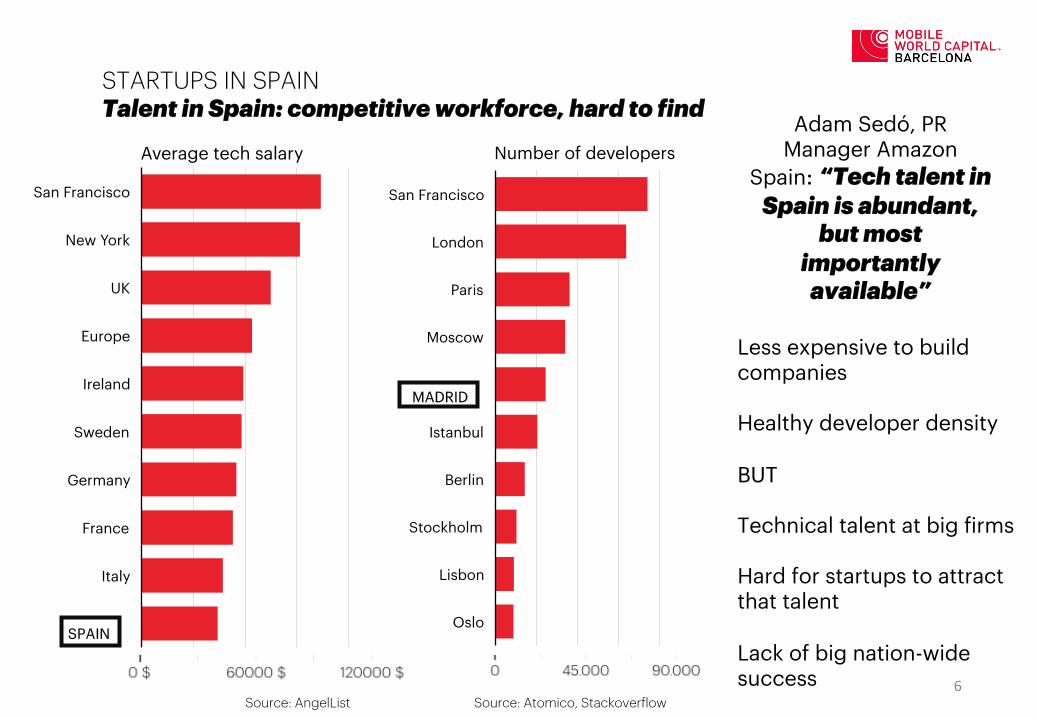

STARTUPS IN SPAIN Talent in Spain: competitive workforce, hard to find

Source: AngelList

SPAIN

MADRID

Less expensive to build companies Healthy developer density BUT Technical talent at big firms Hard for startups to attract that talent Lack of big nation-wide success Source: Atomico, Stackoverflow

USD0 USD30000 USD60000 USD90000 USD120000

San Francisco

New York

UK

Europe

Ireland

Sweden

Germany

France

Italy

0 22.500 45.000 67.500 90.000

San Francisco

London

Paris

Moscow

Istanbul

Berlin

Stockholm

Lisbon

Oslo

Adam Sedó, PR Manager Amazon

Spain: “Tech talent in Spain is abundant,

but most importantly

available”

Average tech salary

Number of developers

6

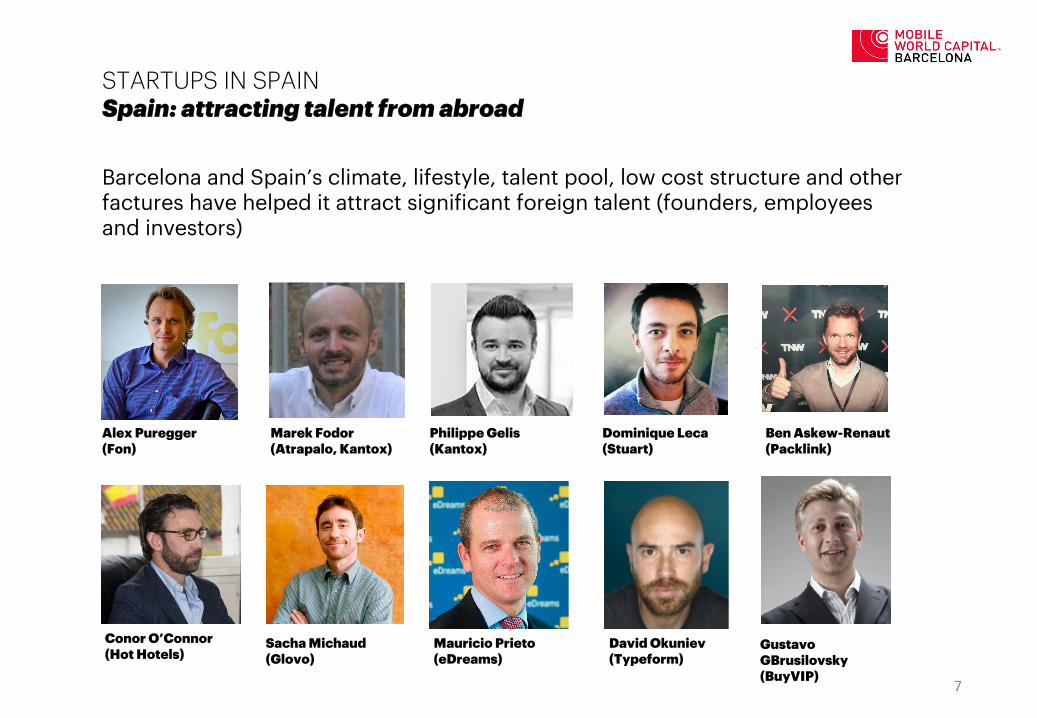

Barcelona and Spain’s climate, lifestyle, talent pool, low cost structure and other factures have helped it attract significant foreign talent (founders, employees and investors)

STARTUPS IN SPAIN Spain: attracting talent from abroad

Alex Puregger (Fon)

Marek Fodor (Atrapalo, Kantox)

Philippe Gelis (Kantox)

Dominique Leca (Stuart)

Ben Askew-Renaut (Packlink)

Sacha Michaud (Glovo)

Mauricio Prieto (eDreams)

David Okuniev (Typeform)

Gustavo GBrusilovsky (BuyVIP)

Conor O’Connor (Hot Hotels)

7

Source: Novobrief

2015, RECORD YEAR €500m + raised by Spanish startups for the 1st time ever

222

286

535

122 135 149

0

150

300

450

600

2013 2014 2015

Investment received by Spanish startups

Investment (m€)

More quality and mature startups Growth capital mostly provided by international VC firms More local talent available

Steady growth in startups, exponential growth in fundraising

2015 2014

+29% (YoY)

+10% (YoY)

+87% (YoY)

+10% (YoY) Deals

Capital raised

8

MEGA ROUNDS 13 rounds bigger than €10m

2013 2014

2015

2X €10m+ rounds in 2015 vs. 2013 and 2014 combined

9

HEALTHY MIX OF INVESTOR TYPES VCs and business angels as key ecosystem drivers

Source: Venture Watch

59% (69) 43%

(69)

15% (17)

27% (37)

0%

25%

50%

75%

100%

125%

2014 2015

Distribution of deals by investor type (Q1-3 2015 vs. 2014)

Venture Capital Business Angel BA Network Public funding Corporation Corporate VC Crowdfunding Accelerator 10

WHERE DOES THE MONEY GO? An ecommerce (or mobile classifieds) country

Source: Venture Watch

0 17,5 35 52,5 70

Ecommerce

Marketing

Lifestyle

Fintech

Travel

Communications

Education

Gaming

Data

Food

Top investment sectors 2013-15 (number of deals)

€0 €100 €200 €300 €400

Ecommerce

Fintech

eGovernance

Security

Marketing

Communications

Employment

Gaming

Data

Lifestyle

Sectors that have received most investment volume 2013-15 (M€)

11

FOREIGN INVESTORS NOT ONLY COME FOR THE SUN Growth capital mostly provided by international investors

Most ever: 44 VCs Fueling growth: 73% of all capital invested in 2015 Only one round of €10m+ (Jobandtalent) with no participation of foreign VCs

35%

15% 19%

13%

17%

In what type of rounds did foreign VCs participate in in 2015?

€1 to €5m €6 to €10m €11 to €15m €16 to €20m €20+m

Source: Novobrief 12

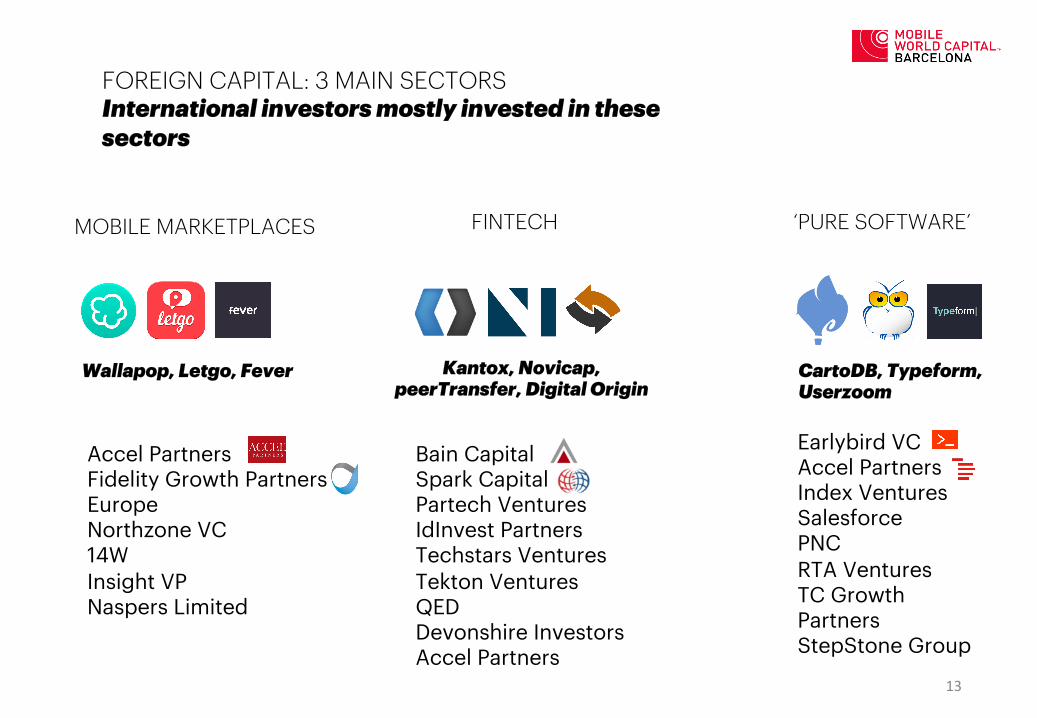

FOREIGN CAPITAL: 3 MAIN SECTORS International investors mostly invested in these sectors

Wallapop, Letgo, Fever

Accel Partners Fidelity Growth Partners Europe Northzone VC 14W Insight VP Naspers Limited

Kantox, Novicap, peerTransfer, Digital Origin

Bain Capital Spark Capital Partech Ventures IdInvest Partners Techstars Ventures Tekton Ventures QED Devonshire Investors Accel Partners

CartoDB, Typeform, Userzoom

Earlybird VC Accel Partners Index Ventures Salesforce PNC RTA Ventures TC Growth Partners StepStone Group

MOBILE MARKETPLACES FINTECH ‘PURE SOFTWARE’

13

Barcelona Digital Hub

14

A DIGITAL HUB Barcelona drives digital economy

10,700 ICT companies 73,000 employees €14.5b in turnover (1/5 of Spain) €214m in R&D Barcelona startups:

Revenue: €6b Workforce: 9,500 International activity: 60% are active abroad

Source: Barcelona Activa (early 2015) & BCN Tech City survey 15

A DIGITAL HUB Barcelona startup ecosystem

Source: BCN Tech City / Startupxplore

YOUNG: 4.8 years

MARKET: 41% B2B 26% B2C 33% B2B2C

SECTORS: 13% media 12% mobile 11% enterprise 6% marketing

FUNDING: 52% have received investment from business angels 33% went through an accelerator

INTERNATIONAL: 60% active outside of Spain, in more than 50 countries

16

A DIGITAL HUB Education + entrepreneurs + funding + public institutions/coworkings = success

Education

Funding

Entrepreneurs

Accelerators

* Non representative 17

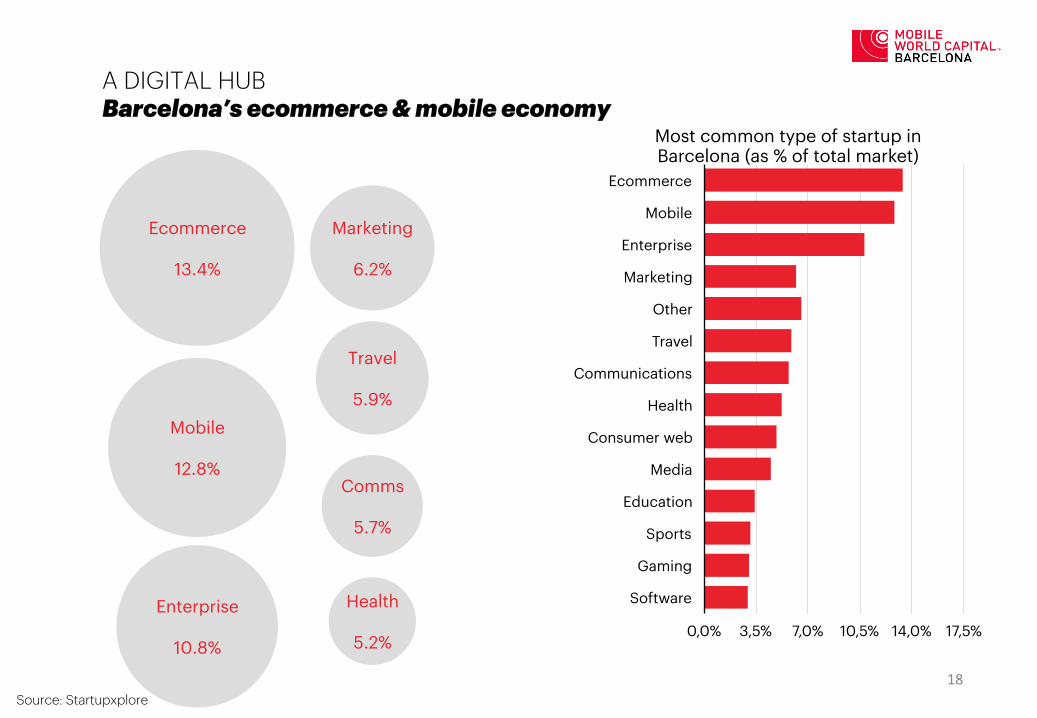

A DIGITAL HUB Barcelona’s ecommerce & mobile economy

Source: Startupxplore

0,0% 3,5% 7,0% 10,5% 14,0% 17,5%

Ecommerce

Mobile

Enterprise

Marketing

Other

Travel

Communications

Health

Consumer web

Media

Education

Sports

Gaming

Software

Most common type of startup in Barcelona (as % of total market)

Ecommerce

13.4%

Mobile

12.8%

Enterprise

10.8%

Marketing

6.2%

Travel

5.9%

Comms

5.7%

Health

5.2%

18

BARCELONA DOMINATES STARTUP INVESTMENTS 60% of all euros invested in 2015 went to Barcelona-based startups*

324

165

20

€0

€175

€350

€525

€700

Barcelona* Madrid Valencia

2015 2014 2013 2011

Source: Webcapitalriesgo, Novobrief * Barcelona and rest of Catalonia

19

BIGGEST ROUNDS IN BARCELONA Explosive growth

Source: Webcapitalriesgo, Novobrief

€92

€40

€30

€15

€13

0 25 50 75 100

Letgo

Wallapop

UserZoom

Digital Origin

Typeform

Kantox

Softonic

Deporvillage

Loanbook

Marfeel

Largest investment rounds in 2015 (€m)

€264m invested in Barcelona startups Hypergrowth: +96% (YoY) 92% of all capital invested inall of Spain in 2014 (€285m)

20

€6

€10

€4 €3 €3

BARCELONA’S TOP SECTORS Mobile classifieds, ecommerce & fintech

Source: Webcapitalriesgo, Novobrief

61% 13%

10%

3% 13%

Startup sectors that attracted more investment in 2015

Ecommerce ‘Pure software’ Fintech Health Other

Wallapop, Letgo & other ecommerce/classifieds startups lead the way Enterprise technology represented by UserZoom, Typeform, comes in second Fintech (payments - Digital Origin, FX - Kantox) third 5 investment rounds of €1m+ for health startups

21

INCREASING M&A ACTIVITY Creating wealth through exits

Trovit! Akamon! La Nevera Roja*!

Founded in…! 2006! 2011! 2011!

Number of years to exit! 8! 4! 3!

Selling price! €80m! €25! €80m!

Rounds of funding!1

(€150,000)!

3+

(€2.8m)!

3+

(€10m)!

Revenue in last full fiscal year

before exit!€17.5m (2013)! €15m (2014)!

€2m

(€40m in reported restaurant sales)!

EBITDA in same period! €6.2m! €800K (profit)!

Undisclosed

(not profitable)!

Revenue multiple paid by acquirer! 4.5X! 1.6X! 40X!

Employees! 92! ~ 100! ~ 40!

Stake (%) of founders at time of

exit!~ 90%! ~ 78%! ~ 30%!

Founder earnings! €72m! €19.5m! €24m!

Investor earnings! €8m (57X)! €5.2m! €48m!

SIGNIFICANT EXITS IN RECENT YEARS Key to spark entrepreneurship, new startups and redistribution of wealth More than $155 million in exits in past two years Recent exits:

Trovit (Next Co): €80m bodas.net (Weddingwire) Akamon (Imperus): €25m Icebergs (Pinterest) Ducksboard (New Relic) Nubera (Gartner)

Source: Novobrief *Madrid-based

22

Room for improvement Opportunity to foster the ecosystem 23

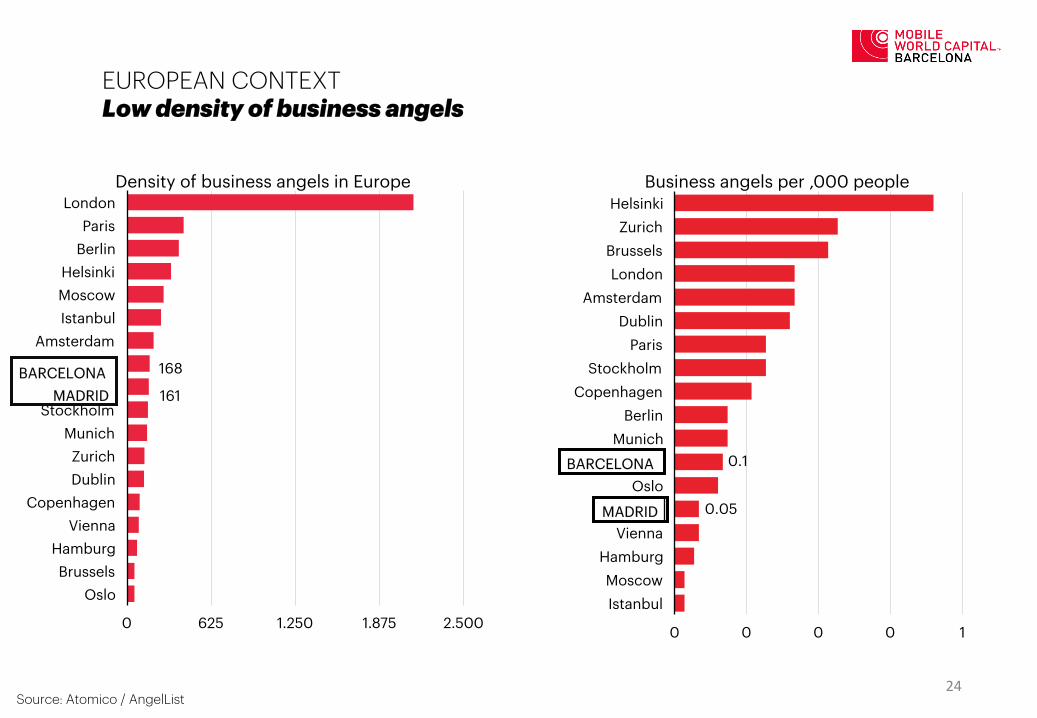

EUROPEAN CONTEXT Low density of business angels

Source: Atomico / AngelList

0 625 1.250 1.875 2.500

London Paris

Berlin Helsinki Moscow Istanbul

Amsterdam

Stockholm Munich Zurich Dublin

Copenhagen Vienna

Hamburg Brussels

Oslo

Density of business angels in Europe

BARCELONA MADRID

0 0 0 0 1

Helsinki Zurich

Brussels London

Amsterdam Dublin

Paris Stockholm

Copenhagen Berlin

Munich

Oslo

Vienna Hamburg Moscow Istanbul

Business angels per ,000 people

BARCELONA

MADRID

161

0.1

0.05

168

24

EUROPEAN CONTEXT Spain accounts for small fraction of EU exits & M&A value

93%

7%

M&A deals in Europe (Q1-3 2015)

Rest of Europe Spain

7% of all EU deals 446 in EU:

Germany: 88 UK: 62 Israel: 50 Spain: 29 France: 28

6% of all M&A value (€8b)

Telco-driven

Source: tech.eu 25

EUROPEAN CONTEXT Limited impact of Spain’s ‘Ley de emprendedores’

Spanish government approved in 2013 ‘Ley de emprendedores’, an entrepreneur-friendly law to promote startups and the creation of new companies Its impact has been very limited Spanish entrepreneurs and investors continue to face significant challenges:

High taxes at the early stage for founders

Exit tax when expanding and changing residency to a non-EU country

Lack of stock option schemes due to high taxes

High taxes for business angels

Source: tech.eu 26

CONCLUSIONS 2015: A YEAR TO REMEMBER

Record investment numbers & notable exits 2015 was a record year for Spain and Barcelona on various fronts: for the first time ever, Spanish technology companies received investment of more than €500 million, fueled by the participation of a record number of international investors (44 VC firms) and producing notable exits such as Trovit, La Nevera Roja or Akamon. Worldwide category leaders Startups such as Wallapop and Letgo -both based in Barcelona- have become category leaders in the mobile classifieds sector, becoming the two most well funded startups in the world to try to conquer the US market. Scytl, born in 2002 and the most successful spin-off in the technology history of Spain, has also consolidated its position as the leading eGovernment company in the world and plans to IPO on the Nasdaq in 2017. Things can, and should, get better Investment per capita in Spain represents a small fraction compared to other European countries, and so do the number of startup exits or business angels. This, coupled with unfriendly laws for entrepreneurs and investors (exit tax, no stock options and high taxation of business angels’ activity), pose a strong challenge for the development of the country’s technology ecosystem.

27

THANK YOU

28

All of the charts, tables and figures that are included in this report come from publicly available sources. Special thanks to:

METHODOLOGY

29

30