S&P BSE CARBONEX · RobecoSAM uses the Global Industry Classification System ... (GICS ®)...

24

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 1 S&P BSE CARBONEX Methodology July 2014

-

Upload

duongduong -

Category

Documents

-

view

218 -

download

2

Transcript of S&P BSE CARBONEX · RobecoSAM uses the Global Industry Classification System ... (GICS ®)...

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 1

S&P BSE CARBONEX Methodology

July 2014

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 2

Table of Contents

Introduction 4

Partnership 4

Highlights 4

Index Family 5

Eligibility Criteria and Index Construction 6

Index Eligibility and Construction 6

Constituent Weights 6

Index Calculations 7

Index Maintenance 8

Rebalancing 8

Ongoing Maintenance 8

Additions 8

Deletions 8

Constituent Weights 8

Corporate Actions 9

Currency of Calculation 9

Base Date and History Availability 9

Float Adjustment 10

Index Data 11

Total Return Index 11

Index Governance 12

Index Committee 12

Index Policy 13

Announcements 13

Pro-forma Files 13

Holiday Schedule 13

Unscheduled Market Closures 14

Recalculation Policy 14

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 3

Index Dissemination 15

Tickers 15

FTP 15

Web site 15

Appendix I 16

RobecoSAM Industries 16

Appendix II 18

Determining the Carbon Re-Weighting Factors 18

Carbon Adjusted Float Weight 19

Appendix III 20

Determining Float Factors of Companies 20

Float Bands 20

S&P Dow Jones Indices’ Contact Information 21

Index Management 21

Product Management 21

Media Relations 21

Client Services 21

Disclaimer 22

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 4

Introduction

Partnership

On February 19, 2013, S&P Dow Jones Indices and the BSE Ltd. (formerly Bombay Stock Exchange (“BSE”) announced their strategic partnership to calculate, disseminate, and license the widely followed BSE suite of indices.

Highlights

Launched in November 2012, the S&P BSE CARBONEX is designed to provide a cost effective way for equity investors to manage the risks associated with climate change over the long term, by identifying key climate change exposure, sensitivity and responsiveness factors. The UK Foreign & Commonwealth Office, through its Prosperity Fund and British High commission in India, contributed to the cost of development up to the launch of the index.

The index is based on the S&P BSE 100, with the constituent weights modified in accordance with the companies’ relative carbon performance as measured by the level of their greenhouse gas (GHG) emissions and carbon policies. S&P Dow Jones Indices has partnered with RobecoSAM, a specialist in sustainability investing to provide the Carbon Performance Scores and Industry Tilt Factors. Founded in 1995, RobecoSAM is headquartered in Zurich and employs approximately 100 staff. Carbon Performance Scores of Indian companies are calculated by RobecoSAM in the framework of the annual Corporate Sustainability Assessment (CSA) of companies from around the world. The first CSA was undertaken in 1999, with the launch of the original family of the Dow Jones Sustainability Indices, or DJSI. Companies in each of the underlying broad market indices are asked to respond to an extensive industry-specific CSA questionnaire. Not all companies choose to respond to the CSA questionnaire. For all companies in the underlying benchmarks that do not respond to the questionnaires, RobecoSAM completes the CSA questionnaire, to the extent possible, based on publically available information only, in order to ensure that certain minimum representativeness requirements are met. This methodology was created by S&P Dow Jones Indices to achieve the aforementioned objective of measuring the underlying interest of each index governed by this methodology document. Any changes to or deviations from this methodology are made in the sole judgment and discretion of S&P Dow Jones Indices so that the index continues to achieve its objective.

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 5

Index Family

The S&P BSE CARBONEX is part of the S&P BSE sustainability indices. For information on the other S&P BSE thematic indices, please refer to the S&P BSE Indices Methodology document located on our Web site at www.spdji.com.

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 6

Eligibility Criteria and Index Construction

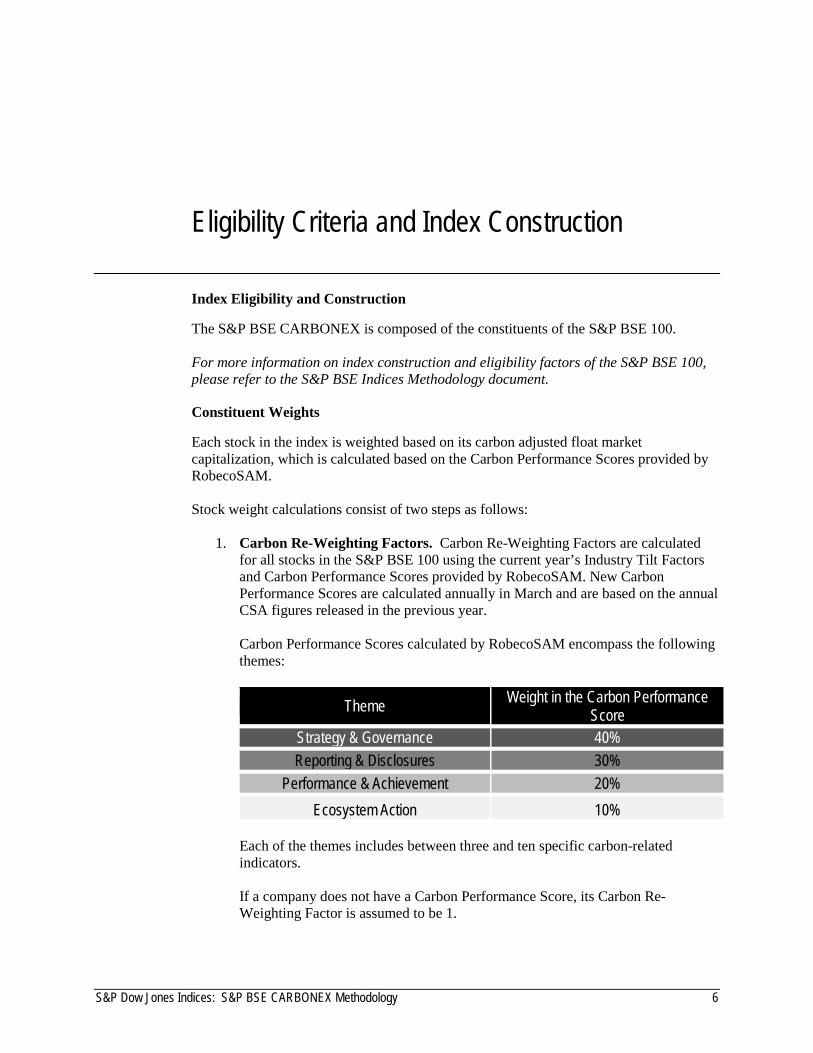

Index Eligibility and Construction

The S&P BSE CARBONEX is composed of the constituents of the S&P BSE 100. For more information on index construction and eligibility factors of the S&P BSE 100, please refer to the S&P BSE Indices Methodology document.

Constituent Weights

Each stock in the index is weighted based on its carbon adjusted float market capitalization, which is calculated based on the Carbon Performance Scores provided by RobecoSAM. Stock weight calculations consist of two steps as follows:

1. Carbon Re-Weighting Factors. Carbon Re-Weighting Factors are calculated for all stocks in the S&P BSE 100 using the current year’s Industry Tilt Factors and Carbon Performance Scores provided by RobecoSAM. New Carbon Performance Scores are calculated annually in March and are based on the annual CSA figures released in the previous year.

Carbon Performance Scores calculated by RobecoSAM encompass the following themes:

Theme Weight in the Carbon Performance Score

Strategy & Governance 40% Reporting & Disclosures 30%

Performance & Achievement 20% Ecosystem Action 10%

Each of the themes includes between three and ten specific carbon-related indicators.

If a company does not have a Carbon Performance Score, its Carbon Re-Weighting Factor is assumed to be 1.

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 7

Industry Tilt Factors are provided by RobecoSAM and calculated to represent each industry’s relative exposure to carbon-related risks and opportunities. They are calculated based on the weights of the carbon-related questions in each overall industry-specific RobecoSAM CSA questionnaire. In the course of the CSA process, companies are assigned to one of the 59 industries defined by RobecoSAM (the “RobecoSAM Industries”). RobecoSAM uses the Global Industry Classification System (GICS®) as its starting point for determining industry classification1. At the industry group and sector levels, the RobecoSAM Industries match the standard GICS® classifications. However, some non-standard aggregations are made at the industry level. Please see Appendix I for a list of RobecoSAM Industries.

Companies in industries with greater exposure to carbon-related risks and opportunities receive a higher Industry Tilt Factor and therefore, a higher weight restatement compared to companies in other industries belonging to the same sector.

2. Carbon Adjusted Float Weights. Once the Carbon Re-Weighting Factors are determined, the float weights of the stocks are tilted based on their Carbon Re-Weighting Factors.

After the float weight tilting, the overall sector exposure is again realigned with that of S&P BSE 100 to arrive at the Carbon Adjusted Float Weight of each constituent stock in the index.

For details on formulas used in steps 1 and 2 above, please refer to Appendix II. Stock weights are adjusted at each semi-annual rebalancing to reflect each constituent’s Carbon Adjusted Float Weight.

Index Calculations

The S&P BSE CARBONEX employs a modified market capitalization weighting scheme. The index is calculated by means of the divisor methodology used in all S&P Dow Jones Indices’ equity indices. For more information on the index calculation methodology, please refer to the Modified Market Capitalization Weighted Indices section of S&P Dow Jones Indices’ Index Mathematics Methodology document.

1 For more information about GICS®, please refer to the Global Industry Classification Standard (GICS®)

Methodology available at www.spdji.com.

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 8

Index Maintenance

Rebalancing

Frequency. Index rebalancing follows that of the S&P BSE 100 and is detailed in the table below. Note: The Effective and Reference dates are after the market close.

Index Frequency Effective Date Reference Date

S&P BSE CARBONEX Semi-annual 3rd Friday of Jun & Dec

Last Trading Day of Apr & Oct

Ongoing Maintenance

The index is reviewed on an ongoing basis to account for corporate events such as mergers, takeovers, delistings or bankruptcies. Changes to index composition and related weight adjustments are made as soon as they are effective. These changes are typically announced two business days prior to the implementation date.

Additions

No companies are added to the index between semi-annual rebalancings. As such, the number of stocks in the index may fall below the targeted constituent count of 100 due to any deletions made between rebalancings.

Deletions

Between semi-annual rebalancings, a company can be deleted from the index due to corporate events such as mergers, acquisitions, takeovers, delistings or bankruptcies.

• Whenever possible, changes in the index’s components are announced at least two business days prior to their implementation date.

• Whenever practicable, S&P Dow Jones Indices uses the closing price for all deletions.

Constituent Weights

Stock weights are adjusted at each semi-annual rebalancing to reflect each constituent’s Carbon Adjusted Float Weight. For further details, please see Eligibility Criteria and Index Construction.

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 9

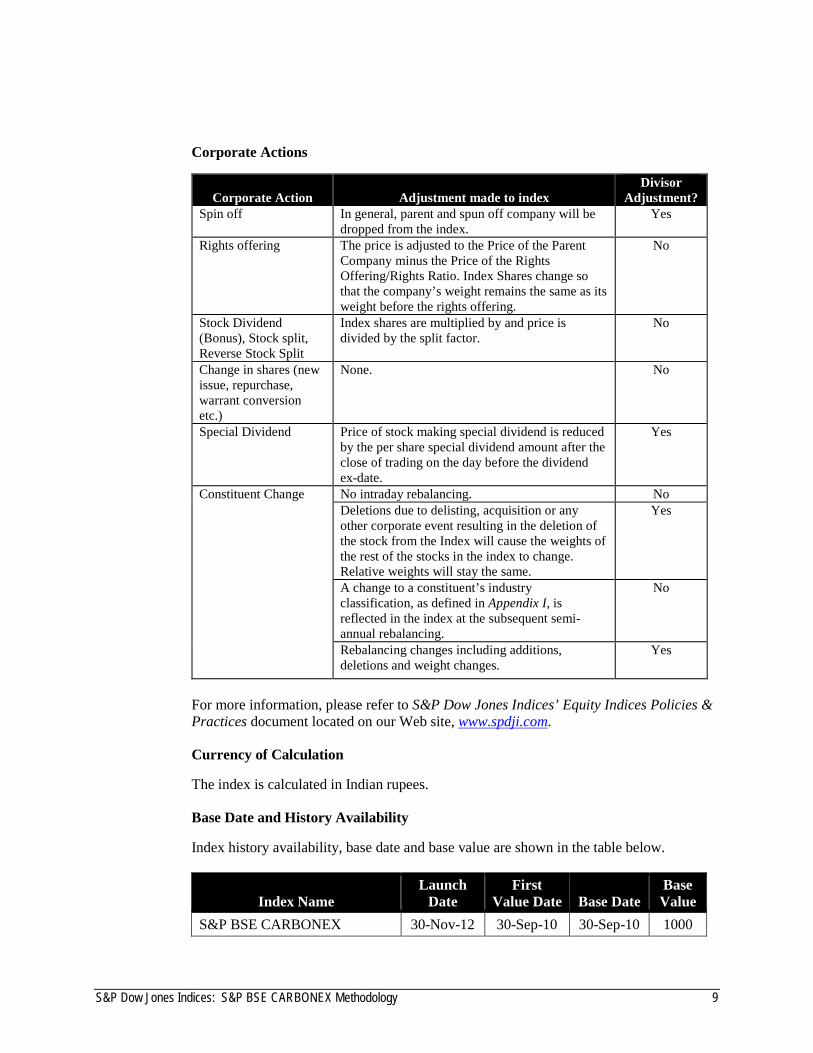

Corporate Actions

Corporate Action Adjustment made to index Divisor

Adjustment? Spin off In general, parent and spun off company will be

dropped from the index. Yes

Rights offering The price is adjusted to the Price of the Parent Company minus the Price of the Rights Offering/Rights Ratio. Index Shares change so that the company’s weight remains the same as its weight before the rights offering.

No

Stock Dividend (Bonus), Stock split, Reverse Stock Split

Index shares are multiplied by and price is divided by the split factor.

No

Change in shares (new issue, repurchase, warrant conversion etc.)

None. No

Special Dividend Price of stock making special dividend is reduced by the per share special dividend amount after the close of trading on the day before the dividend ex-date.

Yes

Constituent Change No intraday rebalancing. No Deletions due to delisting, acquisition or any other corporate event resulting in the deletion of the stock from the Index will cause the weights of the rest of the stocks in the index to change. Relative weights will stay the same.

Yes

A change to a constituent’s industry classification, as defined in Appendix I, is reflected in the index at the subsequent semi-annual rebalancing.

No

Rebalancing changes including additions, deletions and weight changes.

Yes

For more information, please refer to S&P Dow Jones Indices’ Equity Indices Policies & Practices document located on our Web site, www.spdji.com.

Currency of Calculation

The index is calculated in Indian rupees.

Base Date and History Availability

Index history availability, base date and base value are shown in the table below.

Index Name Launch

Date First

Value Date Base Date Base Value

S&P BSE CARBONEX 30-Nov-12 30-Sep-10 30-Sep-10 1000

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 10

Float Adjustment

For detailed information on float adjustment, please refer to Appendix III of this document.

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 11

Index Data

Total Return Index

Total return index is calculated for the S&P BSE CARBONEX, as well as the price return index. Ordinary cash dividends are applied on the ex-date in calculating the total return index. “Special dividends” are dividends greater than 5% of the close price one day prior to the dividend ex-date. Whether a dividend is funded from operating earnings or from other sources of cash does not affect the determination of whether it is ordinary or special. “Special dividends” are treated as corporate actions with offsetting price and divisor adjustments; the total return index reflects both ordinary and special dividends. Total return index reflects the return to an investor where gross dividends are reinvested. Please refer to S&P Dow Jones Indices’ Index Mathematics Methodology for more detail on total and net return index calculations.

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 12

Index Governance

Index Committee

The S&P BSE CARBONEX is maintained by the S&P BSE Index Committee. The Index Committee meets regularly. At each meeting, the Index Committee reviews pending corporate actions that may affect index constituents, statistics comparing the composition of the index to the market, companies that are being considered as candidates for addition to the index, and any significant market events. In addition, the Index Committee may revise index policy covering rules for selecting companies, treatment of dividends, share counts or other matters. S&P Dow Jones Indices considers information about changes to its indices and related matters to be potentially market moving and material. Therefore, all Index Committee discussions are confidential. For information on Quality Assurance and Internal Reviews of Methodology, please refer to S&P Dow Jones Indices’ Equity Indices Policies & Practices document located on our Web site, www.spdji.com.

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 13

Index Policy

Announcements

All index constituents are evaluated daily for data needed to calculate index levels and returns. All events affecting the daily index calculation are typically announced 30 days in advance via the Index Corporate Events report (.SDE), delivered daily via ftp to all clients. Any unusual treatment of a corporate action or short notice of an event may be communicated via email to clients. Index methodology is constantly under review for best practices, and any changes are announced well ahead of time via the Web site and email to all clients.

Pro-forma Files

In addition to the corporate events file (.SDE), S&P Dow Jones Indices provides constituent proforma files each time the index rebalances. The proforma file is typically provided daily five business days in advance of the rebalancing date and contains all constituents and their corresponding weights and index shares effective for the upcoming rebalancing. Since index shares are assigned based on prices one week prior to the rebalancing, the actual weight of each stock at the rebalancing differs from these weights due to market movements. Please visit www.spdji.com for a complete schedule of rebalancing timelines and pro-forma delivery times.

Holiday Schedule

The S&P BSE CARBONEX is calculated on all business days when the BSE is open. A complete holiday schedule for the year is available on the BSE Ltd. Web site at www.bseindia.com.

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 14

Unscheduled Market Closures

In situations where an exchange is forced to close early due to unforeseen events, such as computer or electric power failures, weather conditions or other events, S&P Dow Jones Indices will calculate the closing price of the indices based on (1) the closing prices published by the exchange, or (2) if no closing price is available, the last regular trade reported for each security before the exchange closed. If an exchange fails to open due to unforeseen circumstances, S&P Dow Jones Indices treats this closure as a standard market holiday. The index will use the prior day’s closing prices and shifts any corporate actions to the following business day. If all exchanges fail to open or in other extreme circumstances, S&P Dow Jones Indices may determine not to publish the index for that day. For further information on Unexpected Exchange Closures, please refer to S&P Dow Jones Indices’ Equity Indices Policies & Practices document located on our Web site, www.spdji.com.

Recalculation Policy

S&P Dow Jones Indices reserves the right to recalculate an index under certain limited circumstances. S&P Dow Jones Indices may choose to recalculate and republish an index if it is found to be incorrect or inconsistent within two trading days of the publication of the index level in question for one of the following reasons:

1. Incorrect or revised closing price

2. Missed corporate event

3. Late announcement of a corporate event

4. Incorrect application of corporate action or index methodology Any other restatement or recalculation of an index is only done under extraordinary circumstances to reduce or avoid possible market impact or disruption as solely determined by the Index Committee. For more information on the recalculation policy please refer to S&P Dow Jones Indices’ Equity Indices Policies & Practices document located on our Web site, www.spdji.com. For information on Calculations and Pricing Disruptions, Expert Judgment and Data Hierarchy, please refer to S&P Dow Jones Indices’ Equity Indices Policies & Practices document located on our Web site, www.spdji.com.

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 15

Index Dissemination

Index levels are available through S&P Dow Jones Indices’ Web site at www.spdji.com, major quote vendors (see codes below), numerous investment-oriented Web sites, and various print and electronic media.

Tickers

Index Bloomberg Reuters S&P BSE CARBONEX BSECRBN .BSECRBX

FTP

Daily stock level and index data are available via FTP subscription. For product information, please contact S&P Dow Jones Indices, www.spdji.com/contact-us.

Web site

For further information, please refer to S&P Dow Jones Indices’ Web site at www.spdji.com.

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 16

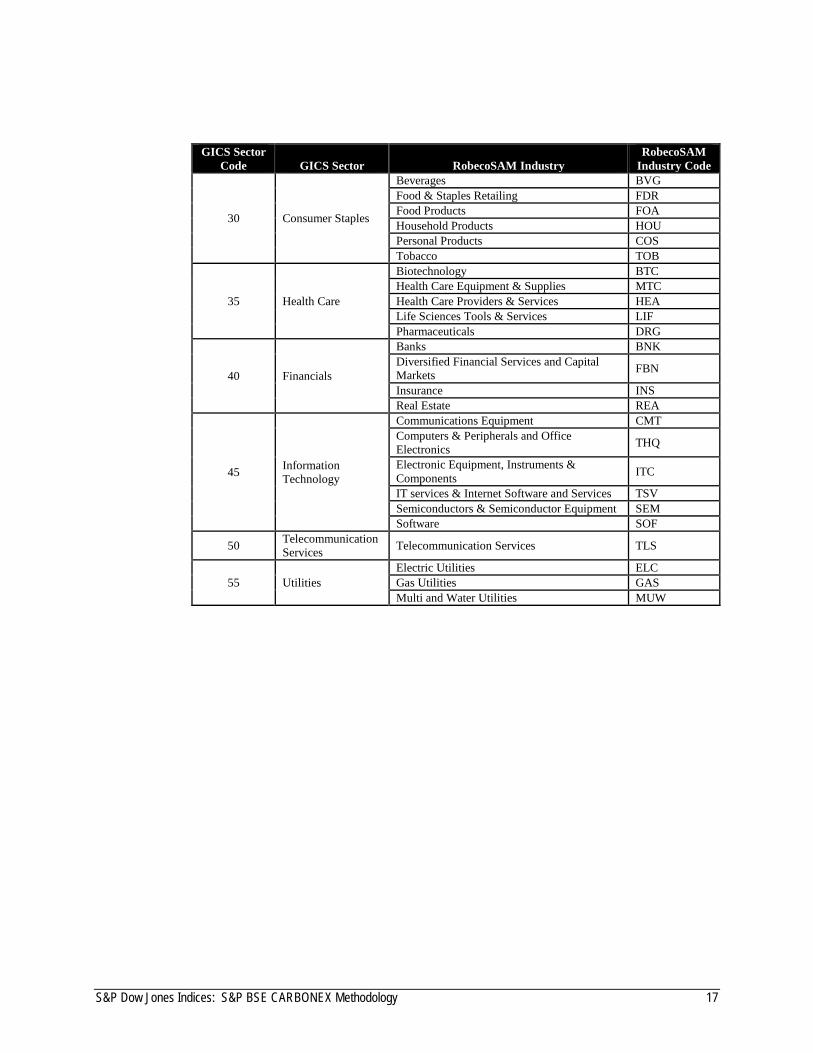

Appendix I

RobecoSAM Industries

Industry Tilt Factors are calculated and specific Corporate Sustainability Assessment Questionnaires are created for the following RobecoSAM Industries:

GICS Sector Code GICS Sector RobecoSAM Industry

RobecoSAM Industry Code

10 Energy

Coal & Consumable Fuels COL Energy Equipment & Services OIE Oil & Gas OIX Oil & Gas Storage & Transportation PIP

15 Materials

Aluminum ALU Chemicals CHM Construction Materials COM Containers & Packaging CTR Metals & Mining MNX Paper & Forest Products FRP Steel STL

20 Industrials

Aerospace & Defense ARO Airlines AIR Building Products BLD Commercial Services & Supplies ICS Construction & Engineering CON Electrical Components & Equipment ELQ Industrial Conglomerates IDD Machinery and Electrical Equipment IEQ Professional Services PRO Trading Companies & Distributors TCD Transportation and Transportation Infrastructure TRA

25 Consumer Discretionary

Auto Components ATX Automobiles AUT Casinos & Gaming CNO Diversified Consumer Services CSV Homebuilding HOM Hotels, Resorts & Cruise Lines TRT Household Durables DHP Leisure Equipment & Products and Consumer Electronics LEG

Media PUB Restaurants & Leisure Facilities REX Retailing RTS Textiles, Apparel & Luxury Goods TEX

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 17

GICS Sector Code GICS Sector RobecoSAM Industry

RobecoSAM Industry Code

30 Consumer Staples

Beverages BVG Food & Staples Retailing FDR Food Products FOA Household Products HOU Personal Products COS Tobacco TOB

35 Health Care

Biotechnology BTC Health Care Equipment & Supplies MTC Health Care Providers & Services HEA Life Sciences Tools & Services LIF Pharmaceuticals DRG

40 Financials

Banks BNK Diversified Financial Services and Capital Markets FBN

Insurance INS Real Estate REA

45 Information Technology

Communications Equipment CMT Computers & Peripherals and Office Electronics THQ

Electronic Equipment, Instruments & Components ITC

IT services & Internet Software and Services TSV Semiconductors & Semiconductor Equipment SEM Software SOF

50 Telecommunication Services Telecommunication Services TLS

55 Utilities Electric Utilities ELC Gas Utilities GAS Multi and Water Utilities MUW

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 18

Appendix II

Determining the Carbon Re-Weighting Factors

1. Sector specific 𝑍 scores are calculated for all index constituents as follows:

𝒁𝒄 =𝑺𝒄 − 𝝁𝒄𝝈𝒄

where:

𝒁𝒄 = Standardized Carbon Performance Score for the company

𝑺𝒄 = Carbon Performance Score for the company provided by RobecoSAM

𝝁𝒄 = Mean of the Carbon Performance Scores for the sector

𝝈𝒄 = Standard deviation of the Carbon Performance Scores for the sector Note: 𝒁𝒄 has a cap of -3 on the negative side and 3 on the positive side. Therefore:

• when 𝒁𝒄 < −𝟑, 𝒁𝒄 = −𝟑

• when 𝒁𝒄 > 𝟑, 𝒁𝒄 = 𝟑

2. Carbon Re-Weighting Factors for all companies in the BSE 100 are calculated as follows:

𝑪𝒇 = 𝟏 +(𝟏 + 𝑰𝒊) × 𝒁𝒄

𝟔

where:

𝑪𝒇 = Carbon Re-Weighting Factor for the company

𝑰𝒊 = Industry Tilt Factor provided by RobecoSAM

𝒁𝒄 = Standardized Carbon Performance Score for the company Note: If a company does not have a score, its 𝑪𝒇 is assumed to be 1.

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 19

Carbon Adjusted Float Weight

1. Tilted weight with respect to the Carbon Re-Weighting Factor is calculated as follows:

𝑻𝒘 = 𝑭𝒘 × 𝑪𝒇

where:

𝑻𝒘 = Tilted weight for the company

𝑭𝒘 = Float Market Cap weight for the company

𝑪𝒇 = Carbon Re-Weighting Factor for the company

2. Realignment of the overall sector exposure to that of the S&P BSE 100 is calculated as follows:

𝑪𝒘 = 𝑻𝒘𝑻𝒘𝒔

× 𝑭𝒘𝒔

where:

𝑪𝒘 = Carbon Adjusted Float Weight for the company

𝑻𝒘 = Tilted weight for the company

𝑭𝒘 = Float Market Cap weight for the company

𝑻𝒘𝒔 = Sum of all 𝑻𝒘 in the sector the company belongs to

𝑭𝒘𝒔 = Sum of all 𝑭𝒘 in the sector the company belongs to

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 20

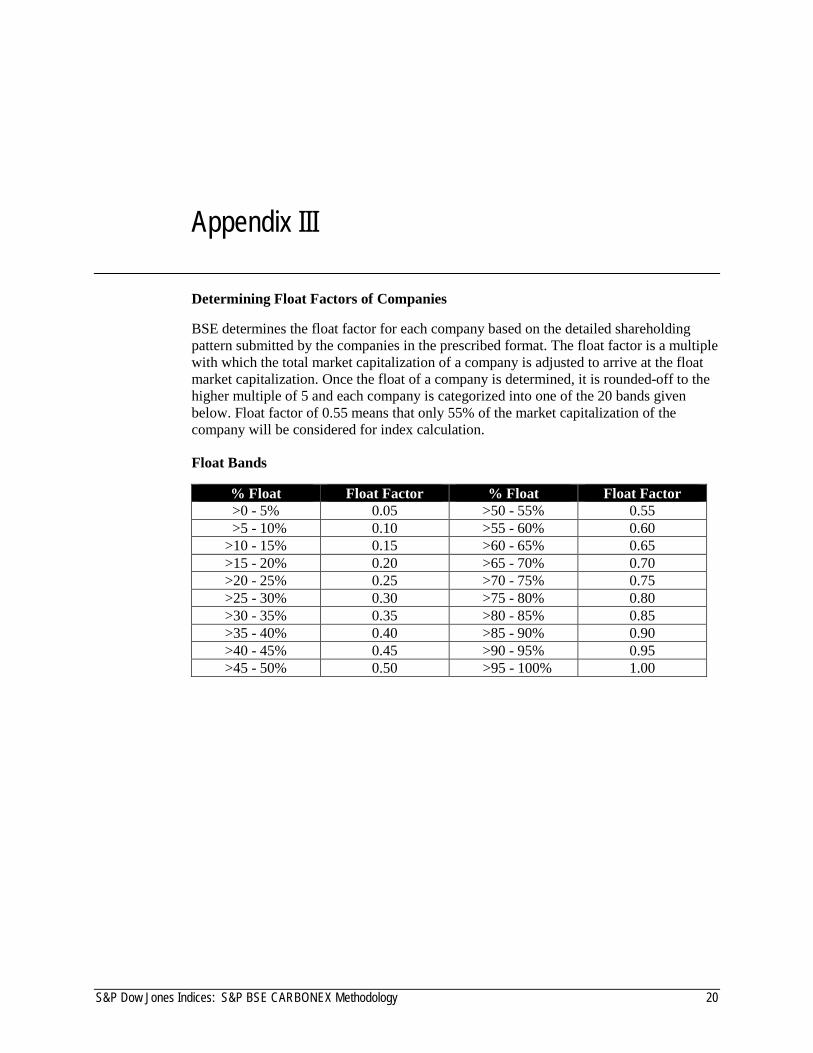

Appendix III

Determining Float Factors of Companies

BSE determines the float factor for each company based on the detailed shareholding pattern submitted by the companies in the prescribed format. The float factor is a multiple with which the total market capitalization of a company is adjusted to arrive at the float market capitalization. Once the float of a company is determined, it is rounded-off to the higher multiple of 5 and each company is categorized into one of the 20 bands given below. Float factor of 0.55 means that only 55% of the market capitalization of the company will be considered for index calculation.

Float Bands

% Float Float Factor % Float Float Factor >0 - 5% 0.05 >50 - 55% 0.55

>5 - 10% 0.10 >55 - 60% 0.60 >10 - 15% 0.15 >60 - 65% 0.65 >15 - 20% 0.20 >65 - 70% 0.70 >20 - 25% 0.25 >70 - 75% 0.75 >25 - 30% 0.30 >75 - 80% 0.80 >30 - 35% 0.35 >80 - 85% 0.85 >35 - 40% 0.40 >85 - 90% 0.90 >40 - 45% 0.45 >90 - 95% 0.95 >45 - 50% 0.50 >95 - 100% 1.00

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 21

S&P Dow Jones Indices’ Contact Information

Index Management

David M. Blitzer, Ph.D. – Managing Director & Chairman of the Index Committee [email protected] +1.212.438.3907 Khushro Bulsara – Head of Listing Compliance & Legal [email protected] +91.22.2272.8241 Jitendra Gulabani – Index Manager [email protected] +91.22.2272.5217

Product Management

Arunkumar Dolas [email protected] +91.22.2272.5211 Mahavir Kaswa [email protected] +91.22.2272.5206

Media Relations

David Guarino – Communications [email protected] +1.212.438.1471

Client Services

[email protected] Beijing +86.10.6569.2770 Dubai +971.4.371.7131 Hong Kong +852.2532.8000 London +44.20.7176.8888 New York +1.212.438.2046 or +1.877.325.5415 Sydney +61.2.9255.9802 Tokyo +81.3.4550.8564

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 22

Disclaimer

© Asia Index Private Limited 2013. All rights reserved. The S&P BSE Indices (the “Indices”) are published by Asia Index Private Limited (“AIPL”), which is a joint venture among affiliates of S&P Dow Jones Indices LLC (“SPDJI”) and BSE Limited (“BSE”). Standard & Poor’s® and S&P® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”) and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). BSE® and SENSEX® are registered trademarks of BSE. These trademarks have been licensed to AIPL. Redistribution, reproduction and/or photocopying in whole or in part are prohibited without written permission. This document does not constitute an offer of services in jurisdictions where AIPL, BSE, S&P Dow Jones Indices LLC or their respective affiliates (collectively “AIPL Companies”) do not have the necessary licenses. All information provided by AIPL Companies is impersonal and not tailored to the needs of any person, entity or group of persons. AIPL Companies receive compensation in connection with licensing its indices to third parties. Past performance of an index is not a guarantee of future results. It is not possible to invest directly in an index. Exposure to an asset class represented by an index is available through investable instruments based on that index. AIPL Companies do not sponsor, endorse, sell, promote or manage any investment fund or other investment vehicle that is offered by third parties and that seeks to provide an investment return based on the performance of any index. AIPL Companies make no assurance that investment products based on the index will accurately track index performance or provide positive investment returns. AIPL and S&P Dow Jones Indices LLC are not investment advisors, and the AIPL Companies make no representation regarding the advisability of investing in any such investment fund or other investment vehicle. A decision to invest in any such investment fund or other investment vehicle should not be made in reliance on any of the statements set forth in this document. Prospective investors are advised to make an investment in any such fund or other vehicle only after carefully considering the risks associated with investing in such funds, as detailed in an offering memorandum or similar document that is prepared by or on behalf of the issuer of the investment fund or other vehicle. Inclusion of a security within an index is not a recommendation by the AIPL Companies to buy, sell, or hold such security, nor is it considered to be investment advice. Closing prices for S&P BSE Indices are calculated by AIPL or its agent based on the closing price of the individual constituents of the index as set by their primary exchange. Closing prices are received by AIPL from the BSE. Real-time intraday prices are calculated similarly without a second verification.

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 23

These materials have been prepared solely for informational purposes based upon information generally available to the public from sources believed to be reliable. No content contained in these materials (including index data, ratings, credit-related analyses and data, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse-engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of AIPL. The Content shall not be used for any unlawful or unauthorized purposes. AIPL and its third-party data providers and licensors and the other AIPL Companies (collectively “AIPL Parties”) do not guarantee the accuracy, completeness, timeliness or availability of the Content. The AIPL Parties are not responsible for any errors or omissions, regardless of the cause, for the results obtained from the use of the Content. THE CONTENT IS PROVIDED ON AN “AS IS” BASIS. THE AIPL PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT’S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall the AIPL Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs) in connection with any use of the Content even if advised of the possibility of such damages. Credit-related and other analyses, including ratings, research and valuations are generally provided by affiliates of S&P Dow Jones Indices LLC, including but not limited to Standard & Poor’s Financial Services LLC and Capital IQ, Inc. Such analyses and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. Any opinion, analyses and rating acknowledgement decisions are not recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. AIPL does not assume any obligation to update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. AIPL and S&P Dow Jones Indices LLC does not act as a fiduciary or an investment advisor. AIPL or its agent has obtained information from sources they believe to be reliable, AIPL does not perform an audit or undertake any duty of due diligence or independent verification of any information it receives. To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P Ratings Services reserves the right to assign, withdraw or suspend such acknowledgement at any time and in its sole discretion. The AIPL Companies, including S&P Ratings Services, disclaim any duty whatsoever arising out of the assignment, withdrawal or suspension of an acknowledgement as well as any liability for any damage alleged to have been suffered on account thereof.

S&P Dow Jones Indices: S&P BSE CARBONEX Methodology 24

Affiliates of S&P Dow Jones Indices LLC may receive compensation for its ratings and certain credit-related analyses, normally from issuers or underwriters of securities or from obligors. Such affiliates of S&P Dow Jones Indices LLC reserve the right to disseminate its opinions and analyses. Public ratings and analyses from S&P Ratings Services are made available on its Web sites, www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription), and may be distributed through other means, including via S&P Rating Services publications and third-party redistributors. Additional information about our ratings fees is available at www.standardandpoors.com/usratingsfees. AIPL and/or its agent keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of AIPL and/or its agent may have information that is not available to other business units. AIPL and its agent have established policies and procedures to maintain the confidentiality of certain non-public information received in connection with each analytical process. In addition, AIPL and/or its agent provides a wide range of services to, or relating to, many organizations, including issuers of securities, investment advisers, broker-dealers, investment banks, other financial institutions and financial intermediaries, and accordingly may receive fees or other economic benefits from those organizations, including organizations whose securities or services they may recommend, rate, include in model portfolios, evaluate or otherwise address. The Global Industry Classification Standard (GICS®) was developed by and is the exclusive property and a trademark of Standard & Poor’s and MSCI. Neither MSCI, Standard & Poor’s nor any other party involved in making or compiling any GICS classifications makes any express or implied warranties or representations with respect to such standard or classification (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such standard or classification. Without limiting any of the foregoing, in no event shall MSCI, Standard & Poor’s, any of their affiliates or any third party involved in making or compiling any GICS classifications have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. Sustainability scores as well as industry tilt factors used in the calculation of the S&P BSE CARBONEX are provided by RobecoSAM AG (“RobecoSAM”).