SOVEREIGN RATING MODEL - Piraeus Bank · To accomplish the above objective we needed to develop a...

35

SOVEREIGN RATING MODEL: GREEK SOVEREIGN RATING WORSE THAN WE DESERVE FEBRUARY 2017 Ilias Lekkos Dimitria Rotsika Haris Giannakidis ECONOMIC RESEARCH & INVESTMENT STRATEGY

Transcript of SOVEREIGN RATING MODEL - Piraeus Bank · To accomplish the above objective we needed to develop a...

SOVEREIGN RATING MODEL:

GREEK SOVEREIGN RATING WORSE THAN WE DESERVE

FEBRUARY 2017

Ilias Lekkos

Dimitria Rotsika

Haris Giannakidis

ECONOMIC RESEARCH & INVESTMENT STRATEGY

CONTENTS

2

Introduction

Aim of the Study & Conclusion

Sovereign Ratings Analysis

Greek Credit Rating

Appendix I: Methodology

Appendix II: Factor-Driven Credit Rating Decisions vs. Actual

Full Sample

3

INTRODUCTION

INTRODUCTION

4

One of the main factors exerting –one could even argue excessive- influence on the decisions andconsiderations of both policy makers and market participants is the sovereign rating assigned by themain rating agencies to each economy.

The significance of sovereign ratings stems from the influence they exert on the ability of eachgovernment to issue debt on local and global bond markets as well as on the pricing of this debt.

Furthermore, sovereign ratings in most cases impose a ceiling on the ratings of all financial and non-financial corporates, thus affecting both the cost of funding and the cost of capital of the entire economy.

The profound effect of sovereign credit ratings on economic activity is all too well known in the case ofGreece, where the downgrade of the Hellenic Republic to below investment grade led to the “financialisolation” of the Greek state from the global financial system.

Yet, given that the Greek economy stands once again on the cusp of recovery and the Greek bankingsystem is confident and robust enough to start planning forward for the upcoming three to five years,the rating outlook of the Greek sovereign debt is coming back to the fore with a vengeance.

For that reason, we have developed a sovereign rating model that allows us to examine and forecast thecredit rating of the Hellenic Republic – as well as the sovereign rating of a large number of othereconomies - under various macroeconomic scenarios in an objective and transparent way.

AIM OF THE STUDY

5

As we have already stated, the ultimate objective of this study is to explain and forecast the credit rating ofthe Greek Sovereign. To accomplish the above objective we needed to develop a fully-fledged sovereignrating model able to describe the sovereign ratings of more than 120 countries. The main features of ourmodel are:

Objectivity: contrary to most rating agencies that base their ratings on both quantitative and qualitative criteria(and delegate the final ratings decision to “Rating Committees”), we used only publicly available data andindicators as inputs to our model.

Sensitivity: most agencies pride themselves on the “stability” of their ratings. Instead, we believe that ratingsshould change when data change. For that reason, we used cross-sectional data (instead of pooled panel data)to allow our ratings to vary at each particular point in time.

Non-recursiveness: one way to improve the in-sample performance of the model is to include a laggeddependent variable (in our case past credit ratings) as an explanatory factor. We chose not to go down this roadsince we desired to identify a pure relationship between macro-factors and ratings.

SUMMARY OF RESULTS

6

The main conclusion of our research is that Greece’s actual rating was out of step with macroeconomicfundamentals throughout the period we examine.

In the pre-crisis period, rating agencies over-rated Greece perhaps taking into consideration an implicit“positive” premium from Greece’s participation in a strong monetary union such as the EuroArea, its robustbanking system and a history of a strong economic performance. This translated into a rating in the Single-A rating band as opposed to our fundamentals-based rating assessment in the Baa rating band.

This “premium” turned negative as the crisis broke out. As a result, Greece is now being penalised beyondfundamentals. This penalty is carried over into the future depriving Greece of a rating upgrade into thesingle-B rating band. Finally, we run a sensitivity analysis where we examined the evolution of Greece’ssovereign rating under both an adverse and a positive macro scenario for 2016 – 2017.

The findings revealed that the size of the “negative Premium” currently embedded in Greece’s rating is ofsuch a magnitude that Greece deserves an upgrade to the single-B band even under the pessimist'sassumption incorporated in the adverse scenario.

7

SOVEREIGN RATINGS ANALYSIS

SOVEREIGN RATINGS: DEFINITION

8

In principle sovereign ratings (like any other form of credit rating) fall in one of two categories:

1. The ones that try to capture the relative likelihood of a borrower defaulting on itsobligations.

2. The ones that try to reflect not only the probability of a default, but also the relative loss inthe event of default.

In our case, we focus on the second type of sovereign ratings (such as Moody’s) because we believe that –given the PSI experience- it is the assessment of total loss that is relevant for the rating of Greek sovereigndebt and not just the probability of default, which could occur for purely technical reasons and withoutany material loss to bondholders.

SOVEREIGN RATINGS: DESCRIPTION

9

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

Analytical Rating Grouped Rating Band Indicates

Aaa Aaa Highest quality with minimal risk.

Aa1

Aa High quality, subject to very low default risk.Aa2

Aa3

A1

A Upper-medium grade, subject to low credit risk.A2

A3

Baa1

BaaMedium-grade, moderate credit risk, may have

speculative characteristics.Baa2

Baa3

Ba1

Ba Substantial credit risk, have speculative characteristics.Ba2

Ba3

B1

B High credit risk, considered speculative.B2

B3

Caa1

Caa Very high credit risk, poor standing.Caa2

Caa3

Ca CaHighly speculative. Likely in or very near default with

some prospect of recovery of principal or interest.

C CLowest rated class of bonds. Typically in default with

little prospect for recovery of principal or interest.

SOVEREIGN RATINGS: RATINGS EVOLUTION

10

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

Moody’s Sovereign Ratings 2006-16

0

10

20

30

40

C Ca Caa B Ba Baa A Aa Aaa

Fre

qu

en

cy

2006

2016

o In the past ten years we witnessed important fluctuations in the sovereign

rating scores with a downward shift towards the lower end of the rating

distribution. In 2006, for example, only 15% of the total number of

countries examined had been rated by Moody’s in the B rating band.

However, in 2016 the percentage of countries rated in the same rating

band had doubled. Interestingly, the very low rating band Caa, which

stands just one step before the characterization “very near default”,

increased substantially in absolute terms from four countries in 2006 to

eight in 2016.

o On the other hand, rating scores in the upper bands of the rating

distribution declined by half in 2016 in comparison to their sovereign

ratings ten years ago. In particular, the percentage of countries rated in

the Aaa and A rating bands, which in 2006 was 19% and 24% respectively,

declined in 2016 by ten percentage points.

o The severity of the economic events after 2007-2008 and the emphasis

given to debt sustainability and fiscal prudence had an important impact

on rating decisions. Specifically, from a total of 124 countries, only 14%

were upgraded to a higher rating while 31% were downgraded.

Furthermore, the ratio of downgrades/upgrades differed with respect to

geographic regions. For example, only one out of 38 (3%) European

countries was upgraded compared to non-European regions where this

number was 13 out of 86 (15%). On the contrary, the percentage of

downgrades in Europe reached 42% while in non-European countries it

was 18%, i.e. less than half.

Sovereign Rating Revisions in a Decade

19

16

1

38

16

13

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

neutral downgrade upgrade

Europe Non-Europe

55%31%

14%

neutral

downgrade

upgrade

SOVEREIGN RATINGS: METHODOLOGY

11

Rating decisions are initiated by the implementation of three steps:

i) data collection and aggregation,

ii) creation of a scoring system and

iii) the rating decision

The factors that drive Moody’s rating procedure are identified as:

i) Economic Strength

ii) Institutional Strength

iii) Fiscal Strength

iv) Event Risk, which represents the sensitivity of each country’s economy to unanticipatedevents such as market crashes, political uncertainty or geopolitical risks.

In particular, the publicly available methodology of Moody’s is based on 31 macroeconomic and survey-based indicators which are aggregated into four broad indicators or factors. We follow the same procedurewith slight modifications in the variable construction process whenever data are not available.

12

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

SOVEREIGN RATINGS: METHODOLOGY

Rating

Economic

Strength

Institu-

tional

Strength

Event

Risk

Fiscal

Strength

Growth Dynamics

Average Real GDP Growth, Volatility of

Real GDP Growth, WEF Competitiveness

Index

Scale of Economy Nominal GDP ($bn)

National Income GDP/Capita (PPP,$)

Adjustment FactorCredit Boom (Credit Growth/NGDP

Growth)(t-2-->t) >2

Political Risk

Domestic Political Risk (Voice &

Accountability, GDP per capita),

Geopolitical Risk (Global Conflict Risk

Index)

Government

Liquidity Risk

Fundamental Metrics (Government

External Debt to Government Debt)

Banking Sector Risk

Banking System Size (Total Bank Assets to

GDP), Funding Vulnerabilities (Gross Loans

to Deposits)

External

Vulnerability Risk

(Current Account Balance & FDI) to GDP,

External Vulnerability Indicator t+2, Net

International Investment Position to GDP

Debt BurdenGeneral Govt. Debt to GDP, General Govt.

Debt to Revenues

Debt Affordability

General Govt. Interest Payments to

Revenues, General Govt. Interest Payments

to GDP

Adjustment Factor

Debt to GDP Trend (t-4-->t+1), General

Govt. Foreign Currency Debt to General

Govt. Debt

Institutional Framework & Effectiveness

Government Effectiveness, Rule of Law,

Control of Corruption

Policy & Credibility Inflation Level, Inflation volatility

ECONOMIC STRENGTH FACTOR

o The economic factor is constructed by aggregating five indicators of

economic activity representing three aspects of economic activity, namely

growth dynamics, economy’s size and income per individual. Following that,

the aforementioned five economic indicators are adjusted to account for the

diversification in the country’s economic activities as well as to the degree of

growth that is generated by credit growth.

o The standardised values of the economic factor in 2015 for the 124 countries

rated by Moody’s ranged between -4.81 standard deviations (std) for

Azerbaijan and 28.3 std for the United States because of its relatively large

size indicated by its Nominal GDP in US dollars.

o In terms of economic strength, Greece stands at -1.13 std due to its very low

average real GDP growth rate over the past seven years. Clearly, the debt crisis

in Europe has significantly affected the economic potential for several

countries in the Eurozone. However, after 2012 there are signs of recovery for

all these countries, albeit with great differences on the speed of returning to a

positive growth environment.

13

Distribution of Economic Strength Factor: 2015

Economic Strength Comparisons

0

5

10

15

20

25

30

35

40

-4.8

-2.6

-0.4

1.8

4.0

6.2

8.4

10

.6

12

.8

15

.1

17

.3

19

.5

21

.7

23

.9

26

.1

28

.3

Fre

qu

en

cy

US

Greece

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

-3

-2

-1

0

1

2

3

Greece Cyprus Ireland Portugal Spain

Economic Strength

2007 2009 2012 2015

Economic Growth

Volatility of GDP

Competitiveness Index

Nominal GDP

Per Capita GDP

Credit Expansion

FISCAL STRENGTH FACTOR

14

Fiscal Strength Comparisons

Distribution of Fiscal Strength Factor: 2015

0

2

4

6

8

10

12

14

16

-7.0

-6.3

-5.7

-5.0

-4.3

-3.6

-2.9

-2.2

-1.6

-0.9

-0.2

0.5

1.2

1.8

2.5

3.2

Fre

qu

en

cy

Lebanon

Greece

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

-5

-4

-3

-2

-1

0

1

2

3

Greece Cyprus Ireland Portugal Spain

Fiscal Strength

2007 2009 2012 2015

Debt to GDP

Debt to GDP Trend

Debt to Revenues

Interest Payments to Revenues

Interest Payments to GDP

o Similarly, the fiscal factor is based on five ratio indicators related to

public fiscal position and more specifically to the collection of

revenues, the interest paid on government debt and most importantly

to the government debt level. We can therefore conclude that the fiscal

strength factor provides a picture of the debt burden and the ability of

a country’s government to repay it.

o The standardised values of the fiscal factor in 2015 ranged between -7

std for Lebanon and 3.2 std for Hong Kong. Despite the fact that

Greece was under a significant fiscal adjustment, its fiscal strength lies

at the lower left region of the distribution at -2.56 std. This relates

mostly to its very high debt level rather than to the interest paid or the

revenue collection. For example, in Greece the debt/GDP ratio stands at

5.83 std compared to the other countries in our extensive sample.

o Clearly the picture is pretty much the same in the countries that were in

a programme during the Eurozone debt crisis. Typically the fiscal

strength factor plummeted by more than one std in the period 2007-

2012 and there are no signs of a noteworthy improvement during the

more recent years with the exception of Ireland.

INSTITUTIONAL STRENGTH FACTOR

o Perhaps the most important, but at the same time the most overlooked,

aspect in economic analysis is a country’s ability to function properly. The

institutional strength factor relates to two inflation-based variables that

correspond to policy effectiveness and three World Bank indicators that

represent the government efficiency and the level of corruption in a country.

o The standardised values of the institutional indicator in 2015 ranged between

-8.1 std for the Republic of Congo and 5.4 std for Singapore. In Greece, the

institutional strength stands in the middle of the factor’s distribution.

Nevertheless, it is important to note that the institutional strength decreased

from two std in 2007 to less than 0.5 std in 2015 in sharp contrast to the rest

of the Eurozone members.

o With respect to the World Bank’s indicators, the Greek debt crisis resulted in

severe instability in the political stage. As a result, over the 7-year period since

2007, government effectiveness deteriorated by 50%, law enforcement and

law acceptance by the citizens declined by 72% and the control of corruption

plummeted by 150%.

15

Distribution of Institutional Strength Factor: 2015

Distribution of Event Risk Factor: 2015

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

0

2

4

6

8

10

12

14

16

-8.1

-7.2

-6.3

-5.4

-4.5

-3.6

-2.7

-1.8

-0.9

0.0

0.9

1.8

2.7

3.6

4.5

5.4

Fre

qu

en

cy

Congo

Greece

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Greece Cyprus Ireland Portugal Spain

Institutional Strength

2007 2009 2012 2015

Government Effectiveness

Rule of Law

Control of Corruption

Inflation Level

Inflation Volatility

EVENT RISK FACTOR

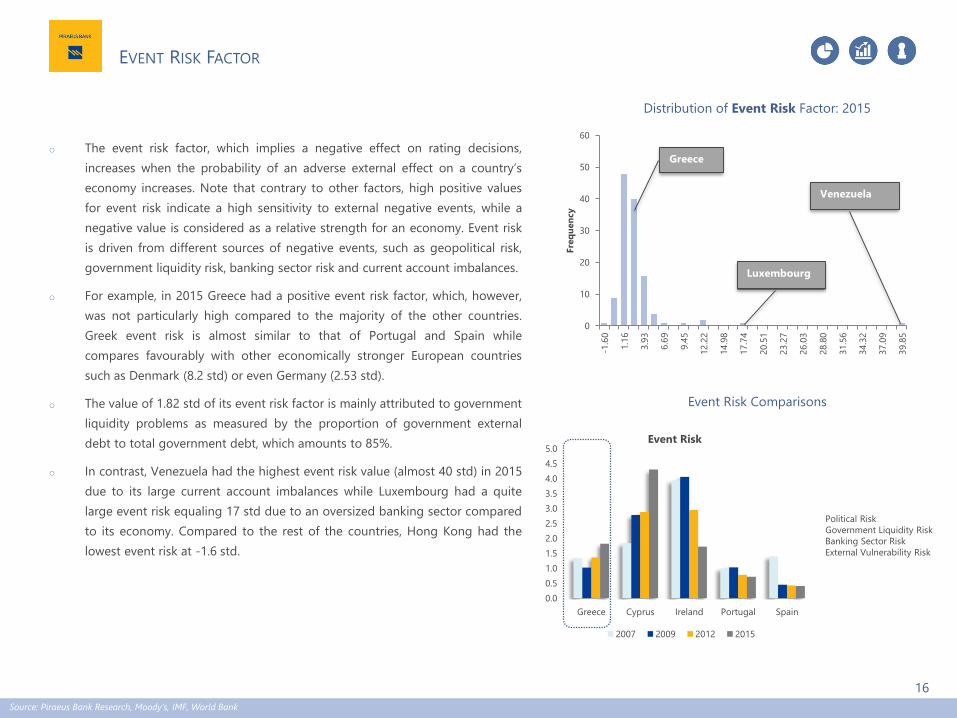

o The event risk factor, which implies a negative effect on rating decisions,

increases when the probability of an adverse external effect on a country’s

economy increases. Note that contrary to other factors, high positive values

for event risk indicate a high sensitivity to external negative events, while a

negative value is considered as a relative strength for an economy. Event risk

is driven from different sources of negative events, such as geopolitical risk,

government liquidity risk, banking sector risk and current account imbalances.

o For example, in 2015 Greece had a positive event risk factor, which, however,

was not particularly high compared to the majority of the other countries.

Greek event risk is almost similar to that of Portugal and Spain while

compares favourably with other economically stronger European countries

such as Denmark (8.2 std) or even Germany (2.53 std).

o The value of 1.82 std of its event risk factor is mainly attributed to government

liquidity problems as measured by the proportion of government external

debt to total government debt, which amounts to 85%.

o In contrast, Venezuela had the highest event risk value (almost 40 std) in 2015

due to its large current account imbalances while Luxembourg had a quite

large event risk equaling 17 std due to an oversized banking sector compared

to its economy. Compared to the rest of the countries, Hong Kong had the

lowest event risk at -1.6 std.

16

Distribution of Event Risk Factor: 2015

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

0

10

20

30

40

50

60

-1.6

0

1.1

6

3.9

3

6.6

9

9.4

5

12

.22

14

.98

17

.74

20

.51

23

.27

26

.03

28

.80

31

.56

34

.32

37

.09

39

.85

Fre

qu

en

cy

Luxembourg

Greece

Venezuela

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Greece Cyprus Ireland Portugal Spain

Event Risk

2007 2009 2012 2015

Political Risk

Government Liquidity Risk

Banking Sector Risk

External Vulnerability Risk

Event Risk Comparisons

DATA DESCRIPTION

17

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

# of Countries 124

# of Years 11 years

Time Span 2007-2017

Outliers

To facilitate the statistical properties of our scoring

model we truncate outliers in each of the four

factor variables. As a result, we avoid extreme

values that distort the statistical analysis. The

maximum and minimum values used for

truncation purposes are decided on a factor by

factor case and are affected by qualitative and

judgmental criteria.

Standardisations

We standardise each variable with a mean and

standard deviation that are consistent with the

rating system of Moody’s. In particular for the

mean we take the average for Moody’s middle (or

‘M’) rating band. Similarly for the standard

deviation we get the average range of the 15

notch rating system and divide it by 0.4 which is

the value (in std’s) of each notch value change

Data SourcesMoody’s Rating Agency, International Monetary

Fund, World Bank.

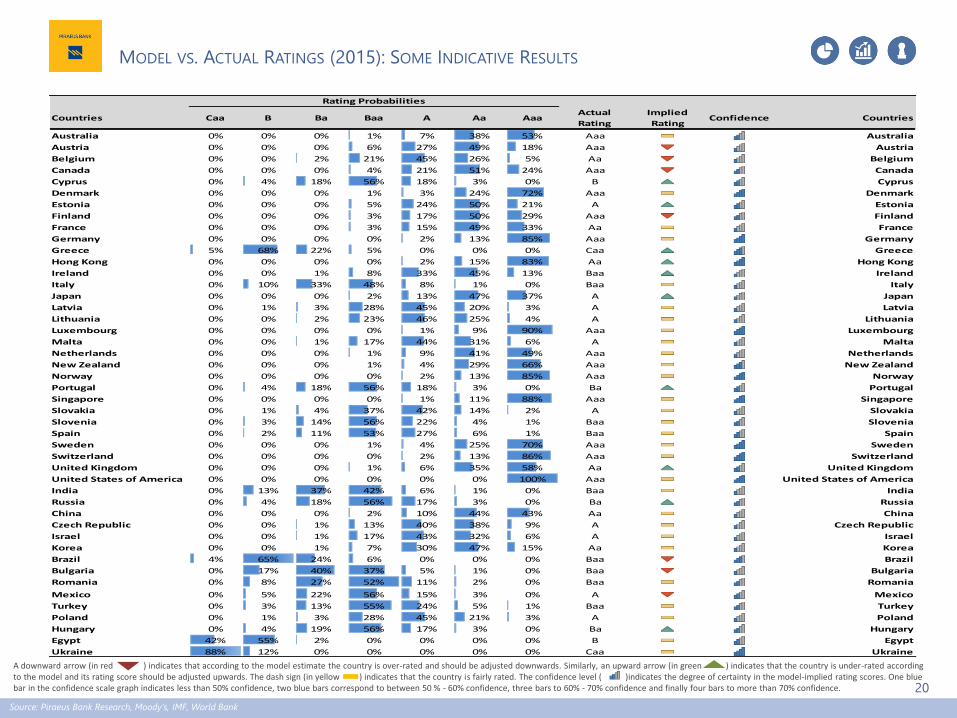

STATISTICAL ANALYSIS: MULTINOMIAL RATING SCORE MODELS

o Our main goal is to extract implied ratings from actual agency

rating decisions and more specifically those made by Moody’s.

One helpful statistical tool for this task is the multinomial ordered

logit models (in the appendix we provide a thorough explanation

on how these models work), which are considered useful when

the variable of interest takes discrete values. The specific model

can be used to test which of the underlying factors are

statistically relevant in explaining rating decisions as well as to

enable projecting the probability distribution of rating decisions

in a forward-looking context.

o The results presented in the table are based on the model

estimates for 2015. We should keep in mind that the

interpretation of the parameter estimates for non-linear

regression models is not straightforward as in more standard

models. However, if the coefficient sign is positive, the higher the

value of the corresponding factor the more likely it is for a

country to be assigned the highest rating band (i.e. Aaa), while

the opposite holds for a negative coefficient value.

o According to our methodology, the four factors that are used to

explain credit ratings are jointly statistically significant and

consequently their use is considered helpful in explaining and

projecting rating decisions. On the other hand, the standalone

coefficient of the event risk factor (i.e. domestic political

uncertainty, liquidity risk, banking sector strength and current

account imbalances) is not statistically significant. This might be

explained by the fact that these events occur rather infrequently

and as a result the impact of this factor is difficult to be reflected

on the rating decisions.

18

Multinomial Logit Estimates & Performance

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

Variable coefficient z-statistic p-value

Economic Strength 0.43 3.04 0.00

Institutional Strength 0.95 6.63 0.00

Fiscal strength 1.06 6.29 0.00

Event Risk 0.08 0.56 0.58

Pseudo-R² 0.44

Overall Developed Developing

Hit ratio 57% 61% 56%

Over Rated 21% 13% 24%

Under Rated 22% 26% 20%

o The performance of the model estimates is better assessed by

the hit ratio of the implied versus the actual rating scores. The

hit ratio indicates the percentage of implied ratings that are in

line with the actual ratings. In general, the multinomial logit

model performs relatively well since more than 50% of the

implied ratings were the same with the actual ratings.

Furthermore, the hit ratio of developed countries is higher than

the hit ratio of developing countries indicating the importance

of other factors in the rating decision process for emerging

market economies. Interestingly, according to our findings

based on our model’s estimates for 2015, it is more likely for a

developed country to be under-rated rather than over-rated.

MULTINOMIAL RATING SCORE MODELS

o It is important to note that we can perform comparisons of each

factor’s impact on the likely outcome of a rating decision. We showed

previously that not all factors are of equal importance from the credit

rating agencies’ perspective. In particular, according to the coefficient

of our statistical model the most important factors are those that

measure economic, institutional and fiscal strength.

o Interestingly, economic strength is only half as important as

institutional and fiscal strength. For example, the marginal effect (i.e.

neglecting the impact from all other factors) for Greece’s Baa

probability from an increase in the economic factor by 1 standard

deviation is 5%, while the corresponding effect of a similar increase in

the fiscal factor is 18%. A probable explanation can be the high debt

to GDP levels in the Eurozone and in developed economies as well as

the substantial impact of political uncertainty and governance

indicators on the soundness of fiscal policies management in a

country.

19

Marginal Factor Effects

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Caa B Baa

Economic Fiscal Institutional

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

20

MODEL VS. ACTUAL RATINGS (2015): SOME INDICATIVE RESULTS

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

A downward arrow (in red ) indicates that according to the model estimate the country is over-rated and should be adjusted downwards. Similarly, an upward arrow (in green ) indicates that the country is under-rated according to the model and its rating score should be adjusted upwards. The dash sign (in yellow ) indicates that the country is fairly rated. The confidence level ( )indicates the degree of certainty in the model-implied rating scores. One blue bar in the confidence scale graph indicates less than 50% confidence, two blue bars correspond to between 50 % - 60% confidence, three bars to 60% - 70% confidence and finally four bars to more than 70% confidence.

Countries Caa B Ba Baa A Aa AaaActual

Rating

Implied

RatingConfidence Countries

Australia 0% 0% 0% 1% 7% 38% 53% Aaa Australia

Austria 0% 0% 0% 6% 27% 49% 18% Aaa Austria

Belgium 0% 0% 2% 21% 45% 26% 5% Aa Belgium

Canada 0% 0% 0% 4% 21% 51% 24% Aaa Canada

Cyprus 0% 4% 18% 56% 18% 3% 0% B Cyprus

Denmark 0% 0% 0% 1% 3% 24% 72% Aaa Denmark

Estonia 0% 0% 0% 5% 24% 50% 21% A Estonia

Finland 0% 0% 0% 3% 17% 50% 29% Aaa Finland

France 0% 0% 0% 3% 15% 49% 33% Aa France

Germany 0% 0% 0% 0% 2% 13% 85% Aaa Germany

Greece 5% 68% 22% 5% 0% 0% 0% Caa Greece

Hong Kong 0% 0% 0% 0% 2% 15% 83% Aa Hong Kong

Ireland 0% 0% 1% 8% 33% 45% 13% Baa Ireland

Italy 0% 10% 33% 48% 8% 1% 0% Baa Italy

Japan 0% 0% 0% 2% 13% 47% 37% A Japan

Latvia 0% 1% 3% 28% 45% 20% 3% A Latvia

Lithuania 0% 0% 2% 23% 46% 25% 4% A Lithuania

Luxembourg 0% 0% 0% 0% 1% 9% 90% Aaa Luxembourg

Malta 0% 0% 1% 17% 44% 31% 6% A Malta

Netherlands 0% 0% 0% 1% 9% 41% 49% Aaa Netherlands

New Zealand 0% 0% 0% 1% 4% 29% 66% Aaa New Zealand

Norway 0% 0% 0% 0% 2% 13% 85% Aaa Norway

Portugal 0% 4% 18% 56% 18% 3% 0% Ba Portugal

Singapore 0% 0% 0% 0% 1% 11% 88% Aaa Singapore

Slovakia 0% 1% 4% 37% 42% 14% 2% A Slovakia

Slovenia 0% 3% 14% 56% 22% 4% 1% Baa Slovenia

Spain 0% 2% 11% 53% 27% 6% 1% Baa Spain

Sweden 0% 0% 0% 1% 4% 25% 70% Aaa Sweden

Switzerland 0% 0% 0% 0% 2% 13% 86% Aaa Switzerland

United Kingdom 0% 0% 0% 1% 6% 35% 58% Aa United Kingdom

United States of America 0% 0% 0% 0% 0% 0% 100% Aaa United States of America

India 0% 13% 37% 42% 6% 1% 0% Baa India

Russia 0% 4% 18% 56% 17% 3% 0% Ba Russia

China 0% 0% 0% 2% 10% 44% 43% Aa China

Czech Republic 0% 0% 1% 13% 40% 38% 9% A Czech Republic

Israel 0% 0% 1% 17% 43% 32% 6% A Israel

Korea 0% 0% 1% 7% 30% 47% 15% Aa Korea

Brazil 4% 65% 24% 6% 0% 0% 0% Baa Brazil

Bulgaria 0% 17% 40% 37% 5% 1% 0% Baa Bulgaria

Romania 0% 8% 27% 52% 11% 2% 0% Baa Romania

Mexico 0% 5% 22% 56% 15% 3% 0% A Mexico

Turkey 0% 3% 13% 55% 24% 5% 1% Baa Turkey

Poland 0% 1% 3% 28% 45% 21% 3% A Poland

Hungary 0% 4% 19% 56% 17% 3% 0% Ba Hungary

Egypt 42% 55% 2% 0% 0% 0% 0% B Egypt

Ukraine 88% 12% 0% 0% 0% 0% 0% Caa Ukraine

Rating Probabilities

21

GREEK SOVEREIGN RATING

22

GREEK SOVEREIGN RATING

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

The next step is to employ our estimated sovereign ratings model to compare our model’s implied ratingfor Greece against Moody’s actual rating, but also to project the evolution of Greece’s sovereign rating in2017 under three alternative scenarios:

i) A Baseline

ii) An Adverse Case

iii) A Best Case

The way we operationalise these projections is by translating our macroeconomic views regarding GDP,unemployment rate, inflation, etc. into values for the four factors (Economic, Fiscal, Institutional Strengthand Event Risk) and examine the assessed rating distribution.

23

GREECE: FACTOR EVOLUTION UNDER THE BASELINE SCENARIO

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

o In our Baseline scenario the four rating factors reflect the central tendency of our macroeconomic projections.

o Specifically, we assume that the Greek government will reach an agreement on the Programme Review with the Institutions in H1 2017. As a result, the ongoing

political stability will continue and there will be no derailment of the 3rd Economic Adjustment Programme. The latter will be implemented gradually and thus

restoring the market’s confidence and boost domestic sentiment.

o The growth prospects in the base scenario underline a robust real GDP growth of circa 2.1% in the current year and a respective nominal GDP at 2.8% on an

annual basis. Inflation is expected to turn to a positive in 2017, at 0.8%, whereas the unemployment rate will continue to moderate at about 22%.

o From an Institutional and Event risk perspective, the capital controls regime introduced in mid-2015 is expected to continue being in force. We expect this will

continue in 2017, but there will be a further relaxation of the capital controls that are mainly related to payments and imports/exports activity.

0

1

2

3

4

5

6

-3.0

-2.0

-1.0

0.0

1.0

2.0

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

e

20

17

f

Avg. Real GDP Growth (in pp) (LHS) Vol. Real GDP Growth (in pp) (RHS)

Economic Strength

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.0

0.5

1.0

1.5

2.0

2.5

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

e

20

17

f

Inflation Volatility (in pp) (LHS) Government Effectiveness (RHS)

Institutional Strength

0

50

100

150

200

0.0

5.0

10.0

15.0

20.0

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

e

20

17

f

Gen. Government Interest Payments/ Revenue (in pp) (RHS)

Gen. Government Debt/ GDP (in pp) (LHS)

Fiscal Strength

0

50

100

150

200

-20.0

-15.0

-10.0

-5.0

0.0

5.0

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

e

20

17

f

(Current Account Balance+FDI)/GDP (in pp) (RHS)

Gross Loans to Deposits (in pp) (LHS)

Event Risk

o The model-implied ratings for Greece differ from

the rating agency’s actual decisions in all years we

examined. In the pre-crisis period Greece’s actual

rating was better than it deserved purely based

on macro-fundamentals. During the crisis period

the opposite holds true, with Greece being heavily

penalised, far beyond what is justified by macro

data.

o These results are consistent with a “positive”

premium in the early years (possibly due to EA

participation), which has turned massively

“negative” in the post-PSI era.

o Looking forward, the case for a rating upgrade

towards the single B rating band increases under

our baseline projections. Our 2016 and 2017

projections for the evolution of the main

economic indicators imply a rating upgrade to the

range of B3 to B1.

o Consequently, current judgment about Greece’s

rating decision might be more dependent on

qualitative factors (economic programme, MoU)

rather than on quantitative factors and economic

indicators.

24

Year Estimated Rating Probabilities Actual

C Ca Caa3-Caa1 B3-B1 Ba3-Ba1 Baa3-Baa1 A3-A1 Aa3-Aa1 Aaa

2007 - - - 5% 14% 39% 37% 3% 1% A

2009 - - - 10% 40% 43% 7% 1% - A

2012 3% - 8% 83% 5% 1% - - - C

2015 - - 5% 68% 22% 5% - - - Caa

2016f - - 4% 61% 27% 7% 1% - - Caa

2017f - - 1% 41% 40% 16% 1% - - na

0%

10%

20%

30%

40%

50%

Aaa

AaA

Baa

BaB

Caa

CaC

0%

20%

40%

60%

80%

100%

Aaa

AaA

Baa

BaB

Caa

CaC

Actual

2007 2012

0%

20%

40%

60%

80%

Aaa

AaA

Baa

BaB

Caa

CaC

2015

2017f

2016

GREECE: OUR CREDIT RATING PROJECTIONS – WE DESERVE BETTER

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

25

GREECE: FACTOR EVOLUTION UNDER ALTERNATIVE SCENARIOS - ADVERSE

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

o Under the adverse case scenario (RED-DOTTED LINE) we anticipate a decline in economic growth with a further deterioration in institutional strength and an

increase in the debt level followed by higher interest payments.

o Specifically, we assume that the Greek government will reach an agreement on the Programme Review with the Institutions with a delay, hence in

H2 2017. As a result, the ongoing political stability will be shaken leading to a minor chance for early elections. This will cause a further decline in

the disposable income due to the extensive fiscal measures.

o Growth prospects in the Adverse Scenario are negative with real GDP ranging between -1.0%-0.5% and nominal GDP between -1.5%-0.6% on an

annual basis. The deflationary pressures will continue, whereas the unemployment rate will increase.

o From an Institutional and Event risk perspective, the capital controls regime is assumed to remain in force throughout 2017.

Economic Strength

Event Risk

Institutional Strength

Fiscal Strength

0

1

2

3

4

5

6

-3.0

-2.0

-1.0

0.0

1.0

2.0

Avg. Real GDP Growth (in pp) (LHS) Vol. Real GDP Growth (in pp) (RHS)

0

1

1

2

2

3

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Government Effectiveness (RHS) Inflation Volatility (in pp) (LHS)

0

5

10

15

20

0.0

50.0

100.0

150.0

200.0

Gen. Government Debt/ GDP (in pp) (LHS)

Gen. Government Interest Payments/ Revenue (in pp) (RHS)

-20

-15

-10

-5

0

5

0.0

50.0

100.0

150.0

200.0

Gross Loans to Deposits (in pp) (LHS)

(Current Account Balance+FDI)/GDP (in pp) (RHS)

26

GREECE: FACTOR EVOLUTION UNDER ALTERNATIVE SCENARIOS - BEST

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

o Conversely, our best case scenario (GREEN-DOTTED LINE) is associated with stronger economic growth and a substantial relief in the debt level. We also allow for a

slight improvement in government effectiveness in 2017 which is relevant under the scenario of higher economic growth.

o Specifically, we assume that the Greek government will reach an agreement on the Programme Review with the Institutions with no delays in Q1 2017. As a

result, the ongoing political stability will continue and there will be no derailment of the 3rd Economic Adjustment Programme. The latter will be

implemented gradually, thus restoring market confidence and boosting domestic sentiment. The growth prospects in the Best Scenario underline a robust

real GDP growth with balanced prices and a further decline in unemployment rates.

o Moreover, Greece will be able to enter the international debt markets by end-2017 and the Greek Government bonds will participate in the QE programme.

o From an Institutional and Event risk perspective, the capital controls regime is expected to remain in force but with significant relaxation of restrictions.

o A combination of implementing a strong reform agenda and investment approach along with the implementation of the measures passed by the Greek

parliament (e.g. privatisations) are catalysts. Several infrastructure projects (e.g. construction of highways) are expected to be finished by the end of 2017.

Economic Strength

Event Risk

Institutional Strength

Fiscal Strength

0

1

2

3

4

5

6

-3.0

-2.0

-1.0

0.0

1.0

2.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016e2017f

Avg. Real GDP Growth (in pp) (LHS) Vol. Real GDP Growth (in pp) (RHS)

0

1

1

2

2

3

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016e2017f

Government Effectiveness (RHS) Inflation Volatility (in pp) (LHS)

0

5

10

15

20

0.0

50.0

100.0

150.0

200.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016e2017f

Gen. Government Debt/ GDP (in pp) (LHS)

Gen. Government Interest Payments/ Revenue (in pp) (RHS)

-20

-15

-10

-5

0

5

0.0

50.0

100.0

150.0

200.0

Gross Loans to Deposits (in pp) (LHS) (Current Account Balance+FDI)/GDP (in pp) (RHS)

27

Year Scenario Estimated Rating Probabilities Estimated

C Ca Caa3-Caa1 B3-B1 Ba3-Ba1

Baa3-

Baa1 A3-A1

Aa3-

Aa1 Aaa

2016 Base - - 4% 61% 27% 7% 1% - - B

Worst - - 4% 64% 25% 6% 0% - - B

Best - - 3% 54% 33% 10% 1% - - B

2017 Base - - 1% 41% 40% 16% 1% - - B

Worst - - 2% 51% 35% 11% 1% - - B

Best - - 1% 38% 42% 17% 2% - - Ba

GREECE: SCENARIO ANALYSIS

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

o We evaluated the rating model’s sensitivity to

underlying factors by evaluating alternative

scenarios related to the evolution of the Greek

economy.

o Since our main conclusions depend on the

baseline scenario, we created Best and Worst

case settings by varying the anticipated

evolution of the underlying factors in the

Greek economy.

o We concluded that the implied rating band

does not change under the alternative

assumptions, with the exception of a higher

likelihood of an upgrade from the current

actual rating of Caa towards the Ba band

under the best case scenario in 2017. In

particular, under the worst case scenario the

implied probability of a B3-B1 rating remains

almost unchanged for 2016. Still, in 2017 the

probability of a B3-B1 rating increases

substantially compared to the base case

scenario.

o In contrast, under the best case scenario, the

whole ratings distribution shifts upwards. The

probability of a B3-B1 rating declines to 38%,

while the probability for a Ba3-Ba1 rating

increases to 42%.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

AaaAaABaaBaBCaaCaC

2016

Base Worst Best

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

AaaAaABaaBaBCaaCaC

2017

Base Worst BestActualActual

28

APPENDIX I: METHODOLOGY

FROM DATA TO RATINGS: ORDERED CHOICE MODELS

o Rating agency decisions fit naturally with ordered choice models where an individual, i.e. the

rating agency in our case, must choose among an ordered set of discrete scores that characterise

the capacity of a country to pay off its debt obligations. By ordered set, we mean that the scores

follow a natural ordering from low ability (C) to high ability of debt repayment (Aaa). Ordered

choice models can be thought of as an indirect regression of the observed rating decisions (𝑦) to a

set of instrument variables (𝑥) that define several economic and qualitative characteristics of the

country’s debt repayment ability.

o The difference with the standard linear regression framework is that it is not possible to relate

discrete rating scores in a linear way with the continuum of values observed in 𝑥. In order to

overcome this problem we assume that the underlying process of choosing a country’s discrete

rating score is driven by a continuous preference strength random variable (𝑧) that relates

indirectly the rating decision 𝑦 with the economic characteristics of each country 𝑥. In particular

we relate the observed rating decisions 𝑦 with the unobserved preference strength 𝑧 which in turn

is related with the observed characteristics in 𝑥.

o Perhaps the notion of ordered choice models can be better understood in the context of two

country-two-rating scores example (binary choice model). For the sake of simplicity lets say that

the rating agency must choose between two scores for Greece and Italy, C and Aaa, where the first

rating indicates low ability of debt repayment and the second a high ability of debt repayment. For

each country the rating agency observes a single characteristic that indicates the country’s

GDP growth 𝑥𝐺 for Greece and 𝑥𝐼 for Italy. We further assume that the rating agency assigns an

Aaa rating to Italy and an C rating to Greece based on the GDP growth and on some other

unobserved factors that we cannot measure accurately or are not available publicly.

o Our goal is to estimate how the rating score outcome is related to the observed characteristic. For

this reason we assume that the rating agency makes decisions according to a preference index 𝑧

that is positively related to the observed characteristic (GDP growth) and the unobserved factors.

In other words we assume that as GDP growth increases, the tendency (or preference) of the

rating agency to assign an Aaa rating is greater. Additionally, preferences are also affected

(positively or negatively) by some other unknown factor 𝜀, (𝑧𝑖 = 𝛽0 + 𝛽1 ∗ 𝑥𝑖 + 𝜀𝑖).

29

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

o Now assume that the values of 𝑧 can be partitioned into two areas

representing the two observed rating score choices, those that lie

above a specific threshold 𝑚0 and those that lie below. For example,

since 𝑧G < 𝑚0 then 𝑦G = C while for Italy 𝑧I > 𝑚0 so 𝑦I = Aaa.

o Up to now we managed to relate the rating decisions for the two

countries with their GDP growth indirectly through the preference

strength variable 𝑧. Since 𝑧 depends also on the unobserved term 𝜀

which is random, the next step is to make assumptions on the

distribution of this unobserved term.

Italy

0

Greece

𝑥

𝑧

𝑚0

𝑦 =

𝑦 =

𝑥𝐼

𝑥𝐺

Ordered Choice Models

FROM DATA TO RATINGS: THE MULTINOMIAL LOGIT MODEL

o The model suggested provides a crude description of the mechanism underlying an observed rating decision. The next crucial assumption is that of the

distribution of the random error component 𝜀, i.e. the country’s unobserved or unmeasured features.

o The standard assumption here is that errors are randomly drawn from some theoretical distribution allowing us to attach probabilities to each rating

decision. In other words, by specifying the error distribution in the model we transform the rating score preferences 𝑧 to a probability function of the rating

score outcome conditional on 𝑥, 𝛽0, 𝛽1 and 𝑚0. Intuitively, the conditional probability function works as the preference strength variable transformed in

such a way so that it takes values between zero and one and changes analogously with the economic characteristics of the country. That is, if 𝑥𝐺 increases,

then the probability of assigning a higher rating to Greece increases as well.

o For each choice of error distribution we should apply an appropriate transformation. Usually these transformations are non-linear function and the most

common are the probit function (for normally distributed errors) and the logit function (for errors drawn from a logistic distribution). In our study we prefer

to work with the latter S-shaped function as shown in the figure above.

o Multinomial logit or probit models are extensions of this simple binary choice example to a setting where the rating agency has to choose among more than

two rating scores. The parameters that we estimate in the multinomial logit model are the β from the linear equation as well as the 𝑛 − 1 threshold

parameters 𝑚 that correspond to the 𝑛 rating scores.

30

Logit Transformation and Error Distribution

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

1

Italy

0

Greece

0

𝑥

𝑧

𝑚0

𝑦 =

𝑦 =

𝑥

𝑥𝑖

𝑦 = 𝑥

31

APPENDIX II: FACTOR-DRIVEN CREDIT RATING DECISIONS vs.

ACTUAL RATINGS

32

FACTOR-DRIVEN CREDIT RATING DECISIONS IN LINE WITH ACTUAL RATINGS IN 2015

FULL SAMPLE – 1/3

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

Countries Caa B Ba Baa A Aa Aaa Actual Rating Implied Rating Confidence Countries

Australia 0% 0% 0% 1% 7% 38% 53% Aaa Australia

Austria 0% 0% 0% 6% 27% 49% 18% Aaa Austria

Belgium 0% 0% 2% 21% 45% 26% 5% Aa Belgium

Canada 0% 0% 0% 4% 21% 51% 24% Aaa Canada

Cyprus 0% 4% 18% 56% 18% 3% 0% B Cyprus

Denmark 0% 0% 0% 1% 3% 24% 72% Aaa Denmark

Estonia 0% 0% 0% 5% 24% 50% 21% A Estonia

Finland 0% 0% 0% 3% 17% 50% 29% Aaa Finland

France 0% 0% 0% 3% 15% 49% 33% Aa France

Germany 0% 0% 0% 0% 2% 13% 85% Aaa Germany

Greece 5% 68% 22% 5% 0% 0% 0% Caa Greece

Hong Kong 0% 0% 0% 0% 2% 15% 83% Aa Hong Kong

Ireland 0% 0% 1% 8% 33% 45% 13% Baa Ireland

Italy 0% 10% 33% 48% 8% 1% 0% Baa Italy

Japan 0% 0% 0% 2% 13% 47% 37% A Japan

Latvia 0% 1% 3% 28% 45% 20% 3% A Latvia

Lithuania 0% 0% 2% 23% 46% 25% 4% A Lithuania

Luxembourg 0% 0% 0% 0% 1% 9% 90% Aaa Luxembourg

Malta 0% 0% 1% 17% 44% 31% 6% A Malta

Netherlands 0% 0% 0% 1% 9% 41% 49% Aaa Netherlands

New Zealand 0% 0% 0% 1% 4% 29% 66% Aaa New Zealand

Norway 0% 0% 0% 0% 2% 13% 85% Aaa Norway

Portugal 0% 4% 18% 56% 18% 3% 0% Ba Portugal

Singapore 0% 0% 0% 0% 1% 11% 88% Aaa Singapore

Slovakia 0% 1% 4% 37% 42% 14% 2% A Slovakia

Slovenia 0% 3% 14% 56% 22% 4% 1% Baa Slovenia

Spain 0% 2% 11% 53% 27% 6% 1% Baa Spain

Sweden 0% 0% 0% 1% 4% 25% 70% Aaa Sweden

Switzerland 0% 0% 0% 0% 2% 13% 86% Aaa Switzerland

United Kingdom 0% 0% 0% 1% 6% 35% 58% Aa United Kingdom

United States of America 0% 0% 0% 0% 0% 0% 100% Aaa United States of America

Botswana 0% 2% 9% 50% 31% 7% 1% A Botswana

Chile 0% 0% 0% 6% 28% 48% 17% Aa Chile

China 0% 0% 0% 2% 10% 44% 43% Aa China

Czech Republic 0% 0% 1% 13% 40% 38% 9% A Czech Republic

Israel 0% 0% 1% 17% 43% 32% 6% A Israel

Korea 0% 0% 1% 7% 30% 47% 15% Aa Korea

Kuwait 0% 1% 7% 46% 35% 9% 1% Aa Kuwait

Macao 0% 0% 1% 10% 36% 43% 11% Aa Macao

Malaysia 0% 1% 4% 35% 43% 15% 2% A Malaysia

Mexico 0% 5% 22% 56% 15% 3% 0% A Mexico

Peru 0% 8% 29% 51% 9% 2% 0% A Peru

Poland 0% 1% 3% 28% 45% 21% 3% A Poland

Qatar 0% 0% 1% 14% 41% 36% 8% Aa Qatar

Rating Probabilities

A downward arrow (in red ) indicates that according to the model estimate the country is over-rated and should be adjusted downwards. Similarly, an upward arrow (in green ) indicates that the country is under-rated according to the model and its rating score should be adjusted upwards. The dash sign (in yellow ) indicates that the country is fairly rated. The confidence level ( ) indicates the degree of certainty in the model-implied rating scores. One blue bar in the confidence scale graph indicates less than 50% confidence, two blue bars correspond to between 50 % - 60% confidence, three bars to 60% - 70% confidence and finally four bars to more than 70% confidence.

33

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

FACTOR-DRIVEN CREDIT RATING DECISIONS IN LINE WITH ACTUAL RATINGS IN 2015

FULL SAMPLE – 2/3

Countries Caa B Ba Baa A Aa Aaa Actual Rating Implied Rating Confidence Countries

Saudi Arabia 0% 0% 1% 15% 42% 35% 7% Aa Saudi Arabia

Taiwan 0% 0% 1% 8% 31% 47% 14% Aa Taiwan

United Arab Emirates 0% 0% 0% 2% 13% 48% 36% Aa United Arab Emirates

Bahamas 0% 5% 21% 56% 15% 3% 0% Baa Bahamas

Bulgaria 0% 17% 40% 37% 5% 1% 0% Baa Bulgaria

Colombia 1% 24% 43% 28% 3% 0% 0% Baa Colombia

Iceland 0% 0% 1% 8% 32% 46% 14% Baa Iceland

India 0% 13% 37% 42% 6% 1% 0% Baa India

Indonesia 0% 11% 34% 47% 7% 1% 0% Baa Indonesia

Kazakhstan 0% 8% 28% 52% 10% 2% 0% Baa Kazakhstan

Mauritius 0% 2% 10% 52% 29% 6% 1% Baa Mauritius

Namibia 0% 4% 16% 56% 20% 4% 0% Baa Namibia

Oman 0% 1% 4% 37% 42% 14% 2% A Oman

Panama 0% 19% 41% 35% 4% 1% 0% Baa Panama

Philippines 0% 9% 30% 50% 9% 1% 0% Baa Philippines

Romania 0% 8% 27% 52% 11% 2% 0% Baa Romania

South Africa 0% 6% 25% 54% 12% 2% 0% Baa South Africa

Thailand 0% 2% 8% 48% 34% 8% 1% Baa Thailand

Trinidad & Tobago 0% 15% 39% 40% 5% 1% 0% Baa Trinidad & Tobago

Turkey 0% 3% 13% 55% 24% 5% 1% Baa Turkey

Uruguay 0% 3% 13% 55% 24% 5% 1% Baa Uruguay

Azerbaijan 5% 68% 22% 5% 0% 0% 0% Baa Azerbaijan

Bahrain 0% 9% 31% 50% 9% 1% 0% Baa Bahrain

Bangladesh 1% 32% 43% 21% 2% 0% 0% Ba Bangladesh

Bolivia 2% 49% 36% 12% 1% 0% 0% Ba Bolivia

Brazil 4% 65% 24% 6% 0% 0% 0% Baa Brazil

Costa Rica 0% 17% 40% 37% 5% 1% 0% Ba Costa Rica

Cote d'Ivoire 0% 6% 24% 54% 13% 2% 0% Ba Cote d'Ivoire

Croatia 0% 12% 35% 45% 7% 1% 0% Ba Croatia

El Salvador 7% 72% 17% 4% 0% 0% 0% Ba El Salvador

Georgia 0% 12% 35% 45% 7% 1% 0% Ba Georgia

Guatemala 2% 44% 39% 14% 1% 0% 0% Ba Guatemala

Hungary 0% 4% 19% 56% 17% 3% 0% Ba Hungary

Morocco 0% 14% 37% 42% 6% 1% 0% Ba Morocco

Paraguay 2% 44% 39% 14% 1% 0% 0% Ba Paraguay

Russia 0% 4% 18% 56% 17% 3% 0% Ba Russia

Suriname 3% 56% 32% 9% 1% 0% 0% Ba Suriname

Tunisia 1% 42% 40% 15% 1% 0% 0% Ba Tunisia

Albania 1% 32% 43% 21% 2% 0% 0% B Albania

Angola 26% 69% 5% 1% 0% 0% 0% Ba Angola

Rating Probabilities

A downward arrow (in red ) indicates that according to the model estimate the country is over-rated and should be adjusted downwards. Similarly, an upward arrow (in green ) indicates that the country is under-rated according to the model and its rating score should be adjusted upwards. The dash sign (in yellow ) indicates that the country is fairly rated. The confidence level ( )indicates the degree of certainty in the model-implied rating scores. One blue bar in the confidence scale graph indicates less than 50% confidence, two blue bars correspond to between 50 % - 60% confidence, three bars to 60% - 70% confidence and finally four bars to more than 70% confidence.

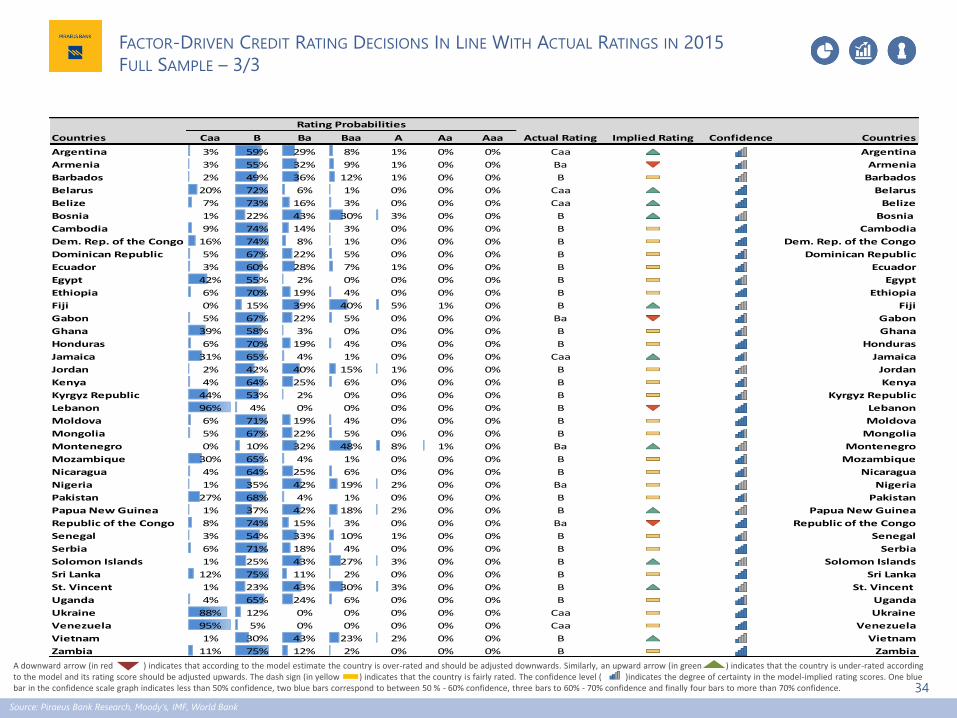

34

Source: Piraeus Bank Research, Moody’s, IMF, World Bank

FACTOR-DRIVEN CREDIT RATING DECISIONS IN LINE WITH ACTUAL RATINGS IN 2015

FULL SAMPLE – 3/3

Countries Caa B Ba Baa A Aa Aaa Actual Rating Implied Rating Confidence Countries

Argentina 3% 59% 29% 8% 1% 0% 0% Caa Argentina

Armenia 3% 55% 32% 9% 1% 0% 0% Ba Armenia

Barbados 2% 49% 36% 12% 1% 0% 0% B Barbados

Belarus 20% 72% 6% 1% 0% 0% 0% Caa Belarus

Belize 7% 73% 16% 3% 0% 0% 0% Caa Belize

Bosnia 1% 22% 43% 30% 3% 0% 0% B Bosnia

Cambodia 9% 74% 14% 3% 0% 0% 0% B Cambodia

Dem. Rep. of the Congo 16% 74% 8% 1% 0% 0% 0% B Dem. Rep. of the Congo

Dominican Republic 5% 67% 22% 5% 0% 0% 0% B Dominican Republic

Ecuador 3% 60% 28% 7% 1% 0% 0% B Ecuador

Egypt 42% 55% 2% 0% 0% 0% 0% B Egypt

Ethiopia 6% 70% 19% 4% 0% 0% 0% B Ethiopia

Fiji 0% 15% 39% 40% 5% 1% 0% B Fiji

Gabon 5% 67% 22% 5% 0% 0% 0% Ba Gabon

Ghana 39% 58% 3% 0% 0% 0% 0% B Ghana

Honduras 6% 70% 19% 4% 0% 0% 0% B Honduras

Jamaica 31% 65% 4% 1% 0% 0% 0% Caa Jamaica

Jordan 2% 42% 40% 15% 1% 0% 0% B Jordan

Kenya 4% 64% 25% 6% 0% 0% 0% B Kenya

Kyrgyz Republic 44% 53% 2% 0% 0% 0% 0% B Kyrgyz Republic

Lebanon 96% 4% 0% 0% 0% 0% 0% B Lebanon

Moldova 6% 71% 19% 4% 0% 0% 0% B Moldova

Mongolia 5% 67% 22% 5% 0% 0% 0% B Mongolia

Montenegro 0% 10% 32% 48% 8% 1% 0% Ba Montenegro

Mozambique 30% 65% 4% 1% 0% 0% 0% B Mozambique

Nicaragua 4% 64% 25% 6% 0% 0% 0% B Nicaragua

Nigeria 1% 35% 42% 19% 2% 0% 0% Ba Nigeria

Pakistan 27% 68% 4% 1% 0% 0% 0% B Pakistan

Papua New Guinea 1% 37% 42% 18% 2% 0% 0% B Papua New Guinea

Republic of the Congo 8% 74% 15% 3% 0% 0% 0% Ba Republic of the Congo

Senegal 3% 54% 33% 10% 1% 0% 0% B Senegal

Serbia 6% 71% 18% 4% 0% 0% 0% B Serbia

Solomon Islands 1% 25% 43% 27% 3% 0% 0% B Solomon Islands

Sri Lanka 12% 75% 11% 2% 0% 0% 0% B Sri Lanka

St. Vincent 1% 23% 43% 30% 3% 0% 0% B St. Vincent

Uganda 4% 65% 24% 6% 0% 0% 0% B Uganda

Ukraine 88% 12% 0% 0% 0% 0% 0% Caa Ukraine

Venezuela 95% 5% 0% 0% 0% 0% 0% Caa Venezuela

Vietnam 1% 30% 43% 23% 2% 0% 0% B Vietnam

Zambia 11% 75% 12% 2% 0% 0% 0% B Zambia

Rating Probabilities

A downward arrow (in red ) indicates that according to the model estimate the country is over-rated and should be adjusted downwards. Similarly, an upward arrow (in green ) indicates that the country is under-rated according to the model and its rating score should be adjusted upwards. The dash sign (in yellow ) indicates that the country is fairly rated. The confidence level ( )indicates the degree of certainty in the model-implied rating scores. One blue bar in the confidence scale graph indicates less than 50% confidence, two blue bars correspond to between 50 % - 60% confidence, three bars to 60% - 70% confidence and finally four bars to more than 70% confidence.

35

Disclaimer: This document is produced by the Economic Research & Investment Strategy Department of Piraeus Bank (hereinafter "the Bank"), which is supervised by the Bank of Greece and is

sent or provided to third parties, without any obligation of its author. This document or any part of it should not be duplicated in any way without the prior written consent of its author.

The information or opinions included in this document are addressed to existing or potential clients in a general manner, without taking into account the particular circumstances, the investment

objectives, the financial ability, the experience and/or knowledge of the potential recipients of this document and, as a result, they do not constitute or should not be considered neither as a

solicitation or offer for the conduct of transactions in financial instruments or currencies nor as a recommendation or advice for decision making in relation to those. Taking into account the

aforementioned, the recipient of the information contained in this document should proceed with his/her own research, analysis, and confirmation of the information which is included in this

document and seek for independent and professional legal, tax and investment advice, before proceeding with any investment decision making.

The information depicted in this document is relied on sources that the Bank considers to be reliable and is provided on an "as is" basis, however, the Bank cannot warrant as to their accuracy and

completeness. The opinions and estimates herein are related to the trend of the local and international financial markets at the indicated date (prices at closing time) and are subject to changes

without any prior notice. Notwithstanding the above, the Bank might include in this document investment researches, which have been conducted by third persons. In this case, the Bank does not

modify those researches, but it presents them on an "as is" basis, therefore, no responsibility is assumed in relation to the content of the aforementioned investment researches. The Bank is under

no duty to update the information contained in this document. Considering the above, the Bank, the members of its Board of Directors and the relevant persons assume no responsibility for the

information included in the present document and/or for the outcome of any investment decisions made according to such information.

Piraeus Bank Group is an organisation with a significant presence in the Greek market and an increasing one in the international markets providing a wide range of investment services. In the

context of investment services offered by the Bank and/or any other Piraeus Group companies in general, there might be cases whereby conflict of interests may arise in relation to the information

provided herein. Reference should be made to the fact that the Bank, the relevant persons and/or other Piraeus Group companies indicatively:

a. Are not subject to any prohibition in relation to trading on own account or in the course of providing portfolio management services prior to the publication of this

document or the acquisition of any shares prior to any public offering or the acquisition of any other securities.

b. May offer upon remuneration investment banking services to issuers for whom this document may contain information.

c. May participate to the issuers' share capital or acquire other securities issued by the aforementioned issuers or attract other financial interests from them.

d. Might provide market making or underwriting services to issuers that might be mentioned in this document.

e. Might have published papers the content of which is different or incompatible to the information presented herein.

The Bank as well as the other Piraeus Group's companies have enacted, implement and maintain an effective policy, which prevents circumstances that may give rise to conflicts of interests and

the dissemination of any information among the departments ("chinese walls") and they also constantly comply with the provisions and regulations relevant to inside information and market

abuse. Also, the Bank confirms that it doesn't have any kind of interest or conflict of interest with a) any other legal entity or person that could have participated in the preparation of the present

document and b) with any other legal entity or person that couldn't have participated in the preparation of the present document, but had access to it before its publication.

It is duly stated that: the investments described in the present document include investment risks, among which the risk of losing the entire capital invested. In particular, it is stated that;

a. The figures presented herein refer to the past and that the past performance is not a reliable indicator of future performance.

b. In case the figures refer to simulated past performance, that past performance is not a reliable indicator of future performance.

c. The return on investments might be positively or negatively affected as a result of currency fluctuations, in case the figures are denominated in a foreign currency (other than

Euro).

d. Any forecasts in relation to future performance, may not be a reliable indicator of future performance.

e. The tax treatment of the information as well as transactions pertained in this document, depends on each investor's individual circumstances and may be subject to change in

the future. As a result, the recipient should seek for independent advice in relation to the applicable tax legislation.

The distribution of the present document outside Greece and/or to persons governed by foreign law may be subject to restrictions or prohibitions according to the applicable legislation.

Therefore, the recipient of the present should seek for independent advice in relation to the applicable legislation, in order to look into such restrictions and/or prohibitions.