SOUTHWEST FLORIDA STAKEHOLDER · PDF fileSOUTHWEST FLORIDA . STAKEHOLDER WORKSHOP . ......

169

November 2, 2012 Southwest Florida Regional Planning Council SOUTHWEST FLORIDA STAKEHOLDER WORKSHOP

Transcript of SOUTHWEST FLORIDA STAKEHOLDER · PDF fileSOUTHWEST FLORIDA . STAKEHOLDER WORKSHOP . ......

November 2, 2012 Southwest Florida Regional Planning Council

SOUTHWEST FLORIDA STAKEHOLDER WORKSHOP

Regional Planning Councils • Intergovernmental Solutions • Regional Planning • Technical Assistance • Economic Development • Emergency Management

PROGRAMS AND PROJECTS

3

CHARLOTTE HARBOR NATIONAL ESTUARY PROGRAM

• Water Conservation, Important Cost Savings Strategy

• Water Quality Protection, Important to Tourism & Development Economy

• Ecosystem Services

COMPREHENSIVE ECONOMIC DEVELOPMENT STRATEGY

• Strategic Economic Development Plans for Southwest Florida Development District

• Vital Projects • Technical Assistance

• New Infrastructure of the 21st Century

• Job Creation & Regional Competitiveness

• Connecting Communities

GEOGRAPHIC INFORMATION SERVICES

•Data Clearinghouse •Demographics • Spatial Analytics •Database Management •Geo Statistics •Graphics Design

EMERGENCY MANAGEMENT

•Evacuation Study/Planning •Hazardous Materials

Compliance/Training • LEPC Coordination •Public Safety Analysis •Homeland Security •Emergency Response

Coordination

PROJECTS IN GRANTS

•Brownfields Program •Energy Resiliency Study •Transportation

Disadvantaged (Glades & Hendry)

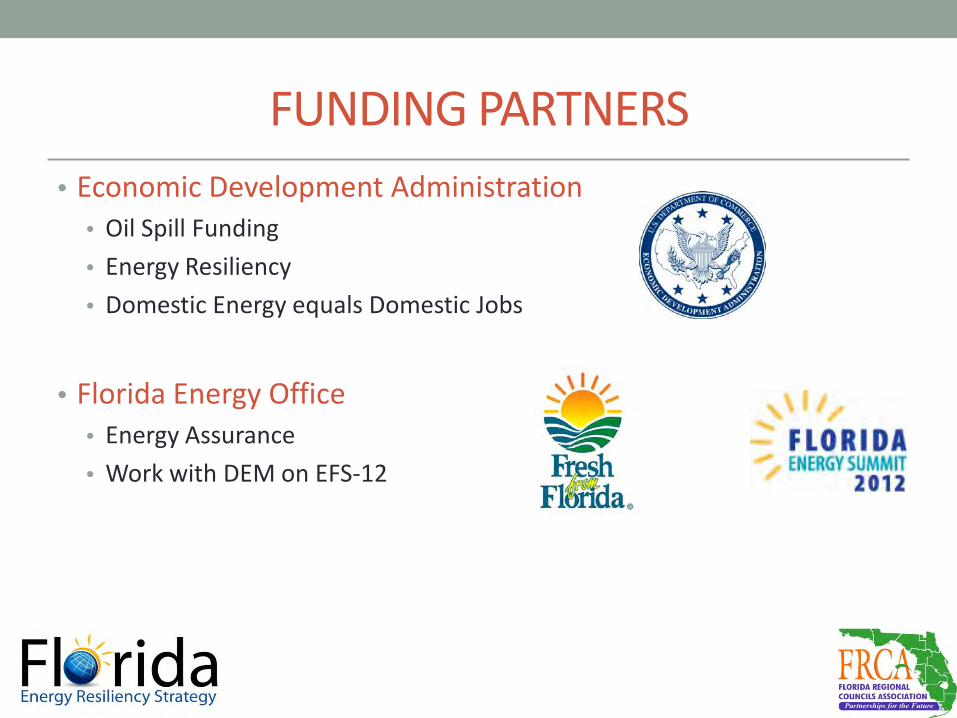

FUNDING PARTNERS • Economic Development Administration

• Oil Spill Funding • Energy Resiliency • Domestic Energy equals Domestic Jobs

• Florida Energy Office

• Energy Assurance • Work with DEM on EFS-12

WORKSHOP FORMAT • Presentation

• Project Scope and Purpose • Survey Results • Energy Experts • Scenario Modeling Results

• Stakeholder Participation • Breakout Groups • Report Outs • Audience Response System

• Some representative questions from the survey(s) to compare and discuss. • Bonus Session – Broadband Planning and Strategies

ENERGY PLANNING AREAS

1 2

3

4 5

1 2 3 4 5

WORKSHOP SCHEDULE • August 13 – Gainesville • August 29 – Jacksonville • October 23- Delray Beach (postponed) • October 29 – Pinellas Park • October 30 – Bartow • November 1 – Ocala • November 2 – Fort Myers, 10:00am to 2:00pm, SWFRPC • November 7 - Orlando • November 14 – Panama City

OBJECTIVES OF THE STUDY • Energy Resiliency Strategies

• Diversification of energy source • Reduce reliance on foreign imports • Increase use of domestic sources • Job creation from domestic energy usage

• Alternatives, renewable, local sources traditional sources

• Outcomes • Findings and recommendations

• Useful information so policymakers can make decisions • Customized by EPA when applicable

• Stakeholder input • Surveys and Workshops

EXPECTED OUTCOMES • Useful information so policymakers can make decisions

• Behavioral • Survey results

• Scientific telephone poll • Web based survey

• Customized by EPA when applicable • Economic Analyses

• What are the economic benefits of different alternative energy scenarios? • What is the pay back period for investments?

• What we are not doing • Promoting one energy source over another • Not judging the viability of one alternative source over another

Nov 2011 March 2013

Task

s Wor

ked

On

Five EPAs 11 RPCs

Findings and

Recommendations

Surveys Scenario Modeling

Stakeholders

BASIC PROCESS OVERVIEW

Phillip Downs, Ph.D. Kerr & Downs Research

Tallahassee, FL 32308 850.906.3111

ENERGY SURVEY Florida Regional Councils Association

This study examines individuals’ reactions to a broad range of energy issues including conservation, investment in energy saving devices, motivations for conserving energy, impact of energy cost increases on lifestyle, and government policies affecting energy. Methodology • Population definition

• All households in the following areas: EPA 1, EPA 2, EPA 3, EPA 4, & EPA 5 • Person most knowledgeable about energy issues

• Sampling frame • All working cellular and landline telephone numbers

• Sample size • 750 in total study • 150 in EPA 1 • 150 in EPA 2 • 150 in EPA 3 • 150 in EPA 4 – Southwest Florida + Central Florida • 150 in EPA 5

• Sampling error (given a 95% confidence interval) • 3.6% points in total study • 8.0% points for each EPA

• Data collection • Telephone interviews conducted from Kerr & Downs Research's office using CATI system • Conducted in May & June 2012

PURPOSE OF THE SURVEY

How long would the payback period from energy savings have to be for you to invest $500 in window tinting?

9%

17%

19%

1%

29%

25%

Less than 1 year

1 year to less than 2 years

2 to 5 years

6+ years

Would not purchase

Not sure

Mean: 22 months Median: 1 year

Motivations for using alternative energy or renewable sources:

80%

65%

53%

47%

45%

85%

77%

64%

61%

66%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Reduced energy costs

Environmental concerns

Price discounts on products

Rebates

Tax incentives

Business Resident

ENERGY POLICY

There should be more focus on domestic energy sources and less focus on foreign energy sources.

33%

55%

4%

2%

0%

5%

Strongly agree

Agree

Neither agree nor disagree

Disagree

Strongly disagree

Not sure

Presentations

Outlook for Federal & State Energy Policy

Presented at The Energy Workshop of the Southwest Florida Regional Planning Council

Fort Myers, Florida November 2, 2012

1

About Us Abraham & Roetzel is a joint venture of

The Abraham Group (energy consulting firm) &

Roetzel & Andress (law firm).

Our offices are located in Washington DC & Harrisburg, Pennsylvania.

Roetzel & Andress has offices in

Florida, Ohio, DC, Illinois & New York.

2

Outline

• Macro Trends and Game Changers in Energy Landscape

• Current Big Issues in Washington • Energy & Environment Policies of Obama vs.

Romney • Potential Policy Path Regardless of Outcome • Florida

3

Natural Gas

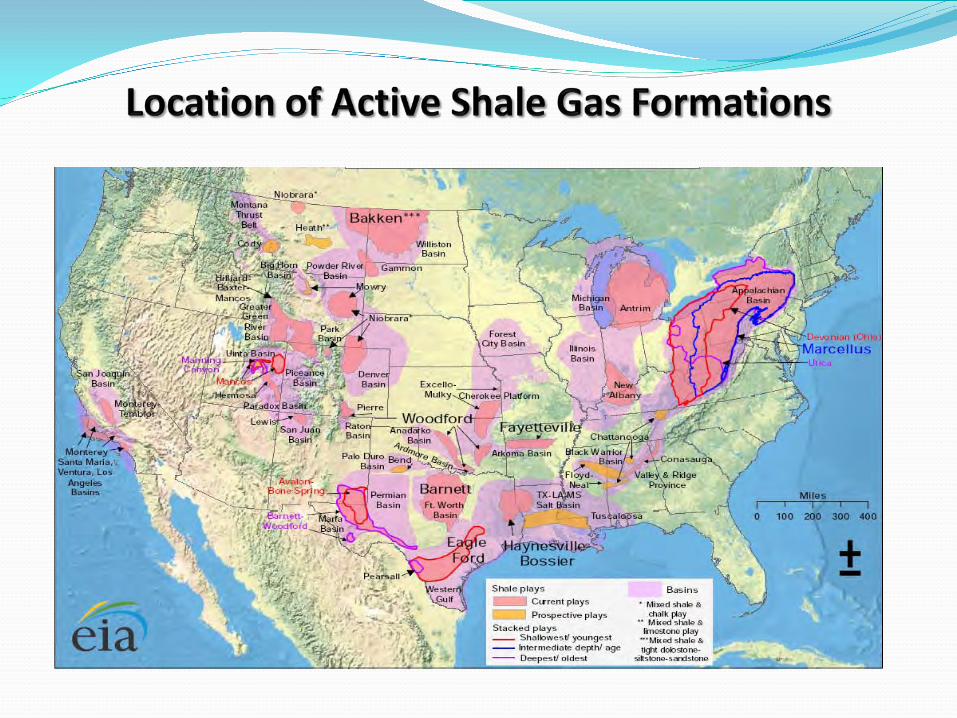

• Unconventional Shale Gas in Pennsylvania, Ohio & Texas

• US proven natural gas reserves surpassed 300 trillion cubic feet (Tcf) in 2010; technically recoverable nat gas is estimated at 2,203 Tcf according to EIA

• Good News – clean energy, lower prices, lower electricity rates, more manufacturing jobs in plastics, fertilizer & chemicals

• Bad News – hurts renewables, coal & nuclear; more regulation on the way

4

Unconventional Oil

Quick: What country will overtake Russia and Saudi Arabia to become the world’s leading oil producer in just a couple of years?

5

Saudi America • Now it is clear, the US has more spare capacity in

development than anyone else on the earth. It will soon be the US again, and not OPEC, that is the world’s swing producer.

• DOE forecasts the US crude production will average 11.4 million barrels per day next year.

• That will be a record for the US and just below Saudi Arabia’s output of 11.6 million barrels.

• Citibank forecasts US production could reach 13-15 million barrels per day by 2020, helping to make North America “the new Middle East.”

6

How did it happen?

• New technology – hydraulic fracturing and horizontal drilling – newfound ability to squeeze oil out of rock once thought too difficult and expensive to tap.

• Black Gold in new shale formations in North Dakota and Texas. Also, Oklahoma, Colorado & Ohio.

• Production from shale formations expected to grow from 1.6 million BPD this year to 4.2 million BPD by 2020, which means these new formations alone would yield more oil by 2020 than major oil suppliers such as Iran and Canada produce today.

7

More US Oil

• Less imported oil: With domestic oil production climbing rapidly since 2008, oil imports have been cut to just over 40 percent , the lowest level in two decades, from 60 percent.

• Transportation Issues – shipping oil by rail to refineries while new pipelines are built

• Price Spread Widens to $22.49 a barrel – WTI $89.33 vs. Brent at $111.82 for Nov contracts – big advantage for US refiners

8

Nuclear • 104 nuclear reactors in US – about 20 percent of

electricity generation • But the Fukishima pause button on new nuclear in the US

& impacted by low natural gas prices • DOE Loan Guarantees: Southern Company in Vogtle,

Georgia (received) & South Carolina Electric & Gas in Summer, South Carolina (on short list)

• Others planned in TVA, FPL Turkey Point • Compare to China 14 current plants; 40 new plants

coming. • UAE – one plant under construction; 4 plants by 2020.

9

Renewables • Electrical generation from wind, solar, geothermal and

biomass expanded to 5.8 percent in the US, from 3.1 percent about four years ago.

• State Renewable Energy Standards – 29 states, DC & Puerto Rico have renewable portfolio standards, which require utilities to obtain a certain amount of their power from renewable sources.

• Aggregated State RPS implies about 17% nationally; Compare to Proposed Federal RPS of 25% by 2025.

• Depending on growth, current RPS Goals imply 250GW or about $1 trillion in new investment (by 2025)

• Plethora of new technologies: wind, solar, PV, wave, algae, bioenergy, smart grid, storage, energy efficiency

10

Head Winds

• No more stimulus funds for renewables • Loan guarantee programs ending • Headline risk – Solyndra • Tax incentives may end • Low natural gas prices is probably the number

one problem for expanded renewables.

11

Next Big Thing • Defense Dept. Procurement is major new initiative of the

Obama Administration for renewables. • DoD playing critical role in advancement of clean energy

technologies. • Scale, purchasing power, R&D; DOD energy budget has

increased 200 percent. • DOD microgrid market expected to grow to by 375% $1.6

billion in 2020. • Army mulit-faceted $7 billion RFP for large scale renewable

and alternative energy for federal facilities • Navy biofuels program – investing $500 million to cofinance

construction of biorefineries; test flights of 50/50 biofuel blend tests for commercial flights

12

Current Federal Energy Issues

• Production Tax Credit for Renewables • Keystone Pipeline • DOE Loan Guarantee Programs • Oil & Gas Tax Incentives • Offshore Drilling • Federal Regulation of hydraulic fracturing • EPA regulations impacting coal

13

Obama vs. Romney

Obama • PTC Extension • End oil/gas tax cuts • Opposed Keystone, but will

probably approve after election

• Limited drilling on federal lands

• Federal RES • Limited fossil fuel exports • More restrictive policies for

coal and electricity generation from coal

Romney • No PTC Extension • Only end oil/gas tax cuts as

part of tax reform • Will approve Keystone • Double drilling on federal

lands; supports state regulation on federal lands

• No Federal RES • Supports fossil fuel exports • Policies to support coal &

reverse/delay restrictive regulation on coal

14

Environmental Regulation

• Bigger differences between Obama & Romney on environmental regulation

• President Obama’s EPA has imposed first carbon dioxide limits on new power plants & completed or proposed other regulations on greenhouse gas emissions

• Romney has expressed concern over several EPA regulations including mercury and greenhouse gas regulation & EPA regulations impacting coal. Some of these rules are implemented or in the courts and hard to reverse (but delay maybe).

• Expect a probably more aggressive environmental agenda in a second Obama term

• Also in second Obama term: Federal regulation of hydraulic fracturing, not due to water concerns, but focused on methane and greenhouse gas emissions from drilling. Romney will let states regulate.

15

Florida

• Offshore energy • Big opportunities in Bio Energy – cellulosic

ethanol & bioplastics from sugar cane bagasse & other resources

• Solar • Wave energy • Diversity of sources • Reliability

16

VW @ Cyano Biofuels, May 02, 2012, Berlin – Algenol, Dirk Radzinski 3

Advanced Industrial Biotechnology Company

Commercializing Proprietary Direct To Ethanol ® Technology

Fort Myers, FL Commercial Development Campus

§ Headquartered in Bonita Springs, Florida; European operations based in Zug, Switzerland

§ Research labs in Fort Myers, Florida and Berlin, Germany

§ 160 employees including 50+ Ph.D.‘s

Process Development Unit Fort Myers Research Labs

Algenol Overview

§ $160M from private investors § $25M DOE grant for

Integrated Biorefinery § $10M Lee County economic

development grant § Integrated Biorefinery (IBR):

major construction complete; initial operations begin Q1/13, expanded through Q4/13

§ R&D lab operations began in early August 2010

§ 50,000 ft2 of biology and engineering lab space

§ 4 acre outdoor Process Development Unit (PDU)

§ 36 acre outdoor commercial demonstration IBR

Integrated Biorefinery

VW @ Cyano Biofuels, May 02, 2012, Berlin – Algenol, Dirk Radzinski 4

Direct to Ethanol® Technology – Key Benefits

Commercial Production Rates and Costs are Compelling § Ethanol production cost below $1.00 per gallon § Initial commercial production rate of 6,000 gal/acre-yr (corn ethanol 400 gal/ac-yr)

Necessary Inputs Are Abundant § Sunshine! § CO2 from industrial sources (1 tonne of CO2 becomes 160 gallons of ethanol) § Salt water or brackish water as inputs § Fresh water output. 1 gallon of ethanol produced – 2 gallons of fresh water provided

Does Not Require § Killing or harvesting algae § Farm land or food crops § Fresh water

Technology Platform for Future Development and Co-products from CO2 § Biomass and Ethanol to jet and diesel § Green chemicals from CO2

VW @ Cyano Biofuels, May 02, 2012, Berlin – Algenol, Dirk Radzinski

Sustainable and Scalable Process

Advantages Over Other Biofuel Technologies

Technology Overview: Key Benefits

Direct to Ethanol® does not Require: § Daily harvesting algae to produce ethanol § Farm land or food crops § Fresh water

At Algenol: Only waste algae is processed into jet and diesel fuels

Necessary Inputs Are Abundant: § Sunshine § CO2 from industrial sources (1 tonne of CO2

becomes 160 gallons of ethanol) § Salt water or brackish water as inputs § Salt water or brackish water (1 gallon of

ethanol produced = 2 gallons of fresh water provided)

Productivity >8,000

gallons per acre per year

Cost Capex ≤ $10 per gallon

Opex $1 per gallon

VW @ Cyano Biofuels, May 02, 2012, Berlin – Algenol, Dirk Radzinski

§ Over expressed genes for fermentation pathway enzymes

§ Enhanced cells to improve

photosynthetic efficiency § 2,300 algae strains collected

globally and screened for optimal commercial Direct to Ethanol® strains

§ Ethanol secreted by hybrid algae is

recovered via condensate collection

§ Commercial strains of algae have

been selected

Technology Overview: Enhanced Algae

Algenol’s Direct to Ethanol® process uses enhanced algae to produce ethanol

Photosynthesis Intracellular Fermenta3on

Pyruvate

Blue Green Algae

Ethanol

Water

CO2

Nutrients

O2

Each Cell is a Tiny Ethanol Factory

VW @ Cyano Biofuels, May 02, 2012, Berlin – Algenol, Dirk Radzinski

Technology Overview: Photobioreactors

Low-cost, dual-purpose photobioreactors are key to Direct to Ethanol®

technology’s success § Algenol’s 1st generation patented

photobioreactors (PBRs) facilitate the initial stages of product creation, separation and collection, all of which are powered by the sun

§ PBRs are low-cost, modular and deployable at large scale

§ 1st generation PBRs are producing ethanol today

§ 2nd generation designs are being evaluated to optimize advancements in biology, namely increased ethanol production from the algae, and engineering gains in optics and temperature mitigation

§ Fresh water usage reduced to very low levels compared to large losses in open ponds

§ Closed system provides increased protection from environmental contamination

7

VW @ Cyano Biofuels, May 02, 2012, Berlin – Algenol, Dirk Radzinski

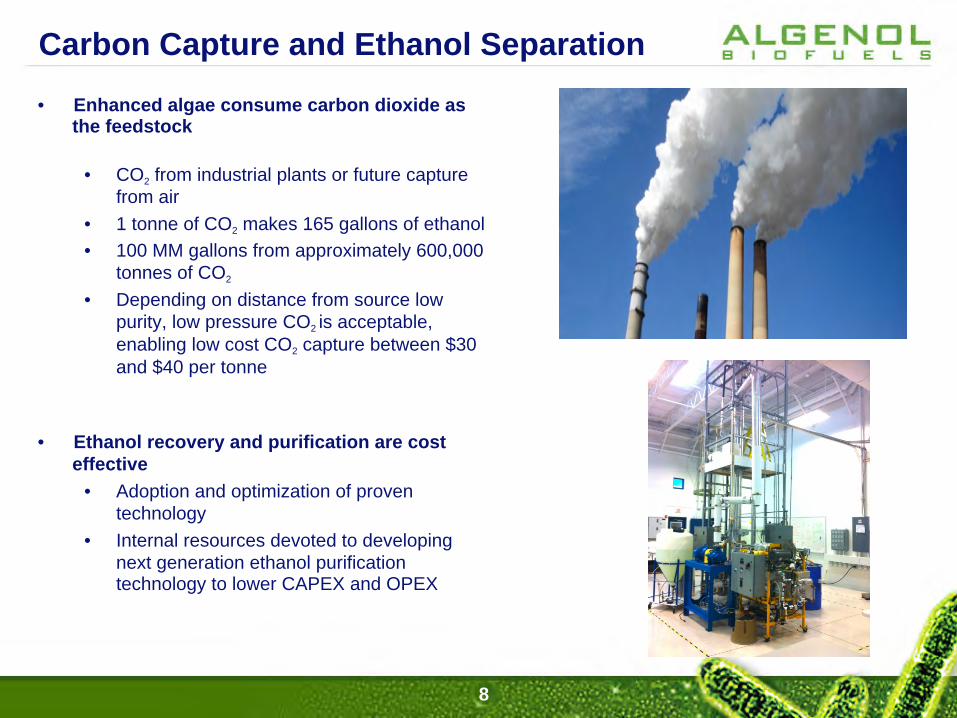

• Enhanced algae consume carbon dioxide as the feedstock

• CO2 from industrial plants or future capture from air

• 1 tonne of CO2 makes 165 gallons of ethanol • 100 MM gallons from approximately 600,000

tonnes of CO2

• Depending on distance from source low purity, low pressure CO2 is acceptable, enabling low cost CO2 capture between $30 and $40 per tonne

• Ethanol recovery and purification are cost effective

• Adoption and optimization of proven technology

• Internal resources devoted to developing next generation ethanol purification technology to lower CAPEX and OPEX

Carbon Capture and Ethanol Separation

8

VW @ Cyano Biofuels, May 02, 2012, Berlin – Algenol, Dirk Radzinski

Carbon Footprint by Life Cycle Analysis (Peer reviewed Publication)

§ Published in Environmental Science & Technology Journal

§ Renewable Fuel Standard’s requirements for reduction of GHG is met in all scenarios studied.

§ LCA, along with techno-economic analysis, is important part of the evaluation of new technology options

§ LCA study is designed to be evergreen – continuously updated as part of our DOE project.

Life Cycle Analysis Appears in: D. Luo, Z. Hu, D. Choi, V. Thomas, M. Realff, and R. Chance, Env. Sci. & Tech., 2010, 44 pp 8670–8677.

9

VW @ Cyano Biofuels, May 02, 2012, Berlin – Algenol, Dirk Radzinski

From the Laboratory to the Field

1-L PBR systems

4500-L foil-mixed integrated systems 150-L foil-mixed

integrated systems

Strain Development Physiology

Aquaculture Engineering

IBR

Petri Dishes

Algenol has the capability to move biology and engineering from lab scale to the field at one site

Shake Flasks

VW @ Cyano Biofuels, May 02, 2012, Berlin – Algenol, Dirk Radzinski 11

We’re All Students in the Lab § Algenol’s foundation is STEM

§ Over 115 employees in Florida; 63 with advanced degrees

§ Disciplines include: molecular biology; physiology; analytical chemistry; chemical and mechanical engineering; and information technology

§ Commercialization requires applying academic excellence in an entrepreneurial collaborative environment

§ Critical thinking and problem solving are imperative skills, as well as: § Teamwork: Algenol has established a collaborative

matrix of cross-functional project teams § Creativity: 21 patents issued; 44 patent applications

filed § Verbal and written communication: project teams

present to executive technical committee for guidance and gate review; our reports database catalogs years worth of reports and data; heavy reliance on IT

§ We do little on the job training because we hire elite skilled people

VW @ Cyano Biofuels, May 02, 2012, Berlin – Algenol, Dirk Radzinski 12

We’re All Residents of Florida Direct to Ethanol® technology is safe and provide significant economic development opportunities

§ Algenol intends to commercialize in Florida and in other suitable climates around the world

§ 2,000-3,000 jobs per commercial facility § Commercialization can be done while preserving

and improving the environment § Algenol cannot build if people are afraid of

Algenol and our algae • NIMBY (not in my back yard) • Algenol conducts open access tours every 4 months

• Algenol is regulated by Department of Agriculture’s division of Aquaculture

• Non Toxic • Not a Plant Pest • Non-Invasive

VW @ Cyano Biofuels, May 02, 2012, Berlin – Algenol, Dirk Radzinski

Commercial Development Campus

VW @ Cyano Biofuels, May 02, 2012, Berlin – Algenol, Dirk Radzinski

“The use of vegetable oils for engine fuels may seem

insignificant today, but such oils may become, in

the course of time, as important as petroleum and the coal-tar products of the

present time.” Rudolf Diesel - 1912 1

What is Biodiesel?

A renewable fuel commercially refined from a diverse array of fats and oils

by-products & used in normal diesel engines

Biodiesel Raw Materials Oil or Fat Soybean Corn Canola Cottonseed Sunflower Beef tallow Pork lard Used cooking oils

Oil from Coffee Grounds

The Economist Technology Quarter 1 - 2009 4

Biodiesel Reaction

100 Lbs. Vegetable Oil

+

20 Lbs. Methanol

90 Lbs. Biodiesel

+ 5 Lbs.

Glycerin +

5 Lbs Methanol

In the presence of a catalyst Reacting: Yields:

Produces mono-alkyl esters – chemically similar to diesel fuel

6

Better For Your Health • Biodiesel is:

• Biodegradable • Nontoxic:

• LD50 =17.4 g/Kg - less toxic than table salt • Skin irritation less than that of 4% soap and water solution

• Safer to handle: Flash point above 200 Degrees F, Non-Reactive, Non-Corrosive

• Compared to petrodiesel, biodiesel reduces black smoke (particulates), Carbon Monoxide, and harmful unburned hydrocarbons that cause smog.

8

Emissions Reduction: Particulate Matter (PM): 12% reduction with B20, 48% reduction with B100 Carbon Monoxide (CO): 12% reduction with B20, 48% reduction with B100 Carbon Dioxide (CO2): 16% reduction with B20, 78% reduction with B100 (life-cycle reduction) Hydrocarbons (VOCs): 20% reduction with B20, 68% reduction with B100 Nitrogen Oxides (NOx): +/- 1-2% change with B20 or B100 Sulfur Dioxide (SOx): 20% reduction with B20, 100% reduction with B100

9

• Last year the industry supported more than 39,000 jobs and

$3.8 billion in GDP* • The 4.6 billion gallons of biodiesel produced in the U.S. since

2005 have displaced 4.6 billon gallons of diesel fuel and • Reduced lifecycle greenhouse gas emissions by 56.2 billion

pounds - the equivalent of removing 4.96 million passenger vehicles from America's roadways.**

*Cardno ENTRIX, an International Economic Consulting Firm **National Biodiesel Board, 9/14/2012

10

Impacts on Planning and Dev. Opportunities • Creates technical, upper-income positions – adds to tax base • Growing Industry • Florida’s location for importing/exporting • Climate for oilseed production Challenges for the Industry • RFS – remember the date - December 19, 2007 • EPA’s acceptable feedstock pathways • Oil extraction (i.e. crushing) facilities for oilseed feedstocks

11

12

Incentives State Incentives • Biofuels Investment Tax Credit • Alternative Fuel Economic Development • Provision for Renewable Fuels Investment Federal Incentives • USDA

• Biomass Crop Assistance Program (rural) • Advanced Biofuel Production Grants and Loans (rural) • Advanced Biofuel Production Payments (all)

• IRS – tax advantages for alternative fuel use • See other programs at www.afdc.energy.gov

13

Ease of Use & Performance

• Using Biodiesel is easy! • B20 and lower blends are a drop-in replacement for

diesel fuel; no vehicle modifications needed • Can be used in any diesel engine / vehicle according to

OEM’s recommendations • www.biodiesel.org/using-biodiesel/oem-information/oem-

statement-summary-chart for OEM positions • No trade-offs in terms of engine performance, fuel economy, horsepower,

torque – essentially the same as diesel

• Dispensed through existing fueling stations 14

OEM Support for Biodiesel

15

OEM Warranty Statements • All major OEMs selling diesel equipment in the U.S. support at least

B5 and lower blends, provided they are made with biodiesel meeting ASTM D 6751

• 10 new OEM statements of B20 support so far in 2012, with more

expected soon! • Now 77% of U.S. manufacturers (30 brands) support B20 or higher

blends in at least some of their equipment; • More than 95% of the medium- and heavy-duty truck markets now

support B20 • For a complete listing of OEM position statements on biodiesel, as

well as the current U.S. Diesel Vehicles List, visit: www.biodiesel.org/using-biodiesel/oem-information

OEMs Supporting B20+

Biodiesel Infrastructure • Biodiesel and biodiesel blends are now available nationwide from

more than: • 575 Distributors • 850 Retailers • 450 Truck Stops • At least 1,875 Public Locations

• Visit the new NBB website at: www.biodiesel.org/using-biodiesel/finding-biodiesel/retail-locations to view biodiesel retailers by state or along a route

Thank You! Questions…?

Mindy Collier FL Biofuels LLC State Farmers Market 2744 Edison Ave., Unit 8 Fort Myers, Florida 33916 T: 239-313-6205 [email protected]

19

Presentation to Energy In Southwest Florida Workshop

November 2, 2012

The Major Difference!

U.S. Pipeline Grid

Florida Natural Gas Service Availability

Segment

Number of Customers

Residential

674,090

Commercial

59,549

Industrial

607

Total

734,246

Distributors and

Pipelines

Number of Service

Providers

IOU 5

Municipal 27

Gas Districts 4

Intrastate Pipeline

1

Interstate Pipelines

4

Florida Natural Gas Service Availability

Interstate Pipelines Serving Florida

Florida Gas Transmission 3.1 BCF/Day

Gulfstream Natural Gas System 1.3 Bcf/Day

Southern Natural Gas .370 Bcf/Day Gulf South

Pipeline .200 Bcf/Day

Total Capacity into State is 4.97 Bcf/Day

Per EIA Average 2011 Daily

Consumption was 3.2 Bcf/Day

2011 production at highest level in 25

years

30% of production

from shale gas January 2012 production up 10% from January 2011

US Proved Reserves -2009

11,813

2,871

10,869

2,773

23,058

7

3,279

2,782

20,688

2,763

917

976

15,598

196

1,079

896

22,769

6,985

80,424

7,257

3,091 5,946

35,283

200% Increase

145% Increase

Total US Proved

Reserves 262,320 Bcf

57% Increase from 2000

Source: EIA

Access to Natural Gas Storage

Bay Gas

Southern Pines

Napoleonville

Egan

Golden Triangle

Spindletop

Tres Palacios Pine Prairie

Bobcat Petrologistics

10 Storage Facilities with Over 175 Bcf of Working Gas

Capacity

At 50% of Capacity Over 28

Days of Peak Deliveries

SONAT, Gulf South, And Gulfstream Have Access

to Additional Storage Facilities

Energy Realities

ExxonMobil’s 2012 Outlook for Energy

USA Electric Generation Mix

Cost Related to Generation

ExxonMobil’s 2012 Outlook for Energy

The Direct Use of Natural Gas

Source: AGA 2011 Playbook

Benefits of Direct Use of NG

More effective use of the energy Lower GHG per residence by 2-3 tons annually Reduces load on the electric grid Reduces the need to build more electric generation

plants Lower costs for residences and businesses

Contact Information: Scott Ranck, CEA Senior Conservation & Energy Specialist Florida Public Utilities Company [email protected]

Compressed Natural Gas in Florida

Keith Gruetzmacher Senior Manager Marketing Services

TECO Energy

TECO Energy, Inc. (NYSE: TE) is an energy-related holding company headquartered in Tampa, Florida. Its regulated Florida operations include Tampa Electric and Peoples Gas. Other business companies include TECO Clean Advantage and TECO Partners. • Tampa Electric is a regulated electric utility with nearly 4,700 megawatts of

capacity. Its service area covers 2,000 square miles in West Central Florida, including nearly all of Hillsborough County and parts of Polk, Pasco and Pinellas counties. Tampa Electric delivers reliable power to more than 677,000 residential, commercial and industrial customers.

• Peoples Gas is Florida’s leading provider of regulated natural gas distribution

services, with a presence in most of the state’s metropolitan areas. Peoples Gas delivers reliable, clean energy to almost 340,000 residential, commercial and industrial customers.

• TECO Partners is an energy-related sales and marketing company dedicated to

providing comprehensive energy solutions for residential and business clients.

PGS Service Area

PGS Territory • Local Distribution Company (LDC) • Deliver natural gas to homes and businesses

through underground pipelines

NGV Infrastructure

City of Milton

PGS Jax

Waste Pro (Port Orange)

Kennedy Space Center

FL City Gas (Rockledge)

Waste Management (Pompano Beach)

City of N. Miami PGS Miami

City of Hollywood

Quality Transportation (Wise Gas) Clean Energy (Choice Environmental)

Veolia

PGS Ft. Myers WM (Venice)

PGS St. Pete

Clearwater Gas (City of Clearwater)

PGS Channelside

Clean Energy (TIA)

Travis Career Center (Polk Co)

Republic

PGS Orlando City of Apopka PGS Ocala

Leon Co. Schools

Republic - Volusia Co.

Saddle Creek

ESP

Waste Pro Ft. Pierce

Marion County

Existing Under Construction PGS 29 stations total

Public NGV Infrastructure

City of Milton

Waste Management (Pompano Beach)

Quality Transportation (Wise Gas)

Clearwater Gas (City of Clearwater)

Clean Energy (TIA)

Leon Co. Schools

ESP

Marion County

Public (current) Under construction

Currently, only 6 stations open to the public. Lack of fueling infrastructure has been a major inhibitor to fleet conversions. But that’s changing…..

Today’s Fuel Costs Public Stations CNG vs. FL Petroleum

Rate Schedule

Cost/ GGE

Cost/ DGE

CNG FL Avg.1

$2.134 $2.433

CNG US Avg. 2

$2.050 $2.337

Unleaded3 $3.811

Mid3 $3.987

Premium3 $4.118

Diesel3 $4.084

1 – www.cngprices.com 2 – Clean Cities Alternative Fuels Price Report (July 2012) 3 – FL average fuel prices. AAA Fuel Gauge Report (September 14, 2012)

Price Projection

Vehicle Technology

• NGV America (www.ngvamerica.org) – 30 different manufacturers and 100 models of

light, medium and heavy-duty vehicles and engines from OEM or certified retrofit.

– 2012 updated list available

NGVs Under 14,000 Pounds

NGVs Over 14,000 Pounds

Florida Activity

Refuse Industry • Part of every portfolio • Over 400 trucks • Operating since 2010

• TIA opened 3/9/12 • 10yr plan to convert

majority of fleet • Opportunity for use

by support fleets

• Headquartered in Lakeland • Provides third-party logistics operations across the U.S. • CNG operation started December 30, 2011 • 1st tractors in Florida • Over 1 million CNG miles • 120 CNG tractors by 2014

Statewide Distribution

Work with you and your CNG providers to: • Establish Natural Gas availability

– Available pressure

• Identify fueling needs – Annual consumption – Peak fueling demand

• Determine gas marketing needs – Lock-in your fuel price

The PGS Role

Presented by Diana Giraldo

Sustainability Coordinator City of Fort Myers

[email protected] (239) 321-7926

Energy & Efficiency Planning

Understanding The Task Funding Following a Plan

Understanding Regional Considerations Florida’s Hot & Humid Climate Zone

Understanding Ratings/Certifications & Requirements For EE

Energy & Efficiency Planning

Researching Materials & Implementation

Would you ever use Wikipedia to make an informed decision?

Working With The Right Team Building Owner Project Manager/Planner Designer Builder Building Science Professional

4

New Buildings

Lot Orientation/Preservation of the Natural Environment

Connectivity & Transportation Shade Trees/Landscaping Site Grading

New Buildings

Building Envelope Walls/Windows/Roofs Thermal Performance

HVAC Plumbing** Electrical Appliances Building Science/Verification*

Existing Buildings

Enhanced Landscape Building Envelope

Thermal Performance Whole House Infiltration

HVAC Electrical & Plumbing As Needed Appliances Building Science/Verification*

What To Consider Before You Think

Solar Is The Only Solution?

Solar Systems Must Work As A System With The Building…

There Are Other Considerations!

Best Practices-Existing Buildings

Building Science/Verification* HERS/BERS Testing

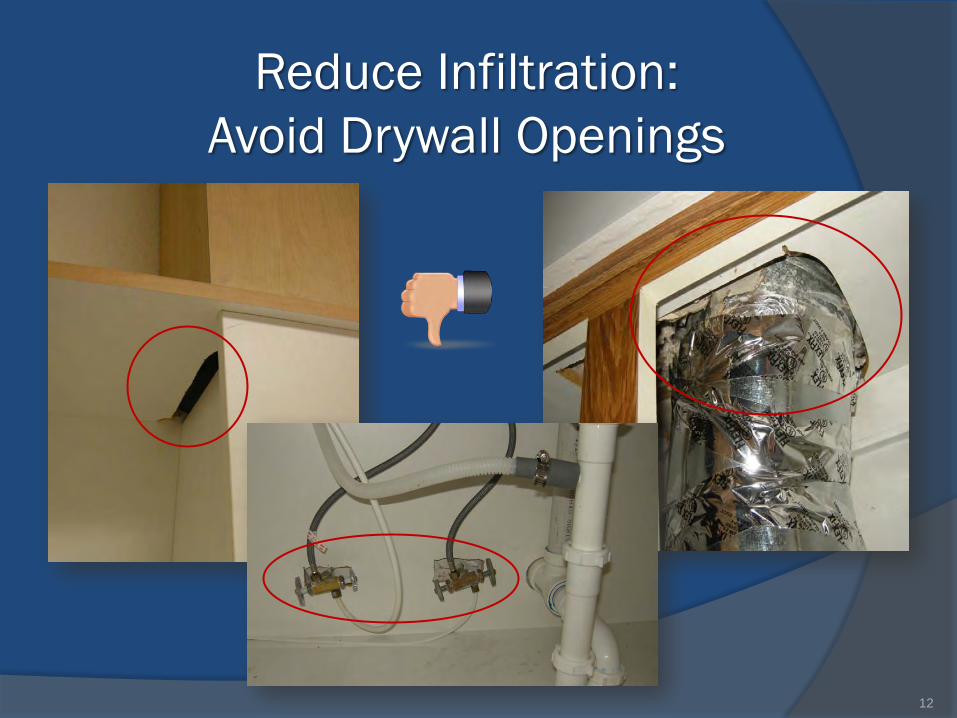

Reduce Infiltration: Avoid Drywall Penetrations

10

Seal Penetrations/Install Insulation Properly

11

Reduce Infiltration: Avoid Drywall Openings

12

Large holes between air handler closet and attic were a large source of infiltration in this retrofit.

Reduce Infiltration: Seal Air Handler Closet

Looking up toward the ceiling, air handler is on the right

13

Avoid Buried/Compressed Ductwork

Burying ducts with blown insulation lowers the surface temperature of the duct work, creating a condensation risk. Ducts should be strapped above the insulation where ever

possible per Florida mechanical code 14

Add Insulation & Radiant Barriers

R-38 Insulation in vented attics Radiant Barrier with low emissivity

Air barrier required @ garage/truss bay

15

Appliances

Energy Star Low Energy use (ranges & HWH) HWH, washer & dryer outside conditioned space For a regular HWH, install most efficient and wrap with R-5 blanket

**Heat pump WH most efficient-Energy Star •Needs 1,000 cubic feet of space •Temperatures of 40°-90° F

16

Electric fixtures

Max 100 W bathroom fixtures Energy Star fans/lights Install CFL or LED light bulbs only

17

Plumbing

Toilets 1.28 gal/flush Shower heads max 1.6 gpm Aerators 1.5 gpm Lavatory faucets 1.6 to 1.0 gpm + aerator Gutters and downspouts installed (downspouts directing

water at least 3’ from building or into stormwater collector for reuse)

18

Windows Impact Energy Efficient windows U-Factor=0.6 SHGC<0.27 recommended) Install window screens Add window tint (if window is not being replaced) U-Factor=0.87

SHGC=<0.4- Not Every tint is adequate

19

Other Stuff

Manage Energy Consumption Assess Performance Set Goals Create A Plan & Implement Evaluate/Tune-Up

Train The User of The Space Understanding Their Building Applying Simple EE Tasks (i.e., thermostat

settings, driving habits, etc)

The Bottom Line

SOUTH DISTRICT

ENERGY and the ENVIRONMENT

N 2 2012Nov 2, 2012

ENERGY & the Environment

Jon IglehartDirector

Florida Department ofFlorida Department of Envrionmental Protection

South District

Website: www.dep.state.fl.us/southp

11/2/2012 2

Contact Information Florida Department of Environmental

ProtectionProtection 2295 Victoria Ave, Fort Myers Fl.

S it 364Suite 364 P.O. Box 259

Fort Myers, Fl, 33902 – 2549Phone: 239 – 334 – 5600Phone: 239 334 5600

OMBUDSMANt ll @d t t [email protected]

11/2/2012 3

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Pat Steed Central Florida Regional Planning Council

Energy Resiliency Strategy

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

3500 BC--Fixed wheels on carts are invented - the first wheeled vehicles in history. Other early

wheeled vehicles include the chariot.

Transportation and Land Use

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

181-234—The wheelbarrow is invented.

1662-- Blaise Pascal invents the first public bus - horse-drawn, regular route,

schedule, and fare system

Transportation and Land Use

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

1790 Modern bicycles invented

Transportation and Land Use

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

1862--Jean Lenoir makes a gasoline engine automobile

Transportation and Land Use

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

1903 The Wright Brothers invent and fly the first engine airplane

Transportation and Land Use

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

1964 Bullet train invented

Transportation and Land Use

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

1981--Space Shuttle launched

Transportation and Land Use

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

1925 Primary mode of transportation becomes the automobile

Transportation and Land Use

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

1925 Primary mode of transportation becomes the automobile

2012 Primary mode of transportation remains the automobile

Transportation and Land Use

AND

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Transportation and Land Use

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Transportation and Land Use

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Transportation and Land Use

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Transportation and Land Use

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

16

Existing System Cannot Meet Demand Congested Corridors, 2025

Source: Florida Department of Transportation

16

17

Cross-Modal Integration: Florida’s Future Supply Chain?

Ocean transit Port discharge to rail Rail line-haul

Highway delivery

Inland Rail Terminal

Distribution center

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Central and Southwest Florida: 2005

Developed Land

Conservation Lands Permanently Protected

Central and Southwest Florida: 2060 Trend

Developed Land

Conservation Lands Permanently Protected

Changing Demographics Complete Streets

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Enhancing and Creating Resilient Communities

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

H2O Car?

Electric Car?

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Fueled by Natural Gas?

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Transportation of the Future Poster Contest

Jonathan Concepcion

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Transportation and Land Use

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Resiliency Analysis: Natural Gas and Gasoline

Jay McLeod Central Florida Regional Planning Council

Energy Resiliency Strategy

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Natural Gas

Economic Resiliency Modeling

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Background: Electricity Generation

• Within a decade, FL projected to rely on natural gas for ~60% of electricity generation

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Past Prices

Taken from 2012 FL Energy Summit presentation (by Buck Martinez), without permission.

Current price: ~$2.00

Previous trend: ~$6.00

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Learning From the Past – What to model?

Taken from 2012 FL Energy Summit presentation (by Buck Martinez), without permission.

Current price: ~$2.00

Supply disruption: price spike to ~$12.00 for ~6 months

Future price: ???

Previous trend: ~$6.00

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

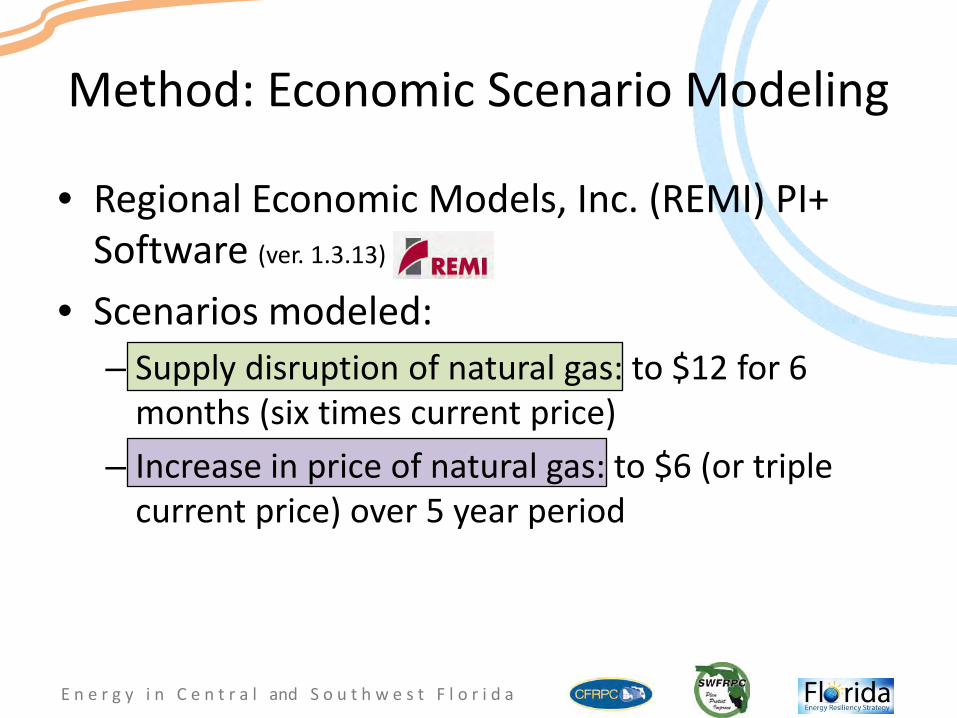

• Regional Economic Models, Inc. (REMI) PI+ Software (ver. 1.3.13)

• Scenarios modeled: – Supply disruption of natural gas: to $12 for 6

months (six times current price) – Increase in price of natural gas: to $6 (or triple

current price) over 5 year period

Method: Economic Scenario Modeling

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

State of Florida

Scenario = Statewide six month natural gas shortage (with price spike to 6X current price)

Region = Entire State

Today (2012)

Loss in first year

Loss over first year

Avg. Annual Loss

over five years

Avg. Annual

Loss over 5 years

Total Employment 10,234,017 -126,128 -1.19% -44,877 -0.41% Gross Domestic Product (billions of 2005 dollars) $767.7 -$10.760 -1.35% -$4.33 -0.52% Real Disposable Personal Income (billions of 2005 dollars) $675.2 -$21.702 -3.11% -$6.01 -0.84% Source: Florida Regional Planning Councils, Energy Resiliency Strategies project, modeled using REMI PI+ v1.3.13, 2012.

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Southwest Florida RPC

Scenario = Statewide six month natural gas shortage (with price spike to 6X current price) Region =

Southwest FL RPC

Today (2012)

Loss in first year

(2013)

Difference over first

year

Avg. Annual

Loss over five years

Avg. Annual

Loss over 5 years

Total Employment 771,984 -11,224 -1.39% -3,988 -0.48% Gross Domestic Product (billions of 2005 dollars) $50.2 -$0.847 -1.61% -0.338 -0.61% Real Disposable Personal Income (billions of 2005 dollars) $64.7 -$2.086 -3.09% -0.58 -0.82% Source: Florida Regional Planning Councils, Energy Resiliency Strategies project, modeled using REMI PI+ v1.3.13, 2012.

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

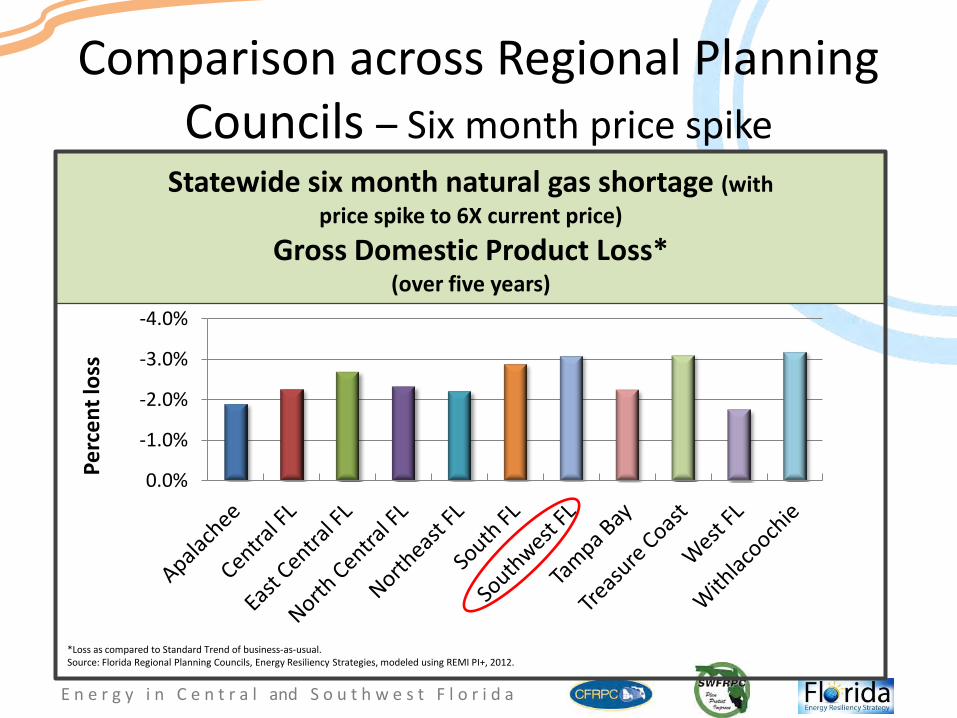

Comparison across Regional Planning Councils – Six month price spike

-3.0%

-2.0%

-1.0%

0.0%

Perc

ent l

oss

Statewide six month natural gas shortage (with price spike to 6X current price)

Total Employment Loss* (over five years)

*Loss as compared to Standard Trend of business-as-usual. Source: Florida Regional Planning Councils, Energy Resiliency Strategies, modeled using REMI PI+, 2012.

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Comparison across Regional Planning Councils – Six month price spike

-4.0%

-3.0%

-2.0%

-1.0%

0.0% Perc

ent l

oss

Statewide six month natural gas shortage (with price spike to 6X current price)

Gross Domestic Product Loss* (over five years)

*Loss as compared to Standard Trend of business-as-usual. Source: Florida Regional Planning Councils, Energy Resiliency Strategies, modeled using REMI PI+, 2012.

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

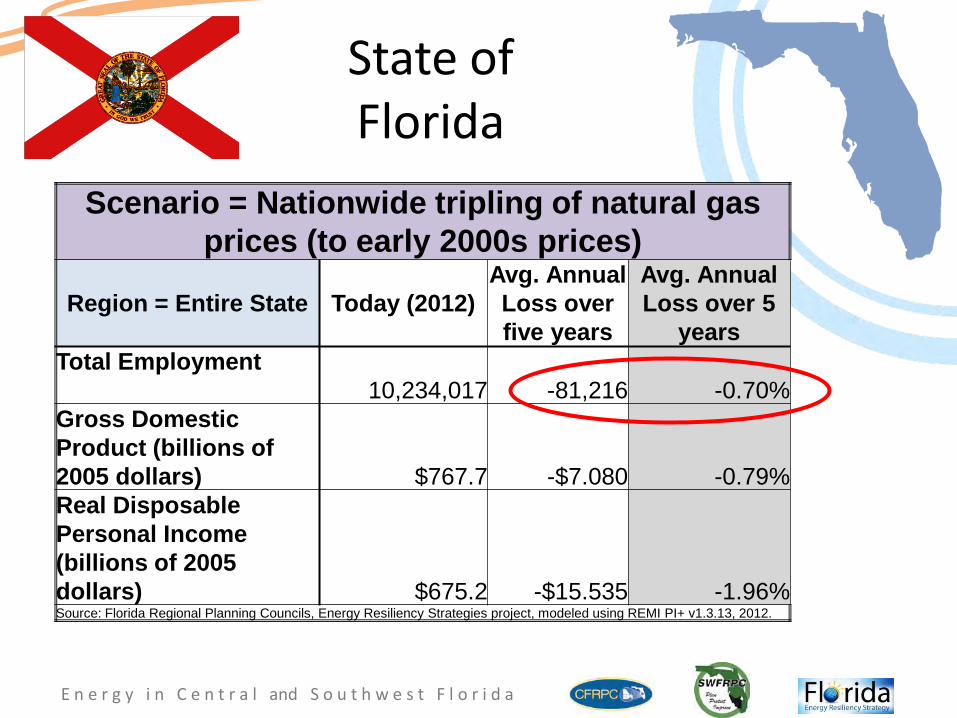

State of Florida

Scenario = Nationwide tripling of natural gas prices (to early 2000s prices)

Region = Entire State Today (2012) Avg. Annual Loss over five years

Avg. Annual Loss over 5

years Total Employment 10,234,017 -81,216 -0.70% Gross Domestic Product (billions of 2005 dollars) $767.7 -$7.080 -0.79% Real Disposable Personal Income (billions of 2005 dollars) $675.2 -$15.535 -1.96% Source: Florida Regional Planning Councils, Energy Resiliency Strategies project, modeled using REMI PI+ v1.3.13, 2012.

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Southwest Florida RPC

Scenario = Nationwide tripling of natural gas prices (to early 2000s prices)

Region = Southwest FL RPC Today (2012)

Avg. Annual Loss over five years

Avg. Annual Loss over 5

years Total Employment 771,984 -7,066 -0.79% Gross Domestic Product (billions of 2005 dollars) $50.2 -$0.56 -0.93% Real Disposable Personal Income (billions of 2005 dollars) $64.7 -$1.544 -1.97% Source: Florida Regional Planning Councils, Energy Resiliency Strategies project, modeled using REMI PI+ v1.3.13, 2012.

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Comparison across Regional Planning Councils - Back to early 2000s prices

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

Perc

ent l

oss

Nationwide tripling of natural gas prices (to early 2000s prices)

Total Employment Loss* (over five years)

*Loss as compared to Standard Trend of business-as-usual. Source: Florida Regional Planning Councils, Energy Resiliency Strategies, modeled using REMI PI+, 2012.

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Comparison across Regional Planning Councils - Back to early 2000s prices

-6.0% -5.0% -4.0% -3.0% -2.0% -1.0% 0.0%

Perc

ent l

oss

Nationwide tripling of natural gas prices (to early 2000s prices)

Gross Domestic Product Loss* (over five years)

*Loss as compared to Standard Trend of business-as-usual. Source: Florida Regional Planning Councils, Energy Resiliency Strategies, modeled using REMI PI+, 2012.

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Gasoline

Economic Resiliency Modeling

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Gasoline Usage

• Roughly 98% of automobiles in US use diesel or unleaded gas – Less than 1% Electric – Roughly 2.5% are hybrid

• Future goals/trends: – USA Goal – Have 1,000,000 electric cars by 2020 – That’s still less than 10% of all cars

• ExxonMobil projects petroleum will be fuel for ~90% of global transportation by 2040

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

8 Year Historical Price Chart

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Scenario Modeling: Gas Price Increase

$3.50 $5.00

$7.00

$10.00 $10.00

$-

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

2012 2013 2014 2015 2016

National Retail Gasoline Price

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

State of Florida Nationwide increasing gasoline prices

Today (2012)

Average Annual Loss @ $5/gallon

Average Annual Loss @ $7.5/gallon

Average Annual Loss @ $10/gallon

US Employment 178,913,875 -5.8 Million -9.9 Million -16.3 Million

FL Employment 10,284,524 -322,000 -536,000 -885,000 Percent of FL Employment 100% -3.06% -5.01% -8.12%

FL GDP (2012 $ Billion) $883 - $28 - $49 - $82

FL Income (2012 $ Billion) $927 - $15 - $26 - $45

Source: Florida Regional Planning Councils, Energy Resiliency Strategies project, modeled using REMI PI+ v1.3.13, 2012.

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

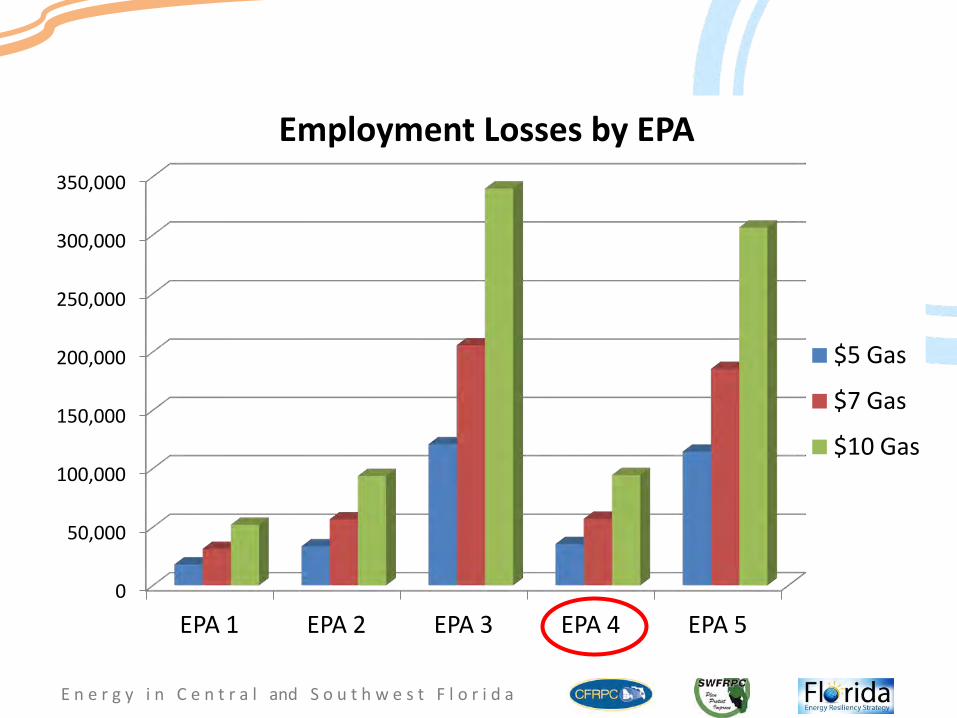

EPA 1 EPA 2 EPA 3 EPA 4 EPA 5

Employment Losses by EPA

$5 Gas

$7 Gas

$10 Gas

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

EPA 1 EPA 2 EPA 3 EPA 4 EPA 5

Employment Percent Losses by EPA

$5 Gas $7 Gas $10 Gas

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Conclusion

• Energy resiliency is important to economic resiliency.

• Energy price increases and supply disruptions have varying economic impacts.

• Planning for energy resiliency can have large economic benefits.

E n e r g y i n C e n t r a l and S o u t h w e s t F l o r i d a

Thank you

Jay McLeod Central Florida Regional Planning Council

www.cfrpc.org