SOUTH AFRICAN REVENUE SERVICE - World...

50

SOUTH AFRICAN REVENUE SERVICE Tax Administration Reform Case Study Presentation by Mbongeni Manqele Transformation Director And Leonard Radebe General Manager - Operations

Transcript of SOUTH AFRICAN REVENUE SERVICE - World...

SOUTH AFRICAN REVENUE SERVICETax Administration Reform

Case Study

Presentation by Mbongeni ManqeleTransformation Director

AndLeonard Radebe

General Manager - Operations

Background

In order to meet our Transformation deadline… The project team is finding innovative methods to save time.

Some fun before we start

1996

1996/7

Katz CommissionTax Administration ReformTax Policy ReformFiscal Reform.

SARS as an Autonomous Agency

Integrating Internal Revenue and Customs

1998/9

Harmonising SARS2000

2004

2009

Siyakha 1Conducted a Diagnostic;Set Objectives;

Enhance Revenue Collection through enforcement;Improve effectiveness and efficiency of core business processes through standardisation;Improve customer service and education; andDevelop a high performing organisation.Standardise processesCapacitate SARS via people enablement & role clarityExcluded major technology enhancements

First

serie

s of

chan

ge

Renewed transformation

initiatives

WHERE HAVE WE COME FROM?

SARS Transformation from 1996…

SARS Autonomy

• Establishment of SARS

• Objectives

• Functions

• Powers

SARS ACT (1997)

SARS VOLUMETRICS

1,7 Million Import Transactions

1,8 Million SACU Movements

1851 Total Seizures

68, 775 Consignment

stopped

300, 268 PAYE

Employers

4,3 MillionIndividualTaxpayers

14 Million Passengers

moving through Customs

573, 876 VAT

Vendors

1, 4 Million Corporate Taxpayers

998, 221 Export

Transactions

14 Million Returns Processed

14 600 SARSEMPLOYEES

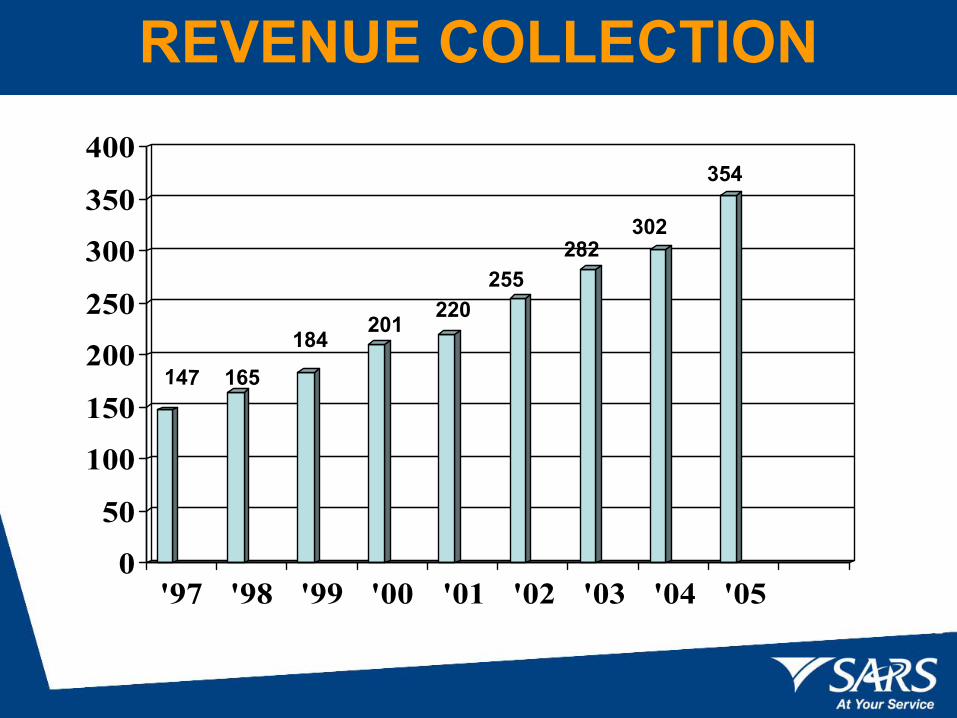

REVENUE COLLECTION

0

50

100

150

200

250

300

350

400

'97 '98 '99 '00 '01 '02 '03 '04 '05

147 165

184201

220255

282302

354

STAFF PLACEMENTS

KZN 1280

W.C. 1518

E.C. 837

F.S. 611

GAUTENG 2278

CUSTOMS 2540

The Situation

THE BEGINNING OF THE JOURNEY

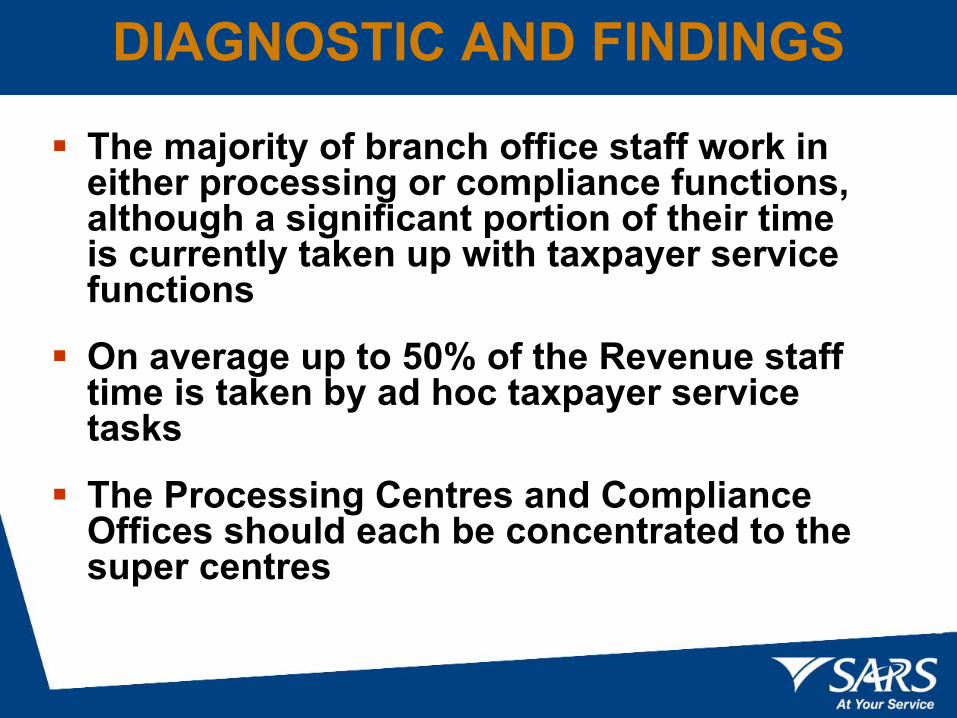

Diagnostic and Findings

DIAGNOSTIC AND FINDINGSDIAGNOSTIC AND FINDINGS

Lack of a clearly defined strategy which could shape and guide the activities of the organisation

The existence of a significant tax gap, which denoted the revenue effect of non-compliance and organisational inefficiency

Inefficient and non-standardised Core business processes, leading to an organisational structure that functioned sub-optimally

Weak Human Resource practices, affecting in particular the training and development of staff, and the creation of a performance-driven management culture; and

A poor service culture in delivering services aligned to the needs of taxpayers, traders and the public at large.

DIAGNOSTIC AND FINDINGSDIAGNOSTIC AND FINDINGS

DIAGNOSTIC AND FINDINGS

The majority of branch office staff work in either processing or compliance functions, although a significant portion of their time is currently taken up with taxpayer service functions

On average up to 50% of the Revenue staff time is taken by ad hoc taxpayer service tasks

The Processing Centres and Compliance Offices should each be concentrated to the super centres

Processing Centres should be located in large out of town one storey buildings while Compliance Offices can be located in current SARS buildings

In assessing the impact of concentration on a typical office the staff demographics need to be considered

These Processing Centres and Compliance Offices will form separate business units reporting to Executives

DIAGNOSTIC AND FINDINGS

SARS PERFORMED

SIGNIFICANTLY BELOW ITS FULL

POTENTIAL

SARS Performed Significantly Below Its Full Potential

Strategy is not clearly defined

Organisation structure does not operate

efficiently

Core businessprocesses arevery inefficient

HR practices arein transition, but

are weak

Significant tax gap remains

SARS PERFORMEDSIGNIFICANTLY BELOW ITS FULL POTENTIAL

Strategy is not clearly defined

Organisation structure does not operate

efficiently

Core businessprocesses arevery inefficient

Significant tax gap remains

HR practices arein transition, but

are weak

STRATEGY

Senior management did not believe that a clear strategy existed and was understood by the organisation

Taxpayer strategy had not been clearly defined and communicated to taxpayers

SARS CURRENTLY PERFORMS SIGNIFICANTLY BELOW ITS FULL POTENTIAL

Strategy was not clearly defined

Organisation structure did not operate

efficiently

Core businessprocesses werevery inefficient

HR practices werein transition, but

are weak

Significant tax gap remains

ORGANISATION STRUCTURESenior management believed that the current structure did not function efficiently

Roles and responsibilities were not clearly defined

within managementbetween Head Office, Regional and Branch Offices

Branches have become “little empires” with significant differences in

performanceprocesses

Customs and Revenue as were two separate organizations, duplicating a number of activities where synergies were possible

The structure was too bureaucratic, with too many layers of management and too narrow spans of control

Senior management decision-making was efficient

ORGANISATION STRUCTURE

ORGANISATION STRUCTURE

SARS was organized around functions, not around processes

SARS was not sufficiently customer focused

The law administration function was treated differently by Revenue and by Customs

SARS CURRENTLY PERFORMS SIGNIFICANTLY BELOW ITS FULL POTENTIAL

Strategy was not clearly defined

Organisation structure did not operate

efficiently

Core businessprocesses werevery inefficient

HR practices werein transition, but

were weak

Significant tax gap remains

CORE BUSINESS PROCESSES

Core processes were not efficient

Process duplication existed between tax types

Many processes were performed at sub-scale locations

Processes did not prioritize work

Process efficiencies varied significantly between offices, due to lack of adequate performance targets/measures

Processes were fragmented, and contained too many handoffs and too many steps

CORE BUSINESS PROCESSES

Processes retained high levels of duplicative, manual tasks that had to be automated

Information flows/hand-offs between processes was not efficient

Internal processing delays resulting from non-prioritization and lack of training resulted in long wait times

CORE BUSINESS PROCESSES

SARS CURRENTLY PERFORMED SIGNIFICANTLY BELOW ITS FULL POTENTIAL

Strategy was not clearly defined

Organisation structure did not operate

efficiently

Core businessprocesses werevery inefficient

HR practices werein transition, but

were weak

Significant tax gap remains

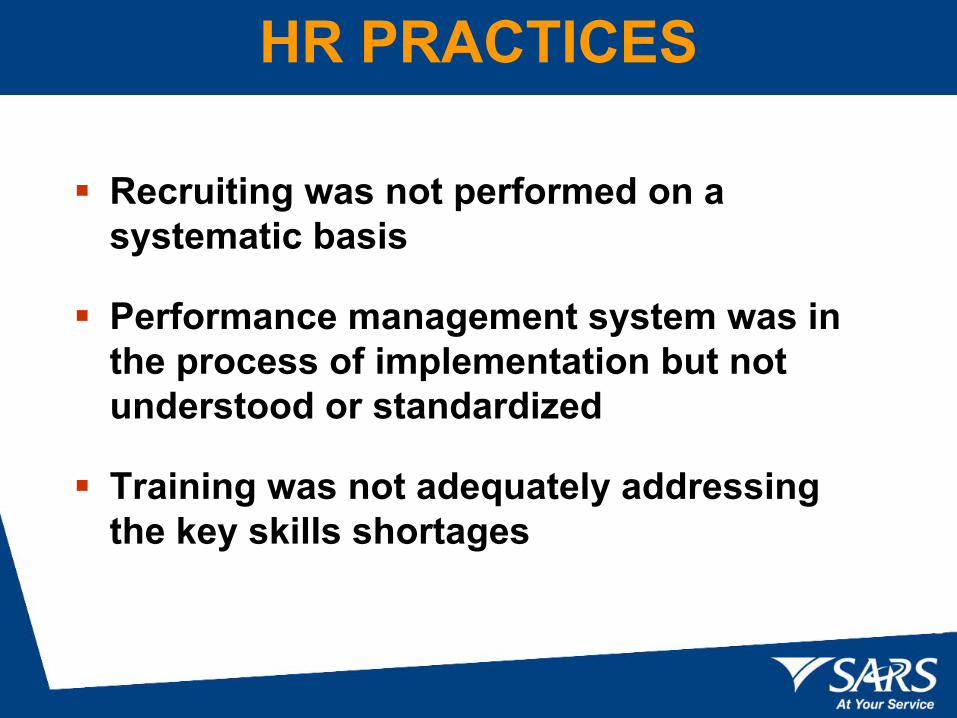

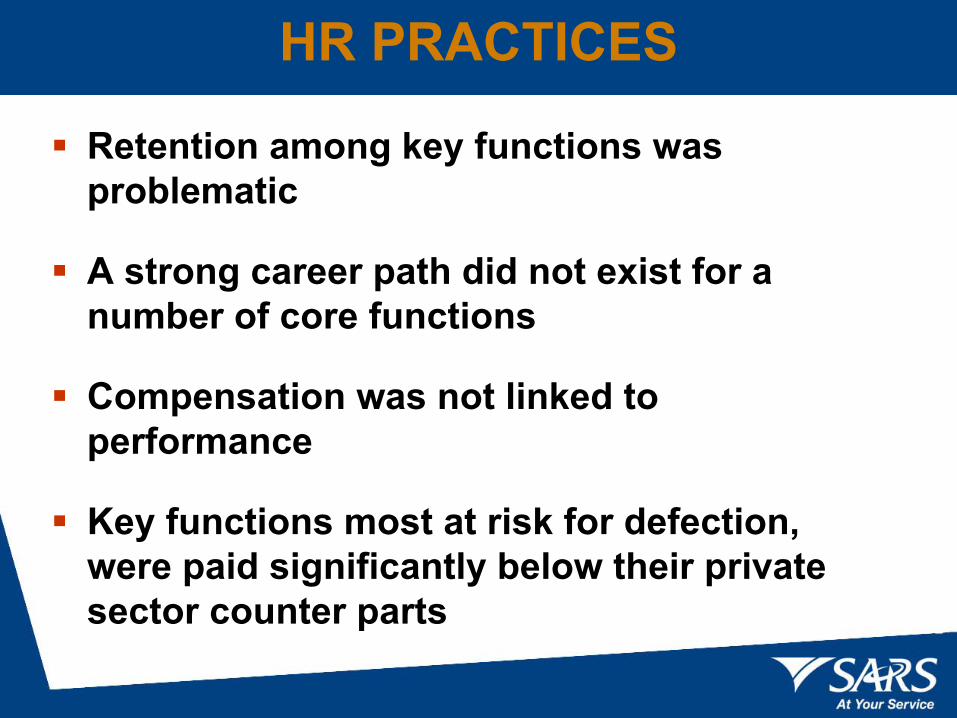

HR PRACTICES

Current state of HR was a legacy of historic SARS practices

Employee morale was low

Allocation of employees to functions was sub-optimal

Recruiting was not performed on a systematic basis

Performance management system was in the process of implementation but not understood or standardized

Training was not adequately addressing the key skills shortages

HR PRACTICES

Retention among key functions was problematic

A strong career path did not exist for a number of core functions

Compensation was not linked to performance

Key functions most at risk for defection, were paid significantly below their private sector counter parts

HR PRACTICES

SARS CURRENTLY PERFORMS SIGNIFICANTLY BELOW ITS FULL POTENTIAL

Strategy was not clearly defined

Organisation structure did not operate

efficiently

Core businessprocesses werevery inefficient

HR practices werein transition, but

were weakSignificant tax

gap remains

HR PRACTICES

SIGNIFICANT TAX GAP REMAINS

“Between 25 and 30 percent of businesses in South Africa where not paying taxes, while the majority of the population - who where marginalised in the past - had not been incorporated in the system.”- Pravin Gordhan, SARS Commissioner

RESULTANT STRATEGIC GOALS

High levels of compliance across the taxpayer base

High levels of taxpayer service

Broadening tax base through taxpayer education

Responsible enforcement and border and industry protection

Efficiency and fairness in administrationeffective management and decision makingefficient processesclear and unambiguous policies and procedures

Motivated and competent Human Capital that is also representative of the broad South African society

Pro-active collaboration with RSA Government in influencing taxation legislation and policies

RESULTANT STRATEGIC GOALS

OUR TRANSFORMATION AGENDA

Diagnostics

SARS Transformation Agenda

Resultant Strategic Goals

WHAT SUCCESSFUL TRANSFORMATION WOULD LOOK LIKE

WHAT SUCCESSFUL TRANSFORMATION WOULD LOOK LIKE

Changed the physical environmentChanged the culture and collective mindsetRe-engineered business processesEnabling technologyChanged demographic profile of our workforceChanged leadership ethos and structureChanged organisational structure

THE BIRTH OF SIYAKHA

OBJECTIVES OF SIYAKHAOBJECTIVES OF SIYAKHA

Enhance Revenue Collection through enforcement;Improve effectiveness and efficiency of core business processes through standardisation;Improve customer service and customer education;Develop a high performing organisation;Structural change in terms of physical and organisational infrastructure;Capacitate SARS via people enablement and role clarity, and excluded major technology enhancement.

THE NEW SARS’ BUSINESS CHALLENGETHE NEW SARS’ BUSINESS CHALLENGE

Reducing the tax gapImproving taxpayer and other stakeholder service (importers, exporters, intermediaries, etc)Reducing the costs of complianceImproving the protection of the economyFacilitating legitimate trade

CENTRALISED ENFORCEMENTCENTRALISED ENFORCEMENT

Compliance Centres have resulted in scarce expertise being identified, enabling experience sharing among staff, this has also led to risk methods and audit systems being standardised and adopted – and deployed across all tax types.

PROCESS FOCUSPROCESS FOCUS

Fundamental shift from a silo-based product approach to a functional and process driven view. Taxpayer Service Centres, supported by Call Centres and Processing Centres, enable frontline staff to focus on meeting the needs of all taxpayers.

BETTER CUSTOMER EXPERIENCEBETTER CUSTOMER EXPERIENCE

Better customer experiences with heightened taxpayer respect for the way we interact with themEnhanced human capacity in better skilled, motivated and empowered people

PEOPLE PROCESSPEOPLE PROCESS

Building professional working environmentsProviding people with necessary toolsBuilding cross functional teamsCreating a sense of positive direction through engagement

KEY INITIATIVES

Concentrate registration, assessment, collection and audit processes

Develop centrally coordinated taxpayer service strategy

Break product silos and introduce standardised process irrespective of tax type

Audit prioritisation based on risk profiling

Move to electronic filing for majority of revenue collected

Flatten organisation structure and organise in teams

Human Resourcesperformance based team incentives

performance measures linked to appropriate staffing levels

KEY INITIATIVES

42 BRANCHES

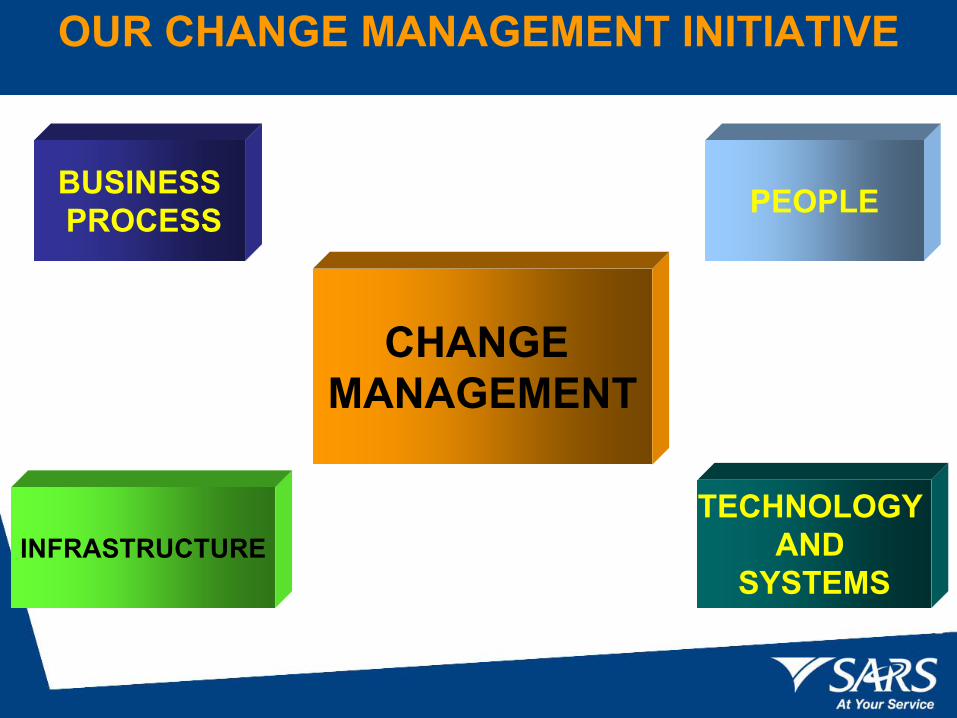

CENTRALISATION

BUSINESSPROCESS PEOPLE

CHANGE MANAGEMENT

TECHNOLOGY AND

SYSTEMSINFRASTRUCTURE

OUR CHANGE MANAGEMENT INITIATIVE

OUR SUCCESS STORY

Leadership buy-in and commitmentEmployee buy-in and support

Large scale interventions

THANK YOU