SORP 2005 Statement of recommended practice. Contents What is changing What is changing SORP 2005...

21

SORP 2005 SORP 2005 Statement of Statement of recommended practice recommended practice

-

Upload

kelley-kennedy -

Category

Documents

-

view

219 -

download

1

Transcript of SORP 2005 Statement of recommended practice. Contents What is changing What is changing SORP 2005...

SORP 2005SORP 2005

Statement of Statement of recommended practicerecommended practice

ContentsContents

What is changingWhat is changing SORP 2005SORP 2005 Charities ActCharities Act

Trustee responsibilities for Accounts Trustee responsibilities for Accounts and reportsand reports

RequirementsRequirements Book keepingBook keeping Receipts and Payments accountsReceipts and Payments accounts Accruals accountsAccruals accounts The Annual reportThe Annual report

What changes under SORP What changes under SORP 20052005

It applies to ALL churchesIt applies to ALL churches It applies to all accounts for It applies to all accounts for

periods ending after 31 March periods ending after 31 March 20062006

The accounts and annual report The accounts and annual report are effectively combinedare effectively combined

The report and accounts should The report and accounts should show how the church has show how the church has performed against its objectivesperformed against its objectives

What is comingWhat is coming A new Charities Act probably in 2007A new Charities Act probably in 2007 Churches will cease to be “excepted” Churches will cease to be “excepted”

and be covered by normal Charities and be covered by normal Charities act and treated like all other charities act and treated like all other charities probably from October 2007probably from October 2007

Only largest churches will need to Only largest churches will need to register (> £100,000 turnover)register (> £100,000 turnover) Others can registerOthers can register Registered churches will get a Charity Registered churches will get a Charity

NumberNumber Registered charities must submit a Registered charities must submit a

return to the Charity Commissionersreturn to the Charity Commissioners

Trustee responsibilitiesTrustee responsibilities

The report and accounts are the The report and accounts are the responsibility of the Trustees not responsibility of the Trustees not just the Treasurer!just the Treasurer!

The Trustees are accountable for The Trustees are accountable for the way the resources are usedthe way the resources are used Usually the Elders Meeting are the Usually the Elders Meeting are the

TrusteesTrustees Status of finance should be Status of finance should be

reviewed regularlyreviewed regularly

The Annual reportThe Annual report It should tell the story of the church It should tell the story of the church What is the church trying to doWhat is the church trying to do How is it going about itHow is it going about it Content is more definedContent is more defined Should contain the following sections:Should contain the following sections:

Reference and administrationReference and administration Structure, governance and managementStructure, governance and management Objectives and activitiesObjectives and activities Achievements and performanceAchievements and performance Financial reviewFinancial review Plans for future periodsPlans for future periods

Statement from Auditor/ExaminerStatement from Auditor/Examiner

The Annual Report - 1The Annual Report - 1

It must contain:It must contain: Administration detailsAdministration details

– The name of the church or charityThe name of the church or charity– Charity Registration number (if Charity Registration number (if

applicable)applicable)– The address of the church and for The address of the church and for

correspondence if differentcorrespondence if different– The names of the trusteesThe names of the trustees

Usually the serving elders Usually the serving elders Including those retiring and Including those retiring and

appointed during accounting period appointed during accounting period & up to approval date& up to approval date

The Annual Report - 2The Annual Report - 2 The constitution or legal frameworkThe constitution or legal framework

The URC ActsThe URC Acts Appointment of trusteesAppointment of trustees Objectives and purposeObjectives and purpose Achievements and performanceAchievements and performance

Numbers or members, average attendanceNumbers or members, average attendance Special eventsSpecial events

Purpose of special or designated fundsPurpose of special or designated funds Reserves policyReserves policy The accounts and report should be The accounts and report should be

presented and approved by Elders or a presented and approved by Elders or a church meetingchurch meeting

Size of accountsSize of accounts Based on greater of income or expenditureBased on greater of income or expenditure Up to £10,000Up to £10,000

Receipts and payments and assets and liabilities; Receipts and payments and assets and liabilities; no independent examinationno independent examination

£10,000 to £100,000£10,000 to £100,000 Receipts and payments and assets and liabilities; Receipts and payments and assets and liabilities;

independent examinationindependent examination £100,000 to £250,000£100,000 to £250,000

Accrual accounting, statement of financial Accrual accounting, statement of financial activities plus balance sheet; independent activities plus balance sheet; independent examinationexamination

Over £250,000Over £250,000 Accrual accounting, statement of financial Accrual accounting, statement of financial

activities plus balance sheet; auditactivities plus balance sheet; audit Smaller churches can use accrual accounting; Smaller churches can use accrual accounting;

larger churches must use itlarger churches must use it

Book keepingBook keeping Keep it simpleKeep it simple Show all transactions as grossShow all transactions as gross

Keep records for EVERY transactionKeep records for EVERY transaction Separate fundsSeparate funds

UnrestrictedUnrestricted DesignatedDesignated RestrictedRestricted EndowmentEndowment

Reconcile against bank Reconcile against bank statementsstatements

Take care over cash handlingTake care over cash handling

Receipts and paymentsReceipts and payments Must include all funds of church Must include all funds of church

including those of sub-groupsincluding those of sub-groups Simply adds all common Simply adds all common

transactions for the yeartransactions for the year Classifications for income:Classifications for income:

Planned giving; gift aid; grants; money Planned giving; gift aid; grants; money raising; letting; investment income; other raising; letting; investment income; other incomeincome

For expenditureFor expenditure M&M; charitable giving; ministry M&M; charitable giving; ministry

expenses; manse costs; building expenses; manse costs; building maintenance; worship costs; capital maintenance; worship costs; capital expenditure; other costsexpenditure; other costs

Assets and liabilitiesAssets and liabilities Must include ALL assets and all accountsMust include ALL assets and all accounts AssetsAssets

Cash and bank depositsCash and bank deposits Other monetary assetsOther monetary assets

Loans; tax claims made; unpaid accountsLoans; tax claims made; unpaid accounts InvestmentsInvestments Fixed AssetsFixed Assets

Buildings; manses; equipment; cars; Buildings; manses; equipment; cars; LiabilitiesLiabilities

Amounts owed but not paidAmounts owed but not paid Special collections not forwardedSpecial collections not forwarded Grant commitmentsGrant commitments Loans & hire purchaseLoans & hire purchase

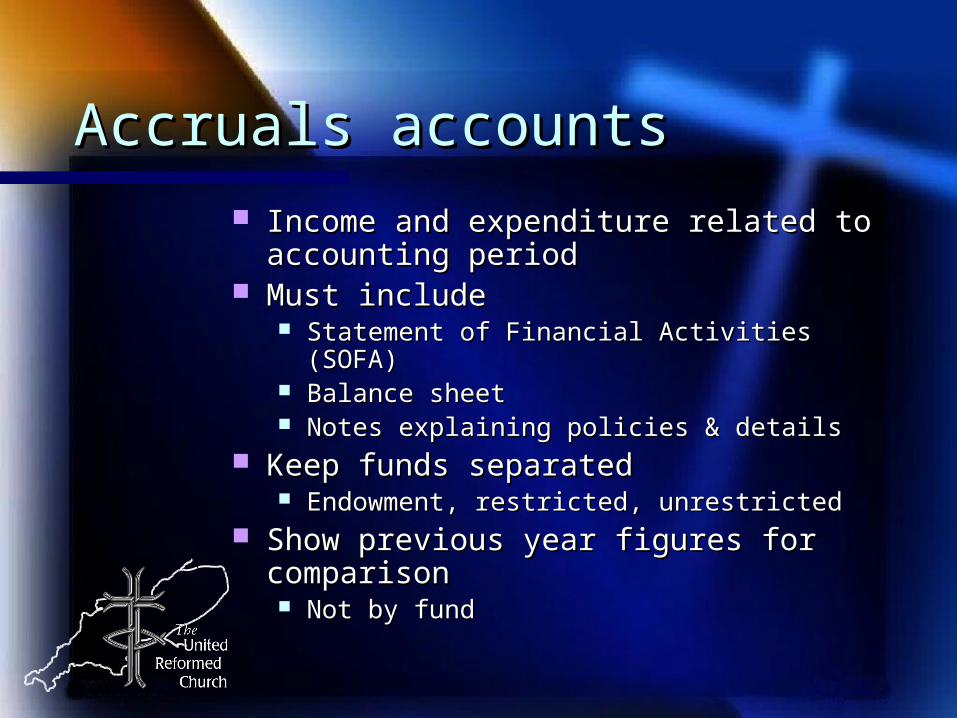

Accruals accountsAccruals accounts Income and expenditure related to Income and expenditure related to

accounting periodaccounting period Must includeMust include

Statement of Financial Activities (SOFA)Statement of Financial Activities (SOFA) Balance sheetBalance sheet Notes explaining policies & detailsNotes explaining policies & details

Keep funds separatedKeep funds separated Endowment, restricted, unrestrictedEndowment, restricted, unrestricted

Show previous year figures for Show previous year figures for comparisoncomparison Not by fundNot by fund

Statement of Financial Statement of Financial Activities (SOFA)Activities (SOFA)

Format is prescribed by Charity Format is prescribed by Charity CommissionCommission

IncomeIncome Voluntary incomeVoluntary income

Gifts, donations, collections, gift aid, Gifts, donations, collections, gift aid, legacieslegacies

Grants, gifts in kindGrants, gifts in kind– Details in notesDetails in notes

Activities for generating fundsActivities for generating funds Fund raising events, fees for weddings, Fund raising events, fees for weddings,

shop income, lettingsshop income, lettings Investment incomeInvestment income

Other incomeOther income

SOFA 2SOFA 2 ExpenditureExpenditure

Costs of generating fundsCosts of generating funds Costs of generating incomeCosts of generating income Costs of tradingCosts of trading Investment management feesInvestment management fees

Charitable activitiesCharitable activities M&MM&M Maintenance of church and manseMaintenance of church and manse Clergy expensesClergy expenses Charitable donationsCharitable donations

Governance costsGovernance costs Audit/examination costs and legal and Audit/examination costs and legal and

professional feesprofessional fees Other costsOther costs

SOFA 3SOFA 3

Show any transfers between Show any transfers between fundsfunds

Show any gains/losses on Show any gains/losses on assets and liabilities assets and liabilities (pensions)(pensions)

Show funds at start of year, Show funds at start of year, changes and end of yearchanges and end of year

SOFA notesSOFA notes Disclose details of significant Disclose details of significant

spend or income itemsspend or income items Disclose any payment to trustees Disclose any payment to trustees

including expensesincluding expenses Any wages or salary items split Any wages or salary items split

between salary, NI and pension between salary, NI and pension and average number of staffand average number of staff

If there is a defined benefit If there is a defined benefit pension scheme details are pension scheme details are requiredrequired

Explanation of any unusual itemsExplanation of any unusual items

Balance sheetBalance sheet Format is defined by SORPFormat is defined by SORP Must include all assets and liabilitiesMust include all assets and liabilities Fixed assetsFixed assets

Tangible, heritage, investmentsTangible, heritage, investments– Includes halls, buildings, manses, equipment, carsIncludes halls, buildings, manses, equipment, cars

Clarity required about depreciationClarity required about depreciation Current assetsCurrent assets

Cash, bank and deposit accounts, investments, Cash, bank and deposit accounts, investments, debtorsdebtors

LiabilitiesLiabilities Creditors due within 1 yearCreditors due within 1 year Loans and Long term liabilitiesLoans and Long term liabilities

Net assets/liabilitiesNet assets/liabilities Funds by typeFunds by type

Notes to accountsNotes to accounts

Accounting policies should Accounting policies should be set outbe set out

How assets are valuedHow assets are valued Major incoming and Major incoming and

outgoing resourcesoutgoing resources Purposes of specific fundsPurposes of specific funds Authorisation by trusteesAuthorisation by trustees

SummarySummary

The purpose of the report and The purpose of the report and accounts is to give a clear accounts is to give a clear picture of the churchpicture of the church What is happeningWhat is happening What is goodWhat is good Where there are weaknessesWhere there are weaknesses Actions planned for the futureActions planned for the future

What is plannedWhat is planned

The URC will offer guidanceThe URC will offer guidance The URC will produce shortly a The URC will produce shortly a

model Excel spreadsheet for the model Excel spreadsheet for the accountsaccounts Receipts and paymentsReceipts and payments

The Baptist Union has produced The Baptist Union has produced draft guidance notes which are gooddraft guidance notes which are good

The ACAT document has much The ACAT document has much supporting documentation and supporting documentation and adviceadvice