Sonic Corporation Equity Analysis and Valuation Final...

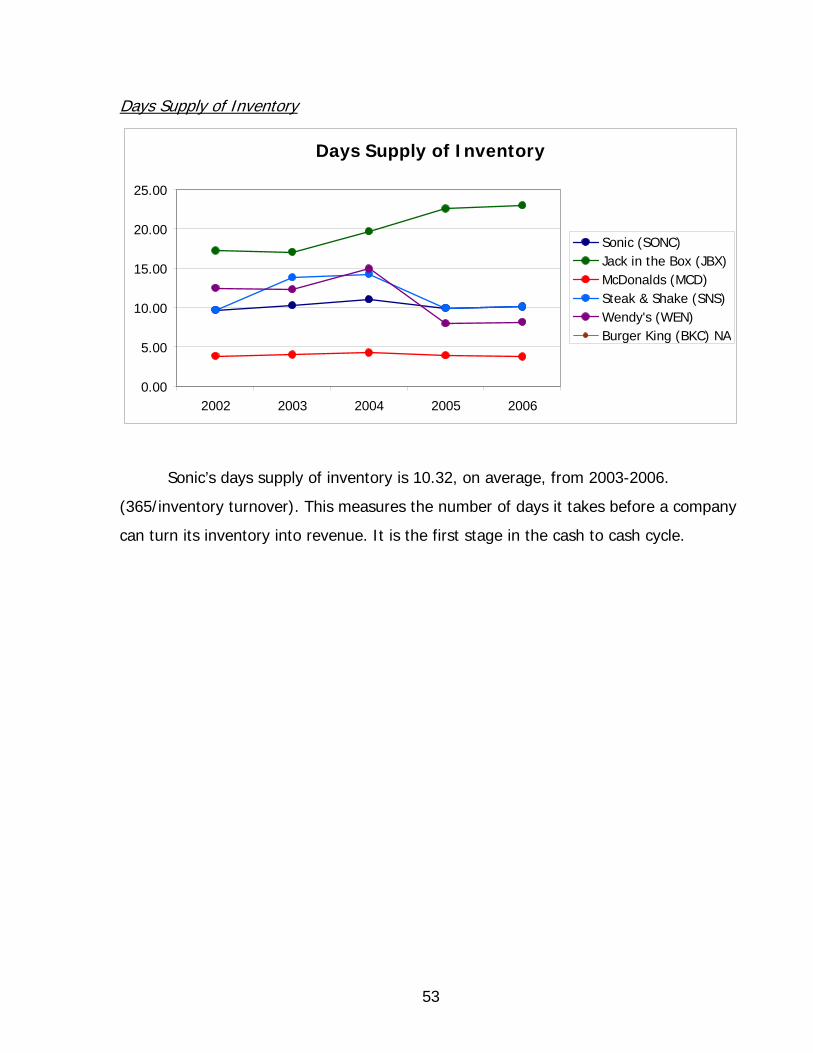

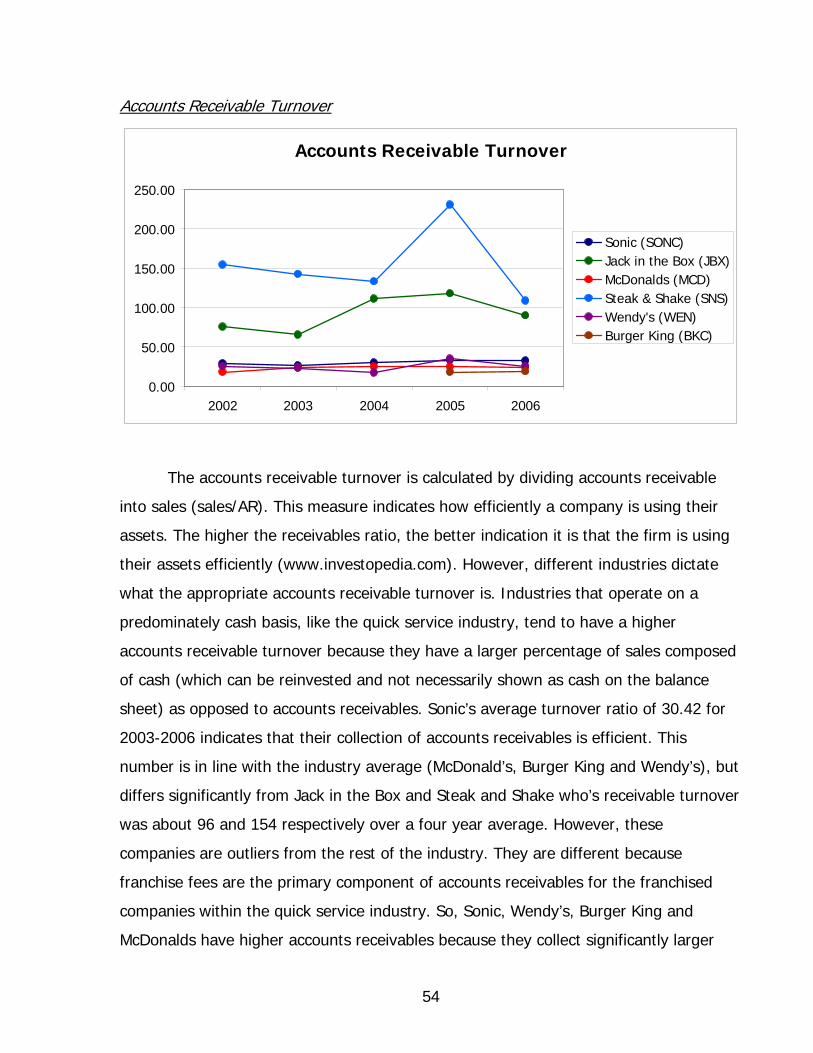

153

Sonic Corporation Equity Analysis and Valuation Analysis Group CJ Edgmon [email protected] Mel Shook [email protected] Nathan Fernandez [email protected] Chris Walker [email protected] Eddie Valls [email protected]

Transcript of Sonic Corporation Equity Analysis and Valuation Final...

Sonic Corporation Equity Analysis

and Valuation

Analysis Group

CJ Edgmon [email protected]

Mel Shook [email protected]

Nathan Fernandez [email protected]

Chris Walker [email protected]

Eddie Valls [email protected]

Table of Contents Executive Summary 4

Business and Industry Analysis 10

Company Overview 10

Industry Overview 12

Five Forces Model 13

Rivalry Among Existing Firms 14

Threat of New Entrants 17

Threat of Substitute Products 19

Bargaining Power of Customers 21

Bargaining Power of Suppliers 22

Value Chain Analysis 24

Firm Competitive Advantage Analysis 26

Accounting Analysis 29

Key Accounting Policies 29

Potential Accounting Flexibility 32

Actual Accounting Strategy 36

Qualitative Analysis of Disclosure 37

Quantitative Analysis of Disclosure 38

Potential “Red Flags” 46

Undo Accounting Distortions 47

Ratio Analysis, Forecast Financials, and Cost of Capital Estimation 49

Financial Analysis 49

Liquidity Analysis 49

Profitability Analysis 58

Capital Structure Analysis 64

Internal Growth Rate and Sustainable Growth Rate Analysis 69

Financial Statement Forecasting 71

Cost of Capital Estimation 74

Analysis of Valuations 77

Method of Comparables 77

Intrinsic Valuations 82

Analyst’s Recommendation 91

Appendix 93

Sales Manipulation Diagnostic Ratios 93

Core Expense Manipulation Diagnostic Ratios 94

Effects of Goodwill on Net Income Table 95

Capitalization of Operating Lease Tables 96

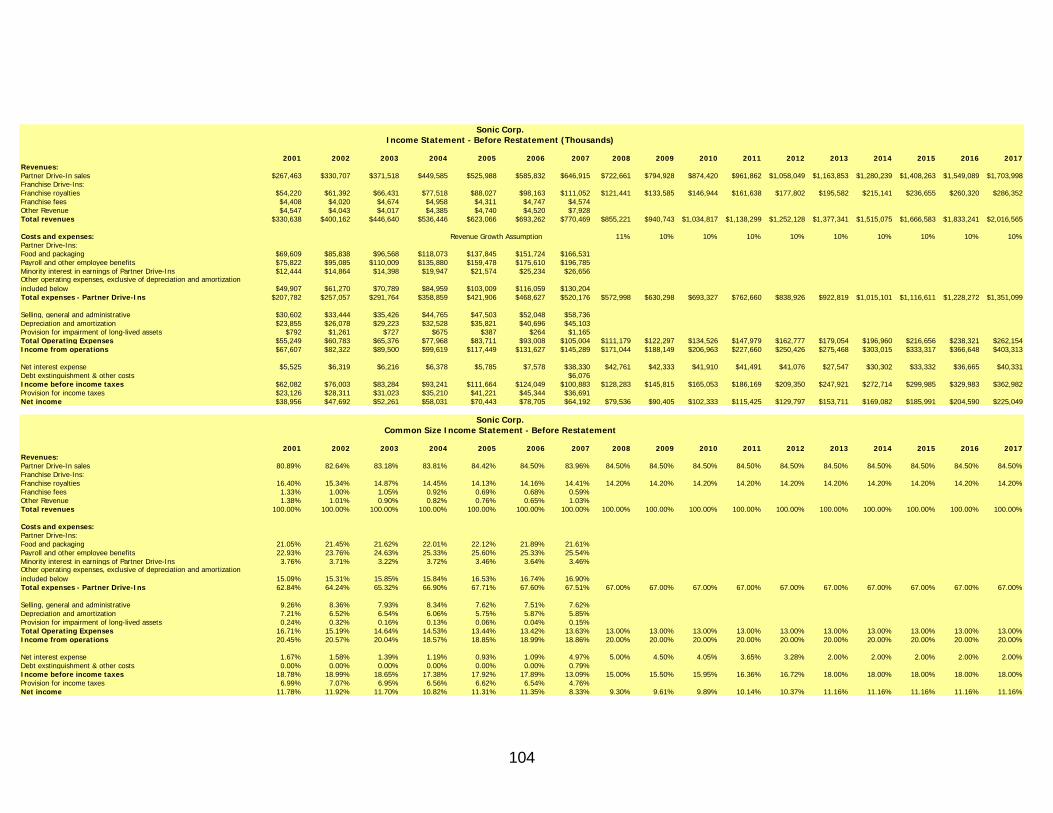

Income Statements – Actual and Forecast 104

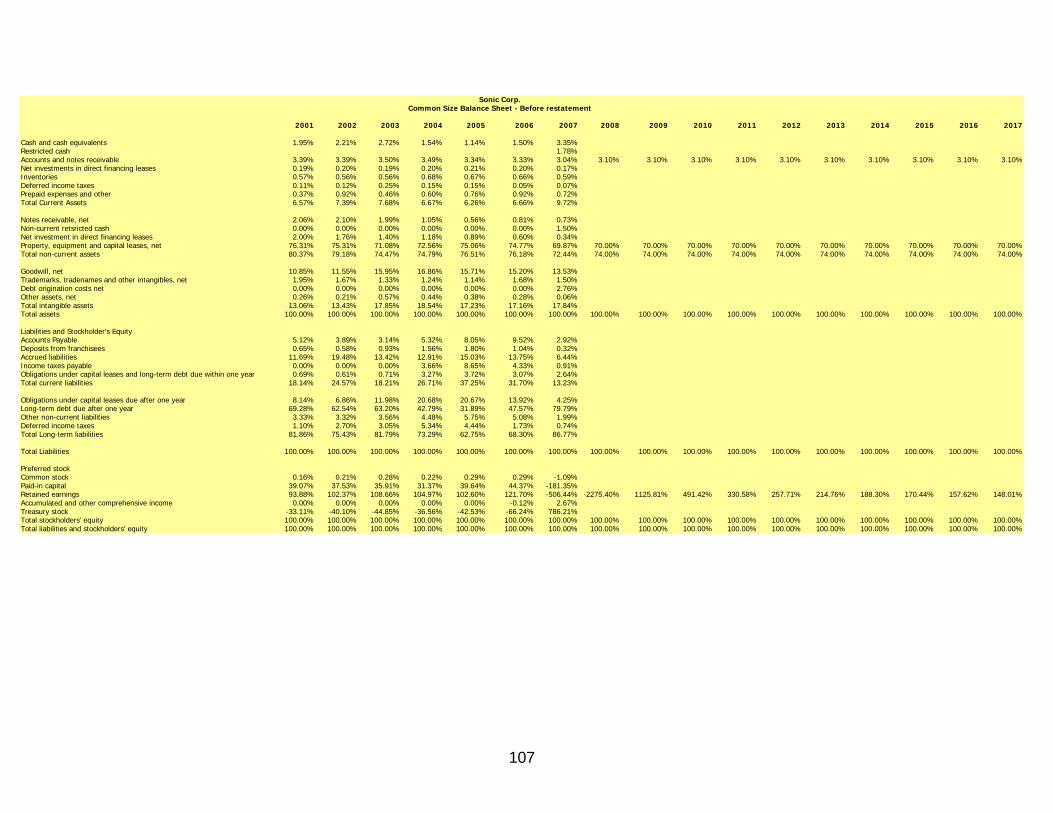

Balance Sheets – Actual and Forecast 106

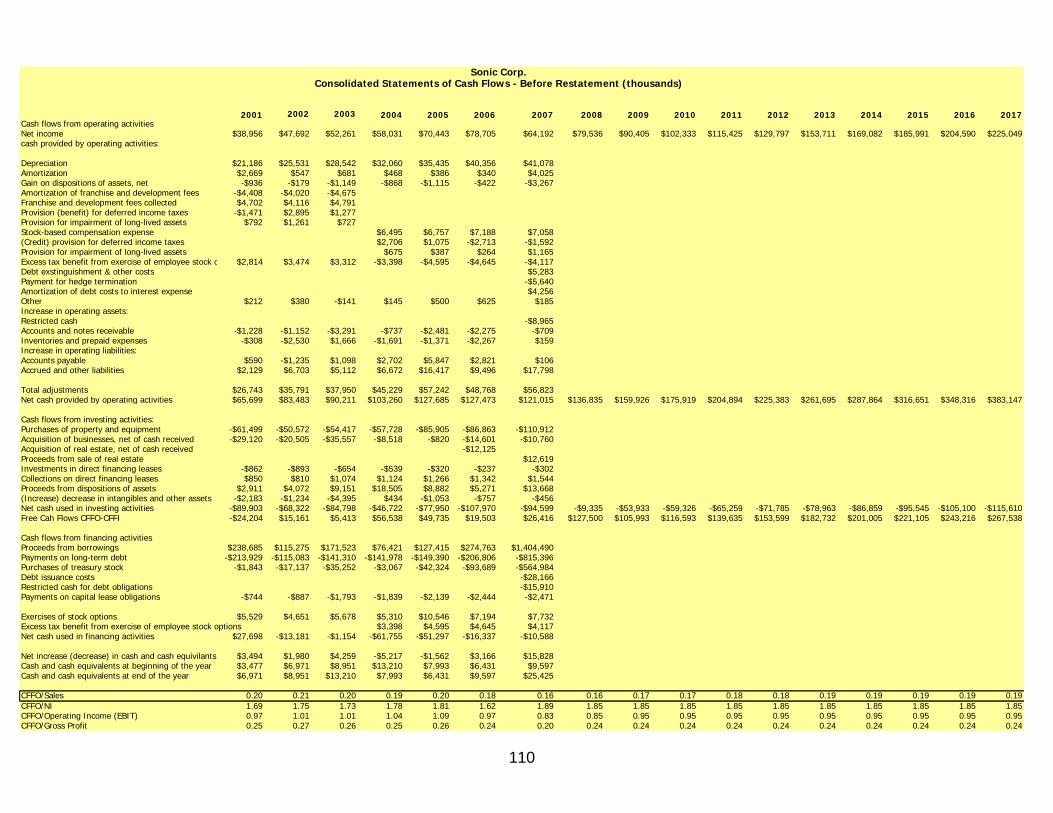

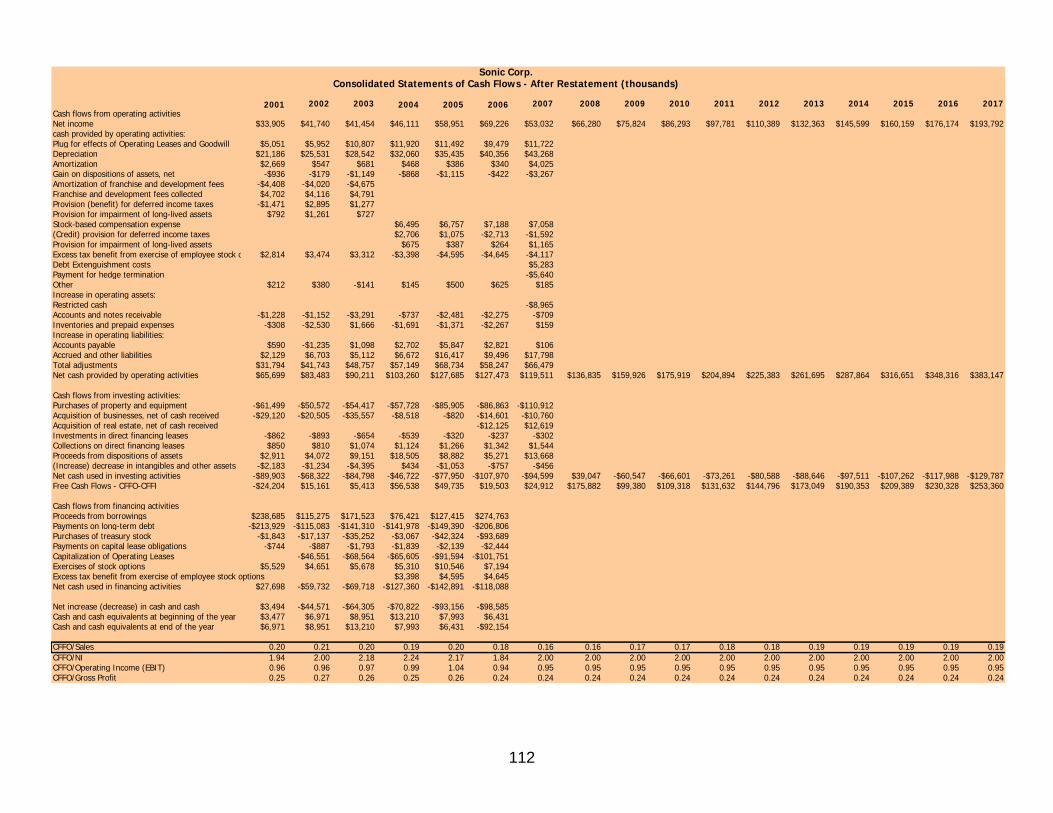

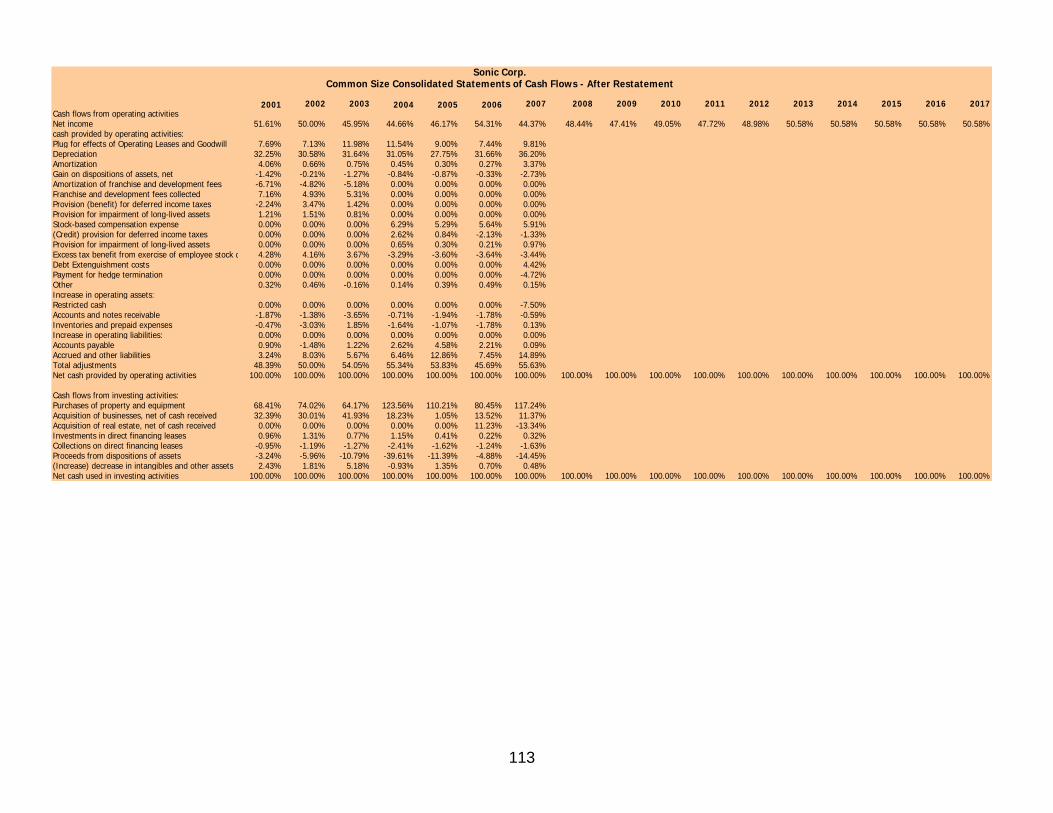

Cash Flow Statements – Actual and Forecast 110

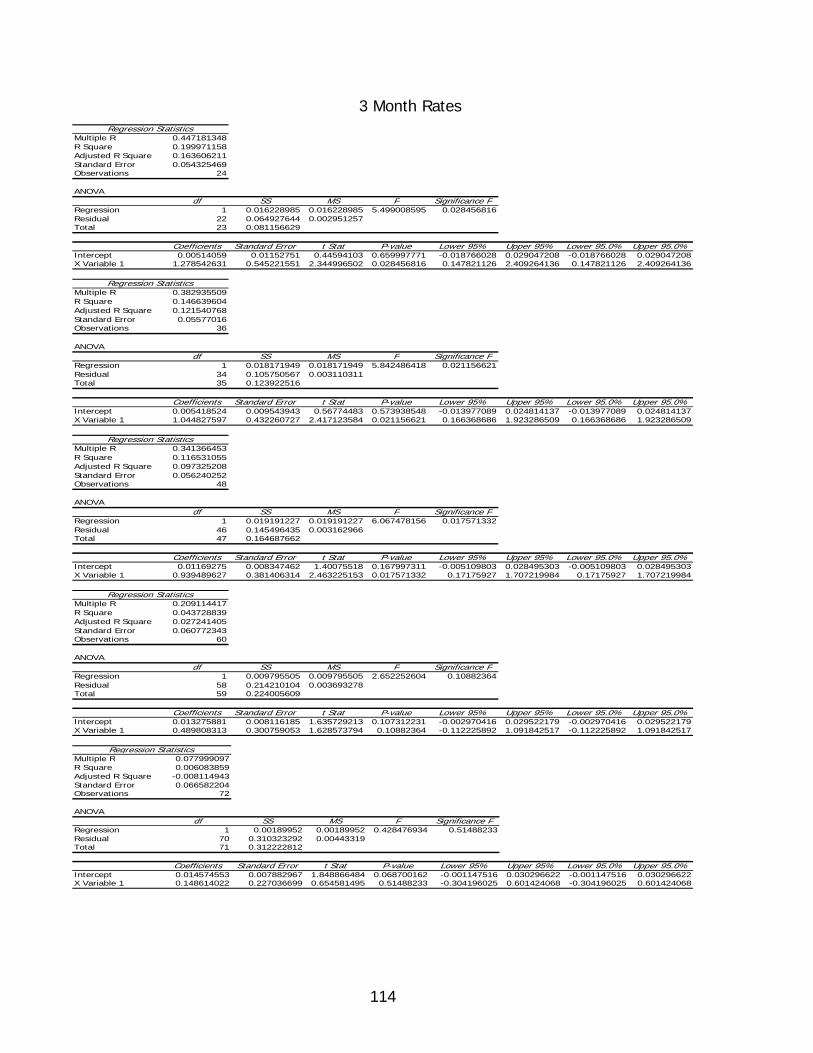

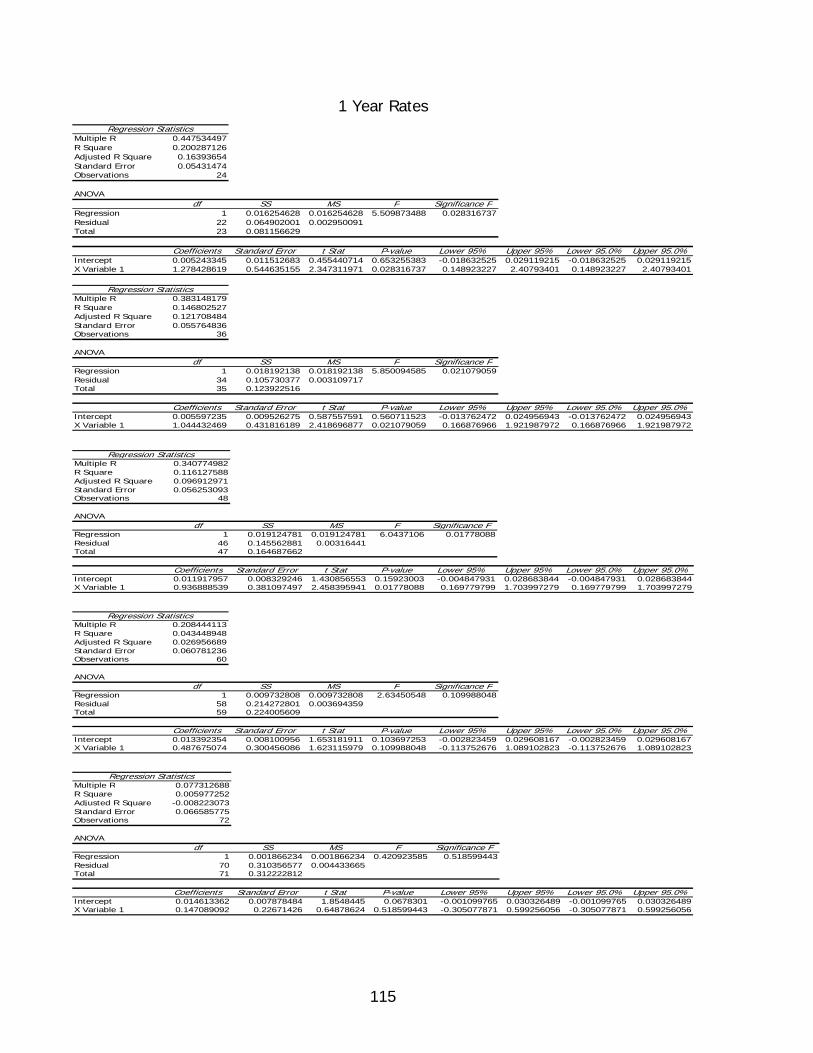

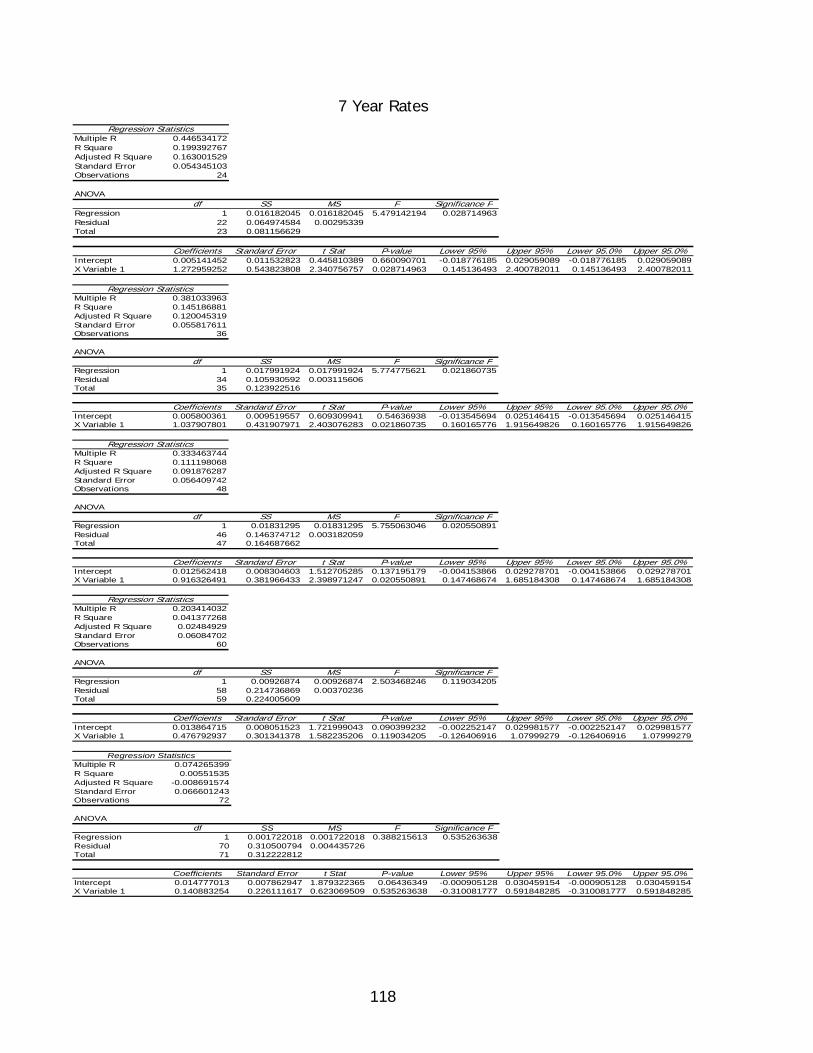

Regression Summaries 114

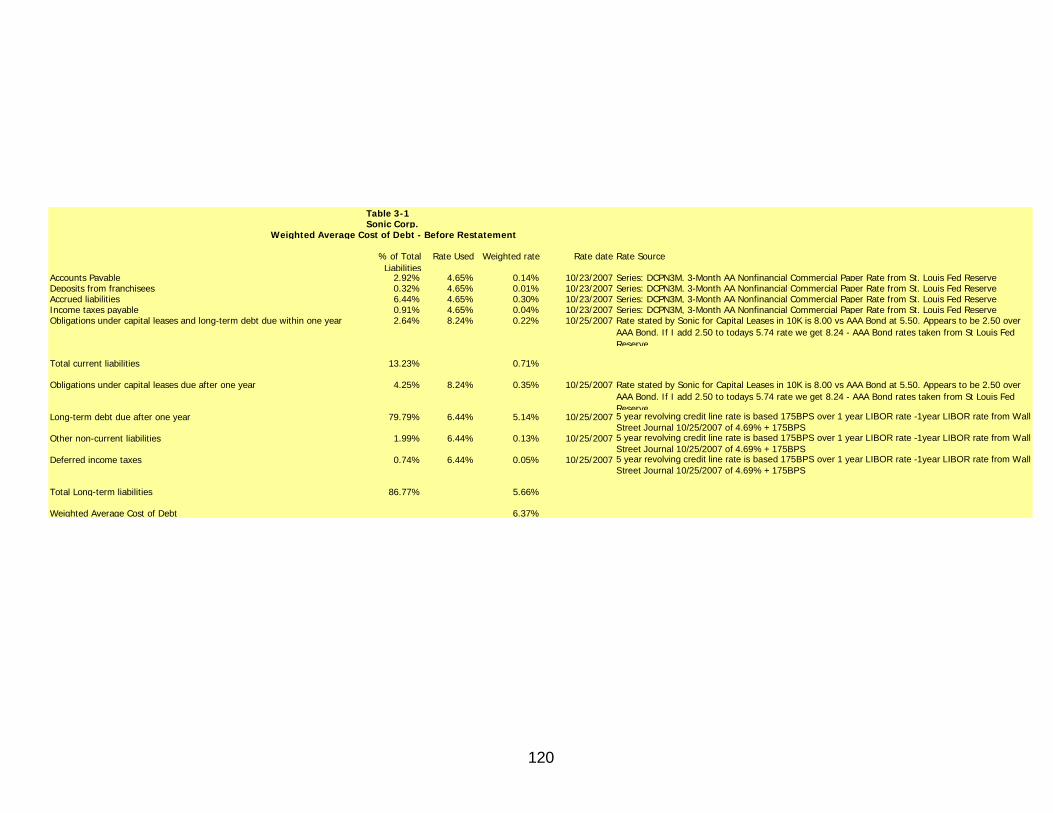

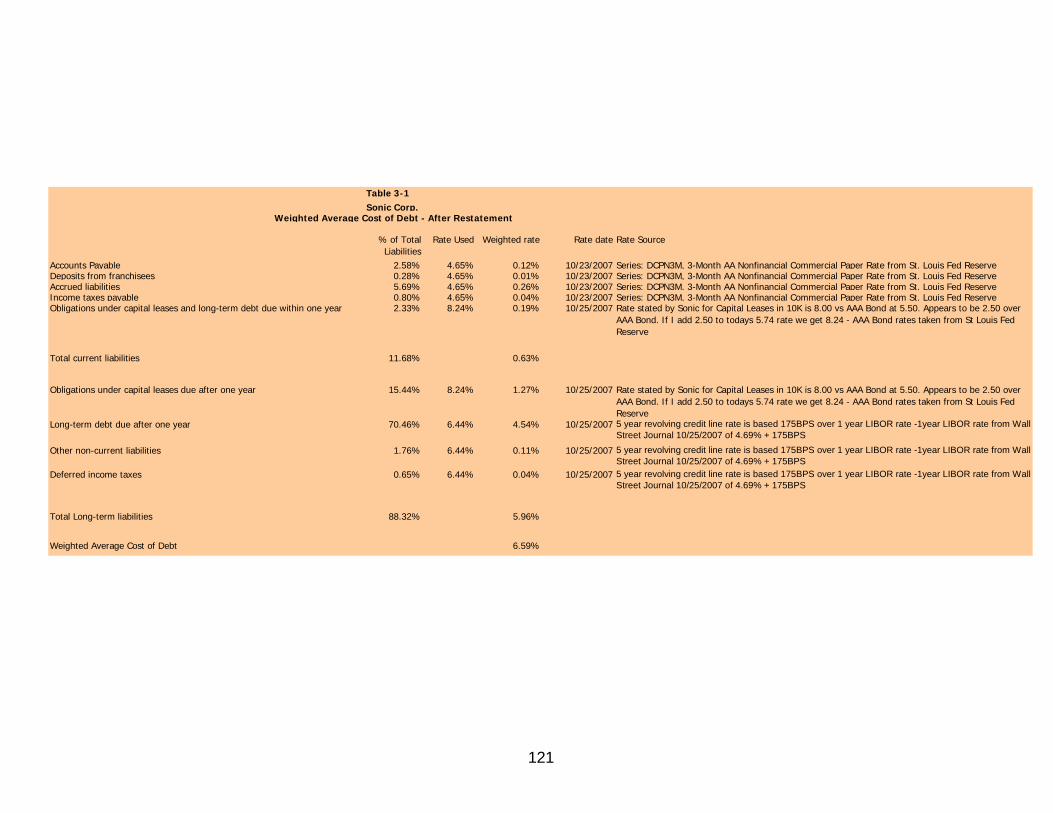

Weighted Average Cost of Debt Table 120

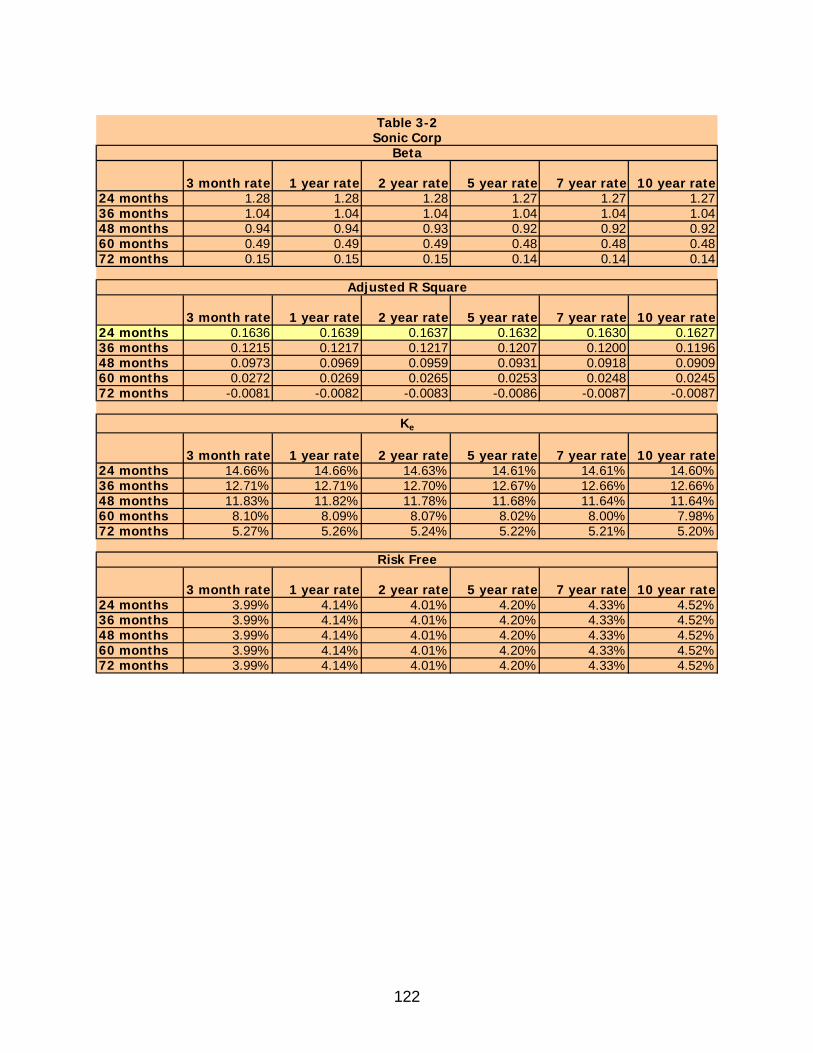

Beta Summary Table 122

Weighted Average Cost of Capital Table 123

Liquidity Analysis Tables 125

Profitability Analysis Tables 128

Capital Structure Analysis Tables 130

IGR & SGR Table 131

Ratio Tables 132

Free Cash Flow Models 141

Residual Income Models 142

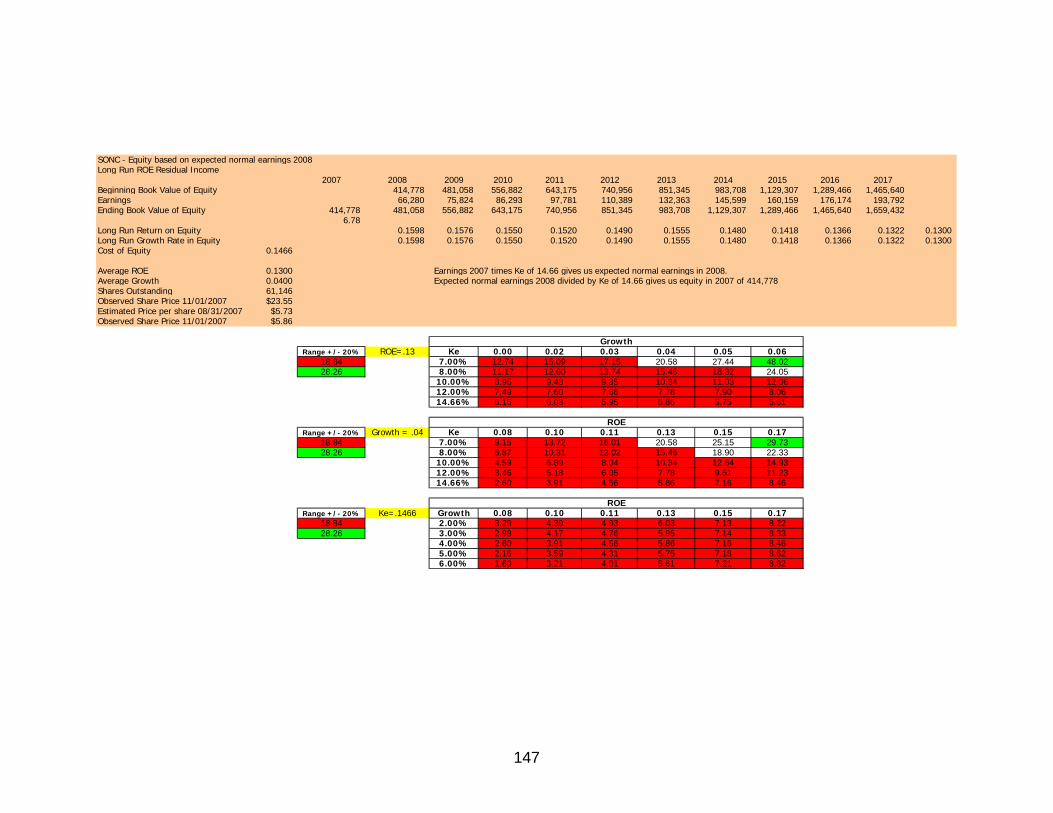

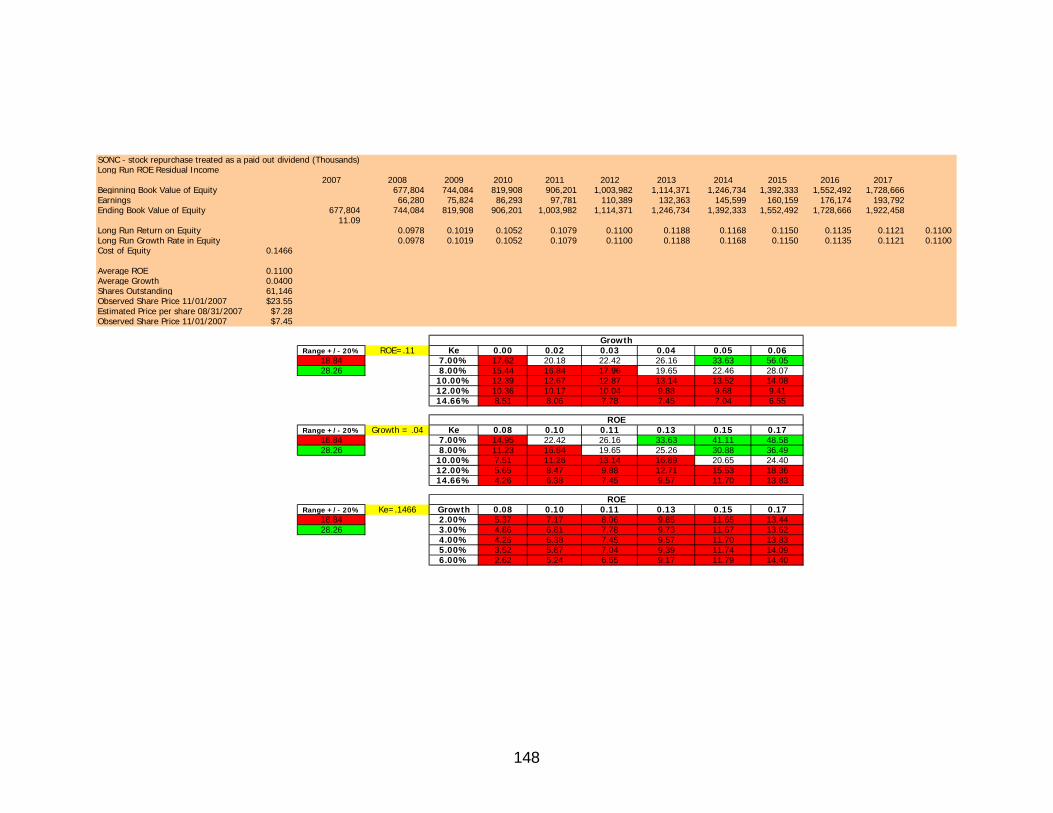

Long Run ROE Residual Income Models 147

Abnormal Earnings Growth Models 150

Method of Comparables 152

References 153

4

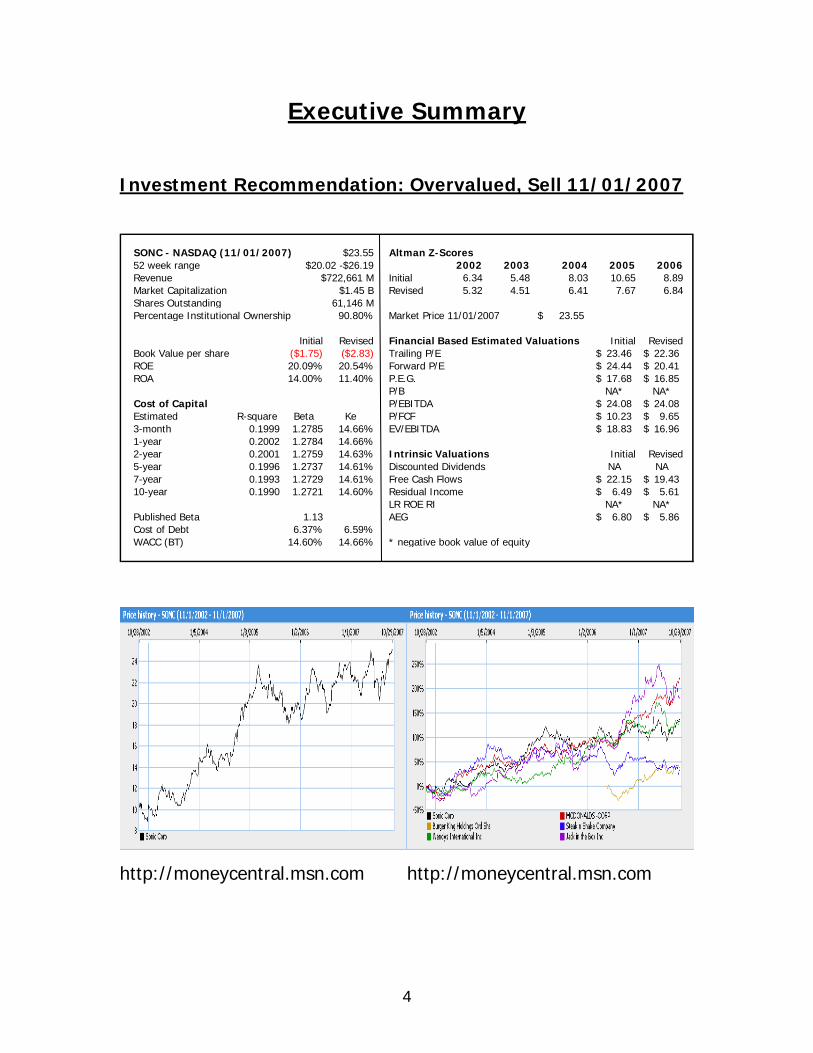

Executive Summary

Investment Recommendation: Overvalued, Sell 11/01/2007

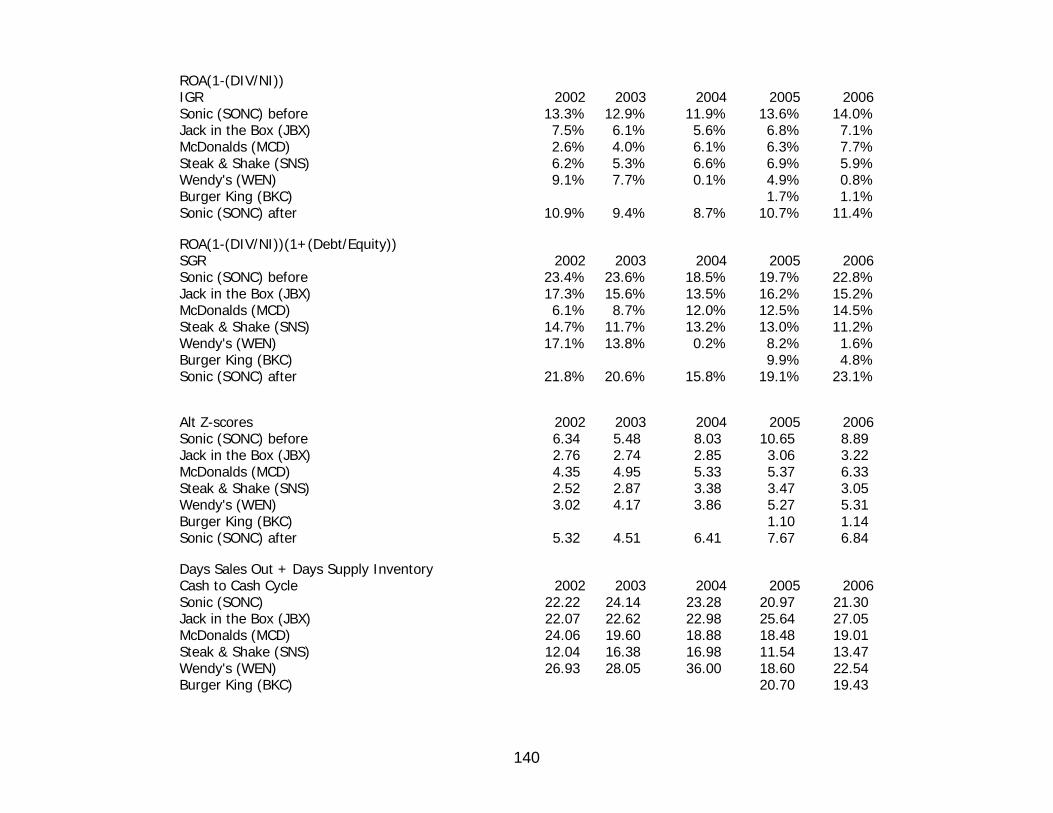

SONC - NASDAQ (11/01/2007) $23.55 Altman Z-Scores52 week range $20.02 -$26.19 2002 2003 2004 2005 2006Revenue $722,661 M Initial 6.34 5.48 8.03 10.65 8.89Market Capitalization $1.45 B Revised 5.32 4.51 6.41 7.67 6.84Shares Outstanding 61,146 MPercentage Institutional Ownership 90.80% Market Price 11/01/2007 23.55$

Initial Revised Financial Based Estimated Valuations Initial RevisedBook Value per share ($1.75) ($2.83) Trailing P/E 23.46$ 22.36$ ROE 20.09% 20.54% Forward P/E 24.44$ 20.41$ ROA 14.00% 11.40% P.E.G. 17.68$ 16.85$

P/B NA* NA*Cost of Capital P/EBITDA 24.08$ 24.08$ Estimated R-square Beta Ke P/FCF 10.23$ 9.65$ 3-month 0.1999 1.2785 14.66% EV/EBITDA 18.83$ 16.96$ 1-year 0.2002 1.2784 14.66%2-year 0.2001 1.2759 14.63% Intrinsic Valuations Initial Revised5-year 0.1996 1.2737 14.61% Discounted Dividends NA NA7-year 0.1993 1.2729 14.61% Free Cash Flows 22.15$ 19.43$ 10-year 0.1990 1.2721 14.60% Residual Income 6.49$ 5.61$

LR ROE RI NA* NA*Published Beta 1.13 AEG 6.80$ 5.86$ Cost of Debt 6.37% 6.59%WACC (BT) 14.60% 14.66% * negative book value of equity

http://moneycentral.msn.com http://moneycentral.msn.com

5

Industry Analysis

Sonic Corporation began in 1953 in Shawnee, Oklahoma. Since the

beginning, their growth in the quick-service industry has been positive. Sonics

initial public offering was in 1994 and has expanded to over 3000 stores in the

United States. Sonics has a retro style drive in environment with car hops who

deliver food to the consumer’s vehicle. Sonic has extended its franchise from an

old fashion burger stand to include specialty products that make it better suited

to survive in the quick-service market. Its target consumers are middle income

individuals who want a quality hamburger at an affordable price.

Direct competitors of Sonic include Jack in the Box, Steak N’ Shake,

McDonalds, Wendy’s and Burger King. The industry competes on economies of

scale, tight cost controls, brand image, and product differentiation, variety,

customer service. The main factor of competition in industry is cost because the

industry is homogenous. The companies try to compete at the lowest cost

possible and differentiate themselves through public image. The way firms do

this is by advertising their differences. People go to McDonalds because of price,

advertising and it’s’ cornerstone on the market. People go to Sonic because of

price, advertising, specialty products, and its different retro style image.

Quick-service industry has a high rivalry among existing firms, high threat

of new entrants, and high threat of substitute products. The quick-service

industry also has a low bargaining power of customers and low bargaining power

of suppliers because of vast amount of quick-service hamburger stands. The

quick service industry is a highly competitive industry.

The quick-service industry key success factors are cost leadership and

differentiation. Difference within the industry vary slightly and depend heavily

upon how successful a company can compete on these factors. The better the

differentiation and keeping cost to a minimum gives a slight advantage among

competitors. Each company will excel at this in order to grab their share of the

market.

6

Accounting Analysis

The basis for an accurate valuation is the analysis of the financial

statements. In order to get good information from the company’s reports it is

essential that a company fully disclose as much information as possible. Some

companies may attempt to hide deficiencies in the company by being less than

forthcoming in their accounting policies. Manipulation of expenses or sales can

be hidden by disclosing only what is required by the SEC rather than disclosing

what may be needed by analysts or other external readers to fairly value the

firm.

Sonic did a good job of disclosing information in their 10-k’s. Even though

they list operating leases off the balance sheet, they did an adequate job of

showing the off balance sheet operating leases, allowing us to restate them as

capital leases. Sonic was also slow to write off goodwill, but adequate disclosure

allowed us to calculate the amortization of goodwill in our restated financials.

Source of funds and interest rate calculations were readily available allowing us

to calculate the cost of debt and the weighted average cost of capital.

One area of concern was Sonic’s repurchase of stock in 2007. The

accounting flexibility provided by the repurchase allowed Sonic to show a

negative stockholder’s equity. This was a concern to us because it made the

valuation more difficult. There is no disclosure in management’s discussion about

why the repurchase took place. The negative value of stockholder’s equity, along

with our valuations, only added to our apprehension about buying or holding

Sonic stock.

7

Financial Analysis, Forecast Financials, and Cost of Capital

Estimation

An analysis was performed on the financial statements of Sonic in order to

determine which items needed to be forecasted and, more importantly, what

would be used to drive the forecast. Average growth of sales at Sonic has

exceeded the industry average by over 7% over the last 6 years. The success of

Sonic, in large part, will depend on continued future growth. We estimated a

future growth in sales of 11% in 2008 and 10% years 2009-2017. An asset

turnover rate of 1.11 was used to forecast future asset balances. This number

came from an average for Sonic over the past 6 years. Retained earnings and

stockholder equity were adjusted each year by the amount of net income

earned. Cash flows were forecast based on a CFFO/sales ratio of .16 in year

2008 climbing to .19 years 2013 to 2017.

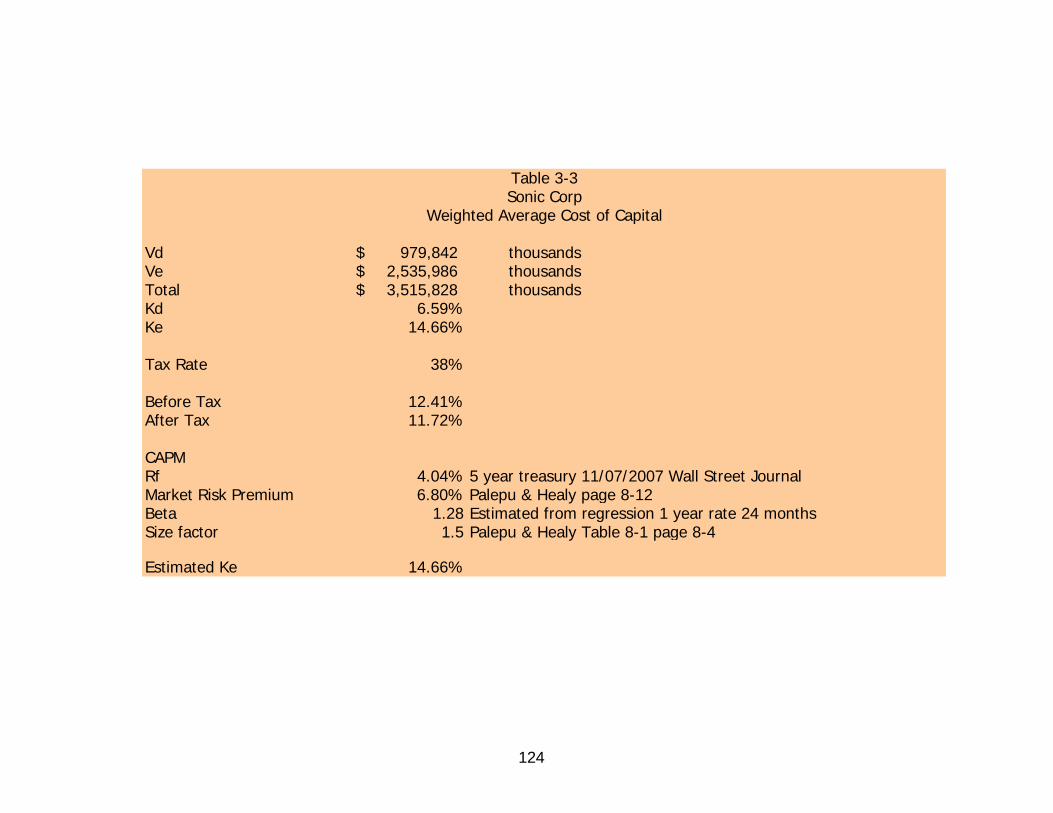

A beta of 1.28 was calculated by using regression models on the return of

the S & P 500, Sonic’s returns, and risk free rates. A weighted average cost of

debt was calculated using data we collected from Sonic’s 10-k. This information

was put into the Capital Appreciation Model to calculate a cost of capital of

14.66%. This allowed us to arrive at a before tax weighted average cost of

capital of 12.41%

This data allowed us to utilize the various valuation models to determine

whether or not Sonic is overvalued, fairly valued or undervalued. In liquidity

analysis Sonic is overvalued even with manipulation of the cost of equity and the

growth rate. The forecasted financials ratios shows that Sonic had high gross

margin, operating margin, net margin, and return on assets. These ratios

convey that Sonic has high profit margins. The capital structure analysis of Sonic

was at average with the industry. The only outlier was the debt service margin

which was high because of low current assets from 2002-2004.

8

Valuations

Once the industry analysis, accounting polices, and financial ratios are

examined thoroughly, a future investor can evaluate the firms share price

through equity valuations. Using various models of valuations, a firm share price

can be determined as fairly valued, undervalued, or overvalued.

The first valuation model that is used to formulate a share price for Sonic

is the method of comparables. The method of comparables provides the investor

with seven ratios to compute both before and after restated share prices. From

this valuation method, Sonic is classified as being in between a fairly valued to

an overvalued firm. The relevant ratios that produced share prices are the P/E

forward and trailing, P.E.G., P/EBITDA, EV/EBITDA, and P/FCF. Two other ratios,

P/B and D/P, were irrelevant to our valuation. The P/B produces a negative share

value due to a negative book value of equity and Sonic is not a dividend paying

firm. However, this model is inaccurate because it is based on industry averages

and excludes intrinsic information.

The intrinsic valuation models, which are based on theory, are essential in

estimating the firm’s market value of equity. Not all of the models are equally

useful. The degree of reliance on the perpetuity determines the sensitivity and

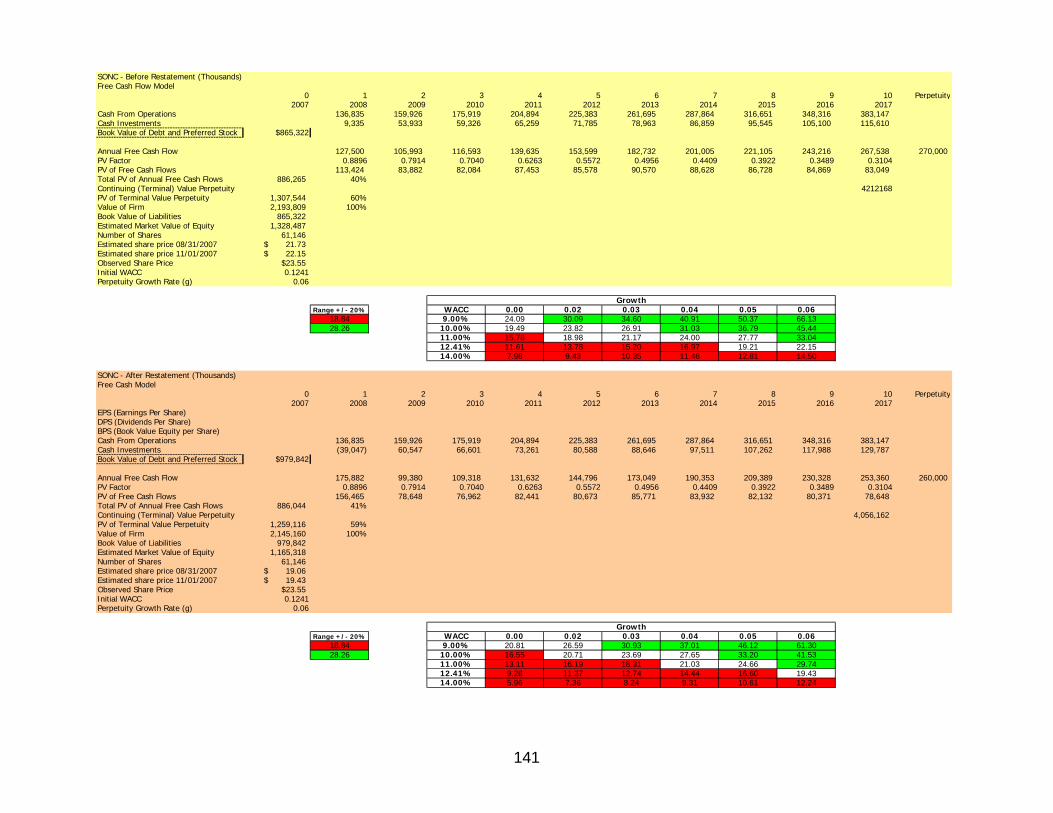

therefore the reliability of the model. The free cash flow model and the dividend

discount model are highly sensitive and should not be considered to be as

accurate as the residual income model, the long run residual income model, and

the abnormal earnings growth model. The dividend discount model was not used

to value Sonic because they do not pay a dividend. In order to have the after

restatement FCF model equal to the observed share price, the WACC would have

to be 12.4% with a 7% growth rate. However, a 7% growth rate is not

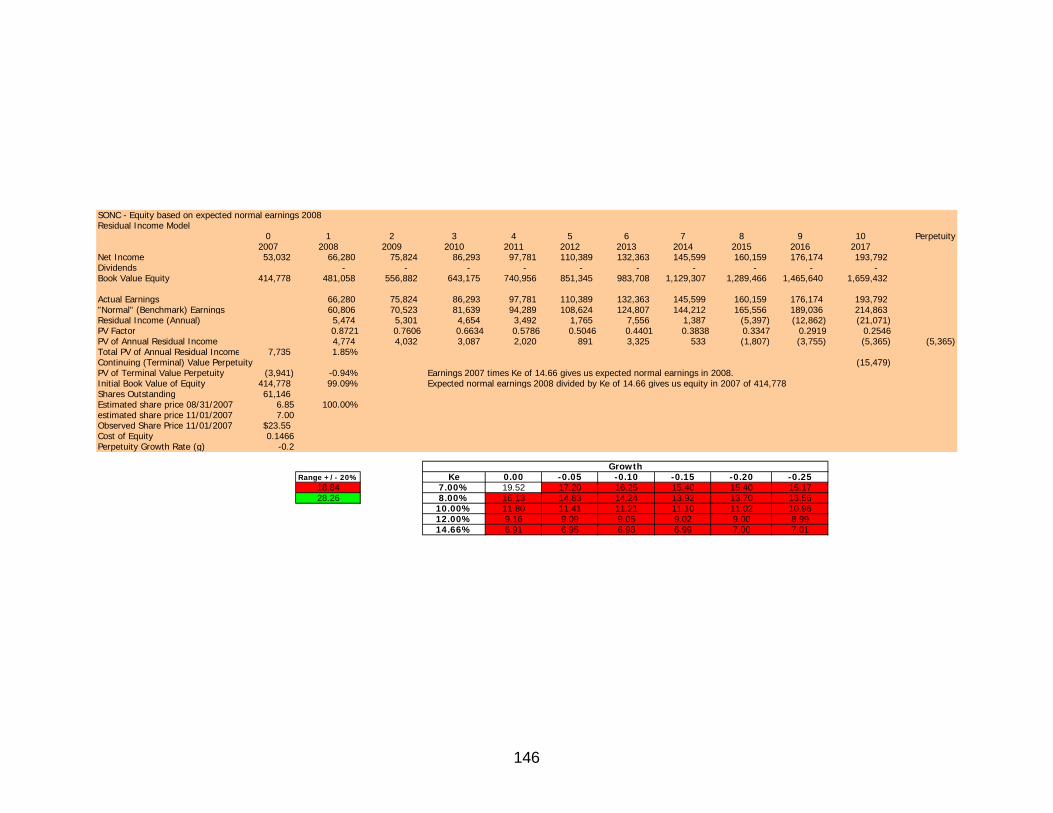

reasonable or sustainable. The Residual Income model would have to have a

cost of equity of 5.1% and a growth rate of zero to equal the observed share

price. This is also unreasonable because the cost of equity is estimated to be at

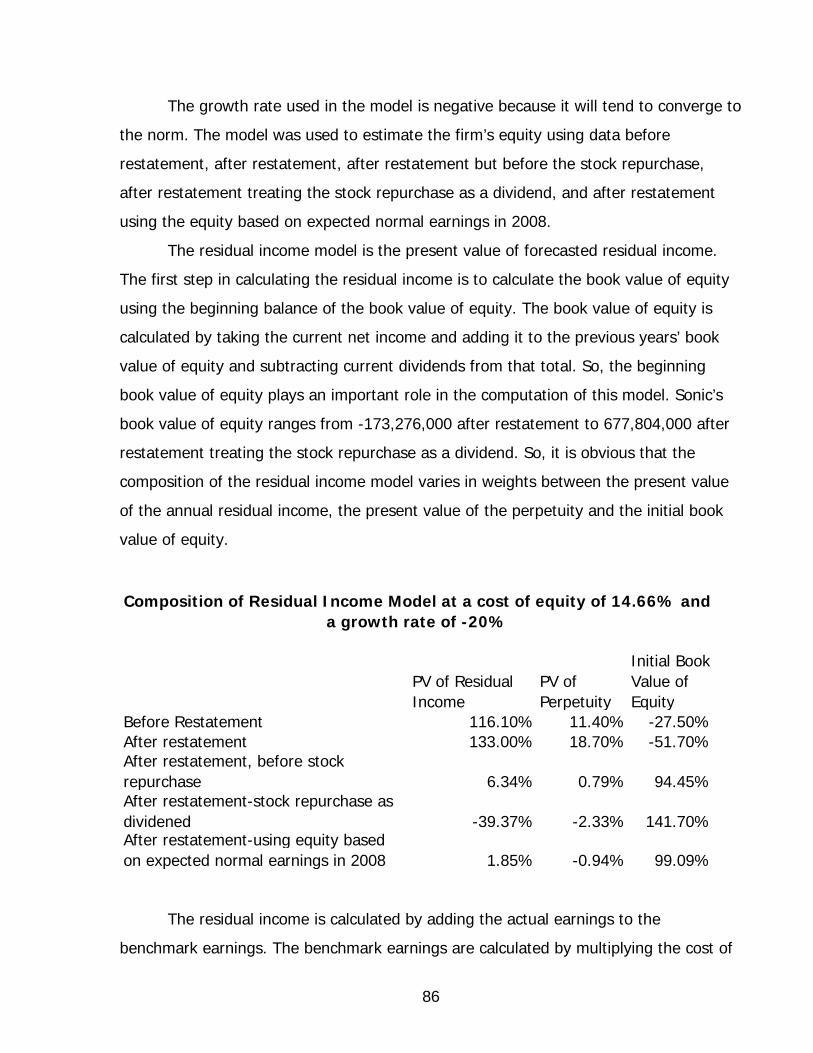

least twice 5.1%. The residual income model was used for four different data

9

sets; including before restatement, after restatement, after restatement but

before the stock repurchase, and after restatement treating the stock repurchase

as a dividend. This was necessary because the stock repurchase created a

negative book value of equity. The last two data sets allowed us to see Sonic

with a positive book value of equity. However, all four data sets used in the RI

model suggested that Sonic is overvalued. The long run RI model also used data

sets that allowed Sonic’s book value of equity to be positive. The long-run RI

model suggested that the firm was overvalued, because the majority of the

prices generated by the model fell below the 20% range, which surrounds the

observed share price. The AEG model was used with data before and after the

restatement. The AEG model is the second most reliable behind the RI model. It

also suggested that Sonic is overvalued. In conclusion, the method of

comparables and the intrinsic valuations both indicate that Sonic is overvalued.

10

Business and Industry Analysis

Company Overview

The Sonic Corporation began as a single root beer stand in 1953 in

Shawnee, Oklahoma. Troy Smith, the owner of the stand, eventually added an

intercom system and carhops in order to differentiate his business from the

competition. These innovative ideas are what helped propel Sonic Corp. to

become the Nation’s largest drive-in chain (www.sonicdrivein.com). However,

Sonic’s main competitors are not drive-in chains. They primarily compete with

McDonald’s Corp., Steak and Shake Company, Burger King Corp., Jack in the Box

Inc., and Wendy’s International Inc. As of August 31, 2006, Sonic Corp. had a

market cap of 1.44 billion and had 3,188 Sonic Drive-Ins, which consisted of

2,565 Franchise Drive-Ins and 623 Partner Drive-Ins. These drive-ins are mainly

located in the southern two thirds of the United States and also include 2 drive-

ins in Mexico. Their executive headquarters are located at 300 Johnny Bench

Drive, Oklahoma City, Oklahoma.

A Sonic Drive-In consists of 24 to 36 covered Drive-In spaces where a

customer is able to place their order over an intercom system. The customer is

able to choose from an array of made-to-order items; such as extra long cheese

coneys, slushes, limeades, hamburgers, and tator tots. They also offer an

extensive breakfast menu which is available throughout the day. The order is

then delivered to the customer’s car by a carhop within an average of four

minutes (Sonic 10-k 2006). Sonic Corp. claims that they will continue to grow if

they continue to offer “made-to-order American classics, signature menu items,

and speedy service from friendly Carhops” (www.sonicdrivein.com).

11

Sonic Corp. says that their primary “objective is to maintain their position

as, or to become, a leading operator in terms of the number of quick-service

restaurants within each of their core and developing markets (Sonic 10-k 2006).”

Since August 31, 2005, Sonic Corp. has increased the number of drive-ins by

149. Another specific element of their strategy is to grow by expanding existing

markets as well as developing new markets. Over the past year, their growth

rate has exceeded the industry average of about 4%.

2002 2003 2004 2005 2006Assets $405,356 $486,119 $518,633 $563,316 $638,018Partner Drive-In Sales $330,707 $371,518 $449,585 $525,988 $585,832Partner Drive-In Growth 23.65% 12.34% 21.01% 16.99% 11.38%Franchise Drive-In Sales * $1,945,735 $2,052,161 $2,306,118 $2,561,135 $2,800,980Franchise Drive-In Growth 10.09% 5.47% 12.38% 11.06% 9.36%Franchise Revenues $65,412 $71,105 $82,476 $92,338 $102,910Franchise Revenue Growth 11.57% 8.70% 15.99% 11.96% 11.45%Total Sales Growth 11.87% 6.47% 13.70% 12.03% 9.71%* calculated from reported average francise location sales times # of franchise locations

Total Assets, Partner Sales, Franchise Sales, Franchise Revenues (in thousands)

http://moneycentral.msn.com/investor/home.asp

12

Industry Overview

The restaurant industry is a part of the consumer services sector.

According to the National Restaurant Association (NRA), there are approximately

935,000 restaurant and food-service outlets in the United States. These firms

employ more than 12 million people. Sales for all outlets exceeded $500 billion in

2006, and sales for 2007 are estimated to reach $537 billion

(www.restaurant.org). Restaurant sector sales, classified as eating places by

Standard Industry Code (SIC) 5812, accounted for approximately $345 billion in

2006. There are approximately 400,000 locations that are classified in the eating

places sector.

The eating places sector is about equally divided into full-service

restaurants and quick-service restaurants. Full-service restaurants are defined as

locations where customers sit down and are waited on by a waitperson or server.

These restaurant companies include Chili’s, Morton’s, Applebee’s, and Outback

Steakhouse. Sonic Corp. (SONC) primarily competes in the quick-service (QSR)

or limited-service burger segment. Sonic Corp. competes with companies such as

McDonalds Corp (MCD), Burger King Holdings Ord Shares (BKC), Wendy’s

International Inc (WEN), Jack in the Box Inc (JBX), and Steak n Shake Company

(SNS).

QSR magazine.com defines the market for these competitors as the

“burger” segment, and they estimate 2006 sales to be approximately $59 billion.

Overall, the restaurant industry is highly fragmented. However, these major

competitors in the burger segment control a significant market share of this

segment.

13

Consumer income and convenience are the major drivers in the choice to

dine out or eat at home. Income and convenience also play roles in whether a

consumer chooses to dine at a full-service restaurant or a quick-service

restaurant.

Five Forces Model

The Five Forces Model is a framework for an analyst to classify an

industries structure and deriving average profitability. This model allows the

analyst to breakdown the competition and asses the value drivers within a

particular industry. In addition, this model explores the bargaining power

relationships between the consumers as well as the suppliers. When breaking

down the competition the analyst evaluates the rivalry among existing firms,

threat of new entrants, and threat of substitute products. The rest of the model

focuses on the bargaining power of consumers and the bargaining power of the

suppliers. With this intricate information the analyst can understand where the

industry creates value, and provides an overview of the risks affecting

profitability.

Restaurant Industry – Quick Service Segment Rivalry Among Existing Firms HighThreat of New Entrants HighThreat of Substitute Products HighBargaining Power of Customers LowBargaining Power of Suppliers Low

14

Rivalry Among Existing Firms

Rivalry among existing firms in an industry depends on the level of

concentration, industry growth, switching costs, differentiation, economies of

scale, fixed to variable costs, excess capacity and exit barriers.

Industry Growth

Growth of Top 50 by category - QSR segment

QSR Categories Top 50 Sales (MM)

in 2006

Top 50 Sales

Change 2004

Top 50 Sales Change 2005

Top 50 Sales Change 2006

Sandwich - Top 50 $15,600 12.3% 14.6% 8.3%Asian - Top 50 $889 19.4% 24.3% 20.9%Seafood - Top 50 $1,313 1.5% -1.8% 0.9%Burger - Top 50 $59,009 4.0% 4.0% 4.1%Mexican - Top 50 $7,979 7.0% 9.0% 4.7%Chicken - Top 50 $12,515 4.7% 7.0% 7.0%Pizza/Pasta - Top 50 $12,672 -1.0% 4.3% 0.9%Snacks - Top 50 $11,197 23.6% 16.9% 15.9%QSR Segment 5.9% 6.9% 5.7%www.qsrmagazine.com

Overall, firms within the quick-service industry have experienced low

growth within the past few years, as indicated in the graph. The low growth

forces these firms to increase their market share through competitive pricing and

marketing campaigns. Since there is low growth in this industry, firms are forced

to compete against one another for a limited market share. The low level of

growth in the quick-service industry increases the amount of rivalry among firms.

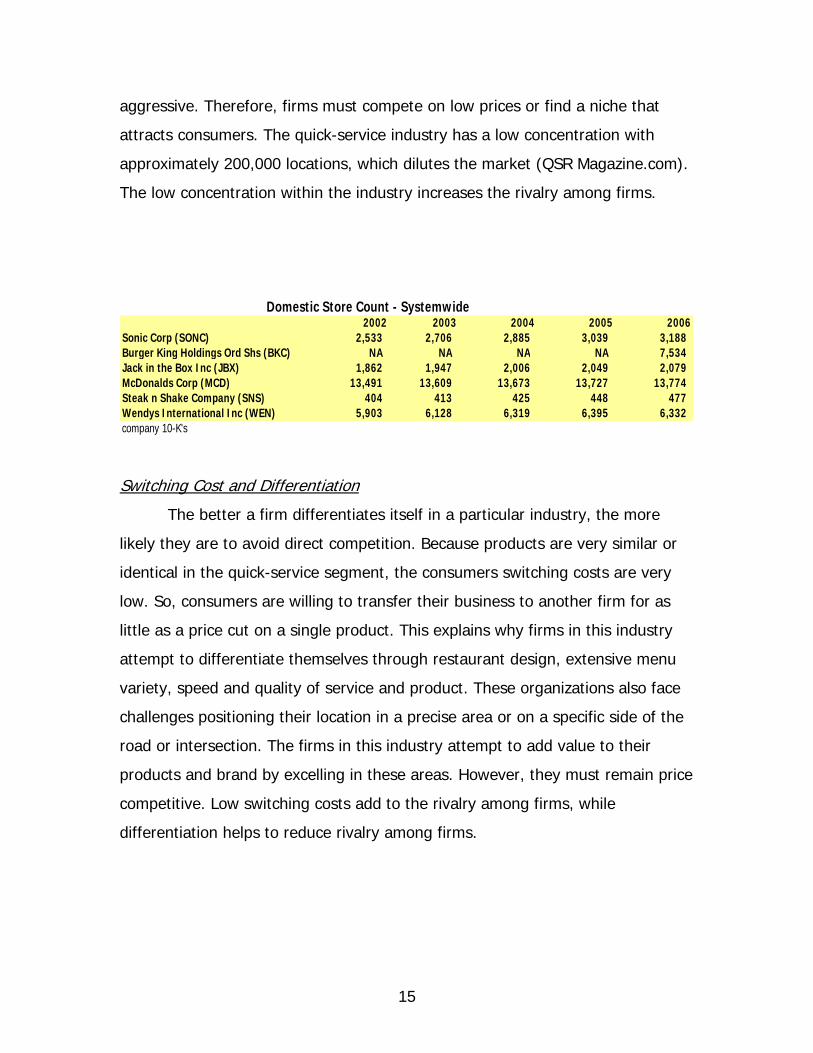

Concentration

An industry that only has one or few players is highly concentrated. An

industry of this nature faces price fixing as well as collusion. In contrast, an

industry that consists of numerous firms has a low concentration and is price

15

aggressive. Therefore, firms must compete on low prices or find a niche that

attracts consumers. The quick-service industry has a low concentration with

approximately 200,000 locations, which dilutes the market (QSR Magazine.com).

The low concentration within the industry increases the rivalry among firms.

2002 2003 2004 2005 2006Sonic Corp (SONC) 2,533 2,706 2,885 3,039 3,188 Burger King Holdings Ord Shs (BKC) NA NA NA NA 7,534 Jack in the Box Inc (JBX) 1,862 1,947 2,006 2,049 2,079 McDonalds Corp (MCD) 13,491 13,609 13,673 13,727 13,774 Steak n Shake Company (SNS) 404 413 425 448 477 Wendys International Inc (WEN) 5,903 6,128 6,319 6,395 6,332 company 10-K's

Domestic Store Count - Systemwide

Switching Cost and Differentiation

The better a firm differentiates itself in a particular industry, the more

likely they are to avoid direct competition. Because products are very similar or

identical in the quick-service segment, the consumers switching costs are very

low. So, consumers are willing to transfer their business to another firm for as

little as a price cut on a single product. This explains why firms in this industry

attempt to differentiate themselves through restaurant design, extensive menu

variety, speed and quality of service and product. These organizations also face

challenges positioning their location in a precise area or on a specific side of the

road or intersection. The firms in this industry attempt to add value to their

products and brand by excelling in these areas. However, they must remain price

competitive. Low switching costs add to the rivalry among firms, while

differentiation helps to reduce rivalry among firms.

16

Economies of Scale

In some industries, the size of the organization determines the success of

the firm. However, that is not the case within the quick-service industry. Even

though there are a number of large firms in the quick-service industry, there are

also mom and pop restaurants that find their niche in the industry.

Total Assets (in millions) 2002 2003 2004 2005 2006Sonic Corp (SONC) $405 $486 $519 $563 $638McDonalds Corp (MCD) $23,971 $25,838 $27,838 $29,989 $29,024Burger King Holdings Ord Shs (BKC) NA NA NA NA $2,552Wendy’s International Inc (WEN) $2,667 $3,133 $3,198 $3,440 $2,060Jack in the Box Inc (JBX) $1,063 $1,142 $1,325 $1,338 $1,520Steak n Shake Company (SNS) $396 $417 $436 $475 $543derived from 10-K's

Excess Capacity and Exit Barriers

Excess capacity occurs when the firms’ resources are not utilized to their

potential. When excess capacity occurs, firms are forced to cut prices in order to

utilize their capacity. They maximize capacity through sales and discounts during

non-traditional day parts.

The more exit barriers there are in an industry, the more risky it is for

firms to enter the industry. Firms in industries that are highly invested in their

assets or have high fixed costs struggle to exit an industry. These obstacles can

force a firm to continue to produce at an economic loss because shutting down is

even less profitable. Larger firms in the quick-service industry are often

committed to operation in order to overcome their invested capital as well as

their established reputation. However, smaller mom and pop restaurants can cut

their losses and exit the industry much easier.

17

Conclusions

The quick-service industry is a low concentrated, highly competitive

industry that has seen low growth in recent years. While there is some

differentiation within the industry, low switching costs offset any advantage

gained from differentiation. In addition, few firms have the economies of scale

needed to gain a competitive advantage. Also, firms in the industry reach their

full capacity through price competition.

Threat of New Entrants

The threat of new entrants in an industry is dependent on several factors.

Economies of scale, first mover advantage, access to channels of distribution,

supplier relations, and legal barriers are all determinates of this threat. The

industry is structured so that smaller businesses can battle for market share by

providing a service that the larger competitors can not, such as superior

customer service or healthy and quality food products. In some cases, a low

concentrated industry, like the quick-service industry, is forced to lower prices

and attempts to recover profits by cutting expenses or tightening the entire

supply chain.

Economies of Scale

The quick-service industry faces high risks of new entrants. A new firm

can enter the industry without being dragged down by large amounts of debt

which means that the new entrants do not need a significant number of assets or

large amounts of capital to be profitable in the industry. The quick-service

industry also does not take an extensive degree of research and development

18

prior to entering. However, the new entrant still must find a niche in the market

because they will be at a disadvantage to existing firms in the industry.

Supplier Relations and Channel Access

The major firms in the quick-service industry gain a portion of their

competitive advantage through supply chain management. The larger players in

the industry are able to buy their products in bulk. So, these firms are able to

enjoy discounts and price cuts. Not to mention, the larger existing firms have

long well established relationships with loyal suppliers. However, this is where

few industry players also clash for a competitive edge, and provide fresh non-

frozen healthy products with fewer supplier channels. This illustrates those firms

with un-established supply chains can still enter the industry and not necessarily

be at a competitive disadvantage.

Legal Barriers

Throughout the quick-service industry there are multiple segments. Sonic

is a part of the burger segment within the industry, which faces state laws that

regulate franchises as well as regulations adopted by the Federal Trade

Commission. Additional laws consist of abiding by federal and state

environmental regulations, labor laws, safety and fire codes, and most

importantly licensing restrictions. However, these legal barriers are not

significant enough to defer a firm from entering the quick-service industry.

Conclusions

The threat of new entrants in the quick-service industry is high because

there are few barriers to entry. The threat of new entrants in the quick service

industry is a high risk to the existing organizations. The information provides an

19

illustration of how new entrants do not necessarily have to have large economies

of scale to enter the industry. The legal barriers that new entrants are forced to

face are manageable. Therefore, existing firms are at risk of new entrants.

Threat of Substitute Products

The threat of substitute products has a major effect on the quick-service

industry. Ultimately, every industry competitor produces virtually the same menu

items in a differentiated fashion. Therefore, firms in this industry that are

profitable are the firms that not only compete on price, but on the overall

perception of value experienced by the customer.

Relative Price and Performance

When firms in a particular industry primarily compete on a very similar

product, such as hamburgers, the firms in that industry tend to be forced to

charge a relatively similar price to one another.

Quick-Service Provider Burger Combo

Combo Price + Tax

McDonalds #2 Quarter Pounder $4.35

Wendy's #1 1/4 lb Single $4.39

Burger King #1 Whopper $4.49

Steak & Shake N/A N/A

Sonic #1 Sonic Burger $4.49

Jack in the Box #2 Jumbo Jack $4.39 (Lubbock drive thru menus and Houston Jack in the Box)

Furthermore, the quick-service industry has low consumer switching costs,

so each firm must ensure that their price level is adequate for the consumer.

20

Ultimately, all competitors within the quick-service industry provide the same

generalized function to the consumer; therefore, firms must extract as much

value as possible while simultaneously providing a fair market price. These

organizations in this industry attempt to extract maximum value by providing

speedy and quality customer service, differentiated menu items, and a

convenience factor. Also, consumers interpret added value when they receive a

lower price. So, many of the burger quick-service firms have began adding value

menus.

Buyers’ Willingness to Switch

The quick-service industry provides the consumer with such a wide variety

of choices that it forces the firms to take extreme measures when determining

the geographic locations of their stores. Because all industry competitors provide

the same function, consumers’ willingness to switch is very high. Therefore,

convenience is a major factor in determining the location of a firm; even to the

extreme of what side of the street the business is on. In addition to location,

new signature products, upcoming sales promotion, consumer service

commitments, and economic conditions all have significant impact on the firms’

ability to overcome the consumers’ willingness to switch (Sonic 10-k 2006). This

is the basis for establishing a loyal customer base and attracting new consumers,

which will eventually lead to higher profits and firm growth.

Conclusions

When competing in the quick-service industry there is no method to

avoiding substitute products. This demonstrates why substitute products are a

major risk for existing firms. To succeed in an industry with low switching costs,

firms must focus on their core competencies. Sonic’s commitment to speedy

service and assortment of products is a few of their core competencies used to

21

achieve desirable profits and increase shareholder value. They must also

continue to attract and build a loyal clientele to reach future growth

expectations. Sonic currently has the “industry-leading customer frequency,”

showing how repeat business is a crucial part in being successful

(www.sonicdrivein.com).

Bargaining Power of Customers

One-fifth of the United States of America’s population eats in a quick

service restaurant every day. The QSR industry offers food, a necessity, and

affordable prices. So it is no wonder why so many people eat at these places.

When millions of people gladly pay these low prices there can not be much

room, if any, to bargain for cheaper food.

Price Sensitivity

The price sensitivity of an average customer is derived from the

relationship between their perceived value and the cost of the product. High

price sensitive customers can be found in industries where there are

undifferentiated products and low switching costs. The switching costs are low

due to an abundance of quick service restaurants in a given area, and

transferring between two is effortless. In the fast food industry, menus consist

of similar products however, differentiate among type: burgers, chicken, or

Mexican. In a customer’s cost structure, food is ranked very high because it is a

necessity in every day life. Dollar and Value Menus allow people with the

tightest budgets to remain customers of the fast food industry. Most quick-

service restaurants maintain approximately the same price level, and customers

expect them to. A burger is a burger, and so people value one restaurant’s

products equal to the next one. A substantial upward or downward change in

22

price would result in equal reactions by the customers. In this instance, the

customer would eat at the below market priced restaurant. But a large drop or

increase in price is rare for the QSR industry, and so customers do not shop by

price. When a person has decided to eat fast food he or she must choose from

the restaurants located in the area (convenience) and from his or her perceived

value (taste) of the different product lines. In the case of the quick-service

industry, customers are considered low price sensitive for not shopping on price.

Relative Bargaining Power

The relative bargaining power of a customer is their ability to demand a

drop in prices. The customers’ bargaining power comes from the cost of not

doing business with the fast food restaurant. However, for the individual

customer, this power is miniscule because “On average, one-fifth of the

population of the USA (45 million people) eat in a fast-food restaurant each day,”

(Oxford University Press). Thus, a handful of price-disputing customers are not

threatening to the industry. Also, the individual customer holds little power when

considering the proportion of loss in sales to total revenue a restaurant will

sustain. However, one of the few instances when the customer holds bargaining

power is when a restaurant prices their items too high. In this case the

customer can choose to go elsewhere as long as alternatives are offered. Even

for highly price sensitive fast food customers, there is a slim chance for price

reduction, because individually they have no bargaining power in scale of such a

large customer base.

Bargaining Power of Suppliers

Fast Food suppliers are abundant and compete heavily for the supply contracts

of these businesses. The differences between each supplier are minimal, so, the

23

price and quality of service will be a major factor in determining suppliers.

Besides lower prices, in comparison to other suppliers, quick-service restaurants

want consistent supplier services. Restaurants want the quality of food supplies

to consistently meet their food standards and be delivered on time. The

restaurants reputation is hurt when cases of food poisoning arise, and the

restaurant looses sales if food or container supplies arrive late. In both cases

the restaurant is initially hurt, but blame falls on the supplier. The supplier is

demanded to have low prices and consistent services if they want a profiting

business.

Price Sensitivity

In the quick-service restaurant industry suppliers are viewed as having

low price sensitivity for favoring the accumulation of contracts and retention with

restaurants more important than getting a higher price for their service. The

supplier is in a position to receive more contracts from restaurants if they can

offer lower prices in comparison to the overall supply industry. They can retain

their restaurant contracts with consistent quality of service and willingness to

alter prices along with the changes in market.

Relative Bargaining Power

The bargaining power in the restaurant-supplier relationship gravitates to

the prior party. Restaurants buy in bulk volumes and buy regularly. For the

supplier this relationship delivers a steady stream of revenue, and is highly

desirable. The little bargaining power of the supplier is threatened even more

when a competitor is able to offer lower costing products, which, at a price

would not return a profit for the original supplier. Some instances, the supplier

will take a loss in profits if it means keeping the contract (cost cuts can always

be made in the future to reduce profit loss). In this relationship the restaurants

24

hold the power to bargain, while suppliers must cut costs, reduce prices, and

even take profit losses in order compete in this industry.

Value Chain Analysis

Competitive Strategies

The quick service industry has a high degree of rivalry among existing

firms, a threat of new entrants, and a threat of substitute products. Also, there is

low bargaining power of customers and a moderate power with suppliers. The

quick service industry is a highly competitive market that relies on price and

brand imaging. In order to remain profitable, the companies take into great

consideration the economies of scale, brand imaging, tight cost control, and

product differentiation.

Economies of scale

The quick service industry is a highly competitive market that places an

emphasis on marketing similar products with a different brand image.

Competitors try and use their large scale to influence buying power from

suppliers in the quick-service industry. Also there are many competing quick

service restaurants; there is additional competition with the mom & pop stores.

Brand image

Brand Image identifies what the industry represents. Consumers relate to

brand imaging by gathering some information from the media to inform them on

the quick-service industry. Ways brand image can be affected in the quick

25

service segment is health concerns like reports of contaminated meats, which

decrease sales. This and other factors can have a significant impact on the whole

industry. Brand image is a factor in the quick-service industry but can not be the

focus of the quick service industry because of cost controls.

Tight cost controls

Tight cost control is a way to achieve a competitive advantage in a highly

undifferentiated market, such as the quick service industry. In order to do this,

companies need to “achieve cost leadership, economies of scale and scope,

efficient production, better sourcing and lower input costs” (Business Analysis

and Valuation). Economies of scale and scope in an undifferentiated market

decrease in cost because of large scale operations (www.answers.com). Lower

input costs require minimizing cost of materials, direct labor, and overhead.

Efficient production is achieving cost leadership by producing products at the

lowest cost with the fewest resources (www.investopedia.com). In conclusion,

implementing tight cost controls is an important aspect of the quick-service

industry.

Product differentiation quality, variety, customer service

Product differentiation brings customers to a place of business. Whether it

be because of quality, variety or customer service; differentiation between the

different quick service companies helps bring in the revenue. There are multiple

burger businesses across the nation, and in order to bring business to a specific

firm there needs to be a reason for the consumer to choose one firm over the

other. All of the quick service giants incorporate themes and characters to help

bring out their core values and ideas. In effect advertising is necessary in order

to compete with the large quick service chains but not at the local level.

26

Competitors in the industry try to differentiate themselves through innovation

and reinventing other competitors’ products.

Firm Competitive Advantage Analysis

There are two ways that a company can compete in a market. They are

through cost leadership or differentiation. The difference between the two is that

in a cost leadership industry there are very similar products that must be

produced at the lowest cost possible; while differentiation relies on the

differences in products. Sonic Corporation, like most of the industry, can be

classified as falling somewhere between cost leadership and differentiation.

Economies of Scale

The quick service industries major players are synonymous with low cost

production of its products. McDonalds, Burger King, and Jack in the Box have

centralized distribution centers where they store stock and materials to be

shipped out. Sonic differs from the competition because they contract with local

and regional suppliers to gather its resources without a central distribution

center. This reduces their inventory overhead cost and helps them compete with

larger competitors.

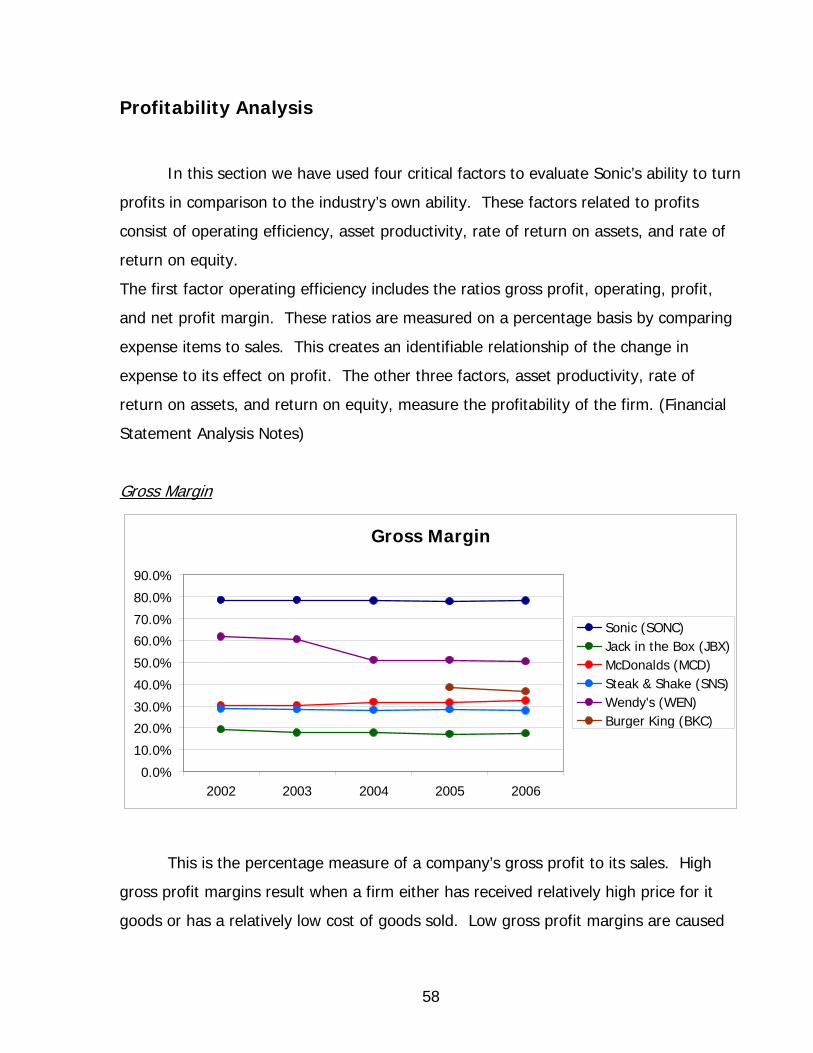

2002 2003 2004 2005 2006Sonic Corp (SONC) 0.79 0.78 0.78 0.78 0.78Burger King Holdings Ord Shs (BKC) 0.37 NA NA NA NAJack in the Box Inc (JBX) 0.19 0.18 0.18 0.17 0.17McDonalds Corp (MCD) 0.30 0.30 0.32 0.31 0.32Steak n Shake Company (SNS) 0.29 0.28 0.28 0.28 0.28Wendys International Inc (WEN) 0.28 0.27 0.21 0.20 0.18derived from 10-K's

Comparative Gross Margins

27

Tight Cost Control

Sonic utilizes cost control by minimizing cost of materials, direct labor, and

overhead. In order to minimize materials and overhead Sonic differs from

McDonalds, Burger King, and Wendy’s by using local resources to gather their

product. This lowers the overhead costs. Also, Sonic minimizes direct labor costs

through efficient production by cutting back employee time during non peak

hours and increasing employee hours during peak hours for maximum

production. Another way they use effective productivity is by having drink

specials from 3-5 pm. This draws customers in at slow points during the day

maximizing productivity.

Brand Image

A firm can face a tremendous set back if the image of their company is

perceived negatively by the customer. Each of the quick service chains rely on

their specific image. Advertisements play a huge role in conveying why each

consumer should try or come back to a quick service business. During the past

couple of years, Sonic has come up with two quirky personas through advertising

to draw attention towards new items They also have car-hops who deliver food

to the car instead of picking it up by drive through. Another difference is Sonics

wide variety of specialty beverages like the Limeades and slushes. Sonic spent

“approximately $145 million for fiscal year 2006” and will increase its advertising

expense to “160 million for fiscal year 2007” (Sonic 10-K 2006). Assuming that

Sonic will be spending more money on advertising next year their brand image

will continue to be a source for attracting new and continued customers.

28

Product differentiation, variety, and customer service

Product differentiation is hard to accomplish when the firm is in the burger

segment, because a burger is just a burger. Differentiation does not only come

from changing an existing industry product. Firms can also differentiate by

offering different products. Sonic’s ability to draw on its specialty beverages,

such as its limeades and slushes, differs from its competitors because they are

offering something that no one else has. Another differentiating factor for Sonic

is its variety. It offers the same variety of burgers and fries but also adds tator-

tots, corn dogs, extra long cheese coneys and various other products that the

other competitors do not have to the menu. Also Sonic’s buildings stand out from

the competitions because they have a new, unique retro fitted look. They also

put a twist on customer service by bringing the food to the customer’s drive-in

space. This makes the customer service more personal and interactive. Sonic

personalizes the quick service experience by this interaction, yet they still

maintain an average “wait time of 4 minutes.”(Sonic 10-K 2006)

29

Accounting Analysis

A firm’s financial statements do not always credibly reflect economic

consequences of business activities. In fact, a lot of the information within a

financial report is reliant on the firm’s interpretations and judgments. So, the

implementation of accounting analysis helps to view the financial statements

with as little managerial bias as possible. Thus, outsiders can see a more true

and transparent picture of how the firm operates. There is a series of six steps

that analysts follow in order to successfully complete the accounting analysis.

The first step is identifying a firm’s key accounting policies and seeing how they

relate to their key success factors and how they relate to the industry. The

second step is to assess the degree of potential accounting flexibility given to

managers as it relates to the key accounting policies. The next step is to

evaluate the actual accounting strategies used by managers as well as the

motives behind those strategies. After that, the quality and depth of disclosure

needs to be evaluated. The fifth step is to determine if there are any red flags,

which might need to be evaluated more in depth. The final step in the

accounting analysis process is to undo the accounting distortions. So, the analyst

is left with accounting numbers that are free of management biases (Palepu &

Healy).

Key Accounting Policies

The industry characteristics and the firm’s competitive strategy are

important factors in determining the firm’s risks and key success factors. It is

also important for an analyst to ensure that their accounting policies are in line

with the firm’s key success factors. Therefore, it is imperative for an analyst to

identify and evaluate the policies that are used by managers to measure those

30

key factors and risks. As determined in the “Firms Competitive Advantage

Analysis” section, Sonic’s key success factors are tight cost control, economies of

scale, brand image, differentiation through menu variety and personal service,

and growth through sales and new locations. Sonic sufficiently discloses, in the

management’s discussion and analysis section, their position on brand image.

They state that they “expand the Sonic brand through new unit growth” and

media spending (Sonic 2006 10-k). Their number of stores and media spending

continues to increase annually. They disclose their spending on media in the

Management Discussion and Analysis Section, so they sufficiently disclose one of

the key parts relating to brand image.

Recent Media Spending (in Millions) 2005 2006 2007 (estimated) Network Cable Television Advertising $60 $72 N/A Total System-wide Media Spending $125 $145 $160

Sonic 10-k 2006

The other part, new unit growth, is also fully disclosed and is broken

down by States and by core and developing markets. This will be further

discussed in the growth section because they both relate to one another through

new unit growth.

Sonic also discloses their stance on product differentiation through menu

variety and personal service, which is one of their key success factors. They will

continue to provide personal car-hop service at the drive-in stalls. This is fully

disclosed in the Management Discussion and Analysis Section and it is repeated

throughout their 10-k. Sonic also says, in their 10-k, that they will offer new

products. The best evidence of menu variety is their menu, which continues to

change with the palettes of their customers.

It is unnecessary to address Sonic’s accounting policy regarding franchise

financing, even though it is a potential liability. This is because it is an

insignificant amount and it is sufficiently disclosed. Unearned revenue, most

31

recently called “Deposits from franchises” by Sonic, is another area that is an

insignificant amount and does not need to be evaluated.

Although firms in this industry attempt to differentiate themselves from

the competition, cost is a major success factor. In particular, selling, general and

administrative costs, food and packaging costs, labor costs, and overall operating

expenses are important factors for managing costs. Thus, managers have an

incentive to make financial statements appear as though they are adequately

managing costs. Sonic makes it clear within their Management Discussion and

Analysis Section what these costs are and their changes relative to the previous

year.

Sonic’s Costs as a Percentage of Total Revenues- after restatement 2001 2002 2003 2004 2005 2006Total revenues 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%Food and packaging 21.05% 21.45% 21.62% 22.01% 22.12% 21.89%Payroll and Labor 22.93% 23.76% 24.63% 25.33% 25.60% 25.33%Selling, general and administrative 9.26% 8.36% 7.93% 8.34% 7.62% 7.51%Total Operating Expenses 16.47% 14.08% 13.76% 13.57% 12.58% 12.86%

Sonic 10-k

Growth is another important aspect of Sonic’s continued success. Even

though this industry is highly competitive, growth is important in the quick

service industry because the market is not stagnant. Consumers increasingly rely

on convenient food sources to save time and money. So, firms must continue to

grow as the market expands in order to maintain or increase their market share.

The following table shows Sonic’s location growth over the past 6 years and is

broken down into their core and developing markets. Their major core markets

include Texas, Oklahoma, Arkansas, Louisiana, Mississippi, Missouri, and

Tennessee. Their major developing markets include Arizona, California, North

32

and South Carolina, Georgia, and Virginia. Most of the developing markets are

located near core markets. Sonic uses media and advertising to reach locations

in the developing markets long before they have a Sonic. Thus, Sonic’s brand

image is more established when a new store is built (Sonic 10-k).

Location Growth 2001 2002 2003 2004 2005 2006Core Markets 1795 1878 1977 2059 2165 2435Developing Markets 564 655 729 826 874 753Total 2359 2533 2706 2885 3039 3188

Sonic 10-K 2001-2006

Sonic continues to grow and develop their core markets in order to be

successful in the quick service industry. As they expand, it is crucial to evaluate

their accounting policy regarding operating vs. capital leases. The determination

about whether to capitalize a lease or consider it an operating lease is a big issue

in the quick service industry. It is an issue because an operating lease does not

reflect a true and fair picture of the firm’s liabilities. The determination is based

on whether the lease is considered a rental contract or if it is equivalent to a

purchase. The effect of capitalizing a lease is an increase in a firm’s assets and

liabilities. On the other hand, if a firm considers a lease to be an operating lease

they do not show it as an asset or liability on the balance sheet. This type of

accounting is an “off-balance sheet” transaction because it fails to increase their

liabilities. So, it appears as though they have fewer future obligations (Palepu &

Healy).

Potential Accounting Flexibility

The degree of accounting flexibility allowed by the Generally Accepted

Accounting Principles continues to change. In fact, prior to January 1, 2002,

33

“purchased goodwill and identifiable intangible assets were capitalized and

amortized over their useful lives” (www.unilever.com P.3). However, post

January 1, 2002 GAAP, under SFAS 142, states that goodwill and other

identifiable intangible assets that have indefinite useful lives will no longer be

amortized (www.unilever.com P.3). This allows managers the freedom to

amortize goodwill only when they believe that it is impaired. In fact, the common

policy across the quick service industry is to amortize goodwill only when

managers believe that it has been impaired. The majority of the goodwill comes

from repurchasing franchise owned locations. The most recent goodwill increase

of $8.5 million was a result of the Tennessee and Kentucky acquisition. This

obviously allows for a lot of management interpretation and provides no “real”

policy regarding when a company should amortize goodwill. Companies in the

quick service industry undoubtedly use this policy to their advantage because the

majority of them have not found it necessary to decrease a significant amount of

their goodwill.

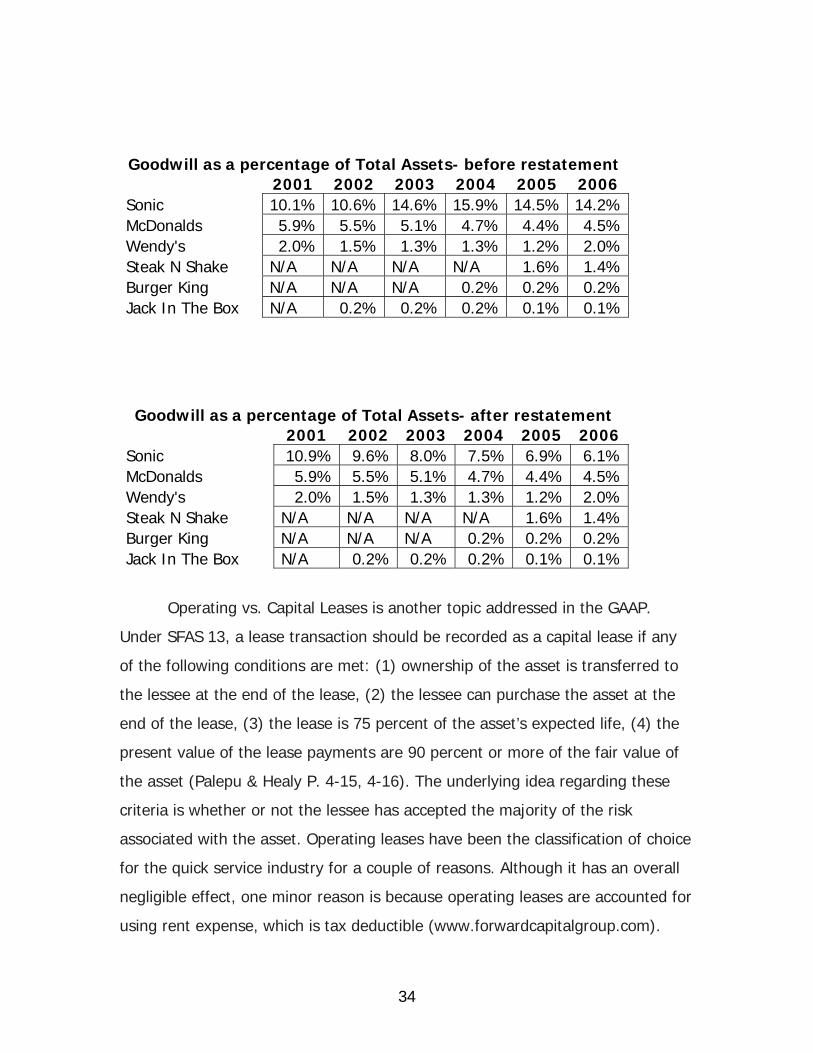

As noted in the following graphs, Sonic’s percentage of Goodwill to Total

Assets is very large compared to its competitors before restatement. This is

because Sonic has a large amount of operating leases which should be

capitalized. So, a smaller total assets value means that the same amount of

goodwill will increase the percentage of goodwill to total assets. After operating

leases were capitalized, the total asset value increased and was a truer picture of

the firm’s total assets. As a result, Sonic’s percentage of goodwill to total assets

became more in line with their competitors.

Goodwill 2001 2002 2003 2004 2005 2006Sonic $38,850,000 $46,826,000 $77,551,000 $87,420,000 $88,471,000 $96,949,000McDonalds $1,320,400,000 $1,558,500,000 $1,665,100,000 $1,828,300,000 $1,924,400,000 $2,209,200,000Wendy's $41,214,000 $272,325,000 $320,959,000 $166,998,000 $81,875,000 $85,353,000Steak N Shake N/A N/A N/A N/A $7,458,000 $14,485,000Burger King N/A N/A N/A $5,000,000 $17,000,000 $995,000,000Jack In The Box N/A $1,988,000 $90,218,000 $90,218,000 $92,187,000 $92,187,000 Source: Respective 10-k’s 2001-2006

34

Goodwill as a percentage of Total Assets- before restatement 2001 2002 2003 2004 2005 2006 Sonic 10.1% 10.6% 14.6% 15.9% 14.5% 14.2% McDonalds 5.9% 5.5% 5.1% 4.7% 4.4% 4.5% Wendy's 2.0% 1.5% 1.3% 1.3% 1.2% 2.0% Steak N Shake N/A N/A N/A N/A 1.6% 1.4% Burger King N/A N/A N/A 0.2% 0.2% 0.2% Jack In The Box N/A 0.2% 0.2% 0.2% 0.1% 0.1%

Goodwill as a percentage of Total Assets- after restatement 2001 2002 2003 2004 2005 2006 Sonic 10.9% 9.6% 8.0% 7.5% 6.9% 6.1% McDonalds 5.9% 5.5% 5.1% 4.7% 4.4% 4.5% Wendy's 2.0% 1.5% 1.3% 1.3% 1.2% 2.0% Steak N Shake N/A N/A N/A N/A 1.6% 1.4% Burger King N/A N/A N/A 0.2% 0.2% 0.2% Jack In The Box N/A 0.2% 0.2% 0.2% 0.1% 0.1%

Operating vs. Capital Leases is another topic addressed in the GAAP.

Under SFAS 13, a lease transaction should be recorded as a capital lease if any

of the following conditions are met: (1) ownership of the asset is transferred to

the lessee at the end of the lease, (2) the lessee can purchase the asset at the

end of the lease, (3) the lease is 75 percent of the asset’s expected life, (4) the

present value of the lease payments are 90 percent or more of the fair value of

the asset (Palepu & Healy P. 4-15, 4-16). The underlying idea regarding these

criteria is whether or not the lessee has accepted the majority of the risk

associated with the asset. Operating leases have been the classification of choice

for the quick service industry for a couple of reasons. Although it has an overall

negligible effect, one minor reason is because operating leases are accounted for

using rent expense, which is tax deductible (www.forwardcapitalgroup.com).

35

Also, capitalizing a lease increases the amount of interest expense in current

years, which results in lower earnings in current years (Kieso, Weygandt, and

Garfield P. 1100). However, these effects, as shown in subsequent sections, are

negligible. The most significant reason a firm would choose to have an operating

lease is because it would be “off the balance sheet”. There will not be a large

asset or liability on the balance sheet reflecting a lease contract. Thus, the firm

will appear more attractive to lenders because it appears as though they have a

lower amount of future obligations.

36

Actual Accounting Strategy

Managers can exploit accounting flexibility when preparing their financial

statements. Managers can either utilize aggressive, conservative, or a

combination of the two accounting strategies when reporting the firm’s economic

situation. However, this discretion provides the ability to conceal a firm’s true

performance and yet still meet GAAP requirements. GAAP standards allow firms

the luxury of disclosure. Higher levels of disclosure allow users to get a true and

fair picture of the firm. In contrast, lower levels of disclosure force users to make

assumptions and can be at times misleading. Sonic displays a moderately

aggressive strategy in their financial reports.

Within Sonics’ financial statements there is a high level of disclosure.

However, Sonic fails to report their operating leases on their balance sheet, but

they do provide sufficient disclosure to make the adjustment. Instead Sonic

includes their operating leases within their operating expenses on their income

statement in order to keep the lease “off the balance sheet”. Reclassifying these

operating leases to capital leases would increase Sonics debt on the balance

sheet and also make them less attractive to future investors, as shown in the

subsequent sections.

Sonic demonstrates their aggressive or “liberal” strategy when

communicating the firm’s goodwill and other intangible assets. The majority of

Sonics intangible assets is not subject to amortization and is only tested for

impairment annually. The impairment process provides the managers of Sonic

with strong incentives to take an aggressive approach because goodwill consists

of over 15% of their total assets. The amount of goodwill that will be impaired

for a given year depends on managements expectations of net income for that

particular year. Sonic has no detailed structure for impairing goodwill, and only

impairs a small amount each year. Furthermore, when restating Sonics goodwill

was impaired the goodwill over a five year period. For instance, when taking a

“liberal” approach if Sonic has a better year than expected, managers will want

37

to impair more goodwill in order to reduce taxes. However, in the circumstance

that Sonic has a below average year the managers would likely avoid impairing

goodwill in order to represent a higher net income that year. This “liberal”

strategy of impairing goodwill is consistent throughout the quick-service industry,

except for Wendy’s. Wendy’s takes a much more conservative approach to

impairing goodwill. Goodwill is reported to the tune of $320,959,000 in Wendys

10k as of 2003, and $166,998,000 as of 2004. Consequently this significant

reduction has a major effect on Wendy’s net income in year 2004. Wendys net

income as of 2003 was $235,999,000 and 2004’s net income was a staggering

$52,035,000 (Wendy’s 03’ and 04’ 10Ks). The $153,961,000 reduction to

goodwill makes up over 80% of the reduction to net income. This fluctuation in

net income illustrates why Sonic chooses a more “liberal” approach to impairing

goodwill.

Qualitative Analysis of Disclosure

All companies have to disclose their financial information in a report called

a 10-K. This report gives investors information on a companies well being.

Moreover the qualitative analysis section divulges the overall satisfaction of

information for the company being evaluated.

Sonic’s overall transparency is fair. There are some areas of concern in

Sonic’s 10-k specifically goodwill. It seems that there has been major increases

over the past couple years of Sonic’s goodwill, boosting its overall intangible

assets. Goodwill can not be measured accurately. Sonic has shown no interest in

impairing its goodwill or depreciating it. Also, Sonic provides very little

information about their operating leases. “An operating lease is not capitalized; it

is accounted for as a rental expense” (investopedia.com). This increases both

their assets and liabilities making it hard to evaluate. Another area of concern is

38

the fact that sonic is selling and buying back its capital leases. This is caused by

the underperforming of its franchisees and Sonic, under contract, has the ability

to buy back the franchised businesses. In the process some value is lost and

Sonic incorporates this as goodwill. Furthermore, Sonic, like other competitors,

does not provide supplementary data and financial statements. Meaning that it

believes the information it provides is sufficient.

Sonic also discloses good information. Some of the good items Sonic

discloses compared to other competitors are franchise operations and sales. It

gives specific information on the average sales for franchises and company

owned drive-ins. There is also good information on how Sonic is trying to expand

and where. Last of all Sonic has been including more information in its 2005 and

2006 10-k’s than in previous years.

Quantitative Analysis

Here we examine the accounting ratios of core sales manipulation and

core expense manipulation in relation to the quick service industry. In doing

quantitative analysis for an industry, the given numbers of the different financial

statements are compared and examined for inconsistencies. Any noted

inconsistency should be investigated for motives. Such motives are the result of

distortions in sales and expense accounting methods used to hide information

from investors.

In the quantitative analysis of the QSI we compare the financial

disclosures of Sonic and its competitors. The graphs were created from the

information given in the I-Metrix program from Edgar Online, which is composed

of our competitor’s 10-k’s.

39

Core Sales Manipulation Diagnostics

Core sales diagnostics or revenue diagnostics is a set of tools we have

used in this section to expose any possible discrepancies with the company’s

accounting concerning sales. Here, we use several ratios related to Sonic’s sales

over the past five years and compare it to five of its biggest competitors. These

ratios that we have used are comprised of the sales of the year and dividing it by

either cash from sales, accounts receivables, or inventory. Once Sonic’s and its

competitor’s ratios have been taken, we look at the anomalies to see whether

these were company specific or industry specific. The company specific

anomalies are subject for investigation.

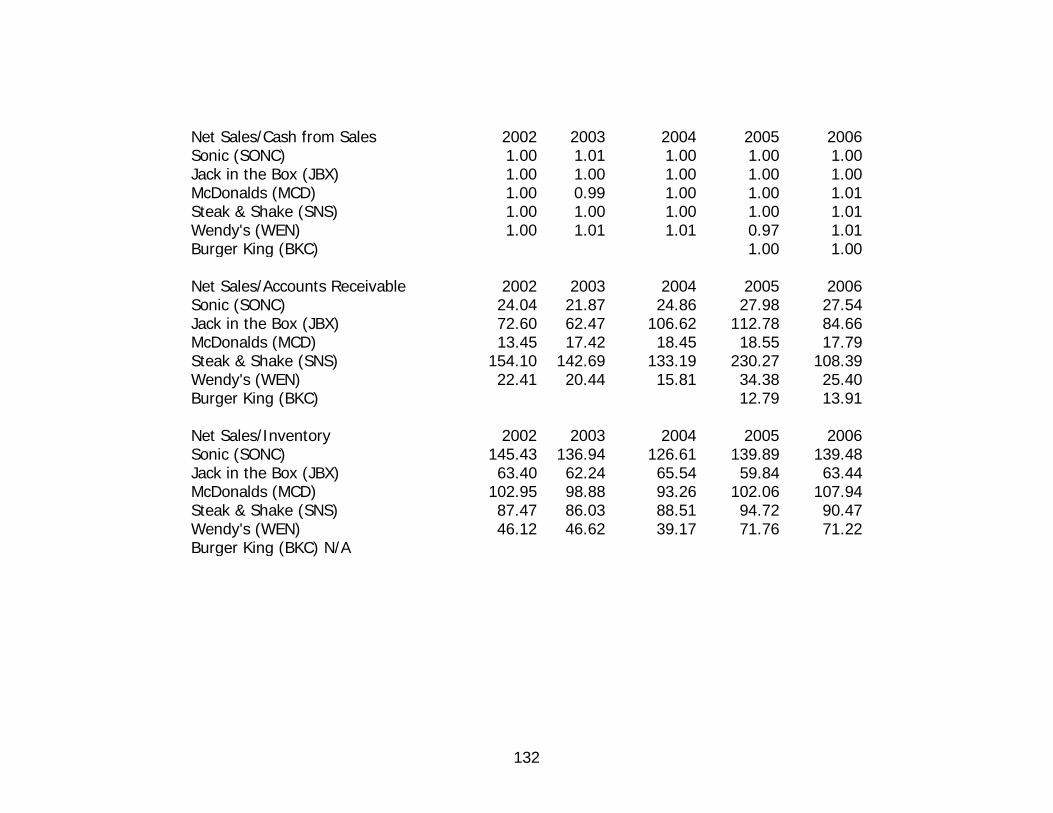

Net Sales/Cash From Sales

0.94

0.95

0.96

0.97

0.98

0.99

1.00

1.01

1.02

2002 2003 2004 2005 2006

Sonic (SONC)Jack in the Box (JBX)McDonalds (MCD)Steak & Shake (SNS)Wendy's (WEN)Burger King (BKC)

The net sales to cash from sales ratio gives an idea of how much of the

sales in a period is collected in cash. The graph above shows us the quick

service industry’s revenue, including Sonic, is almost entirely supported through

cash sales. This is shown by the lines going through and around the ratio

measure of one. The ratio allows us to conclude that cash from sales, such as

the transaction of five dollars for a value meal, are the primary sources of

revenue generation.

40

Wendy’s seems to stand out a little in 2005 because of a drop that looks

big on the graph. However, it is just a one time dip and it should not matter

since we are looking for trends. This could be the result of its decrease in sales,

a climb in receivables, or a huge increase in net income.

Net Sales/Accounts Receivable

0.00

50.00

100.00

150.00

200.00

250.00

2002 2003 2004 2005 2006

Sonic (SONC)Jack in the Box (JBX)McDonalds (MCD)Steak & Shake (SNS)Wendy's (WEN)Burger King (BKC)

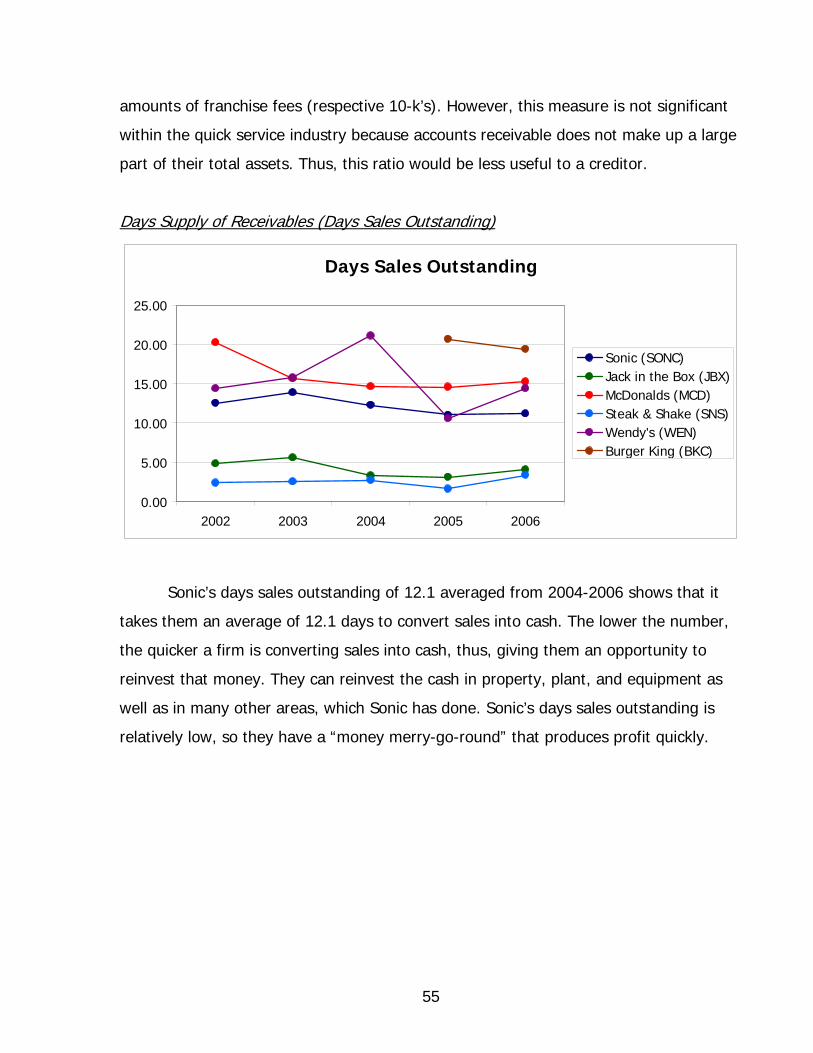

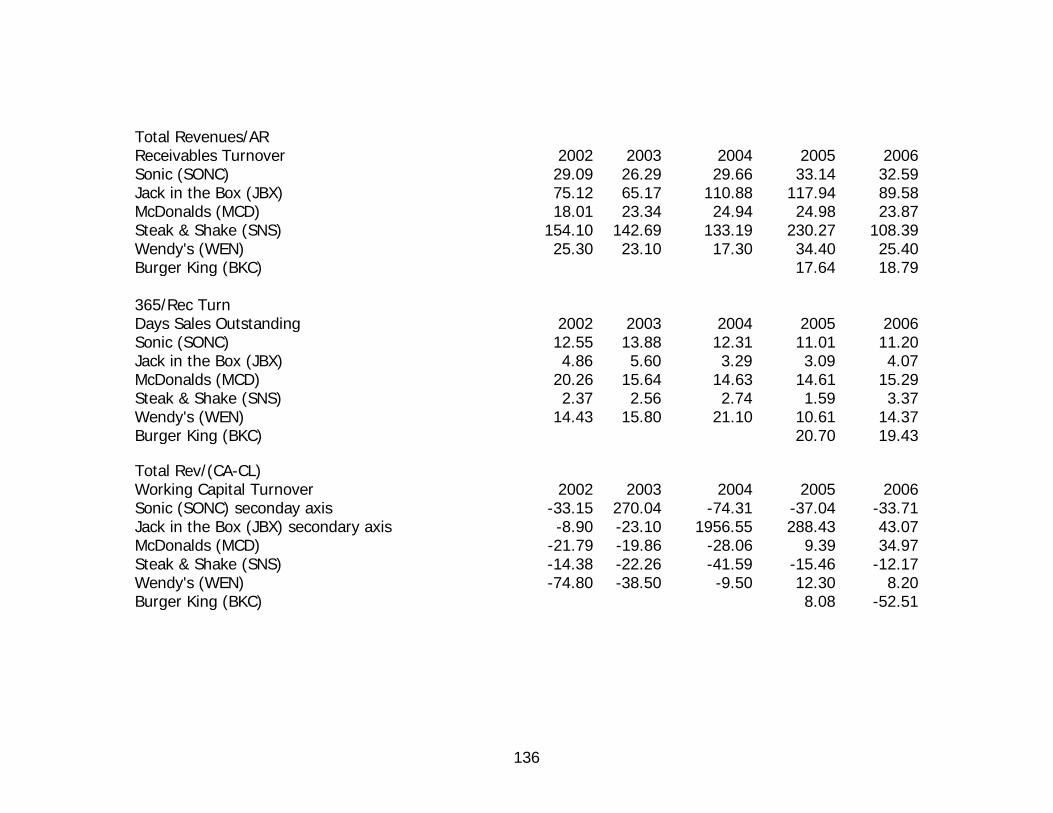

Days Sales Outstanding

0.00

5.00

10.00

15.00

20.00

25.00

2002 2003 2004 2005 2006

Sonic (SONC)Jack in the Box (JBX)McDonalds (MCD)Steak & Shake (SNS)Wendy's (WEN)Burger King (BKC)

The net sales to net accounts receivable ratio shows analyst how much of

sales were credit transactions. In our graph, the industry, including Sonic,

displays low ratios and thus low accounts receivable, which is favorable. For the

most part, the industry keeps a consistently low amount of accounts receivables.

41

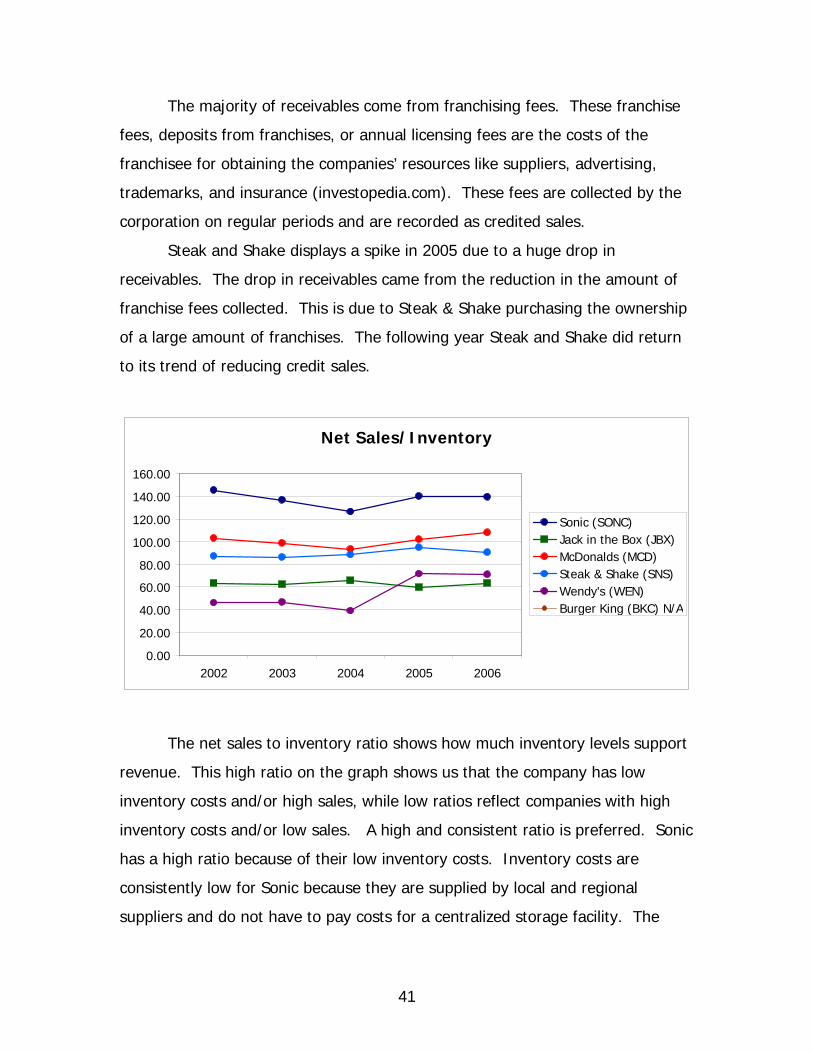

The majority of receivables come from franchising fees. These franchise

fees, deposits from franchises, or annual licensing fees are the costs of the

franchisee for obtaining the companies’ resources like suppliers, advertising,

trademarks, and insurance (investopedia.com). These fees are collected by the

corporation on regular periods and are recorded as credited sales.

Steak and Shake displays a spike in 2005 due to a huge drop in

receivables. The drop in receivables came from the reduction in the amount of

franchise fees collected. This is due to Steak & Shake purchasing the ownership

of a large amount of franchises. The following year Steak and Shake did return

to its trend of reducing credit sales.

Net Sales/Inventory

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

2002 2003 2004 2005 2006

Sonic (SONC)Jack in the Box (JBX)McDonalds (MCD)Steak & Shake (SNS)Wendy's (WEN)Burger King (BKC) N/A

The net sales to inventory ratio shows how much inventory levels support

revenue. This high ratio on the graph shows us that the company has low

inventory costs and/or high sales, while low ratios reflect companies with high

inventory costs and/or low sales. A high and consistent ratio is preferred. Sonic

has a high ratio because of their low inventory costs. Inventory costs are

consistently low for Sonic because they are supplied by local and regional

suppliers and do not have to pay costs for a centralized storage facility. The

42

other companies have lower ratios because of their use in centralized storage

facilities to store inventory.

There are no anomalies to investigate in this graph. Companies did have

drops and gains, but were of no concern because they returned to their normal

levels. For instance, Sonic dropped below their average level in 2004, but

returned to the average the following year. The initial drop means sales are not

supported by inventory. An example of a red flag would look like a drop from

the normal level to a jump above the normal level.

Conclusion

Based on our investigation of Sonic, through the use of sales manipulation

diagnostics, it does not appear that Sonic has manipulated sales. Also, Sonic

was found to be either averaging or out performing in comparison to the quick

service industry averages.

43

Core Expense Manipulation Diagnostics

Core expense diagnostics or expense diagnostics is a set of tools we have

used in this section to expose any possible discrepancies with the company’s

accounting of expenses. Here we use several ratios related to Sonic over the

past five years and compare them to five of its biggest competitors’ ratios. Once

Sonic’s and its competitors’ ratios have been taken, we look to see whether these

were company specific or industry specific. The company specific instances are

subject to investigation.

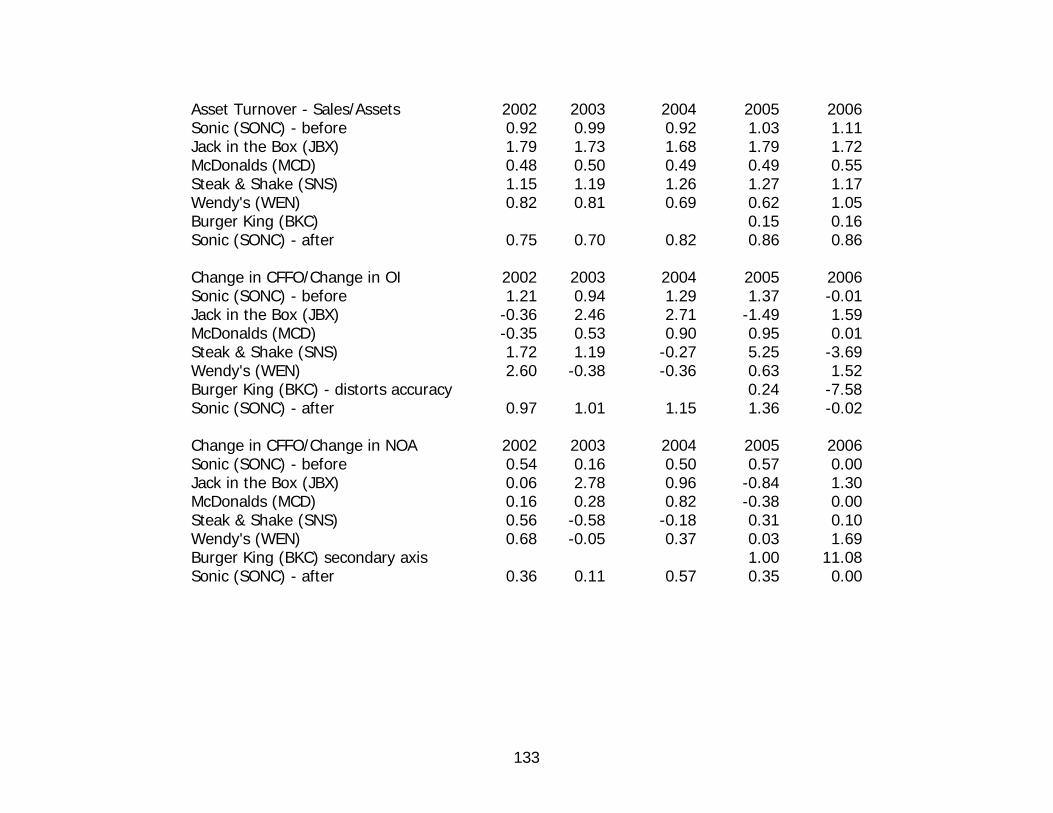

Asset Turnover - Sales/Assets

0.000.200.400.600.801.001.201.401.601.802.00

2002 2003 2004 2005 2006

Sonic (SONC) - beforeJack in the Box (JBX)McDonalds (MCD)Steak & Shake (SNS)Wendy's (WEN)Burger King (BKC)Sonic (SONC) - after

Asset turnover explains whether total assets support net sales. The ratio

is found by dividing net sales by total assets. The graph shows Sonic before and

after the restatement. The rise in the ratio before the restatement reflects a

faster increase in sales than assets. The restatement shows the affect from

capitalization of operating leases. By capitalizing the operating leases we add

operating leases to assets. From the beginning of 2002 to the end of 2007, 114

million in operating leases had been added to Sonic’s assets. The resulting ratios

44

from the restatement are stable and there seems to be no expense manipulation

with assets.

Change in CFFO/Change in OI

-10.00

-8.00

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

2002 2003 2004 2005 2006

Sonic (SONC) - before

Jack in the Box (JBX)

McDonalds (MCD)

Steak & Shake (SNS)

Wendy's (WEN)

Burger King (BKC) - distortsaccuracySonic (SONC) - after

Here we relate the change in cash flow from operations to the change in

operating income. We are looking to see if accrued or deferred expenses have

been manipulated in order to affect net operating income.

Sonic shows consistency and there appears to be no signs of manipulation.

However, Steak and Shake shows signs of possible manipulation. In 2005 the

ratio jumps due to a 17 million dollar increase in CFFO. Over 12 million dollars is

due to a change in income taxes payable. An additional 3 million comes from an

increase in net income. The large drop in 2006 to below 2002 to 2004 levels may

indicate some manipulation.

45

Change in CFFO/Change in NOA

-1.50

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

3.00

2002 2003 2004 2005 20060.00

2.00

4.00

6.00

8.00

10.00

12.00 Sonic (SONC) - before

Jack in the Box (JBX)

McDonalds (MCD)

Steak & Shake (SNS)

Wendy's (WEN)

Sonic (SONC) - after

Burger King (BKC)secondary axis

The change in cash flow from operations to net operating activity ratio

provides us with an idea of how well property, plant, and equipment are

supporting income. High ratios tell us that additional fixed assets are receiving a

higher return. Sonic’s before and after the restatement is relatively close. Sonic

appears slightly lower after the restatement due to the capitalization in operating

leases which increased the change in net operating assets, thus decreasing the

ratio.

Conclusion

We found no evidence that Sonic attempted to manipulate expenses in an

attempt to over or under report earnings. In fact, they seem to perform better

than their industry competitors.

46

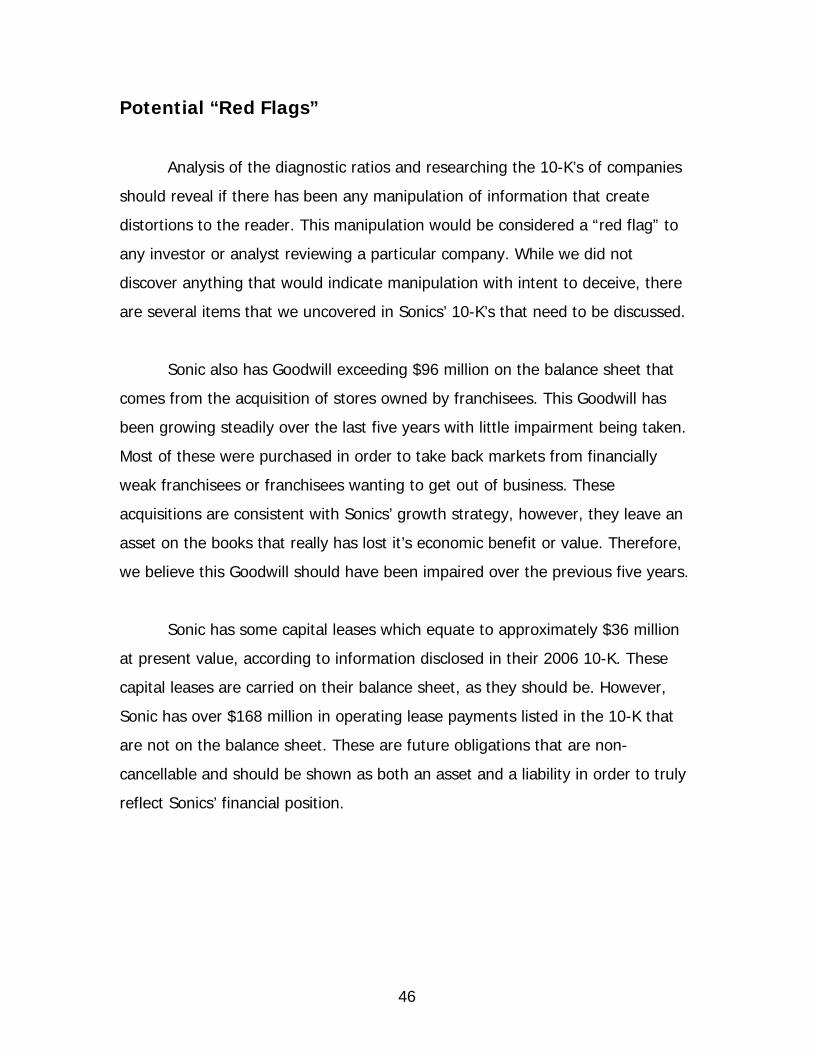

Potential “Red Flags”

Analysis of the diagnostic ratios and researching the 10-K’s of companies

should reveal if there has been any manipulation of information that create

distortions to the reader. This manipulation would be considered a “red flag” to

any investor or analyst reviewing a particular company. While we did not

discover anything that would indicate manipulation with intent to deceive, there

are several items that we uncovered in Sonics’ 10-K’s that need to be discussed.

Sonic also has Goodwill exceeding $96 million on the balance sheet that

comes from the acquisition of stores owned by franchisees. This Goodwill has

been growing steadily over the last five years with little impairment being taken.

Most of these were purchased in order to take back markets from financially

weak franchisees or franchisees wanting to get out of business. These

acquisitions are consistent with Sonics’ growth strategy, however, they leave an

asset on the books that really has lost it’s economic benefit or value. Therefore,

we believe this Goodwill should have been impaired over the previous five years.

Sonic has some capital leases which equate to approximately $36 million

at present value, according to information disclosed in their 2006 10-K. These

capital leases are carried on their balance sheet, as they should be. However,

Sonic has over $168 million in operating lease payments listed in the 10-K that

are not on the balance sheet. These are future obligations that are non-

cancellable and should be shown as both an asset and a liability in order to truly

reflect Sonics’ financial position.

47

Undo Accounting Distortions

Goodwill is the excess amount above identifiable assets and liabilities paid

in the acquisition of another company. Sonic has been accumulating Goodwill for

a number of years with little impairment being taken. We believe this distorts the

true value of the company and should be undone. We began to undo this

distortion in 2001 by taking the ending balance in 2001 and writing the

impairment off over 5 years. Each subsequent year we took the increase in

Goodwill and wrote it off over the next 5 years. This leaves Sonic with a balance

of Goodwill in 2006 of $17,506 to be charge in 2007-2010. This is a considerable

difference from the $96,949 shown on the balance sheet in the 2006 10-K. Table

2-4 reflects the impairment of Goodwill over the previous years, beginning in

2001.

In order to compute the present value of the $168,707,000 in outstanding

lease payments we had to find the current discount rate that would be applicable

to Sonic. Fortunately, Sonic was able to help with the information disclosed in

the 10-K by providing us information on interest paid on capital leases, future

value of all payments, and the present value of all payments. From that data we

were able to get an implied interest rate for each of the years 2001-2006. Using

that interest rate, and information provided on future operating lease payments,

we were able to discount operating leases back to present value. Tables 2-5

through 2-10 provide our calculations.

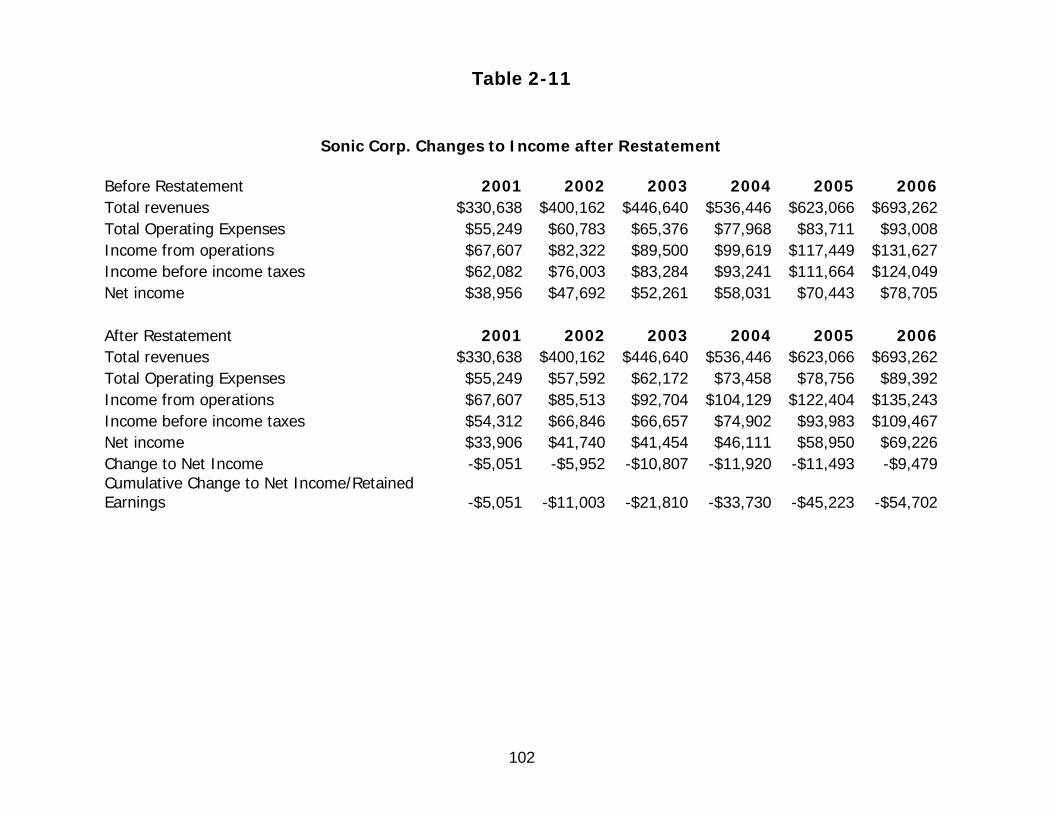

Once the calculations were available, balance sheets and income

statements were recalculated to reflect the changes. Table 2-11 reflects the

changes to the income statement for each period reflecting both the impairment

of Goodwill and the capitalization of operating leases. Not only do these changes

affect the current period, it is worthy to note the cumulative effect to Net Income

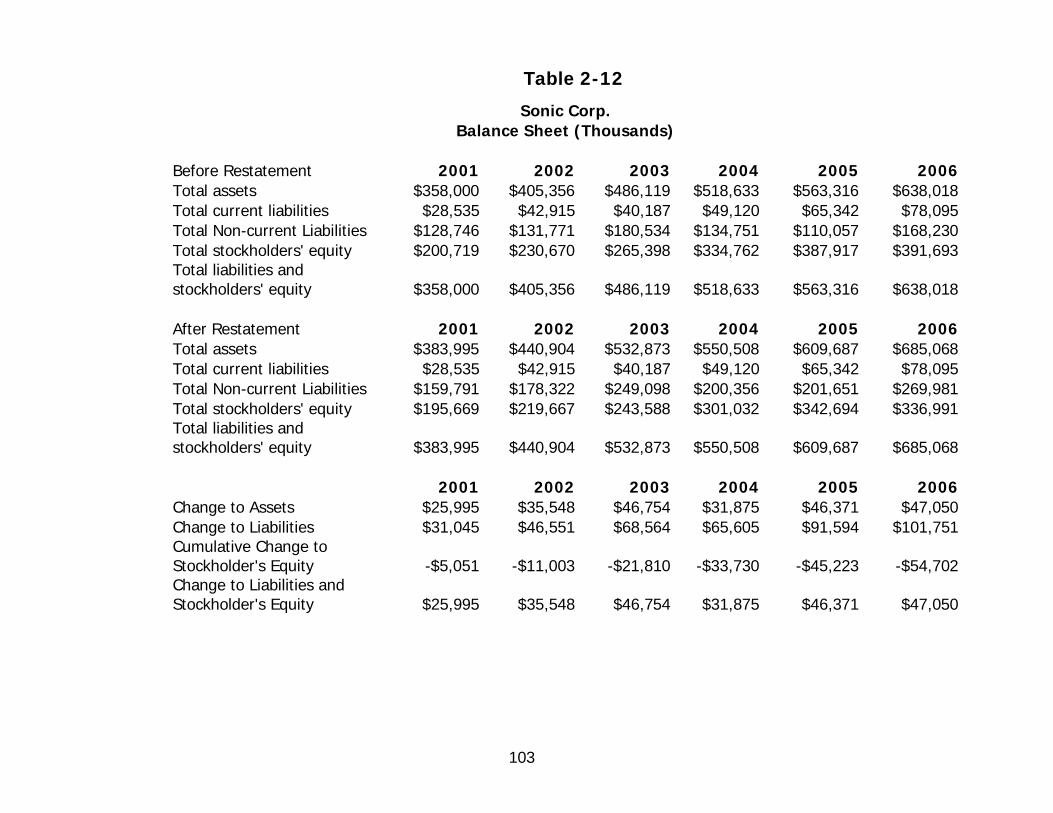

which flows into Retained Earnings. Table 2-12 reflects the changes in the

48

Balance Sheet. As mentioned, you can see the cumulative effect to Retained

Earnings.

Another item worth noting is the effect on assets and liabilities. In the

earlier years the difference between Assets and Liabilities is small, but it

increases each year. This gives a true reflection to the reader about the impact

of impairing Goodwill and capitalizing operating leases. At first glance, one might

not notice the change in Liabilities and Stockholder’s Equity of $47 million.

However, this really reflects a decrease of over $54 million in Retained Earnings

and an increase in Non-Current Liabilities of over $101 million. This information

will be useful to the reader moving forward into the valuation of the company.

49

Financial Analysis, Forecast Financials, and Cost of

Capital Estimation

Financial Analysis

The value of a firm is measured by its profitability and its growth (business

analysis & valuation book). The value and growth of a firm can be seen through

company ratios. Ratios are used to help give a financial analyst an idea of how a

company compares to its competitors. Ratios can also used to help forecast financials.

These ratios are divided into three sections: liquidity ratios, profitability ratios, and

capital structure ratios. Firms that have the most accurate ratios and financial

understanding will have a better chance at forecasting future profitability and growth.

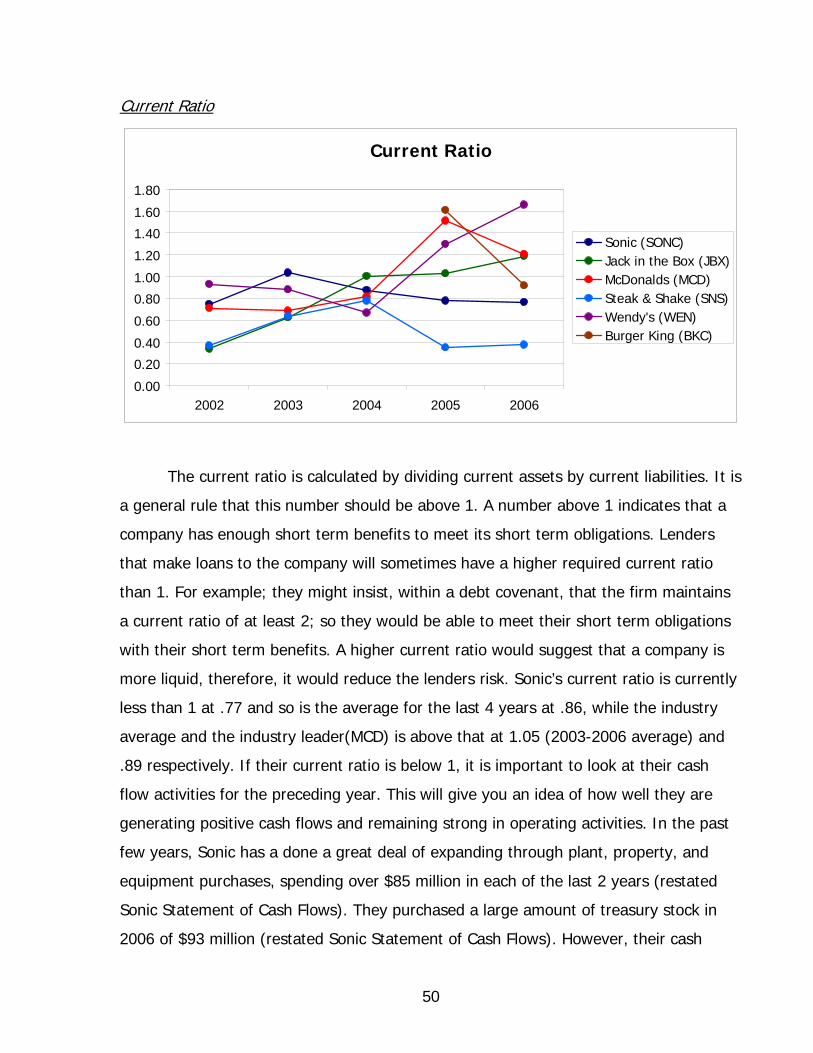

Liquidity Analysis

The results from the liquidity ratios offer insight into how capable a firm is at

meeting their short term obligations. The inventory turnover, receivables turnover, and

working capital turnover indicate the firm’s operating efficiency. The larger these ratios

are, the more efficient the company is. Other liquidity ratios include the quick ratio and

the current ratio. If these ratios are too low, it might suggest that the company does

not have enough liquid assets to meet their short term obligations. On the other hand,

if these ratios are too high, it might indicate that firm is failing to expand their business

because they are holding too much short term assets. All of these ratios are important

to lenders that analyze the risk associated with lending money to a firm. A general rule

is that higher liquidity ratios are better. However, not every rule associated with

liquidity is universal because the results have to be analyzed in the context of the

industry. Also, the ratio averages within the text have been computed using the 2003-

2006 data because it is a closer reflection of the businesses today and because they are

free of distortions from September 11th, 2001.

50

Current Ratio

Current Ratio

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2002 2003 2004 2005 2006