Some “Pilgrim Tales” about Financial Reform in...

34

1 1 Some Some “ “ Pilgrim Tales Pilgrim Tales ” ” about about Financial Reform in Mexico Financial Reform in Mexico Secretar Secretar í í a de Hacienda y Cr a de Hacienda y Cr é é dito P dito P ú ú blico blico

-

Upload

trinhxuyen -

Category

Documents

-

view

217 -

download

2

Transcript of Some “Pilgrim Tales” about Financial Reform in...

11

Some Some ““Pilgrim TalesPilgrim Tales”” about about Financial Reform in MexicoFinancial Reform in Mexico

SecretarSecretaríía de Hacienda y Cra de Hacienda y Créédito Pdito Púúblicoblico

22

An FSAP is always goodAn FSAP is always goodHowever its impact can be maximized if:However its impact can be maximized if:

•• FSAP exercises can be coordinated with the FSAP exercises can be coordinated with the political calendar.political calendar.

•• Assuming financial reform is a Assuming financial reform is a ““technicaltechnical””ongoing process that can ignore politics is a ongoing process that can ignore politics is a grave misunderstanding.grave misunderstanding.

•• FSAPsFSAPs give credibility to past effort reforms give credibility to past effort reforms and provide guidelines for the future reform and provide guidelines for the future reform agenda.agenda.

33

The 2001 FSAP found that “the Mexican financial system was on the path towards greater resiliency to shocks and enjoyed an increasingly favorable environment for its development.”

No banking resolution framework.No banking resolution framework.

There were deficiencies in the strategic role, operations, and There were deficiencies in the strategic role, operations, and financial performance of development banks, which the authoritiefinancial performance of development banks, which the authorities s were addressing through legal, regulatory, institutional, and were addressing through legal, regulatory, institutional, and governance reforms. governance reforms.

The existing framework for housing finance required a major The existing framework for housing finance required a major overhaul. overhaul.

Financial sector supervision required further strengthening and Financial sector supervision required further strengthening and the regulatory framework was being moved toward best the regulatory framework was being moved toward best international practices. international practices.

Regulatory agencies lacked adequate autonomy, and further Regulatory agencies lacked adequate autonomy, and further improvements were needed in the coordination of dayimprovements were needed in the coordination of day--toto--day day supervisory activities, the regulatory field for financial servisupervisory activities, the regulatory field for financial services ces across institutions, and the disclosure practices of some entitiacross institutions, and the disclosure practices of some entities.es.

44

IndexIndexI. Macroeconomic stability as a pre-

requisite.

II. Structural reform in the financial sector as series of many steps

III. Chronicle of a reform foretold: The new Securities Market Law

IV. 2006 FSAP

55

Macroeconomic stability and the development of the financial secMacroeconomic stability and the development of the financial sector are tor are anchored on fiscal discipline. The drop of the public sector financhored on fiscal discipline. The drop of the public sector financial ancial requirements (RFSP) and that of the traditional deficit have redrequirements (RFSP) and that of the traditional deficit have reduced the uced the crowding out of private investment.crowding out of private investment.

*Domestic HBPSBR as a percentage of domestic *Domestic HBPSBR as a percentage of domestic financial savings. financial savings. Source: SHCPSource: SHCP

Domestic Absorption by the Public Sector Domestic Absorption by the Public Sector (Crowding out)*(Crowding out)*

(%)(%)

**The traditional deficit for 2002 excludes the Fin. Rural. Oper**The traditional deficit for 2002 excludes the Fin. Rural. Operation. ation. Source: SHCP.Source: SHCP.

0

10

20

30

40

50

60

70

1999

2000

2001

2002

2003

2004

2005

Traditional Deficit *Traditional Deficit *(% of GDP)(% of GDP)

0.00

0.25

0.50

0.75

1.00

1.25

2000

2001

2002

2003

2004

2005

2006

e

66Source: BanxicoSource: BanxicoQuarterly Data as of march 2006Quarterly Data as of march 2006

An adequate monetary policy targeting a 3% inflation target has An adequate monetary policy targeting a 3% inflation target has been key for macroeconomic stability. The fall in inflation has been key for macroeconomic stability. The fall in inflation has contributed to a decrease in exchange rate volatility.contributed to a decrease in exchange rate volatility.

Exchange rate Volatility(4-m ma)

0.00

0.01

0.02

0.03

0.04

0.05

0.06

I 199

5

I 199

6

I 199

7

I 199

8

I 199

9

I 200

0

I 200

1

I 200

2

I 200

3

I 200

4

I 200

5

I 200

6

Annual Inflation RateAnnual Inflation Rate(%)(%)

Source: Banco de Mexico.

123456789

Jan-

01Ju

l-01

Jan-

02Ju

l-02

Jan-

03Ju

l-03

Jan-

04Ju

l-04

Jan-

05Ju

l-05

Jan-

06Ju

l-06

HeadlineCore

77

As a result of macroeconomic stability there has been a favorablAs a result of macroeconomic stability there has been a favorable decrease in e decrease in interest rates. Sovereign risk has reached historically low levinterest rates. Sovereign risk has reached historically low levels and compares els and compares positively with that of other emerging markets.positively with that of other emerging markets.

Source: BanxicoSource: BanxicoData as of August, 2006.Data as of August, 2006.

MexicoMexico’’s Sovereign Risk: EMBI+s Sovereign Risk: EMBI+(basis points)(basis points)

95

435

775

1115

1455

1795

2135

2475

Jan-

95Ja

n-96

Jan-

97Ja

n-98

Jan-

99Ja

n-00

Jan-

01Ja

n-02

Jan-

03Ja

n-04

Jan-

05Ja

n-06

Note: Before 1998 the EMBI index is presented.Note: Before 1998 the EMBI index is presented.Source: JPMorgan.Source: JPMorgan.

0

15

30

45

60

75

E-95

E-97

E-99

E-01

E-03

E-05

%

Interest RatesInterest Rates(Cetes 28(Cetes 28--d, %)d, %)

88

Debt levels have decreased, external debt has been reduced and the public sector’s financial position has improved.

Source: SHCP (MexicoSource: SHCP (Mexico’’s data) and the World Factbook s data) and the World Factbook 2006, Central Intelligence Agency (for other countries)2006, Central Intelligence Agency (for other countries)

Public Sector Net DebtPublic Sector Net Debt(% of GDP)(% of GDP)

e: Expected for 2006e: Expected for 2006Source: SHCPSource: SHCP

0%

20%

40%

60%

80%

100%

1999

2000

2001

2002

2003

2004

2005

2006

*/

External Internal

0

20

40

60

80

100

120

Italia

Ale

man

iaFr

anci

aEU

Hun

gría

Bra

sil

Polo

nia

Taila

ndia

Mal

asia RU

Sudá

frica

Bul

garia

R

. Che

ca C

hina

C

orea

Méx

ico

Chi

le

%

Public Sector DebtPublic Sector Debt(% of GDP)(% of GDP)

99SourceSource: SHCP: SHCP

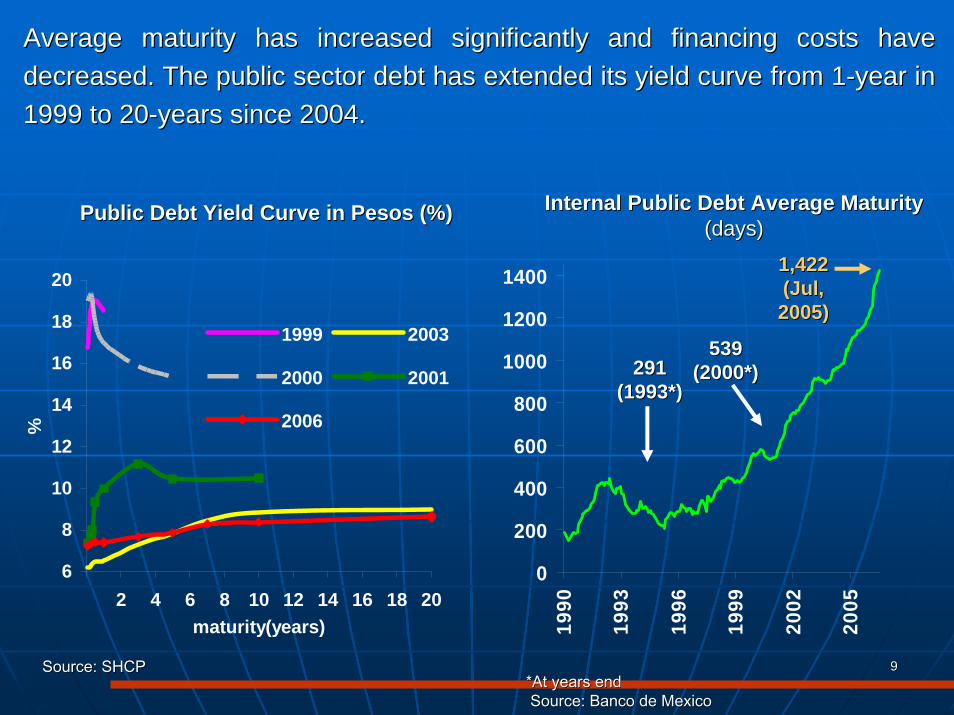

Average maturity has increased significantly and financing costsAverage maturity has increased significantly and financing costs have have decreased. The public sector debt has extended its yield curve fdecreased. The public sector debt has extended its yield curve from 1rom 1--year in year in 1999 to 201999 to 20--years since 2004.years since 2004.

**AtAt yearsyears endendSourceSource: Banco de Mexico: Banco de Mexico

Internal Public Debt Average MaturityInternal Public Debt Average Maturity(days)(days)

291291(1993*)(1993*)

539539(2000*)(2000*)

1,4221,422(Jul,(Jul,2005)2005)

0

200

400

600

800

1000

1200

1400

1990

1993

1996

1999

2002

2005

Public Debt Yield Curve in Pesos (%)Public Debt Yield Curve in Pesos (%)

6

8

10

12

14

16

18

20

2 4 6 8 10 12 14 16 18 20maturity(years)

%

1999 2003

2000 2001

2006

1010

IndexIndexI. Macroeconomic stability as a pre-

requisite.

II. Structural reform in the financial sector as series of many steps

III. Chronicle of a reform foretold: The new Securities Market Law

IV. 2006 FSAP

1111

Financial Sector Depth is highly correlated with income percapita.

Fuente: i) ProfundizaciFuente: i) Profundizacióón financiera: n financiera: LevineLevine, , et. al.et. al., , iiii) PIB ) PIB perper ccáápitapita (Banco Mundial) 2004(Banco Mundial) 2004Cifras de MCifras de Mééxico al 2005: Banxico e INEGIxico al 2005: Banxico e INEGI

Relación entre PIB percapita y profundización financiera

Canada

Korea

Suiza

Argentina Brasil

Chile

España

Alemania

Francia

Japon

México

Estados Unidos

Reino Unido

0

10

20

30

40

50

60

0 50 100 150 200 250 300 350 400 450Profundización financiera (activos financieros % del PIB)

PIB

per

capi

ta, d

ólar

es 2

004

1212

Rather than a single all encompassing structural Rather than a single all encompassing structural reform in the financial sector, during this reform in the financial sector, during this administration there were over 45 legislative administration there were over 45 legislative initiatives approved and many other regulatory initiatives approved and many other regulatory modifications.modifications.

As a whole, these incremental changes translate As a whole, these incremental changes translate into a far reaching structural reform.into a far reaching structural reform.

The financial sector was turned from a The financial sector was turned from a vulnerability and a drag on the economy into an vulnerability and a drag on the economy into an engine for growth with more palpable results as engine for growth with more palpable results as time evolves.time evolves.

At the beginning of the administration the financial At the beginning of the administration the financial sector was a source of vulnerability and not sector was a source of vulnerability and not contributing to economic growthcontributing to economic growth

1313

BANKING SYSTEMBANKING SYSTEMReforms to the Credit Institutions Law (Jun. 01, Jun. 03 & Jun. Reforms to the Credit Institutions Law (Jun. 01, Jun. 03 & Jun. 04)04)Law of Law of BansefiBansefi and its reform (Jun. 01 & Jun. 02)and its reform (Jun. 01 & Jun. 02)Law of Law of FinancieraFinanciera RuralRural (Dec. 02)(Dec. 02)Law of the Law of the SociedadSociedad HipotecariaHipotecaria FederalFederal and its reforms (Oct.01, Jun. 02 & Apr. 06)and its reforms (Oct.01, Jun. 02 & Apr. 06)Law of Transparency and Promotion of Competition in Guaranteed CLaw of Transparency and Promotion of Competition in Guaranteed Credit (Dec.02 & Jun. 03)redit (Dec.02 & Jun. 03)Law for the Transparency and Ordering of Financial Services (04)Law for the Transparency and Ordering of Financial Services (04)Bank Resolutions (Bank Resolutions (aprapr. 06). 06)

NON BANK FINANCIAL INSTITUTIONS, INSURANCE AND BONDING COMPANIESNON BANK FINANCIAL INSTITUTIONS, INSURANCE AND BONDING COMPANIESReform to the Securities Market Law (Jun. 01). The New SecuritieReform to the Securities Market Law (Jun. 01). The New Securities Markets Law (Dec, 05)s Markets Law (Dec, 05)Reform to the Reform to the LeyLey General de General de OrganizacionesOrganizaciones y y ActividadesActividades AuxiliaresAuxiliares de de CrCrééditodito (Jun. 01)(Jun. 01)Savings and Popular Credit Law (Jun. 01)Savings and Popular Credit Law (Jun. 01)Reform to the Insurance Law (Jan. 02, Mar. 06)Reform to the Insurance Law (Jan. 02, Mar. 06)Reform to the Federal Bonding Institutions Law (Jan. 02)Reform to the Federal Bonding Institutions Law (Jan. 02)Reform to the Law of the Reform to the Law of the ComisiComisióónn NacionalNacional BancariaBancaria y de y de ValoresValores (Jun. 01)(Jun. 01)FIBRAS (Fiscal: Art. 223 y 224 LISR, Jan. 04; Bill, May 04 & DecFIBRAS (Fiscal: Art. 223 y 224 LISR, Jan. 04; Bill, May 04 & Decree, Jan. 05, Dec. 05)ree, Jan. 05, Dec. 05)FICAPS (Fiscal: Art 227 & 228 LISR, Dec. 05)FICAPS (Fiscal: Art 227 & 228 LISR, Dec. 05)SOFOMES (Apr. 06)SOFOMES (Apr. 06)

INSTITUTIONAL INVESTORSINSTITUTIONAL INVESTORSReforms to the Law of Saving Systems for Retirement (Dec. 02 & JReforms to the Law of Saving Systems for Retirement (Dec. 02 & Jan. 04)an. 04)Mutual Funds Law (Jun. 01)Mutual Funds Law (Jun. 01)

OTHERSOTHERSPayment Systems Law (Dec. 02)Payment Systems Law (Dec. 02)Reform to the Law for the regulation of financial institutions (Reform to the Law for the regulation of financial institutions (Jun. 01)Jun. 01)Law that rules the credit information companies (credit bureau) Law that rules the credit information companies (credit bureau) (Jan. 02)(Jan. 02)Guarantees Bill (Jun. 03)Guarantees Bill (Jun. 03)Money laundering and terrorism financing bill. (Jan. & May 04)Money laundering and terrorism financing bill. (Jan. & May 04)

*Dates correspond to the publication, in the DOF, of the Law (wh*Dates correspond to the publication, in the DOF, of the Law (when it is new) or the reform. en it is new) or the reform.

Some examples of the legislative initiatives approved Some examples of the legislative initiatives approved indicate the numerous reforms touched on a wide indicate the numerous reforms touched on a wide spectrum of financial sector activities.spectrum of financial sector activities.

1414

Some results: The banking sector is solvent Some results: The banking sector is solvent and aggressively returned to lending. and aggressively returned to lending.

Source: Banxico, CNBVSource: Banxico, CNBV* End of year data* End of year data

Source: BanxicoSource: BanxicoIncludes: securities, outstanding credit portfolio, unperformed Includes: securities, outstanding credit portfolio, unperformed loans; interests ant securities related to the restructuring loans; interests ant securities related to the restructuring process.process.** Last figure July 2006** Last figure July 2006

Capitalization Index (net capital / total risky assets, %)

3.8

4.4

4.44.5

4.02.1 2.1

1.81.4 1.3 1.1

6.1 6.79.1

5.3

10.9

11.3

13.612.7

12.8

13.3

1.4

5.5

4.5

0

4

8

12

16

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Inde

x (%

)

Basic Capital Complementary Capital

Bank financing to the non-bank private sector

(yoy, % growth)

-25

0

25

50

75

100

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

%

Consumption Housing Businesses

Miscellany on Credit Collateral

1515

Some results: The Some results: The ““CertificadoCertificado BursatilBursatil”” opened the opened the possibility of foreign and domestic firms to obtain financing possibility of foreign and domestic firms to obtain financing in the Mexican corporate bond market. Non bank lending in the Mexican corporate bond market. Non bank lending increased in importance as wellincreased in importance as well

Source: Mexican Stock Exchange (BMV) and CNBV

Corporate Debt Market Outstanding (Billion Dollars)

3.8

38.7

-

10

20

30

40

92 94 96 98 00 02 04 Feb-06

Bill

ion

Dol

lars

Other instruments* Certificado Bursátil

0.5

1.0

1.5

2.0

2.5

2000

2001

2002

2003

2004

2005

Outstanding Credit by Outstanding Credit by SofolesSofoles

(% of GDP)(% of GDP)

1616

The fastThe fast--growing mortgage market complemented the Federal growing mortgage market complemented the Federal GovernmentGovernment’’s housing programs.s housing programs.

Includes Includes SedesolSedesol, , BanobrasBanobras, state organisms, , state organisms, PemexPemex, CFE, , CFE, IssfamIssfam and and PEFVM. p/ preliminaryPEFVM. p/ preliminarySource: Source: InformesInformes de de GobiernoGobierno and and ConafoviConafovi..

Public Sector Credit for Housing*Public Sector Credit for Housing*(Billion 2005 pesos)(Billion 2005 pesos)

Number of Credits Awarded in each Number of Credits Awarded in each Administration*Administration*

(millions)(millions)

*/ Total (public and private)*/ Total (public and private)**/ Expected**/ ExpectedSource: SHF.Source: SHF.

0

20

40

60

80

100

120

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

/p

Others**FONHAPO FOVISSSTESHF-FOVIINFONAVIT

1.1

1.6 1.5

3.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1983 -1988

1989 -1994

1995 -2000

2001 -2006**

1717

Institutional investors are increasingly important Institutional investors are increasingly important and have proved to be an important vehicle to and have proved to be an important vehicle to broaden the investor base.broaden the investor base.

Fuente: BanxicoFuente: Banxico

Número de inversionistas en sociedades de inversión (miles)

1358

438

0

200

400

600

800

1000

1200

1400

2000

2001

2002

2003

2004

2005

2006

*\2

Mile

s de

inve

rsio

nist

as

Fuente: CNBVFuente: CNBV

Cartera de valores deinversionistas institucionales

a pesos de dic. 2005

0

400

800

1,200

1,600

2000

2001

2002

2003

2004

2005

2006

*

Mile

s de

mill

ones

de

peso

s

Soc Inversión Aseguradoras SIEFORES Pensiones

1818

As a combined result of all the reform efforts, financial As a combined result of all the reform efforts, financial sector depth as a share of GDP increased after a period sector depth as a share of GDP increased after a period of stagnation.of stagnation.

*M3a minus currency*M3a minus currencySource: BanxicoSource: Banxico

Financial domestic savings (% of GDP)

25

30

35

40

45

50

55

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

%

1919

IndexIndexI. Macroeconomic stability as a pre-

requisite.

II. Structural reform in the financial sector as series of many steps

III. Chronicle of a reform foretold: The new Securities Market Law

IV. 2006 FSAP

2020

Examples: Mexico's stock market and its share of Examples: Mexico's stock market and its share of private equity funds is small by almost any measureprivate equity funds is small by almost any measure..

Source: Capitalization (BMV), GDP (World Bank)Source: Capitalization (BMV), GDP (World Bank)** 2004 data (other countries) and June 2005 for Mexico ** 2004 data (other countries) and June 2005 for Mexico NVCA Yearbook 2004.

Market capitalization (% of GDP)

0

30

60

90

120

150

180

210

Vene

zuel

aM

exic

oPo

land

Turk

eyPh

ilipp

ines

Italy

Bra

zil

Indi

aK

orea

Thai

land

Japa

nSp

ain

USA

Can

ada

Chi

leSi

ngap

ore

%

Brazil32%

North America68%

Europe22%

Asia9%

Latin America

0.9%

Argentina29%

Mexico10%

Others29%

World Private equity flows

2121

In 2005, the World Bank Doing Business Survey ranked MIn 2005, the World Bank Doing Business Survey ranked Mééxico 125 xico 125 out of 145 countries in investor protection indicating that a prout of 145 countries in investor protection indicating that a proper oper regulatory framework for publicly listed companies was at least regulatory framework for publicly listed companies was at least partly partly to blame for the lack of stock market development.to blame for the lack of stock market development.

Source: Doing Business 2006, World Bank.

Minority Protection Index 9.79.3

8.78.3

6.76.3 6 6

5.7 5.7 5.75.3 5.3 5 5 4.7 4.7 4.7

4.3 4.34 3.7 3.7 3.7 3.7

3.3 32.3

0.7

0

1

2

3

4

5

6

7

8

9

10

N. Z

elan

dia

1 S

inga

pur

2C

anad

á3

EU

A 6

Japó

n 1

5P

erú

22In

dia

29

Taila

ndia

33

Col

ombi

a 3

7C

hile

38

Par

agua

y 4

6A

rgen

tina

52

Bra

sil

54N

icar

agua

73

Turq

uía

75

Cor

ea 7

9E

l Sal

vado

r 83

Latin

oam

éric

aB

oliv

ia 9

8C

hina

100

Ecu

ador

113

Hai

tí12

3Jo

rdan

ia 1

24M

EXIC

O12

5S

eneg

al 1

26H

ondu

ras

129

Cos

ta R

ica

134

V

enez

uela

142

Afg

anis

tán

145

Prior to the new law

2222

Main objectives of the new Securities LawMain objectives of the new Securities Law

The new Law attempts to increase the depth of the Stock market by increasing the supply of listed firms and the demand for their stock. In particular:

• It promotes the introduction of new companies into the stock market by making medium size private firms more attractive for venture capital and private equity investments and easing the process of going pubic.

• It improves transparency, minority rights, and radically modernizes the corporate structure of listed companies in line with international practices.

• Other innovations include: modernization of the stock brokerage houses regime, clarification the notification process and the redefinition of legal violations and penalties, and a reasigment of responsibilities between the Ministry and the Supervisor.

2323

A radical modernization of the corporate structure and A radical modernization of the corporate structure and responsibilities of board members and management in responsibilities of board members and management in publicly traded firmspublicly traded firms

..Old RegimeOld Regime New regimeNew regime

AplicationAplicationofof thethe lawlaw

Only to the listed entity.

The entire conglomerate

Board Board functionfunction

Day-to-day administration (including accounting).

Overall business strategy.Surveillance of the company’s

management.

General General DirectorDirector

Without specific responsibilities.

Day-to-day administration.

ComisarioComisario Supervision of the company at all times in an unlimited way

Disappears and replaced by the committees below.

Corporate Corporate and Audit and Audit CommitteeCommittee

Independent and its responsibilities follow international standards

Fiduciary Fiduciary dutiesduties

Clearly defined: create value for the company without benefiting a particular group of shareholders.

2424

2001: Amendments to the 1974 law introducing many modern concepts of corporate governance to public firms.

• The problem was that the modern concepts sat on top of corporate standards that were based on legislation dating back to 1934.

Summer-2002: Corporate Governance scandals in the United States provide a “potential opportunity” to make further adjustments.

February- 2003A small team of 6 people from the Ministry, the Supervisory Agency and two external lawyers begin working on a draft.

January -2003: Technically consensus is reached that a new law is needed instead of a new set of amendments.

2001 2002 2004 20052003

March 2004: First draft is finished and distributed widely. (Too late to submit it to Congress).

2525

April-December 2004 : A wide consultation and ownership process

• A “lead” group of the top 15 corporate lawyers in met every Thursday from 5-8 from April to December to review every article of the law.• There were meetings with representatives of all groups involved: Investment banks, investment advisors, accountants, lawyers, exchanges, etc.• There were over 200 meetings with external groups to hear comments.• There were hundreds of written comments received and thousands of oral comments incorporated.•The spirit of the law was maintained but the actual draft of the law was completely different.• A wide ownership process took place. Individuals involved would talk about “their initiative” no the President's.

August-2002: US Corporate Scandals

2003 January: New law over amendments

2003 February Drafting begins

2001 Amendments

2001 2002 2004 20052003

March 2004: First draft finished.

2626

April-December 2004 : A wide consultation and ownership process

August-2002: US Corporate Scandals

2003 January: New law over amendments

2003 February Drafting begins

2001 Amendments

2001 2002 2004 20052003

March 2004: First draft finished.

March 2005: Bill is submitted to Congress.

April - 2005: The law is approved by the Senate. Modifications do not fundamentally change the law:

May-December-2005: The lobbying continued in the lower chamber.• The Doing Business Report played a key role:

2727

The World Bank study indicates a substantial improvement in Mexico's investor protection with the approval of the new Securities Law

Source: Doing business Report, World Bank. *The ranking and grade after passing the New Law corresponds to the latest data released by the WB in the Doing Business Report 2007.**he ranking and grade for Mexico under the Old Law and with the revisions proposed during its negotiation process correspond to those published in the Doing Business Report 2006, as they were published by the World Bank in 2005.

Investor Protection, Corporate Governance Index

9.79.3

8.3 8.3

6.76.3

5.75.3 5.3 5.3

4.7 4.74.3 4.3

3.7 3.73.3

2.7

0.7

3

44

55

6666

7

012345

6789

10N

ew Z

elan

d 1

Sing

apor

e 2

Can

ada

5U

SA 5

Japa

n 12

Peru

15

Chi

le 1

9C

olom

bia

33In

dia

33M

exic

o 33

*Th

aila

nd 3

3Pa

ragu

ay 4

6B

razi

l 60

Kor

ea 6

0Tu

rkey

60

Chi

na 8

3N

icar

agua

83

Arg

entin

a 99

El S

alva

dor 9

9B

oliv

ia 1

18Jo

rdan

118

Ecua

dor 1

35Se

nega

l 135

Mex

ico

125

**H

aiti

142

Hon

dura

s 15

1C

osta

Ric

a 15

6Ve

nezu

ela

162

Afg

hani

stan

173

With Old Law**

With the New Law*

c

2828

The investor protection index and the size of the stock market are correlated.

Source: i) Market capitalization, BMV; ii) GCP World Development Indicators, World Bank and for Mexican data INEGI; iii) Investor protection index: Doing Business 2006, World Bank.

Investor Protection Index vs. MarketCapitalization as % of GDP

Fil

Ita Cor

EUACan

FranChile

Ven

México Current

Pol

Tur AlemBraInd

Esp

AustraliaMexico new Law

Arg

Per

0

2

4

6

8

10

0 20 40 60 80 100 120 140Market capitalization (% of GDP) 2004

Inve

stor

prot

ecio

nin

dex

(200

4)

Potential growth withthe new Law

2929

IndexIndexI. Macroeconomic stability as a pre-

requisite.

II. Structural reform in the financial sector as series of many steps

III. Chronicle of a reform foretold: The new Securities Market Law

IV. 2006 FSAP

3030

2006: As concerns for financial system stability have eased, policy attention has increasingly turned toward issues of competition, efficiency, and access.

EVOLUTION OF FINANCING TO THE PRIVATE SECTOREVOLUTION OF FINANCING TO THE PRIVATE SECTOR•• The prospects for continued private sector financing growth are The prospects for continued private sector financing growth are positive although not positive although not

uniformly so across all segments. uniformly so across all segments.

COMPETITION ISSUES IN PAYMENT SERVICES AND CREDIT MARKETSCOMPETITION ISSUES IN PAYMENT SERVICES AND CREDIT MARKETS•• Current indications are that there is no good balance between coCurrent indications are that there is no good balance between cooperation and operation and

competition in the retail payments area, with banks tending to lcompetition in the retail payments area, with banks tending to limit access to imit access to infrainfra--structure instead of competing on fees and services. structure instead of competing on fees and services.

•• The analysis of competition in different credit markets is hindeThe analysis of competition in different credit markets is hindered by lack of data.red by lack of data.

ORGANIZATIONAL ARRANGEMENTS FOR EFFECTIVE FINANCIAL SYSTEM ORGANIZATIONAL ARRANGEMENTS FOR EFFECTIVE FINANCIAL SYSTEM REGULATION, SUPERVISION, AND FINANCIAL SECTOR POLICYMAKINGREGULATION, SUPERVISION, AND FINANCIAL SECTOR POLICYMAKING•• Substantive progress was made to adapt the arrangements for effeSubstantive progress was made to adapt the arrangements for effective financial ctive financial

system regulation, supervision, and policymaking to the new condsystem regulation, supervision, and policymaking to the new conditionsitions•• However, further reforms are needed for the Commissions to attaiHowever, further reforms are needed for the Commissions to attain full autonomy. n full autonomy. •• Reforms are also required to implement a fullReforms are also required to implement a full--fledged consolidated supervision of fledged consolidated supervision of

financial groupsfinancial groups•• The system of cross opinions on proposed new regulations, which The system of cross opinions on proposed new regulations, which reflects a desire to reflects a desire to

establish adequate checks and balances, is unduly cumbersome. establish adequate checks and balances, is unduly cumbersome.

3131

20062006……FINANCIAL SAFETY NET ARRANGEMENTSFINANCIAL SAFETY NET ARRANGEMENTS•• Significant reforms to the banking safety net introduced inSignificant reforms to the banking safety net introduced in 2001 include the 2001 include the

revamping of the prompt corrective action regime and the phasingrevamping of the prompt corrective action regime and the phasing out of the out of the previously unlimited guarantee on bank liabilitiespreviously unlimited guarantee on bank liabilities..

•• In addition, the new bank resolution framework needs to be complIn addition, the new bank resolution framework needs to be complemented by emented by legal reforms to create a suitable framework for bank liquidatiolegal reforms to create a suitable framework for bank liquidation.n.

PRIVATE PENSIONS, INSURANCE, AND ANNUITIESPRIVATE PENSIONS, INSURANCE, AND ANNUITIES•• The authorities have succeeded in significantly increasing compeThe authorities have succeeded in significantly increasing competition on fees in tition on fees in

the definedthe defined--contribution (DC) pension fund industry.contribution (DC) pension fund industry.•• CONSAR should step up efforts to promote competition on net (risCONSAR should step up efforts to promote competition on net (riskk--adjusted) adjusted)

returns. returns. •• Over the medium term, CONSAR should consider further relaxing thOver the medium term, CONSAR should consider further relaxing the ceilings on e ceilings on

pension fund investment in foreign assets and equities. pension fund investment in foreign assets and equities.

HOUSING FINANCE MARKETSHOUSING FINANCE MARKETS•• SinceSince 2001, there has been impressive progress in establishing the key2001, there has been impressive progress in establishing the key building building

blocks for sustainable mortgage securitization and private mortgblocks for sustainable mortgage securitization and private mortgage origination age origination markets. markets.

•• Further steps should be taken toward establishing a centralized,Further steps should be taken toward establishing a centralized, integrated integrated policy on housing finance subsidies for lowpolicy on housing finance subsidies for low--income households. income households.

•• The start of a mortgageThe start of a mortgage--backed securities market is an important and backed securities market is an important and fundamental achievement but some questions have been raised overfundamental achievement but some questions have been raised over what what appears to be lessappears to be less--thanthan--satisfactory due diligence reviews on securitized satisfactory due diligence reviews on securitized portfolios. portfolios.

3232

20062006……STRATEGIC ISSUES IN THE REFORM OF DEVELOPMENT STRATEGIC ISSUES IN THE REFORM OF DEVELOPMENT BANKSBANKS•• Substantial progress has taken place over the last five years inSubstantial progress has taken place over the last five years in

reforming the system of development banks and funds (reforming the system of development banks and funds (DBsDBs), ), along the lines recommended in the 2001 FSAPalong the lines recommended in the 2001 FSAP..

•• Beyond the mentioned general improvements, however, the Beyond the mentioned general improvements, however, the depth and breadth of reform in other respects has been very depth and breadth of reform in other respects has been very uneven across uneven across DBsDBs. .

•• In the case of other In the case of other DBsDBs, mandates remain unclear and their , mandates remain unclear and their initial raison dinitial raison d’’être is loosing relevance in the face of rapid être is loosing relevance in the face of rapid financial market development; however, NAFIN has shown financial market development; however, NAFIN has shown notable managerial improvements and instrument innovation. notable managerial improvements and instrument innovation.

•• Over the longer term, the DB system should be further Over the longer term, the DB system should be further consolidated, mandates reformed and made dynamic in some consolidated, mandates reformed and made dynamic in some cases, and major improvements introduced in the way in cases, and major improvements introduced in the way in which which DBsDBs performance is measured and rewarded. performance is measured and rewarded.

3333

Final Final ThoughtsThoughts

Mexico has achieved macroeconomic Mexico has achieved macroeconomic stability which is a necessary but not stability which is a necessary but not sufficient condition for growth.sufficient condition for growth.

Financial reform is not apolitical.Financial reform is not apolitical.

FSAPsFSAPs can provide credibility to past reform can provide credibility to past reform efforts and help set the reform agenda.efforts and help set the reform agenda.

FSAPsFSAPs do not (and could not) provide do not (and could not) provide guidance in the reform process.guidance in the reform process.

3434

Some Some ““Pilgrim TalesPilgrim Tales”” about about Financial Reform in MexicoFinancial Reform in Mexico

SecretarSecretaríía de Hacienda y Cra de Hacienda y Créédito Pdito Púúblicoblico