Some instability puzzles in Kaleckian models of growth and distribution Eckhard Hein, Marc Lavoie...

29

Some instability puzzles in Kaleckian models of growth and distribution Eckhard Hein, Marc Lavoie and Till van Treeck

-

Upload

loreen-dickerson -

Category

Documents

-

view

216 -

download

2

Transcript of Some instability puzzles in Kaleckian models of growth and distribution Eckhard Hein, Marc Lavoie...

Some instability puzzles in Kaleckian models of growth

and distribution Eckhard Hein, Marc Lavoie and

Till van Treeck

The Kaleckian model

• Three essential equations– A saving function– A pricing function (income distribution)– An investment function

• The actual rate of capacity utilization is endogenous, determined by demand, even in the long run, and so in general will not be equal to the normal rate of capacity utilization

• Consequences: the paradox of thrift, and under some specifications, the paradox of costs

Justification• The Kaleckian model of growth has become a

workhorse of heterodox economics since the early 1980s, proving to be highly flexible.

• Some authors claim however that one may be Kaleckian or ‘Keynesian in the short run’ but needs to be ‘Classical in the long run’ (Duménil and Lévy 1999, Shaikh 2007).

• Others argue that ‘the current dominance of the Kaleckian model (…) is unfortunate’ for post-Keynesian and Structuralist macroeconomics (Skott 2008).

• The purpose of this paper is to show that these opinions are premature.

Consequences of the critique

• Somehow the actual rate of capacity utilization must be brought back to its normal rate

• Somehow Harrod’s warranted rate of growth must constrain the economy, and the classical equation must hold:

• gw = s/v =sprn

• The paradoxes of thrift and of costs don’t hold anymore

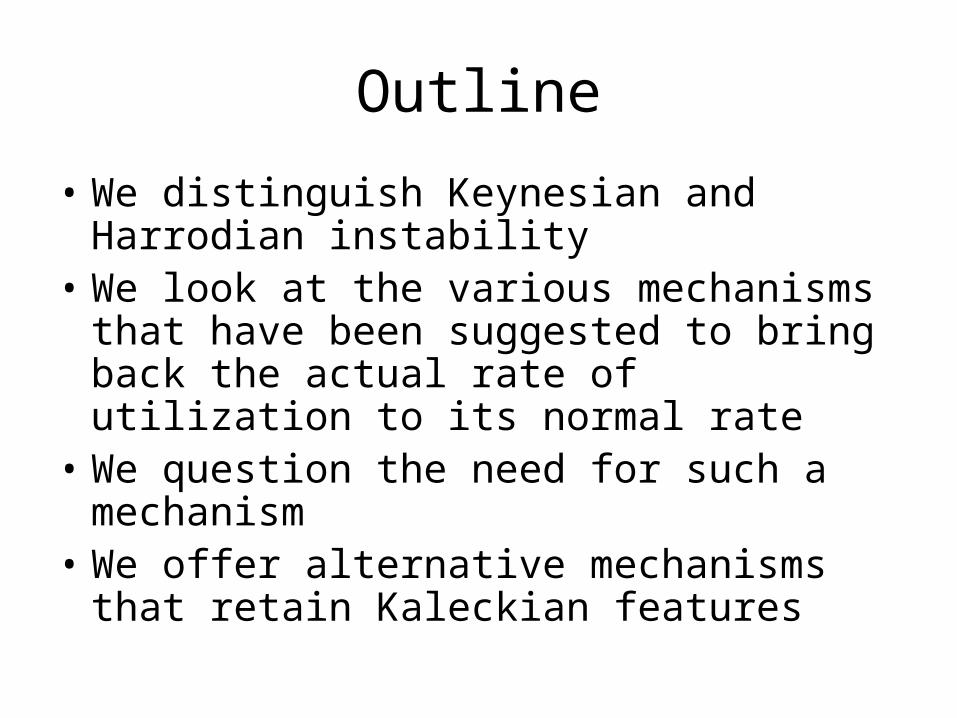

Outline

• We distinguish Keynesian and Harrodian instability

• We look at the various mechanisms that have been suggested to bring back the actual rate of utilization to its normal rate

• We question the need for such a mechanism

• We offer alternative mechanisms that retain Kaleckian features

Instability

• There have been two somewhat related kinds of criticisms:– Keynesian stability (the slope of the saving function is

steeper than that of the investment function), as assumed in Kaleckian models, is doubtful.

– Harrodian instability (the investment function shifts out if u > un)), as assumed away by Kaleckians, is likely.

– Therefore, there must exist some other mechanism that brings back the economy towards its normal rate of capacity utilization (shifting back in the investment function, or shifting the saving function)

gsgig

uu*

g*

uK

gi(ue)

ue

Keynesian instabilityShort period

0),( eKe uuu

gs

gi

g

uun

γ0=g0

u1

γ3

γ2

g3

u2 u3

A

C

Bg2

Harrodian instability 0),*( nuu

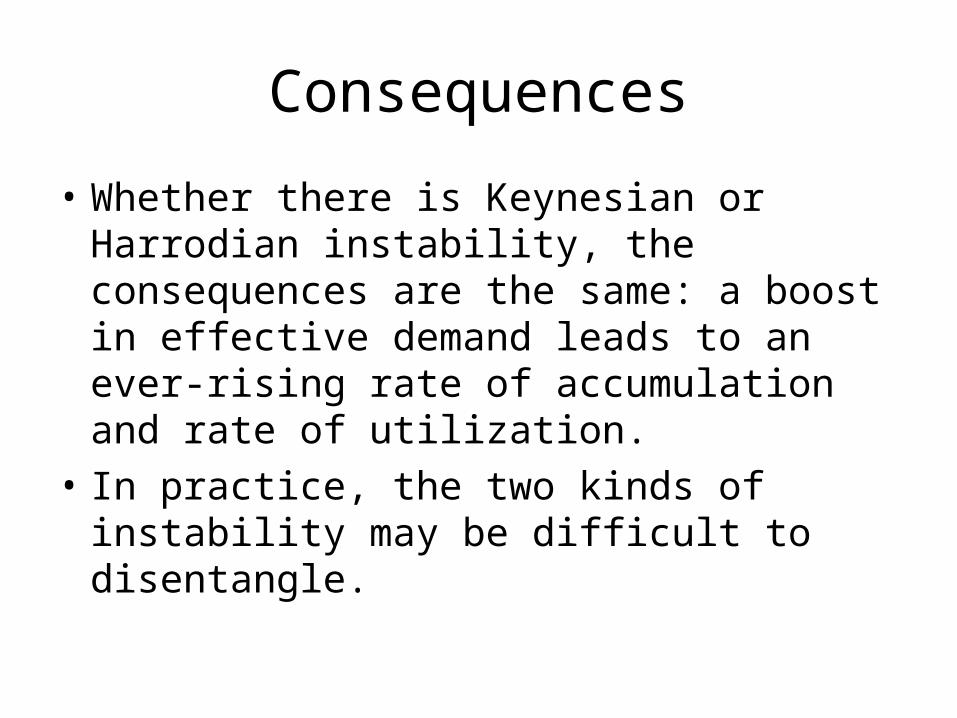

Consequences

• Whether there is Keynesian or Harrodian instability, the consequences are the same: a boost in effective demand leads to an ever-rising rate of accumulation and rate of utilization.

• In practice, the two kinds of instability may be difficult to disentangle.

The “classical” mechanisms designed to bring back utilization to its normal rate

• Mechanisms acting on the saving function – The Cambridge price mechanism, acting on

the profit margin– The retention rate solution, acting on the

overall propensity to save

The Cambridge price mechanism

• (Robinson 1956, Kaldor 1956; Harcourt Kenyon 1977, Eichner 1976, Wood 1975, Marglin 1984, Skott 1989)

• The profit margin rises as long as u > un, thus rotating the saving function.

• The paradox of thrift is only retained if accumulation depends on the profit rate

• The mechanism has been described either as an ultra-short run mechanism, or as a long-run mechanism.

• The profit margin, hence real wages fall, when employment rates and growth are high. Doubtful?

0),*( nn uur

,

The retention rate solution

• This is the Shaikh I solution (2007)• “This classical synthesis allows us to preserve central

Keynesian arguments such as the dependence of savings on investment and the regulation of investment on expected profitability, without having to claim that actual capacity utilization will persistently differ from the rate desired by firms” (Shaikh)

• The retention ratio of firms rises as long as u > un, thus rotating the saving function

• However, the paradoxes of saving and of costs disappear, because: g** = γrrn

• Doubtful?

0),*( nf uus

Shaikh I solution

gs

gi

g

uun

g0

u1

g2

g1

The “classical” mechanisms designed to bring back utilization to its normal rate

• Mechanisms acting on the investment function – Monetary authorities get scared of inflation

and raise real interest rates– Capitalists get scared of full employment and

reduce the rate of growth of output– Capitalists have perfect foresight and revise

their sales expectations

Monetary authorities get scared of inflation, and raise real interest rates, thus lowering investment

• The Duménil and Lévy (1999) mechanism• Similar to the New consensus mechanism• Also has resemblance with Robinson’s inflation frontier• Both the paradoxes of thrift and of costs get wiped out

0, nuu

The Duménil and Lévy mechanism: low saving rates lead to high growth in the short run, but lower

growth in the long run

gs

gi

g

uus

g0

u1

g2

g1

Drawbacks of the Duménil and Lévy mechanism

• Higher rates of utilization may not mean higher or accelerating inflation rates

• Higher rates of interest may not succeed in slowing down demand (it may increase consumer demand instead)

• When demand needs to be pumped up, it may be impossible to lower real interest rates sufficiently (zero lower-bound problem)

• Raising the interest rate is likely to lead to a lower “normal” rate of utilization (a different NAIRU), as firms raise their profit margins, and there is no guarantee that the actual rate will converge to this evolving normal rate (Hein 2006, 2008).

Capitalists get scared of full employment and reduce the rate of growth of output

• This is the Skott mechanism (1989, 2007, 2008).• In the ‘mature economy’, the rate of output growth is a

positive function of the profit share and a negative function of the employment rate.

• If the employment rate rises above its steady state value, capitalists reduce output growth, sales growth declines, the actual rate of utilization falls, and the constant in the investment function starts to shrink.

• The cause: firms have increasing problems to recruit additional workers, workers and labour unions are strengthened vis-à-vis management, workers’ militancy increases, monitoring and surveillance costs rise, and hence the overall business climate deteriorates.

0, nuu

Drawbacks of the Skott mechanism

• It is not clear why output growth should be a positive function of the profit share: his excludes Kaleckian effects by assumption.

• It is not clear why high employment rates, accompanied by more powerful workers and labour unions, should induce capitalists to reduce output growth in the first place.

• One would rather think that high employment rates generate rising nominal wage growth. This should cause either rising inflation or a falling profit share, or both.

• But the latter would intensify Harrodian instability!• What about labour supply growth being driven by labour

demand growth?

Capitalists have perfect foresight and revise their sales expectations

• The Shaikh II (2007) mechanism• Based on a special ‘Hicksian’ stock-flow

investment adjustment function.• Investment depends on the rate of utilization and

the growth rate of sales that will be realized in the current period

• If so, it can be shown that the actual rate of capacity utilization necessarily converges to its normal rate.

0,, uynuyi guugg

un

u

u

û

ggs

+0−

γ = gk0 = gy0gi = gy + γu(u−un)

gy2

gkal

u1u2

gk2

gk3 = gy3

ukal

Figure 12

Drawbacks of the Shaikh II mechanism

• Firms must know the growth rate of their sales.• But this rate depends on the investment

expenditures of all other firms.• Thus, each firm needs to know what all other

firms simultaneously decide.• The informational requirements are huge.• The behaviour of managers is unlikely: following

a period of rising rates of utilization, firms need to believe that sales will grow more slowly.

• If firms act in some adaptive way, Harrodian instability reappears.

Questioning the necessity of any adjustment of u towards un

• Provisional equilibrium; everything moves anyway (Chick and Caserta 1997)

• Other stock-flow norms in growth models are not realized, even when agents try to achieve them – wealth/income targets (Godley)

• There is a large range of acceptable “desired” or “normal” rates of capacity utilization (Dutt 1990).

• A firm may operate each running plant at optimal capacity (cost-minimizing), while being unable to to run all plants (idle capacity) (Caserta 1990).

Acceptable range

• ‘The stock adjustment principle, with its particular desired level of stocks, is itself a simplification. It would be more realistic to suppose that there is a range or interval, within which the level of stock is “comfortable”, so that no special measures seem called for to change it. Only if the actual level goes outside that range will there be a reaction.’ (Hicks 1974, p. 19)

Even Sraffians accept that firms usually have idle capacity

• ‘It is virtually impossible for the investment-saving mechanism … to result in an optimal degree of capacity utilization…. It is, rather, expected, that the economy will generally exhibit smaller or larger margins of unutilized capacity over and above the difference between full and optimal capacity’. (Kurz 1994)

• ‘One must keep in mind that although each entrepreneur might know the optimal degree of capacity utilization, this is not enough to insure that each of them will be able to realize this optimal rate’. (Kurz 1993)

Still, we do not wish to sweep the the problem under the carpet

• There are mechanisms that can bring together the actual and the normal rates of capacity utilization, by making the normal rate endogenous to the values taken by the actual rate (Lavoie 1992, 1996, 2003; Cassetti 2006, Commendatore 2006).

• So normal rates adjust to the actual rates.• With some specifications, these hysteresis models

safeguard both the paradoxes of thrift and of costs.• A critique of these has been: why would firms modify the

normal rate of utilization just because it has not been achieved recently (Skott 2008)?

A possible answer: because firms have multiple targets !

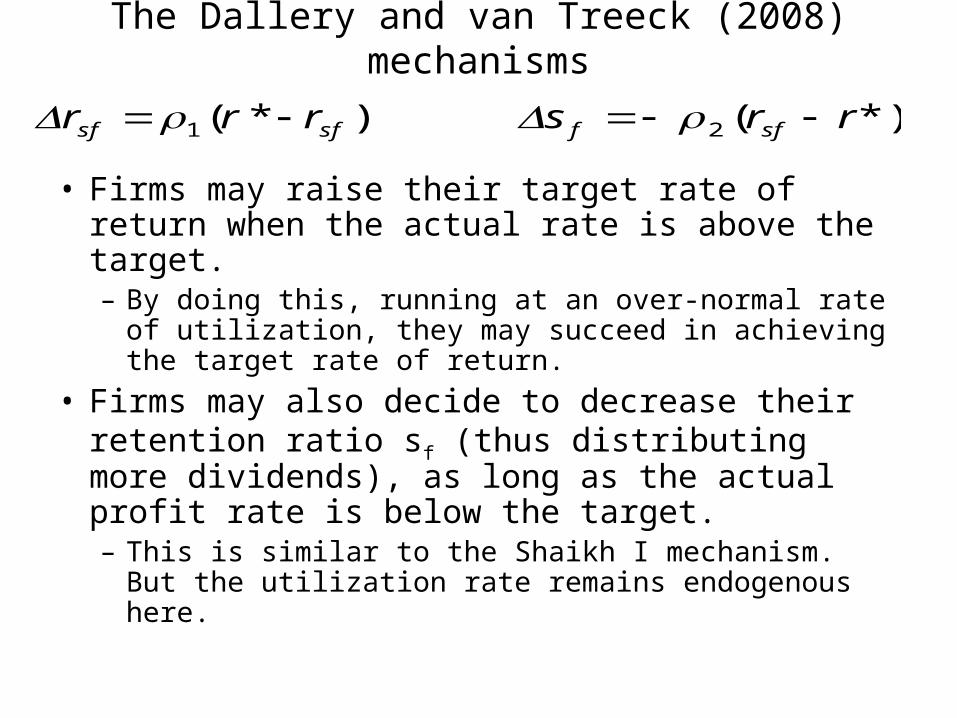

• This is the Dallery and van Treeck (2008) model, partly based on Lavoie (2003).

• Firms may set themselves “target” or “normal” rates of utilization.

• But they also may have other targets, such as target rates of return (rsf), imposed or suggested by shareholders.

• In addition, workers may have a target real wage, equivalent to some target rate of return (rw), which stops the firms from achieving their target rate of return.

• Thus, to follow Skott’s analogy, although I may always be late arriving at work (u > un) , I may be unable to leave any earlier to arrive on time (u = un), because of other commitments (rw, rsf).

The Dallery and van Treeck (2008) mechanisms

• Firms may raise their target rate of return when the actual rate is above the target.– By doing this, running at an over-normal rate of

utilization, they may succeed in achieving the target rate of return.

• Firms may also decide to decrease their retention ratio sf (thus distributing more dividends), as long as the actual profit rate is below the target. – This is similar to the Shaikh I mechanism. But the

utilization rate remains endogenous here.

)*(1 sfsf rrr *)(2 rrs sff

Conclusion

Anything goes ?

Feyerabend