SOLUTIONS TO ASSIGNMENT PROBLEMS - vidyardhi.comvidyardhi.com/gntmasterminds/2. Amalgamation -...

23

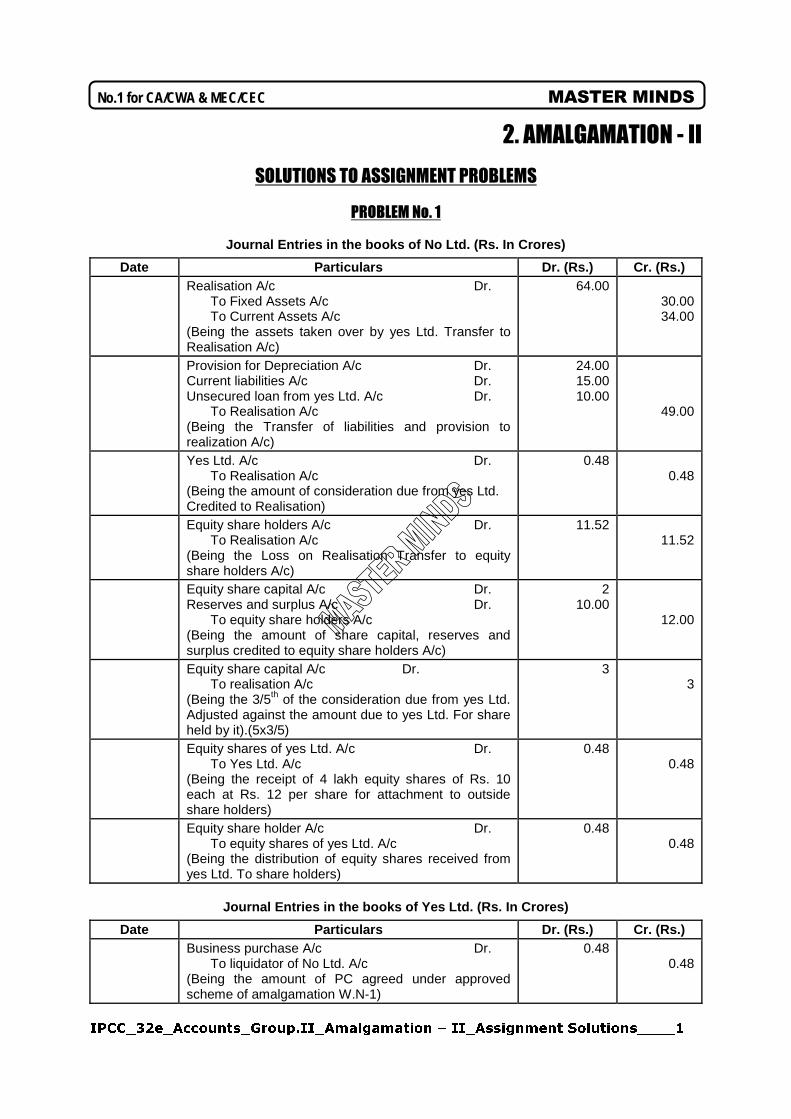

No.1 for CA/CWA & MEC/CEC MASTER MINDS 2. AMALGAMATION - II SOLUTIONS TO ASSIGNMENT PROBLEMS PROBLEM No. 1 Journal Entries in the books of No Ltd. (Rs. In Crores) Date Particulars Dr. (Rs.) Cr. (Rs.) Realisation A/c Dr. To Fixed Assets A/c To Current Assets A/c (Being the assets taken over by yes Ltd. Transfer to Realisation A/c) 64.00 30.00 34.00 Provision for Depreciation A/c Dr. Current liabilities A/c Dr. Unsecured loan from yes Ltd. A/c Dr. To Realisation A/c (Being the Transfer of liabilities and provision to realization A/c) 24.00 15.00 10.00 49.00 Yes Ltd. A/c Dr. To Realisation A/c (Being the amount of consideration due from yes Ltd. Credited to Realisation) 0.48 0.48 Equity share holders A/c Dr. To Realisation A/c (Being the Loss on Realisation Transfer to equity share holders A/c) 11.52 11.52 Equity share capital A/c Dr. Reserves and surplus A/c Dr. To equity share holders A/c (Being the amount of share capital, reserves and surplus credited to equity share holders A/c) 2 10.00 12.00 Equity share capital A/c Dr. To realisation A/c (Being the 3/5 th of the consideration due from yes Ltd. Adjusted against the amount due to yes Ltd. For share held by it).(5x3/5) 3 3 Equity shares of yes Ltd. A/c Dr. To Yes Ltd. A/c (Being the receipt of 4 lakh equity shares of Rs. 10 each at Rs. 12 per share for attachment to outside share holders) 0.48 0.48 Equity share holder A/c Dr. To equity shares of yes Ltd. A/c (Being the distribution of equity shares received from yes Ltd. To share holders) 0.48 0.48 Journal Entries in the books of Yes Ltd. (Rs. In Crores) Date Particulars Dr. (Rs.) Cr. (Rs.) Business purchase A/c Dr. To liquidator of No Ltd. A/c (Being the amount of PC agreed under approved scheme of amalgamation W.N-1) 0.48 0.48

Transcript of SOLUTIONS TO ASSIGNMENT PROBLEMS - vidyardhi.comvidyardhi.com/gntmasterminds/2. Amalgamation -...

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____1

No.1 for CA/CWA & MEC/CEC MASTER MINDS

2. AMALGAMATION - II

SOLUTIONS TO ASSIGNMENT PROBLEMS

PROBLEM No. 1

Journal Entries in the books of No Ltd. (Rs. In Crores)

Date Particulars Dr. (Rs.) Cr. (Rs.) Realisation A/c Dr.

To Fixed Assets A/c To Current Assets A/c

(Being the assets taken over by yes Ltd. Transfer to Realisation A/c)

64.00 30.00 34.00

Provision for Depreciation A/c Dr. Current liabilities A/c Dr. Unsecured loan from yes Ltd. A/c Dr.

To Realisation A/c (Being the Transfer of liabilities and provision to realization A/c)

24.00 15.00 10.00

49.00

Yes Ltd. A/c Dr. To Realisation A/c

(Being the amount of consideration due from yes Ltd. Credited to Realisation)

0.48 0.48

Equity share holders A/c Dr. To Realisation A/c

(Being the Loss on Realisation Transfer to equity share holders A/c)

11.52 11.52

Equity share capital A/c Dr. Reserves and surplus A/c Dr.

To equity share holders A/c (Being the amount of share capital, reserves and surplus credited to equity share holders A/c)

2 10.00

12.00

Equity share capital A/c Dr. To realisation A/c

(Being the 3/5th of the consideration due from yes Ltd. Adjusted against the amount due to yes Ltd. For share held by it).(5x3/5)

3 3

Equity shares of yes Ltd. A/c Dr. To Yes Ltd. A/c

(Being the receipt of 4 lakh equity shares of Rs. 10 each at Rs. 12 per share for attachment to outside share holders)

0.48 0.48

Equity share holder A/c Dr. To equity shares of yes Ltd. A/c

(Being the distribution of equity shares received from yes Ltd. To share holders)

0.48

0.48

Journal Entries in the books of Yes Ltd. (Rs. In Crores)

Date Particulars Dr. (Rs.) Cr. (Rs.) Business purchase A/c Dr.

To liquidator of No Ltd. A/c (Being the amount of PC agreed under approved scheme of amalgamation W.N-1)

0.48 0.48

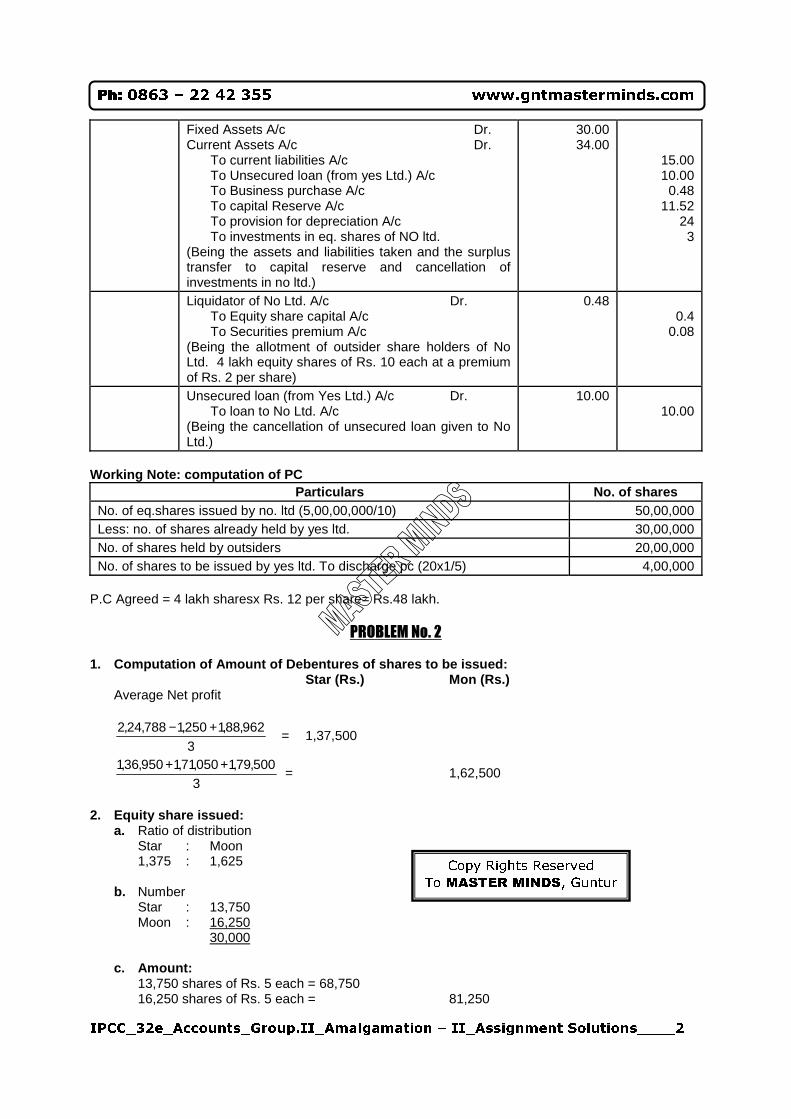

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____2

Ph: 0863 – 22 42 355 www.gntmasterminds.com

Fixed Assets A/c Dr. Current Assets A/c Dr.

To current liabilities A/c To Unsecured loan (from yes Ltd.) A/c To Business purchase A/c To capital Reserve A/c To provision for depreciation A/c To investments in eq. shares of NO ltd.

(Being the assets and liabilities taken and the surplus transfer to capital reserve and cancellation of investments in no ltd.)

30.00 34.00

15.00 10.00

0.48 11.52

24 3

Liquidator of No Ltd. A/c Dr. To Equity share capital A/c To Securities premium A/c

(Being the allotment of outsider share holders of No Ltd. 4 lakh equity shares of Rs. 10 each at a premium of Rs. 2 per share)

0.48 0.4

0.08

Unsecured loan (from Yes Ltd.) A/c Dr. To loan to No Ltd. A/c

(Being the cancellation of unsecured loan given to No Ltd.)

10.00 10.00

Working Note: computation of PC

Particulars No. of shares No. of eq.shares issued by no. ltd (5,00,00,000/10) 50,00,000 Less: no. of shares already held by yes ltd. 30,00,000 No. of shares held by outsiders 20,00,000 No. of shares to be issued by yes ltd. To discharge pc (20x1/5) 4,00,000

P.C Agreed = 4 lakh sharesx Rs. 12 per share= Rs.48 lakh.

PROBLEM No. 2 1. Computation of Amount of Debentures of shares to be issued:

Star (Rs.) Mon (Rs.) Average Net profit

3

962,88,1250,1788,24,2 +− = 1,37,500

3

500,79,1050,71,1950,36,1 ++ = 1,62,500

2. Equity share issued:

a. Ratio of distribution Star : Moon 1,375 : 1,625

b. Number

Star : 13,750 Moon : 16,250 30,000

c. Amount: 13,750 shares of Rs. 5 each = 68,750 16,250 shares of Rs. 5 each = 81,250

Copy Rights Reserved

To MASTER MINDS, Guntur

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____3

No.1 for CA/CWA & MEC/CEC MASTER MINDS

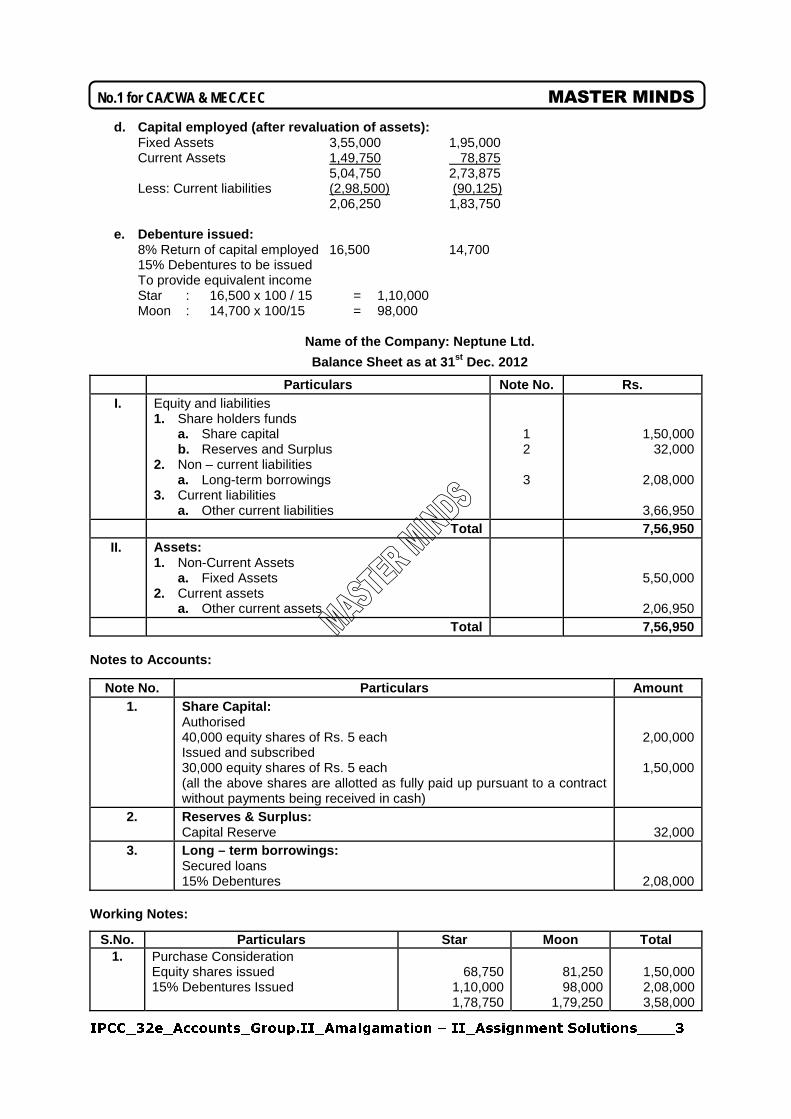

d. Capital employed (after revaluation of assets): Fixed Assets 3,55,000 1,95,000 Current Assets 1,49,750 78,875 5,04,750 2,73,875 Less: Current liabilities (2,98,500) (90,125) 2,06,250 1,83,750

e. Debenture issued: 8% Return of capital employed 16,500 14,700 15% Debentures to be issued To provide equivalent income Star : 16,500 x 100 / 15 = 1,10,000 Moon : 14,700 x 100/15 = 98,000

Name of the Company: Neptune Ltd.

Balance Sheet as at 31st Dec. 2012

Particulars Note No. Rs. I. Equity and liabilities

1. Share holders funds a. Share capital b. Reserves and Surplus

2. Non – current liabilities a. Long-term borrowings

3. Current liabilities a. Other current liabilities

1 2 3

1,50,000 32,000

2,08,000

3,66,950

Total 7,56,950 II. Assets:

1. Non-Current Assets a. Fixed Assets

2. Current assets a. Other current assets

5,50,000

2,06,950 Total 7,56,950

Notes to Accounts:

Note No. Particulars Amount 1. Share Capital:

Authorised 40,000 equity shares of Rs. 5 each Issued and subscribed 30,000 equity shares of Rs. 5 each (all the above shares are allotted as fully paid up pursuant to a contract without payments being received in cash)

2,00,000

1,50,000

2. Reserves & Surplus: Capital Reserve

32,000

3. Long – term borrowings: Secured loans 15% Debentures

2,08,000 Working Notes:

S.No. Particulars Star Moon Total 1. Purchase Consideration

Equity shares issued 15% Debentures Issued

68,750

1,10,000 1,78,750

81,250 98,000

1,79,250

1,50,000 2,08,000 3,58,000

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____4

Ph: 0863 – 22 42 355 www.gntmasterminds.com

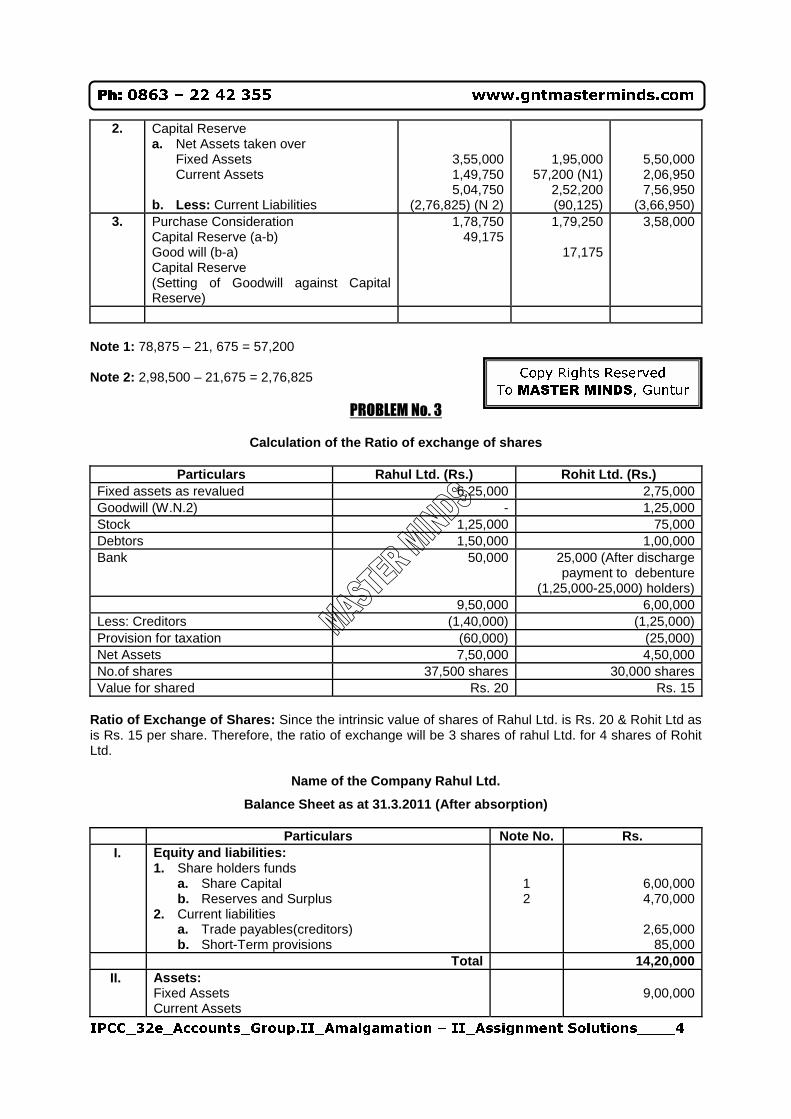

2. Capital Reserve a. Net Assets taken over

Fixed Assets Current Assets

b. Less: Current Liabilities

3,55,000 1,49,750 5,04,750

(2,76,825) (N 2)

1,95,000 57,200 (N1)

2,52,200 (90,125)

5,50,000 2,06,950 7,56,950

(3,66,950) 3. Purchase Consideration

Capital Reserve (a-b) Good will (b-a) Capital Reserve (Setting of Goodwill against Capital Reserve)

1,78,750 49,175

1,79,250

17,175

3,58,000

Note 1: 78,875 – 21, 675 = 57,200 Note 2: 2,98,500 – 21,675 = 2,76,825

PROBLEM No. 3

Calculation of the Ratio of exchange of shares

Particulars Rahul Ltd. (Rs.) Rohit Ltd. (Rs.) Fixed assets as revalued 6,25,000 2,75,000 Goodwill (W.N.2) - 1,25,000 Stock 1,25,000 75,000 Debtors 1,50,000 1,00,000 Bank 50,000 25,000 (After discharge

payment to debenture (1,25,000-25,000) holders)

9,50,000 6,00,000 Less: Creditors (1,40,000) (1,25,000) Provision for taxation (60,000) (25,000) Net Assets 7,50,000 4,50,000 No.of shares 37,500 shares 30,000 shares Value for shared Rs. 20 Rs. 15

Ratio of Exchange of Shares: Since the intrinsic value of shares of Rahul Ltd. is Rs. 20 & Rohit Ltd as is Rs. 15 per share. Therefore, the ratio of exchange will be 3 shares of rahul Ltd. for 4 shares of Rohit Ltd.

Name of the Company Rahul Ltd.

Balance Sheet as at 31.3.2011 (After absorption)

Particulars Note No. Rs. I. Equity and liabilities:

1. Share holders funds a. Share Capital b. Reserves and Surplus

2. Current liabilities a. Trade payables(creditors) b. Short-Term provisions

1 2

6,00,000 4,70,000

2,65,000

85,000 Total 14,20,000

II. Assets: Fixed Assets Current Assets

9,00,000

Copy Rights Reserved

To MASTER MINDS, Guntur

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____5

No.1 for CA/CWA & MEC/CEC MASTER MINDS

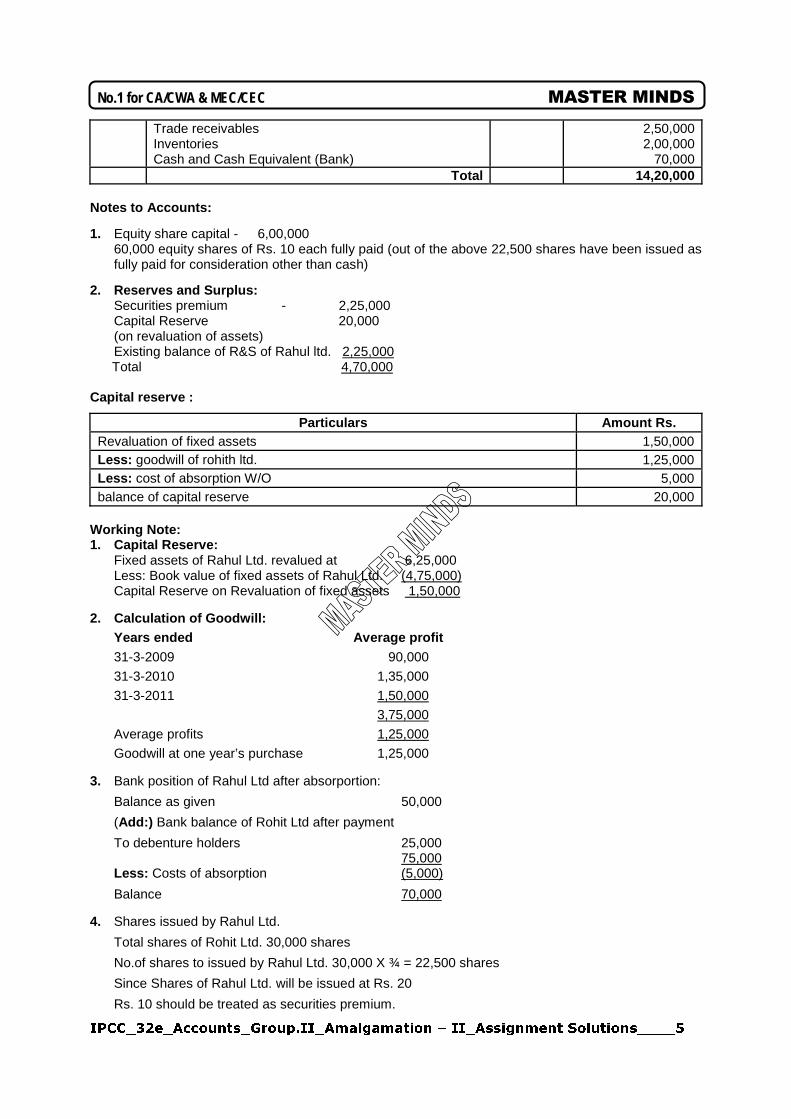

Trade receivables Inventories Cash and Cash Equivalent (Bank)

2,50,000 2,00,000

70,000 Total 14,20,000

Notes to Accounts:

1. Equity share capital - 6,00,000 60,000 equity shares of Rs. 10 each fully paid (out of the above 22,500 shares have been issued as fully paid for consideration other than cash)

2. Reserves and Surplus: Securities premium - 2,25,000 Capital Reserve 20,000 (on revaluation of assets) Existing balance of R&S of Rahul ltd. 2,25,000

Total 4,70,000 Capital reserve :

Particulars Amount Rs. Revaluation of fixed assets 1,50,000 Less: goodwill of rohith ltd. 1,25,000 Less: cost of absorption W/O 5,000 balance of capital reserve 20,000

Working Note: 1. Capital Reserve:

Fixed assets of Rahul Ltd. revalued at 6,25,000 Less: Book value of fixed assets of Rahul Ltd. (4,75,000) Capital Reserve on Revaluation of fixed assets 1,50,000

2. Calculation of Goodwill:

Years ended Average profit 31-3-2009 90,000

31-3-2010 1,35,000

31-3-2011 1,50,000

3,75,000

Average profits 1,25,000

Goodwill at one year’s purchase 1,25,000 3. Bank position of Rahul Ltd after absorportion:

Balance as given 50,000

(Add:) Bank balance of Rohit Ltd after payment

To debenture holders 25,000 75,000 Less: Costs of absorption (5,000)

Balance 70,000 4. Shares issued by Rahul Ltd.

Total shares of Rohit Ltd. 30,000 shares

No.of shares to issued by Rahul Ltd. 30,000 X ¾ = 22,500 shares

Since Shares of Rahul Ltd. will be issued at Rs. 20

Rs. 10 should be treated as securities premium.

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____6

Ph: 0863 – 22 42 355 www.gntmasterminds.com

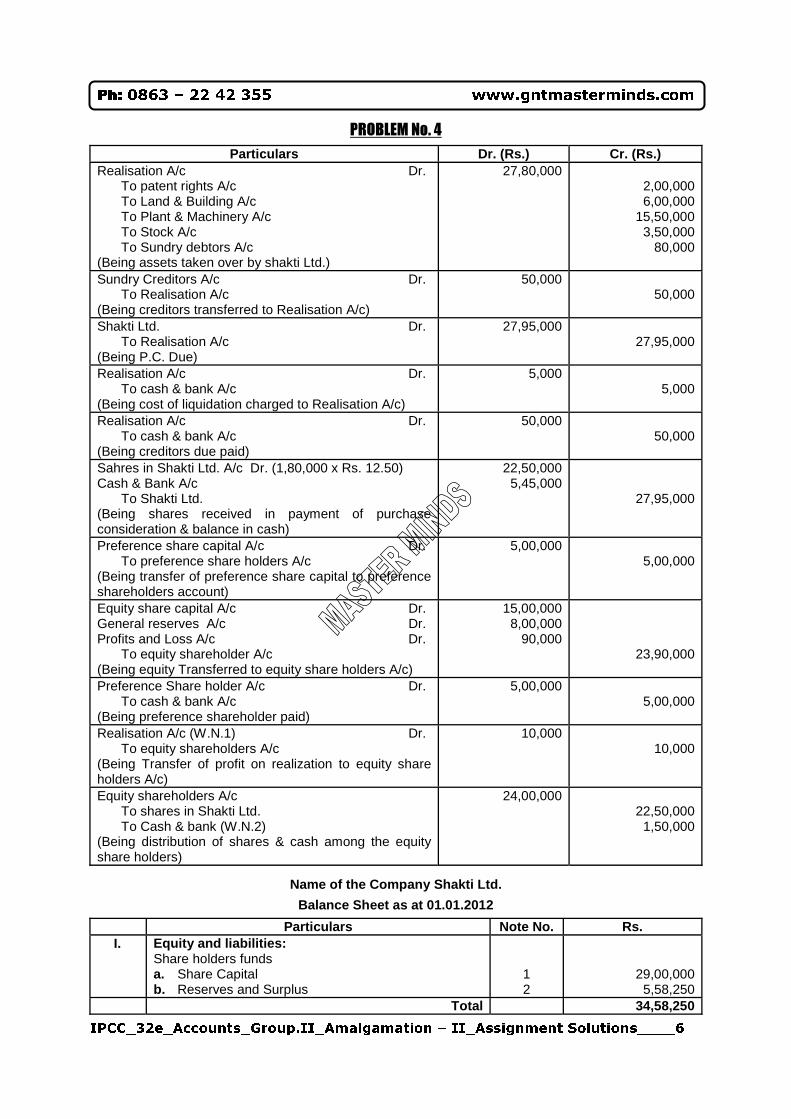

PROBLEM No. 4

Particulars Dr. (Rs.) Cr. (Rs.) Realisation A/c Dr.

To patent rights A/c To Land & Building A/c To Plant & Machinery A/c To Stock A/c To Sundry debtors A/c

(Being assets taken over by shakti Ltd.)

27,80,000 2,00,000 6,00,000

15,50,000 3,50,000

80,000

Sundry Creditors A/c Dr. To Realisation A/c

(Being creditors transferred to Realisation A/c)

50,000 50,000

Shakti Ltd. Dr. To Realisation A/c

(Being P.C. Due)

27,95,000 27,95,000

Realisation A/c Dr. To cash & bank A/c

(Being cost of liquidation charged to Realisation A/c)

5,000 5,000

Realisation A/c Dr. To cash & bank A/c

(Being creditors due paid)

50,000 50,000

Sahres in Shakti Ltd. A/c Dr. (1,80,000 x Rs. 12.50) Cash & Bank A/c

To Shakti Ltd. (Being shares received in payment of purchase consideration & balance in cash)

22,50,000 5,45,000

27,95,000

Preference share capital A/c Dr. To preference share holders A/c

(Being transfer of preference share capital to preference shareholders account)

5,00,000 5,00,000

Equity share capital A/c Dr. General reserves A/c Dr. Profits and Loss A/c Dr.

To equity shareholder A/c (Being equity Transferred to equity share holders A/c)

15,00,000 8,00,000

90,000

23,90,000

Preference Share holder A/c Dr. To cash & bank A/c

(Being preference shareholder paid)

5,00,000 5,00,000

Realisation A/c (W.N.1) Dr. To equity shareholders A/c

(Being Transfer of profit on realization to equity share holders A/c)

10,000 10,000

Equity shareholders A/c To shares in Shakti Ltd. To Cash & bank (W.N.2)

(Being distribution of shares & cash among the equity share holders)

24,00,000 22,50,000

1,50,000

Name of the Company Shakti Ltd.

Balance Sheet as at 01.01.2012

Particulars Note No. Rs. I. Equity and liabilities:

Share holders funds a. Share Capital b. Reserves and Surplus

1 2

29,00,000 5,58,250

Total 34,58,250

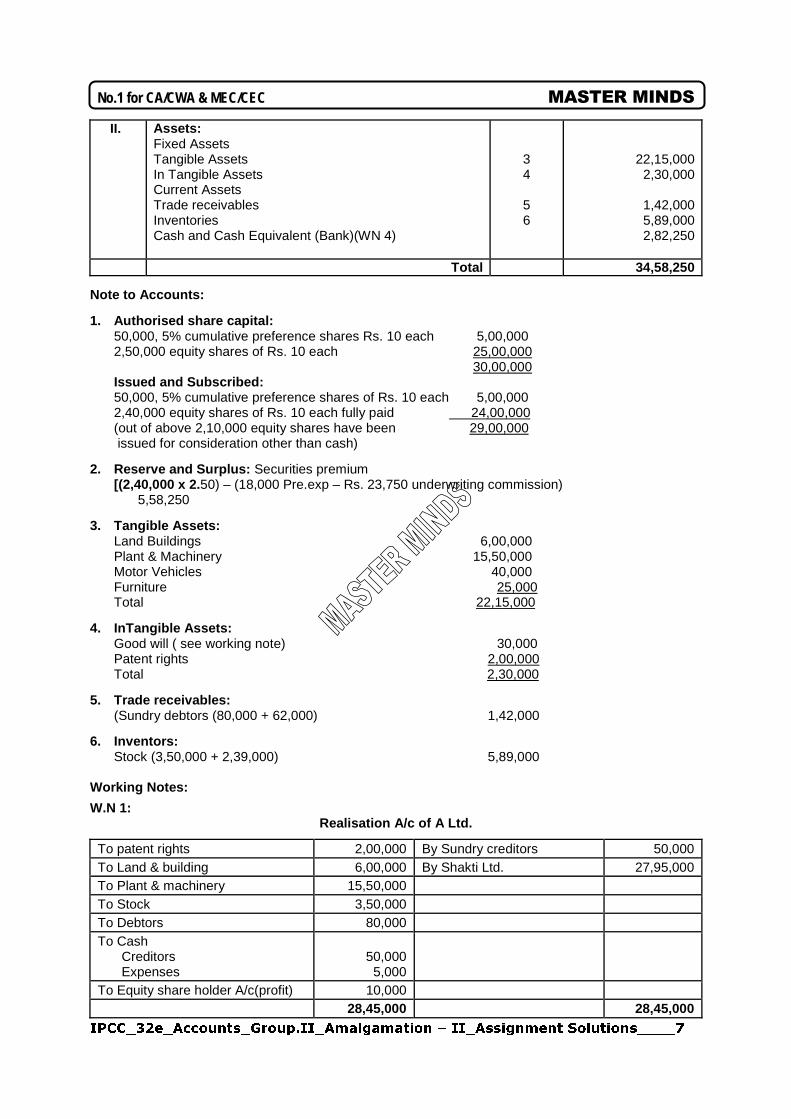

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____7

No.1 for CA/CWA & MEC/CEC MASTER MINDS

II. Assets: Fixed Assets Tangible Assets In Tangible Assets Current Assets Trade receivables Inventories Cash and Cash Equivalent (Bank)(WN 4)

3 4 5 6

22,15,000 2,30,000

1,42,000 5,89,000 2,82,250

Total 34,58,250

Note to Accounts:

1. Authorised share capital: 50,000, 5% cumulative preference shares Rs. 10 each 5,00,000 2,50,000 equity shares of Rs. 10 each 25,00,000 30,00,000 Issued and Subscribed: 50,000, 5% cumulative preference shares of Rs. 10 each 5,00,000 2,40,000 equity shares of Rs. 10 each fully paid 24,00,000 (out of above 2,10,000 equity shares have been 29,00,000 issued for consideration other than cash)

2. Reserve and Surplus: Securities premium [(2,40,000 x 2.50) – (18,000 Pre.exp – Rs. 23,750 underwriting commission) 5,58,250

3. Tangible Assets: Land Buildings 6,00,000 Plant & Machinery 15,50,000 Motor Vehicles 40,000 Furniture 25,000 Total 22,15,000

4. InTangible Assets: Good will ( see working note) 30,000 Patent rights 2,00,000 Total 2,30,000

5. Trade receivables: (Sundry debtors (80,000 + 62,000) 1,42,000

6. Inventors: Stock (3,50,000 + 2,39,000) 5,89,000

Working Notes:

W.N 1: Realisation A/c of A Ltd.

To patent rights 2,00,000 By Sundry creditors 50,000 To Land & building 6,00,000 By Shakti Ltd. 27,95,000 To Plant & machinery 15,50,000 To Stock 3,50,000 To Debtors 80,000 To Cash

Creditors Expenses

50,000 5,000

To Equity share holder A/c(profit) 10,000 28,45,000 28,45,000

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____8

Ph: 0863 – 22 42 355 www.gntmasterminds.com

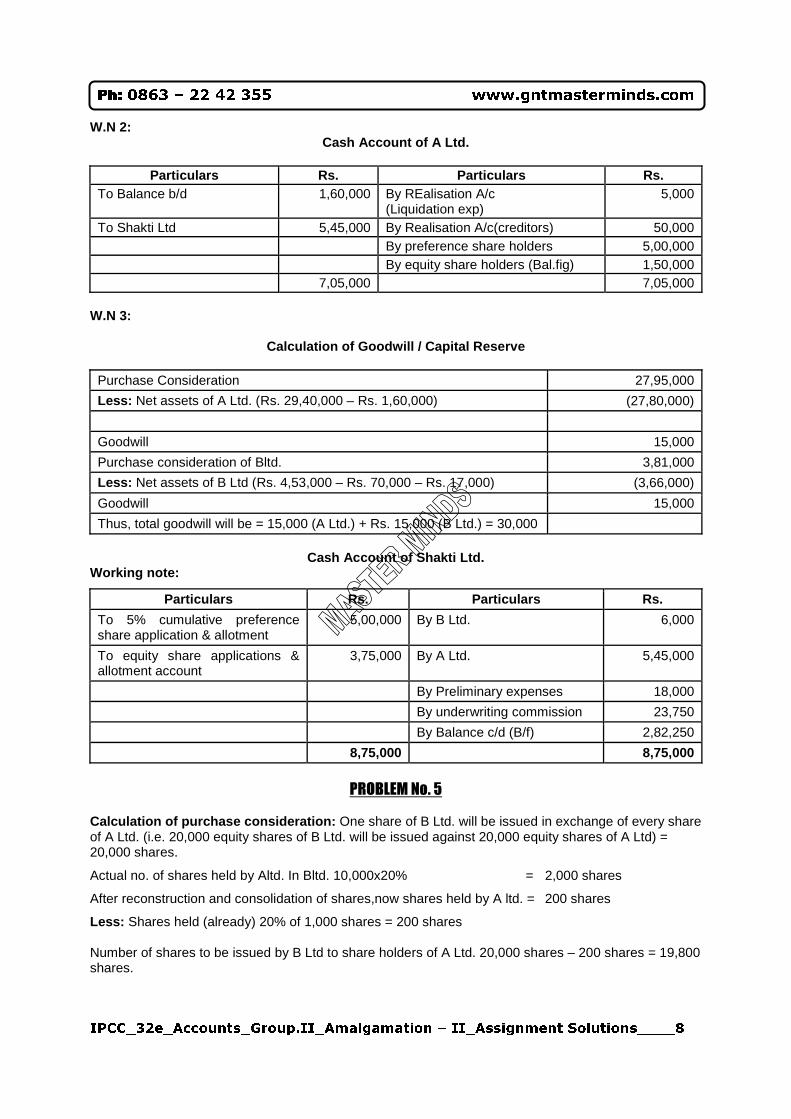

W.N 2: Cash Account of A Ltd.

Particulars Rs. Particulars Rs.

To Balance b/d 1,60,000 By REalisation A/c (Liquidation exp)

5,000

To Shakti Ltd 5,45,000 By Realisation A/c(creditors) 50,000 By preference share holders 5,00,000 By equity share holders (Bal.fig) 1,50,000 7,05,000 7,05,000

W.N 3:

Calculation of Goodwill / Capital Reserve

Purchase Consideration 27,95,000

Less: Net assets of A Ltd. (Rs. 29,40,000 – Rs. 1,60,000) (27,80,000)

Goodwill 15,000

Purchase consideration of Bltd. 3,81,000

Less: Net assets of B Ltd (Rs. 4,53,000 – Rs. 70,000 – Rs. 17,000) (3,66,000)

Goodwill 15,000

Thus, total goodwill will be = 15,000 (A Ltd.) + Rs. 15,000 (B Ltd.) = 30,000

Cash Account of Shakti Ltd. Working note:

Particulars Rs. Particulars Rs.

To 5% cumulative preference share application & allotment

5,00,000 By B Ltd. 6,000

To equity share applications & allotment account

3,75,000 By A Ltd. 5,45,000

By Preliminary expenses 18,000

By underwriting commission 23,750

By Balance c/d (B/f) 2,82,250

8,75,000 8,75,000

PROBLEM No. 5 Calculation of purchase consideration: One share of B Ltd. will be issued in exchange of every share of A Ltd. (i.e. 20,000 equity shares of B Ltd. will be issued against 20,000 equity shares of A Ltd) = 20,000 shares.

Actual no. of shares held by Altd. In Bltd. 10,000x20% = 2,000 shares

After reconstruction and consolidation of shares,now shares held by A ltd. = 200 shares

Less: Shares held (already) 20% of 1,000 shares = 200 shares Number of shares to be issued by B Ltd to share holders of A Ltd. 20,000 shares – 200 shares = 19,800 shares.

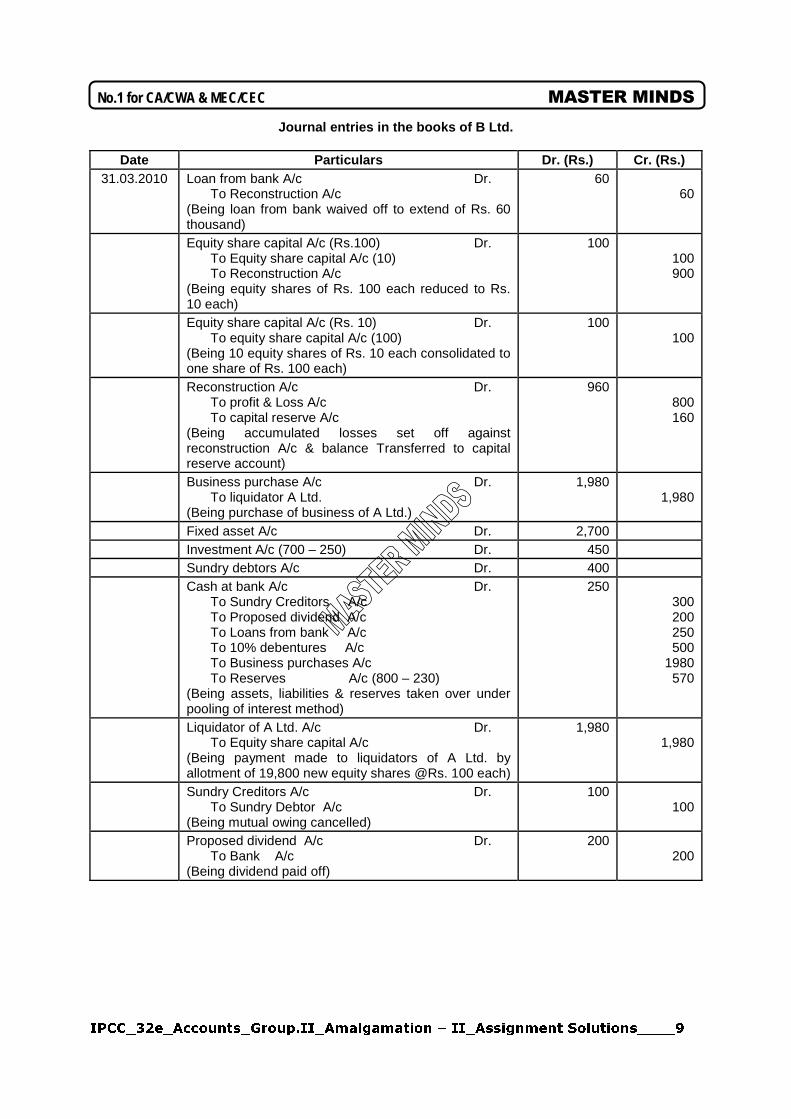

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____9

No.1 for CA/CWA & MEC/CEC MASTER MINDS

Journal entries in the books of B Ltd.

Date Particulars Dr. (Rs.) Cr. (Rs.) 31.03.2010 Loan from bank A/c Dr.

To Reconstruction A/c (Being loan from bank waived off to extend of Rs. 60 thousand)

60 60

Equity share capital A/c (Rs.100) Dr. To Equity share capital A/c (10) To Reconstruction A/c

(Being equity shares of Rs. 100 each reduced to Rs. 10 each)

100 100 900

Equity share capital A/c (Rs. 10) Dr. To equity share capital A/c (100)

(Being 10 equity shares of Rs. 10 each consolidated to one share of Rs. 100 each)

100 100

Reconstruction A/c Dr. To profit & Loss A/c To capital reserve A/c

(Being accumulated losses set off against reconstruction A/c & balance Transferred to capital reserve account)

960 800 160

Business purchase A/c Dr. To liquidator A Ltd.

(Being purchase of business of A Ltd.)

1,980 1,980

Fixed asset A/c Dr. 2,700 Investment A/c (700 – 250) Dr. 450 Sundry debtors A/c Dr. 400 Cash at bank A/c Dr.

To Sundry Creditors A/c To Proposed dividend A/c To Loans from bank A/c To 10% debentures A/c To Business purchases A/c To Reserves A/c (800 – 230)

(Being assets, liabilities & reserves taken over under pooling of interest method)

250 300 200 250 500

1980 570

Liquidator of A Ltd. A/c Dr. To Equity share capital A/c

(Being payment made to liquidators of A Ltd. by allotment of 19,800 new equity shares @Rs. 100 each)

1,980 1,980

Sundry Creditors A/c Dr. To Sundry Debtor A/c

(Being mutual owing cancelled)

100 100

Proposed dividend A/c Dr. To Bank A/c

(Being dividend paid off)

200 200

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____10

Ph: 0863 – 22 42 355 www.gntmasterminds.com

Name of company: B Ltd.

Balance sheet date: 31.3.2010 (after merger)

Particulars Note No. Amount

Equity & liabilities: Share holder funds Share capital Reserves & Surplus

1 2

2,080 730

Non current liabilities: Long term borrowings Other long term borrowings

3 4

500 640

Current liabilities: Trade payables Other current liabilities

5 6

500 50

4,500

Assets: Fixed assets Non current Investments

7

3,550

450

Current Assets: Trade receivables Cash & Cash equivalent

8 9

450 50

4,500 Notes to Accounts:

No. Particulars Rs.

1. Share capital: 20,800 equity share of Rs. 100 each fully paid (Out of the above 19,800 shares hence been issued for consideration other than cash)

2,080

2. Reserves & Surplus: Capital Reserves General Reserves

160 570

3. Long term borrowings: 10% Debentures

500

4. Other long term borrowings: Loan from bank (250 + 450 – 60)

640

5. Trade payables: Sundry creditors (300 + 300 – 100)

500

6. Other Current liabilities: Bank overdraft

50

7. Fixed assets: (2,700 + 850)

3,550

8. Trade receivables: Sundry debtors (400 + 150 – 100)

450

9. Cash & Cash equivalent: Cash at bank (250 – 200)

50

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____11

No.1 for CA/CWA & MEC/CEC MASTER MINDS

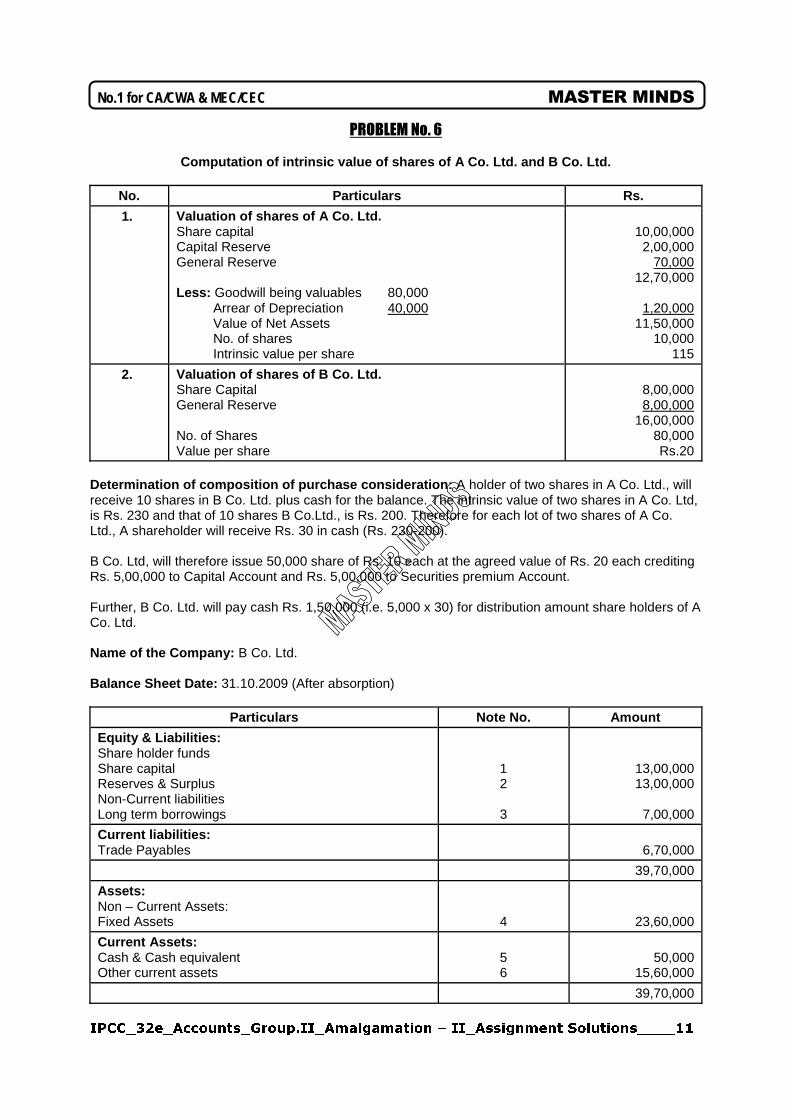

PROBLEM No. 6

Computation of intrinsic value of shares of A Co. Ltd. and B Co. Ltd.

No. Particulars Rs.

1. Valuation of shares of A Co. Ltd. Share capital Capital Reserve General Reserve Less: Goodwill being valuables 80,000 Arrear of Depreciation 40,000 Value of Net Assets No. of shares Intrinsic value per share

10,00,000

2,00,000 70,000

12,70,000

1,20,000 11,50,000

10,000 115

2. Valuation of shares of B Co. Ltd. Share Capital General Reserve No. of Shares Value per share

8,00,000 8,00,000

16,00,000 80,000 Rs.20

Determination of composition of purchase consideration: A holder of two shares in A Co. Ltd., will receive 10 shares in B Co. Ltd. plus cash for the balance. The intrinsic value of two shares in A Co. Ltd, is Rs. 230 and that of 10 shares B Co.Ltd., is Rs. 200. Therefore for each lot of two shares of A Co. Ltd., A shareholder will receive Rs. 30 in cash (Rs. 230-200). B Co. Ltd, will therefore issue 50,000 share of Rs. 10 each at the agreed value of Rs. 20 each crediting Rs. 5,00,000 to Capital Account and Rs. 5,00,000 to Securities premium Account. Further, B Co. Ltd. will pay cash Rs. 1,50,000 (i.e. 5,000 x 30) for distribution amount share holders of A Co. Ltd. Name of the Company: B Co. Ltd. Balance Sheet Date: 31.10.2009 (After absorption)

Particulars Note No. Amount

Equity & Liabilities: Share holder funds Share capital Reserves & Surplus Non-Current liabilities Long term borrowings

1 2 3

13,00,000 13,00,000

7,00,000

Current liabilities: Trade Payables

6,70,000

39,70,000

Assets: Non – Current Assets: Fixed Assets

4

23,60,000

Current Assets: Cash & Cash equivalent Other current assets

5 6

50,000

15,60,000

39,70,000

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____12

Ph: 0863 – 22 42 355 www.gntmasterminds.com

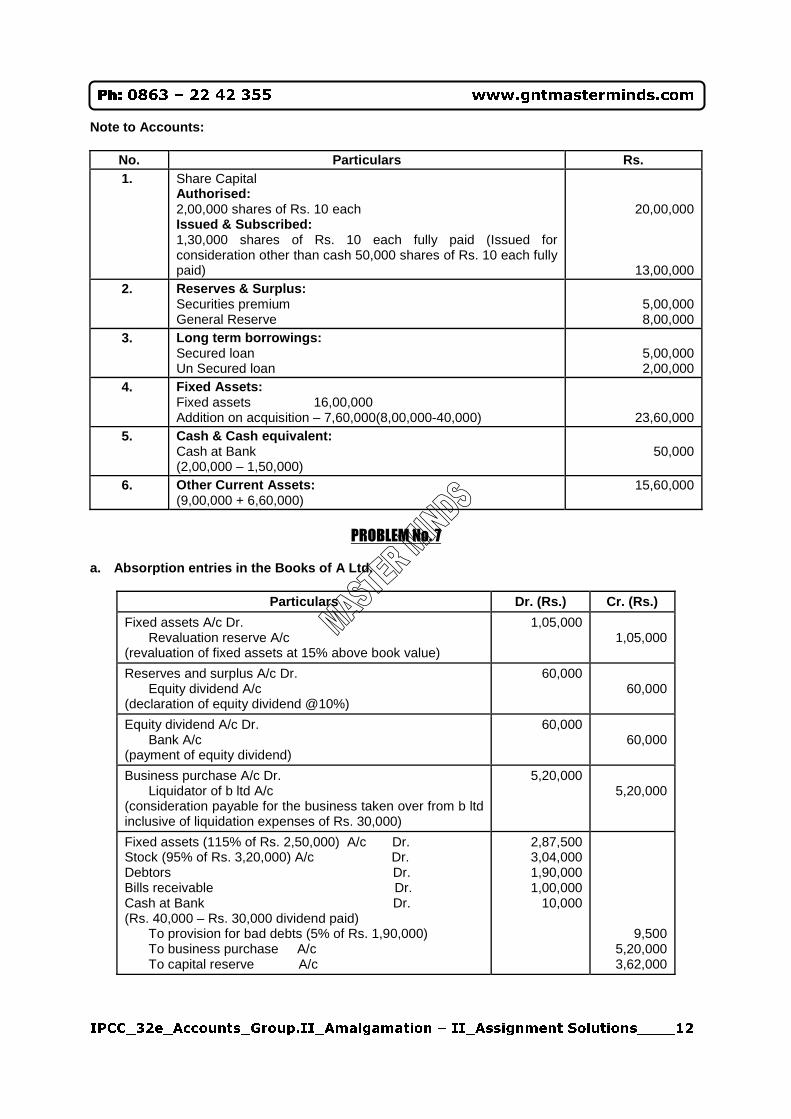

Note to Accounts:

No. Particulars Rs. 1. Share Capital

Authorised: 2,00,000 shares of Rs. 10 each Issued & Subscribed: 1,30,000 shares of Rs. 10 each fully paid (Issued for consideration other than cash 50,000 shares of Rs. 10 each fully paid)

20,00,000

13,00,000 2. Reserves & Surplus:

Securities premium General Reserve

5,00,000 8,00,000

3. Long term borrowings: Secured loan Un Secured loan

5,00,000 2,00,000

4. Fixed Assets: Fixed assets 16,00,000 Addition on acquisition – 7,60,000(8,00,000-40,000)

23,60,000 5. Cash & Cash equivalent:

Cash at Bank (2,00,000 – 1,50,000)

50,000

6. Other Current Assets: (9,00,000 + 6,60,000)

15,60,000

PROBLEM No. 7

a. Absorption entries in the Books of A Ltd.

Particulars Dr. (Rs.) Cr. (Rs.)

Fixed assets A/c Dr. Revaluation reserve A/c

(revaluation of fixed assets at 15% above book value)

1,05,000 1,05,000

Reserves and surplus A/c Dr. Equity dividend A/c

(declaration of equity dividend @10%)

60,000 60,000

Equity dividend A/c Dr. Bank A/c

(payment of equity dividend)

60,000 60,000

Business purchase A/c Dr. Liquidator of b ltd A/c

(consideration payable for the business taken over from b ltd inclusive of liquidation expenses of Rs. 30,000)

5,20,000 5,20,000

Fixed assets (115% of Rs. 2,50,000) A/c Dr. Stock (95% of Rs. 3,20,000) A/c Dr. Debtors Dr. Bills receivable Dr. Cash at Bank Dr. (Rs. 40,000 – Rs. 30,000 dividend paid)

To provision for bad debts (5% of Rs. 1,90,000) To business purchase A/c To capital reserve A/c

2,87,500 3,04,000 1,90,000 1,00,000

10,000

9,500 5,20,000 3,62,000

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____13

No.1 for CA/CWA & MEC/CEC MASTER MINDS

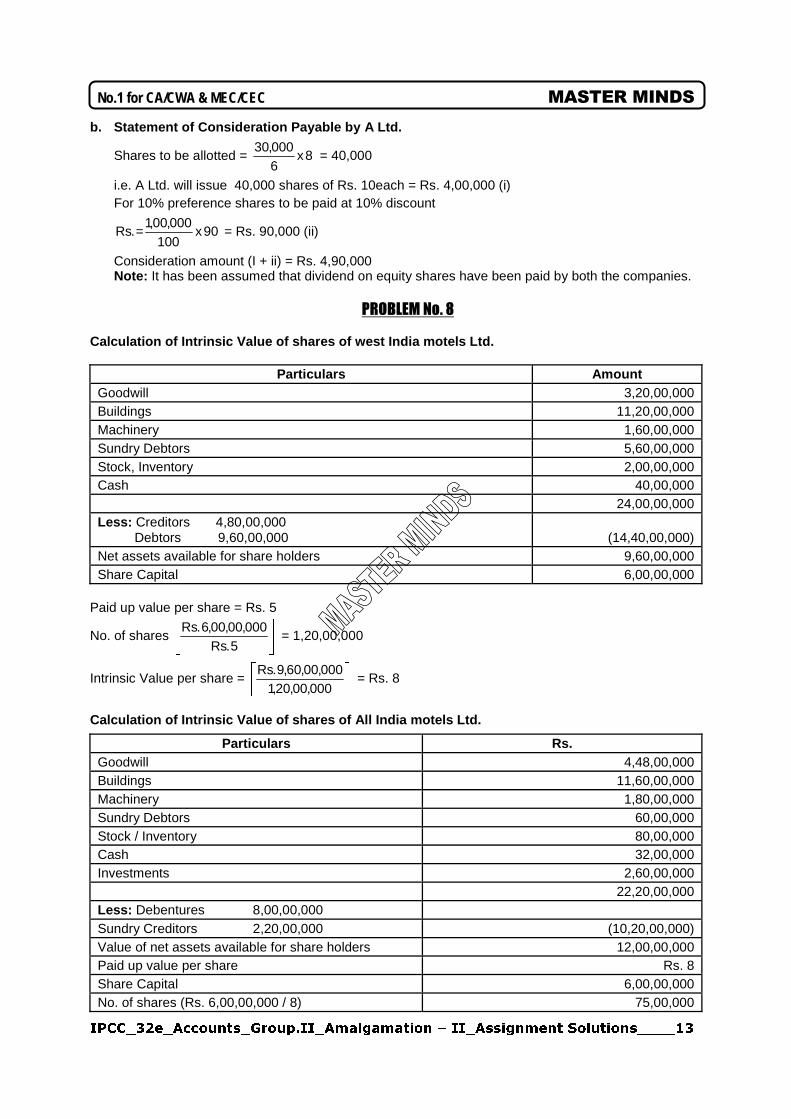

b. Statement of Consideration Payable by A Ltd.

Shares to be allotted = 8x6000,30

= 40,000

i.e. A Ltd. will issue 40,000 shares of Rs. 10each = Rs. 4,00,000 (i) For 10% preference shares to be paid at 10% discount

90x100

000,00,1.Rs = = Rs. 90,000 (ii)

Consideration amount (I + ii) = Rs. 4,90,000 Note: It has been assumed that dividend on equity shares have been paid by both the companies.

PROBLEM No. 8

Calculation of Intrinsic Value of shares of west India motels Ltd.

Particulars Amount Goodwill 3,20,00,000 Buildings 11,20,00,000 Machinery 1,60,00,000 Sundry Debtors 5,60,00,000 Stock, Inventory 2,00,00,000 Cash 40,00,000 24,00,00,000 Less: Creditors 4,80,00,000 Debtors 9,60,00,000

(14,40,00,000)

Net assets available for share holders 9,60,00,000 Share Capital 6,00,00,000

Paid up value per share = Rs. 5

No. of shares

5.Rs000,00,00,6.Rs

= 1,20,00,000

Intrinsic Value per share =

000,00,20,1000,00,60,9.Rs

= Rs. 8

Calculation of Intrinsic Value of shares of All India motels Ltd.

Particulars Rs. Goodwill 4,48,00,000 Buildings 11,60,00,000 Machinery 1,80,00,000 Sundry Debtors 60,00,000 Stock / Inventory 80,00,000 Cash 32,00,000 Investments 2,60,00,000 22,20,00,000 Less: Debentures 8,00,00,000 Sundry Creditors 2,20,00,000 (10,20,00,000) Value of net assets available for share holders 12,00,00,000 Paid up value per share Rs. 8 Share Capital 6,00,00,000 No. of shares (Rs. 6,00,00,000 / 8) 75,00,000

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____14

Ph: 0863 – 22 42 355 www.gntmasterminds.com

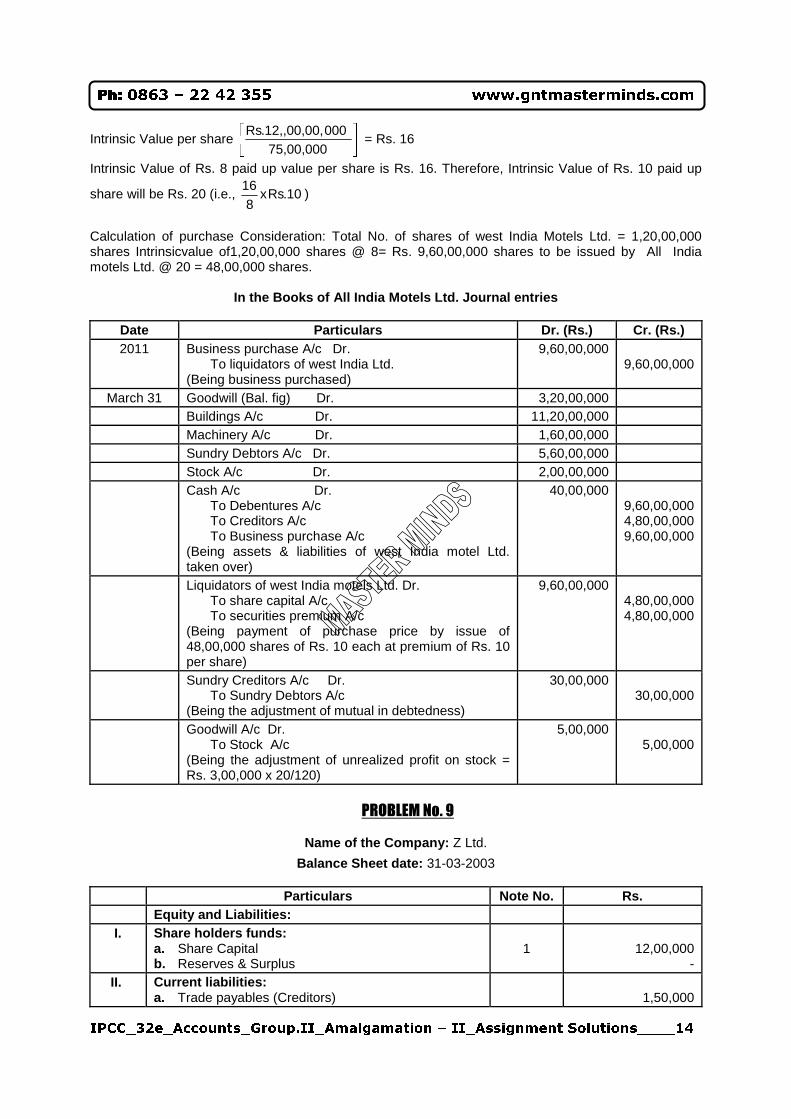

Intrinsic Value per share

75,00,000 00012,,00,00,.Rs

= Rs. 16

Intrinsic Value of Rs. 8 paid up value per share is Rs. 16. Therefore, Intrinsic Value of Rs. 10 paid up

share will be Rs. 20 (i.e., 10.Rsx8

16)

Calculation of purchase Consideration: Total No. of shares of west India Motels Ltd. = 1,20,00,000 shares Intrinsicvalue of1,20,00,000 shares @ 8= Rs. 9,60,00,000 shares to be issued by All India motels Ltd. @ 20 = 48,00,000 shares.

In the Books of All India Motels Ltd. Journal entries

Date Particulars Dr. (Rs.) Cr. (Rs.) 2011 Business purchase A/c Dr.

To liquidators of west India Ltd. (Being business purchased)

9,60,00,000 9,60,00,000

March 31 Goodwill (Bal. fig) Dr. 3,20,00,000 Buildings A/c Dr. 11,20,00,000 Machinery A/c Dr. 1,60,00,000 Sundry Debtors A/c Dr. 5,60,00,000 Stock A/c Dr. 2,00,00,000 Cash A/c Dr.

To Debentures A/c To Creditors A/c To Business purchase A/c

(Being assets & liabilities of west India motel Ltd. taken over)

40,00,000

9,60,00,000 4,80,00,000 9,60,00,000

Liquidators of west India motels Ltd. Dr. To share capital A/c To securities premium A/c

(Being payment of purchase price by issue of 48,00,000 shares of Rs. 10 each at premium of Rs. 10 per share)

9,60,00,000 4,80,00,000 4,80,00,000

Sundry Creditors A/c Dr. To Sundry Debtors A/c

(Being the adjustment of mutual in debtedness)

30,00,000 30,00,000

Goodwill A/c Dr. To Stock A/c

(Being the adjustment of unrealized profit on stock = Rs. 3,00,000 x 20/120)

5,00,000 5,00,000

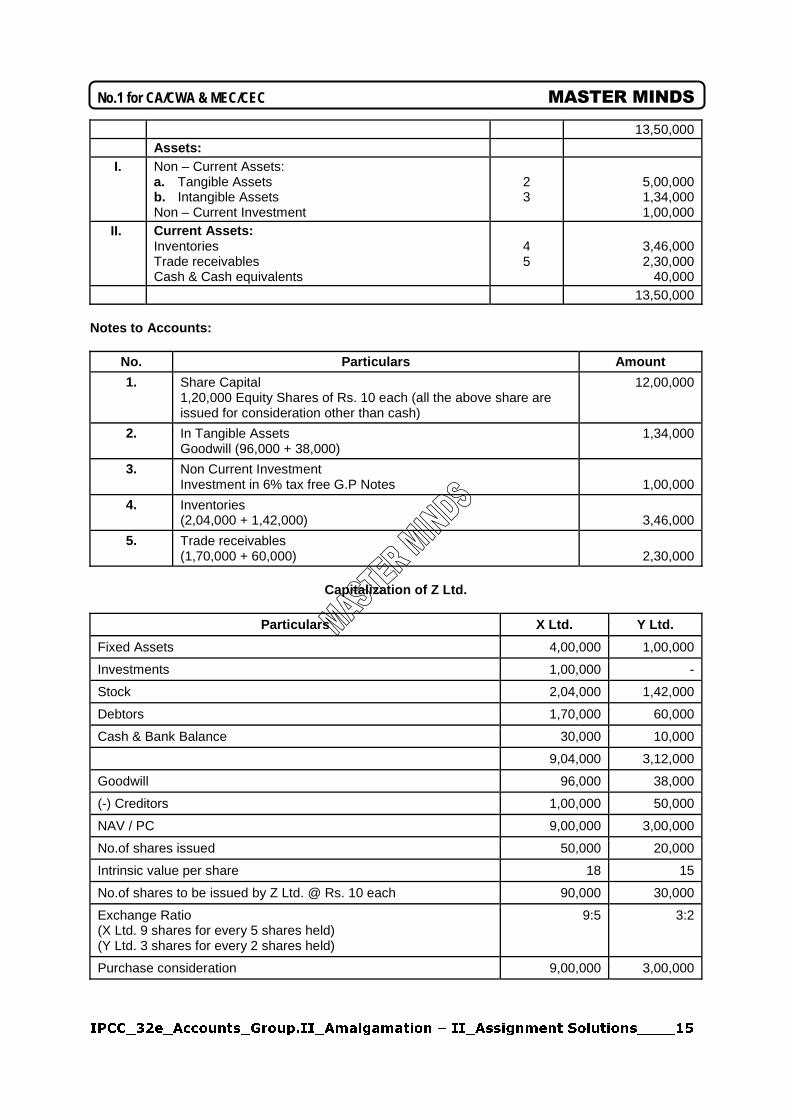

PROBLEM No. 9

Name of the Company: Z Ltd.

Balance Sheet date: 31-03-2003

Particulars Note No. Rs. Equity and Liabilities:

I. Share holders funds: a. Share Capital b. Reserves & Surplus

1

12,00,000

- II. Current liabilities:

a. Trade payables (Creditors)

1,50,000

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____15

No.1 for CA/CWA & MEC/CEC MASTER MINDS

13,50,000 Assets:

I. Non – Current Assets: a. Tangible Assets b. Intangible Assets Non – Current Investment

2 3

5,00,000 1,34,000 1,00,000

II. Current Assets: Inventories Trade receivables Cash & Cash equivalents

4 5

3,46,000 2,30,000

40,000 13,50,000

Notes to Accounts:

No. Particulars Amount

1. Share Capital 1,20,000 Equity Shares of Rs. 10 each (all the above share are issued for consideration other than cash)

12,00,000

2. In Tangible Assets Goodwill (96,000 + 38,000)

1,34,000

3. Non Current Investment Investment in 6% tax free G.P Notes

1,00,000

4. Inventories (2,04,000 + 1,42,000)

3,46,000

5. Trade receivables (1,70,000 + 60,000)

2,30,000

Capitalization of Z Ltd.

Particulars X Ltd. Y Ltd.

Fixed Assets 4,00,000 1,00,000

Investments 1,00,000 -

Stock 2,04,000 1,42,000

Debtors 1,70,000 60,000

Cash & Bank Balance 30,000 10,000

9,04,000 3,12,000

Goodwill 96,000 38,000

(-) Creditors 1,00,000 50,000

NAV / PC 9,00,000 3,00,000

No.of shares issued 50,000 20,000

Intrinsic value per share 18 15

No.of shares to be issued by Z Ltd. @ Rs. 10 each 90,000 30,000

Exchange Ratio (X Ltd. 9 shares for every 5 shares held) (Y Ltd. 3 shares for every 2 shares held)

9:5 3:2

Purchase consideration 9,00,000 3,00,000

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____16

Ph: 0863 – 22 42 355 www.gntmasterminds.com

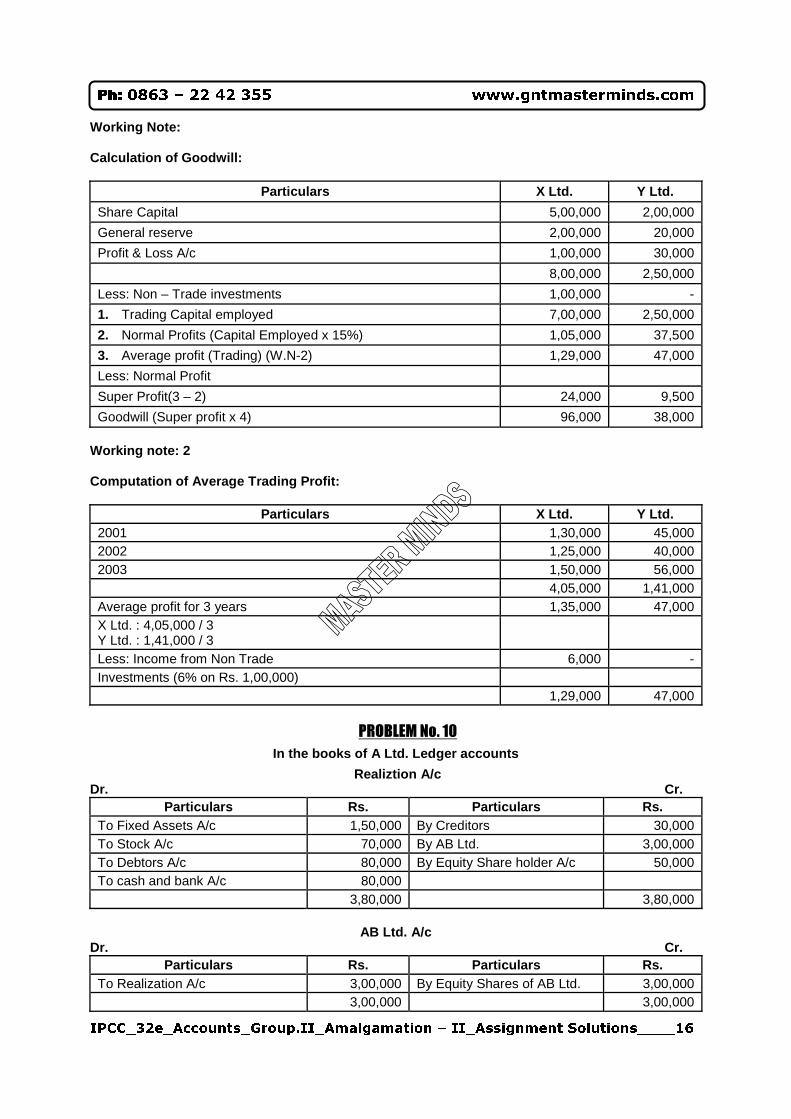

Working Note: Calculation of Goodwill:

Particulars X Ltd. Y Ltd.

Share Capital 5,00,000 2,00,000

General reserve 2,00,000 20,000

Profit & Loss A/c 1,00,000 30,000

8,00,000 2,50,000

Less: Non – Trade investments 1,00,000 -

1. Trading Capital employed 7,00,000 2,50,000

2. Normal Profits (Capital Employed x 15%) 1,05,000 37,500

3. Average profit (Trading) (W.N-2) 1,29,000 47,000

Less: Normal Profit

Super Profit(3 – 2) 24,000 9,500

Goodwill (Super profit x 4) 96,000 38,000 Working note: 2 Computation of Average Trading Profit:

Particulars X Ltd. Y Ltd. 2001 1,30,000 45,000 2002 1,25,000 40,000 2003 1,50,000 56,000 4,05,000 1,41,000 Average profit for 3 years 1,35,000 47,000 X Ltd. : 4,05,000 / 3 Y Ltd. : 1,41,000 / 3

Less: Income from Non Trade 6,000 - Investments (6% on Rs. 1,00,000) 1,29,000 47,000

PROBLEM No. 10

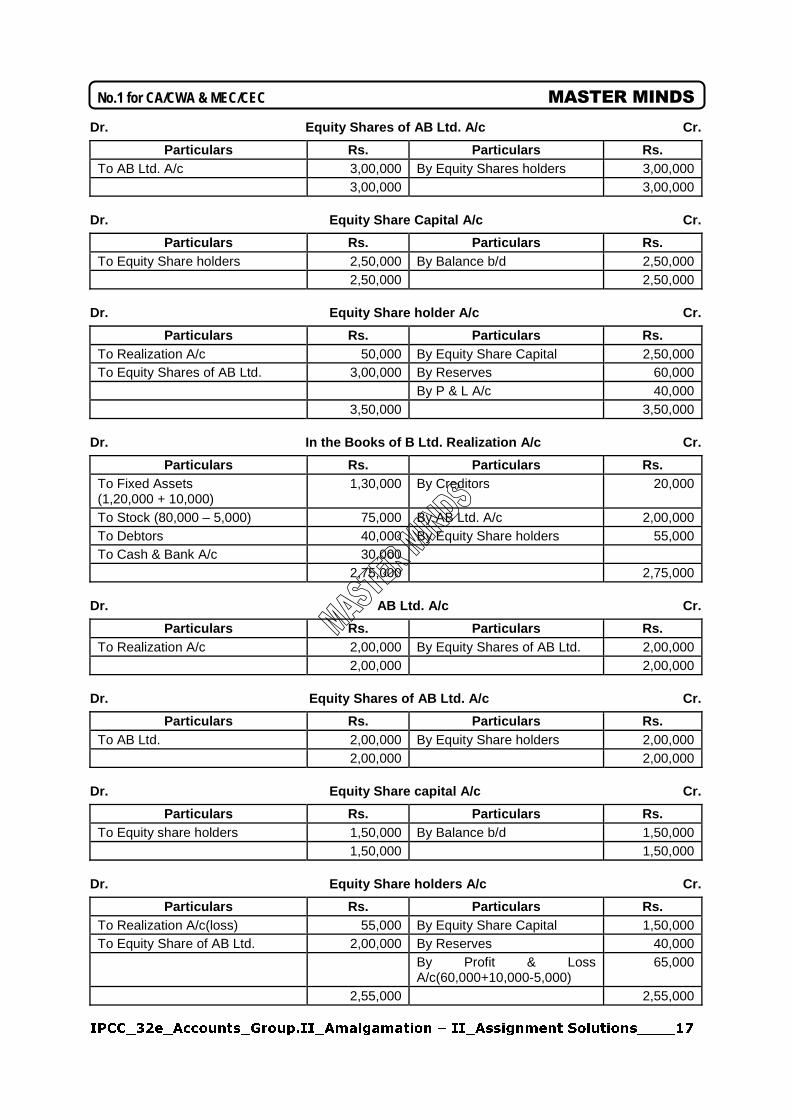

In the books of A Ltd. Ledger accounts

Realiztion A/c Dr. Cr.

Particulars Rs. Particulars Rs. To Fixed Assets A/c 1,50,000 By Creditors 30,000 To Stock A/c 70,000 By AB Ltd. 3,00,000 To Debtors A/c 80,000 By Equity Share holder A/c 50,000 To cash and bank A/c 80,000 3,80,000 3,80,000

AB Ltd. A/c

Dr. Cr. Particulars Rs. Particulars Rs.

To Realization A/c 3,00,000 By Equity Shares of AB Ltd. 3,00,000 3,00,000 3,00,000

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____17

No.1 for CA/CWA & MEC/CEC MASTER MINDS

Dr. Equity Shares of AB Ltd. A/c Cr.

Particulars Rs. Particulars Rs. To AB Ltd. A/c 3,00,000 By Equity Shares holders 3,00,000 3,00,000 3,00,000

Dr. Equity Share Capital A/c Cr.

Particulars Rs. Particulars Rs. To Equity Share holders 2,50,000 By Balance b/d 2,50,000 2,50,000 2,50,000

Dr. Equity Share holder A/c Cr.

Particulars Rs. Particulars Rs. To Realization A/c 50,000 By Equity Share Capital 2,50,000 To Equity Shares of AB Ltd. 3,00,000 By Reserves 60,000 By P & L A/c 40,000 3,50,000 3,50,000

Dr. In the Books of B Ltd. Realization A/c Cr.

Particulars Rs. Particulars Rs. To Fixed Assets (1,20,000 + 10,000)

1,30,000 By Creditors 20,000

To Stock (80,000 – 5,000) 75,000 By AB Ltd. A/c 2,00,000 To Debtors 40,000 By Equity Share holders 55,000 To Cash & Bank A/c 30,000 2,75,000 2,75,000

Dr. AB Ltd. A/c Cr.

Particulars Rs. Particulars Rs. To Realization A/c 2,00,000 By Equity Shares of AB Ltd. 2,00,000 2,00,000 2,00,000

Dr. Equity Shares of AB Ltd. A/c Cr.

Particulars Rs. Particulars Rs. To AB Ltd. 2,00,000 By Equity Share holders 2,00,000 2,00,000 2,00,000

Dr. Equity Share capital A/c Cr.

Particulars Rs. Particulars Rs. To Equity share holders 1,50,000 By Balance b/d 1,50,000 1,50,000 1,50,000

Dr. Equity Share holders A/c Cr.

Particulars Rs. Particulars Rs. To Realization A/c(loss) 55,000 By Equity Share Capital 1,50,000 To Equity Share of AB Ltd. 2,00,000 By Reserves 40,000 By Profit & Loss

A/c(60,000+10,000-5,000) 65,000

2,55,000 2,55,000

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____18

Ph: 0863 – 22 42 355 www.gntmasterminds.com

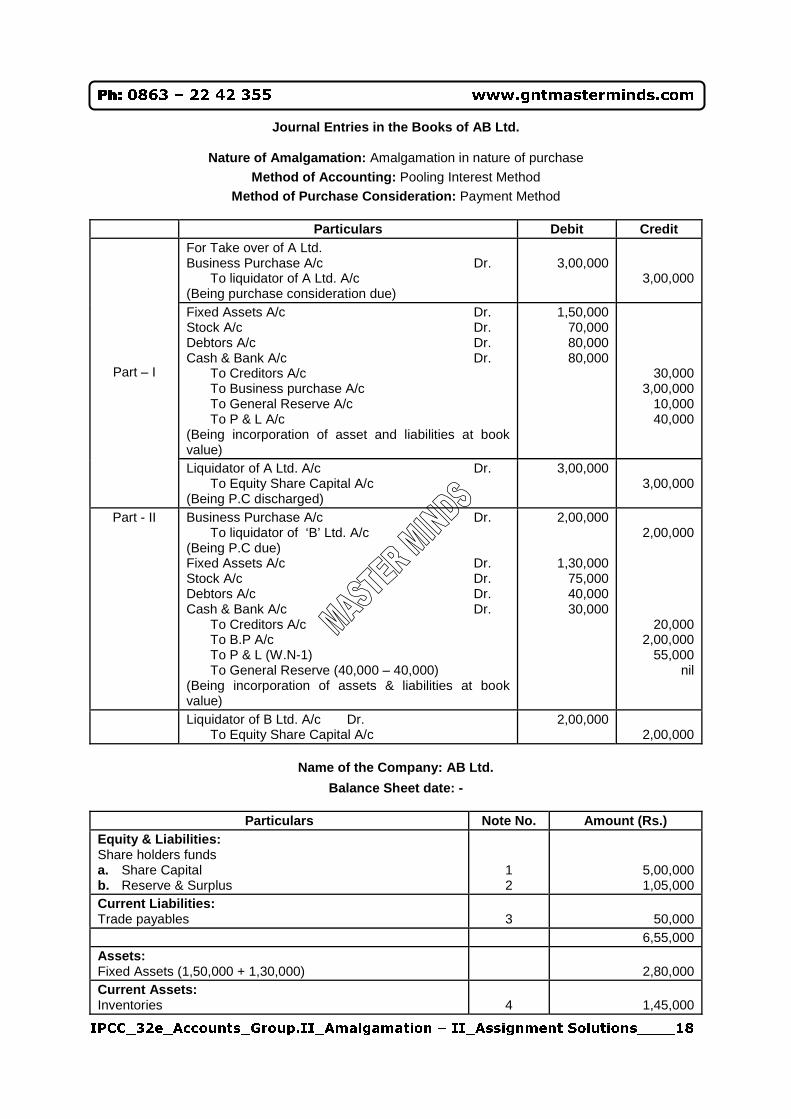

Journal Entries in the Books of AB Ltd.

Nature of Amalgamation: Amalgamation in nature of purchase

Method of Accounting: Pooling Interest Method

Method of Purchase Consideration: Payment Method

Particulars Debit Credit For Take over of A Ltd. Business Purchase A/c Dr.

To liquidator of A Ltd. A/c (Being purchase consideration due)

3,00,000

3,00,000

Fixed Assets A/c Dr. Stock A/c Dr. Debtors A/c Dr. Cash & Bank A/c Dr.

To Creditors A/c To Business purchase A/c To General Reserve A/c To P & L A/c

(Being incorporation of asset and liabilities at book value)

1,50,000 70,000 80,000 80,000

30,000 3,00,000

10,000 40,000

Part – I

Liquidator of A Ltd. A/c Dr. To Equity Share Capital A/c

(Being P.C discharged)

3,00,000 3,00,000

Part - II Business Purchase A/c Dr. To liquidator of ‘B’ Ltd. A/c

(Being P.C due) Fixed Assets A/c Dr. Stock A/c Dr. Debtors A/c Dr. Cash & Bank A/c Dr.

To Creditors A/c To B.P A/c To P & L (W.N-1) To General Reserve (40,000 – 40,000)

(Being incorporation of assets & liabilities at book value)

2,00,000

1,30,000 75,000 40,000 30,000

2,00,000

20,000 2,00,000

55,000 nil

Liquidator of B Ltd. A/c Dr. To Equity Share Capital A/c

2,00,000 2,00,000

Name of the Company: AB Ltd.

Balance Sheet date: -

Particulars Note No. Amount (Rs.) Equity & Liabilities: Share holders funds a. Share Capital b. Reserve & Surplus

1 2

5,00,000 1,05,000

Current Liabilities: Trade payables

3

50,000

6,55,000 Assets: Fixed Assets (1,50,000 + 1,30,000)

2,80,000

Current Assets: Inventories

4

1,45,000

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____19

No.1 for CA/CWA & MEC/CEC MASTER MINDS

Trade Receivables Cash & Cash Equivalent

5 6

1,20,000 1,10,000

6,55,000

Note to Accounts Amount

1. Share Capital 50,000 shares of Rs. 10 each (all the above shares were issued for consideration other than cash)

5,00,000

2. Reserves & Surplus a. General Reserve(60,000-50,000) loss on merger b. Profit & Loss A/c (40,000 + 55,000)

10,000 95,000

3. Trade Payables (30,000 + 20,000) 50,000

4. Inventories (70,000 + 75,000) 1,45,000

5. Trade receivables (80,000 + 40,000) 1,20,000

6. Cash & Cash Equivalent Cash & Bank (80,000 + 30,000)

1,10,000

Working note 1: Calculation of Profit & Loss on Merger

Particulars A LTd. B LTd.

Paid up share capital 2,50,000 1,50,000

Where as agreed PC 3,00,000 2,00,000

Loss on merger 50,000 50,000

Free reserves of Selling company

General reserve (50,000) (40,000)

Profit&loss A/c - (10,000)

Balance of General Reserve A/c(60,000-50,000) 10,000 -

Balance of Profit & Loss A/c 40,000 55,000

PROBLEM No. 11

Calculation of Earning per share

Particulars Amount

Profit before interest and Tax 6,00,000

Less: 10% Interest on debentures 60,000

11% Interest on term loan 77,000

Profit before Tax 4,63,000

Less: Tax @ 45% 2,08,350

Profit after Tax 2,54,650

Less: Preference dividend (5L x 12%) 60,000

No. of Equity shares 80,000

Earning per share (EPS)(1,94,650/80,000) 2.433

Price Earning Ratio (MPS / EPS) 9

MPS (9 x 2.433) 21.89 Note: earnings available to equity share holders=2,54,650-60,000=1,94,650

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____20

Ph: 0863 – 22 42 355 www.gntmasterminds.com

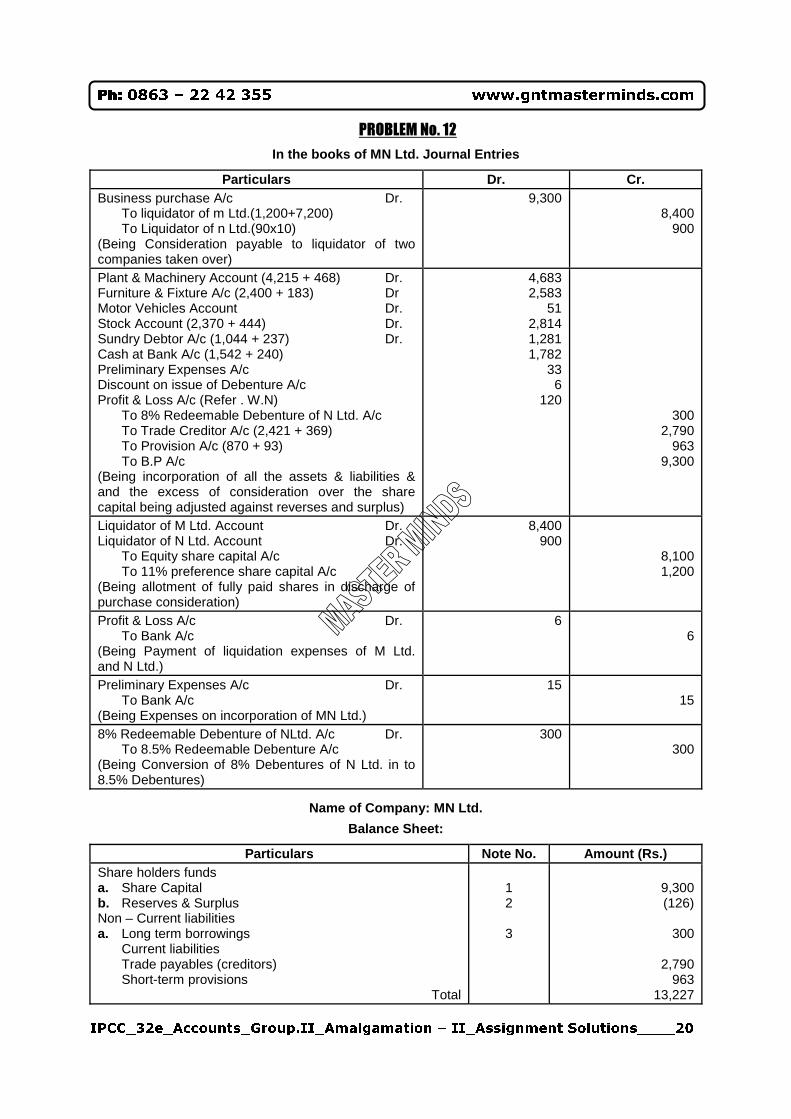

PROBLEM No. 12

In the books of MN Ltd. Journal Entries

Particulars Dr. Cr. Business purchase A/c Dr.

To liquidator of m Ltd.(1,200+7,200) To Liquidator of n Ltd.(90x10)

(Being Consideration payable to liquidator of two companies taken over)

9,300 8,400

900

Plant & Machinery Account (4,215 + 468) Dr. Furniture & Fixture A/c (2,400 + 183) Dr Motor Vehicles Account Dr. Stock Account (2,370 + 444) Dr. Sundry Debtor A/c (1,044 + 237) Dr. Cash at Bank A/c (1,542 + 240) Preliminary Expenses A/c Discount on issue of Debenture A/c Profit & Loss A/c (Refer . W.N)

To 8% Redeemable Debenture of N Ltd. A/c To Trade Creditor A/c (2,421 + 369) To Provision A/c (870 + 93) To B.P A/c

(Being incorporation of all the assets & liabilities & and the excess of consideration over the share capital being adjusted against reverses and surplus)

4,683 2,583

51 2,814 1,281 1,782

33 6

120

300 2,790

963 9,300

Liquidator of M Ltd. Account Dr. Liquidator of N Ltd. Account Dr.

To Equity share capital A/c To 11% preference share capital A/c

(Being allotment of fully paid shares in discharge of purchase consideration)

8,400 900

8,100 1,200

Profit & Loss A/c Dr. To Bank A/c

(Being Payment of liquidation expenses of M Ltd. and N Ltd.)

6 6

Preliminary Expenses A/c Dr. To Bank A/c

(Being Expenses on incorporation of MN Ltd.)

15 15

8% Redeemable Debenture of NLtd. A/c Dr. To 8.5% Redeemable Debenture A/c

(Being Conversion of 8% Debentures of N Ltd. in to 8.5% Debentures)

300 300

Name of Company: MN Ltd.

Balance Sheet:

Particulars Note No. Amount (Rs.) Share holders funds a. Share Capital b. Reserves & Surplus Non – Current liabilities a. Long term borrowings

Current liabilities Trade payables (creditors) Short-term provisions

Total

1 2 3

9,300 (126)

300

2,790

963 13,227

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____21

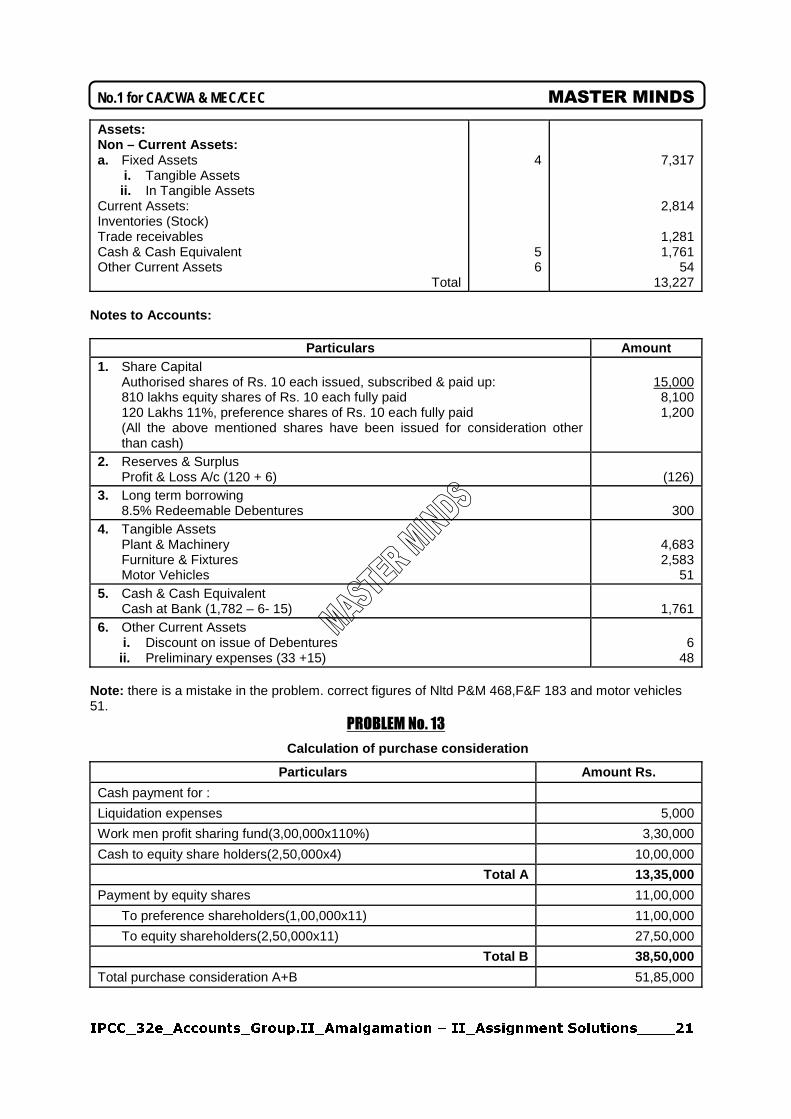

No.1 for CA/CWA & MEC/CEC MASTER MINDS

Assets: Non – Current Assets: a. Fixed Assets

i. Tangible Assets ii. In Tangible Assets

Current Assets: Inventories (Stock) Trade receivables Cash & Cash Equivalent Other Current Assets

Total

4

5 6

7,317

2,814

1,281 1,761

54 13,227

Notes to Accounts:

Particulars Amount 1. Share Capital

Authorised shares of Rs. 10 each issued, subscribed & paid up: 810 lakhs equity shares of Rs. 10 each fully paid 120 Lakhs 11%, preference shares of Rs. 10 each fully paid (All the above mentioned shares have been issued for consideration other than cash)

15,000 8,100 1,200

2. Reserves & Surplus Profit & Loss A/c (120 + 6)

(126)

3. Long term borrowing 8.5% Redeemable Debentures

300

4. Tangible Assets Plant & Machinery Furniture & Fixtures Motor Vehicles

4,683 2,583

51 5. Cash & Cash Equivalent

Cash at Bank (1,782 – 6- 15)

1,761 6. Other Current Assets

i. Discount on issue of Debentures ii. Preliminary expenses (33 +15)

6

48 Note: there is a mistake in the problem. correct figures of Nltd P&M 468,F&F 183 and motor vehicles 51.

PROBLEM No. 13

Calculation of purchase consideration

Particulars Amount Rs.

Cash payment for :

Liquidation expenses 5,000

Work men profit sharing fund(3,00,000x110%) 3,30,000

Cash to equity share holders(2,50,000x4) 10,00,000

Total A 13,35,000

Payment by equity shares 11,00,000

To preference shareholders(1,00,000x11) 11,00,000

To equity shareholders(2,50,000x11) 27,50,000

Total B 38,50,000

Total purchase consideration A+B 51,85,000

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____22

Ph: 0863 – 22 42 355 www.gntmasterminds.com

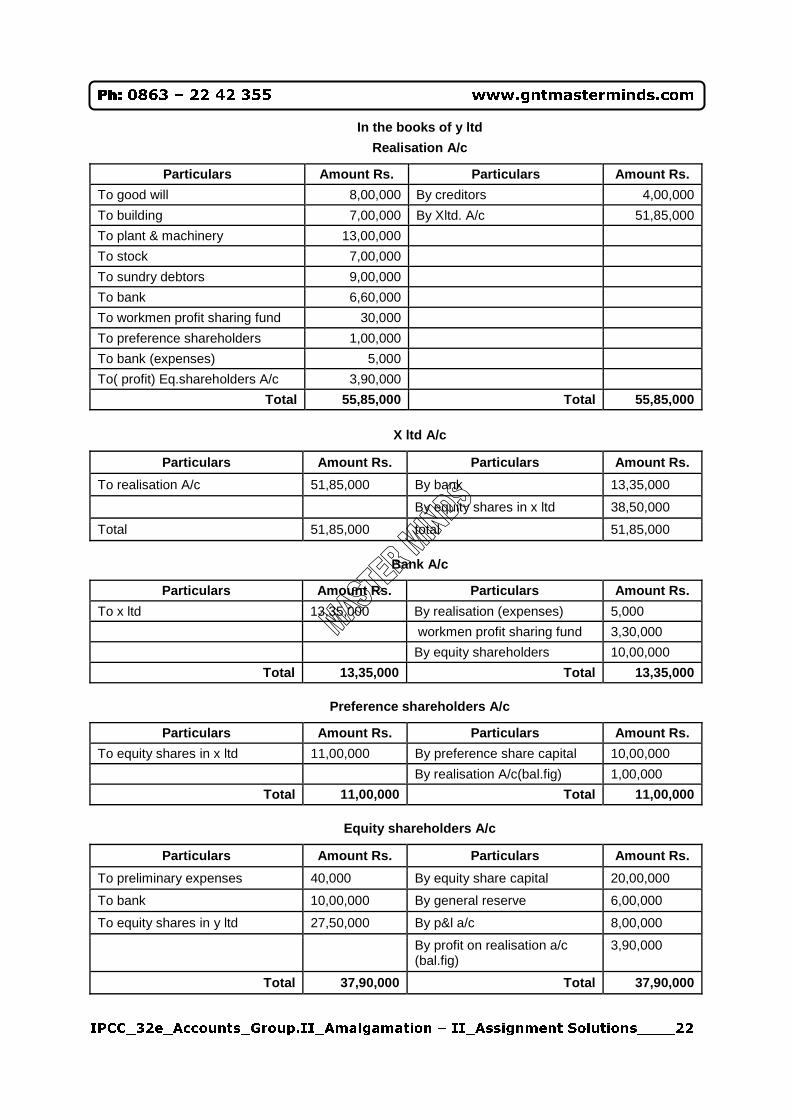

In the books of y ltd

Realisation A/c

Particulars Amount Rs. Particulars Amount Rs.

To good will 8,00,000 By creditors 4,00,000

To building 7,00,000 By Xltd. A/c 51,85,000

To plant & machinery 13,00,000

To stock 7,00,000

To sundry debtors 9,00,000

To bank 6,60,000

To workmen profit sharing fund 30,000

To preference shareholders 1,00,000

To bank (expenses) 5,000

To( profit) Eq.shareholders A/c 3,90,000

Total 55,85,000 Total 55,85,000

X ltd A/c

Particulars Amount Rs. Particulars Amount Rs.

To realisation A/c 51,85,000 By bank 13,35,000

By equity shares in x ltd 38,50,000

Total 51,85,000 total 51,85,000

Bank A/c

Particulars Amount Rs. Particulars Amount Rs.

To x ltd 13,35,000 By realisation (expenses) 5,000

workmen profit sharing fund 3,30,000

By equity shareholders 10,00,000

Total 13,35,000 Total 13,35,000

Preference shareholders A/c

Particulars Amount Rs. Particulars Amount Rs.

To equity shares in x ltd 11,00,000 By preference share capital 10,00,000

By realisation A/c(bal.fig) 1,00,000

Total 11,00,000 Total 11,00,000

Equity shareholders A/c

Particulars Amount Rs. Particulars Amount Rs.

To preliminary expenses 40,000 By equity share capital 20,00,000

To bank 10,00,000 By general reserve 6,00,000

To equity shares in y ltd 27,50,000 By p&l a/c 8,00,000

By profit on realisation a/c (bal.fig)

3,90,000

Total 37,90,000 Total 37,90,000

IPCC_32e_Accounts_Group.II_Amalgamation – II_Assignment Solutions____23

No.1 for CA/CWA & MEC/CEC MASTER MINDS

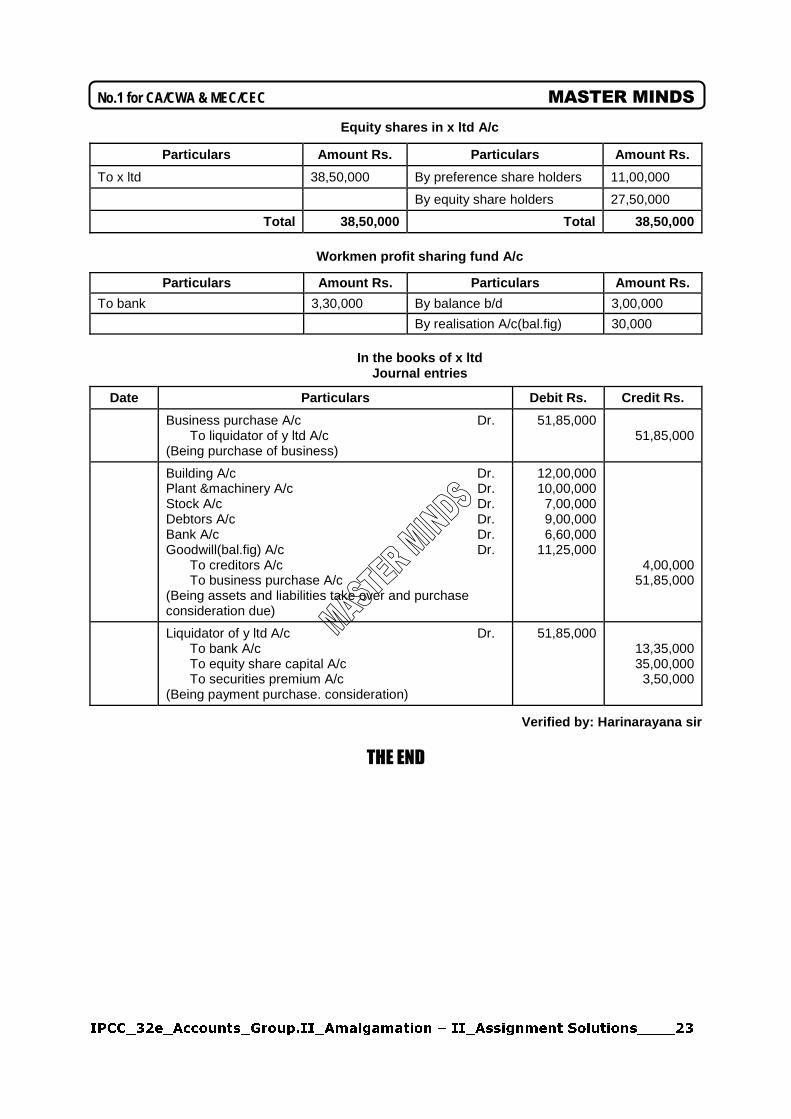

Equity shares in x ltd A/c

Particulars Amount Rs. Particulars Amount Rs.

To x ltd 38,50,000 By preference share holders 11,00,000

By equity share holders 27,50,000

Total 38,50,000 Total 38,50,000

Workmen profit sharing fund A/c

Particulars Amount Rs. Particulars Amount Rs.

To bank 3,30,000 By balance b/d 3,00,000

By realisation A/c(bal.fig) 30,000

In the books of x ltd Journal entries

Date Particulars Debit Rs. Credit Rs.

Business purchase A/c Dr. To liquidator of y ltd A/c

(Being purchase of business)

51,85,000 51,85,000

Building A/c Dr. Plant &machinery A/c Dr. Stock A/c Dr. Debtors A/c Dr. Bank A/c Dr. Goodwill(bal.fig) A/c Dr.

To creditors A/c To business purchase A/c

(Being assets and liabilities take over and purchase consideration due)

12,00,000 10,00,000

7,00,000 9,00,000 6,60,000

11,25,000

4,00,000 51,85,000

Liquidator of y ltd A/c Dr. To bank A/c To equity share capital A/c To securities premium A/c

(Being payment purchase. consideration)

51,85,000 13,35,000 35,00,000

3,50,000

Verified by: Harinarayana sir

THE END