Solar Water Heater Market Assessment Consolidated Report · Bangladesh, Sri Lanka, Thailand, ......

158

Data submitted herein is intended for the sole use of the Client in evaluating IIEC’s offer and is considered proprietary to IIEC. Pages containing this proprietary data are annotated with reference to this paragraph Small Scale Funding Agreement (SSFA) Solar Water Heater Market Assessment Bangladesh, Sri Lanka, Thailand, The Philippines, Vietnam Prepared for United Nations Environment Programme (UNEP) 15 rue de Milan, F-75441, Paris CEDEX 09 France by International Institute for Energy Conservation - Asia 12th Floor, United Business Centre II Building, 591, Sukhumvit Road Wattana, Bangkok 10110, THAILAND August 2011

Transcript of Solar Water Heater Market Assessment Consolidated Report · Bangladesh, Sri Lanka, Thailand, ......

Data submitted herein is intended for the sole use of the Client in evaluating IIEC’s offer and is considered proprietary to IIEC. Pages containing

this proprietary data are annotated with reference to this paragraph

SSmmaallll SSccaallee FFuunnddiinngg AAggrreeeemmeenntt ((SSSSFFAA))

SSoollaarr WWaatteerr HHeeaatteerr MMaarrkkeett AAsssseessssmmeenntt

BBaannggllaaddeesshh,, SSrrii LLaannkkaa,, TThhaaiillaanndd,, TThhee PPhhiilliippppiinneess,, VViieettnnaamm

Prepared for

United Nations Environment Programme (UNEP) 15 rue de Milan, F-75441, Paris CEDEX 09

France

by

International Institute for Energy Conservation - Asia 12th Floor, United Business Centre II Building, 591, Sukhumvit Road

Wattana, Bangkok 10110, THAILAND

August 2011

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA)

August 2011 i

CONTENTS

ABBREVIATIONS .................................................................................................................... 4

EXECUTIVE SUMMARY ............................................................................................................ 8

1 INTRODUCTION .................................................................................................... 11

1.1 Methodology ...................................................................................................... 13

2 OVERVIEW OF REGIONAL COUNTRIES .................................................................... 14

2.1 Bangladesh ....................................................................................................... 14

2.1.1 Electricity Scenario in Bangladesh ............................................................................................... 15

2.1.2 Bangladesh Climate ..................................................................................................................... 16

2.1.3 Solar Radiation in Bangladesh ..................................................................................................... 17

2.2 Sri Lanka ........................................................................................................... 18

2.2.1 Electricity Scenario in Sri Lanka ................................................................................................... 19

2.2.2 Sri Lanka Climate ......................................................................................................................... 20

2.2.3 Solar Radiation in Sri Lanka ......................................................................................................... 22

2.3 Thailand ............................................................................................................ 23

2.3.1 Electricity Scenario in Thailand .................................................................................................... 24

2.3.2 Thailand Climate ........................................................................................................................... 24

2.3.3 Solar Radiation in Thailand .......................................................................................................... 25

2.4 The Philippines .................................................................................................. 26

2.4.1 Electricity Scenario in the Philippines ........................................................................................... 28

2.4.2 Philippines Climate ....................................................................................................................... 29

2.4.3 Solar Radiation in the Philippines ................................................................................................. 30

2.5 Vietnam ............................................................................................................. 30

2.5.1 Electricity Scenario in Vietnam ..................................................................................................... 31

2.5.2 Vietnam Climate ........................................................................................................................... 33

2.5.3 Solar Radiation in Vietnam ........................................................................................................... 34

3 OVERVIEW OF SOLAR WATER HEATER (SWH) MARKET ......................................... 36

3.1 Bangladesh ....................................................................................................... 36

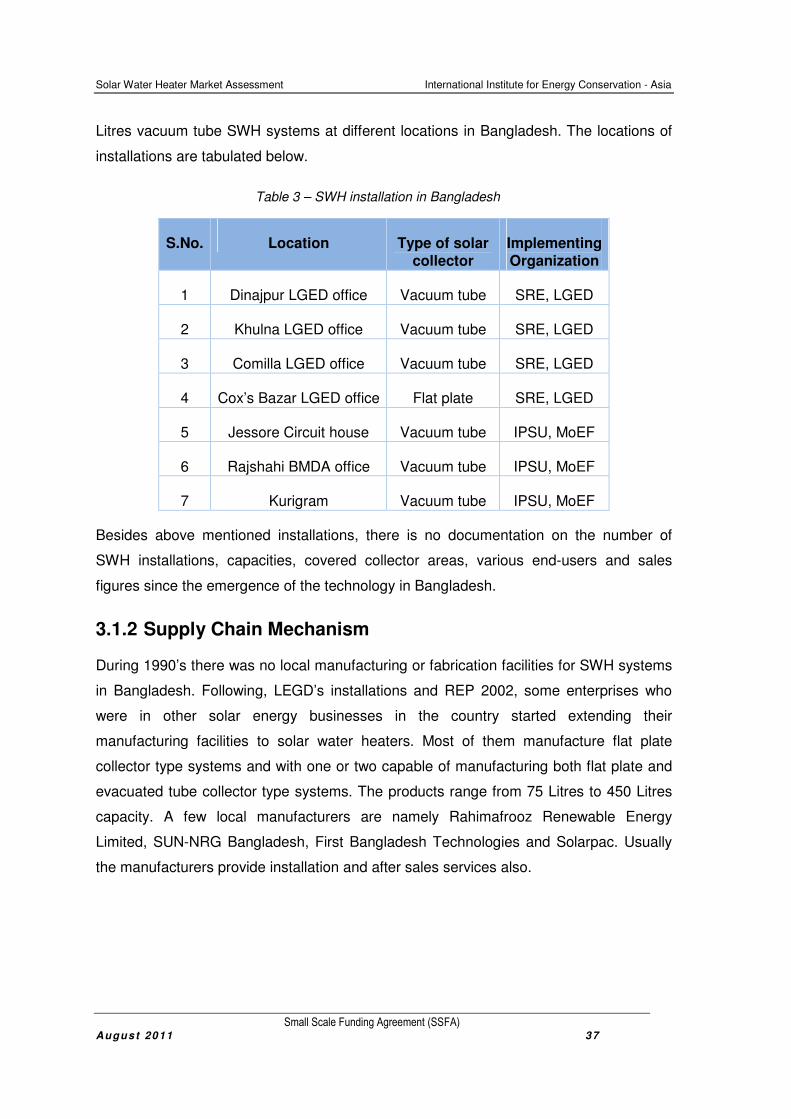

3.1.1 Installed Capacity ......................................................................................................................... 36

3.1.2 Supply Chain Mechanism ............................................................................................................. 37

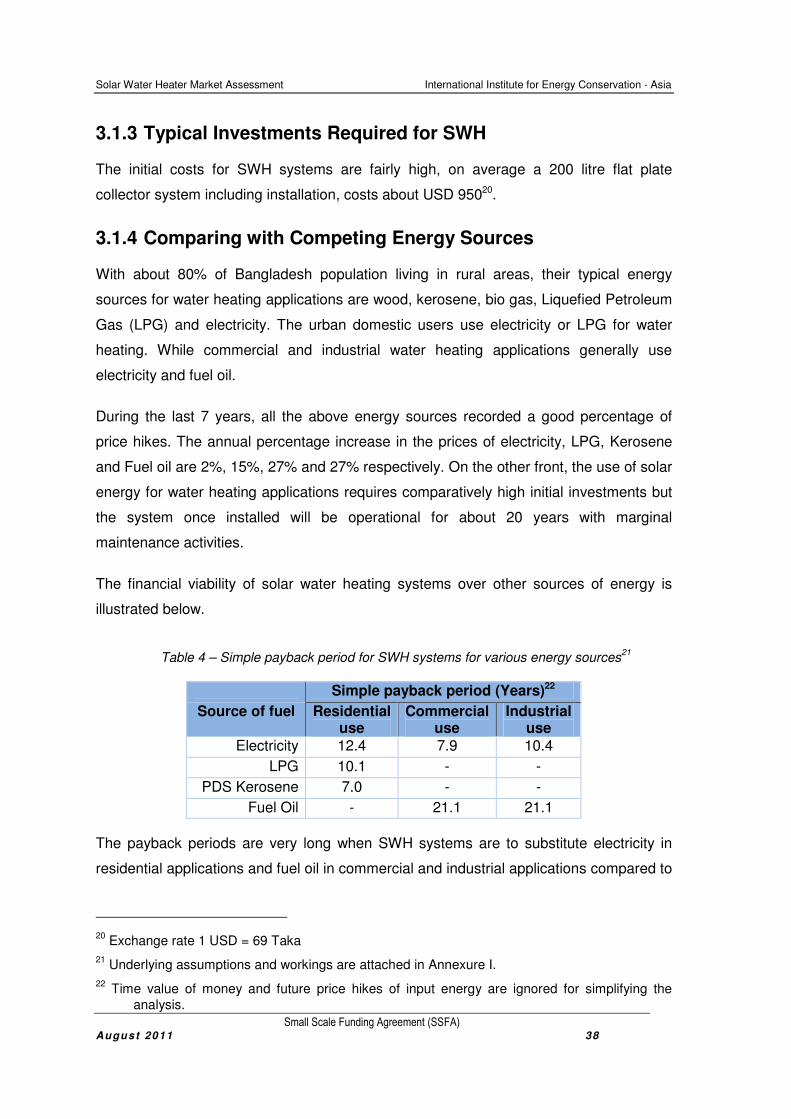

3.1.3 Typical Investments Required for SWH ....................................................................................... 38

3.1.4 Comparing with Competing Energy Sources ............................................................................... 38

3.2 Sri Lanka ........................................................................................................... 39

3.2.1 Installed Capacity ......................................................................................................................... 39

3.2.2 Supply Chain Mechanism ............................................................................................................. 39

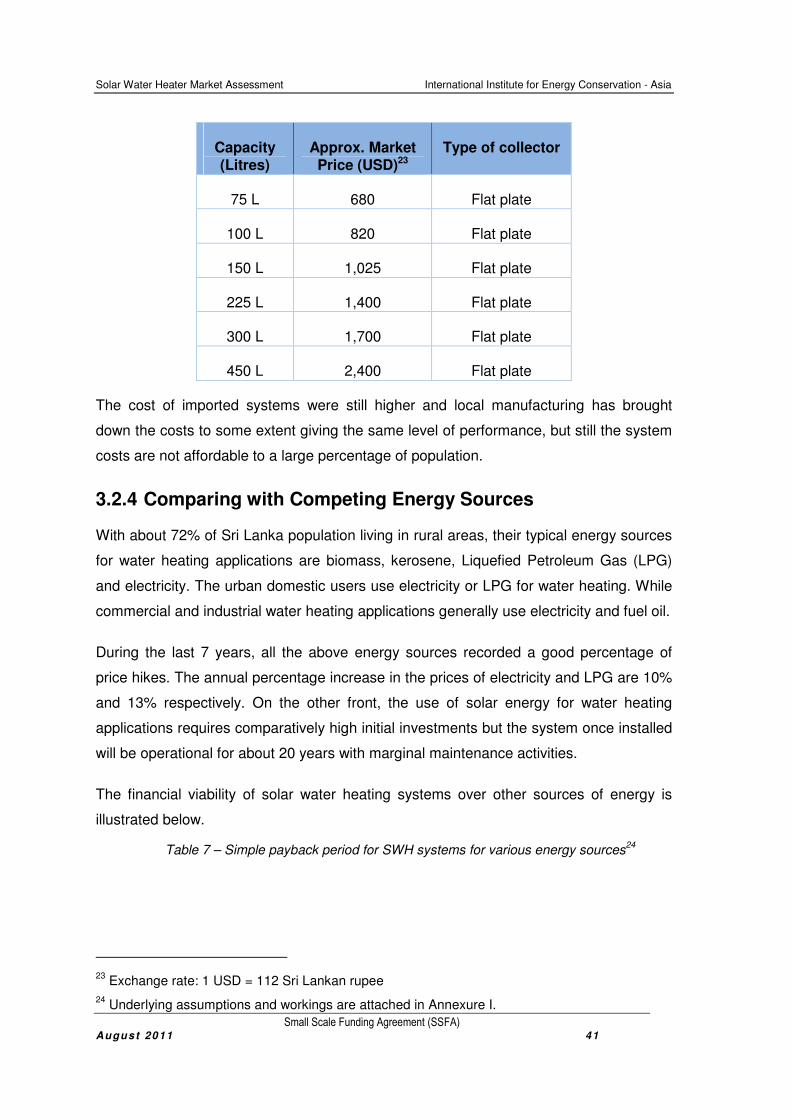

3.2.3 Typical Investments Required for SWH ....................................................................................... 40

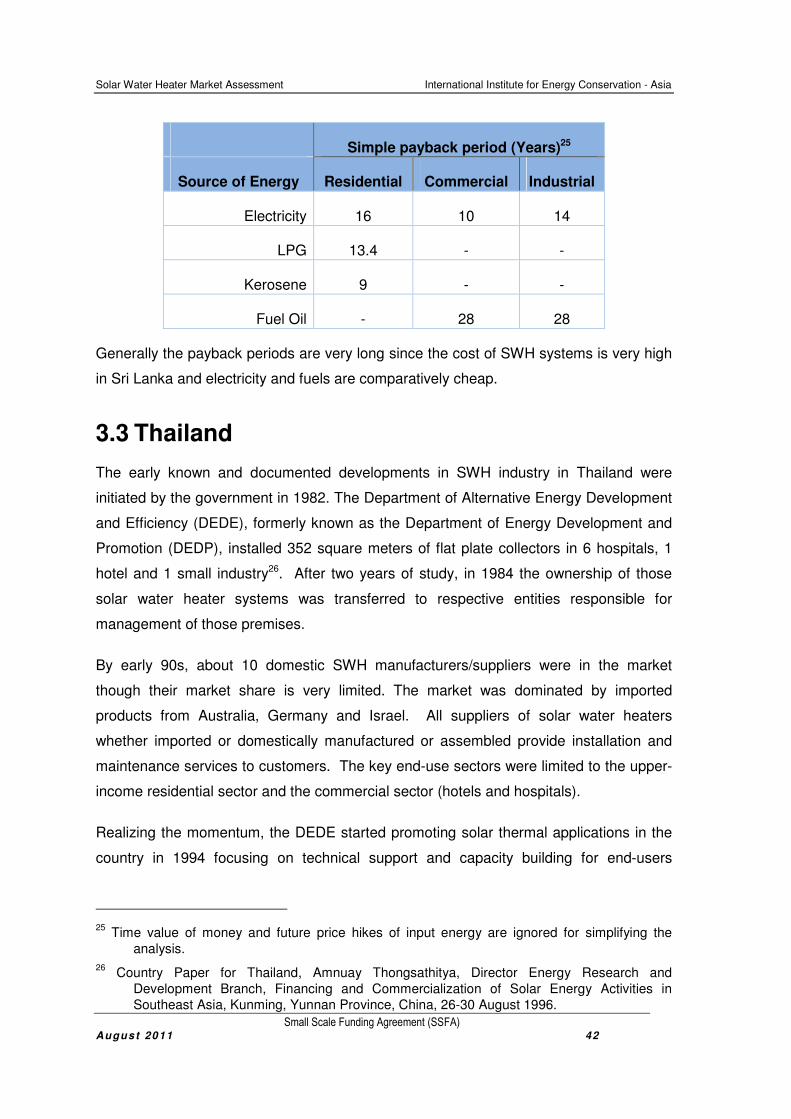

3.2.4 Comparing with Competing Energy Sources ............................................................................... 41

3.3 Thailand ............................................................................................................ 42

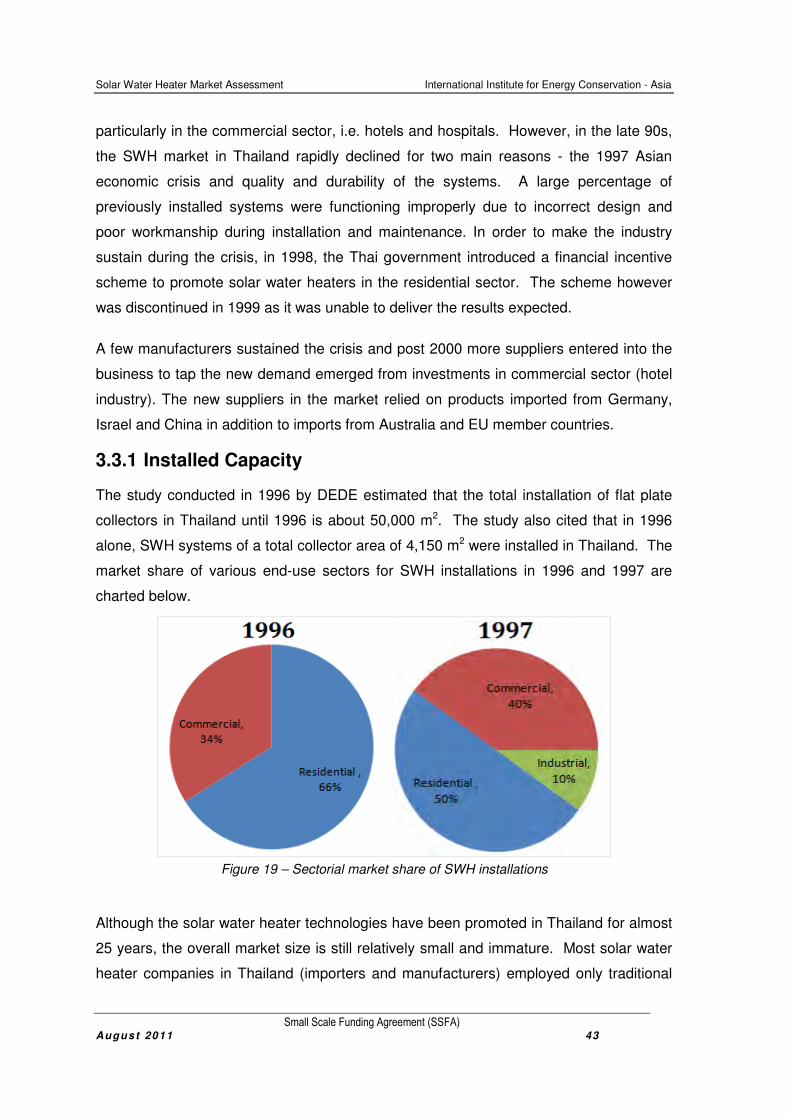

3.3.1 Installed Capacity ......................................................................................................................... 43

3.3.2 Supply Chain Mechanism ............................................................................................................. 44

3.3.3 Typical Investments Required for SWH ....................................................................................... 47

3.3.4 Comparison with Competing Energy Sources .............................................................................. 48

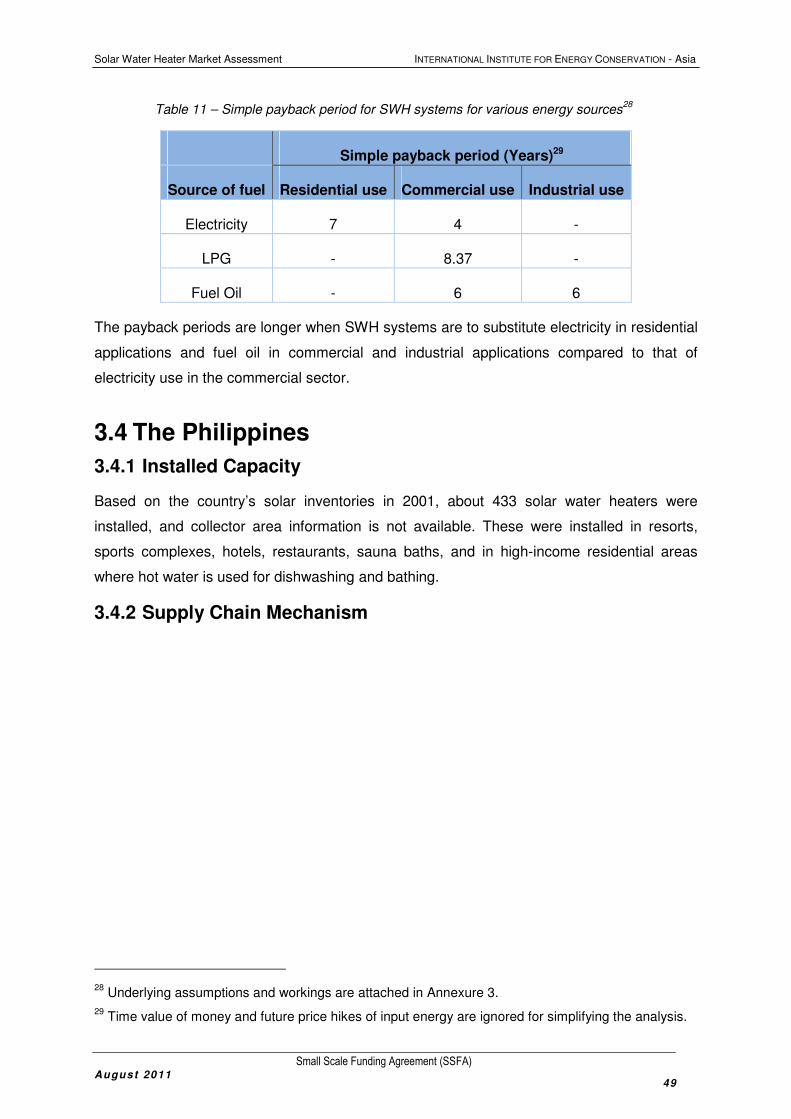

3.4 The Philippines .................................................................................................. 49

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA)

August 2011 i i

3.4.1 Installed Capacity ......................................................................................................................... 49

3.4.2 Supply Chain Mechanism ............................................................................................................. 49

3.4.3 Typical Investments Required for SWH ....................................................................................... 51

3.5 Vietnam ............................................................................................................. 51

3.5.1 Installed Capacity ......................................................................................................................... 51

3.5.2 Supply Chain Mechanism ............................................................................................................. 51

3.5.3 Typical Investments Required for SWH ....................................................................................... 52

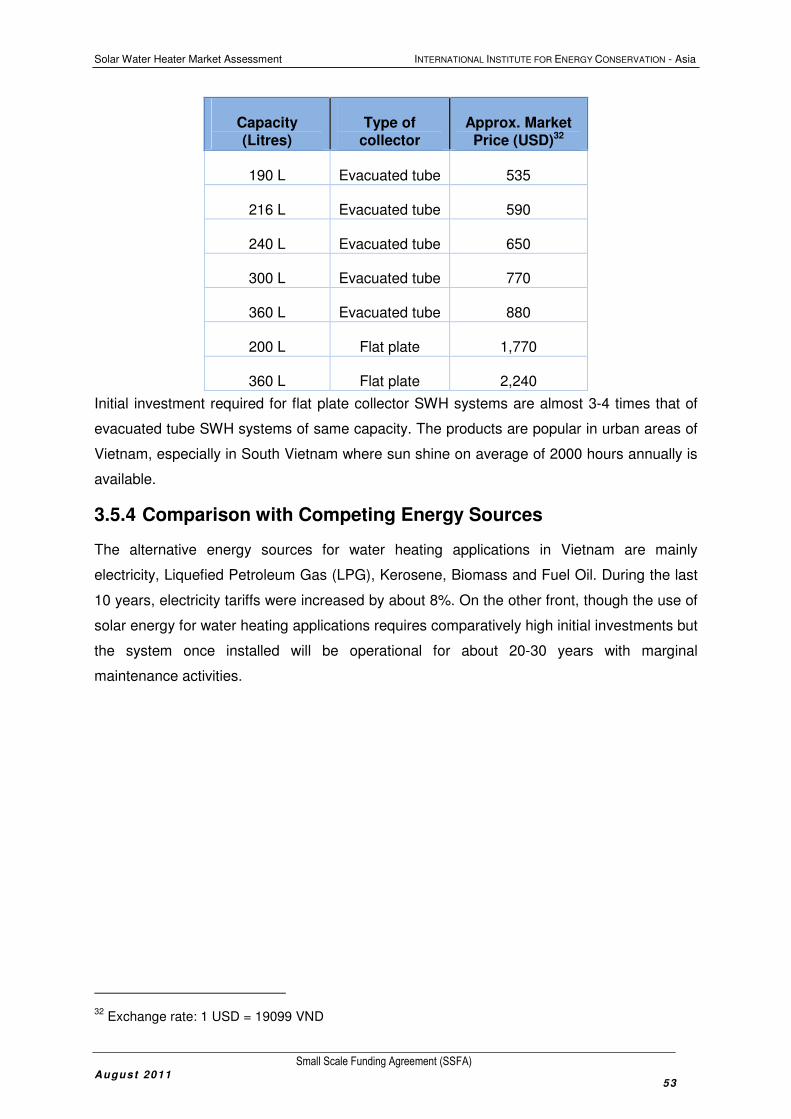

3.5.4 Comparison with Competing Energy Sources .............................................................................. 53

4 SOLAR WATER HEATERS – SYSTEM COMPONENTS, DESIGN & INSTALLATION ......... 55

4.1 Bangladesh ....................................................................................................... 55

4.2 Sri Lanka ........................................................................................................... 57

4.3 Thailand ............................................................................................................ 59

4.4 The Philippines .................................................................................................. 61

4.5 Vietnam ............................................................................................................. 63

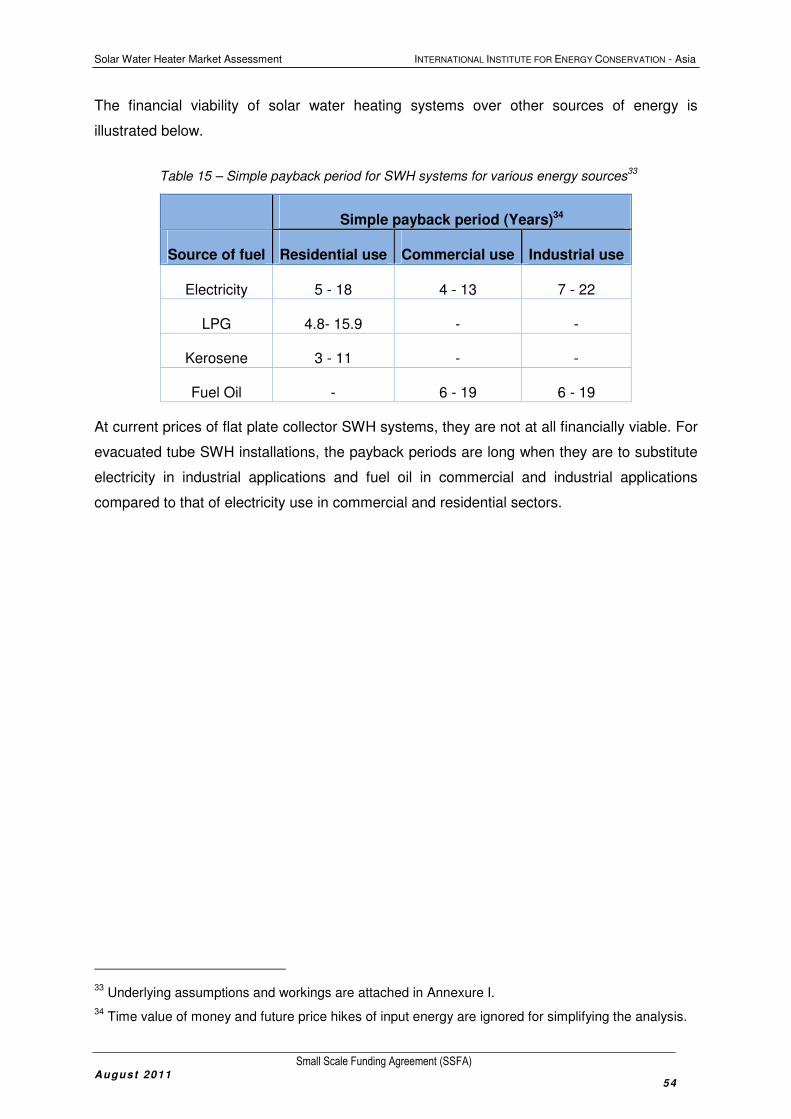

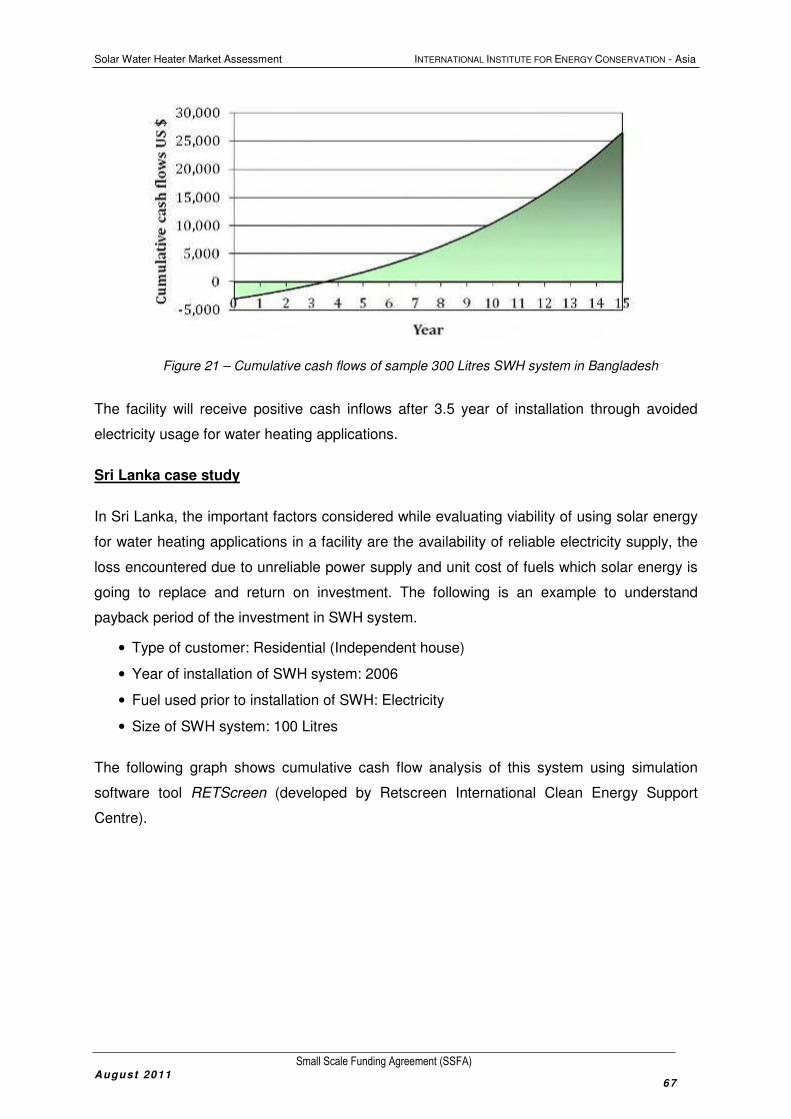

5 ECONOMIC EVALUATION OF SWH APPLICATIONS .................................................. 66

6 NATIONAL PRODUCT STANDARDS FOR SWH ......................................................... 72

6.1 Need for Quality Products ................................................................................. 72

6.2 SWH Standards for Bangladesh ....................................................................... 73

6.3 SWH Standards for Sri Lanka ........................................................................... 73

6.4 SWH Standards for Thailand ............................................................................. 73

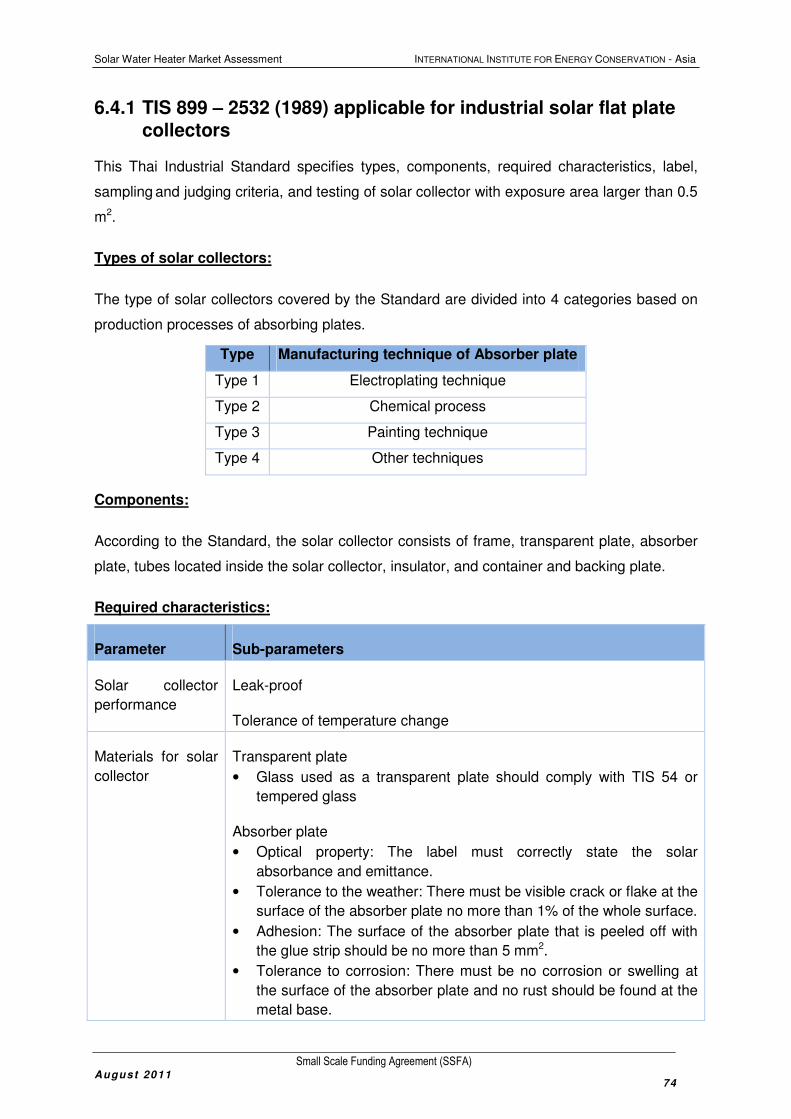

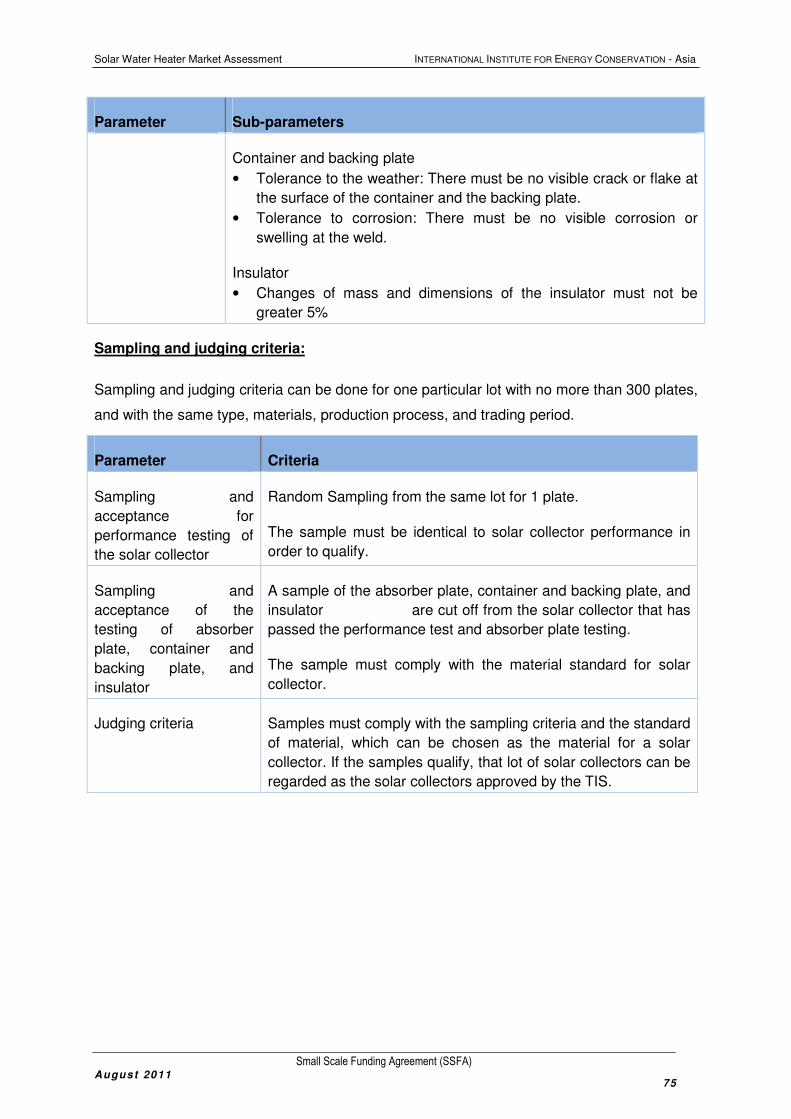

6.4.1 TIS 899 – 2532 (1989) applicable for industrial solar flat plate collectors .................................... 74

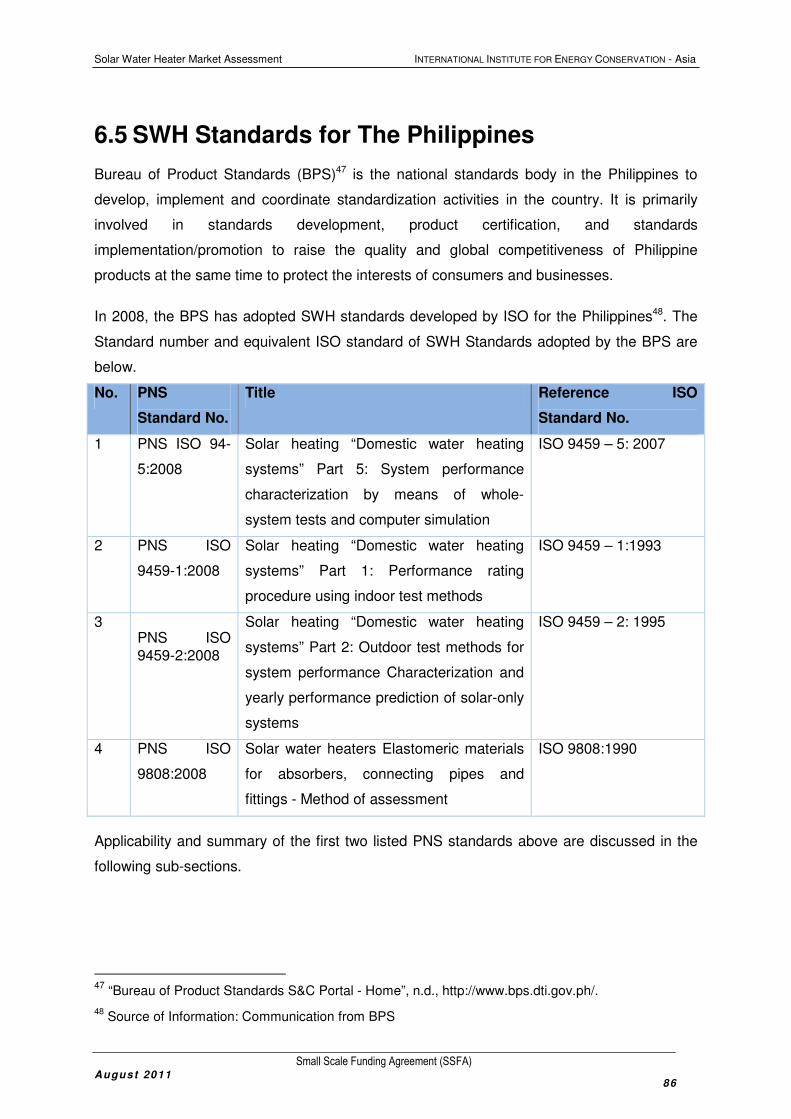

6.5 SWH Standards for The Philippines .................................................................. 86

6.5.1 PNS ISO 94 – 5: 2008 Solar heating “Domestic water heating systems” Part 5: System

performance characterization by means of whole-system tests and computer simulation .............................. 87

6.5.2 PNS ISO 9459 – 1: 2008 Solar heating “Domestic water heating systems” Part 1:

Performance rating procedure using indoor test methods ............................................................................... 88

6.6 SWH Standards for Vietnam ............................................................................. 89

6.7 Planning, Installation and Maintenance ............................................................. 90

6.7.1 Accreditation /Certification of Planners or Installers ..................................................................... 90

6.7.2 Commissioning & Certificate of Installation .................................................................................. 90

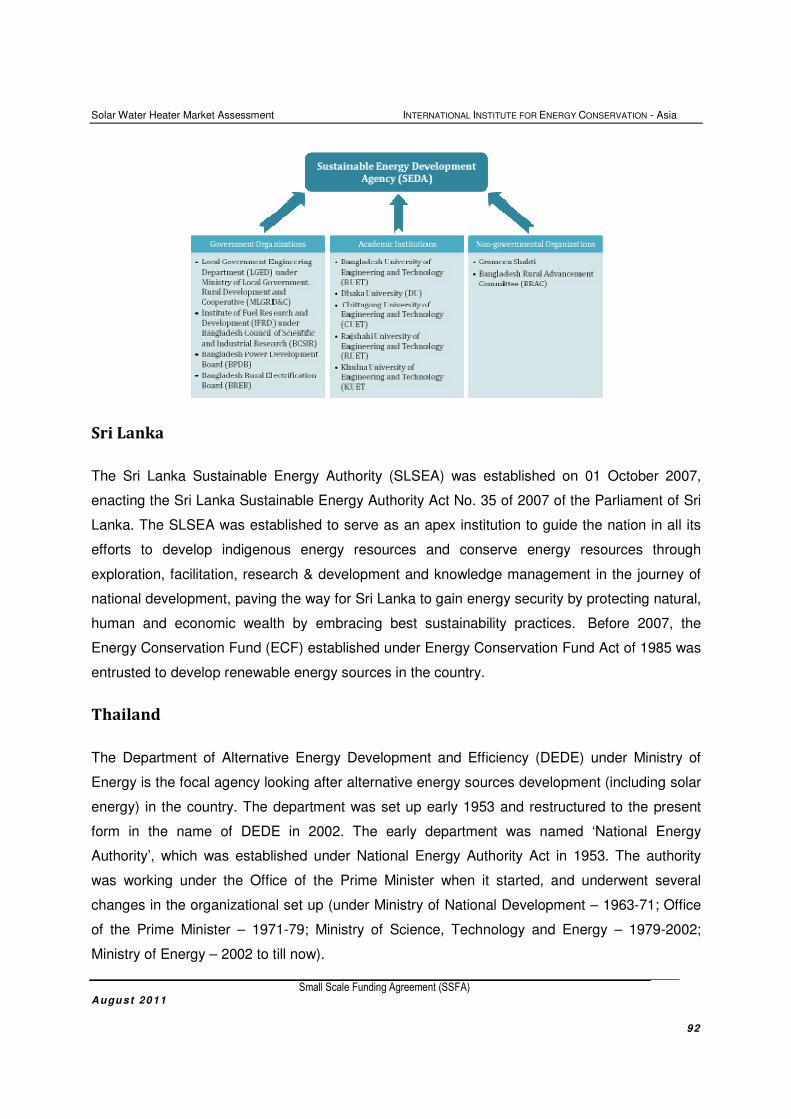

7 IN-COUNTRY INSTITUTIONAL AND POLICY FRAMEWORK FOR SWH........................... 91

7.1 Policy Interventions for SWH Systems .............................................................. 95

7.1.1 Bangladesh ................................................................................................................................... 95

7.1.2 Sri Lanka ....................................................................................................................................... 95

7.1.3 Thailand ........................................................................................................................................ 96

7.1.4 The Philippines ............................................................................................................................. 96

7.1.5 Vietnam ......................................................................................................................................... 96

7.2 In-country Testing Facilities, Accredited Test Laboratories and Certification .... 97

7.2.1 Bangladesh ................................................................................................................................... 97

7.2.2 Sri Lanka ....................................................................................................................................... 97

7.2.3 The Philippines ............................................................................................................................. 97

7.2.4 Thailand ........................................................................................................................................ 98

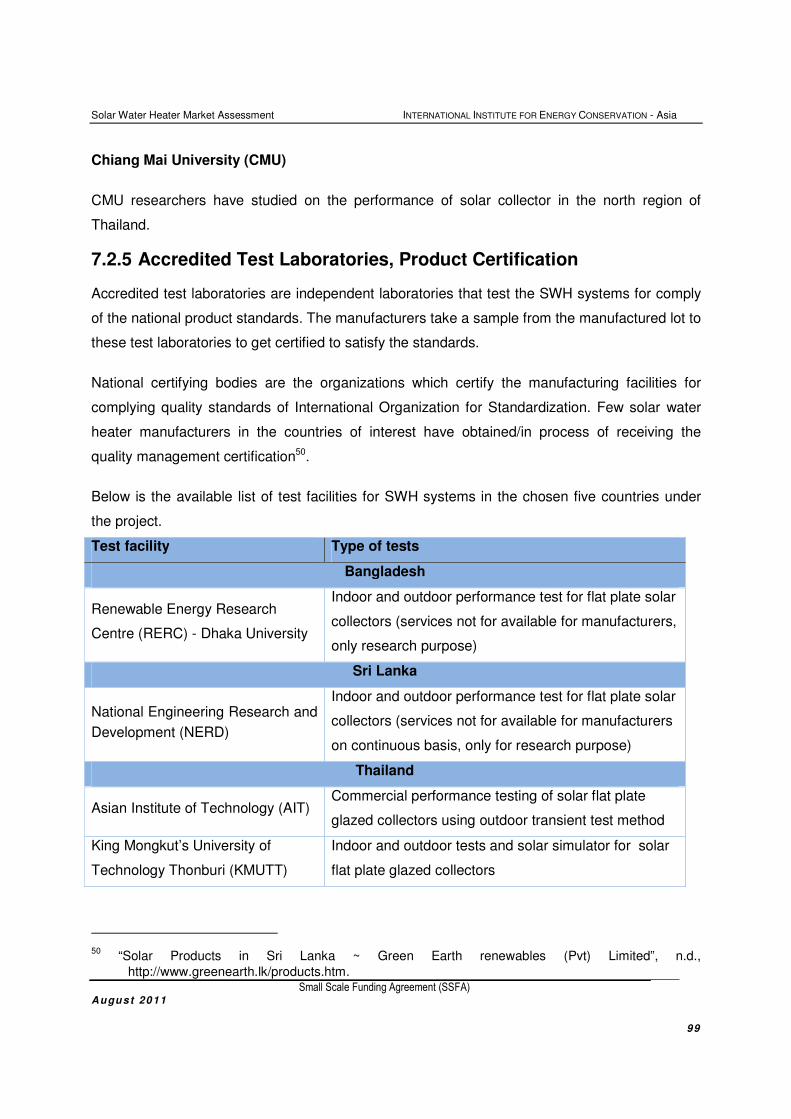

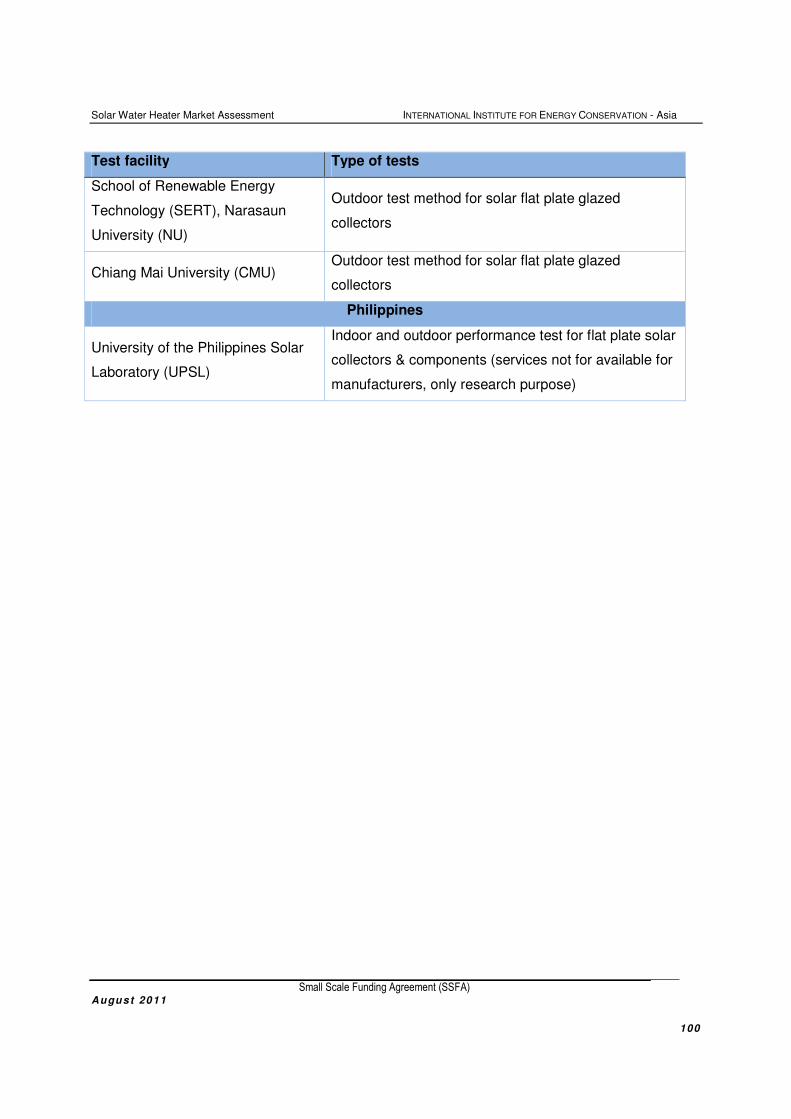

7.2.5 Accredited Test Laboratories, Product Certification ..................................................................... 99

8 SWH PROMOTIONAL MEASURES ........................................................................ 101

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA)

August 2011 i i i

8.1 Financial Measures and Incentives ................................................................. 101

8.1.1 Bangladesh ................................................................................................................................. 101

8.1.2 Sri Lanka ..................................................................................................................................... 101

8.1.3 Thailand ...................................................................................................................................... 101

8.1.4 The Philippines ........................................................................................................................... 102

8.1.5 Vietnam ....................................................................................................................................... 102

8.2 Marketing and Awareness Programs .............................................................. 103

8.2.1 Bangladesh ................................................................................................................................. 103

8.2.2 Sri Lanka ..................................................................................................................................... 103

8.2.3 Thailand ...................................................................................................................................... 103

8.2.4 The Philippines ........................................................................................................................... 104

8.2.5 Vietnam ....................................................................................................................................... 104

9 SOLAR WATER HEATERS – COUNTRY SUCCESSES .............................................. 105

9.1 Bangladesh ..................................................................................................... 105

9.2 Sri Lanka ......................................................................................................... 106

9.3 The Philippines ................................................................................................ 107

9.4 Thailand .......................................................................................................... 107

9.5 Vietnam ........................................................................................................... 109

10 BARRIERS ......................................................................................................... 112

10.1 Bangladesh ..................................................................................................... 112

10.2 Sri Lanka ......................................................................................................... 113

10.3 Thailand .......................................................................................................... 114

10.4 The Philippines ................................................................................................ 115

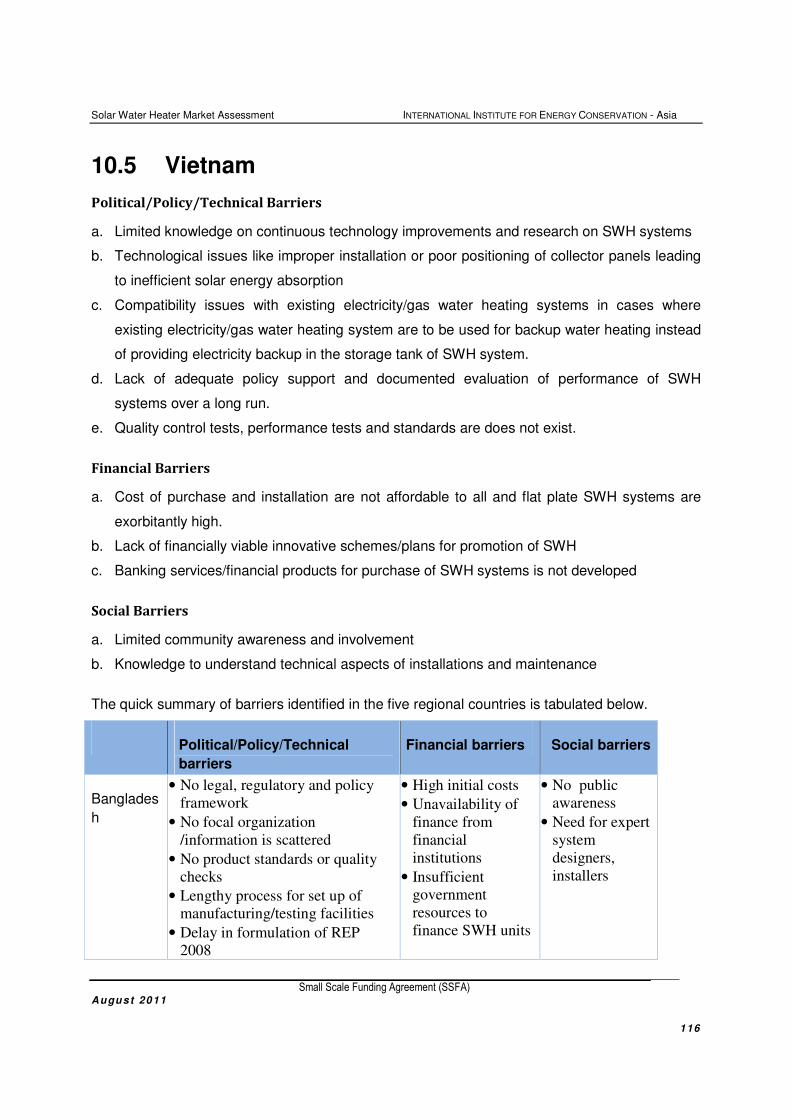

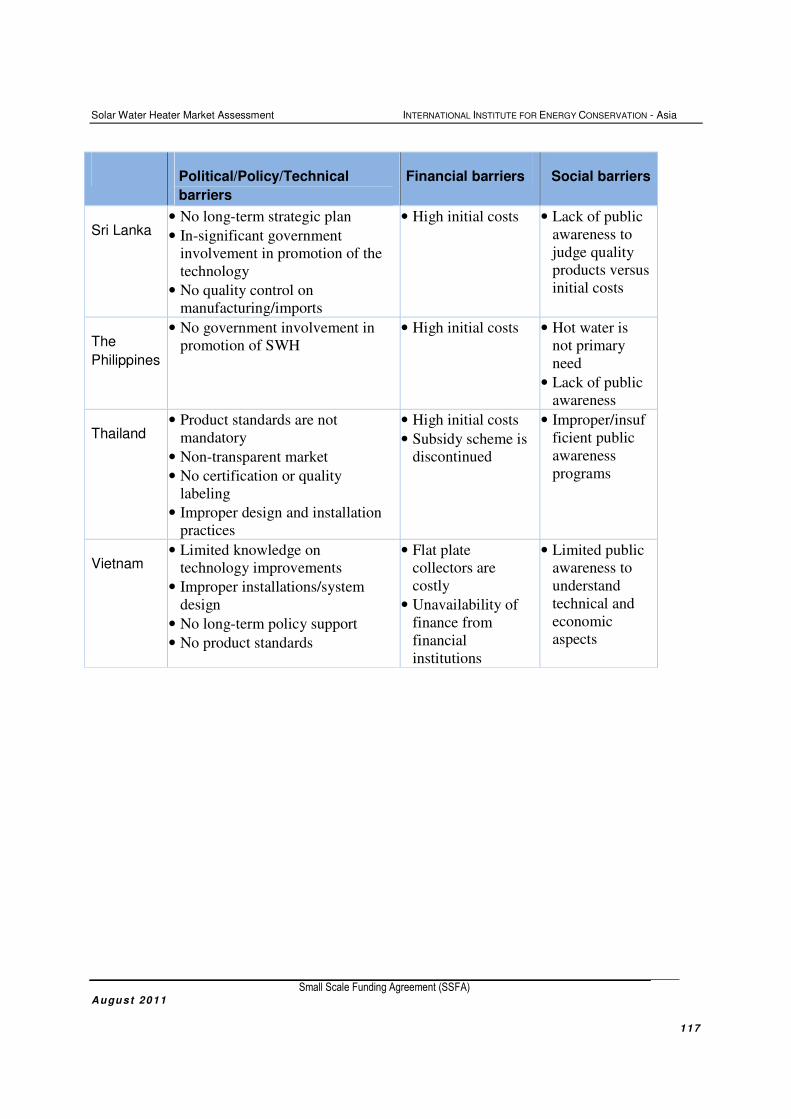

10.5 Vietnam ........................................................................................................... 116

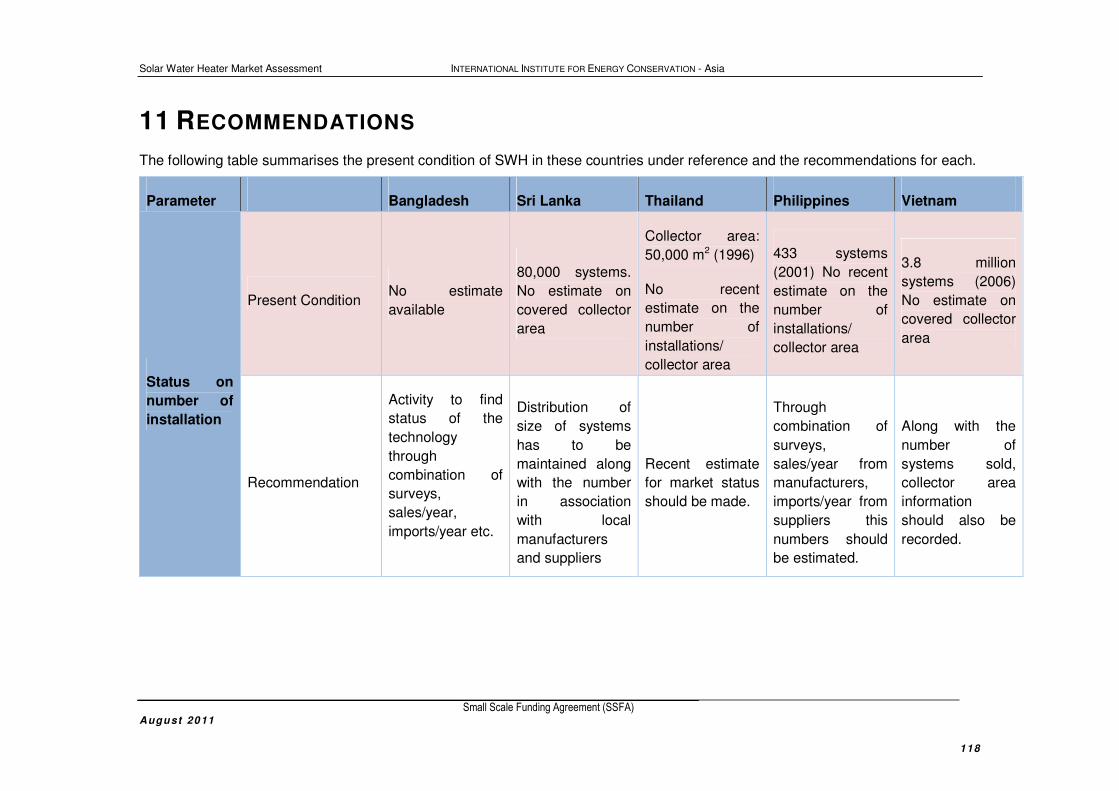

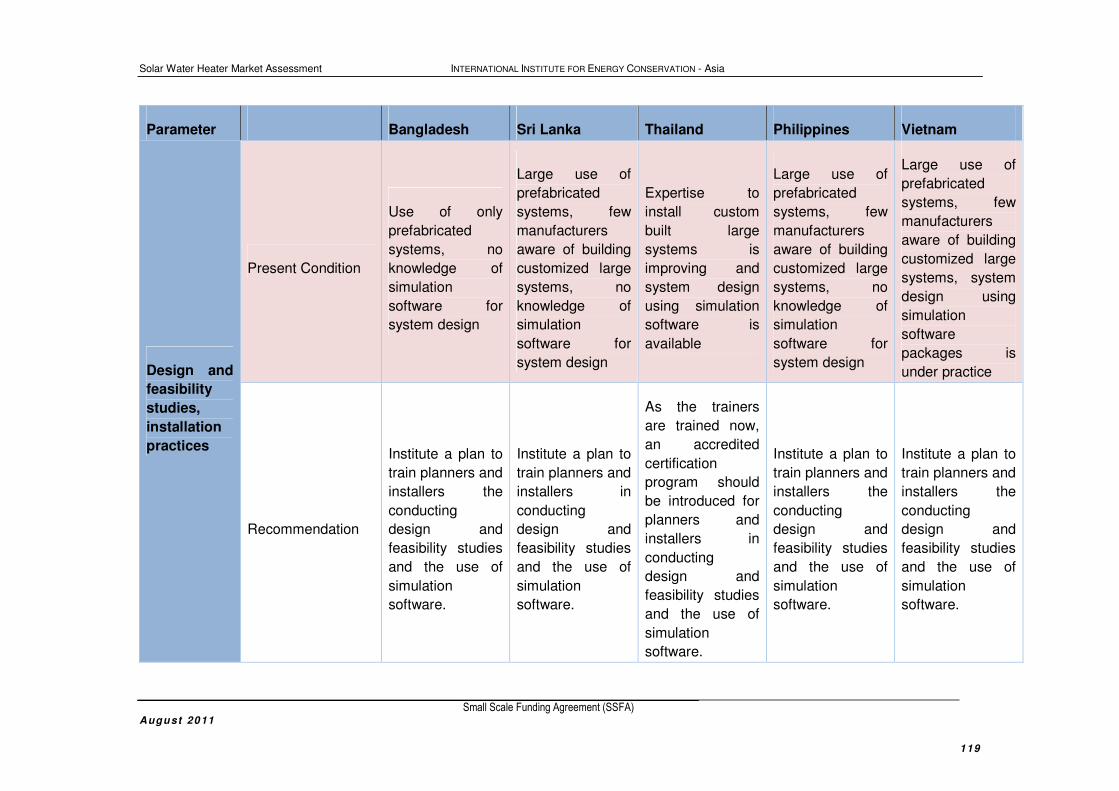

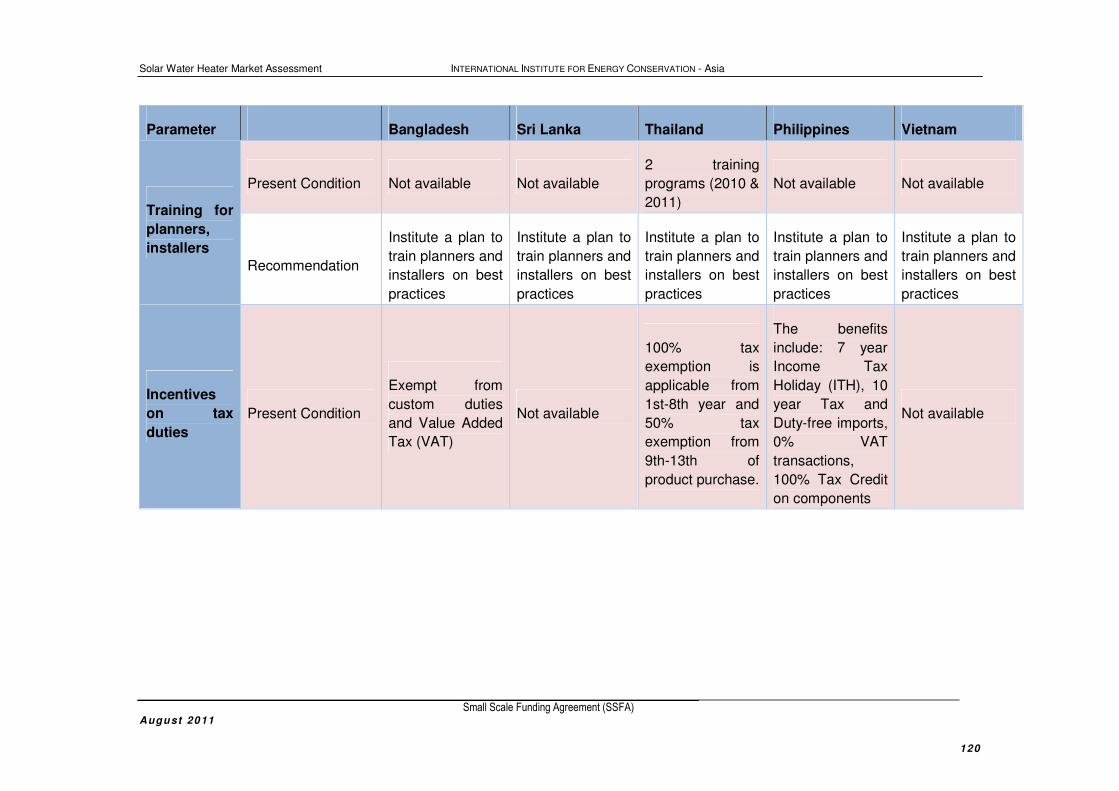

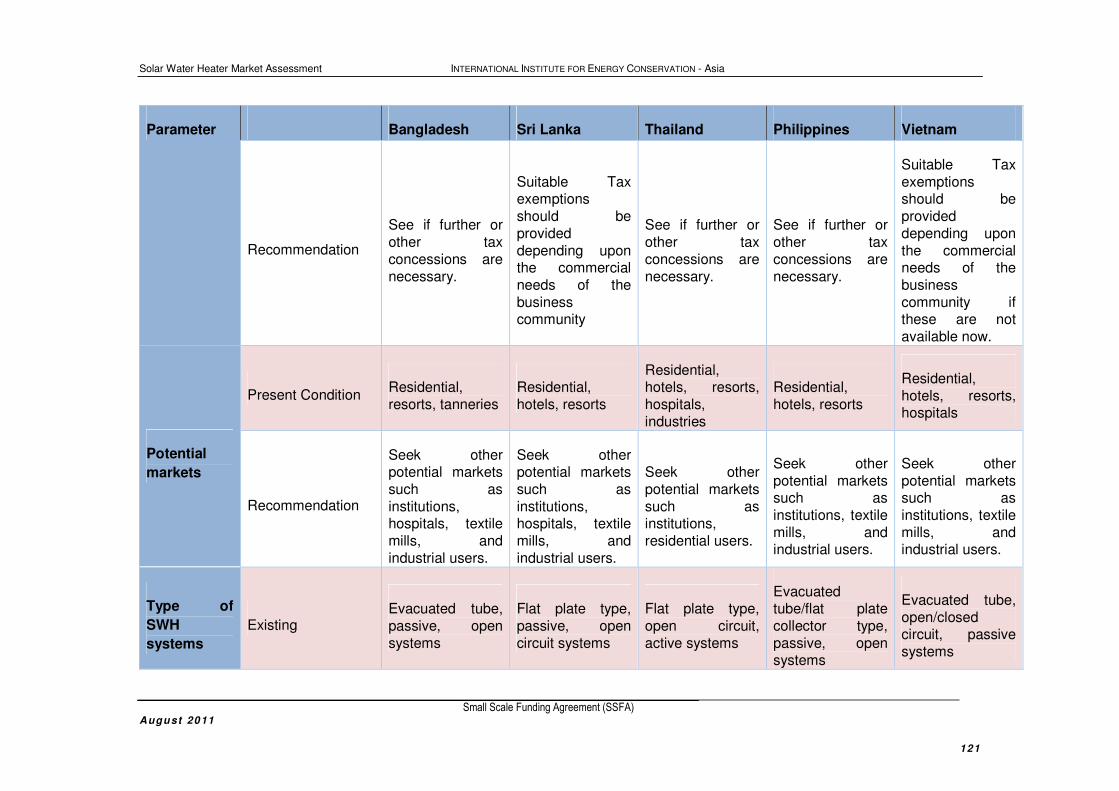

11 RECOMMENDATIONS .......................................................................................... 118

11.1 Bangladesh ..................................................................................................... 127

11.2 Sri Lanka ......................................................................................................... 127

11.3 Thailand .......................................................................................................... 128

11.4 The Philippines ................................................................................................ 129

11.5 Vietnam ........................................................................................................... 130

ANNEXURE I ...................................................................................................................... 131

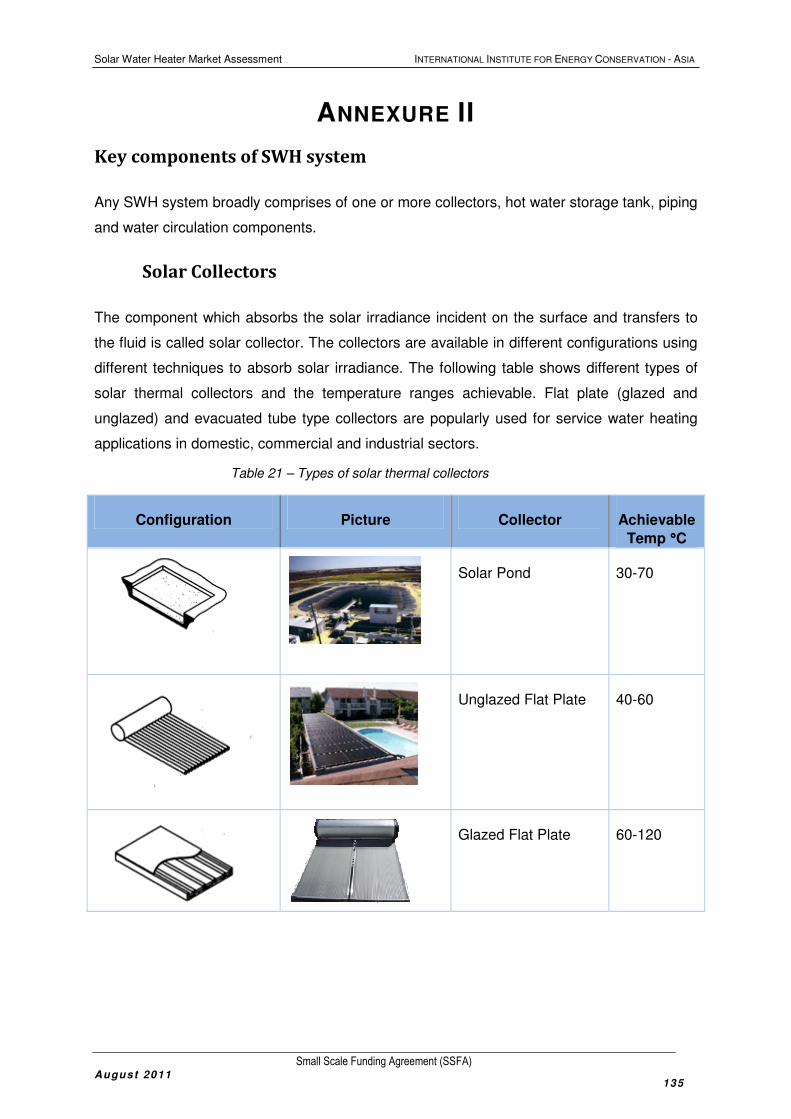

ANNEXURE II ..................................................................................................................... 135

ANNEXURE III .................................................................................................................... 149

ANNEXURE IV .................................................................................................................... 150

ANNEXURE V ..................................................................................................................... 156

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011

4

ABBREVIATIONS

ADB Asian Development Bank

AIT Asian Institute of Technology

ANEC Affiliated Non-Conventional Energy Centre

ANSI American National Standards Institute

APEC Asia-Pacific Economic Cooperation

ASEAN Association of Southeast Asian Nations

ASQC American Society for Quality Control

AST Asian Institute of Technology

BCSIR Bangladesh Council of Scientific and Industrial Research

BIMSTEC Bay of Bengal Initiative for Multi Sectorial Technical and Economic

Cooperation

BPDB Bangladesh Power Development Board

BPS Bureau of Product Standards

BRAC Bangladesh Rural Advancement Committee

BSTI Bangladesh Standards and Testing Institute

BUET Bangladesh University of Engineering and Technology

CAGR Compounded Annual Growth Rate

CEB Ceylon Electricity Board

CFL Compact Fluorescent Lamp

CIA Central Intelligence Agency

CMES Centre for Mass Education in Science

CMU Chiang Mai University

CUET Chittagong University of Engineering and Technology

DEDE Department of Alternative Energy Development and Efficiency

DEDP Department of Energy Development and Promotion

DLC Direct Load Control

DoE Department of Energy

DOST Department of Science and Technology

DSM Demand Side Management

DU Dhaka University

EAS East Asia Summit

ECC Energy Conservation Centre

EE Energy Efficiency

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011

5

EGAT Electricity Generating Authority of Thailand

ESCO Energy Service Companies

ETC Evacuated Tube Collector

EU-SPF European Union – Small Project Facility

EVN Electricity of Vietnam

FPC Flat Plate Collector

FTL Fluorescent Tube Lamp

GEF Global Environment Facility

GHG Green House Gas

GI Galvanized Iron

GoB Government of Bangladesh

GTZ German Technical Corporation

HCMC Ho Chi Minh City

IEA International Energy Agency

IFRD Institute of Fuel Research & Development

IIEC International Institute for Energy Conservation

IMF International Monetary Fund

IPCC Intergovernmental Panel on Climate Change

IPP Independent Power Producers

IPSU Institution and Policy Support Unit

ISE Fraunhofer Institute for Solar Energy Systems

ISO International Standardization Organization

ITH Income Tax Holiday

JGSEE Joint Graduate School of Energy and Environment

KM Knowledge Management

KMUTT King Mongkut’s University of Technology Thonburi

KUET Khulna University of Engineering and Technology

LECO Lanka Electricity Company

LGED Local Government Engineering Department

LPG Liquefied Petroleum Gas

MoEF Ministry of Environment and Forest

MoIT Ministry of Industry and Trade

MPRMR Ministry of Power, Energy and Mineral Resources

NCED Non-Conventional Energy Division

NEP National Energy Policy

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011

6

NEPO National Energy Policy Office

NERD National Engineering Research and Development

NREB National Renewable Energy Board

NU Narasaun University

O&M Operation and Maintenance

PE Polyethylene

PNS Philippine National Standard

PVC Polyvinyl Chloride

QA Quality Assurance

R & D Research & Development

RE Renewable Energy

REAP Renewable Energy Association of the Philippines

REB Rural Electrification Board

REDA Renewable Energy Development Agency

REIN Renewable Energy Information Network

REMB Renewable Energy Management Bureau

REP Renewable Energy Policy

RERC Renewable Energy Research Centre

RET Renewable Energy Technologies

RREL Rahimafrooz Renewable Energy Limited

RUET Rajshahi University of Engineering and Technology

SAARC South Asian Association for Regional Cooperation

SEDA Sustainable Energy Development Agency

SEMP Sustainable Environmental Management Program

SERT School of Renewable Energy Technology

SGF Sustainable Guarantee Facility

SHS Solar Home Systems

SIDA Swedish International Development Cooperation Agency

SLSEA Sri Lanka Sustainable Energy Authority

SLSI Sri Lanka Standards Institute

SRE Sustainable Rural Energy

SRET School of Renewable Energy Technology

SSFA Small Scale Funding Agreement

STA Solar Thermal Association

SWERA Solar and Wind Energy Resource Assessment

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011

7

SWH Solar Water Heating

TIS Thai Industry Standard

TISI Thai Industries Standard Institute

ToU Time of Use

TSTA Thai Solar Thermal Association

UNDP United Nations Development Programme

UNEP United Nations Environment Programme

UPSL University of the Philippines Solar Laboratory

VAT Value Added Tax

VNEEP Vietnam National Energy Efficiency Program

VSQI Vietnam Standards and Quality Institution

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011

8

EXECUTIVE SUMMARY

United Nations Development Programme (UNDP) and United Nations Environment

Programme (UNEP) have initiated Global Knowledge Management (KM) and Networking

activities within framework of its global project “Solar Water Heating (SWH) Market

Transformation and Strengthening Initiative”. International Institute for Energy Conservation

(IIEC) as a regional partner to the project is committed to the development of knowledge

products and services for SWH applications in five of South Asian and Southeast Asian

counties – Bangladesh, Sri Lanka, Thailand, The Philippines and Vietnam. The SSFA

contract included developing of three reports – Solar Water Heater Market Assessment of the

five countries, SWH – Study of Country Successes, Study of SWH Product Standards in five

countries. This is a consolidated version of the three Reports.

This report also presents a detailed discussion on solar water heaters – system components,

design and installation practices in the five countries along with life cycle cost evaluation. The

successful nationwide projects/initiatives that helped in catalysing the uptake of SWH

technology in each of the countries are discussed. This was studied for the second

deliverable under the SSFA contract.

The efforts of the regional countries in adoption of product standards for solar water heaters,

third party tests, test procedures, certification of solar water heaters are discussed. It also

presents efforts of several organizations working it these countries to improve quality of

installation and hot water servicing of the installed systems. The third deliverable under the

SSFA contract also included this information.

Bangladesh

Bangladesh with close proximity to Tropic of Cancer, receives an average solar radiation

between 4 and 6.6 kWh/m2/day. Being densely populated developing country with acute

electricity access to all and energy shortage issues, solar thermal applications especially

solar water heating could be good opportunity for the country. Though the government’s

current focus is on Solar Photovoltaic, several research and academic organizations in

Bangladesh realized the potential for solar water heating applications and are striving to

promote the technology. The technology has its origins in the country since late 1990s and

local manufacturing on commercial scale has been started since 2002. To say, SWH are

costlier in Bangladesh compared to neighbouring developing countries like India and are

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011

9

more economical in residential and commercial sector to replace use of kerosene and

electricity respectively.

Promotion of SWH was one of the focus areas in Bangladesh’s Renewable Energy Plan

(2008) and financial incentives were introduced to the local manufacturers of SWH products.

However, the technology is not popularized due to lack of proper marketing & awareness

activities and documentation and dissemination of successful installations.

Sri Lanka

Sri Lanka located near to Equator, receives mean solar radiation between 4.5 kWh/m2/day

and 6 kWh/m2/day. Solar water heating applications has its origins in the country since early

1970s when few SWH systems were imported into the country and after a decade local

manufacturing was started. The SWH systems are popular in high-end residential

consumers, hotels and tourism centres. Flat plate type collector systems are well known in

the country compared to evacuated tube type.

The Government’s focus on promotion of SWH systems in Sri Lanka is less; the till-day

market development can be attributed to the research institutions and SWH manufacturers.

The Philippines

The Philippines located near to Equator, receives mean solar radiation of 5 kWh/m2/day while

variation all over the country ranges between 3 and 7 kWh/m2/day. Solar energy for water

heating applications has its origins in the country since 1989-90 with studies focusing on

SWH applicability and research related to local manufacturing, but it is only after 2001-02

SWH installations grown in number after a few local manufacturers entering into the

business. To an extent, both flat plate and evacuated tube type collectors are equally

popular. Irrespective of type of collector, the initial cost of technology is very high and

financial incentives are provided to local manufacturers in the country.

The country does not have any national policies and regulations or product standards for

promotion of SWH systems. However, tax incentives are provided to the manufacturers and

importers of the units. Exclusive promotional projects/initiatives are missing in the

Philippines.

Thailand

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011

10

Thailand lying between Equator and Tropic of cancer, receives an annual mean solar

radiation between 4.5 kWh/m2/day (winter) and 4.7 kWh/m2/day. Solar water heating

applications has its origins in the country since 1982 when the government installed few

systems for test purpose. The industry realized big growth in 1900s with as many as 12 firms

in the market and later during 1997 economic crisis many of the businesses closed down.

SWH industry regained its momentum after 2002. However, the SWH industry in Thailand is

severely hit by low quality products, improper installations and servicing with which the public

lost faith on prolonged use of the technology. The government responded to this by

introducing quality and performance standards on voluntary basis and training programs for

service providers. The SWH systems are affordable to industrial, commercial and high-end

residential customers because of high initial costs.

SWH promotional activities are on high with parallel activities by the government – training of

SWH service providers, financial incentive for integrated SWH systems. If the government’s

efforts continue along with proper marketing and awareness strategies, Thailand may

develop as a good market for SWH installations.

Vietnam

Vietnam located near to Tropic of cancer, receives an annual mean solar radiation between

3.7 kWh/m2/day and 5.9 kWh/m2/day. Solar water heating applications has its origins in the

country since early 1990s when high-end residential consumers imported SWH products

installing in their bungalows. The government started research on SWH applications in 1996

and a few systems were installed for test purpose and after 10 years, by 2006 about 3.8

million systems were installed throughout the country. The growth of SWH industry can be

attributed to combined effort of large number of imports (comparatively affordable evacuated

tube type systems) from neighbouring China, high costs of competing energy sources, the

government’s efforts through subsidy scheme, demand side management programs and

technical assistance or grants from donor agencies. SWH promotional activities are on high

with a national target to cover 1,760,000 m2 of collector area under SWH applications by

2015.

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011

11

1 INTRODUCTION

Through the 1990s and beginning of 2000, the global solar thermal market has undergone a

favourable development with a steady annual growth. At the end of 2004, a total of 141

million square meters of collector area were installed in 41 countries studied in the

International Energy Agency (IEA) Market Review for 20061, which is expected to represent

about 85-90% of the solar thermal market worldwide. By using the conversion factor of 0.7

kWth/m2, as agreed to by solar thermal experts from seven countries at a meeting in 2004,

the total installed capacity was estimated at 98.4 GWth. The annual collector yield of all solar

thermal systems in the countries studied was estimated at 58,117 GWh and the annual

avoidance of GHG emissions 25.4 million tons of CO2.

Although strong market development has been evidenced in some Global Environment

Facility (GEF) program countries, notably in China and Turkey, in many others, solar water

heating is hardly utilized despite the most favourable climatic conditions. By any standards,

the global, economically feasible potential for increased use of solar thermal applications for

hot water preparation is huge and comparable to any other form of renewable energy the

GEF has supported during its operations. As demonstrated by the experiences in China, it is

a technology that can provide cost-effective energy solutions also to the lower income part of

the population and as further demonstrated, for instance, in Cyprus, Israel and Greece, can

become a mass product leading to permanent market shift at the national level for the benefit

of both the end users and the environment. There can also be other considerations to

stimulate solar water heating. In summary, it is an economic, commercially viable and

available technology, which due to the different market barriers, however, has not reached

the market penetration rate that it could reach on simply economic grounds.

With respect to the above discussion the GEF has mandated the United Nations

Development Programme (UNDP) and United Nations Environment Programme (UNEP) to

establish a project titled “Solar Water Heating (SWH) Market Transformation and

Strengthening Initiative” at a global level. The project consists of two components as follows:

• Component 1 - Global Knowledge Management (KM) and Networking: Effective

initiation and co-ordination of the country specific support needs and improved access of

1 W., Bergmann, I. & Faninger, G., 2006. Solar Heat Worldwide - Markets and Contribution to the

Energy Supply 2004, Solar Heating & Cooling Programme (SHC), International Energy Agency

(IEA). Available at: http://www.iea.org/impagr/cip/pdf/SHCWorldwide2006.pdf [Accessed August

12, 2010].

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011

12

national experts to state of the art information, technical backstopping, training and

international experiences and lessons learnt.

• Component 2 - UNDP Country Programs: The basic conditions for the development of

a SWH market on both the supply and demand side established, conducive to the overall,

global market transformation goals of the project.

International Institute for Energy Conservation (IIEC) as a regional partner to the program is

committed to generate knowledge products and services to ensure that developmental

experiences and benefits of knowledge can be effectively disseminated to other regional

countries.

The report was prepared within the framework of “Solar Water Heating Market

Transformation and Strengthening Initiative” under UNEP’s Small Scale Funding Agreement

(SSFA). The objective of the report is to provide the existing status and overview of SWH

industry in the focused regional countries – Bangladesh, Sri Lanka, The Philippines,

Thailand, Vietnam with respect to the solar energy availability and applicability for water

heating applications, achieved or installed capacities, supply chain mechanisms,

investments, and supportive institutional and policy frameworks, solar water heaters –

system components, design and installation practices in the five countries along with life

cycle cost evaluation, in adoption of product standards for solar water heaters, third party

tests, test procedures and certification of solar water heaters.

Section 2 of the report gives a simple country overview on electricity scenario, geographic,

climate and solar radiation analysis. Section 3 presents overview of SWH market in the

countries with details such as installed capacities, supply chain mechanism, typical

investments required; Section 4 discusses SWH system components, design & installation

procedures in the five countries; Section 5 presents economic evaluation of SWH with help of

case studies; Section 6 discusses need for quality assurance of SWH systems, product

standards available, tests for fabrication, installation etc.; Section 7 discusses institutional

and policy framework for SWH (policy interventions, testing facilities and certifications

available in the five countries; Section 8 outlines SWH programs undertaken in the past or

present, marketing and financial measures that helped in the uptake of existing installations.

Section 9 gives an overview of successful programs/initiatives undertaken for promotion of

SWH in the five countries. In section 10 the barriers to the use of solar water heaters are

discussed and section 11 lists the recommendations to overcome the barriers listed in

section 10 and mentioned in other parts of this Report.

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011

13

1.1 Methodology

The analysis in this report is based on compilation of secondary data readily available from

various web sources, one-to-one communication with industry experts in the countries,

referring product standards developed by the Regional Standard Bureaus in these countries,

discussions or email exchanges with industry experts, SWH manufacturers, primary data

gathering from questionnaires sent out to SWH manufacturers, organizations endeavouring

to promote SWH and local associations through IIEC regional offices. The details and

potential sources of information are cited in respective sections of the report. The value of

this report lies in its bringing together data from many sources which is extremely difficult to

obtain. In cases where sufficient data is unavailable either in the form of secondary data or

quick primary data collection; further detailed studies are recommended and are not covered

under the current SSFA contract.

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 14

Figure 1 – Map of Bangladesh

2 OVERVIEW OF REGIONAL COUNTRIES

2.1 Bangladesh

Bangladesh, officially the People’s

Republic of Bangladesh is a South

Asian country located between 20° 34’

and 26° 38’ North latitude and 88° 01’

and 92° 41’ East longitude. The capital

city of Bangladesh is Dhaka.

Bangladesh was a part of the British

Indian province till 1947, which then

was separated and formed a part of

Pakistan called ‘East Pakistan’. It

emerged as an independent and

sovereign country in 1971, currently

practicing democratic parliamentary

government. It is bordered by India on

North, West and a part of East, Bay of

Bengal on South and Myanmar on

South-east.

Bangladesh is one of the largest deltas of the world with a total area of 147,570 km2. It is

covered with a network of rivers and canals from Ganges-Brahmaputra emptying into

Bay of Bengal. It is the seventh most populous country with population of 142 million.

Bangladesh is among the top ten densely populated countries of the world added with a

high poverty rate. Bangladesh has an agrarian economy with more than 75% of the

population living in rural areas. The country is an active participator in United Nations

(UN) activities and is also a member of the Commonwealth of Nations, South Asian

Association for Regional Cooperation (SAARC) and Bay of Bengal Initiative for Multi

Sectorial Technical and Economic Cooperation (BIMSTEC).

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 15

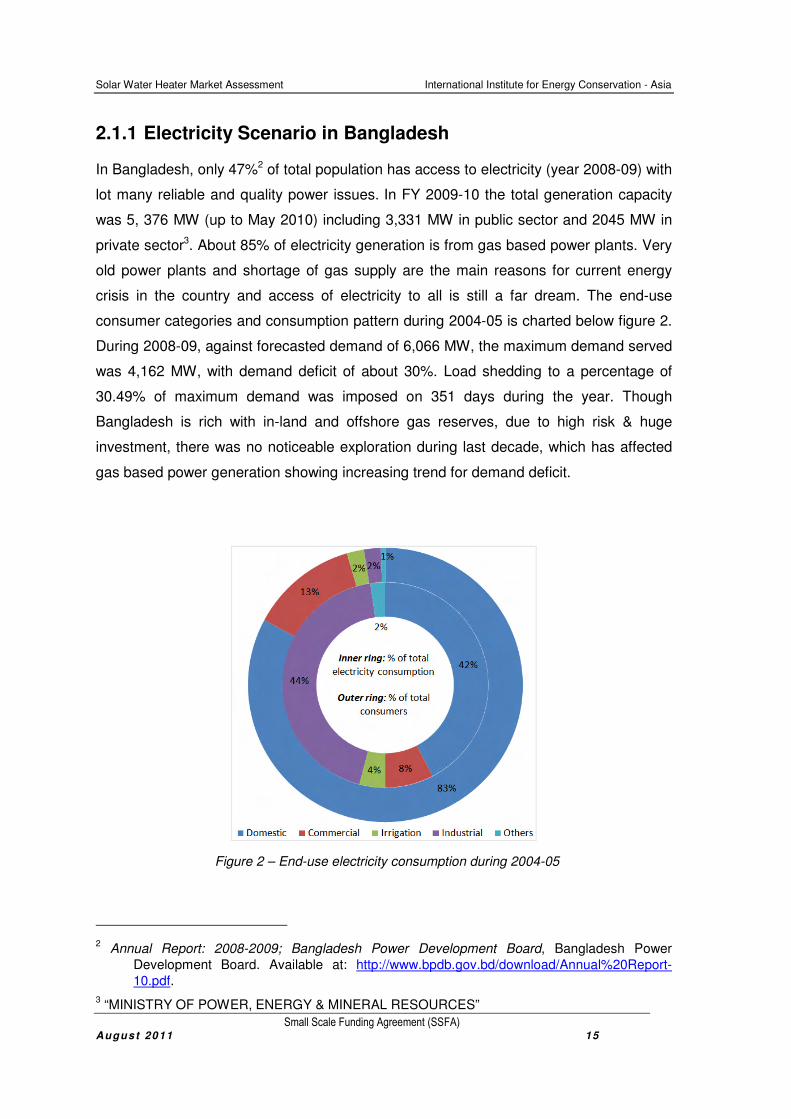

2.1.1 Electricity Scenario in Bangladesh

In Bangladesh, only 47%2 of total population has access to electricity (year 2008-09) with

lot many reliable and quality power issues. In FY 2009-10 the total generation capacity

was 5, 376 MW (up to May 2010) including 3,331 MW in public sector and 2045 MW in

private sector3. About 85% of electricity generation is from gas based power plants. Very

old power plants and shortage of gas supply are the main reasons for current energy

crisis in the country and access of electricity to all is still a far dream. The end-use

consumer categories and consumption pattern during 2004-05 is charted below figure 2.

During 2008-09, against forecasted demand of 6,066 MW, the maximum demand served

was 4,162 MW, with demand deficit of about 30%. Load shedding to a percentage of

30.49% of maximum demand was imposed on 351 days during the year. Though

Bangladesh is rich with in-land and offshore gas reserves, due to high risk & huge

investment, there was no noticeable exploration during last decade, which has affected

gas based power generation showing increasing trend for demand deficit.

2 Annual Report: 2008-2009; Bangladesh Power Development Board, Bangladesh Power

Development Board. Available at: http://www.bpdb.gov.bd/download/Annual%20Report-

10.pdf.

3 “MINISTRY OF POWER, ENERGY & MINERAL RESOURCES”

Figure 2 – End-use electricity consumption during 2004-05

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 16

Policy makers started looking at other face of demand deficit to tackle it from demand-

side by various measures such as - encouraging irrigation during off-peak hours,

enhancing consumer awareness of electricity conservation during peak hours and

undertaking a demand-side management programme that encourages the use of

energy-efficient equipment. In the last few years it was estimated that 400 MW irrigation

load was shifted from peak hour. Further initiatives include requesting industries and

commercial customers to use their own captive generation and not to operate during

peak hours, whenever possible, encouraging commercial establishments to operate only

during daylight hours and forming crisis management committees to face emergencies

and implement demand-side management measures in their area. In addition to the

above measures, time-of-day, peak and off-peak tariff rate structures are employed to all

consumer categories except agricultural and residential consumers. Off-peak

consumptions are encouraged by means of a discount in the range of 15-47% over flat-

rate tariff, whereas peak consumptions are penalized by an imposing a higher tariff in the

range of 40-95% over flat-rate tariff.

2.1.2 Bangladesh Climate

Straddling the Tropic of Cancer, Bangladesh has a subtropical monsoonal climate

characterized by heavy seasonal rainfall, moderately warm temperatures, and high

humidity. Natural calamities, such as floods, tropical cyclones, tornadoes, and tidal bores

affect the country almost every year. Historically Bangladesh is affected by major

cyclones about 16 times a decade. About 230 rivers and its tributaries cover about 8% of

Bangladesh land along with principal rivers namely Ganges, Meghna, Jamuna,

Brahmaputra, Teesta, Surma and Karnaphuli. The Intergovernmental Panel on Climate

Change's (IPCC) 2007 report estimated that a one-meter rise in the sea level due to

Global Warming could sink nearly one fifth of Bangladesh's land mass and displace 20

million people.

Three seasons are generally recognized in the country: a hot, muggy summer from

March to May; a hot, humid and rainy monsoon season from June to November; and a

warm-hot, dry winter from December to February. The relative humidity ranges from 73%

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 17

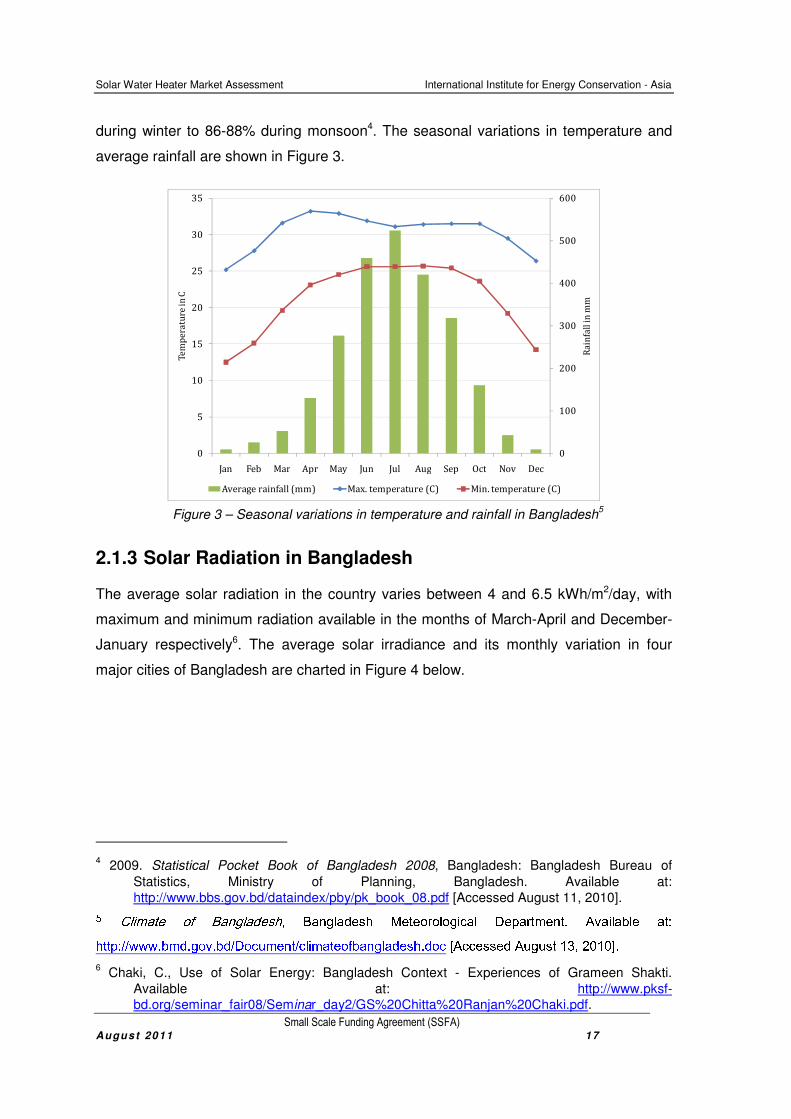

during winter to 86-88% during monsoon4. The seasonal variations in temperature and

average rainfall are shown in Figure 3.

0

100

200

300

400

500

600

0

5

10

15

20

25

30

35

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Ra

infa

ll i

n m

m

Te

mp

era

ture

in C

Average rainfall (mm) Max. temperature (C) Min. temperature (C)

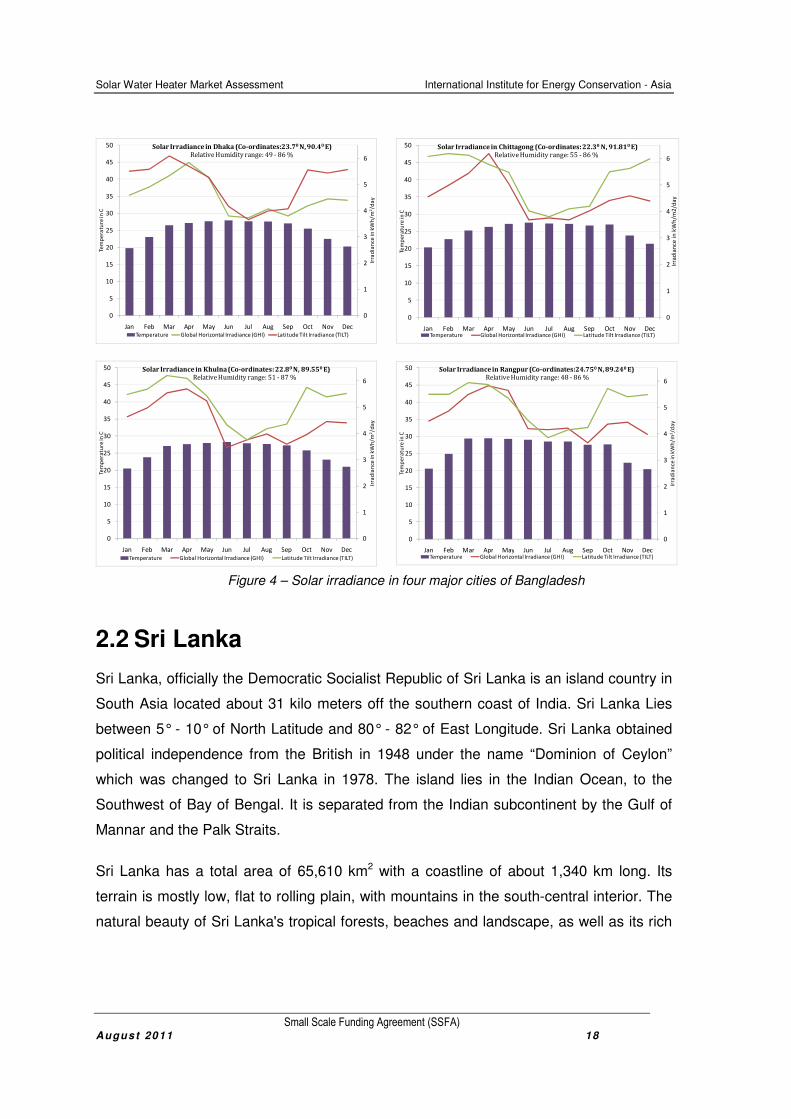

2.1.3 Solar Radiation in Bangladesh

The average solar radiation in the country varies between 4 and 6.5 kWh/m2/day, with

maximum and minimum radiation available in the months of March-April and December-

January respectively6. The average solar irradiance and its monthly variation in four

major cities of Bangladesh are charted in Figure 4 below.

4 2009. Statistical Pocket Book of Bangladesh 2008, Bangladesh: Bangladesh Bureau of

Statistics, Ministry of Planning, Bangladesh. Available at:

http://www.bbs.gov.bd/dataindex/pby/pk_book_08.pdf [Accessed August 11, 2010]. 5 Climate of Bangladesh, Bangladesh Meteorological Department. Available at: http://www.bmd.gov.bd/Document/climateofbangladesh.doc [Accessed August 13, 2010]. 6 Chaki, C., Use of Solar Energy: Bangladesh Context - Experiences of Grameen Shakti.

Available at: http://www.pksf-bd.org/seminar_fair08/Seminar_day2/GS%20Chitta%20Ranjan%20Chaki.pdf.

Figure 3 – Seasonal variations in temperature and rainfall in Bangladesh5

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 18

0

1

2

3

4

5

6

0

5

10

15

20

25

30

35

40

45

50

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Irra

dia

nce

in k

Wh

/m2/d

ay

Tem

pe

ratu

re in

C

Solar Irradiance in Dhaka (Co-ordinates:23.70 N, 90.40 E) Relative Humidity range: 49 - 86 %

Temperature Global Horizontal Irradiance (GHI) Latitude Tilt Irradiance (TILT)

0

1

2

3

4

5

6

0

5

10

15

20

25

30

35

40

45

50

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Irra

dia

nce

in

kW

h/m

2/d

ay

Tem

pe

ratu

re in

C

Solar Irradiance in Chittagong (Co-ordinates: 22.30 N, 91.810 E)Relative Humidity range: 55 - 86 %

Temperature Global Horizontal Irradiance (GHI) Latitude Tilt Irradiance (TILT)

0

1

2

3

4

5

6

0

5

10

15

20

25

30

35

40

45

50

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Irra

dia

nce

in k

Wh

/m2/d

ay

Tem

pe

ratu

re in

C

Solar Irradiance in Khulna (Co-ordinates: 22.80 N, 89.550 E) Relative Humidity range: 51 - 87 %

Temperature Global Horizontal Irradiance (GHI) Latitude Tilt Irradiance (TILT)

0

1

2

3

4

5

6

0

5

10

15

20

25

30

35

40

45

50

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Irra

dia

nce

in k

Wh

/m2/d

ay

Tem

pe

ratu

re in

C

Solar Irradiance in Rangpur (Co-ordinates:24.750 N, 89.240 E)Relative Humidity range: 48 - 86 %

Temperature Global Horizontal Irradiance (GHI) Latitude Tilt Irradiance (TILT)

2.2 Sri Lanka

Sri Lanka, officially the Democratic Socialist Republic of Sri Lanka is an island country in

South Asia located about 31 kilo meters off the southern coast of India. Sri Lanka Lies

between 5° - 10° of North Latitude and 80° - 82° of East Longitude. Sri Lanka obtained

political independence from the British in 1948 under the name “Dominion of Ceylon”

which was changed to Sri Lanka in 1978. The island lies in the Indian Ocean, to the

Southwest of Bay of Bengal. It is separated from the Indian subcontinent by the Gulf of

Mannar and the Palk Straits.

Sri Lanka has a total area of 65,610 km2 with a coastline of about 1,340 km long. Its

terrain is mostly low, flat to rolling plain, with mountains in the south-central interior. The

natural beauty of Sri Lanka's tropical forests, beaches and landscape, as well as its rich

Figure 4 – Solar irradiance in four major cities of Bangladesh

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 19

Figure 5 – Map of Sri Lanka

cultural heritage, make it a world famous tourist destination. It was ranked the fifty fifth

with a population of about 21 million by the Central Intelligence Agency7 (CIA).

Sri Lanka is a member of the Commonwealth, the South Asian Association for Regional

Cooperation (SAARC), the World Bank, International Monetary Fund (IMF), Asian

Development Bank (ADB), and the Colombo Plan.

2.2.1 Electricity Scenario in Sri Lanka

The national electrification level in Sri Lanka

is close to 80% by the end of year 2007. Grid

connected generation capacity in FY 2006-07

is 2435MW and electricity generated

amounted to 9,901 GWh. About 60% of the

generation was from oil burning thermal

power plants, close to 40% is from hydro

power and share of electricity generation from

non-conventional sources is minimal. Ceylon

Electricity Board (CEB), eight Independent

Power Producers and over fifty privately-

owned renewable energy based small power

producers are responsible for generation of

electricity in the country while CEB and Lanka

Electricity Company (LECO) jointly distribute

electricity. The annual increase in the

electricity consumption in 2007 was found to

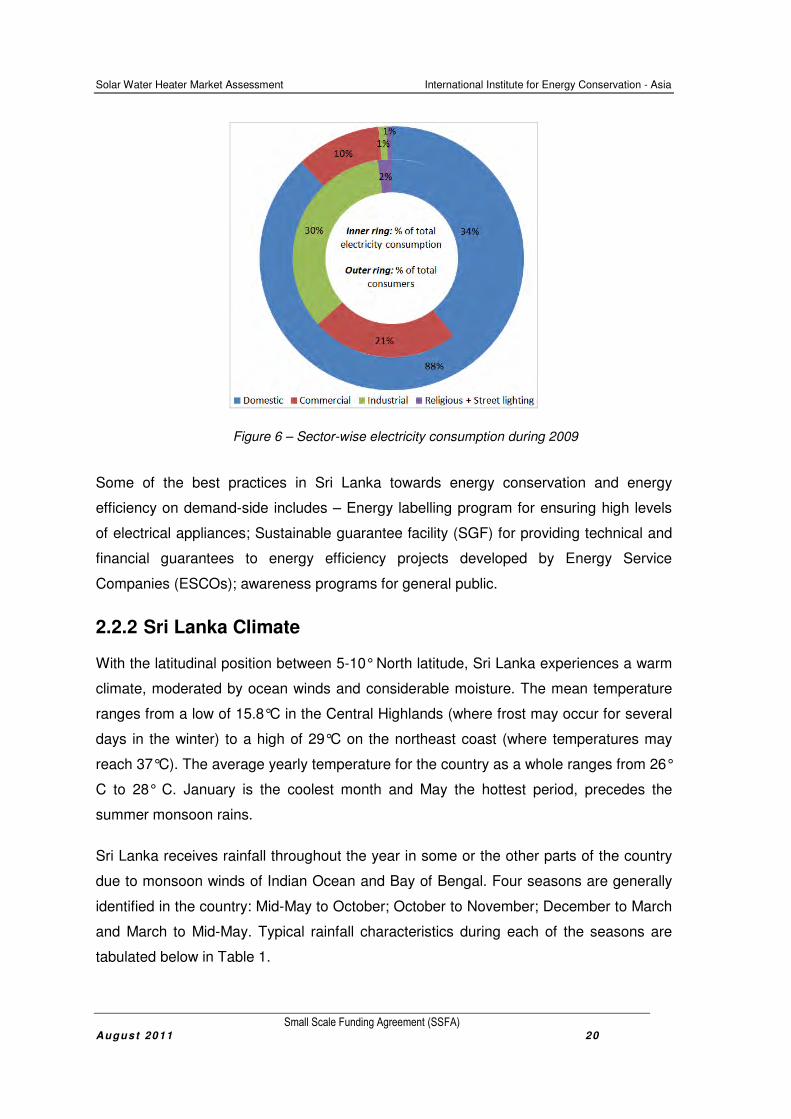

be 5% compared to 2006. The consumer profile and consumption during 2009 is charted

below figure 6. Recently, the cost of power generation has risen to unbearable

proportions mainly due to the inadequacy of water resources used for power generation

and price hike of other principal mediums of electricity generation. More use of non-

conventional energy sources (to meet about 10% of country’s total electricity generation)

and efficient use of energy have been identified as the key to counter the increase in

electricity demand and cost of power generation.

7 CIA - The World Fact book. Available at: https://www.cia.gov/library/publications/the-world-factbook/geos/ce.html [Accessed August 20, 2010].

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 20

Some of the best practices in Sri Lanka towards energy conservation and energy

efficiency on demand-side includes – Energy labelling program for ensuring high levels

of electrical appliances; Sustainable guarantee facility (SGF) for providing technical and

financial guarantees to energy efficiency projects developed by Energy Service

Companies (ESCOs); awareness programs for general public.

2.2.2 Sri Lanka Climate

With the latitudinal position between 5-10° North latitude, Sri Lanka experiences a warm

climate, moderated by ocean winds and considerable moisture. The mean temperature

ranges from a low of 15.8°C in the Central Highlands (where frost may occur for several

days in the winter) to a high of 29°C on the northeast coast (where temperatures may

reach 37°C). The average yearly temperature for the country as a whole ranges from 26°

C to 28° C. January is the coolest month and May the hottest period, precedes the

summer monsoon rains.

Sri Lanka receives rainfall throughout the year in some or the other parts of the country

due to monsoon winds of Indian Ocean and Bay of Bengal. Four seasons are generally

identified in the country: Mid-May to October; October to November; December to March

and March to Mid-May. Typical rainfall characteristics during each of the seasons are

tabulated below in Table 1.

Figure 6 – Sector-wise electricity consumption during 2009

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 21

Season Characteristics Rainfall receiving areas

Mid-May to

October

Winds from Southwest brings moisture

from the Indian Ocean

• Mountain slopes of

Central Highlands

• Southwest region

October to

November

Periodic violent winds and tropical

cyclones

• Southwest

• Northeast

• Eastern

December to

March

Winds from Northeast brings moisture

from the Bay of Bengal

• North-eastern slopes of

mountains

March to Mid-

May

Variable winds • Evening thundershowers

in the island

Relative humidity is typically higher in the southwest and mountainous areas and also

depends on the seasonal patterns of rainfall. The average annual relative humidity of the

country is 79.8% and average monthly relative humidity ranges from 75% in January to

83% in October.

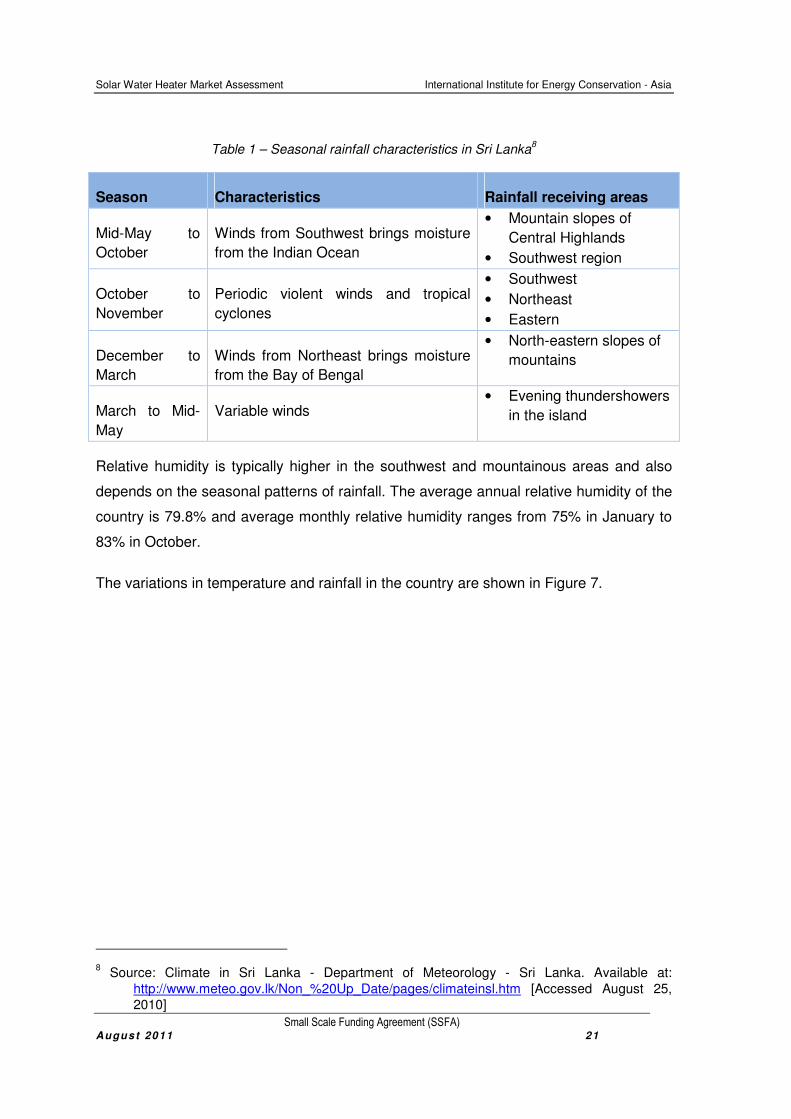

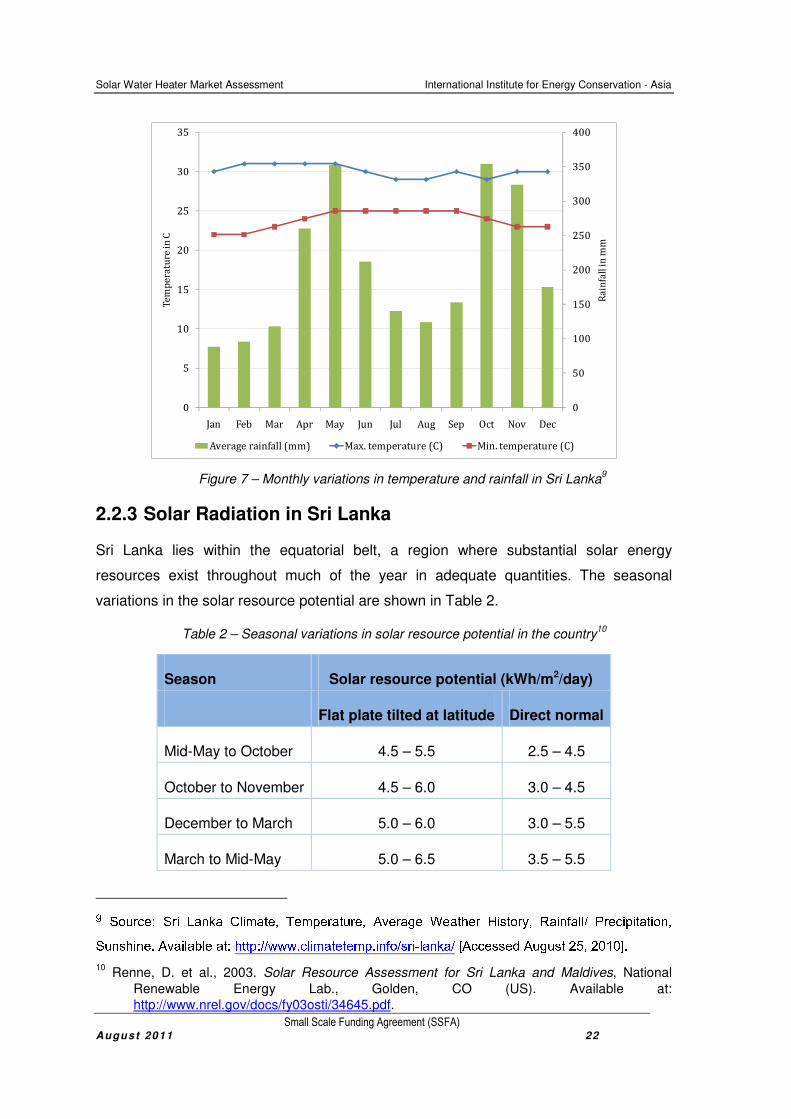

The variations in temperature and rainfall in the country are shown in Figure 7.

8 Source: Climate in Sri Lanka - Department of Meteorology - Sri Lanka. Available at:

http://www.meteo.gov.lk/Non_%20Up_Date/pages/climateinsl.htm [Accessed August 25,

2010]

Table 1 – Seasonal rainfall characteristics in Sri Lanka8

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 22

0

50

100

150

200

250

300

350

400

0

5

10

15

20

25

30

35

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Ra

infa

ll i

n m

m

Te

mp

era

ture

in C

Average rainfall (mm) Max. temperature (C) Min. temperature (C)

2.2.3 Solar Radiation in Sri Lanka

Sri Lanka lies within the equatorial belt, a region where substantial solar energy

resources exist throughout much of the year in adequate quantities. The seasonal

variations in the solar resource potential are shown in Table 2.

Season Solar resource potential (kWh/m2/day)

Flat plate tilted at latitude Direct normal

Mid-May to October 4.5 – 5.5 2.5 – 4.5

October to November 4.5 – 6.0 3.0 – 4.5

December to March 5.0 – 6.0 3.0 – 5.5

March to Mid-May 5.0 – 6.5 3.5 – 5.5

9 Source: Sri Lanka Climate, Temperature, Average Weather History, Rainfall/ Precipitation, Sunshine. Available at: http://www.climatetemp.info/sri-lanka/ [Accessed August 25, 2010]. 10

Renne, D. et al., 2003. Solar Resource Assessment for Sri Lanka and Maldives, National

Renewable Energy Lab., Golden, CO (US). Available at:

http://www.nrel.gov/docs/fy03osti/34645.pdf.

Figure 7 – Monthly variations in temperature and rainfall in Sri Lanka9

Table 2 – Seasonal variations in solar resource potential in the country10

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 23

From the above table, the average annual solar resource potential of the country ranges

from 4.5 to 6 kWh/m2/day for flat plate type collectors tilted at latitude. The highest

resources are in the northern and southern regions, and the lowest resources are in the

interior hill country. The seasonal variations in solar resources are location specific

based on the change in wind flow directions and storm patterns between the southwest

and the northeast monsoons. During the southwest monsoon (Mid-May to October), with

airflow generally from the southwest to the northeast, the lee side of the mountains (the

northeast portion of the country) shows quite high solar resources. During the northeast

monsoon (December to March), the southern and western portions of the country show

higher resources. However, the highest resources occur during the hot dry period from

March and April when the transition between the northeast and the southwest monsoon

occurs.

2.3 Thailand

Thailand, officially the Kingdom of Thailand is a country in the heart of Southeast Asia,

well known for its record as ‘the only Southeast Asian country that has never been

colonized’. Thailand lies between 5.6° and 20.44° North Latitude and 97.36° and 105.63°

East Longitude. The country is bordered to the North by Myanmar and Laos, to the East

by Laos and Cambodia, to the West by the Andaman Sea and Myanmar and to the

South by the Gulf of Thailand and Malaysia.

Thailand has a total area of 513,000 km2 with a coastline of about 3,219 km long. The

country’s geographical terrain is very distinct, with mountainous ranges towards the

North, plateau region towards Northeast and flat river valley in the centre of the country.

It was ranked the twentieth most populous country in the world by the Central

Intelligence Agency11 (CIA) with a population of about 65 million.

Thailand fully participates and is a member of several international and regional

organizations. It is an active member of the Association of South East Asian Nations

(ASEAN).

11 CIA - The World Fact book. Available at: https://www.cia.gov/library/publications/the-world-factbook/geos/th.html [Accessed September 2, 2010].

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 24

2.3.1 Electricity Scenario in Thailand

As of December 2008, the total installed capacity in the country is 29,140 MW,

comprising about 49% from Electricity Generating Authority of Thailand’s (EGAT) power

plants, 48.8% from domestic private power producers

(IPPs) and small portion of 2.2% from neighbouring

country power purchases. About 73% of the electricity is

generated from oil and gas based power plants, 21%

from coal based power plants and about 6% from

renewable energy technologies.

2.3.2 Thailand Climate

Thailand experiences a tropical climate, characterized by

considerable monsoon. The average temperature for the

country is 28°C with April (35°C) and January (20°C)

being the hottest and coldest month in a year.

Thailand receives an average of 1492 mm of rainfall per

year mainly during two seasons: a rainy, warm and

cloudy Southwest monsoon from mid-May to September;

a dry, cool Northeast monsoon from November to mid-

March.

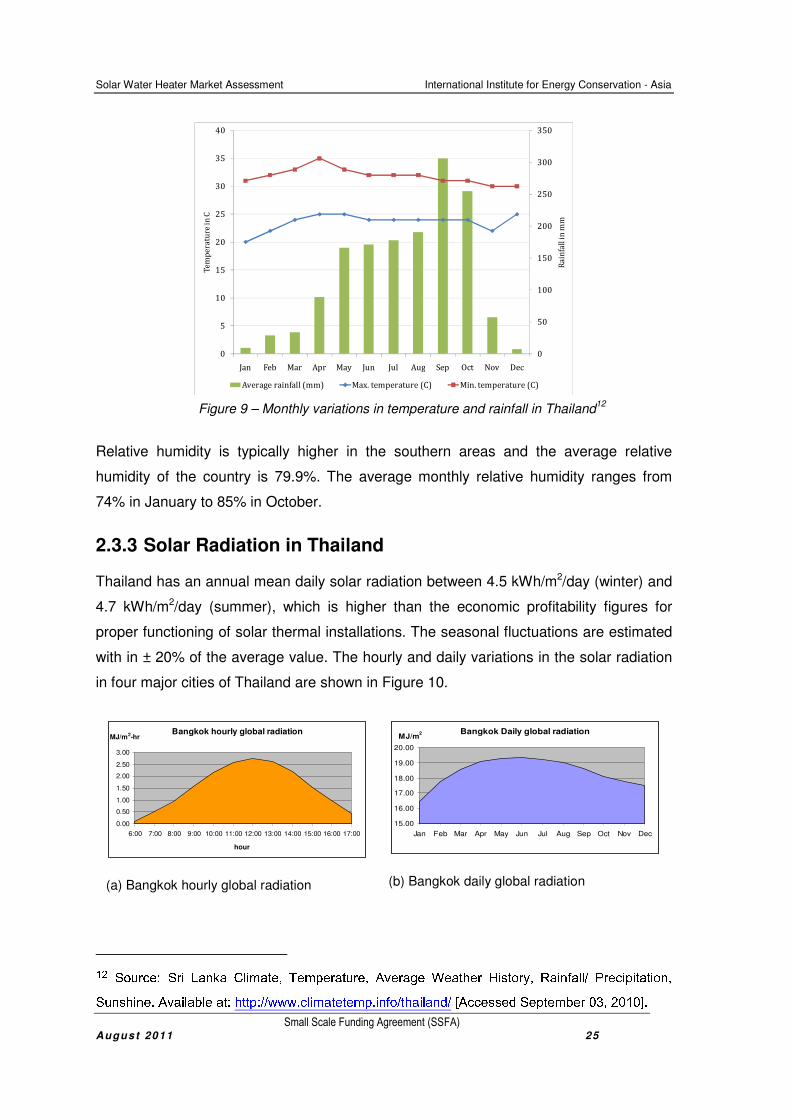

The monthly variations in temperature and rainfall in the

country are shown in Figure 9.

Figure 8 – Map of Thailand

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 25

0

50

100

150

200

250

300

350

0

5

10

15

20

25

30

35

40

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Ra

infa

ll i

n m

m

Te

mp

era

ture

in

C

Average rainfall (mm) Max. temperature (C) Min. temperature (C)

Relative humidity is typically higher in the southern areas and the average relative

humidity of the country is 79.9%. The average monthly relative humidity ranges from

74% in January to 85% in October.

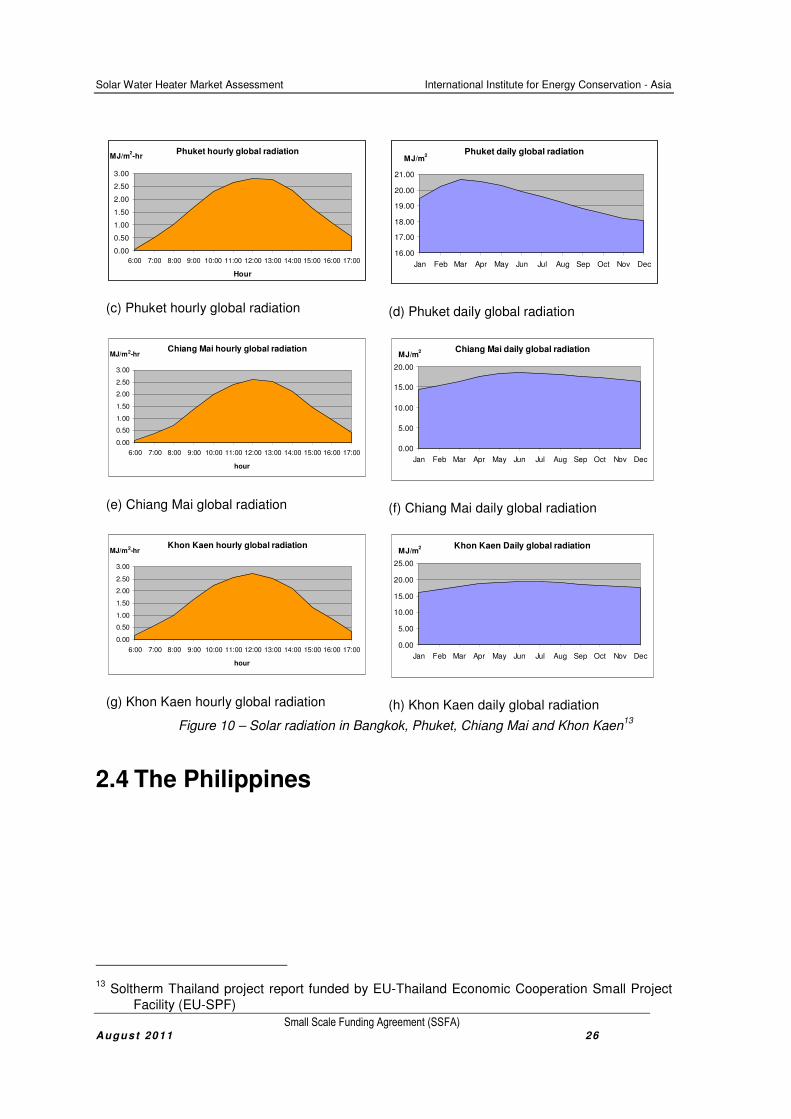

2.3.3 Solar Radiation in Thailand

Thailand has an annual mean daily solar radiation between 4.5 kWh/m2/day (winter) and

4.7 kWh/m2/day (summer), which is higher than the economic profitability figures for

proper functioning of solar thermal installations. The seasonal fluctuations are estimated

with in ± 20% of the average value. The hourly and daily variations in the solar radiation

in four major cities of Thailand are shown in Figure 10.

Bangkok hourly global radiation

0.00

0.50

1.00

1.50

2.00

2.50

3.00

6:00 7:00 8:00 9:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00 17:00

hour

MJ/m2-hr

(a) Bangkok hourly global radiation

Bangkok Daily global radiation

15.00

16.00

17.00

18.00

19.00

20.00

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MJ/m2

(b) Bangkok daily global radiation

12 Source: Sri Lanka Climate, Temperature, Average Weather History, Rainfall/ Precipitation, Sunshine. Available at: http://www.climatetemp.info/thailand/ [Accessed September 03, 2010].

Figure 9 – Monthly variations in temperature and rainfall in Thailand12

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 26

Phuket hourly global radiation

0.00

0.50

1.00

1.50

2.00

2.50

3.00

6:00 7:00 8:00 9:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00 17:00

Hour

MJ/m2-hr

(c) Phuket hourly global radiation

Phuket daily global radiation

16.00

17.00

18.00

19.00

20.00

21.00

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MJ/m2

(d) Phuket daily global radiation

Chiang Mai hourly global radiation

0.00

0.50

1.00

1.50

2.00

2.50

3.00

6:00 7:00 8:00 9:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00 17:00

hour

MJ/m2-hr

(e) Chiang Mai global radiation

Chiang Mai daily global radiation

0.00

5.00

10.00

15.00

20.00

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MJ/m2

(f) Chiang Mai daily global radiation

Khon Kaen hourly global radiation

0.00

0.50

1.00

1.50

2.00

2.50

3.00

6:00 7:00 8:00 9:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00 17:00

hour

MJ/m2-hr

(g) Khon Kaen hourly global radiation

Khon Kaen Daily global radiation

0.00

5.00

10.00

15.00

20.00

25.00

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MJ/m2

(h) Khon Kaen daily global radiation

2.4 The Philippines

13 Soltherm Thailand project report funded by EU-Thailand Economic Cooperation Small Project

Facility (EU-SPF)

Figure 10 – Solar radiation in Bangkok, Phuket, Chiang Mai and Khon Kaen13

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 27

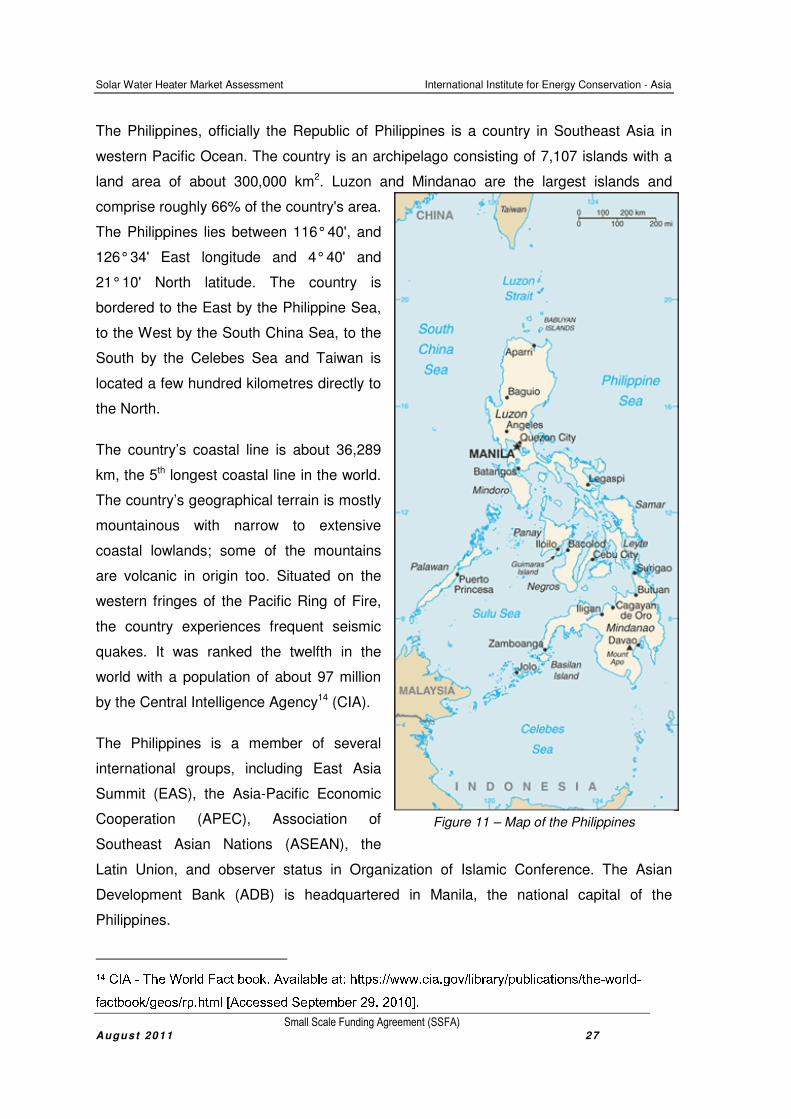

Figure 11 – Map of the Philippines

The Philippines, officially the Republic of Philippines is a country in Southeast Asia in

western Pacific Ocean. The country is an archipelago consisting of 7,107 islands with a

land area of about 300,000 km2. Luzon and Mindanao are the largest islands and

comprise roughly 66% of the country's area.

The Philippines lies between 116° 40', and

126° 34' East longitude and 4° 40' and

21° 10' North latitude. The country is

bordered to the East by the Philippine Sea,

to the West by the South China Sea, to the

South by the Celebes Sea and Taiwan is

located a few hundred kilometres directly to

the North.

The country’s coastal line is about 36,289

km, the 5th longest coastal line in the world.

The country’s geographical terrain is mostly

mountainous with narrow to extensive

coastal lowlands; some of the mountains

are volcanic in origin too. Situated on the

western fringes of the Pacific Ring of Fire,

the country experiences frequent seismic

quakes. It was ranked the twelfth in the

world with a population of about 97 million

by the Central Intelligence Agency14 (CIA).

The Philippines is a member of several

international groups, including East Asia

Summit (EAS), the Asia-Pacific Economic

Cooperation (APEC), Association of

Southeast Asian Nations (ASEAN), the

Latin Union, and observer status in Organization of Islamic Conference. The Asian

Development Bank (ADB) is headquartered in Manila, the national capital of the

Philippines.

14 CIA - The World Fact book. Available at: https://www.cia.gov/library/publications/the-world-factbook/geos/rp.html [Accessed September 29, 2010].

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 28

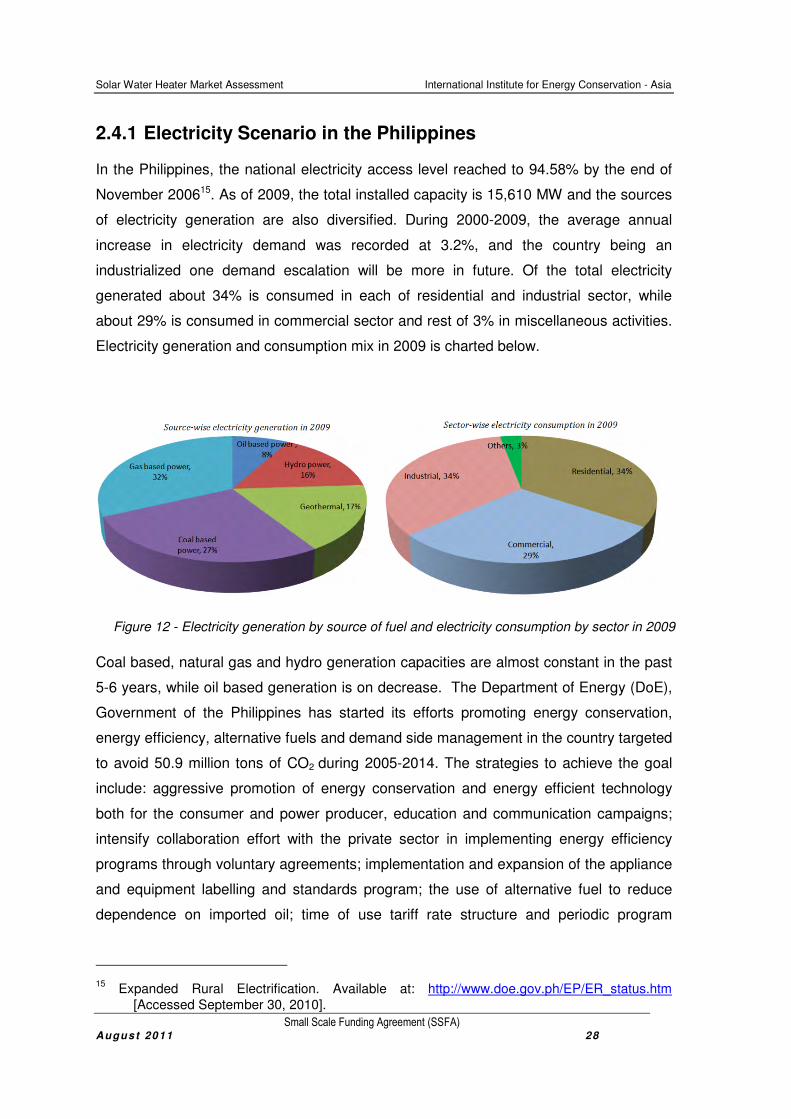

2.4.1 Electricity Scenario in the Philippines

In the Philippines, the national electricity access level reached to 94.58% by the end of

November 200615. As of 2009, the total installed capacity is 15,610 MW and the sources

of electricity generation are also diversified. During 2000-2009, the average annual

increase in electricity demand was recorded at 3.2%, and the country being an

industrialized one demand escalation will be more in future. Of the total electricity

generated about 34% is consumed in each of residential and industrial sector, while

about 29% is consumed in commercial sector and rest of 3% in miscellaneous activities.

Electricity generation and consumption mix in 2009 is charted below.

Coal based, natural gas and hydro generation capacities are almost constant in the past

5-6 years, while oil based generation is on decrease. The Department of Energy (DoE),

Government of the Philippines has started its efforts promoting energy conservation,

energy efficiency, alternative fuels and demand side management in the country targeted

to avoid 50.9 million tons of CO2 during 2005-2014. The strategies to achieve the goal

include: aggressive promotion of energy conservation and energy efficient technology

both for the consumer and power producer, education and communication campaigns;

intensify collaboration effort with the private sector in implementing energy efficiency

programs through voluntary agreements; implementation and expansion of the appliance

and equipment labelling and standards program; the use of alternative fuel to reduce

dependence on imported oil; time of use tariff rate structure and periodic program

15 Expanded Rural Electrification. Available at: http://www.doe.gov.ph/EP/ER_status.htm

[Accessed September 30, 2010].

Figure 12 - Electricity generation by source of fuel and electricity consumption by sector in 2009

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 29

monitoring and evaluation to assess the effectiveness of the energy efficiency and

conservation plan.

2.4.2 Philippines Climate

The Philippines has a tropical maritime climate and is usually hot and humid. The two

seasons in a year are identified as: dry season or summer (cool dry: December to

February & hot dry: March to May); rainy season (from June to November). Most of the

rainfall is experienced during the southwest monsoon (from June to November), and a

little during the northeast monsoon characterized by dry winds (from December to April).

The average temperature for the country is 27.7° C with May (34°C) and January &

February (22°C) being the hottest and coldest months in a year. The country receives an

average of 2061 mm of rainfall per year.

The variations in temperature and rainfall in the country are shown in Figure 13.

0

50

100

150

200

250

300

350

400

450

500

0

5

10

15

20

25

30

35

40

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Ra

infa

ll i

n m

m

Te

mp

era

ture

in C

Average rainfall (mm) Max. temperature (C) Min. temperature (C)

The elevations above sea level have significant effect on the temperature and relative

humidity. The average monthly relative humidity ranges from 64% in April to 82% in

August-September.

16 Source: Sri Lanka Climate, Temperature, Average Weather History, Rainfall/ Precipitation, Sunshine. Available at: http://www.climatetemp.info/philippines/ [Accessed September 30, 2010].

Figure 13 – Monthly variations in temperature and rainfall in the Philippines16

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 30

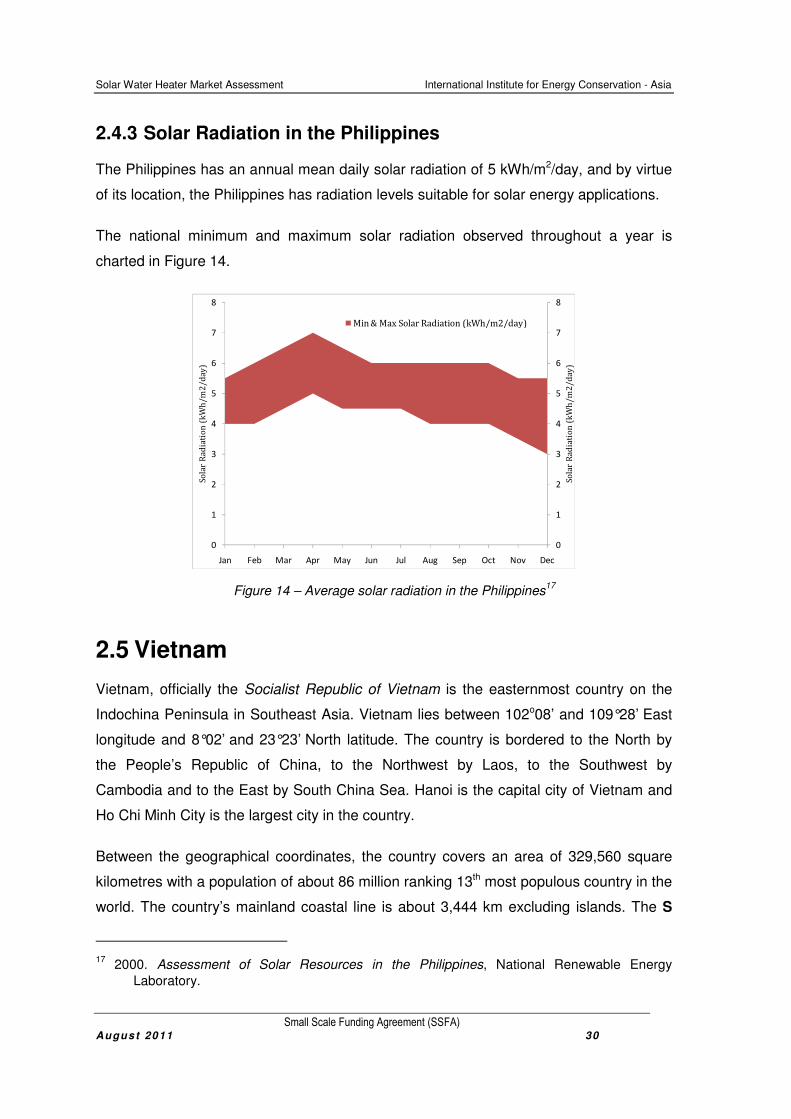

2.4.3 Solar Radiation in the Philippines

The Philippines has an annual mean daily solar radiation of 5 kWh/m2/day, and by virtue

of its location, the Philippines has radiation levels suitable for solar energy applications.

The national minimum and maximum solar radiation observed throughout a year is

charted in Figure 14.

0

1

2

3

4

5

6

7

8

0

1

2

3

4

5

6

7

8

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecS

ola

r R

ad

iati

on

(k

Wh

/m

2/

da

y)

So

lar

Ra

dia

tio

n (

kW

h/

m2

/d

ay

)

Min & Max Solar Radiation (kWh/m2/day)

2.5 Vietnam

Vietnam, officially the Socialist Republic of Vietnam is the easternmost country on the

Indochina Peninsula in Southeast Asia. Vietnam lies between 102o08’ and 109°28’ East

longitude and 8°02’ and 23°23’ North latitude. The country is bordered to the North by

the People’s Republic of China, to the Northwest by Laos, to the Southwest by

Cambodia and to the East by South China Sea. Hanoi is the capital city of Vietnam and

Ho Chi Minh City is the largest city in the country.

Between the geographical coordinates, the country covers an area of 329,560 square

kilometres with a population of about 86 million ranking 13th most populous country in the

world. The country’s mainland coastal line is about 3,444 km excluding islands. The S

17

2000. Assessment of Solar Resources in the Philippines, National Renewable Energy

Laboratory.

Figure 14 – Average solar radiation in the Philippines17

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 31

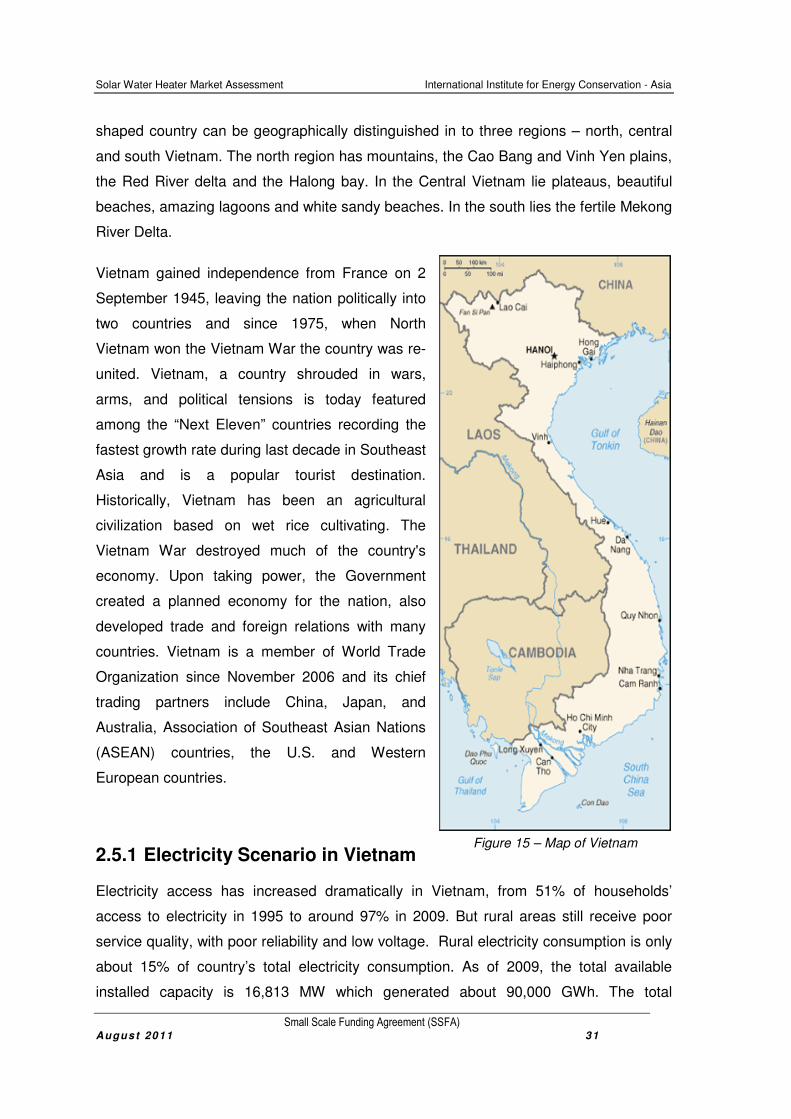

Figure 15 – Map of Vietnam

shaped country can be geographically distinguished in to three regions – north, central

and south Vietnam. The north region has mountains, the Cao Bang and Vinh Yen plains,

the Red River delta and the Halong bay. In the Central Vietnam lie plateaus, beautiful

beaches, amazing lagoons and white sandy beaches. In the south lies the fertile Mekong

River Delta.

Vietnam gained independence from France on 2

September 1945, leaving the nation politically into

two countries and since 1975, when North

Vietnam won the Vietnam War the country was re-

united. Vietnam, a country shrouded in wars,

arms, and political tensions is today featured

among the “Next Eleven” countries recording the

fastest growth rate during last decade in Southeast

Asia and is a popular tourist destination.

Historically, Vietnam has been an agricultural

civilization based on wet rice cultivating. The

Vietnam War destroyed much of the country's

economy. Upon taking power, the Government

created a planned economy for the nation, also

developed trade and foreign relations with many

countries. Vietnam is a member of World Trade

Organization since November 2006 and its chief

trading partners include China, Japan, and

Australia, Association of Southeast Asian Nations

(ASEAN) countries, the U.S. and Western

European countries.

2.5.1 Electricity Scenario in Vietnam

Electricity access has increased dramatically in Vietnam, from 51% of households’

access to electricity in 1995 to around 97% in 2009. But rural areas still receive poor

service quality, with poor reliability and low voltage. Rural electricity consumption is only

about 15% of country’s total electricity consumption. As of 2009, the total available

installed capacity is 16,813 MW which generated about 90,000 GWh. The total

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 32

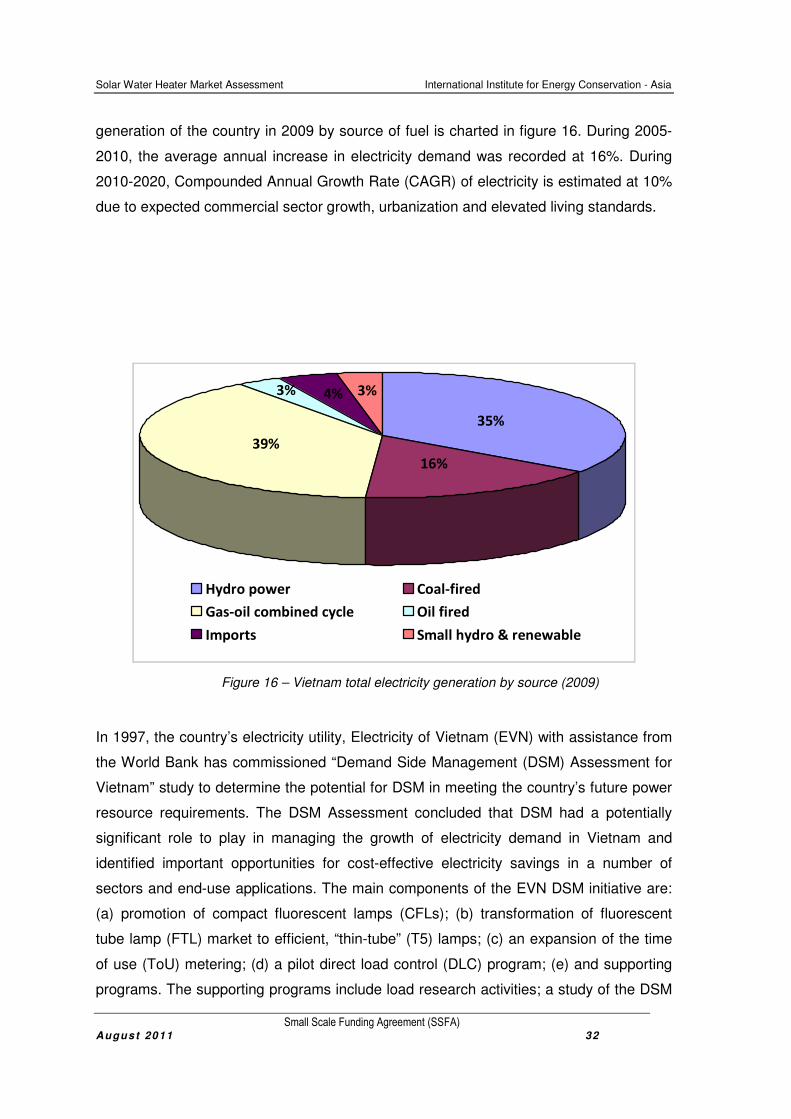

generation of the country in 2009 by source of fuel is charted in figure 16. During 2005-

2010, the average annual increase in electricity demand was recorded at 16%. During

2010-2020, Compounded Annual Growth Rate (CAGR) of electricity is estimated at 10%

due to expected commercial sector growth, urbanization and elevated living standards.

35%

16%

39%

3%4%3%

Hydro power Coal-fired

Gas-oil combined cycle Oil fired

Imports Small hydro & renewable

In 1997, the country’s electricity utility, Electricity of Vietnam (EVN) with assistance from

the World Bank has commissioned “Demand Side Management (DSM) Assessment for

Vietnam” study to determine the potential for DSM in meeting the country’s future power

resource requirements. The DSM Assessment concluded that DSM had a potentially

significant role to play in managing the growth of electricity demand in Vietnam and

identified important opportunities for cost-effective electricity savings in a number of

sectors and end-use applications. The main components of the EVN DSM initiative are:

(a) promotion of compact fluorescent lamps (CFLs); (b) transformation of fluorescent

tube lamp (FTL) market to efficient, “thin-tube” (T5) lamps; (c) an expansion of the time

of use (ToU) metering; (d) a pilot direct load control (DLC) program; (e) and supporting

programs. The supporting programs include load research activities; a study of the DSM

Figure 16 – Vietnam total electricity generation by source (2009)

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 33

regulatory framework and business opportunities; DSM screening and implementation of

pilot programs; and a consultancy on program monitoring & evaluation.

2.5.2 Vietnam Climate

Vietnam's climate is as complex as its topography. Although the country lies entirely

within the tropics, its diverse range of latitude, altitude, and weather patterns produces

enormous climatic variation. North Vietnam (resembling China) has two basic seasons: a

cold, humid winter (from November to April); and a warm, wet summer (for rest of the

year). In this region, summer temperatures average around 22°C, with occasional

typhoons. South Vietnam is generally warm, the hottest months being March through

May (temperatures around 30°C). This is the dry season in the south, followed by the

April-October monsoon season. In Central Vietnam, provinces towards North share

climate of North Vietnam and climate of provinces that are towards south have climate

resembling to South Vietnam. The average temperature for the country is 24.1° C with

June & July (33°C) and January (13°C) being the hottest and coldest months in a year.

The country receives an average of 1680 mm of rainfall per year.

The variations in temperature and rainfall in the country are shown in Figure 17.

0

50

100

150

200

250

300

350

400

0

5

10

15

20

25

30

35

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Ra

infa

ll i

n m

m

Te

mp

era

ture

in C

Average rainfall (mm) Max. temperature (C) Min. temperature (C)

Solar Water Heater Market Assessment International Institute for Energy Conservation - Asia

Small Scale Funding Agreement (SSFA) August 2011 34

Vietnam receives tropical and subtropical monsoon type rain. The relative humidity is

high throughout the year in most parts of the country, the average annual relative

humidity being 71.1% and average monthly relative humidity ranging from 67% in

December to 76% in March.

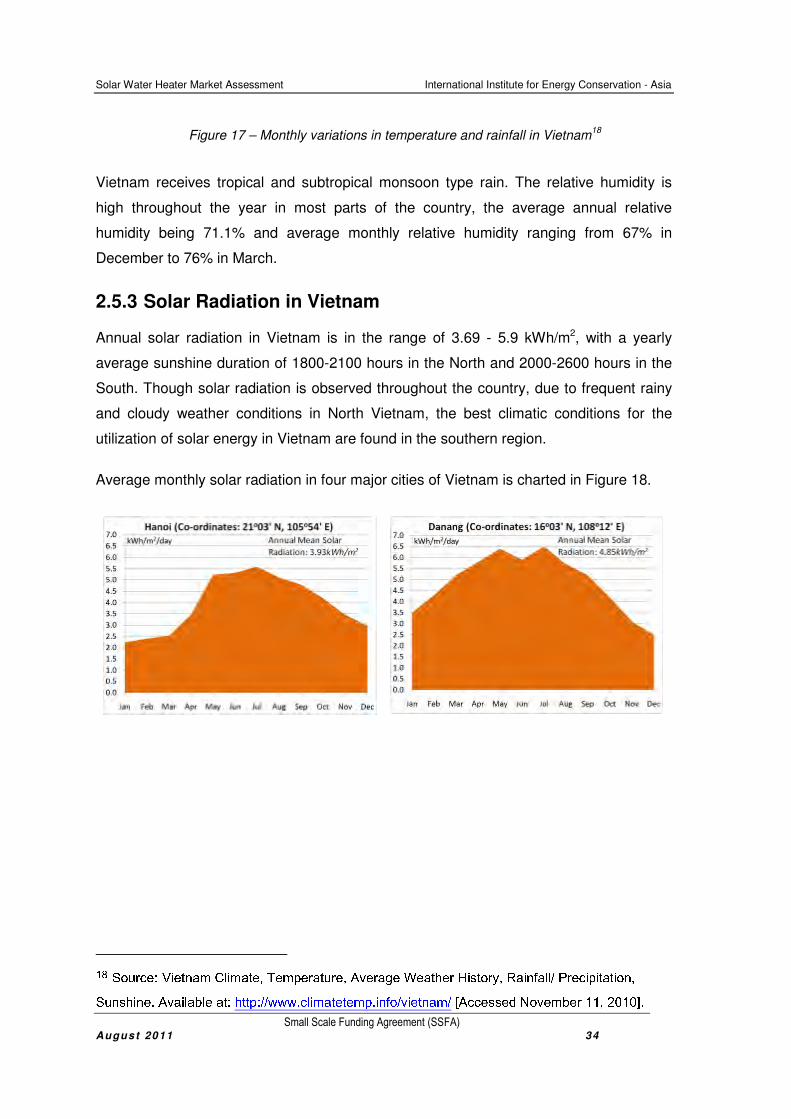

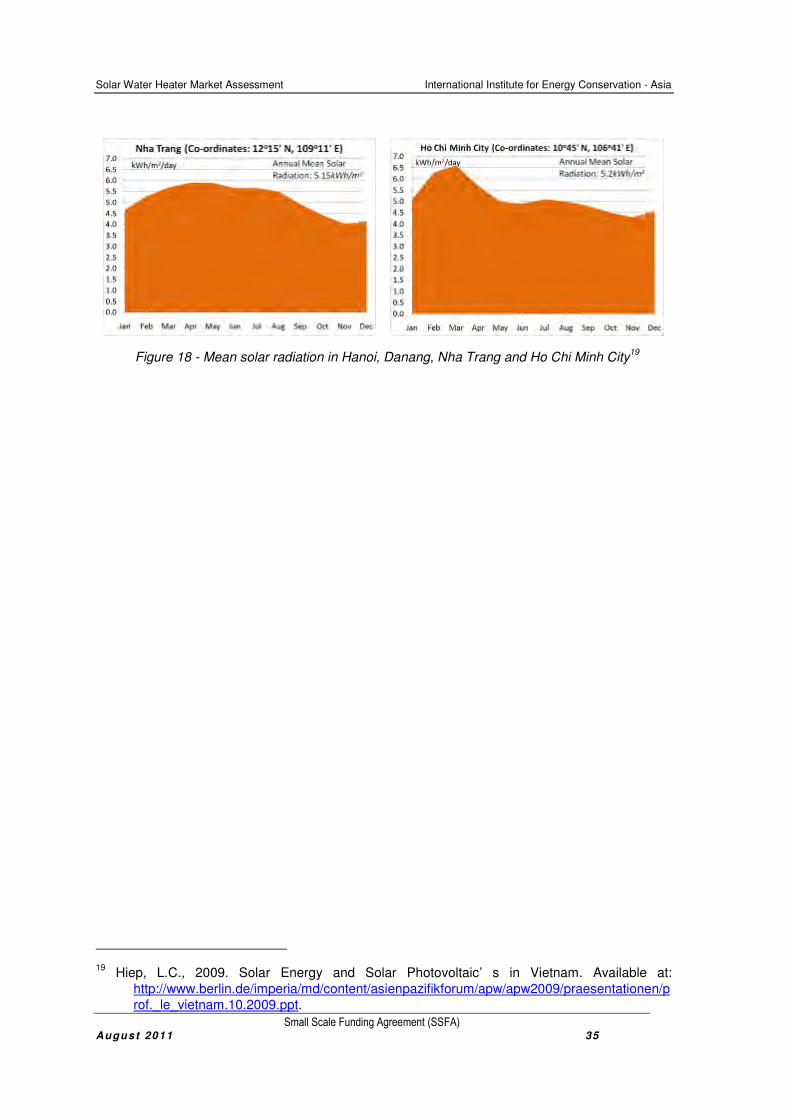

2.5.3 Solar Radiation in Vietnam

Annual solar radiation in Vietnam is in the range of 3.69 - 5.9 kWh/m2, with a yearly

average sunshine duration of 1800-2100 hours in the North and 2000-2600 hours in the

South. Though solar radiation is observed throughout the country, due to frequent rainy

and cloudy weather conditions in North Vietnam, the best climatic conditions for the

utilization of solar energy in Vietnam are found in the southern region.