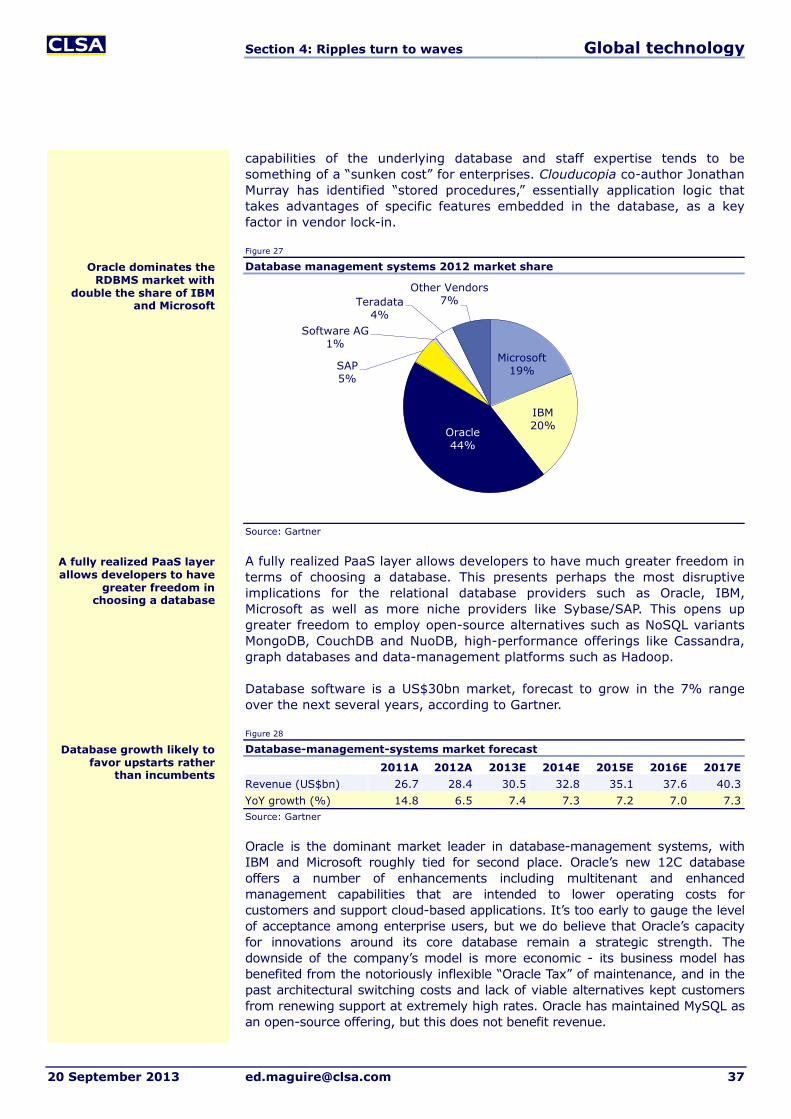

Soft machines - Cloud computing and the software ascendancy - Ed Maguire

144

Soft machines Cloud computing and the software ascendancy Special report September 2013

-

Upload

edward-maguire -

Category

Software

-

view

290 -

download

4

Transcript of Soft machines - Cloud computing and the software ascendancy - Ed Maguire

Soft machines Cloud computing and the software ascendancy

Special report

September 2013

Global technology

2 [email protected] 20 September 2013

Contents Executive summary .......................................................................... 3

Vaporizing IT .................................................................................... 4

PaaS - Key to the hybrid cloud .........................................................13

The cloud as an economic catalyst ...................................................22

Ripples turn to waves ......................................................................33

Company profiles

Akamai ..................................... 57

Amazon ..................................... 61

Delta ........................................ 67

EMC .......................................... 69

Google ...................................... 73

IBM .......................................... 77

Intel ......................................... 83

Microsoft ................................... 87

Oracle ....................................... 93

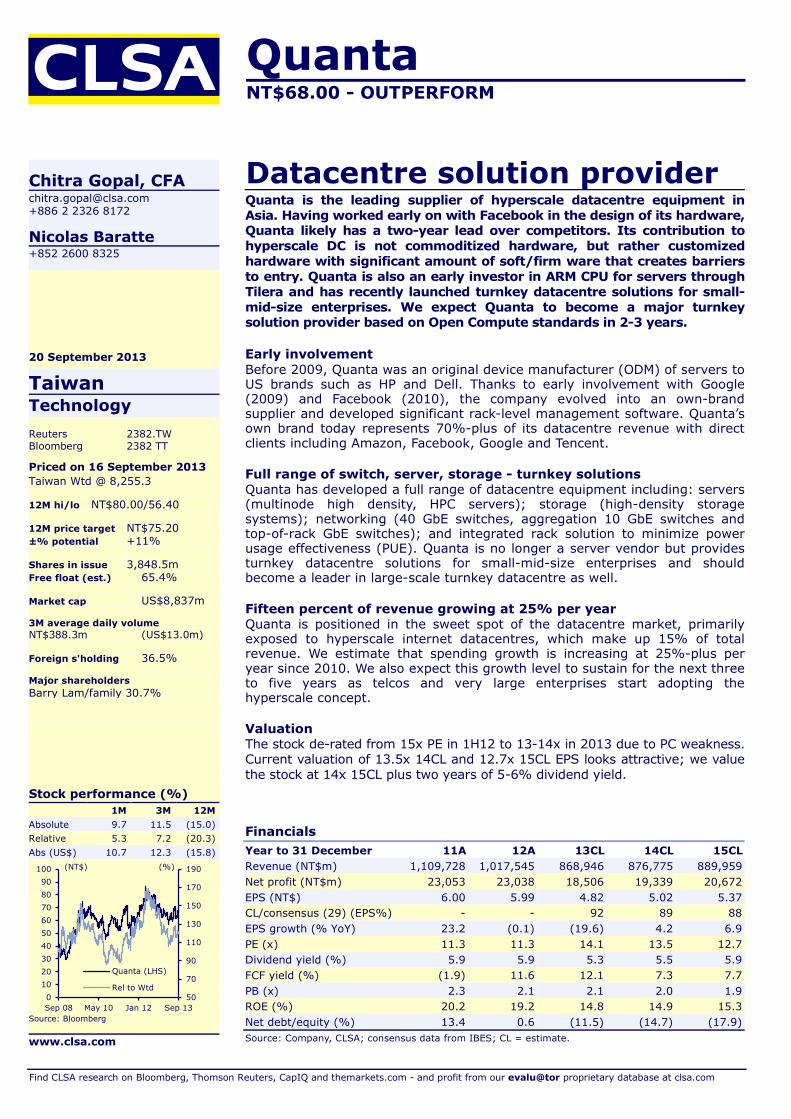

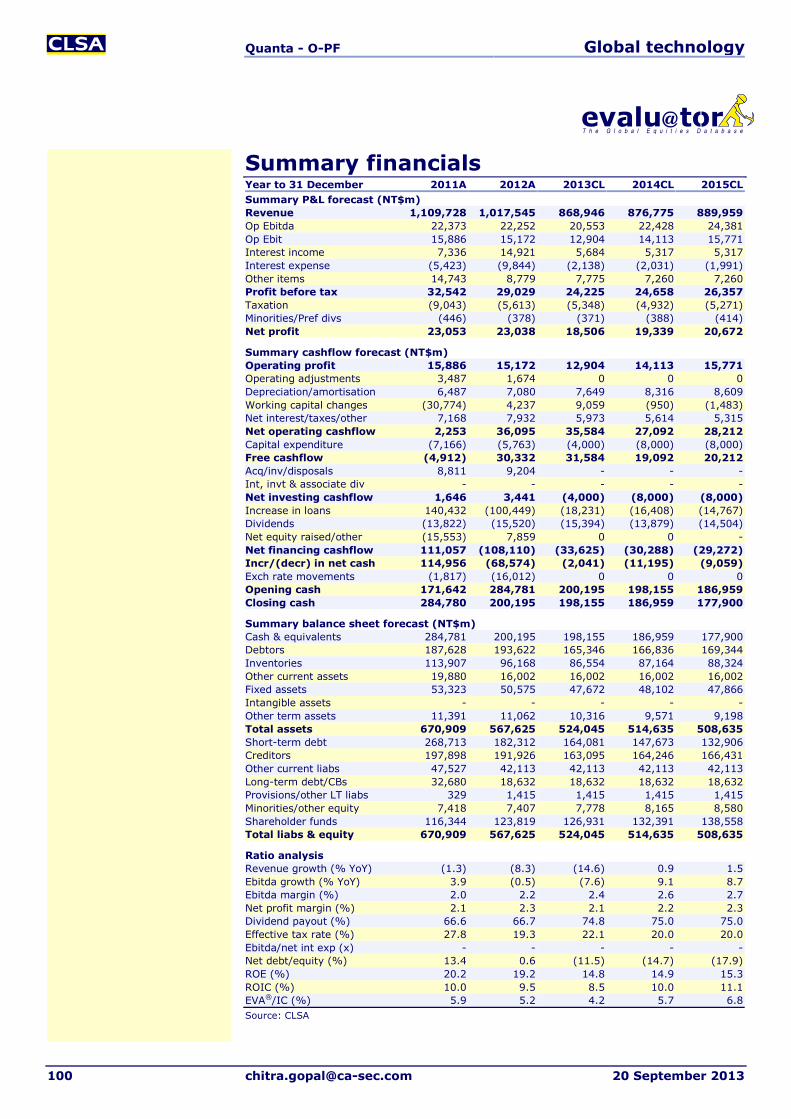

Quanta ...................................... 99

Rackspace ............................... 101

Salesforce.com ......................... 105

Tata Consultancy ...................... 111

PC OEMs ................................. 115

Appendices 1: What it’s all about ......................................................................... 117 2: The software cloudscape ................................................................ 126

All prices quoted herein are as at close of business 16 September 2013, unless otherwise stated

Read Nic Baratte’s companion report Hard rain: Cloud computing and the hardware demise

CLSA technology incites new perspectives

Produced by CLSA Americas, LLC. For important disclosures please refer to page 140

Ed Maguire [email protected] +1 212 549 8200

With contributions from Avi Silver, CLSA Americas Chitra Gopal, CLSA James Lee, CLSA Americas Lou Miscioscia, CLSA Americas Nicolas Baratte, CLSA Nimish Joshi, CLSA Srini Pajjuri, CLSA Americas

Executive summary Global technology

20 September 2013 [email protected] 3

Soft machines The soft machines of cloud computing transform the technology landscape, economic models and strategies. The Platform-as-a-Service (PaaS) architecture will play a key role in unlocking applications from the components of infrastructure, which is subject to the forces of commoditization. As cloud computing disrupts the entrenched IT leaders, new innovations power emerging economic benefits. Open-source and services models exacerbate competitive pressures for infrastructure software and hardware vendors. We see value accruing towards Software as a Service (SaaS) and solutions. Salesforce.com, Akamai and Microsoft are our top picks.

Cloud computing changes IT from a bespoke to utility model. Commoditization of IT will accelerate demand and innovation. Adoption has passed the inflection and signs point to the hybrid public/private cloud as the preferred approach. As a wave of new social, mobile and analytic applications emerges, custom software development becomes a key competitive weapon.

The PaaS market is far smaller than SaaS and Infrastructure as a Service (IaaS), but size vastly understates its strategic consequence. PaaS promises code portability, the ability to swap out infrastructure components as a commodity. Microsoft, Pivotal, Google and Salesforce.com lead this highly fragmented landscape. We expect consolidation of smaller vendors to accelerate mainstream adoption.

Cloud computing alters the economic calculus of information technology via transition from products to services, from capex to opex. Quantifying ROI is elusive, as lower costs spur elastic demand. The broader benefits of cloud computing translate into innovation, net job creation and economic growth.

Cloud architecture amplifies competitive threats to middleware, database, operating-system and hardware vendors from open-source and service-delivery models. Storage should do better than networking, which should do better than servers (see Nicolas Baratte’s Hard rain report, which explores the shrinking hardware profit pool). IT services will see value churn as IaaS commoditizes outsourcing and automation displaces people-intensive tasks. As value accrues towards SaaS and solutions, our top cloud picks are Salesforce.com, Akamai and Microsoft. We also like cloud-service providers Amazon and Google, while Rackspace appears at risk. EMC is a cloud-infrastructure beneficiary, whereas HP, VMware, Oracle and Intel look vulnerable. Share performance across the software sector reflects this bifurcation of value creation.

Comparable valuations

(Local currency) Ticker Rating Analyst Curr Target Last close

EPS FY13

EPS FY14

PE (x) FY13

PE (x) FY14

Upside (%)

Akamai AKAM US BUY1 Ed Maguire US$ 66.0 51.37 1.96 2.32 26.3 22.3 28.5 Amazon AMZN US O-PF1 James Lee US$ 325.0 296.06 3.83 6.02 77.3 49.2 9.8 EMC EMC US O-PF1 Louis Miscioscia, CFA US$ 30.0 26.88 1.87 2.20 14.3 12.2 11.6 Google GOOG US BUY1 James Lee US$ 1,075.0 887.76 43.87 54.49 20.2 16.3 21.1 Hewlett Packard HPQ US U-PF1 Avi Silver US$ 23.0 21.74 3.55 3.40 6.1 6.4 5.8 IBM IBM US O-PF1 Ed Maguire US$ 225.0 193.15 16.57 18.72 11.7 10.3 16.5 Intel INTC US U-PF1 Srini Pajjuri US$ 22.5 23.39 1.89 1.82 12.4 12.9 (3.8) Microsoft MSFT US O-PF1 Ed Maguire US$ 38.0 32.79 2.58 2.72 12.7 12.1 15.9 Oracle ORCL US U-PF1 Ed Maguire US$ 35.0 32.97 2.68 2.88 12.3 11.5 6.2 Rackspace RAX US SELL1 Louis Miscioscia, CFA US$ 40.0 52.26 0.69 0.85 75.2 61.7 (23.5) Salesforce.com CRM US BUY1 Ed Maguire US$ 64.0 49.65 0.41 0.34 122.6 147.7 28.9 Delta 2308 TT O-PF2 Chitra Gopal, CFA NT$ 157.5 135.00 7.07 8.16 19.1 16.5 16.7 Quanta 2382 TT O-PF2 Chitra Gopal, CFA NT$ 75.2 68.00 4.82 5.02 14.1 13.5 10.6 Tata Consultancy TCS IB O-PF2 Nimish Joshi Rs 2,200.0 1,902.55 71.23 92.47 27.3 21.1 15.7 1Covered by CLSA Americas, 2CLSA. Source: CLSA Americas, CLSA

Cloud computing and the software ascendancy

Vaporizing IT: Commoditization

accelerates innovation

PaaS is a small but important catalyst for

technological disruption

Cloud as a net-positive economic catalyst

Ripples turn to waves

Nicolas Baratte’s Hard rain report

Section 1: Vaporizing IT Global technology

4 [email protected] 20 September 2013

Vaporizing IT Cloud computing is more than an architectural shift, it’s a massive wave with profound implications for strategies, business models and the technology landscape. A new architecture decouples applications from infrastructure, providing increased agility and immense scalability at declining cost. As these factors lower barriers to accelerate innovation in social business, mobile and analytics (Big Data) use cases, the corporate view of technology shifts from operating expense to strategic asset. Consequently, we expect aggregate IT spending to continue to grow while share of wallet moves away from a bespoke infrastructure towards applications and solutions that generate business value.

Cloud computing represents the transition of information technology to a utility model. A new architecture is emerging that lowers costs and stimulates innovation. Business adoption has hit an inflection point as the preferred deployment model evolves towards the hybrid cloud, embracing both the public and private clouds. As infrastructure becomes commoditized, value migrates upwards to applications as custom development gains increasing strategic importance.

Cloud computing commoditizes technology infrastructure “from the bottom up”. It’s increasingly difficult for proprietary hardware, storage, networking and software vendors to charge premium “rents” in the face of software-defined automation and open-source alternatives.

Declining costs will grow IT spending in aggregate. The Jevons Paradox refers to the proposition that technology advancements that improve the efficiency of resource usage will raise (rather than reduce) the rate of consumption of that resource. We believe this applies to cloud computing.

Adoption of cloud architecture accelerates “creative destruction”. Incumbent vendors face existential threats from disruptive models: alternative delivery approaches (everything as a service); economics (pay as you go/subscription); architecture (PaaS); and development and intellectual-property (IP) paradigms (open source).

Infrastructure becomes a commodity game. Providers of cloud compute infrastructure (compute, storage and networking) will compete on economies of scale and supply-chain efficiencies.

It’s all about business value. Value migrates upwards from platform to applications as infrastructure components become automated. When infrastructure is a commodity, a greater proportion of the value comes from solving business problems. Apps rule the day through specialized knowledge, domain expertise and process automation.

What’s old is new again . . . really new In recent years, cloud computing has been the subject of massive hype and speculation; however, the impact of this shift is profound for the technology sector and economic activity overall. In 2013, cloud computing is being broadly embraced by the mainstream.

There are many aspects of the cloud delivery model that are a natural reiteration of prior computing models such as the time-sharing and resource-pooling characteristic of the mainframe era. However, it is the combination of declining costs, open standards, easy availability, increasingly powerful

Cloud computing industrializes technology

as applications are engines of business value

The mainstream is embracing cloud

computing

Cloud computing is a massive wave with

profound implications

Section 1: Vaporizing IT Global technology

20 September 2013 [email protected] 5

development and management technologies, and above all, the enormous expansion of connected devices that accelerate the transformative impact on the technology landscape, industries of all types and the economy at large.

Commoditization of infrastructure is moving up the stack as technologies and cloud architecture mature. The first cloud wave of public IaaS adoption disrupted the server-hardware market. The adoption of maturing PaaS solutions will further commoditize infrastructure software, particularly application servers and related middleware.

A new cloud software architecture causes a shift away from the enterprise IT economic model built around tightly coupled systems, proprietary software & hardware and extensive IT implementation, development, monitoring and support services towards a more open model built for massive scale. It emphasizes commodity hardware, open-source software and more automated processes.

The decoupling of apps from the underlying infrastructure alters competitive dynamics as advantages for vendors of cloud-infrastructure components are derived from economies of scale and efficient delivery models.

Cloud computing also enables the decoupling of business processes from the underlying technology stack, with profound ramifications for companies across industries. Those businesses that are most able to harness the cloud economic model in their favor will prosper, while those that fail to adapt to disruption will struggle. A key capability is code portability - the ability to run applications on public or private clouds with minimal changes.

Cloud computing alters usage and consumption of IT resources by transforming the enterprise technology model from dedicated “silos” to a sharing architecture. The term cloud computing encompasses more than public infrastructure services providers. Cloud computing also refers to an emerging management model for organizing computing resources. This has implications for the vendors that provide the various components of infrastructure as well, not just their technologies but also their business models.

Like all major technology transitions, cloud computing gives rise to winners and losers, although it’s still early days. Beneficiaries include internet/ecommerce vendors, tech startups, application software companies, consumers and forward-thinking businesses across industries. At risk are incumbent vendors of enterprise hardware, infrastructure software, IT implementation and support services and businesses subject to competitive or secular disruption.

The cloud industrializes computing to a utility model The IT industry is undergoing a process of industrialization around cloud-computing architecture, as the cloud model allows resources to be easily provisioned and paid for on a per-use model. We have previously discussed why cloud computing matters and some of the key aspects of what is becoming arguably the most significant paradigm shift in technology since the introduction of the worldwide web. The benefits of cloud delivery models are helping organizations of all sizes scale their investments, enjoy increased flexibility and spur innovation.

Simon Wardley, researcher at Computer Sciences Corporation’s (CSC) Leading Edge Forum, developed a model that illustrates how activities in new markets evolved due to competition on both the demand (user) and supply (vendor)

IT industry is undergoing a process of

industrialization around cloud computing

Transforming the enterprise tech model

from dedicated silos to a sharing architecture

Moving towards a more open model built for

massive scale

Cloud computing gives rise to winners and losers

Section 1: Vaporizing IT Global technology

6 [email protected] 20 September 2013

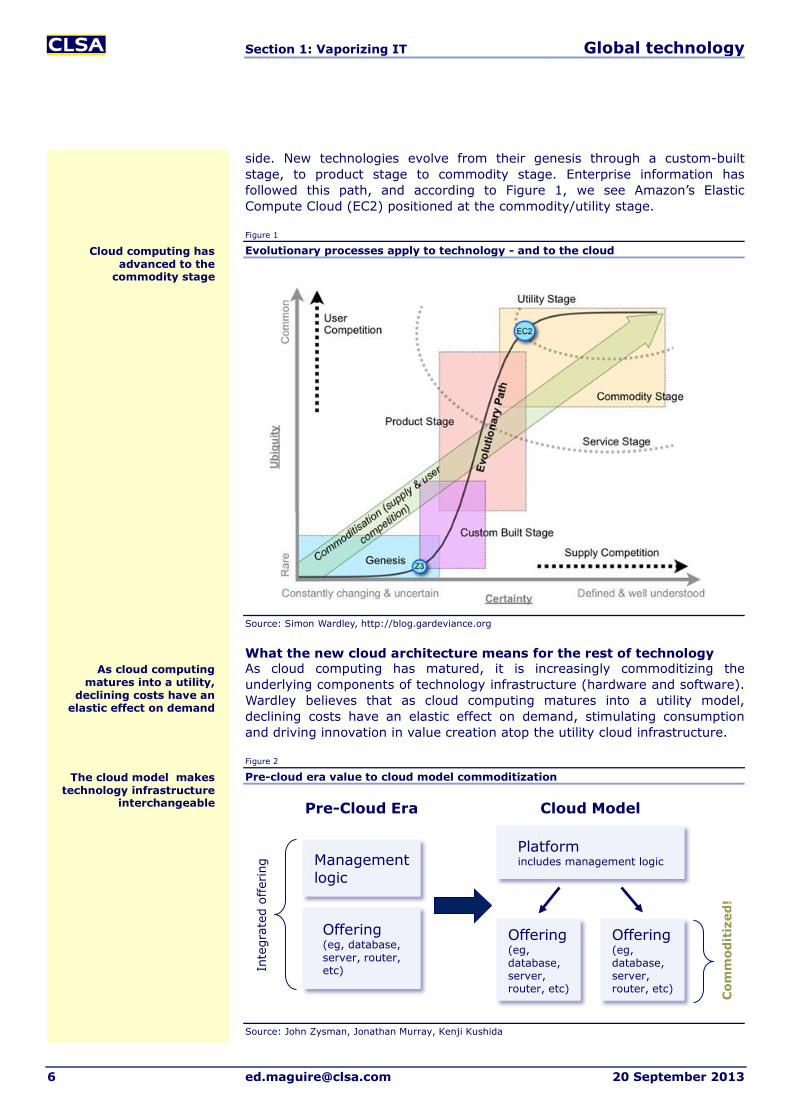

side. New technologies evolve from their genesis through a custom-built stage, to product stage to commodity stage. Enterprise information has followed this path, and according to Figure 1, we see Amazon’s Elastic Compute Cloud (EC2) positioned at the commodity/utility stage.

Figure 1

Evolutionary processes apply to technology - and to the cloud

Source: Simon Wardley, http://blog.gardeviance.org

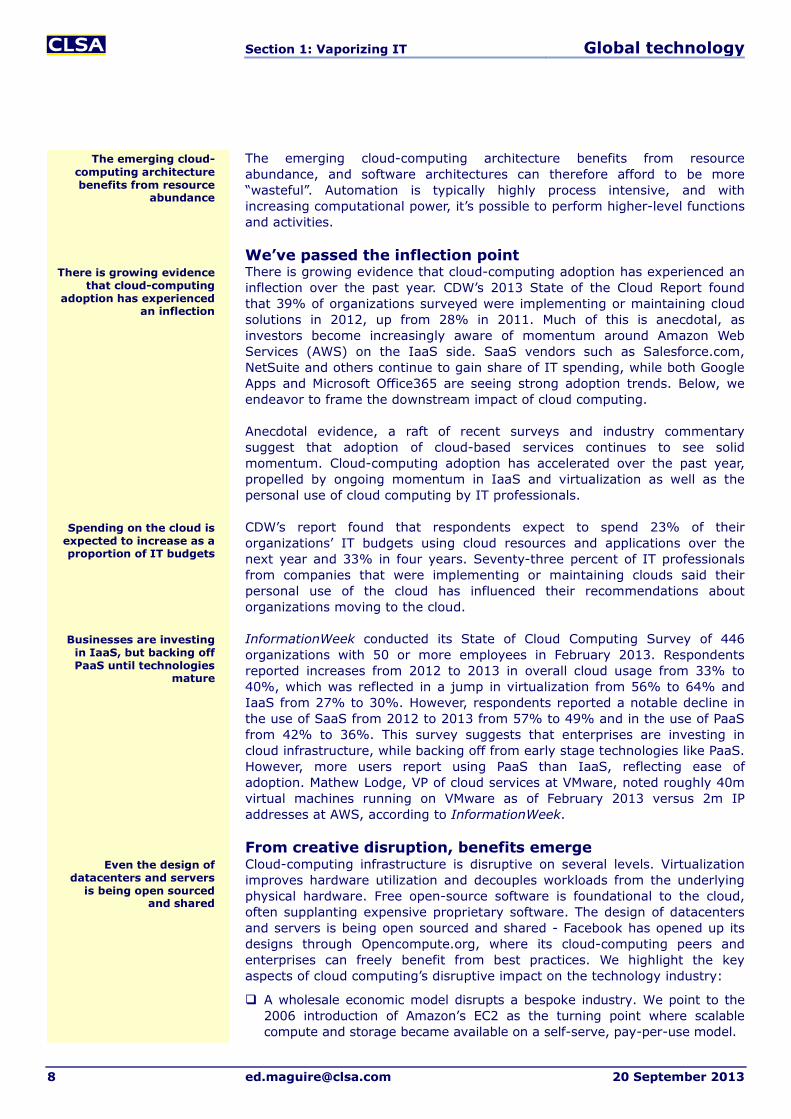

What the new cloud architecture means for the rest of technology As cloud computing has matured, it is increasingly commoditizing the underlying components of technology infrastructure (hardware and software). Wardley believes that as cloud computing matures into a utility model, declining costs have an elastic effect on demand, stimulating consumption and driving innovation in value creation atop the utility cloud infrastructure.

Figure 2

Pre-cloud era value to cloud model commoditization

Source: John Zysman, Jonathan Murray, Kenji Kushida

Platformincludes management logic

Offering(eg, database, server, router, etc)

Management logic

Offering(eg, database, server, router, etc)

Offering(eg, database, server, router, etc)

Cloud ModelPre-Cloud Era

Inte

grat

ed o

ffer

ing

Com

mod

itiz

ed!

Cloud computing has advanced to the

commodity stage

As cloud computing matures into a utility,

declining costs have an elastic effect on demand

The cloud model makes technology infrastructure

interchangeable

Section 1: Vaporizing IT Global technology

20 September 2013 [email protected] 7

As we wrote with Jonathan Murray, John Zysman and Kenji Kushida in Clouducopia in January 2012: ‘Management functions within software are increasingly migrating to the platform rather than being encapsulated in individual components of datacenters, whether it be storage, networking or databases. This drives commoditization of the components.’

With industrialization comes commoditization, spurring innovation The evolution of the cloud-computing model reflects a steady process of maturity of enterprise IT. Commoditization occurs when users perceive competitive offerings as more or less similar commodities to be bought or sold - hence price becomes a determining factor in purchase decisions. Cloud-infrastructure services are increasingly commoditized, and a measure of this is the willingness to switch for small price differences. According to a Gartner survey in September 2012, buyers of public cloud services demonstrated early signs of price sensitivity particularly for IaaS. A survey of 556 organizations revealed that 19% of leading cloud adopters would change cloud providers for less than a 5% price difference.

As we discussed in our CLSA Blue Book Clouducopia, the rapid declines in the cost of compute power and storage give rise to a transition from eras of scarcity to an era of abundance, in the words of Jonathan Murray, EVP of strategy at Warner Music Group. When compute power was expensive and limited, and technical expertise at a premium, enterprise systems were typically custom built while software was architected to squeeze the maximum amount of performance out of hardware. With compute and storage costs declining, the abundance of resources allows a new generation of architecture to emerge. Over time this technology itself matures and fades from the foreground to become an enabling component of the next generation of applications.

Figure 3

Componentization of technologies

Source: Simon Wardley, http://blog.gardeviance.org

Computinginfrastructure

Electricity

Mechanicalcomponents

Large-scaleanalytics

IndustrialisedTransitionalUncharted

Genesis Custombuilt

Product(+ rental)

Commodity(+ utility)

Evolution

Invi

sib

leV

isib

le

Val

ue

chai

n

As the cloud commoditizes computing infrastructure,

this enables new types of apps to emerge

Buyers of public cloud services demonstrate

early signs of price sensitivity for IaaS

Management functions within software are

increasingly migrating to the platform

Section 1: Vaporizing IT Global technology

8 [email protected] 20 September 2013

The emerging cloud-computing architecture benefits from resource abundance, and software architectures can therefore afford to be more “wasteful”. Automation is typically highly process intensive, and with increasing computational power, it’s possible to perform higher-level functions and activities.

We’ve passed the inflection point There is growing evidence that cloud-computing adoption has experienced an inflection over the past year. CDW’s 2013 State of the Cloud Report found that 39% of organizations surveyed were implementing or maintaining cloud solutions in 2012, up from 28% in 2011. Much of this is anecdotal, as investors become increasingly aware of momentum around Amazon Web Services (AWS) on the IaaS side. SaaS vendors such as Salesforce.com, NetSuite and others continue to gain share of IT spending, while both Google Apps and Microsoft Office365 are seeing strong adoption trends. Below, we endeavor to frame the downstream impact of cloud computing.

Anecdotal evidence, a raft of recent surveys and industry commentary suggest that adoption of cloud-based services continues to see solid momentum. Cloud-computing adoption has accelerated over the past year, propelled by ongoing momentum in IaaS and virtualization as well as the personal use of cloud computing by IT professionals.

CDW’s report found that respondents expect to spend 23% of their organizations’ IT budgets using cloud resources and applications over the next year and 33% in four years. Seventy-three percent of IT professionals from companies that were implementing or maintaining clouds said their personal use of the cloud has influenced their recommendations about organizations moving to the cloud.

InformationWeek conducted its State of Cloud Computing Survey of 446 organizations with 50 or more employees in February 2013. Respondents reported increases from 2012 to 2013 in overall cloud usage from 33% to 40%, which was reflected in a jump in virtualization from 56% to 64% and IaaS from 27% to 30%. However, respondents reported a notable decline in the use of SaaS from 2012 to 2013 from 57% to 49% and in the use of PaaS from 42% to 36%. This survey suggests that enterprises are investing in cloud infrastructure, while backing off from early stage technologies like PaaS. However, more users report using PaaS than IaaS, reflecting ease of adoption. Mathew Lodge, VP of cloud services at VMware, noted roughly 40m virtual machines running on VMware as of February 2013 versus 2m IP addresses at AWS, according to InformationWeek.

From creative disruption, benefits emerge Cloud-computing infrastructure is disruptive on several levels. Virtualization improves hardware utilization and decouples workloads from the underlying physical hardware. Free open-source software is foundational to the cloud, often supplanting expensive proprietary software. The design of datacenters and servers is being open sourced and shared - Facebook has opened up its designs through Opencompute.org, where its cloud-computing peers and enterprises can freely benefit from best practices. We highlight the key aspects of cloud computing’s disruptive impact on the technology industry:

A wholesale economic model disrupts a bespoke industry. We point to the 2006 introduction of Amazon’s EC2 as the turning point where scalable compute and storage became available on a self-serve, pay-per-use model.

Even the design of datacenters and servers

is being open sourced and shared

Spending on the cloud is expected to increase as a proportion of IT budgets

There is growing evidence that cloud-computing

adoption has experienced an inflection

Businesses are investing in IaaS, but backing off PaaS until technologies

mature

The emerging cloud-computing architecture benefits from resource

abundance

Section 1: Vaporizing IT Global technology

20 September 2013 [email protected] 9

Open-source alternatives to proprietary technologies gain ground. The shift to cloud computing occurs as open source is increasingly viable for the enterprise.

Native cloud architecture commoditizes infrastructure hardware and software. A mature PaaS layer decouples the application logic from the underlying infrastructure and makes infrastructure components increasingly interchangeable and subject to the forces of commoditization.

Cloud computing facilitates a range of new use cases around social computing, mobile services and high-performance analytics, all of which have potential to create new economic value. Cloud computing reflects the industrialization of information technology. While this has disruptive effects on certain providers of infrastructure components and services, there are many beneficiaries of broad-based adoption of cloud computing.

Businesses benefit from lower costs for technology, IT staff and overhead, while gaining benefits of agility. Lowering the marginal cost of failure accelerates innovation and allows for rapid value creation. The extensible aspects of cloud computing allows businesses to scale online operations far more quickly than possible on their own, for less capital, with less risk.

Consumers benefit directly and indirectly from the availability of cloud-enabled applications. Cloud-enabled search, entertainment, information services, location-based services and applications democratize access to culture, knowledge and commerce. Dematerialization of physical goods (for instance, the digitization of books, music and video) into cloud-delivered services reduces friction around information flow.

Further elevating applications to the top of the IT food chain In our February 2010 report Compubiquity, we argued that applications are the top of the software food chain (as software itself is the top of the IT food chain). Applications are the raison d’etre of technology; compute, storage and connectivity are all in the service of applications. Applications are where ultimate value resides, by automating business processes, facilitating communications and collaboration, entertaining and informing users and enabling business models - the value to the users is defined by their utility. Cloud computing provides an essential enabling role in the delivery of business value, allowing applications to be developed and deployed with speed, flexibility and cost efficiency.

It’s a broad generalization, but it’s our view that the higher the vendor operates up the stack, the better cushioned from forces of commoditization. Applications can be deployed both as SaaS and on-premise offerings, and broadly include enterprise and consumer applications as well as the proprietary code powering ecommerce and internet sites. Latency and data gravity considerations inform the choice to deploy on premise or in the cloud.

Figure 4

Value moves up in stacks

Source: Jonathan Murray (Murray's First Law of Platform Economics)

Application

Platform

Infrastructure

Val

ue

Cloud computing provides an essential enabling role

in the delivery of business value

Cloud computing enables social computing, mobile

services and high-performance analytics

Value migrates from infrastructure to platform

to application

Section 1: Vaporizing IT Global technology

10 [email protected] 20 September 2013

In many respects, infrastructure becomes a commodity. The interchangeability of compute, memory and storage changes industry dynamics for providers of infrastructure technologies. There are broader implications for the adoption of hybrid cloud strategies with a fully realized PaaS layer as this commoditizes higher levels of the software stack.

There is increasing focus on the characteristics of the next generation of applications, which differ from the prior generation given the use of new languages and frameworks (such as Node.js, Spring, Rails and Python). These new applications are often social or location-aware, primarily accessed by mobile devices (smartphones and tablets). In fact, a new acronym has emerged to describe the new generation of apps: SMAC, which refers to social, mobile, analytics and cloud. What characterizes the new generation of applications?

Social - Socially enabled applications need global scale, ability to perform multiple real-time operations, relatively low latency and a distributed architecture.

Mobile - With mobile applications, more of the application logic resides in centralized datacenters, delivered as a service to mobile endpoint devices. There’s an increasing importance of location-based services.

Analytics - With the immense proliferation of data, the opportunities to deliver context-aware, real-time analytics demand scalable data-management systems with intelligent filtering capabilities.

Cloud - Application architectures that incorporate the principles of next-generation PaaS and IaaS have requirements of massive scalability. The flexible architecture accelerates the forces that commoditize underlying infrastructure components.

Figure 5

Catching the fifth wave of corporate IT

Source: Cognizant Technologies

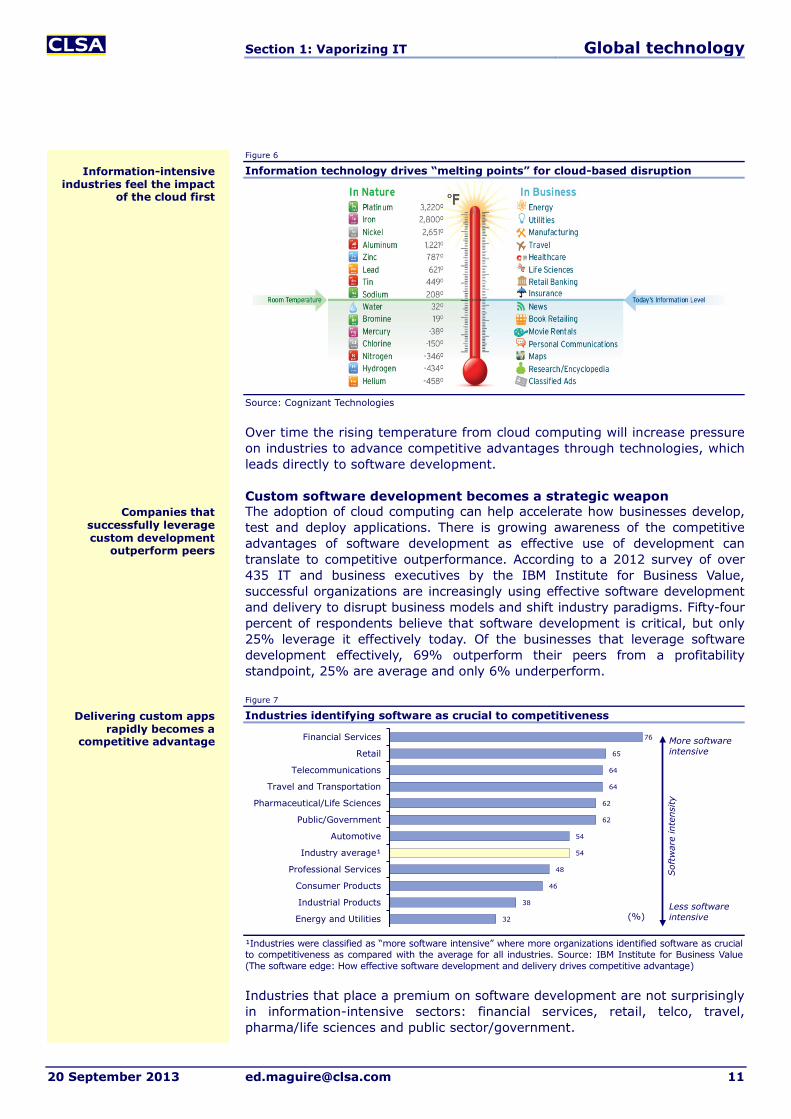

Cloud computing hastens existential threats for certain industries Looking at the potential for competitive threats, a study by Cognizant Technologies likened the decoupling of business process from underlying technologies from the cloud to the impact that rising temperatures have upon different elements. Businesses that have been disrupted so far include information-based businesses with products subject to digitization, such as classified ads, movie rentals and maps.

Next-generation applications embrace

social, mobile, analytics and cloud

The SMAC stack represents a new wave

of corporate IT

Decoupling of business process from underlying

technologies increases competitive pressures

Section 1: Vaporizing IT Global technology

20 September 2013 [email protected] 11

Figure 6

Information technology drives “melting points” for cloud-based disruption

Source: Cognizant Technologies

Over time the rising temperature from cloud computing will increase pressure on industries to advance competitive advantages through technologies, which leads directly to software development.

Custom software development becomes a strategic weapon The adoption of cloud computing can help accelerate how businesses develop, test and deploy applications. There is growing awareness of the competitive advantages of software development as effective use of development can translate to competitive outperformance. According to a 2012 survey of over 435 IT and business executives by the IBM Institute for Business Value, successful organizations are increasingly using effective software development and delivery to disrupt business models and shift industry paradigms. Fifty-four percent of respondents believe that software development is critical, but only 25% leverage it effectively today. Of the businesses that leverage software development effectively, 69% outperform their peers from a profitability standpoint, 25% are average and only 6% underperform.

Figure 7

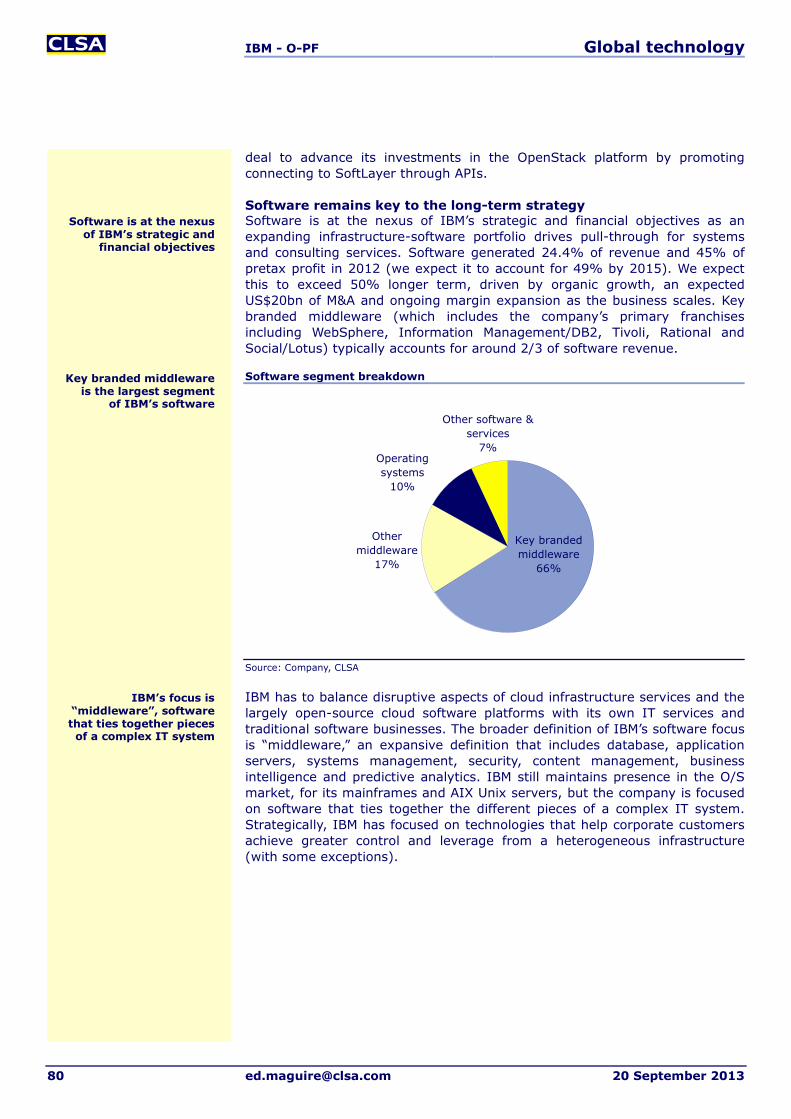

Industries identifying software as crucial to competitiveness

¹Industries were classified as “more software intensive” where more organizations identified software as crucial to competitiveness as compared with the average for all industries. Source: IBM Institute for Business Value (The software edge: How effective software development and delivery drives competitive advantage)

Industries that place a premium on software development are not surprisingly in information-intensive sectors: financial services, retail, telco, travel, pharma/life sciences and public sector/government.

76

65

64

64

62

62

54

54

48

46

38

32

Financial Services

Retail

Telecommunications

Travel and Transportation

Pharmaceutical/Life Sciences

Public/Government

Automotive

Industry average¹

Professional Services

Consumer Products

Industrial Products

Energy and Utilities (%)

More software intensive

Less software intensive

Sof

twar

e in

tens

ity

Companies that successfully leverage custom development

outperform peers

Delivering custom apps rapidly becomes a

competitive advantage

Information-intensive industries feel the impact

of the cloud first

Section 1: Vaporizing IT Global technology

12 [email protected] 20 September 2013

The emergence of public cloud services like Amazon, Google AppEngine and others has also seen growing adoption of new programming languages and frameworks to support the next generation of applications. EMC, in a presentation in March 2013, forecast the number of applications built on the next-generation cloud architecture to increase from 6m in 2012 to almost 50m in 2016, while traditional applications will grow far more in absolute terms. It’s the new generation of applications that are poised for the most robust growth.

Figure 8

Next-generation cloud applications set to surge

Source: March 2013 EMC presentation citing IDC, Gartner, AWS Workload estimates

In a generational shift, traditional languages like C++, Java and JavaScript are being supplanted by Perl, Python, Ruby, Node.Js, Erlang and others. A notable aspect of the evolution of cloud stacks - the software that enables infrastructure as a service - is that leading technologies are mostly open source. OpenStack (a consortium of roughly 200 vendors spearheaded by RackSpace), CloudStack (purchased by Citrix and open sourced to the Apache Foundation), Eucalyptus and Amazon’s Elastic Beanstalk are open source. VMware remains the proprietary enterprise standard for cloud infrastructure.

A key consequence of adoption of the new cloud-computing architecture is that we will see more organizations elevate the importance of the software development function. We are seeing large investments pour into the development platforms for next-generation architecture. GE has invested US$100m in the EMC/VMware Pivotal spinout, which has brought together people (the Pivotal Labs development organization) with new technologies (the Spring framework, HAWQ database processing technology and Pivotal HD Hadoop distribution).

One of the most important players in the new paradigm is GitHub, a collaborative site for developers with over 3.4m users. The company has received US$100m from venture-capital firm Andreesen Horowitz, its largest single investment to date. GitHub was designed to make the processes around software code management (SCM) into a social, collaborative service. The site provides repositories and sharing functions that allow programmers to upload and download shareable open-source code that can be used to build and enhance applications and services. It is a cloud-based SCM service that helps teams of developers with the complexities and challenges of aggregating code, tracking changes and managing collaboration. Over the past couple of years, the site has become de riguer for startups and GitHub accounts are becoming the preeminent means for developers to show off their coding chops to the world. With a GitHub account, engineers have access to a cornucopia of open-source software, which when combined with low-cost cloud services provides a compelling catalyst for accelerating innovations.

It’s notable that leading cloud technologies are

mostly open source

It’s the new generation of applications that are

poised for the most robust growth

New generation of applications poised

for growth

One of the most important players in the new paradigm is GitHub

More organizations elevate the importance of the software development

function

Section 2: PaaS - Key to the hybrid cloud Global technology

20 September 2013 [email protected] 13

PaaS - Key to the hybrid cloud The Platform-as-a-Service market is far smaller than SaaS and IaaS, but size understates its strategic consequence. PaaS promises code portability, the ability to swap out infrastructure components as a commodity. It decouples applications and data from underlying infrastructure software and hardware, eroding the effective differentiation between vendors at lower levels of the stack. The market is highly fragmented, but has attracted growing focus from IT giants. Microsoft, Pivotal, Google and Salesforce.com lead this highly fragmented landscape and we expect consolidation of smaller vendors to accelerate mainstream adoption.

First-generation public clouds from Amazon, Google, Rackspace, Salesforce.com and Microsoft Azure have helped to validate viability of the model. Now traditional hosting companies, outsourcers and service providers target cloud-infrastructure services as a way to retain customers and drive new revenue growth. There is currently a battle over standards, as PaaS vendors battle for leadership in the critically important layer of the technology stack. Salesforce.com, VMware, Red Hat, Microsoft, Google, Amazon, IBM, Oracle and a host of private companies are all angling to capture a share of PaaS users, while ongoing debate and evolution of standards seek to balance ease of interoperability with “vendor lock-in.”

The distinction between public and private clouds has been meaningful in the early stages of the market, as most of what investors and users think of when they hear the term cloud computing is public clouds like Amazon’s EC2. Privately operated clouds that take advantage of the same architectural characteristic of extensibility, dynamic pooling of resources and massive scalability are the province of the largest, most leading-edge companies for now. Purely public or private cloud models can lend themselves to vendor lock-in because application code typically runs on a single IaaS.

Code portability defines the hybrid cloud Users and vendors are increasingly emphasizing the hybrid cloud model as the preferred model for businesses. The term applied loosely refers to deployment of applications on both public and private cloud infrastructure, but, in our view, the critical distinction of a hybrid model is the portability of application code to run on the private or public cloud with minimal modification.

When the application code can be shifted easily from across public clouds and into private clouds, this renders IaaS interchangeable. This commodifies the technology components that comprise IaaS, altering competitive market dynamics. A fully realized PaaS layer will be the key technology that renders IaaS a commodity, and it is here that we believe the most important (and most interesting) dynamics are at work. Investors should pay increasing attention to the merging PaaS market, with dynamics analogous to the application server/middleware wars at the early part of the last decade.

We highlight the critical role we believe PaaS will play in furthering the commoditization of infrastructure hardware, software and services. Investors may not fully appreciate the extent to which the competitive battles between PaaS vendors mirror prior battles over the application server. PaaS advances the decoupling of application logic from the underlying infrastructure - the benefits of PaaS include faster innovation, more efficient use of resources (developer, software and hardware) and better consistency across applications.

A critical distinction of a hybrid model is the

portability of application code

Purely public or private cloud model can lend themselves to vendor

lock-in

PaaS is a small but important catalyst for

technological disruption

First wave of public clouds sets the stage

for new battles

Section 2: PaaS - Key to the hybrid cloud Global technology

14 [email protected] 20 September 2013

PaaS is the least mature and most highly fragmented of the cloud “layers” with over 150 vendors offering basic functionality.

PaaS for application development and deployment will play an essential role enabling hybrid clouds.

Increasing preference for hybrid cloud architectures will elevate the importance of PaaS offerings that allow application code to be deployed on public and private clouds with minimal modification.

The relatively small size of the PaaS market belies its strategic importance to the rest of the tech ecosystem.

Adoption of mature PaaS will accelerate commoditization of infrastructure - hardware, storage, operating system, database, various flavors of middleware, application servers and IaaS as well.

Interest in PaaS adoption is gaining ground. In a September 2012 survey of 554 organizations with over 500 employees, Gartner found that roughly two out of five respondents have evaluated and planned to use PaaS for integrating applications, managing application portfolios and developing new applications.

We expect the battle lines to become more distinct with IBM, Oracle, Microsoft, Red Hat, Salesforce.com, Google and Amazon, as well as newer entrants Pivotal, Apprenda and CloudBees. EngineYard, Stackato and others seek to command share of the market. It’s too early to handicap the likely winners, and public PaaS should continue to be a vibrant market.

PaaS: Revenue may be small but impact is big So far, cloud computing has seen the most momentum at the top and bottom layers of the stack. SaaS application vendors including Salesforce.com, Workday, NetSuite, Concur and others have seen impressive growth, disrupting incumbents and carving out new market segments. IaaS vendors such as Amazon, Google and Rackspace have experienced rapid growth from supporting a range of startup companies and projects and increasingly assuming a role as core infrastructure providers for companies of all sizes.

It’s our view that the PaaS layer is strategically the most important in the cloud stack, far more significant than the relative size of the market would suggest. At present, the market for PaaS is broadly fragmented with over 150 vendors tracked by Gartner. This is a sign of a young market, where there is no single, obvious answer to users’ needs.

PaaS commonly refers to a type of framework that enables the deployment of SaaS applications on a common platform, taking advantage of common services, resources and quality controls. The predominant vision of PaaS is to provide developers an environment that accelerates creation and deployment of applications, which share common services such as authentication, billing and database integration while benefiting from scalability and resilience.

Benefits of the PaaS approach include cost reductions due to the ability to re-use services (eg, security and transactional capabilities), run applications on shared infrastructure with scalability and failover capabilities and support geographically disparate development teams, as well as the quality controls associated with a specifically proscribed development and runtime environment. Developers can get around capacity constraints dependent on

PaaS addresses the needs of users to better support cloud-based applications

Interest in PaaS adoption is gaining ground

The PaaS layer is strategically the most

important in the cloud stack

Section 2: PaaS - Key to the hybrid cloud Global technology

20 September 2013 [email protected] 15

having to forecast requirements accurately. Benefits include better utilization of infrastructure, significant reductions in hardware costs, notably improved uptime and the ability to leverage common components.

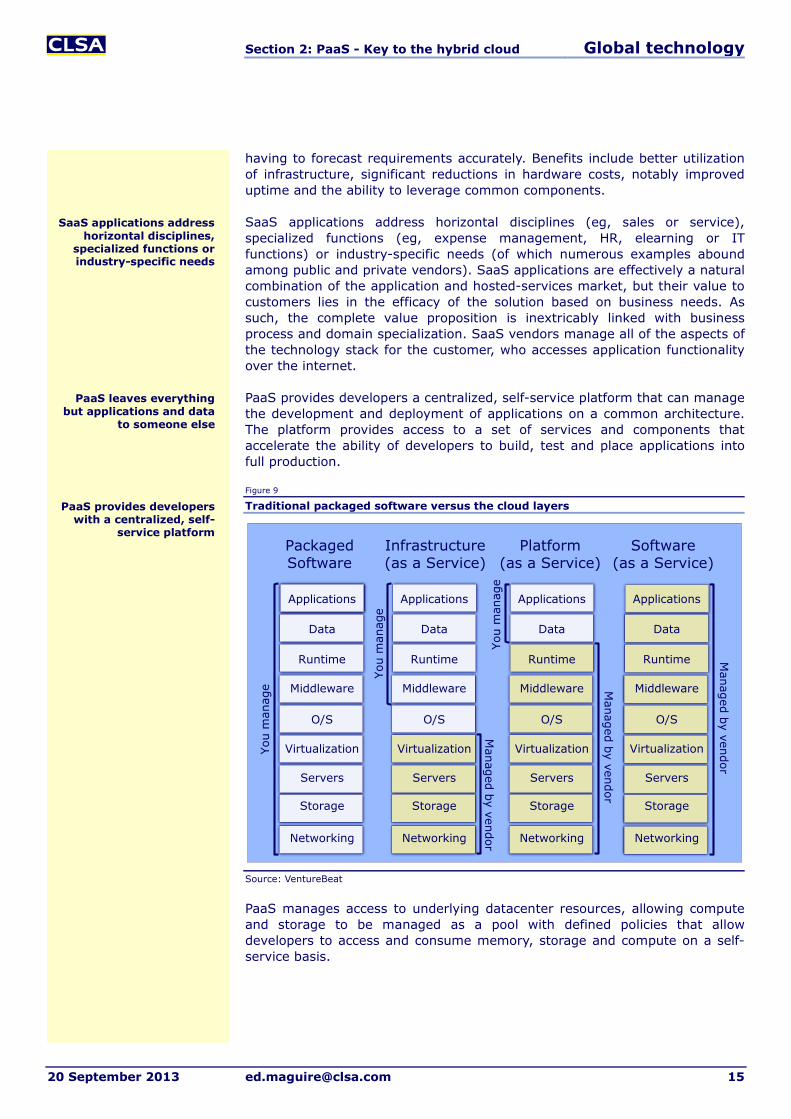

SaaS applications address horizontal disciplines (eg, sales or service), specialized functions (eg, expense management, HR, elearning or IT functions) or industry-specific needs (of which numerous examples abound among public and private vendors). SaaS applications are effectively a natural combination of the application and hosted-services market, but their value to customers lies in the efficacy of the solution based on business needs. As such, the complete value proposition is inextricably linked with business process and domain specialization. SaaS vendors manage all of the aspects of the technology stack for the customer, who accesses application functionality over the internet.

PaaS provides developers a centralized, self-service platform that can manage the development and deployment of applications on a common architecture. The platform provides access to a set of services and components that accelerate the ability of developers to build, test and place applications into full production.

Figure 9

Traditional packaged software versus the cloud layers

Source: VentureBeat

PaaS manages access to underlying datacenter resources, allowing compute and storage to be managed as a pool with defined policies that allow developers to access and consume memory, storage and compute on a self-service basis.

Applications

Data

Runtime

Middleware

O/S

Virtualization

Servers

Storage

Networking

You

man

age

Managed by vendor

Managed by vendor

Managed by vendor

PackagedSoftware

Infrastructure(as a Service)

Platform(as a Service)

Software(as a Service)

Applications

Data

Runtime

Middleware

O/S

Virtualization

Servers

Storage

Networking

Applications

Data

Runtime

Middleware

O/S

Virtualization

Servers

Storage

Networking

Applications

Data

Runtime

Middleware

O/S

Virtualization

Servers

Storage

Networking

You

man

age

You

man

age

SaaS applications address horizontal disciplines,

specialized functions or industry-specific needs

PaaS provides developers with a centralized, self-

service platform

PaaS leaves everything but applications and data

to someone else

Section 2: PaaS - Key to the hybrid cloud Global technology

16 [email protected] 20 September 2013

Figure 10

Characteristics of IaaS versus PaaS

IaaS PaaS

Virtual machines (VMs) and storage Middleware in the cloud

Rapid datacenter resource provisioning and delegated hardware management

Rapid application development, deployment and change; fully delegated datacenter responsibility

Coarse-grained elasticity and payment Fine-grained elasticity and payment

Developer responsible for platform and application stack as well as his code

Developer is responsible only for his code

Shared-hardware multitenancy Shared processing, shared database or shared-everything multitenancy

Portability at the VM level Little or no portability

You can run anything you want within VM (provided it is technically feasible and you can get a cloud license)

What you can run is restricted to what the PaaS provider offers

Source: Gartner

PaaS setups tend to sit on top of IaaS offerings. These can be maintained on platforms from the likes of Amazon, Google or Microsoft or on IaaS platforms like VMware’s VSphere or OpenStack.

Figure 11

Conceptual view of cloud-computing architecture

Source: Microsoft

An advantage of decoupling the application platform from the underlying infrastructure is that businesses can use different vendors for platform and infrastructure in many cases. For instance, Heroku and EngineYard run on AWS, while CloudFoundry and CloudBees enable developers to run their apps on either OpenStack or VMware VSphere despite being priced on a per-use basis. The cloud-computing models abstract resources and automate many of the functions that would previously require custom coding.

PaaS can provide self service, services

management, orchestration and

management

PaaS offers higher level functionality than IaaS,

with more restrictions on what runs on the platform

Businesses can use different vendors for

platform and infrastructure

Section 2: PaaS - Key to the hybrid cloud Global technology

20 September 2013 [email protected] 17

Developers are the key to the PaaS market In contrast to SaaS (which targets end users and business) and IaaS (which targets datacenter/infrastructure managers), the PaaS market targets developers. We see significant growth in the category as users seek to leverage increasing capabilities to support cloud-based applications, while providers (both IaaS and SaaS) seek to engage customers more deeply, achieving the practical objectives of lock-in without the negative implications.

Businesses are using PaaS in order to simplify the processes involved with managing hardware and software, so that they can develop and bring to market applications and innovation more quickly. Speed to market is the most important benefit of PaaS; companies that use PaaS are able to save time managing infrastructure and basic services to bring applications live in a fraction of the time.

A diverse, shifting landscape Gartner identifies over 150 vendors with offerings that directly or indirectly target different categories of PaaS. Gartner tracks over a dozen segments. These functions include application platform services, application lifecycle management services, integration services, analytic services, managed file transfer services, database services and others. Cloud application platform services (aPaaS) offer functions similar to application servers, which intermediate between application logic and infrastructure (server, storage and database). We are primarily concerned with application platform services that support custom applications.

Gartner estimates that worldwide PaaS revenue reached US$1.2bn in 2012, an increase from US$900m in 2011. It forecasts the market to reach US$3.5bn by 2017, a Cagr of 24%.

Figure 12

PaaS forecast, 2011-17

Note: AD - Application Development; AIM - Application Infrastructure and Middleware; BI - Business Intelligence Platform; DBMS - Database Management Systems. Source: Gartner

The number of vendors and fragmentation are an indication of a young market as there’s no obvious answer to the market need. At this point, the market for PaaS consists of a number of smaller subsegments including application development/application lifecycle management PaaS; application PaaS, business process management PaaS, integration PaaS and other

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2011 2012 2013 2014 2015 2016 2017

(US$bn) AD AIM BI DBMS

The PaaS market targets developers

Gartner identifies over 150 vendors with

offerings that target different categories

of PaaS

Gartner estimates that worldwide PaaS revenue

reached US$1.2bn in 2012

Shakeouts and consolidation likely to

characterize the market in the near term

Section 2: PaaS - Key to the hybrid cloud Global technology

18 [email protected] 20 September 2013

functions. Over time we expect PaaS to be subsumed into broader offerings, which is likely to include PaaS suites and hosted development platforms.

Leading players in traditional application PaaS remain Salesforce.com (both Force.com and Heroku), Microsoft’s Windows Azure Services Platform and Google’s App Engine. There are also privately held providers including CloudBees, EngineYard, Stackato (based on Cloud Foundry), Apprenda (primarily .NET focused), Appistry (Hadoop analytics), AppFog (recently acquired by Savvis) and others. We would expect shakeouts and consolidation to characterize the market in the near term, as a crowded landscape typical of nascent markets is unsustainable over the medium term. We expect competition to remain fierce as cloud stack providers seek their own ways to lock in customers.

Users expect hybrid cloud model to predominate According to the North Bridge/Giga Om 2013 Future of Cloud Computing Survey, public cloud use is expected to decline relatively from 39% to 32% in five years, while hybrid clouds increase as a proportion of all uses from 27% to 43%. Today, public clouds account for 39% of usage, with 27% hybrid and 34% private, but in five years hybrid should be the most prominent model at 43% versus 32% public and 25% private.

The expectation that enterprises will increasingly prefer a hybrid cloud model over pure public or private approaches has a few key implications. Application portability (the ability to run applications on a public or private cloud depending on business requirements) will become a critical capability for hybrid PaaS offerings. This may leave public-IaaS-only vendors such as Heroku and Google App Engine at a modest disadvantage.

Public PaaS versus private PaaS - Towards hybrid PaaS The first generation of PaaS offerings was predominantly public - Heroku and Force.com (Salesforce.com), Engine Yard and Google App Engine all offered developers the ability to write applications without worrying about the underlying infrastructure. However, public PaaS failed to address enterprise concerns over security and governance, and hence did not see significant adoption. Deploying applications on a hybrid-enabled PaaS middleware layer allows users to move applications as they see fit - from one public cloud to another, or behind the firewall on a cloud-based architecture.

According to David Linthicum of GigaOm, advantages to private PaaS include:

A common self-service application development platform allows developers to design, test and deploy applications within an environment that provides consistency, control and quality assurance.

Developers can access datacenter resources more effectively. PaaS handles server utilization by helping to abstract the application logic from the underlying server and storage. This improves utilization and efficiency of hardware and results in more effective operations.

Developers can utilize their existing skill sets while taking advantage of new management capabilities around application management and datacenter resource services.

Initial PaaS products primarily supported application server capabilities, but the market has broadened to encompass other middleware functions. The conditions are in place for accelerating innovation in custom applications, as increasing sophistication and ease of use of development tools and backend

The barriers to develop, deploy and scale custom

applications have dramatically decreased

Hybrid clouds are expected to increase as a

proportion from 27% to 43% in five years

Applications on hybrid-enabled PaaS can more

easily move between public and private cloud

Section 2: PaaS - Key to the hybrid cloud Global technology

20 September 2013 [email protected] 19

services available from PaaS providers obviate the need for developers and startups to invest in their own IT infrastructure. Programming languages and tools continue to evolve and are more accessible. Various ROI studies for PaaS (most notably an IDC analysis of Force.com) have shown up to 75% reduction in development time and four-five times improvement in payback from hosted development and deployment models.

Balancing control and openness, focus and heterogeneity Among the various approaches to PaaS, users must weigh the benefits and disadvantages of closed versus open models. Salesforce.com’s Force.com leveraged the company’s underlying infrastructure and services, which included vetting of code to run on the platform (analogous to Apple’s AppStore process). The limitation was that developers had to use Salesforce.com’s Application Exchange (APEX) programming language, a variant of Java but a specialized skill set nonetheless. While the vision of an application exchange built on the Force.com platform was sound, the APEX requirements limited adoption by developers, leading Salesforce.com into a short-lived partnership with VMware to harness the Java developers that used its open-source SpringSource framework. The alliance fizzled; Salesforce.com bought Heroku, a Ruby-based platform that has since extended to other languages (eg, Java, Python, Node.js and others), while VMware launched CloudFoundry, an open-source platform that supports several languages.

Battle to control the platform - Legacy versus cloud native It is critically important to control the platform - the infrastructure, standards, etc. Every application is written to the middleware, and the PaaS layer is evolving to be a high-stakes battle for developer share.

Figure 13

On-premises application platforms - Magic Quadrant

Source: Gartner

In the late 1990s and early 2000s, there was a life and death battle between Microsoft, BEA Systems, IBM, Sun and others for the platform architecture. Microsoft had .NET and everyone else had a mix of Java, CORBA and object-request brokers. These vendors united around Java Enterprise Edition (JavaEE) to successfully build a common front against Microsoft.

Users must weigh the benefits and

disadvantages of closed versus open models

IBM, Oracle, Microsoft and Red Hat are on-premise application

platform incumbents

It is critically important to control the platform

Section 2: PaaS - Key to the hybrid cloud Global technology

20 [email protected] 20 September 2013

A new generation of innovation goes cloud native There is a subtle, but distinct difference in PaaS offerings between cloud based (where existing technologies are deployed on a cloud underneath) and cloud native (where middleware is designed for the cloud). Cloud-native technologies are engineered to be elastic, to use in-memory computing and other capabilities. Customers are migrating to the cloud because they expect high productivity and ease of use. However, existing languages like Java and C# programming have lower productivity in the cloud. Most of the innovation is no longer going to JavaEE or .NET, but these skill sets are still in short supply among traditional enterprises.

Initially the cloud-native platforms are all proprietary. Force.com. Rollbase and Zoho Creator are key examples of this. One vendor, LongJump, was similar to Force.com and has been acquired by Software AG. Rollbase is another cloud-native PaaS vendor acquired by Progress Software. Both LongJump and Rollbase are cloud-native platforms currently in the hands of vendors with more resources. They now have sales channels. Tibco is also moving in this direction, moving through organic development. IBM has been working on a strategic project with WebSphere to create a new technology stack designed specifically for the cloud, and in the interim has launched its own BlueMix project focused on building solutions around CloudFoundry and OpenStack. Google and Red Hat created a partnership around a project called CapeDwarf, which is focused on creating a standard for cloud-native platforms. This project aims to provide on-premise software running on JBoss with application program interfaces (APIs) compatible with AppEngine that can be modified to become more cloud native.

Cloud-enabled (and backward compatible) versus cloud native Over the past year, all of the major enterprise Java platform vendors have launched versions of PaaS. IBM, Oracle, SAP, Red Hat and VMware (through its Pivotal spinoff) have all launched cloud application infrastructure services based on core Java technologies. Oracle, SAP and Red Hat use Java and JavaEE as primary models, while CloudFoundry uses the Spring framework.

Red Hat’s OpenShift and Pivotal’s Cloud Foundry are squaring off to compete directly in the market as independent PaaS offerings. We see one of these two projects emerging as a potential challenge to the proprietary offerings seen elsewhere. Red Hat’s OpenShift is a PaaS offering that supports Java, Perl, PHP, Python and Ruby. The technology is not yet open sourced, but there are plans to open up the platform. For now, OpenShift is focused on public clouds, though there are plans to support on-premise deployments. VMware’s Cloud emerged from the company’s SpringSource acquisition, has been open sourced and currently supports Java, .NET, Ruby, Scala, Node.js, PHP and Python. At this point Cloud Foundry appears to be seeing the strongest momentum among the independent PaaS projects, but Red Hat is investing in technology and partners around its own project.

The key consideration for the Java-leading vendors (as well as Microsoft’s .NET-based Azure Platform Services) is backward compatibility, and this is largely a defensive measure. The leading vendors will be able to benefit from a “long tail” in business usage of Java, .NET, JBoss and WebSphere - these technologies will not go away before the CIOs retire.

Is backward-compatible PaaS the equivalent of “screen-scraping”? Our discussions with industry analysts reveal the view early on that cloud adoption is “radio on TV” – like old wine in new bottles. Older applications are in an introductory stage, like screen scraping, so backward compatibility is

Red Hat’s OpenShift and VMware’s Cloud Foundry

are squaring off

Initially the cloud-native platforms are all

proprietary

Existing languages like Java and C# programming

have lower productivity in the cloud

Section 2: PaaS - Key to the hybrid cloud Global technology

20 September 2013 [email protected] 21

essentially an emulation. It’s likely that over time we will see backward compatibility give way to a new architecture.

According to Gartner, PaaS vendors that are locked into supporting JavaEE will be challenged. IBM has four big customers, Oracle’s PaaS is now just generally available and the company’s focus is more on hosting, and Red Hat just recently became generally available. In terms of consolidation, it’s likely that the smaller companies will be acquired on the merits of their technology. The big vendors like HP, Dell and the telecoms will be acquirers of PaaS. Clearwire/Savvis acquired AppFog, which was reportedly close to a fire sale.

Cloud agnostic or integrated stack? Still evolving PaaS providers are distinguished by whether they are locked into an underlying IaaS platform (as is the case with Force.com, Google AppEngine, Amazon’s Elastic Beanstalk and Windows Azure) or cloud agnostic (in the case of VMware/Pivotal’s CloudFoundry, Red Hat’s OpenShift and independent providers such as CloudBees and others). There are advantages to each approach: offerings tied to an underlying platform provide better integration with underlying compute, management and storage services, while the cloud-agnostic platforms theoretically provide users the option to choose the most appropriate IaaS provider.

Even more so than with IaaS, lock-in concerns around PaaS are top of mind for users. In many respects, there is no way to get around reliance on proprietary programming languages or service interfaces; this is inherent to the nature of applications. Additionally, the ability to shift applications between platforms is limited in many cases. That said, this dynamic is not that much different from the on-premises development model (where .NET and Java development platforms have competed). However, the cost and reliability benefits offered by leading PaaS providers nevertheless provide an attractive solution in light of the economic downturn.

ISV success will determine the winners in PaaS Success with independent software vendors (ISVs) will be a key indicator of traction. To be a leader, the PaaS provider needs a healthy SaaS ecosystem and one of the predictors for success is the ability to attract a healthy ecosystem of partners and applications running on the platform. Salesforce.com was early to the market with Force.com and its proprietary platform. We note that Salesforce.com already has several companies running on its platforms that are writing large checks, with management alluding on recent earnings calls that some may potentially be considering IPOs. However, we’d note that Salesforce.com’s technology does not work on premises and this could limit relevance as a broad platform provider. AWS currently supports a broad range of startups and established companies running on its services, including FourSquare, Pinterest and Netflix.

An emerging concern over PaaS is potential for

vendor lock-in

Success with ISVs will be a key indicator

of traction

PaaS vendors that are locked into supporting

JavaEE will be challenged

Section 3: The cloud as an economic catalyst Global technology

22 [email protected] 20 September 2013

The cloud as an economic catalyst The cloud-computing model alters the economic calculus of information technology. In our view, the transition from products to services, from capex to opex, parallels the electrification of industry in the 19th Century as widespread access to distributed power catalyzed massive value creation and innovation. The benefits that cloud computing delivers to users and organizations translate into innovation, job creation and economic growth.

The cloud-computing impact is multifaceted. The adoption of cloud computing creates new competitive challenges as well as shifts in the business model for vendors, and this impacts spending on traditional IT, which can be bucketed into capital and operating costs:

Capital expenditures - Areas potentially impacted include middleware, database, operating systems, storage, server, networking and IT consulting. The cloud-computing wave impacts capital expenditures in several ways: shifting consumption of on-premise purchase of hardware and software to public cloud services; substituting of free open-source software licenses and hardware designs for proprietary offerings; subsuming previously distinct infrastructure-management-software functions into a platform layer; and improving utilization of server and storage hardware through virtualization and other ways.

Operating expenditures - Potentially impacted areas include maintenance and support for software and hardware, corporate IT staff and support, real estate, heating, ventilation & air conditioning (HVAC), energy and third-party IT services (support and helpdesk). Cloud computing can potentially reduce the need for software maintenance and support (as well as third-party IT services) through standardization of infrastructure architecture, while reductions in overhead costs come from consolidation of facilities into more efficient design or use of outside providers.

Scope varies, but robust growth expectations concur Industry analyst forecasts differ in terms of scope and definition of what is characterized as cloud, but concur in expectations for healthy growth. Gartner forecasts cloud computing to grow from US$93bn in 2011 to US$237bn in 2017, a 17% Cagr.

Gartner sizes the global information and communications technology (ICT) market at US$3.6tn, with telecom services making up the greatest portion of overall spend. Adoption of cloud computing drives demand for all major categories of spending, although changes afoot in technology, business models and customer priorities will give rise to new winners and losers.

Figure 14

ICT spending by category, worldwide (US$bn) 2011 2012 2013 2014 2015 2016 2017 Cagr (%)

2012-17 Devices 610 676 695 740 788 828 863 5.0 Datacenter Systems 138 140 143 149 155 160 165 3.4 Enterprise Software 273 285 304 324 346 370 395 6.7 IT Services 888 906 926 968 1,018 1,071 1,127 4.5 Telecom Services 1,653 1,641 1,655 1,694 1,732 1,769 1,803 1.9 Overall IT 3,560 3,648 3,723 3,875 4,039 4,198 4,354 3.6 Source: Gartner

A disruptive force as well as a net-positive

economic catalyst

Industry analyst forecasts differ in scope, but concur in expectations of healthy

growth

Cloud-computing impact is multifaceted

Software is forecast to grow faster than other technology categories

Section 3: The cloud as an economic catalyst Global technology

20 September 2013 [email protected] 23

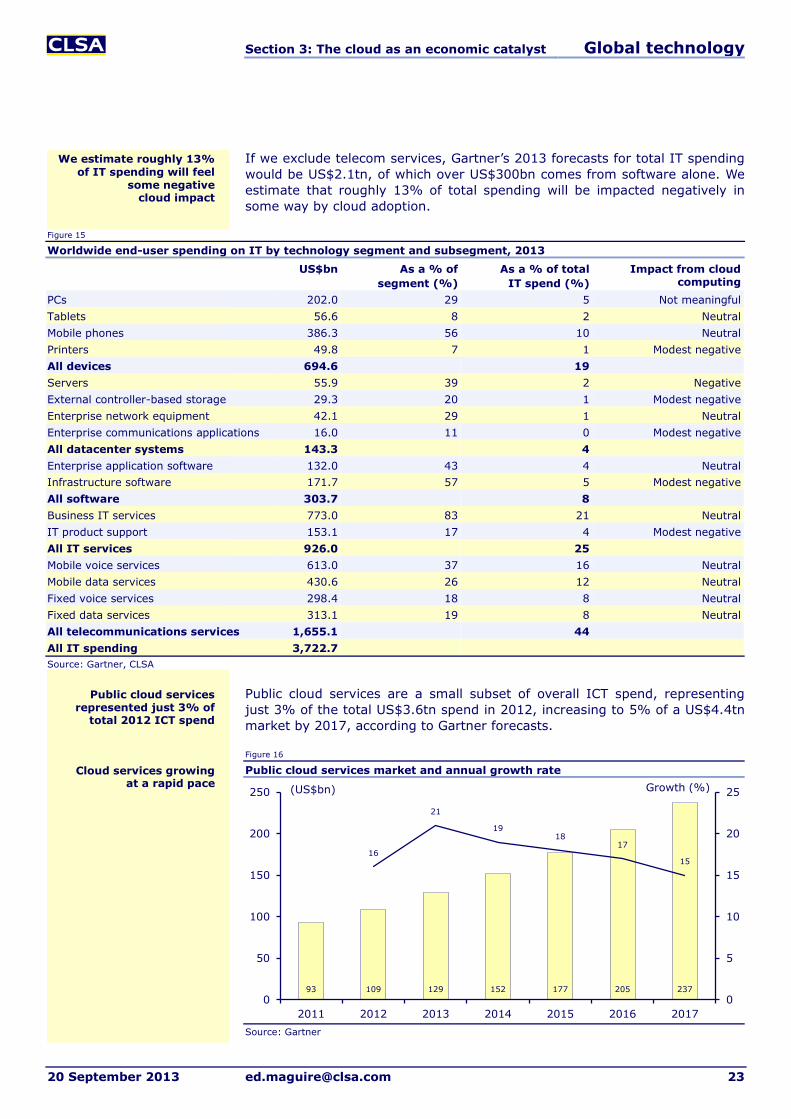

If we exclude telecom services, Gartner’s 2013 forecasts for total IT spending would be US$2.1tn, of which over US$300bn comes from software alone. We estimate that roughly 13% of total spending will be impacted negatively in some way by cloud adoption.

Figure 15

Worldwide end-user spending on IT by technology segment and subsegment, 2013

US$bn As a % of segment (%)

As a % of total IT spend (%)

Impact from cloud computing

PCs 202.0 29 5 Not meaningful Tablets 56.6 8 2 Neutral Mobile phones 386.3 56 10 Neutral Printers 49.8 7 1 Modest negative All devices 694.6 19 Servers 55.9 39 2 Negative External controller-based storage 29.3 20 1 Modest negative Enterprise network equipment 42.1 29 1 Neutral Enterprise communications applications 16.0 11 0 Modest negative All datacenter systems 143.3 4 Enterprise application software 132.0 43 4 Neutral Infrastructure software 171.7 57 5 Modest negative All software 303.7 8 Business IT services 773.0 83 21 Neutral IT product support 153.1 17 4 Modest negative All IT services 926.0 25 Mobile voice services 613.0 37 16 Neutral Mobile data services 430.6 26 12 Neutral Fixed voice services 298.4 18 8 Neutral Fixed data services 313.1 19 8 Neutral All telecommunications services 1,655.1 44 All IT spending 3,722.7 Source: Gartner, CLSA

Public cloud services are a small subset of overall ICT spend, representing just 3% of the total US$3.6tn spend in 2012, increasing to 5% of a US$4.4tn market by 2017, according to Gartner forecasts.

Figure 16

Public cloud services market and annual growth rate

Source: Gartner

93 109 129 152 177 205 237

16

21

1918

17

15

0

5

10

15

20

25

0

50

100

150

200

250

2011 2012 2013 2014 2015 2016 2017

(US$bn) Growth (%)

Public cloud services represented just 3% of

total 2012 ICT spend

We estimate roughly 13% of IT spending will feel

some negative cloud impact

Cloud services growing at a rapid pace

Section 3: The cloud as an economic catalyst Global technology

24 [email protected] 20 September 2013

Cloud application services (SaaS) will continue to be the largest proportion of public cloud services, forecast to grow from US$16.2bn in 2012 to US$27.8bn in 2017. CRM, enterprise resource planning (ERP) and collaboration applications are the largest SaaS segment, with the most robust growth expected from digital content creation, office suites and business intelligence platforms. As the most mature segment of cloud services, SaaS in 2012 accounted for 69% of the public cloud services market; Gartner expects this to decline to 53% by 2017 as IaaS becomes a larger portion of the market (and custom-build applications increasingly go into production).

Figure 17

Market-size forecast for IaaS, PaaS and SaaS

Source: Gartner

Gartner expects cloud application infrastructure services (PaaS) to grow in line with the market, increasing from US$1.2bn in 2012 to US$3.6bn in 2017, a Cagr of 23.5%. Overall PaaS is likely to remain roughly 5% of public cloud services through 2017. Cloud system infrastructure services (IaaS) should grow at the most robust rate, increasing from US$6.2bn in 2012 to US$30.6bn in 2017, a Cagr of 37.8%. IaaS should jump from 26% of public cloud services in 2012 to 43% by 2017.

Measuring return on the cloud Quantifying the economics of cloud computing is an inexact discipline; there are so many variable inputs that defining payback is necessarily situation-specific. Calculations need to incorporate not just cost factors, but also the creation of incremental value (whether in the form of additional revenue, new innovation, competitive advantages, etc). Nonetheless, there are a few key measures that businesses in particular must assess to determine the economic rationale for a cloud investment.

According to CDW’s 2013 State of the Cloud Report Survey (comprising 1,242 IT professionals including 479 organizations implementing or maintaining cloud computing), respondents are currently saving an average of 13% of their organizations’ IT budgets using cloud resources and applications, with savings expected to increase to 17% in one year and 25% in four years.

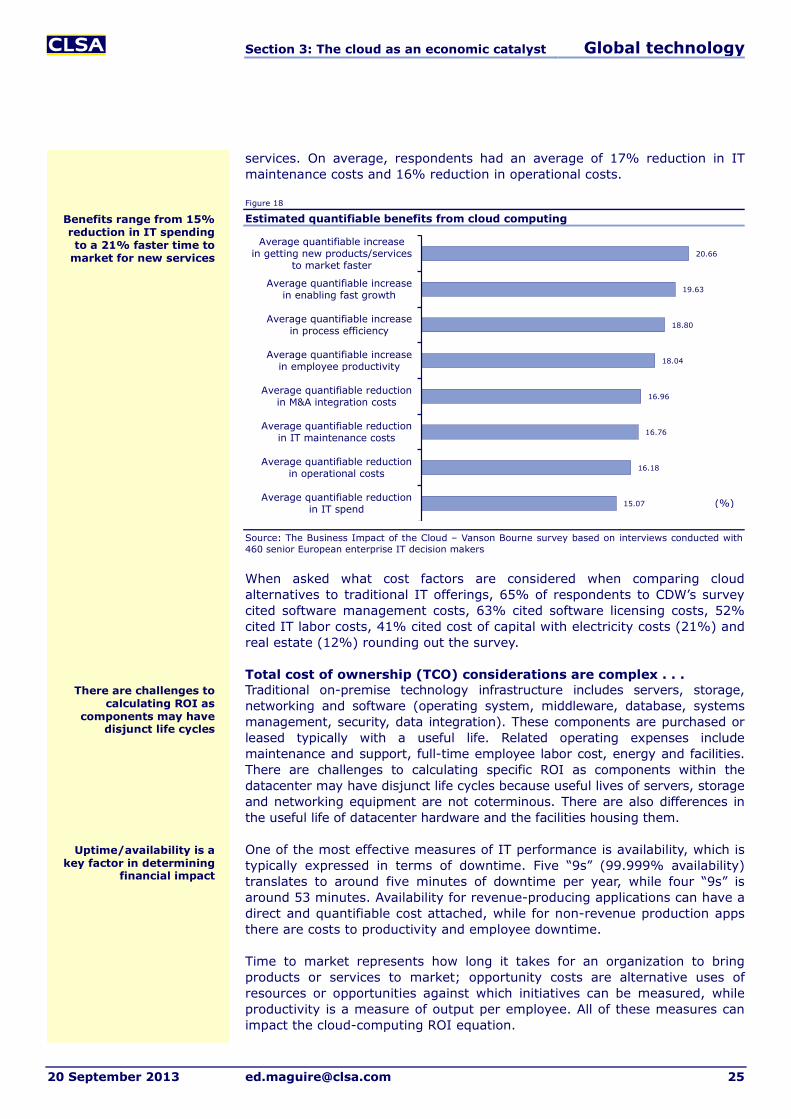

The Business Impact of the Cloud, a March 2012 report by Vanson Bourne, found benefits from cloud computing ranging from 15% for quantifiable reduction in IT spending to a 21% acceleration in time to market for new

0

10

20

30

40

50

60

70

80

2011 2012 2013 2014 2015 2016 2017

(US$bn) IaaS PaaS SaaS

SaaS is the largest portion of the market, forecast at an 18.5%

Cagr through 2017

Quantifying economics of cloud computing is an

inexact discipline

CDW survey respondents cite an average 13% IT

budget savings from cloud, increasing to

25% in four years

SaaS, PaaS and IaaS to grow from US$23.6bn in

2012 to US$72bn in 2017, a 25% Cagr

Section 3: The cloud as an economic catalyst Global technology

20 September 2013 [email protected] 25

services. On average, respondents had an average of 17% reduction in IT maintenance costs and 16% reduction in operational costs.

Figure 18

Estimated quantifiable benefits from cloud computing

Source: The Business Impact of the Cloud – Vanson Bourne survey based on interviews conducted with 460 senior European enterprise IT decision makers

When asked what cost factors are considered when comparing cloud alternatives to traditional IT offerings, 65% of respondents to CDW’s survey cited software management costs, 63% cited software licensing costs, 52% cited IT labor costs, 41% cited cost of capital with electricity costs (21%) and real estate (12%) rounding out the survey.

Total cost of ownership (TCO) considerations are complex . . . Traditional on-premise technology infrastructure includes servers, storage, networking and software (operating system, middleware, database, systems management, security, data integration). These components are purchased or leased typically with a useful life. Related operating expenses include maintenance and support, full-time employee labor cost, energy and facilities. There are challenges to calculating specific ROI as components within the datacenter may have disjunct life cycles because useful lives of servers, storage and networking equipment are not coterminous. There are also differences in the useful life of datacenter hardware and the facilities housing them.

One of the most effective measures of IT performance is availability, which is typically expressed in terms of downtime. Five “9s” (99.999% availability) translates to around five minutes of downtime per year, while four “9s” is around 53 minutes. Availability for revenue-producing applications can have a direct and quantifiable cost attached, while for non-revenue production apps there are costs to productivity and employee downtime.

Time to market represents how long it takes for an organization to bring products or services to market; opportunity costs are alternative uses of resources or opportunities against which initiatives can be measured, while productivity is a measure of output per employee. All of these measures can impact the cloud-computing ROI equation.

15.07

16.18

16.76

16.96

18.04

18.80

19.63

20.66

Average quantifiable reductionin IT spend

Average quantifiable reductionin operational costs

Average quantifiable reductionin IT maintenance costs

Average quantifiable reductionin M&A integration costs

Average quantifiable increasein employee productivity

Average quantifiable increasein process efficiency

Average quantifiable increasein enabling fast growth

Average quantifiable increasein getting new products/services

to market faster

(%)

Benefits range from 15% reduction in IT spending to a 21% faster time to

market for new services

There are challenges to calculating ROI as

components may have disjunct life cycles

Uptime/availability is a key factor in determining

financial impact

Section 3: The cloud as an economic catalyst Global technology

26 [email protected] 20 September 2013

. . . and cloud ROI is an inexact science The Economics of Cloud Computing by Bill Williams provides a framework for calculating the ROI of cloud-computing projects. Line items that can be measured include disk storage, disk maintenance, server hardware, server maintenance, firewalls and load balancers, network switches, software licenses, software maintenance, facilities and full-time equivalent (FTE) labor. A business calculating the ROI of SaaS versus traditional on-premise IT (or PaaS or IaaS) would need to calculate the costs of all of the prior components over a period of several years (typically three years) then compare this to the cost of a SaaS subscription.

Once annual costs have been calculated, then multiyear costs should be reflected. Typically, a documented payment on a cloud investment in less than a year is respectable. ROI = (gains from investment less costs of investment)/costs of investment. Net present value (NPV) uses a discount rate applied to cash inflows and outflows starting in the first year. If the NPV is high enough (and positive), that would suggest a project makes economic sense (if assumptions are correct).

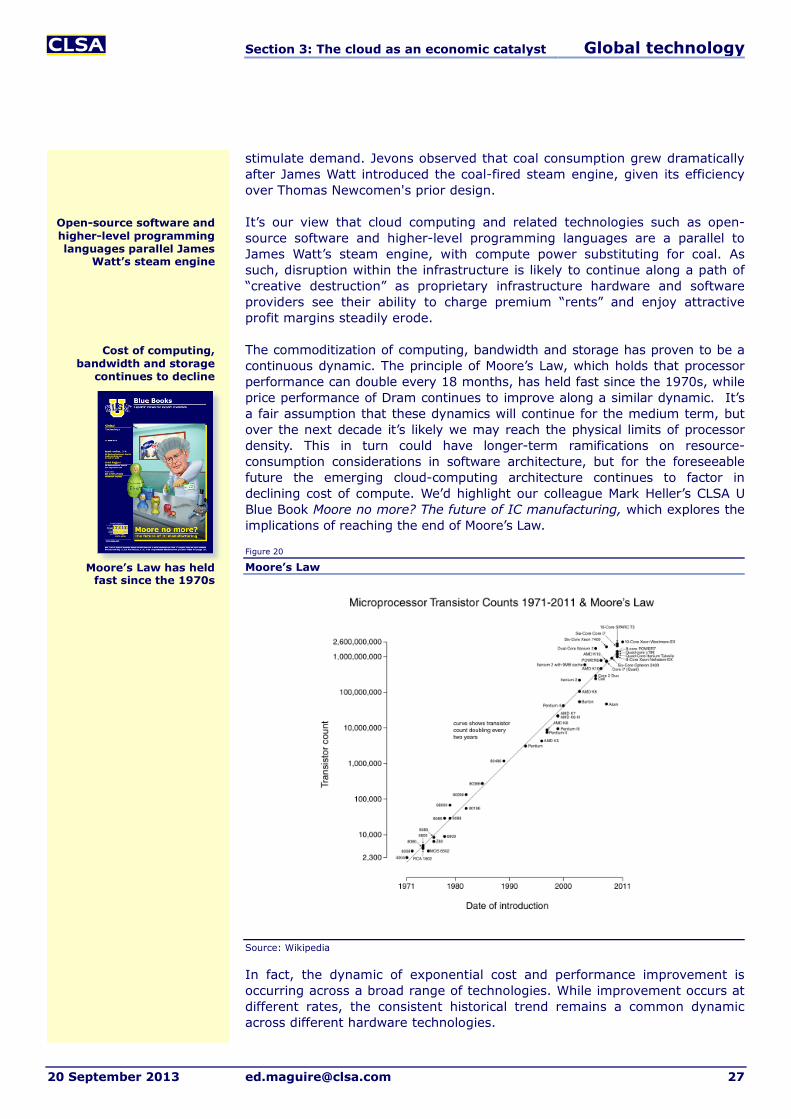

Will cloud computing reduce or increase aggregate IT spending? An ongoing investor concern is that the deflationary aspects for IT - declining cost of computing, emergence of free open-source software and the shared efficiencies from cloud architecture - will ultimately dampen IT spending. We would concur with author Simon Wardley’s view that cloud computing is subject to the Jevons Paradox, the theory that technological progress that increases the efficiency with which a resource is used will increase the rate of its consumption.

Figure 19

Cloud computing has parallels with the Jevons Paradox

Source: Wikipedia

English economist William Stanley Jevons first described this paradox in his 1865 book The Coal Question. At that time, there were concerns that British coal reserves were dwindling, and some experts believed that improvements in efficiency would reduce coal consumption. The Jevons Paradox was the argument that fuel-efficiency improvements would actually increase fuel use, not reduce demand, as greater output per unit of coal would actually

Improved technology doubles the amount of Work produced with a given amount of Fuel

Demand for Fuel rises

Elastic demand

Costs falls by half

Price

0 QuantityQuantity demanded more than doubles

ROI is commonly calculated over a period

of three years

We believe cloud computing reduces costs,

which will accelerate demand

As prices of a commodity decline, demand elasticity

significantly boosts consumption

The Jevons Paradox was first observed with UK

coal consumption in the 19th Century

Section 3: The cloud as an economic catalyst Global technology

20 September 2013 [email protected] 27

stimulate demand. Jevons observed that coal consumption grew dramatically after James Watt introduced the coal-fired steam engine, given its efficiency over Thomas Newcomen's prior design.

It’s our view that cloud computing and related technologies such as open-source software and higher-level programming languages are a parallel to James Watt’s steam engine, with compute power substituting for coal. As such, disruption within the infrastructure is likely to continue along a path of “creative destruction” as proprietary infrastructure hardware and software providers see their ability to charge premium “rents” and enjoy attractive profit margins steadily erode.