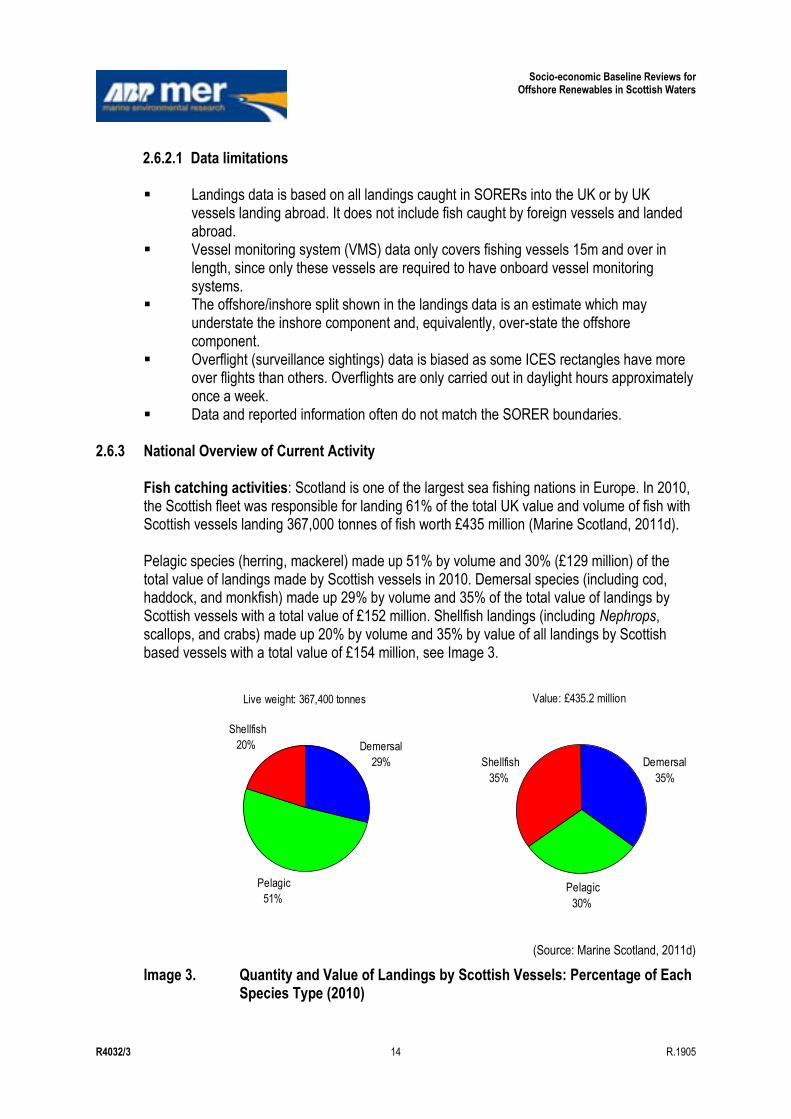

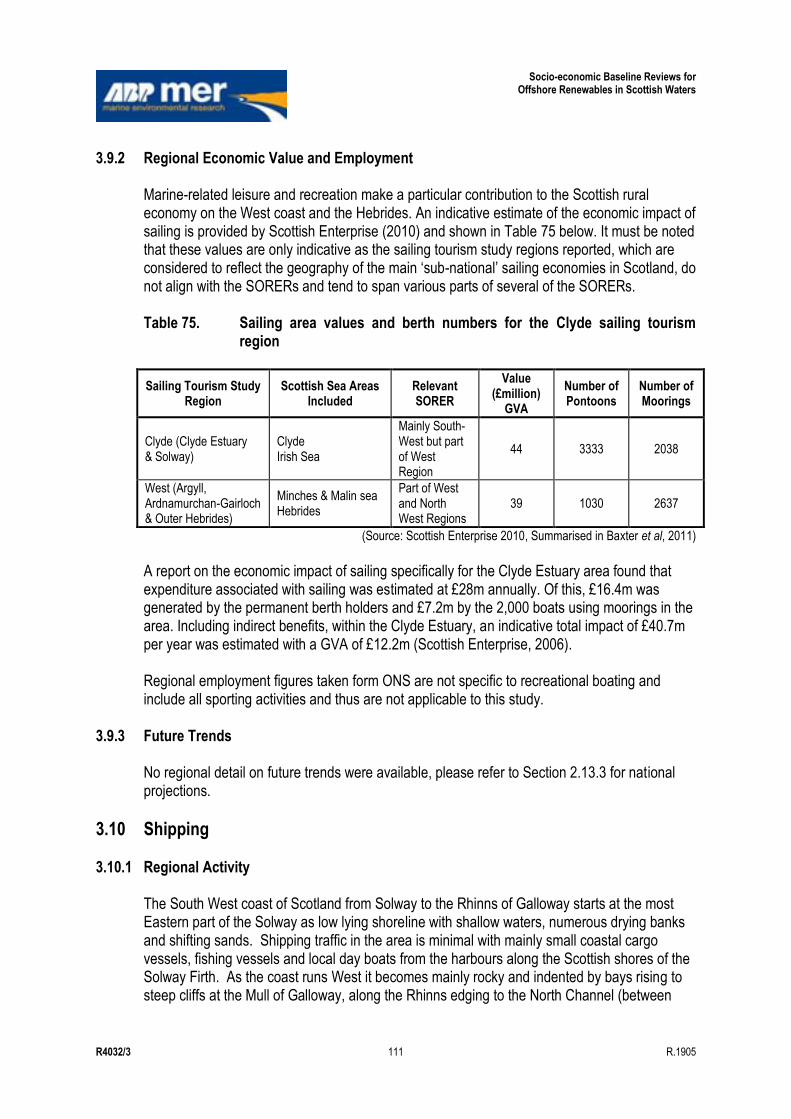

Socio-economic Baseline Reviews for Offshore Renewables in … · 2018-09-10 · Socio-economic...

329

Marine Scotland Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters Volume 1: Main Text Report R.1905 September 2012 RPA.

Transcript of Socio-economic Baseline Reviews for Offshore Renewables in … · 2018-09-10 · Socio-economic...

Marine Scotland

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters Volume 1: Main Text Report R.1905 September 2012

RPA.

Marine Scotland

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters Volume 2: Figures Report R.1905 September 2012

RPA.

All images copyright ABPmer apart from front cover (wave, anemone, bird) and policy & management (rockpool) Andy Pearson www.oceansedgephotography.co.uk

Marine Scotland

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters Date: September 2012

Project Ref: R4032/3

Report No: R.1905

© ABP Marine Environmental Research Ltd

Version Details of Change Authorised By Date

1 Working Copy C E Brown 02.12.11

2 Final C E Brown 07.02.12

3 Final C E Brown 26.04.12

4 Final C E Brown 28.06.12

5 Final C E Brown 24.09.12

Document Authorisation Signature Date

Project Manager: C E Brown

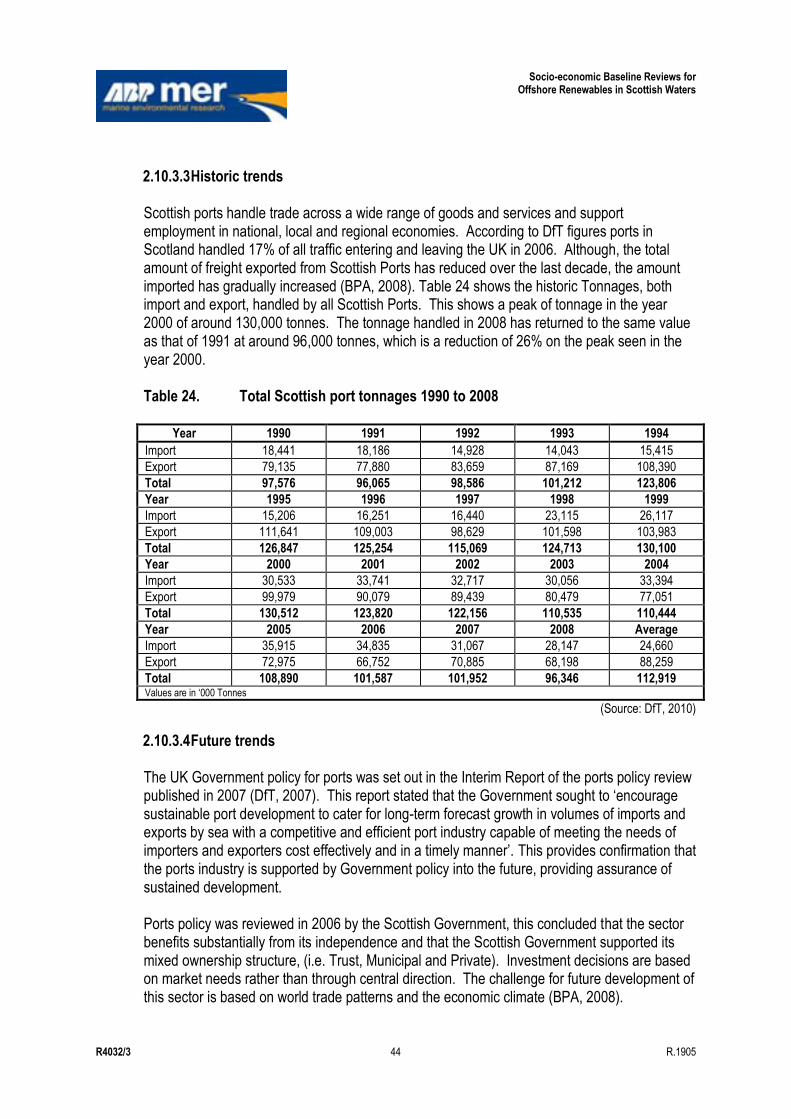

Quality Manager: H Roberts

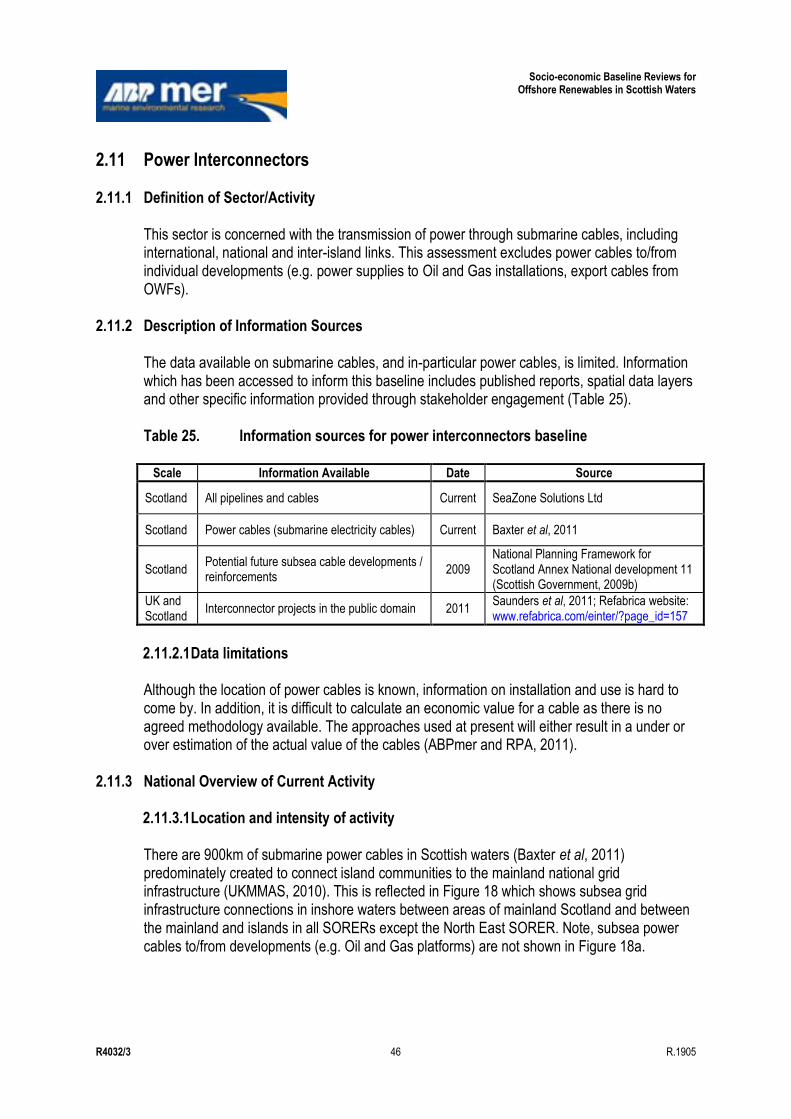

Project Director: S C Hull

ABP Marine Environmental Research Ltd Quayside Suite, Medina Chambers Town Quay Tel: +44(0)23 8071 1840 SOUTHAMPTON Fax: +44(0)23 8071 1841 Hampshire Web: www.abpmer.co.uk SO14 2AQ Email: [email protected]

ABPmer is certified by:

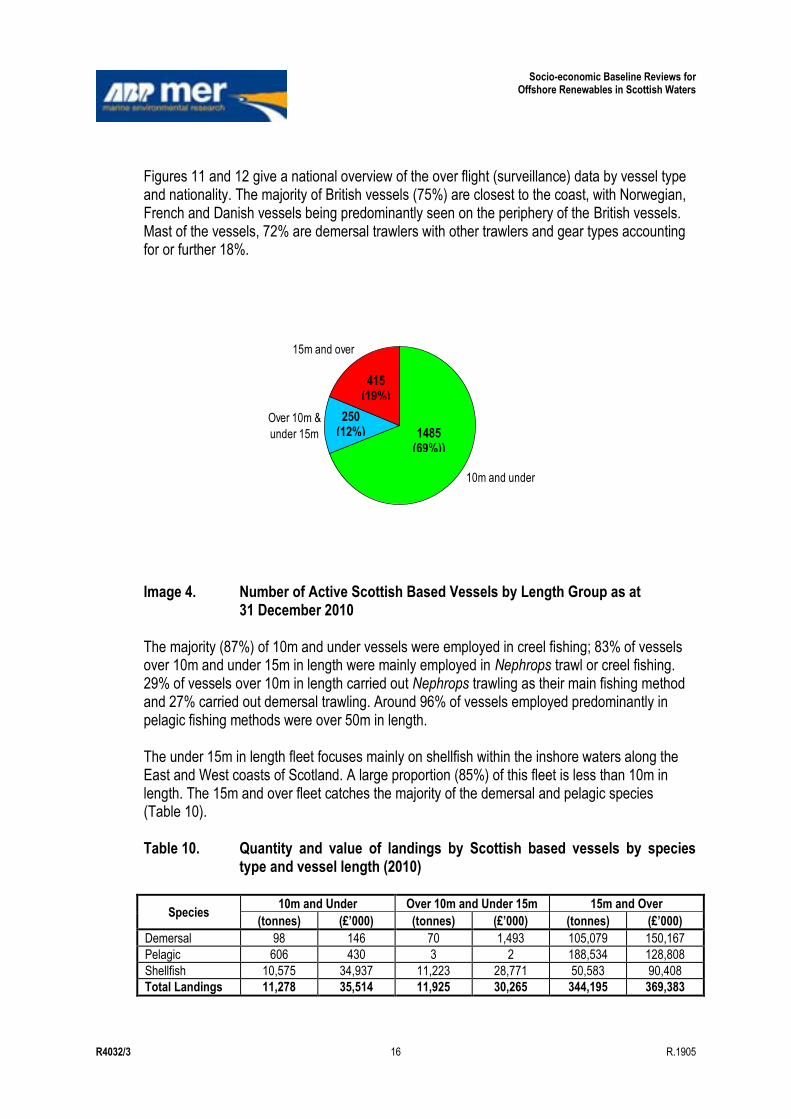

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

R4032/3 i R.1905

Summary ABP Marine Environmental Research Ltd (ABPmer) and RPA were commissioned by Marine Scotland to prepare a baseline socio-economic review to inform impact assessments of future sectoral plans for offshore wind and wave and tidal energy in Scottish Territorial Waters and waters offshore of Scotland (hereafter „Scottish Waters‟). This report provides a national overview of socio-economic activities together with regional baseline reviews covering the six Scottish Offshore Renewable Energy Regions (SORERs). The document is divided into two parts, the second providing the Figures referred to within this report.

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

R4032/3 ii R.1905

Abbreviations ABI Annual Business Inquiry ABP Associated British Ports ABPmer ABP Marine Environmental Research Ltd AIS Automatic Identification System ASP Association of Surfing Professionals ATM Air traffic Movements BAA British Aviation Authority BBC British Broadcasting Corporation BMF British Marine Federation BMI Body Mass Index BP BP Global BPA British Port Authority BSAC British Sub-Aqua Club BUTEC British Underwater Test and Evaluation Centre CAA Civil Aviation Authority CCS Carbon Capture and Storage Cefas Centre for Environment, Fisheries and Aquaculture Science CFP Common Fisheries Policy C-in-C Commander-in-Chief CNS Central North Sea CO2 Carbon dioxide COSLA Convention of Scottish Local Authorities CRC Control and Reporting Centre DAS Days at Sea DASA Defence Analytical Services and Advice DE&S Defence Equipment and Support DECC Department of Energy and Climate Change Defra Department for Environment, Food and Rural Affairs DEL Department Expenditure Limits DfT Department for Transport DMC Defence Munitions Centre DMK Denmark DNC Declared Net Capacity DUKES Digest of UK Energy Statistics DWT Deadweight ton E East EC European Community EEZ Exclusive Economic Zone EKOS EKOS Limited EMEC European Marine Energy Centre ERM Environmental Resources Management Ltd EU European Union FAA Fleet Air Arm FAO Food and Agriculture Organization FEE Foundation for Environmental Education

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

R4032/3 iii R.1905

FTE Full-time Equivalent GB Great Britain GC Gas Condenstate Field GDP Gross Domestic Product GHG Greenhouse Gas GLA General Lighthouse Authorities GP General Practitioners GVA Gross Value Added HDVC High Voltage Direct Current HIAL Highlands and Islands Airports Ltd. HIE Highlands and Islands Enterprise HIH Highest Income Householder HMNB Her Majesty‟s Naval Base HMS Her Majesty's Ship HPHT High Pressure High Temperature HVDC High-voltage Direct Current ICES International Council for the Exploration of the Sea ICIT International Centre of Island Technology ID Identity IFAW International Fund for Animal Welfare IMO International Maritime Organization IOM Isle of Man IPA IPA Energy + Water Economics IRM Inspection, repair and maintenance ITV ITV plc KIS-CA Kingfisher Information Service - Cable Awareness LA Local Authority LIMPET Land Installed Marine Powered Energy Transformer MCA Maritime and Coastguard Agency MCCIP Marine Climate Change Impacts MEDIN Marine Environmental Data and Information Network MMO Marine Management Organisation MOD Ministry of Defence MORI Market & Opinion Research International Ltd. MSc Master of Science MSC Marine Stewardship Council MSP Marine Spatial Plan MSY Maximum Sustainable Yield MW DNC Megawatts Declared Net Capacity N North NATO North Atlantic Treaty Organization NATS National Air Traffic Services NE North East NERL NATS En Route Plc NGL Natural Gas Liquids NI Northern Ireland NLB Northern Lighthouse Board

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

R4032/3 iv R.1905

NOMIS Service provided by the Office for National Statistics, ONS, to give you free access to the most detailed and up-to-date UK labour market statistics from official sources

NOx Nitrogen Oxide NRIP National Renewables Infrastructure Plan NVQ National Vocational Qualification NW North West OER Offshore Energy Region Ofgem Office of the Gas and Electricity Markets ONS Office for National Statistics OSGB Ordnance Survey Great Britain OSPAR International cooperation on the protection of the marine environment of the North-East

Atlantic. Commission is made up of representatives of the Governments of 15 Contracting Parties and the European Commission, representing the European Union.

OWF Offshore Wind Farm OWIG Offshore Wind Industry Group PAR Precision Approach Radar PEXA Practise and Exercise Training Area PFFPA Peterhead and Fraserburgh Fish Processors Association PFOW Pentland Firth and Orkney Waters PGI Protected Geographical Indication PSR Primary Surveillance Radar R&D Research and Development RAF Royal Air Force RoRo Roll-on/Roll-off RPA Risk and Policy Analysts RSW Refrigerated Seawater RYA Royal Yachting Association SAC Special Areas of Conservation SAS Surfers Against Sewage SCCS Scottish Centre for Carbon Storage ScotSAC Scottish Sub-Aqua Club SCSS Scottish Centre for Carbon Storage SCUBA Self Contained Underwater Breathing Apparatus SE Scottish Enterprise SEA Strategic Environmental Assessment SEB Scottish Enterprise Borders SECA SOx Emission Control Area SEPA Scottish Environment Protection Agency SFSAG Scottish Fisheries Sustainable Accreditation Group SHA Statutory Harbour Authorities SHEFA Shetland-Faroes SHQS Scottish Housing Quality Standard SIC Standard Industrial Classification SIMA Surf Industry Manufacturers Association SNH Scottish Natural Heritage SOAS School of Oriental and African Studies, University of London SORER Scottish Offshore Renewable Energy Regions

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

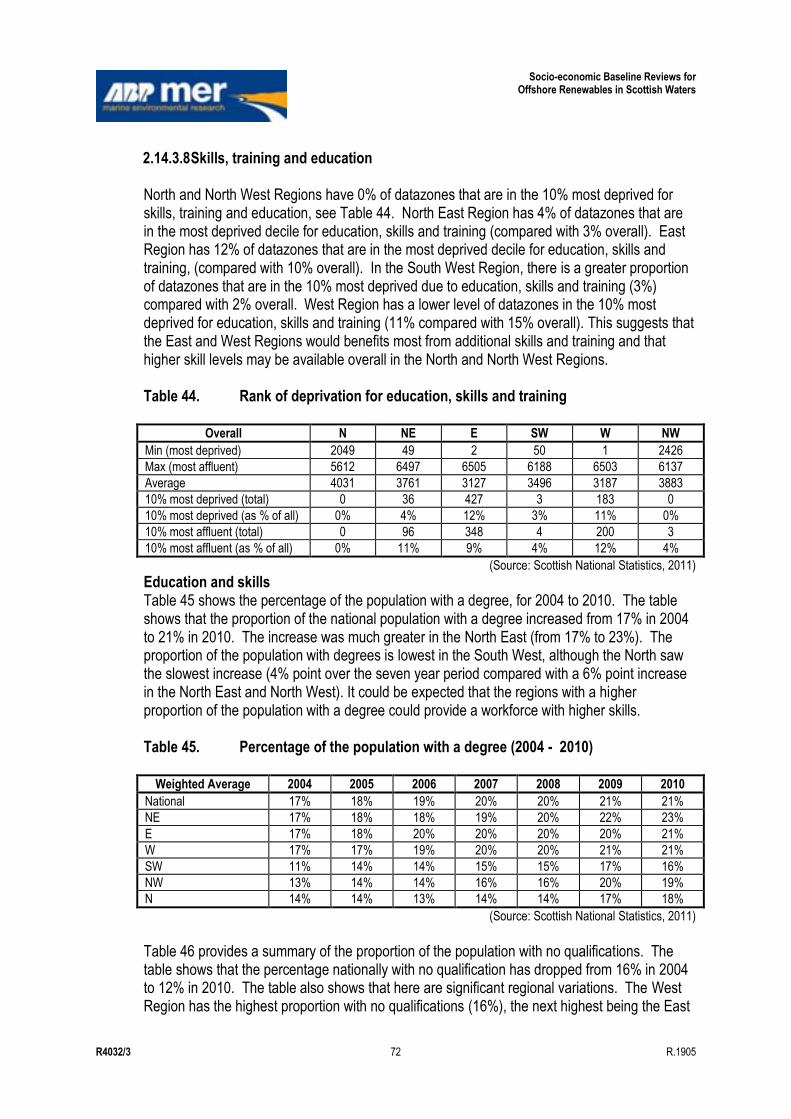

R4032/3 v R.1905

SOx Sulphur Oxide SPSG Scottish Pelagic Sustainability Group SQW SQW Consulting SREZ Scottish Renewable Energy Zone SRO Scottish Renewable Order SSACN Scottish Sea Angling Conservation Network SSE South South East SW South West SXA Scottish Exercise Area TAC Total Allowable Catch TNS The Naturist Society TSO The Stationery Office UK United Kingdom UKCPC UK Cable Protection Committee (to become Subsea Cables UK in 2012) UKCS UK Continental Shelf UKDEAL Oil & Gas UK DEAL Common Data Access Limited UKMMAS UK Marine Monitoring and Assessment Strategy USA United States of America VLCC Very-large Crude Carriers VMS Vessel Monitoring System W West WQS World Qualifying Series WWF World Wide Fund for Nature Units boe Barrel of Oil Equivalent m metre(s) km kilometre(s) km² kilometre(s) squared NM nautical mile(s) h hour lb pound(s) Kg kilogram(s) kV kilovolt(s) Mt million tonnes kW kilowatt(s) MW megawatt(s) MWe megawatt energy MWh megawatt hour GW gigawatt(s) GWh gigawatt hour GT gross tonnage p.a. per annum p.p. per person % per cent mppa million passengers per annum

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

R4032/3 vi R.1905

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

Contents Page

Summary .................................................................................................................................................. i

Abbreviations ........................................................................................................................................... ii

1. Introduction ................................................................................................................................. 1

2. National Overview ...................................................................................................................... 2 2.1 Introduction ................................................................................................................................. 2 2.2 Aquaculture ................................................................................................................................ 2

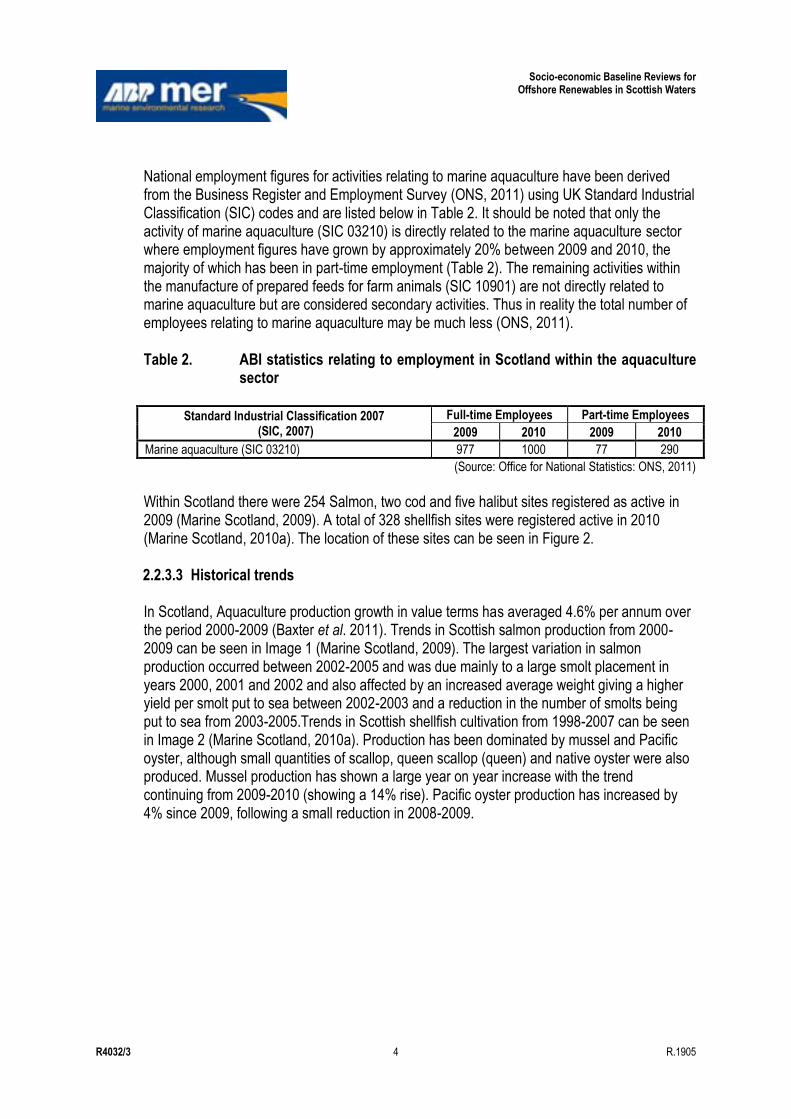

2.2.1 Definition of Sector/Activity........................................................................................... 2 2.2.2 Description of Information Sources .............................................................................. 2 2.2.3 National Overview of Current Activity ........................................................................... 3

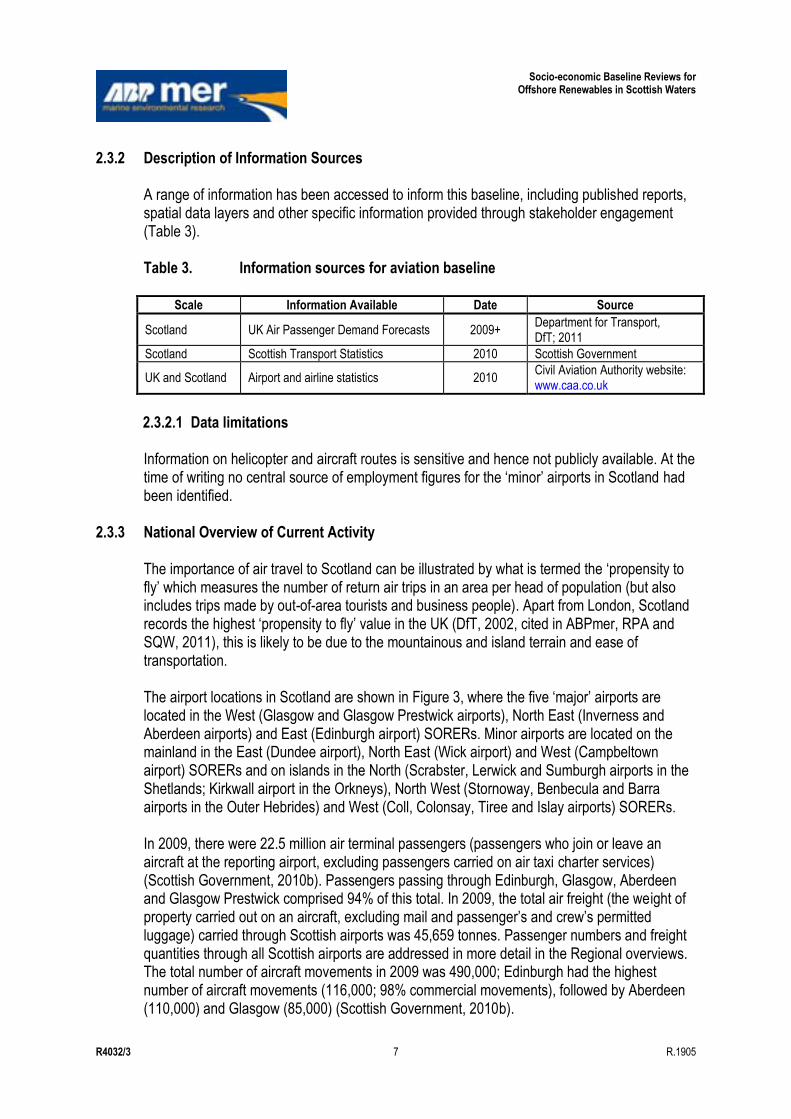

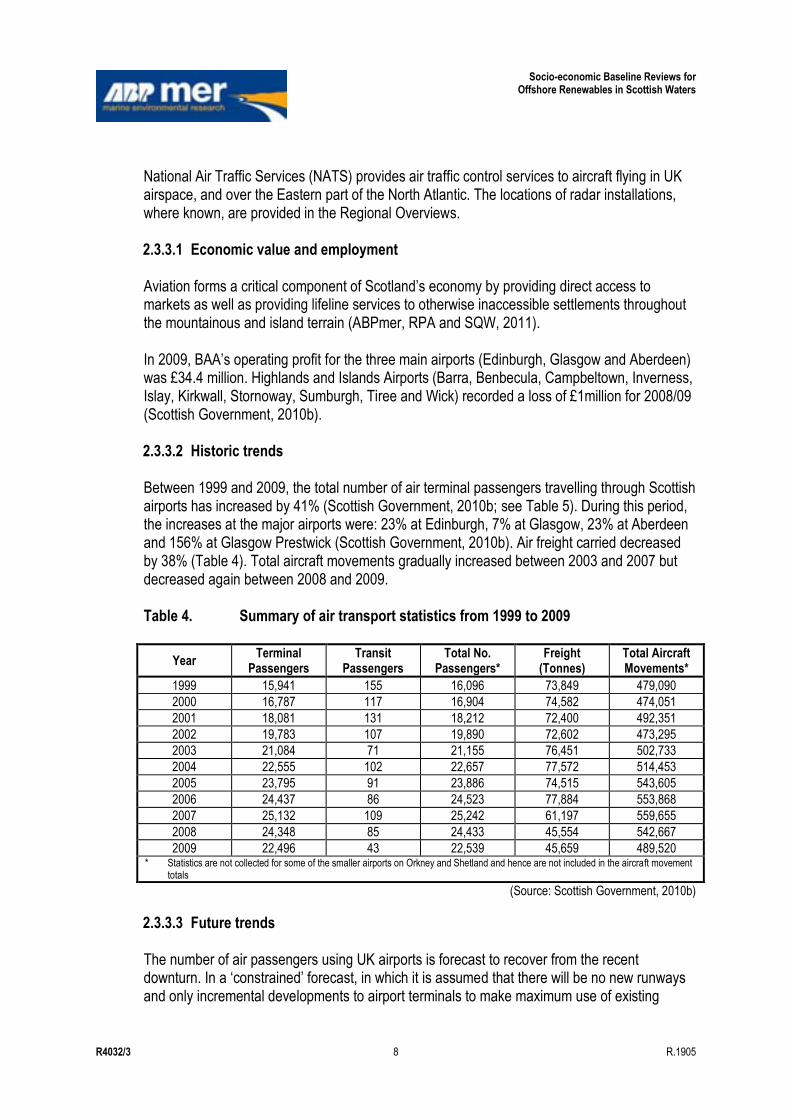

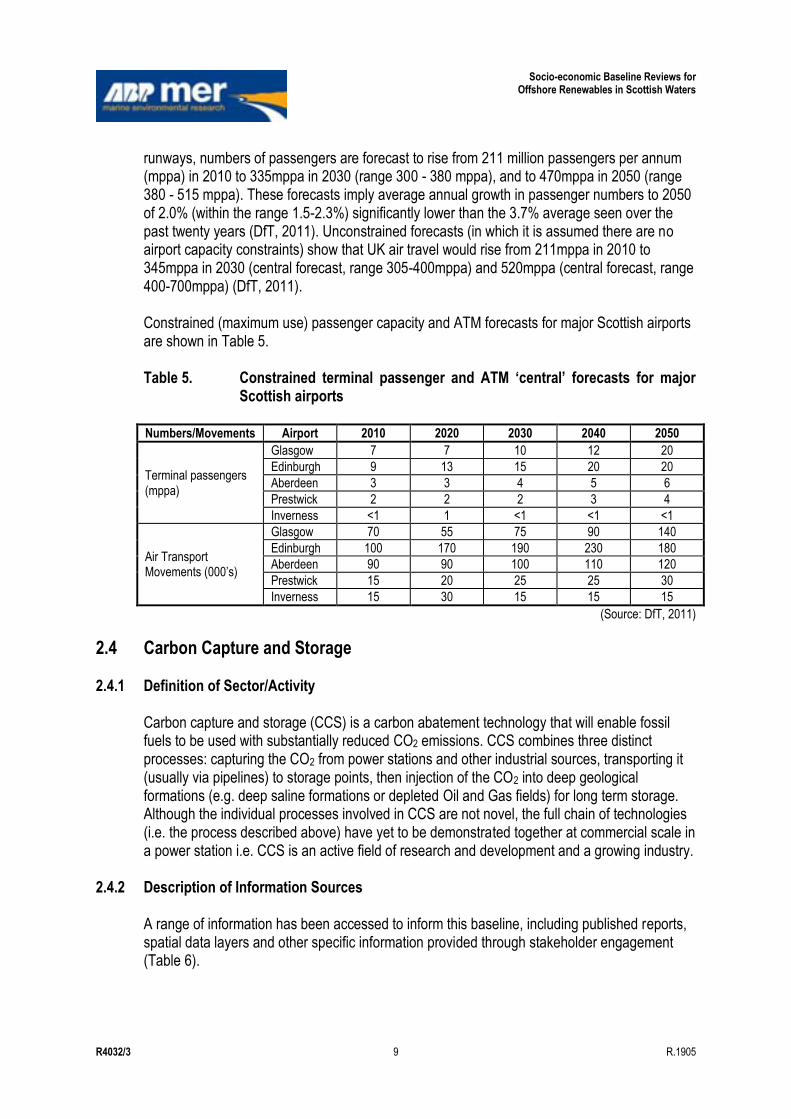

2.3 Aviation ....................................................................................................................................... 6 2.3.1 Definition of Sector/Activity........................................................................................... 6 2.3.2 Description of Information Sources .............................................................................. 7 2.3.3 National Overview of Current Activity ........................................................................... 7

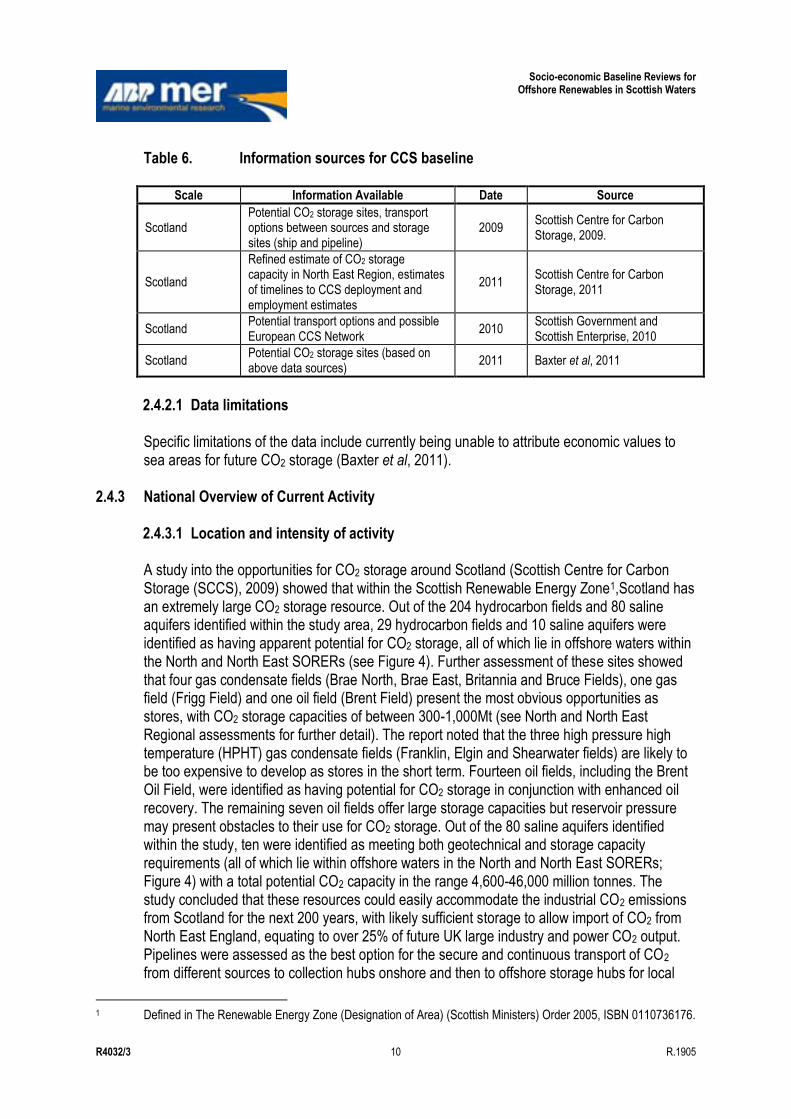

2.4 Carbon Capture and Storage ..................................................................................................... 9 2.4.1 Definition of Sector/Activity........................................................................................... 9 2.4.2 Description of Information Sources .............................................................................. 9 2.4.3 National Overview of Current Activity ......................................................................... 10

2.5 Coast Protection and Flood Defence ........................................................................................ 11 2.5.1 Definition of Sector/Activity......................................................................................... 11 2.5.2 Description of Information Sources ............................................................................ 12 2.5.3 National Overview of Current Activity ......................................................................... 12

2.6 Commercial Fisheries ............................................................................................................... 13 2.6.1 Definition of Sector/Activity......................................................................................... 13 2.6.2 Description of Information Sources ............................................................................ 13 2.6.3 National Overview of Current Activity ......................................................................... 14 2.6.4 Wild Salmon and Sea Trout ....................................................................................... 22

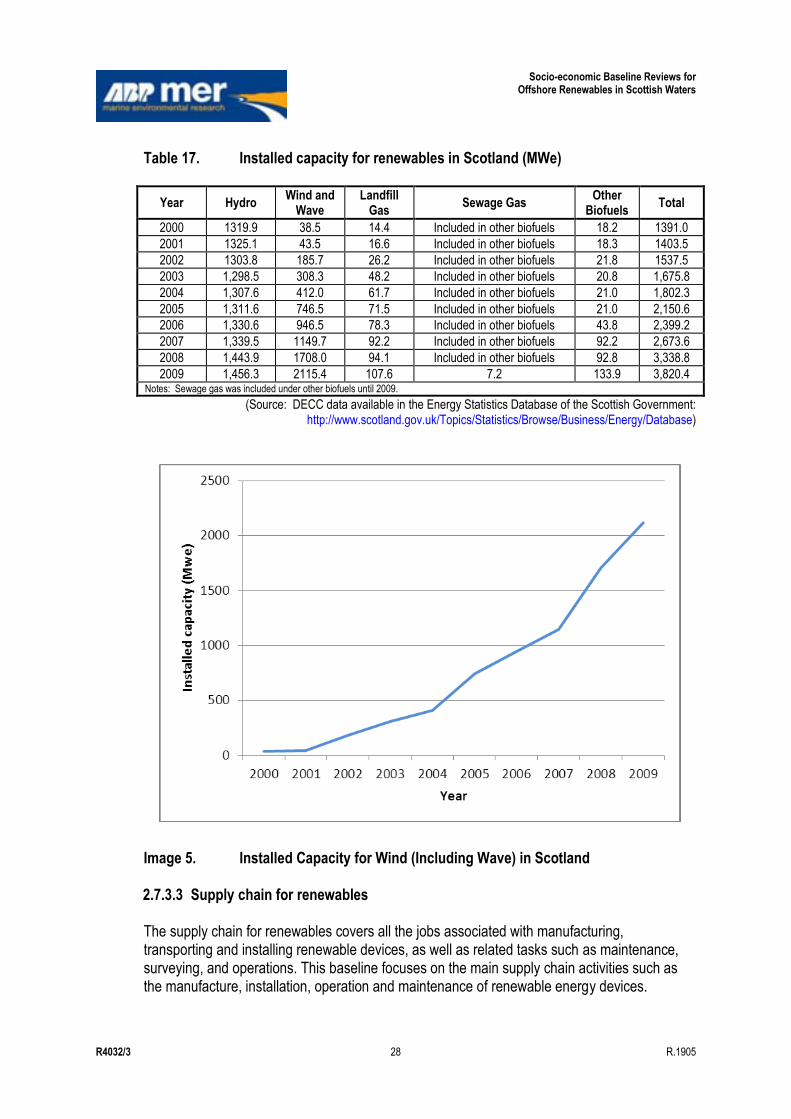

2.7 Energy Generation ................................................................................................................... 24 2.7.1 Definition of Sector/Activity......................................................................................... 24 2.7.2 Description of Information Sources ............................................................................ 25 2.7.3 National Overview of Current Activity ......................................................................... 26

2.8 Military Interests ....................................................................................................................... 34 2.8.1 Definition of Sector/Activity......................................................................................... 34 2.8.2 Description of Information Sources ............................................................................ 35 2.8.3 National Overview of Current Activity ......................................................................... 35

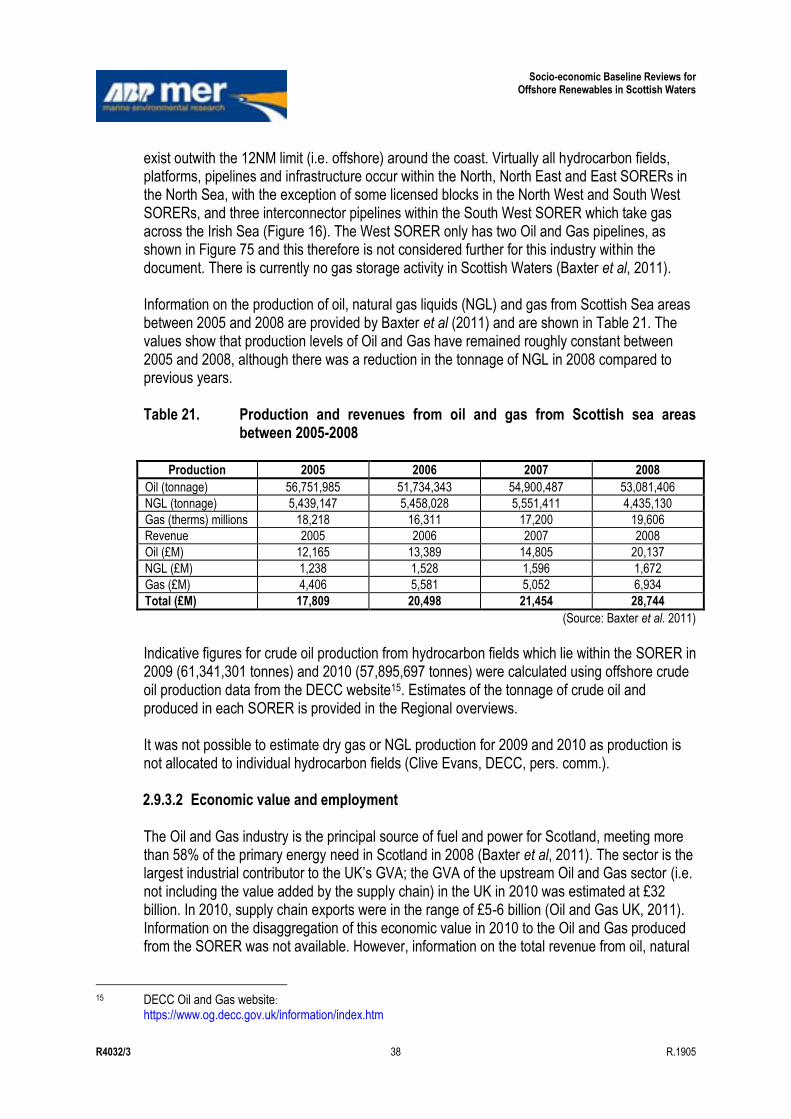

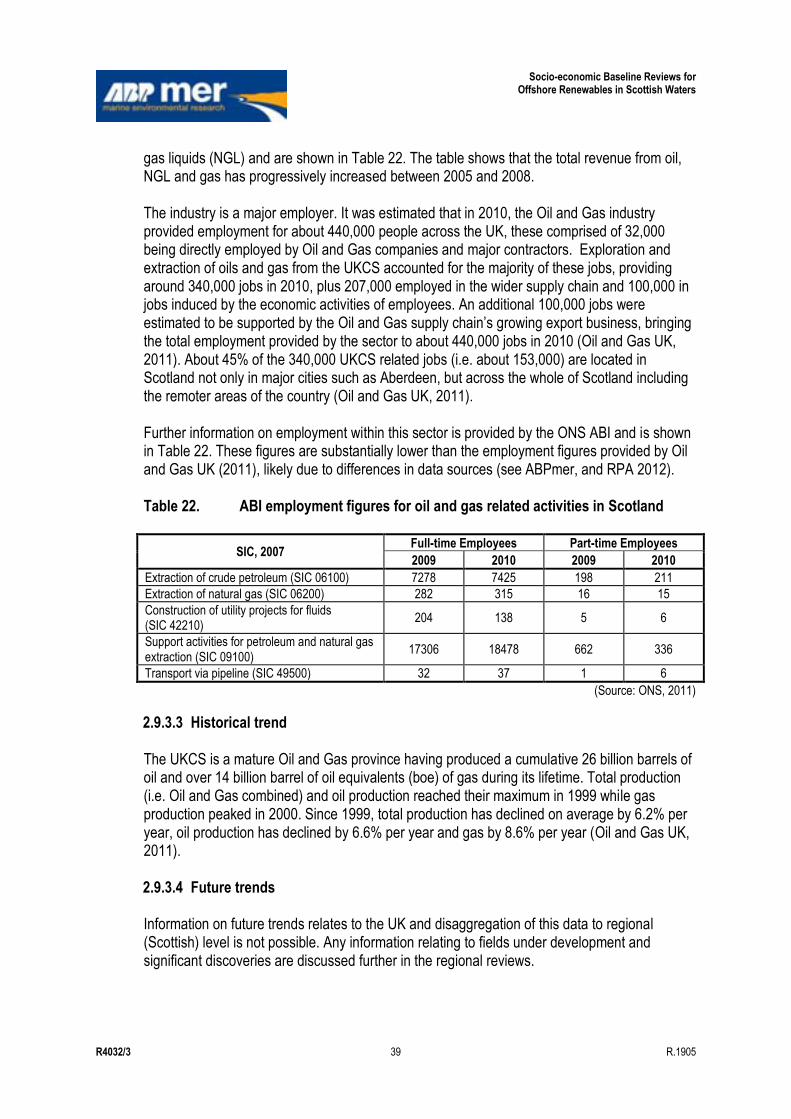

2.9 Oil and Gas .............................................................................................................................. 37 2.9.1 Definition of Sector/Activity......................................................................................... 37 2.9.2 Description of Information Sources ............................................................................ 37 2.9.3 National Overview of Current Activity ......................................................................... 37

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

R4032/3 vii R.1905

2.10 Ports and Harbours .................................................................................................................. 40

2.10.1 Definition of Sector/Activity......................................................................................... 40 2.10.2 Description of Information Sources ............................................................................ 40 2.10.3 National Overview of Current Activity ......................................................................... 41

2.11 Power Interconnectors .............................................................................................................. 46 2.11.1 Definition of Sector/Activity......................................................................................... 46 2.11.2 Description of Information Sources ............................................................................ 46 2.11.3 National Overview of Current Activity ......................................................................... 46

2.12 Recreational Boating ................................................................................................................ 48 2.12.1 Definition of Sector/Activity......................................................................................... 48 2.12.2 Description of Information Sources ............................................................................ 48 2.12.3 National Overview of Current Activity ......................................................................... 49

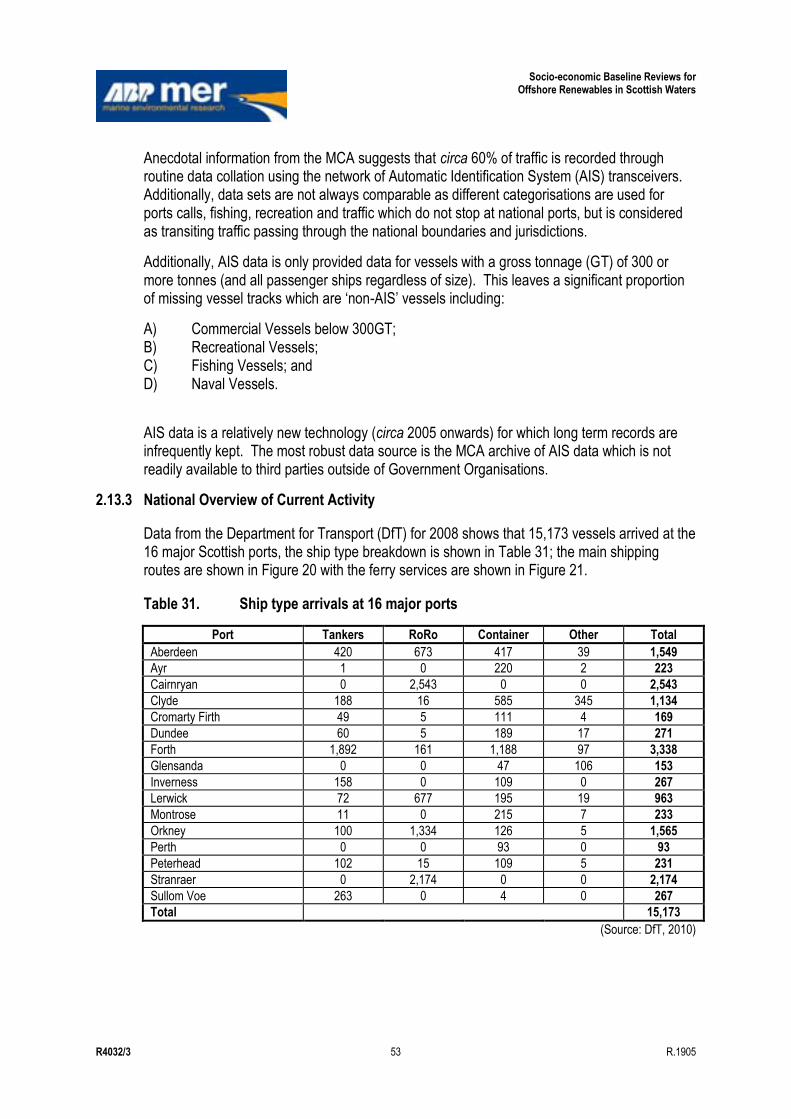

2.13 Shipping ................................................................................................................................... 52 2.13.1 Definition of Sector/Activity......................................................................................... 52 2.13.2 Description of Information Sources ............................................................................ 52 2.13.3 National Overview of Current Activity ......................................................................... 53

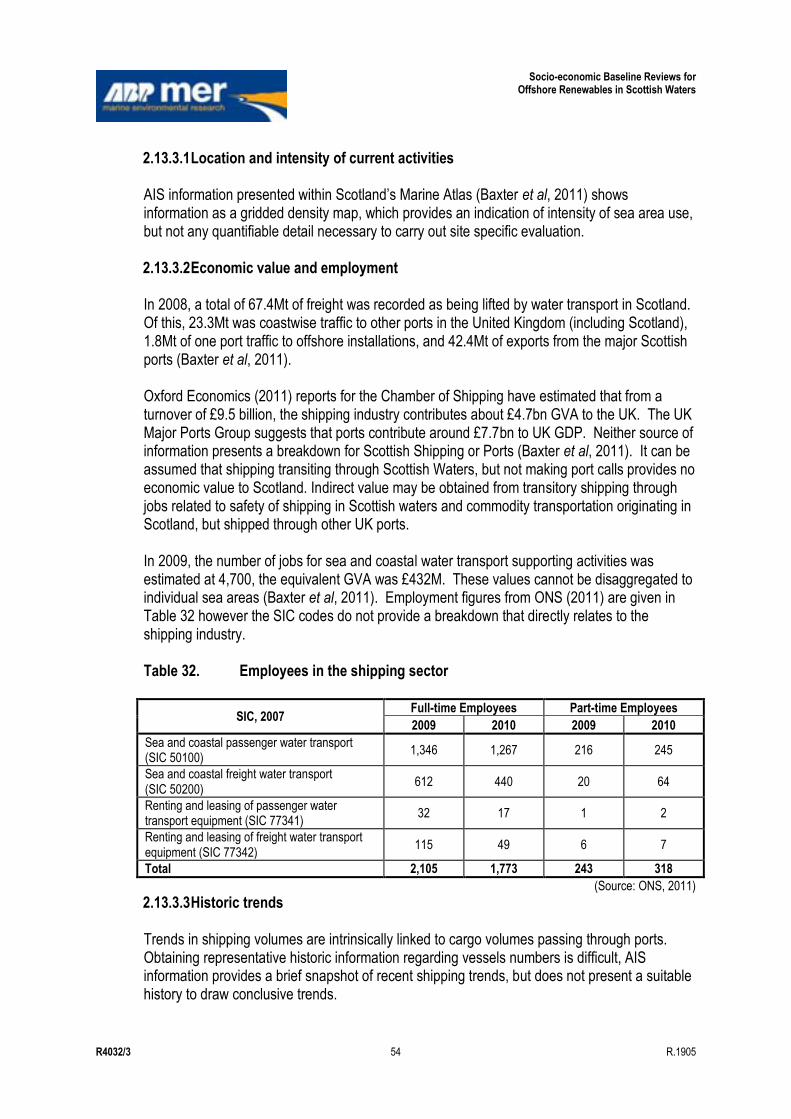

2.14 Social and Community .............................................................................................................. 56 2.14.1 Definition of Sector/Activity......................................................................................... 56 2.14.2 Description of Information Sources ............................................................................ 56 2.14.3 National Overview of Current Activity ......................................................................... 58

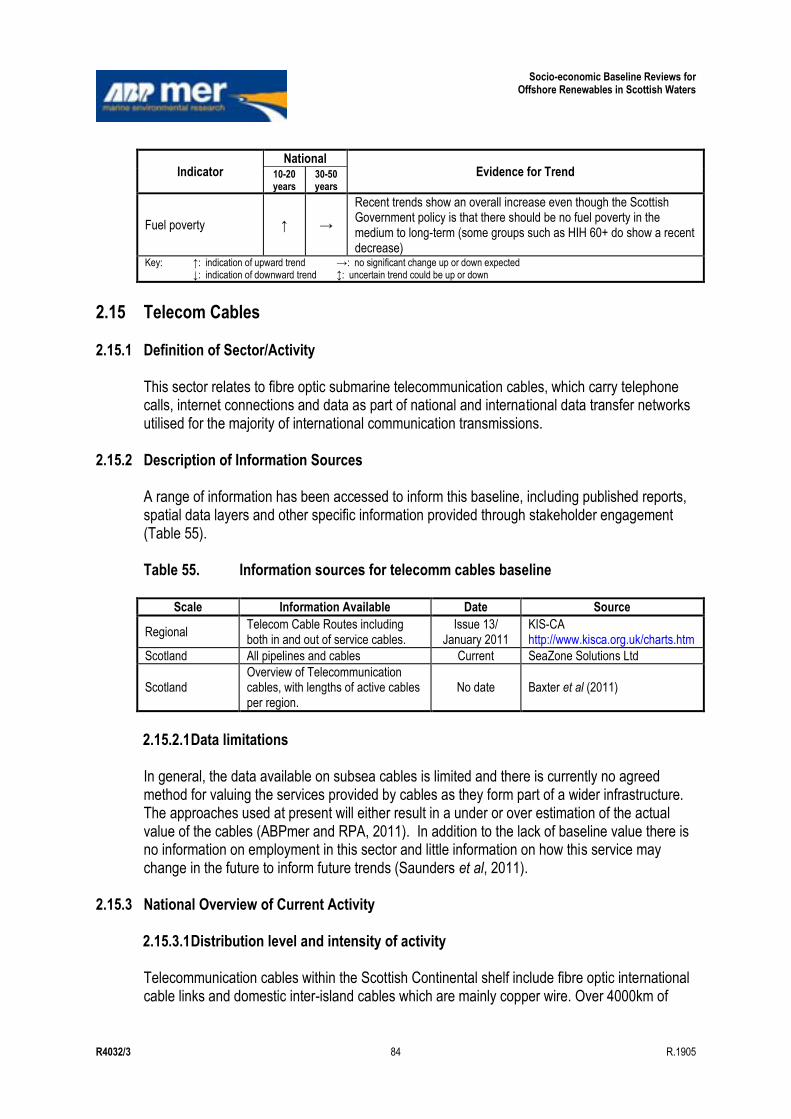

2.15 Telecom Cables........................................................................................................................ 84 2.15.1 Definition of Sector/Activity......................................................................................... 84 2.15.2 Description of Information Sources ............................................................................ 84 2.15.3 National Overview of Current Activity ......................................................................... 84

2.16 Tourism .................................................................................................................................... 86 2.16.1 Definition of Sector/Activity......................................................................................... 86 2.16.2 Description of Information Sources ............................................................................ 87 2.16.3 National Overview of Current Activity ......................................................................... 88

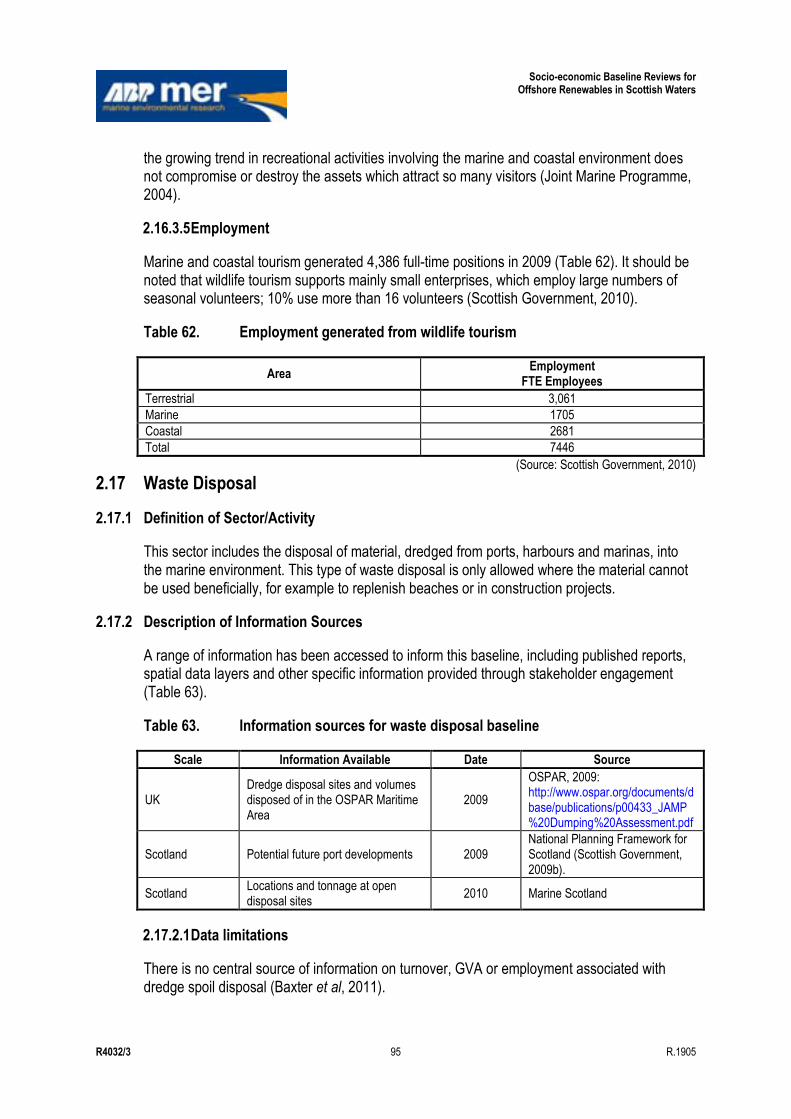

2.17 Waste Disposal......................................................................................................................... 95 2.17.1 Definition of Sector/Activity......................................................................................... 95 2.17.2 Description of Information Sources ............................................................................ 95 2.17.3 National Overview of Current Activity ......................................................................... 96 2.17.4 Economic value and employment .............................................................................. 96

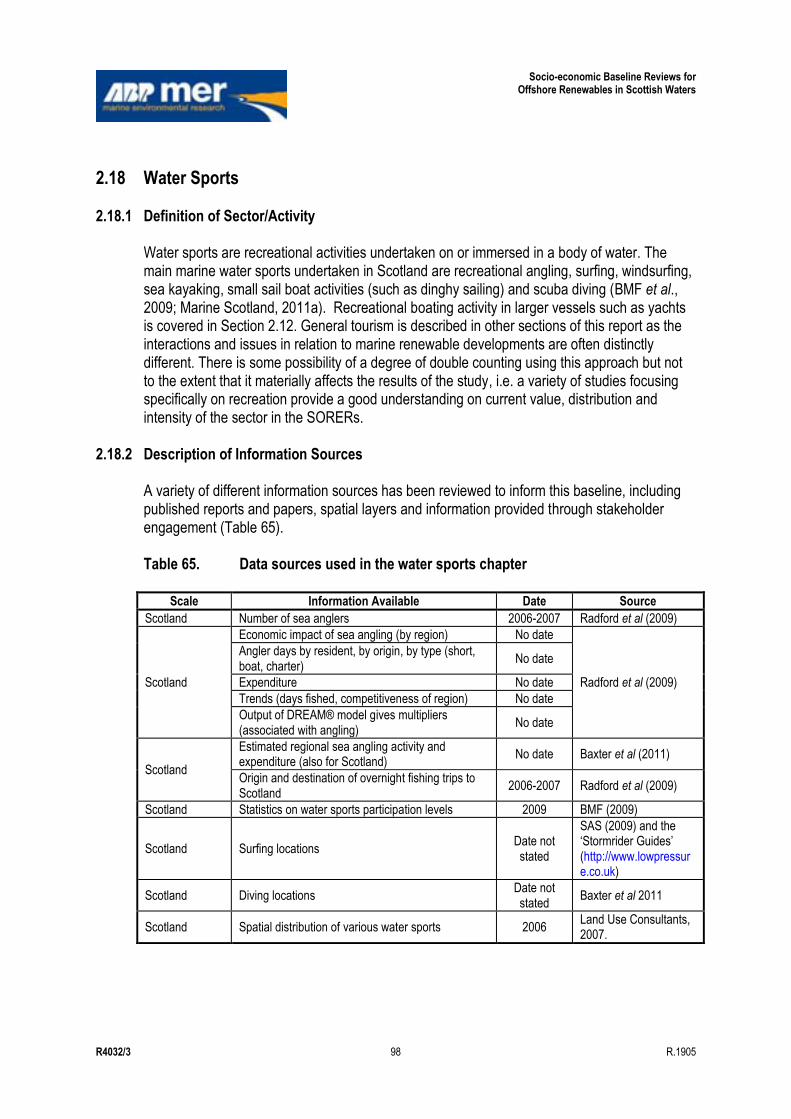

2.18 Water Sports ............................................................................................................................ 98 2.18.1 Definition of Sector/Activity......................................................................................... 98 2.18.2 Description of Information Sources ............................................................................ 98 2.18.3 National Overview of Current Activity ......................................................................... 99

3. South West Region ................................................................................................................. 103 3.1 Introduction ............................................................................................................................. 103 3.2 Aquaculture ............................................................................................................................ 103

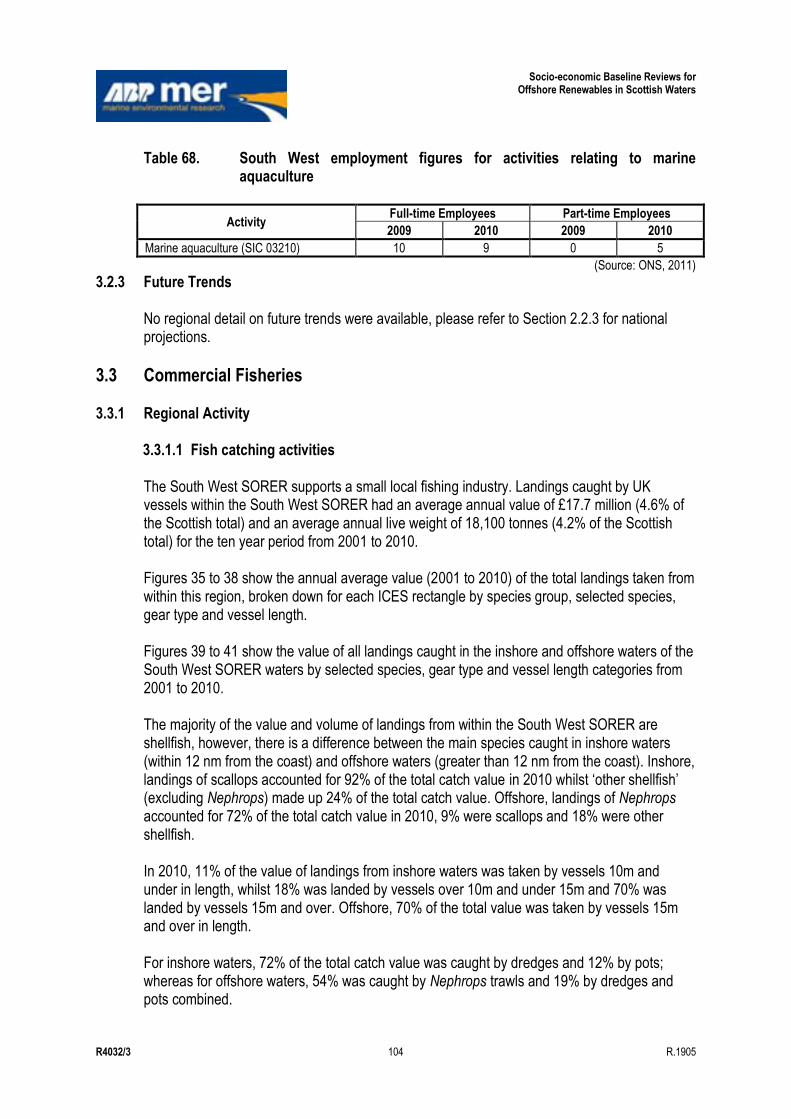

3.2.1 Regional Activity ....................................................................................................... 103 3.2.2 Regional Economic Value and Employment ............................................................ 103 3.2.3 Future Trends ........................................................................................................... 104

3.3 Commercial Fisheries ............................................................................................................. 104 3.3.1 Regional Activity ....................................................................................................... 104 3.3.2 Regional Economic Value and Employment ............................................................ 105 3.3.3 Future Trends ........................................................................................................... 106

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

R4032/3 viii R.1905

3.4 Energy Generation ................................................................................................................. 106

3.4.1 Regional Activity ....................................................................................................... 106 3.4.2 Regional Economic Value and Employment ............................................................ 106 3.4.3 Future Trends ........................................................................................................... 107

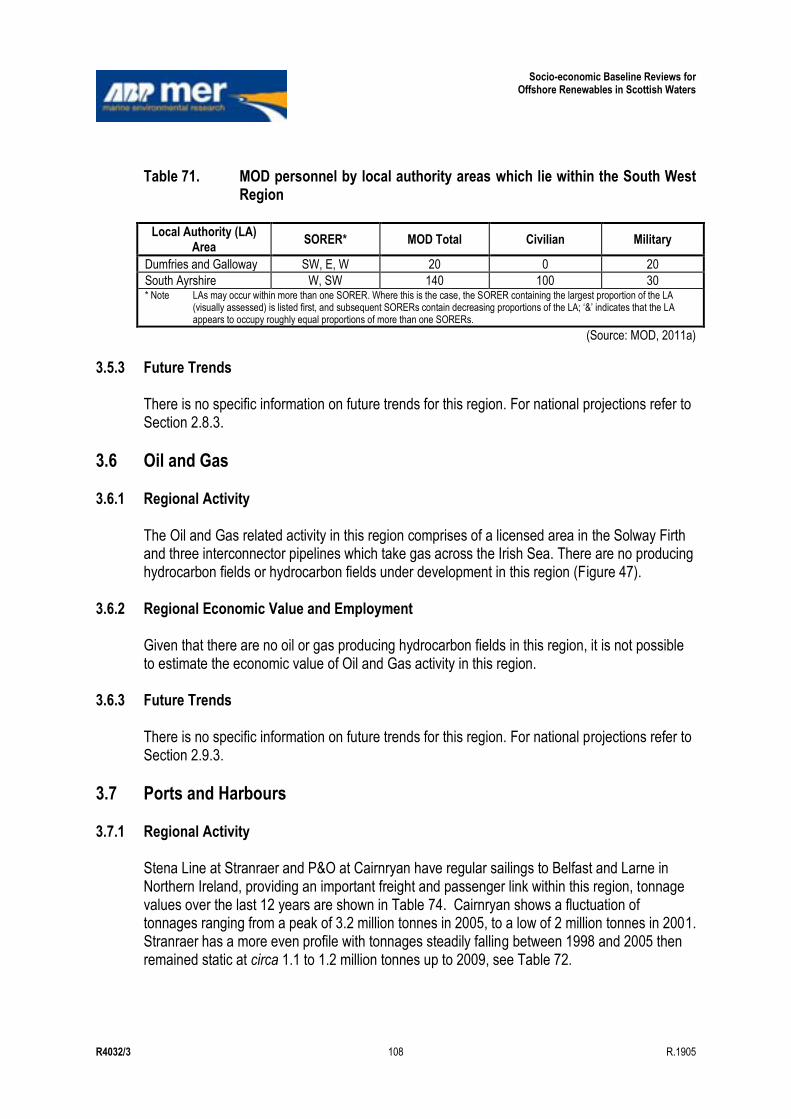

3.5 Military Interests ..................................................................................................................... 107 3.5.1 Regional Activity ....................................................................................................... 107 3.5.2 Regional Economic Value and Employment ............................................................ 107 3.5.3 Future Trends ........................................................................................................... 108

3.6 Oil and Gas ............................................................................................................................ 108 3.6.1 Regional Activity ....................................................................................................... 108 3.6.2 Regional Economic Value and Employment ............................................................ 108 3.6.3 Future Trends ........................................................................................................... 108

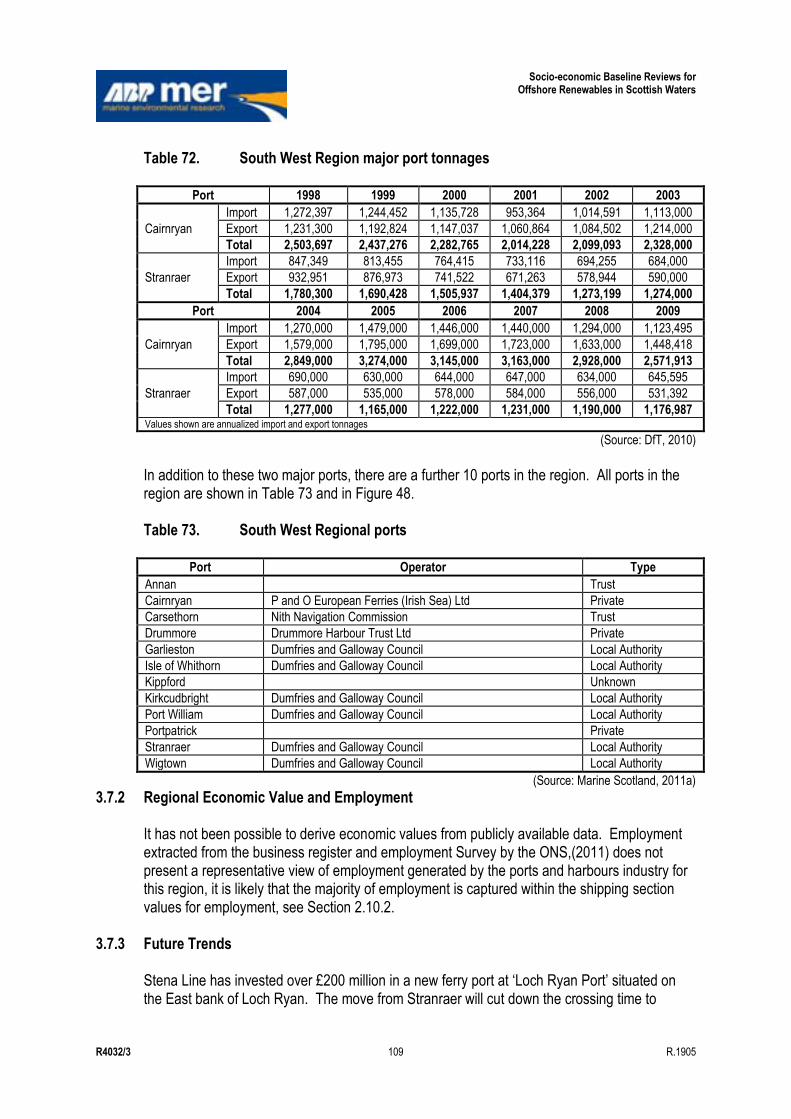

3.7 Ports and Harbours ................................................................................................................ 108 3.7.1 Regional Activity ....................................................................................................... 108 3.7.2 Regional Economic Value and Employment ............................................................ 109 3.7.3 Future Trends ........................................................................................................... 109

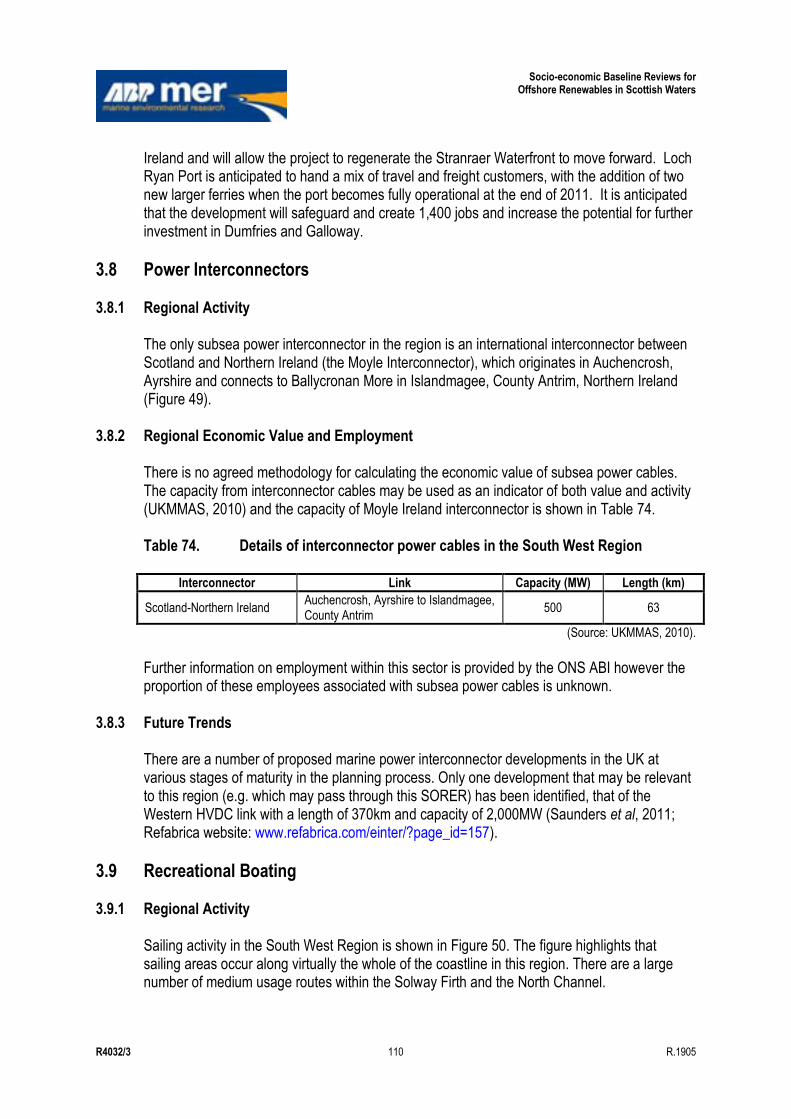

3.8 Power Interconnectors ............................................................................................................ 110 3.8.1 Regional Activity ....................................................................................................... 110 3.8.2 Regional Economic Value and Employment ............................................................ 110 3.8.3 Future Trends ........................................................................................................... 110

3.9 Recreational Boating .............................................................................................................. 110 3.9.1 Regional Activity ....................................................................................................... 110 3.9.2 Regional Economic Value and Employment ............................................................ 111 3.9.3 Future Trends ........................................................................................................... 111

3.10 Shipping ................................................................................................................................. 111 3.10.1 Regional Activity ....................................................................................................... 111 3.10.2 Regional Economic Value and Employment ............................................................ 112 3.10.3 Future Trends ........................................................................................................... 113

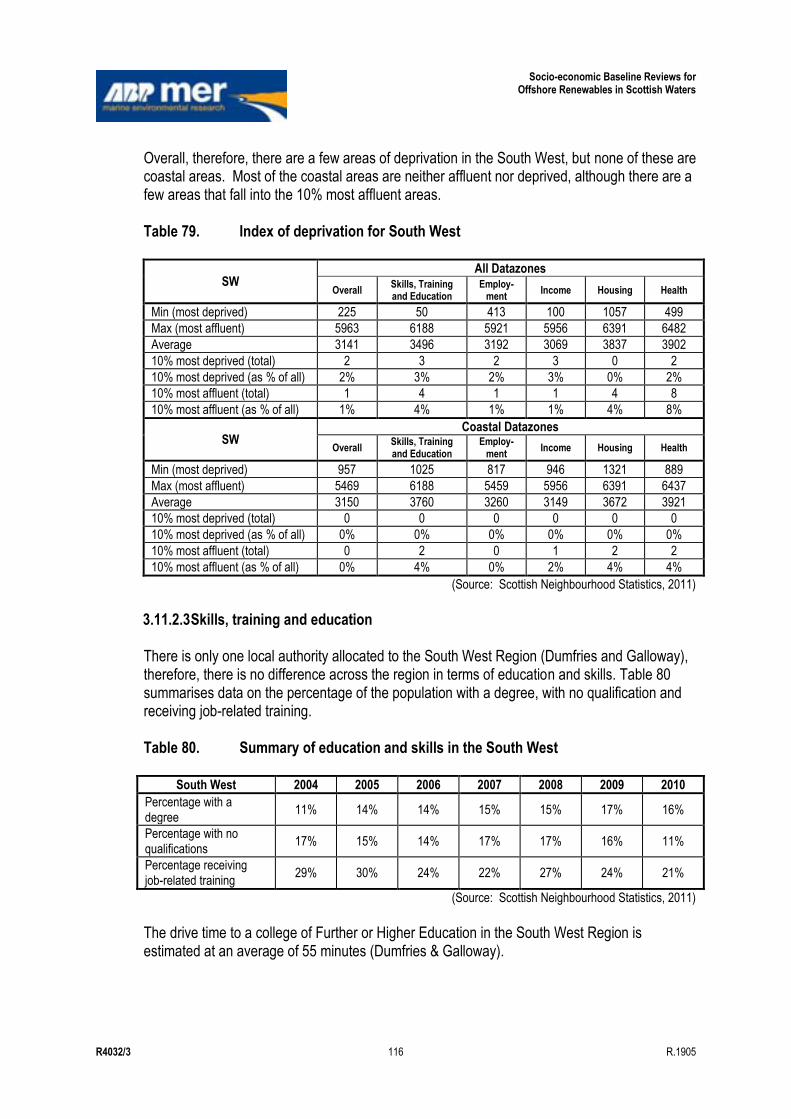

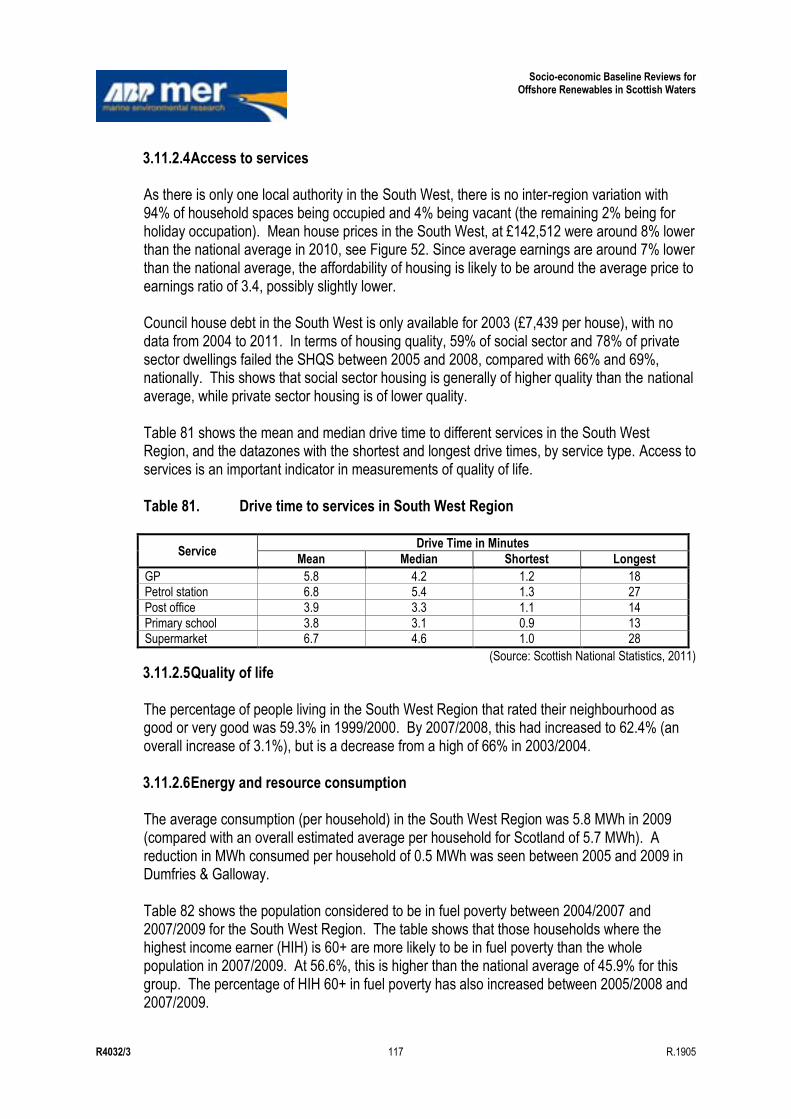

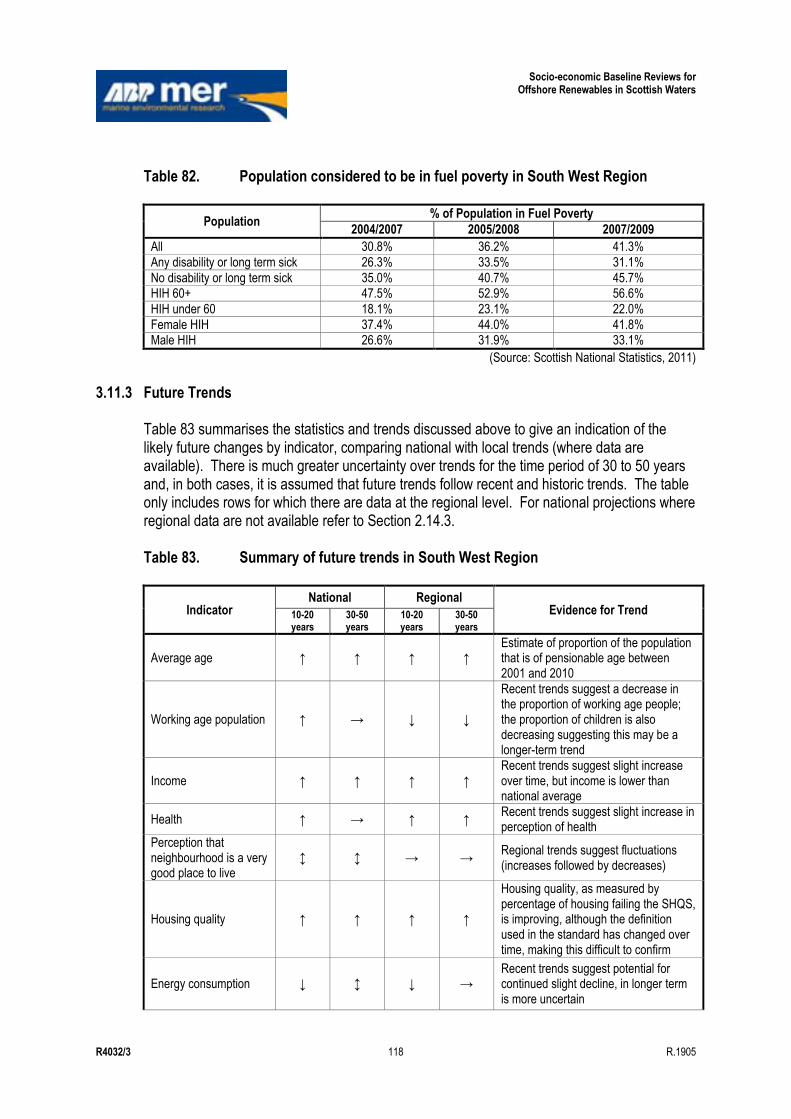

3.11 Social and Community ............................................................................................................ 113 3.11.1 Regional Activity ....................................................................................................... 113 3.11.2 Regional Economic Value and Employment ............................................................ 114 3.11.3 Future Trends ........................................................................................................... 118

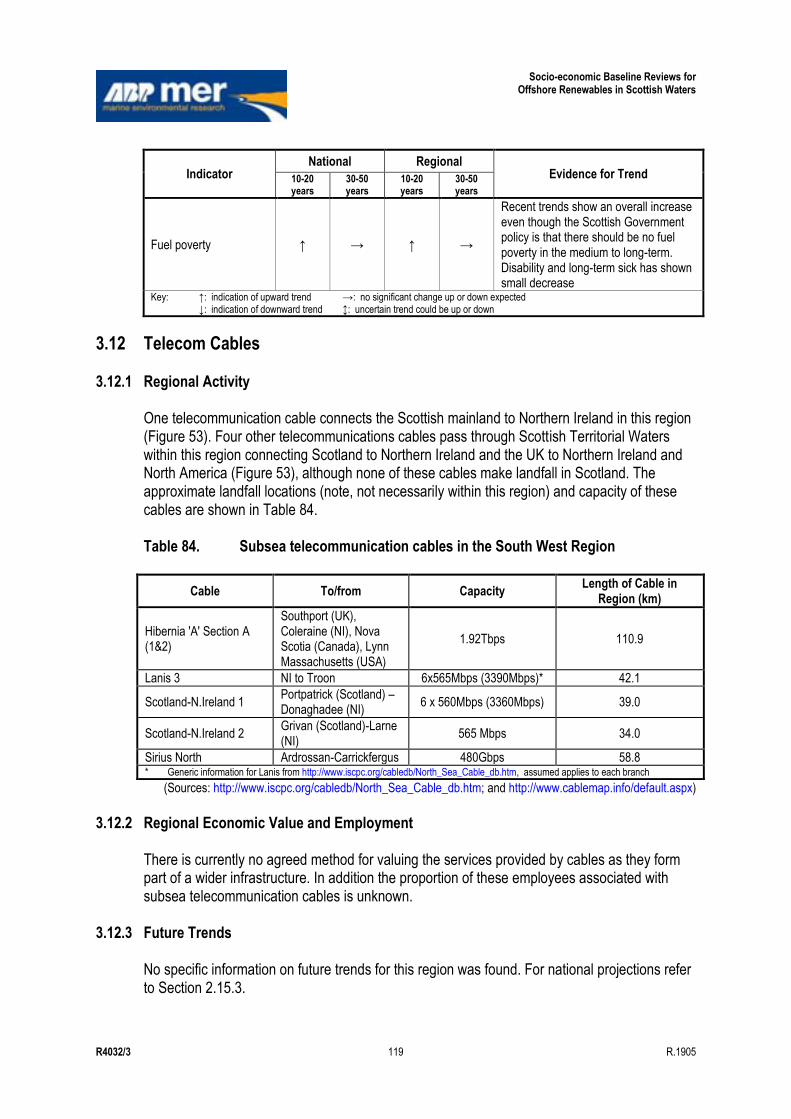

3.12 Telecom Cables...................................................................................................................... 119 3.12.1 Regional Activity ....................................................................................................... 119 3.12.2 Regional Economic Value and Employment ............................................................ 119 3.12.3 Future Trends ........................................................................................................... 119

3.13 Tourism .................................................................................................................................. 120 3.13.1 Regional Activity ....................................................................................................... 120 3.13.2 Regional Economic Value and Employment ............................................................ 120 3.13.3 Future Trends ........................................................................................................... 120

3.14 Waste Disposal....................................................................................................................... 120 3.14.1 Regional Activity ....................................................................................................... 120 3.14.2 Regional Economic Value and Employment ............................................................ 121 3.14.3 Future Trends ........................................................................................................... 121

3.15 Water Sports .......................................................................................................................... 122 3.15.1 Regional activity ....................................................................................................... 122 3.15.2 Regional Economic Value and Employment ............................................................ 122 3.15.3 Future Trends ........................................................................................................... 123

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

R4032/3 ix R.1905

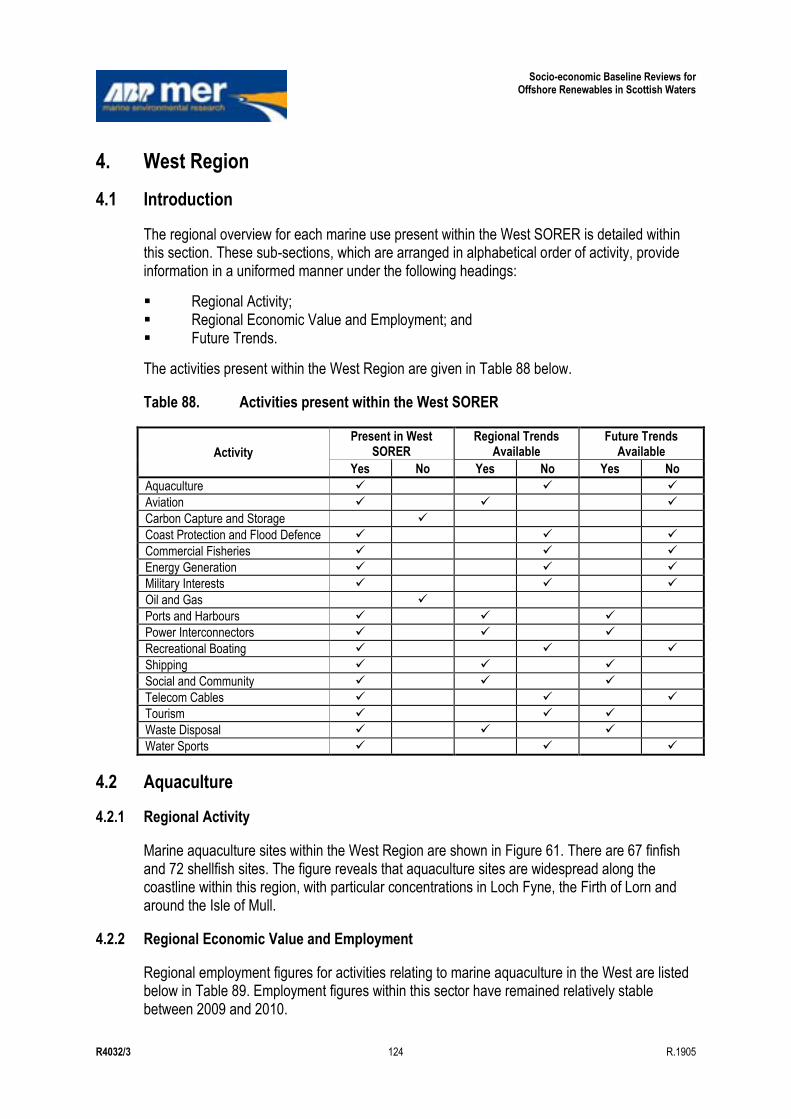

4. West Region ........................................................................................................................... 124 4.1 Introduction ............................................................................................................................. 124 4.2 Aquaculture ............................................................................................................................ 124

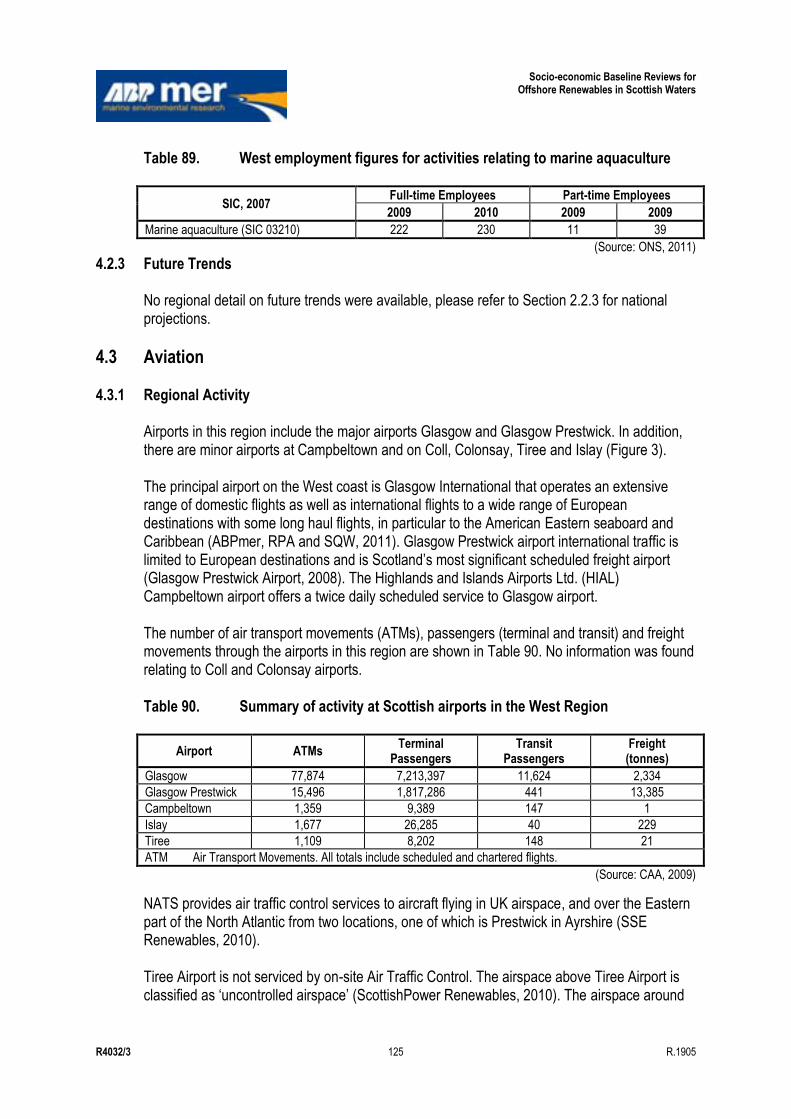

4.2.1 Regional Activity ....................................................................................................... 124 4.2.2 Regional Economic Value and Employment ............................................................ 124 4.2.3 Future Trends ........................................................................................................... 125

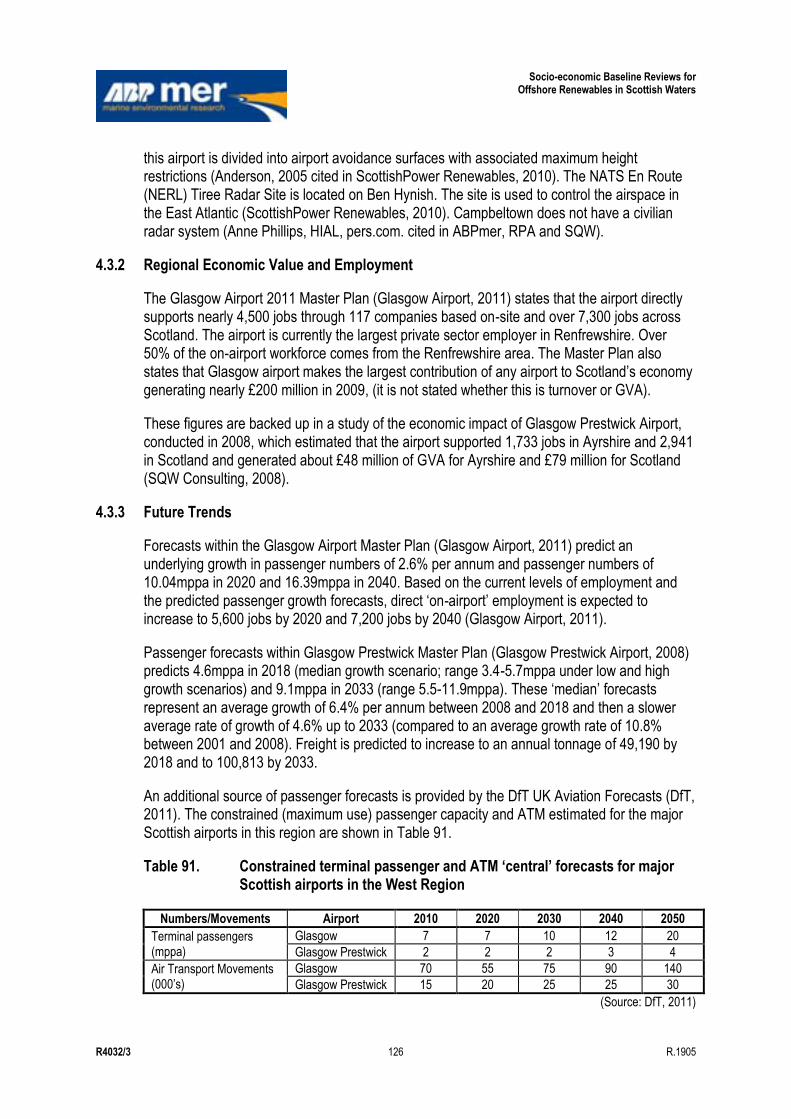

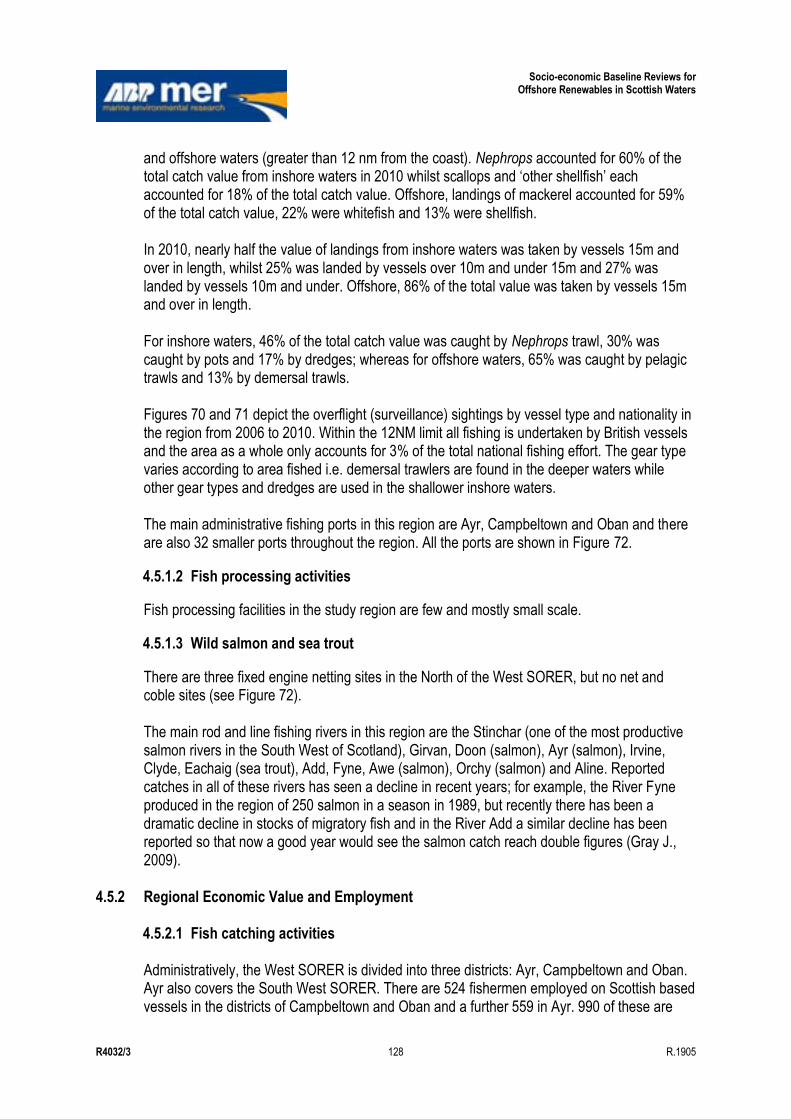

4.3 Aviation ................................................................................................................................... 125 4.3.1 Regional Activity ....................................................................................................... 125 4.3.2 Regional Economic Value and Employment ............................................................ 126 4.3.3 Future Trends ........................................................................................................... 126

4.4 Coast Protection and Flood Defence ...................................................................................... 127 4.4.1 Regional Activity ....................................................................................................... 127 4.4.2 Regional Economic Value and Employment ............................................................ 127 4.4.3 Future Trends ........................................................................................................... 127

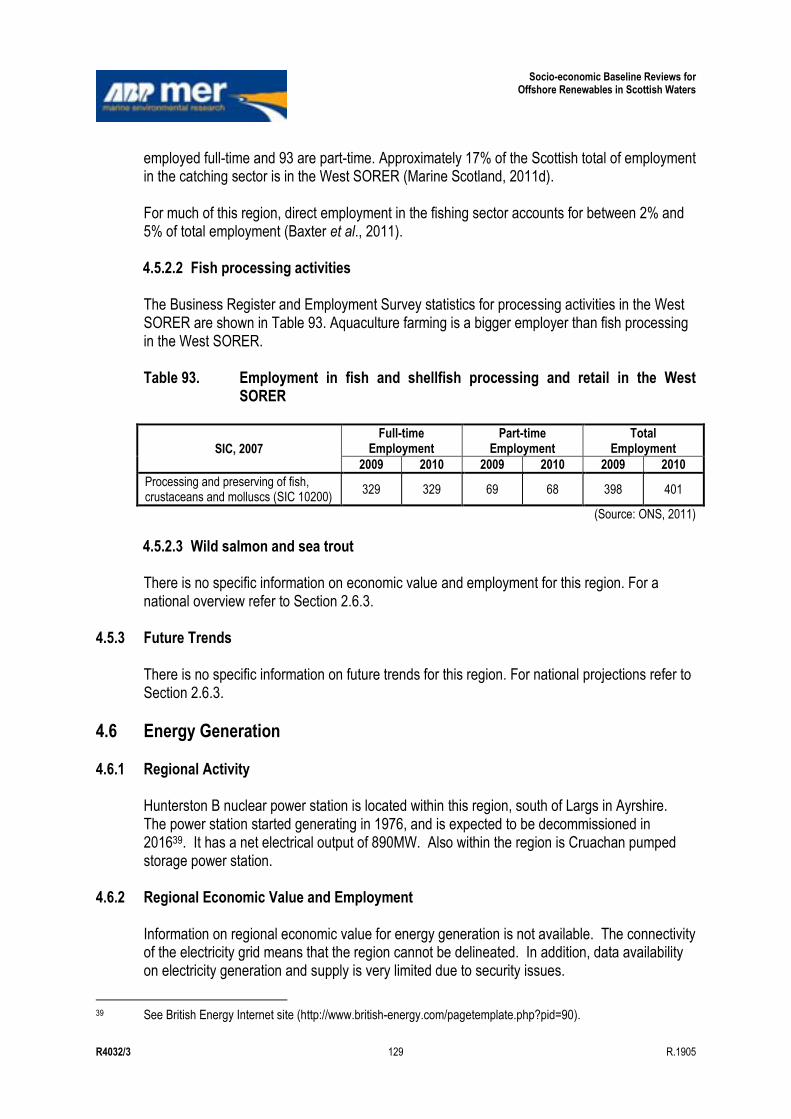

4.5 Commercial Fishing ................................................................................................................ 127 4.5.1 Regional Activity ....................................................................................................... 127 4.5.2 Regional Economic Value and Employment ............................................................ 128 4.5.3 Future Trends ........................................................................................................... 129

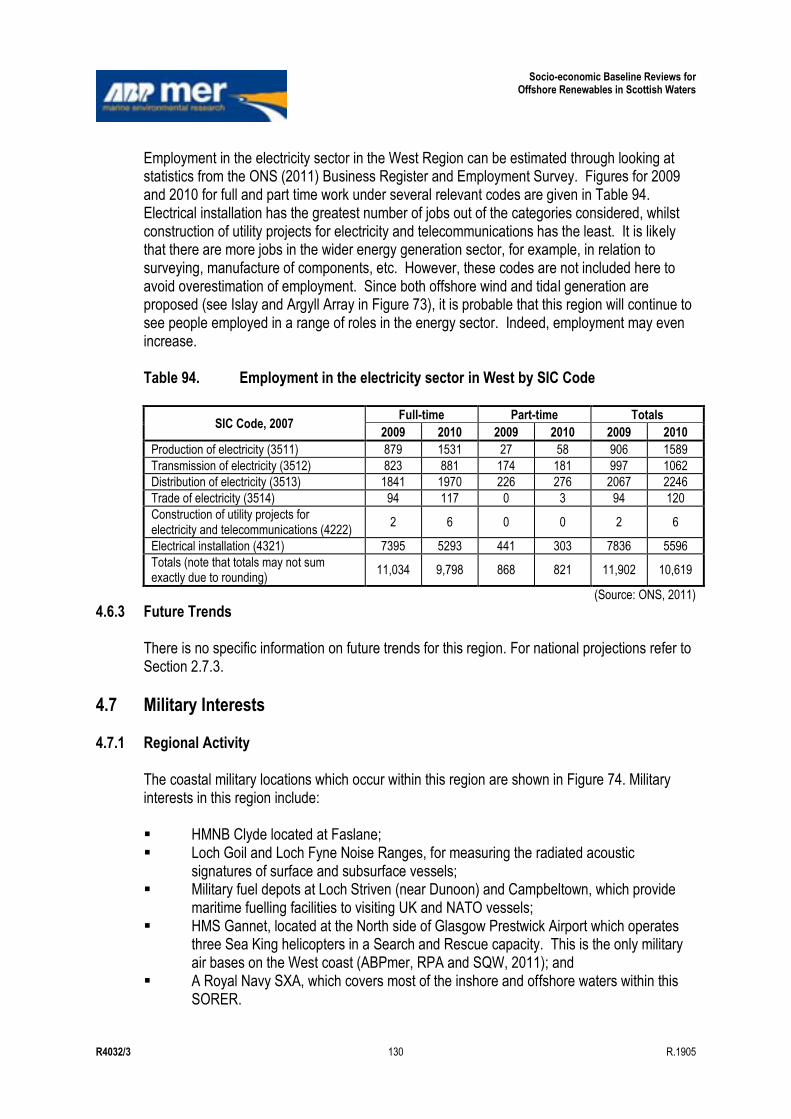

4.6 Energy Generation ................................................................................................................. 129 4.6.1 Regional Activity ....................................................................................................... 129 4.6.2 Regional Economic Value and Employment ............................................................ 129 4.6.3 Future Trends ........................................................................................................... 130

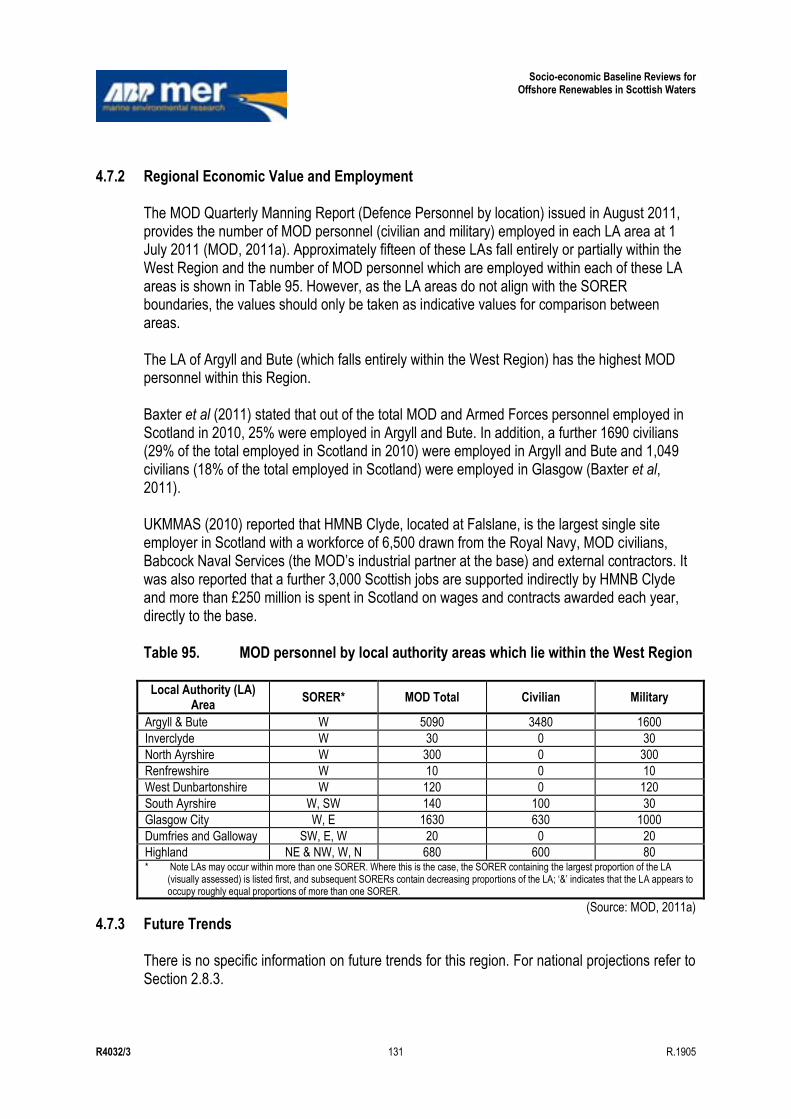

4.7 Military Interests ..................................................................................................................... 130 4.7.1 Regional Activity ....................................................................................................... 130 4.7.2 Regional Economic Value and Employment ............................................................ 131 4.7.3 Future Trends ........................................................................................................... 131

4.8 Port and Harbours .................................................................................................................. 132 4.8.1 Regional Activity ....................................................................................................... 132 4.8.2 Regional Economic Value and Employment ............................................................ 134 4.8.3 Future Trends ........................................................................................................... 135

4.9 Power Interconnectors ............................................................................................................ 135 4.9.1 Regional Activity ....................................................................................................... 135 4.9.2 Regional Economic Value and Employment ............................................................ 135 4.9.3 Future Trends ........................................................................................................... 136

4.10 Recreational Boating .............................................................................................................. 136 4.10.1 Regional Activity ....................................................................................................... 136 4.10.2 Regional Economic Value and Employment ............................................................ 137 4.10.3 Future Trends ........................................................................................................... 137

4.11 Shipping ................................................................................................................................. 137 4.11.1 Regional Activity ....................................................................................................... 137 4.11.2 Regional Economic Value and Employment ............................................................ 139 4.11.3 Future Trends ........................................................................................................... 140

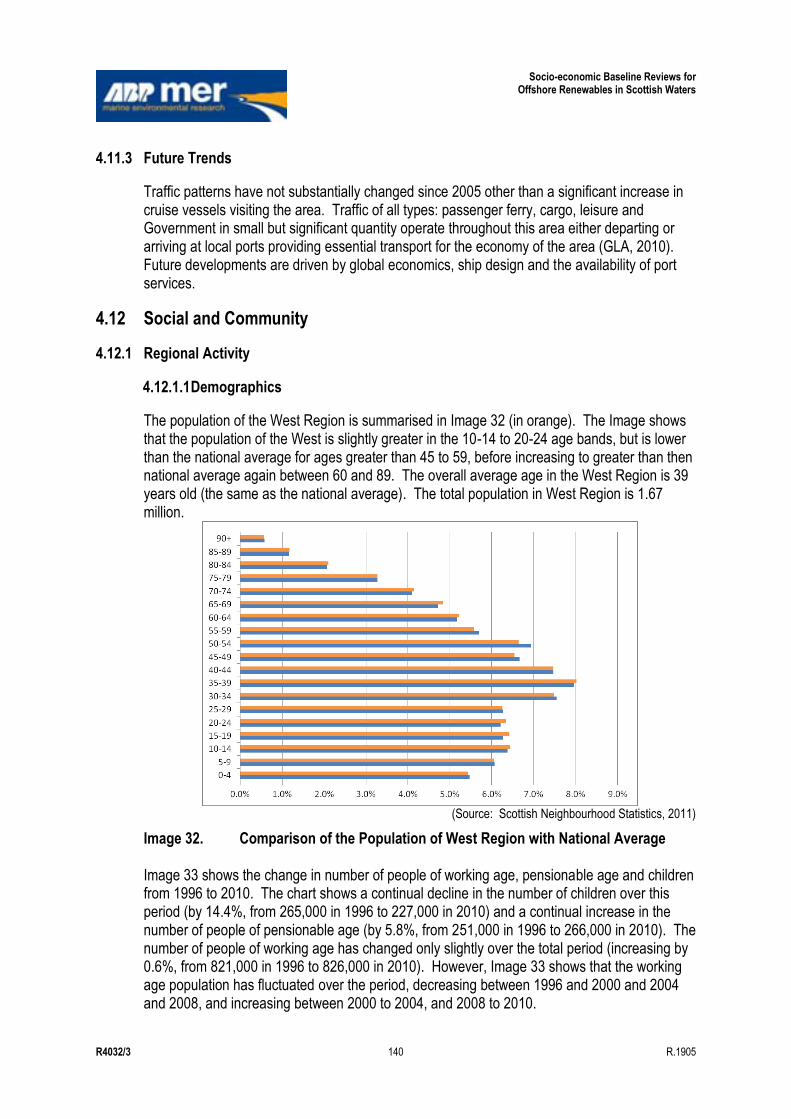

4.12 Social and Community ............................................................................................................ 140 4.12.1 Regional Activity ....................................................................................................... 140 4.12.2 Regional Economic Value and Employment ............................................................ 141 4.12.3 Future Trends ........................................................................................................... 146

4.13 Telecomm Cables................................................................................................................... 147 4.13.1 Regional Activity ....................................................................................................... 147 4.13.2 Regional Economic Value and Employment ............................................................ 148 4.13.3 Future Trends ........................................................................................................... 148

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

R4032/3 x R.1905

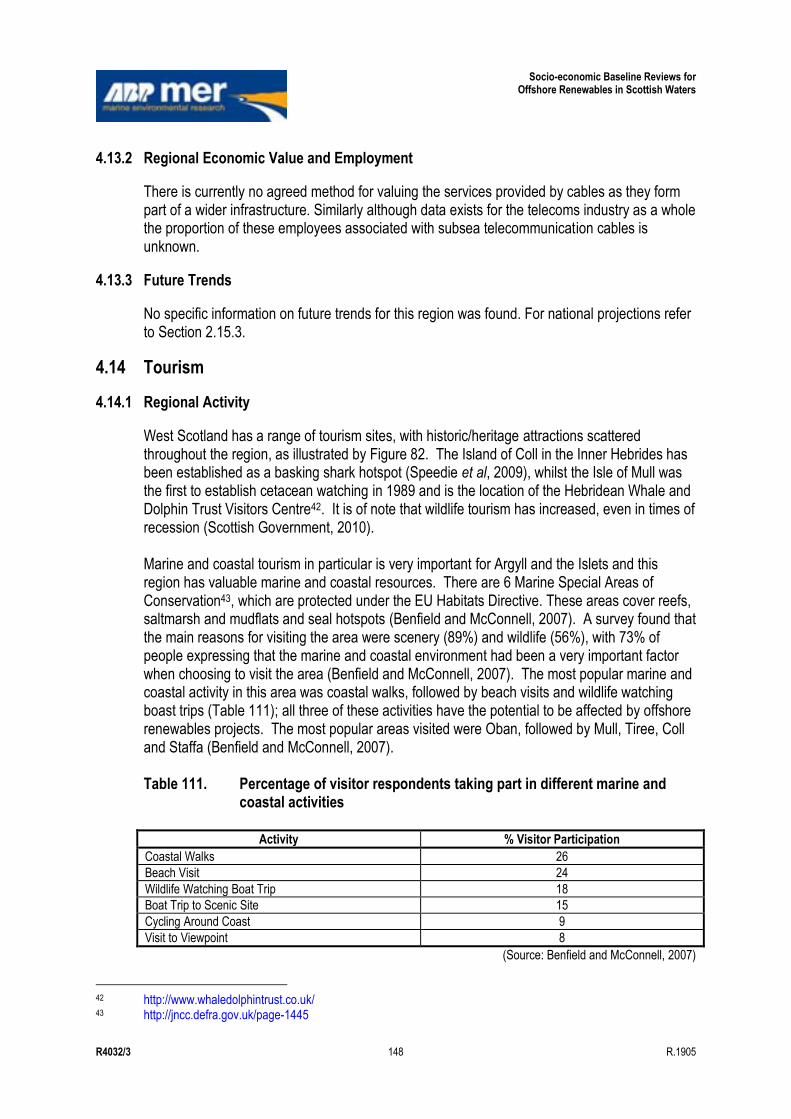

4.14 Tourism .................................................................................................................................. 148 4.14.1 Regional Activity ....................................................................................................... 148 4.14.2 Regional Economic Value and Employment ............................................................ 149 4.14.3 Future Trends ........................................................................................................... 149

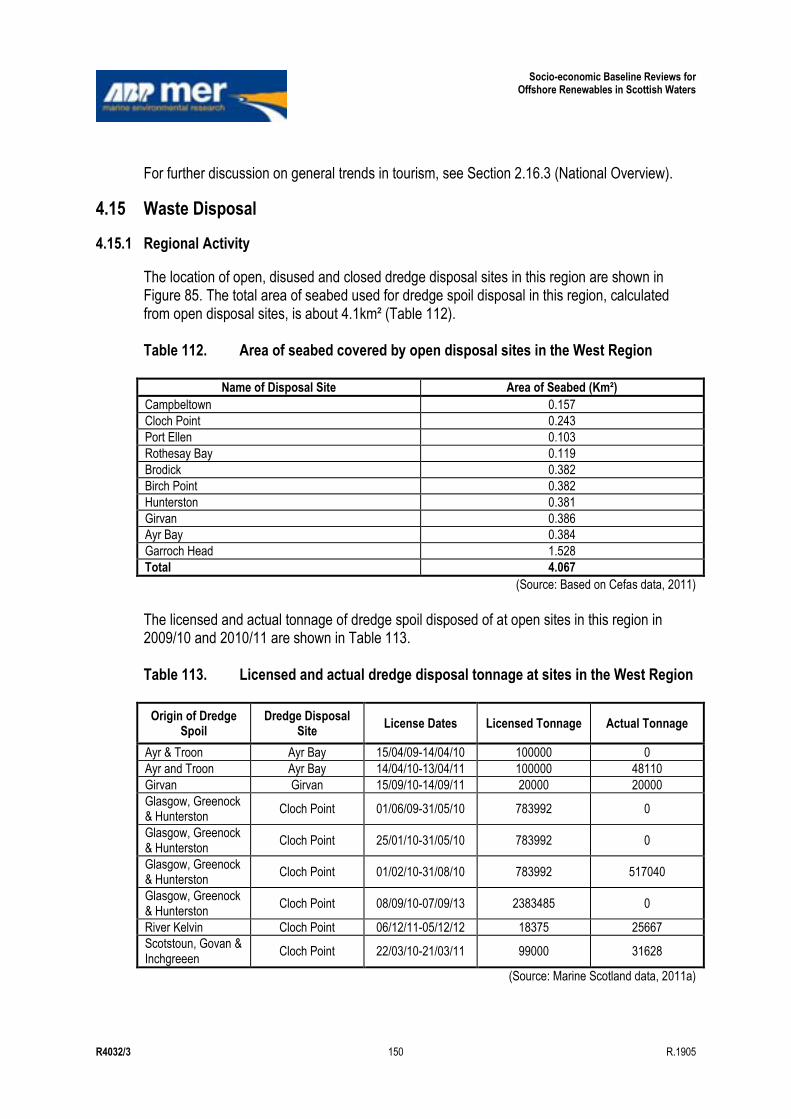

4.15 Waste Disposal....................................................................................................................... 150 4.15.1 Regional Activity ....................................................................................................... 150 4.15.2 Regional Economic Value and Employment ............................................................ 151 4.15.3 Future Trends ........................................................................................................... 151

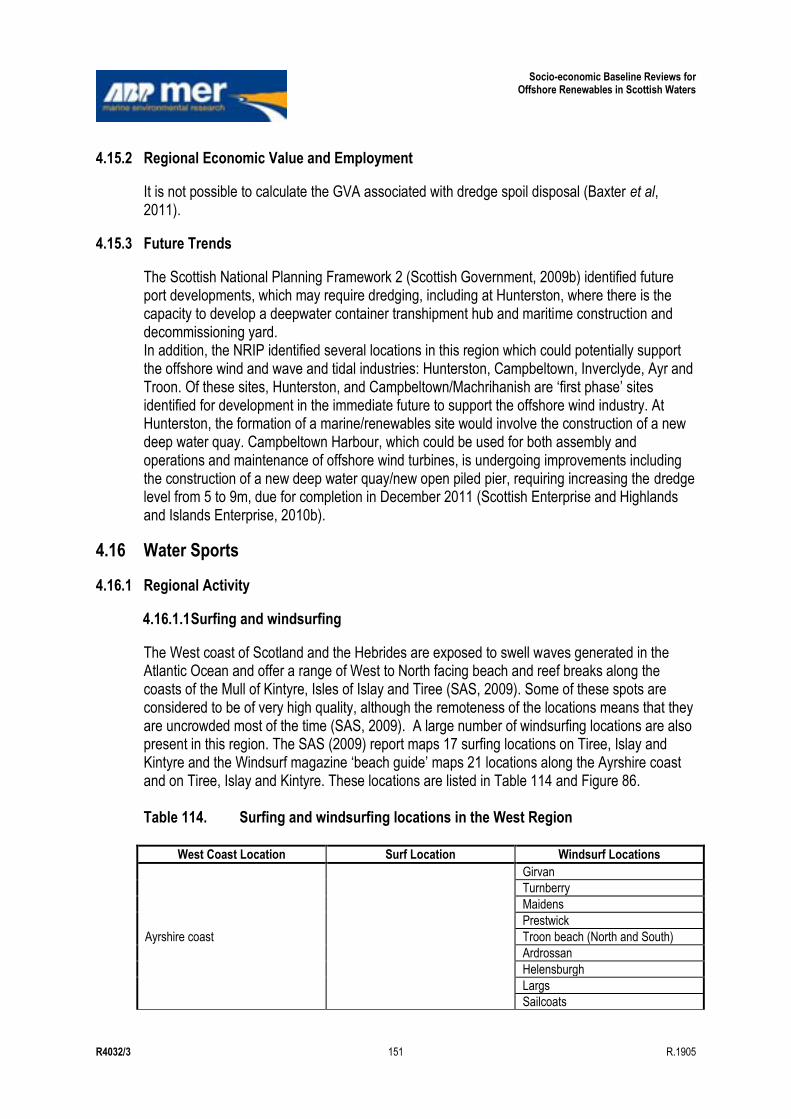

4.16 Water Sports .......................................................................................................................... 151 4.16.1 Regional Activity ....................................................................................................... 151 4.16.2 Regional Economic Value and Employment ............................................................ 153 4.16.3 Future Trends ........................................................................................................... 154

5. North West Region ................................................................................................................. 155 5.1 Introduction ............................................................................................................................. 155 5.2 Aquaculture ............................................................................................................................ 155

5.2.1 Regional Activity ....................................................................................................... 155 5.2.2 Regional Economic Value and Employment ............................................................ 155 5.2.3 Future Trends ........................................................................................................... 156

5.3 Aviation ................................................................................................................................... 156 5.3.1 Regional Activity ....................................................................................................... 156 5.3.2 Regional Economic Value and Employment ............................................................ 156 5.3.3 Future Trends ........................................................................................................... 156

5.4 Coast Protection and Flood Defence ...................................................................................... 156 5.4.1 Regional Activity ....................................................................................................... 156 5.4.2 Regional Economic Value and Employment ............................................................ 157 5.4.3 Future Trends ........................................................................................................... 157

5.5 Commercial Fisheries ............................................................................................................. 157 5.5.1 Regional Activity ....................................................................................................... 157 5.5.2 Regional Economic Value and Employment ............................................................ 159 5.5.3 Future Trends ........................................................................................................... 160

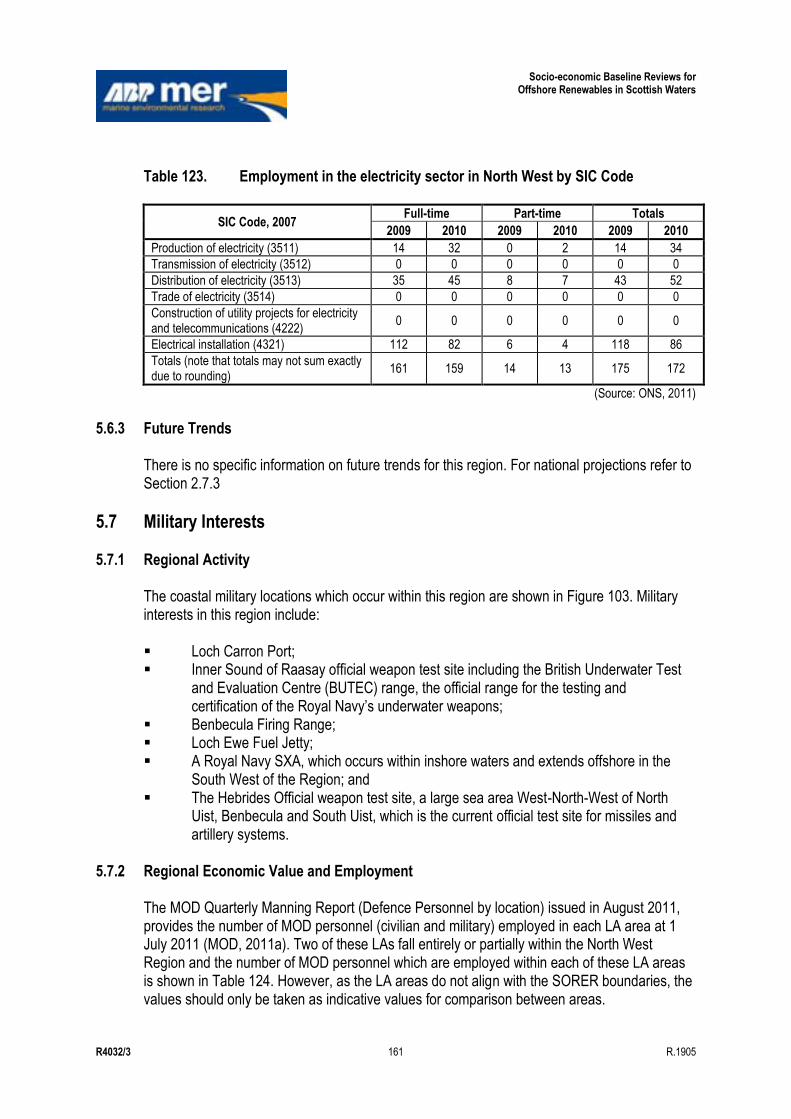

5.6 Energy Generation ................................................................................................................. 160 5.6.1 Regional Activity ....................................................................................................... 160 5.6.2 Regional Economic Value and Employment ............................................................ 160 5.6.3 Future Trends ........................................................................................................... 161

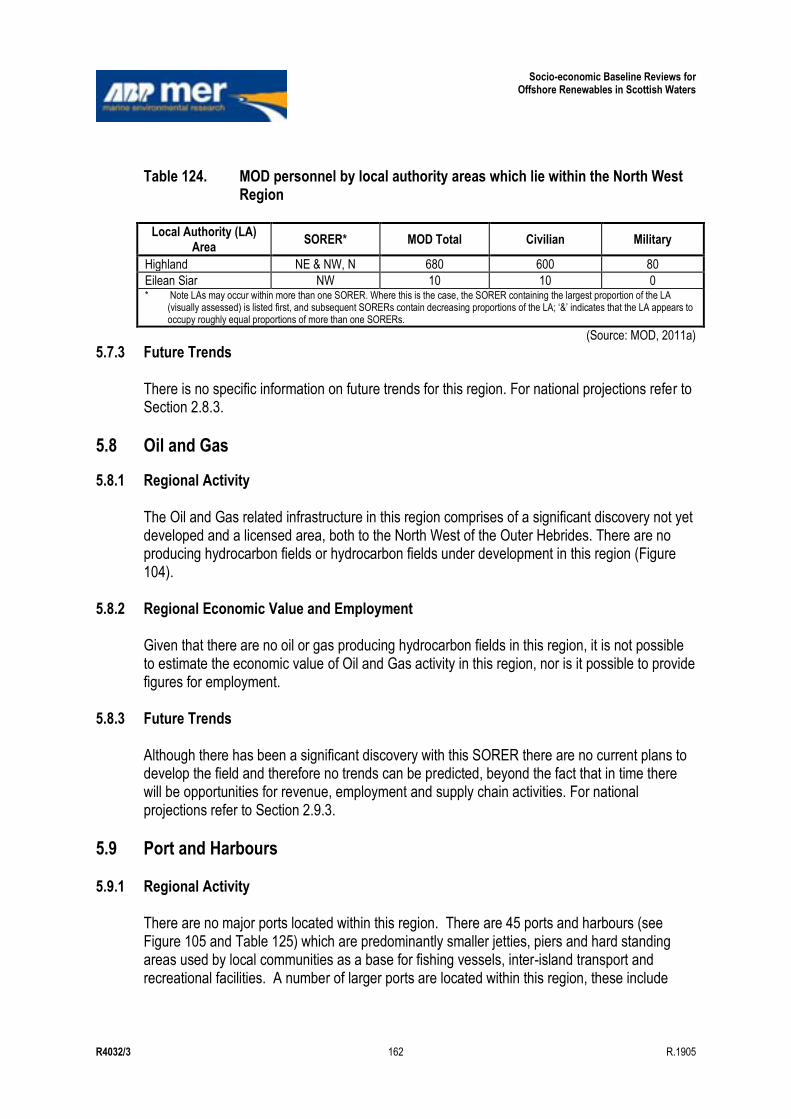

5.7 Military Interests ..................................................................................................................... 161 5.7.1 Regional Activity ....................................................................................................... 161 5.7.2 Regional Economic Value and Employment ............................................................ 161 5.7.3 Future Trends ........................................................................................................... 162

5.8 Oil and Gas ............................................................................................................................ 162 5.8.1 Regional Activity ....................................................................................................... 162 5.8.2 Regional Economic Value and Employment ............................................................ 162 5.8.3 Future Trends ........................................................................................................... 162

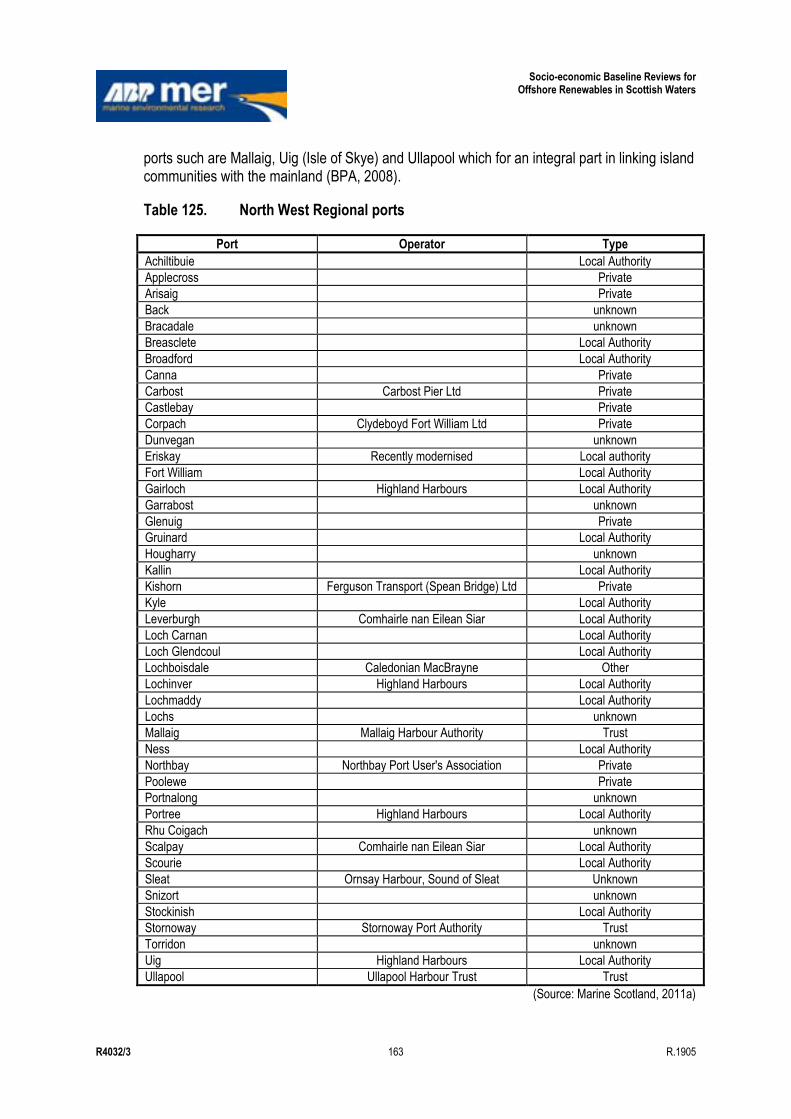

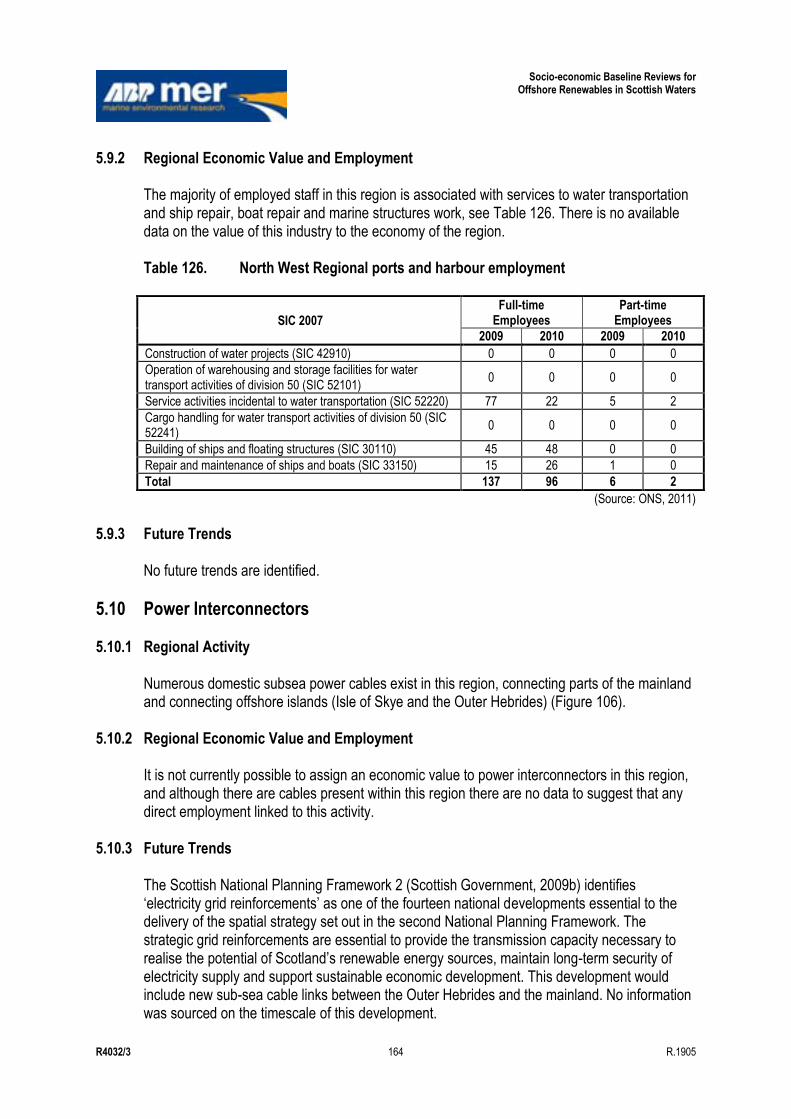

5.9 Port and Harbours .................................................................................................................. 162 5.9.1 Regional Activity ....................................................................................................... 162 5.9.2 Regional Economic Value and Employment ............................................................ 164 5.9.3 Future Trends ........................................................................................................... 164

5.10 Power Interconnectors ............................................................................................................ 164 5.10.1 Regional Activity ....................................................................................................... 164 5.10.2 Regional Economic Value and Employment ............................................................ 164 5.10.3 Future Trends ........................................................................................................... 164

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

R4032/3 xi R.1905

5.11 Recreational Boating .............................................................................................................. 165 5.11.1 Regional Activity ....................................................................................................... 165 5.11.2 Regional Economic Value and Employment ............................................................ 165 5.11.3 Future Trends ........................................................................................................... 165

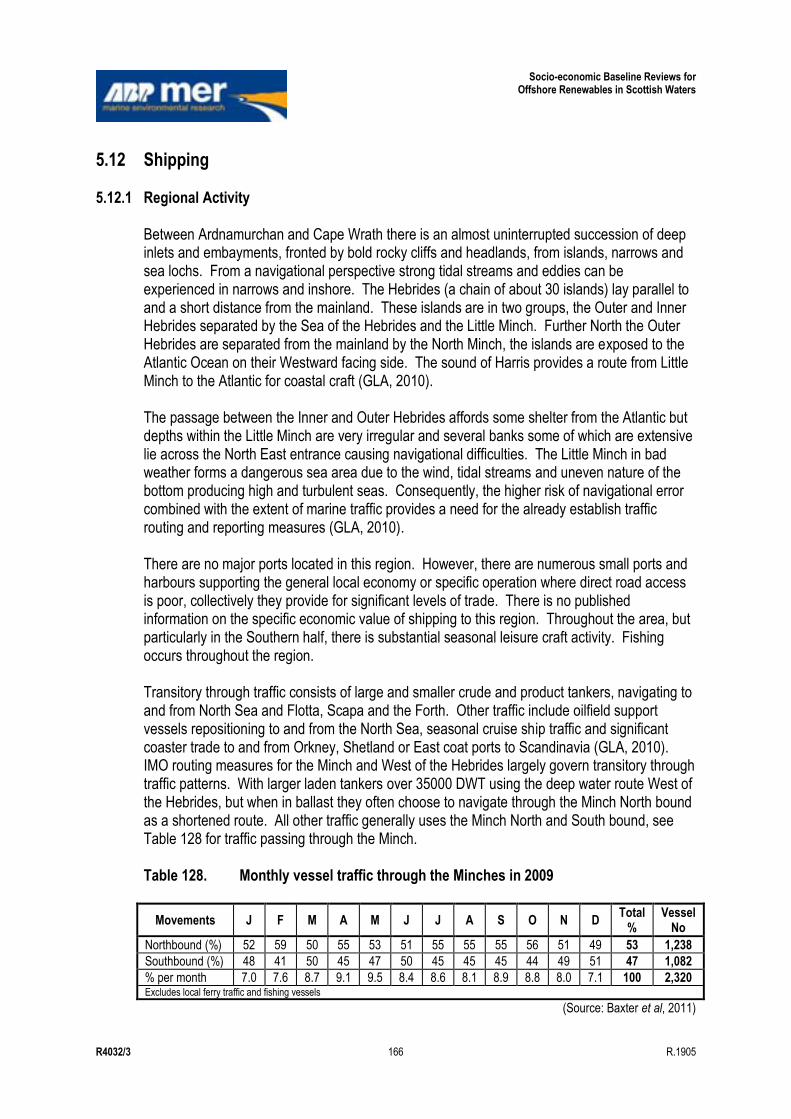

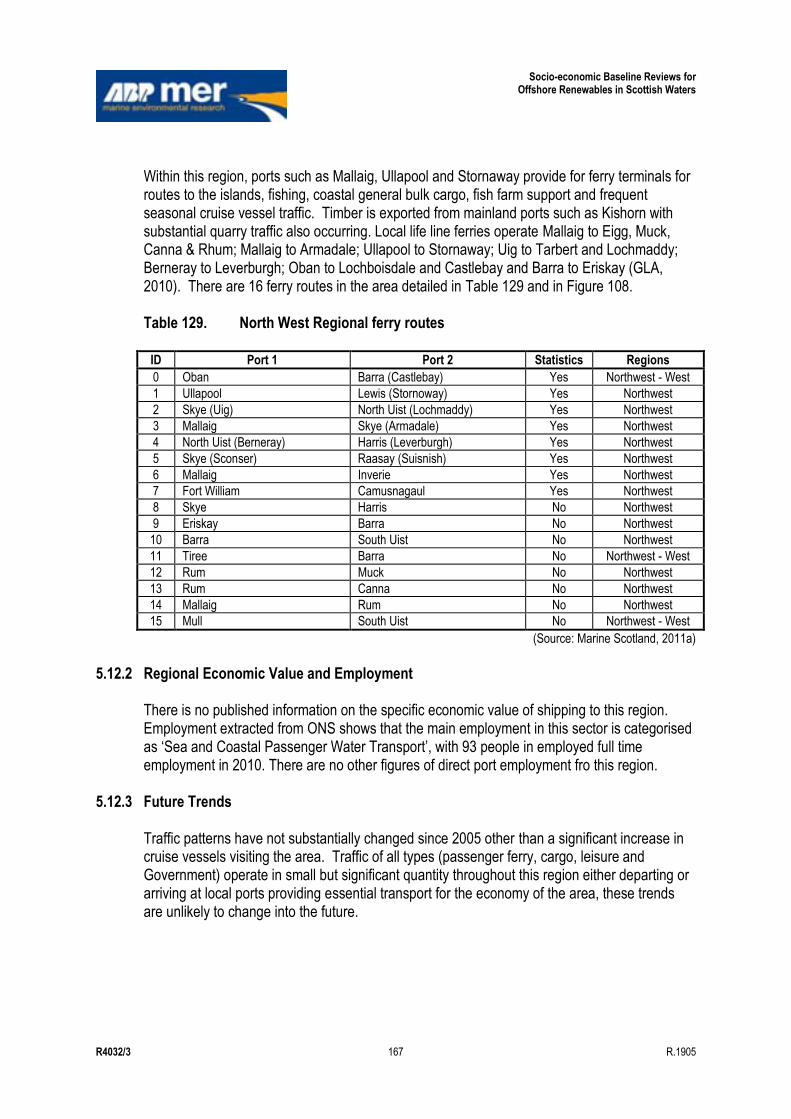

5.12 Shipping ................................................................................................................................. 166 5.12.1 Regional Activity ....................................................................................................... 166 5.12.2 Regional Economic Value and Employment ............................................................ 167 5.12.3 Future Trends ........................................................................................................... 167

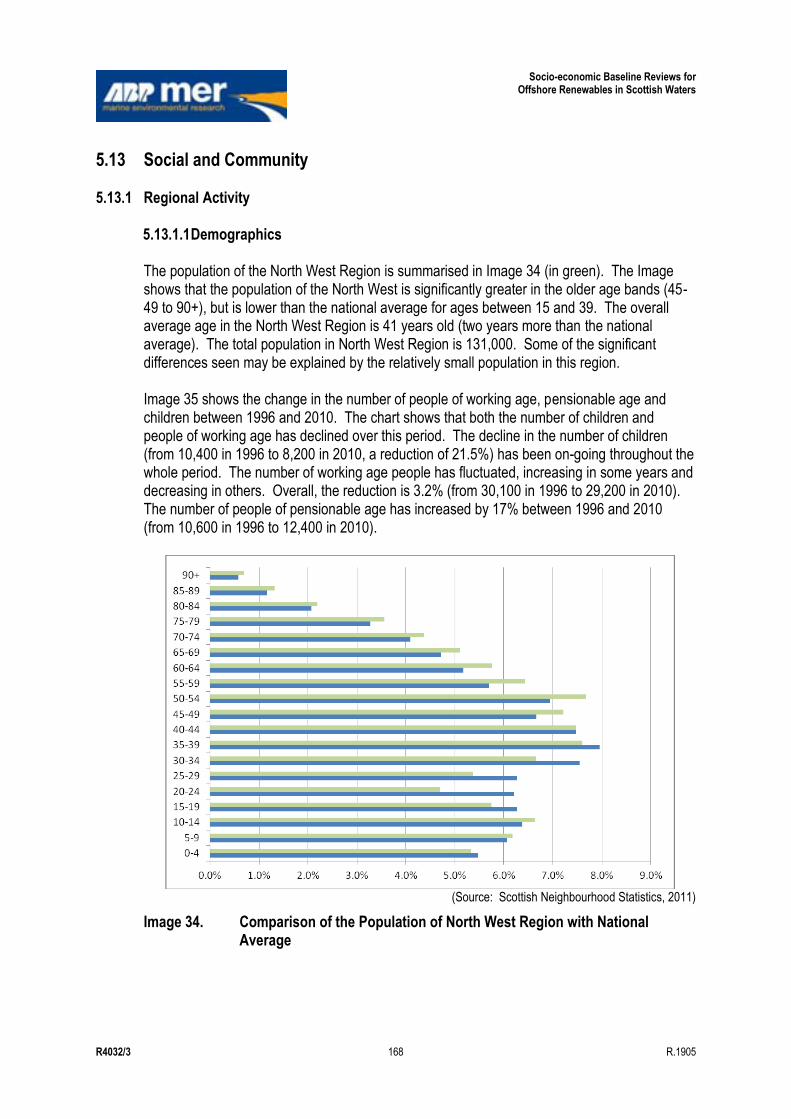

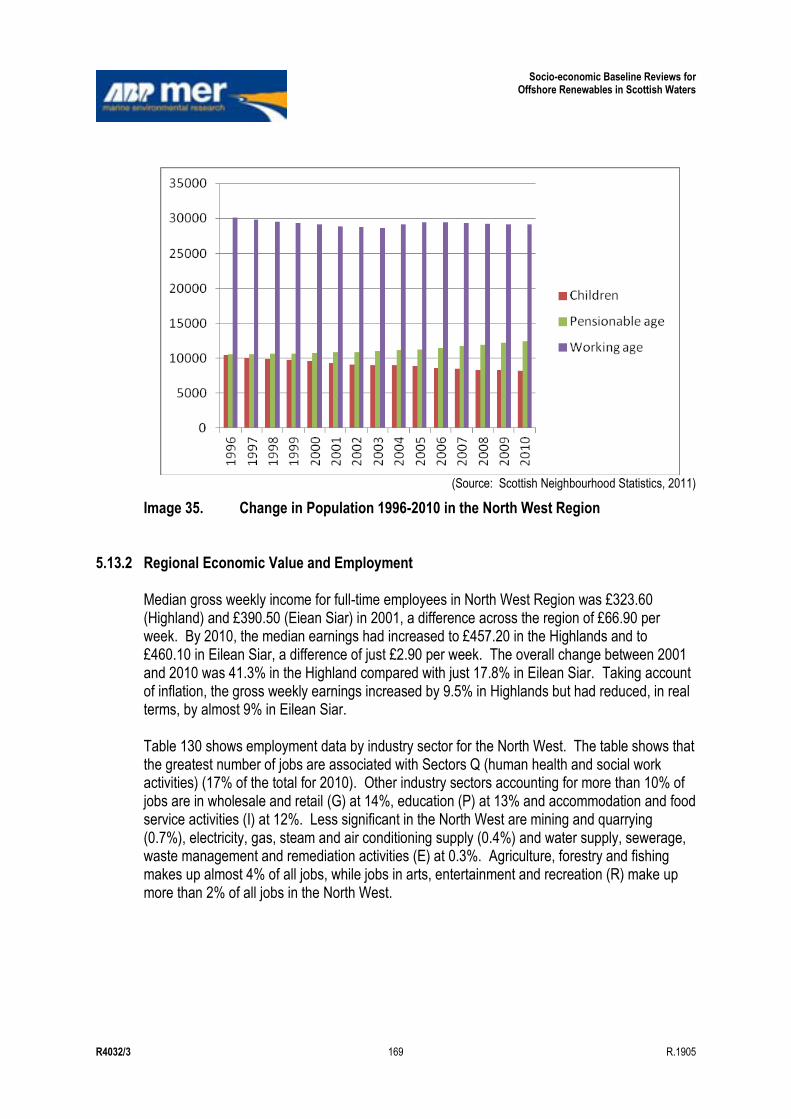

5.13 Social and Community ............................................................................................................ 168 5.13.1 Regional Activity ....................................................................................................... 168 5.13.2 Regional Economic Value and Employment ............................................................ 169 5.13.3 Future Trends ........................................................................................................... 175

5.14 Telecomm Cables................................................................................................................... 175 5.14.1 Regional Activity ....................................................................................................... 175 5.14.2 Regional Economic Value and Employment ............................................................ 176 5.14.3 Future Trends ........................................................................................................... 176

5.15 Tourism .................................................................................................................................. 176 5.15.1 Regional Activity ....................................................................................................... 176 5.15.2 Regional Economic Value and Employment ............................................................ 177 5.15.3 Future Trends ........................................................................................................... 177

5.16 Waste Disposal....................................................................................................................... 177 5.16.1 Regional Activity ....................................................................................................... 177 5.16.2 Regional Economic Value and Employment ............................................................ 178 5.16.3 Future Trends ........................................................................................................... 178

5.17 Water Sports .......................................................................................................................... 178 5.17.1 Regional Activity ....................................................................................................... 178 5.17.2 Regional Economic Value and Employment ............................................................ 179 5.17.3 Future Trends ........................................................................................................... 180

6. North Region .......................................................................................................................... 181 6.1 Introduction ............................................................................................................................. 181 6.2 Aquaculture ............................................................................................................................ 181

6.2.1 Regional Activity ....................................................................................................... 181 6.2.2 Regional Economic Value and Employment ............................................................ 181 6.2.3 Future Trends ........................................................................................................... 182

6.3 Aviation ................................................................................................................................... 182 6.3.1 Regional Activity ....................................................................................................... 182 6.3.2 Regional Economic Value and Employment ............................................................ 182 6.3.3 Future Trends ........................................................................................................... 182

6.4 Carbon Capture and Storage ................................................................................................. 182 6.4.1 Regional Activity ....................................................................................................... 182 6.4.2 Regional Economic Value and Employment ............................................................ 183 6.4.3 Future Trends ........................................................................................................... 183

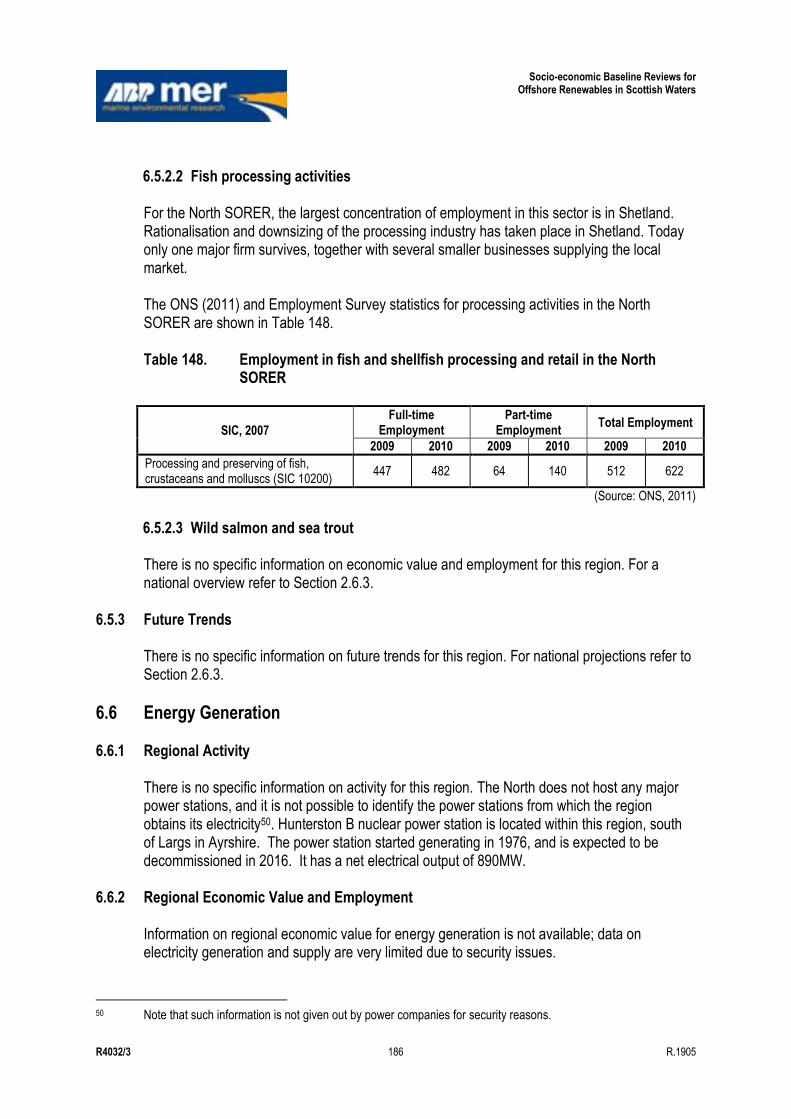

6.5 Commercial Fisheries ............................................................................................................. 184 6.5.1 Regional Activity ....................................................................................................... 184 6.5.2 Regional Economic Value and Employment ............................................................ 185 6.5.3 Future Trends ........................................................................................................... 186

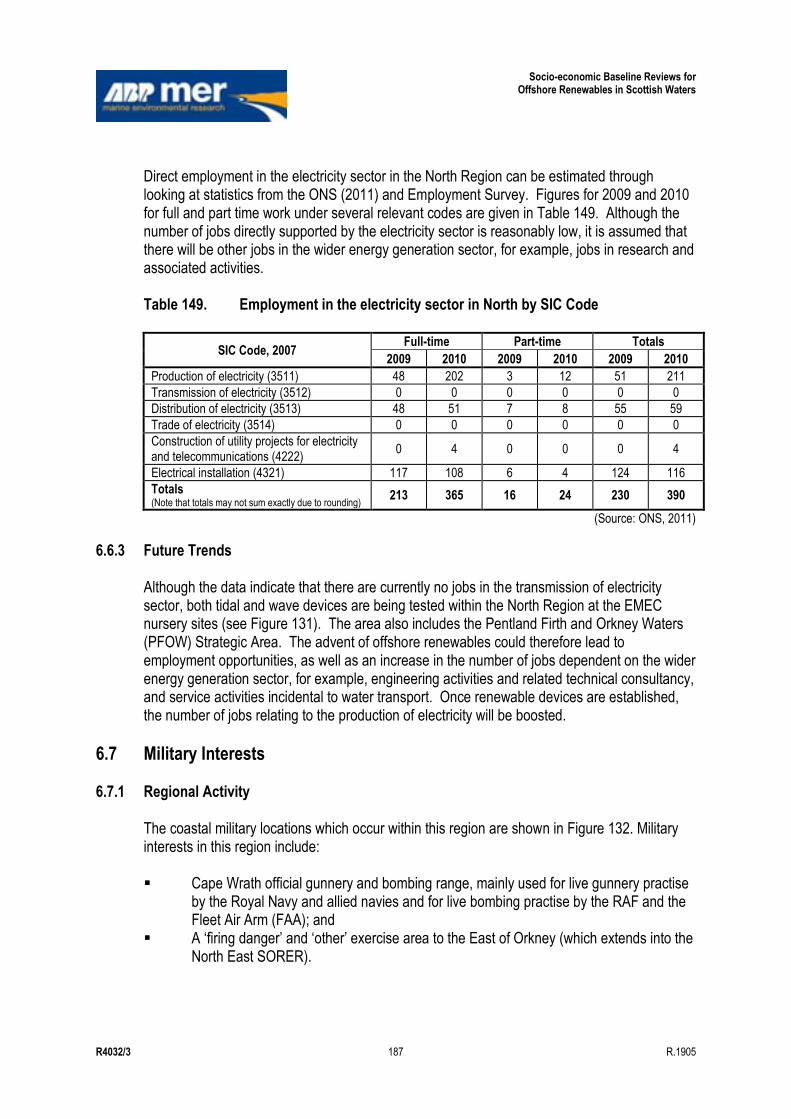

6.6 Energy Generation ................................................................................................................. 186 6.6.1 Regional Activity ....................................................................................................... 186 6.6.2 Regional Economic Value and Employment ............................................................ 186 6.6.3 Future Trends ........................................................................................................... 187

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

R4032/3 xii R.1905

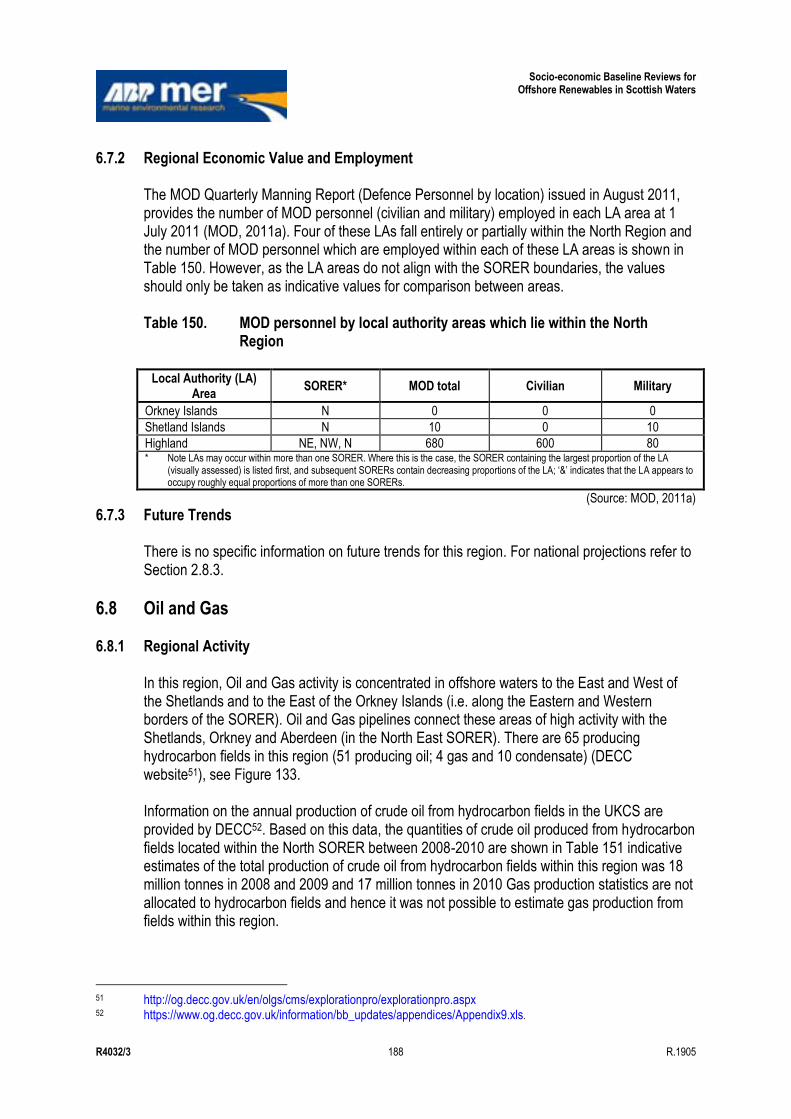

6.7 Military Interests ..................................................................................................................... 187 6.7.1 Regional Activity ....................................................................................................... 187 6.7.2 Regional Economic Value and Employment ............................................................ 188 6.7.3 Future Trends ........................................................................................................... 188

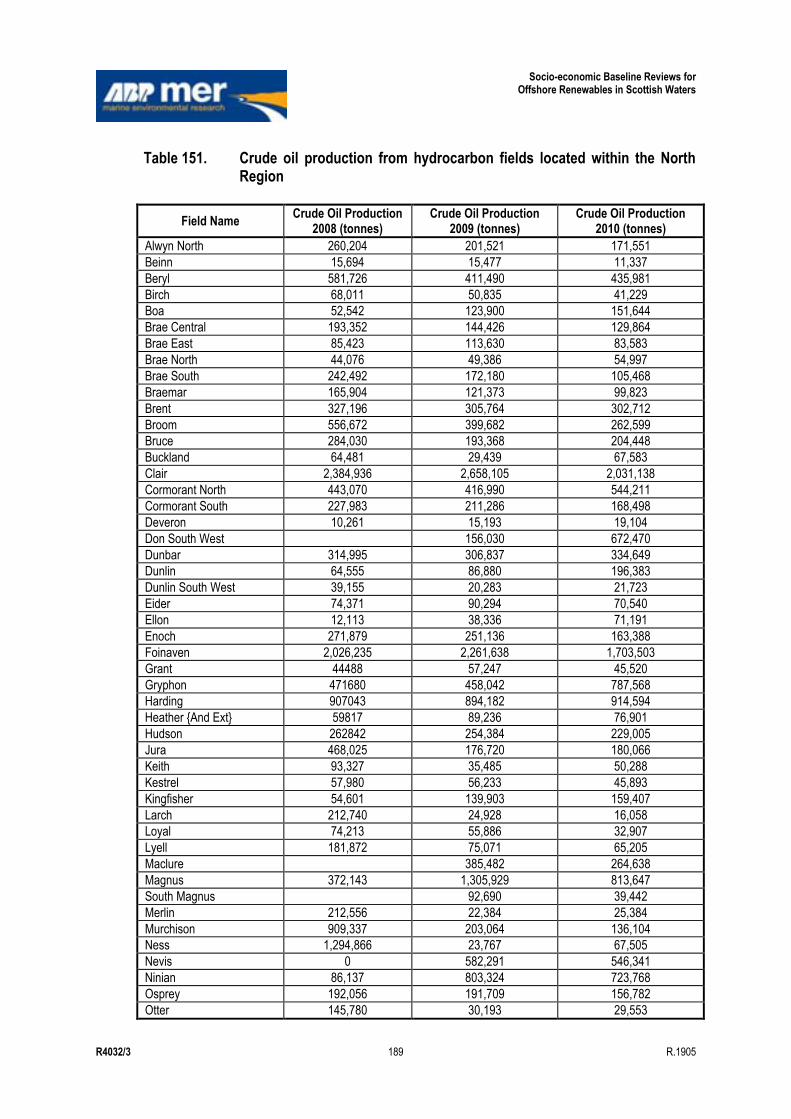

6.8 Oil and Gas ............................................................................................................................ 188 6.8.1 Regional Activity ....................................................................................................... 188 6.8.2 Regional Economic Value and Employment ............................................................ 190 6.8.3 Future Trends ........................................................................................................... 190

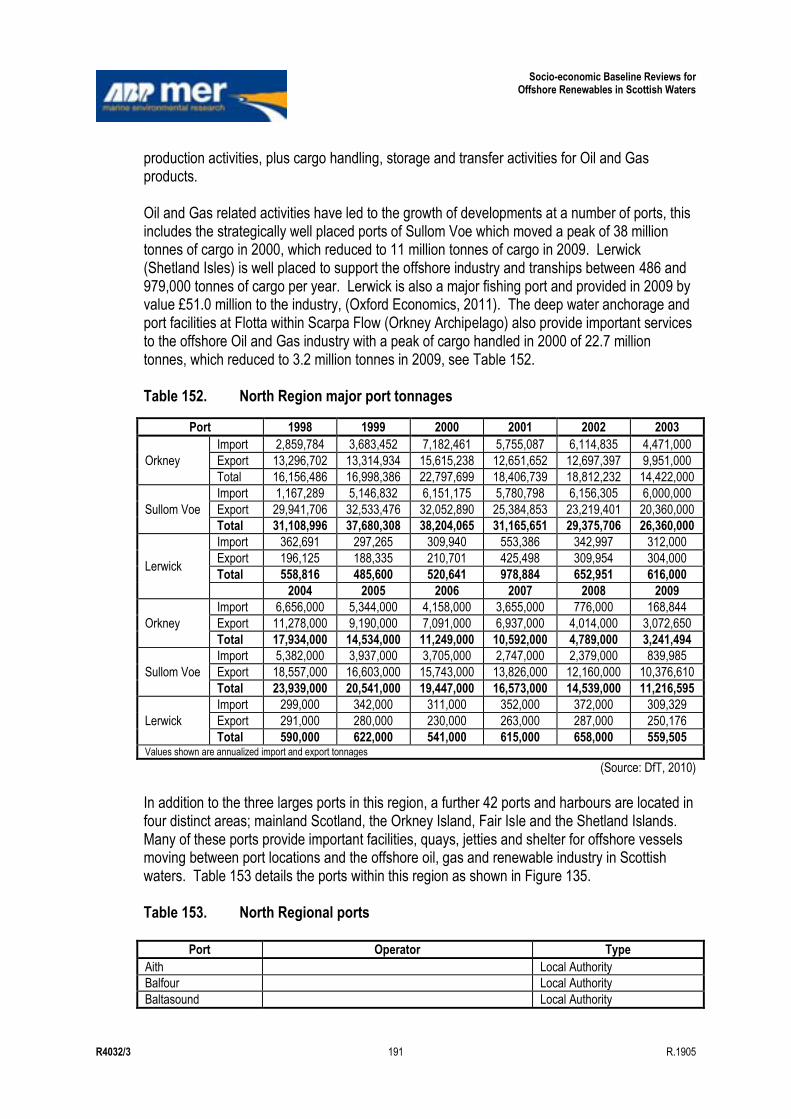

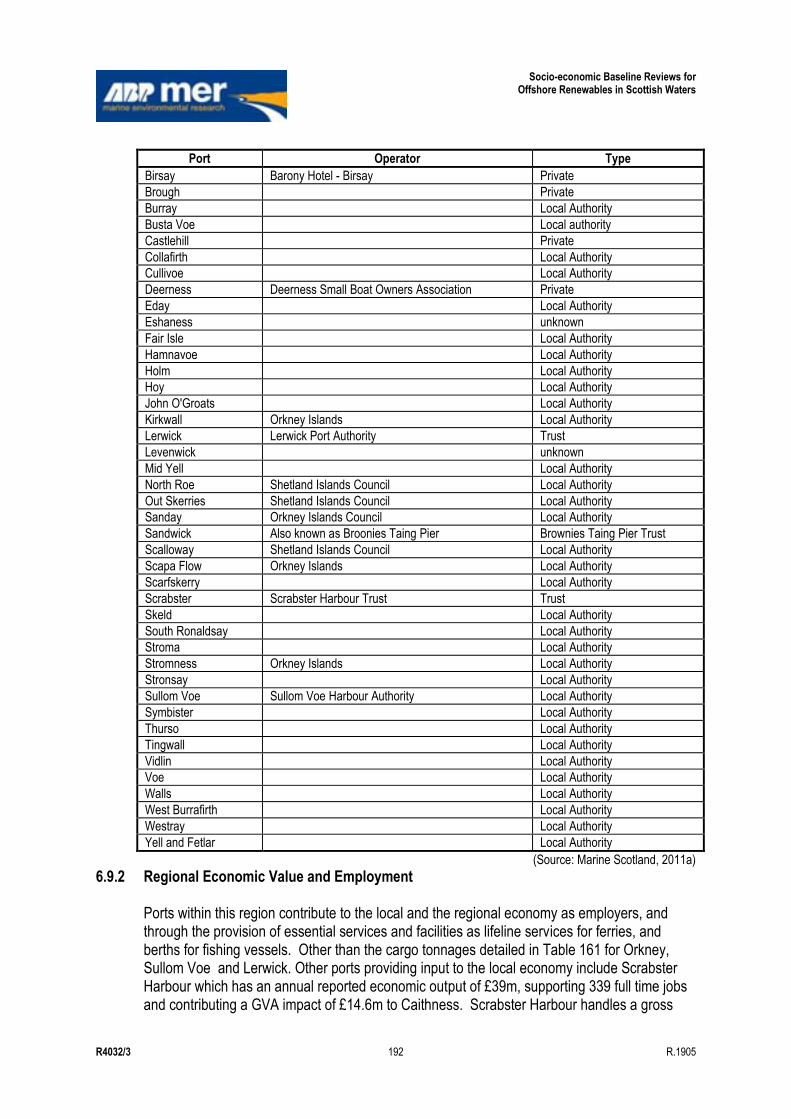

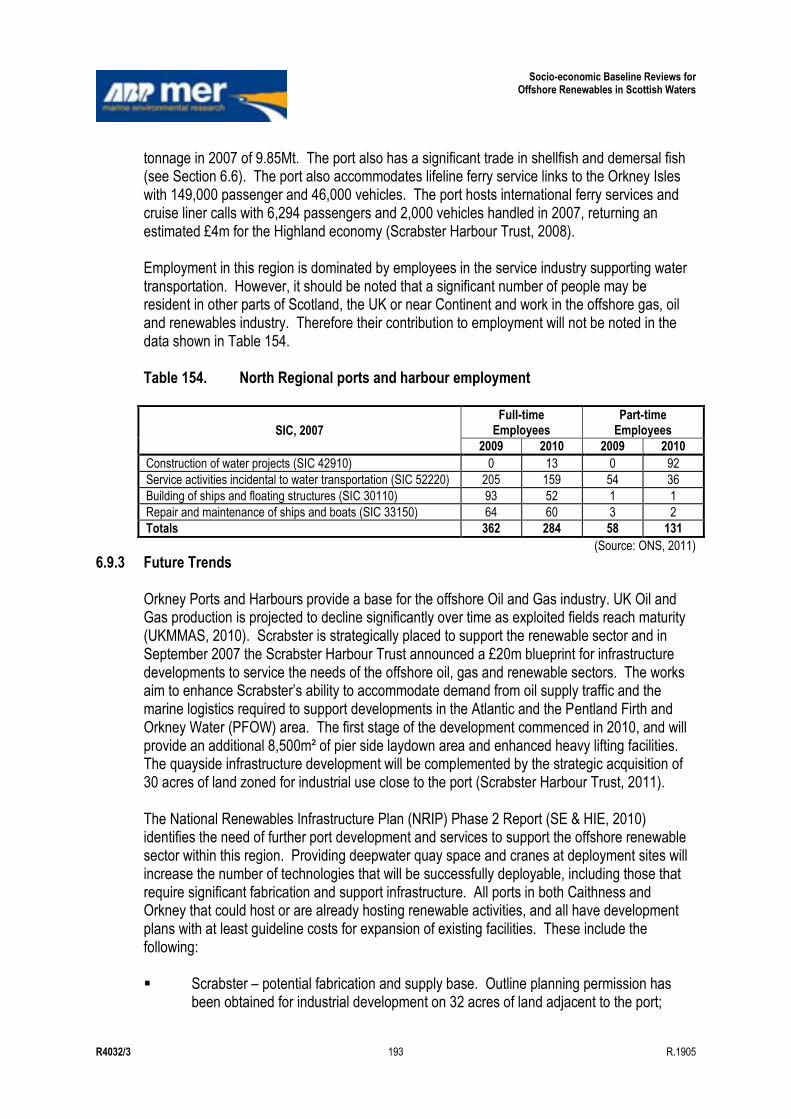

6.9 Ports and Harbours ................................................................................................................ 190 6.9.1 Regional Activity ....................................................................................................... 190 6.9.2 Regional Economic Value and Employment ............................................................ 192 6.9.3 Future Trends ........................................................................................................... 193

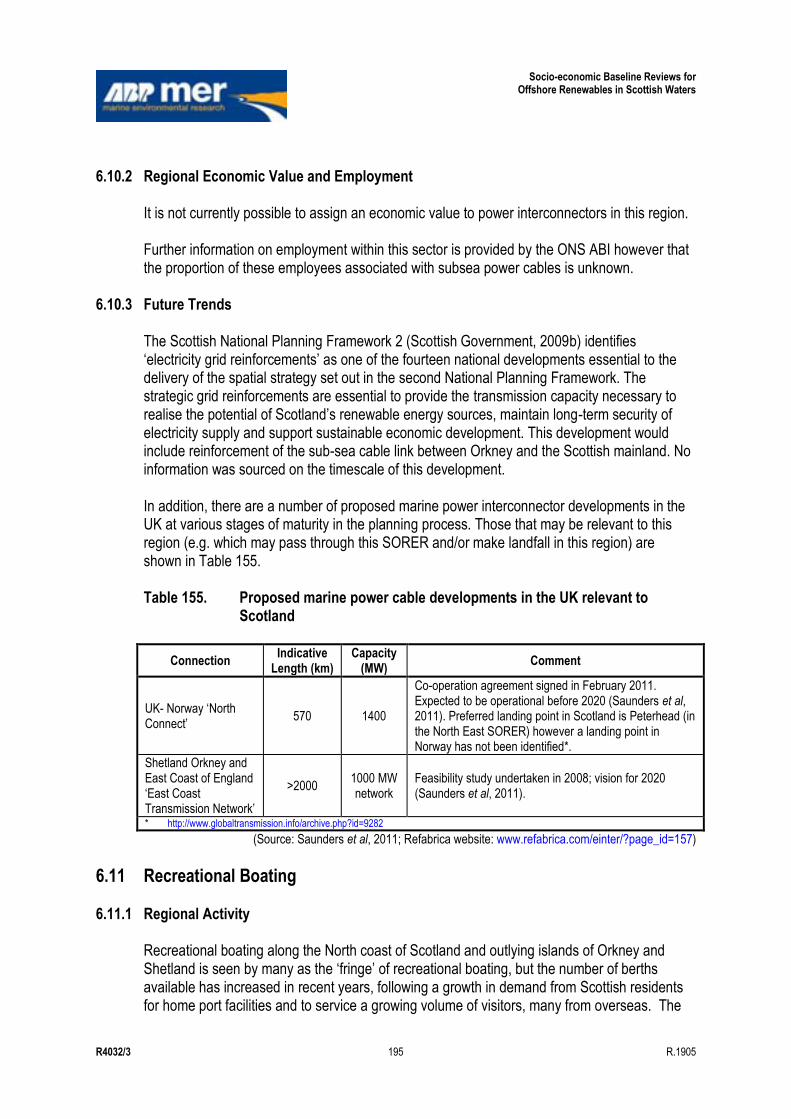

6.10 Power Interconnectors ............................................................................................................ 194 6.10.1 Regional Activity ....................................................................................................... 194 6.10.2 Regional Economic Value and Employment ............................................................ 195 6.10.3 Future Trends ........................................................................................................... 195

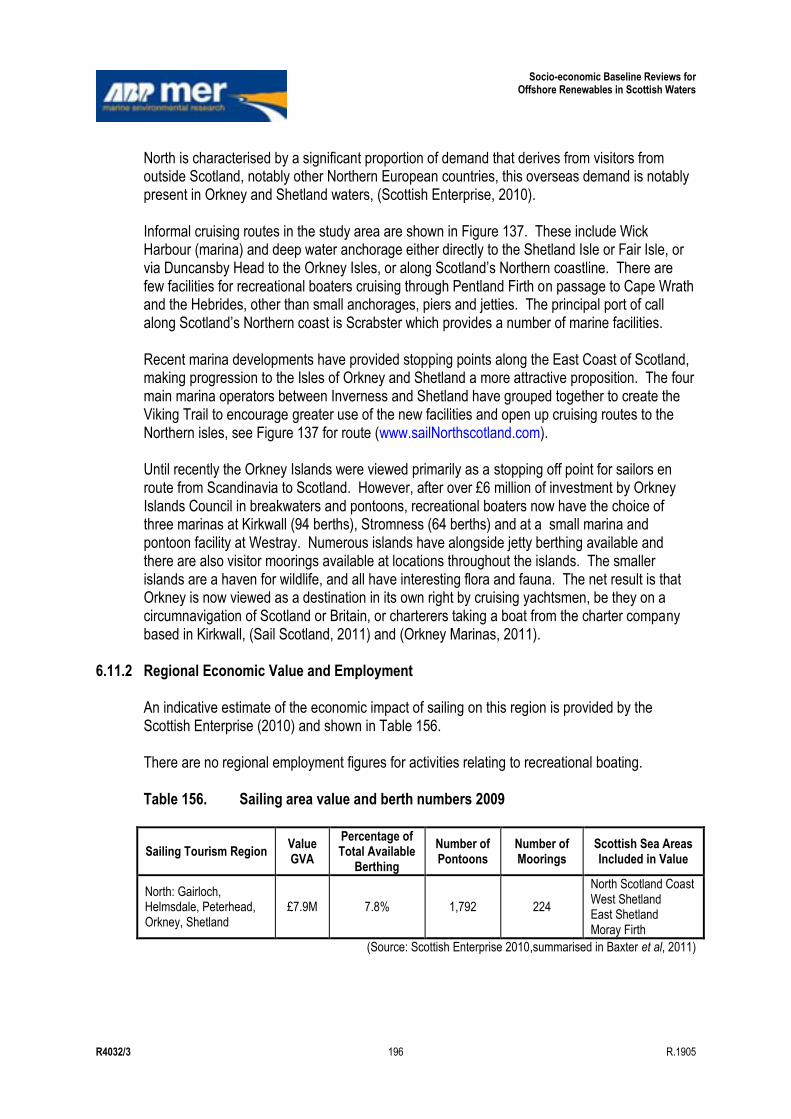

6.11 Recreational Boating .............................................................................................................. 195 6.11.1 Regional Activity ....................................................................................................... 195 6.11.2 Regional Economic Value and Employment ............................................................ 196 6.11.3 Future Trends ........................................................................................................... 197

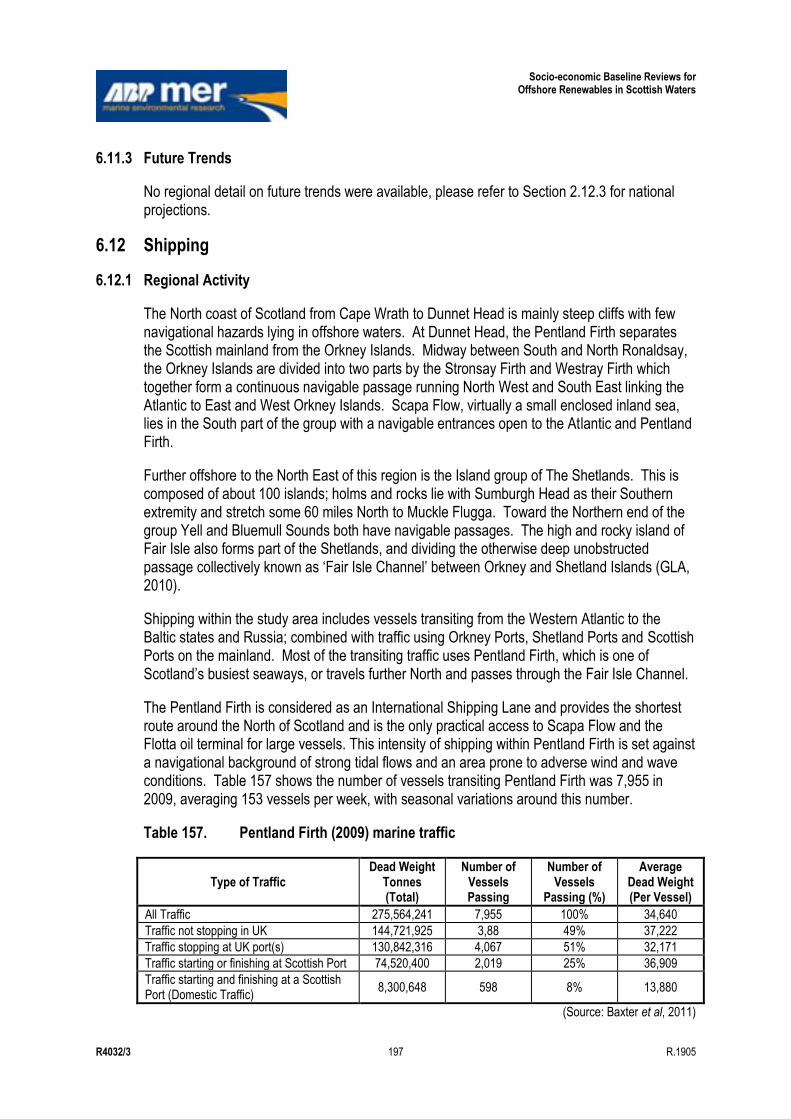

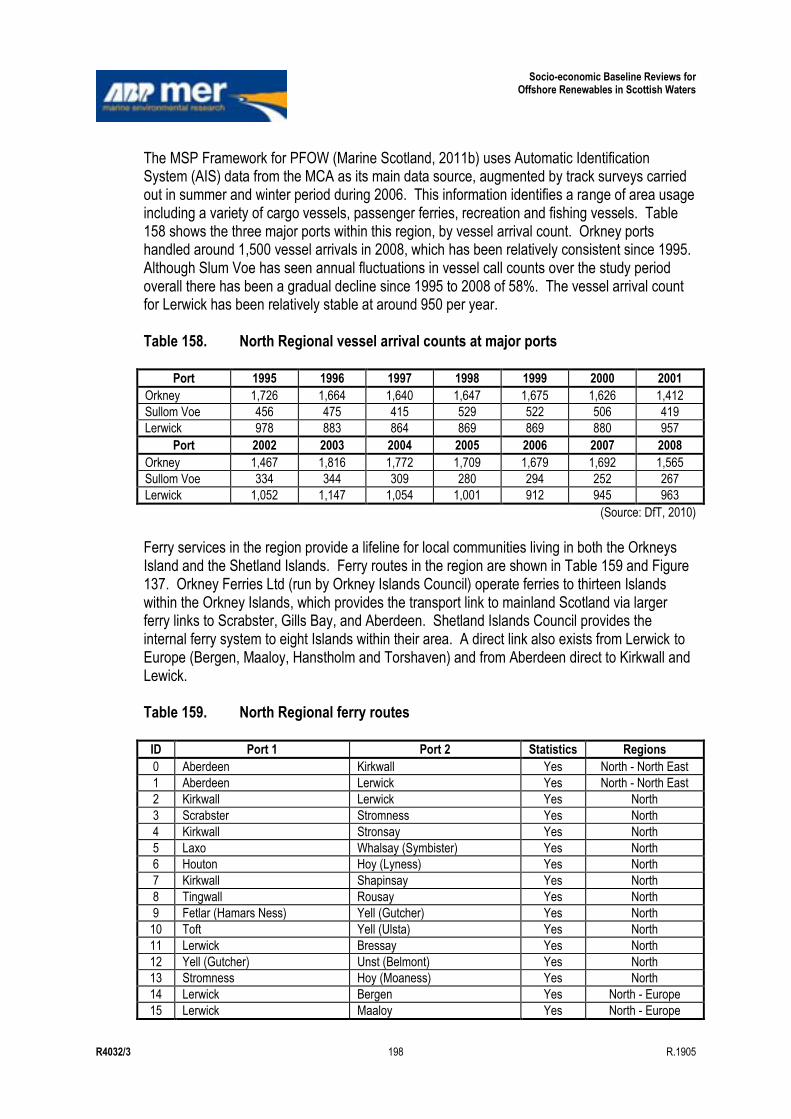

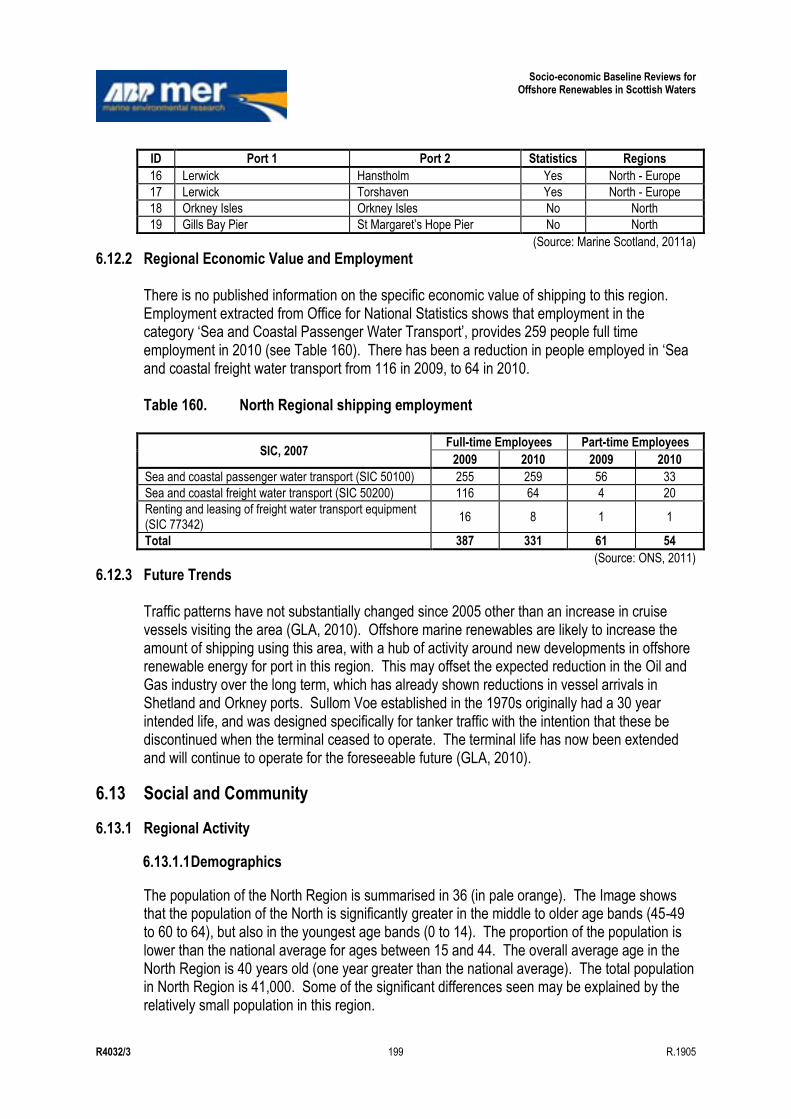

6.12 Shipping ................................................................................................................................. 197 6.12.1 Regional Activity ....................................................................................................... 197 6.12.2 Regional Economic Value and Employment ............................................................ 199 6.12.3 Future Trends ........................................................................................................... 199

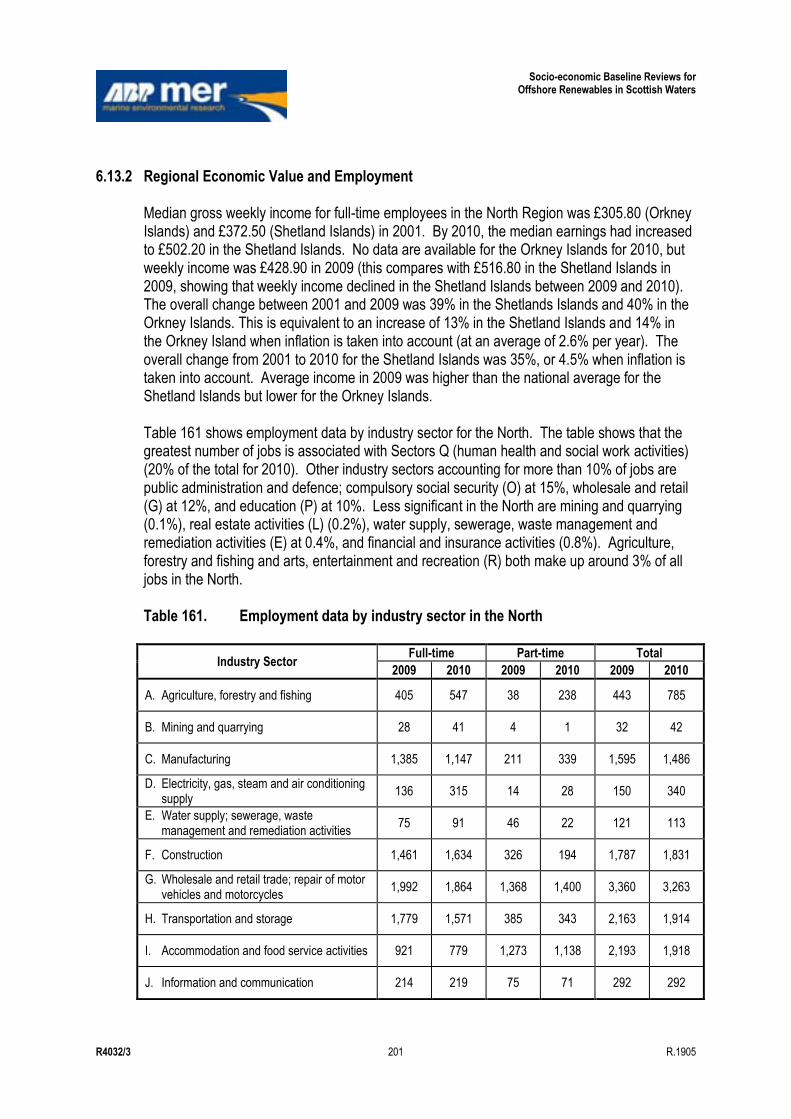

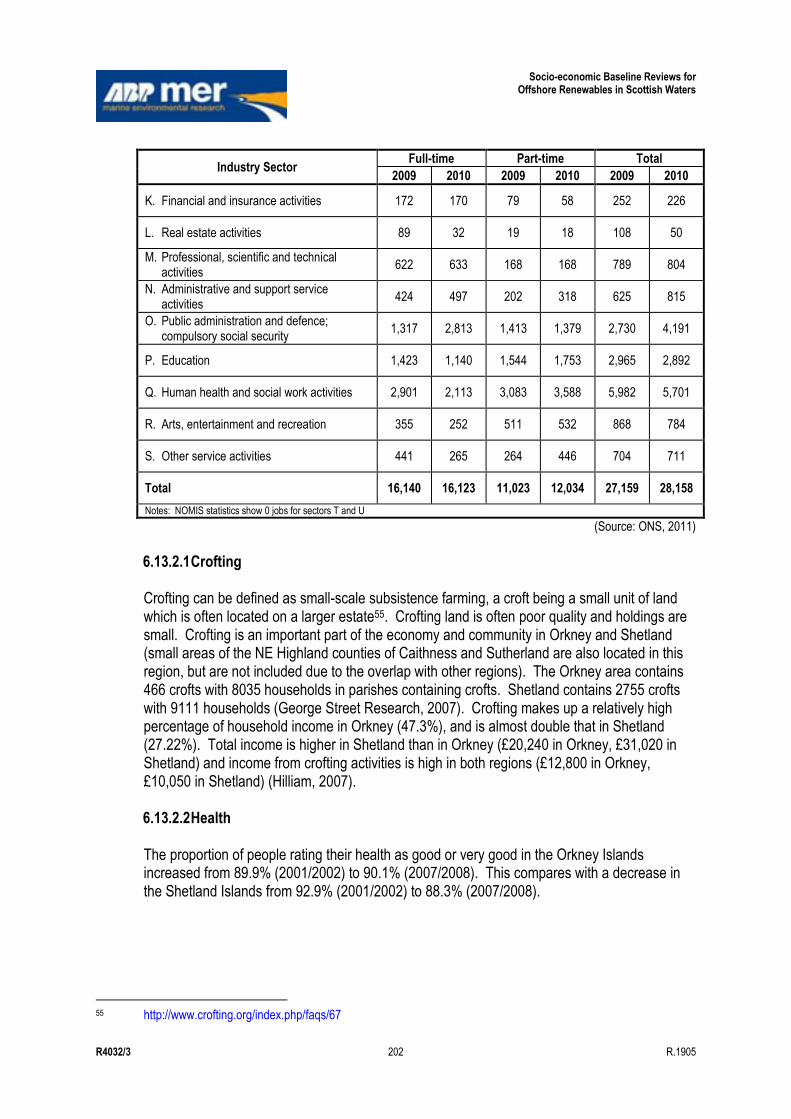

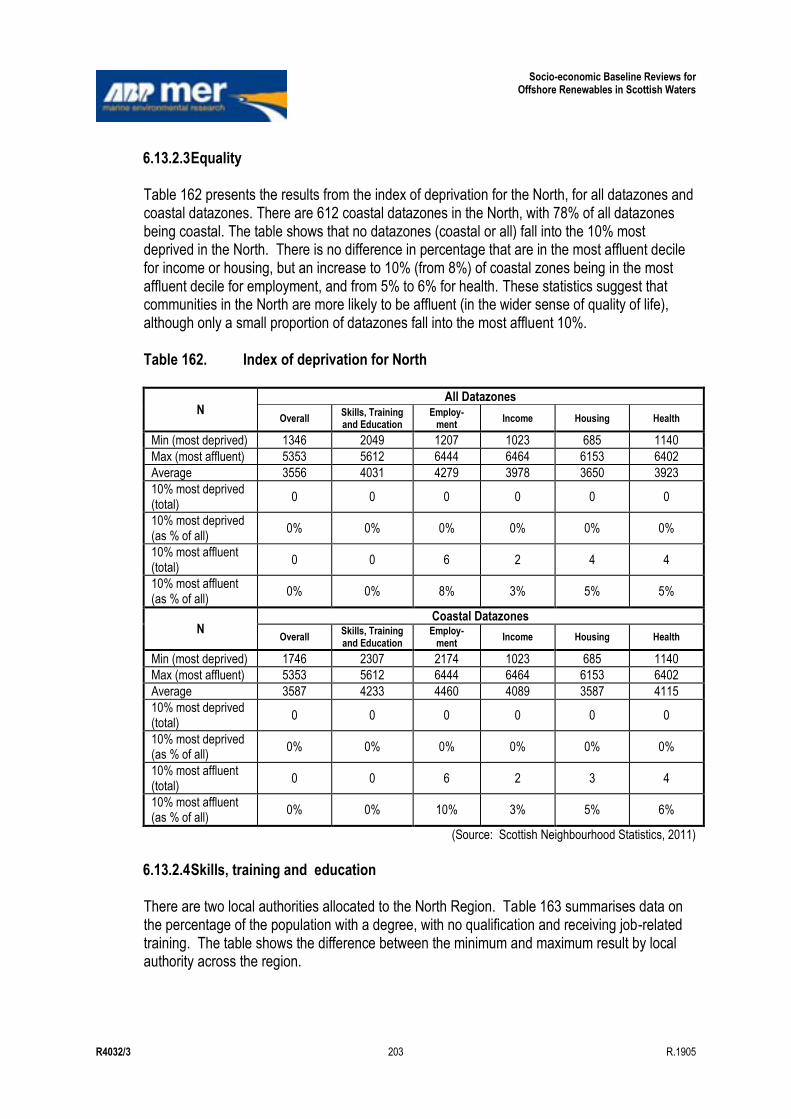

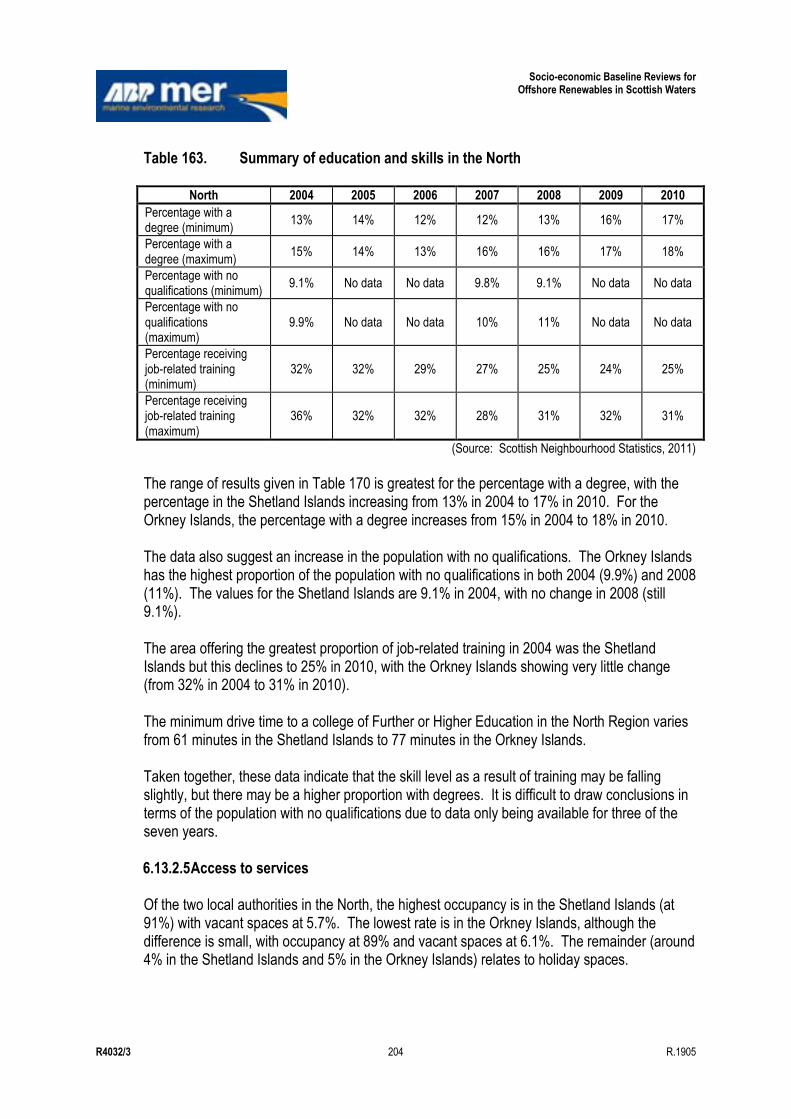

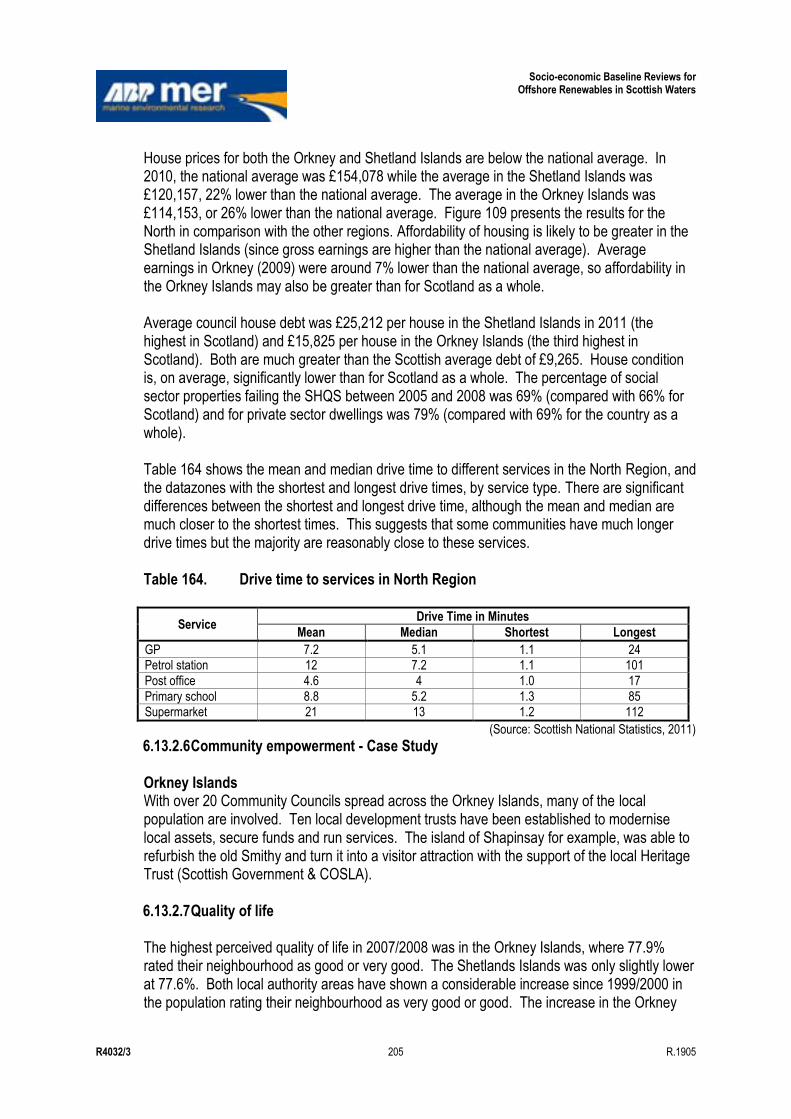

6.13 Social and Community ............................................................................................................ 199 6.13.1 Regional Activity ....................................................................................................... 199 6.13.2 Regional Economic Value and Employment ............................................................ 201 6.13.3 Future Trends ........................................................................................................... 207

6.14 Telecomm Cables................................................................................................................... 208 6.14.1 Regional Activity ....................................................................................................... 208 6.14.2 Regional Economic Value and Employment ............................................................ 208 6.14.3 Future Trends ........................................................................................................... 208

6.15 Tourism .................................................................................................................................. 209 6.15.1 Regional Activity ....................................................................................................... 209 6.15.2 Regional Economic Value and Employment ............................................................ 209 6.15.3 Future Trends ........................................................................................................... 209

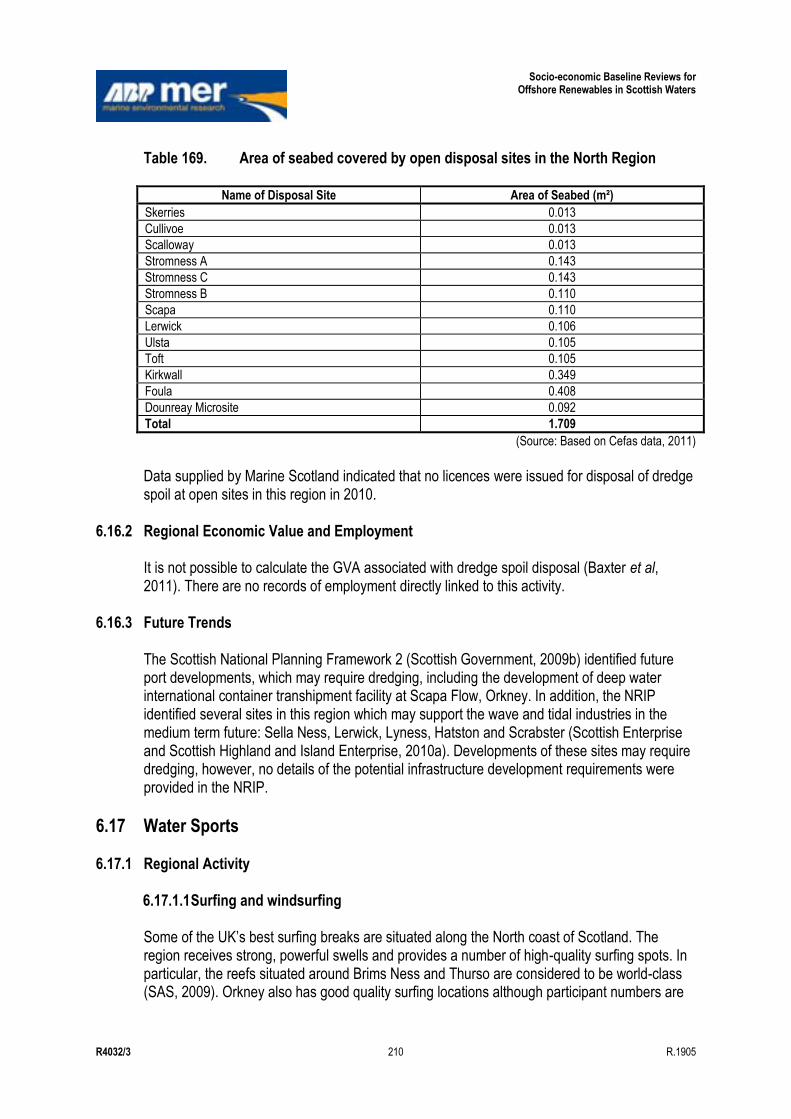

6.16 Waste Disposal....................................................................................................................... 209 6.16.1 Regional Activity ....................................................................................................... 209 6.16.2 Regional Economic Value and Employment ............................................................ 210 6.16.3 Future Trends ........................................................................................................... 210

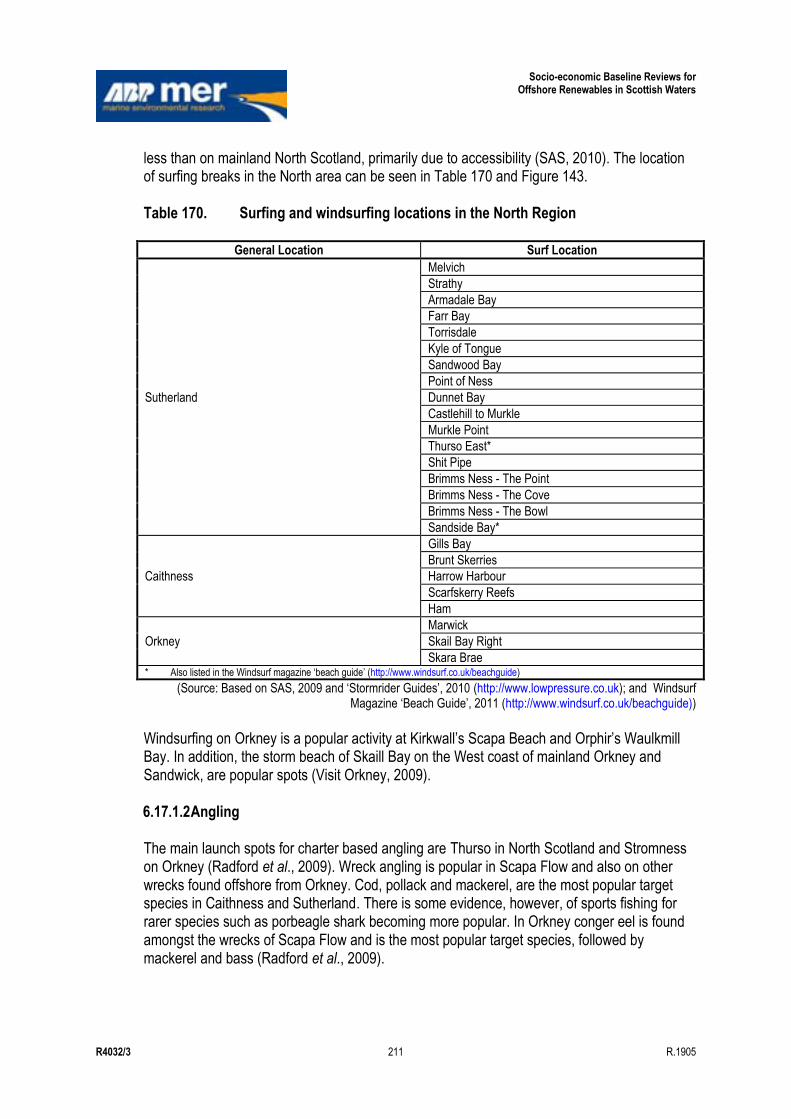

6.17 Water Sports .......................................................................................................................... 210 6.17.1 Regional Activity ....................................................................................................... 210 6.17.2 Regional Economic Value and Employment ............................................................ 212 6.17.3 Future Trends ........................................................................................................... 213

7. North East Region .................................................................................................................. 214 7.1 Introduction ............................................................................................................................. 214 7.2 Aquaculture ............................................................................................................................ 214

7.2.1 Regional Activity ....................................................................................................... 214 7.2.2 Regional Economic Value and Employment ............................................................ 215 7.2.3 Future Trends ........................................................................................................... 215

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

R4032/3 xiii R.1905

7.3 Aviation ................................................................................................................................... 215 7.3.1 Regional Activity ....................................................................................................... 215 7.3.2 Regional Economic Value and Employment ............................................................ 216 7.3.3 Future Trends ........................................................................................................... 216

7.4 Carbon Capture and Storage ................................................................................................. 216 7.4.1 Regional Activity ....................................................................................................... 216 7.4.2 Regional Economic Value and Employment ............................................................ 217 7.4.3 Future Trends ........................................................................................................... 217

7.5 Coast Protection and Flood Defence ...................................................................................... 218 7.5.1 Regional Activity ....................................................................................................... 218 7.5.2 Regional Economic Value and Employment ............................................................ 218 7.5.3 Future Trends ........................................................................................................... 218

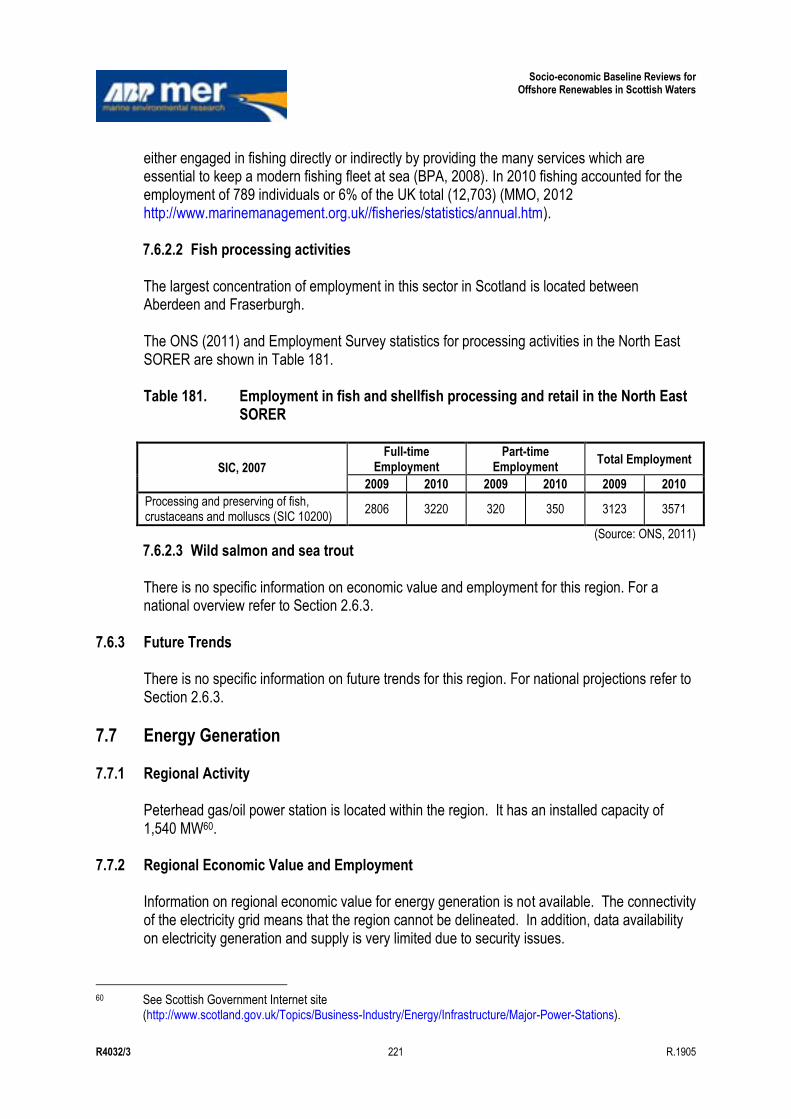

7.6 Commercial Fisheries ............................................................................................................. 219 7.6.1 Regional Activity ....................................................................................................... 219 7.6.2 Regional Economic Value and Employment ............................................................ 220 7.6.3 Future Trends ........................................................................................................... 221

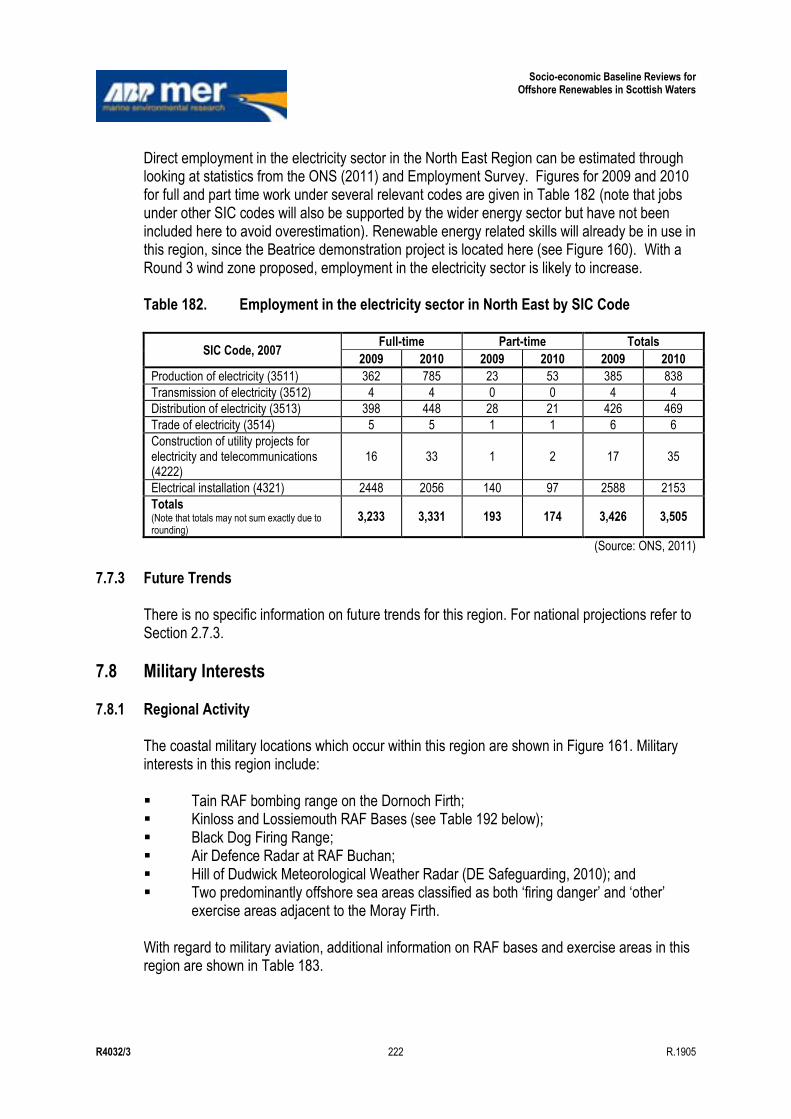

7.7 Energy Generation ................................................................................................................. 221 7.7.1 Regional Activity ....................................................................................................... 221 7.7.2 Regional Economic Value and Employment ............................................................ 221 7.7.3 Future Trends ........................................................................................................... 222

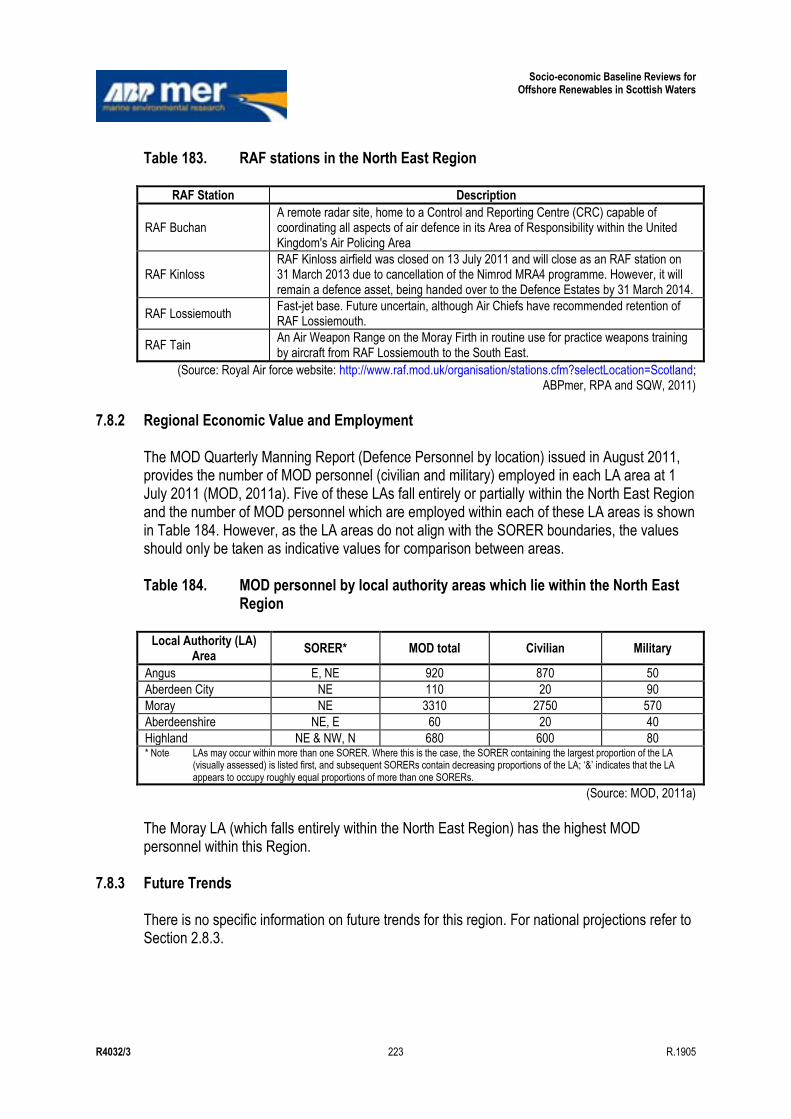

7.8 Military Interests ..................................................................................................................... 222 7.8.1 Regional Activity ....................................................................................................... 222 7.8.2 Regional Economic Value and Employment ............................................................ 223 7.8.3 Future Trends ........................................................................................................... 223

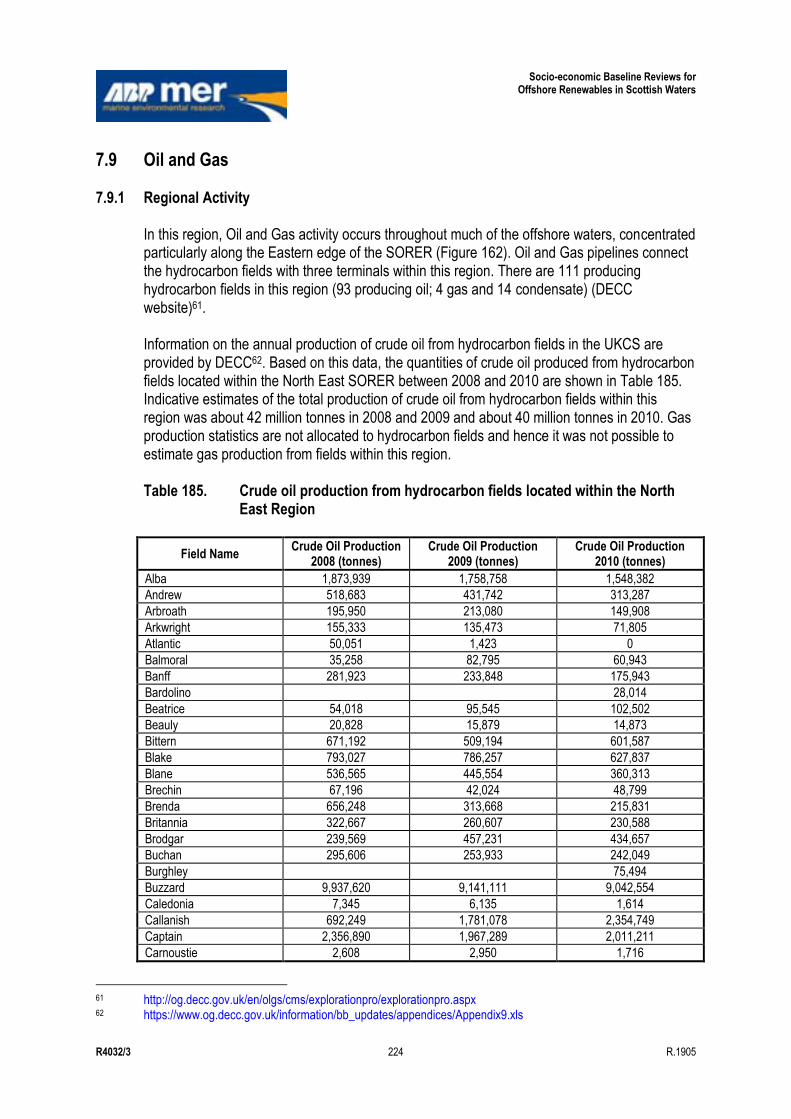

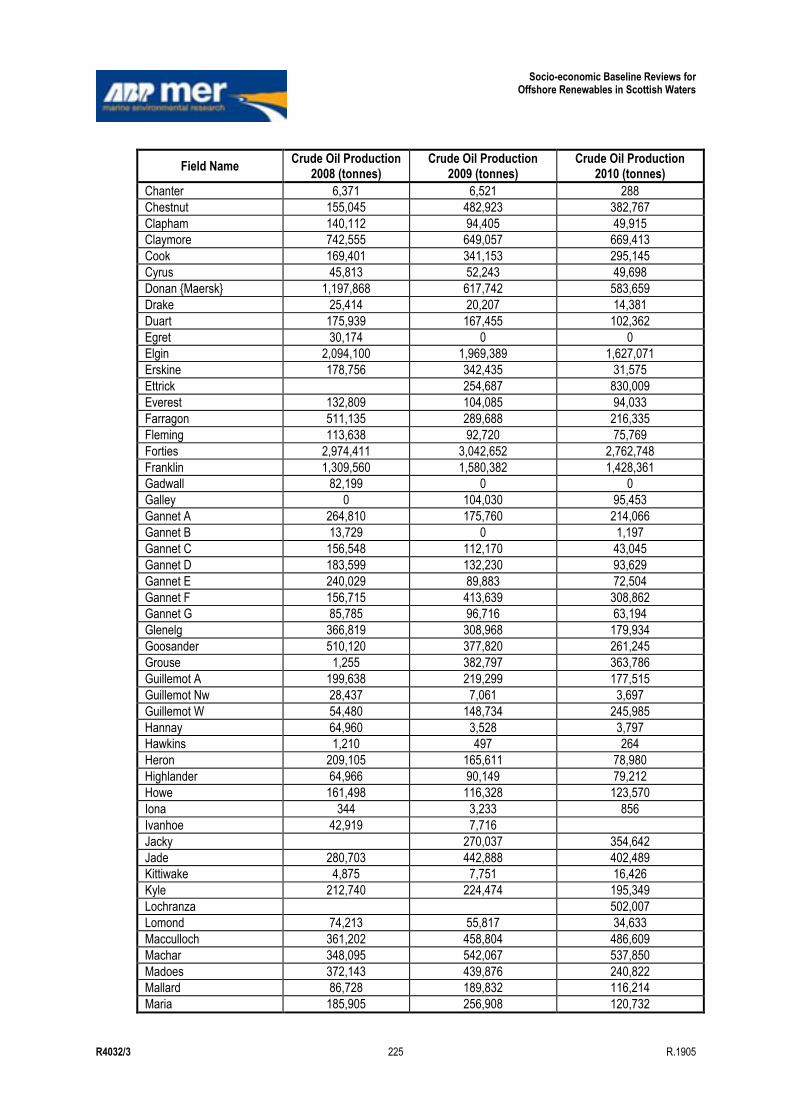

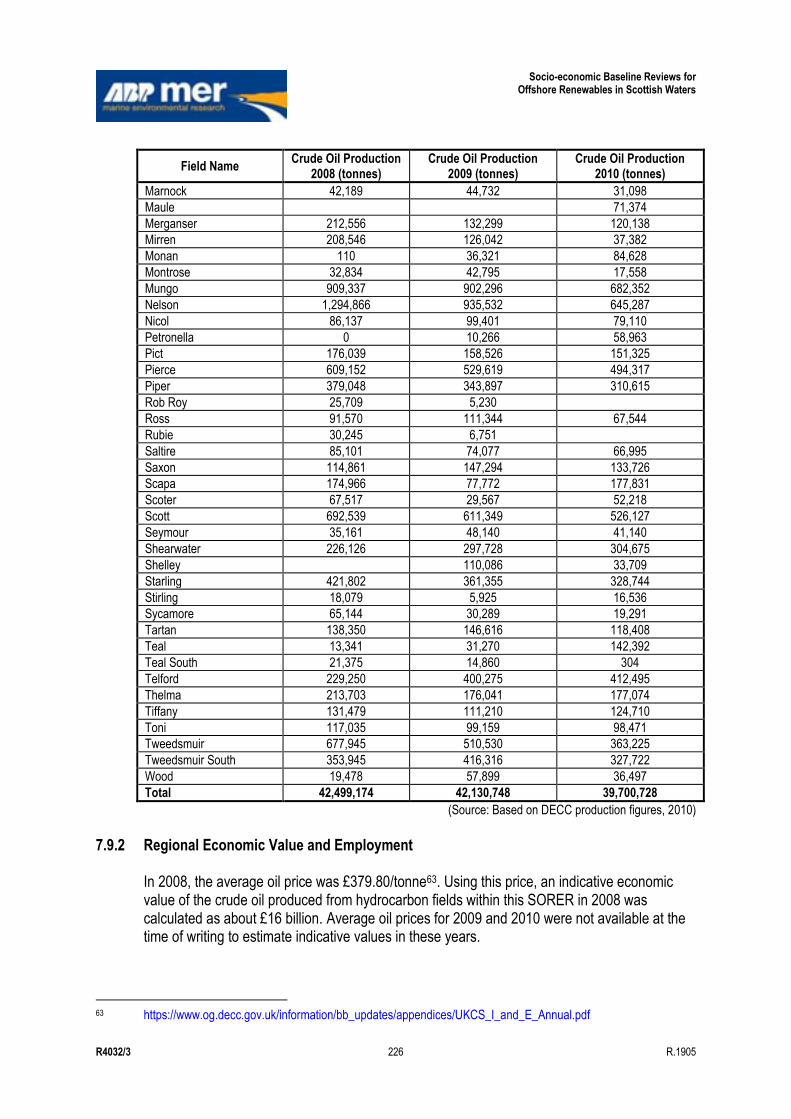

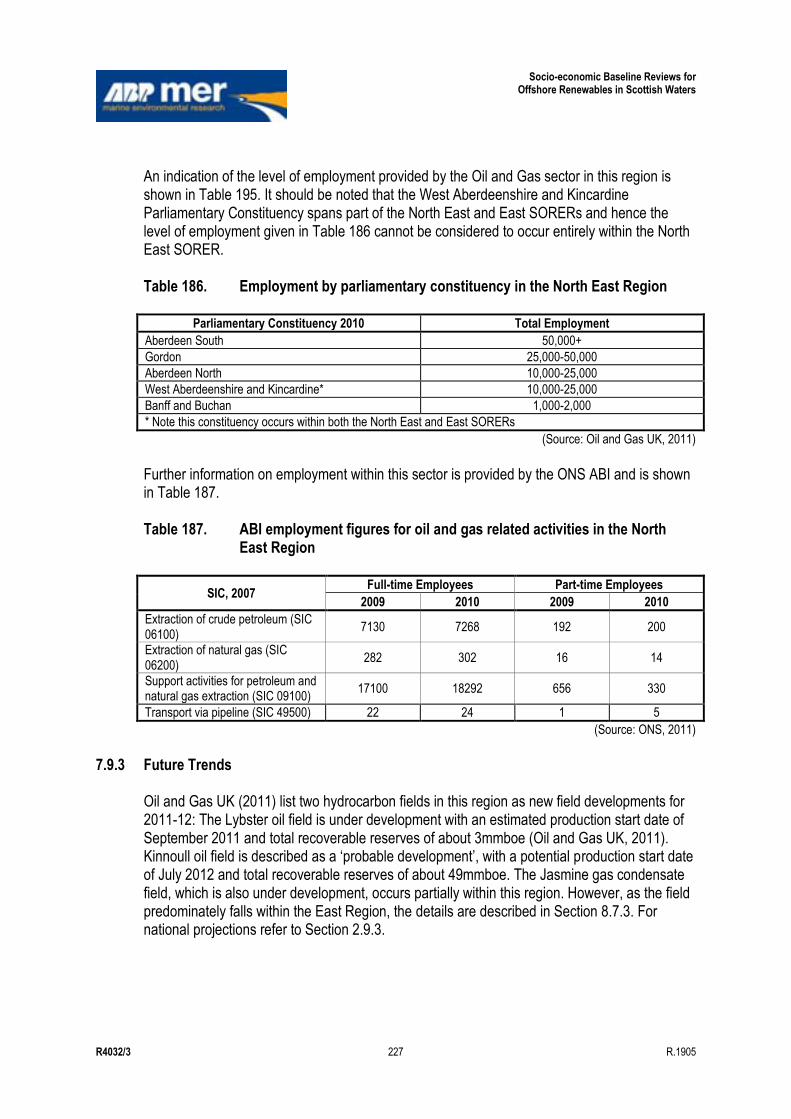

7.9 Oil and Gas ............................................................................................................................ 224 7.9.1 Regional Activity ....................................................................................................... 224 7.9.2 Regional Economic Value and Employment ............................................................ 226 7.9.3 Future Trends ........................................................................................................... 227

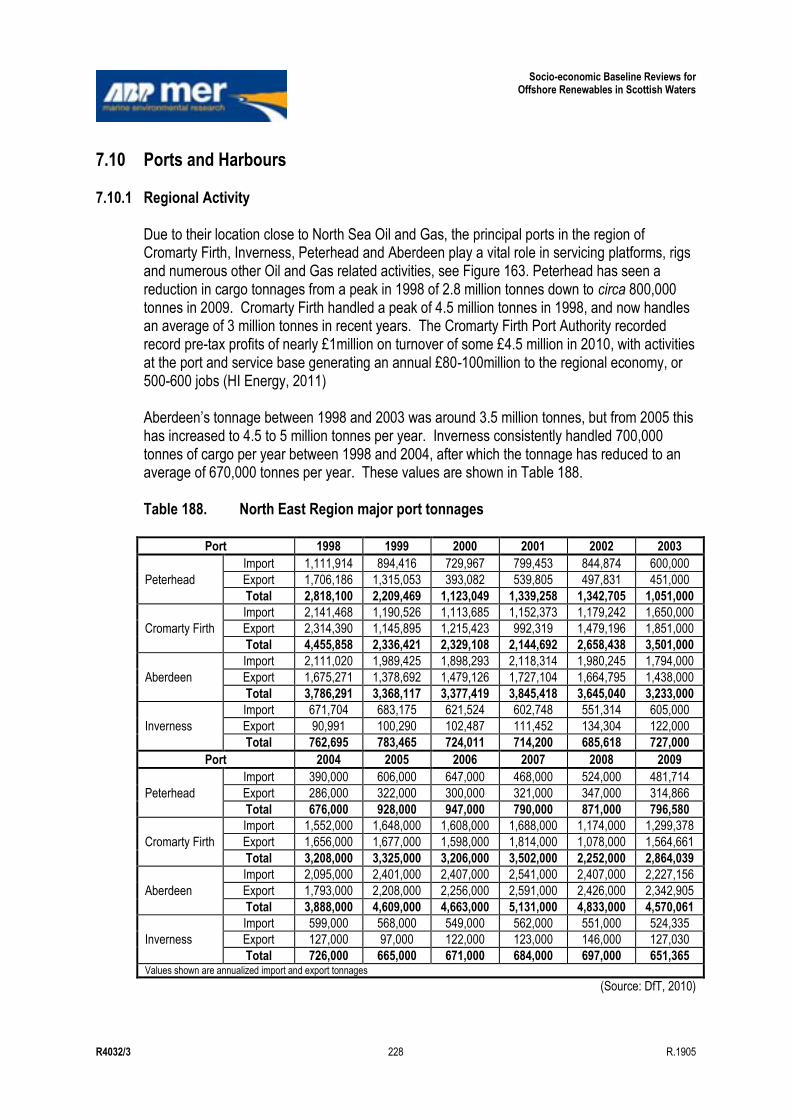

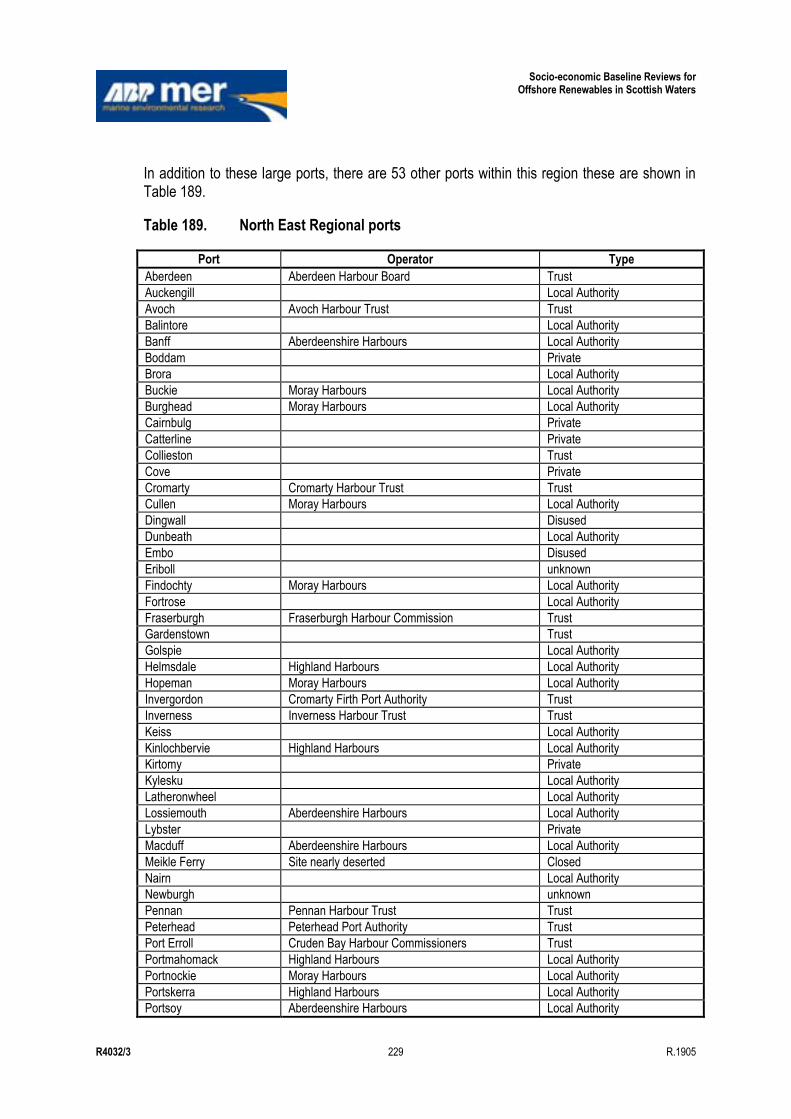

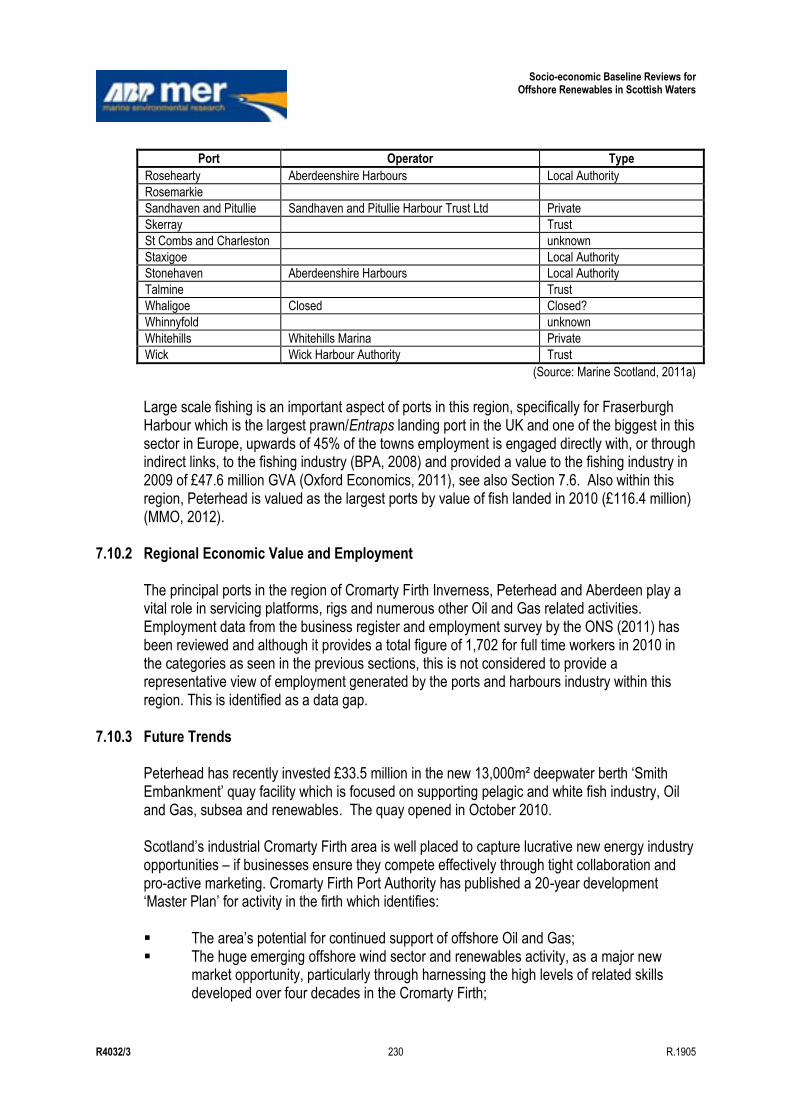

7.10 Ports and Harbours ................................................................................................................ 228 7.10.1 Regional Activity ....................................................................................................... 228 7.10.2 Regional Economic Value and Employment ............................................................ 230 7.10.3 Future Trends ........................................................................................................... 230

7.11 Power Interconnectors ............................................................................................................ 231 7.11.1 Regional Activity ....................................................................................................... 231 7.11.2 Regional Economic Value and Employment ............................................................ 231 7.11.3 Future Trends ........................................................................................................... 231

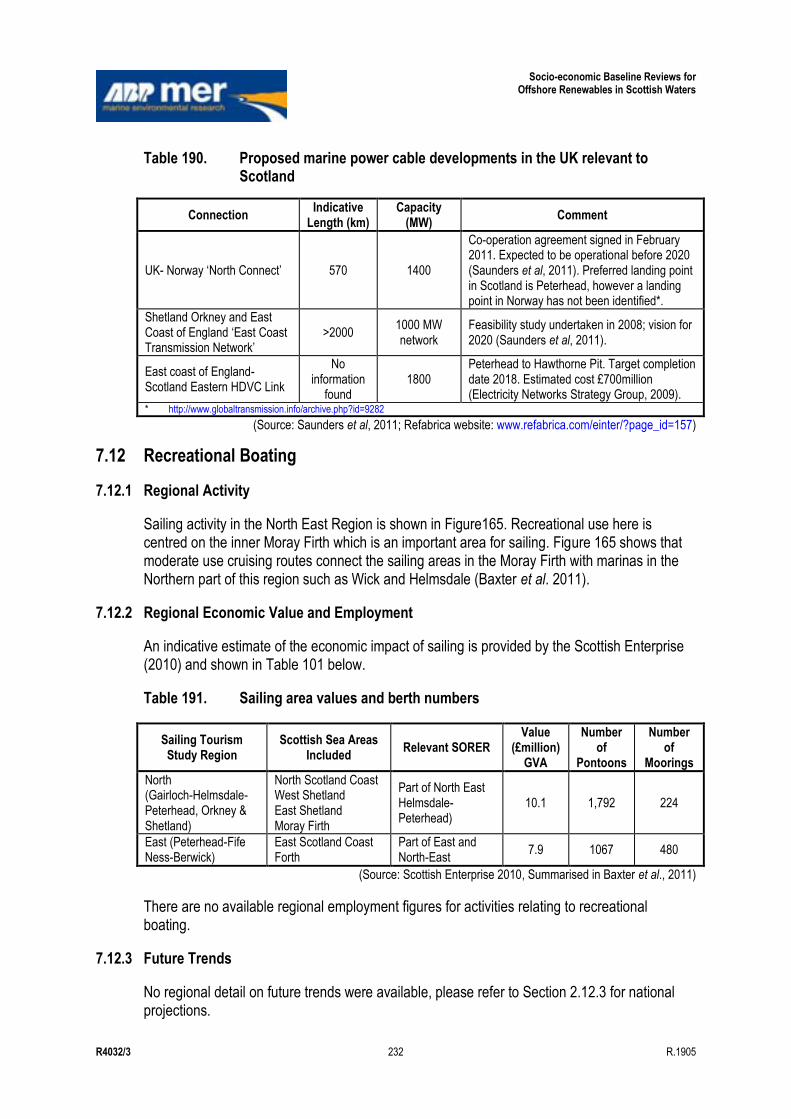

7.12 Recreational Boating .............................................................................................................. 232 7.12.1 Regional Activity ....................................................................................................... 232 7.12.2 Regional Economic Value and Employment ............................................................ 232 7.12.3 Future Trends ........................................................................................................... 232

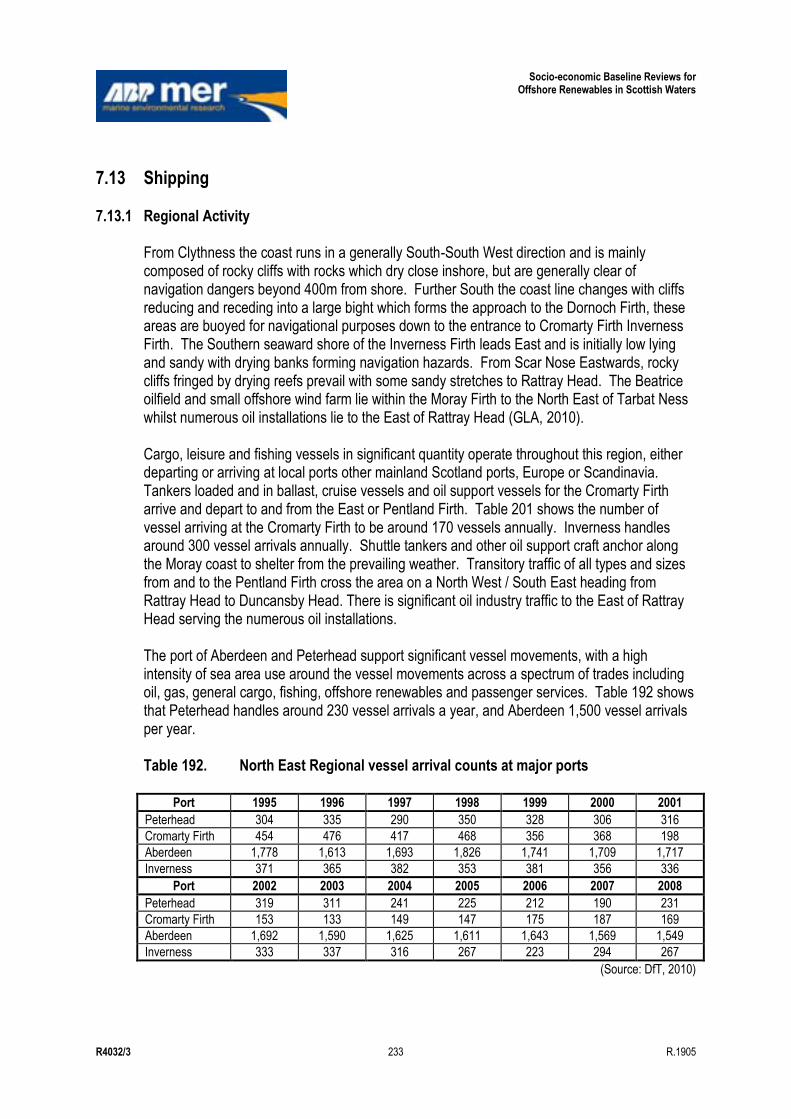

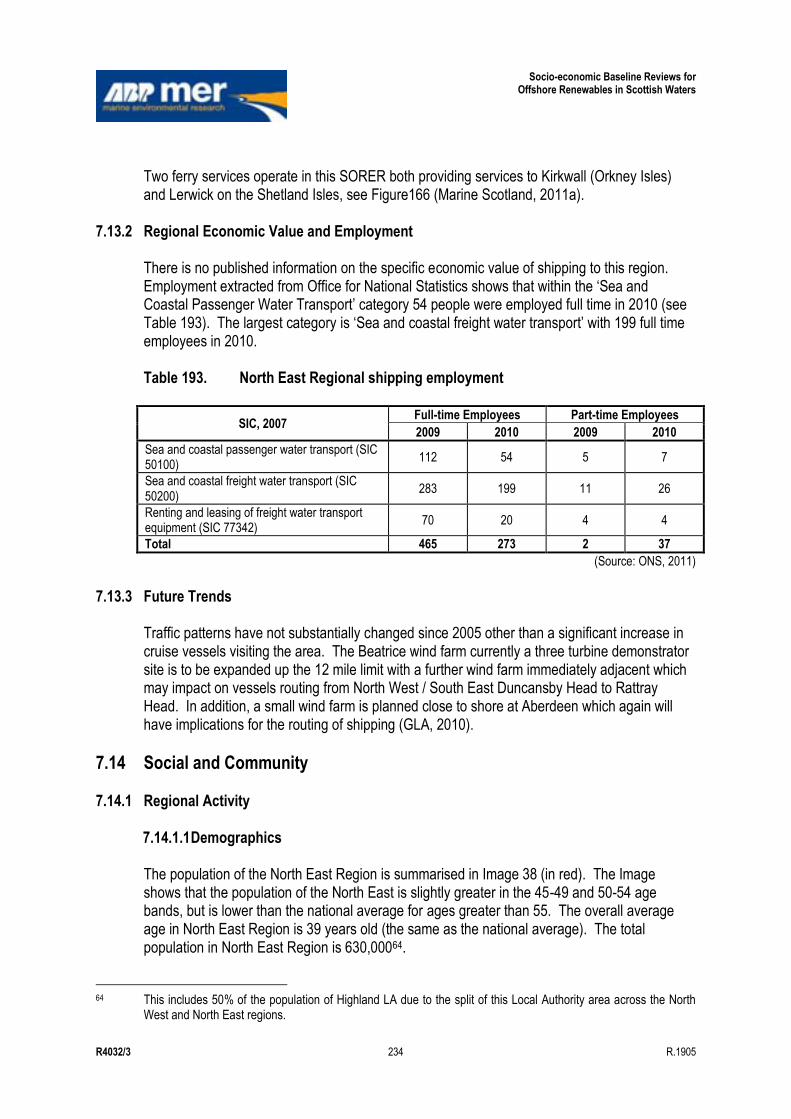

7.13 Shipping ................................................................................................................................. 233 7.13.1 Regional Activity ....................................................................................................... 233 7.13.2 Regional Economic Value and Employment ............................................................ 234 7.13.3 Future Trends ........................................................................................................... 234

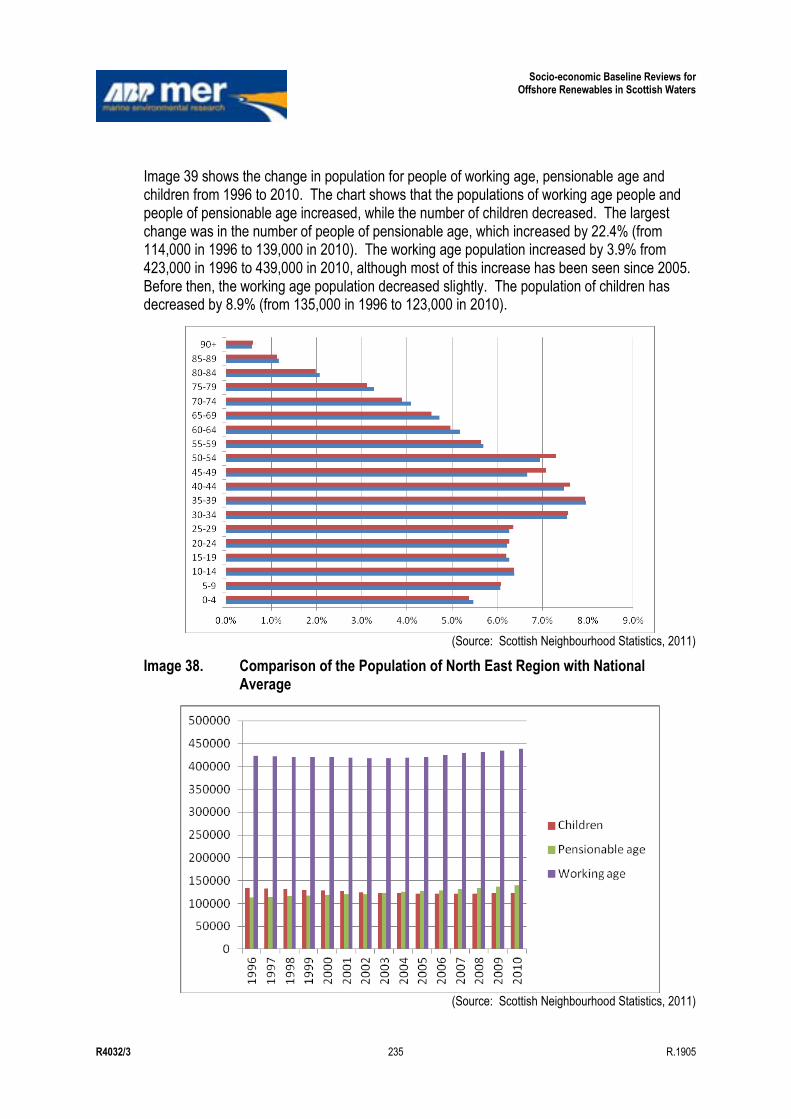

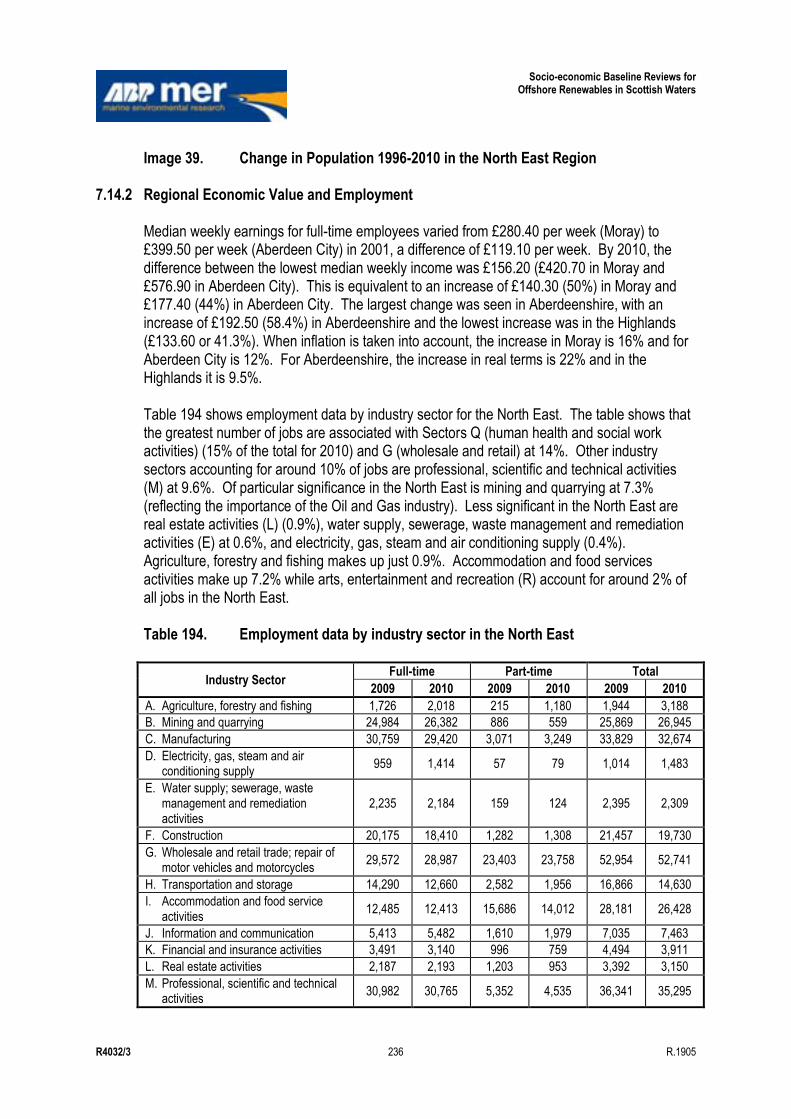

7.14 Social and Community ............................................................................................................ 234 7.14.1 Regional Activity ....................................................................................................... 234 7.14.2 Regional Economic Value and Employment ............................................................ 236 7.14.3 Future Trends ........................................................................................................... 241

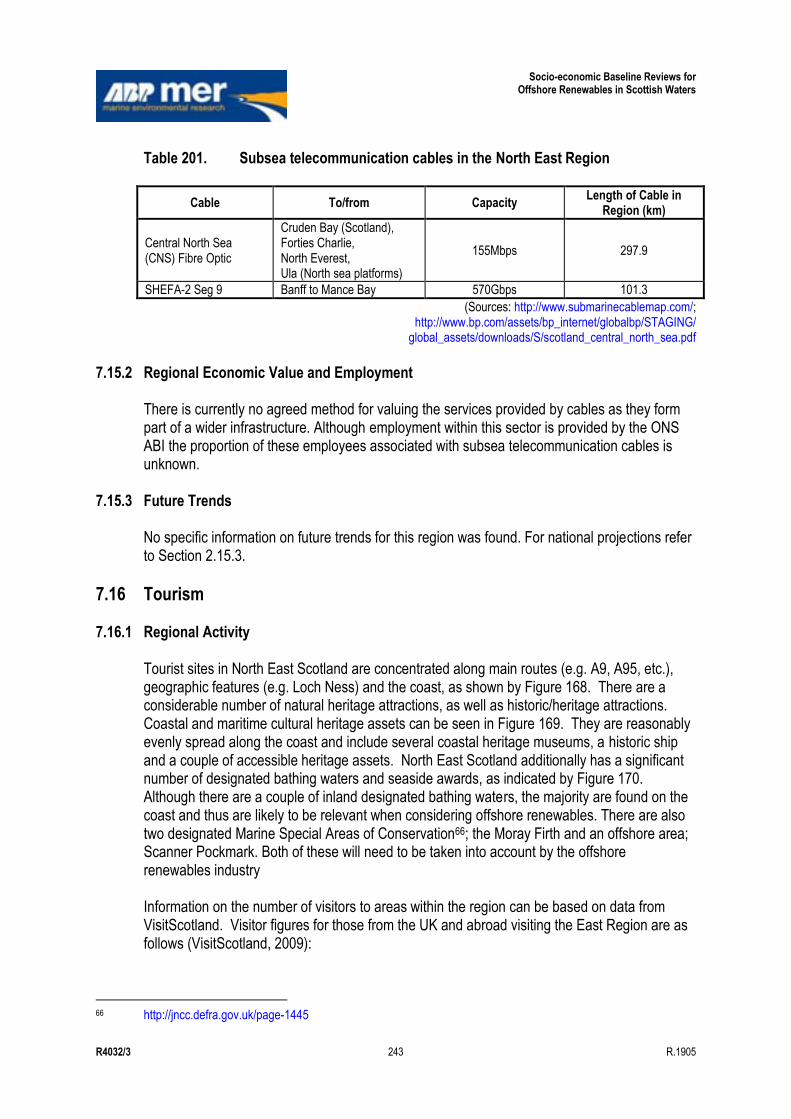

7.15 Telecomm Cables................................................................................................................... 242 7.15.1 Regional Activity ....................................................................................................... 242 7.15.2 Regional Economic Value and Employment ............................................................ 243 7.15.3 Future Trends ........................................................................................................... 243

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

R4032/3 xiv R.1905

7.16 Tourism .................................................................................................................................. 243 7.16.1 Regional Activity ....................................................................................................... 243 7.16.2 Regional Economic Value and Employment ............................................................ 244 7.16.3 Future Trends ........................................................................................................... 244

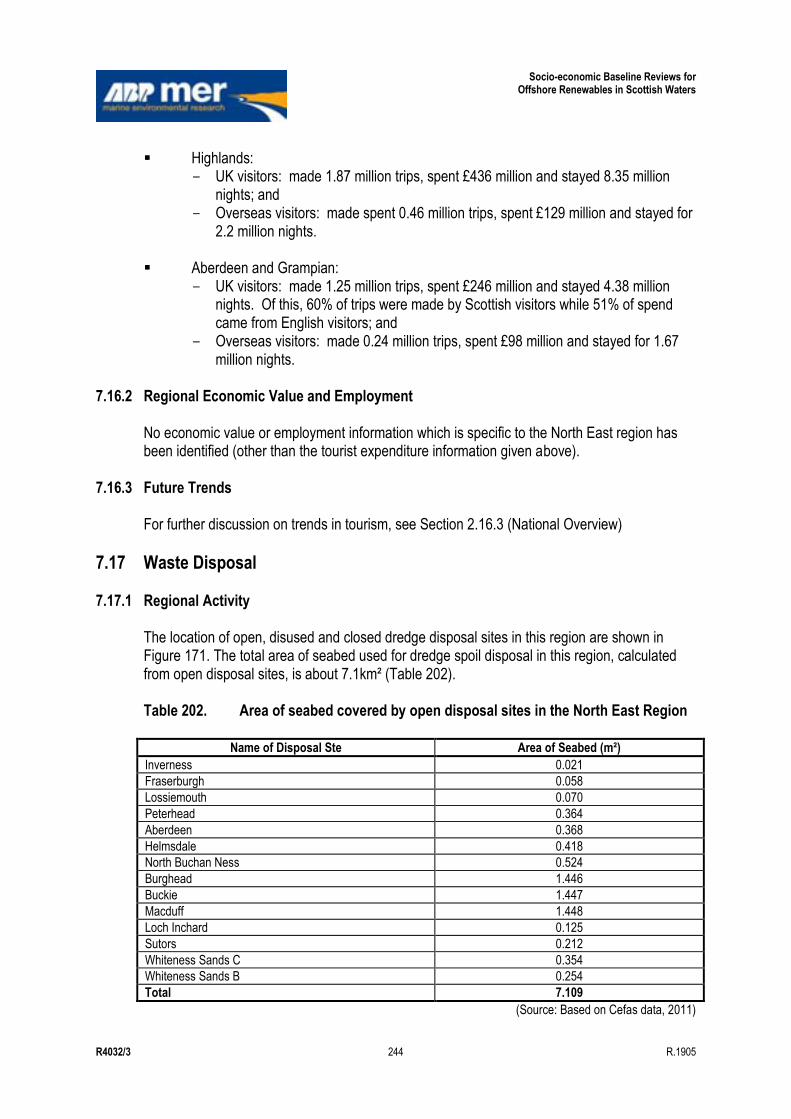

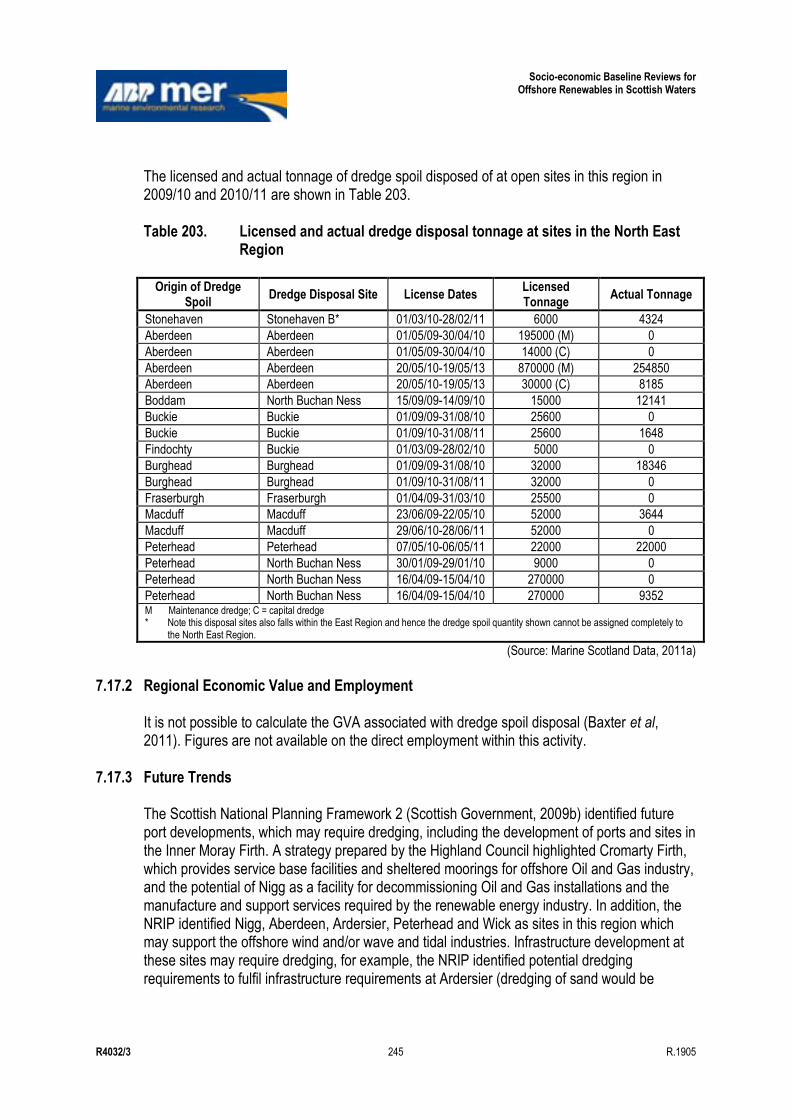

7.17 Waste Disposal....................................................................................................................... 244 7.17.1 Regional Activity ....................................................................................................... 244 7.17.2 Regional Economic Value and Employment ............................................................ 245 7.17.3 Future Trends ........................................................................................................... 245

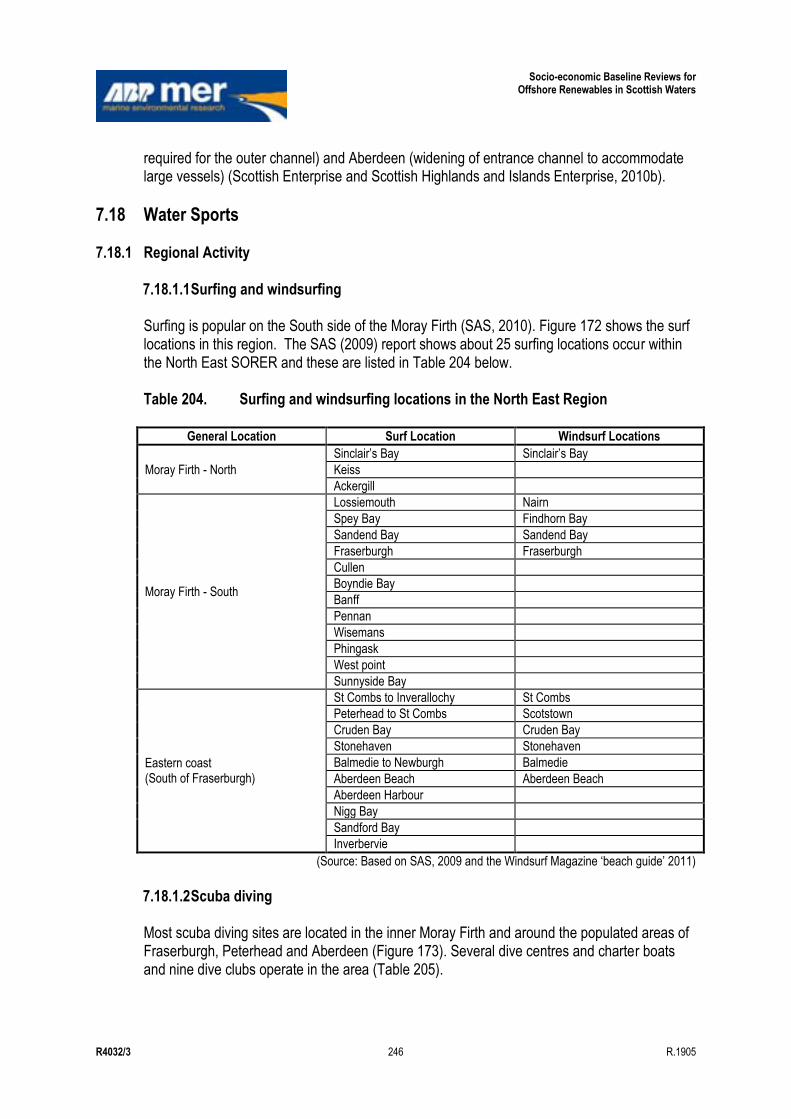

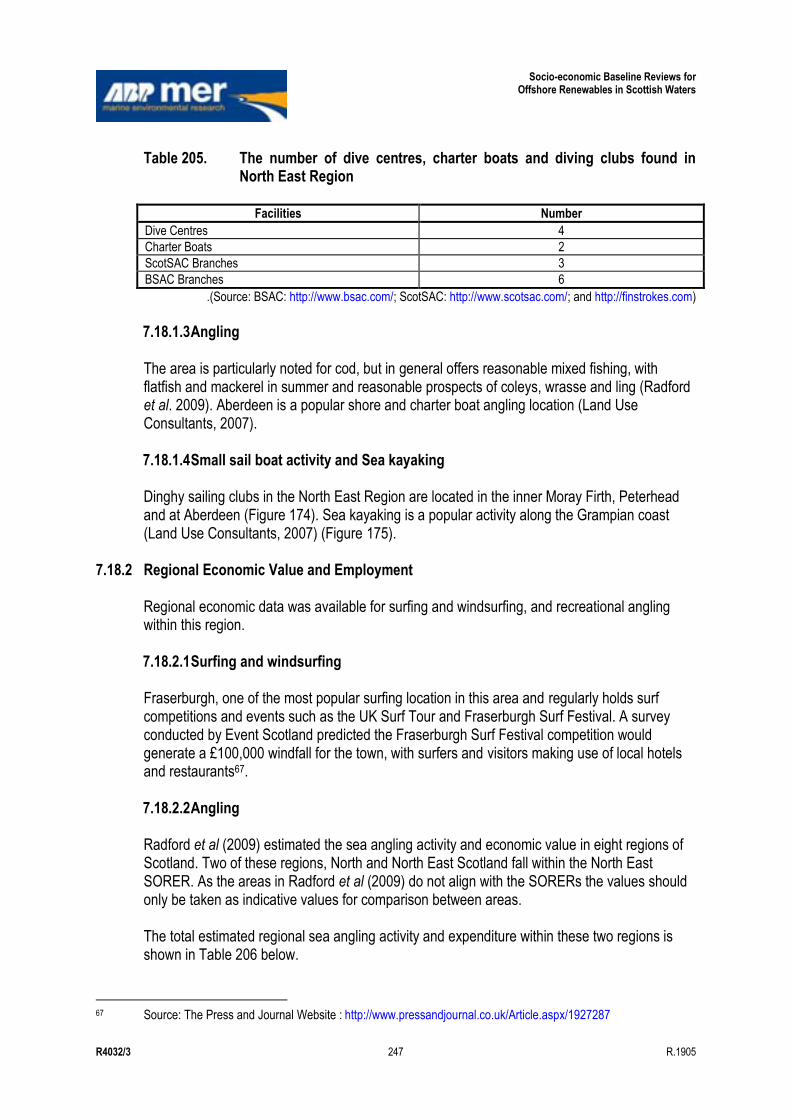

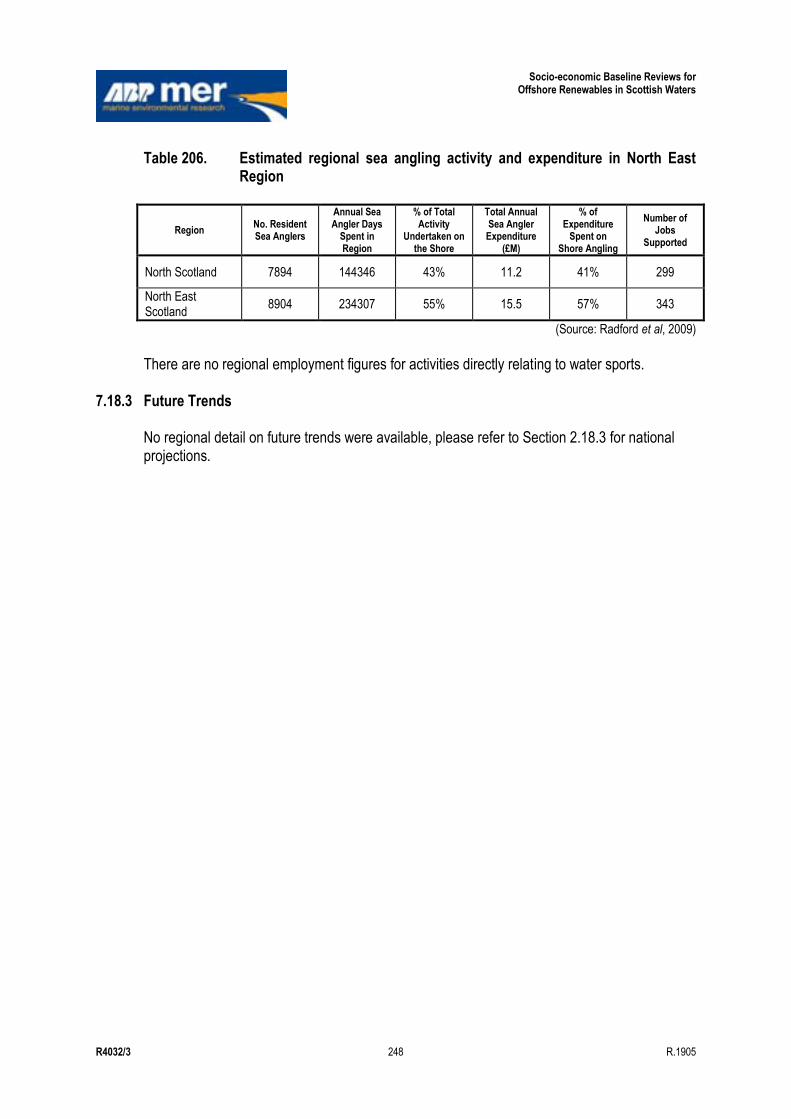

7.18 Water Sports .......................................................................................................................... 246 7.18.1 Regional Activity ....................................................................................................... 246 7.18.2 Regional Economic Value and Employment ............................................................ 247 7.18.3 Future Trends ........................................................................................................... 248

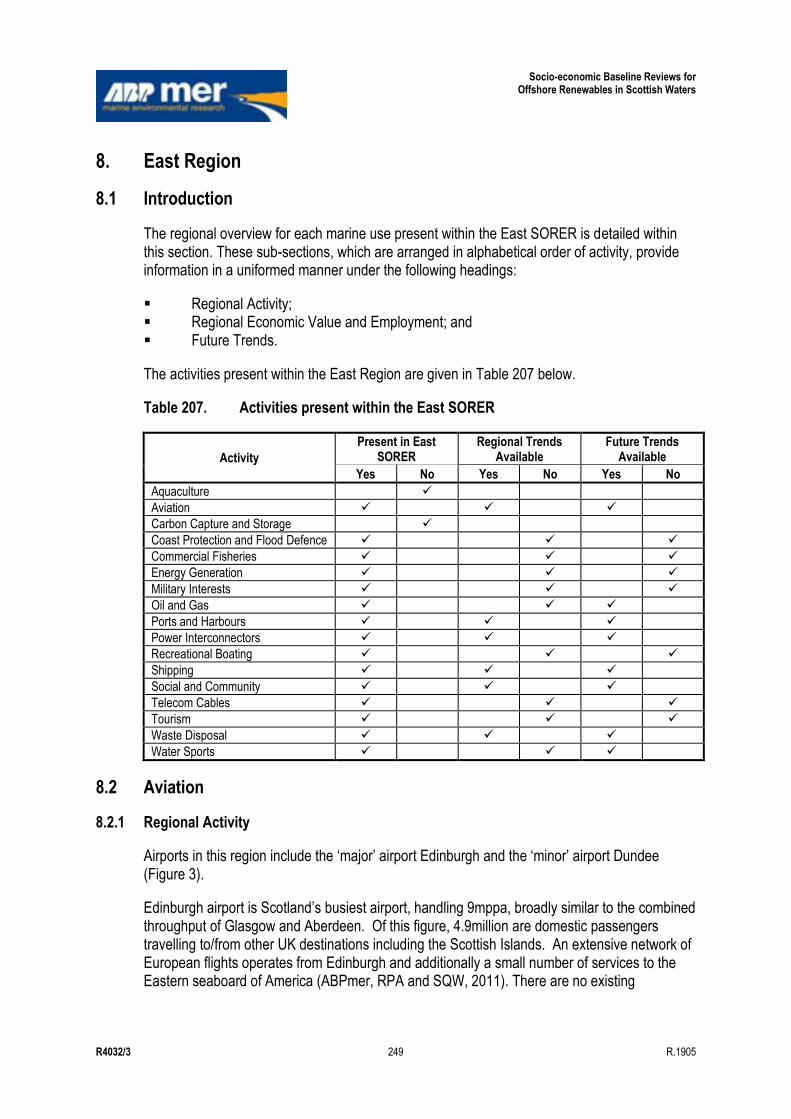

8. East Region ............................................................................................................................ 249 8.1 Introduction ............................................................................................................................. 249 8.2 Aviation ................................................................................................................................... 249

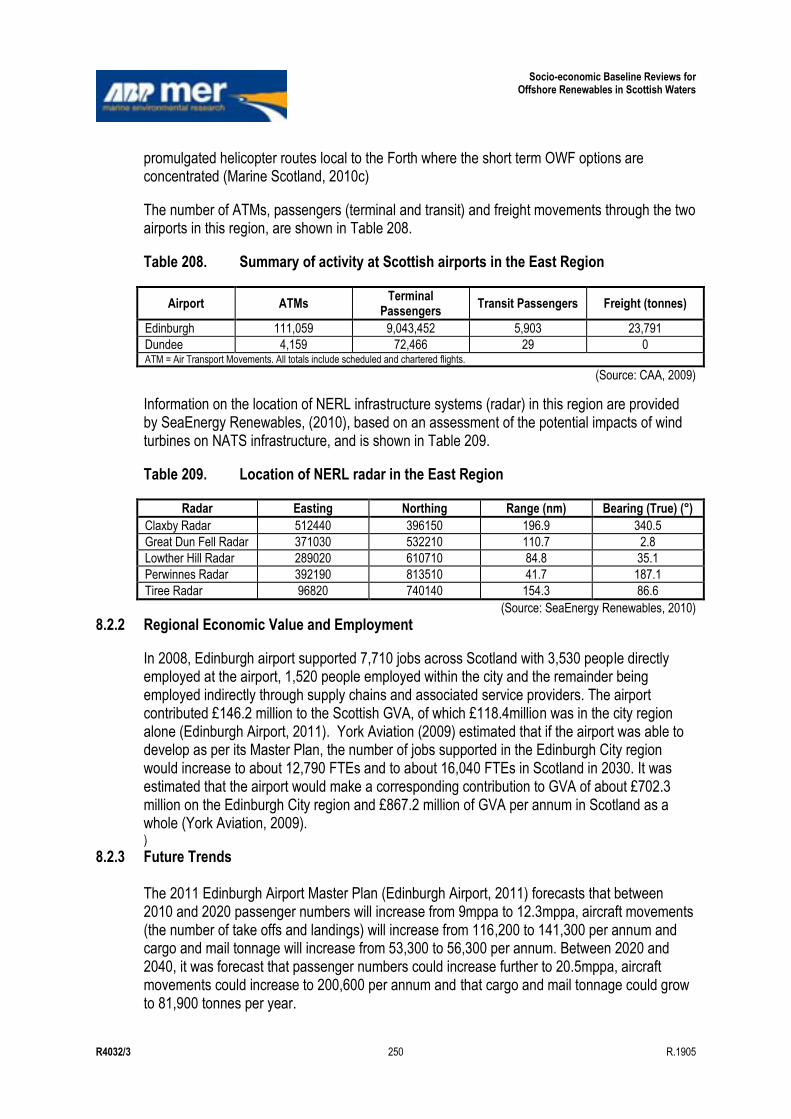

8.2.1 Regional Activity ....................................................................................................... 249 8.2.2 Regional Economic Value and Employment ............................................................ 250 8.2.3 Future Trends ........................................................................................................... 250

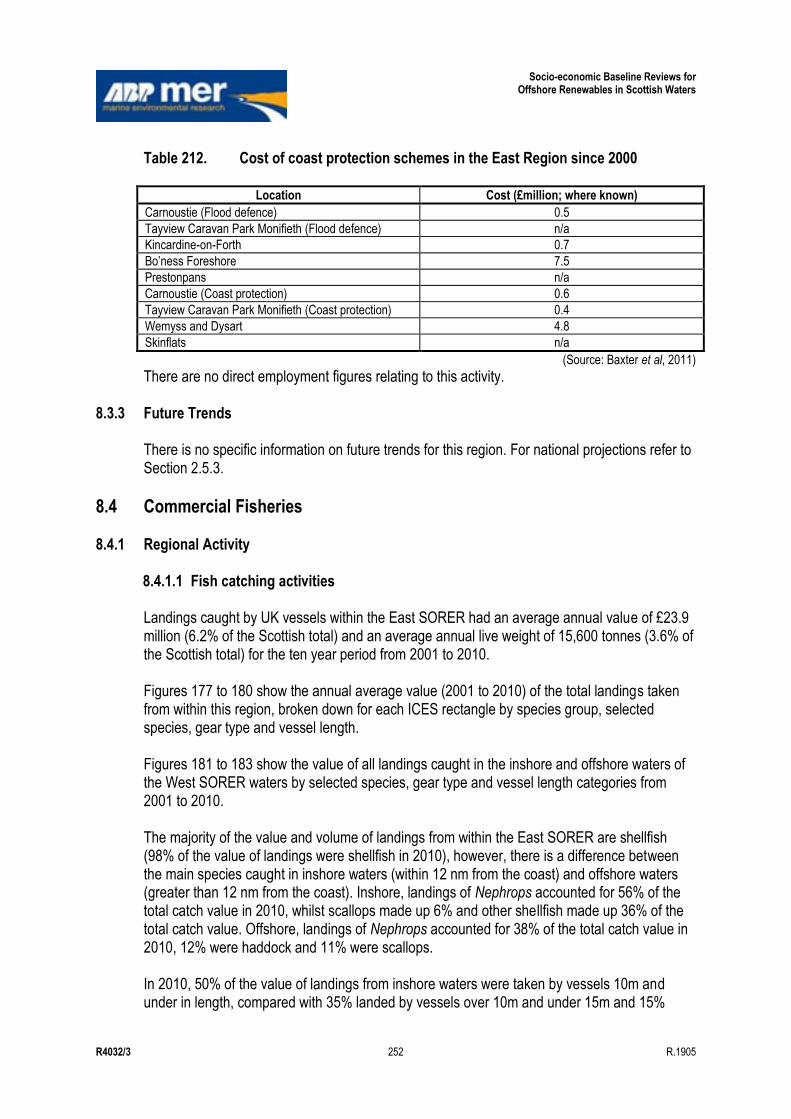

8.3 Coast Protection and Flood Defence ...................................................................................... 251 8.3.1 Regional Activity ....................................................................................................... 251 8.3.2 Regional Economic Value and Employment ............................................................ 251 8.3.3 Future Trends ........................................................................................................... 252

8.4 Commercial Fisheries ............................................................................................................. 252 8.4.1 Regional Activity ....................................................................................................... 252 8.4.2 Regional Economic Value and Employment ............................................................ 254 8.4.3 Future Trends ........................................................................................................... 254

8.5 Energy Generation ................................................................................................................. 254 8.5.1 Regional Activity ....................................................................................................... 254 8.5.2 Regional Economic Value and Employment ............................................................ 255 8.5.3 Future Trends ........................................................................................................... 255

8.6 Military Interests ..................................................................................................................... 255 8.6.1 Regional Activity ....................................................................................................... 255 8.6.2 Regional Economic Value and Employment ............................................................ 256 8.6.3 Future Trends ........................................................................................................... 257

8.7 Oil and Gas ............................................................................................................................ 257 8.7.1 Regional Activity ....................................................................................................... 257 8.7.2 Regional Economic Value and Employment ............................................................ 258 8.7.3 Future Trends ........................................................................................................... 258

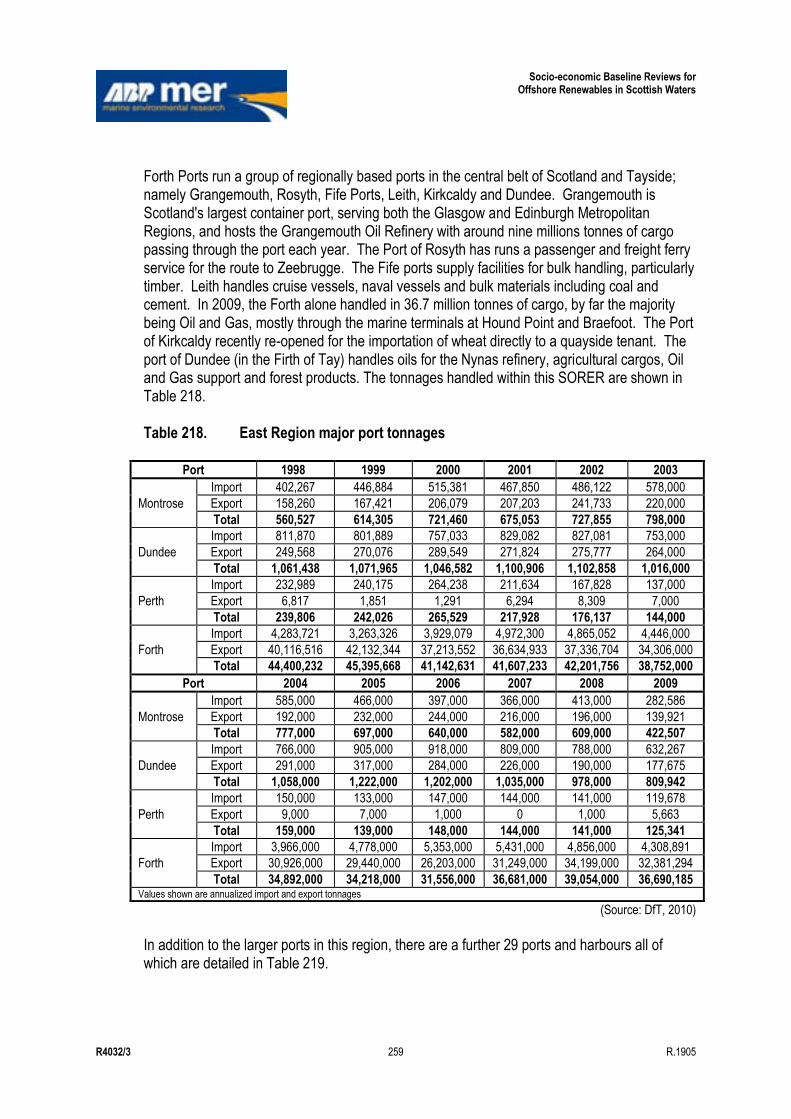

8.8 Ports and Harbours ................................................................................................................ 258 8.8.1 Regional Activity ....................................................................................................... 258 8.8.2 Regional Economic Value and Employment ............................................................ 260 8.8.3 Future Trends ........................................................................................................... 261

8.9 Power Interconnectors ............................................................................................................ 261 8.9.1 Regional Activity ....................................................................................................... 261 8.9.2 Regional Economic Value and Employment ............................................................ 261 8.9.3 Future Trends ........................................................................................................... 262

8.10 Recreational Boating .............................................................................................................. 262 8.10.1 Regional Activity ....................................................................................................... 262 8.10.2 Regional Economic Value and Employment ............................................................ 262 8.10.3 Future Trends ........................................................................................................... 262

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

R4032/3 xv R.1905

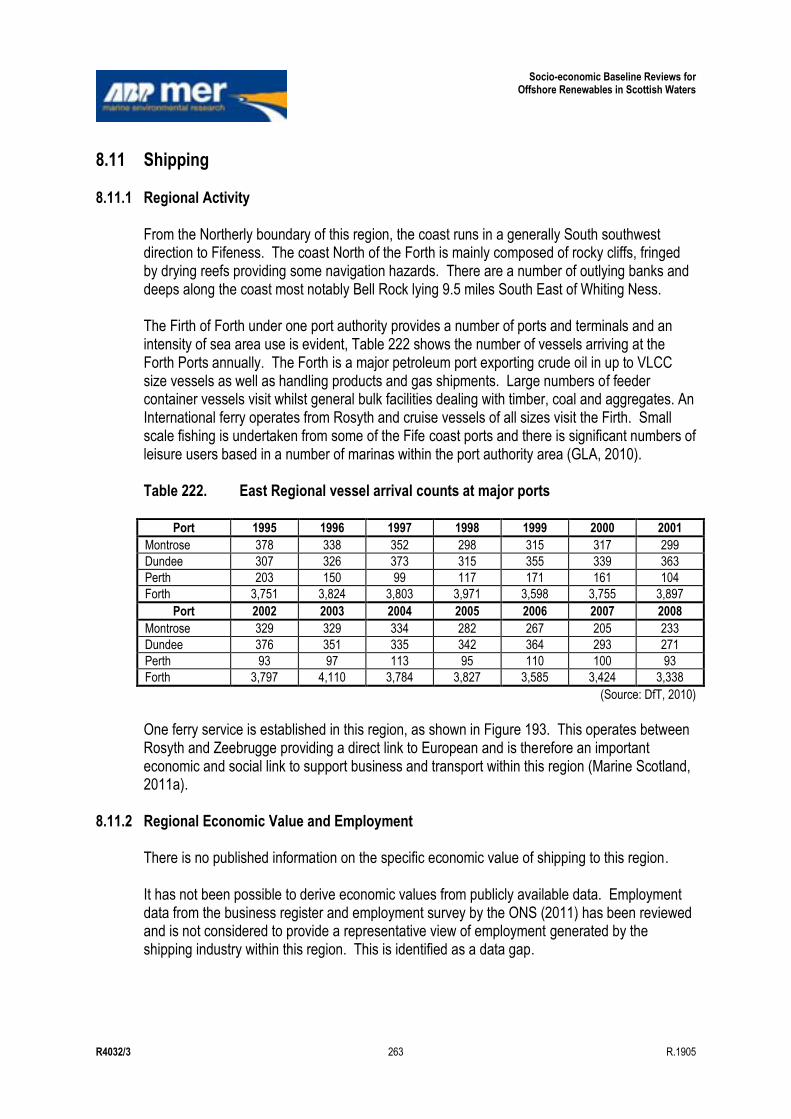

8.11 Shipping ................................................................................................................................. 263 8.11.1 Regional Activity ....................................................................................................... 263 8.11.2 Regional Economic Value and Employment ............................................................ 263 8.11.3 Future Trends ........................................................................................................... 264

8.12 Social and Community ............................................................................................................ 264 8.12.1 Regional Activity ....................................................................................................... 264 8.12.2 Regional Economic Value and Employment ............................................................ 265 8.12.3 Future Trends ........................................................................................................... 271

8.13 Telecomm Cables................................................................................................................... 271 8.13.1 Regional Activity ....................................................................................................... 271 8.13.2 Regional Economic Value and Employment ............................................................ 272 8.13.3 Future Trends ........................................................................................................... 272

8.14 Tourism .................................................................................................................................. 272 8.14.1 Regional Activity ....................................................................................................... 272 8.14.2 Regional Economic Value and Employment ............................................................ 274 8.14.3 Future Trends ........................................................................................................... 274

8.15 Waste Disposal....................................................................................................................... 274 8.15.1 Regional Activity ....................................................................................................... 274 8.15.2 Regional Economic Value and Employment ............................................................ 275 8.15.3 Future Trends ........................................................................................................... 275

8.16 Water Sports .......................................................................................................................... 276 8.16.1 Regional Activity ....................................................................................................... 276 8.16.2 Regional Economic Value and Employment ............................................................ 277 8.16.3 Future Trends ........................................................................................................... 278

9. References ............................................................................................................................. 279

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

R4032/3 xvi R.1905

Tables 1. Data sources used in the aquaculture baseline .......................................................................... 2 2. ABI statistics relating to employment in Scotland within the aquaculture sector ........................ 4 3. Information sources for aviation baseline ................................................................................... 7 4. Summary of air transport statistics from 1999 to 2009 ................................................................ 8 5. Constrained terminal passenger and ATM „central‟ forecasts for major Scottish airports ........... 9 6. Information sources for CCS baseline ...................................................................................... 10 7. Information sources for coast protection and flood defence baseline ....................................... 12 8. Information sources for commercial fisheries baseline ............................................................. 13 9. Information sources for salmon and sea trout baseline ............................................................ 13 10. Quantity and value of landings by Scottish based vessels by species type and vessel

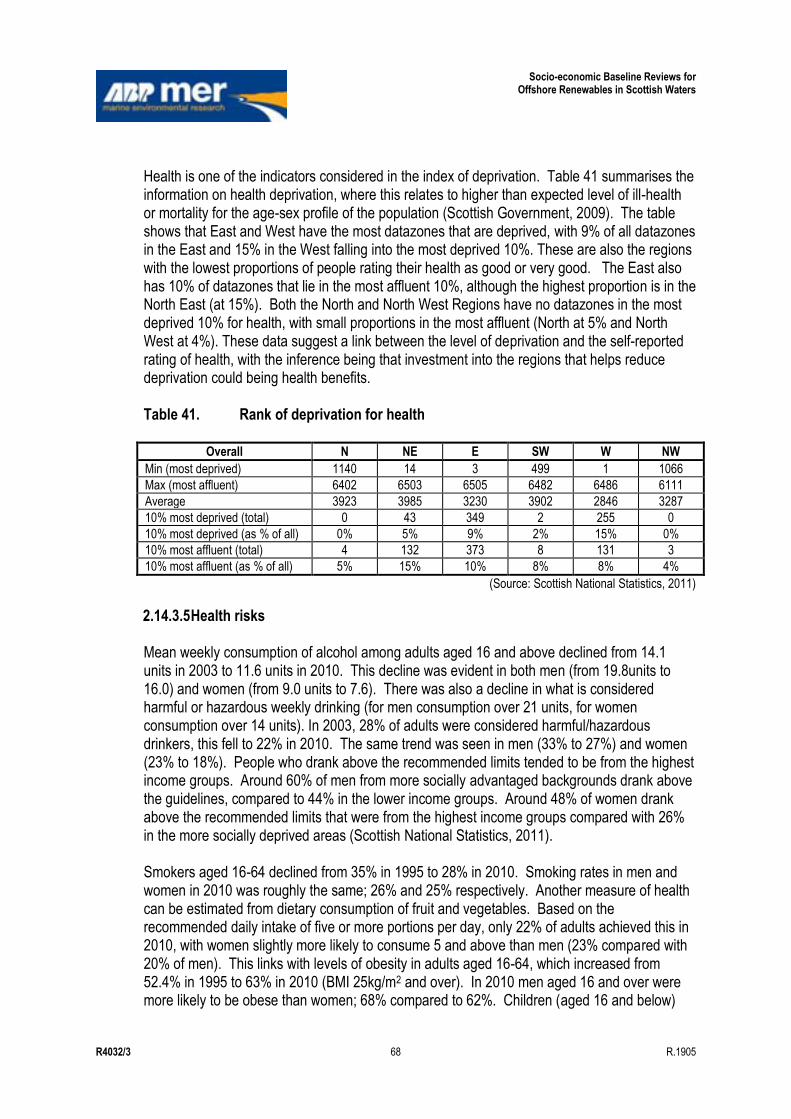

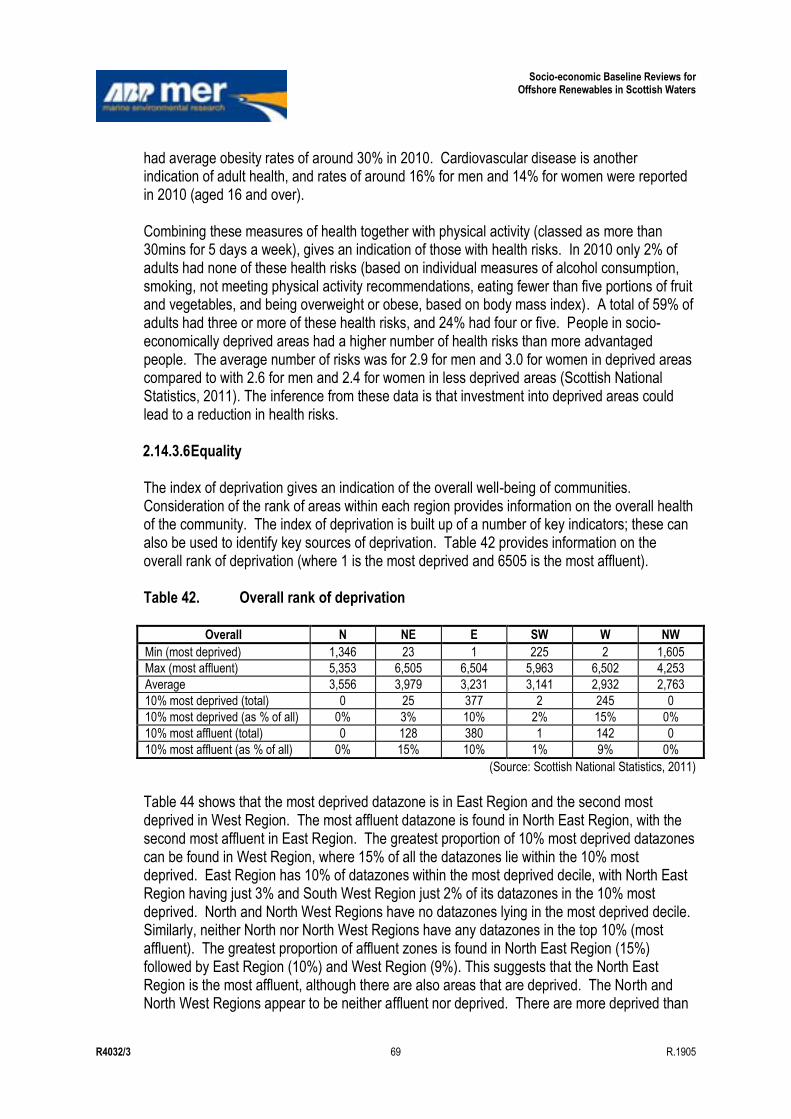

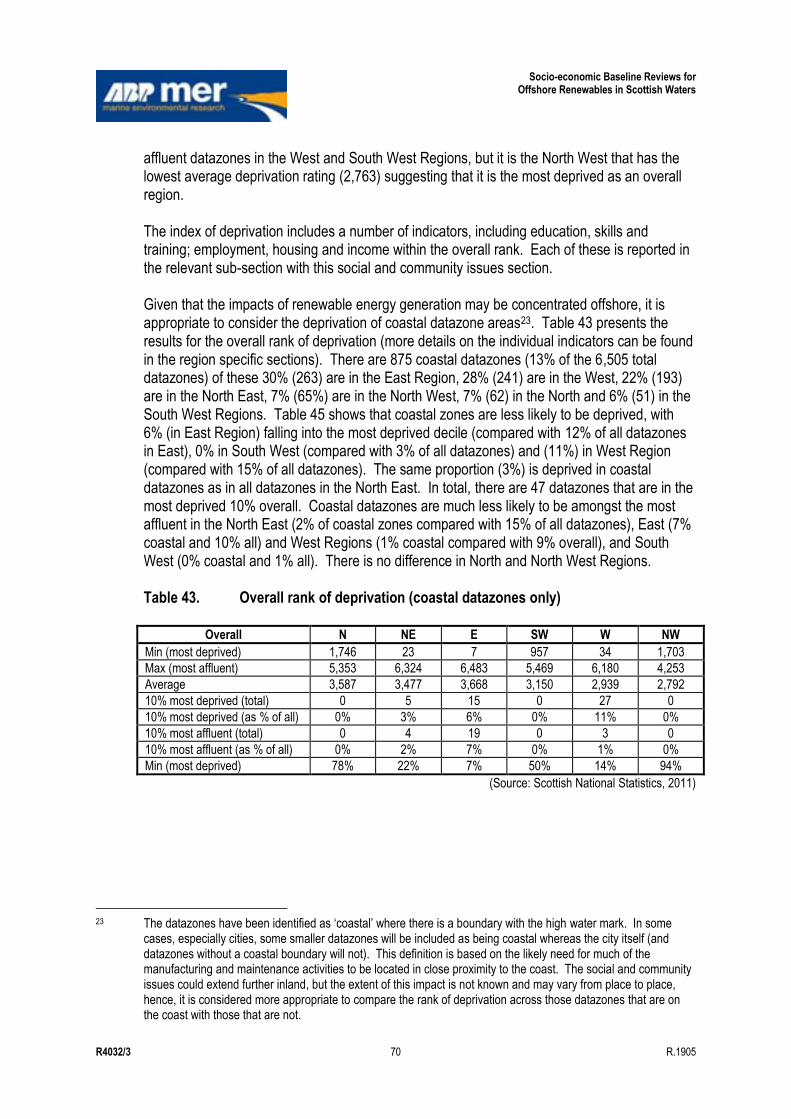

length (2010) ............................................................................................................................ 16 11. Landings into the top three Scottish ports (2010) ..................................................................... 17 12. Number of fishermen employed on Scottish based vessels, by district (2010) ......................... 18 13. Employment in fish and shellfish processing and retail in Scotland .......................................... 19 14. Reported annual catches, number of salmon (2006 - 2010) ..................................................... 23 15. Reported annual catches, number of sea trout (2006 - 2010) .................................................. 23 16. Data sources used in the energy generation chapter ............................................................... 25 17. Installed capacity for renewables in Scotland (MWe) ............................................................... 28 18. Direct employment in the electricity sector in Scotland by SIC Code ........................................ 31 19. Information sources for military interests baseline .................................................................... 35 20. Information sources for oil and gas baseline ............................................................................ 37 21. Production and revenues from oil and gas from Scottish sea areas between 2005-2008 ........ 38 22. ABI employment figures for oil and gas related activities in Scotland ....................................... 39 23. Information sources for ports and harbours baseline ................................................................ 41 24. Total Scottish port tonnages 1990 to 2008 ............................................................................... 44 25. Information sources for power interconnectors baseline ........................................................... 46 26. Proposed marine power cable developments in the UK relevant to Scotland ........................... 48 27. Data sources used in the recreational boating baseline ........................................................... 49 28. Economic impact of sailing in Scotland..................................................................................... 50 29. Estimate of annual compound growth in 'core' marina operations ............................................ 51 30. Data sources used in the shipping baseline ............................................................................. 52 31. Ship type arrivals at 16 major ports .......................................................................................... 53 32. Employees in the shipping sector ............................................................................................. 54 33. Data sources used in the social and community chapter .......................................................... 56 34. Total population within each region (2001 census) ................................................................... 58 35. Total population within each region, broken down by age (2001 census) ................................. 60 36. Rank of deprivation for income ................................................................................................. 63 37. Rank of deprivation for employment ......................................................................................... 64 38. Employment data by industry sector ......................................................................................... 64 39. Number of crofts and crafting income by region ....................................................................... 66 40. Turnover of social economy in Scotland (2004 to 2009) ........................................................... 66 41. Rank of deprivation for health ................................................................................................... 68 42. Overall rank of deprivation ........................................................................................................ 69 43. Overall rank of deprivation (coastal datazones only) ................................................................ 70

Socio-economic Baseline Reviews for Offshore Renewables in Scottish Waters

R4032/3 xvii R.1905