SME Bank Limited - privatisation.gov.pk Teaser Final.pdf · | 1 This Preliminary Information...

22

SME Bank Limited Preliminary Information Memorandum / Transaction Teaser February 2017 Financial Advisors

Transcript of SME Bank Limited - privatisation.gov.pk Teaser Final.pdf · | 1 This Preliminary Information...

SME Bank LimitedPreliminary Information Memorandum / Transaction Teaser

February 2017

Financial Advisors

| 1

This Preliminary Information Memorandum/Transaction Teaser (the “PIM“ or the “Teaser”) describes and summarizes the key highlights of SME Bank Limited (the “Bank”) and has been prepared by Elixir Securities Pakistan (Private)

Limited (“ES”) and Bridge Factor (Private) Limited (“BF”), the Financial Advisors (the “FA”) , on behalf of the Privatisation Commission (the “PC”), solely for informational purposes and to be used by prospective investors in

considering their interest in the privatisation process of the Bank. KPMG Taseer Hadi & Company and Mohsin Tayebaly & Company (the “Sub-Consultants”), appointed for this transaction, along with the FA express no opinion on

any of the financial statements or other data/ information included in this PIM.

This PIM has been prepared to assist prospective investors in making their own evaluation of the Bank and does not purport to contain all the information which a prospective investor may desire. In all cases, prospective investors

should conduct their own investigation/due diligence and analysis of the Bank and the data set forth in this PIM. In making an investment decision, each recipient must rely on their own examination of the Bank and the terms &

conditions of the transaction and any offering, including the merits and risks involved in making an investment in the Bank. The contents of this PIM are not to be construed as legal, financial or tax advice. Each recipient should

consult their own legal advisor, financial advisor or tax advisor for legal, financial or tax advice. The PC, the Bank or the FA do not make any representation or warranty as to the accuracy or completeness of the information

contained in this PIM or made available in connection with any further investigation/due diligence of the Bank, including estimates or forecasts, and neither shall have any liability for any representations, expressed or implied,

contained in, or omitted from, this PIM or any other written or oral communications transmitted to the recipient in the course of the evaluation of the Bank.

This PIM contains statements which constitute forward looking statements. These statements appear in a number of places in this PIM. Recipients are cautioned that such forward looking statements are not guarantees of future

performance and involve risks and uncertainties, and that actual results may differ materially from those in the forward looking statements as a result of various factors. With respect to the management of the Bank, any estimated

financial information presented by the Bank in this PIM, it is clarified that FA did not audit, compile, or apply agreed-upon procedures to such information. The FA, the Sub-Consultants, and their affiliated partnerships or bodies

corporate, the partners, directors, principals, managers, employees or agents of any of them (the “Parties”) have not independently verified or validated the information and therefore do not make any undertaking, representation

or provide any warranty, expressed or implied, as to the accuracy, reasonableness or completeness of the information contained in this document or of any other information relating to the Bank or its subsidiaries whether written,

oral or in a visual or electronic form (including, without limitation, in a digital form) transmitted or made available to the recipients or their respective advisors. An investment in the existing opportunity, the Bank, involves a certain

degree of risk and could involve restrictions on transfer, and therefore, should be considered only by sophisticated investors who are able to bear the economic risks of their investment for an indefinite period of time and who can

afford to sustain a loss of their investment, if any. There will usually be differences between estimated and actual results, because events and circumstances frequently do not occur as expected, and those differences may be

material.

The recipient of this PIM acknowledges and agrees that: (i) neither the PC nor the Bank nor the FA nor the Sub-Consultants will be subject to any liability based on the information contained in the PIM, errors therein or omissions

there from, whether or not the PC, the Bank, the FA or the Sub-Consultants knew or should have known of any such errors or omissions, or was responsible for or participated in its inclusion in or omission from this PIM; (ii) the

recipient will not copy, reproduce or distribute to any third party this PIM, in whole or in part, other than with the prior written consent of the PC & the FA; and (iii) any proposed actions by the recipient which are inconsistent in

any manner with the foregoing will require the prior written consent of the PC & the FA.

PC & FA reserve the right not to pursue the matters discussed herein and to terminate, at any time, further participation in the transaction and proposal process by any investor, and to modify data, documentation and other

procedures without assigning any reason thereto.

This PIM is not, and under no circumstances is to be construed as, a prospectus, offering memorandum, a public offering of the Bank or the business, as defined under applicable securities legislation and does not constitute or form

any part of any offer to sell or recommendation to subscribe for, underwrite or purchase securities, nor shall it, or any part of it, be relied upon in any way in connection with any contract for the acquisition of an equity interest in

the Bank. Any sale of securities will be made pursuant to a share purchase agreement and/or shareholder’s agreement or similar agreement(s) as described herein. The information contained in this PIM may be subject to updating,

expansion, revision and amendment. However, neither the Bank nor the FA undertake any obligation to update, expand, revise or amend any information or to correct any inaccuracies contained in this PIM or to provide the

recipients with additional information.

Each recipient agrees not to contact any owners, officers, directors, employees, representatives, agents, customers, suppliers or any other affiliates of the Bank. All such interested persons should contact only PC & FA if they have

any questions. Only pre-qualified investors, subject to PC’s and Regulator’s approval, will be allowed to conduct a more detailed review of the Bank’s business and to perform other due diligence procedures required to formulate a

transaction.

All inquiries regarding the Bank and any requests for additional information should be directed to Key Contacts of PC & FA.

SME Bank Limited Disclaimer

| 2

Transaction OverviewA

Pakistan’s EconomyB

Pakistan’s Banking SectorC

SME Bank LimitedD

Indicative Transaction TimelineE

Key ContactsF

SME Bank Limited Table of Contents

| 3

Transaction OverviewA

| 4

The Government of Pakistan (“GOP”) is in the process of divesting GOP’s equity stake

in SME Bank Limited (the “Bank”) along with management control to a strategic

investor (the “Transaction”)

In this regard, Privatisation Commission (“PC”) on behalf of the GOP, invites

Expressions of Interest (“EOI”) from investors interested in acquiring up to 93.88% in

the share capital of the Bank

THE TRANSACTION

THE ADVISORY TEAM

The Bank is a public limited company incorporated in Pakistan on October 30, 2001

under the Companies Ordinance, 1984. It is engaged in the business of banking

focusing specifically on the objective of supporting and developing small and medium

enterprise sector in Pakistan through required financial assistance and business

support services on sustainable basis

The registered office of the Bank is situated at 56-F, Nazim-ud-Din Road, F-6/1, Blue

Area, Islamabad

The Bank is operating through a network of 13 branches located across major cities of

Pakistan

The PC has appointed a Financial Advisory Consortium (“FAC”) comprising of Elixir

Securities Pakistan (Private) Limited and Bridge Factor (Private) Limited (Financial

Advisors), KPMG Taseer Hadi & Company (Accounting/Tax Advisor Sub-Consultant),

Mohsin Tayebaly & Company (Legal Sub-Consultant to conduct this Transaction

THE BANK

BANK’S PRESENCE ACROSS PAKISTAN

THE TRANSACTION KEY HIGHLIGHTS

The Bank is operating through a network of

branches in all major cities of Pakistan

Reduced Paid-up Capital Requirements

Opportunity for Branchless

Banking/Fintech

SBP to incentivize Sponsor through Credit/Guarantee

Schemes

Significant exposure to Commercial and

Retail Sector

Only Specialized SME Bank in Pakistan

Diversification into Leasing and Broking

Sectors

Transaction OverviewPrivatisation of SME Bank Limited

| 5

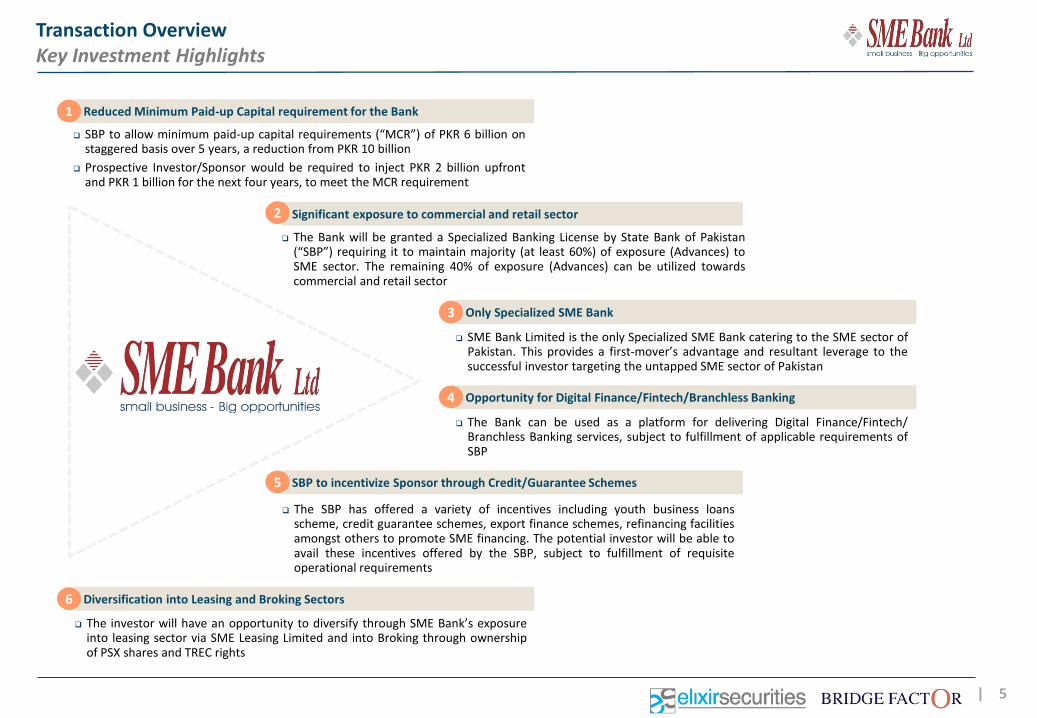

Reduced Minimum Paid-up Capital requirement for the Bank

SBP to allow minimum paid-up capital requirements (“MCR”) of PKR 6 billion onstaggered basis over 5 years, a reduction from PKR 10 billion

Prospective Investor/Sponsor would be required to inject PKR 2 billion upfrontand PKR 1 billion for the next four years, to meet the MCR requirement

1

Significant exposure to commercial and retail sector

The Bank will be granted a Specialized Banking License by State Bank of Pakistan(“SBP”) requiring it to maintain majority (at least 60%) of exposure (Advances) toSME sector. The remaining 40% of exposure (Advances) can be utilized towardscommercial and retail sector

2

Opportunity for Digital Finance/Fintech/Branchless Banking

The Bank can be used as a platform for delivering Digital Finance/Fintech/Branchless Banking services, subject to fulfillment of applicable requirements ofSBP

4

Only Specialized SME Bank

SME Bank Limited is the only Specialized SME Bank catering to the SME sector ofPakistan. This provides a first-mover’s advantage and resultant leverage to thesuccessful investor targeting the untapped SME sector of Pakistan

3

SBP to incentivize Sponsor through Credit/Guarantee Schemes

The SBP has offered a variety of incentives including youth business loansscheme, credit guarantee schemes, export finance schemes, refinancing facilitiesamongst others to promote SME financing. The potential investor will be able toavail these incentives offered by the SBP, subject to fulfillment of requisiteoperational requirements

5

Diversification into Leasing and Broking Sectors

The investor will have an opportunity to diversify through SME Bank’s exposureinto leasing sector via SME Leasing Limited and into Broking through ownershipof PSX shares and TREC rights

6

Transaction OverviewKey Investment Highlights

| 6

Pakistan’s EconomyB

| 7

Income Per Capita

Source: Bloomberg, IMF, Economic Survey, OICCI, Elixir Research

Pakistan’s economy continued to maintain growth momentum for the 4th year in a row with real GDP growing at 4.71% in FY2016 which is the highest in eight years, with projected GDP growth for FY 2017 at 5.7%

The economy will continue to witness strong growth, supported by higher infrastructural spending, lower commodity prices,improvement in law & order situation and strong domestic demand

China-Pakistan Economic Corridor will bring in USD 55 billion in foreign direct investment (“FDI”), nearly five times of FDIreceived during the past five years

The GDP of Pakistan, world’s sixth most populous country, where 35% of the population is below age 14, is expected todisplay strong growth over the next decade

Higher Business Confidence score published by Overseas Investors Chamber of Commerce and Industry (“OICCI”) validatesimprovement in overall sentiments towards economic outlook

Economic indicators validated positive trend; CPI continued to ease, interest rate flattened and law and order improved torecord level in eight years

Comments

Pakistan’s GDP is expected to display

resilient growth

Increased business confidence

domestically expected to be a key

factor

Foreign Inflows, including those from

CPEC will strengthen the economy

Controlled Inflation to augment

growth in the country

Increasing Purchasing Power to also

support GDP growth

Increase in GDP supports enhancement

in the consumer savings potential

resulting in potential growth in Deposits

Factors such as inflation, increase in

market capitalization, increase in

Public Private Partnerships etc. will

directly result in a nominal increase in

savings

Savings increase coupled with lower

inflation will drive growth for banking

sector within Pakistan

B3 B2 B1 B2 B3 Caa1 B3

Feb-02 Oct-03 Nov-06 May-08 Dec-08 Jul-12 Jun-15

ECONOMIC UPTURN IN THE OFFING RATING OUTLOOK (MOODY’S)

-40%

-20%

0%

20%

40%

60%

2010 2011 2012 2013 2014 2015

OICCI Members Overall

BUSINESS CONFIDENCE UPBEAT

INCREASED FOREIGN INVESTMENT INCREASING PURCHASING POWER HEALTHY INFLATION

USD (Bn) USD

-

500

1,000

1,500

2,000

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7F

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7F

0.0%

5.0%

10.0%

15.0%FY

10

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7F

-1.0%

4.0%

9.0%

14.0%

2010 2011 2012 2013 2014 2015 2016

GDP Growth (%) Inflation (%)

Pakistan’s EconomyPakistan Economic Overview

| 8

A major decline in the Fiscal Deficit hasbeen witnessed from 8.2% in 2013 to 4.6%in 2016. Declining fiscal deficit has provento be beneficial towards keeping inflationunder check

Increasing Investor Confidence

MSCI has added Pakistan Index to the confirmed list for reclassification to “Emerging Markets” as part of the 2016 ‘Annual Market Classification Review’. The Reclassification will coincide with the May 2017 Semi-Annual Index, which will be conducted for Pakistan alongside India, China, Thailand, Malaysia, Korea, Indonesia, Philippines and Taiwan – from Asia. The upgrade from Frontier to Emerging Markets is expected to bring in additional Foreign Investments

China-Pakistan Economic Corridor

CPEC is an economic initiative under China’s ‘One Belt, One Road’ to connect Gwadar and Xinjiang via a network of highways, railways combined with investment in energy and infrastructure with an estimated investment outlay of ~USD55bn, divided between energy (~USD36bn) and infrastructure and other projects (~USD19bn)

Winning the War on Terror

There is broad and deep consensus across society against militancy and extremism. This is personified by the ongoing successful military operation against extremist groups. Since the military offensive in 2013, more than 6,500 terrorists have been killed while there has been a significant decline in civilian casualties

Political Stability

The country is now a vibrant democracy. There are four power centers, all providing a check on each other. The government, the military, a free press and an independent judiciary. From an unstable political background, the country has witnessed a successful democratic transition providing political stability and increasing investor confidence

A

B

C

D

MAJOR SHIFTS IN ECONOMIC PARADIGM

Current Account Deficit has not seensignificant rise despite sluggish exports andrise in import of capital goods

CDS Spreads of Pakistan have beenwitnessing a declining trend since June 2012highlighting declining country risk andincrease in investor confidence

GDP growth of 4.7% in FY 2016 is the highestlevel of growth achieved by Pakistan since FY2008. Services sector has been the highestcontributor since last two years

STRONG MACROECONOMIC METRICS

0

200

400

600

800

1000

Dec

-11

Ap

r-1

2

Au

g-1

2

Dec

-12

Ap

r-1

3

Au

g-1

3

Dec

-13

Ap

r-1

4

Au

g-1

4

Dec

-14

Ap

r-1

5

Au

g-1

5

Dec

-15

Ap

r-1

6

Au

g-1

6

Bps CDS Spreads

5.8% 5.5%

5.0%

0.4%2.6% 3.6%

3.8%3.7%

4.1%

4.0%

4.7%

-5.0%

-3.0%

-1.0%

1.0%

3.0%

5.0%

7.0%

9.0%

11.0%

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Agri Manufacturing Services GDP Growth

GDP Growth

4.0% 4.1%

7.3%

5.2%

6.2%6.5%

6.8%

8.2%

5.5% 5.3%

4.6%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

Fiscal Deficit (As % of GDP)

Source: Bloomberg, IMF, Economic Survey, OICCI, Elixir Research

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

(1,000)

-

1,000

2,000

3,000

4,000

5,000

FY2011 FY2012 FY2013 FY2014 FY2015 FY2016

Current Account Deficit (LHS) % of GDP (RHS)USD (Mn)

Current Account Deficit

Pakistan’s EconomyPakistan Economic Overview

| 9

Pakistan’s Banking SectorC

| 10Source: Bloomberg, Economic Survey, SBP, Elixir Research

Pakistan Banking Sector comprises of 36 institutions including Local Private Banks, Public Sector Banks, Foreign Banks and

Specialized Banks

Local private banks remain the key division which dominates the industry with share of 79.3% and 78.4% in assets and

profitability, respectively

Pakistan's Banking sector witnessed phenomenal resilience over the last 5 years, despite recently observed monetary easing

During 9M2016, the profitability of the sector contracted by 6% YoY to PKR 138.9 billion whereas the asset base

expanded by 12.0% YoY to PKR 15,134 billion (USD 144.1 billion) in September 2016

Private sector advances registered a growth of 12.8% YoY, reaching PKR 3,656 billion (USD 34.8 billion) as of December

2016 primarily due to 12.1% YoY increase in credit to manufacturing sector

Considering the stellar performance and strong financials of the sector, Moody’s upgraded Pakistan’s Banking Sector’s

outlook from negative to stable in November 2015. Fitch Ratings has also rated Pakistan a stable ‘B’ in February 2017

Advances to SME sector of Pakistan grew by 22.5% in September 2016 compared with the same period last year. These

advances account for a mere 6.0% of industry advances, highlighting significant potential for growth

Comments

Deposit Growth to Remain Healthy

Banking sector deposits haveposted robust growth over the pastfive years on account of sizablemonetary expansion mainly due toexpansion in net domestic assets

Going forward, industry depositsmay demonstrate an upwardmomentum owing to expectedincrease in credit off-takes andhigher net foreign assets

Improved Profitability

Superior ROE profile support stronggrowth in Banking sector, as banksremain keen to focus on growinglow cost current accounts andcapture CPEC related investments

Asset Mix Trend to Reverse

Due to structural bottlenecks, theindustry assets are mainlydominated by investments

Going forward, the trend mayreverse considering accommodativemonetary policy coupled with GoPcommitment towards reformprocess

CONSISTENTLY IMPROVING PROFITS* UPWARD MOVEMENT IN ROES/ROAS DECLINING NPL RATIO AND RISING COVERAGE

UPWARD TREND IN ASSETS GROWING INDUSTRY DEPOSITS AND NETWORK INVESTMENTS GROWTH OUTPACING ADVANCES

- 2,000 4,000 6,000 8,000 10,000 12,000 14,000

-

2,000

4,000

6,000

8,000

10,000

12,000

CY0

2

CY0

3

CY0

4

CY0

5

CY0

6

CY0

7

CY0

8

CY0

9

CY1

0

CY1

1

CY1

2

CY1

3

CY1

4

CY1

5

Deposits (LHS) Branches (RHS)PKR (Bn)

-

4,000

8,000

12,000

16,000

CY0

6

CY0

7

CY0

8

CY0

9

CY1

0

CY1

1

CY1

2

CY1

3

CY1

4

CY1

5

Sep

-16

PKR Bn

-

2,000

4,000

6,000

8,000

CY0

6

CY0

7

CY0

8

CY0

9

CY1

0

CY1

1

CY1

2

CY1

3

CY1

4

CY1

5

Sep

-16

Net Investments Net AdvancesPKR Bn

-

50

100

150

200

250

CY0

6

CY0

7

CY0

8

CY0

9

CY1

0

CY1

1

CY1

2

CY1

3

CY1

4

CY1

5

Sep

-16

PKR Bn

*Annualized for Sep-2016

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

CY0

6

CY0

7

CY0

8

CY0

9

CY1

0

CY1

1

CY1

2

CY1

3

CY1

4

CY1

5

Sep

-16

ROA (RHS) ROE (LHS)

0.0%

5.0%

10.0%

15.0%

20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%C

Y06

CY0

7

CY0

8

CY0

9

CY1

0

CY1

1

CY1

2

CY1

3

CY1

4

CY1

5

Sep

-16

NPL Ratio (RHS) Coverage Ratio (LHS)

Pakistan’s Banking SectorIndustry Outline & Performance

| 11

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

CY0

6

CY0

7

CY0

8

CY0

9

CY1

0

CY1

1

CY1

2

CY1

3

CY1

4

CY1

5

CY1

6E

Consumer Financing – Auto and Mortgage financing to be the maindrivers After touching a low of PKR 282 billion in April 2012, consumer credit has

started to pick up in recent years as multi-year low inflation, risingdisposable income and low interest rates has spurred consumer demand

Relatively lower private credit penetration compared to other developingcountries indicates that consumer loans still have much room to growwhere auto financing and mortgage financing are yet to gain traction withdomestic auto sales booming and pick up in real estate activity

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

CY0

6

CY0

7

CY0

8

CY0

9

CY1

0

CY1

1

CY1

2

CY1

3

CY1

4

CY1

5

CY1

6E

Credit growth to steadily pick up pace in medium term Unprecedented monetary easing during last couple of years took place

when the SBP reduced discount rate to multi decade low of 6.25%

Credit growth has been less than exceptional as continued borrowing from

GoP has crowded out credit available to the private sector

DECLINING CONSUMER LOANS TO GDP

PRIVATE CREDIT TO GDP RATIO

DEPOSIT GROWTH

Corporate loans: Revival in progress Pakistan’s Banking Sector is poised to achieve similar traction in the

backdrop of revival in business activity supported by shrinking of energydeficit, improving law and order situation, multi-year low interest rates andinfrastructure financing for projects under CPEC

Private Sector business loans made up 67% of Non-Government Loans inSeptember 2016 with majority of the chunk allocated to Manufacturing(56%), Textiles (18%) and Power (10%). The share of power sector isexpected to increase with massive investments in the sector lined up in next3-5 years

PKR Bn

Deposit growth to remain in limelight Deposit growth is expected to remain robust in the backdrop of gradual

economic recovery with the forecasted GDP growth of 5.7% in 2017 Banks with large branch networks will remain ahead of the curve with

regard to deposit mobilization and deployment -

5,000

10,000

15,000

CY0

6

CY0

7

CY0

8

CY0

9

CY1

0

CY1

1

CY1

2

CY1

3

CY1

4

CY1

5

CY1

6E

CY1

7F

CY1

8F

Source: SBP, Elixir Research

Pakistan’s Banking SectorIndustry Outline & Performance

| 12

0%

20%

40%

60%

80%

100%

120%

AB

L

AK

BL

BA

FL

BA

HL

FAB

L

HB

L

HM

B

MC

B

MEB

L

SCB

PL

UB

L

NPL Ratio Coverage

IMPROVING CAPITAL ADEQUACY RATIOS

DECLINING NPL RATIO & RISING COVERAGE

BANK WISE INFECTION RATIO (2015)

Investment Income from PIBs Pakistan banks had extensively participated in Long term Government paper

in 2014 which were offered at a premium of 2-3 percent points over KIBOR Significantly higher premium was largely due to GoP’s effort to re-profile its

debt profile from short term to longer term maturity However, sizable high yielding PIB maturity of PKR 1.3 trillion in July 2016

will keep pressure on NIMs

Adequately Capitalized Governed under Basel III regulations, Pakistan Banks are required to hold

minimum capital of 10% of their risk weighted assets with the requirementexpected to gradually increase to 12.5% by 2019

Capital Adequacy ratio (“CAR”) as set by SBP for the banking sector isgenerally used to gauge the overall financial health of the sector

Banking sector in Pakistan is adequately capitalized with a CAR of 16.8%

Asset quality to remain impressive Asset quality of the banking industry has shown marked improvement over

the years where NPL ratio lowered to 11.3% in September 2016 from thepeak of 15.7% in 2011 on the back of stringent risk management practicescoupled with subdued credit demand from the private and consumer sector

Asset quality, particularly of top tier banks, will remain strong owing to strictrisk management framework along with cautious lending approach

Fee-based income to support attrition in core earnings Where multi decade low interest rates will likely restrict banking sector’s

Net Interest Margin (“NIM”) growth, rising fee income is expected to lendsupport to sector’s profitability

Sustained growth in fee income is expected to emanate from; 1) furtherpenetration of consumer banking products like credit cards in a largelyunbanked population, 2) growing bancassurance activities, 3) mutual funddistribution, 4) rapid expansion in branchless banking and Fintech, 5)growing trade and remittances

0.0%

5.0%

10.0%

15.0%

20.0%

CY0

6

CY0

7

CY0

8

CY0

9

CY1

0

CY1

1

CY1

2

CY1

3

CY1

4

CY1

5

Sep

-16

Capital Adequacy Ratio Capital to Total Assets

0.0%

5.0%

10.0%

15.0%

20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

CY0

6

CY0

7

CY0

8

CY0

9

CY1

0

CY1

1

CY1

2

CY1

3

CY1

4

CY1

5

Sep

-16

Coverage Ratio (LHS) NPL Ratio (RHS)

Source: SBP, Elixir Research

Pakistan’s Banking SectorIndustry Outline & Performance

| 13

66%

23%

11%

Working Capital Financing Fixed Investment Trade Finance

SME sector of Pakistan has continued to show positive trajectory with SME financing standing at PKR 298

billion as of June 2016, up ~14% when compared with the same period last year

12,238 additional borrowers have availed SME loans during FY2016, growing by ~8% over last year

A major share of the SME financing is facilitated by private banks, accounting for ~67% of the total

outstanding SME financing, followed by public sector banks, financing ~27% of the amount during FY2016

There is immense growth potential for the SME sector considering that SME financing accounts for a mere

7.3% of total private sector financing as of June 2016

Quality of SME loans has also witnessed considerable progress YoY with NPLs as % of total SME loans showed

considerable improvement

SME sector presents great opportunity for investors offering relatively higher yields on loans, which becomes

an added attraction due to declining SME NPLs to Outstanding SME financing

The SBP has been actively introducing incentives to promote the growth of the sector through programs such

as Credit Guarantee Schemes for small and rural enterprises, whereby 40% of the credit losses on the short

term loans are shared

In addition to this, SBP has designed National Financial Inclusion Strategy whereby it plans to extend SME

credit to 300,000 SMEs and increase the proportion of SMEs financing to private sector loans from ~7% to

15% by 2020

Source: SBP’s Quarterly SME Finance Review

BREAKUP OF SME FINANCING (JUNE 2016)

SME Sector Profile (PKR billion)June2015

June2016

Outstanding SME Financing 260.8 297.5

Total Private Sector Financing 3,561.0 4,055.5

NPLs as % of SME Financing 31.36% 27.37%

No. of SME Borrowers 152,495 164,733

Ratio of SME Financing to GDP 0.88% 1.00%

PERFORMANCE OF SPECIALIZED BANKSTRENDS IN SME FINANCING

Pakistan’s Banking SectorSME Sector – Outline & Performance

-

50

100

150

200

250

CY11 CY12 CY13 CY14 CY15 Sep-16

Assets Advances Borrowings Deposits

PKR Bn

| 14

SME Bank LimitedD

| 15

2,647 3,328 3,713 3,343

4,770 4,815

0

2,000

4,000

6,000

2011 2012 2013 2014 2015 Sep-16

SME Bank Limited was formed pursuant to the Regional Development Finance

Corporation (RDFC) and Small Business Finance Corporation (SBFC)

(Amalgamation and Conversion) Ordinance 2001, whereby net assets of RDFC

and SBFC were vested with the Bank

SME Bank started its operations on April 16, 2005

It has been operating with a paid up capital of PKR 2.39 billion since 2007 on the

back of SBP’s exemption to meet the minimum paid-up capital requirement of

PKR 10 billion

Due to low equity base, the Bank has been making losses resulting in erosion of

net assets from PKR 1 billion in 2013 to PKR 68 million by September 2016

Deposit base implied an average growth rate of around 13% during the period

2011 to September 2016

Investments account for 51%, whereas Advances contribute 32% of the total

assets of the Bank as of September 2016

The Bank was rated ‘B’ for long-term and short-term credits by PACRA in April

2016

SHAREHOLDING

KEY FINANCIAL HIGHLIGHTS

PKR (million) 2011 2012 2013 2014 2015 9M2016*

Net Equity 1,866 1,345 1,004 689 356 68

Deposits 2,647 3,328 3,713 3,343 4,770 4,815

Total Liabilities 5,331 7,623 6,020 4,611 8,260 7,634

Net Advances 2,719 2,855 2,852 2,929 2,752 2,467

Investment 3,929 4,663 2,653 1,447 4,118 3,925

Total Assets 7,198 8,968 7,024 5,300 8,617 7,702

Interest Income 694 790 715 789 705 459

Total Income 715 809 741 876 753 475

INTRODUCTION

DEPOSIT GROWTH

EMPLOYEES

SME Bank has a total employee strength of approximately 377 permanent and

contractual individuals

Source: Company AccountsNBL = National Bank of Pakistan; UBL = United Bank Limited; HBL = Habib Bank Limited; MCB = MCB Bank Limited; ABL = Allied Bank Limited; IDBL = Industrial Development Bank Limited

Shares (Mn) Shareholding

Government of Pakistan 224.62 93.88%

NBP, UBL, HBL, MCB, ABL, IDBL 14.63 6.12%

Total 239.25 100.00%

BRANCH NETWORK

SME Bank has a branch network of 13 branches across major cities of Pakistan.

The Bank had been unable to expand its network due to non-compliance with the

statutory MCR requirement

*Unaudited

SME Bank LimitedOverview

| 16

-

2,000

4,000

6,000

8,000

10,000

2011 2012 2013 2014 2015 Sep-16

Assets Liabilities Equity

PKR (Mn)

0%

10%

20%

30%

40%

50%

-

200

400

600

800

1,000

2011 2012 2013 2014 2015 Sep-16

Interest Income (LHS) Non-Interest Income (LHS)

Net Interest Spreads (RHS)

PKR (Mn)

51%

32%

17%

Investments Advances Other Assets

CURRENT ASSET COMPOSITION (SEPTEMBER 2016)

97%

3%

Interest Income Non Interest Income

EXISTING INCOME COMPOSITION (SEPTEMBER 2016)

TREND OF INCOME VS. SPREADS BALANCE SHEET COMPOSITION

SME Bank LimitedFinancials at a Glance

| 17

SME Leasing Limited is a subsidiary of SME Bank Limited, which holds 73.14% of

the shareholding of SME Leasing Limited

It was incorporated in Pakistan on July 12, 2002 as an unlisted public company

and acquired the status of a listed company on December 13, 2006

The core objective of the company is to extend lease and working capital

financing facilities to small and medium enterprises of the country

SME Leasing Limited has been assigned ‘B+’ for long-term and ‘B’ for short-term

rating by PACRA in January 2017

The net assets of SME Leasing amounted to PKR 167 million, as of September

2016

SME Leasing Limited posted losses of PKR 4.1 million during 9M2016 compared

with a loss of PKR 8.0 million during the same period last year. The reduction in

losses was mainly due to taxation

The decline in earnings is majorly attributed to decrease in earning assets and a

larger cost base

OVERVIEW

KEY FINANCIAL HIGHLIGHTS

PKR (million) 2011 2012 2013 2014 2015 9M2016

Total Equity 237 208 200 190 174 167

Gross Lease Receivable 914 718 697 777 676 NA

Net Investment in Lease 663 482 460 519 443 NA

Total Assets 789 587 542 658 568 534

Lease Income 53 45 26 46 28 26

Total Revenue 60 46 28 46 28 30

Total Expenses 127 75 36 57 49 37

(Loss) After Taxation (63) (29) (8) (11) (17) (4)

SHAREHOLDING STRUCTURE

73%

11%

10%

6%

Associated Companies (SME Bank)

Banks, NBFCs, DFIs

Individuals

Others

LEASE INCOME VS. ADMIN EXPENSES

KEY INDICATORS

PKR (million) 2011 2012 2013 2014 2015

Book Value per share (PKR) 7.42 6.51 6.26 5.95 5.45

Current Ratio (x) 1.28 1.50 1.51 1.08 1.34

Loss Per Share (PKR) -1.95 -0.91 -0.24 -0.35 -0.54

Income Expense Ratio (times) 0.49 0.60 0.73 0.81 0.57

Net Profit Margin (%) (104.71) (63.47) (27.18) (23.90) (62.07)

Return on Equity (%) (23.11) (13.05) (3.78) (5.55) (9.06)

Revenue Per Share (PKR) 1.87 1.43 0.89 1.44 0.87

BVPS, EPS, RPS* - ANNUAL

-5

0

5

10

2011 2012 2013 2014 2015

BVPS EPS RPS

PKR

Source: Company Accounts*BVPS: Book Value per share; EPS: Earnings per share; RPS: Revenue per share

-

20

40

60

2011 2012 2013 2014 2015 Sep-16

Lease Income Adminstrative ExpensesPKR (Mn)

SME Bank LimitedSME Leasing Limited

| 18

Indicative Transaction TimelineE

| 19

Timeline February March April May

Weeks 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Issuance of EOIs & RSOQs

Roadshows

Receipt and Evaluation of SOQs

Announcement of Prequalified Bidders and Issuance of Bidding Documents

Commencement of Bidders Due Diligence

Submission of comments on Bidding Documents from Prequalified Bidders

Completion of Bidders Due Diligence

Pre-Bid Meeting

Issuance of Final Bidding Documents and Announcement of Bidding Date

Valuation and Approval of Reference Price

Bidding / Approval & Announcement of Successful Bidder / Issuance of LOA

Execution of SPA / Payment of Purchase Price/ Transfer of Shares and Financial Close

Du

e D

ilige

nce

Pro

cess

Indicative Transaction Timeline16-weeks Process

| 20

Key ContactsF

| 21

Mukhtar Paras Shah Muhammad Moazzam Ali Ahmad Khan

Director GeneralPrivatisation Commission

T: +92 51 920 [email protected]

Head – Corporate FinanceElixir Securities Pakistan Private Limited

T: +92 21 111 354 947M: +92 334 999 8889

DirectorBridge Factor Private Limited

T: +92 51 285 1112M: +92 333 234 0000

Muhammad Zayed Maud Ghazil Jabbar Harris Chohan

Transaction ManagerPrivatisation Commission

T: +92 51 920 8505 (ext: 244)[email protected]

Deputy Head – Corporate FinanceElixir Securities Pakistan Private Limited

T: +92 21 3568 0757 M: +92 301 822 5534 [email protected]

ManagerBridge Factor Private Limited

T: +92 51 285 1112M: +92 300 989 2232

Key Contacts:

Privatisation of SME Bank Limited