Slide 6-1. Slide 6-2 Chapter 6 Inventories Financial Accounting, Seventh Edition.

date post

19-Dec-2015Category

view

252download

7

Slide 12-1

Slide 12-2

Accounting for Foreign Currency Accounting for Foreign Currency Transactions and Hedging Foreign Transactions and Hedging Foreign Exchange RiskExchange Risk

Advanced Accounting, Fourth Edition

12121212

Slide 12-3

Many U.S. companies engage in international

activities such as:

Exporting or importing goods,

Establishing a foreign branch, or

Holding an equity investment in a foreign

company.

Foreign Currency TransactionsForeign Currency TransactionsForeign Currency TransactionsForeign Currency Transactions

Slide 12-4

Foreign Currency TransactionsForeign Currency TransactionsForeign Currency TransactionsForeign Currency Transactions

Recording and reporting problems with foreign currency transactions:

Transactions in a foreign currency must be translated before they can be aggregated with domestic transactions.

Receivables or payables denominated in foreign currencies are subject to gains and losses.

Companies use hedging strategies with derivatives to minimize the impact of exchange rate changes.

Slide 12-5

Exchange Rates—Means of TranslationExchange Rates—Means of TranslationExchange Rates—Means of TranslationExchange Rates—Means of Translation

Translation - process of expressing amounts stated in a foreign currency in the currency of the reporting entity by using an appropriate exchange rate.

Exchange rate - ratio between a unit of one currency and another currency for which that unit can be exchanged at a particular time.

Slide 12-6

Direct Exchange Rate

Units of domestic currency that can be converted Units of domestic currency that can be converted into into one unit of foreign currencyone unit of foreign currency..

Direct rate =Direct rate = 1.517 ($1.517 U.S. for 1 British 1.517 ($1.517 U.S. for 1 British pound)pound)

Indirect Exchange Rate

Units of foreign currency that can be converted Units of foreign currency that can be converted into into one unit of domestic currencyone unit of domestic currency..

Indirect rate = 1.00/1.517 = .6592 Indirect rate = 1.00/1.517 = .6592 ($1 U.S. for .6592 British pound)($1 U.S. for .6592 British pound)

Exchange Rates—Means of TranslationExchange Rates—Means of TranslationExchange Rates—Means of TranslationExchange Rates—Means of Translation

Slide 12-7

Spot Rate

Rate at which currencies can be exchanged today.Rate at which currencies can be exchanged today.

Forward or Future Rate

Rate at which currencies can be exchanged at Rate at which currencies can be exchanged at some future date.some future date.

Forward Exchange Contract

Contract to exchange currencies of different Contract to exchange currencies of different countries on a stipulated future date, at a countries on a stipulated future date, at a specified rate (the forward rate). specified rate (the forward rate).

Exchange Rates—Means of TranslationExchange Rates—Means of TranslationExchange Rates—Means of TranslationExchange Rates—Means of Translation

Slide 12-8

Floating Rates

Relationship between major currencies is Relationship between major currencies is

determined by supply and demand factors.determined by supply and demand factors.

Increase risk to companies doing business with a Increase risk to companies doing business with a

foreign company.foreign company.

Exchange Rates—Means of TranslationExchange Rates—Means of TranslationExchange Rates—Means of TranslationExchange Rates—Means of Translation

Transaction Change SettlementDate in Rate Date

Yen 100,000 100,000 Direct rate 0.00434$ 0.00625$ Payable 434.00$ 625.00$

Example – Payable to be settled in 100,000 yen

Slide 12-9

Transactions are normally measured and recorded in terms of the currency where the company is located.

Reporting Currency - usually the currency where the company located.

Measured Versus DenominatedMeasured Versus DenominatedMeasured Versus DenominatedMeasured Versus Denominated

LO 1 Measured versus denominated.LO 1 Measured versus denominated.

Transaction between a U.S. firm and a foreign company:

Companies negotiate whether settlement is to be made in dollars or in the foreign currency.

If settled by foreign currency, U.S. firm measures the receivable or payable in dollars, but the transaction is denominated in the foreign currency.

Slide 12-10

Foreign Currency Transaction - requires payment or receipt (settlement) in a foreign currency.

U.S. firm exposed to risk of unfavorable changes in the exchange rate.

Foreign Currency TransactionsForeign Currency TransactionsForeign Currency TransactionsForeign Currency Transactions

LO 2 Foreign Currency Transactions.LO 2 Foreign Currency Transactions.

Direct exchange rate increasing, or foreign

currency unit strengthening.

More dollars needed to acquire the foreign

currency units.

Direct exchange rate decreasing, or foreign

currency unit weakening.

Fewer dollars needed to acquire the foreign

currency units.

=

=

Slide 12-11

Foreign Currency TransactionsForeign Currency TransactionsForeign Currency TransactionsForeign Currency Transactions

LO 3 Common transactions.LO 3 Common transactions.LO 4 Three stages of concern.LO 4 Three stages of concern.

Translating Accounts Denominated in Foreign Currency

Importing or Exporting of Goods or Services

Transaction date

Settlement date

Balance sheet date

Units of foreign currency x Current direct exchange rate

Increase or decrease is generally reported as a foreign currency transaction gain or loss, sometimes referred to as an

exchange gain or loss, in determining net income for the current period.

Slide 12-12

Importing and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting Transactions

LO 3 Common transactions.LO 3 Common transactions.LO 4 Three stages of concern.LO 4 Three stages of concern.

Exercise 12-2: During December of the current year, Teletex Systems, Inc., a company based in Seattle,Washington, entered into the following transactions:

Dec. 10 Sold seven office computers to a company located in Colombia for 8,541,000 pesos. On this date,

the spot rate was 365 pesos per U.S. dollar.

U.S. firm (Teletex)

Inventory delivered 12/10/2009

8,541,000 pesos received on 1/10/2010

Columbia firm

Slide 12-13

Importing and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting Transactions

LO 3 Common transactions.LO 3 Common transactions.LO 4 Three stages of concern.LO 4 Three stages of concern.

Exercise 12-2: Dec. 10, Sold seven office computers to a company located in Colombia for 8,541,000 pesos. On this date, the spot rate was 365 pesos per U.S. dollar. Prepare the journal entry on the books of Teletex Systems, Inc.

Accounts receivable 23,400

Sales23,400

Sales price in pesos 8,541,000

Pesos per U.S. dollar / 365Sales price in U.S. dollars $ 23,400

Slide 12-14

Importing and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting Transactions

LO 3 Common transactions. LO 4 Three stages of concern.LO 3 Common transactions. LO 4 Three stages of concern.

Exercise 12-2: Prepare journal entry necessary to adjust the accounts as of December 31. Assume that on December 31 the direct exchange rates was Colombia peso $.00268.

Transaction loss 510

Accounts receivable 510

Receivable in pesos 8,541,000

Direct exchange rate to U.S. dollar$ .00268Receivable in U.S. dollars $ 22,890Balance in receivable 23,400Transaction loss $ 510

Slide 12-15

Importing and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting Transactions

LO 3 Common transactions. LO 4 Three stages of concern.LO 3 Common transactions. LO 4 Three stages of concern.

Exercise 12-2: Prepare journal entry to record settlement of the account on January 10. Assume that the direct exchange rate on the settlement date was Colombia peso $.00320.

Cash (8,541,000 x $.00320) 27,331

Accounts receivable ($23,400 - $510) 22,890

Transaction gain 4,441

Slide 12-16

Importing and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting Transactions

LO 3 Common transactions.LO 3 Common transactions.LO 4 Three stages of concern.LO 4 Three stages of concern.

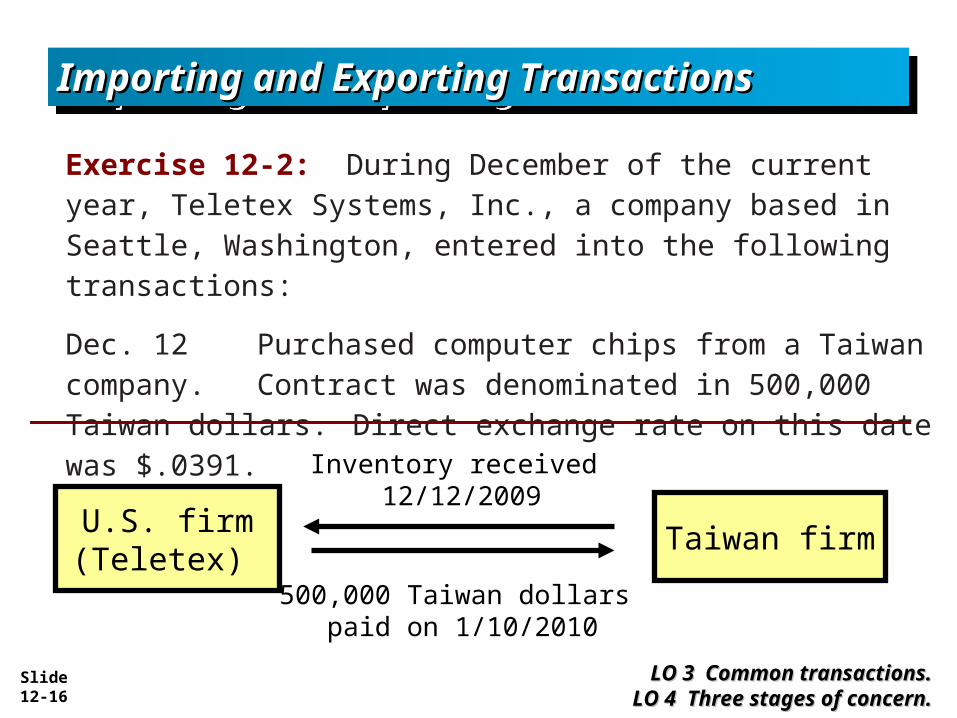

Exercise 12-2: During December of the current year, Teletex Systems, Inc., a company based in Seattle, Washington, entered into the following transactions:

Dec. 12 Purchased computer chips from a Taiwan company. Contract was denominated in 500,000 Taiwan dollars. Direct exchange rate on this date was $.0391.

U.S. firm (Teletex)

Inventory received 12/12/2009

500,000 Taiwan dollars paid on 1/10/2010

Taiwan firm

Slide 12-17

Importing and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting Transactions

LO 3 Common transactions.LO 3 Common transactions.LO 4 Three stages of concern.LO 4 Three stages of concern.

Exercise 12-2: Dec. 12, Purchased computer chips from a company domiciled in Taiwan. The contract was denominated in 500,000 Taiwan dollars. The direct exchange spot rate on this date was $.0391. Prepare the journal entry on the books of Teletex Systems, Inc.

Inventory 19,550

Accounts payable19,550

Purchase price in Taiwan dollars 500,000

Direct exchange rate to U.S. dollar x $.0391Purchase price in U.S. dollars $ 19,550

Slide 12-18

Importing and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting Transactions

LO 3 Common transactions. LO 4 Three stages of concern.LO 3 Common transactions. LO 4 Three stages of concern.

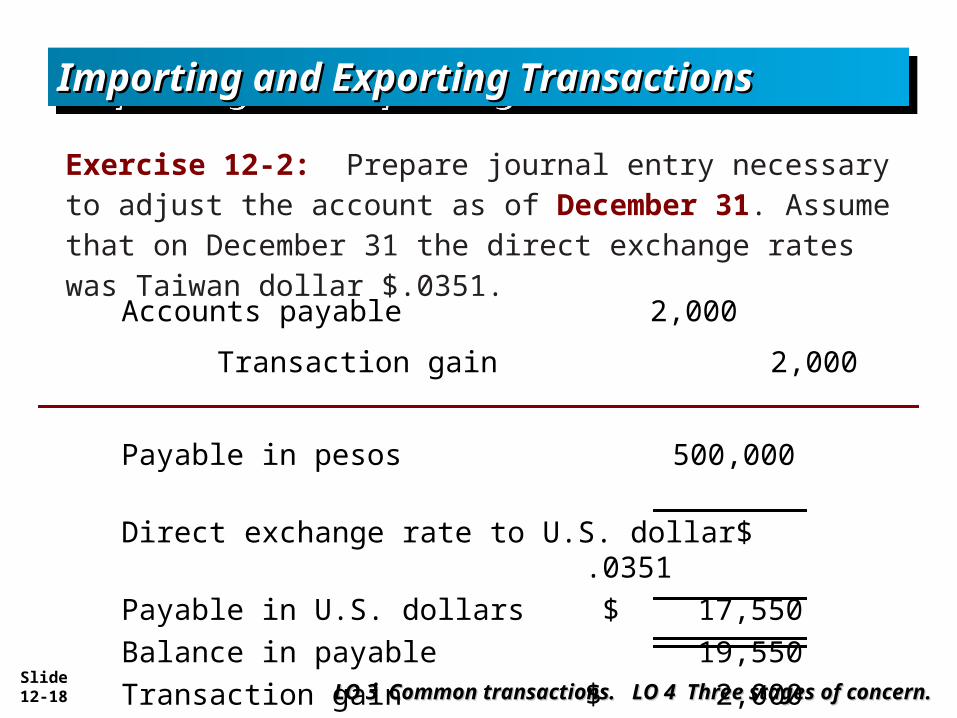

Exercise 12-2: Prepare journal entry necessary to adjust the account as of December 31. Assume that on December 31 the direct exchange rates was Taiwan dollar $.0351.

Accounts payable 2,000

Transaction gain 2,000

Payable in pesos 500,000

Direct exchange rate to U.S. dollar$ .0351Payable in U.S. dollars $ 17,550Balance in payable 19,550Transaction gain $ 2,000

Slide 12-19

Importing and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting Transactions

LO 3 Common transactions. LO 4 Three stages of concern.LO 3 Common transactions. LO 4 Three stages of concern.

Exercise 12-2: Prepare journal entry to record settlement of account on January 10. Assume that the direct exchange rate on the settlement date was Taiwan dollar $.0398.

Transaction loss 2,350

Accounts payable ($19,550 - $2,000)17,550

Cash (500,000 x $.0398) 19,900

Slide 12-20

Importing and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting TransactionsImporting and Exporting Transactions

LO 3 Common transactions. LO 4 Three stages of concern.LO 3 Common transactions. LO 4 Three stages of concern.

Foreign currency transaction gains and losses are included in net income.

Importing or Exporting of Goods or Services

Slide 12-21

Copyright © 2011 John Wiley & Sons, Inc. All rights

reserved. Reproduction or translation of this work beyond

that permitted in Section 117 of the 1976 United States

Copyright Act without the express written permission of

the copyright owner is unlawful. Request for further

information should be addressed to the Permissions

Department, John Wiley & Sons, Inc. The purchaser may

make back-up copies for his/her own use only and not for

distribution or resale. The Publisher assumes no

responsibility for errors, omissions, or damages, caused by

the use of these programs or from the use of the

information contained herein.

CopyrightCopyrightCopyrightCopyright