SKassegne - Effective Capex Management

28

Effective Capex Management Challenges & Success Factors Sultana Kassegne Sr. Finance Manager Cricket Wireless, San Diego, CA

-

Upload

sultana-kassegne-mba -

Category

Documents

-

view

96 -

download

4

Transcript of SKassegne - Effective Capex Management

Effective Capex ManagementChallenges & Success Factors

Sultana Kassegne

Sr. Finance Manager

Cricket Wireless, San Diego, CA

Capital Projects Turning into a

Financial Disaster?

• Cost Overruns

• Time Delays

Capital Planning

BudgetingCapex

ManagementResidual Capex

Capital Project Life Cycle

Laun

ch

Our Position

As financial managers, we are in a unique

position to promote fiscal responsibility and

making informed and educated decisions within

our organizations. As we continuously interact

with different functional and leadership team

members, we are able to identify best practices

and spread the word to others who can benefit

from it.

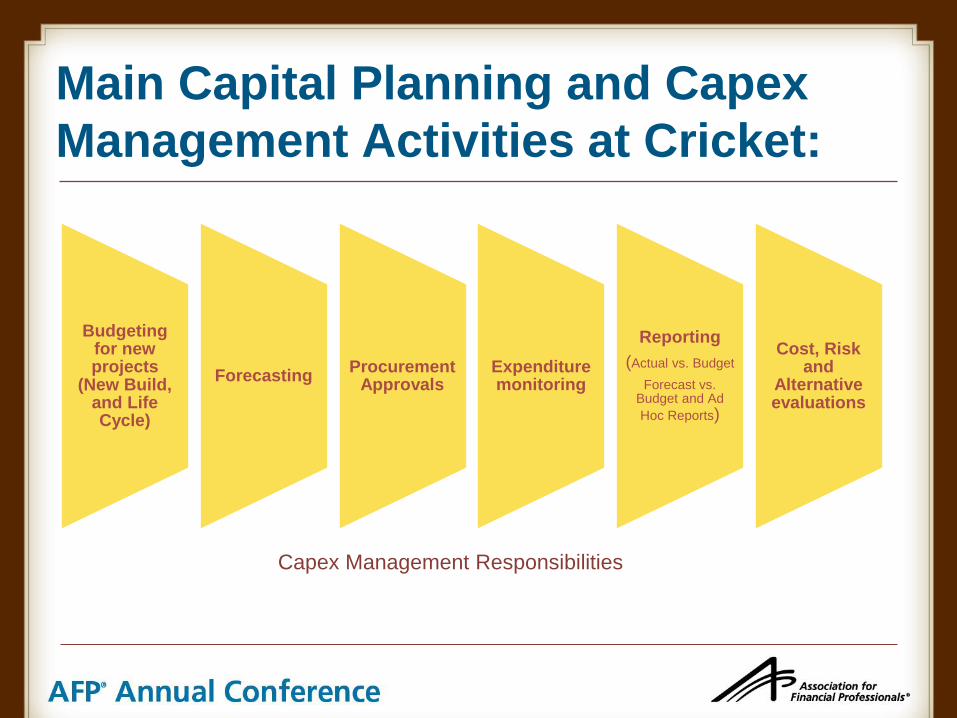

Main Capital Planning and Capex

Management Activities at Cricket:

Budgeting for new projects

(New Build, and Life Cycle)

ForecastingProcurement

ApprovalsExpenditure monitoring

Reporting

(Actual vs. Budget

Forecast vs. Budget and Ad

Hoc Reports)

Cost, Risk and

Alternative evaluations

Capex Management Responsibilities

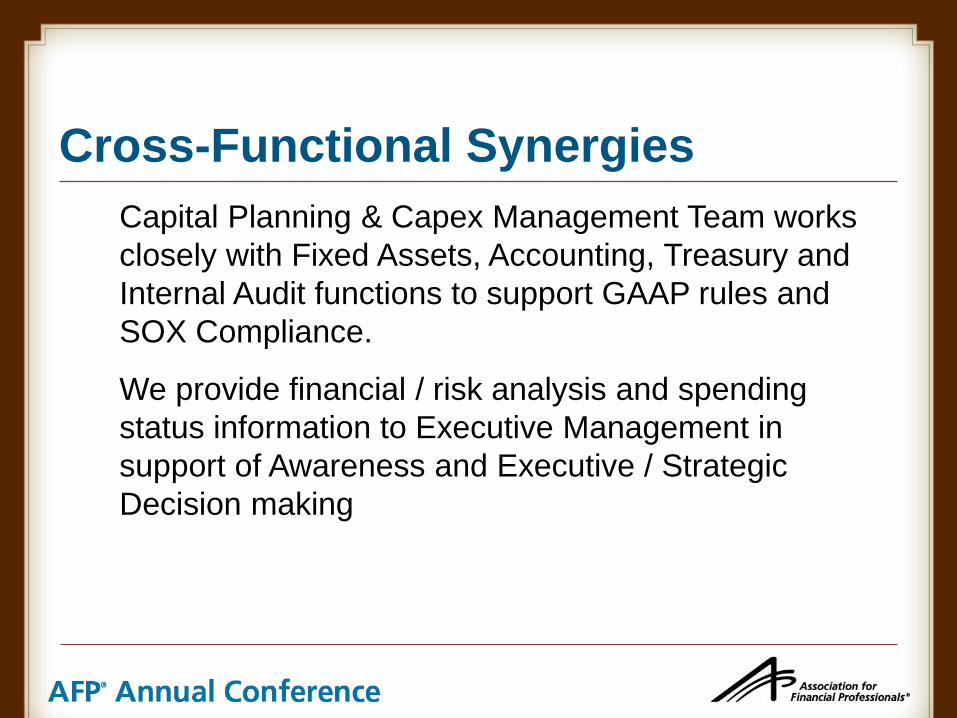

Cross-Functional Synergies

Capital Planning & Capex Management Team works

closely with Fixed Assets, Accounting, Treasury and

Internal Audit functions to support GAAP rules and

SOX Compliance.

We provide financial / risk analysis and spending

status information to Executive Management in

support of Awareness and Executive / Strategic

Decision making

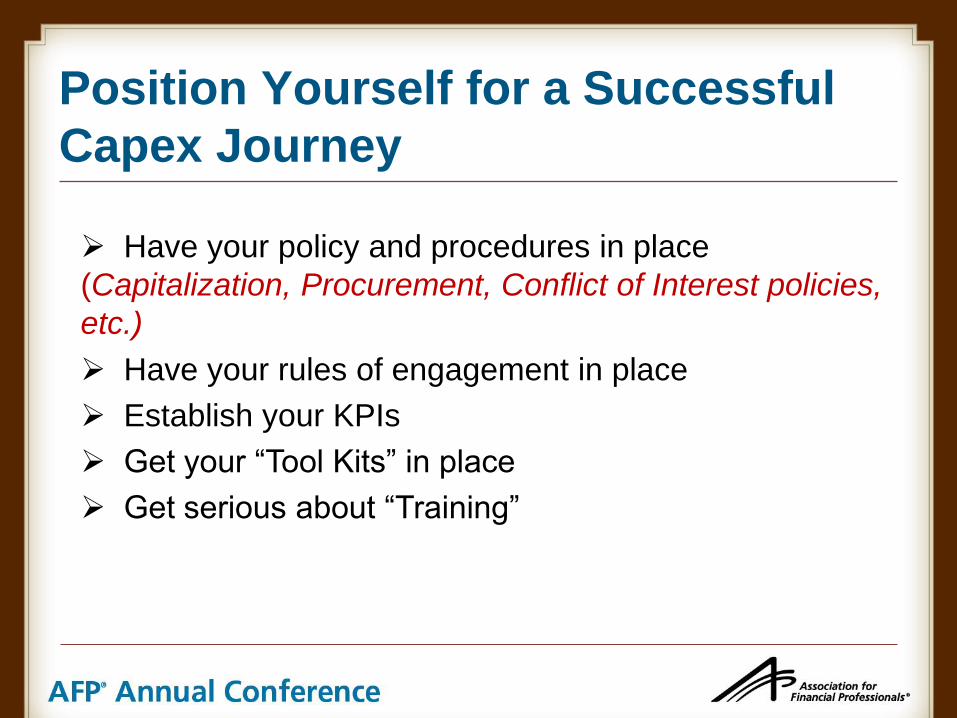

Position Yourself for a Successful

Capex Journey

Have your policy and procedures in place

(Capitalization, Procurement, Conflict of Interest policies,

etc.)

Have your rules of engagement in place

Establish your KPIs

Get your “Tool Kits” in place

Get serious about “Training”

REPORTING

&

FORECASTING

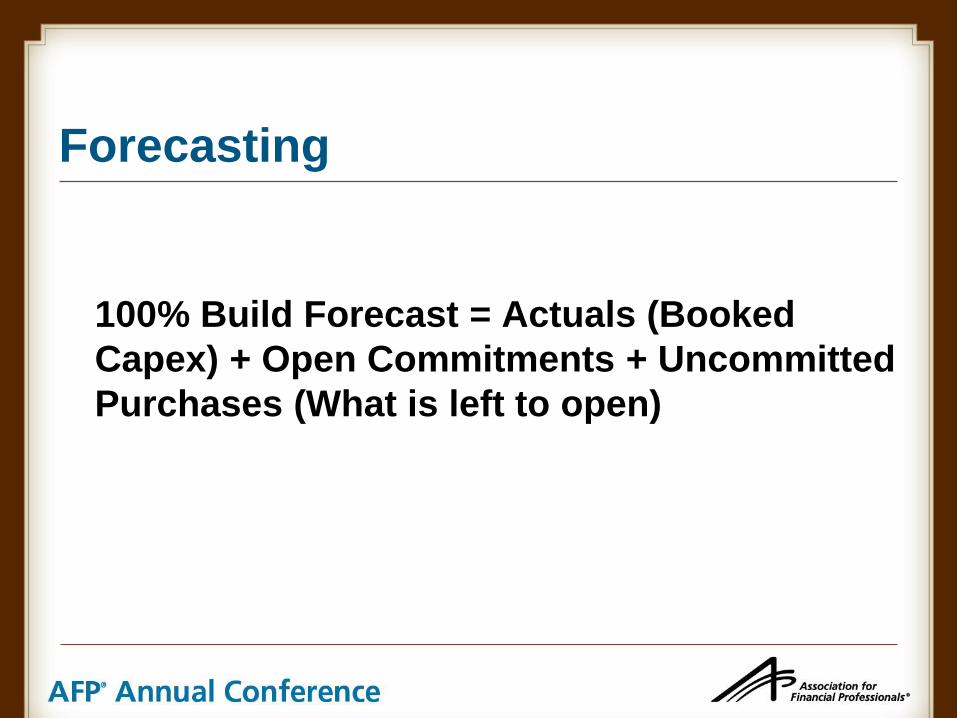

Forecasting

100% Build Forecast = Actuals (Booked

Capex) + Open Commitments + Uncommitted

Purchases (What is left to open)

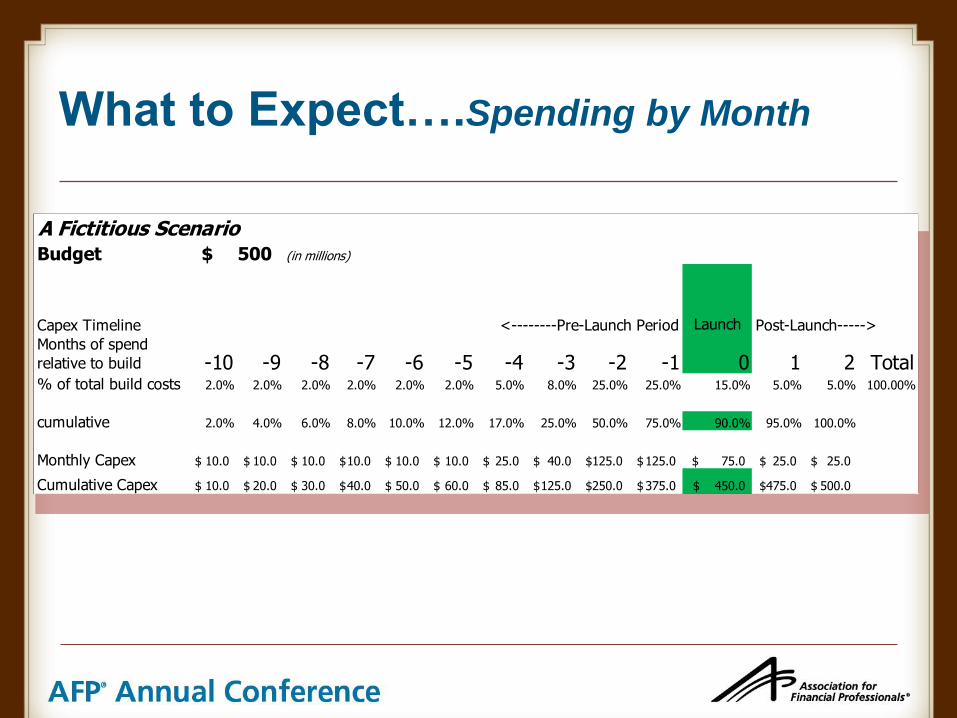

What to Expect….Spending by Month

A Fictitious ScenarioBudget (in millions)

Capex Timeline <--------Pre-Launch Period Launch Post-Launch----->

Months of spend

relative to build -10 -9 -8 -7 -6 -5 -4 -3 -2 -1 0 1 2 Total% of total build costs 2.0% 2.0% 2.0% 2.0% 2.0% 2.0% 5.0% 8.0% 25.0% 25.0% 15.0% 5.0% 5.0% 100.00%

cumulative 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 17.0% 25.0% 50.0% 75.0% 90.0% 95.0% 100.0%

Monthly Capex 10.0$ 10.0$ 10.0$ 10.0$ 10.0$ 10.0$ 25.0$ 40.0$ 125.0$ 125.0$ 75.0$ 25.0$ 25.0$

Cumulative Capex 10.0$ 20.0$ 30.0$ 40.0$ 50.0$ 60.0$ 85.0$ 125.0$ 250.0$ 375.0$ 450.0$ 475.0$ 500.0$

500$

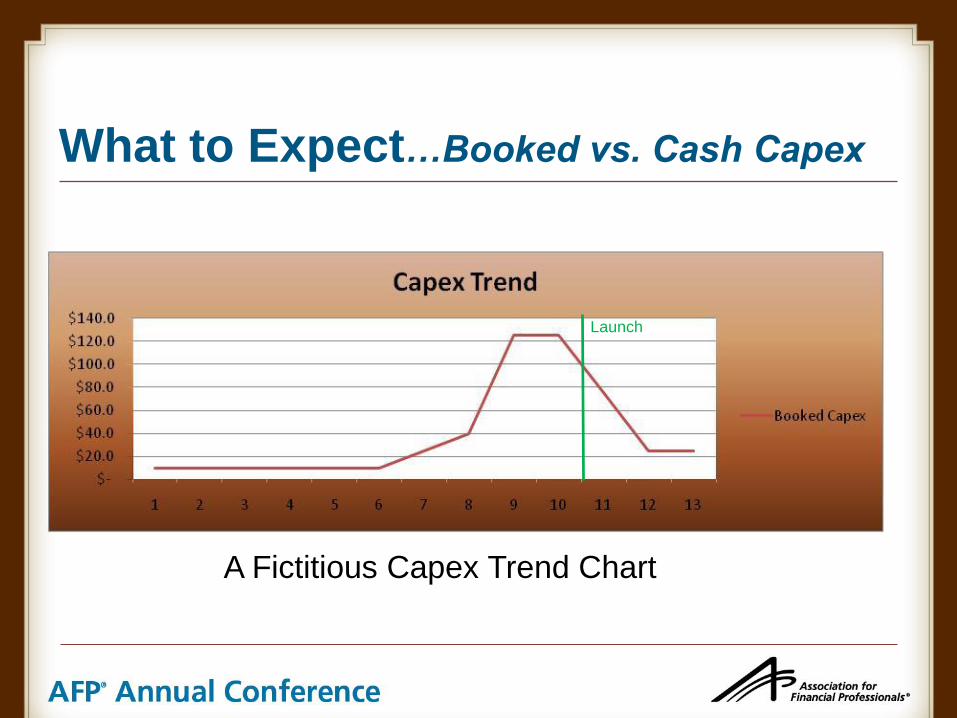

What to Expect…Booked vs. Cash Capex

A Fictitious Capex Trend Chart

Launch

Booked Capex vs. Cash Capex

Booked Capex : Deliveries of Goods and Services

Recognized

Cash Capex: Money out the door. Vendors paid.

Challenge: Reconciliation of Booked Capex and

Cash Capex within a certain period of time.

What Helps?

Streamlined vendor payment terms and forecasting

made easier.

Upgrades and Replacements

• Do an apple-to-apple comparison between the

current state and the future state (components,

functionality, etc)

• Any cost component that may not have been

included in the business case, if realized later,

can make the business case virtually

unprofitable

Reporting and Forecasting

Status of Capital Spending Relative to the Approved

Budget

100% Build Forecast = Actuals (Booked Capex) + Open Commitments

+ Uncommitted Purchases (What is left to open)

Periodic Reporting on Capital Spending

Inception to Date, Incremental Monthly, Quarterly

and Yearly Figures (Actuals and Forecast Figures for

upcoming months), Variance analysis between

budget & forecast, and current forecast to actuals.

Forecasting Process Tips

Make forecasting an ongoing/continuous activity for all Subject Matter Experts (SMEs) to reflect changes in the market/budget/spending in real time and to promote fiscal responsibility.

Avoid Email Jungle: Prevent SMEs getting dozens of emails with huge attachments from Budget Managers. Cut down on redundancy, bureaucracy while relieving network bandwidth and freeing up scarce IT resources.

Central, Secured Repository of Forecasts: House all forecasting information in a single, access-controlled and backed-up network location which is easy to access and manage, where SMEs can easily go and update their forecasts dynamically to reflect developments/changes taking place in their markets.

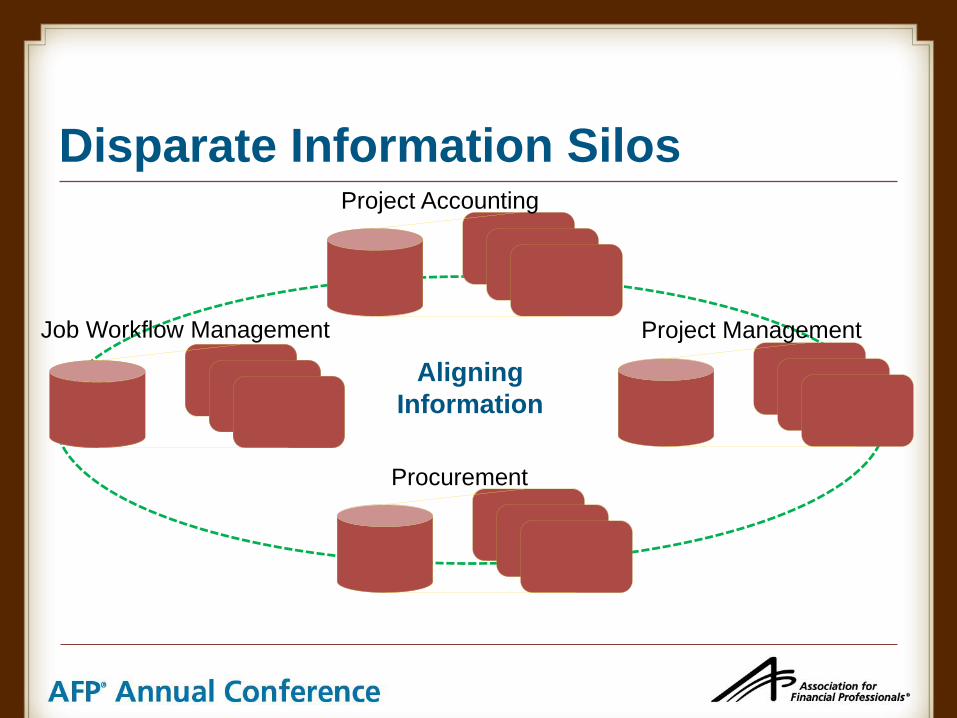

Task-Centric Forecasting

Capital Planning Team introduced a bottom-up

approach to forecast the A66 markets build

activities capital spending. This new approach

evolves around forecasting at build task level to

promote granular accuracy and fiscal awareness

and responsible spending amongst all Subject

Matter Experts (SMEs) that were part of the A66

build project.

Disparate Information Silos

Job Workflow Management

Project Accounting

Project Management

Procurement

Aligning

Information

Project Schedule and Capex

Schedule Alignment

– Realistic time-phasing of deliveries / booked capex

– Accurate allocation of costs by task

– Accurate assessment of “lead time” for procured

goods /services.

Security of Information

• Keep all of your forecast files in a central and

backed up and access-controlled electronic

library

• Avoid email attachments.

Things To Watch Out for Budgets• Scope Changes

– Monitor what is being build against what was in the original budget.

• Unbudgeted / Under-budgeted Items– Additional sites, stores, underestimated budget amount

• Project Schedule Changes– Unforeseen, beyond-control market realities such Spectrum

Clearing, municipal bottlenecks, force majeure, capital constraints

• Schedule and Cost Integration– Realistic time-phasing of deliveries, cost needs to align with

schedule

– Accurate allocation of costs by task - Stay alert on coding errors, catch them before requisitions turn into POs.

Always keep track of these and detail them in budget management kits. Bring to Management’s attention in a timely manner.

No surprises in the end!!!! No After the Fact Reporting!!!

INFLUENCING

PROCUREMENT

PROCESS

Total Cost of Ownership (TCO)

As Capex / Opex Managers, we are the Main

Ambassadors in our organizations to promote

awareness of TCO.

Shift focus in procuring

materials, services and

equipment from price to

total cost!

Components of Total Cost

• Acquisition Costs

• Ownerships Costs

• Post-Ownership Costs

Source:

World Class Supply ManagementSM , Burt, Dobler & Starling, ISBN 0-07-229070-6, Copyright © 2003 by The McGraw-Hill Companies

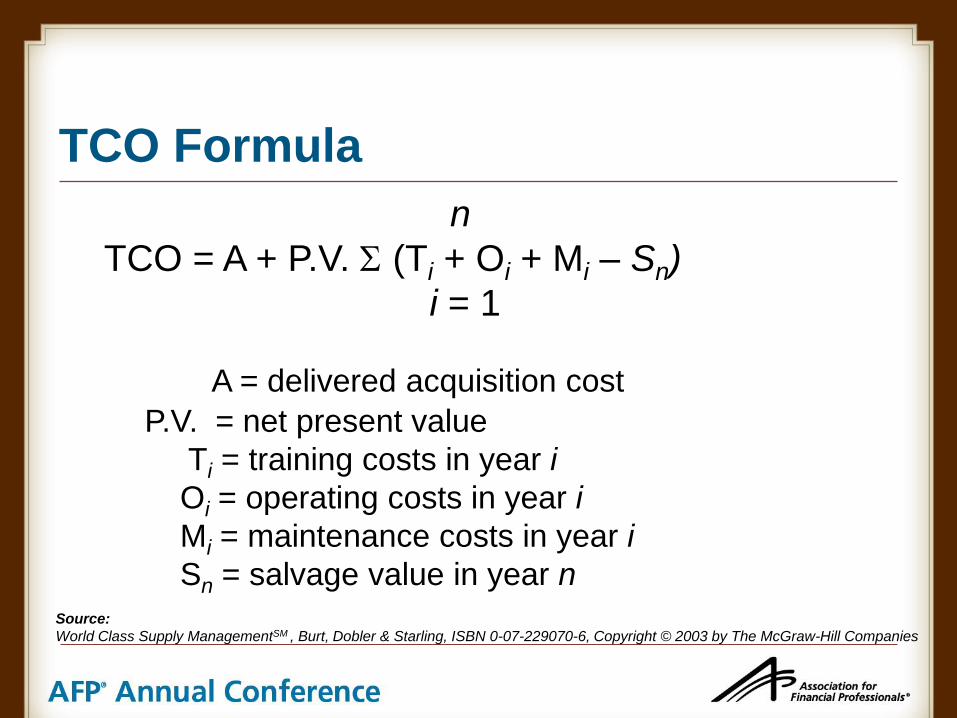

TCO Formula

n

TCO = A + P.V. (Ti + Oi + Mi – Sn)

i = 1

Source:

World Class Supply ManagementSM , Burt, Dobler & Starling, ISBN 0-07-229070-6, Copyright © 2003 by The McGraw-Hill Companies

A = delivered acquisition cost

P.V. = net present value

Ti = training costs in year i

Oi = operating costs in year i

Mi = maintenance costs in year i

Sn = salvage value in year n

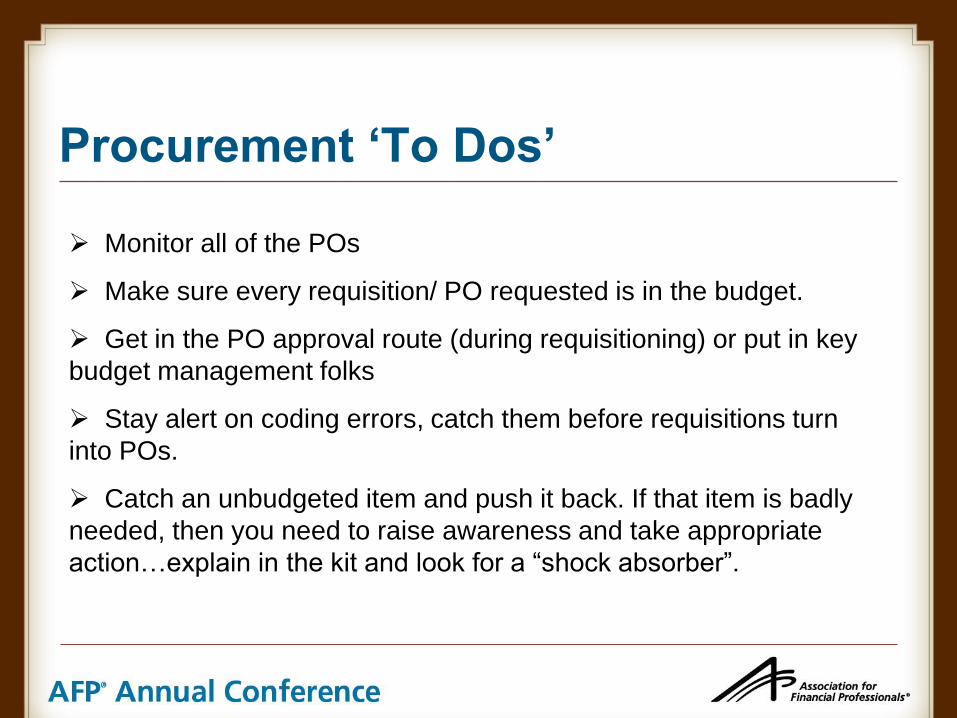

Procurement ‘To Dos’

Monitor all of the POs

Make sure every requisition/ PO requested is in the budget.

Get in the PO approval route (during requisitioning) or put in key

budget management folks

Stay alert on coding errors, catch them before requisitions turn

into POs.

Catch an unbudgeted item and push it back. If that item is badly

needed, then you need to raise awareness and take appropriate

action…explain in the kit and look for a “shock absorber”.

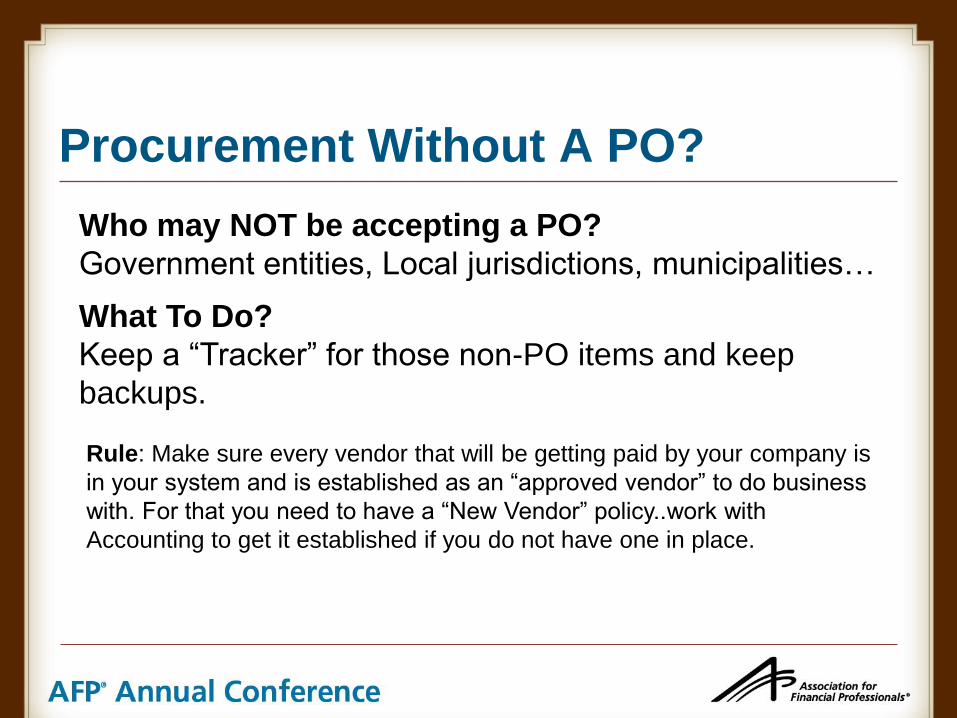

Procurement Without A PO?

Who may NOT be accepting a PO?

Government entities, Local jurisdictions, municipalities…

What To Do?

Keep a “Tracker” for those non-PO items and keep

backups.

Rule: Make sure every vendor that will be getting paid by your company is

in your system and is established as an “approved vendor” to do business

with. For that you need to have a “New Vendor” policy..work with

Accounting to get it established if you do not have one in place.

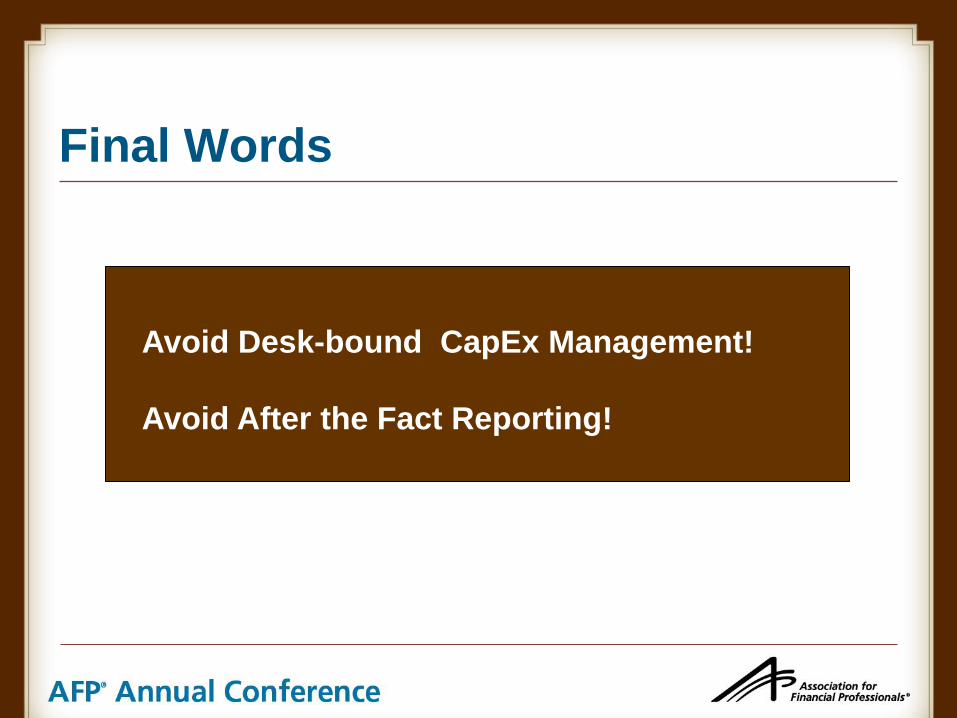

Final Words

Avoid Desk-bound CapEx Management!

Avoid After the Fact Reporting!