Simplifying the Equity Method of Accounting November 19 ...

26

Board Meeting Handout ________________________ The staff prepares Board meeting handouts to facilitate the audience's understanding of the issues to be addressed at the Board meeting. This material is presented for discussion purposes only; it is not intended to reflect the views of the FASB or its staff. Official positions of the FASB are determined only after extensive due process and deliberations. Page 1 of 6 Simplifying the Equity Method of Accounting November 19, 2015 PURPOSE OF THIS MEETING 1. The November 19, 2015 Board meeting is a decision-making meeting to discuss a summary of comments received on the June 2015 proposed FASB Accounting Standards Update, Investments—Equity Method and Joint Ventures (Topic 323): Simplifying the Equity Method of Accounting, and next steps of the project. BACKGROUND 2. On March 18, 2015, the Board added a project to its agenda to simplify the equity method of accounting and subsequently published a proposed Update for comment on June 5, 2015. The amendments in the proposed Update were issued as part of the Board’s Simplification Initiative, the objective of which is to identify, evaluate, and improve areas of generally accepted accounting principles (GAAP) for which cost and complexity can be reduced while maintaining or improving usefulness of the information provided to financial statement users. The amendments in the proposed Update would eliminate the requirements to (a) account for the basis difference as if the investment were a consolidated subsidiary (Issue 1) and (b) retroactively adopt the equity method of accounting if an investment qualifies for use of the equity method as a result of an increase in ownership or degree of influence (Issue 2). 3. The comment period for the proposed Update ended on August 4, 2015. Forty-two comment letters were received, a summary of which was separately distributed. ISSUE 1: BASIS DIFFERENCE 4. FASB Accounting Standards Codification ® Topic 323, Investments—Equity Method and Joint Ventures, requires that an investor measure an investment in the common

Transcript of Simplifying the Equity Method of Accounting November 19 ...

Board Meeting Handout

________________________

The staff prepares Board meeting handouts to facilitate the audience's understanding of the issues to be

addressed at the Board meeting. This material is presented for discussion purposes only; it is not intended to

reflect the views of the FASB or its staff. Official positions of the FASB are determined only after extensive

due process and deliberations.

Page 1 of 6

Simplifying the Equity Method of Accounting

November 19, 2015

PURPOSE OF THIS MEETING

1. The November 19, 2015 Board meeting is a decision-making meeting to discuss a

summary of comments received on the June 2015 proposed FASB Accounting

Standards Update, Investments—Equity Method and Joint Ventures (Topic 323):

Simplifying the Equity Method of Accounting, and next steps of the project.

BACKGROUND

2. On March 18, 2015, the Board added a project to its agenda to simplify the equity

method of accounting and subsequently published a proposed Update for comment

on June 5, 2015. The amendments in the proposed Update were issued as part of the

Board’s Simplification Initiative, the objective of which is to identify, evaluate, and

improve areas of generally accepted accounting principles (GAAP) for which cost

and complexity can be reduced while maintaining or improving usefulness of the

information provided to financial statement users. The amendments in the proposed

Update would eliminate the requirements to (a) account for the basis difference as if

the investment were a consolidated subsidiary (Issue 1) and (b) retroactively adopt

the equity method of accounting if an investment qualifies for use of the equity

method as a result of an increase in ownership or degree of influence (Issue 2).

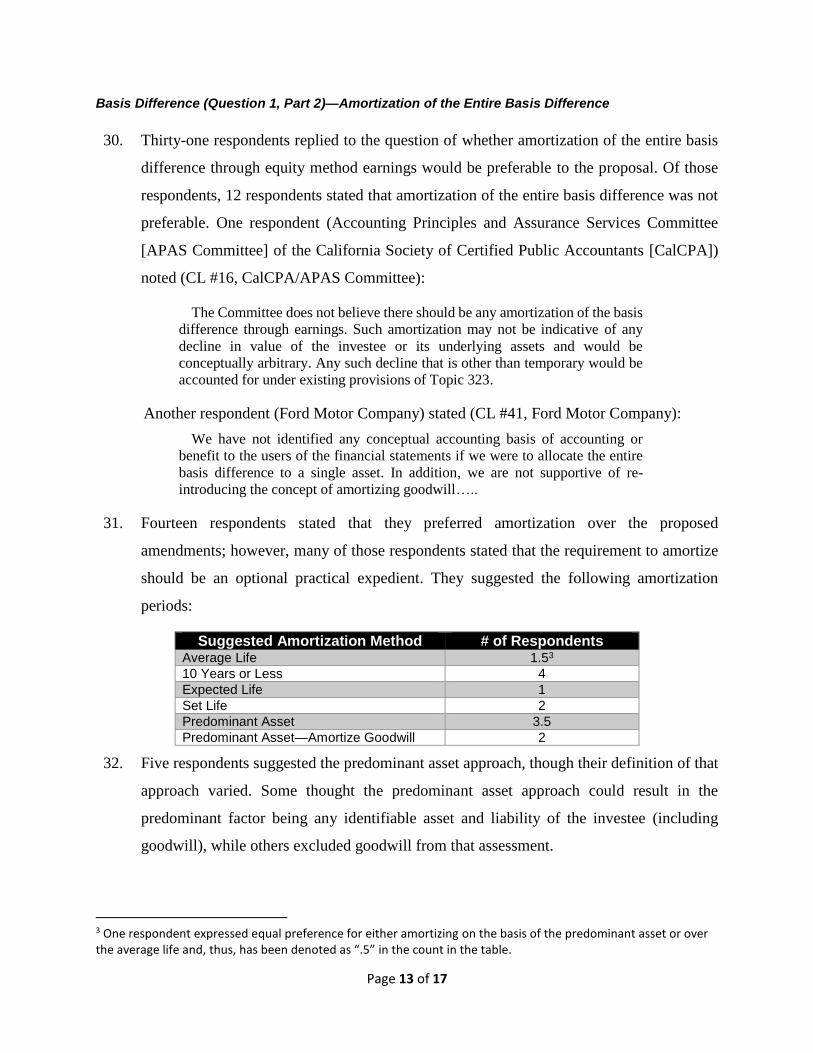

3. The comment period for the proposed Update ended on August 4, 2015. Forty-two

comment letters were received, a summary of which was separately distributed.

ISSUE 1: BASIS DIFFERENCE

4. FASB Accounting Standards Codification® Topic 323, Investments—Equity Method

and Joint Ventures, requires that an investor measure an investment in the common

Page 2 of 6

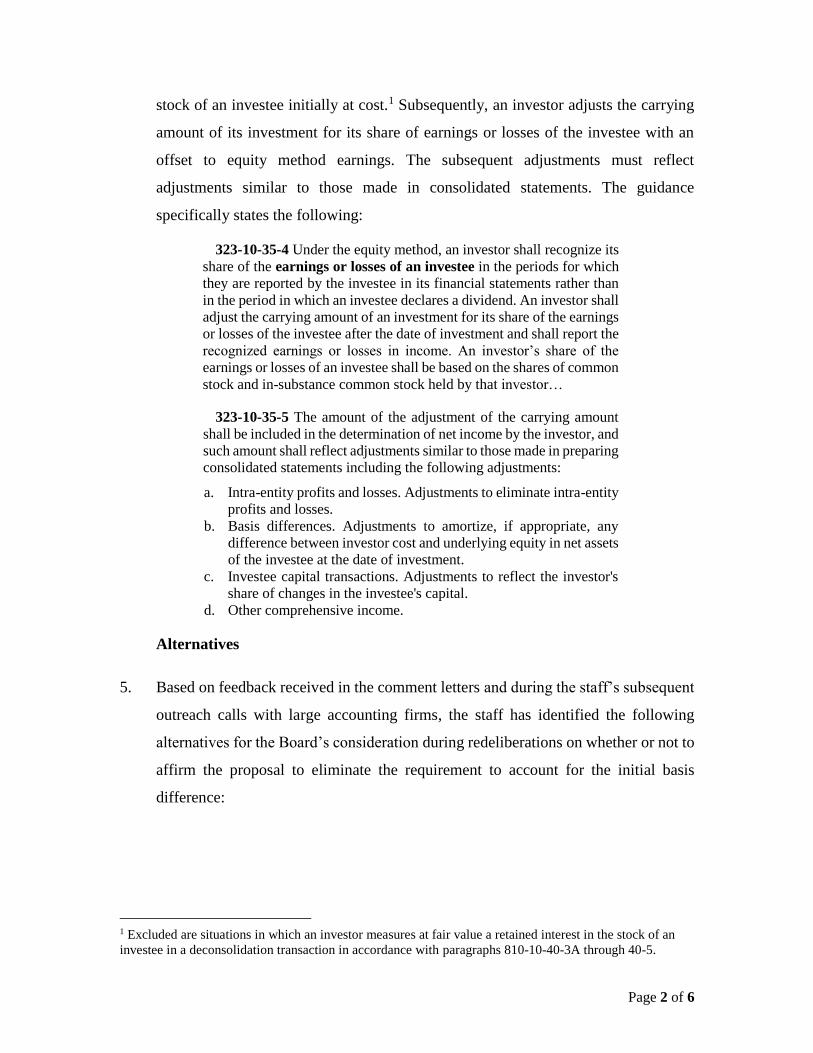

stock of an investee initially at cost.1 Subsequently, an investor adjusts the carrying

amount of its investment for its share of earnings or losses of the investee with an

offset to equity method earnings. The subsequent adjustments must reflect

adjustments similar to those made in consolidated statements. The guidance

specifically states the following:

323-10-35-4 Under the equity method, an investor shall recognize its

share of the earnings or losses of an investee in the periods for which

they are reported by the investee in its financial statements rather than

in the period in which an investee declares a dividend. An investor shall

adjust the carrying amount of an investment for its share of the earnings

or losses of the investee after the date of investment and shall report the

recognized earnings or losses in income. An investor’s share of the

earnings or losses of an investee shall be based on the shares of common

stock and in-substance common stock held by that investor…

323-10-35-5 The amount of the adjustment of the carrying amount

shall be included in the determination of net income by the investor, and

such amount shall reflect adjustments similar to those made in preparing

consolidated statements including the following adjustments:

a. Intra-entity profits and losses. Adjustments to eliminate intra-entity

profits and losses.

b. Basis differences. Adjustments to amortize, if appropriate, any

difference between investor cost and underlying equity in net assets

of the investee at the date of investment.

c. Investee capital transactions. Adjustments to reflect the investor's

share of changes in the investee's capital.

d. Other comprehensive income.

Alternatives

5. Based on feedback received in the comment letters and during the staff’s subsequent

outreach calls with large accounting firms, the staff has identified the following

alternatives for the Board’s consideration during redeliberations on whether or not to

affirm the proposal to eliminate the requirement to account for the initial basis

difference:

1 Excluded are situations in which an investor measures at fair value a retained interest in the stock of an

investee in a deconsolidation transaction in accordance with paragraphs 810-10-40-3A through 40-5.

Page 3 of 6

(a) Alternative A—Predominant Source: Provide an optional practical

expedient to account for the basis difference based on the nature of the

predominant source of the basis difference.

(b) Alternative B—Weighted Average: Provide an optional practical

expedient that allows an investor to account for the basis difference

based on a group of similar assets or liabilities.

(c) Alternative C—Predominant Source/Set Period: Provide an optional

practical expedient that allows an investor to account for the basis

difference based on the predominant source, or if there is no

predominant source, amortize the basis difference over a set period.

(d) Alternative D—No change to current GAAP: Determine that this

proposed requirement should not be pursued further; that is, make no

change to existing guidance.

Questions for the Board

1. Does the Board want to affirm its decision to eliminate the requirement to

account for the basis difference between the cost of an investment and the

underlying net assets of the investee (the initial basis difference) as if the

investee were a consolidated subsidiary?

The following question applies only if the Board answers “no” to

Question 1.

2. Does the Board want to further pursue any of the alternatives above? If

so, what additional research would the Board like the staff to perform?

ISSUE 2: INCREASE IN THE LEVEL OF OWNERSHIP INTEREST OR

DEGREE OF INFLUENCE

6. If an investment that was previously accounted for on other than the equity method

becomes qualified for use of the equity method by an increase in the level of

ownership interest or degree of influence, the investor would retroactively adopt the

equity method of accounting. This would require an investor to retrospectively

Page 4 of 6

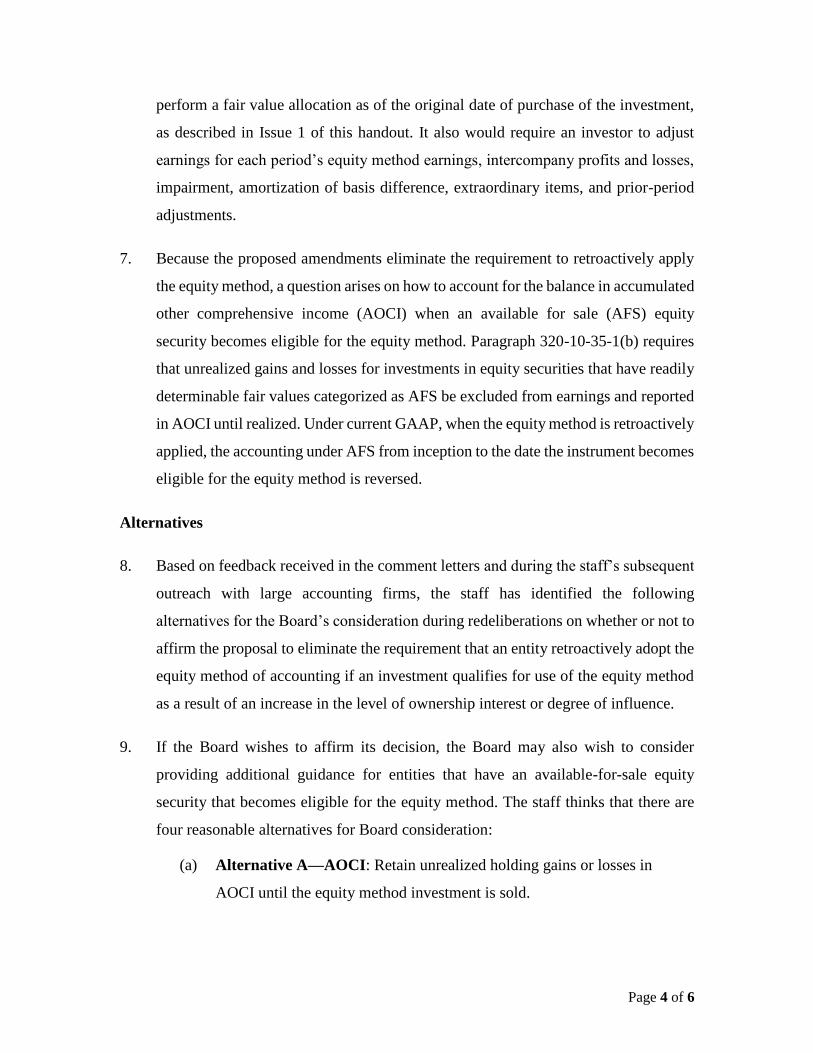

perform a fair value allocation as of the original date of purchase of the investment,

as described in Issue 1 of this handout. It also would require an investor to adjust

earnings for each period’s equity method earnings, intercompany profits and losses,

impairment, amortization of basis difference, extraordinary items, and prior-period

adjustments.

7. Because the proposed amendments eliminate the requirement to retroactively apply

the equity method, a question arises on how to account for the balance in accumulated

other comprehensive income (AOCI) when an available for sale (AFS) equity

security becomes eligible for the equity method. Paragraph 320-10-35-1(b) requires

that unrealized gains and losses for investments in equity securities that have readily

determinable fair values categorized as AFS be excluded from earnings and reported

in AOCI until realized. Under current GAAP, when the equity method is retroactively

applied, the accounting under AFS from inception to the date the instrument becomes

eligible for the equity method is reversed.

Alternatives

8. Based on feedback received in the comment letters and during the staff’s subsequent

outreach with large accounting firms, the staff has identified the following

alternatives for the Board’s consideration during redeliberations on whether or not to

affirm the proposal to eliminate the requirement that an entity retroactively adopt the

equity method of accounting if an investment qualifies for use of the equity method

as a result of an increase in the level of ownership interest or degree of influence.

9. If the Board wishes to affirm its decision, the Board may also wish to consider

providing additional guidance for entities that have an available-for-sale equity

security that becomes eligible for the equity method. The staff thinks that there are

four reasonable alternatives for Board consideration:

(a) Alternative A—AOCI: Retain unrealized holding gains or losses in

AOCI until the equity method investment is sold.

Page 5 of 6

(b) Alternative B—Retained Earnings: Recognize a cumulative-effect

adjustment to the statement of financial position as of the date the

investment qualifies for use of the equity method.

(c) Alternative C—Earnings: Recognize unrealized holding gain or loss

from AOCI at the date in which the investment qualifies for use of the

equity method.

(d) Alternative D—Basis of the Investment: Reclassify the unrealized

gain or loss to the basis of the investment at the date in which the

investment qualifies for use of the equity method.

Questions for the Board

3. Does the Board want to affirm its decision to eliminate the requirement

that an entity retroactively adopt the equity method of accounting if an

investment qualifies for use of the equity method as a result of an increase

in the level of ownership interest or degree of influence?

The following question applies only if the Board answers “yes” to

Question 3.

4. Does the Board want to provide additional guidance for entities that have

an available-for-sale equity security that becomes eligible for equity method

treatment?

NOTE: The following questions are only relevant if the Board decides to address and proceed with Issue 2.

ISSUE 3: BENEFITS, COSTS, AND COMPLEXITY

Questions for the Board

5. Have all relevant issues been deliberated and have Board members

received sufficient information and analysis to make informed decisions on

Issue 2? If not, what other information or analysis does the Board need?

6. Do the expected benefits of the change justify the perceived costs of the

change?

Page 6 of 6

ISSUE 4: TRANSITION AND TRANSITION DISCLOSURES

Questions for the Board

7. Does the Board want to affirm the amendments in the proposed Update

on Topic 323 that would require the changes for Issue 2 to be applied

prospectively to increases that result in qualifying for the equity method

occurring after the proposed amendments become effective?

8. Does the Board want to affirm the amendments in the proposed Update

on Topic 323 on transition disclosures for Issue 2?

ISSUE 5: EFFECTIVE DATE AND EARLY ADOPTION

Questions for the Board

9. What should be the effective date(s) of the final guidance for (a) public

business entities and (b) all other entities for Issue 2?

10. Should early adoption be permitted for Issue 2?

ISSUE 6: PERMISSION TO BALLOT

Questions for the Board

11. Does the Board grant the staff permission to begin drafting a final

Accounting Standards Update for vote by written ballot for Issue 2?

Proposed FASB Accounting Standards Update, Investments—Equity Method and

Joint Ventures (Topic 323): Simplifying the Equity Method of Accounting

Feedback Summary

November 19, 2015

Background Information

1. On March 18, 2015, the Board added a project to its agenda to simplify the equity method

of accounting. The proposed FASB Accounting Standards Update, Investments—Equity

Method and Joint Ventures (Topic 323): Simplifying the Equity Method of Accounting, was

published for comment on June 5, 2015. The proposed Update was issued as part of the

Board’s Simplification Initiative, the objective of which is to identify, evaluate, and

improve areas of generally accepted accounting principles (GAAP) for which cost and

complexity can be reduced while maintaining or improving usefulness of the information

provided to users of the financial statements. The amendments in the proposed Update

would eliminate the requirements to (a) account for the basis difference as if the investment

were a consolidated subsidiary and (b) retroactively adopt the equity method of accounting

if an investment qualifies for use of the equity method as a result of an increase in ownership

or influence.

2. The comment period for the proposed Update ended on August 4, 2015.

Comment Letter Demographics

3. The Board received 42 comment letters, which are summarized below by respondent type.

Professional organizations include the American Institute of Certified Public Accountants

(AICPA), the Association of Accountants and Financial Professionals in Business (IMA),

CFA Institute, and state societies of certified public accountants.

Page 2 of 17

Constituency Number

Accounting Firm 10

Individual 3

Industry Organization 2

Preparer 19

Professional Organization 8

Total 42

4. The following table disaggregates preparers and industry organizations into industries:

Industry Number

Banking/Financial Services 3

Consumer Products 3

Energy/Utility 4

Insurance 5

Oil and Gas 1

Pharmaceutical 2

Real Estate 3

Total 21

Summary of Comments Letters

5. Stakeholders were asked to comment on the following questions in the proposed Update:

Question 1: Should accounting for the basis difference of equity method investments

as if the investment were a consolidated subsidiary be eliminated? Why or why not?

Would amortization of the entire basis difference through equity method earnings be

preferable? If so, what would be the suggested amortization period?

Question 2: Should the accounting for capitalized interest, which adds to the basis of

an entity’s equity method investment and is amortized, also be eliminated for equity

method investments? Why or why not?

Question 3: Should an entity be required to apply the proposed amendments related to

accounting for the basis difference on a modified prospective basis as of the effective

date? Why or why not?

Question 4: Should an entity no longer be required to retroactively adopt the equity

method of accounting if an investment qualifies for use of the equity method as a result

of an increase in the level of ownership interest? Why or why not?

Page 3 of 17

Question 5: Should the proposed guidance to eliminate the requirement to retroactively

adopt the equity method of accounting be applied prospectively? Why or why not?

Question 6: How much time will be necessary to adopt the amendments in this proposed

Update? Should early adoption be permitted? Should the amount of time needed to

apply the proposed amendments by entities other than public business entities be

different from the amount of time needed by public business entities?

Question 7: Would the proposed amendments meet the objective of the Simplification

Initiative, which is to improve GAAP by reducing cost and complexity while

maintaining or improving the usefulness of the information provided to users of

financial statements? Why or why not?

6. The comment letters are summarized within the following sections:

(a) Basis Difference (Question 1, Part 1)

(b) Basis Difference (Question 1, Part 2)

(c) Capitalized Interest (Question 2)

(d) Increase in the Level of Ownership Interest or Degree of Influence (Question 4)

(e) Objective of Simplification (Question 7)

(f) Transition Method (Questions 3 and 5)

(g) Effective Date and Early Adoption Considerations (Question 6)

(h) Additional Issues.

Basis Difference (Question 1, Part 1)

7. Sixteen respondents (including 10 preparers, 3 professional organizations, 2 practitioners,

and an individual) indicated that they agreed with the proposal to eliminate the accounting

for basis differences. The preparers included pharmaceutical, automotive, aerospace,

hospitality, utilities, and financial services industries. The majority of these respondents

cited that accounting for equity method basis differences is costly and complex and

provides little value to users of financial statements. Additionally, many respondents

Page 4 of 17

indicated that it is difficult for an investor with significant influence to obtain the data

necessary to accurately determine acquisition date fair values.

8. Six respondents indicated that they neither strongly support nor strongly oppose the

proposal to eliminate the accounting for equity method basis difference. Of those

respondents, three respondents had split views wherein they agreed with the proposal to

eliminate the accounting for basis difference, but they also believed further clarifications,

research, and outreach would be necessary to make the proposal operational. Two

respondents agreed with the proposal for most industries, but expressed significant

concerns about the insurance industry (further explored in the “Other” subsection below).

One respondent expressed support for the proposal contingent upon the FASB retaining the

current model for goodwill; however, this respondent stated that if the current FASB

project, Accounting for Goodwill for Public Business Entities and Not-for-Profit Entities1

(the Goodwill project), results in the amortization of goodwill, then similar changes to the

equity method should be considered.

9. Twenty-nine respondents—many of which agreed with the proposal—added that they

agreed with the Board’s rationale that a “one-line consolidation” makes little conceptual

sense because, in an equity method scenario, control has not been obtained. The

respondents that disagreed with the proposal, but agreed with the Board’s rationale, largely

suggested some type of alternative approach.

10. Twenty respondents, including all of the large accounting firms, indicated that they either

fully or conditionally disagreed with the proposal to eliminate the accounting for equity

method basis difference. The respondents that conditionally disagreed suggested potential

alternatives to the proposal, including various amortization methods. These respondents

commonly cited one or more of the following reasons for dissent:

(a) Increased impairments and inflation of investment balance

1 On November 25, 2013, the Board added a project to its agenda to address goodwill impairment issues and to consider whether it should change the subsequent measurement of goodwill for public business entities and not-for-profit entities. The International Accounting Standards Board (IASB) also is considering changes to the subsequent accounting for goodwill. At a joint FASB and IASB meeting in September 2015, the Boards discussed the importance of staying converged on this issue; however, no decisions were made on how to move forward.

Page 5 of 17

(b) No conceptual basis

(c) Not reflective of economic reality

(d) Expanded regulatory requirements

(e) Gain and loss issues

(f) Statement of cash flows classification

(g) Other.

Each of these are discussed in more detail in the sections below.

Increased Impairments and Inflation of Investment Balance

11. Twenty-three respondents in total—17 of which disagreed with the proposal for basis

difference—stated that the proposed amendments would likely result in an increase in

impairments of equity method investments. The majority of these respondents reasoned that

the basis difference originating at an investment’s inception relates to assets that have a fair

value that differs from their carrying value because of perceived future resource inflows.

According to these respondents, as resource inflows materialize in future periods and are

recognized by the investor as equity method earnings, the frontloaded fair value should be

amortized accordingly. Without amortization, the carrying value of the original investment

grows each period (via equity method earnings) by the resource inflows that were included

in that investment’s original valuation, resulting in double recognition and an inflated

investment balance by not recognizing associated costs of acquiring those resource inflows.

Respondents concluded that this situation consistently overvalues equity investments and,

thus, primes them for serial impairment.

12. The majority of these respondents cited cost and complexity concerns of performing more

frequent impairment assessments as a reason for dissenting. These respondents expressed

that the valuations required to evaluate whether an impairment has occurred would be costly

to obtain and complex to perform. Furthermore, more frequent valuations would be

necessary, which would result in higher costs then are incurred under current GAAP. Many

respondents noted that any expected cost savings achieved by eliminating basis difference

Page 6 of 17

accounting would be partially or wholly offset by the increased costs of testing for

impairment.

13. A few respondents indicated that because stakeholders commonly equate an impairment

with poor investment decisions, an increase in occurrence after the proposal could create

unintended consequences for managers. PricewaterhouseCoopers LLP noted a similar

reason when describing why the benefits did not outweigh the costs of the proposal (CL

#12, PricewaterhouseCoopers LLP):

…the recognition of an impairment charge in a subsequent period due to the

recognition of inflated earnings in earlier periods will likely confuse users and

may not necessarily arise from or occur contemporaneous with any actual

change in economic circumstances underlying the investment.

14. Similarly, it is worth noting that a few respondents expressed that the perceived risks, costs,

and complexities of impairment would not outweigh the benefits of the proposed

amendments. Prudential Financial, Inc. captures these respondents’ views (CL#24,

Prudential Financial, Inc.):

While this simplification could result in additional focus on the impairment

analysis in certain investees, we do not view this as burdensome or costly as this

analysis is already required. Furthermore, the impairment model should mitigate

concerns that reduced amortization will inflate earnings since any other than

temporary loss in value will be reflected in earnings, regardless of cause.

The majority of respondents that were concerned about increased cost and complexity as a

result of increased impairment testing suggested that allowing for systematic amortization

would help to curtail the potential increase in impairments. For additional discussion on

whether respondents believe amortization of the entire basis difference was preferable to

the proposal and what methodologies were suggested, see “Basis Difference (Question 1,

Part 2)” below.

No Conceptual Basis

15. Six respondents, including all of the large accounting firms, were disturbed that the Board

would cease to identify the equity method as a “one-line consolidation.” These respondents

noted that by moving away from the concept of a one-line consolidation, the equity method

of accounting would lack a conceptual basis for existence. The views expressed by these

Page 7 of 17

respondents were reflected in Financial Reporting Advisors, LLC’s comment letter (CL #7,

Financial Reporting Advisors, LLC):

If the Board believes that equity method accounting need not be similar to the

consolidation model, then what concept governs the accounting? What objective

is the equity method trying to achieve? Why not eliminate the equity method

entirely? The Board does not address these questions. Nor does the Board

discuss why the alternative accounting model ignores basis differences but

requires consideration of intra-entity profits and losses. Why is “significant

influence” different enough from “control” to ignore the economic

consequences of basis differences but similar enough to consider the economic

consequences of intra-entity transactions. Why not simplify things by ignoring

intra-entity transactions too? Companies most certainly incur costs to identify

and track those transactions. If ignoring intra-entity transactions seems “wrong”

at some fundamental level, why isn’t ignoring the basis difference equally

troublesome?

16. Ernst & Young LLP expressed concern that while in the specific area of basis difference

accounting, the proposal moves the equity method away from a “one-line consolidation,”

other vestiges still exist connecting equity method to consolidation accounting (CL #20,

Ernst & Young LLP):

In addition, many equity method investors analogize to the accounting for

consolidated subsidiaries when certain events and transactions occur that are not

specifically addressed in ASC 323. This analogy is based on the historical view

that the equity method is one-line consolidation. It is not clear whether the

following analogies and practices, which are common under current GAAP,

would still be appropriate if the Proposal is finalized:

An equity method investor that is a public business entity conforms any

accounting policies used by investees that would be unacceptable in its

financial statements (e.g., a PCC alternative) when calculating equity

method earnings.

When an equity method investor has a direct investment in a subsidiary

of the investee, it “looks through” the investee and considers that parent-

subsidiary relationship to evaluate whether it can exercise significant

influence and should apply the equity method to its direct investment in

the subsidiary of its equity method investee.

Equity method investors generally follow ASC 810-10-45-12,

Consolidation—Overall, if the equity method investor and investee

have different fiscal periods.

ASC 323-10-35-6 allows an equity method investor to record its share

of the earnings or losses of an investee on a lag. Equity method investors

generally apply the same maximum difference allowed in Rule 3A-

Page 8 of 17

02(b) of SEC Regulation S-X with respect to consolidated subsidiaries

(i.e., a lag of no more than 93 days).

Some equity method investors interpret ASC 323-10-35-15 as referring

to one-line consolidation and, therefore, record their share of an

investee’s capital transaction even if it doesn’t affect the equity method

investor’s share of the investee’s net assets (e.g., when investee

accounts for share-based payments, it does not affect its net assets),

despite the fact that an equity method investee’s capital is not part of the

parent’s capital.

Not Reflective of Economic Reality

17. Twelve respondents in total (all of which disagreed with the proposal) indicated that the

elimination of accounting for equity method basis differences would not properly reflect

the economic reality of the underlying investment. These respondents stated that equity

method investments represent an investor purchasing an asset, which is acquired with the

expectation that it will materialize into future economic benefits. These future benefits take

the form of equity earnings and, thus, the basis difference must be amortized to properly

reflect that the company is reaping the value it originally prepaid for in obtaining the

investment.

Expanded Regulatory Requirements

18. Four respondents in total either qualified support for or did not support the proposal to

eliminate the accounting for equity method basis differences because elimination could

cause expanded disclosures for the Securities and Exchange Commission (SEC) registrants

due to the requirements of SEC Regulation S-X. Specifically, Rule 3-09 requires that a

registrant provide separate financial statements for each equity method investee that meets

or exceeds 20 percent significance by applying the investment or income tests set in Rule

1-02(w) of Regulation S-X. Rule 4-08 of Regulation S-X requires a registrant to disclose

summarized financial information about equity method investees if, individually or in the

aggregate, they exceed 10 percent significance under any one of 3 significant subsidiary

tests: asset, income, and investment.

Page 9 of 17

Gain and Loss Issues

19. Eight respondents in total, including three of the large accounting firms, cited that by

eliminating the accounting for equity method basis differences, the Board complicated

accounting for certain gains and losses on investee decisions. Respondents cited two

primary scenarios under which their concerns could emerge: dilution gains and losses and

investee sales of assets.

20. Dilution gains and losses (see paragraph 323-10-40-1), which occur when an equity method

investee issues additional securities, are currently measured as the difference between the

investor’s postdilution share of the investee’s net assets and its predilution share, adjusted

for the proportionate share of its basis difference. Respondents, however, were concerned

how current practice would evolve under the amendments in the proposed Update. KPMG

LLP expressed a common concern for the ambiguity in these circumstances in its comment

letter (CL #18, KPMG LLP):

While the Board’s intent relative to dilution transactions is unclear, even if the

amendments to the standard are finalized as proposed, investors may still need

to adjust their dilution gains or losses for a portion of any excess cost over their

share of the investee’s net assets in order to properly reduce the gain or increase

the loss because that excess is an integral part of the carrying value of the

investment. The Board should clarify its intent regarding dilution transactions

and evaluate whether it impacts its initial decisions reflected in the proposed

ASU.

21. Respondents cited additional gain and loss issues in cases where an investee sells assets

that had already appreciated when the investor obtained significant influence. Since the fair

values of these assets differ from their carrying values, a gain typically results, which, under

current GAAP, would require the investor to only record the excess of the sales price over

the acquisition date fair value (which may be less or more than its proportionate share of

the gain). Theoretically, the investor is able to do this if the asset sold was separately

identified when the investor assessed its basis difference. Under the proposed amendments,

respondents believed the treatment of these gains would be much less clear. Echoing the

other respondents, Ernst & Young LLP expressed concern that (CL #20, Ernst & Young

LLP):

Under the Proposal, the equity method investor would record its share of the

investee’s gain without any adjustment, regardless of the underlying asset’s fair

value on the date of the equity method investment. This may provide

Page 10 of 17

information that is not meaningful, or potentially misleading, because it would

not reflect the economics to the equity method investor because the investor may

have paid a higher purchase price for the equity method investment to obtain its

portion of the gain.

Statement of Cash Flow Classification

22. Four respondents expressed concern that the amendments in the proposed Update would

create complexities in practice for displaying equity method distributions on the statement

of cash flows2. ConocoPhillips Company captured the concerns of these respondents (CL

#19, ConocoPhillips Company):

Under FASB ASC Topic No. 230, Statement of Cash Flows (ASC 230), an

assessment of distributions of cash received from equity method investee

companies should be performed to determine the appropriate classification of

those distributions in the statement of cash flows. Specifically, a determination

must be made with respect to whether the distributions represent a return on the

investor's investment versus a return of the investor's investment. Returns on an

investor's investment are classified as operating activities while returns of an

investor's investment are classified as investing activities in the statement of

cash flows. In practice, this assessment has typically been performed by many

preparers, including ConocoPhillips, utilizing a “cumulative earnings”

approach. Under that approach, all distributions received by an investor are

considered to be returns on the investment and classified as operating cash flows

unless the cumulative distributions exceed the cumulative equity method

investment earnings recognized by the investor. Any excess distributions are

considered returns of the investment and are accordingly classified as investing

cash flows. We believe application of the proposed amendment would generally

result in the recognition of higher equity method investment earnings by the

investor. Consequently, we believe distributions that would otherwise be

classified as returns of investment under existing applicable accounting

standards would likely be classified as returns on investment if the

Exposure Draft were ultimately finalized as proposed. [Emphasis added]

Further Evaluate the Equity Method

23. Various respondents suggested that the Board further evaluate the purpose of the equity

method and not just simplify certain aspects of it. Other respondents requested that the

Board consider taking additional time to consider and explore other alternatives. These

respondents suggested the results of the Goodwill project may result in changes that the

Board would want to consider before moving forward with this project. In addition, some

noted that the Board should consider any changes that are brought about by the International

2 The Emerging Issues Task Force of the FASB discussed this issue at its September 17, 2015 meeting.

Page 11 of 17

Accounting Standards Board (IASB)’s research project on the equity method of accounting.

The IASB staff is currently working on identifying the financial reporting problem(s) that

the application of the equity method is attempting to resolve to consider both alternatives

and simplifications to the equity method.

Other

24. Respondents, primarily those that disagreed with the proposal, cited a variety of other

concerns with eliminating the accounting for equity method basis differences.

25. One respondent, CFA Institute, stated that the proposal appears to reduce the cost of

reporting; however, it does not maintain or improve the usefulness of information reported

to users (CL #42, CFA Institute):

While we don’t see the current accounting as providing the most useful

information – because it is not fair value with changes in fair value recognized

in income to reflect the total return on the investment – it at least provides

earnings on a basis consistent with other historical financial statements to which

users are accustomed.

26. A few respondents expressed concern with the fact that substantially similar investments

could—depending on whether control or significant influence was obtained—result in very

different accounting. The Financial Reporting Committee of the Institute of Management

Accountants (IMA) (CL #10, IMA) detailed an example in which 2 investors acquired an

identical 40 percent interest in an investee at the same time; however, 1 investor (as a result

of owning a license to the investee’s primary revenue source) consolidated and the other

applied the equity method. In this situation, under the proposal, the investor that

consolidates would track basis differences, which may offset investee income because of

depreciation and amortization, whereas the investor that used equity method would not do

so.

27. Similar to concern over the disparity in accounting between substantially similar investors,

a few respondents expressed concern over the disparity in the investment’s measurement

between the investor and investee. Joseph Maresca (CL #13, Joseph S. Maresca) expressed

the commonly held concern among these respondents that the proposal would allow the

investor to recognize equity method earnings without amortization, whereas the investee

would factor both into calculating its noncontrolling interest. Therefore, the measurement

Page 12 of 17

values on the financial statements of both the investor and investee would differ

substantially over time under the proposal. However, these respondents argued that under

current GAAP, the chances of such differences arising is less common and—if they do

arise—less pronounced.

28. A few respondents expressed concern that the proposal to eliminate the accounting for basis

differences of equity method investments would create problems for equity method

investors using the recast financial statements approach when applying hypothetical

liquidation at book value (HLBV). These respondents expressed concern that under the

proposal, all investors using HLBV would be required to compute the equity in earnings

only on the basis of changes in the investee’s financial statements with no recast financial

statements. This may be particularly troublesome because it would require those applying

the HLBV method to recast prior period financial statements upon adopting the

amendments in the proposed Update to obtain the beginning balance of their unadjusted

share of the investee’s net assets.

29. Respondents in the insurance industry expressed a concern that the proposal to eliminate

the accounting for equity method basis differences may be inoperable when an equity

method investment in an insurance company is acquired. The American Council of Life

Insurers (ACLI) described this scenario in its comment letter (CL #31, ACLI):

For acquired insurance company equity method investments that did not

previously prepare GAAP financial information, absent a purchase accounting

exercise, the “conversion” of certain long duration insurance liabilities and

deferred acquisition costs to GAAP would pose significant operational issues.

GAAP currently requires insurance liabilities for traditional long duration

contracts to be valued using assumptions for mortality, interest, lapses,

expenses, etc. that are locked-in at the time the insurance contracts are issued,

generally separated into annual cohorts. If the investee had not previously

accounted for these contracts with locked-in assumptions, the equity method

investor would be required, under the Exposure Draft, to “recreate” the

assumptions that the investee “would have used” at the date of original issuance

of all inforce policies (potentially having to go back years or even decades), in

order to initially and subsequently measure these insurance liabilities in

accordance with GAAP. Conversion to GAAP in this situation would most

likely be deemed impracticable, as that term is defined and used in ASC 250,

Accounting Changes and Error Corrections (ASC 250).

Page 13 of 17

Basis Difference (Question 1, Part 2)—Amortization of the Entire Basis Difference

30. Thirty-one respondents replied to the question of whether amortization of the entire basis

difference through equity method earnings would be preferable to the proposal. Of those

respondents, 12 respondents stated that amortization of the entire basis difference was not

preferable. One respondent (Accounting Principles and Assurance Services Committee

[APAS Committee] of the California Society of Certified Public Accountants [CalCPA])

noted (CL #16, CalCPA/APAS Committee):

The Committee does not believe there should be any amortization of the basis

difference through earnings. Such amortization may not be indicative of any

decline in value of the investee or its underlying assets and would be

conceptually arbitrary. Any such decline that is other than temporary would be

accounted for under existing provisions of Topic 323.

Another respondent (Ford Motor Company) stated (CL #41, Ford Motor Company):

We have not identified any conceptual accounting basis of accounting or

benefit to the users of the financial statements if we were to allocate the entire

basis difference to a single asset. In addition, we are not supportive of re-

introducing the concept of amortizing goodwill…..

31. Fourteen respondents stated that they preferred amortization over the proposed

amendments; however, many of those respondents stated that the requirement to amortize

should be an optional practical expedient. They suggested the following amortization

periods:

Suggested Amortization Method # of Respondents Average Life 1.53

10 Years or Less 4

Expected Life 1

Set Life 2

Predominant Asset 3.5

Predominant Asset—Amortize Goodwill 2

32. Five respondents suggested the predominant asset approach, though their definition of that

approach varied. Some thought the predominant asset approach could result in the

predominant factor being any identifiable asset and liability of the investee (including

goodwill), while others excluded goodwill from that assessment.

3 One respondent expressed equal preference for either amortizing on the basis of the predominant asset or over the average life and, thus, has been denoted as “.5” in the count in the table.

Page 14 of 17

33. One respondent that agreed with the proposal stated that although it agrees that amortization

is not appropriate in most circumstances, it could see the value in allowing amortization of

the entire basis difference in certain situations (finite-lived investments). The staff notes a

number of respondents that preferred the predominant asset approach would not object to a

set amortization period.

34. Four respondents preferred retaining current GAAP. These respondents generally felt that

neither the proposal nor amortization sufficiently reduced the perceptually greater risk for

impairments and, as such, failed to meet the goal of simplification or be cost effective.

These respondents additionally expressed that any alternative method of amortization, other

than that established in current GAAP, would be arbitrary.

Capitalized Interest (Question 2)

35. Seven of the 28 respondents that answered Question 2 disagreed with the elimination of

interest capitalization for equity method investments. These respondents expressed that

capitalizing interest was reflective of the total investment and, thus, should be retained.

TransCanada Corporation summarized the common reason for this belief (CL #37,

TransCanada Corporation):

As per US GAAP, ‘the objective of capitalizing interest is to obtain a measure

of acquisition cost that more closely reflects an entity's total investment in the

asset and to charge a cost that relates to the acquisition of a resource that will

benefit future periods against the revenues of the periods benefited’. If the

accounting for capitalized interest is eliminated for equity investments, the

acquisition cost may not reflect the total investment in the asset. This would

contradict the objective of capitalizing interest and also eliminates the notion

that the incurrence of interest cost is a direct cost of acquiring the asset.

Furthermore, determination of the interest cost and the amortization period over

which to amortize the interest is straightforward and does not add any

complexity to accounting for the equity investment.

36. Twenty respondents agreed that if accounting for the equity method basis difference is

eliminated, the capitalization of interest should be eliminated as well. These respondents

agreed primarily on the basis that if the accounting for the equity method basis difference

is eliminated, capitalizing interest seems superfluous because it further creates a basis

difference. Some respondents cited that there is no conceptual basis for capitalization of

interest.

Page 15 of 17

37. One respondent (CL #42, CFA Institute) noted the elimination of capitalized interest “is

not related to the acquisition of the equity method investee [the proposed Update] and is a

separate simplification initiative not prominently articulated as such.”

Increase in the Level of Ownership Interest or Degree of Influence (Question 4)

38. Thirty-seven respondents, including all of the large accounting firms, agreed with the

proposal to eliminate retroactive adoption of the equity method of accounting if an

investment qualifies for use of the equity method as a result of an increase in the level of

ownership interest. The remaining respondents did not provide an answer.

39. A large majority of the 37 respondents that agreed with the proposed change to retroactive

adoption of the equity method cited that the retroactive application is inconsistent with the

reality of the investments at a historic point in time. The Virginia Society of CPAs

(VSCPA) provided a good summary of this view (CL #29, VSCPA):

The nature of an investor’s relationship with an investee is different in periods

in which the investor did not have significant influence over the investee and is

consistent with the application of different accounting principles in each

circumstance.

40. Many of the 37 respondents that agreed with the proposed amendments cited cost and

complexity improvements as reasons why they preferred the proposal. Respondents

indicated that applying current GAAP is particularly complex because an investor with

significant influence may not have the access to the investee’s prior period financial

information necessary for applying the equity method retroactively. Furthermore,

respondents believed that the cost incurred to retroactively track basis differences

(assuming current GAAP) did not provide users with incrementally better information.

41. One respondent (Ernst & Young LLP) supported the amendments in the proposed Update,

but recommended the Board include additional guidance for situations in which an investor

obtains significant influence over an investee that was previously accounted for as an

available-for-sale investment (AFS) and applies the equity method for the first time (CL

#20, Ernst & Young LLP):

…if the Board finalizes the Proposal to eliminate the retroactive application of equity

method, we encourage it to consider including additional guidance on the accounting for

Page 16 of 17

unrealized gains and losses accumulated in OCI when an equity method investor obtains

significant influence over an investee that was previously accounted for as an available-for-

sale investment and applies the equity method for the first time. The Proposal does not

address whether such amounts should remain accumulated within OCI until the equity

method investee is sold, should be recycled into earnings or should become part of the cost

of the investment.

Objective of Simplification (Question 7)

Basis Difference

42. Fifteen out of the 31 respondents that answered Question 7 indicated their belief that the

proposed amendments meet the objective of the Simplification Initiative, which is to

improve GAAP by reducing cost and complexity while maintaining or improving the

usefulness of the information provided to users of financial statements. These respondents

cited that the information provided to users by accounting for equity method basis

differences in memo accounts is minimal.

43. Fourteen respondents to Question 7 indicated that they did not believe that the proposed

amendments meet the objective of the Simplification Initiative. The respondents

universally cited that the issues caused by eliminating accounting for the basis difference

of equity method investments outweigh any expected benefits of the proposed amendments.

44. Two respondents neither agreed nor disagreed strongly that the proposed amendments met

the objectives of the Simplification Initiative. These respondents indicated that additional

outreach or alignment with the IASB’s efforts in this area would help them determine

whether this was simplification.

Increase in the Level of Ownership Interest

45. Twenty-three out of the 31 respondents that answered Question 7 indicated that the

proposed amendments to eliminate retrospective application of the equity method meet the

objective of the Simplification Initiative; this number does not include those who left the

question blank, despite supporting the second issue in the proposal earlier in the letter. The

majority of these respondents added that the benefits conferred through retroactive equity

method application were minimal because many users did not know these provisions

existed.

Page 17 of 17

46. The remaining eight that responded to Question 7 did not directly address whether

retrospective application met the objective of the Simplification Initiative.

Transition Method (Questions 3 and 5)

47. Independent of respondents’ views on whether the accounting for basis differences of

equity method investments should be eliminated, 25 respondents largely agreed that if the

Board voted to finalize that proposal, the provisions should be adopted on a modified

prospective basis. That is, for existing equity method investments, accounting for the basis

difference would cease as of the effective date of the proposed guidance and any remaining

basis difference would be treated as part of the basis of the investment. Similarly, all

respondents that addressed the transition method for the elimination of retroactive

application of the equity method (25 respondents) agreed that if the Board voted to finalize

that proposal, the provisions should be adopted on a prospective basis.

Effective Date and Early Adoption Considerations (Question 6)

48. Fifteen out of the 23 that responded to Question 6, including 2 of the large accounting firms,

indicated that the provisions of the proposed Update would take minimal time for

companies to implement. These respondents generally indicated that the provisions of the

proposed Update primarily affected “memo accounts” and, as such, did not require any

large scale systems or procedural changes, which generally take the most time. For identical

reasons, 13 respondents indicated that there should be no effective date differences for

public and private companies. Twenty respondents indicated that early adoption should be

permitted.

Board Meeting Handout

The staff prepares Board meeting handouts to facilitate the audience's understanding of the issues to be

addressed at the Board meeting. This material is presented for discussion purposes only; it is not intended to

reflect the views of the FASB or its staff. Official positions of the FASB are determined only after extensive

due process and deliberations.

Page 1 of 3

Insurance—Targeted Improvements to the Accounting for

Long-Duration Contracts

November 19, 2015

PURPOSE OF THIS MEETING

1. The November 19, 2015 Board meeting is a decision-making meeting. At this

meeting, the Board will discuss the following:

(a) Presentation of changes in fair value of market risk benefits attributable to

an entity’s own credit risk

(b) Timing and frequency of assumption updates.

TOPIC 1: PRESENTATION OF CHANGES IN FAIR VALUE OF MARKET RISK

BENEFITS ATTRIBUTABLE TO AN ENTITY’S OWN CREDIT RISK

2. At the September 16, 2015 meeting, the Board tentatively decided that insurance

entities would be required to measure market risk benefits at fair value. That

tentative decision applies to contracts and benefits that meet both of the following

criteria:

(a) Contract: The contract holder has the ability to direct funds to one or more

separate account investment alternatives and investment performance, net of

contract fees and assessments, is passed through to the contract holder.

(b) Benefit: The insurance entity provides a benefit protecting the contract

holder from adverse capital market performance, exposing the insurance

entity to other than nominal capital market risk.

(i) A benefit is presumed to have other than nominal capital

market risk if the net amount at risk would vary significantly

in response to capital market volatility.

Page 2 of 3

(ii) Capital market risk includes equity, interest rate, and foreign

exchange risk.

3. Additionally, at the September meeting, the Board directed the staff to perform

additional research and analysis on the presentation of changes in fair value

attributable to an entity’s own credit risk. Accordingly, the staff has identified the

following alternatives for the Board’s consideration:

(a) Alternative A—Present changes in fair value attributable to an entity’s own

credit risk in net income

(b) Alternative B—Present changes in fair value attributable to an entity’s own

credit risk in other comprehensive income.

Question for the Board

1. Should changes in fair value attributable to an entity’s own credit risk be

presented in net income or in other comprehensive income?

TOPIC 2: TIMING AND FREQUENCY OF ASSUMPTION UPDATES

4. At the August 27, 2014 meeting, the Board tentatively decided that insurance

entities would be required to update certain assumptions annually in the fourth

quarter.

5. Subsequently, at the July 24, 2015 meeting, the Board discussed what method

should be used to calculate and record the effect of updating assumptions used in

determining the liability for future policy benefits for traditional contracts. The

Board decided to require the updating of cash flow assumptions using a

retrospective approach through net income and the updating of discount rate

changes using an immediate approach through other comprehensive income. At

that meeting, certain Board members directed the staff to consider the effect of the

assumption update method decision on the prior decision on the timing and

frequency of assumption updates. The staff has also received feedback from

stakeholders requesting clarification of the Board’s prior decision on the timing

and frequency of assumption updates.

Page 3 of 3

6. The staff has identified the following alternatives for the Board’s consideration:

(a) Alternative A—Cash flow assumptions should be updated on an annual

basis or more frequently if actual experience or other evidence indicates that

earlier assumptions should be revised. Discount rate assumptions should be

updated quarterly. Market risk benefits measured at fair value should be

updated quarterly.

(b) Alternative B—Update all assumptions annually in the fourth quarter only.

Question for the Board

2. How often should assumptions used in determining the liability for future

policy benefits be updated?