SIBF NPA

48

NPA Management in banks Presentation By : Dr.Narinder Kumar Bhasin Director - Gyan Bharti Institute of Technology CEO –Smart Institute of Banking Insurance and Finance PhD Research Scholar –Amity University Batch 2015 -2018

-

Upload

ramesh-thangavel-t -

Category

Documents

-

view

222 -

download

0

description

NPA

Transcript of SIBF NPA

NPA Management in banks

Presentation By :

Dr.Narinder Kumar Bhasin

Director - Gyan Bharti Institute of Technology

CEO –Smart Institute of Banking Insurance and Finance

PhD Research Scholar –Amity University Batch 2015 -2018

WHAT IS NPA

NPA ACCOUNTS ARE THOSE ACCOUNTS WHICH DO NOT YEILD ANY INCOME OR CEASED TO GENERATE INCOME FOR THE BANK.

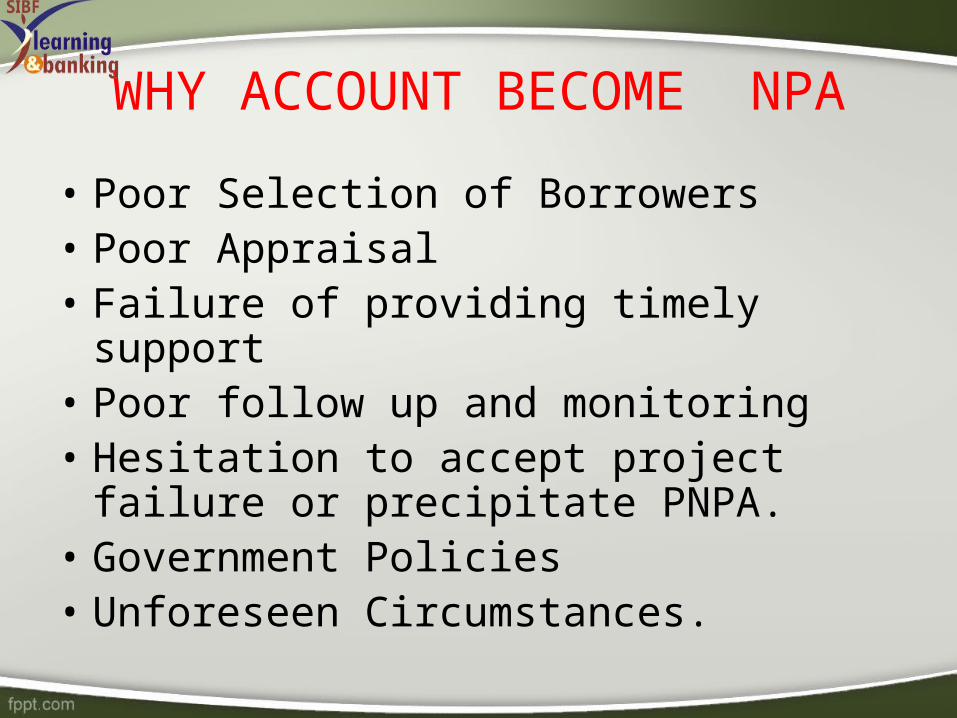

WHY ACCOUNT BECOME NPA

• Poor Selection of Borrowers• Poor Appraisal• Failure of providing timely support• Poor follow up and monitoring• Hesitation to accept project failure or

precipitate PNPA.• Government Policies• Unforeseen Circumstances.

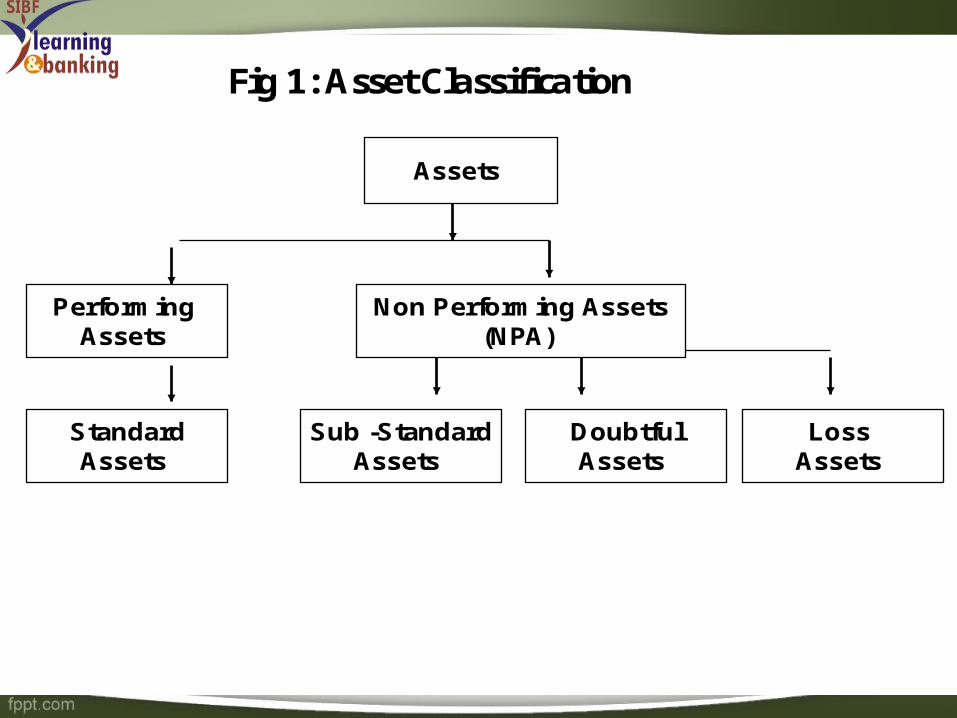

Fig 1: Asset Classification

Assets

Performing Assets

StandardAssets

Non Performing Assets(NPA)

Sub -StandardAssets

DoubtfulAssets

Loss Assets

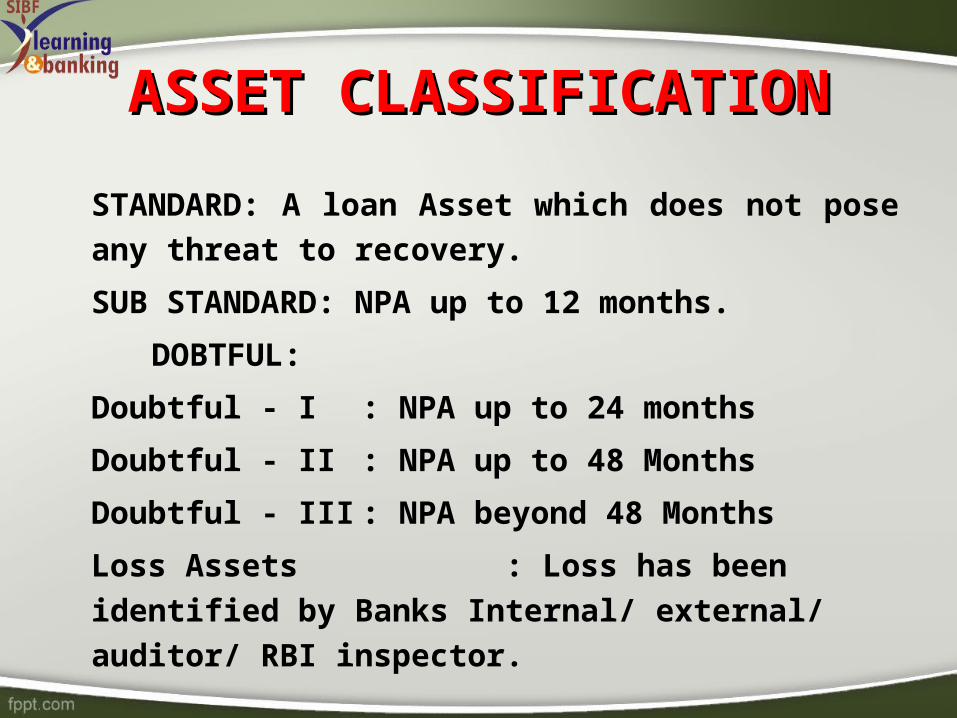

ASSET CLASSIFICATIONASSET CLASSIFICATION

STANDARD: A loan Asset which does not pose

any threat to recovery.

SUB STANDARD: NPA up to 12 months.

DOBTFUL:

Doubtful - I : NPA up to 24 months

Doubtful - II : NPA up to 48 Months

Doubtful - III : NPA beyond 48 Months

Loss Assets : Loss has been identified by

Banks Internal/ external/ auditor/ RBI inspector.

Performing Asset

• An account does not disclose any problems and carry more than normal risk attached to the business

• All loan facilities which are regular !

Non Performing Assets

• Non Performing Asset means a loan or an account of borrower, which has been classified by a bank or financial institution as sub-standard, doubtful or loss asset, in accordance with the directions or guidelines relating to asset classification issued by RBI.

Introduction

• Earlier assets were declared as NPA after completion of the period for the payment of total amount of loan and 30 days grace.

• In present scenario assets are declared as NPA if none of the installment is paid till 180 days i.e. six months in respect of a term loan.

With effect form March 31, 2004 a non-performing asset (NPA) shell be a loan or an advance where;

interest and /or installment of principal remain overdue for a period of more than 90 days in respect of a Term Loan,

the account remains 'out of order' for a period of more than 90 days, in respect of an overdraft/ cash Credit(OD/CC),

the bill remains overdue for a period of more than 90 days in the case of bills purchased and discounted,

Introduction

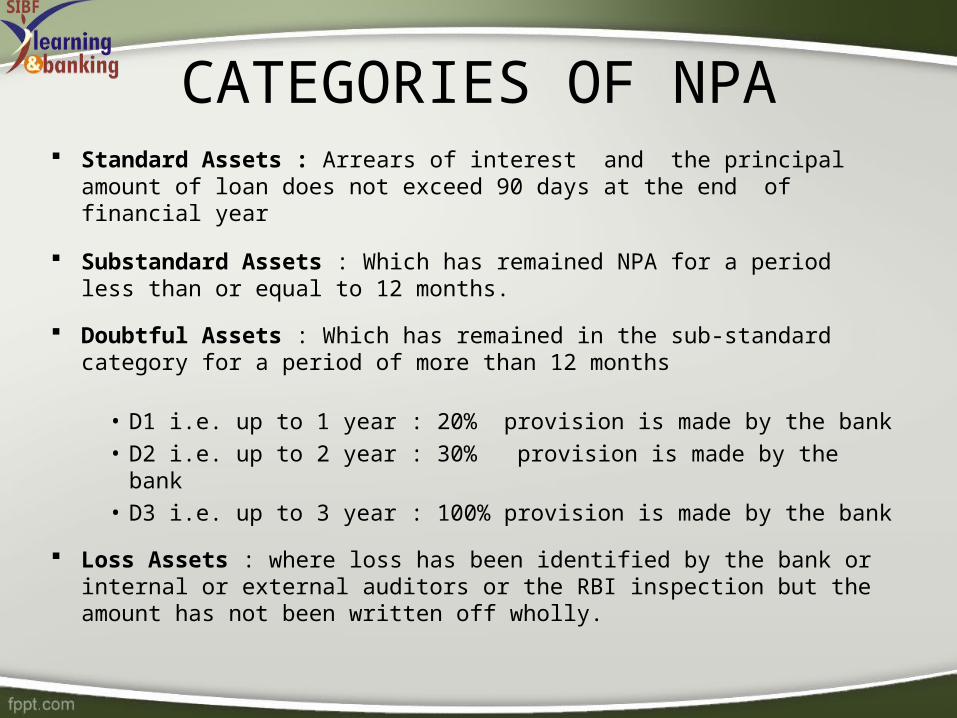

CATEGORIES OF NPA Standard Assets : Arrears of interest and the principal

amount of loan does not exceed 90 days at the end of financial year

Substandard Assets : Which has remained NPA for a period less than or equal to 12 months.

Doubtful Assets : Which has remained in the sub-standard category for a period of more than 12 months

• D1 i.e. up to 1 year : 20% provision is made by the bank• D2 i.e. up to 2 year : 30% provision is made by the bank • D3 i.e. up to 3 year : 100% provision is made by the bank

Loss Assets : where loss has been identified by the bank or internal or external auditors or the RBI inspection but the amount has not been written off wholly.

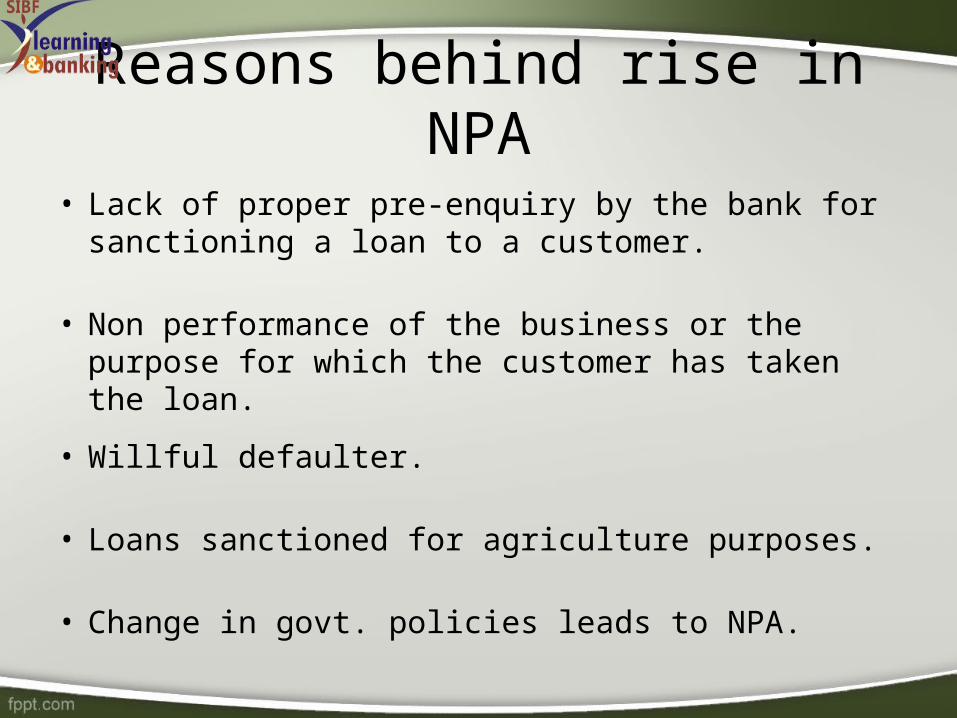

Reasons behind rise in NPA

• Lack of proper pre-enquiry by the bank for sanctioning a loan to a customer.

• Non performance of the business or the purpose for which the customer has taken the loan.

• Willful defaulter.

• Loans sanctioned for agriculture purposes.

• Change in govt. policies leads to NPA.

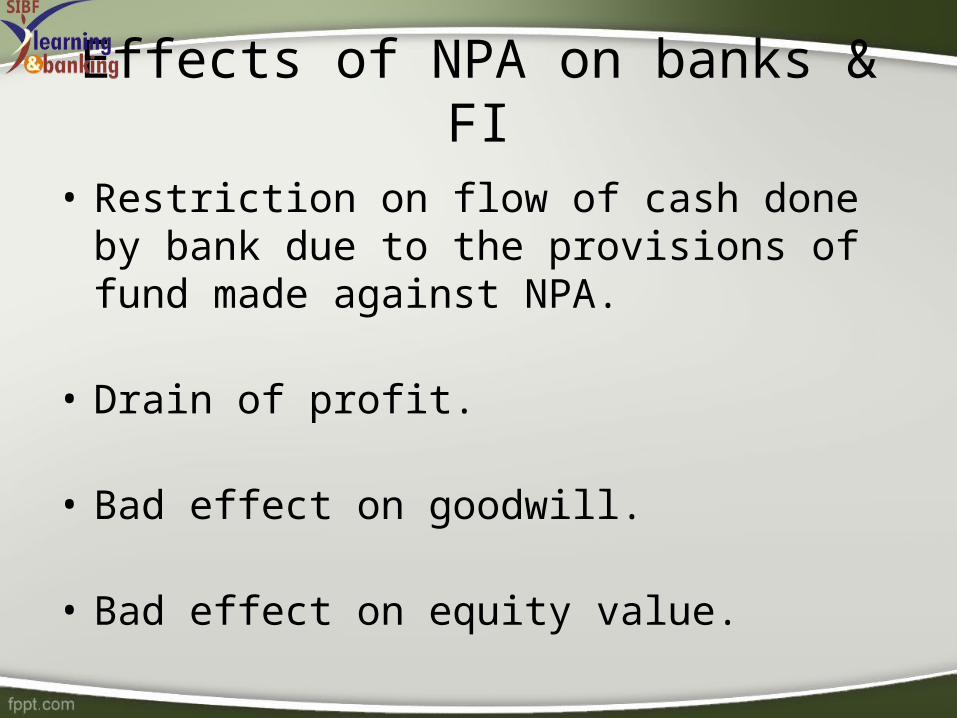

Effects of NPA on banks & FI

• Restriction on flow of cash done by bank due to the provisions of fund made against NPA.

• Drain of profit.

• Bad effect on goodwill.

• Bad effect on equity value.

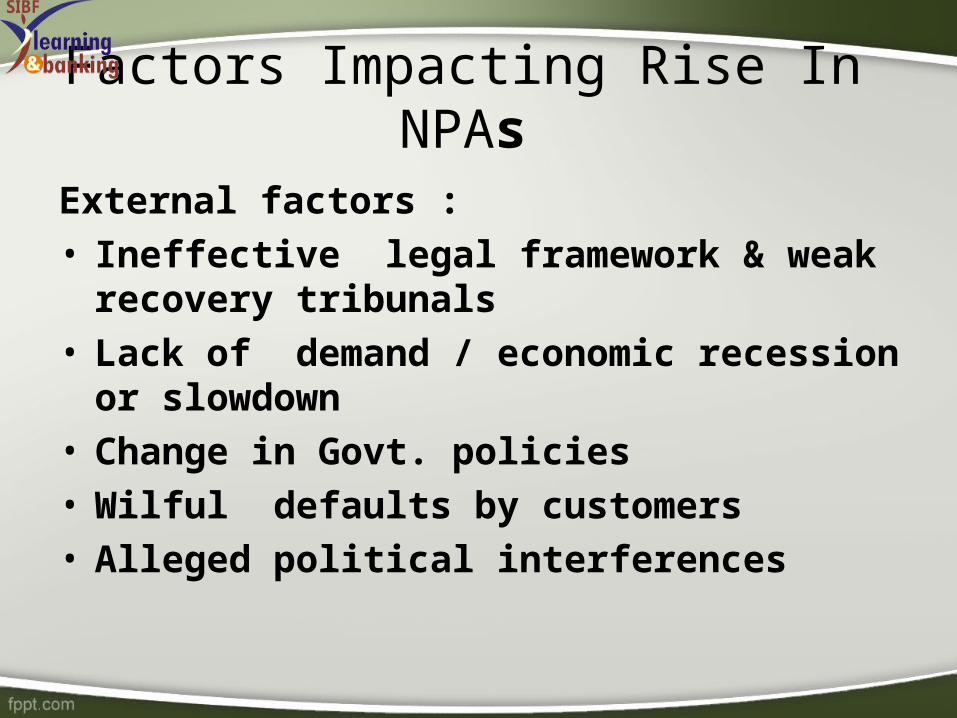

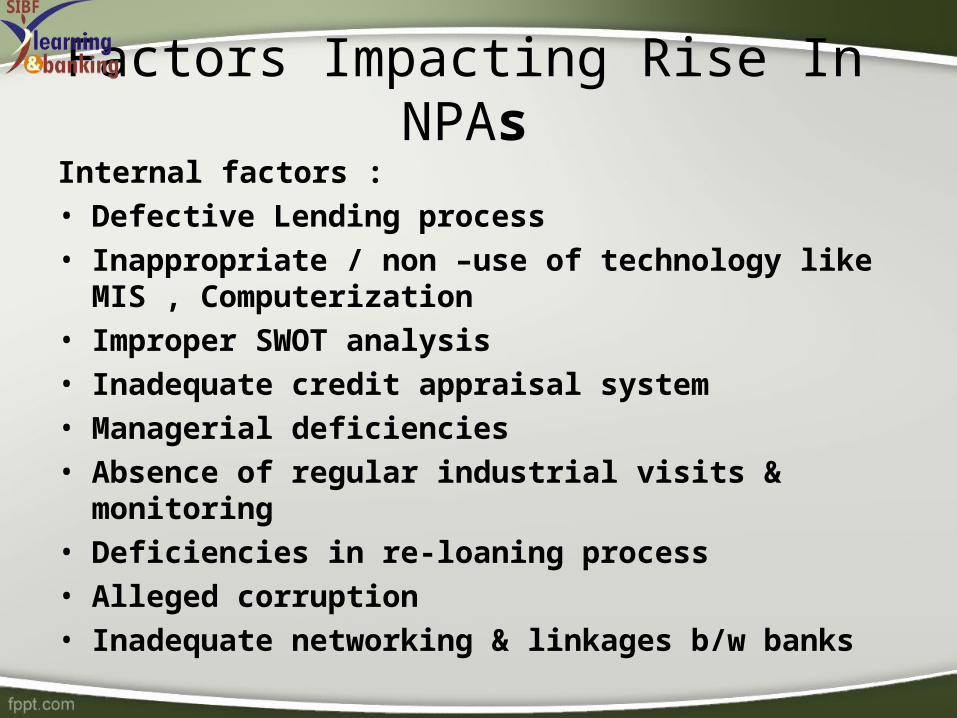

Factors Impacting Rise In NPAs

External factors :• Ineffective legal framework & weak

recovery tribunals • Lack of demand / economic recession

or slowdown• Change in Govt. policies • Wilful defaults by customers • Alleged political interferences

Factors Impacting Rise In NPAs

Internal factors :• Defective Lending process • Inappropriate / non –use of technology like MIS

, Computerization• Improper SWOT analysis • Inadequate credit appraisal system• Managerial deficiencies• Absence of regular industrial visits &

monitoring • Deficiencies in re-loaning process• Alleged corruption• Inadequate networking & linkages b/w banks

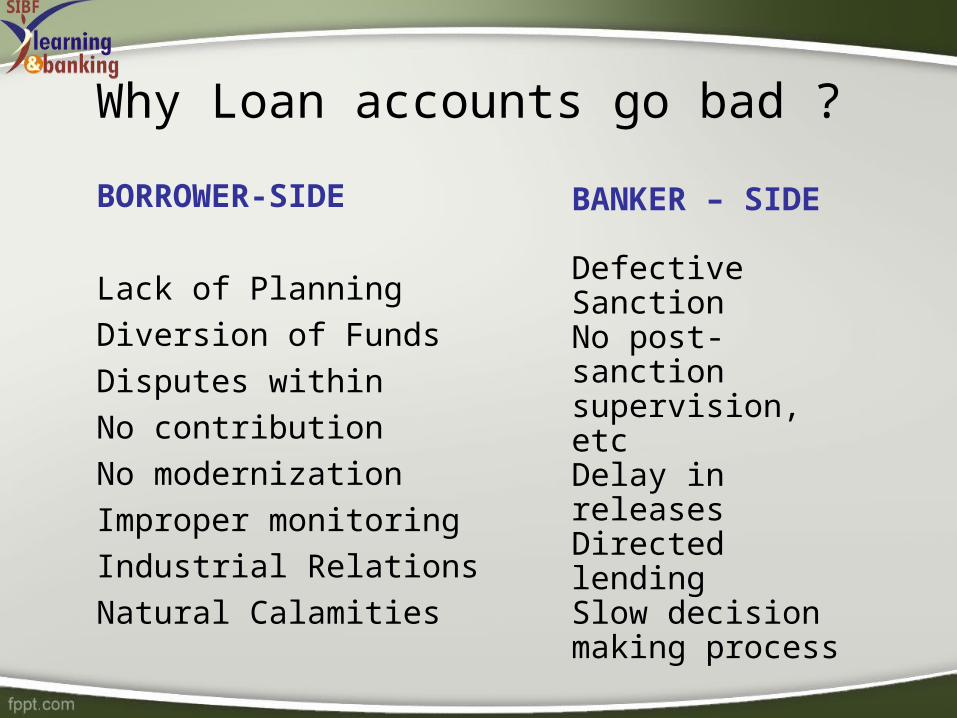

BANKER – SIDE

Defective SanctionNo post-sanction supervision, etcDelay in releasesDirected lending Slow decision making process

BORROWER-SIDE

Lack of PlanningDiversion of FundsDisputes withinNo contribution No modernizationImproper monitoringIndustrial RelationsNatural Calamities

Why Loan accounts go bad ?

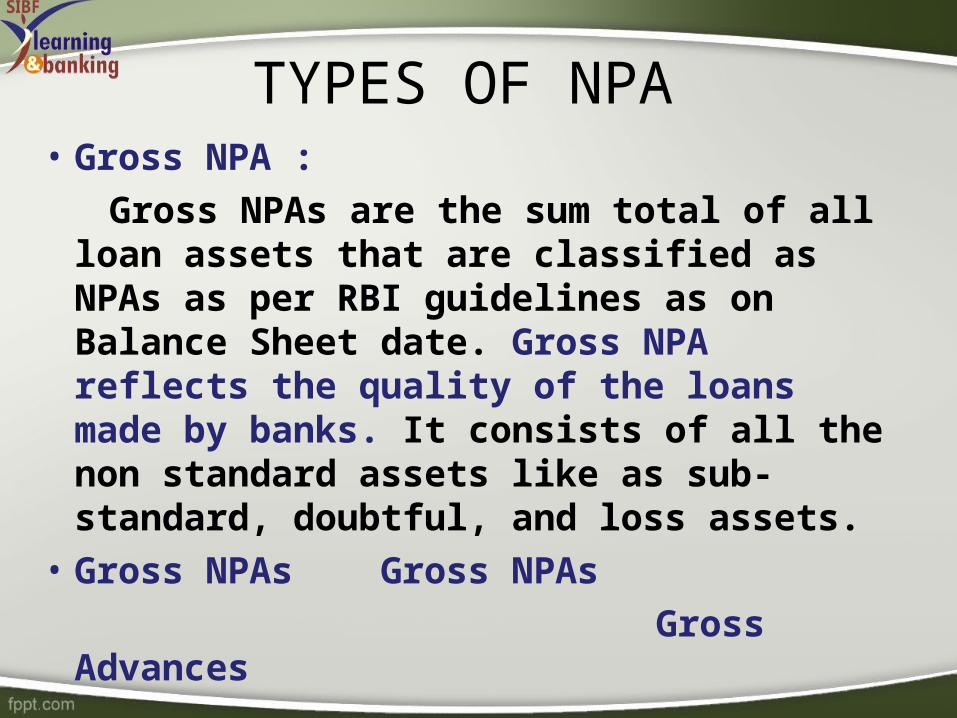

TYPES OF NPA• Gross NPA : Gross NPAs are the sum total of all

loan assets that are classified as NPAs as per RBI guidelines as on Balance Sheet date. Gross NPA reflects the quality of the loans made by banks. It consists of all the non standard assets like as sub-standard, doubtful, and loss assets.

• Gross NPAs Gross NPAs

Gross Advances

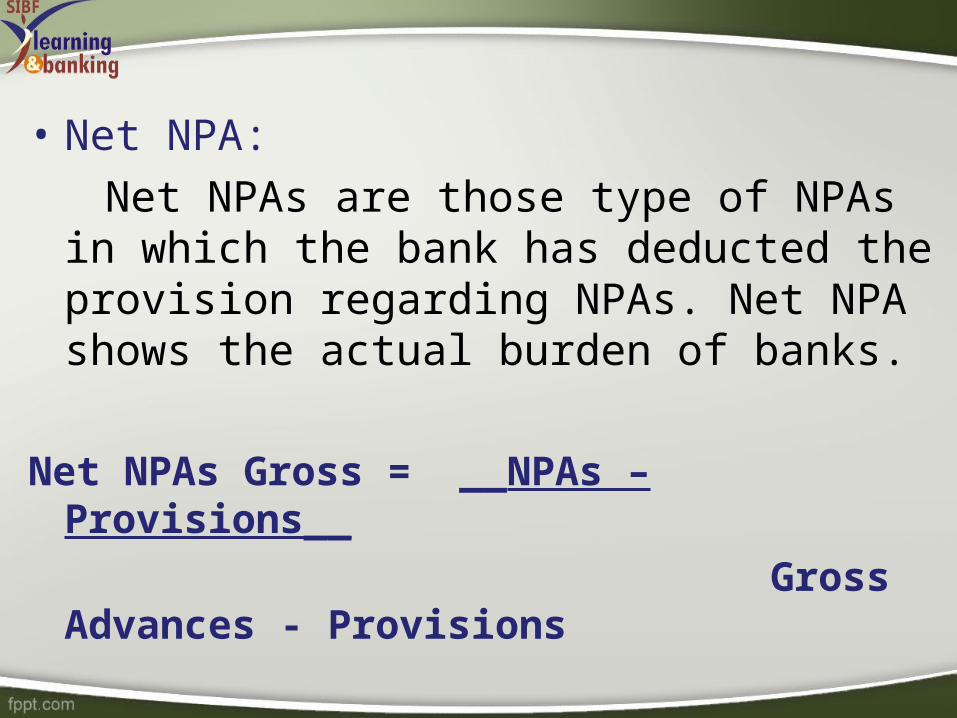

• Net NPA: Net NPAs are those type of NPAs in

which the bank has deducted the provision regarding NPAs. Net NPA shows the actual burden of banks.

Net NPAs Gross = __NPAs – Provisions__

Gross Advances - Provisions

Causes • NPA arises due to a number of factors or causes like:-• Speculation : Investing in high risk assets to earn high income.• Default : Willful default by the borrowers.• Fraudulent practices : Fraudulent Practices like advancing loans to

ineligible persons, advances without security or references, etc.• Diversion of funds : Most of the funds are diverted for unnecessary

expansion and diversion of business.• Internal reasons : Many internal reasons like inefficient management,

inappropriate technology, labour problems, marketing failure, etc. resulting in poor performance of the companies.

• External reasons : External reasons like a recession in the economy, infrastructural problems, price rise, delay in release of sanctioned limits by banks, delays in settlements of payments by government, natural calamities, etc.

SBI

• State Bank of India

Net NPAs : Rs 12,347.90 croreGross NPAs : Rs 25,326.29 crore

• The gross non-performing assets (NPAs) of public sector banks increased by 20 per cent during June-September 2011.

• Standard & Poor's, which had in September downgraded standalone ratings of State Bank of India, said high credit risks in the Indian banking sector reflects that the country has a weak payment culture and legal system that often result in low recoveries and delayed settlement of foreclosures.

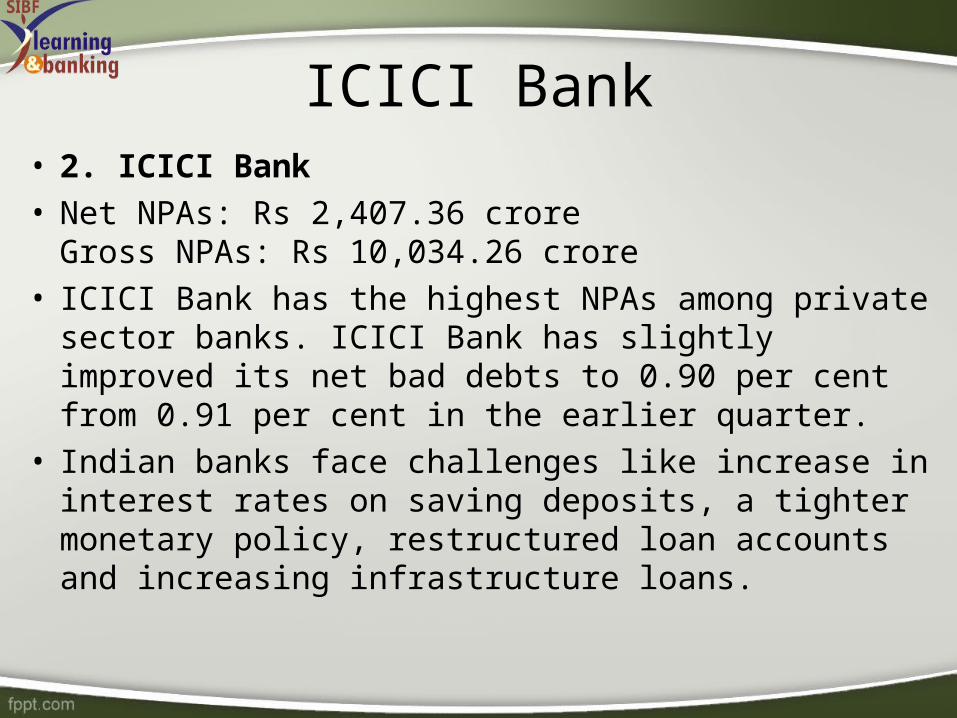

ICICI Bank• 2. ICICI Bank• Net NPAs: Rs 2,407.36 crore

Gross NPAs: Rs 10,034.26 crore• ICICI Bank has the highest NPAs among private

sector banks. ICICI Bank has slightly improved its net bad debts to 0.90 per cent from 0.91 per cent in the earlier quarter.

• Indian banks face challenges like increase in interest rates on saving deposits, a tighter monetary policy, restructured loan accounts and increasing infrastructure loans.

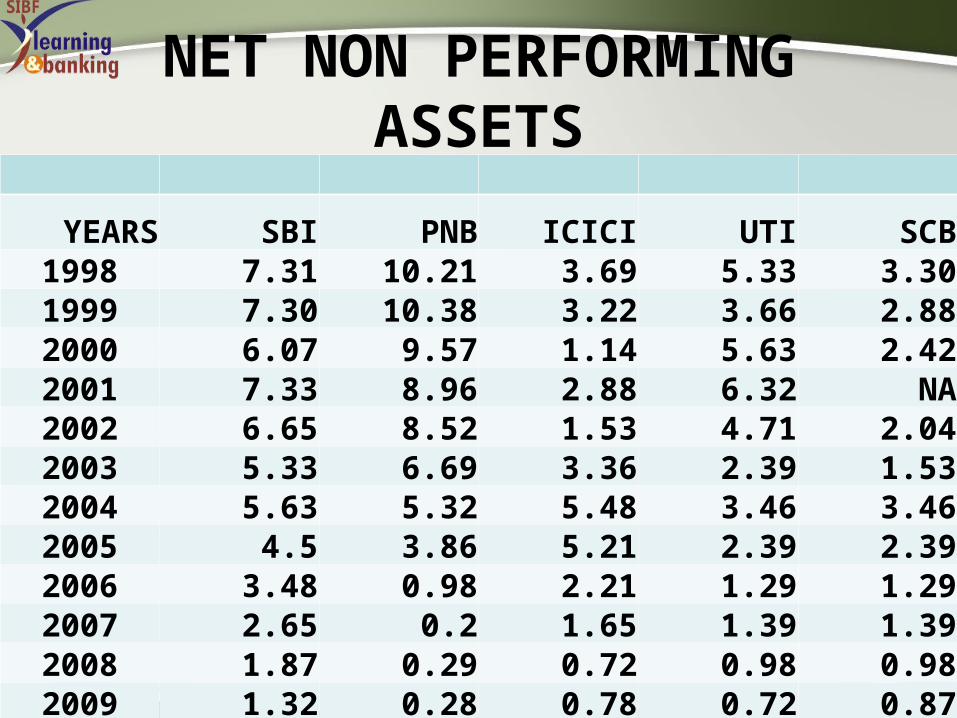

NET NON PERFORMING ASSETS

YEARS SBI PNB ICICI UTI SCB1998 7.31 10.21 3.69 5.33 3.301999 7.30 10.38 3.22 3.66 2.882000 6.07 9.57 1.14 5.63 2.422001 7.33 8.96 2.88 6.32 NA2002 6.65 8.52 1.53 4.71 2.042003 5.33 6.69 3.36 2.39 1.532004 5.63 5.32 5.48 3.46 3.462005 4.5 3.86 5.21 2.39 2.392006 3.48 0.98 2.21 1.29 1.292007 2.65 0.2 1.65 1.39 1.392008 1.87 0.29 0.72 0.98 0.982009 1.32 0.28 0.78 0.72 0.87

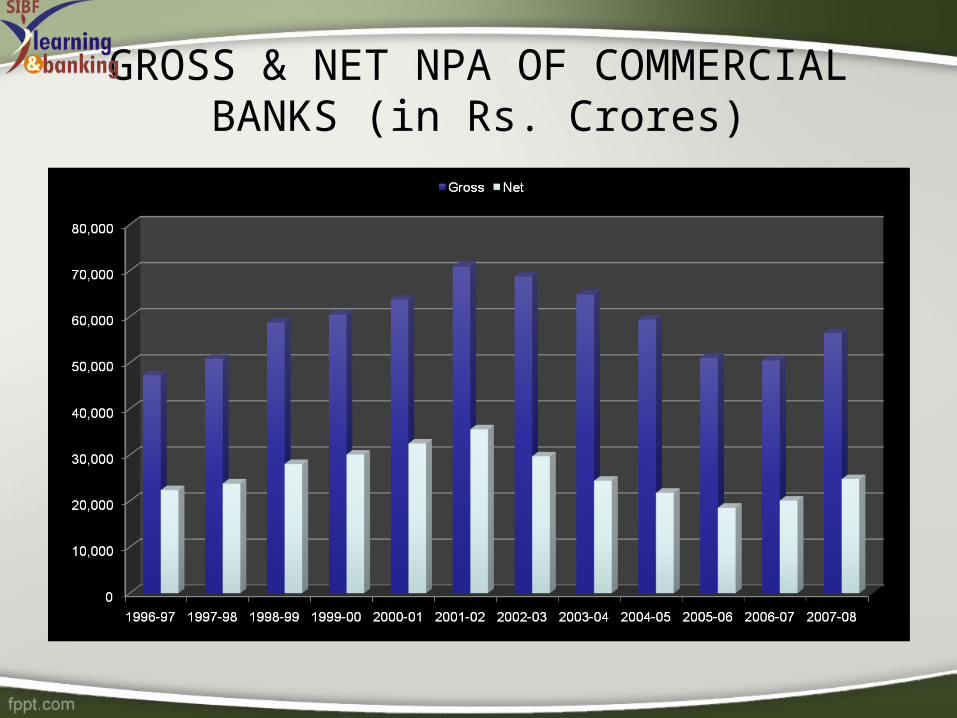

GROSS & NET NPA OF COMMERCIAL BANKS (in Rs. Crores)

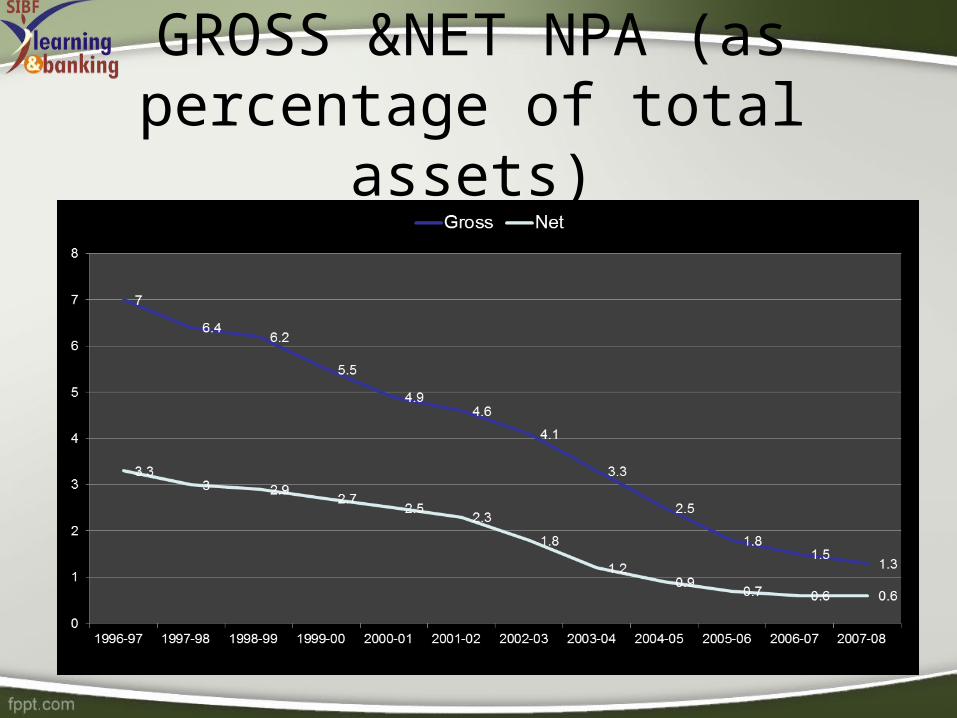

GROSS &NET NPA (as percentage of total assets)

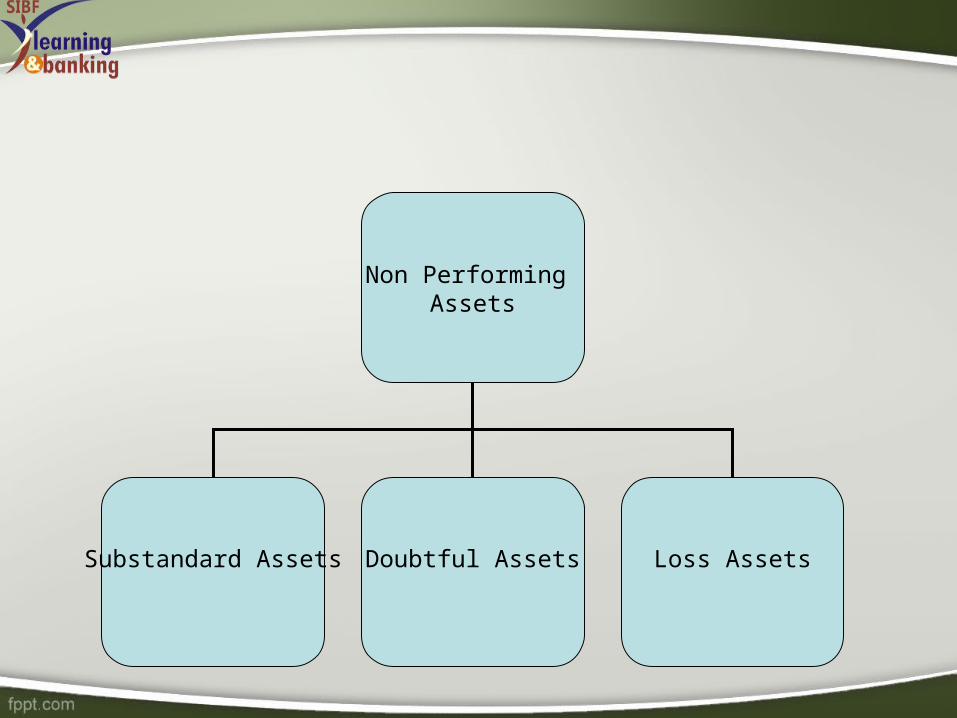

Non Performing Assets

Substandard Assets Doubtful Assets Loss Assets

Sub-Standard Assets: An asset which has remained NPA for a period less than or equal to 12 months.

Doubtful Assets: An asset that has remained in the substandard category for a period of 12 months.

Loss Assets: An asset where loss has been identified by the bank or internal or external auditors or the RBI inspection but the amount has not been written off wholly.

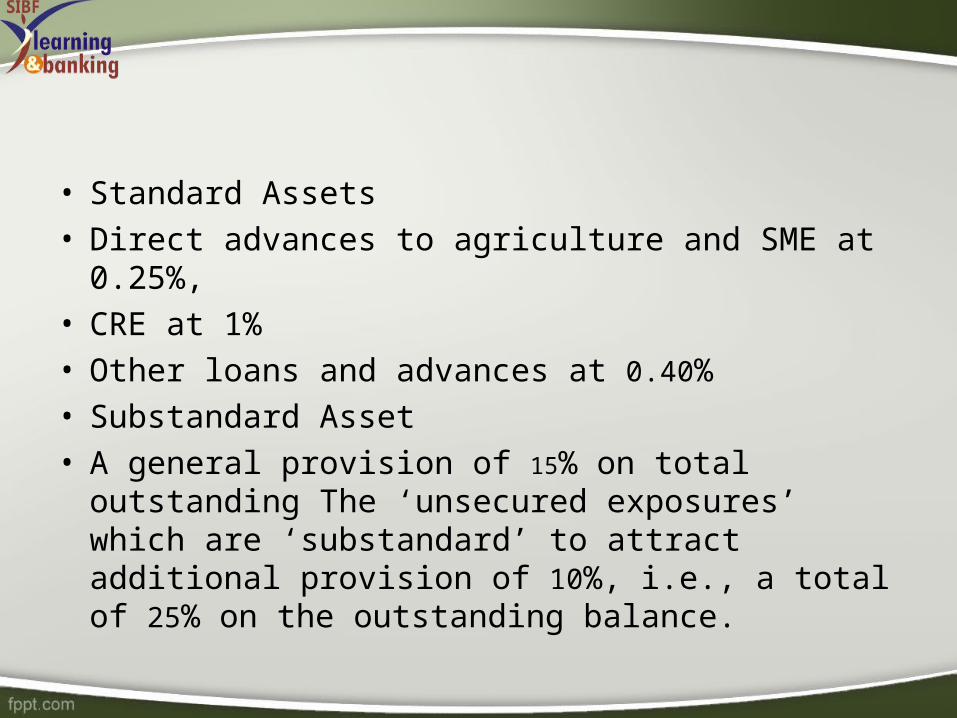

• Standard Assets• Direct advances to agriculture and SME at

0.25%,• CRE at 1%• Other loans and advances at 0.40%• Substandard Asset• A general provision of 15% on total outstanding

The ‘unsecured exposures’ which are ‘substandard’ to attract additional provision of 10%, i.e., a total of 25% on the outstanding balance.

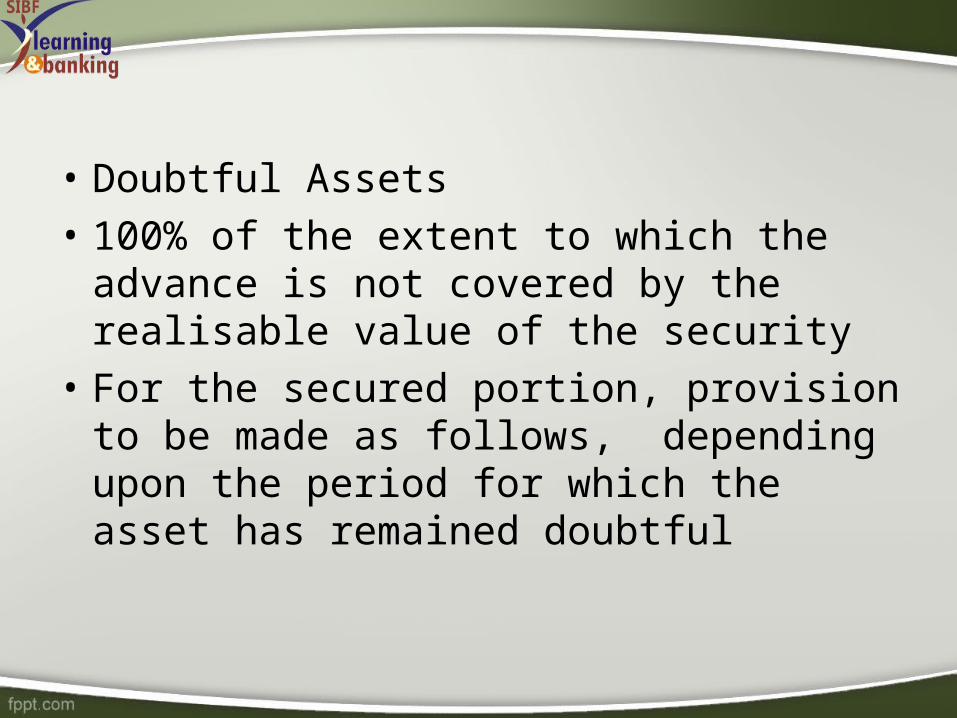

• Doubtful Assets• 100% of the extent to which the

advance is not covered by the realisable value of the security

• For the secured portion, provision to be made as follows, depending upon the period for which the asset has remained doubtful

• Loss Assets

• Write Off or provision of 100% of outstanding

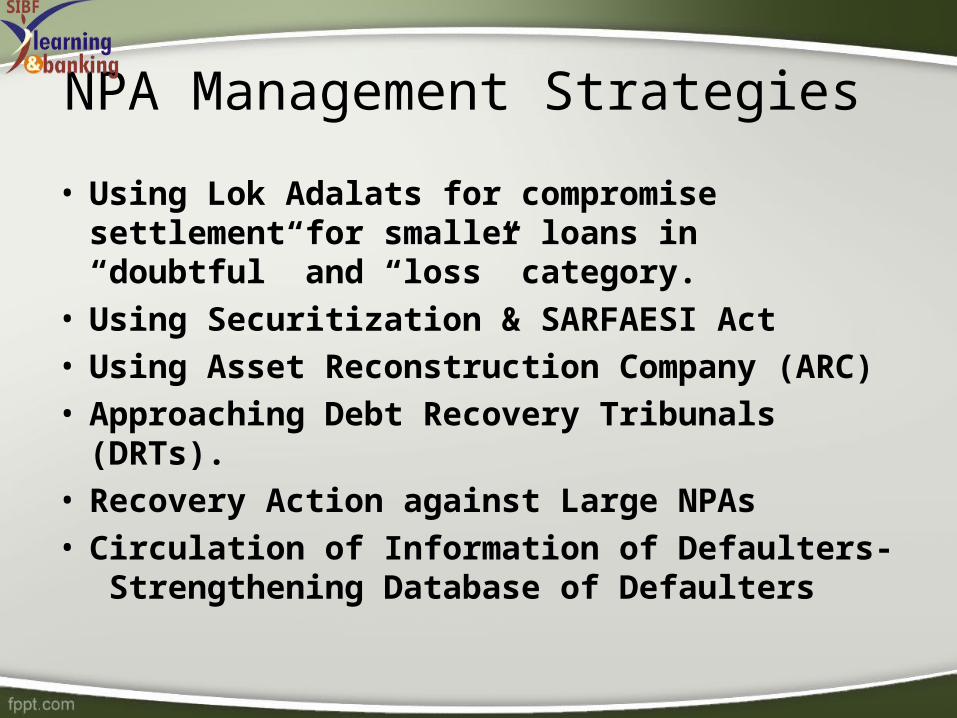

NPA Management Strategies

• Indian Banks are pursuing variety of strategies to control NPAs, which can be studied under two broad categories as under :

– a. Preventive Management – b. Curative Management

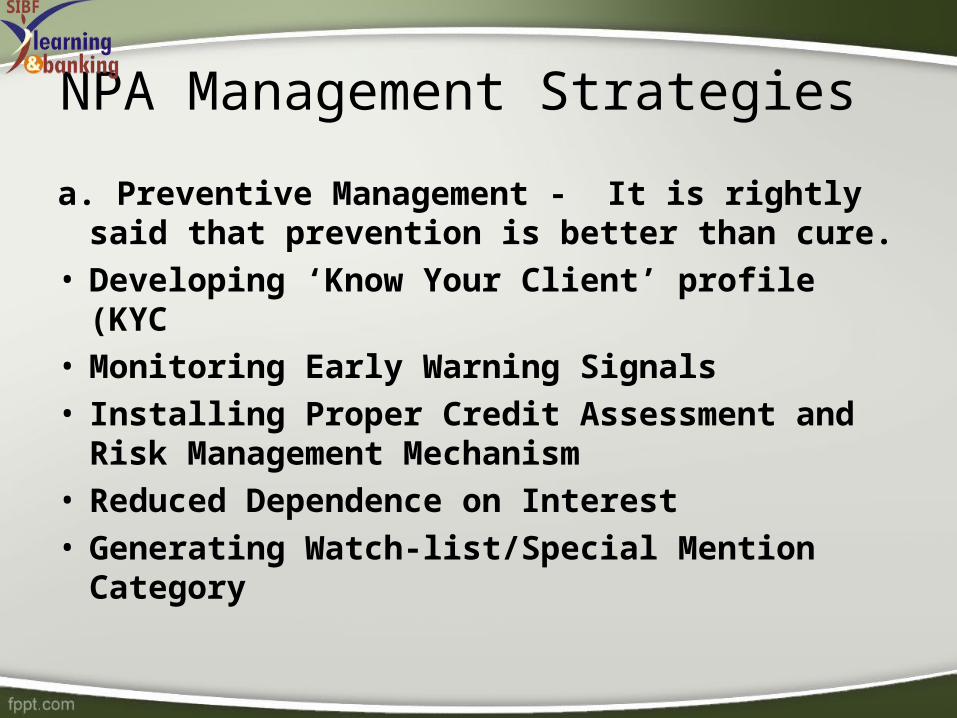

NPA Management Strategies

a. Preventive Management - It is rightly said that prevention is better than cure.

• Developing ‘Know Your Client’ profile (KYC

• Monitoring Early Warning Signals • Installing Proper Credit Assessment and

Risk Management Mechanism• Reduced Dependence on Interest• Generating Watch-list/Special Mention

Category

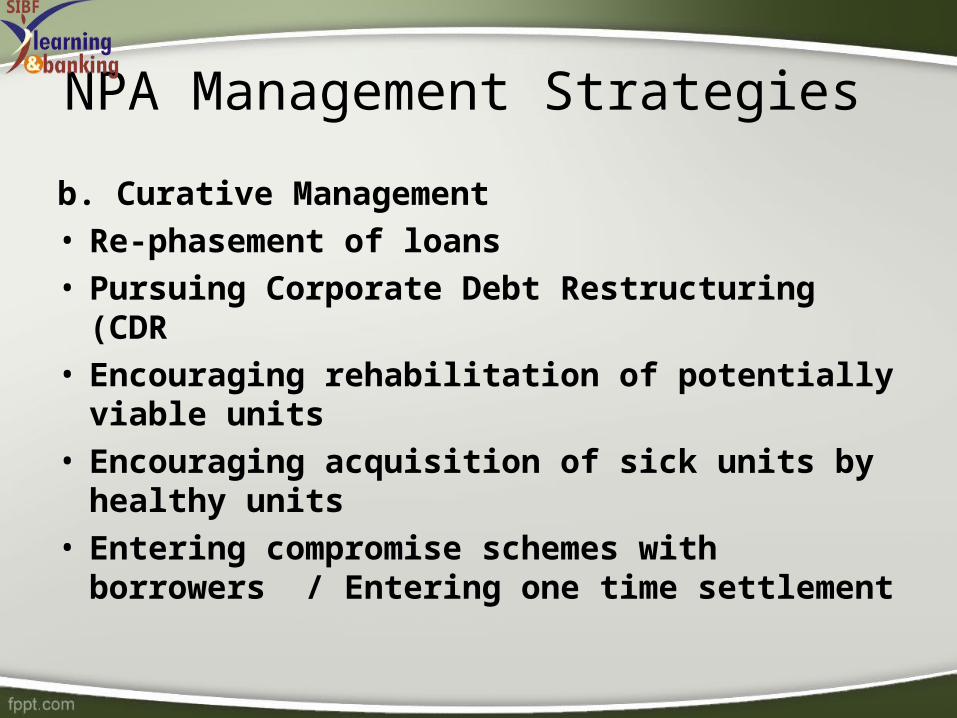

NPA Management Strategies

b. Curative Management • Re-phasement of loans • Pursuing Corporate Debt Restructuring (CDR• Encouraging rehabilitation of potentially viable

units• Encouraging acquisition of sick units by healthy

units• Entering compromise schemes with borrowers /

Entering one time settlement

NPA Management Strategies

• Using Lok Adalats for compromise settlement for smaller loans in “doubtful” and “loss” category.

• Using Securitization & SARFAESI Act• Using Asset Reconstruction Company

(ARC)• Approaching Debt Recovery Tribunals

(DRTs). • Recovery Action against Large NPAs• Circulation of Information of Defaulters-

Strengthening Database of Defaulters

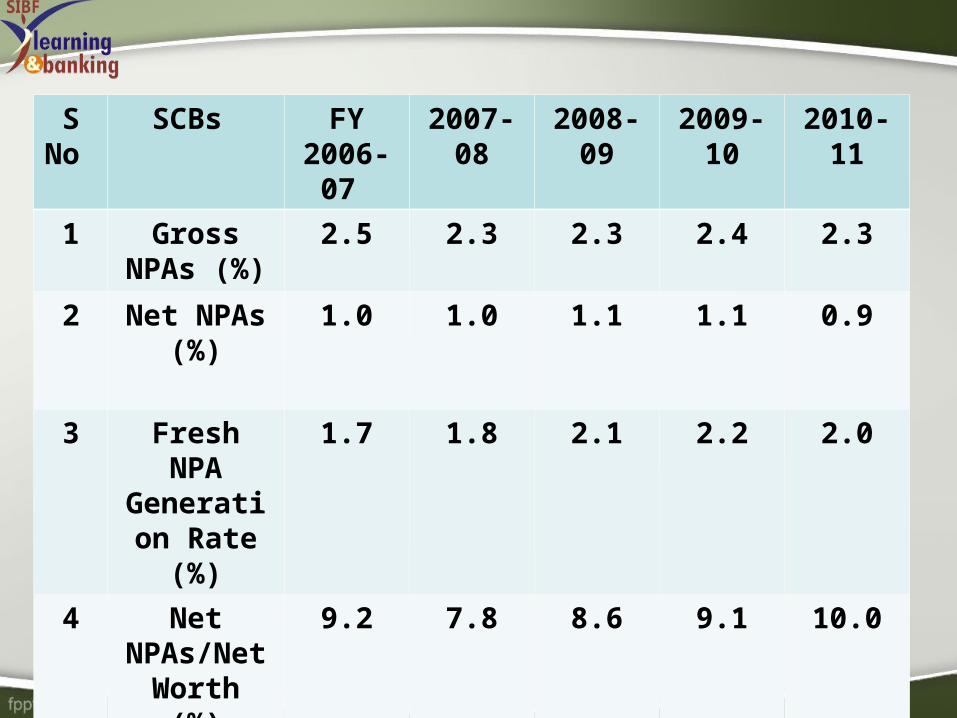

S No

SCBs FY 2006-07

2007-08 2008-09 2009-10 2010-11

1 Gross NPAs (%)

2.5 2.3 2.3 2.4 2.3

2 Net NPAs (%)

1.0 1.0 1.1 1.1 0.9

3 Fresh NPA Generation Rate (%)

1.7 1.8 2.1 2.2 2.0

4 Net NPAs/Net

Worth (%)

9.2 7.8 8.6 9.1 10.0

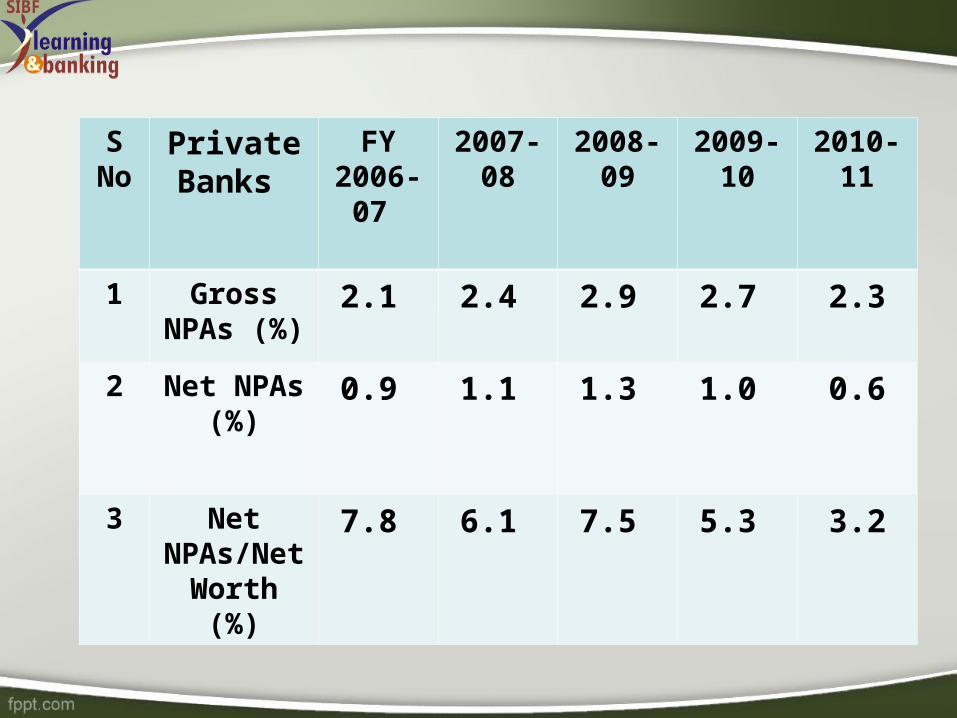

S No

Private Banks

FY 2006-07

2007-08 2008-09 2009-10 2010-11

1 Gross NPAs (%)

2.1 2.4 2.9 2.7 2.3

2 Net NPAs (%)

0.9 1.1 1.3 1.0 0.6

3 Net NPAs/Net

Worth (%)

7.8 6.1 7.5 5.3 3.2

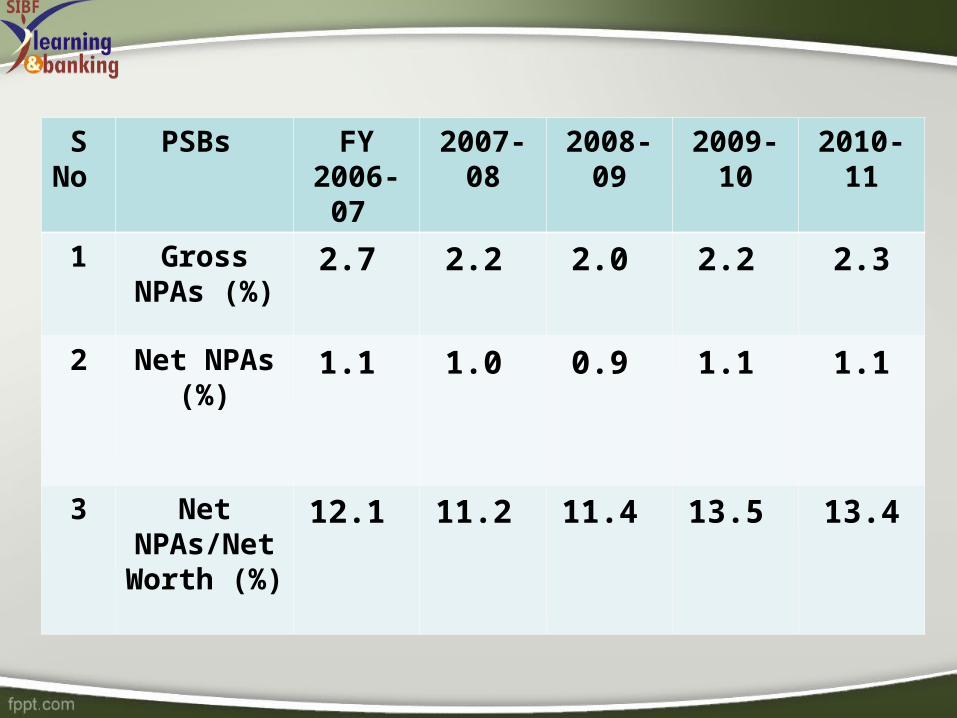

S No

PSBs FY 2006-07

2007-08 2008-09 2009-10 2010-11

1 Gross NPAs (%)

2.7 2.2 2.0 2.2 2.3

2 Net NPAs (%)

1.1 1.0 0.9 1.1 1.1

3 Net NPAs/Net

Worth (%)

12.1 11.2 11.4 13.5 13.4

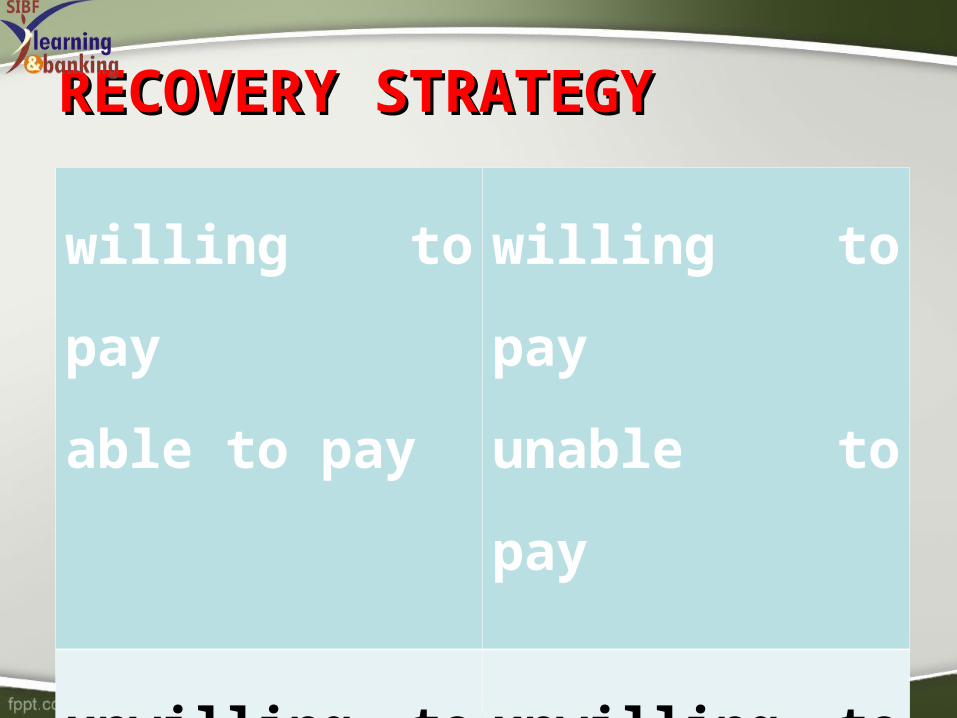

RECOVERY STRATEGYRECOVERY STRATEGY

willing to pay

able to pay

willing to pay

unable to pay

unwilling to pay

able to pay

unwilling to pay

unable to pay

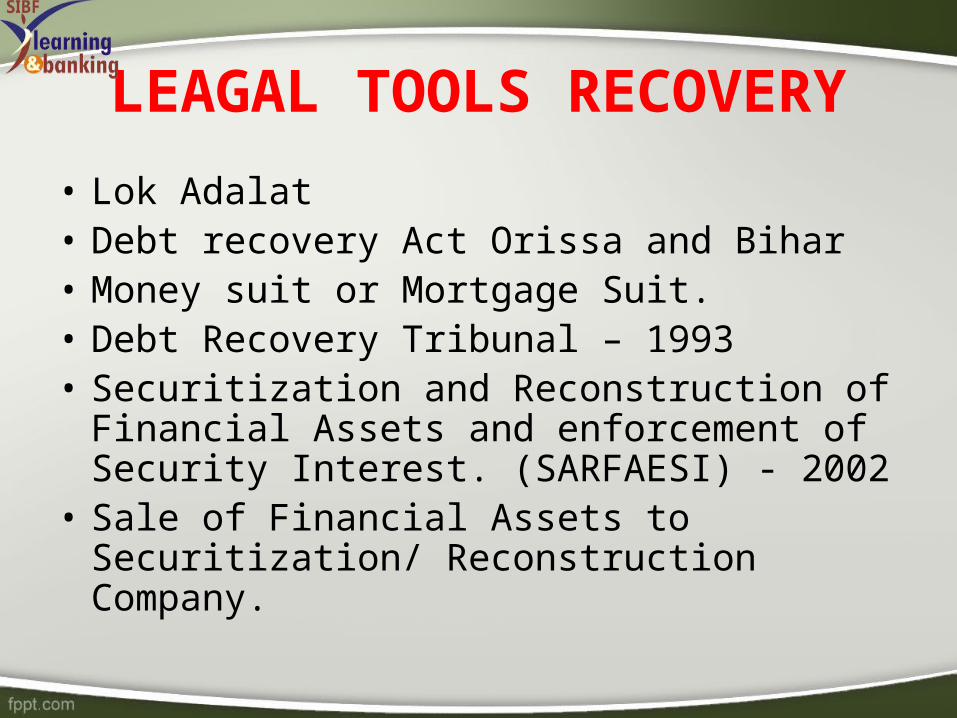

LEAGAL TOOLS RECOVERY

• Lok Adalat• Debt recovery Act Orissa and Bihar• Money suit or Mortgage Suit.• Debt Recovery Tribunal – 1993• Securitization and Reconstruction of

Financial Assets and enforcement of Security Interest. (SARFAESI) - 2002

• Sale of Financial Assets to Securitization/ Reconstruction Company.

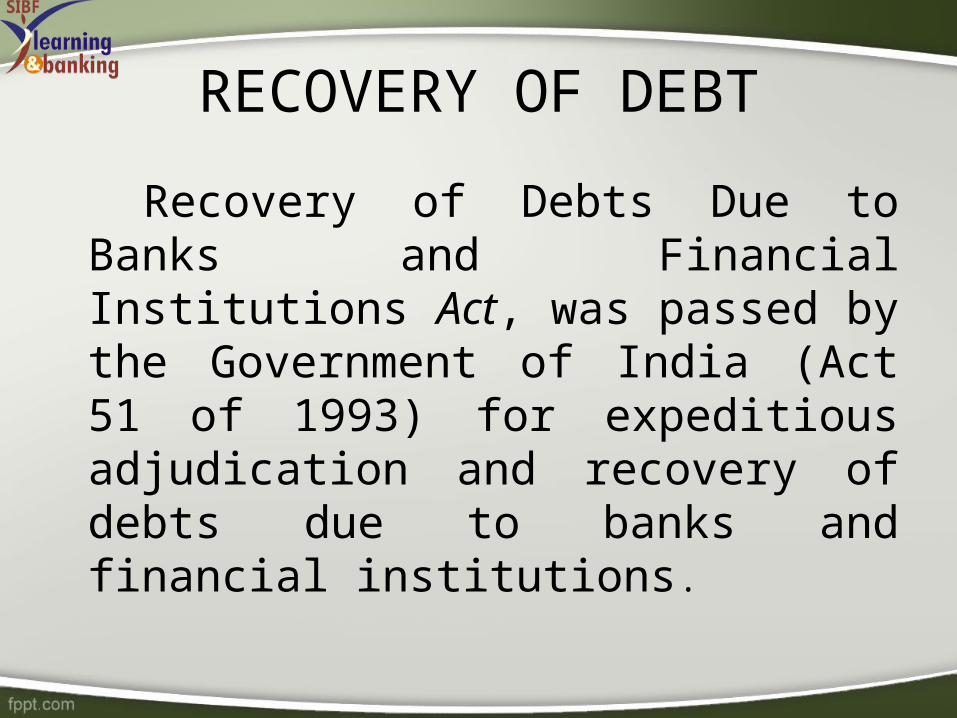

RECOVERY OF DEBT

Recovery of Debts Due to Banks and Financial Institutions Act, was passed by the Government of India (Act 51 of 1993) for expeditious adjudication and recovery of debts due to banks and financial institutions.

DRT

• The Debts Recovery Tribunal have been constituted under Section 3 of the Recovery of Debts Due to Banks and Financial Institutions Act, 1993.

• Appointment of Presiding Officer (PO) and Recovery officer. (RO)

• Setting of DRT Offices.

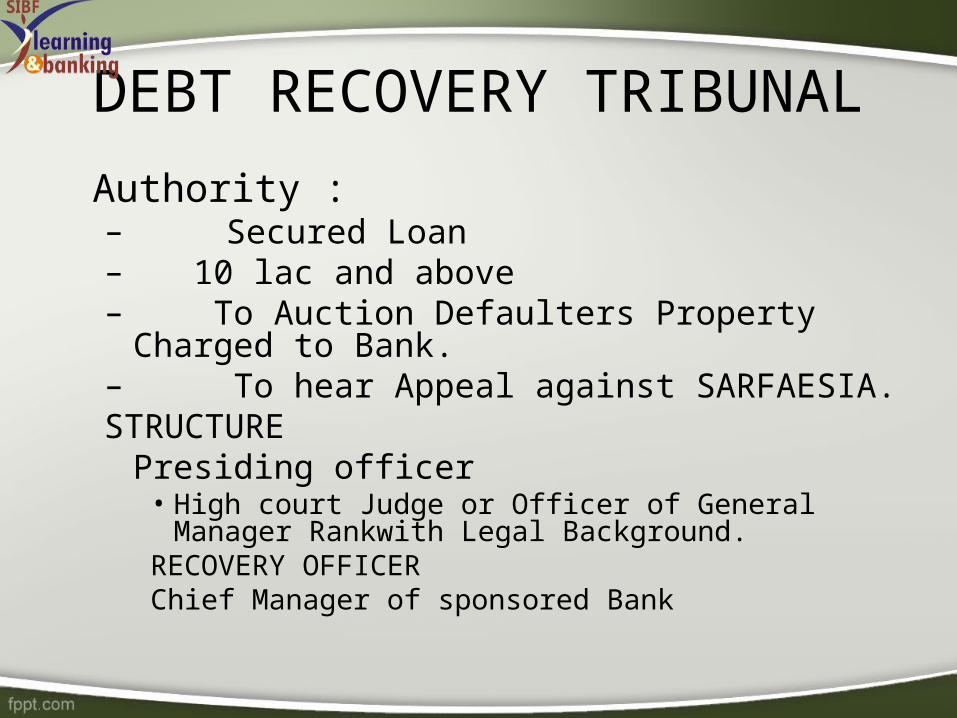

DEBT RECOVERY TRIBUNAL

Authority : – Secured Loan– 10 lac and above– To Auction Defaulters Property Charged to

Bank.– To hear Appeal against SARFAESIA.STRUCTURE

Presiding officer • High court Judge or Officer of General Manager

Rankwith Legal Background.RECOVERY OFFICERChief Manager of sponsored Bank

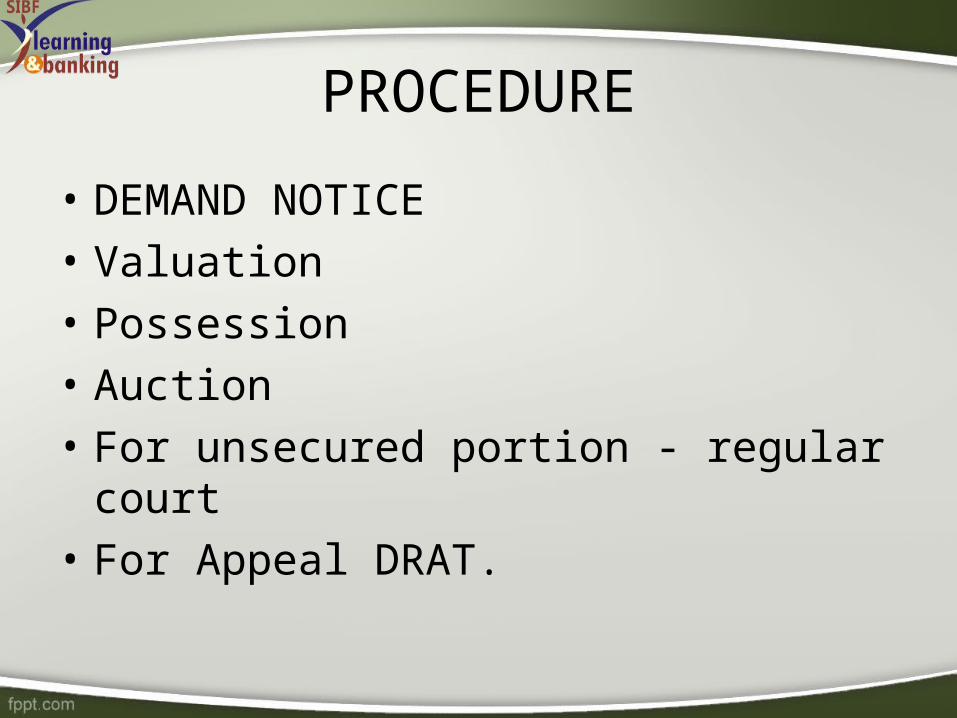

PROCEDURE

• DEMAND NOTICE

• Valuation

• Possession

• Auction

• For unsecured portion - regular court

• For Appeal DRAT.

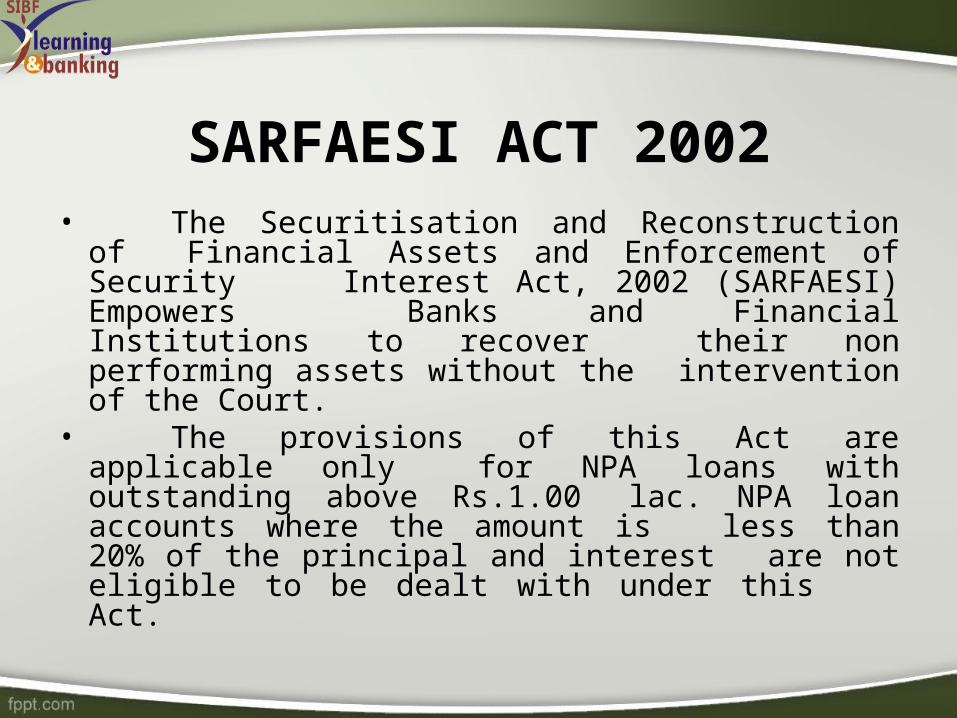

SARFAESI ACT 2002• The Securitisation and Reconstruction of

Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI) Empowers Banks and Financial Institutions to recover their non performing assets without the intervention of the Court.

• The provisions of this Act are applicable only for NPA loans with outstanding above Rs.1.00 lac. NPA loan accounts where the amount is less than 20% of the principal and interest are not eligible to be dealt with under this Act.

SARFAESI ACT 2002

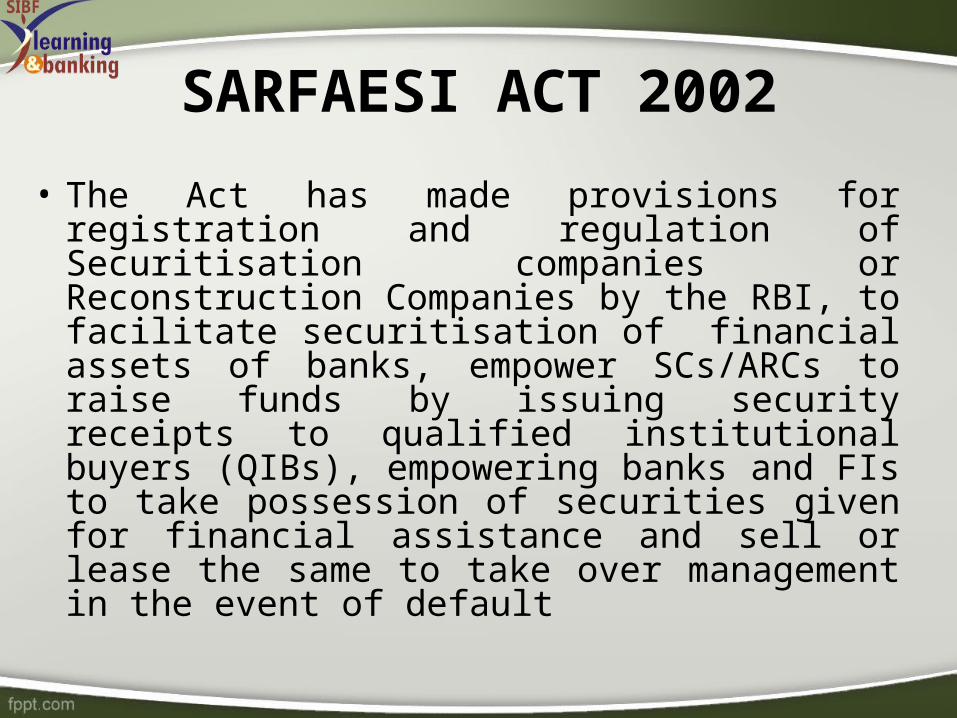

• The Act has made provisions for registration and regulation of Securitisation companies or Reconstruction Companies by the RBI, to facilitate securitisation of financial assets of banks, empower SCs/ARCs to raise funds by issuing security receipts to qualified institutional buyers (QIBs), empowering banks and FIs to take possession of securities given for financial assistance and sell or lease the same to take over management in the event of default

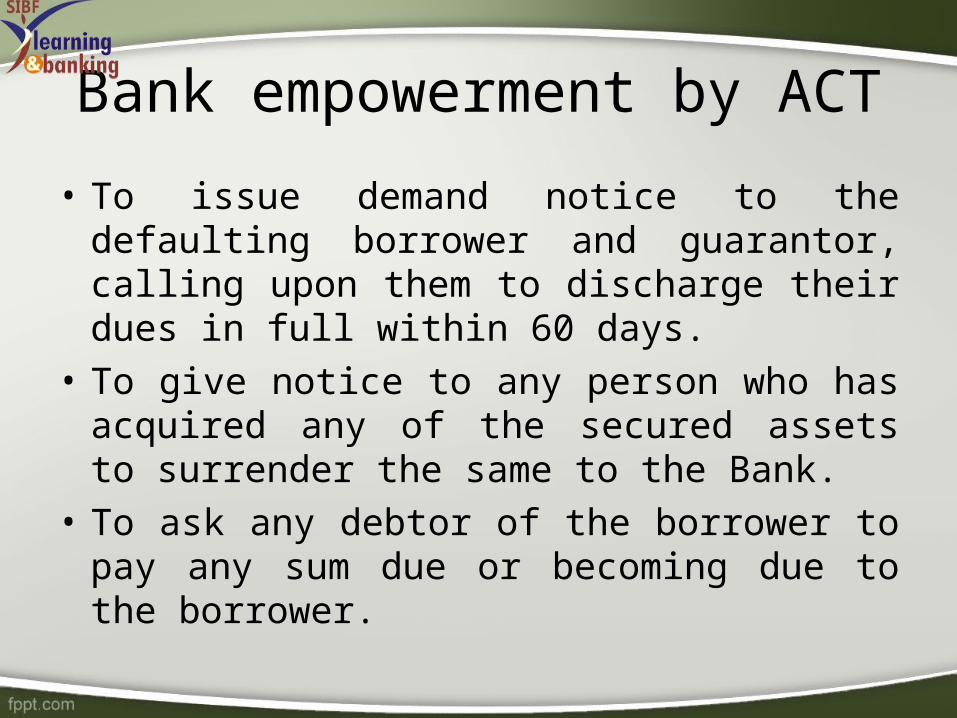

Bank empowerment by ACT

• To issue demand notice to the defaulting borrower and guarantor, calling upon them to discharge their dues in full within 60 days.

• To give notice to any person who has acquired any of the secured assets to surrender the same to the Bank.

• To ask any debtor of the borrower to pay any sum due or becoming due to the borrower.

Bank empowerment by ACT

• If the borrower fails to comply with the notice, the Bank may take recourse to one or more of the following measures:

• Take possession of the security

• Sale or lease or assign the right over the security

• Manage the same or appoint any person to manage the same

Implementation of SARFAESIA

Sale to reconconstruction company.

• There are many Assets reconstruction Companies to whom Bank Sale its NPA Assets for which SARFAESI Act has spelt out the detail procedure. Some of them are

• Assets care and Reconstruction enterprises.(ACRE)

• ARCIL• Pridhvi Asset Reconstruction and

Securitisation Company Limited (PARAS)

Smart Institute of Banking Insurance and Finance ( SIBF)

THANK YOU